What Does a 50 Basis Point Cut Really Mean?

Did you know that in a significant move, the Federal Reserve just reduced the fed funds rate by 50 basis points, bringing it down to a range of 4.75 – 5.00%?

This is the first cut since the early days of 2020, marking an end to what has been the most intense period of rate hikes in over four decades.

Why such a decisive cut, you might wonder?

Well, while some might see this as a signal of concern from the Fed about the economy, let’s dig a little deeper. Despite a slight uptick in unemployment and a slowdown in job growth, most indicators suggest that the economy is still expanding.

Even Fed Chief Powell has echoed this sentiment, providing a bit of reassurance to investors. He's betting on a smooth adjustment—a so-called economic soft landing.

Powell’s Perspective: Playing It Safe?

During his latest press conference, Powell maintained that the economy is "in good shape."

But, he hinted that this larger rate cut is more of a precaution—an "insurance" against potential slowdowns. It’s about reinforcing the job market now while it’s strong, not when layoffs start hitting the news.

Think of it as a balancing act. If the Fed waits too long or moves too slowly, it risks a recession. Move too quickly, and it could overheat the economy, sparking inflation. It’s a delicate line to walk, and today, everyone's tuned into how they're managing it.

Market Reactions and Long-term Strategies

Either way, the response from the markets has been generally positive given that it finally got what it’s wanted for years: a Fed Pivot.

Indeed, with profit growth stabilizing, inflation moderating, and interest rates either stable or falling, conditions are ripe for investment. Just this September, both the Dow and S&P 500 reached new heights, a reassuring move given the initial underestimation of inflation by the Fed.

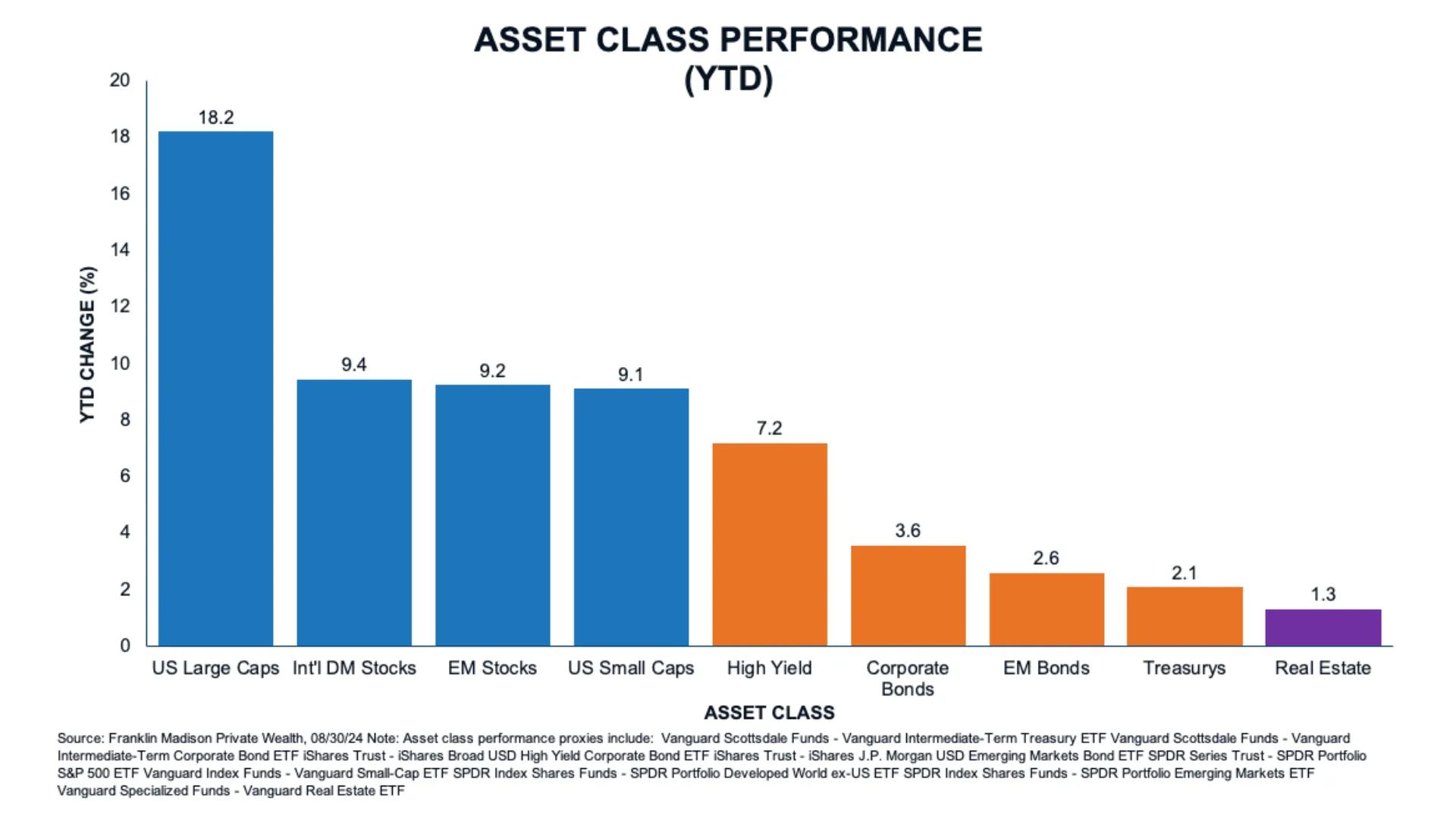

Here’s a quick snapshot of the latest index performances:

- Dow Jones Industrial Average: 1.8% month-to-date, 12.3% year-to-date

- NASDAQ Composite: 2.7% MTD, 21.2% YTD

- S&P 500 Index: 2.0% MTD, 20.8% YTD

Now, it’s worth noting that while strong market performance can stir investor enthusiasm, it also brings with it the temptation for risk-taking. This is where a disciplined investment strategy comes into play.

You see, it’s not just about chasing returns; it’s about managing risks and ensuring you have a portfolio that balances both risks and returns.

The Big Takeaway

So, why should this matter to you?

Well, this situation underscores the critical lesson of diversification—not just in types of investments but also in understanding market movements and central bank strategies.

You see, while markets have rallied strongly this year, recent volatility is a stark reminder that market conditions can change on a whim, so it’s essential to be prepared and not take more risk than necessary.

That’s why, by diversifying your investments, you not only shield yourself from unforeseen market shifts but also position yourself to capitalize on various global opportunities. This kind of strategic positioning ensures that your portfolio captures potential gains while distributing risks, allowing you to focus on what truly matters.

So, as we think on the Fed's recent move, consider this: Is your investment portfolio as diversified as it should be, or are you relying too much on certain assets?

Remember, a disciplined investment strategy isn’t just about picking stocks—it’s about preparing for whatever the future holds while ensuring that your financial foundation is as solid as it can be.

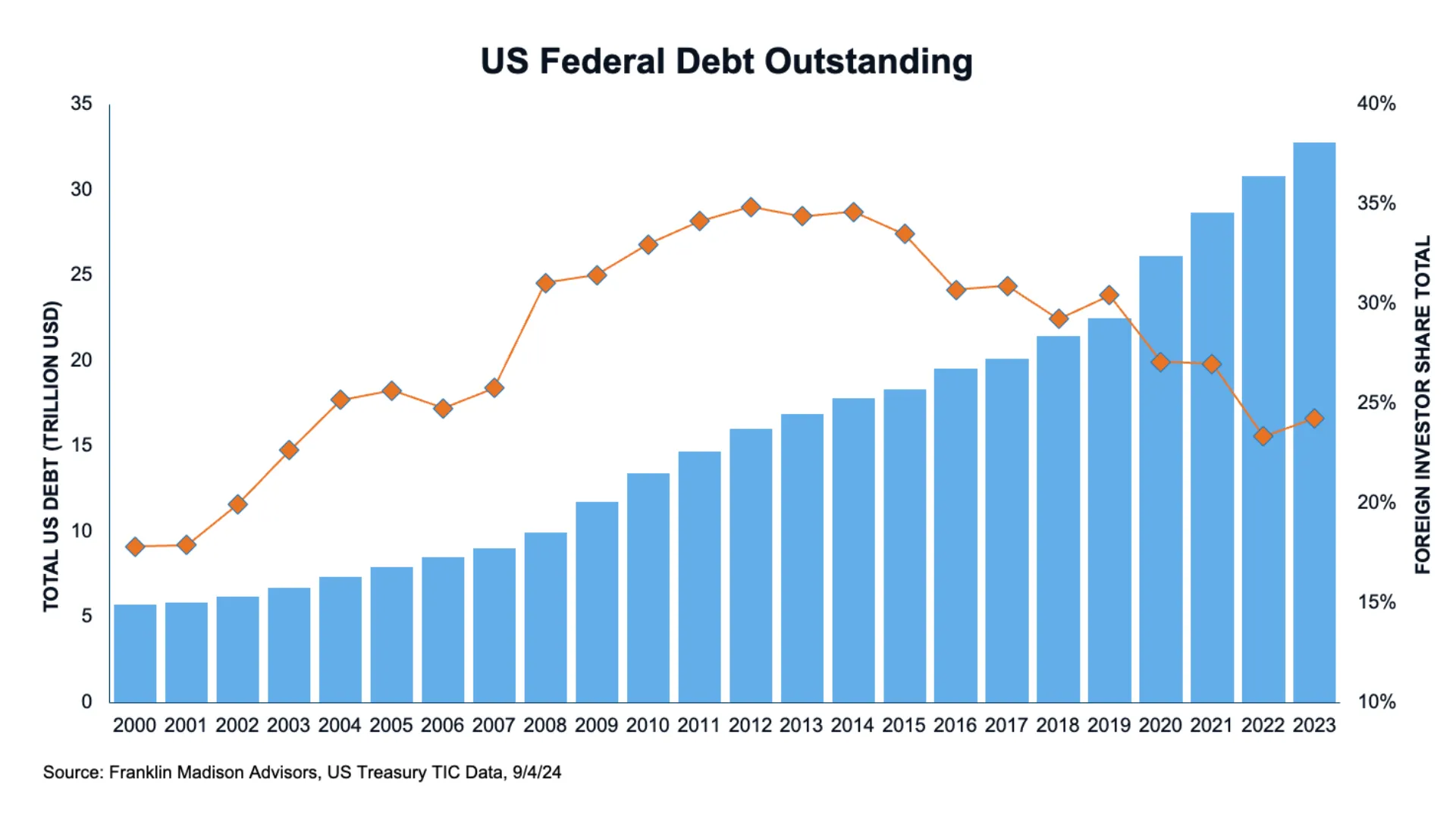

What Can We Learn from Big Government Bond Investors?

Did you know that nearly a quarter of all US government debt outstanding is held by foreign investors?

And, what if I told you that this number has been falling in recent years?

In fact, This figure was at a peak of 35% in 2014 but has declined to 24% as of the end of 2023.

Well, this shift might remind you about concerns about the US dollar's dominance, right?

The Decline in Foreign Holdings: A Sign of Shifting Trends

Well, as a high-achieving professional, you likely understand that these global movements can provide valuable insights into managing your own investment portfolio.

And you see, this market development actually highlights a critical lesson in financial wisdom: the importance of diversification.

How so?

The Real Story: Global Asset Diversification

Well, while some may argue that fewer foreign investors holding Treasuries reflects a decline in US dollar dominance, the fact is that the USD is still the world's preeminent reserve currency.

So then, the decline in foreign holdings must be attributed to something else, right?

So, what's really happening?

Well, it looks like what we're seeing is a broader trend towards global asset diversification as global economic and financial conditions have evolved over the past decade.

The Evolution of Foreign Investment in US Debt

In fact, recent research from the Treasury Department shows that the percentage of US debt held by foreigners has started to decline from its peak in 2015, signaling a shift towards a more diversified global investment strategy.

You see, at the turn of the century, treasuries held by foreign investors accounted for about 18% of total federal debt outstanding, which is a figure that’s substantially less than it is today.

Think about this: after surging during events like the Global Financial Crisis and the European Debt Crisis, when US treasuries were the go-to safe haven, the percentage of US debt held by foreigners has begun to moderate.

Why?

Because as markets stabilize, investors start looking for opportunities beyond the US. It's like they're spreading their bets rather than putting all their eggs in one basket.

Case Study: The European Debt Crisis and Its Aftermath

For example, during the European Debt Crisis, investors flocked to US treasuries as a safe haven, which spiked the percentage of US debt held by foreigners.

But once the dust settled and global markets got back on their feet, these investors started diversifying their portfolios with a mix of assets, showing a savvy approach to investment that we can all learn from.

So then, the main takeaway here is not just that diversification is wise; it's a necessary strategy in today’s interconnected financial landscape.

Personal Portfolio Implications

Why should you, as a tech professional with significant earnings, care about this?

Well, diversification isn't just a practice for institutional investors. It’s equally crucial for your personal portfolio.

By diversifying your investments, you’re not only protecting yourself from unforeseen market shifts but also positioning yourself to take advantage of various global opportunities.

And this kind of positioning ensure that your portfolio captures upside potential while spreading out risk even as you spend your precious little time on things that truly matter to you.

Evaluating Your Investment Strategy

So then, take a lesson from foreign investors and ask yourself, “is my portfolio truly diversified, or am I relying on a single big position to carry my retirement and financial independence goals?”

Remember, building a disciplined investment strategy is not just about picking stocks or sectors; it’s about preparing for the future, wherever it might lead.

So then, take this opportunity to make sure your investments are as globally savvy as you are.

Risk Sentiment Improves as Economic Data Fuels Rate Cut Expectations

Risk-on sentiment has returned to global markets this week, fueled by easing inflation data that continues to support the case for more accommodative rate cuts by the Federal Reserve at its next FOMC meeting. Overall, market expectations suggest that policymakers can "thread the needle" of cutting interest rates to support a soft landing in the economy and ultimately avoid a recession.

This optimistic view has been bolstered by incoming economic data. A revised second look at GDP figures revealed that the US economy grew faster than expected in the second quarter. This positive trend was further supported by a solid expansion in retail sales during July. Simultaneously, while initial jobless claims have remained relatively flat, job openings are slowly starting to dwindle. This labor market dynamic likely supports the Fed's case for cutting rates to put a floor under potentially slowing growth.

In Asia, stocks largely closed the week out in mixed fashion, led lower by China due to concerns about the country's waning growth prospects. This outlook comes on the heels of news that policymakers are considering plans to allow homeowners to refinance $5.4 trillion worth of debt, as sagging property prices have weighed on spending and household wealth. Despite these challenges, stocks in mainland China rallied into Friday's close but still ended down for the week, with the Shanghai Composite off 0.40% and the CSI 300 largely flat.

Other Asian markets managed to look past China's concerns, with stocks in Hong Kong gaining 2% on the week, spurred by positive economic data from the US. Japanese stocks also moved higher despite concerns surrounding a potential rate hike by the Bank of Japan, with the Nikkei closing up around 1.2% for the week. Indian and Australian markets followed suit, with the Sensex up 1.6% and the ASX adding nearly half a percent.

In Europe, the mood is solidly risk-positive as investors digest data showing waning inflation and moderating economic growth across the region. Most major European markets are higher this week, with Italian stocks leading the way with a gain of roughly 2.2%. German stocks are trading flat on Friday but still up nearly two percent for the week, while the UK's FTSE has posted a solid gain of around 1%.

On Wall Street, stocks are set to close out the week in mixed fashion. The big story this week was NVIDIA's earnings and whether demand for the company's AI-related products would be enough to support the broader rally in tech stocks this year. As a result, we're seeing mixed performance, with the Nasdaq down around one percent for the week, large-cap stocks as measured by the S&P 500 mostly flat, while the Dow and small-cap stocks carried US equity market performance.

In the fixed income market, rates have stabilized, with 10-year Treasury yields falling to 3.9% from about 4.25% a month ago. The expectation that the Fed will cut rates in September is being priced into the market. Internationally, yields on 10-year German bunds and British gilts are trading largely flat for the week, while Japanese JGBs have caught a bid recently, with yields falling and prices supported by BOJ intervention.

In currency markets, the US dollar is trading modestly higher this week, with the DXY US dollar index at 101 on Friday morning, off around 0.75% over the past week. As a result, the euro is down around one percent, trading at 1.10 to the dollar, while the British pound has pared about 0.25% but remains at its highest level in over two years at 1.31 to the dollar. The Japanese yen is up modestly as BOJ policymakers signal readiness to continue raising interest rates, and the Chinese yuan closed at its strongest level since June 2023.

Looking ahead to next week, we'll be entering a new month in which the Fed is expected to cut rates for the first time since the start of the pandemic. Key economic releases include business sentiment data on Tuesday, followed by trade and JOLTS data on Wednesday. However, the main focus will be on jobs data, with the ADP report on Thursday and the crucial Non-Farm Payrolls data on Jobs Friday.

As we enter the back-to-school season, portfolio managers will be reassessing their holdings and evaluating whether their current positions still make sense after this year's strong run in prices. Investors should be prepared for potentially volatile conditions in risk assets in the month ahead as the market digests new economic data and central bank decisions.

Why Does the Market Care About FOMC Meetings?

Why does the market care about FOMC meetings?

And more importantly, why should you care?

Well, the short answer is that the decisions made by the Fed can influence the economy, can influence business earnings, and, hence, can influence the direction of the markets.

You see, the Fed was created by Congress well over a hundred years ago.

The Federal Reserve's Role in the Economy

And today, it has two main mandates: the first is to ensure maximum employment and the second is to maintain price stability.

In other words, the Fed’s role is to ensure that inflation remains in check and that unemployment doesn’t get too far out of control for too long.

So then, at regular intervals throughout the year, during these Federal Open Market Committee (or FOMC) meetings, policymakers assess whether they’re doing what’s necessary to stick to their commitment.

Now, there’s only so much that any one institution can do to control what businesses charge for goods or services or whether they’re prepared to keep hiring.

How Interest Rates Affect the Economy

However, the one thing that the Fed does have control over is short-term interest rates.

And so, you likely know that when the interest rate on your credit cards, or your auto loan or your mortgage goes up, your willingness to spend likewise goes down, right?

Well, in a similar way, the Fed sets its policy rate so that it’s more expensive for businesses to borrow when inflation is getting out of control.

And when inflation is stabilizing, and jobless claims are on the rise, then policymakers consider cutting rates to incentivize borrowing and boost economic activity.

Put a different way, it’s all about the way that money flows through the economy.

When the tap is open and money is flowing freely, the economy is typically humming, but inflation tends to take off as well.

Why You Should Pay Attention to FOMC Meetings

Alright, so with all that said, why does the market care about FOMC meetings?

Well, when the Fed begins raising or lowering rates, it’s typically part of a broader trend. Here again, when interest rates are set to fall, businesses could benefit from lower borrowing costs, and potentially lead to increased profitability and therefore support higher stock prices over the long-term.

So then, why should you care about what the Fed is doing?

Well, when the Fed does something in line with market expectations, this often translates into a higher portfolio value for your retirement savings.

What’s more, understanding the Fed’s decisions can help you make better spending choices, especially if you plan to finance a big-ticket purchase like buying a new home.

At the same time, it can also help you determine whether it’s a prudent time to go out and find that new job.

That’s because when the Fed starts cutting rates, it can signal that a potential economic slowdown is underway and suggest that the job market might soon tighten.

So then from this perspective, it's crucial to approach job changes with caution when the Fed is preparing to cut rates.

Either way, staying on top of the Fed’s latest policy rate decision, and more importantly, understanding why markets respond the way they do, will likely help you make better financial decisions and at the same time, help you make career choices that ultimately set you up for success.

What Does Today’s GDP Release Mean to Your Money?

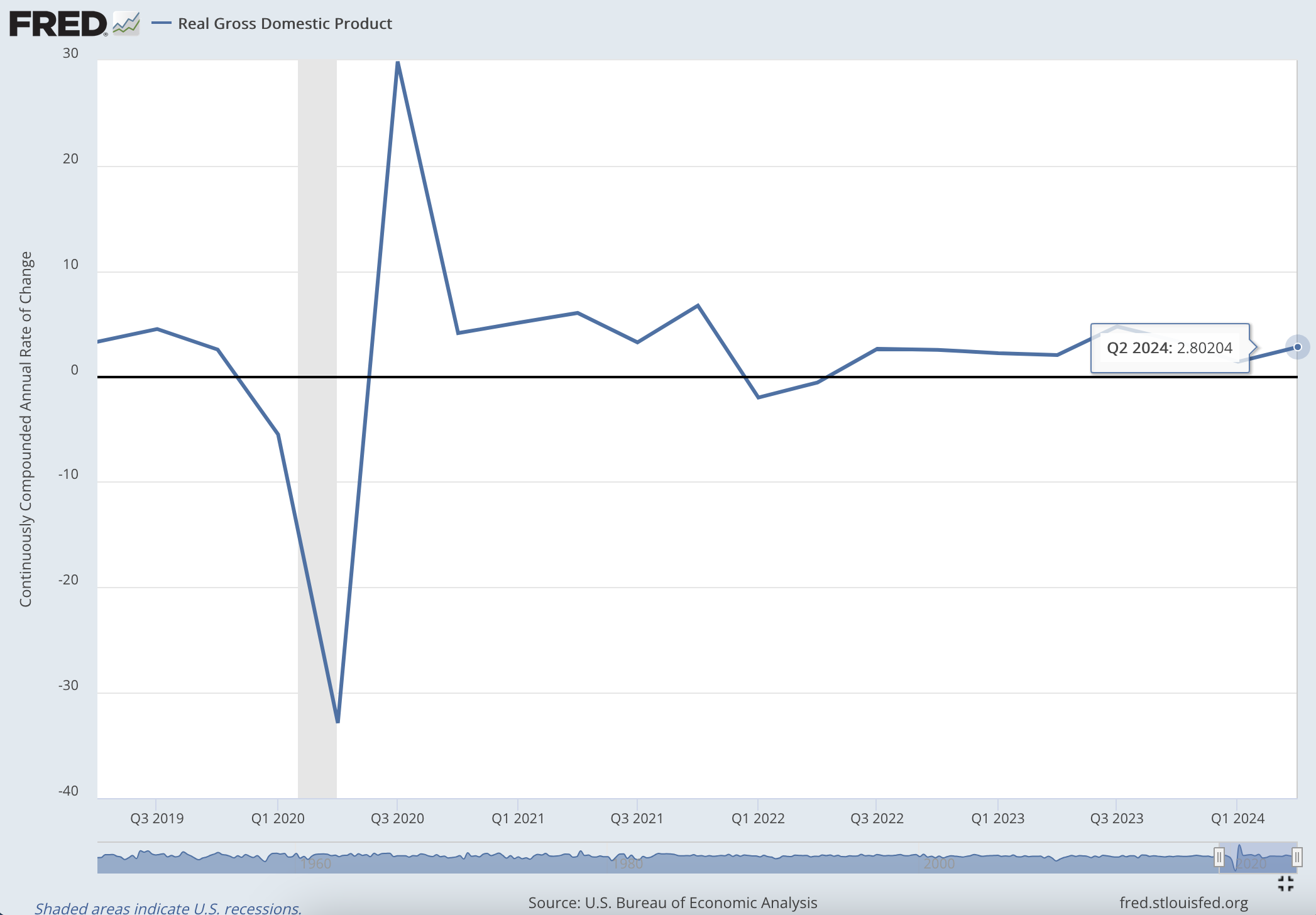

Data came out this morning showing that Gross Domestic Product here in the US grew faster than expected in the second quarter.

The Bureau of Economic Analysis reported that the economy expanded 2.8% on a quarter-over-quarter annualized pace in 2Q24, besting economist expectations of 2.0% growth.

But what exactly does this data point mean? And more importantly, what does it mean to your money?

Well, Gross Domestic Product (or GDP) is one measure of how the economy is performing from quarter to quarter and year to year.

How GDP Influences Business Decisions and Personal Finance

Now, this data is helpful because it's used by business leaders, policymakers, and even consumers like you and me to make decisions with our money.

For example, when the economy is doing well, business leaders are more likely to spend more money on things like software and equipment or hiring workers.

At the same time, policymakers, like those at the Federal Reserve, are keeping an eye on inflation and whether interest rates need to go higher or lower.

For everyday people, our financial choices, such as spending or saving, are influenced by the health of the job market and the cost of borrowing money.

And so, all these factors are interlinked with the performance of GDP.

So then, how does understanding GDP data impact our daily life?

Well, understanding trends in GDP data can helps you better anticipate changing economic conditions and make smarter choices with your money.

So far, so good, right?

Market Reactions to GDP Data and Future Expectations

Now, leaves us with another key question, and that’s : why are markets so keen to paying attention to this data?

Well, over the long term, robust GDP growth usually supports strong corporate earnings, which can support trends of rising asset prices.

But, in the near term, the impact of GDP data often relates to how it fits into the current market narrative, which influences daily market movements based on whether it supports or contradicts prevailing investor expectations.

And what exactly does this mean?

Well, it means that despite solid GDP growth this year, a dominant market narrative is the expectation of a potential rate cut by the Federal Reserve.

Now, typically, the Fed might lower rates to stimulate the economy during periods of slower growth, not when it's expanding.

But, if inflation remains under control despite solid growth this year, the Fed could consider a rate cut to preemptively mitigate a deep economic downturn, which would align with investors' expectations of a soft economic landing.

Therefore, market participants are keenly analyzing today's GDP report for indications that strong growth can coexist with controlled inflation and potentially lead to a rate cut later this year.

Either way, having a basic understanding of the macro data will not only help you make more informed financial decisions, it will also give you something to talk about during your next team call.

Global Economic Outlook: Why Economic Forecasts Still Matter in 2024

Economic and market forecasts are often wrong, but they're still useful.

Indeed, looking back on the past year, most market prognosticators and economists got the year's forecasts wrong.

That's because last year was supposed to be the year that the US economy fell into a recession, which led markets to bet that the Federal Reserve would cut interest rates by the end of 2023.

And while risk assets eventually rallied on expectations of policy changes, interest rates are still nowhere near where the markets had predicted at the start of last year.

And how about that well-telegraphed recession?

Well, even the Fed, which employs the most Ph.D. economists globally, got that call wrong.

So then, you'd think that they should have at least had the forecast partially correct, right?

Well, even so, policymakers ultimately decided to scrap their recession forecasts early last year despite the best predictions of their brain trust.

Add in financial doom and gloom from high-profile social media accounts that tipped off a run on some small regional banks, and still, the financial collapse that some market prognosticators anticipated simply did not pan out.

So then, if forecasts are so wrong so often, what's the point of paying attention to them in the first place?

Well, it all comes down to understanding directionally where the economy and markets are headed.

You see, well-known economist John Maynard Keynes was once quoted to have said that, "I'd rather be vaguely right than precisely wrong."

And what does this mean?

It means that you'll be better equipped to make solid financial decisions with your money and your wealth in the coming year by focusing on the factors that might affect the direction of the markets and economy rather than trying to divine the precise outcomes of one or another.

Still an Uncertain Economic Outlook

Alright, so then, from this perspective, what direction is the global economy likely headed in the coming year?

Well, as it stands today, the global economic outlook for 2024 remains highly uncertain due to several competing factors.

These factors include ongoing household and business adjustments in the post-pandemic economic environment, varying global central bank policies, heightened geopolitical tensions, and the complex interplay between inflation, employment, and consumer spending.

Overall, however, global inflationary pressures are expected to ease from post-pandemic highs, and economic output could come in modestly softer than the surprisingly strong growth we experienced in 2023.

And what's driving this outlook?

Well, this optimism stems from several key areas, such as technological advancements driving productivity, some emerging markets showing resilience and growth potential, and expectations of easier money policies as inflation comes under control.

At the same time, some economic sectors and global regions are demonstrating strong fundamentals and resilience, which could buffer against a broader global economic downturn.

US Outlook

More specifically, here in the US, the economic outlook for 2024 is mixed, but generally positive. That's because the economy, while now feeling the pressures of higher interest rates, is still navigating the after-effects of historically high prices.

Overall, however, inflation is forecast to fall to around 2.5% in 2024, compared to 4.1% last year, according to consensus estimates.

Even so, cautious optimism is starting to form among market watchers that the inflation beast that has tortured the markets for so long may finally have been tamed following December's better-than-expected inflation data.

This outcome is arguably due to the Fed's restrictive monetary policies, which have tightened credit conditions in big-ticket lending sectors, like housing and autos, and has gradually influenced the economy's overall trajectory.

And while elections are once again likely to prove contentious here in the US, policies emanating from various campaigns in 2024 likely will be something to watch in 2025 and beyond.

At the same time, critical technological advancements and a still resilient labor market continue to support growth through business investment and household spending.

With that said, fissures are beginning to form in retail spending as household debt rises to record levels and discretionary savings fall, suggesting consumption could take a breather in the first half of this year.

And while some economists continue to project a US recession in the coming year, consensus expectations suggest that there's still a chance the US economy could manage a "soft landing" and avoid a full-on downturn.

This outcome is likely to happen as growth slows in the first two quarters of the year, and then reaccelerating to growth rate of around 1.5% (QoQ SAAR) into year-end.

International Outlook – Europe

Outside of the US, forecasts suggest that growth is likely to moderate after experiencing a solid rebound last year.

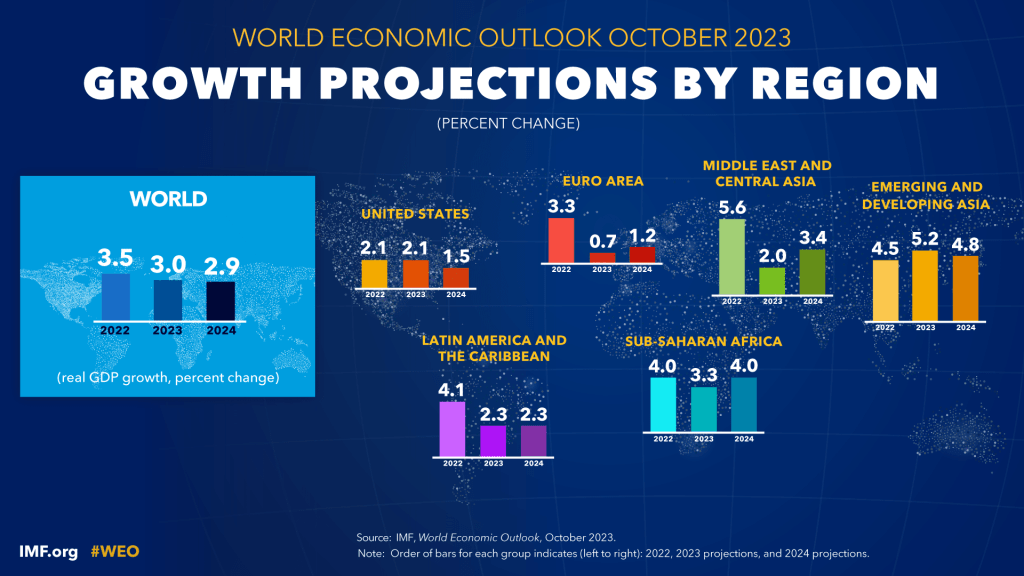

Indeed, according to forecasts from the IMF, we're looking at year-over-year global growth estimates of 3.0% for 2023, which then slows to 2.9% in 2024.

This outlook is largely influenced by global policymakers keeping a tight grip on monetary and fiscal policies as the fight against inflation battles outside of the US continues.

In fact, these policies have arguably influenced overall inflation trends in developed and emerging market economies, which are each expected to see price growth continue to slow in the year ahead.

Even so, we expect major economies in Europe to face their own set of challenges, mostly due to high energy prices and the ongoing war in Ukraine. And while these factors are causing a drag on growth in the near term, assuming no further military escalation in Eastern Europe, we anticipate growth to stabilize as policies become accommodative later in the year.

International Outlook – Asia

Turning our attention to Asia, the outlook in this region is likely to vary on a country-by-country basis.

For example, we anticipate Japan's economy to stabilize this year as inflationary pressures ease and labor market conditions remain solid.

And while South Korea's fortunes are linked with global trade demand, which has been historically soft in this post-pandemic era, we nevertheless anticipate global trade to firm up in the year ahead, which should be a positive boon to the South Korean economy.

Along these same lines, while China likely experienced a decent growth rebound in 2023 following its own pandemic shutdown, the growth trajectory in the year ahead is less certain. That's because a cooler real estate market and easing infrastructure development have weighed on household wealth and, hence, consumer spending.

Overall, economic growth is likely to remain balanced, albeit somewhat softer in the year ahead, as inflationary pressures in developed markets ease and trade slowly rebounds in emerging economies.

Cash Remains King

So then, how should you position your wealth, given the current economic backdrop?

Well, when it comes to your money, cash is still king.

That's because factors like fluctuating central bank policies, geopolitical tensions, and still volatile inflation could lead to unpredictable economic and market shifts this year.

More specifically, these changes might impact your W2 or business income and investment returns in the months ahead. That's why you'll want to make sure that your cash management strategy is appropriately dialed-in, and that you have enough liquidity on hand to match your current lifestyle demands.

At the same time, while the probability of a "soft landing" in the US is greater than zero, what this past year has taught us is how essential it is to be prepared for the unexpected.

Indeed, should we experience a period of heightened economic and market uncertainty, then having "dry powder", or adequate cash on hand, may enable you to capitalize on potential market opportunities should they present themselves during a brief period of market volatility.

To be sure, at the end of the day, maintaining an extra cash reserve in such an uncertain economic environment ultimately serves as both a safety net and a strategic reserve.

Monetary Policy: Pivot to Neutral

Alright, so now that we've covered the economic outlook, let's talk about monetary policy.

Now, monetary policy was a central point of contention for market participants this past year.

And that's because markets gyrated up and down as investors adjusted their bets on the timing and degree of rate cuts from the Fed all throughout 2023.

Now, looking into the year ahead, the story likely will be more of the same, but less about a matter of "if" policymakers will cut rates, and more about "when" the cuts will occur and how much the Fed will cut.

Indeed, as inflationary pressures continue to ease in the coming year, policymakers are likely to shift their focus toward supporting economic growth and stabilizing the labor market.

And so, as far as the markets are concerned, this policy transition often involves lowering interest rates to stimulate borrowing and spending once it's clear that the economy is off the rails.

But we're not at that point yet.

Even so, should incoming economic data show that the economy is slowing faster than what would appear to be a soft landing, then lower rates likely could become a tool to prevent a recession, thereby sustaining economic growth.

Overall, however, FOMC (Federal Open Market Committee) projections for 2024 suggest the median Federal funds rate will come in at 4.6% versus 5.4% in 2023, with many economists anticipating (3) three quarter-point rate cuts starting in the year's second half.

A Focus on a Higher Neutral Rate

Now, while lower rates are on the horizon for the coming year, it's crucial to note here that we're likely not going back to pre-pandemic zero-interest rate policy levels anytime soon.

That's because policymakers never intended for interest rates to remain so low for so long.

Indeed, had policymakers in 2019 hiked interest rates to levels we have now, we likely would have experienced a severe recession as we anticipated at the time (barring the effects of the pandemic, of course).

But, thanks to massive money printing and fiscal spending following pandemic-era economic shutdowns, the US economy was better positioned to tolerate Fed tightening, which allowed interest rates to effectively reset to normal levels.

That's why, in the year ahead, we're likely to hear more about terms like "R-Star" and "neutral interest rate."

And what do these terms mean?

Well, the neutral interest rate represents the "just right" rate levels where the economy is balanced and not overheating or underperforming.

So then, assuming economic growth slows and policymakers begin cutting rates this year, their focus will shift from supporting growth to finding the ideal policy rate to prevent economic overheating.

And that's where R-Star, or the neutral rate, comes into play.

Certainly, figuring out this neutral rate will be challenging.

That's because evolving inflation dynamics, shifts in global economic conditions, and changing consumer and business behaviors post-pandemic will not only keep policymakers on their toes, they'll also likely offer another critical factor influencing this year's market narrative.

Don't Bet on Lower Rates

Indeed, as central banks dial in their models to identify R-Start or the natural rate level, financial markets, naturally, will be hard at work trying to get ahead of policymakers, likely influencing business and consumer borrowing costs along the way.

Here again, the focus isn't so much on a "pivot" but rather on an ideal neutral rate level.

That's why, in the year ahead, even though interest rates are likely to fall, you should still consider approaching borrowing to purchase big-ticket items in a cautious manner.

And why's that?

Well, while interest rates are likely to decline in the year ahead, there's still a possibility that they likely won't fall as fast as we've seen in past business cycles.

And so what this means for you is that if you're borrowing to make a big-ticket purchase now because you expect significantly lower rates down the road, you could be in for a rude surprise.

That's why it's crucial to consider the impact of potentially higher-for-longer borrowing costs on your finances, especially for mortgages or large business loans and consider debt service affordability based on your current financial circumstances rather than anticipated lower interest rates.

Market Outlook: More Balanced Market Risks and Returns

Alright, so now that we've discussed the economy and monetary policy outlook, the last thing we'll take into consideration is the market outlook.

And so, where is the market headed in 2024?

Well, while nobody I know has a crystal ball, the key takeaway from what we know and expect to happen in the year ahead is to remain flexible and adaptable to ever-changing market conditions.

More specifically, while the markets could continue to rally because rates are expected to fall, market returns could turn out to be more balanced than what we saw last year.

Indeed, in the current market environment, the equity outlook is likely to be marked by a mood of cautious optimism.

That's because the Fed Pivot celebration that has driven asset prices higher in recent months likely will give way to a reflection on fundamentals and what fair valuations look like in a more normalized rate environment.

As a result, we're likely to experience bouts of market ebbs and flows as investors once again try to divine Fed speak in anticipation of a target for policy rates.

Add to this last year's substantial risk asset rally, and many professional investors will likely turn their attention to fundamentals, like earnings multiples, with a focus on sustainable growth and resilience in a still uncertain environment.

And when it comes to the bond market, the picture here remains mixed, but positively biased.

That's because the prospect of falling interest rates is likely to be supportive of bond prices overall, with some performance discrepancies likely surfacing in already richly valued high-yield and emerging market sectors.

Even so, the silver lining here for fixed-income investing is that as rates stabilize at higher levels, they likely could revitalize the bond market as an attractive long-term savings destination should zero-interest-rate policies finally fade into the sunset.

Nevertheless, bond quality and duration will likely remain the key focus as we navigate the current economic landscape.

That's why taking a selective approach in the bond market will be essential to optimizing returns and managing risk in a changing interest rate environment.

Longer-term Investment Opportunities

Overall, expectations are set for modest risk asset gains in the near term and higher risk-adjusted returns over the longer term should the neutral risk-free rate stay pegged higher.

Even so, the start of the year is a crucial time to reevaluate your investment strategy to ensure you're on the right track.

Sure, you may be tempted to just "let it ride" when it comes to your portfolio this year, but some caution is still warranted.

More crucially, given the evolving economic and market landscape, now may be a good time to ensure that your current asset allocation is optimally aligned with your long-term lifestyle and savings goals.

And what does this look like?

Well, to effectively reevaluate your asset allocation strategy in the current market climate, start by revisiting your long-term life goals, reflecting on how you plan to use your money to get there, and evaluating whether your risk tolerance reflects your desired outcome.

This is an essential topic we discussed last month and worth considering now as you plan for the year ahead.

Nevertheless, at the very least, consider the market and economic outlook presented here today, and ask yourself if your company stock concentrations and sector allocations held in your investment portfolio are still suitable in the current market environment. Then, adjust your portfolio to align with your long-term strategy so you can ensure its geared to weather the market's ups and downs this year.

A Balanced Market Outlook for 2024

You know, when it comes down to it, economic and market forecasts often miss their targets, as evidenced by the unpredicted developments in 2023.

Even so, their value to investors is found in acting as a directional guide rather than a precise predictor of future events.

And so, as we look to the year ahead, we anticipate modest financial market returns, directionally supported by the Fed's rate normalization, which could unfold in an environment of still solid growth.

With all that said, we're guided by another quote from John Maynard Keynes, and that's that "...when the facts change, I change my mind."

So then, while we have a general idea of the factors that may affect the global markets and economy this year, it's crucial, now more than ever, to remain nimble.

That's why its crucial to square up your cash management plan and prepare to service debt at higher rates, all the while maintaining a disciplined investment strategy reflective of your overall risk tolerance.

Doing so won't just help you navigate the uncertainties of the year ahead, these moves will help take you one step closer to becoming the master of your own financial independence journey.

What Benjamin Graham Can Teach Us About Investing when the World is Falling Apart

Lately, it feels like we're staring into an abyss that makes even the most seasoned investors want to get out of the markets.

It feels like there's a lot that's going wrong with the world right now, and many things are quickly coming to a head.

That's because, among many developments, the Middle East has once again become a flashpoint for geopolitical tensions.

Now, conflict in the Middle East is nothing new for the seasoned investor.

In fact, these uncertainties have largely become a typical part of the investing narrative for the past few decades.

But with that said, something FEELS different.

And now this change in sentiment comes as the US is at risk of being pulled into another regional conflict as it rightfully supports its close ally Israel following the tragic terrorist attacks in early October.

Now, on any other day, this latest military ramp-up likely would be just another typical day in the region.

But things are different now than where they were over two decades ago.

That’s because the US is already fighting a proxy war with Russia in Ukraine, while the potential for a conflict with China in the Taiwan Strait increasingly feels less like a matter of "if" and more of "when."

And why does this matter?

Well, such an outcome could potentially leave our country exposed to three simultaneous theaters of war at a time when trust in the media, trust in our politicians, and, most importantly, trust in our neighbors and our communities is plumbing all-time lows.

In many ways, it feels like we're staring into the abyss of calamity that's coming at us from all directions and society appears to be coming undone at the seams.

So then, what should an investor do at such a time of instability and uncertainty?

Should you move to the sidelines and wait until things settle down before risking more of your hard-earned wealth in this market?

Well, the simple answer here is a resounding "no."

In fact, while things feel different, they also appear eerily familiar.

That’s why one of the greatest investing minds, Benjamin Graham, likely would argue that now is the time to strap yourself in and focus on your disciplined investment strategy.

Laying the Groundwork for the Intelligent Investor

Alright, so what qualifies Graham in today's market environment?

Well, while he's widely known for his work in the book, "the Intelligent Investor," his earlier work with David Dodd laid the groundwork for what would become the authority in behavioral finance, and influence the disciplined strategies used by many professional money managers during times of heightened market volatility.

You see, before writing the "Intelligent Investor" after World War 2, Graham and Dodd wrote a book called "Security Analysis," which is a fundamental read for any budding investment professional.

In fact, this book is often widely touted by the likes of Warren Buffett and is a primary source when it comes to learning the basics of value investing.

And so, how is this book relevant almost 100 years later?

Well, consider the context in which it was written.

You see, Security Analysis was written by Graham and Dodd at a time when the investing world was coming unhinged and in a seemingly perpetual state of upheaval.

That's because the economic landscape during this time was shaped largely by the aftermath of the stock market crash of 1929, which precipitated the worst economic downturn in modern history.

Now, many of you likely will recall that in the years leading up to the market crash, speculative excesses ruled the day on Walls Street, with numerous investors borrowing money to purchase stocks all the while banking on the hope that the price of the day's meme stocks would rise to the moon.

Sound familiar?

Well, as one would expect, this approach ultimately failed spectacularly and left the finances of many individuals in tatters.

And adding insult to injury, many banks were also caught up in the speculative boom and bust because many of these institutions had extended risky loans on speculative bets. And so, as these loans soured and the economy spiraled, a domino effect of bank failures ensued, leading to the Great Depression.

So then, almost simultaneously, the markets were collapsing, the banking system froze up, the economy was on the brink and social and political agitations in Europe and Asia were setting the stage for the start of the Second World War.

Any of this sound familiar at all?

A Disciplined Process

To be sure, we’re living in a time of social disharmony, political fragmentation, and low trust in news media. From a fiscal perspective, the government has borrowed so much that now its ability to meet its obligations to its own citizens is in question. And all of this is happening at a time when our country’s global influence is being challenged on all corners.

So, now that we’re once again on the brink of a global conflict that could involve any great power countries, what lessons can we take from Benjamin Graham’s writings to help stay grounded?

Margin of Safety

Well, to begin, one of the foundational principles of Graham's investment philosophy was introduced in the concept of a margin of safety, which means investing in securities only when they are priced significantly below their estimated intrinsic value.

And, you'll likely recall that intrinsic value is just a fancy way of saying what a security is worth when you factor in the earnings ability of the underlying firm.

Now, the difference between the intrinsic value and the purchase price represents that margin of safety and provides a buffer against unforeseen events or mispricings. In other words, what Graham is telling us to do is to focus on buying assets that cheaply valued, or are on sale.

And why is this important?

Well, it's crucial because in uncertain times, when the future is even more unpredictable, many investors want to sell even high quality stocks. So then, when geopolitical risks and uncertainties rise, now may be the time to check out the discounts.

Mr. Market

Another lesson we can take away from Graham's experiences is his observations of Mr. Market.

Now, Mr. Market represents the stock market's day-to-day fluctuations and the often-irrational behavior of market participants.

You see, Mr. Market is a manic-depressive character who offers wildly varying prices for shares, swinging between undue pessimism and unwarranted optimism.

And so, the key takeaway here is to not be swayed by the daily noise and sentiment of the news or what you see going on in the broader market due to economic or geopolitical concerns.

To be sure, instead of being reactive, Graham reminds us that it's essential to stay grounded in your own analysis, convictions, and to take the long-term perspective.

Indeed, in a world filled with noise and panic, keeping a level head and not being swayed by the crowd is essential now more than ever.

Focus on What You Can Control

Finally, in the book, “the Intelligent Investor,” Graham emphasizes the importance of focusing on what you can control.

And so, what does this look like?

Well, it involves approaching your investing decisions from the perspective of thorough analysis and a clear understanding of what you're investing in.

And, ultimately, this means concentrating on factors within your control, like your research, your analysis, your decisions, and your reactions.

And in broader life terms, this means focusing on your own actions, responses, and preparations made to manage your wealth rather than getting overwhelmed by global events beyond your control.

Indeed, while it's crucial to be informed, it's equally important to recognize where your influence begins and ends, so you can channel your energy towards areas where you can make a real lasting impact.

Takeaway Lessons

Alright, now, while Graham's work primarily addressed investing, the core of his teachings is about being rational, having patience, and being prepared when the world turns upside down.

Indeed, in a world teetering on the edge of various crises, these principles can guide not only your financial decisions but also your general approach to navigating uncertainty.

So then, how can you apply these principles to your life today?

Lesson 1: Margin of Safety

First, start by cultivating your own margin of safety.

You can do this by not only prudently evaluating your investment decisions but also prioritizing building a financial cushion in your personal finances.

And you can start by evaluating your current financial situation and determining how much more liquid assets you should have set aside from one month to the next to fortify your financial position against potential economic and market uncertainties.

Lesson 2: Ignore Mr. Market

The next point to consider here is to not get swayed by Mr. Market.

And how do you accomplish this end?

Well, you can start by turning off financial entertainment news and by staying consistent in your financial planning strategy, regardless of what's going on in the world around you.

More specifically, what you’ll want to do in this situation is ask yourself if you're making financial decisions based on research and analysis or whether the erratic emotions of the market are influencing your behavior.

This way, by not getting swayed by the daily fluctuations and sentiments, you're ensuring that your financial decisions are grounded in a long-term perspective and research, which can protect you from knee-jerk reactions and potential big financial losses.

Lesson 3: Focus on Your Locus of Control

Finally, concentrate on what's within your control by focusing your energy on actions and decisions that are directly within your sphere of influence.

And so, how do you do this?

Well, you can start by asking yourself what aspects of your financial life you can control and improve upon rather than stressing about global events that are beyond your grasp.

Indeed, by centering your attention on areas where you can make a tangible impact, you can enhance your financial well-being and mental peace, ensuring that you're proactive in areas that matter most while avoiding unnecessary stress from external factors that you can’t control.

How to Invest on the Edge of the Abyss

You know, when it comes down to it, the shadow of the past looms large, reminding us of the eternal dance between calm and chaos, profit and peril.

And make no mistake, no matter how much we’ve been through over the past few years, something clearly feels different all the while feeling eerily familiar.

Indeed, while today's market, economic and geopolitical situation may mirror the eeriness of bygone eras, we’re fortunate enough to benefit from the lessons learned from individual who have lived through similar situations.

So then, the tools and techniques that weathered storms in the past remain our lighthouse, guiding us safely through the tumultuous waves of the present.

Indeed, as we stand on the precipice of the abyss, staring into the swirling vortex of global tensions, economic upheavals, and political theatrics, it's crucial to remember the wisdom of investing visionaries like Graham.

Remember, his professional experiences, born out of the crucible of adversity, offers invaluable insights into not just surviving but thriving as you take one step closer to becoming the master of your own financial independence journey.

Markets are Primed for a Pullback

Evidence suggests that this year's risk asset rally is likely primed for a pullback.

So now, why now?

Why the glum news after the S&P 500 index posted one of its strongest year-to-date gains in a while?

Well, it's essential to remember that most market activity is underpinned by a narrative or a story that influences price swings either higher or lower.

And this year's rally isn't any different.

To be sure, the consensus view among many investors this year was that the Federal Reserve (the Fed) would finally beat inflation by aggressively raising interest rates.

And, while higher rates are typically a market headwind, investors bet that the Fed's aggressive moves would eventually tip the economy into a recession, prompting policymakers to reverse course sooner rather than later.

Now, the Fed tends to cut rates to get ahead of rising unemployment, which tends to happen during a recession, and so financial markets interpret falling interest rates as supportive of market prices.

And so, while headline inflation has fallen this year, the long forecasted recession has failed to materialize.

Now, in any other situation, this would be a win for households, businesses, and policymakers alike.

But the fact that the US economy continues to hum along even as it's now more expensive than ever to borrow money suggests that the fight against inflation isn't over yet, and the story many investors have been betting on this year likely won't happen as quickly as once hoped.

Adjusting Market Expectations

To be sure, according to implied Fed Funds futures coming into the start of this year, market participants expected the Fed to take higher throughout the year before eventually cutting Fed Funds to around 4.25% by December.

Now, as of the end of August, with the Fed funds rate sitting around 5.25%, that same futures data now suggests that policymakers will actually keep rates where they're at now and avoid cutting rates through well into the first half of 2024.

So then, what does this outlook do to the current market narrative?

Well, the truth is that the narrative that had driven asset prices to current levels is likely losing steam, even as higher interest rates have exposed fractures in the regional banking sector, as we discussed some months ago.

Now, what this means is that with interest rates staying higher for longer, there's more risk that something in the economy or financial system could come undone. But for now, economic and systemic concerns appear measured enough for policymakers to hold tight on current monetary policy.

Supply-side Inflation Normalizing

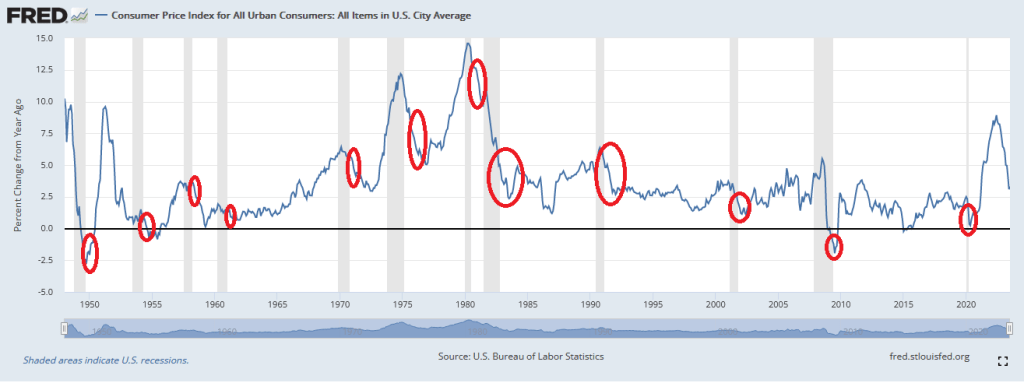

So then, with all that said, it's crucial to note that higher rates likely have influenced inflation's slowing, but the battle isn't over yet. Indeed, headline inflation, which includes food and energy prices, peaked at around 9 percent last June and has since slowed to 3.3 percent through July of this year.

At the same time, core PCE inflation, which is a better gauge of underlying inflationary pressures, peaked at 5.4 percent in February 2022 and declined to 4.3 percent in July.

So then, from this perspective, falling prices should be good for the economy and the markets, right?

Well, while slowing price growth is indeed a positive market development, the drivers of inflation are different now than they were three years ago. More specifically, it could be argued that the cause of today's inflation plight started with supply-side drivers and is now being carried along by demand-side momentum.

And what do we mean here?

Well, you likely experienced the full effects of supply-side inflation during the lockdowns when prices shot up at the supermarkets due to a shortage of goods. In fact, the cost of most goods and services started to increase as everything from toiletries to personal protective gear to cars, semiconductors, and appliances were in short supply, ultimately making most everything more expensive.

That's supply-side inflation, or when prices rise because there's not enough of something to go around.

You see, when inflation first started taking off in 2021, Fed policymakers and indeed central bankers globally turned a blind eye to the problem, assuming that these price moves would only be temporary or what they call transitory.

In other words, they assumed that once pandemic-era supply chain bottlenecks eased up or more goods were available to go around, prices would eventually return to normal or, at the very least, inflation would slow as more products hit store shelves.

Indeed, after hitting a post-Global Financial Crisis peak in 2021, international shipping costs, as measured by the Baltic Dry Index, are today trading around average levels. What's more, overland freight shipments tracked by the Cass Freight index show that activity has slowed over the past year, which likely suggests that store shelves are likely being stocked at normal levels again.

So then, if supply-side inflation appears to be normalizing, then what's the issue?

Changing Inflation Drivers

Well, the concern today isn't so much about supply-side inflation as it is about demand-side inflation.

Indeed, the pandemic not only exposed the shortage of goods in the economy, it also highlighted the shortage of workers for essential jobs. That's why, after years of resistance, many firms decided to raise prices to pass along various costs, including the higher wages needed to draw in more workers.

And when you have hundreds of thousands of individuals making 20% more than they were before the pandemic, then you have a recipe for demand-side inflation.

And what is demand-side inflation?

Well, you'll likely recall that with supply-side inflation, prices rise because there is an equal amount of money chasing fewer available goods.

So then, with demand-side inflation, you have prices taking off because individuals have more money to spend, which means more money chasing after an equal amount of goods and services.

Now, earlier this year, the Fed assumed that it would be able to put a lid on this demand-side inflation by tipping the US economy into a recession through its aggressive monetary policy.

That's because history has shown that demand-side inflation tends to follow suit when the economy slows as businesses lay off workers and households think twice about spending money.

Hence, wage growth and spending both slow.

And so, coming into the start of this year, market watchers and economists alike were betting on the narrative that slowing growth and the potential for a recession could pull the legs out from under the economy and hence allow the demand side of inflation to finally cool off.

But that doesn't seem to be the case today.

How come?

Well, that's because labor market and household spending data, while having softened in recent months, continues to show that the US economy is much more resilient than most had anticipated, prompting many economists to revise higher their year-end US GDP forecasts.

To be sure, this view was solidified by the fact that the Fed's economists had, for all intents and purposes, stopped projecting a US economic recession.

And even at last week's Jackson Hole presser, Fed Chair Jay Powell indicated that economic growth has been stronger than expected and, so much so that now there are concerns among policymakers that if this growth trend sticks around, it could put further upward pressure on inflation, which would require more rate hikes heading into 2024, instead of the rate cuts that markets had expected.

Primed for a Pullback

So then, what should we make of this year's rally?

Should we throw in the towel and move to the sidelines since the narrative seems to be changing?

Well, not so fast.

You see, market narratives evolve and change all the time. They turn on a dime, as they say.

Indeed, that's where we get the old adage, "buy the rumor, sell the news…"

With that said, adapting to changing plot lines is a way of life for most savvy investors.

And the truth is that we've been here before.

In fact, it was precisely this time a year ago that the markets were obsessed with a Fed pivot and were sorely disappointed with Jay Powell's comments about bringing pain to the economy at last year's Jackson Hole Symposium.

You'll also recall that the late summer selloff set the stage for a bull market rally that took hold this year.

Now, make no mistake, we're not calling for an all-clear or a repeat of last year's events.

To be sure, persistent demand-side inflationary momentum and shifting market narratives suggest that markets are likely primed for a pullback in the weeks ahead.

Indeed, with the economy still primed to produce higher prices, the prospects of a year-end rate cut have all but faded away, and now, investors are trying to figure out a new story, or a new narrative, to carry the market momentum forward.

And so, history has shown that market volatility tends to pick up when investors are trying to piece together an investment thesis or story they can sell to themselves, to their investment committees, and to their clients.

Indeed, until markets can get a consensus view on a new market narrative, expect more significant day-to-day and week-to-week price swings.

Either way, staying agile, well-informed, and ready to pivot based on evolving circumstances in this market will be essential to taking one step closer to becoming the master of your own financial independence journey.

Bull Markets, Shifting Catalysts and Evolving Narratives

Stocks in the US are back in bull market territory this month but don't tell that to the market bears.

That's because it seems like just around every corner, there seems to be a risk that could take the steam out of the current rally and send risk assets into a sharp drawdown only matched by those related to recent economic, political, or security dysfunction.

Make no mistake, this year's risk asset rally is likely to be one of the most hated bull markets in history. That's because some major indices continue to charge higher even as various indicators point to hazards ahead for the US and global economy and hence, corporate earnings that underpin corporate asset valuations.

And you see, this is a particular problem for some investors because the thinking goes that it's foolhardy to be fully invested at a time of rising interest rates, slowing economic activity, and looming geopolitical risks because these events have the potential to topple risk asset prices that already appear to be overvalued compared to many historical measures.

Even so, some market bulls are taking even greater risks as they look past events that are likely already priced into the market and shift their focus to up-and-coming developments that could supercharge economic growth over the next decade.

So, who's got it right?

Is the current rally nothing more than a bull trap, that could lead to a renewed bear market and set the stage for one of the sharpest downturns in quite some time, as rising interest rates trigger the next bank panic and economic recession?

Or does this bull market have legs, and will it continue to charge higher into the second half of the year?

Now, while it's still unclear whether bulls or bears are making the right call, which way the market goes in the months and year ahead will likely depend on the dominant market narratives currently underpinning investor sentiment.

How Narratives Influence Market Behavior

And, so what do we mean when we talk about market narratives?

Well, a market narrative is a story that market participants tell themselves to rationalize a near-term or long-term investment decision. To be sure, all you need to do is turn on financial news channels or scroll through social media to get a sense of the story that some market participants are telling themselves and others as they defend their investment views.

And while these views can range from a call on a particular stock, sector, or asset class within the markets, what often drives the broader direction, and hence general investor sentiment, is the macroeconomic narrative.

And what do we mean here?

Well, let's use a hypothetical example to illustrate this point. Imagine we're back in a period of prolonged economic stability, like between 2014-2019. During this time, GDP had been rising steadily, unemployment was at historic lows, and inflation was largely under control.

Generally speaking, in a stable period like this, it created a prevailing narrative of continual, albeit moderate, growth in US corporate earnings.

As a result, risk assets went on a bullish run, with many indices hitting all-time highs. In fact, from the start of 2014 to the end of 2019, the S&P 500 index nearly doubled in value. That's because investors got used to this steady-state, predictable, low-volatility market environment and just kept buying, driving prices ever higher.

Now, you'll likely recall that the narrative at the time was that while the Fed would have to raise interest rates to curb potential economic and market asset bubbles, but it was constrained by the economy's addiction to near-zero interest rates and stubbornly lower inflation that wouldn't move no matter what policymakers threw at it. Therefore, low-interest rates and easy money policies would allow stocks to rise for an extended period of time.

So then, when we think of market narratives from this perspective, it's this sort of thinking that shapes investor behavior, making them more risk-tolerant as they come to expect that the good times will continue. This outlook led to increased investments in equity markets, higher asset prices, and arguably the formation of asset bubbles.

At the same time, economic participants, namely households and businesses, had also become influenced by the narrative as well. Given positive investor sentiment, firms had been more willing to issue new stock or debt offerings, and many investors readily stepped in to buy them up.

What's more, financial institutions continued to openly lend at low-interest rates, fueling economic activity even more, and households gladly opened their wallets to spend.

Now, let's say new information emerges that challenges this narrative. And what could this be?

Well, this catalyst, or new information, could come from reports of potentially disruptive geopolitical tensions, or signs of an economic slowdown in the US or some major economy abroad. And why are such developments relevant when everything else seems to be going ok?

Well, this new narrative of impending uncertainty has the potential to shift investor sentiment quickly. And when an unfavorable catalyst crops up, the risk-averse investors might start pulling out their investments, leading to a selloff in the markets, increased volatility, lower asset prices, and a decline in economic activity.

At the same time, this narrative shift could affect corporate and financial institution behavior as well. That's because firms might hold off on issuing new securities given the uncertain environment, and banks might tighten their lending standards.

How New Catalysts Lead to Narrative Shifts

Alright, now it's critical to note that these narratives don't operate in isolation. That's because they're constantly interacting with catalysts like changing economic data, government policies, and geopolitical tensions that can influence investor psychology. To be sure, when new catalysts present themselves that challenge the current market narrative, it can become a self-fulfilling prophecy, where the belief in a narrative can cause actions that make the narrative come true.

For example, if investors believe there will be a market downturn, their selling activity can actually cause the downturn. Indeed, if we extend our earlier narrative example beyond the end of 2019, you'll likely recall that an unexpected catalyst in March 2020 led to a dramatic shift in the market narrative.

And do you recall what that catalyst was?

That's right, it was the US government announcing a national emergency in response to the COVID outbreak, which paved the way to an unprecedented economic shutdown and trillions of dollars of stimulus to support the economy and markets. Initially, the national emergency announcements led to a sharp market selloff due to the negative catalyst that was the pandemic, but later supported by a positive catalyst that included supportive actions by policymakers that paved the way for an extended market rally only weeks later.

This process underscores the importance of monitoring and understanding the prevailing market narrative and potential catalysts, as they can greatly influence investor behavior, market activity, and, ultimately the economy at large.

Narratives and Catalysts in the Current Environment

Now, considering where we are today, it would seem that there is still some uncertainty about the dominant market narrative. To be sure, the debate between bulls and bears is what leads to price discovery and makes for a more-or-less healthy functioning market. And more often than not, those debates and how they play out in the market through price action are not just about the dominant narrative but also about how various catalysts could potentially influence the direction of the prevailing market story.

So, what are the catalysts that are currently under consideration by market participants?

Well, the dominant catalysts likely up for debate affecting the broader narrative center on 1) inflation, 2) central bank policy, 3) financial instability, and 4) the potential for an economic downturn.

Inflation and Interest Rates Normalizing

Now, as it relates to the first two points on inflation and central bank policy, you'll likely recall that uncertainty surrounding where inflation was headed coupled with the fact that policymakers seemed asleep at the wheel, were the catalysts that led to last year's bear market selloff.

Indeed, inflation that was supposedly transitory due to supply chain constraints transformed into stickier, widespread price hikes from across most economic sectors, leading to declining purchasing power and dented household wallets and confidence.

Now, it's essential to note that central bank policymakers usually aim for a low and steady inflation rate as their target because price stability allows for better financial planning and fosters overall economic well-being among households. That's because when prices are stable, households can more accurately predict their expenses, which makes it easier to budget and plan for the future.

And, so, without price stability, it's difficult to know how much money you'll need to spend on essential goods and services. And when this happens, it can lead to uncertainty and possibly financial hardship. And it was this catalyst that many market watchers had been calling out for quite some time. And, when Fed policymakers finally reversed their stance on “transitory” inflation and began rapidly raising interest rates 18 months ago, the dominant market narrative shifted.

But now, with headline inflation having fallen to just over 4% in May for its lowest reading since April 2021, and producer price inflation falling for 11-straight months, it appears that the two catalysts that had threatened economic stability, that is, high inflation and high-interest rates are likely to come back to normal soon.

And for many of the bulls out there, it's arguably this outlook that has renewed investor demand for risk assets, and underpinned the current market rally as many market participants are looking past the risk of high inflation, and now pricing in central bank rate cuts by the start of next year as price stability returns to the US economy.

Financial Instability and Economic Recession

And so, if inflation seems to be stabilizing and bringing policymakers to the point of normalizing interest rates, you might be asking yourself, "Well, what about the lingering financial instability issues and the looming economic recession on the horizon? Don't these catalysts have the potential to derail the current bull market rally?"

Well, the short answer is: it depends. On the one hand, a spreading bank contagion could bring into question the health of the US and global financial system and spark a greater crisis of confidence in US and global financial markets. To be sure, this risk, while less noticeable than it was a few months ago, remains a salient threat. That's because, even as headlines surrounding the failures of small regional US banks have eased, data according to the Federal Reserve show that banks are three times more reliant now on emergency borrowing from the central bank than during the height of the pandemic.

What's more, the latest Senior Loan Officer Survey shows that both large and small US banks are tightening lending standards and reducing overall lending to businesses and households. Indeed, in recent months, many financial institutions have announced planned exits from various auto lending and mortgage markets. And with central bank policy rates poised to rise to their highest levels in two decades, market bears could argue that it's all but certain that an economic downturn is just around the corner.

So, with all that said, it's possible that these two catalysts may have less bite than their bark. Make no mistake, many financial institutions are facing significant risks. Yet, it could be argued that the current plight of banks adjusting to higher interest rates likely has more to do with balance sheet management practices, than general systemic concerns related to the quality of assets held by these banks.

Indeed, this is a topic we wrote about several weeks ago and pointed out this distinction. Even so, the banks' precarious position is likely to make them less willing to lend, especially at a time when collateral backing many of the loans, like real estate and autos, are falling in value along with the decline in overall inflation.

And what about this recession that we've been waiting for the past year? Well, it's true that higher interest rates have historically led to lower hiring activity and so the potential for layoffs, and subsequent weaker household spending remains an elevated risk.

Even so, this labor market has been one of the most stubbornly strong markets we've seen in decades. To be sure, compared to historical recessionary periods, labor market data this time around has been more resilient, suggesting that, while economic growth likely will slow into the end of the year as many economists predict, a rise in unemployment likely could be less severe than we've seen in cycles past.

Bull Markets, Evolving Narratives and Shifting Catalysts

So then, assuming that inflation and interest rates come down to more normal levels, regional banks find their footing, and the economy experiences a soft landing in the second half of the year, then, there is a case to be made that this bull market has legs.

Again, you might ask yourself, "But aren't valuations already stretched?" and "Isn't the current risk asset rally being led higher by a handful of the largest companies?"

Certainly, from this perspective, some assets appear overpriced. These assets are largely tech related that have rallied in line with expectations that artificial intelligence will lead to future economic efficiencies. With that said, however, many assets remain attractively valued given the market selloff we’ve seen over the past twelve months.

Now, add to this the fact that there is a historic $1.3 trillion parked in retail money market mutual funds and a case could be made that we might see a reallocation in the bull market currently supported by a handful of expensive names to one supported by a broader base of cheaper or fairly valued names as cash moves back into the markets once retail investors are convinced that negative market catalysts are likely to have less of an impact on the overall market narrative.

So then, from this perspective, is now the time to dive into risk assets? Well, if you've been trying to time your way into the markets this year, then you likely missed out on a number of opportunities. Indeed, if you've been following along with us this year, we've made a strong case for remaining fully invested in the markets despite perceived headwinds.

So, who's got it right?

Is the current rally nothing more than a bull trap, that could lead to a renewed bear market and set the stage for one of the sharpest downturns in quite some time, as rising interest rates trigger the next bank panic and economic recession?

Or does this bull market have legs, and will it continue to charge higher into the second half of the year?

While the sustainability of the current bull market rally is questionable, we remain cautiously optimistic on the outlook for the US economy and financial markets alike. Here again, we believe that investors should remain fully invested in the markets and not try to time their way in and out in anticipation of changing market narratives. Rather, you're likely best served by remaining committed to your disciplined long-term investment strategy.

Elections: Why You Shouldn’t Mix Politics and Your Portfolio

Investing based on political preferences can be bad for your portfolio.

As the 2024 presidential election approaches, Americans are preparing to vote in what polls forecast to be a tight race. And, like many investors, you may wonder how the election outcome could affect financial markets and whether your investment strategy should change should one party take office over another.

Well, while elected leaders can influence economic growth by enacting laws and regulations, data suggests that who occupies the White House has little to no impact on investment performance.

Fundamentals Matter More

That’s because fundamental factors like corporate earnings growth and valuations impact the stock market far more than political headlines. And while politicians make many promises during election years, more often than not these often go unfulfilled because of the government’s system of checks and balances.

Moreover, the economic outcomes of policies are less predictable than officials think, with the economy more influenced by factors like job growth, interest rates, and inflation.

Missing Out on Growth

To this point, the charts below illustrate the financial impact of allowing political beliefs to influence investment decisions. The chart below (figure 1) graphs the S&P 500 Index starting with Dwight Eisenhower’s presidency in 1953 and is color-coded by political party.

The graph below (figure 2) compares the investment performance of portfolio decisions made based on political affiliation.

If an investor only invested in the stock market when a Republican was President, $10,000 would have grown into $83k today, excluding dividends. On the other hand, investing only when a Democrat was President would have returned $254k.

And while the gap may seem wide at first glance, the reality is that if an investor ignored the president’s political party and remained invested for the long-term, $10,000 would have grown to over $2.1 million.

The Big Takeaway

Political views can stir strong emotions but making investment choices based on those feelings can lead to poor portfolio outcomes. Instead, it’s better to focus on a time-tested disciplined investment strategy and avoid letting politics influence your long-term strategy.

The U.S. economy’s success, growth, and resiliency don’t change with each new election, and neither should your investment strategy.

That’s why it’s best to express political opinions at the ballot box, not in your portfolio.