Are Vaccine Hopes a Shot in the Arm for the Markets?

Financial markets have posted notable gains month to date. And market optimism concerning the US elections has been amplified this week by hopes for a COVID vaccine. A key question for investors now is whether news of a vaccine will be enough to push risk assets higher through year-end, even as accelerating COVID infection rates threaten an already fragile economic recovery.

Without a doubt, the news of a means to quell the spread of this year's deadly virus is a positive development for our healthcare system, our economy, and the markets. However, of particular concern remains production and distribution obstacles related to getting the vaccine out to those who need it most. These enduring questions mean that the healthcare crisis is likely to intensify before it gets better.

Even so, we believe that the recent vaccine news combined with prospects of a concerted national response to the pandemic and potentially trillions of dollars in additional fiscal spending signals that light is beginning to shine at the end of the tunnel. If hope holds out, and the economy largely remains open, then the current market rotation into cyclical sectors could continue ahead of an economic recovery next year.

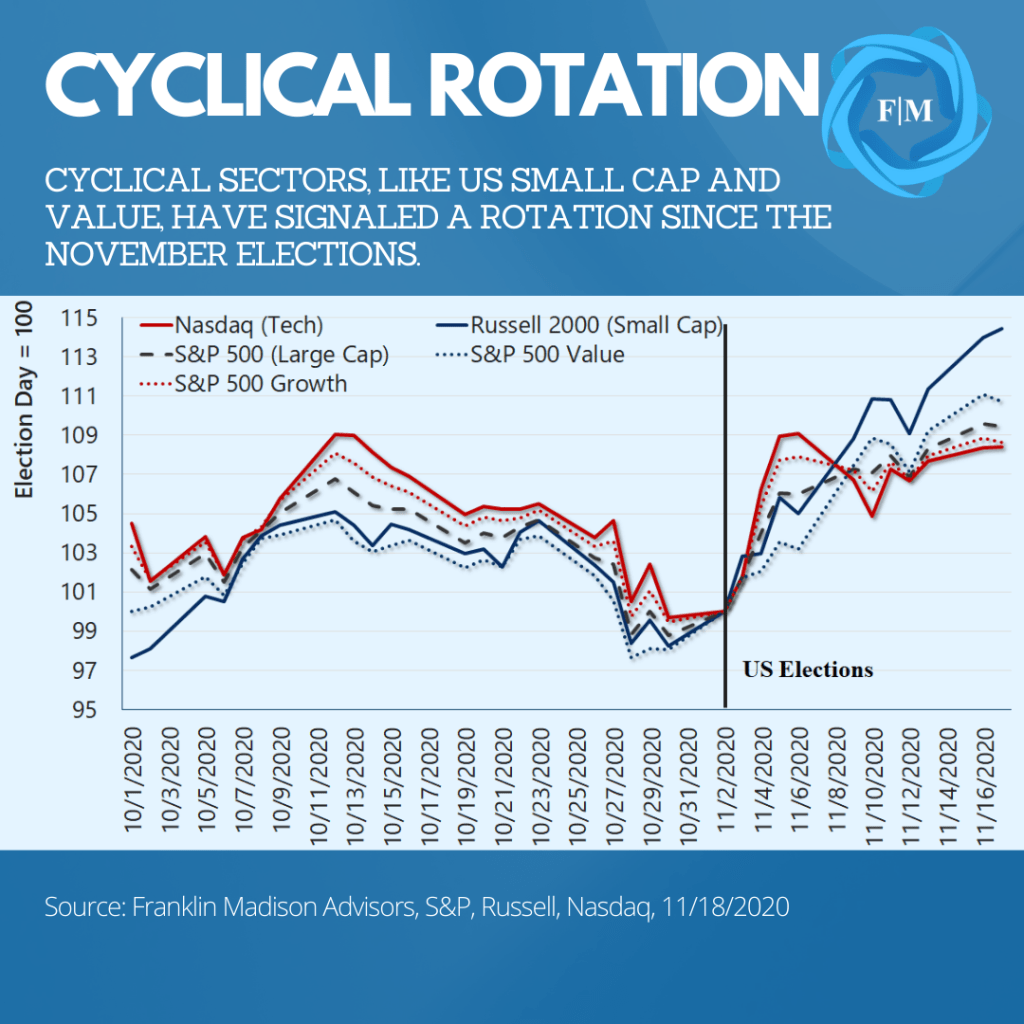

Figure 1: Cyclical Market Sectors Have Benefited in Recent Months

A Rally on Vaccine News

Markets moved higher this week on news of successful COVID vaccine drug trials announced by several large drug companies. These companies reported that their vaccines showed a more than 90% effective rate, which signals that, once the drugs become widely available, the spread of the coronavirus could be curtailed as soon as the second half of next year. With global cases topping 55 million this week, top US healthcare advisors estimate that between 75% to 80% of Americans might need to receive these vaccines to stop the spread of the deadly virus.

Production Issues

While markets indeed have rallied on the vaccine's positive news, the reality is that three key challenges stand between the end to the pandemic and a full-throated economic recovery. First, consider the production issues. One of the large drug companies recently announced that it might have as much as 50 million vaccine doses ready by the end of this year. Now keep in mind that each patient requires two doses of the vaccine to ensure immunization.

And assuming that the other drug companies that have also signaled successful trials can produce a similar quantity, we could see vaccine production reach 100 million doses to treat 50 million individuals every two months. While these production figures are considered optimistic, if we assume that only 80% of Americans need to be vaccinated, then there might be enough of the drug produced to help stem the virus's spread by the summer of 2021.

Distribution Bottlenecks

Now, production is a crucial first step to ending the pandemic, yet the next issue we'll likely contend with is the logistics of getting the vaccines to the right people. To this point, the drugs need to be stored at between negative 1- and negative 100-degrees Fahrenheit to ensure that they'll remain effective. While one company has developed a unique workaround to transport the drug, its solution will likely create a bottleneck in the vaccine's widescale distribution. This limited distribution means that receiving a vaccine probably won't be as simple as walking into your local pharmacy to get a flu shot.

Administration Fatigue

Finally, there's the challenge of handling and administering the vaccine and the potential that mishandlings could affect the stated 90% effective rate. Traditionally, drug testing occurs in highly controlled, structured environments.

However, distribution will take place in real-world settings, where anxiety surrounding the virus remains high, healthcare systems strained, and doctors and nurses burnt out and overwhelmed. Mistakes are likely to occur during vaccine administration, potentially questioning the 90% efficacy rate of the drug treatments. What’s more, while an inoculation rate of 75% to 80% could help stem the COVID spread, polls suggest that a large part of the US population is still unwilling to receive the drug. This fact alone could delay the benefits of administering the vaccine.

Even with these factors in mind, some market participants remain optimistic that the potential issues related to manufacturing, distribution and administration of the vaccine will be overcome. When this happens, social distancing measures likely will ease and struggling businesses could have a fighting chance to stage a comeback. It’s this optimism that arguably appears to be priced into the markets. That is, the potential for a sustained economic recovery, assuming that concerns about COVID begin to fade into the second half of next year.

Figure 2: US Coronavirus Infection Rates Hit Record Highs in November

Market Sentiment Cautious on a Likely Rebound

Make no mistake, markets likely will contend with COVID related issues for the entirety of 2021 and potentially beyond. Of particular concern at the moment is the rapid rise in infection rates taking hold in the US and around the world.

Infections Still a Near-term Economic Concern

This week, data from the Johns Hopkins University showed that daily average infection rates topped 160,000, besting peak infection rates reported during the summer months. This rapid rise in the coronavirus’s spread has recently led to renewed stay at home advisories, school closures, and limits on dining and social gatherings across the US. While a full lockdown of the US economy is not yet in the cards, these measures enacted at the local level could dampen the modest economic recovery that has unfolded over the past few months.

As it relates to infections, the prospects of a harsh winter arguably has been baked into many economists' GDP forecasts for the year. Expectations are set for the US economy to post a gain of roughly 4% in the fourth quarter as consumer spending and construction activity underpin growth.

This positive sentiment is playing out in the markets today. This optimism is arguably evidenced in a rotation away from the market's liquidity-oriented sectors toward a preference for pro-cyclical sectors that historically tend to do well in the early phases of an economic rebound.

Nevertheless, a key risk for the markets now is how quickly the resurgent infection rate can be quelled and what, if any, additional economic impact might come from various stay at home advisories and limited business operating hours.

Looking ahead, an incoming Biden administration focused on broad measures to address the healthcare crisis likely will give business leaders greater confidence in a durable solution to the virus's spread. What's more, the issue of another economic relief package is not a matter of "if," but "when," and this potentially could help prevent the economy from slipping further into a recession.

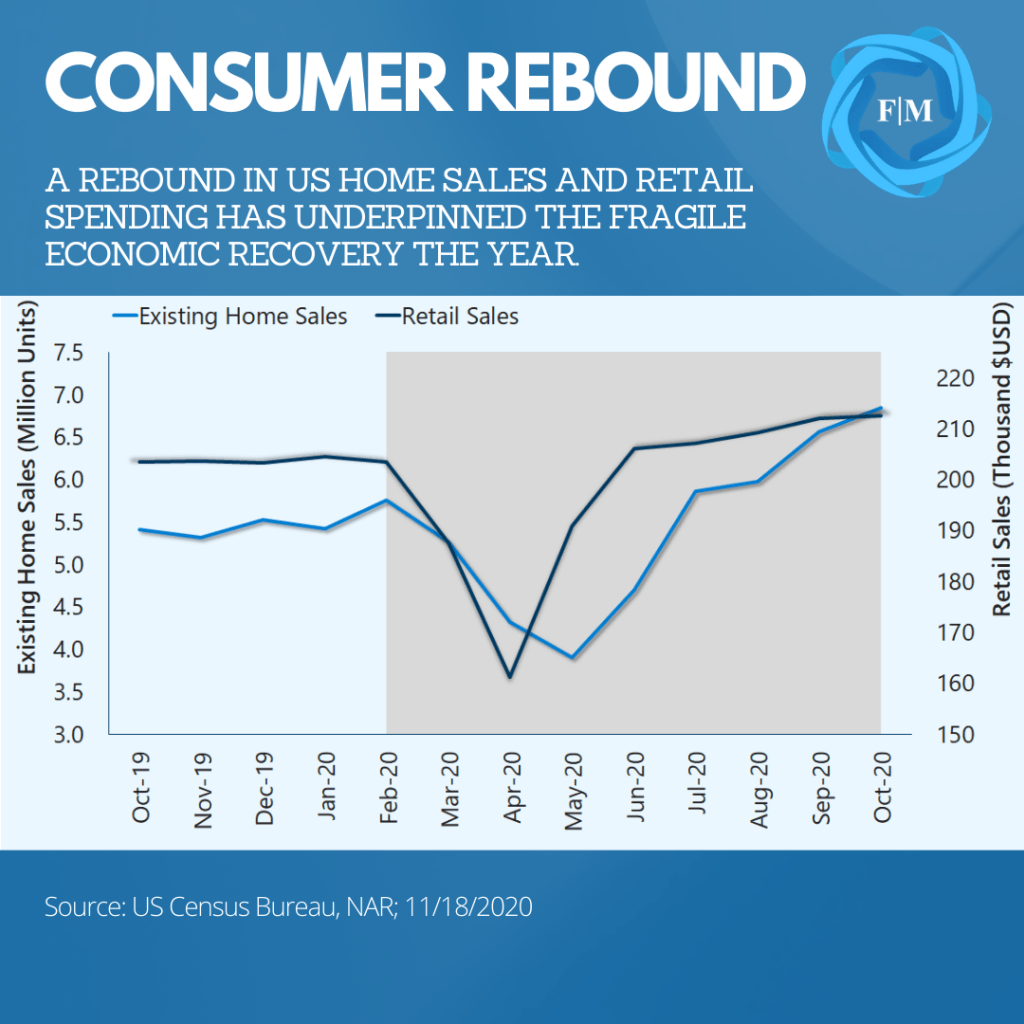

Figure 3: US Consumers Contributing to Stabilizing Economic Growth

Pricing in an Economic Recovery

From this vantage point, clarity around a vaccine, a concerted response to the healthcare crisis, and more fiscal spending may provide the markets with hope that the economy likely will recover even as near-term concerns (like rising infection rates) continue to surface.

Certainly, incoming economic data suggest that the US economy is on the mend. Business sentiment has stabilized recently, and hiring activity has somewhat improved, as evidenced by a declining unemployment rate even as weekly jobless claims remain stubbornly elevated. Consumer confidence is also steadying and evident in solid retail sales and a surge in demand for home purchases.

Cyclical sectors of the markets (those that move in tandem with the economy have benefited from an improving economic narrative and greater post-election policy clarity. These sectors include US small-cap and value-oriented stocks and a weaker US dollar that has led to gains in emerging markets. As the US economy recovers, this rotation could likely overshadow the liquidity theme that supported gains in the work-from-home and the Fed’s money printing theme that has benefited the tech sector.

To be sure, as we pointed out in last month's report, a Biden win and the prospect for higher levels of government spending has set the stage for a pivot towards cyclically oriented sectors of the markets. This view has played out in small-cap and value stocks outperforming tech in the weeks following the elections (see figure 1). Looking ahead, we anticipate this trend to continue as lingering election uncertainties fade, inauguration day passes, and business and consumer confidence steadily improve.

Are Vaccine Hopes a Shot in the Arm for the Markets?

While there is a genuine reason for markets to be optimistic about a COVID vaccine, the very real risk today is that infection rates in the US and around the globe will continue to rise. Local leaders are walking a fine line between enacting more stringent safety protocols and shuttering businesses altogether. To this point, the Fed indicated the real potential for a double-dip US recession if infection rates aren’t mitigated soon. And if this happens, the market’s appetite for cyclical investments might come to a pause.

Nevertheless, this week's vaccine news combined with prospects of a concerted national response to the pandemic and potentially trillions of dollars in additional fiscal spending in the months ahead signals that light is beginning to shine at the end of the tunnel. If hope holds out, and the US economy largely remains open, then the current market sentiment driving a rotation into cyclical sectors could continue ahead of an economic recovery next year.

Look for Investment Opportunities in a Biden Win

The outcome of next month’s Presidential Election is likely to be of great consequence for the US economy and financial markets. Given former Vice President Joe Biden’s recent gains in the polls, it’s possible that the market narrative driving markets could turn if Biden clinches a victory in November.

This narrative shift means that investment strategies that may have worked over the past six months could struggle to maintain their momentum as we move into the coming year. That’s why regardless of your political leanings, we believe that it is critical now more than ever to consider how a change in the White House might affect your investment portfolio in the coming years.

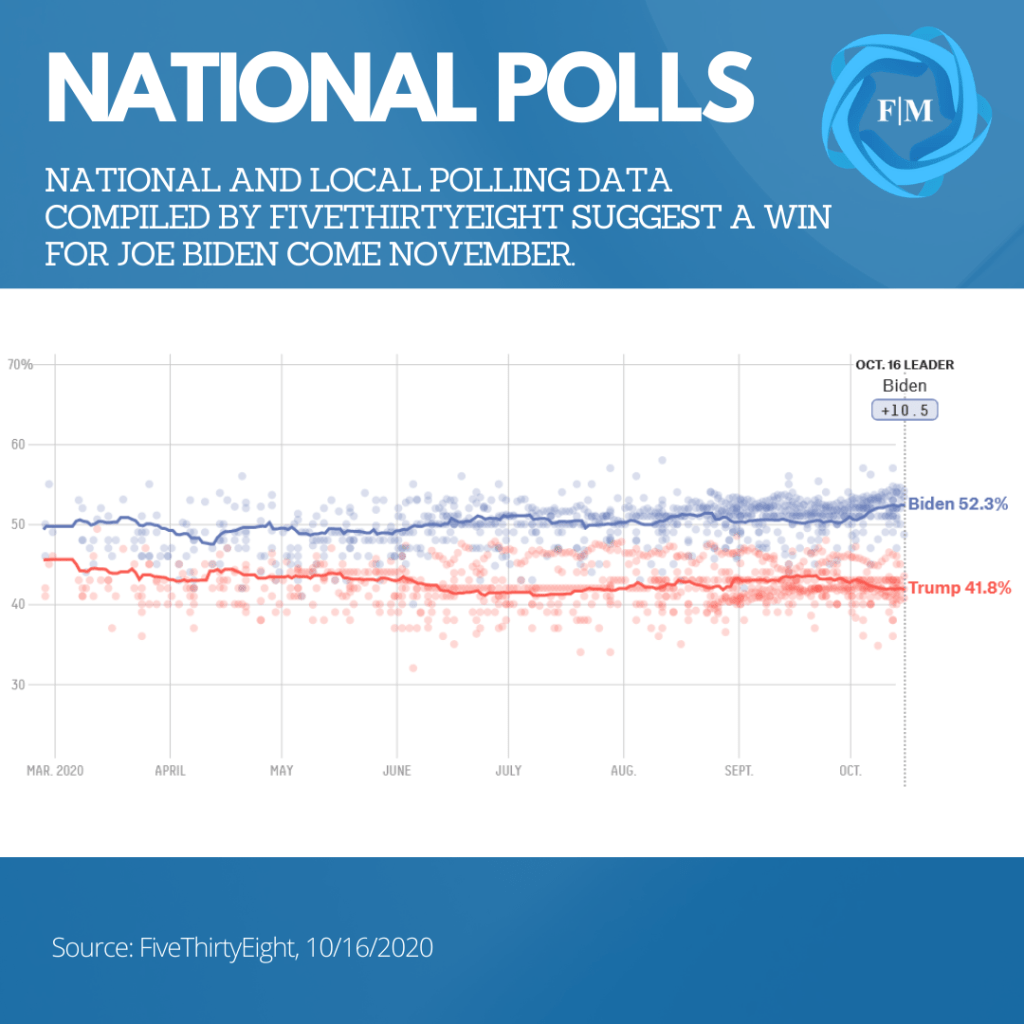

Can We Trust the Polling Data?

Who’s going to win the Presidential Election? Well, a lot can happen in a few short weeks. Nevertheless, Joe Biden has recently enjoyed a double-digit lead ahead of President Donald Trump in the national polls. According to surveys compiled by FiveThirtyEight, Biden is leading Trump by an average ten percentage points at the national level.

Even so, when it comes to presidential elections, what history has shown is that the polling data coming out of state-by-state contests are more instructive than the national figures themselves. And this point was made abundantly clear in 2016 as Hillary Clinton won the national popular vote but lost the electoral college as she trailed in battleground states.

How is Biden projected to do in these critical state races? Well, if elections were held today, data suggest a likely Democratic sweep in the Presidential and Congressional races. This outcome is reflected in data for crucial states like Florida, Pennsylvania, Michigan, and Wisconsin (states lost by Clinton) where polling is more favorable of Biden win.

So, what might such an outcome mean for your investment portfolio? Well, a Democratic sweep could bring significant changes in tax policy, fiscal spending, and infrastructure initiatives that may shift some investor preferences while at the same time bringing in a new set of investment opportunities. Let’s take a look at some of these potential changes in a little more detail.

Potential Pivot Out of Growth?

The tax plan outlined by the Biden campaign is a big deal. It’s crucial to remember that the Tax Cuts and Jobs Act (TCJA) passed in 2017 promised a boost to economic growth as tax rates on high earners and corporations were lowered significantly. Biden has promised to roll back certain provisions of the TCJA to pay for his administration’s economic policies. So, what exactly does this mean for the individual investor?

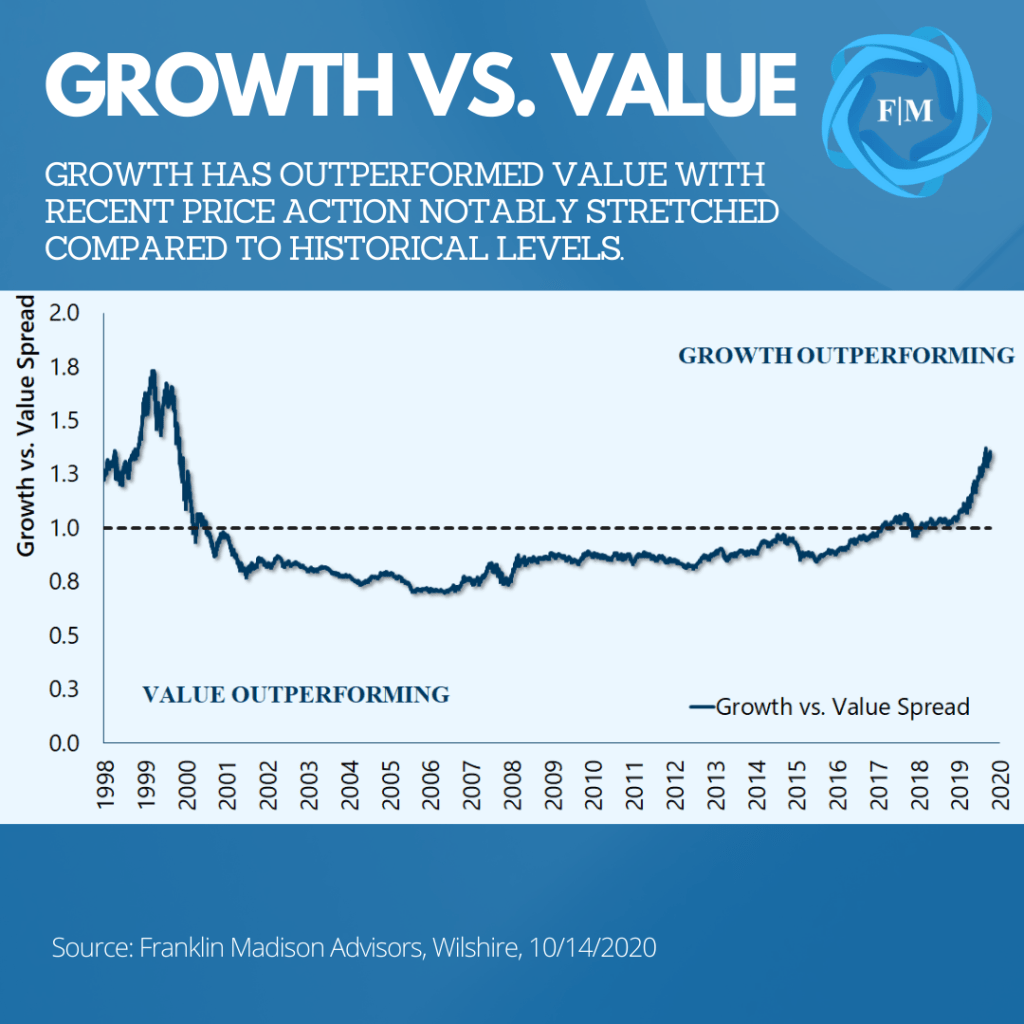

Well, under the scenario of a Biden win, there is a greater incentive for investors to cash out on asset classes that have performed well in recent years. To be sure, the rally in growth-oriented stocks has been seemingly unstoppable over the past few years. More recently, strong performance in this segment of the markets has been underpinned by a flood of cash resulting from government spending and easy central bank policies. Even so, investors will have to contend with two vital issues under a new administration.

First, the prospect of diminished after-tax corporate earnings likely will make it harder to justify holding investments already trading at a significant historical premium. Put differently, growth is expensive, and higher taxes won’t make them any cheaper. And second, the prospect of higher future capital gains taxes might incentivize some investors to lock in tax liabilities at today’s lower capital gains rates. From this perspective, it’s quite possible that the once favored growth/tech sectors could underperform the broader markets following a Biden victory.

While it might take months for a bill to make its way through congress, market participants likely won’t wait around to reposition themselves ahead of such a move. In fact, it’s quite possible that investors could rotate out of favored sectors shortly after an election day win. This means that market sectors that have benefited from lower taxes are likely to face headwinds given higher tax prospects.

Cyclical Opportunities

Another point to consider is that under a new administration, government spending will likely rise substantially due to additional fiscal stimulus and changes in economic policy. As of this writing, congressional leaders are still trying to strike a deal on another round of fiscal stimulus that would address the COVID-related economic slowdown. Whether this package is agreed to before or after the elections, another roughly $2 trillion in government spending will likely make its way into the economy in the months ahead.

This much needed fiscal boost comes at a time when data show that US economic growth is recovering but remains at risk of stalling out. Indeed, weekly jobless claims data this week showed that the number of individuals seeking unemployment benefits rose to a two-month high after declining in recent weeks. And without additional government spending, recent economic gains are likely to falter, leading to stagnating growth and a long road to recovery.

Under Democratic plans, a second stimulus bill would provide support for households and businesses and give aid to state and local governments (a point contested by GOP leaders). From an investment perspective, this additional fiscal boost to state and local governments could open the door to attractive income-oriented opportunities, most notably in the municipal bond space.

What’s more, for an economy struggling to regain its pre-coronavirus footing, relatively higher government spending levels would likely be favorable overall for economic growth. In such a scenario, the pivot away from growth-oriented sectors resulting from higher taxes might lead to greater favor for value and cyclically oriented parts of the market as government spending raises expectations of a faster economic recovery.

Infrastructure Spending and Industrials

It’s also important to note that Biden has proposed policies that could inject over $5 trillion into the US economy over the next decade, with infrastructure leading the spending push. Under the Build Back Better plan, a Democratic sweep could finally usher in a long-awaited infrastructure bill that puts individuals to work addressing the country’s crumbling infrastructure.

While the stimulus bill waiting in the wings could likely support a rally in cyclical sectors broadly, the Biden campaign’s proposed policies may also provide an additional boost to the industrial and materials sectors, specifically as money pours into national construction projects. What’s more, a Biden administration focused on achieving a carbon pollution-free power sector by 2035 might underpin opportunities in the green-energy oriented space and further support gains in certain Environmental, Social, and Governance (ESG) investments.

Reduced Foreign Policy Risk Premium

Finally, an administration change could reduce the foreign policy uncertainty premium that has arguably supported US over international investment exposure. On the China front, Biden is likely to push forward on completing a trade deal with China (and Europe). What's more, it’s also possible that the narrative surrounding trade negotiations under a new administration might present fewer surprises and thus even out policy uncertainties compared to Trade War related events in recent years.

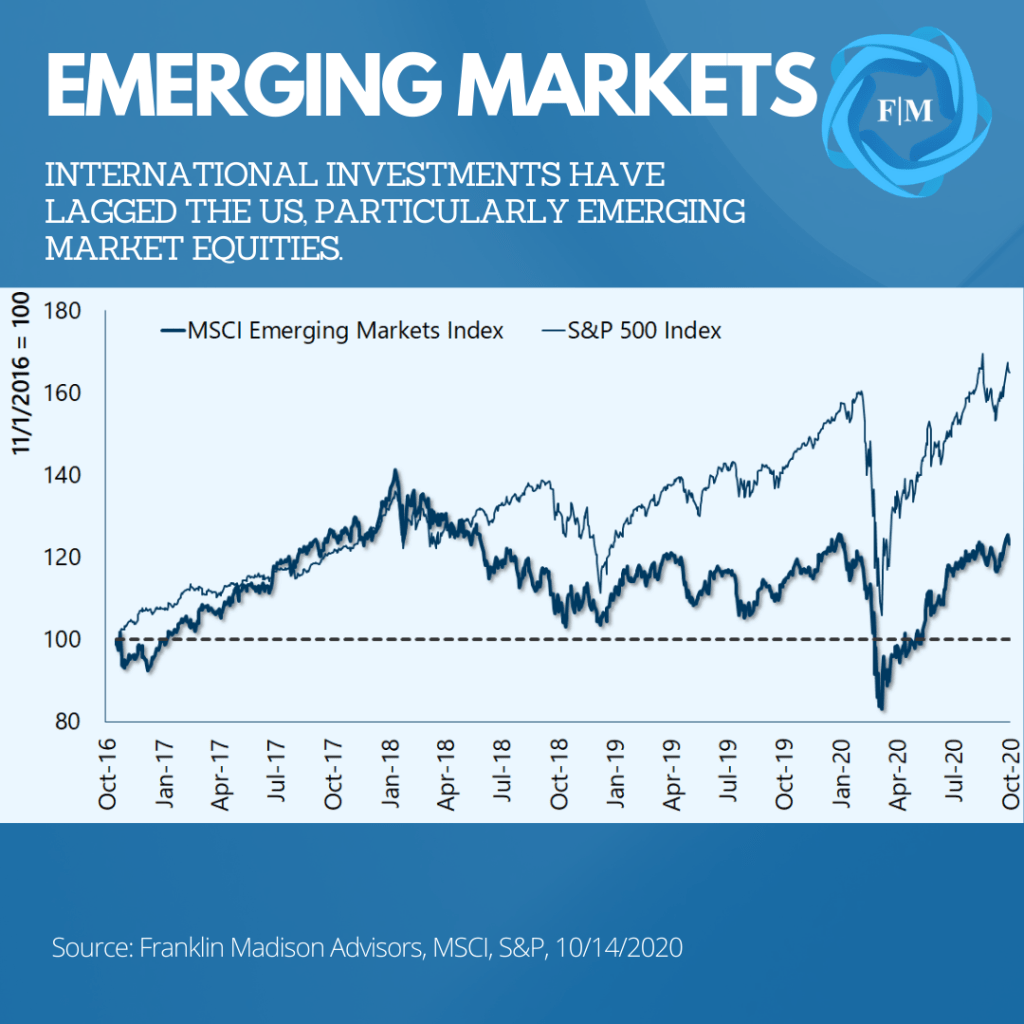

This lower risk premium, combined with ultra-loose Fed policy, could place downward pressure on the US dollar and potentially incentivize increased investor exposure to global investment opportunities. Structurally, we’ve laid out a case for investing in emerging markets for the long-term, but such an outcome could be favorable for non-State Owned Enterprise (SOE) Chinese stocks in the short run.

Domestically, greater policy uncertainty could provide more favorable prospects in traditional high yield opportunities. Like international asset classes, high yield bond prices are susceptible to sudden swings in market sentiment. With a reduced policy risk premium, income-oriented investors might benefit from higher-quality “fallen angel” opportunities in the high yield space.

Look for Investment Opportunities in a Biden Win

Taken together, a Biden win might usher in a greater need for tax efficiency and less reliance on capital gains for income-oriented investors. A change in the White House may also mean a shift in the market narrative that is balanced less towards growth sectors and more towards cyclicals as fiscal spending boosts economic growth up in the coming year. Finally, the foreign policy risk premium that has favored US markets in recent years could open the door to more international opportunities as foreign policy-related volatility ebbs.

In either case, in the days leading up to the election, markets are likely to ebb and flow along with a host of unknowns. As an investor, you may be rethinking your market risk exposure or even contemplating exiting the markets altogether before election day. To be sure, whatever the outcome might be, November 3rd is likely to mark a turning point for the next chapter of the dominant market narrative.

Even so, during this time of uncertainty, we recommend that you consider these post-election investment opportunities before the narrative shifts while staying committed to your long-term investment plan and positioning yourself for higher levels of market volatility.

Has the US Dollar Lost its Dominant Reserve Currency Status?

Is US dollar dominance poised to end, and what might it mean for your finances? Uncertainties surrounding US dollar strength have been top-of-mind for some individuals for many years and for a good reason. A significant decline in our nation's currency could lead to higher prices for the goods and services you consume and make it more expensive to borrow money for big-ticket purchases like a house or a new car.

Today, there is a sensible argument to be made for a diminished worth of the US dollar. Ballooning government borrowing, massive central bank money printing, and the decline of US geopolitical influence suggest to some that the end of the dollar's global dominance may have finally come. Some individuals even point to a near-term rise in gold prices and a falling exchange rate as evidence for such a move.

That being said, the dollar's role is more nuanced than such simple near-term explanations would presume. For now, evidence suggests that the dollar's prominence is likely to remain in place for many years to come. Even so, the growing importance of the euro and Chinese yuan over the long-term could reduce the world's dependence on the dollar. So, what does this mean for your money? A structurally weaker US dollar might lead to higher future living costs and is a vital reason why your savings should account for rising inflation.

Making Sense of Foreign Exchange Market Moves

Is the US dollar in decline? One indicator that some individuals use to signal a fall in the dollar is recent foreign exchange market activity. Between March and August of 2020, the dollar, as measured by the US Dollar Index, lost 9% of its value. At the same time, gold prices pushed past record highs. And these combined moves might suggest that something ominous is happening with the US dollar. While it's tempting to extrapolate near-term developments into the future, let's look at what history has to say about the dollar's movements.

From a purely data-driven perspective, history has shown that periods of US dollar weakness are often preceded by strength, especially during crisis times. In the months leading up to its March 2020 highs, the US dollar rose in value versus its key global trading partners. This move occurred as individuals and institutions piled into perceived safe have US assets as coronavirus uncertainties weighed on the global economic outlook.

Certainly, during times of financial stress and economic uncertainties, the US dollar is often sought after as a globally secure destination to park savings. This ebb and flow in value is not unique to 2020. In fact, it is evident in prior crises, like in March 2009, amidst the Great Recession and during the popping of the Tech Bubble in 2001. In fact, after appreciating in 2008 and early-2009, the US dollar gave up 13% of its value in the five months following stock market lows in March. And in 2001, even with the events surrounding September 11, the dollar trimmed 4% of its value during the year.

The point here is that a dollar decline today might coincide with legitimate concerns about massive fiscal and monetary spending. Even so, correlation should not be confused with causation. Instead, one way to look at the recent dollar moves is from the perspective of a safe-haven currency. When economic and geopolitical uncertainties rise, there is greater demand for the safety of the US dollar. Today, it can be argued that movements in the foreign exchange market reflect less demand for US dollars as global market participants look past economic uncertainties.

What Makes a Global Reserve Currency?

If we presume that dollar fluctuations in foreign exchange markets are consistent with near-term risk-on/risk-off trends, what then can we make of the US dollar's role as a preeminent reserve currency? In other words, why wouldn't market participants look to the euro or Chinese yuan as dollar-alternatives during times of uncertainty? In its simplest form, there are generally three factors that make a currency a dominant global reserve: 1) it's used to settle foreign financial obligations, 2) a means to pay for international trade, and 3) as a store of value.

Settling Foreign Obligations (Liquidity)

It's often assumed that central banks print money out of thin air. The fact is that financial institutions are primarily responsible for affecting money supply in circulation. This occurs as banks take in deposits and issue loans. One factor that has propelled the dollar into its global reserve status is how financial institutions outside of the US have issued US dollar-based loans. We refer to these dollar-based foreign obligations as Eurodollars.

While the term was originally coined to represent dollar-based borrowing in a post-World War II Europe, today it applies to US dollar-based obligations in other parts of the world. Experience tells us that interest is often paid back to a lender on top of the principal owed when we borrow money.

Foreign individuals and firms earning money outside of the US might need to convert their own local currencies in exchange for US dollars to make their lenders whole. And by some estimates, today there well over $10 trillion is Eurodollar deposits outside of the $18 trillion in the US financial system. Taken together with loans issued by the International Monetary Fund, the World Bank and Asian Development Bank the dollar is a key source of liquidity for the global financial system.

Use to Settle Global Trade (Size)

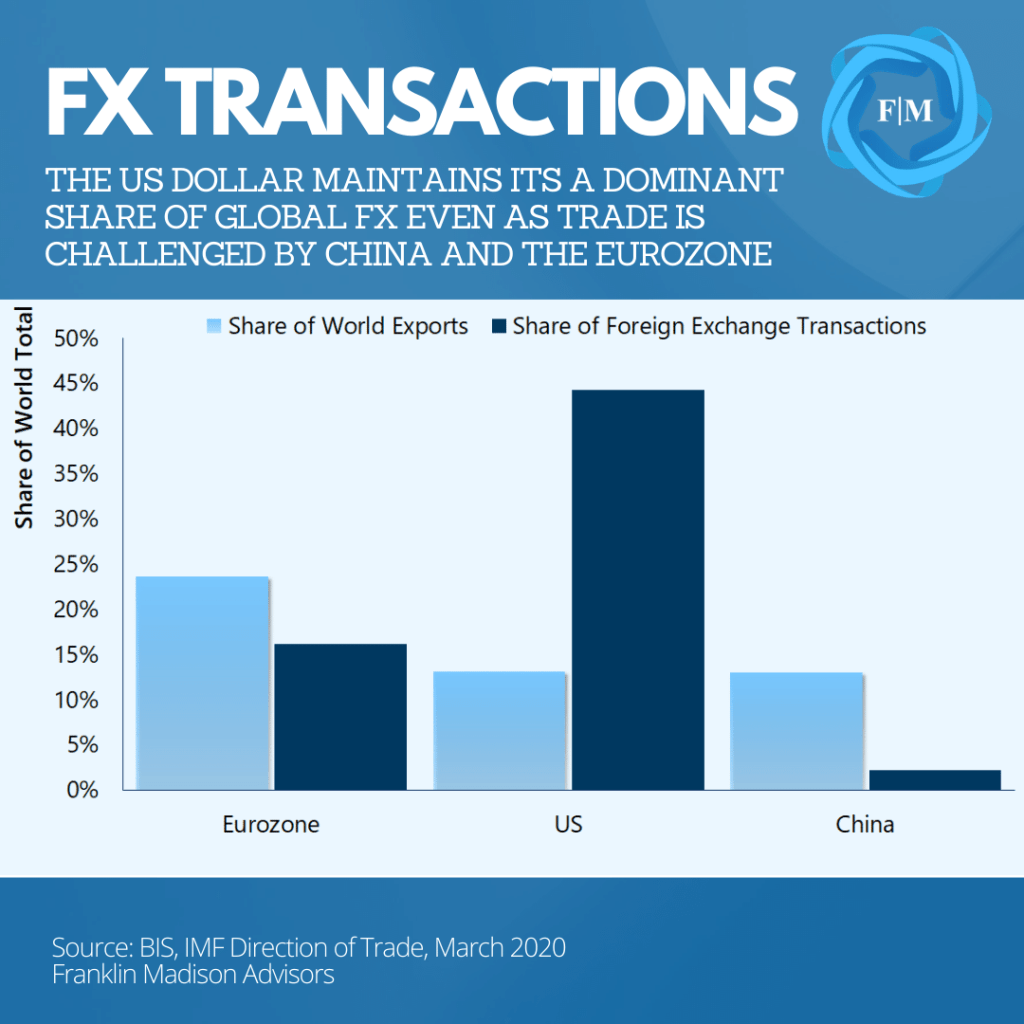

Another factor that distinguishes a global reserve currency is its use to settle trade in international goods and services. In the post-War era, the US was a dominant leader in global trade, given the fact that it was essentially the last major economy standing. In the decades since the Eurozone has become one of the world's largest trading powerhouses and China has risen in prominence as an essential exporter of global goods. Even so, data continue to show that the lion's share of world trade is settled in US dollars.

According to data from the Bank for International Settlements, foreign exchange transactions in US dollars were nearly three times higher than the euro. Indeed, even as China has risen to be a key leader in terms of global trade volumes, the use of the yuan in foreign exchange markets remains a mere fraction compared to the US dollar’s use.

Looking beyond manufactured goods, essential commodity items like gold, oil, and soybeans contracts are largely priced and settled in US dollars. The point here is that buyers and sellers of goods and services globally affect millions of transactions that follow through foreign exchange markets every year and remain overwhelmingly reliant on the US dollar.

Store of Wealth (Stability)

A third factor that makes a global reserve currency is in its perceived ability to store wealth. Put differently, holders of a currency must have a strong belief that its value will remain generally stable over time. Strength in a country's economy, government, and monetary system all contribute to the collective perception of stability underpinning a country's currency.

And despite a number of developments over the past decade, the fundamental factors underpinning the US economy, its government institutions, and monetary system remain on solid footing compared to other global alternatives. To be sure, it's this stability in growth and governance that has led to demand foreign capital flows into US markets and a still outsized demand among foreign central banks for US reserve assets.

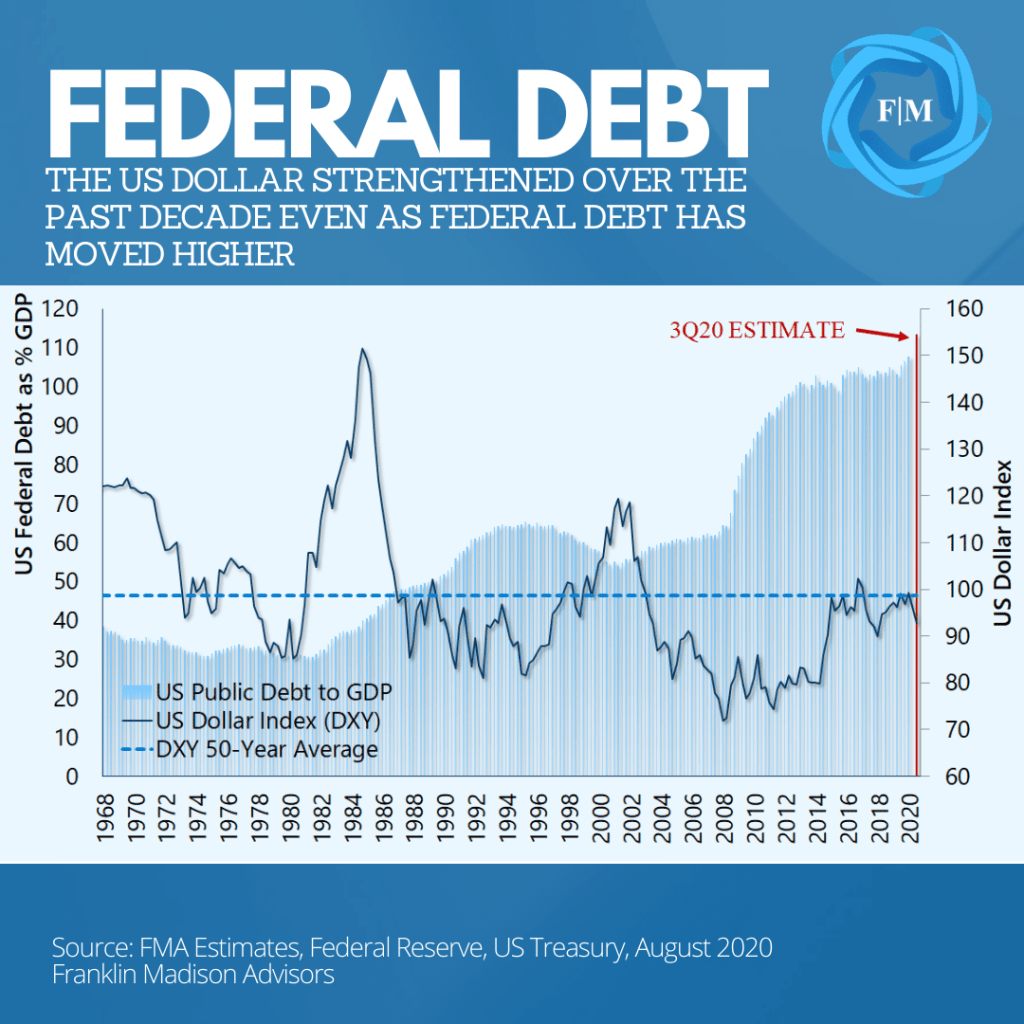

For example, US equity and debt markets account for 40% of global market capitalization. This size makes US markets the single largest and most stable investment destination for foreign investors. And while US government debt continues to rise and foreign policy changes have led to more uncertainties lately, China and Japan, remain two of the world's largest holder of US federal debt reflecting ongoing trust in US institutions.

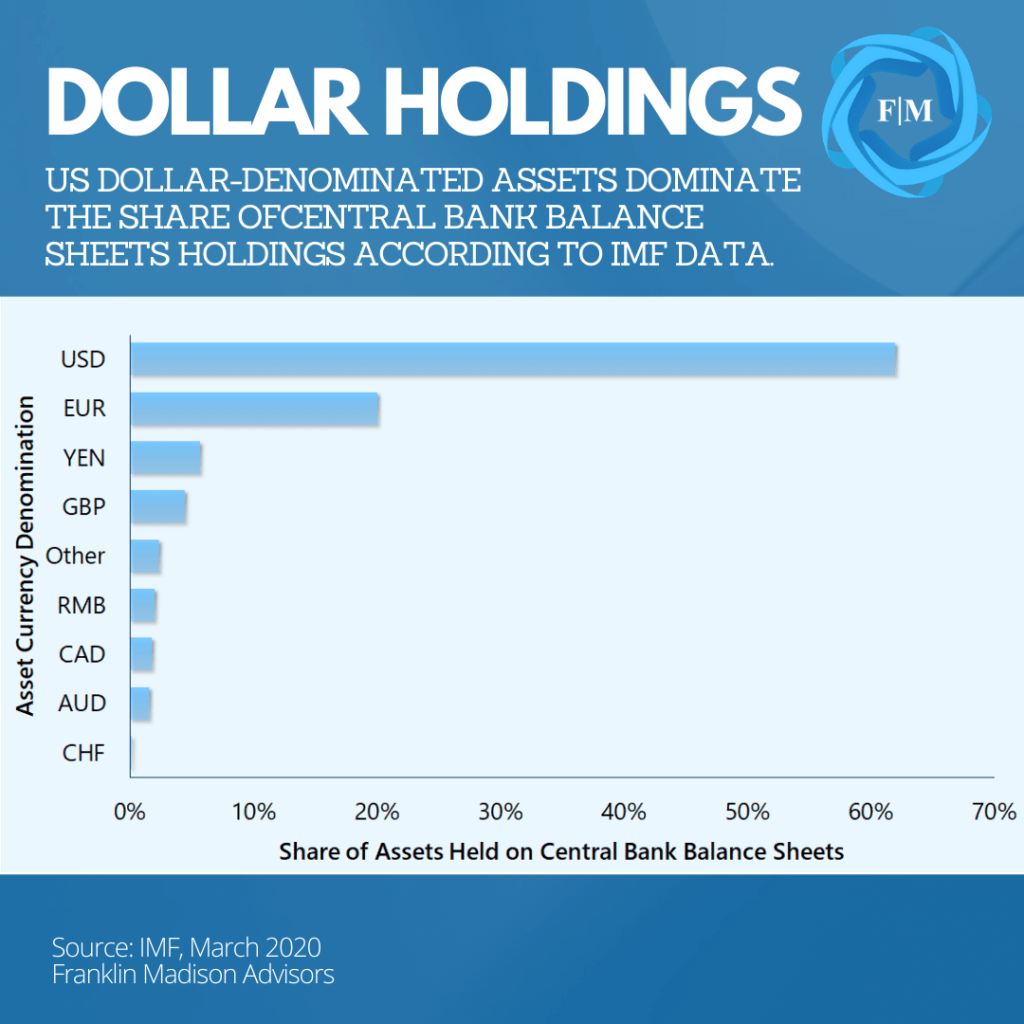

Another factor to consider is that US-dollar denominated holdings make up well over 60% of the world's central banks' assets according to data from the IMF. These assets are used by central banks to help fund obligations in their own domestic financial systems. Indeed, these assets held often reflect a need that banks or institutions in their own country might have for a particular currency. Taken together, this demand for US dollars by foreign individuals, governments, and institutions suggest ongoing faith in the US dollar.

There is No Good Alternative

So far, we've discussed factors that make the US dollar a global reserve currency. Now a key question you might be asking is what could change the US dollar's status. Well, anthropologists have pointed out that when it comes to an individual's choice to migrate from one geography to another, they not only need a desire to leave their current situation but also have a destination to move towards. From a dominant reserve currency perspective, few countries possess the size, liquidity, and stability factors to overwhelmingly support financial transactions, trade, and use as a store of value.

Now, the euro and yuan have often been pointed to as potential alternatives to the US dollar. A key question is whether they meet all three criteria of a dominant reserve currency. In terms of the euro, the currency increasingly benefits from its size and liquidity factors but suffers from uncertainties surrounding its political stability. Consider the Eurozone. It represents a subset of countries within the European Union and its currency, the euro, is largely used to facilitate trade and financial transactions.

Nevertheless, the EU itself remains a confederation of sovereign states and not a single country when compared to federalism in the US. And in recent years, the EU has experienced its fair share of political instability, including the departure of the UK (Brexit) and populism that threatened Greece's EU withdrawal. What about China?

China has undoubtedly made an effort in recent years to internationalize the yuan. It's currency's inclusion in the IMF's Special Drawing Rights basket, lending efforts across the Belt and Road Initiative, easing its peg to the US dollar, and opening up its capital markets have all been aimed at greater foreign adoption of the yuan.

And while China is the world's second-largest economy and accounts for a large portion of global trade, a foreign market for the yuan remains small and illiquid on a global relative basis. In terms of stability, President Xi Jinping's pivot away from Deng and toward Maoist ideology introduces a host of uncertainties related to the rule of law and foreign policy in China.

When it comes to finding a suitable replacement to the dollar as a preeminent reserve currency, the simple fact is that there is no good alternative right now. Until countries like China or the EU step up to address size, liquidity, and stability concerns, the US dollar is likely to remain a dominant reserve currency into the foreseeable future.

Effects of a Structurally Weaker Dollar

Up to this point, we have made a case for a generally stable role for the US dollar as it relates to its status as a dominant reserve currency. However, a moment could come in our lifetimes when the US dollar may lose this coveted status. What might this development mean for your finances?

Well, a slow transition from a dominant role to a second-run reserve currency measured over decades might have little noticeable impact for the average household. Indeed, inflation running at a 4% rate could lead to the cost of living doubling in 18 years compared to 36 years at current inflation rates. Given time, policymakers and business leaders might be able to introduce strategies and technologies that help pivot the economy in light of a changing financial environment.

Indeed, a structurally weaker US dollar could change the economics of US goods manufacturing and lead to higher levels of reshoring and job opportunities at home. At the same time, US firms doing business abroad likely would also see earnings rise as foreign currencies strengthen when US dollars are brought back home.

Sudden Currency Shock

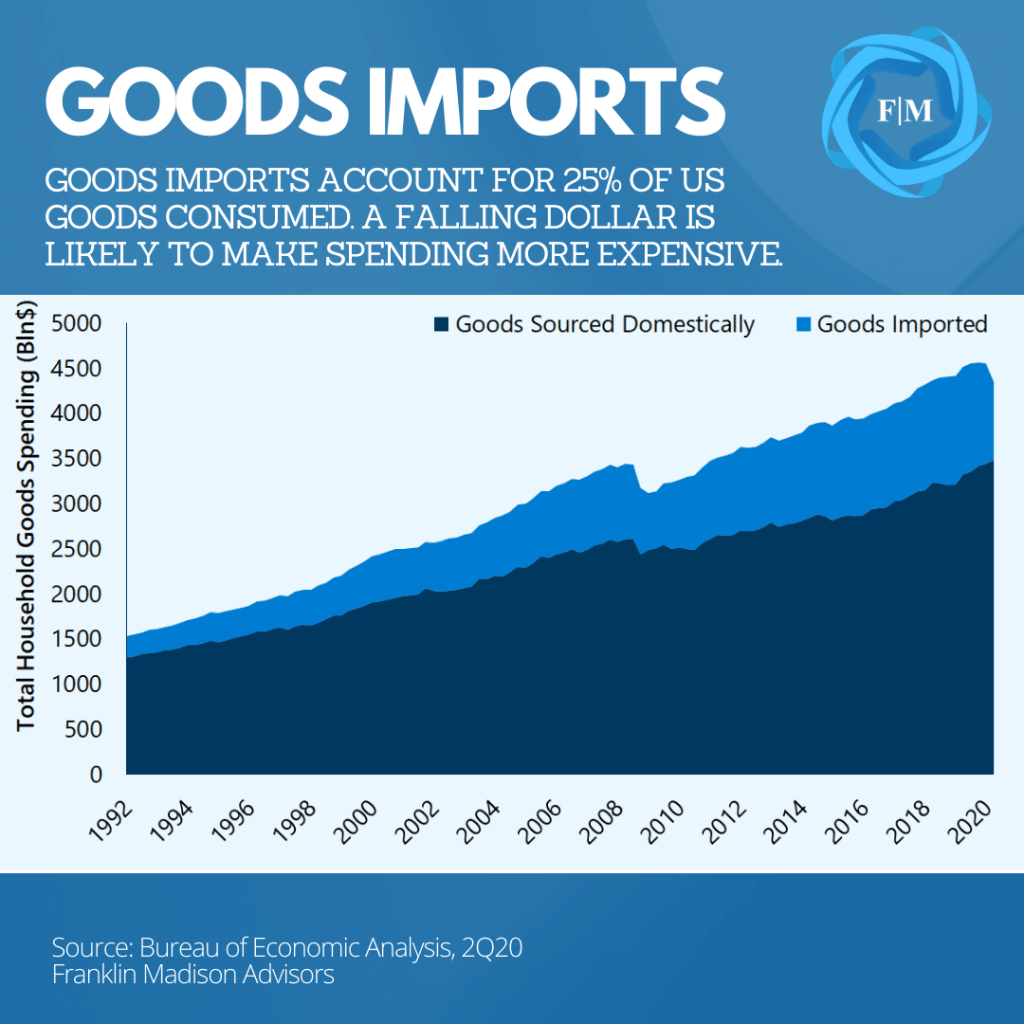

On the other hand, a sudden shock, like war or an unmitigated economic collapse, might lead to a sharp drop in the US dollar and make it more expensive for households to spend or borrow. How so? According to government data, households spent $4.3 trillion on goods at an average annualized rate during the first half of 2020. At the same time, over a quarter of the goods consumed were imported from abroad. This point is important because when the dollar falls, the cost of goods imported rises, leading to higher inflation rates. And a sudden drop in the dollar could lead to noticeably more expensive goods on store shelves.

Another thing that a weaker dollar could do is push up borrowing costs. Should confidence in the US dollar finally wane, the Federal Reserve likely would be forced to raise interest rates to incentivize foreign investors to hold dollars. And when the Fed makes changes to its interest rate policy, it can affect borrowing costs that likely would make spending more expensive.

In fact, rising interest rates might make it more expensive to borrow when it comes to purchases like a house or a new car. At the same time, higher interest rates could lead to stagnating home prices as values are typically inversely related to interest rates. Higher interest rates would also make it more expensive for local and federal governments to borrow, challenging their finances and their ability to fund essential programs like Social Security and Medicare.

The point here is that effect on your finances as it relates to a weaker dollar likely will depend on whether the dollar’s fall from grace occurs over a short or long period of time.

US Dollar Dominance Likely Here to Stay

Today, some individuals point to near-term weakness in foreign exchange markets or the rise of currency alternatives like gold or bitcoin to signal an imminent demise in the US dollar. The fact is that the world remains heavily dependent on the dollar to affect international trade, settle financial transactions, and in its use as a trusted store of value.

And while the impact of a sudden loss in reserve status might lead to higher inflation and borrowing costs, it remains likely that the dollar's fall from grace might occur over an extended period. This potential could give US leaders time to enact policies that could help mitigate the world's shifting preference toward the euro or yuan as a preferred reserve currency.

Even so, as we pointed out in a recent report, if your concern is rising inflation, then history has shown that financial assets are an optimal means for hedging against rising cost of living. Until then, the size, liquidity, and general stability of institutions supporting its use are likely to uphold the US dollar's preeminent status into the foreseeable future.

Has the US Dollar Lost its Dominant Reserve Currency Status?

Is US dollar dominance poised to end, and what might it mean for your finances? Uncertainties surrounding US dollar strength have been top-of-mind for some individuals for many years and for a good reason. A significant decline in our nation's currency could lead to higher prices for the goods and services you consume and make it more expensive to borrow money for big-ticket purchases like a house or a new car.

Today, there is a sensible argument to be made for a diminished worth of the US dollar. Ballooning government borrowing, massive central bank money printing, and the decline of US geopolitical influence suggest to some that the end of the dollar's global dominance may have finally come. Some individuals even point to a near-term rise in gold prices and a falling exchange rate as evidence for such a move.

That being said, the dollar's role is more nuanced than such simple near-term explanations would presume. For now, evidence suggests that the dollar's prominence is likely to remain in place for many years to come. Even so, the growing importance of the euro and Chinese yuan over the long-term could reduce the world's dependence on the dollar. So, what does this mean for your money? A structurally weaker US dollar might lead to higher future living costs and is a vital reason why your savings should account for rising inflation.

Making Sense of Foreign Exchange Market Moves

Is the US dollar in decline? One indicator that some individuals use to signal a fall in the dollar is recent foreign exchange market activity. Between March and August of 2020, the dollar, as measured by the US Dollar Index, lost 9% of its value. At the same time, gold prices pushed past record highs. And these combined moves might suggest that something ominous is happening with the US dollar. While it's tempting to extrapolate near-term developments into the future, let's look at what history has to say about the dollar's movements.

From a purely data-driven perspective, history has shown that periods of US dollar weakness are often preceded by strength, especially during crisis times. In the months leading up to its March 2020 highs, the US dollar rose in value versus its key global trading partners. This move occurred as individuals and institutions piled into perceived safe have US assets as coronavirus uncertainties weighed on the global economic outlook.

Certainly, during times of financial stress and economic uncertainties, the US dollar is often sought after as a globally secure destination to park savings. This ebb and flow in value is not unique to 2020. In fact, it is evident in prior crises, like in March 2009, amidst the Great Recession and during the popping of the Tech Bubble in 2001. In fact, after appreciating in 2008 and early-2009, the US dollar gave up 13% of its value in the five months following stock market lows in March. And in 2001, even with the events surrounding September 11, the dollar trimmed 4% of its value during the year.

The point here is that a dollar decline today might coincide with legitimate concerns about massive fiscal and monetary spending. Even so, correlation should not be confused with causation. Instead, one way to look at the recent dollar moves is from the perspective of a safe-haven currency. When economic and geopolitical uncertainties rise, there is greater demand for the safety of the US dollar. Today, it can be argued that movements in the foreign exchange market reflect less demand for US dollars as global market participants look past economic uncertainties.

What Makes a Global Reserve Currency?

If we presume that dollar fluctuations in foreign exchange markets are consistent with near-term risk-on/risk-off trends, what then can we make of the US dollar's role as a preeminent reserve currency? In other words, why wouldn't market participants look to the euro or Chinese yuan as dollar-alternatives during times of uncertainty? In its simplest form, there are generally three factors that make a currency a dominant global reserve: 1) it's used to settle foreign financial obligations, 2) a means to pay for international trade, and 3) as a store of value.

Settling Foreign Obligations (Liquidity)

It's often assumed that central banks print money out of thin air. The fact is that financial institutions are primarily responsible for affecting money supply in circulation. This occurs as banks take in deposits and issue loans. One factor that has propelled the dollar into its global reserve status is how financial institutions outside of the US have issued US dollar-based loans. We refer to these dollar-based foreign obligations as Eurodollars.

While the term was originally coined to represent dollar-based borrowing in a post-World War II Europe, today it applies to US dollar-based obligations in other parts of the world. Experience tells us that interest is often paid back to a lender on top of the principal owed when we borrow money.

Foreign individuals and firms earning money outside of the US might need to convert their own local currencies in exchange for US dollars to make their lenders whole. And by some estimates, today there well over $10 trillion is Eurodollar deposits outside of the $18 trillion in the US financial system. Taken together with loans issued by the International Monetary Fund, the World Bank and Asian Development Bank the dollar is a key source of liquidity for the global financial system.

Use to Settle Global Trade (Size)

Another factor that distinguishes a global reserve currency is its use to settle trade in international goods and services. In the post-War era, the US was a dominant leader in global trade, given the fact that it was essentially the last major economy standing. In the decades since the Eurozone has become one of the world's largest trading powerhouses and China has risen in prominence as an essential exporter of global goods. Even so, data continue to show that the lion's share of world trade is settled in US dollars.

According to data from the Bank for International Settlements, foreign exchange transactions in US dollars were nearly three times higher than the euro. Indeed, even as China has risen to be a key leader in terms of global trade volumes, the use of the yuan in foreign exchange markets remains a mere fraction compared to the US dollar’s use.

Looking beyond manufactured goods, essential commodity items like gold, oil, and soybeans contracts are largely priced and settled in US dollars. The point here is that buyers and sellers of goods and services globally affect millions of transactions that follow through foreign exchange markets every year and remain overwhelmingly reliant on the US dollar.

Store of Wealth (Stability)

A third factor that makes a global reserve currency is in its perceived ability to store wealth. Put differently, holders of a currency must have a strong belief that its value will remain generally stable over time. Strength in a country's economy, government, and monetary system all contribute to the collective perception of stability underpinning a country's currency.

And despite a number of developments over the past decade, the fundamental factors underpinning the US economy, its government institutions, and monetary system remain on solid footing compared to other global alternatives. To be sure, it's this stability in growth and governance that has led to demand foreign capital flows into US markets and a still outsized demand among foreign central banks for US reserve assets.

For example, US equity and debt markets account for 40% of global market capitalization. This size makes US markets the single largest and most stable investment destination for foreign investors. And while US government debt continues to rise and foreign policy changes have led to more uncertainties lately, China and Japan, remain two of the world's largest holder of US federal debt reflecting ongoing trust in US institutions.

Another factor to consider is that US-dollar denominated holdings make up well over 60% of the world's central banks' assets according to data from the IMF. These assets are used by central banks to help fund obligations in their own domestic financial systems. Indeed, these assets held often reflect a need that banks or institutions in their own country might have for a particular currency. Taken together, this demand for US dollars by foreign individuals, governments, and institutions suggest ongoing faith in the US dollar.

There is No Good Alternative

So far, we've discussed factors that make the US dollar a global reserve currency. Now a key question you might be asking is what could change the US dollar's status. Well, anthropologists have pointed out that when it comes to an individual's choice to migrate from one geography to another, they not only need a desire to leave their current situation but also have a destination to move towards. From a dominant reserve currency perspective, few countries possess the size, liquidity, and stability factors to overwhelmingly support financial transactions, trade, and use as a store of value.

Now, the euro and yuan have often been pointed to as potential alternatives to the US dollar. A key question is whether they meet all three criteria of a dominant reserve currency. In terms of the euro, the currency increasingly benefits from its size and liquidity factors but suffers from uncertainties surrounding its political stability. Consider the Eurozone. It represents a subset of countries within the European Union and its currency, the euro, is largely used to facilitate trade and financial transactions.

Nevertheless, the EU itself remains a confederation of sovereign states and not a single country when compared to federalism in the US. And in recent years, the EU has experienced its fair share of political instability, including the departure of the UK (Brexit) and populism that threatened Greece's EU withdrawal. What about China?

China has undoubtedly made an effort in recent years to internationalize the yuan. It's currency's inclusion in the IMF's Special Drawing Rights basket, lending efforts across the Belt and Road Initiative, easing its peg to the US dollar, and opening up its capital markets have all been aimed at greater foreign adoption of the yuan.

And while China is the world's second-largest economy and accounts for a large portion of global trade, a foreign market for the yuan remains small and illiquid on a global relative basis. In terms of stability, President Xi Jinping's pivot away from Deng and toward Maoist ideology introduces a host of uncertainties related to the rule of law and foreign policy in China.

When it comes to finding a suitable replacement to the dollar as a preeminent reserve currency, the simple fact is that there is no good alternative right now. Until countries like China or the EU step up to address size, liquidity, and stability concerns, the US dollar is likely to remain a dominant reserve currency into the foreseeable future.

Effects of a Structurally Weaker Dollar

Up to this point, we have made a case for a generally stable role for the US dollar as it relates to its status as a dominant reserve currency. However, a moment could come in our lifetimes when the US dollar may lose this coveted status. What might this development mean for your finances?

Well, a slow transition from a dominant role to a second-run reserve currency measured over decades might have little noticeable impact for the average household. Indeed, inflation running at a 4% rate could lead to the cost of living doubling in 18 years compared to 36 years at current inflation rates. Given time, policymakers and business leaders might be able to introduce strategies and technologies that help pivot the economy in light of a changing financial environment.

Indeed, a structurally weaker US dollar could change the economics of US goods manufacturing and lead to higher levels of reshoring and job opportunities at home. At the same time, US firms doing business abroad likely would also see earnings rise as foreign currencies strengthen when US dollars are brought back home.

Sudden Currency Shock

On the other hand, a sudden shock, like war or an unmitigated economic collapse, might lead to a sharp drop in the US dollar and make it more expensive for households to spend or borrow. How so? According to government data, households spent $4.3 trillion on goods at an average annualized rate during the first half of 2020. At the same time, over a quarter of the goods consumed were imported from abroad. This point is important because when the dollar falls, the cost of goods imported rises, leading to higher inflation rates. And a sudden drop in the dollar could lead to noticeably more expensive goods on store shelves.

Another thing that a weaker dollar could do is push up borrowing costs. Should confidence in the US dollar finally wane, the Federal Reserve likely would be forced to raise interest rates to incentivize foreign investors to hold dollars. And when the Fed makes changes to its interest rate policy, it can affect borrowing costs that likely would make spending more expensive.

In fact, rising interest rates might make it more expensive to borrow when it comes to purchases like a house or a new car. At the same time, higher interest rates could lead to stagnating home prices as values are typically inversely related to interest rates. Higher interest rates would also make it more expensive for local and federal governments to borrow, challenging their finances and their ability to fund essential programs like Social Security and Medicare.

The point here is that effect on your finances as it relates to a weaker dollar likely will depend on whether the dollar’s fall from grace occurs over a short or long period of time.

US Dollar Dominance Likely Here to Stay

Today, some individuals point to near-term weakness in foreign exchange markets or the rise of currency alternatives like gold or bitcoin to signal an imminent demise in the US dollar. The fact is that the world remains heavily dependent on the dollar to affect international trade, settle financial transactions, and in its use as a trusted store of value.

And while the impact of a sudden loss in reserve status might lead to higher inflation and borrowing costs, it remains likely that the dollar's fall from grace might occur over an extended period. This potential could give US leaders time to enact policies that could help mitigate the world's shifting preference toward the euro or yuan as a preferred reserve currency.

Even so, as we pointed out in a recent report, if your concern is rising inflation, then history has shown that financial assets are an optimal means for hedging against rising cost of living. Until then, the size, liquidity, and general stability of institutions supporting its use are likely to uphold the US dollar's preeminent status into the foreseeable future.

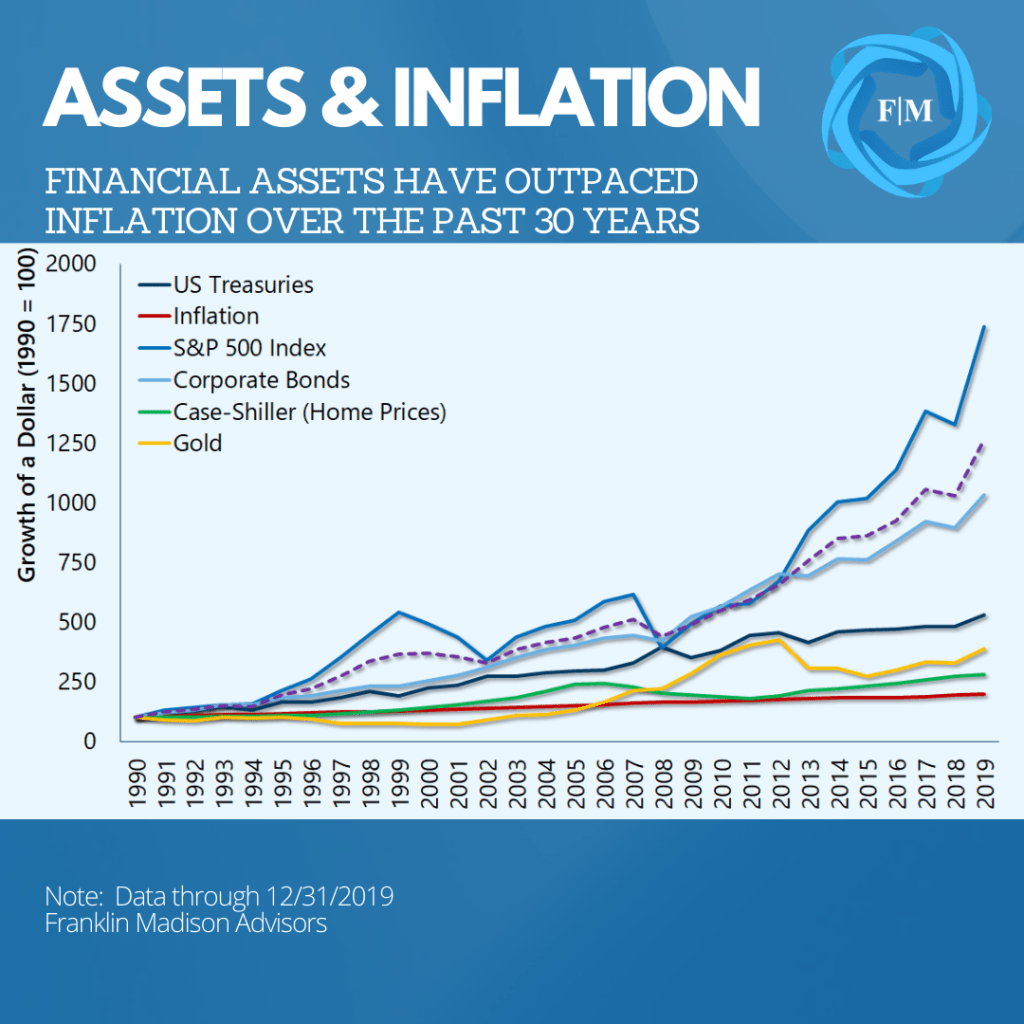

Worried About Inflation? Look Beyond Gold.

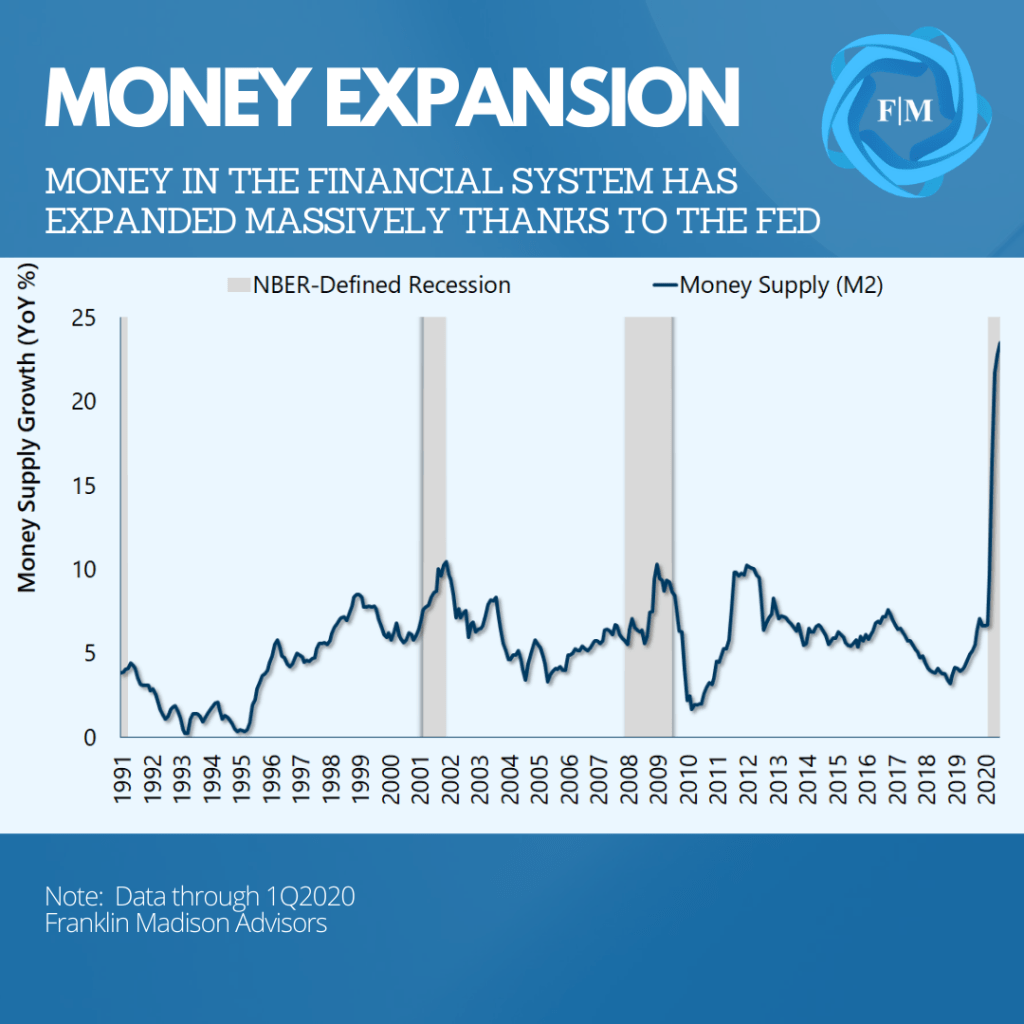

Savers are increasingly looking to gold as a way to address rising inflation and for a good reason. The Federal Reserve's policies in 2020 have massively expanded the supply of money. And more money could lead to higher prices down the road. In anticipation of this concern, some investors are considering gold investments to hedge, or protect against, higher inflation. But a key question for many investors is whether gold is an appropriate way to protect against rising prices.

Our work suggests that relying on gold to protect your savings against inflation may not be optimal. In fact, a survey of historical financial and economic data suggests that assets like stocks and bonds could be better suited to mitigate inflation. More importantly, a diversified portfolio of stocks and bonds provides the benefits of inflation hedging while reducing overall risk to your savings compared to investing in gold alone.

Why Should You Worry About Inflation?

So, what is inflation, and why should you care about it? Well, inflation represents a steady rise in the price of goods and services over time. For example, a can of soda that cost your grandmother ten cents in her youth might now cost you a dollar. And today, inflation is evident in everything from higher housing to education and health care costs.

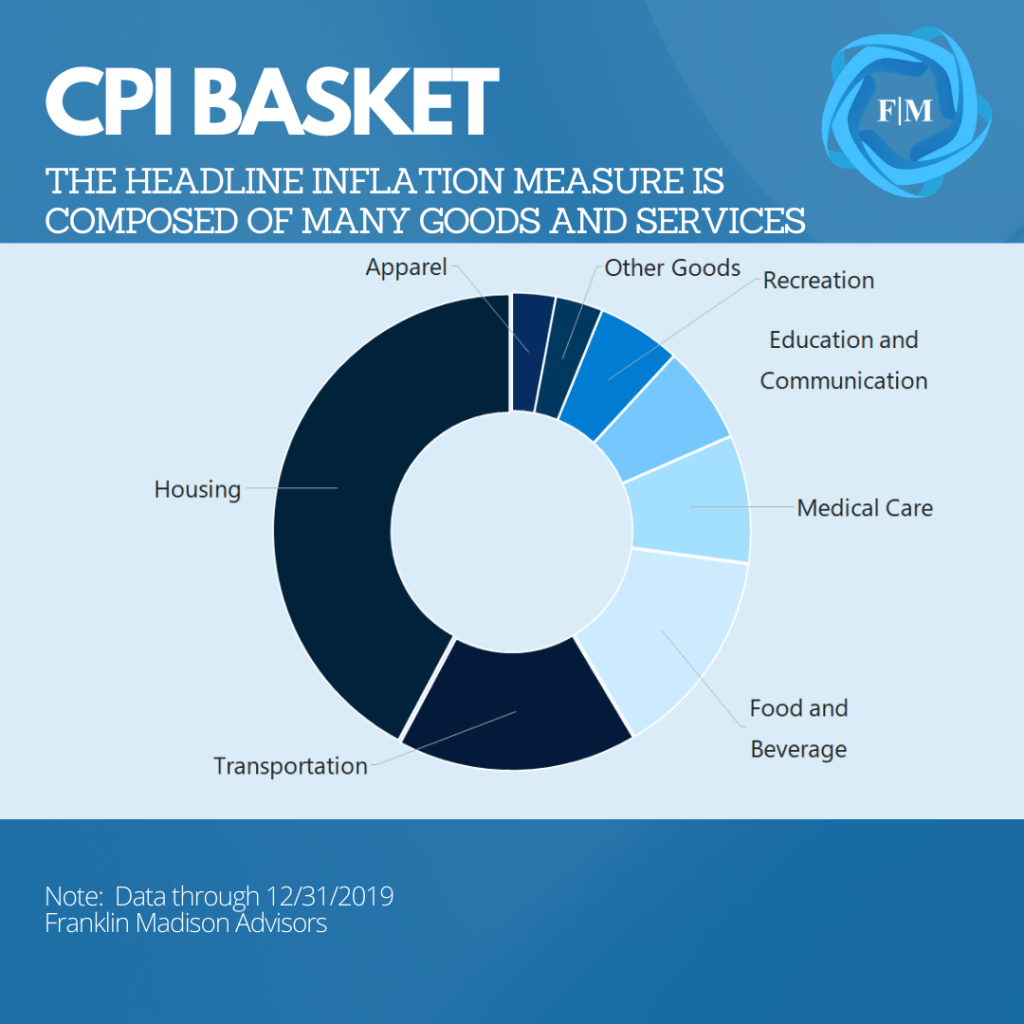

There are many ways to measure inflation. One often-cited inflation measure is the Consumer Price Index (CPI). Every month, government workers survey the prices of hundreds of products and services comprising the CPI basket. The relative importance, or weights, of the items in the CPI basket, is intended to reflect how most Americans spend their paychecks. And while individual prices might ebb and flow from one month to the next, it takes a broad move higher in the basket to signal rising inflation in the economy generally.

Where does inflation come from? Well, there are many schools of thought on the origins of inflation. Ask a Monetarist, and they'll tell you that central banks, with their printing presses, and low-interest rates are the cause of inflation. Ask a Keynesian, and their response might be more nuanced with an emphasis on factors like economic supply and demand and the scarcity of goods or services. Either way you cut it, more money in the financial system and higher levels of future economic growth could lead to faster inflation in the years to come.

Why is inflation important to you? Well, inflation is a vital concept to understand because, when left unchecked, it can erode your purchasing power. That is purchasing power representing the number of goods or services that a dollar saved today can buy you tomorrow. Since 1990, US CPI has risen at an average annual rate of 2.4%. And at this rate, purchasing power is cut in half every 30 years. In other words, while you may have spent $100 on a given good 30 years ago, today, it will cost you $200 thanks to inflation.

This point is notably crucial if you're saving up to buy a home, pay for college, or plan for retirement because not accounting for inflation might leave you short when it comes to paying for these essential financial goals. That's why it's not only enough to just put some away money for the future, it's also vital to grow your money in a way to generate a healthy return that beats inflation.

Is Gold an Optimal Inflation Hedge?

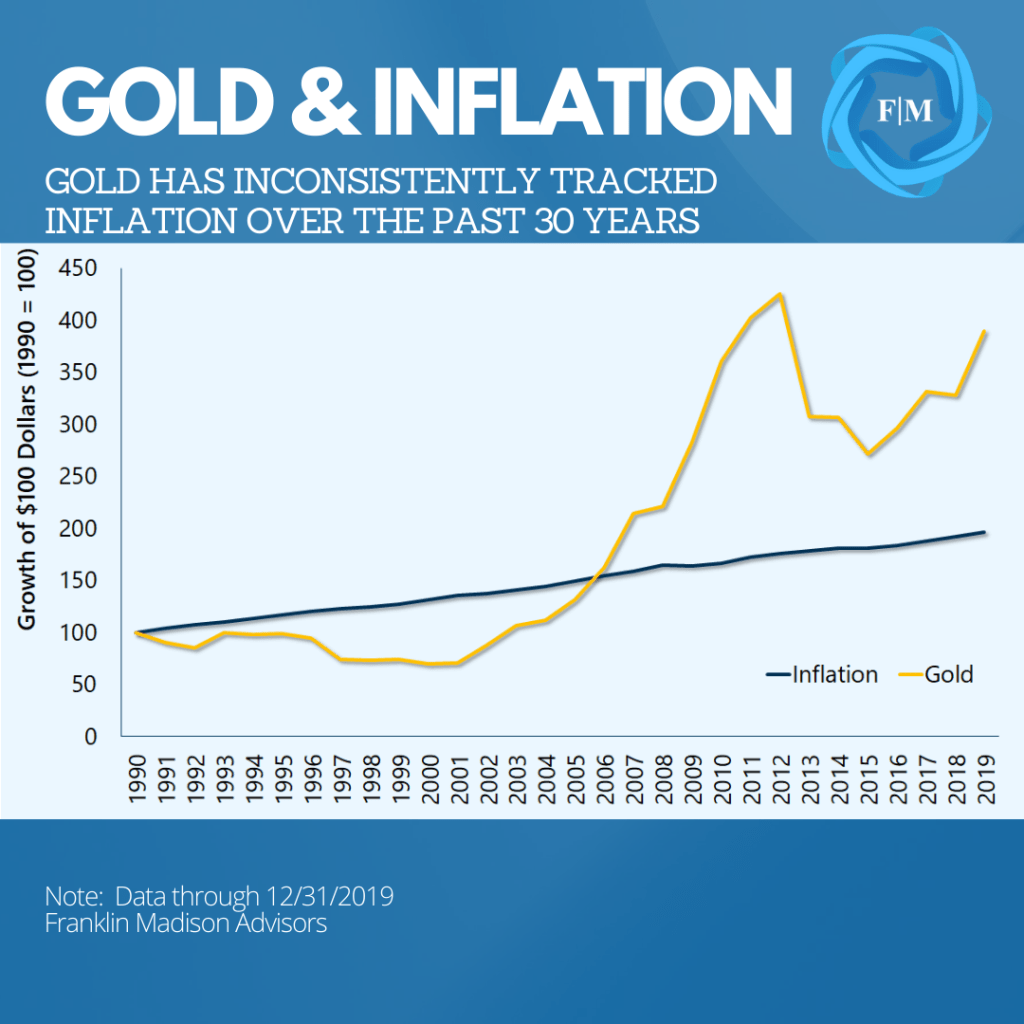

For thousands of years, gold has been relied upon as a form of currency and a store of value. Now gold's worth comes mainly due to its scarcity. This precious metal is so scarce that all of the gold mined throughout history could fit into three Olympic-sized swimming pools. Until the 1970s, the value of the US dollar was tied to a gold standard, and today, global central banks are expanding their holdings of the precious metal as part of their currency reserves.

While there are many reasons to view gold as an essential store of value, history has shown that this precious metal is not the best hedge against inflation. For example, since 1990 gold has increased from $391/oz to over $1,500 by the end of 2019, giving it an average annualized growth rate of 4.8%. How does this stack up against inflation? Over this same 30-year period, as mentioned before, inflation has averaged 2.4%. While gold has bested inflation in some respects, the return on gold is lower than what we would find with other financial assets. A point we'll explore in just a moment.

Besides the issue of underperformance versus financial assets, there are other challenges associated with holding gold. First, gold can be costly and cumbersome. Buying, transporting, and storing large amounts of gold comes with various expenses. And while storing gold at home can alleviate some of these inconveniences, doing so can expose your money to potential theft and loss. What's more, many homeowners' policies provide minimal coverage for the loss or theft of gold. So when your gold is gone, it's gone.

Second, when it's time to sell, finding someone to buy your gold, and getting a reasonable price might be difficult. Certainly, many gold dealers are willing and ready to pay cash for your yellow metal. Even so, fluctuations in gold prices can be as volatile as holding stocks, with a price that can fall as quickly as it rises. Therefore, while gold is on a tear today, the price a dealer will pay you tomorrow is less certain. Given its low return, high volatility, and high holding costs, gold may not be an optimal hedge against inflation. If protecting against inflation is a concern, you may want to consider financial assets.

Financial Assets as an Inflation Hedge

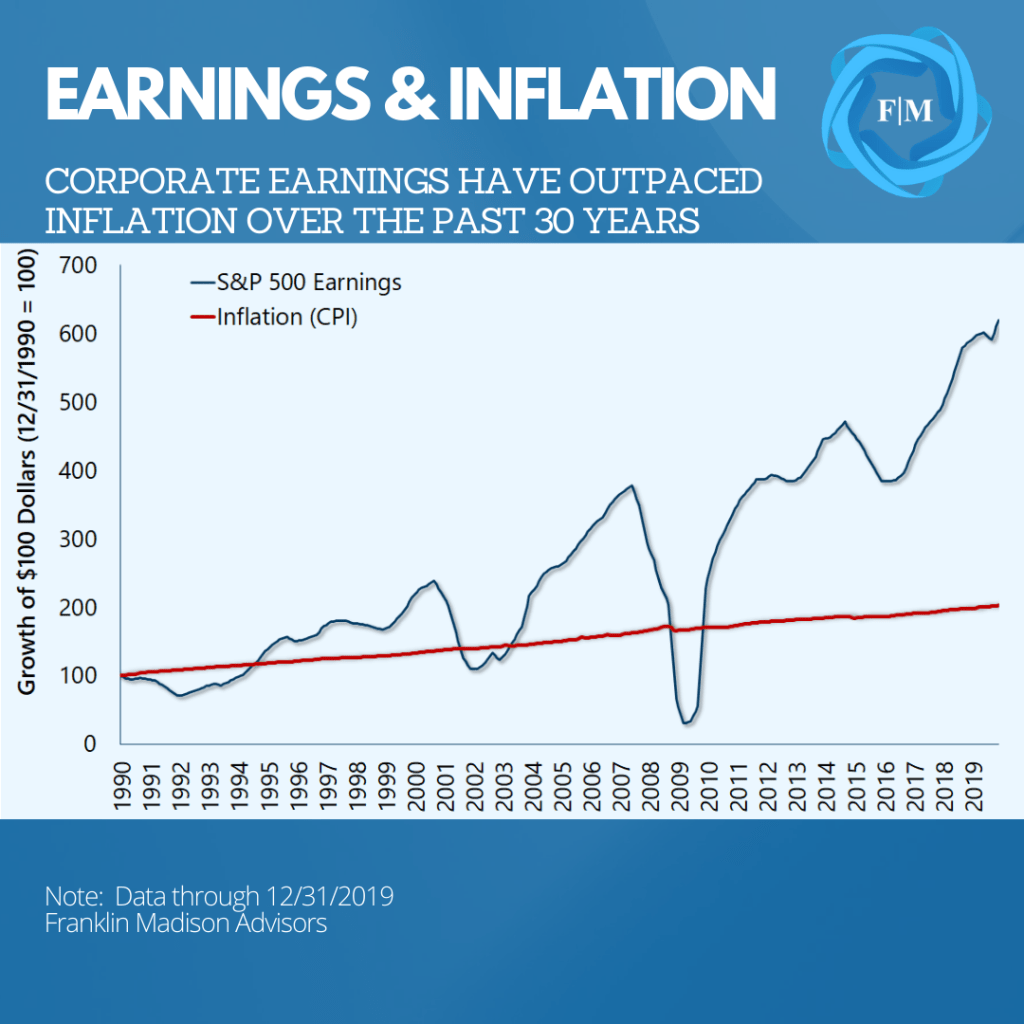

So, how well have financial assets held up against inflation? Well, generally speaking, data have shown that some financial assets, most notably stocks, have handily beaten inflation over the past 30 years. Since 1990, equities (as measured by the S&P 500 index) have appreciated 10.3% per year on a total return basis. This rate of growth has bested gold by a spread of 5.5%.

It's true that many of the same factors that drive stocks higher are evident in gold price movements. Even so, while stock markets are largely seen as driven by supply and demand, the equity gains noted above reflect total returns or the return received with dividends reinvested. This concept of total return is vital because gold does not produce income. Its value is solely based on what an individual buyer or seller thinks the yellow metal is worth.

On the other hand, equity prices are driven by market demand for a given security and expectations of a firm's earnings. Market participants are willing to pay increasingly higher prices for a stock in anticipation of a firms' rise in earnings. These earnings typically grow through a combination of competitive advantages and pricing (inflation) adjustments that flow through to a company's revenues and profits.

To this point, over the past 30 years, S&P 500 companies have been able to grow earnings at an annualized rate of 6.7%. From this perspective alone, we find that equities have a natural inflation hedge built-in through their ability to pass along rising prices to their customers. And it's these intrinsic efficiencies that drive value to shareholders.

Other financial assets, like US Treasuries and corporate bonds, have also posted outsized gains against inflation and gold over the past 30 years. Much of this outperformance has been driven by several factors, including falling interest rates, central bank asset purchases, and investors' search for yield. Even so, bond investors not only receive a return on the price of the bonds themselves, in many cases, they get paid interest while they wait.

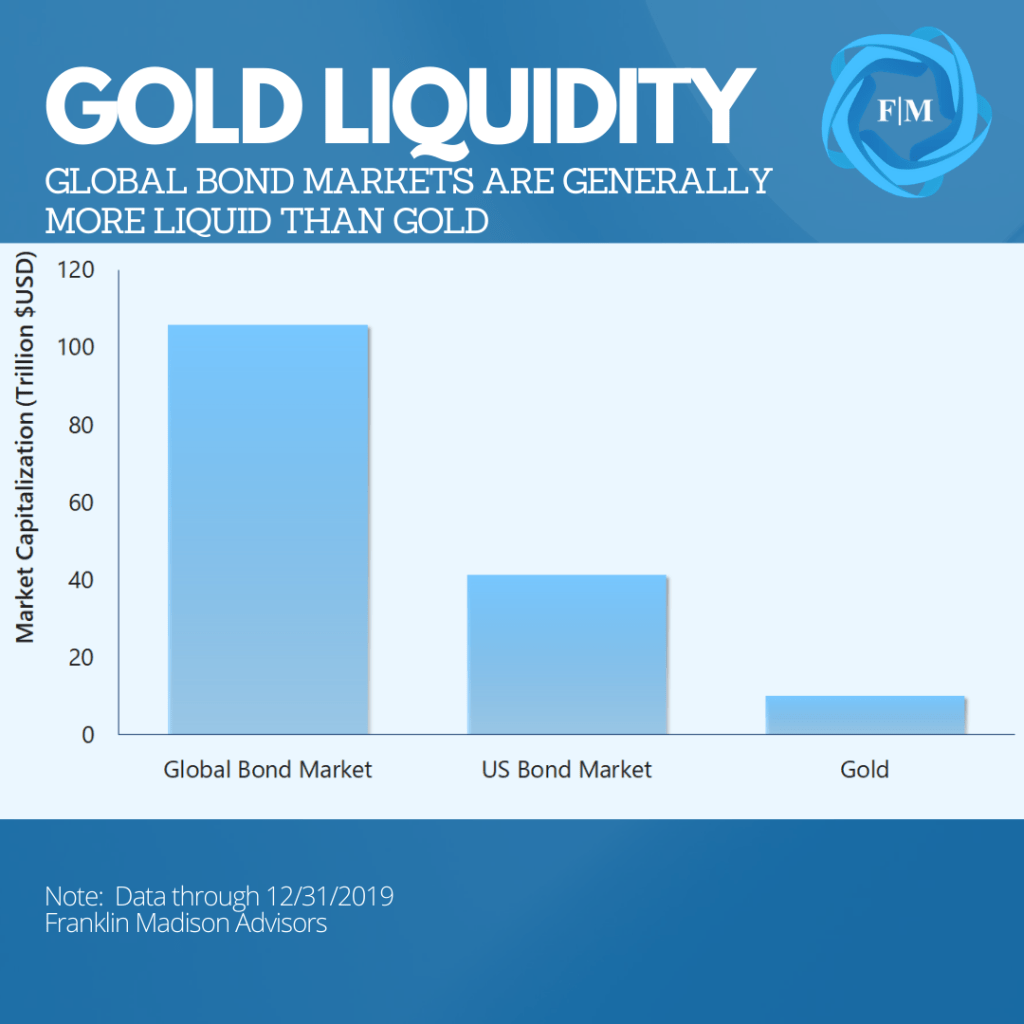

Another thing to consider is that while the total market value of gold globally is around $10 trillion, in the US, total bonds outstanding sat at $46 trillion in the first quarter of 2020. Globally, this figure is well over $100 trillion. And given higher liquidity and marketability, bonds generally have exhibited lower levels of volatility. Add in the earnings power of equities, and historically higher returns, there is a stronger fundamental case for holding financial assets over gold as an inflation hedge.

Getting Paid to Take Risk

One final way to think about the benefits of holding gold versus other assets is to consider how much you're paying to take on investment risk. One standardized measure of this risk-to-reward tradeoff is the Sharpe ratio, a concept we explored in a prior report. From an investment perspective, the Sharpe ratio helps you compare two or more assets to determine whether the return you've received per unit of risk is higher or lower. The higher the Sharpe Ratio, the higher the implied risk-reward tradeoff. How does gold stack up?

Compared to holding large-cap stocks or US Treasuries, gold offers a lower rate of return per unit of risk taken. This observation is notable since gold has returned less than US Treasuries over the past 30 years yet has a volatility measure comparable to stocks.

Even when we expand this measure to include home prices (another poor inflation hedge we'll discuss in a later report), while gold price appreciation beats home values, you're getting paid less on a risk-adjusted basis. Taken together, compared to other investments, gold is likely to pay you less to take on relatively the same amount of risk.

Bringing It All Together

If gold is not an optimal inflation hedge, where should you put your money? How much inflation and when it will arrive is mostly uncertain. What we do know is that when economic uncertainties rise, market volatility often increases as well.

Rather than trying to find one place to invest your money to protect against inflation, you might want to consider holding a diversified basket of stocks and bonds. Doing so might help protect against inflation and help mitigate market volatility when economic uncertainties rise.

As we've written about in the past, diversification is one crucial way to reduce portfolio volatility and smooth out investment returns for the long term. Studies have shown that increasing the number of securities held can reduce overall volatility in an investment portfolio. Therefore, if your goal is to invest for the long term, make an effort to diversify your portfolio across various securities and asset classes to help reduce risk.

Our work suggests that holding a simple 60/40 portfolio of stocks and bonds over the past 30 years protected against inflation, reduced investment risk, and provided generally higher risk-adjusted returns than gold alone.

Worried About Inflation? Gold Alone Might Not Cut It.

Preparing for inflation is a vital concept that all investors should carefully consider. Not accounting for rising prices, particularly at a time of unprecedented central bank policy, could leave you falling short of crucial financial goals. While some investors might look to gold as a way to protect against rising prices, history suggests that the precious metal might not be the best inflation hedge compared to several measures.

In fact, financial assets have a better track record of protecting against inflation. What's more, holding a diversified portfolio of stocks and bonds protects against inflation and can help smooth the ups and downs in the markets. The bottom line here is that if you're looking for a way to hedge against inflation, gold alone might not cut it.

Are Stocks Setting Up for a Second Quarter Repeat?

U.S. stocks had a blockbuster second-quarter. Indeed, both the Dow and S&P 500 have posted their best returns in decades. How long can this outperformance last? With market sentiment still generally positive, some investors are asking whether supportive central bank policies and hope for a rapid economic recovery may be the set up for a third-quarter market surge.

We believe that the dominant narrative that had supported the second-quarter rally is increasingly coming under pressure. Stretched asset valuations and a historical precedent for weaker market returns argue for more caution in the coming quarter. As a result, we recommend that investors use recent market strength to reduce investment risk and raise cash through portfolio rebalancing.

Stocks Had a Stellar Second Quarter – What are the Chances of a Repeat?

Last quarter's rally came on the heels of a sharp market pullback. Efforts to flatten the curve in March led to a massive experiment that had not been tried in well over a century: shut down the economy to curb a pandemic.

Risk assets experienced a sharp selloff in the first quarter on the prospect of weaker economic growth but regained their footing at the start of the second quarter. The rally arguably was fueled by a hope that massive fiscal and monetary stimulus efforts could contribute to a rapid economic rebound.

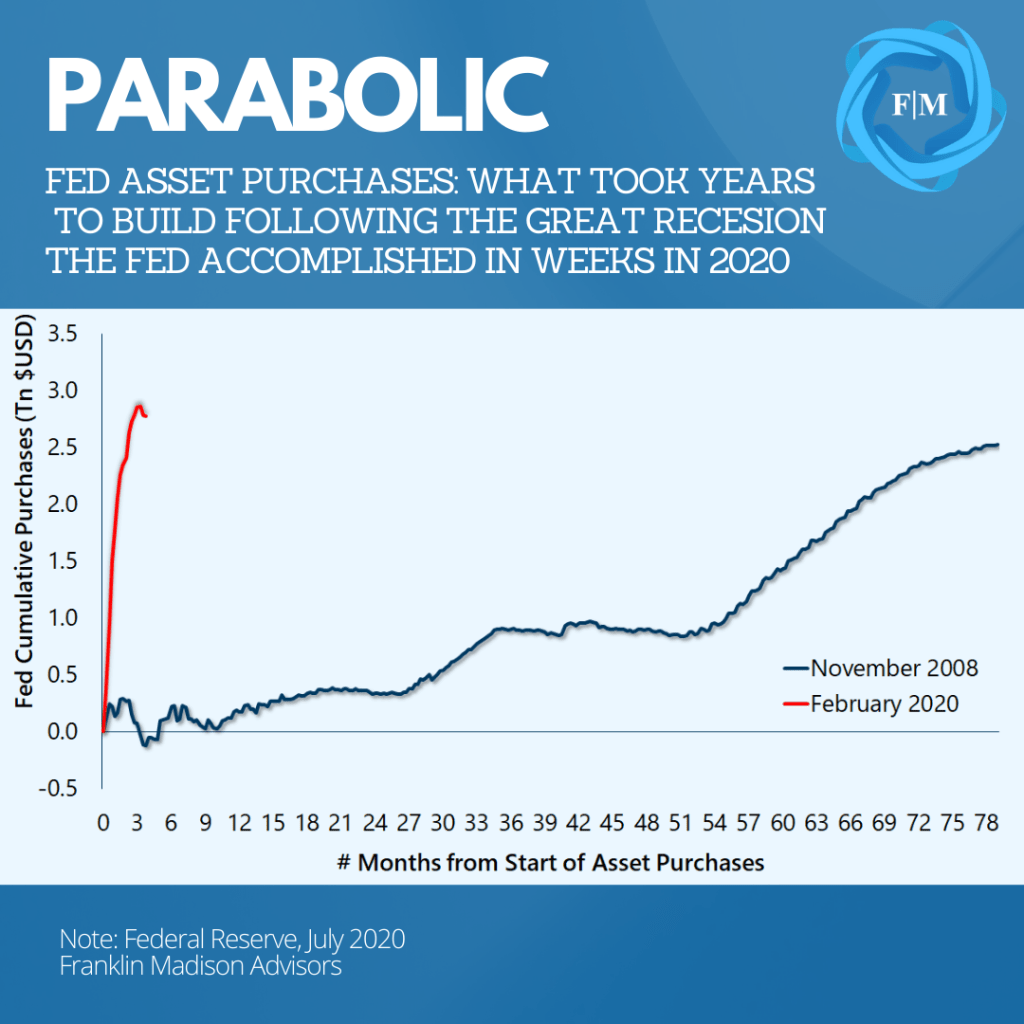

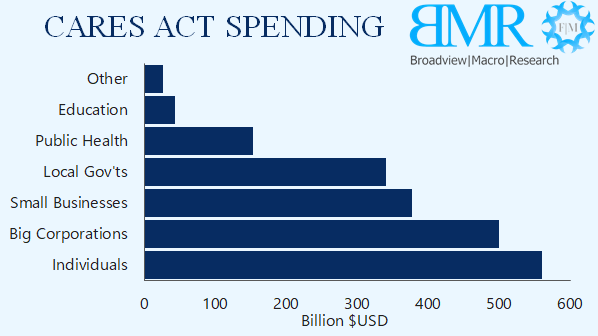

For example, Congress and the Federal Reserve responded to ballooning unemployment and economic uncertainties by launching unprecedented stimulus programs. On the fiscal side, several million businesses in the US received financial support through the Paycheck Protection Program (PPP). The government also issued cash handouts to unemployed workers and households alike.

At the same time, the Fed ramped up purchases of government bonds and mortgage-backed securities. The central bank also launched its Main Street Lending Program to make it easier for small businesses to borrow money. In late June, the Fed began purchasing private firms' bonds through its Secondary Market Corporate Credit Facility (SMCCF). In a matter of weeks, the Fed increased its balance sheet by well over two trillion dollars – a feat that had taken years to accomplish during the Great Recession.

The critical takeaway here is that the second quarter market rally was built upon low price levels and expectations that policy efforts could support a rapid rebound in economic growth. This narrative, however, is increasingly coming into question.

History Suggests Softer Performance

Another important point to consider is that there is little historical precedent for a repeat of second-quarter market performance. We know this because we analyzed data to determine how markets have performed historically following a sizeable rally. Our work suggests that the return on the S&P 500 index in the third quarter could be less than half the 20% realized in the second quarter.

For example, history shows that the S&P 500 rallied 15% in the three months following market lows set in March 2009. How did the index perform in the next quarter? Well, the index gained only 5.5% in the next quarter. And this observation is not limited to just one period in time.

Looking at a distribution of returns going back to 1930, we find that market returns tend to come in between 0-10% in the quarter following a strong market rally at about two-thirds of the time. To be sure, the data showed that market performance on the heels of a massive rally was not only softer in the next quarter, but they were also consistently weaker 98% of the time.

The crucial takeaway here is that, from a historical perspective, strong returns do not beget even higher returns. While the historical data suggest that performance is quite likely to remain positive in the third quarter, from a purely statistical perspective, it's hard to make a case that we'll see even higher returns in the months ahead.

Unmitigated Healthcare Crisis

Finally, it's important to note that the healthcare crisis is not improving, and this will challenge the market's rapid recovery narrative. At the onset of the outbreak, there was a notion that if we locked down the economy and reopened in a deliberate, intentional way (think phase red, yellow, green), we'd be able to contain the coronavirus outbreak, and quickly have life get back to normal.

After initial success in flattening the curve, we're now seeing that COVID19 cases are reaccelerating weeks after much of the US economy has reopened. With vaccine trials still ongoing, and infection rates currently on the rise, there's a real risk that we may end up with a healthcare crisis more severe than the one we had in March.

Such an outcome could lead to delayed household spending and employer hiring decisions, challenging the dominant market narrative that supported second-quarter market performance. Indeed, with more state governors reversing or delaying plans to open their economies, it is becoming increasingly difficult to make a case that markets can continue to rally on hope of a sudden economic recovery.

What Should Investors be Mindful of Heading into the Third Quarter?

Investors should be mindful of the fact that expectations for the future often drive market behavior. Presently, there are arguably two vital expectations supporting market sentiment: 1) policy response will fuel economic growth, and 2) economic growth will quickly recover. Right now, it's unclear whether monetary policy can do more than stabilize economic conditions.

Monetary Policy is not a Panacea

Monetary policy can only do so much to support economic growth. With that said, there is little doubt whether the Fed will pull out all the stops to stabilize growth. The Fed's willingness to support its full employment and inflation mandates is evident in the various programs mentioned earlier. Even so, monetary policy is not a panacea for market-related concerns.

Take, for instance, the Bank of Japan. This central bank has been buying public and private sector stocks, bonds, and real estate for years. It has implemented non-traditional measures such as a negative interest rate policy and yield curve control. Japan's economic growth has nevertheless been weak, and the performance of its markets has lagged its peers. A similar situation is present in the Eurozone.

Anecdotally, history has shown that markets tend to stage an early rally based on expectations of a massive game-changing catalyst, like an election, a rise in government spending, or a favorable change in monetary policy. Today, such expectations are playing out in mantras like "don't fight the Fed." Even so, what we've observed over the past couple of decades is that such rallies tend to wane as market participants eventually reset their expectations to the reality that policy alone does not heal what's ailing a struggling economy.

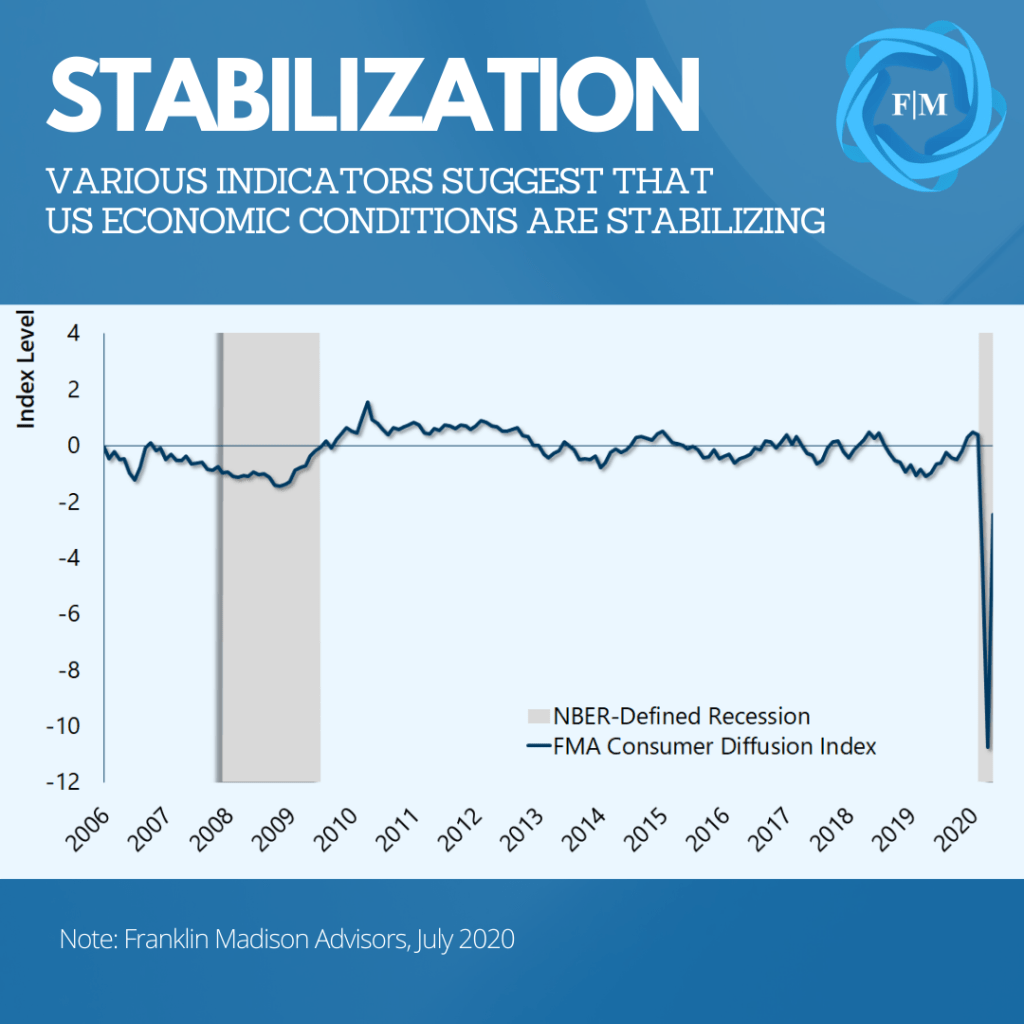

Economy stabilizing, growth likely to struggle

Another issue with which investors must contend in the coming quarter is that weaker growth will challenge market sentiment. While some data have improved, reports are not yet consistent with a robust economic rebound. To this point, the IMF recently downgraded its estimate of a US economic recession from -5% set in April to -8% (consistent with the Great Recession) in June.

This view does not dismiss the fact that by some measures, the economy is stabilizing. Our own consumer and business diffusion indices show that US economic activity is recovering from lows set in April. Even so, these backward-looking indicators need to be reconciled with forward-looking realities: households are increasingly likely to curb spending amid the ongoing healthcare crisis.

A rising number of states are reporting record one-day coronavirus infection rates. The effect of which has led some governors to postpone reopening their economies and others to shut down establishments like bars and restaurants. Prolonging the economic lockdown may curb the recent consumer spending recovery.

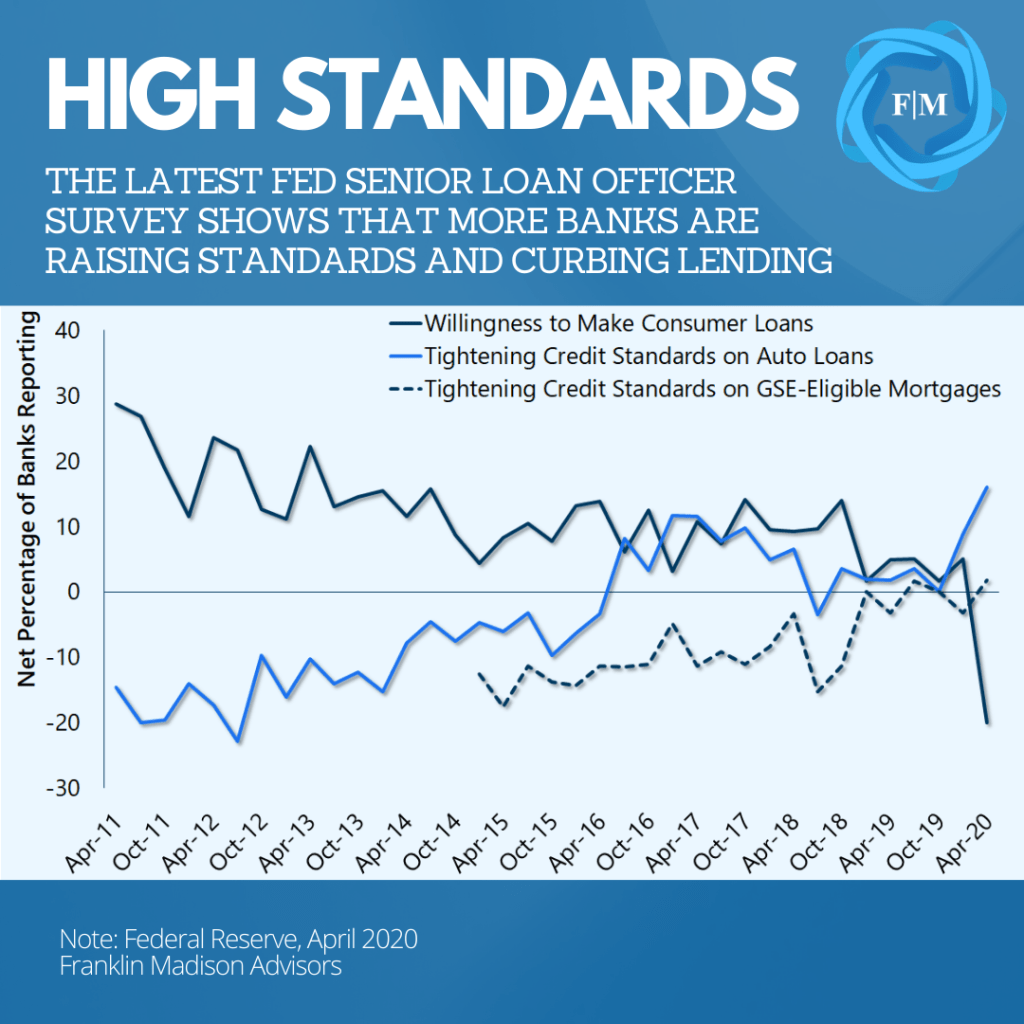

Compounding the problem of lower consumption is the fact that individuals willing and able to spend are finding it harder to borrow money. This issue is evidenced in the Fed's recent Senior Loan Officer Survey. It shows that banks are less willing to lend and that they are also raising lending standards. The implication is that individuals ready to spend, especially on big-ticket items like homes and cars, may find it increasingly difficult to obtain the loan necessary to complete their purchase.

Indeed, there's no question that the US economy is showing signs of having stabilized. Nevertheless, the ongoing healthcare crisis likely will alter household spending behavior and challenge market expectations of a quick economic recovery.

How should investors prepare for lower returns and ongoing uncertainties in the third quarter?

It's important to note that the second quarter rally has led to risk assets becoming expensive when measured by various valuation metrics. The combination of high asset prices and an unmitigated healthcare crisis may contribute to higher market volatility in the months ahead. In anticipation of a market pullback and increased volatility, we suggest that investors pare back recent gains to achieve two ends.

First, during this time of uncertainty, investors need to manage risk and ensure that their portfolios align with their long-term goals. Periods of market strength like we experienced in the second quarter can lead to portfolio drift. Therefore, we suggest that investors use recent market strength to trim winning positions and add to under-allocated holdings. This can be accomplished through portfolio rebalancing that realigns investment holdings with long-term target asset allocations.

Second, we recommend that investors prepare to use market volatility as an opportunity to raise cash. Periods of heightened market volatility may lead to selling assets at inopportune times. This is especially important given the tenable economic environment and ever present need to address unplanned life events. Therefore, we recommend that investors use this period of market strength to bring their portfolios back into alignment with long-term goals through rebalancing while at the same time setting aside some cash to meet unexpected needs.

Feeling Stuck Financially? Hit the Reset Button.

You've been diligent with your money. You've amassed sizable savings. Then life knocks on your door – a once-in-a-lifetime opportunity falls through, work moves you to another state, a family emergency calls, or your primary source of income evaporates. Years of diligent financial progress comes undone in an instant, and now you feel stuck.

Or maybe you're in a position where you've struggled for years to get a handle on your finances, but one disruption after the next keeps you from moving forward. In either case, what can you do when your financial life is stuck? Hit the reset button. Indeed, you can often get your financial life back on track much sooner than you would otherwise by pausing, resetting expectations about your goals, and being methodical in your approach to rebuilding your finances.

Pause and Disconnect

Unplug it and wait a minute. Shutdown your computer. Power down your device. If you've ever encountered a problem with technology, then one of these phrases will likely be the first recommendation you'll receive to correct the problem. While such advice often comes after you've spent many frustrating hours trying to get your router, computer, or phone to do what they're supposed to do, the simple solution often does the trick.

But what do you do if your net worth or savings have declined in value recently? After years of building up your nest egg, what remains today is only a fraction of its once glorious worth after a down move in the markets, a family emergency, or loss of income. During such times it's quite common for feelings of discouragement and negative self-talk to emerge, and you may even feel the temptation to make a big-ticket purchase or have the desire to double down on a loss.

One of the quickest methods, however, to reduce money-related anxieties and regain a sense of financial empowerment in your life during a time of loss or transition is to stop what you are doing, pause and take a break. Doing so may enable you to postpone financial decisions that you may later regret while giving you the ability to assess events that may or may not have been within your control.

What's more, like a project post-mortem or military debrief, the initial act of disconnecting from your financial routine shifts your focus from trying to fix a problem to reviewing lessons learned that might enable you to see opportunities in your new setting. More importantly, pausing and disconnecting may prepare you to rebuild your financial life in a way that is authentic to the present while making room for future growth prospects.

Reset Your Financial Expectations

In his book, Marshall Goldsmith, "What got you here, won't get you there" writes how successful leaders who progress in their careers must let go of old thought processes and adopt a fresh set of beliefs that fit their higher leadership positions. During times of financial adversity, you may double down on your existing financial habits in a bid to restore what you've lost or to get yourself unstuck. You may even end up taking actions that move you away from your problems like avoiding money related matters or procrastinating on critical financial decisions. What can you do if you find yourself in this situation?

If you want to get your finances back on track after a significant loss, then one of the first things you'll likely need to do is pause, disconnect, and identify an ideal financial outcome to move towards. The trouble with repeating old habits or moving away from an unfavorable situation is that your focus remains hinged on the past. For example, an at-bat baseball player is unlikely to get a base hit by worrying about striking out rather than focusing on the pitch.

So, what can you do to shift your focus to the future? Reset your expectations. Start by getting crystal clear about how you want your financial future to play out, given everything that has led you to the present circumstance. If your current financial situation causes feelings of disappointment, start thinking about the kinds of outcomes that would lead to feelings of achievement. And while goals, in general, are an excellent place to start, be sure to create financial objectives that set out specific outcomes for your life’s aim.

To be sure, your chances of getting financially back on track will rise when you reset your expectations from past mistakes and shift your focus toward ideal future outcomes.

Get It All Out on the Table

Your new financial objectives focus on the future and tell you where you're heading. But how exactly will you get there? Now's the time to sort through bills, statements, and reports and get everything on the table to evaluate your available financial resources. Think about this process from the perspective of a professional home organizer.

An individual may hire a professional organizer because they have a vision for how they would like their home to look and feel, but not sure what to do with all of their clutter. In some cases, a professional organizer will clear all the belongings out a room and work with their client, item by item, to decide on which pieces fit (and do not fit) into the future vision set out for their home.

After you've had a chance to reset your expectations, gather financial documents that will help you understand your debts, assets, and cash flows better. Start by pulling a copy of your latest credit report. This information will help you learn more about your outstanding debt, credit availability, and minimum payments on your various loans. Also, review statements or call your lender to determine the interest rate on your accounts.

Then, gather a list of your assets. Start with the current balances on your checking, savings, brokerage, and defined contribution accounts like a 401(k) or 403(b). Be sure to include retirement accounts left behind at an old job and pay particular attention to the cash values of defined benefit pension plans available to you. Also include the equity in your home, value of your automobiles, motorcycles, and any other readily saleable non-financial assets.

Next, make a list of all the expenses you have and expect to address soon. A straightforward approach to this end is to pull up your bank or credit card statement and review your purchases from the past three months. Then, categorize your expenses as either essential, discretionary, or savings. Computer software and phone apps can help automate and simplify this process. Either way, your aim is to capture and understand trends in your spending patterns.

Keep in mind that this process is likely to evoke mixed emotions as you recount past financial decisions. That's why it's essential to pause, disconnect, reset your expectations, and focus on the future as you develop a broad picture of your finances. Remember, a professional organizer removes belongings from a room to decide what to keep and what to throw away. That's why getting all of your finances on the table is crucial to success because without knowing what you've got to work with, it's hard to know what sort of plans to make to achieve your goals.

Prepare for a Marathon, Not a Sprint