Weekly Market Recap: New All-Time Highs as Markets Look Past a Failed Ceasefire

Stocks climbed to new records this week, shrugging off a failed ceasefire deal and a U.S. naval blockade of Iranian ports.

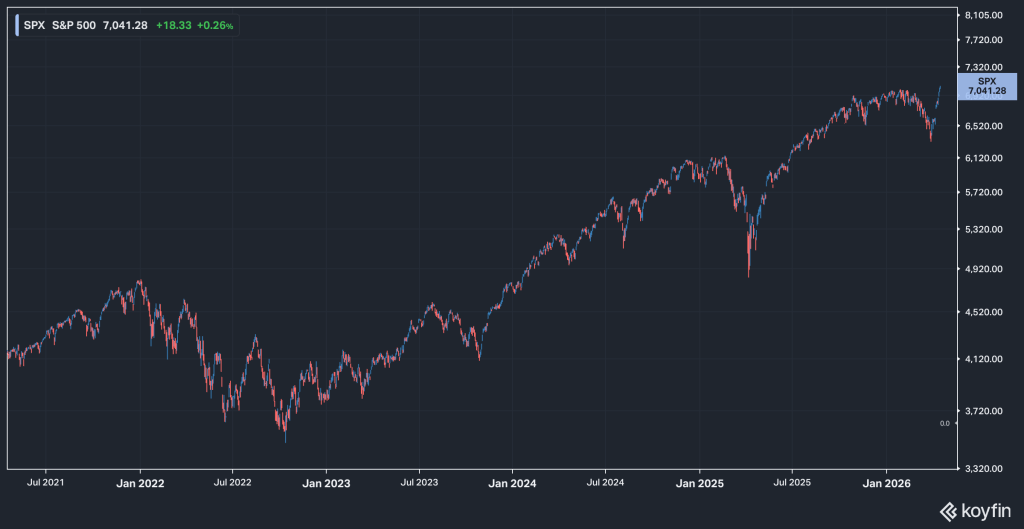

The S&P 500 gained nearly +3%, completing an 11-session V-shaped recovery from the late-March bottom, while the Nasdaq gained nearly +5% to set its own record. Smaller companies participated in the advance but lagged, and defensive sectors along with energy, industrials, and materials declined.

Bonds finished roughly flat, oil ended the week lower despite an early surge, and volatility measures continued to ease as geopolitical risk premiums faded.

Key Takeaways

The S&P 500 Set a New All-Time High

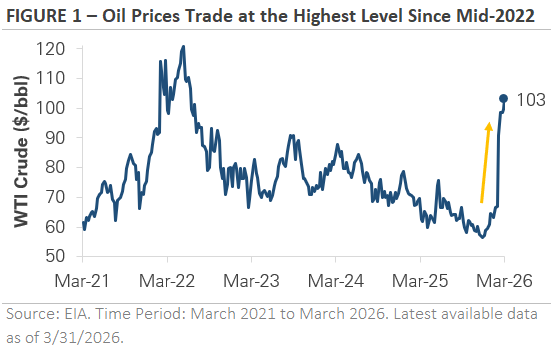

The index traded above 7,000 for the first time since late January, completing a full recovery from the nearly -10% late-March drawdown. Monday was the week's test, with oil briefly surging above $100 on news of the U.S. Navy's blockade of Iranian ports before markets recovered after confirmation that non-Iranian shipping would be unaffected.

The past six weeks were a reminder that trying to time geopolitical events carries a real cost for investors who moved to the sidelines.

Market Risk Premiums Continue to Fade

The VIX, which spiked above 30 at the height of the conflict in late March, has since fallen below 20 and is approaching pre-conflict levels. Credit spreads have tightened steadily, and equity volatility, credit conditions, and interest rate volatility are all improving in tandem.

With the Strait of Hormuz still effectively closed and no official ceasefire in place, these risk metrics will remain closely watched.

Growth and Technology Stocks Have Reasserted Their Leadership

After spending much of the first quarter lagging behind value, smaller companies, and international markets, growth and technology stocks have outperformed value by more than +11% since the late-March low. As a result, the year-to-date performance gap between growth and value has nearly closed.

This year has already cycled through two distinct market environments, underscoring the value of maintaining diversified exposure.

Manufacturing Contracted in March, But April Data Signals Recovery

Industrial production pulled back in March as energy costs surged and supply chain disruptions weighed on activity. More recent data offers a more encouraging picture, with the April Philadelphia Fed Manufacturing Index coming in above expectations as tensions eased and energy prices fell.

The March weakness appears tied to conflict-related disruption rather than a broader deterioration in economic conditions.

Bank Earnings Provided an Encouraging Start to Earnings Season

Major Wall Street banks reported strong first-quarter results, driven by elevated market volatility and increased capital markets activity, while consumer credit quality remained healthy.

Several banks did flag the increasingly complex backdrop as a development worth monitoring going forward.

As always, feel free to reach out with any questions or concerns as they come up.

Weekly Market Recap: Ceasefire, Oil Reversal, and the Rally Markets Were Waiting For

Stocks traded higher for a second consecutive week as de-escalation triggered the strongest single day rally in a year. The S&P 500 gained +3.7%, with the Nasdaq and the Russell 2000 both returning +4.3%.

Most of the rally occurred on Wednesday after the announcement of a two-week ceasefire contingent on Iran reopening the Strait of Hormuz. Oil plunged -11%, the VIX dropped below 20, and international stocks rose as energy-importing nations benefited from the oil reversal. Industrials were the top-performing sector, gaining +5%, with broad strength across most sectors excluding energy.

Treasury yields fell modestly, and corporate bonds outperformed as credit spreads tightened to late January levels. However, the ceasefire was already being tested late in the week, with the market closely monitoring this weekend’s talks.

Key Takeaways

The U.S. and Iran agreed to a two-week ceasefire, triggering a relief rally.

Late Tuesday, the White House announced an agreement contingent on Iran reopening the Strait of Hormuz, less than two hours before a stated deadline to launch strikes on Iranian infrastructure.

Markets reacted decisively Wednesday: the S&P 500 surged +2.5%, its best single-day gain in a year, the Dow jumped +2.9%, the Russell 2000 gained +3.0%, and international equities rallied +3.5%. Unlike prior headlines, this was an actual agreement confirmed by both sides, with talks scheduled for this weekend.

Implication: The ceasefire is meaningful, but its durability was tested within hours. Israel launched strikes across Lebanon, Iran accused the U.S. of violating three conditions, and the Strait remained effectively closed Thursday morning. This weekend's talks will determine whether the agreement marks a turning point.

Oil plunged -16% on Wednesday, its largest single-day decline since April 2020, as the market priced in a Hormuz reopening.

WTI fell from $112 to around $94, erasing weeks of the war-driven rally that had pushed oil up over +65% YTD. The decline triggered immediate secondary effects: airline stocks surged, and the odds of a rate cut increased as inflation expectations eased.

However, the physical reopening remains uncertain. As of Thursday morning, the Strait was still effectively closed, and oil was moving back toward $100.

Implication: Oil is the transmission mechanism through which the conflict reaches inflation, the Fed, consumers, and corporate profits. Wednesday's decline showed how quickly the geopolitical premium can unwind, with the market watching for actual follow-through.

Credit spreads tightened and volatility declined, confirming the risk-appetite shift across asset classes.

High-yield spreads compressed during Wednesday's ceasefire rally and are now the lowest since late January after tightening nearly -0.50% over the past two weeks. Credit spread tightening is an indication the market is starting to price in less stress.

The VIX fell to 21, its first close below 22 since late February, after touching 28 intraday Tuesday before the ceasefire was announced.

Implication: Credit and volatility are the market's most reliable stress indicators, and both confirmed the equity rally as broad-based rather than speculative.

Treasury yields barely moved despite the ceasefire rally.

The 10-year yield fell just -0.03% to 4.28%, a muted response given the magnitude of the oil crash and equity rally. The bond market's reaction reflects the Fed's policy forecast. Seven of nineteen Fed members forecast zero cuts in 2026, and the Fed's March minutes, released this week, reaffirmed its patient approach.

Implication: The bond market's restraint suggests it is waiting for confirmation that the ceasefire will meaningfully improve the inflation and growth outlook.

Next week unofficially kicks off Q1 earnings season, with the big Wall Street banks reporting.

The focus will extend beyond the usual revenue and earnings beats to management commentary on the conflict's impacts, from energy costs and supply chain disruptions to consumer demand and forward estimates.

Implication: Earnings calls will provide the first corporate read on how the energy shock is flowing through margins, pricing, and demand. Forward guidance and tone may matter more than the headline numbers this quarter.

1Q26 Market & Economic Recap & 2Q26 Outlook

Key Updates on the Economy & Markets

The first quarter of 2026 was one of those periods that reminded investors why markets don't move in a straight line.

Stocks started the year on solid footing with January modestly positive, February quiet, and then March arriving with a jolt. The escalation of geopolitical tensions in the Middle East, including the closure of the Strait of Hormuz, sent oil prices surging and rattled markets in ways that few anticipated heading into the year.

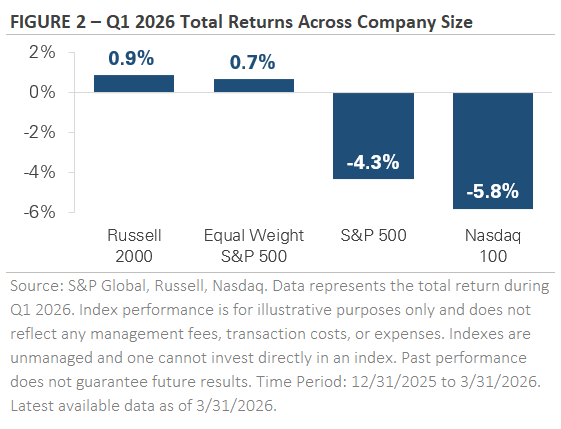

By the time the quarter closed, the S&P 500 was down -4.3%, with the bulk of that decline concentrated in a single month. And if you looked only at that headline number, you might walk away with a grim picture.

But the quarter was more nuanced than the index suggests, and I think it's worth taking a step back to understand what actually happened and what it means for your portfolio going forward.

Higher Oil Prices Changed the Rate Cut Conversation

Indeed, to understand why March felt so disruptive, you have to start with oil.

Crude prices had already been moving higher before tensions escalated with supply concerns tied to Venezuelan output pushing prices up nearly 13% in January, and climbing another 4% in February as geopolitical risks continued to build.

Then March arrived.

The conflict between the U.S. and Iran intensified, and the closure of the Strait of Hormuz, a waterway that carries roughly 20% of the world's oil, sent crude prices surging nearly 50% in a single month. For the full quarter, oil prices rose more than 70%, reaching levels not seen since mid-2022.

And why does that matter for your portfolio?

Because oil prices don't exist in a vacuum. Higher energy costs flow through to what consumers and businesses pay for goods and services. And as a matter of fact, you've likely already noticed it at the pump, as gasoline prices have risen nearly a dollar per gallon since late February.

And this is happening at a moment when inflation was already showing signs of firming before the conflict began. The Federal Reserve's preferred inflation measure, Core PCE, remains near 3%, and producer prices have been trending higher.

So then, coming into 2026, the market expected the Federal Reserve to cut interest rates two to three times by year end.

That expectation quietly eroded as the quarter progressed.

And by the time March ended, those rate cuts had been priced out entirely, and there was even early discussion about whether a rate hike might come back into the conversation.

The situation is still evolving.

The Strait of Hormuz remains closed as of quarter-end, negotiations are ongoing, and oil is trading near $100 per barrel, a signal that the market expects the disruption to persist for some time.

The April and May inflation reports will be the first data to fully reflect the energy price surge, and they'll go a long way toward shaping the Federal Reserve's next move. In the meantime, headlines out of the Middle East are likely to continue influencing how both stocks and bonds behave in early Q2.

Diversification Quietly Did Its Job

Now, one of the most important, and most overlooked, stories of Q1 was what happened beneath the surface of the S&P 500.

The S&P 500 is a market-cap weighted index, meaning the largest companies carry the most influence over the index's return. When those large companies, particularly those in the technology sector, sold off, the headline number felt worse than what most diversified investors actually experienced.

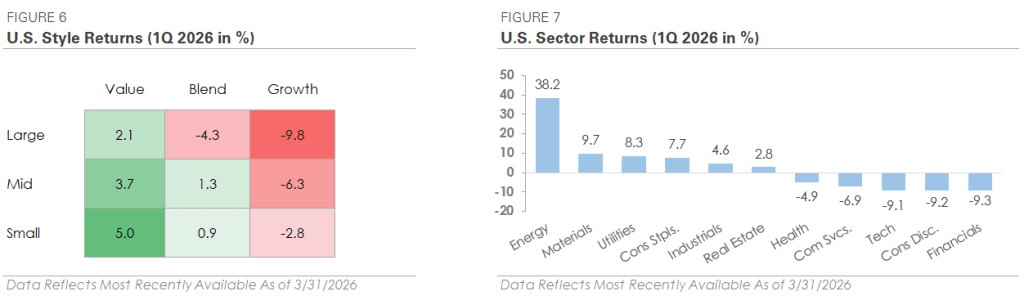

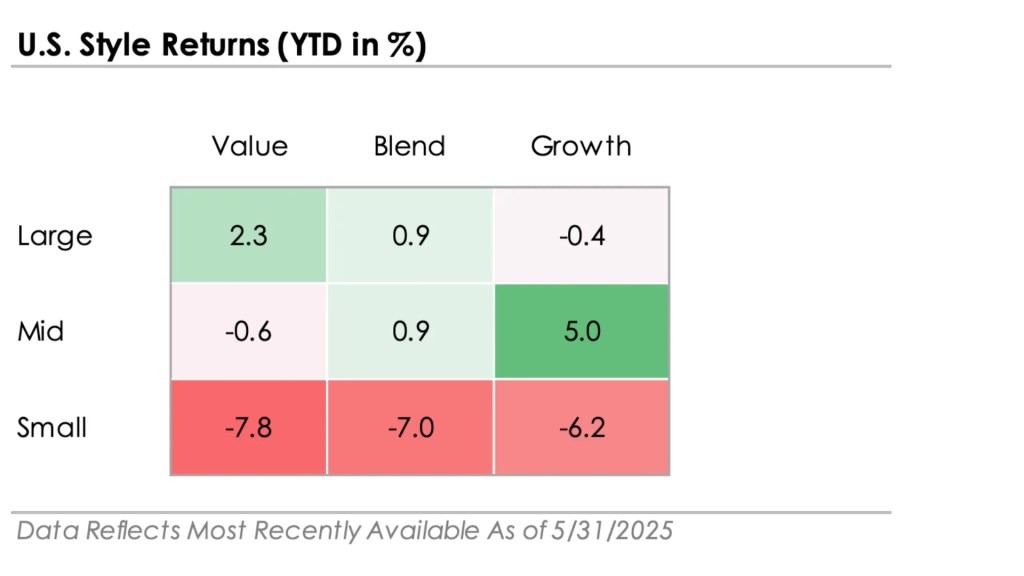

To put it in perspective, the average S&P 500 stock outperformed the broad index by nearly 5% in Q1. Small-cap stocks, as measured by the Russell 2000, actually gained nearly 1%. And international stocks finished the quarter with a gain of nearly 1% as well, outperforming the S&P 500 by more than 5 percentage points.

And what drove that gap? Well, there were two competing forces at work.

The first was a rotation away from mega-cap tech stocks. For the past two years, a handful of the largest companies drove the majority of the market's gains.

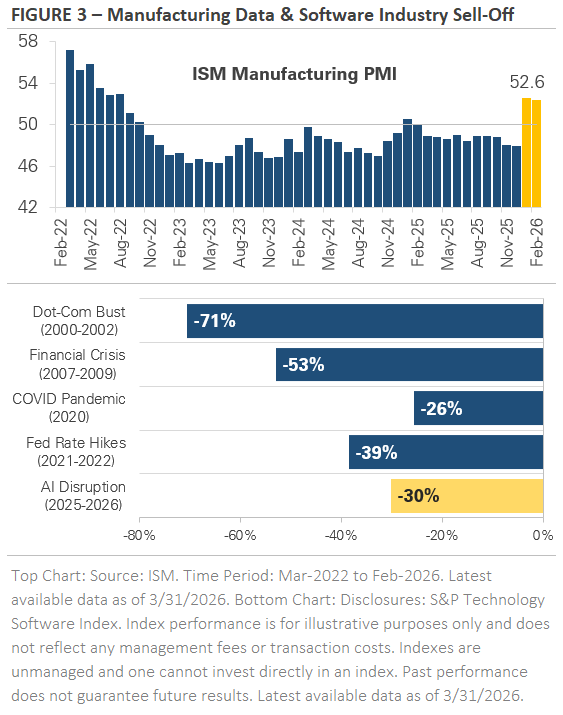

In January, investors started moving away from that concentrated trade. The rotation accelerated in February when concerns about artificial intelligence disruption spread through the software sector, and markets began to price AI not just as a productivity enhancer, but as a potential replacement for entire categories of professional services.

The software sector has now declined nearly 30% from its peak last October, one of the largest non-recessionary drawdowns in over 30 years.

The second force was a genuine improvement in manufacturing activity. After spending nearly a year in contraction, the ISM Manufacturing Index crossed into expansion territory in February and held there in March.

That's a meaningful sign for the economy and potentially for corporate earnings.

Indeed, the manufacturing sector had been a soft spot in the economy since 2022, and the data suggested it was gaining real traction before the conflict began. Industrials was one of the few sectors to set a new all-time high during the quarter.

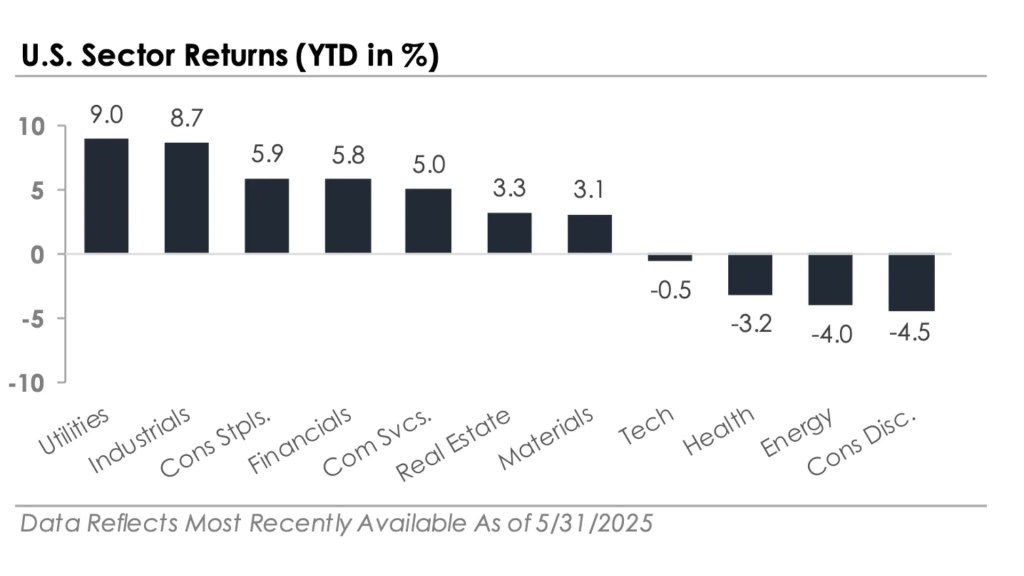

Across the broader equity market, six of the eleven S&P 500 sectors outperformed the index, a sharp contrast to recent years when gains were driven by just a few names. Energy led everything with a 38% return as oil surged.

Materials, Utilities, and Consumer Staples each gained more than 7.5%. On the other end, Technology, Consumer Discretionary, and Financials each declined more than 9%.

The gap between the best and worst sectors was wide. But for investors with diversified exposure across company sizes, sectors, and geographies, the quarter felt more moderate than the S&P 500 return alone would suggest.

Diversification didn't eliminate the volatility. It helped manage it, and that's exactly what it's designed to do.

Bonds Navigated a Volatile Quarter

The bond market had its own version of the quarter's turbulence.

Interest rates rose in January as tariff concerns resurfaced, then fell sharply in February as growth worries, particularly around AI disruption, pulled investors toward safer assets.

March reversed that move quickly.

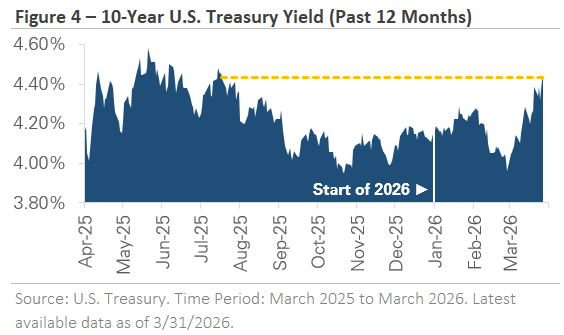

And as oil prices spiked and rate cut expectations faded, yields climbed again. The 10-year Treasury yield ended the quarter near 4.32%, its highest level since mid-2022. The 2-year yield rose nearly 0.35% for the quarter, reflecting how quickly rate cut expectations shifted.

The Bloomberg U.S. Aggregate Bond Index finished the quarter flat, a meaningful step down from the 1% or better returns it produced in each of the prior four quarters. Corporate bonds modestly underperformed higher-quality Treasuries, and credit spreads widened to their highest levels since early 2025.

That widening reflects caution, not crisis, with corporate spreads remaining well below the levels reached during past recessions and financial dislocations.

And what are we to take of all this data?

Well, the bond market is telling us that investors are being careful, but it's not telling us something is broken yet.

What to Watch in Q2

As we move into the second quarter, the central story remains the same: the Middle East, oil prices, inflation, and what the Federal Reserve does next.

Progress toward resolving the Strait of Hormuz closure would ease energy costs and give the Fed more room to maneuver on rates. However, a prolonged disruption means higher oil prices have more time to work through to consumers and businesses, keeping inflation elevated and leaving the Fed in a difficult position.

From a data perspective, the April and May inflation reports are the ones to watch. They'll be the first readings to capture the full impact of higher energy costs, and they'll shape the rate outlook for the rest of the year.

While you're watching those headlines, I want to offer some perspective on the bigger picture.

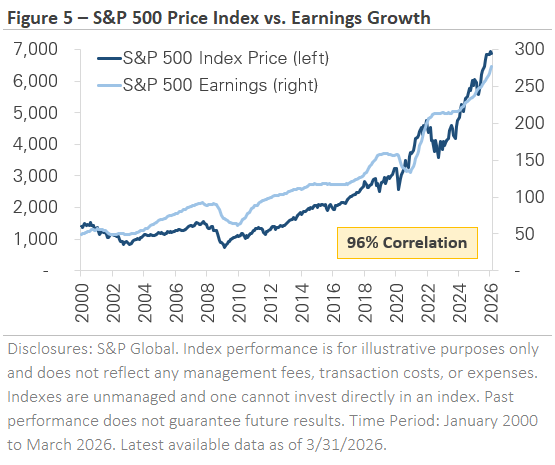

Over the past 26 years, corporate earnings and stock prices have moved together with a 96% correlation.

When earnings rise, prices generally follow.

When earnings deteriorate, as they did in 2001, 2008, and 2020, prices tend to fall with them. What's notable about today's environment is that earnings estimates have continued to rise even as the S&P 500 has pulled back.

Analysts still expect earnings growth in the coming quarters, and profit margins to remain healthy.

Put differently, the market's decline in Q1 was driven by uncertainty around oil, inflation, and Federal Reserve policy, not by a deterioration in the underlying fundamentals that drive stock prices over time.

And that distinction matters.

Certainly, uncertainty is uncomfortable, but it's different from a breakdown in the economic foundation.

The quarter also reinforced something I believe deeply in that staying invested, staying diversified, and keeping a long-term perspective is one of the most effective strategies available to investors. The areas of the market that led over the past two years underperformed in Q1.

Investors with broad exposure across company sizes, styles, and geographies experienced a meaningfully different quarter than the headlines suggested.

When it comes down to it, markets will work through the uncertainty in the Middle East. The data will come in, the Fed will respond, and conditions will shift, as they always do.

In the meantime, your plan was built for periods like this one, and I remain confident in the approach we have in place.

Weekly Market Recap: Oil Shock, Jobs Data, and a Holiday Pause

Market trading this week was driven by a rebound in stocks, rising oil prices, and Friday’s jobs report.

Stocks moved higher through Thursday, even as energy markets reacted to renewed geopolitical tension. Then today, with stock markets closed for Good Friday, the latest payrolls data showed the labor market is still holding up, while bond markets remain open for a shortened session.

By Thursday’s close, the S&P 500 had gained 3.4% for the week, the Nasdaq rose 4.4%, the Dow added 3.0%, and the Russell 2000 climbed 3.3%. That rebound helped markets recover from part of last week’s weakness, but the tone underneath the surface was still shaped by geopolitics.

Oil surged sharply after the latest U.S. rhetoric on Iran reduced confidence in a near-term diplomatic resolution. WTI crude closed Thursday at $111.54 per barrel, while Brent ended at $109.03.

Then on Friday morning, the March jobs report showed payroll growth of 178,000, an unemployment rate of 4.3%, and average hourly earnings up 0.2% month over month and 3.5% year over year.

The week’s other key data reinforced the idea that the economy has not rolled over. ISM Manufacturing came in at 52.7 in March, marking a third straight month of expansion. That matters because it suggests the economy is still holding up even as oil prices rise.

In other words, recession fears did not get confirmed this week, but the inflation side of the equation became harder to ignore.

Key Takeaways

Oil Prices Remain the Market’s Pressure Gauge: Last week, falling oil supported hopes that the conflict might cool off. This week, that changed. The renewed spike in crude is a reminder that geopolitical risk is still feeding directly into inflation concerns and broader market sentiment.

Markets Rebounded, but the Backdrop Is Still Fragile: This week’s rally was constructive, especially because gains were broad enough to include small caps. But the rebound happened alongside a major jump in oil, which means the recovery in stocks did not come with a clean improvement in the macro backdrop.

The Labor Market Still Looks Resilient: Friday’s jobs report helped reinforce that the economy is still holding together. That may ease immediate recession concerns, but it also makes it harder to argue that the Fed will have clear room to turn more dovish if energy prices stay elevated.

Weekly Market Update: Middle East Ceasefire Headlines, Volatile Oil Prices, & Stock Market Rotation

Weekly Market Recap

Market trading was influenced by ceasefire headlines this week.

The S&P 500 rose early after the administration reported talks with Iran, then reversed to close down nearly -0.5% as Iran denied negotiations and the diplomatic window narrowed.

Meanwhile, the market rotation from early 2026 resumed, with small caps, value stocks, and the equal-weight S&P 500 outperforming. Oil dropped nearly -10% on Monday's ceasefire headline before recovering to close the week down roughly -5%.

Treasury yields ended the week higher despite falling mid-week, credit spreads tightened modestly, and the VIX remained elevated.

The week ahead brings the expiration of Trump's five-day strike pause on Iranian energy infrastructure, along with consumer confidence and ISM Manufacturing PMI, the first major economic data releases that will capture the full impact of the war and the oil shock.

Key Takeaways

Oil Prices Remain Volatile

Oil markets whipsawed this week as ceasefire headlines between the U.S. and Iran drove sharp swings in both directions. Prices plunged more than -10% early in the week after President Trump described productive discussions and announced a five-day pause in strikes, raising expectations for a diplomatic resolution.

Those gains reversed when Iran denied active negotiations and later rejected a formal U.S. ceasefire proposal that included reopening the Strait of Hormuz, which remains closed. Iran's counteroffer signals that diplomatic channels are open, but no agreement is imminent.

Bottom Line: Oil prices are unlikely to stabilize until there is clarity on whether negotiations can produce a lasting agreement. Each headline-driven swing is a reminder of how much geopolitical premium remains embedded in energy markets, as well as the stock market.

Markets Traded on Ceasefire Headlines

U.S. equities traded higher early in the week, but reversed lower as the week progressed. The S&P 500 rose over +1%, with most of the advance coming Monday after reports of U.S.–Iran negotiations sparked a broad relief rally.

Markets then pulled back the following session as oil rebounded and uncertainty around a deal resurfaced, staged a rebound when news of a formal ceasefire proposal emerged, and ultimately traded lower as tensions escalated again.

Bottom Line: Stocks remain highly sensitive to ceasefire signals, with the direction of oil prices serving as the most reliable real-time indicator of investor confidence in a diplomatic outcome.

The Stock Market Rotation Resumes

Market leadership broadened again this week as the rotation away from mega-cap stocks reasserted itself. The Russell 2000 outpaced the S&P 500 during the early week rally, and the equal-weight S&P 500 outperformed the cap-weighted index as value stocks pulled ahead of growth.

The divergence is consistent with the trend that emerged in early 2026, when investors began moving toward smaller companies, value stocks, and more economically sensitive areas of the market.

Bottom Line: The rotation paused during the market volatility, but it started to reappear this week. One week doesn't confirm a trend, but the broadening is showing up across multiple measures simultaneously, which is more credible than small-cap leadership alone.

Rate Hike Probabilities Creep Into Fed Pricing

Interest rate expectations shifted again this week as investors began pricing in the possibility that the Federal Reserve could raise rates later in 2026. Futures markets showed rate-hike probabilities rising above 50% in late 2026, with the market starting to price in a rate hike due to concerns that a sustained rise in oil prices will reignite inflation.

At the same time, inflation expectations have reversed slightly lower, suggesting markets still view the current inflation pressures as temporary rather than structural.

Bottom Line: The debate has shifted from the timing of cuts to the possibility of a brief hike, and that repricing matters for duration positioning. If oil stabilizes and inflation expectations remain anchored, the probability of a rate hike could fade.

Market Update: Geopolitical Tensions & Your Financial Plan

Given the deeply concerning headlines about the conflict in the Middle East, I imagine this is a time of worry for you as it is for many.

While the violence and loss of life is distressing, I want to reassure you that your financial plan is designed to weather turbulence, and I’m watching the situation closely on your behalf.

There are still many open questions about how the geopolitical situation will unfold, and near-term market volatility is likely amid the uncertainty.

Some Historical Context

However, in times like these, the chart below offers important historical context in that the U.S. has navigated many challenging periods in the past, so staying focused on your long-term plan is critical.

Indeed, history has shown the wisdom of sticking to your investment discipline and not overreacting to short-term events, difficult as that can feel in the moment.

What to Do Next

As a next step, I would recommend reviewing last week’s email (see link below) because the key takeaways bear repeating:

- Maintain your long-term asset allocation and diversification

- Keep appropriate cash reserves so you're not pressured to sell at bad times

- If needed, we can discuss adjusting your spending temporarily to relieve stress

https://franklinmadisonadvisors.com/cio-corner/market-volatility-heres-what-to-do-about-it/

Rest assured, if I’ve personally worked on your plan with you, your portfolio is built to withstand choppy markets, and we are monitoring developments diligently and ready to make prudent adjustments if warranted.

If You Still Need Help

Ultimately, I'm here as a resource and sounding board for you.

Please don't hesitate to schedule a quick call or reply to this email with any specific questions or concerns you have, I'm happy to talk things through and revisit any details of your plan so you can feel more confident.

While the macro situation is troubling, I have deep faith in the resilience of our country and economy. We will get through this, and I remain optimistic about the long-term future.

Market Volatility – Here’s What to Do About It…

After what feels like nearly a year of markets going straight up, even a modest pullback can feel like a personal hit.

One week you’re checking your account balances with a little extra confidence. And then the next week, when risk assets are sliding and headlines are loud it can feel like the mood shifts fast, right?

So here’s the real question: Should you be worried about market volatility, or should you be expecting it?

Why volatility feels worse after a long rally

Well, while I can tell you that market volatility is a natural part of any market cycle, you’re likely to feel differently these days.

That’s because when markets grind higher for months, we get used to it. That steady climb starts to feel normal and it starts to feel earned.

And when the market finally takes a breather, it can like something broke and make you want to put your money into something “safe”.

The fact is, however, that markets do not move up in a straight line, even when the market and economic backdrop is strong. To be sure, routine pullbacks are part of healthy markets, and part of what keeps longer-term uptrends from overheating.

Even so, minor pullbacks could feel like a sign of a bigger impending move for some individuals.

So, what do you do if you’re feeling this way?

Well, the first step is a simple reframe.

Why this pullback feels different: AI disruption and shifting leadership

Indeed, one reason this bout of volatility feels so intense is that it isn’t only about prices. It’s also about narratives, or the stories that drive market behavior.

Lately, markets have been reacting sharply to AI-related news, including concerns that rapid innovation and shifting leadership can pressure yesterday’s winners and accelerate competitive disruption.

For example, law professionals used to rely on expensive software to give them an edge in their practice. Today, AI can do what the attorneys and software do at a fraction of the cost.

This matters because investors often underestimate how quickly a “winner” stock can turn into a “why is this selling off?”

Because here’s the thing: AI is not merely a theme. It’s a force that can reshape profit pools.

What seemed like an mere augment to business processes is now demonstrating, in real-time, how quickly the innovation can displace earnings potential in more legacy parts of the tech industry.

And when that happens, the market rarely reprices politely over years. More often, it reprices in weeks. And that volatility is what we’re seeing today.

So yes, news about AI being disruptive, including to seasoned incumbents, can absolutely be a catalyst for volatility. The risk is not that the AI story disappears.

The risk is that markets get ahead of themselves, timelines disappoint, competition shows up faster than expected, and leadership rotates while investors are still anchored to the last set of winners.

Nevertheless, time and time again, markets have shown how quickly sentiment can change when the market decides the future arrived sooner than expected.

Markets participation is broadening, and that's not a bad thing

There’s another dynamic worth paying attention to and that’s that market participation is broadening, even as the overall indices chops around.

In other words, it isn’t just the same ten stocks pushing the markets higher. Lately, investors are paying more attention to broader areas of the market, which is a theme we’ve highlighted in recent months, including meaningful moves in small caps.

Now, broadening isn’t a bad thing because it can be a sign of a healthier market structure. But, it does comes with a tradeoff.

That’s because when leadership rotates and participation broadens, dispersion increases. In other words, some sectors rally while others stall out or drop. And this increased disparity can make the market feel more volatile even if the index level does not look dramatic.

So, if you’re looking at your portfolio and thinking, “Why does this feel worse than the headlines suggest?” it’s because the market movements more uneven these days.

The cycle is later, but that does not mean recession is imminent

Another reason we’re likely seeing more market volatility is that we’re likely later in the economic cycle.

Indeed, the latest read on fourth quarter GDP and softening labor market data suggest that economic growth is slowing. This is leading to more economic surprises and frankly, markets are more sensitive to surprises than they were earlier in the cycle.

But “late cycle” does not automatically mean “recession is imminent.”

To be sure, in one of our previous reports, we described an environment where growth remained positive even as the economy softened, with the narrative focused on slowing without slipping into recession.

We have also framed the current data backdrop as modest economic growth, while acknowledging that policy mistakes could change the path.

So yes, the cycle is later.

But the base case is still slower growth, not collapse.

How often does volatility happen?

So then, should we be worried about volatility?

Well, once you understand the frequency of market moves, you’re more likely to stop treating volatility like an emergency.

Because the fact of the matter is that pullbacks happen a lot.

Indeed, in our published work last year, we noted that market dips around 3% have historically happened about seven times per year on average, and declines of 5% or more occur roughly three times annually.

That didn’t happen in 2025.

So, if you’ve felt like you’ve been living through a year with no pullbacks, you’ve been waiting for something that simply feels like it does not show up very often.

Zoom out even further and the point gets even clearer.

For example, in our 2Q25 market update, we shared that since 1928 the S&P 500 has experienced an intra-year decline of at least 5% in the vast majority of calendar years, with the median intra-year drop around 13%.

So volatility is not rare, it’s routine.

The truth is that big down days are rarer, but they still get the headlines.

And that’s the trap, isn’t it?

The scary days are memorable. The normal days are forgettable. And the market uses that to mess with your confidence.

Because the truth is that corrections are not an “if,” they’re a “when.”

When it comes down to it, some investors like a clean framework like, “Markets are due for corrections every 18 to 24 months.”

Whether you like that cadence or not, the core conclusion holds either way.

Smaller pullbacks happen multiple times per year. And, history has shown that a 5% drawdown typically happens in almost every calendar year.

So the takeaway is straightforward: Corrections are not an “if,” they’re a “when.”

What do we do when uncertainty shows up?

So what should you do when market volatility picks up? Well, this is where most investors go wrong.

They spend most of their energy trying to predict what happens next instead of focusing on what they control.

And the one thing you can control is whether you react or respond.

#1: Stick to Your Discipline

Because in moments like this, the winning move is often boring. It’s about sticking to a disciplined investment strategy.

It’s staying diversified.

It’s staying committed to a process built for markets that occasionally misbehave. It’s dollar cost averaging into your portfolio and rebalancing regardless of what the markets are doing.

It’s a point we have made consistently in our updates, including the idea that trying to sidestep volatility through timing can mean missing the best days in the markets, potentially costing you thousands, while staying invested gives compounding room to work.

#2: Review Your Cash Management Process

The other thing you can control is whether you are forced to sell investments at an inopportune time.

That’s where cash management comes in.

The simplest way to avoid panic-selling is to remove the need to sell. Indeed, over the years, we’ve reinforced the use of a cash as a buffer to help you avoid selling at the wrong time, and holding cash reserve ranges that are often appropriate depending on whether you’re working or approaching retirement.

It’s about creating your “sleep-well number,” or the level of cash that lets you stay committed to your strategy when headlines get uncomfortable.

#3: Stick to Your Plan

And finally, you can control how well you’re sticking to your broader financial plan when markets start to feel uncontrollable.

Keep doing the work outlined in your plan, because we’ve already planned for moments like these.

In the short term, markets can feel like a voting machine. In the long term, they act more like a weighing machine.

Pullbacks help reset expectations, cool overheated parts of the market, and set the stage for future gains.

Historically, markets have recovered over time, even through major crises.

So the question is not, “Will this feel uncomfortable?”

It will.

The better question is, “Do I have a plan that assumes discomfort shows up from time to time?”

Bottom line

Should you be worried about market volatility?

Not if you’re prepared for it.

Because the fact is that volatility l is not a surprise guest, it’s part of the ticket to achieving your long-term goals.

So if you’re feeling unsettled right now, then it’s time to get back to the basics. That involves staying disciplined, knowing your sleep-well cash number and keeping your focus on the long-term plan.

That’s how you move through uncertainty without letting it drive the bus.

Market Update: What’s Behind the Market Rally (and Why It Doesn’t Feel Like One)

Have you ever had one of those days where everything looks fine on the outside, but on the inside, you're still uneasy? Like you're waiting for the other shoe to drop?

That’s kind of what the markets feel like right now.

The numbers say we’re back near all-time highs. The headlines might even tell you everything’s recovering nicely.

But if you’ve found yourself thinking, “Something still feels off…” then you’re not alone. So what’s really going on here?

Well, the fact is that this year has been a whirlwind.

We’ve watched the market drop sharply and then bounce back just as fast. One moment it feels like the sky is falling. The next, everything seems fine again.

It’s enough to make anyone feel a little dizzy.

But here’s the truth we often forget: markets move fast, but confidence takes time to recover.

And right now, underneath the surface, there’s still a lot of uncertainty, especially when it comes to trade policy, inflation, and what the Fed does next.

The Story Behind the Numbers

Indeed, since late February, markets have been tossed around by headlines related to shifting trade policy.

For example, the S&P 500 dropped nearly 20% between February and April, then rebounded strongly and is currently sitting just a few percentage points off its all-time high.

But while the market has snapped back, sentiment hasn’t.

Business and consumer confidence have taken a hit in recent months as inflation expectations are rising again. And the Federal Reserve has paused its interest rate cuts, choosing to wait and see how the inflation picture plays out.

Behind the inflation worries is the lingering Trade War 2.0 we’ve covered in recent months. And so far, a full-scale trade war looks less likely at this stage.

That’s because the administration has introduced several 90-day tariff pauses, and most of them run through early July. At the same time, an agreement with China extends through mid-August.

So, there’s breathing room, but not a resolution to the over-arching trade war concerns.

And if things weren’t already complicated enough, a recent court ruling has also added some uncertainty by challenging the government’s authority to impose tariffs. That ruling is under appeal, but it’s another factor that’s keeping businesses, household and investors on edge.

Despite all this, early economic data suggests the impact of tariffs so far has been limited.

The U.S. economy entered 2025 with strong momentum, and current pricing in the market implies investors expect only a modest drag from these policies.

But here’s the thing: the full effects of policy changes like these don’t always show up right away. That’s because it could take months before we see the real impact on earnings and growth.

What Do We Do with All This Uncertainty?

So then, with the markets heading back to all-time highs, is it safe to say that we’re out of the woods?

Well, have you ever noticed how markets sometimes rally when the news is bad, and drop when the headlines are good?

That’s because markets aren’t just reacting to the present, they’re constantly adjusting based on what investors expect the future to look like.

This explains why we’ve seen a sharp selloff followed by a rapid recovery in recent weeks and it also explains why making short-term decisions based on today’s headlines rarely works.

That’s precisely why our approach to investing and how we approach the markets doesn’t change when the narrative does.

To be sure, this kind of environment is exactly what your financial plan was designed for. Because the thing is that we can’t avoid uncertainty, but we certainly can prepare for it.

Periods like this remind us why emotional discipline matters and also reinforces why we diversify.

It also shows us how costly it can be to react impulsively, particularly wanting to get out of the markets when things feel scary, and missing the upside when markets recover before the story fully plays out.

So then, if you’ve been wondering whether it’s time to change course, I’d encourage you to pause and ask a different question, “Is my plan still aligned with my long-term goals?”

If the answer is yes, then the best course of action may be no action at all.

If the answer is no, then we should talk.

So, What’s Next?

Either way, maybe you’re feeling a little uncertain right now.

Maybe the ups and downs of the past few months have made you question whether the plan is still working, and that’s normal.

Just know this: It’s not about knowing exactly what the market will do. It’s about knowing exactly what you will do, no matter what the market does.

The truth is that success doesn’t come from reacting to every headline.

Rather, it comes from staying grounded in a plan that was built for seasons like this because we know that volatility will come.

So if you’re feeling unsettled, here’s the invitation: come back to the plan.

Come back to the first principles that offered you clarity, confidence and peace of mind so you don’t have to figure this out alone.

Because peace of mind doesn’t come from predicting the future.

It comes from preparing for it.

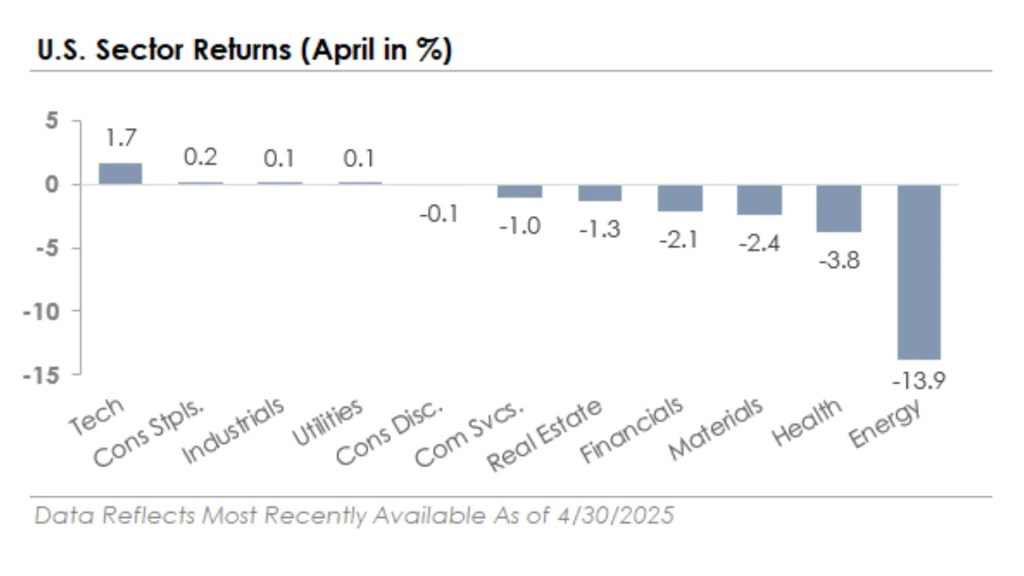

Market Update: A Look Back at April's Market Drama

Have you ever noticed how quickly fear can spread in the financial markets? Or how a headline can send shockwaves through risk assets in a matter of hours?

That's exactly what happened in early April.

And it happened because the White House announced sweeping tariffs, escalating the Trade Wars and just like that, the S&P 500 dropped more than 10% in a single week.

Of course, investors panicked, and uncertainty took center stage.

But then, just as quickly as the fear appeared, it seemingly faded. The administration paused those tariffs, cooler heads began to prevail and by the end of the month, the market had clawed its way back, finishing April with a loss of less than one percent.

The bond market was a completely different story. That's because interest rates didn't know which way to go.

Indeed, they bounced around all month long, responding to every new headline and every ounce of economic doubt. But despite all the noise, they ended up right where they started, flat for the month.

Why Is Policy Driving the Markets?

Now, if you've been wondering what's really moving the markets this year, it all boils down to policy uncertainty.

The truth is that the rules of the game are changing as the direction out of Washington is shifting.

And when the future feels uncertain, people pause, businesses wait and consumers tend to hold back.

At the same time, market participants begin to take notice and start asking, "Is this the start of something bigger?"

Certainly, we've already seen the impact in some corners of the economy. Some consumer demand was pulled forward earlier in the year due to tariff concerns.

But now, there's a hesitation as surveys show that businesses and households are beginning to delay big spending and investment decisions because no one wants to make a move when the rules of the game might change tomorrow.

What's Going On with Stocks?

So then, what has this meant for stocks? Well, the fact of the matter is that what we're seeing in the markets today is when yesterday's winners stop winning. Indeed, the mega-cap Magnificent 7 tech stocks that dominated last year are down more than 15% in 2025 after soaring over 60% in 2024.

Even so, that doesn't mean all stocks are struggling because many investors have already begun shifting their focus to defensive sectors like Utilities, Consumer Staples, Health Care, and Real Estate.

And even though the S&P 500 is down more than five percent, these sectors are showing strength because, in uncertain times, people look for stability.

What's even more striking here is that for the first time since 2023, international stocks are leading the way. In fact, the first quarter was one of their best showings in over two decades.

So then, if you've been ignoring markets outside the U.S., now might be a good time to pay attention.

What About Bonds and the Fed?

And how have bonds done this year? Well, these markets have not been immune from the heightened level of volatility.

Indeed, Treasury yields have been jumping in response to, tariffs, debt concerns, inflation risks, and that ever-present cloud of uncertainty.

At the same time, corporate credit spreads, or the premium that investors demand above holding "safe" investments, have started to widen again.

That's making riskier high-yield bonds less attractive because investors are pricing in the unknown as they're preparing for a wide range of outcomes, and that's exactly what causes volatility.

Now, in the midst of all this volatility, the Fed is waiting patiently on hold. Rate cuts haven't started yet, but the market is betting that the first one will come in June. And not just one, but multiple cuts are now expected by the end of the year.

But that, of course, depends on how the economy holds up and how inflation behaves in the months ahead.

So What Does This Mean for You?

So, what should we make of all of these developments?

Well, the bottom line here is that markets threw a tantrum in April as policy uncertainty stirred the pot.

And for a moment, it felt like everything was up in the air.

But the fact of the matter is that this is what markets do when the path ahead feels unclear.

They test convictions, they expose cracks and they remind investors that uncertainty is the cost of admission for long-term growth.

Nevertheless, uncertainty doesn't have to equal instability.

Because if you have a clear purpose, a thoughtful plan, and a disciplined process for staying on track, then these moments become less about reacting and more about reaffirming what you already know to be true.

That's why now may not be the time to chase returns or make sweeping changes to your investment portfolio.

Even so, it may be the perfect time to revisit your strategy, reassess your positioning, and evaluate whether your plan is built for this kind of environment.

If you're not sure, let's have that conversation.

Because you don't have to predict the future to prepare for it, you just need to know what you own, why you own it, and what to do next.

That's what we help our clients do every day.

Weekly Market Update: Rally Slows as Geopolitics Take Center Stage

Markets moved higher for a fourth consecutive week, with the S&P 500 and Nasdaq both closing at fresh all-time highs for the second week in a row.

The pace of the rally slowed, however, and the gains were uneven beneath the surface. Small cap stocks outperformed both major indexes, while international stocks traded lower as oil prices rebounded and the U.S. dollar strengthened.

Value stocks modestly outperformed growth stocks, and despite the S&P 500’s new high, 5 of 11 sectors traded lower, with defensive sectors lagging the rally.

Bonds ended the week with modest gains despite yields drifting higher, with Treasury and corporate bonds producing similar returns. Oil prices rose after two consecutive weeks of declines, and a measure of market volatility ticked up as investors responded to geopolitical developments during the week.

Key Takeaways

Week Defined by Geopolitical Whipsaw in Middle East

The week was defined by geopolitical whipsaw as U.S.-Iran tensions swung between diplomatic progress and physical deterioration. The headline was constructive: Trump extended the ceasefire indefinitely.

However, the U.S. naval blockade of Iranian ports remained in place, scheduled peace talks were canceled, and questions emerged about a potential Iranian leadership change.

Why it matters: The diplomatic path forward remains open, but the physical confrontation has not been resolved, and the disruption to oil supply has not been removed. Both factors could continue to impact financial markets.

Oil Prices Rise as Naval Blockade Remains in Place

Crude oil surged more than +5% on the week, erasing a portion of the prior two weeks' decline, and Brent crude, the international benchmark, rose back above $100. The move was driven entirely by geopolitical developments, and the ceasefire extension did little to lower oil prices.

On the economic side, March retail sales showed consumer spending held up despite rising energy costs, a sign of resilient demand.

Why it matters: The two-week decline in oil prices had offered an encouraging signal that energy-driven inflation pressures might ease. That picture changed this week. The longer oil remains elevated, the greater the risk that energy costs begin to weigh on consumer spending, corporate profit margins, and broader economic activity. Oil prices are one of the most important variables to monitor in the coming months.

S&P 500 Continues to Set New All-Time Highs

Stocks reached new highs, but the pace of the rally slowed. The S&P 500 and Nasdaq both closed at fresh all-time highs mid-week, supported by the ceasefire extension and a solid start to first-quarter earnings season. Nearly 25% of S&P 500 companies have reported Q1 2026 results, with roughly 80% beating estimates.

Even so, the market's appetite for additional risk appeared to pause. Volatility edged higher, and high-yield credit spreads were flat after three consecutive weeks of tightening, a sign that markets are digesting recent gains rather than pressing further.

Why it matters: The rally remains intact, and the early earnings results are encouraging. However, the pause suggests the market may need a clearer geopolitical signal, such as a geopolitical resolution or positive diplomatic development, before moving higher.

Treasury Yields Reverse Higher as Oil Prices Rise

The 2-year Treasury yield gave back nearly half of a three-week decline that had built on ceasefire optimism and falling oil prices.

Two factors drove the reversal: the collapse of Iran peace talks and the Senate confirmation hearing for Fed Chair nominee Kevin Warsh, which added uncertainty around the future direction of Federal Reserve leadership.

Why it matters: Last week's Fed policy forecast suggested the Fed could have room to cut rates later this year if oil prices continued to fall. This week, that conviction softened. With oil reversing higher and Fed leadership in transition, markets are weighing both inflation risk and institutional uncertainty heading into next week's Fed meeting.

Next Week’s Calendar is Busy

The main event is the Federal Reserve meeting, which will include Chair Powell's second-to-last press conference. The policy decision is widely expected to be a hold, but Powell's characterization of the inflation and growth outlook will be closely watched.

The week also brings a cluster of earnings reports from major technology companies, including Microsoft, Alphabet, Meta, and Amazon, which will offer a window into the state of AI capital spending.

Why it matters: The Fed meeting and tech earnings together make next week one of the more consequential on the calendar this quarter. How Powell frames the inflation picture, and whether leading technology companies confirm or temper expectations around AI investment, could set the tone for markets heading into May.