A Disciplined Investment Strategy Built to Last

Protect and grow your wealth with a proven, cost- and tax-efficient process.

Fiduciary Investment Management for Tech Professionals

Managing your investments shouldn’t slow you down in a world where your career and life change at the speed of technology.

At Franklin Madison Private Wealth, we understand that, as a first-gen tech professional, your investment needs are as unique as your approach.

We know that you’re not just looking for investment management, you’re looking for a trusted advisor to help weave your financial goals into reality.

And we’re here to help.

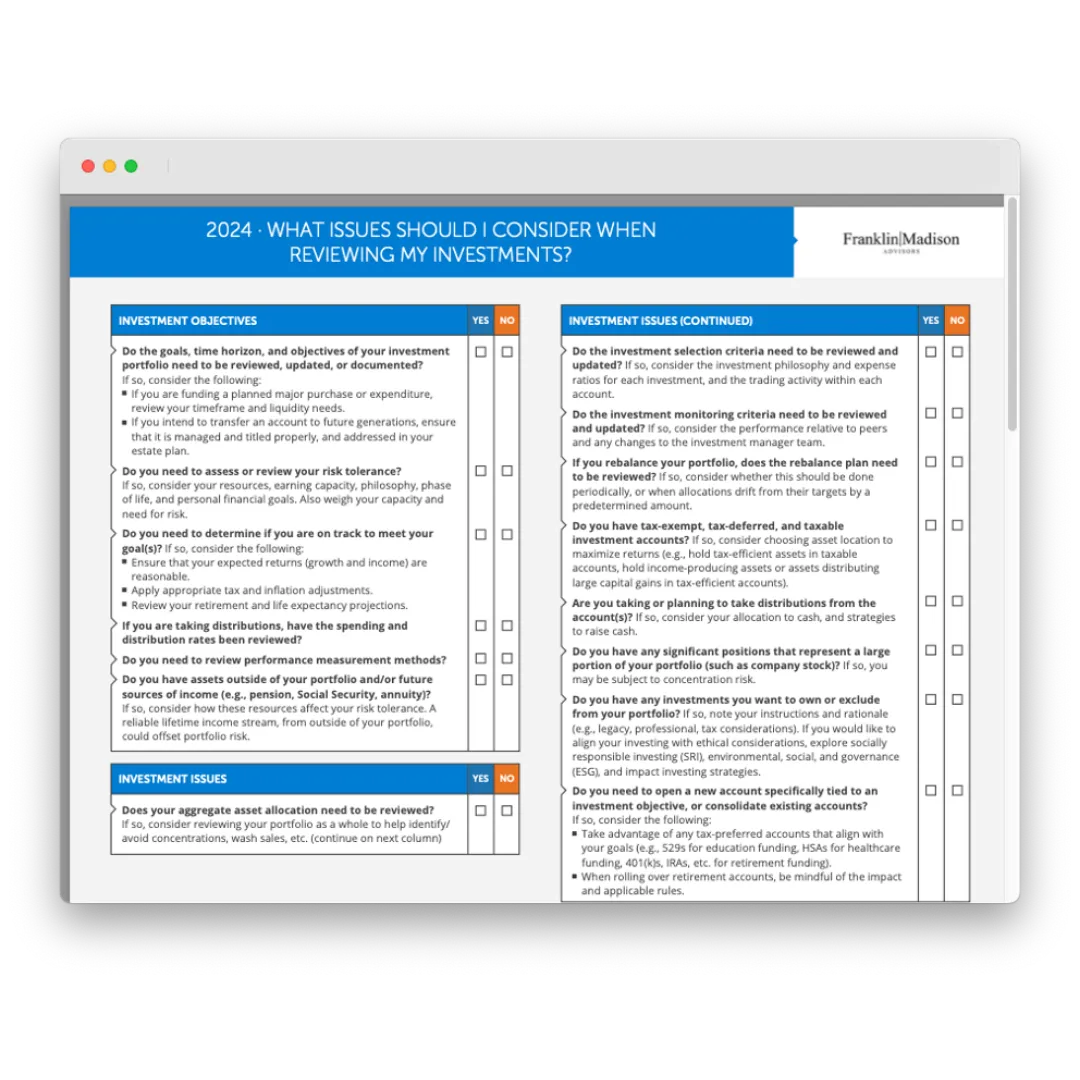

Free Checklist Download: Key Considerations for an Effective Investment Review

This guide is designed to aid tech professionals as they review their investment strategies, focusing on evaluating investment goals, risk tolerance, asset allocation, and the impact of external income sources.

Investment Strategies for High-Net-Worth Tech Professionals

Your journey in the tech world has been anything but conventional.

Why should your investments be?

Whether you’re getting started with investing or a seasoned investor, our investment management services are crafted to meet the unique needs of high-earning tech professionals like you.

Here’s how:

- Understanding Your Unique Narrative: We start by understanding not just your financial goals but the story behind them. Your aspirations, lifestyle, and risk tolerance are the foundation of our bespoke investment strategy.

- Tech-Driven, Human-Guided: Our approach combines the latest in fintech with personalized human expertise. This means sophisticated, data-driven investment strategies delivered with a personal touch.

- Transparent, Ethical Investing: We believe in clear, honest communication. No hidden fees, no complex jargon. Just straightforward, ethical investment management that aligns with your values and goals.

- Diversified Portfolios, Minimized Risk: We don’t just diversify your investments, we tailor them to balance opportunity with risk, aligning with your unique risk profile.

- Continuous Monitoring, Agile Response: The tech market is ever-evolving, and so are your investment needs. Our proactive management ensures your portfolio adapts to market changes and evolving life stages.

- Educational Empowerment: As a tech-savvy individual, you value understanding the ‘why’ and ‘how.’ We empower you with knowledge, helping you grasp the nuances of your investment choices.

- Integrated Financial Planning: Your investments are a piece of a bigger financial puzzle. We ensure they fit perfectly within your overall financial plan, from tax optimization to retirement planning.

- Accessible Expertise: Have a question? Need clarity? Your dedicated wealth manager is just a call or click away, ready to provide expert advice or a listening ear.

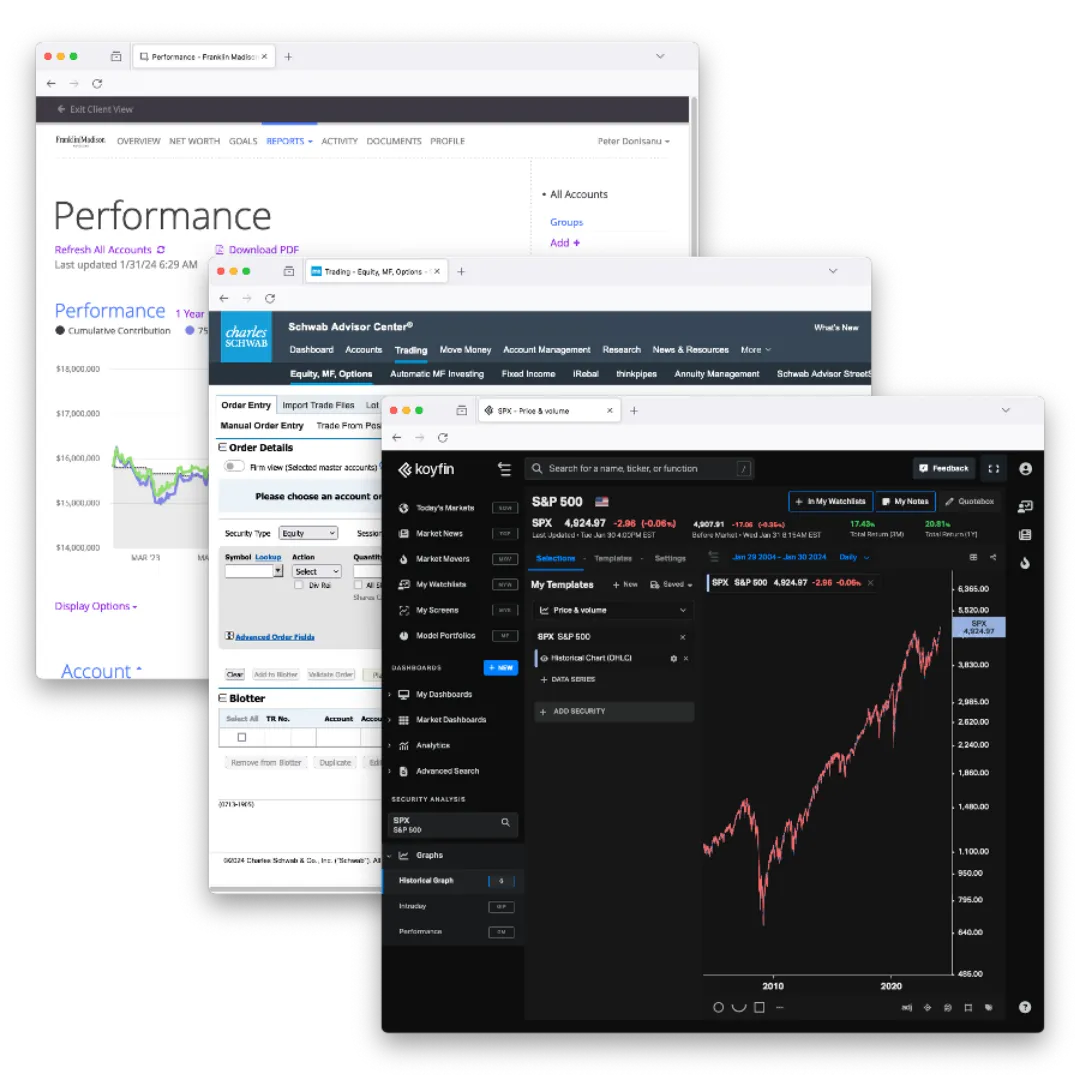

- Unmatched Custodial Services: Partnering with industry leaders like Charles Schwab, we offer secure, reliable custodial services, ensuring your assets are safeguarded with the utmost care.

Stay Informed and Build Your Legacy!

Subscribe to our weekly newsletter where you’ll receive actionable ideas on managing your wealth, including equity comp, taxes, investing, risk management and more to help get your financial house in order so you can live your legacy.

Your Investment, Your Future

At Franklin Madison Private Wealth, we’re more than just your investment manager, we’re here to help you build generational wealth.

We innovate in your financial space as you innovate in the tech space.

Let us manage the complexities of your investment portfolio so you can focus on living your legacy.

Ready to transform your approach to investing? Connect with us today, and let’s start crafting an investment portfolio as advanced and unique as your tech career.