2Q25 Market & Economic Update

Fear and uncertainty are two prevailing themes that emerged as we closed out the first few months of the year.

After a strong start to the year that saw the S&P 500 hit an all-time high in February, markets took a breather as policy uncertainty emerged.

And as winter turned to spring, so did investor sentiment. Concerns about rising policy uncertainty in Washington weighed on the market, and the S&P 500 ended the quarter on a lower footing.

While it’s natural to feel uneasy during a market pullback, it’s important to keep perspective. Markets go through cycles, with some driven by optimism, and others by caution. In this update, we’ll recap the first quarter, explain what’s behind the recent selloff, and share our view on where the economy may be headed.

There are a lot of moving pieces in play, and that can make headlines feel overwhelming. But with a solid financial plan in place, these moments of market stress can become easier to navigate. Our goal with this update is to help you focus on what matters most: making informed decisions that support your long-term financial wellbeing.

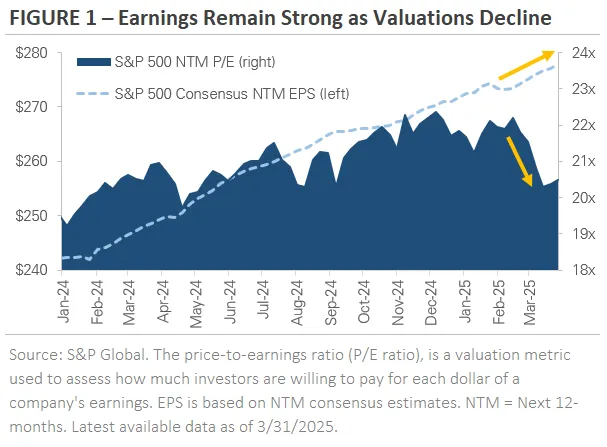

Stocks Trade Lower as Valuations Moderate

One of the biggest developments in the first quarter was a reset in stock valuations. What this means is that investors carefully evaluated how much they were willing to pay for a dollar of a stock’s earnings.

And while corporate earnings expectations held relatively steady, investors became more cautious, especially as policy uncertainty increased. As a result, stocks fell and not because profits disappeared, but because investors were less willing to pay top dollar for those expected profits.

Figure 1 provides helpful context. The dashed blue line shows Wall Street’s 12-month earnings forecast for S&P 500 companies. In contrast, the navy shading illustrates the market’s price-to-earnings (P/E) ratio, or how much investors are willing to pay for each dollar of earnings.

Historically, earnings estimates are less volatile than investor sentiment, and the chart shows that pattern continuing this quarter.

And so, during the first few weeks of 2025, optimism prevailed. But as headlines around tariffs and shifting policy agendas emerged, that optimism gave way to caution. Investors recalibrated their expectations, and valuations declined, falling from over 22x earnings to around 20x.

Now, while that may seem like a small adjustment, it had an outsized impact on stock performance. In short, markets got cheaper, even though company profits stayed largely intact.

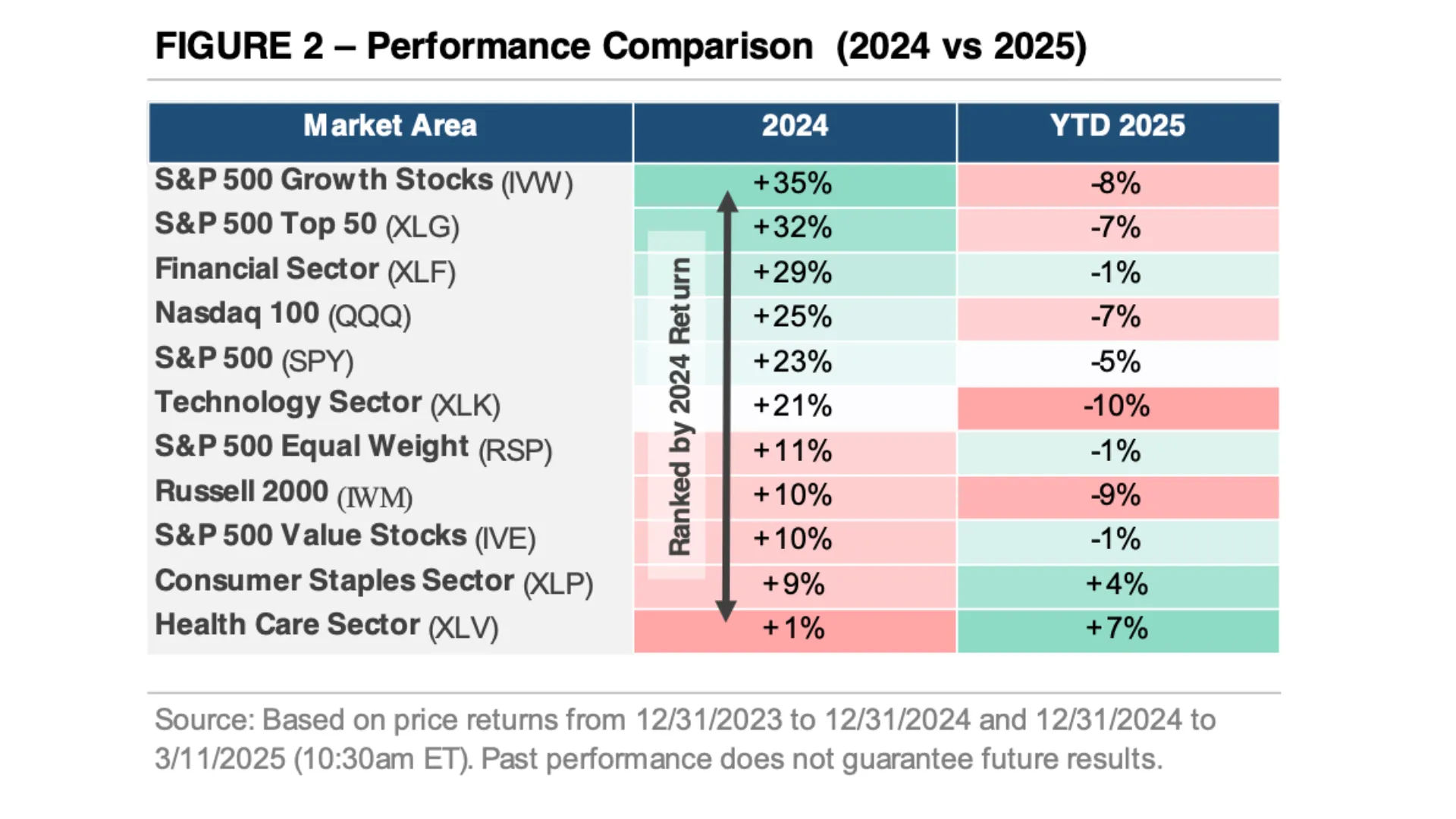

Another theme that emerged this quarter was centered around company size. Last year, the so-called "Magnificent 7" of Nvidia, Microsoft, Alphabet, Amazon, Tesla, Apple, and Meta, soared, lifting the broader S&P 500 by +23%.

This year, those same companies are pulling the index lower, down about -15% as a group. Meanwhile, smaller companies within the index are holding up better. For example, the equal-weighted S&P 500, which gives every company the same influence regardless of size, is down just -1%.

What this means for you: The market’s recent dip has more to do with investor mood than economic fundamentals for the time being. This view could change should policy missteps lead to a broader economic decline. Nevertheless, during this period of uncertainty, it’s essential to remember that your portfolio is built to weather these kinds of shifts, and to take advantage of opportunities when they arise.

Rising Policy Uncertainty is Impacting Sentiment

So, why exactly is policy uncertainty so important? Well, as households and business become less certain about the future, they tend to spend and invest less as well. And one of the main drivers behind this quarter’s market pullback was a shift in sentiment.

As new policies emerged from Washington, focused on trade, tariffs, and government spending, investors, business leaders, and consumers began to show signs of caution. While these developments are still evolving, they’ve introduced a level of uncertainty that markets typically dislike.

Figure 2 tracks three key sentiment indicators that help us understand how people are feeling about the economy:

- Consumer Sentiment (top clip): This comes from the University of Michigan’s well-known survey. After recovering steadily from the lows of the pandemic, consumer confidence dipped again in early 2025. Higher prices, policy shifts, and election-year headlines have likely all contributed to renewed anxiety. Since consumer spending drives nearly 70% of the U.S. economy, a dip in confidence can have ripple effects.

- CEO Confidence (middle clip): Business leaders are also showing signs of concern. The Conference Board’s index fell to its lowest level since 2011. CEOs are facing tough decisions amid uncertainty over tariffs, global trade dynamics, and potential changes to labor and immigration policy. When CEOs feel cautious, they tend to delay hiring, investing, or expanding, which can slow broader economic growth.

- Market Volatility (bottom clip): Measured by the CBOE Volatility Index (VIX), market turbulence picked up noticeably after mid-February. Some volatility is a normal part of investing, but the recent spike reflects investors trying to price in an unclear policy outlook. Until there’s more clarity, we may continue to see wider swings in the market.

Sentiment doesn’t always match reality, but it can influence behavior. People might spend less, hire less, or invest less simply because they feel uncertain. That’s why we monitor these data points.

Ultimately, they can help us anticipate how market participants might behave in the months ahead. While sentiment has softened, the economic data has not yet caught up, suggesting a possible lag between perception and actual economic activity.

So then, what sentiment data are telling us now is that there’s a potential that negative sentiment could feed into a self-perpetuating cycle of slower economic growth, slower earnings growth which could lead to more market volatility in the weeks and months ahead.

An Update on the U.S. Economy

Now, it’s easy to assume that when markets fall, the economy must be weakening too, but that’s not always the case. The stock market can be considered a voting, or discounting machine. It’s a forward-looking mechanism that’s trying to price in expectations about the future into today’s market.

So then, prices tend to move up and down to expectations, not just present conditions. And while market sentiment shifted this quarter due to policy uncertainty, the latest economic data tells a more nuanced story.

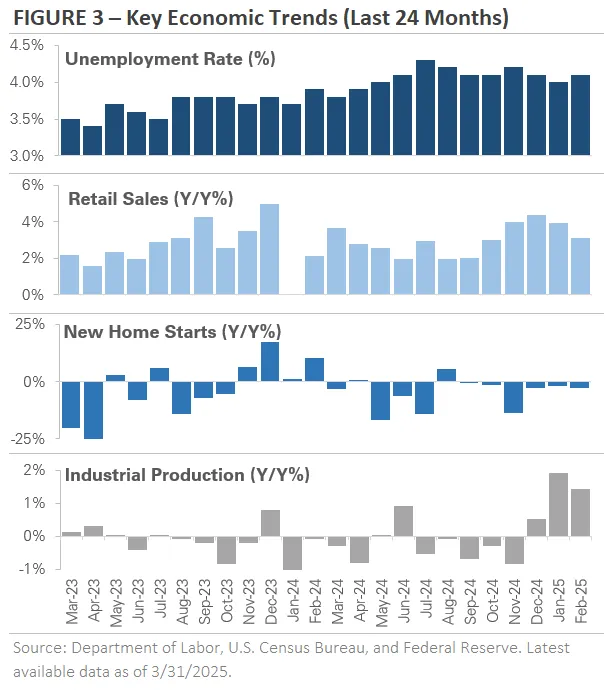

Figure 3 illustrates four key economic indicators that help us evaluate the health of the U.S. economy:

- Unemployment Rate (top clip): Despite headlines, the labor market remains solid. After ticking up in 2023 and early 2024, unemployment has moved lower in recent months as job growth has picked up. A strong job market means continued income for households and stable consumer spending which is the backbone of the economy.

- Retail Sales Growth (second clip): Consumer spending grew strongly in 2023, buoyed by higher wages and leftover savings from the pandemic. In 2024 and early 2025, growth has slowed, but not reversed. This signals that households are still spending, just more cautiously, which is a natural adjustment as interest rates remain elevated.

- Housing Starts (third clip): The housing sector has cooled in recent years due to high mortgage rates and affordability challenges. Builders are also facing added uncertainty as potential tariffs could increase material costs, and immigration policies may impact labor availability. Still, new home construction remains above pre-pandemic levels, a sign of resilience despite the headwinds.

- Industrial Production (fourth clip): This measure of economic output from factories, utilities, and mines declined through much of 2023 and 2024. Recently, however, it has begun to recover. Improved clarity on interest rate cuts and post-election policy direction ahead of tariff decisions could have contributed to renewed business investment.

The bottom line: So are we headed for an economic collapse? Well, it depends. Presently, the data suggests that the economy is still growing, but at a slower pace. The labor market is healthy, consumers are adjusting rather than retreating, and manufacturing is showing early signs of strength.

With that said, the effects of the Trade War are likely not yet fully reflected in the economic data. There’s a potential that, a policy misstep by the current administration could create conditions (weakening sentiment, lower spending and investment) that precipitate an economic slowdown.

That’s why these data points are worth monitoring closely. For now, we’ll continue to monitor the risks, particularly around policy impacts, as the overall data does not reflect that we’re currently in a recession.

Overall, it’s uncertain whether the short-term headlines will evolve into an economic decline. That’s why we believe it’s important to stay focused on long-term trends and avoid letting momentary shifts dictate your financial strategy.

Equity Market Recap: Looking Beyond the Index

So then, what does this valuation, sentiment and economic backdrop mean for stocks as we move through the second quarter?

Well, most of the stock market’s decline this quarter happened after the S&P 500 set a new all-time high on February 19th. And what’s crucial to understand is that this pullback wasn’t spread evenly across the market.

That’s because a handful of the largest, most recognizable companies bore the brunt of the losses, and as we pointed out earlier, their size meant they pulled the overall index down with them.

The “Growth” style of investing, which includes many of the big technology names that led in recent years, declined -10% in Q1. The Nasdaq 100, a tech-heavy index that includes the “Magnificent 7” fell -8%. But underneath the surface, the picture looked very different.

In fact, 9 of the 11 sectors in the S&P 500 outperformed the index. Seven of those sectors actually posted positive returns, while two were flat. Only two sectors, Technology and Consumer Discretionary, saw notable losses, and both are heavily influenced by the Magnificent 7 through the end of March.

In other words, there wasn’t a broad-based selloff per se in the first quarter. Rather, it was a concentrated recalibration of the companies that led the market higher in 2023 and 2024. Indeed, many of last year’s lagging sectors are this year’s leaders, showing how market leadership can rotate quickly.

International stocks also stood out in Q1. For example, the MSCI EAFE Index, which tracks developed markets outside the U.S., gained +8%, and posted one of its strongest quarters of outperformance since 2000.

Europe, in particular, saw strength as governments unveiled new spending initiatives. And the MSCI Emerging Markets Index also gained +4.5%, outpacing the S&P 500 by nearly +9%.

Market headlines often focus on the S&P 500, but that’s just one slice of a broader, globally diversified portfolio. Last quarter’s performance reminds us why we diversify: when one area struggles, others may thrive. That balance helps smooth returns and reduce risk over time.

Credit Market Recap: Bonds Trade Higher in Q1

While stocks declined in the first quarter, the bond market offered a measure of stability. In fact, bonds did what they’re often designed to do: provide diversification and help cushion portfolios during periods of market stress.

There were two main themes in the bond market this quarter: a drop in U.S. Treasury yields and a widening in credit spreads.

First, let’s talk about yields. The 10-year Treasury yield fell from around 4.80% in mid-January to 4.15% by early March. This decline reflected a shift in investor behavior as concerns over policy uncertainty, potential tariffs, and a slowing economy pushed investors to seek safety in longer-term government bonds.

When demand for these bonds rises, their prices go up and their yields fall.

As bond prices rose, investors benefited, especially those with Treasury exposure. This helped offset some of the losses from the stock market and reinforced the value of owning high-quality bonds as part of a diversified strategy.

As we enter the second quarter, this theme is being challenged as some large investors question holding Treasuries. However, it’s crucial to note that the Treasury market still remains the largest and most liquid bond market globally, and is backed by the Federal Reserve.

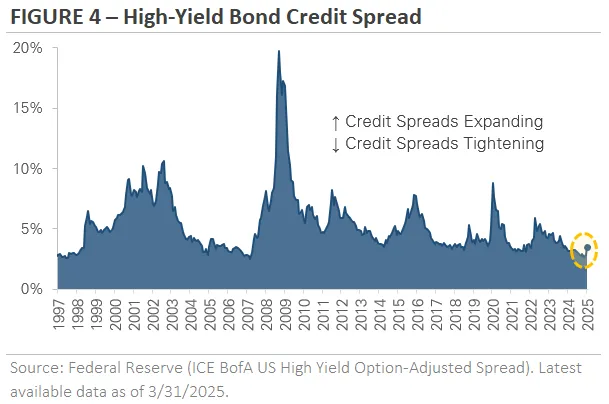

With that said, the second major and notable bond market theme in the first quarter was credit spread expansion. Now, this theme is something to watch as it’s typically reflective of market or economic uncertainties.

That’s because credit spreads measure the extra yield investors demand to lend money to corporations, compared to lending to the U.S. government. Wider spreads mean investors are more cautious because they see greater risk in lending to companies, especially those firms with lower credit ratings.

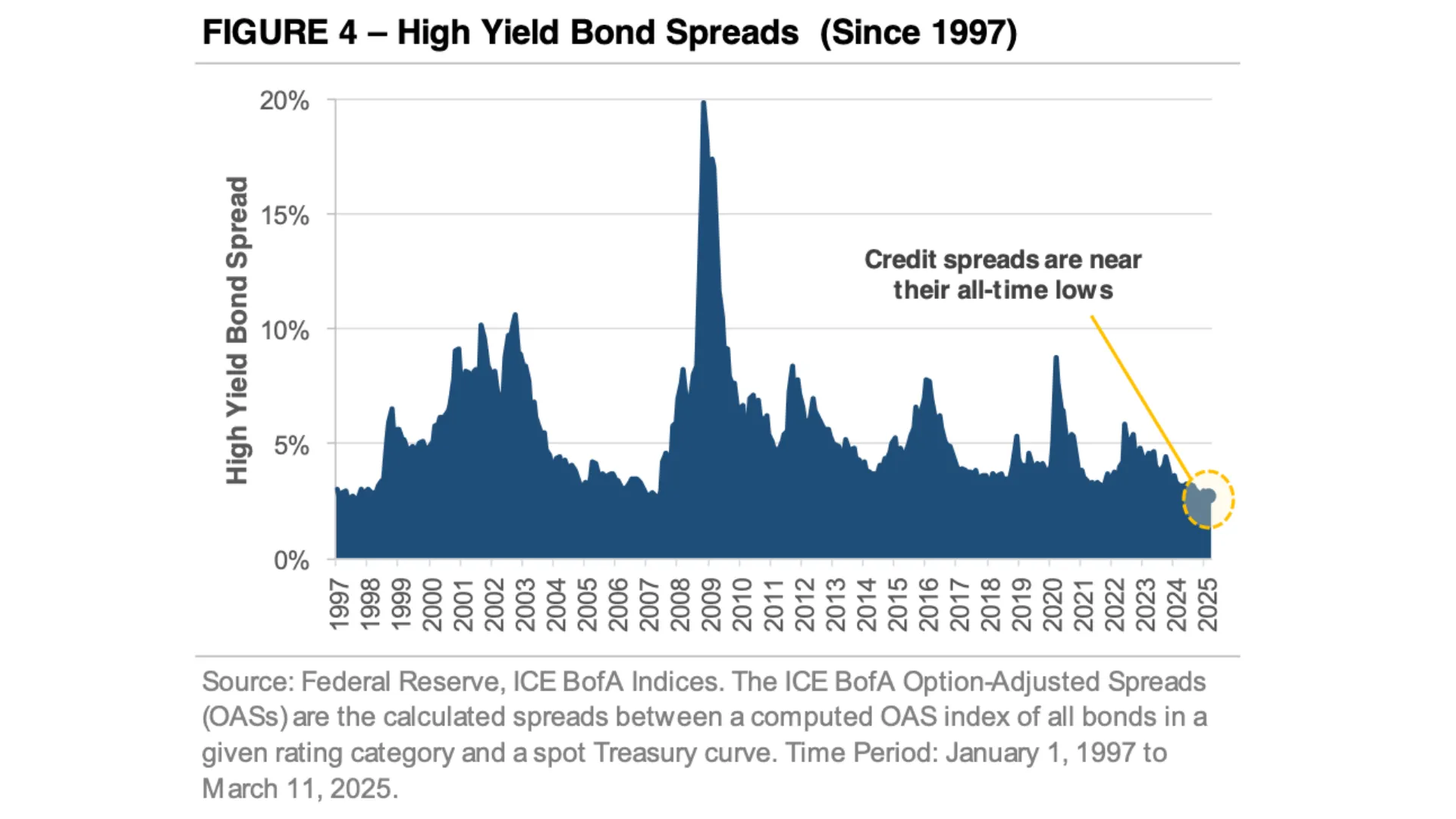

Figure 4 charts the high-yield credit spread going back to 1997. And after narrowing in late 2024, when the Federal Reserve began cutting rates, spreads began to widen again in Q1. The yellow circle highlights this recent shift. This suggests that investors are now more sensitive to risks around tariffs, slower growth, and policy change.

That said, spreads remain low by historical standards, which likely means that while caution has increased, the bond market isn’t flashing warning signs of financial stress. Indeed, by some measures, companies still have access to capital, and credit markets remain functional barring external shocks from further policy mis-steps.

Overall, bonds remain an important stabilizer in your portfolio regardless of what you’re reading in the headlines. Even as uncertainty rises, high-quality bonds continue to provide ballast during turbulent periods. And while credit spreads have widened slightly, the broader financial system remains sound for now, which is another reason to stay grounded and focused on your long-term plan.

2025 Outlook: Maintaining a Long-Term View

Periods of market volatility can feel unsettling, especially when headlines are filled with ambiguity. But these periods are not only normal, they’re expected as part of a typical economic and market cycle.

In fact, they’re part of what makes long-term investing work.

How so?

Well, pullbacks help reset expectations, cool overheated areas of the market, and set the stage for future gains.

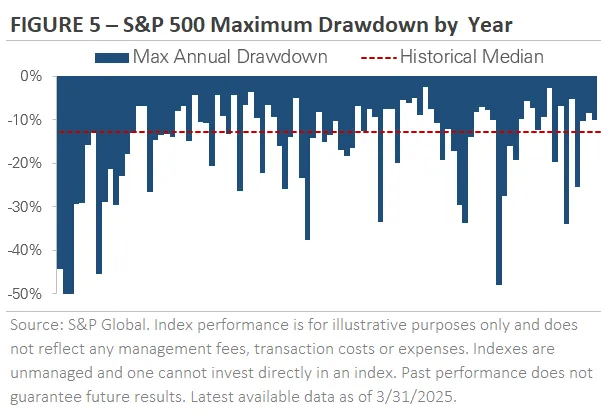

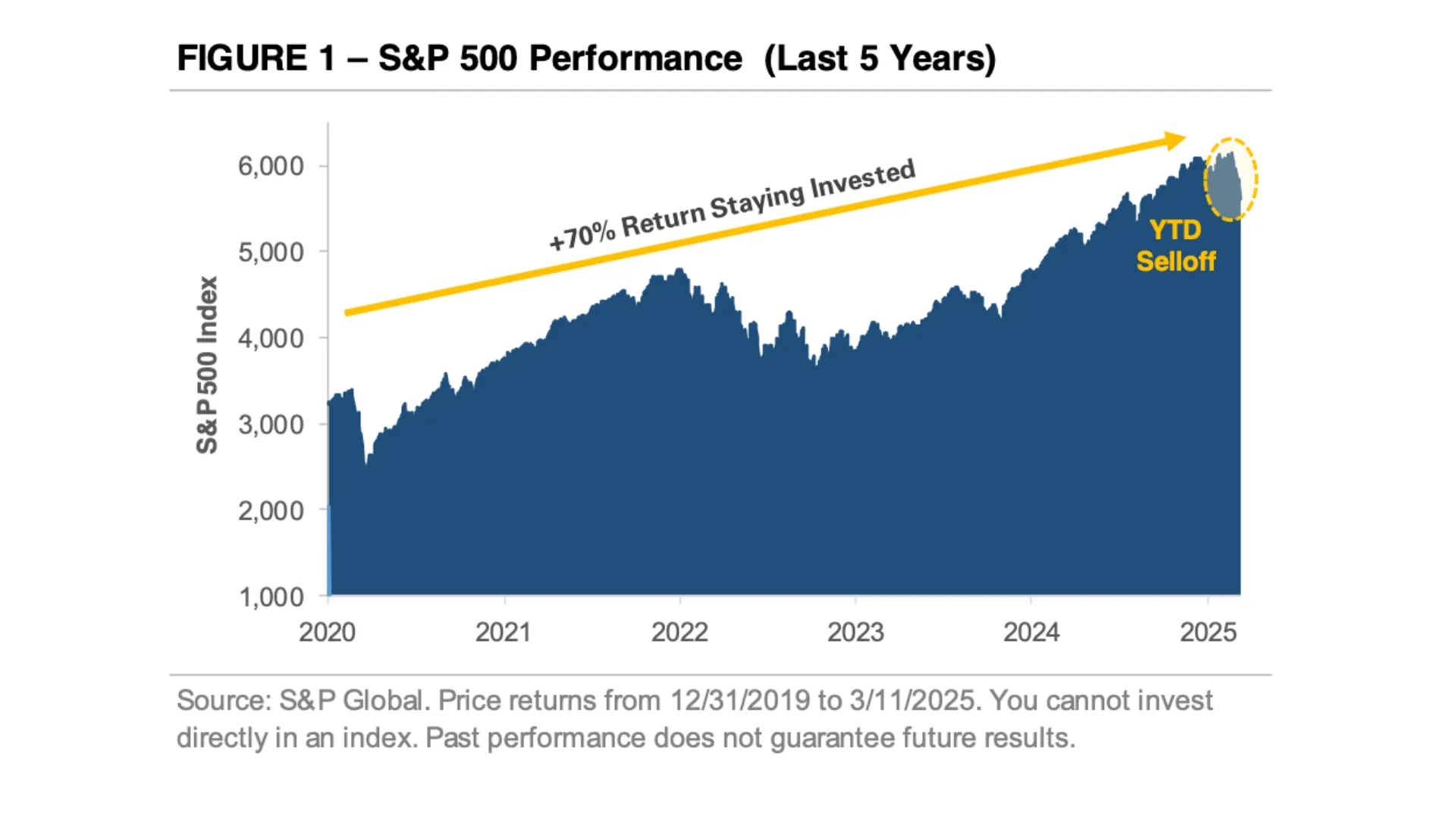

Figure 5 puts this into perspective. It shows nearly a century of S&P 500 data and highlights a simple truth: market pullbacks happen almost every year. Since 1928, the index has experienced a decline of at least -5% in 91 out of 98 calendar years. The median intra-year drop is -13%. This year’s volatility isn’t unusual, it follows a well-established pattern.

In fact, despite wars, recessions, inflation spikes, financial crises, and global pandemics, the market has consistently recovered and moved higher over time. That upward trajectory has been fueled by economic growth, innovation, and corporate profitability and not just investor optimism.

Here’s the key takeaway: volatility is the price of admission for long-term growth.

And trying to avoid short-term swings by timing your way into and out of the market often means missing the eventual rebound. So then, by staying fully invested, no matter what the market is doing, you give your portfolio the chance to participate in compounding returns over time.

Overall, my job is to help you stay focused on what you can control, including your goals, your risk tolerance, your long-term plan. When the headlines shift, your strategy doesn’t have to because we’ve built a plan designed to weather times like these, and we’re here to help you stick with it.

Whether markets are rising or falling, the most powerful tool we have is perspective. And right now, perspective reminds us that temporary setbacks are a normal part of progress, and that long-term success comes not from reacting to every twist and turn, but from remaining committed to a thoughtful plan.

Liberation Day: What to Make of the Latest Tariff Announcement

This week, the U.S. government announced new tariffs starting with a 10% tax on all imported goods starting April 5.

Some countries, like China, will face even higher tariffs as part of a plan to push for fairer trade. These changes have caused markets to react quickly, with some stocks falling sharply and investors turning to safer options like bonds.

Now, it’s natural to have questions about what this means for the economy, your cost of living, and your investments.

That’s why in this update, I’ll walk you through what’s happening, why it matters, and how to think about your next steps.

What’s Happening and Why Now?

The Trump administration is rolling out a major shift in trade policy.

Beginning April 5, a 10% tax will apply to all goods imported into the U.S., with very few exceptions.

Then, on April 9, extra tariffs will be added for about 60 countries that are seen as having unfair trade practices.

For example, goods from China could face tariffs as high as 54%.

The goal?

Reduce the country’s $1.2 trillion trade deficit and bring manufacturing jobs back to the U.S.

This plan has been in the works since the last presidential campaign, and President Trump is calling the launch “Liberation Day,” hinting that these changes could be long-lasting.

Still, other countries may push back, and that could force future changes to the plan.

Are We Headed for a Trade War or Recession?

Right now, countries like China and those in the European Union are warning that they may fight back by placing their own tariffs on U.S. goods.

That raises fears of a trade war, which could slow the global economy. But so far, no official counterattacks have been made.

Economists say these tariffs could reduce U.S. economic growth and increase inflation, meaning prices might go up.

That doesn’t mean a recession is guaranteed, though.

The last time tariffs were raised back in 2018 growth slowed but stayed positive, thanks to strong consumer spending.

These new tariffs cover more goods, so the risks are higher, but the future is still uncertain.

How Are Markets Reacting?

Markets don’t like surprises, and this announcement was a big one.

Stocks dropped as news broke, especially for companies that rely on imports, like Apple, Ford, and Nike.

At the same time, bond prices went up as investors looked for safer places to put their money. Oil prices also fell due to concerns about slower economic growth.

While this reaction feels dramatic, it’s also common.

Markets often move quickly on news before all the details are known. That’s why we stay focused on long-term investing.

Your portfolio was built with days like this in mind, and it includes a mix of assets including U.S. and international stocks, bonds, and real estate that work together to manage risk.

Will This Raise My Everyday Costs?

Possibly, but not right away.

While tariffs begin in early April, it takes time for supply chains to adjust.

Some companies may raise prices, but others might absorb the extra costs at first.

If prices do go up, it could mean an extra $1,000 a year for the average household, with increases on things like phones, cars, and appliances.

Still, these are estimates, not guarantees.

We’ll be watching how companies respond and how prices shift over the next few months.

What Should I Do Right Now?

There’s no need to take action right away.

The effects of these tariffs will unfold over time. If you’ve been planning a big purchase. like a car, it might make sense to move sooner, just in case prices rise.

For everyday expenses, consider leaving a little extra room in your monthly budget.

As for your investments, patience is key.

We’ll keep a close eye on how things develop, and we’re here if you have questions.

Nevertheless, keep in mind that reacting too quickly to headlines can do more harm than good over the long-term.

Big Takeaway

Uncertainty is part of investing, and times like these are exactly why we’ve taken a diversified, long-term approach.

I’ll continue monitoring how these tariffs play out and keep you updated along the way.

If you’re feeling concerned or just want to talk things through, don’t hesitate to reach out, I’m always here to help.

Market Update: Is it a Correction or Something Bigger?

What do you do when the market takes a turn you didn’t expect? Do you panic? Do you make quick decisions? Or do you take a step back and look at the bigger picture?

As we step into the first few months of 2025, the market has given investors plenty to think about. Stocks started the year on a strong note, but since then, we've seen a pullback. The S&P 500 briefly entered correction territory, bringing its year-to-date return down to -5%.

Similarly, the Nasdaq 100, home to some of the biggest names in tech, is down 7% this year, while the small-cap Russell 2000 has fallen 9%. And the what about the Magnificent 7 of Microsoft, Apple, Meta, Alphabet, Amazon, Nvidia, and Tesla? They’re down nearly 15%.

So what’s really going on? More importantly, what should you do about it?

What’s Behind the Market Selloff?

Well, it’s easy to blame market swings on one big event. But in reality, it’s rarely just one thing because there are likely a few reasons this year’s recent pullback.

First, the stocks that led the charge last year are the ones struggling the most today. And it’s not unusual to have yesterday’s winners become today’s laggards. Indeed, figure 2 shows us that the biggest winners of 2024, like tech stocks and the Magnificent 7, have become 2025’s underperformers.

Why?

Because last year’s rally was built on enthusiasm, especially around artificial intelligence. And when enthusiasm drives prices higher, valuations get stretched. Investors pile in, positioning gets crowded, and eventually, the weight of that momentum starts to break down.

That’s what’s happening now.

Second, investors, both individual and institutional, came into 2025 with a high level of exposure to stocks. In fact, some of the largest institutional investors like pension funds, endowments, and insurance companies held a record share of their wealth in equities.

And that strategy works well when markets are climbing, but when momentum reverses, institutional investors start deleveraging. And when they unwind positions quickly, it amplifies the selling pressure.

Finally, there’s the policy backdrop. What started as optimism around pro-growth policies under the Trump administration has shifted to uncertainty. As we’ve written about before, concerns about spending cuts and the impact of tariffs have raised questions about economic growth.

Because the fact of the matter is that investors don’t like uncertainty, and right now, they’re adjusting to a new, highly uncertain reality.

Market Volatility vs. Economic Reality

So, does all this mean the economy is struggling? That’s a great question. And here’s where we need to separate perception from reality.

The stock market reacts quickly to new information, but that doesn’t always mean the economy is following the same path. One way we can test that is by looking at real-time economic data.

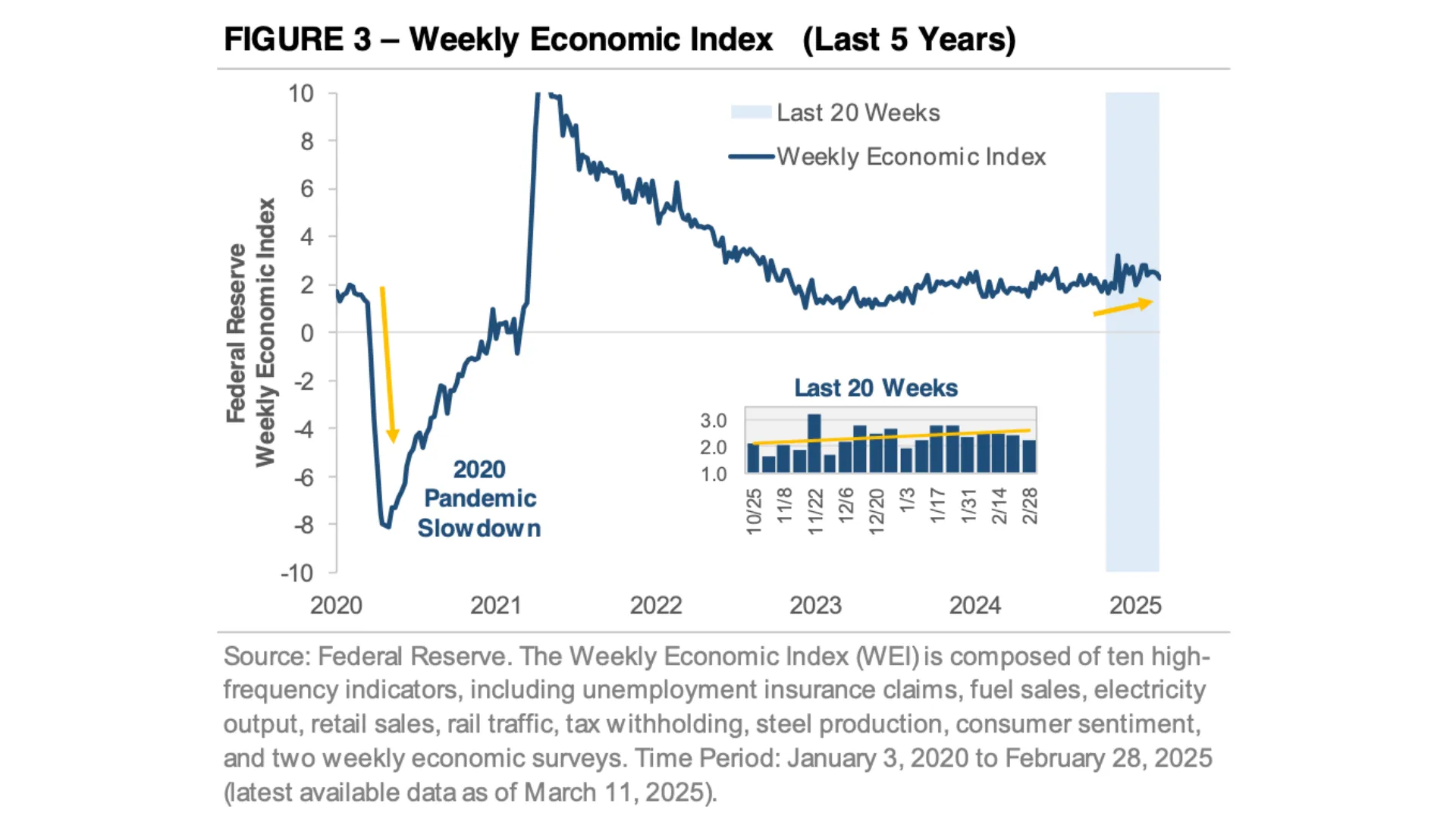

For example, the Federal Reserve’s Weekly Economic Index (WEI) tracks real-world activity using data points like unemployment claims, rail traffic, steel production, and tax withholdings.

And right now? It’s still positive (Figure 3).

Another piece of the puzzle is the bond market. High-yield credit spreads, which are essentially the difference in yield between risky corporate bonds and safer U.S. Treasuries, are a great way to measure financial stress.

And today, those spreads remain near all-time lows (Figure 4). Indeed, if we were facing a deeper economic problem, we’d expect to see those spreads widen. The fact that they haven’t tells us this market selloff could be more about repositioning than it is about a fundamental crisis.

With that said, no one rings a bell when we’ve entered a recession. And it’s very well possible that a policy error from the current administration could push the economy into a downturn. For now, however, the data continue to reflect modest economic growth.

Is This Normal and Can the Market Selloff Continue?

Now, if you’ve been investing for a while, you likely know that market volatility isn’t new. But let’s be honest, knowing that doesn’t make it feel any better when stocks drop, does it?

So what should you do?

Well, one of the best things we can do is put this moment in perspective. For example, since 1928, the S&P 500 has experienced a decline of 5% or more in 91 of the past 98 years.

Read that again.

In almost every year on record, we’ve seen the market pull back like this. And yet, time after time, markets have recovered. Investors who stay the course, who focus on the long-term, are the ones who have been rewarded.

So let me ask you: What’s your plan?

Because the difference between reacting and responding is having a plan. The key isn’t trying to predict every market move. It’s making sure you’re positioned to succeed no matter what happens next.

And that’s why sticking to a disciplined process and having a long-term perspective matter over the long-run.

The Bottom Line

Market volatility often feels personal. It’s your retirement savings on the line, isn’t it?

And so, when you see headlines about market swings, it’s easy to wonder, “Is this the beginning of something bigger? Am I missing something? Should I be doing something differently?”

So then, if that’s where your mind is right now, you’re not alone.

But more importantly, you’re not powerless. You don’t have to let fear dictate your financial future. You can make decisions based on a thoughtful strategy rather than short-term emotions.

Whether you’ve been working with our team for years or you’re just starting to explore your options, here’s what I want you to hear: clarity, confidence, and peace of mind don’t come from guessing the market’s next move. They come from knowing you have a plan that’s built for moments like this.

Because at the end of the day, the market will move up.

It will move down.

That’s a given.

But those who stay focused on the long term, those who stay diversified and patient, won’t just weather today’s volatility. They’ll be in the best position to thrive beyond it.

So, the real question isn’t what will the market do next? The real question is: Are you ready for whatever comes next?

The Market Feels Unstable — Here’s How to Stay on Track

There are times in market cycles when economic, geopolitical, and financial conditions converge in ways that create palpable uncertainty. In many ways, it can feel like standing on the precipice of an abyss.

Today, I would argue that we are in just one of those moments.

Often, it’s not just one event, but a cascade of interconnected developments that lead one to conclude that things are about to get bad.

History Often Rhymes

Early on in my career, it started with the failures of Bear Stearns and Lehman Brothers, the nationalization of Fannie Mae and Freddie Mac, and the bailouts of AIG and Citi, all of which signaled the fragility of the global financial system in 2008.

In 2020, early reports of health warnings, travel restrictions, and border closures eventually escalated into a near-total shutdown of the global economy, prompting widespread existential fear.

Now, in early 2025, we are experiencing heightened uncertainty as the resumption of trade wars with ambiguous objectives, shifting geopolitical alliances, and a retreat from post-war global institutions and a seeming move towards isolationism create a new political and economic reality. These shifts pose significant implications for the global economy and financial markets.

Needless to say, there is much to worry about in the current political, economic, and market environment. It’s enough to make any sane person want to bury their savings in their backyard.

How to Navigate the Uncertainty

That said, having been through multiple market cycles, being an avid student of history, and considering my background in macroeconomic strategy, I would like to share some thoughts on how to frame today’s environment and what you can do about it financially.

Firstly, I want to acknowledge that we are in the midst of an anxiety-provoking time in U.S. history. I am not going to discount the legitimate fear that many of us may be feeling right now amidst all the political tumult and economic uncertainties. This is a natural response.

With that said, when it comes to investing and the markets, it’s crucial to remember that we’ve been through similar challenges in the past. And with history as our guide, during times like these, it’s essential to remain committed to a long-term, disciplined investment strategy.

Make no mistake, what’s happening today will have significant implications for years to come.

Why It’s Essential to Stay Committed for the Long-term

However, history has shown that, from a capital markets perspective, risk assets tend to sell off during political and economic inflection points, before eventually recovering. These ebbs and flows are a natural part of the market process when key narratives change.

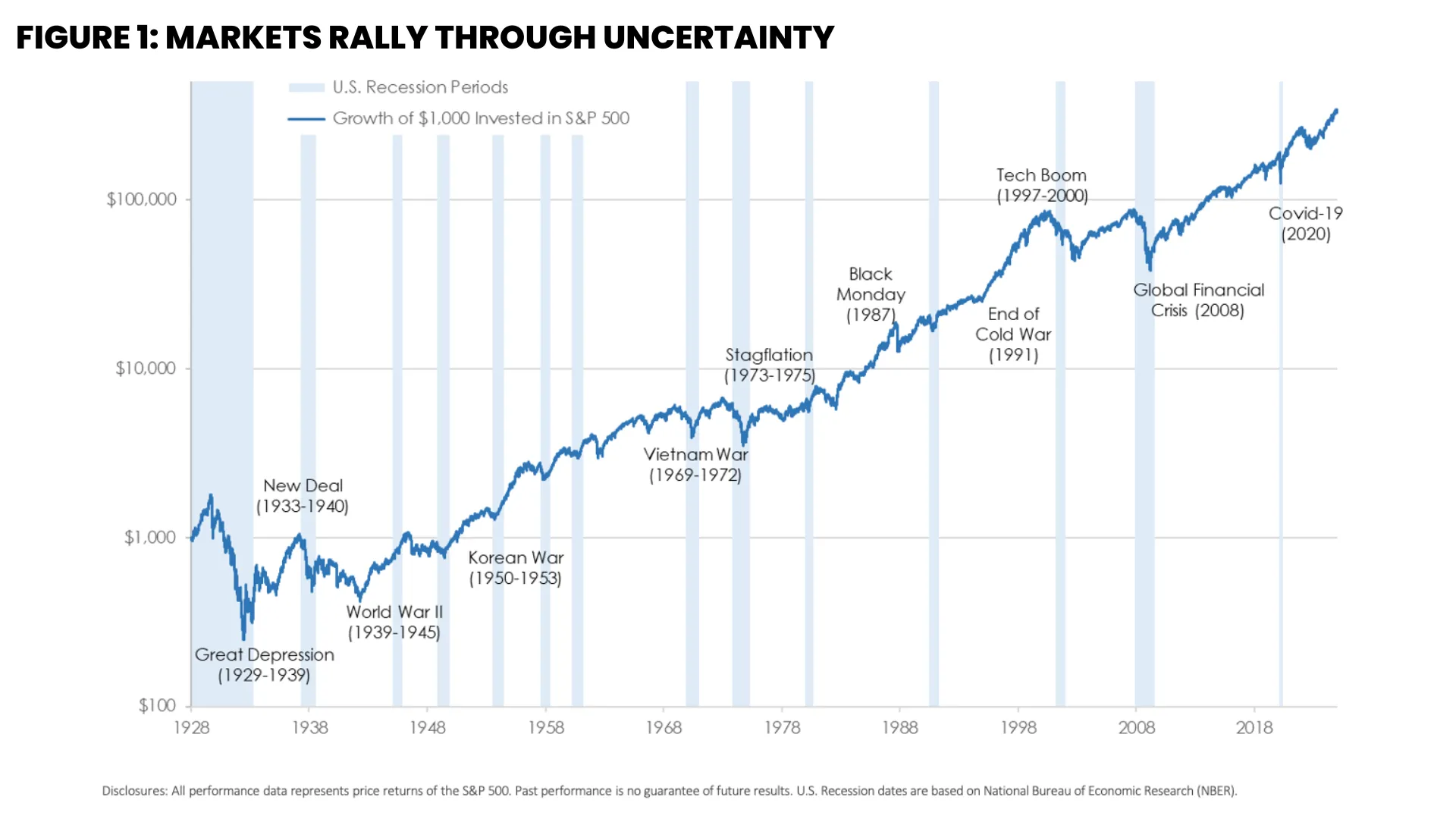

In fact, over the past 100 years, there have been many paradigm-shifting political and economic events, but stock prices continued to march higher thereafter. This point is evidenced in Figure 1.

To be sure, financial markets, after periods of uncertainty, do eventually recover as investors eventually adapt to new political or economic paradigms. Indeed, as figure 1 illustrates, risk asset prices are naturally biased to the upside because if they weren’t, then investing would not be much different from gambling, would it?

Nevertheless, you might say that now is not the right time to be in the markets and that you would prefer to get out. However, history has also shown us that exiting the markets at the wrong time could lead to major disappointment down the road.

For example, Figure 2 shows how missing even the best five days over the past 20 years could have led to significant missed opportunities in the markets. Indeed, back in 2008, it is arguable that peak market fear occurred at the end of the year, just a few months before the market bottomed out in March 2009.

Similarly, in 2020, peak fear occurred in late February before markets bottomed out in March and then took off again in April. Therefore, trying to time the markets or get out when it feels like things are starting to get bad might work against you over the near- and long-term.

Practical Steps to Take

So then, amidst all of this, what should you do about it all?

Well, in uncertain times, many investors often find themselves torn between taking action and standing still.

Here are six key strategies to consider regardless of where you stand today:

#1 Know Your “Sleep Well Number” (Cash Management)

When it comes to cash management, during times like these, it is crucial to know your “sleep-well” number. Depending on where you are in your retirement journey, having enough cash on hand to cover six to eighteen months of living expenses is something to consider now.

Having this number available will enable you to avoid making knee-jerk decisions with your portfolio, enable you to stay committed to your long-term strategy and avoid selling assets at an inopportune time.

#2 Rebalance Your Portfolio

Rebalancing your portfolio now allows you to take some risk off the table. Markets have rallied handsomely over the past eighteen months, which means that your current holdings are very likely out of alignment with your strategic asset allocation.

Rebalancing includes taking gains from positions that have done well in your portfolio and adding to positions that are underallocated in your portfolio relative to your strategic allocation. This approach ensures that you’re not taking any more risk than necessary with your investments.

#3 Stick to Your Long-term Plan

When in doubt, stick to your plan. Remembering your long-term plan is essential during market uncertainty. That’s because it is easy to become distracted and search for a salve to relieve the unease in the near term when things start going off the rails.

However, it’s crucial to remember that your financial plan was created to help you navigate not just the good times, but also uncertain times like the ones we’re experiencing today.

#4 Reconsider Big-Ticket Purchases

If you are contemplating purchasing a new home, car, or other big-ticket item, you may want to consider holding off on any moves for the next few months. This approach will allow you to preserve cash and ensure that you are not locking yourself into a decision at an inopportune time.

#5 Sharpen Your Pencil

At the same time, it is worth sharpening your pencil. Warren Buffett is known to have said, “Be fearful when others are greedy, and greedy when others are fearful.” Depending on your living situation and cash position, fear-driven market sell-offs often provide opportunities to purchase assets at a discount.

If you are in a solid cash position, keeping an eye out for favorable buying opportunities once we have more clarity on the political and economic environment could be worthwhile.

#6 Consider Tax Planning Opportunities

Finally, market sell-offs also present an opportune time for tax planning. And a key tax planning approach includes completing a Roth conversion. That’s because lower portfolio values often translate to lower taxable values. Remember, Roth conversions are not just a fourth-quarter tactic but a year-round opportunity.

Similarly, market downturns can present opportunities for tax-loss harvesting. This approach involves selling stocks at a loss and buying a similar but not identical asset. Even if you do not have gains to offset the losses, you can carry forward the losses as a tax asset to offset future capital gains.

The Big Takeaway

When it comes down to it, the big takeaway from an investment perspective is to stay invested for the long term even though the near term seems so uncertain. While we may be headed for a dark period in the months ahead, I am reminded of how essential it is to remain optimistic.

Viktor Frankl, a Holocaust survivor and author of the book, “Man’s Search for Meaning”, points out in his work that those who adapted and sought meaning in each moment, especially in trying times, had greater ability to endure trials and uncertainty than those who did not.

Make no mistake, we are likely headed for some very trying times in the weeks and months ahead. From a political and social perspective, we do not have a roadmap for navigating what lies ahead, which means we will have to take things one moment at a time. As difficult as that may be, however, finding purpose and direction in uncertain times has always been a defining trait of those who successfully emerge from such events.

What’s more, from a financial perspective, history has repeatedly shown that uncertain times like these often create opportunities for those who stay the course. That’s why having a solid financial plan and a disciplined investment strategy is essential now more than ever. While the near-term outlook may be uncertain, remaining objective and committed to a well-thought-out financial plan continues to be the best way forward.

Fed Policy: Are Rates Poised to Head Higher or Lower in 2025?

Are interest rates headed higher or lower in 2025? Well, it likely depends on the incoming data.

Indeed, not long ago, the Federal Reserve launched one of the fastest rate-hiking cycles in history as it was determined to bring inflation down from a multi-decade high. After keeping rates elevated for more than a year, the Fed shifted course in late 2024, cutting rates by a full percentage point between September and December.

Today, however, policymakers appear to be taking a "wait-and-see" approach as incoming data present conflicting stories.

The Fed's Balancing Act: Inflation vs. Employment

Now, to understand where things stand, it helps to remember that the Fed has two main responsibilities.

First, it aims for price stability, which means keeping inflation low and predictable. Second, its job is to seek out full employment, ensuring conditions that encourage job growth while keeping unemployment in check. The challenge today is that these two goals don't always align perfectly. And right now, the balance between them is changing.

How so?

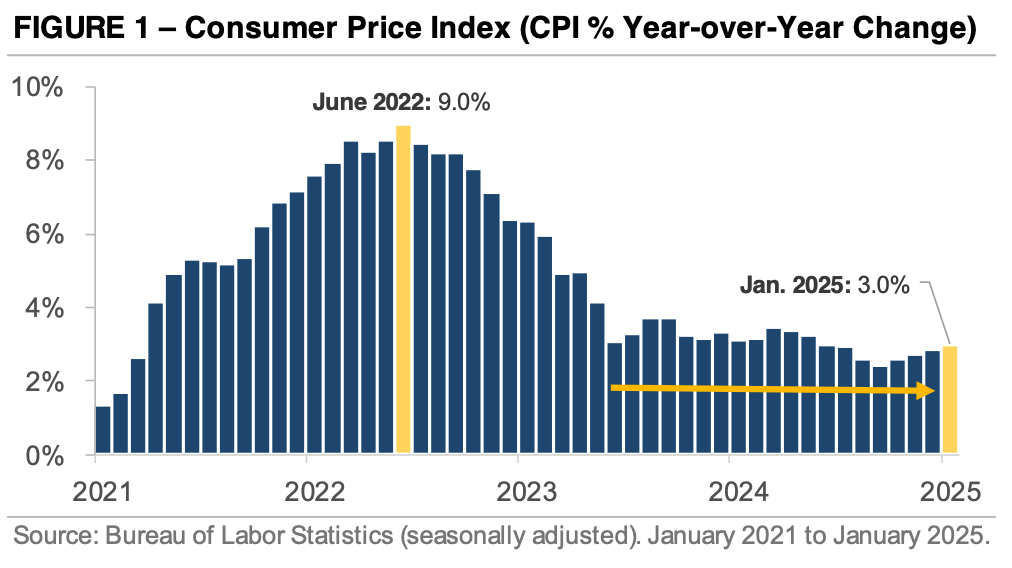

Well, consider inflation. The chart in Figure 1 tracks the year-over-year change in the Consumer Price Index (CPI), which measures how the prices of everyday goods and services fluctuate. Throughout most of 2024, inflation had been steadily declining.

However, in January 2025, inflation picked up again. CPI rose 0.5% from the previous month, marking the largest increase since August 2023. As a result, the annual inflation rate inched up to 3.0%, slightly above December's 2.9%.

And while inflation has come down significantly from its peak of nearly 9% in mid-2022, progress has stalled in recent months. Indeed, since late 2023, CPI has hovered around 3%, raising concerns that inflation could remain above the Fed's 2% target for an extended period.

Conflicting Jobs Data

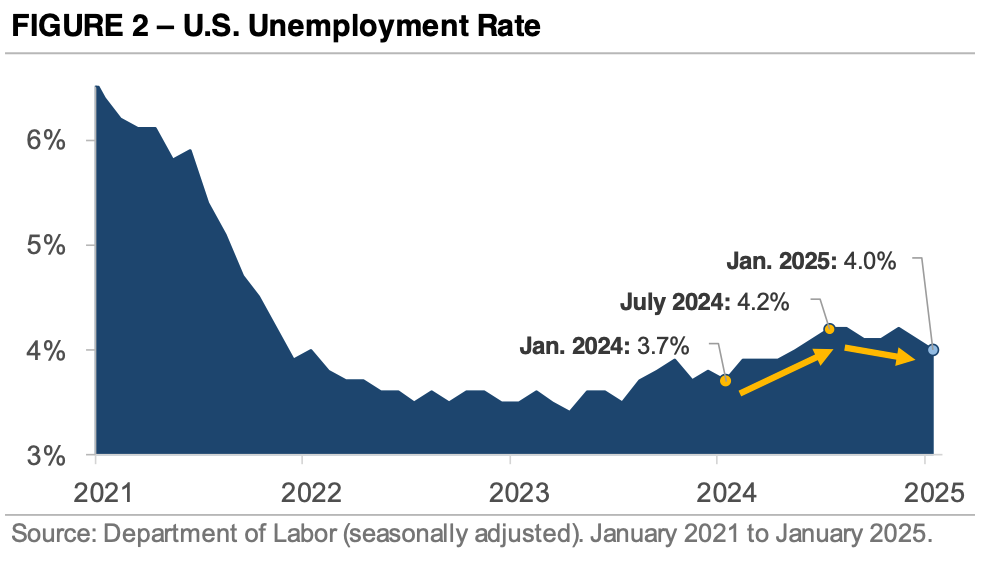

At the same time, the labor market continues to show resilience. Figure 2 highlights the U.S. unemployment rate, which remains strong by historical standards.

In fact, in January, unemployment edged lower to 4.0% which is the lowest its been since May 2024. To be sure, while employers added 143,000 jobs that month, which was a slower pace compared to the post-pandemic hiring boom, it was nevertheless a sign of steady demand for workers.

At the same time, job numbers from November and December were revised higher, revealing that the economy created 100,000 more jobs than initially reported.

And this has been problematic for the Fed given that just a few months ago, policymakers pointed to rising unemployment as a reason to begin cutting rates. However, recent data suggests that the labor market is not weakening as quickly as many had expected.

What Does this Mean for Interest Rates?

So, what does this mean for interest rates?

Well, in 2024, the Fed started cutting rates to shift its focus from controlling inflation to supporting job growth. However, now that inflation progress has stalled and the labor market remains stable, many believe the Fed will pause further rate cuts until it has more clarity.

In fact, at its January 2025 meeting, the central bank chose to keep interest rates steady after three consecutive cuts. At the same time, Fed Chair Jerome Powell reinforced this cautious stance, explaining that there is no immediate need to rush into further adjustments.

What Should You Do About It?

Looking ahead, there are signs that market expectations have shifted.

To be sure, instead of anticipating another rate cut in the early months of the year, many now expect the next adjustment to come in June 2025. However, the real question remains: Will inflation continue to cool, or will the Fed need to rethink its strategy once again?

With the political climate shifting, budget cuts looming, and both households and businesses feeling more cautious, the Fed's decision to pause may not be a sign of confidence but rather a reflection of uncertainty.

Could inflation take another leg down if demand slows further? That remains to be seen. But more importantly, what does all of this mean for your investments?

Right now, it's very well likely that we're in a period of transition. The economy is adjusting, and markets are searching for direction. But if history has taught us anything, it's that trying to predict where markets will go in the next 12 months, or even the next 12 weeks, is rarely a winning strategy.

Indeed, over the past five years, market behavior has looked very different from the decade before.

The Big Takeaway

So, what should you focus on instead?

Well, one thing that hasn't changed is the value of a well-diversified portfolio. While markets shift and economic conditions evolve, diversification remains one of the best ways to manage risk. This approach ensures that no single event, no single policy decision, and no single downturn can completely derail your long-term progress.

Either way, here's the big takeaway: There is still plenty of uncertainty surrounding inflation, interest rates, and the economy. While some indicators point to slower growth ahead, the wisest approach isn't to react to every twist and turn.

Instead, it's to stay disciplined, stay focused, and stay committed to your long-term plan. Now more than ever, doing so will keep you from being caught off guard no matter which way the markets move next.

Changing AI Leadership, Trade War 2.0 and Market Volatility

Monthly Market Summary

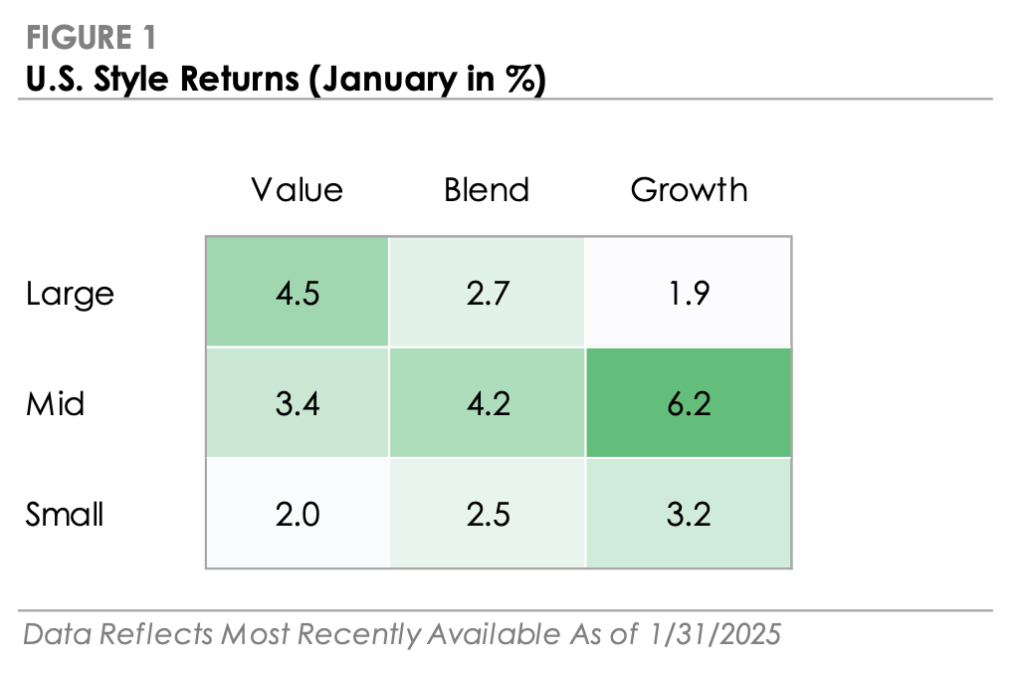

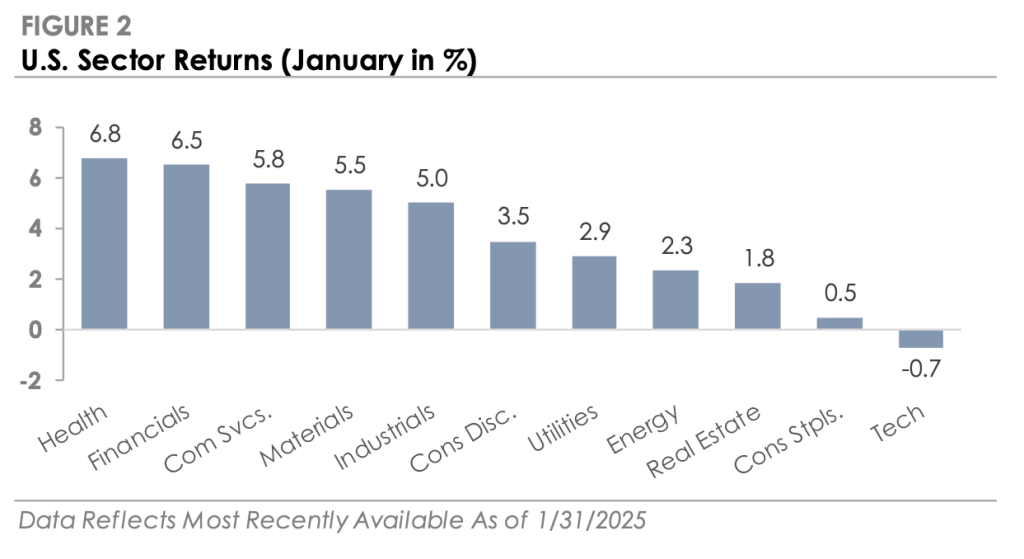

- The S&P 500 Index returned +2.7% in January, marginally outperforming the Russell 2000 Index’s +2.5% return. Seven of the eleven S&P 500 sectors outperformed the index, as AI-related news led to a sell-off in Technology stocks.

- Corporate investment-grade bonds produced a +0.6% total return as Treasury yields edged lower but underperformed corporate high-yield’s +1.4% total return as corporate credit spreads tightened further.

- International stock returns were mixed. The MSCI EAFE developed market stock index returned +4.8% and outperformed the S&P 500 due to strength in Europe, while the MSCI Emerging Market Index returned +2.2%.

Changes in Market Leadership

One month into the new year and markets have continued to rally; however, renewed geopolitical uncertainties could pose challenges to solid market gains. Indeed, after a strong showing in 2024, stocks traded higher to start 2025, but the factors driving the rally took on a different character in the past month than we have seen over the past year. For example, the segment of stocks that powered the recent market gains, Large Cap Value stocks, had lagged over the past year but outperformed Large Cap Growth by more than 2.5% in January.

At the same time, the Dow Jones Industrial Average climbed back toward its all-time high in early December after closing last year on a weaker note. Meanwhile, growth stocks, as measured by the Nasdaq 100 and the Technology sector in general, which led markets higher for most of 2024, underperformed the broader index for the month.

This shift was largely driven by AI-related developments in China, which raised concerns about U.S. dominance in the sector and broader market trends. What this means is that while tech stocks powered last year's gains, other sectors may take the lead in 2025, especially if geopolitical risks remain contained. This kind of shift in leadership is not uncommon following strong market years, as investors look to rebalance portfolios and identify opportunities in areas that were previously overlooked.

Are Tech Stocks Out of Steam?

So then, is tech as a driving force of the current rally down for the count this year? It might be too soon to tell. Indeed, January saw a major shake-up in artificial intelligence (AI), with ripple effects across U.S. markets. That's because Chinese startup DeepSeek introduced an AI model that claims to be able to compete with top U.S. platforms like ChatGPT but at a fraction of the cost. The model was allegedly developed using less advanced and cheaper chips, challenging the assumption that leading AI models require heavy investment in high-performance computing. If this approach catches on, it could significantly alter the industry and affect U.S. leadership in AI.

That's why markets reacted quickly, and the impact was significant, leading to a selloff in U.S. tech stocks, especially those that had seen strong gains on AI growth expectations. That's because the prospect of lower-cost AI development raised concerns about the demand for high-end chips. So then companies like Nvidia, a key supplier of advanced AI hardware, saw its market capitalization fall by nearly $600 billion, which was one of the most significant single-day losses for a U.S. company.

At the same time, the selling pressure extended to Microsoft, Alphabet, and Meta, as investors reassessed what appears to be rich valuations in the AI space. And this market response likely reflects broader worries that progress in the AI space may not be as capital-intensive in the future as once believed, which could challenge the dominance of companies that have benefited from high investment requirements in AI-related infrastructure.

Even so, what's notable here is that although the initial market decline was concentrated in a handful of companies, their heavy weighting in the S&P 500 dragged the broader index lower. Nevertheless, investor sentiment is rarely one-sided, and after the initial selloff, markets stabilized coming into February as some investors viewed the pullback as a buying opportunity, particularly in areas of the market that may benefit from AI-driven cost efficiencies. Still, given AI's significant role in market performance, markets will be keen to keep a close eye on developments in the sector while rebalancing to other market opportunities.

Trade War 2.0 Developments

Changes in trade policy also added another layer of market uncertainty after a solid start to the year. That's because, on February 1, 2025, President Trump announced new tariffs as part of what some are dubbing "Trade War 2.0": 25% on imports from Mexico and Canada (with a 10% levy on Canadian energy products) and 10% on Chinese imports. The move is positioned as an effort to address trade imbalances and immigration concerns and prompted immediate responses from major trading partners. Even so, Canada and Mexico secured temporary delays while committing additional resources to combat organized crime and drug trafficking.

But, China responded swiftly, imposed tariffs on U.S. coal, liquefied natural gas, crude oil, and agricultural machinery while launching an antitrust probe into Alphabet. The reaction in financial markets was immediate, with major indices dropping over 1% and the U.S. dollar reaching a 20-year high against the Canadian dollar. Markets have since recovered modestly since the initial selloff, but the surge in the dollar could have additional implications for U.S. multinational companies, as a stronger currency can weigh on exports by making American goods and services more expensive overseas.

These developments reinforce the risks of an escalating trade war, which could lead to higher inflation, supply chain disruptions, and slower economic growth in affected regions. And while markets have endured trade-related tensions in the past, the unpredictability of policy responses are likely to keep investors on edge, especially as incoming data suggests that economic growth is moderating.

Looking Ahead

So, what does this mean for your portfolio? Well, over the next few months, investors will be watching trade policy developments, AI innovation, and Federal Reserve decisions for signals on market direction. While the broadening of market leadership suggests a more balanced rally, geopolitical and macroeconomic risks remain a central headwind to any potential market rally.

Here's the big takeaway: This complicated environment makes it especially important for investors to avoid reacting too strongly to short-term headlines.

Indeed, it's essential to remember that markets don't move in a straight line, and with AI disruptions and trade tensions shaping 2025, staying committed to your long-term plan will be key. Because the question isn't just how these forces play out, it's how you position yourself in response.

Therefore, taking a proactive approach to portfolio positioning, especially rebalancing your investments rather than being swayed by short-term volatility, will be critical to navigating market volatility.

Either way, how political and economic events unfold will shape the market's trajectory. But for now, the best strategy is to focus on your disciplined investment strategy, ignore the noise, and ensure your financial plan is positioned to give you clarity, confidence, and peace of mind as you move through another period of economic and market uncertainty.

What do Stretched Market Valuations in 2025 Mean for Portfolio Returns?

The S&P 500’s Unprecedented Rally

Since the start of 2023, the S&P 500 has surged more than 50%, building on a remarkable rally of over 150% from its March 2020 pandemic low. These gains have delivered record highs and lifted portfolios, but they’ve also pushed valuations into historically stretched territory. The

S&P 500 now trades at over 21 times its projected earnings for the next 12 months which is a level reminiscent of the late-1990s tech bubble or the post-COVID recovery, when interest rates hovered near zero.

What does this mean for investors? Should you celebrate the recent rally or pause to consider what’s next? While today’s valuations might be cause for concern, recent market experience raises another important question: how can you stay disciplined in a volatile environment?

The fact is that exiting the market during uncertain times or taking on unnecessary risk can lead to costly mistakes. Instead, a balanced, long-term investment strategy remains essential for navigating today’s unique challenges while staying aligned with your financial goals.

Valuations: A Historical Perspective

Nevertheless, a key question that that we’re trying to answer with today’ analysis is, “how often do we see markets trade at such elevated levels, and what does it mean for portfolios?”

Upon inspection, there is no doubt that the current valuation of the S&P 500 is rare, with broad market indices trading at over 21 times forward earnings which is a figure not commonly seen outside exceptional periods.

And why does this matter? Because while valuations may not dictate short-term performance, they play a critical role in shaping long-term returns. But put more simply, understanding how valuations work can help you as an investor by setting realistic expectations for the years ahead.

Short-Term vs. Long-Term: The Role of Starting Valuations

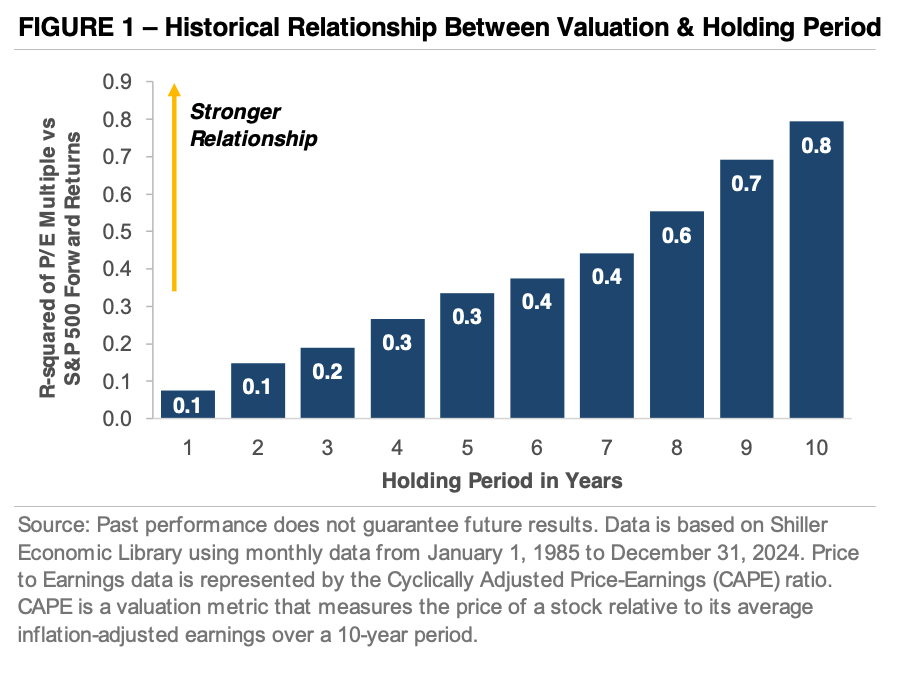

Indeed, figure 1 helps illustrate why starting valuations matter. It tracks the relationship between the S&P 500’s starting valuation and future returns over various holding periods. The horizontal axis shows the length of the holding period in years, while the vertical axis highlights the R-squared (R²) measure, which quantifies how much one variable explains another.

But what does that mean in practical terms? Well, for example, an R² of 0.40 means 40% of changes in one variable can be linked to the other, with the remaining 60% due to randomness or other factors. This means that in the short term, valuations don’t explain much because there’s a low R² for holding periods of just a few years. But over longer time frames, the relationship strengthens. Because by the 10-year mark, starting valuations explain roughly 80% of return variability, underscoring their importance for patient, long-term investors.

What the Numbers Tell Us: Figures That Matter

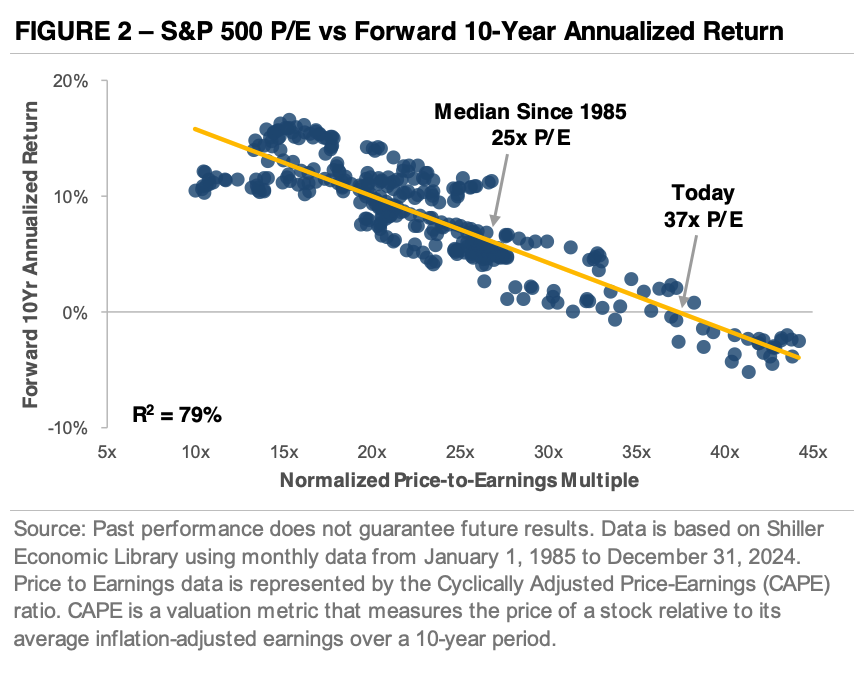

Now, if we zoom out and look at valuations and their impact on longer-term returns we see a different picture. Figure 2 shows how the S&P 500’s starting valuation impacts its next 10 years of annualized returns. This is represented by the normalized price-to-earnings (P/E) ratio, which averages inflation-adjusted earnings over the past decade to smooth out short-term noise.

So then, do higher starting valuations always mean lower returns? Historically, yes. The chart slopes downward, revealing that as valuations increase, forward returns tend to decrease. With today’s normalized P/E ratio sitting at 37, which is an extreme level by historical standards, the S&P 500 could deliver low single-digit annualized returns over the next decade.

Balancing Risk in a Stretched Market

Should you be worried about these numbers? The insights are sobering, but they must be placed in context. While history is an invaluable guide, it’s not a crystal ball. Indeed, figure 1 makes it clear that valuations alone don’t predict short-term results, and markets can stay expensive longer than expected. However, when setting expectations for the years ahead today’s valuations be part of the conversation.

Staying the Course: A Strategy for Long-Term Success

To be sure, current market conditions are a clear signal that it’s prudent to avoid taking on unnecessary risk in today’s market environment. Yet, if the past five years have taught us anything, it’s also the importance of steadiness and staying steadfast to your plan.

Because exiting the market during uncertain times or overreacting to short-term fluctuations can jeopardize your long-term financial planning goals. That’s why now, more than ever, it’s essential to strike the right balance and acknowledge today’s risks while staying committed to a disciplined, long-term investment strategy that aligns with your long-term financial plan.

2025 Economic & Market Outlook

Key Updates on the Economy & Markets

There was no shortage of market-moving events in Q4. The stock market opened the quarter with a slow start in October, but the outcome of the presidential election triggered a broad rally in November.

The rally faded as the year ended, although the S&P 500 trades only a few percentage points below its all-time high. The credit market was equally active in Q4, with the Federal Reserve cutting rates by another -0.50%. However, the major development was the changing 2025 outlook.

The Fed and the market both now expect fewer rate cuts in 2025 compared to the end of Q3, which resulted in a sharp rise in Treasury yields in Q4. This letter recaps the fourth quarter, looks back on the 2024 stock market rally, provides an update on the economy and the Fed’s rate-cutting cycle, and looks ahead to 2025.

Looking Back on the 2024 Stock Market Rally

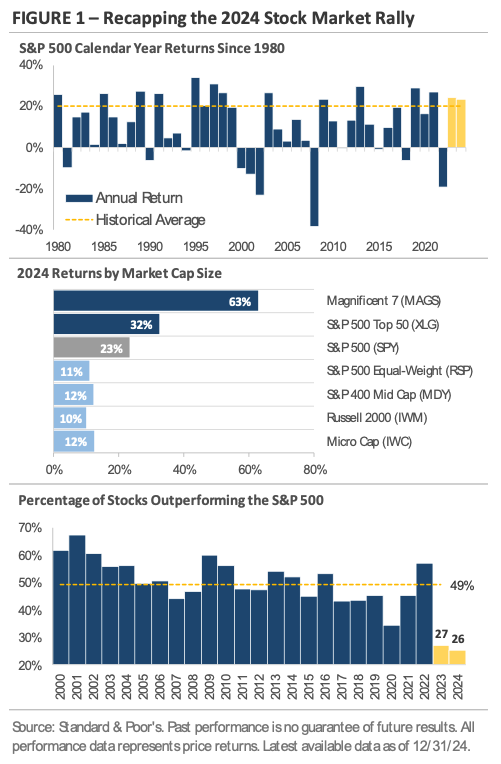

The past two years have been remarkable for investors, with the S&P 500 delivering strong returns in back-to-back years. The three charts in Figure 1 take a closer look at the stock market’s rally in 2024, a year in which the S&P 500 set more than 55 new all-time highs.

The top chart, which graphs the S&P 500’s return for each calendar year since 1980, shows the index posted gains of over +20% in 2023 and 2024. It marked the first time since the 4-year stretch from 1995 to 1998, and like the late 1990s, large-cap technology stocks played a major role in the S&P 500’s gains.

The middle chart shows the 2024 price returns of seven ETFs, each reflecting exposure to companies of different market cap sizes. The chart reveals a significant gap between the returns of large-cap and small-cap stocks in 2024. The top bar tracks the Magnificent 7, a group that includes Microsoft, Apple, Alphabet, Meta, Amazon, Nvidia, and Tesla. These seven companies, which now account for more than 33% of the S&P 500, returned over +60%.

When the group expands from the Magnificent 7 to the 50 largest S&P 500 stocks, the return falls to +32%, still impressive but around half of the Magnificent 7’s return. Broadening the group further to include all S&P 500 companies reduces the index return to approximately +23%, and weighting companies equally rather than by market capitalization lowers the return to +11%.

The key takeaway is that the largest companies contributed a significant portion of the S&P 500’s return in 2024. Smaller companies delivered solid returns around +10%, but they underperformed on a relative basis. An index of mid-cap stocks returned +12%, while small-cap and micro-cap stocks returned +10% and +12%, respectively.

The concentrated stock market rally, which was driven by the outperformance of the largest companies, led to an unusual outcome. The bottom chart tracks the percentage of S&P 500 companies that outperformed the index during each calendar year. For the second consecutive year, fewer than 30% of S&P 500 companies beat the index in 2024. This is significantly below the average of 49% since 2000 and highlights the dominance of the largest companies in 2024.

Data Highlights the U.S. Economy’s Resiliency

The U.S. economy has consistently defied expectations of a slowdown since the Fed started raising interest rates in March 2022. Economists and market participants initially expected growth to slow as the Fed raised interest rates. However, it has now been nearly three years since the Fed’s first rate hike, and the economy continues to grow at an above-trend rate. While higher rates have slowed housing demand and weighed on business investment, the U.S. economy has managed to defy expectations with solid GDP growth.

The top chart in Figure 2 shows the U.S. economy grew at a +3.1% annualized pace in 3Q24, marking the third quarter in the past four with growth above +3%.

The bottom two charts show key drivers of economic growth since early 2022. The middle chart tracks the contribution of personal consumption expenditures (i.e., consumer spending) to U.S. GDP growth. Despite high interest rates, consumer spending has remained a steady driver of growth in recent quarters. Multiple factors have increased household net worth and bolstered consumers’ financial strength, including record-high stock prices, rising home values, and solid wage growth.

Additionally, many borrowers locked in low interest rates during the pandemic, which has made the U.S. economy less sensitive to rising interest rates this cycle.

The bottom chart shows the surge in manufacturing-related construction in recent years. For a long time, manufacturing construction was relatively modest, as most activity was outsourced to China, Mexico, and elsewhere. However, that changed in late 2021, around the time Congress passed trillions in new spending on infrastructure, green energy, and subsidies to incentivize U.S. manufacturing.

These spending bills have been extremely supportive of the U.S. economy and created a boom in the manufacturing of semiconductors, electric vehicles, batteries, and solar panels. The result is a surge in manufacturing-related construction, the largest on record, as companies build new warehouses, industrial facilities, and semiconductor plants. The artificial intelligence industry’s emergence has provided another catalyst, as companies like Microsoft, Amazon, and Meta spend billions on data centers, information processing equipment like semiconductors, and energy production to meet growing power demand.

Economic growth is forecast to slow but remain solid next year, driven by the Trump administration’s pro-growth policies. The new administration’s policy agenda focuses on extending the 2017 tax cuts, reducing regulations across industries, and boosting domestic manufacturing through targeted incentives. These measures have the potential to stimulate capital expenditures, expand manufacturing capacity, and attract foreign investment to the U.S.

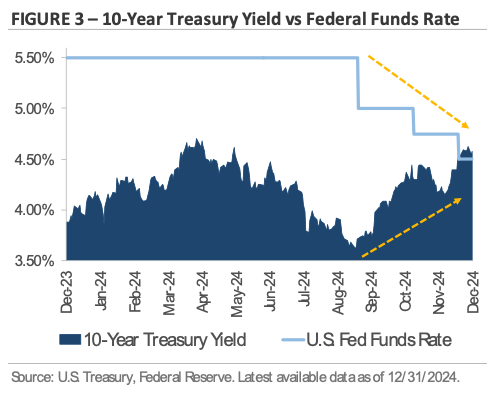

An Update on the Fed’s Interest Rate-Cutting Cycle

The Fed continued its rate-cutting cycle in Q4, lowering interest rates by -0.25% at both the November and December meetings for a total of -0.50%. The two -0.25% rate cuts were well telegraphed by the Fed and widely expected, but the big development in Q4 was the changing outlook for 2025.

Despite the two rate cuts, Fed Chair Jerome Powell and other Fed presidents indicated they are not in a hurry to cut rates further. The change in tone follows the U.S. economy’s recent strength, which has caused the Fed to re-examine the need for additional rate cuts.

Recent economic strength has also led the market to re-evaluate its rate cut forecast. This dynamic can be seen in the bond market, where longer-maturity Treasury yields have risen sharply since the first rate cut in September.

Figure 3 graphs the 10-year Treasury yield against the federal funds rate, which is the interest rate the Fed adjusts to set monetary policy. Since the first rate cut in September, the federal funds rate has decreased by -1.00%. While the Fed controls shorter-maturity interest rates, the market has more control over longer-maturity interest rates. Over the same period, the 10-year Treasury yield has had the opposite reaction: rising by nearly +1.00%.

What caused Treasury yields to rise as the Fed cut interest rates? Two key data points contributed to the Fed’s decision to start cutting rates in September: falling inflation and rising unemployment. Inflation declined from 3.3% in July 2023 to 2.6% in August 2024, while unemployment rose from 3.5% to a high of 4.3%. The two trends caused the Fed to shift its focus from lowering inflation to supporting the labor market.

However, since the Fed started cutting, the trends have reversed. Inflation progress has stalled since September, and unemployment has declined to 4.2%. Heading into 2025, the Fed and the market have similar rate cut expectations: approximately -0.50% in cuts for the entire year. The question is whether they are placing too much emphasis on recent trends and underestimating the need for rate cuts. As both the Fed and the market saw in 2024, forecasting Fed policy is difficult, especially this cycle.

Equity Market Recap – Stocks End the Year Higher

The stock market ended Q4 higher, but the path included periods of volatility. In October, the S&P 500 ended its five-month winning streak, with most of the equity market finishing slightly lower. The sluggishness occurred as Treasury yields rose after the Fed’s first rate cut in September, suggesting the sharp rise in yields may have played a role in October’s market action. However, stocks rebounded in subsequent months.

In November, the quick and decisive election outcome became a tailwind for stocks. Investor enthusiasm fueled the post-election rally, with stocks trading higher in anticipation of tax cuts, deregulation, and U.S.-focused trade policies aimed at benefiting U.S. companies. Small caps led the way during the broad market rally, with the Russell 2000 rising +11% in November to set a record high.

Bank stocks were another popular post-election trade as investors priced in expectations for financial deregulation and strong economic growth. Industrial stocks saw broad-based strength in anticipation of the Trump administration’s pro-growth policies and protectionist policies, which could spark an industrial renaissance in the U.S. By the end of November, the S&P 500’s year-to-date return surpassed +26%, putting the index on track for consecutive gains of more than +20%.

In December, the market’s excitement cooled, with the S&P 500 trading sideways and ending the month lower. Beneath the surface, a familiar trend from earlier in the year impacted returns, with smaller companies underperforming larger ones by a wide margin.

The Russell 2000 Index was hit hardest, falling -8.4% and giving back most of its post-election gains. Value stocks also traded lower in December, with the Russell 1000 Value Index declining by -6.8%. In contrast, the Magnificent 7 stocks discussed earlier gained more than +5%.

Shifting focus to global markets, international stocks underperformed U.S. stocks in Q4. The MSCI Emerging Market Index returned -7.2%, while the MSCI EAFE Index of developed market stocks returned -8.3%.

Both major international equity indices underperformed the S&P 500 by nearly -10% due to currency headwinds (i.e., a stronger U.S. dollar) and the outperformance of U.S. mega-caps. Looking ahead to 2025 for international markets, the potential for tariffs under the Trump administration is creating significant uncertainty across several global regions.

Credit Market Recap – Bonds Trade Lower as Interest Rates Rise Throughout the Quarter

The sharp rise in Treasury yields weighed on bond returns in Q4. The biggest differentiator within the bond market was duration, or the sensitivity of a bond’s price to interest rate movements.

High-yield corporate bonds produced a total return of -0.1% due to their lower sensitivity to rising interest rates and higher absolute yields. In contrast, investment-grade bonds returned -4% as rising yields had a bigger impact on their longer maturities. Excluding interest received and only looking at price returns, an index of investment-grade corporate bonds posted its biggest quarterly loss since Q3 2022.

Full-year credit returns highlight the key themes that shaped the bond market throughout 2024. Higher-quality bonds like U.S. Treasuries, corporate investment-grade, and mortgage-backed securities underperformed as the market debated and ultimately lowered its rate-cut expectations. In contrast, lower-quality bonds outperformed as economic growth and corporate fundamentals remained solid.

Corporate credit spreads, which measure the difference in yield between two bonds with a similar maturity but different credit quality, steadily tightened throughout the year. This provided a boost to lower-quality bonds in 2024 but has left credit spreads near their lowest levels in decades. For context, the U.S. high-yield corporate credit spread is near its lowest level since 2007, which means investors are receiving less yield in return for taking credit risk.

2025 Outlook – Key Themes to Watch

The S&P 500’s steady climb in 2024 reflects the market’s growing confidence. Investors are optimistic about the artificial intelligence industry’s growth potential. The U.S. economy outperformed expectations, growing at an above-trend rate in three of the past four quarters despite high interest rates.

The stock market rally intensified after the election in November, as investors focused on the incoming administration’s policy agenda. Expectations for tax cuts, deregulation, and energy production are fueling hopes for stronger economic growth.

The bond market echoes the equity market’s confidence, and corporate high-yield credit spreads are near their lowest levels in over 15 years.

However, the equity market rally has made broad market indices like the S&P 500 more concentrated and more expensive. The question on many minds is whether the momentum can continue in 2025.

The S&P 500 currently trades at nearly 22x times its next 12-month earnings estimate, a level not seen outside of periods like the late-1990s tech boom and the recent post-COVID recovery, when interest rates were near zero.

Investors have shown a willingness to pay higher multiples, but with valuations now at extremes, earnings growth will likely play an important role in determining the stock market’s path in 2025.

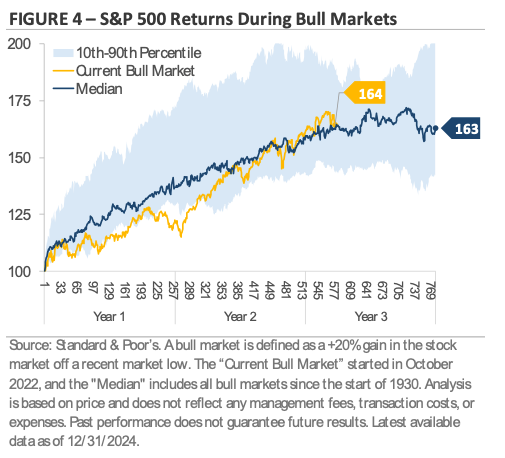

Figure 4 tracks the current bull market, which started in October 2022 and is now in its third year.

The current bull market has performed in line with historical norms, but the chart shows that returns often moderate as bull markets mature. This suggests that the market’s focus could shift to fundamentals and earnings as the next catalyst to push markets higher. 2025 is shaping up to be a year where companies will need to deliver on investors’ expectations to justify their high valuations.

The Bull Market's Unstoppable Momentum in 2024

The past two years have been remarkable for investors, with the S&P 500 posting back-to-back gains of over +20%.

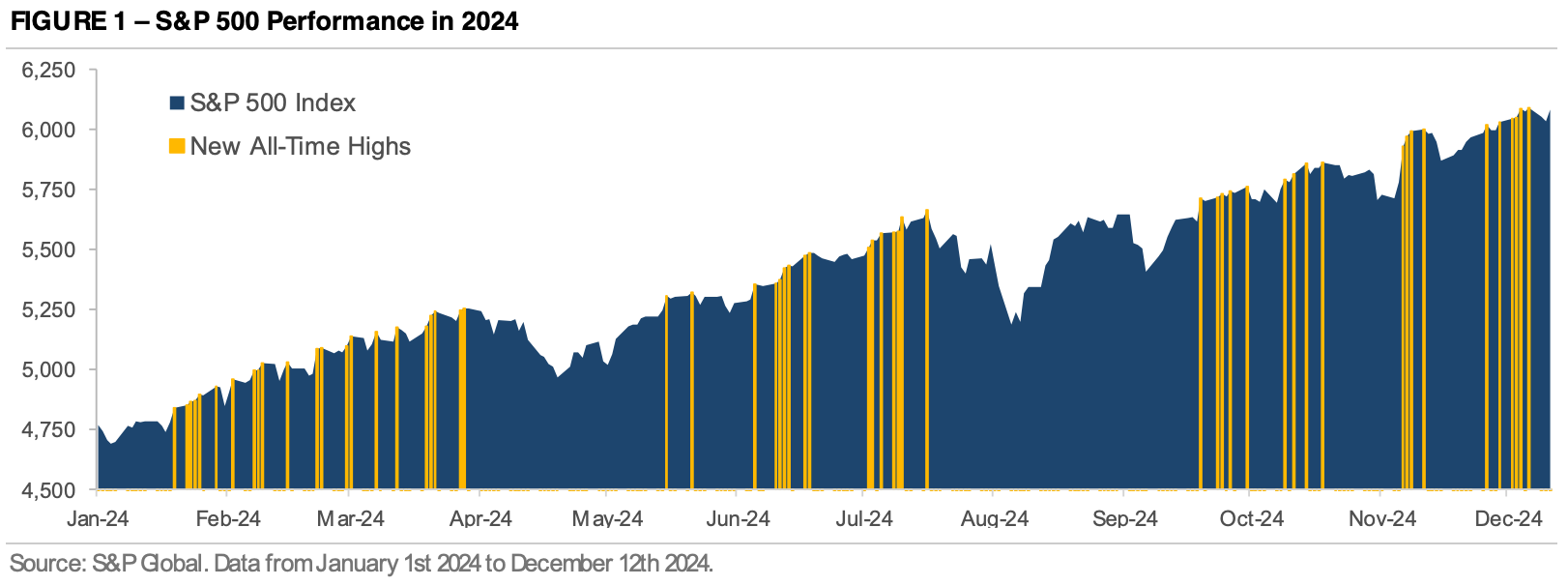

The chart below takes a closer look at 2024’s price movement and uses yellow shading to mark the days when it closed at an all-time high. At the start of this year, the S&P 500’s previous all-time high was set in January 2022.

It took over two years to reclaim the prior high, but once the index broke through in late January 2024, it set more than 50 new highs this year.

The list of all-time highs illustrates the current bull market’s strength and persistence and could grow by year-end.

Large-cap technology stocks, such as Nvidia, Meta, Amazon, and Tesla, have posted strong returns and played a major role in driving the index’s gains. The S&P 500’s record-setting performance is part of a broader cross-asset rally that has lifted stocks, bonds, and commodities.

The stock market’s steady climb this year speaks to investors’ growing confidence. Investors are optimistic about the artificial intelligence industry’s growth potential. The economy has outperformed expectations driven by robust consumer spending, growing at an above-trend rate in Q2 and Q3 despite high interest rates. After the November election, the stock market rally intensified as investors focused on the incoming administration’s policy agenda.

Expectations for tax cuts, deregulation, and energy production are fueling hopes for stronger economic growth. The bond market echoes the confidence in equity markets, and corporate high-yield credit spreads are at levels not seen since May 2007.

The question on many minds is whether the momentum can continue in 2025. The S&P 500 currently trades at over 22x its next 12-month earnings estimate, a level not seen outside of periods like the late-1990s tech boom and the post-COVID recovery. Investors have shown a willingness to pay higher multiples, but with valuations at extremes, earnings could play an important role in determining the stock market’s next move.

The current bull market, which started in October 2022, is now in its third year, and it’s common to see investors shift focus to fundamentals as the bull market matures.

2025 is shaping up to be a year where companies will need to deliver on markets’ expectations to justify their high prices and investors likely will need to remain mindful about taking on more risk than necessary at this point in the market cycle.

What to Make of Weaker First Quarter Growth?

Last week, incoming data showed that the U.S. economy shrank in the first quarter of 2025, the first time in several years we've seen this happen.

Now, it's essential to note that one quarter of decline doesn't mean a recession is inevitable. But with today's unpredictable economic policies, it's fair to wonder if this could be the beginning of a short-term slowdown.

Why Predicting the Economy Is Harder Than Ever

Indeed, trying to figure out where the U.S. economy is going has never been easy. But in the years since the pandemic, it's become even more difficult.

That's because many of the tools economists used to rely on don't seem to work as well anymore. For example, when interest rates rise, that usually signals a slowdown or even a recession in the making.

But in the past five years, even with warning signs in place, Americans kept spending. And since consumer spending makes up over two-thirds of the U.S. economy, this has helped keep things growing.

So, what's changed?

Well, what's likely different this time around is the policy environment. We're dealing with a new set of economic rules and decisions that make predictions more complicated.

And these changing policies create more uncertainty, and that can weigh on both consumers and businesses. Because of this, the chances of a recession, or at least slower growth, may be rising as these policy effects ripple through the economy.

What Caused the First-Quarter Economic Decline?

So then, to better understand what's behind the recent slowdown, we need to look at the key parts of economic growth.

And as you'll likely recall from your economics courses in college, gross domestic product (GDP) is made of: 1) government spending, 2) business investment, 3) household spending, and 4) net exports (exports minus imports).

So, what did the data show us?

Well, in the first quarter, two things stood out as the leading causes of weaker growth: a drop in government spending and a sharp increase in imports.

Now, the rise in imports likely happened because of the Trade War, as businesses and consumers were trying to buy goods before prices increased.

To be sure, as trade tensions have returned, and tariffs on some items are now as high as 150%, that's led many to act early, stocking up before things get worse.

Now, the drop in government spending is more complicated.

That's because overall federal spending is still higher than in past years, but when adjusted for inflation and measured quarter by quarter, it appeared to fall. That technical dip was enough to drag down total economic output.

What the Numbers Don't Tell Us

While hard data like GDP shows us what already happened, it's also essential to pay attention to soft data, like how people and businesses are feeling about the future. This kind of information can help predict what's coming next.

And lately, people haven't been feeling very confident. For example, a recent University of Michigan survey showed consumer confidence hit its lowest point in two years. A lot of that concern comes from worries about inflation and what future policies might bring.

We're also seeing changes in the job market. That's because data are showing there are fewer job openings, and layoffs are becoming more common. These are signs that employers are starting to pull back, something that often happens toward the end of an economic cycle.

And adding insult to injury, even shipping activity has slowed. At major ports on the West Coast, freight volumes have dropped, showing that businesses may be holding off on orders as they wait to see how trade issues unfold. All of this points to a more cautious mood taking hold across the economy.

The New Trade War: What's Changed?

Another factor adding pressure to the economic outlook is the return of Trump's Trade Wars.

But this time, businesses are handling the tariffs in a much different way than they had during Trump's first administration.

That's because, during the first trade war in 2018, many businesses chose to absorb tariff costs to keep their customers. But now, more of them are passing those costs directly to shoppers.

That makes everything more expensive, and if prices keep going up, people may start spending less. If trade problems continue, and if businesses and consumers respond by cutting back, it could create a chain reaction that leads to even slower growth.

So, Are We Heading for a Recession?

Nevertheless, it's too soon to say for sure whether we're heading for recession. Frankly, one quarter of economic decline is not enough to call for a slowdown, particularly when the factors could be temporary.

Indeed, even experienced economists often struggle to predict when a recession will hit.

But one thing is clear: today's policy environment isn't helping. And ongoing uncertainty about trade, inflation, and regulation has made people and companies more cautious about spending and investing.

If that uncertainty doesn't clear up soon, the risk of economic weakness and higher prices will likely grow.

In times like these, it's easy to get distracted by scary headlines or market swings. But this is precisely why having a strong financial plan matters.

When things feel shaky, your plan should be your guide.

Now is not the time to make big changes out of fear. Instead, lean on the thought and strategy that went into your long-term plan.

That kind of discipline is what helps you stay on track, especially when the road ahead feels uncertain.