When will they shut the markets?

Global risk assets continued to move lower on Monday, pushing the current selloff well into bear market territory and on pace with a level of volatility not seen since the market crash of 1987. To be sure, the S&P 500 index shed over 12% in another unpredictable day of trading and follows the surprise FOMC meeting on Sunday that slashed the fed funds rate by 100 basis points and saw the restart of its asset purchase programs.

What has become clear to many market participants and investors is that the precautionary measures used to slow the spread of the coronavirus (social distancing) will have broad and deep economic implications that are still not well understood. It can further be argued that today’s market activity reflects a sentiment that policymakers lack the tools to mitigate the economic pain that is likely to arise in the coming months.

Market closures in context

Considering the seeming failure of current policy to support sentiment, some market participants are now asking whether more direct measures can be taken to halt the selloff. More specifically, it has been suggested that financial markets could be shut altogether to help cooler heads prevail.

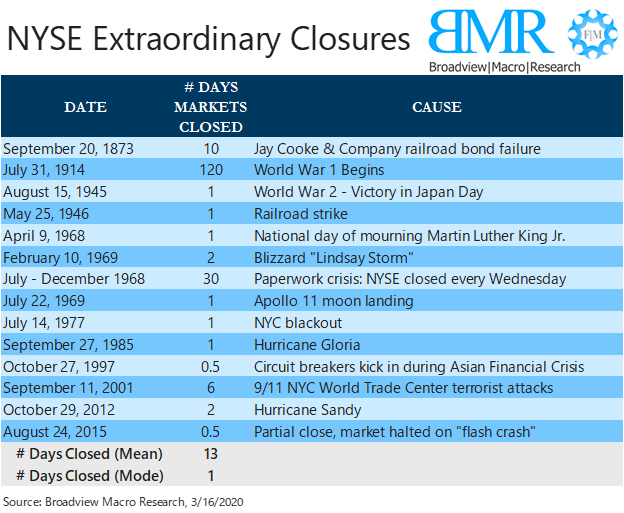

History, nevertheless, has shown that for more than 100 years, closures have sparingly been used to ease market routs. As illustrated in figure 1, there have been a few events over the past century that have led to market closures for more than a day. Some of those events include Hurricane Sandy, the 9/11 terrorist attacks, a Paperwork Crisis in the 60’s and the start of World War 1.

These periods reflect a handful of events that have occurred alongside numerous epidemics, wars, global recessions and financial crises over the same period. Therefore, what the data suggest is that there is little historical precedent for policymakers to outright halt trading in U.S. securities markets for more than a day at a time. What’s more, even during periods of heightened volatility, markets remained opened and largely in normal functioning order.

Figure 1: Days when the New York Stock Exchange was unexpectedly closed

When will they shut the markets?

An argument could be made that closing the markets for even a week or two could preserve household wealth while giving policymakers time to prepare a robust solution set that would help businesses and households navigate what is likely to be a tumultuous economic landscape in the coming months. Nonetheless, what has become clear to us is that the financial markets today act as an important signaling mechanism to policymakers.

For example, indicating a lack of liquidity and other systemically important market dislocations in the case of the Fed, and a lack of confidence in the currently coronavirus policy response to the White House. To shut the markets entirely, therefore, would mean cutting off the feedback mechanism that has helped guide and refine policy as events surrounding the spread of the coronavirus have unfolded. Besides closing the markets, what else can be done to ease market selling pressures?

To be sure, a number of tools exist today that can help prevent negative market sentiment from completely overwhelming asset prices. The New York Stock Exchange, for example, utilizes circuit breakers that halt trading at three different times throughout the trading day: 15 minutes when the S&P 500 index falls 7% and then again after 13% from its previous day’s close; and a complete halt in trading when prices fall more than 20% during the day.

Another tool used by policymakers to stem a market rout is a ban on short selling. This approach was utilized in 2008 to halt speculative selling pressures in financial stocks. And, this approach is being used today in a number of markets outside of the U.S.

In short, after weeks of policy disappointments, investors are eagerly awaiting some catalyst to quickly stop the bleeding and potentially set the stage for a move higher in the markets. While it’s very well possible that market closures could take place in the weeks ahead, their importance as a signaling mechanism suggest such an outcome would be a last resort among a number of other tools.

What this means is that events like today are likely to remain with us until it is evident that the fight against the coronavirus has reached a turning point. Until then, we provide a number of recommendations that households can take to weather this period of heightened market volatility and uncertainty.

Economic update: Downside risks still increasing

The outlook for the U.S. and global economy has deteriorated yet again. Unsurprisingly, the culprit behind the outlook downgrade has been news of the coronavirus’ continued spread. To be sure, risk assets sold off this week and financial market volatility increased as concerns about the virus and its potential impact on the global economy dented investors’ up-until-recent euphoric sentiment.

More importantly, worries about the coronavirus come at a time when economic conditions in the U.S. and around the world remain weak and susceptible to unforeseen shocks. Our view remains that the coronavirus outbreak is likely to have a material impact on the global economy and financial markets assuming its spread is not quickly stemmed. Therefore, we believe that households and investors should prepare for economic and market weakness in the coming months, notably as the effects of the coronavirus remain wildly uncertain.

Data pointing to further 2020 weakness

Each month we evaluate a host of quantitative and qualitative factors that help guide our U.S. and global economic and market outlook. Indeed, we utilize econometric models that rely on developments in the labor market, consumer spending, business and household sentiment and rates, among others, to help frame our U.S and global economic views. The result of this work includes forecasts on U.S. gross domestic product (GDP) growth, inflation and employment conditions as well as a view on major currencies and commodities. So, what does our latest work show?

Well, the latest update to our models for February suggests that economic growth in the U.S. is likely to deteriorate further relative to our view in January. More specifically, our quantitative models show that household spending growth is likely to lag behind 2019 even before accounting for the effects of the coronavirus. At the same time, our models suggest that business investment could slow further as global manufacturing remains weak, while a rebound in the U.S. housing market largely supports positive U.S. private investment activity.

Looking abroad, various data releases over the past few weeks have pointed to potentially stabilizing global economic growth. To be sure, the latest reading of the Organization for Economic Cooperation’s and Development (OECD) Composite Leading Indicators (CLIs) are consistent with a potential growth rebound in both developed and emerging market economies. And this improving trend has been supported, in part, by some better than mixed global business sentiment and a broad rally in risk assets, especially U.S. stocks, from the start of the year.

Figure 1: Downward revision to 2020 growth outlook

Coronavirus uncertainties intensify

Taken by itself, the data would lead us to believe that the growth outlook for the U.S. and global economy, while sluggish today, could pick up into the tail end of 2020. This is because broad money printing by the world’s key central banks and a still resilient consumer have underpinned spending activity.

Nevertheless, as we look into the future, we believe that the hard data will begin to reflect renewed weakness in the global economy as coronavirus concerns take hold. And, as they do, this will challenge corporate earnings growth and subsequently the stock market’s ability to charge to new weekly highs.

To be sure, this view was reflected in one of our past writings and comes as the coronavirus is poised to change the way firms do business and the way households spend. For example, just a few weeks ago, as far as market participants were concerned, the coronavirus was largely a China issue as headlines centered on developments in Wuhan.

Today however, virus headlines have taken a dourer tone as cities in Italy deal with quickly growing number of infections and more reports reflect the spread of the coronavirus across the European continent. Adding insult to injury, even leaders from the Centers for Disease Control (CDC) report a heightened risk for a widespread coronavirus outbreak in the U.S. And what does all this mean for the economy and markets?

Figure 2: Pre-coronavirus tentative signs of global economic stabilization

Unforeseen disruptions

We expect discretionary spending among households in the U.S. and abroad to decline should cases of the coronavirus continue to increase globally. This consumption slowdown is likely to come from not only mandatory quarantines, but also from voluntary confinements reflecting a desire among the general public to avoid places where the virus could potentially spread.

This is important because, while eCommerce has increased notably in recent years, spending at brick and mortar stores still accounts for a large portion of retail sales in the U.S. and many developed and developing economies. And, with household spending being a key component of GDP growth, a slowdown in spending could put renewed downward pressure on the overall global economy and hence earnings growth.

Another impact stemming from the coronavirus spread is that of supply chain disruptions. China remains a key supplier of manufactured goods and is integrated into global supply chains that span not just the Asia Pacific region, but also across Europe, the U.S. and other parts of the world. This is important because it only takes the loss of just one critical component to halt the entire production of a key good. Today, some governments are exploring ways to get around such supply chain disruptions, but the fact is that China remains a key global supplier of critical manufacturing components. How do these developments affect our forecasts for the year?

The prospect of a widespread coronavirus outbreak in the U.S. is likely to notably alter of our current estimates of economic growth. That is, assuming a quick resolution to the viral outbreak is not found and coronavirus concerns intensify, economic growth in the U.S. and globally are likely to move from a moderate slowing in 2020 to sharp slowdown with yet to be determined consequences. How bad could it get?

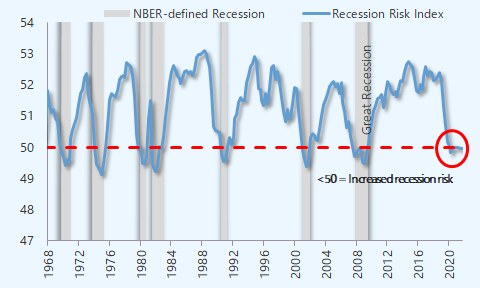

At this point the severity of the slowdown will largely depend on the adaptability of businesses and resilience of consumers to deal with host of uncertainties amidst the threat of a global outbreak. With that said, the virus comes at a time when our quantitative recession risk indicator is pointing to a rising likelihood of an economic downturn in the second half of 2020. What this means is that a sharp decline in business and household spending as a result of the coronavirus could be enough to tip the U.S. and global economy into a recession sooner rather than later.

Figure 3: U.S. recession risk indicator reflects rising likelihood of a 2020 downturn

Preparing for the unexpected

What are households and investors to do in an environment that is charged for more market and economic volatility in the weeks and months ahead? The fact that risk asset prices remain elevated even amidst the coronavirus headlines has given us reason for pause. As we’ve noted in prior reports, we believe that the current rally in risk assets has more to do with the Fed’s unsustainable easy money policies rather than solid economic fundamentals. And this could set the stage for more market pullbacks this year.

While central bank asset purchases have been supportive of lower borrowing rates and a boost to housing market sentiment, we are hard pressed to find positive catalysts that would support a sharp economic rebound this year, particularly as coronavirus risks have yet to be contained and hence challenge the feasibility of a sustained rally in financial markets.

With the economic outlook set to weaken in 2020 and financial market volatility likely to remain elevated, we recommend that households take some constructive steps to prepare for the unexpected. For instance, one way to increase financial preparedness and resilience in a time of uncertainty is to reevaluate big-ticket spending decisions and divert more cash flows toward emergency savings.

This can be accomplished by reducing non-essential spending and refinancing high interest debts in today’s low interest rate environment. We believe that these steps will better prepare households for unexpected life events, particularly as job opportunities have become less plentiful and labor market conditions show signs of continued weakening into the months ahead.

For investors oriented towards asset growth, we recommend maintaining a diversified exposure in investment portfolios. This means not chasing hot stocks or trying to time a market bottom. At the same time, we recommend reevaluating exposure to risky investments to ensure that aggregate portfolio holdings across all investment accounts are in line with long-term goals. This includes rebalancing to target allocations and trimming winning positions to raise cash to keep as dry powder for when market volatility creates favorable buying opportunities.

Finally, for households taking distributions from investment, we recommend rebalancing accounts to long-term investment objectives and reduce unnecessary risk taking. Further, we recommend ensuring that cash positions are adequate to meet 6-12 months of living expenses. This is intended to avoid forced selling at depressed prices, especially as economic and market uncertainties are likely to rise in the coming weeks and months most notably as the overall impacts of the coronavirus remain wildly uncertain.

Are Democratic Candidates' Proposed Economic Policies Disruptive?

The race for the Democratic Presidential nominee remains crowded with eight candidates (as of this writing). Yet, with Super Tuesday just around the corner, the list of candidates is likely to be winnowed quickly. And one deciding factor that could make (or break) the decision for the Democratic Presidential nominee in July is likely to be a candidate’s economic policy.

But what exactly are the candidate’s positions and more importantly, why should they matter to savers and investors? In this week’s post we briefly explore some of the top candidate’s policies and provide an overview of their positions in the context of the current economic environment.

It is our opinion that (regardless of the candidate), the economic policies currently on offer are likely to be disruptive to the U.S. economy and financial markets should a Democrat clinch the presidency in November. Nevertheless, Election Day remains a long way away and we’ll have a better idea of the potential disruption to the economy (and markets) as we get closer to the summer conventions.

Economic policy: why does it matter?

So why should we care about economic policies, particularly as they relate to the election cycle? Well, put simply, political leaders can affect our quality of life through their ability to tax and spend. While the latest enacted key policy (Tax Cuts and Jobs Act of 2017) affected the economy in not so obvious ways, some policies can have more direct effects on our everyday lives, as we pointed out last week in our discussion on the SECURE Act.

The reality is that economic policies can affect the quality of the health care we receive, how much we pay for goods and services we use every day and the extent to which we can find and maintain gainful employment. Today, another generation of voters feel left behind as rising costs of living and debt burdens, notably those related to paying for college, have stifled their ability to get ahead in life financially.

To be sure, while some data suggest that labor markets conditions appear “tight” – with unemployment near multi-year lows and still positive payroll growth – the fact is that wage gains have barely outpaced inflation over the past decade. And simply put, some people feel that the rules have not worked in their favor and this election cycle Democratic politicians are offering up their own solutions to very real problems.

Candidate Economic Policies

It’s important to note that Congress typically is responsible for creating the rules (laws) that affect people’s lives. Nevertheless, the President, in some cases, can help set the legislative agenda and carry the baton on key, highly visible issues. Think the Affordable Care Act. Among many important topics, we believe that issues surrounding student debt, wages and jobs, health care and housing are likely to garner broad based attention from the electorate and the markets in the coming months.

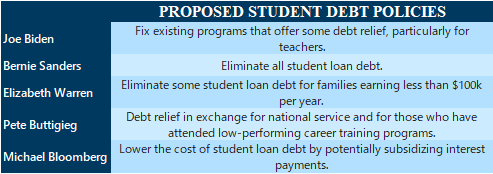

Figure 1: Proposed Student Debt Policies

Student Debt

One issue that has perhaps affected an entire generation’s ability to get ahead in life financially is the burden of borrowing to pay for a college education. To this point, the amount of student loan debt has ballooned from less than $500 billion in 2006 to over $1.6 trillion in 2019. Arguably, this debt has hampered household formations among key demographics, most notably among the Millennial generation. So, what are some of the solutions being offered by Democratic candidates this election season?

Both Senators Elizabeth Warren and Bernie Sanders have proposed to eliminate student loan debt. Where their policies differ is that Sanders would do away with all outstanding student loan debt (all $1.6 trillion of it) while Warren would eliminate debt up to a certain limit and phase out the benefit for higher wage earners.

Other candidates like South Bend Mayor Pete Buttigieg would like to see debt eliminated for some borrowers in exchange for government service. Former New York City Mayor Michael Bloomberg and Senator Joe Biden would prefer options that fix existing issues with the student aid system, offering ways to lower borrowing costs but just short of all out-debt forgiveness.

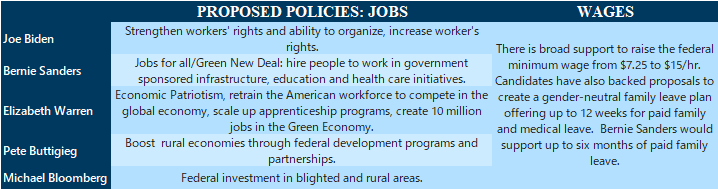

Figure 2: Proposed Jobs and Wages Policies

Wages and Jobs

It has been well over a decade since laws governing the federal minimum wage have been reviewed. In fact, in 2007 Congress raised the federal minimum wage to $7.25 – a rate that is equivalent to a full-time annual salary of $15,080 – and well below the Department of Health and Human Services family of four poverty level of $26,200.

Today, there is broad consensus among Democratic candidates that the federal minimum wage should be at least $15 per hour and many have pledged to pursue legislation that would help increase workers’ earnings. Besides raising the minimum wage, what else have candidates suggested to improve employment opportunities for the American worker?

Well, candidates like Warren and Sanders have each introduced their own versions of a “New Deal”. Warren’s Economic Patriotism is focused on retraining the workforce to compete in a globalized economic environment. This includes scaling up apprenticeship programs and creating incentives for employers to offer other on-the-job training initiatives. Sanders’ Green New Deal meanwhile focuses more specifically on federally funded infrastructure, health care and education initiatives that would directly create jobs.

Bloomberg and Buttigieg have also proposed less-comprehensive programs that would create jobs by improving living circumstances and enhance infrastructure in rural and blighted areas across America. Biden’s focus, meanwhile, is less on introducing new programs than on fine-tuning already implemented policies. This involves focusing on strengthening workers’ ability to organize and generally increase workers’ rights.

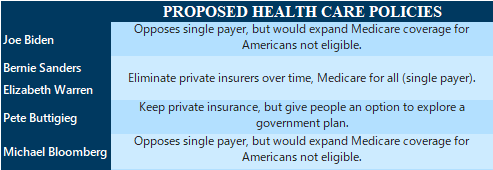

Figure 3: Proposed Health Care Policies

Health care

Health care has been the traditional third rail in American politics for decades. This hasn’t changed in today’s election cycle and arguably has become more of a contentious point, especially at a time when health care costs continue to rise and at a considerable pace. This consternation comes as more people participate in the health care marketplace thanks to the Affordable Care Act. Yet, health care costs continue to increase as an aging U.S. population draws on more health care services. So what solutions are some candidates offering?

Well, some of the solutions vary from completely eliminating private insurers and expanding government programs like Medicare (a single payer option). This position is strongly held by candidates like Warren and Sanders. Bloomberg and Biden, on the other hand, oppose the idea of a single payer but would seek to expand coverage for Americans not currently eligible for Medicare. Either way, no one candidate has offered a quick fix to a very complicated (and costly) topic for many Americans.

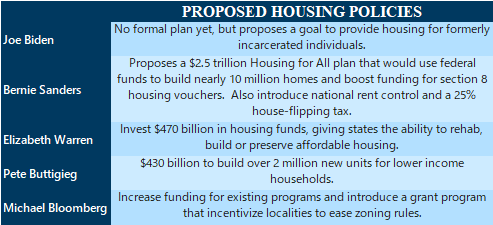

Figure 4: Proposed Housing Policies

Housing

It has been well over a decade since the housing boom went bust, yet its aftereffects continue to live on. Indeed, housing has become an important issue, notably as home prices continue to move past housing-boom highs and instances of working homelessness continues to increase in different parts of the country.

What’s more, housing costs have risen at a pace faster than inflation over the past five years and have yet to show signs of abating thanks, in part, to the Federal Reserve’s not-QE money printing. Among some of the issues affecting affordability is the fact that quality affordable housing stock has dried up as jaded post-housing-crisis builders refrained from constructing lower priced homes, driving down housing affordability. Democratic candidates across the board agree that something should be done to address the current housing issues.

Solutions offered by candidates include everything from grants that incentivize localities to rehab and improve existing stock to federal funding to build more affordable housing. This camp includes candidates Sanders, Warren and Buttigieg whose plans consist of using federal funds to directly add to the housing stock in one form or another. As for Bloomberg and Biden, while they have expressed a desire to address the housing issue, they have focused their efforts on improving and expanding programs and zoning issues than on building more homes.

Figure 5: Paying for it all

Someone needs to pay for it

Finally, many of the programs proposed by the Democratic candidates require additional spending, some at trillion-dollar rates, over the next decade. This is a problem as the national debt today exceeds $23 trillion dollars and the Federal debt-to-GDP ratio has gone from 59% in 2000 to well over 100% today. What this means is that simply borrowing to pay for these economic policies will become progressively more problematic, especially at a time when growth in the U.S. economy is expected to slow. How would candidates pay for their proposed programs?

Simply put, most candidates have suggested raising taxes as a primary means to pay for their projects. Of note have been Warren and Sanders’ proposals to target the wealthy to fund their programs. Warren, for example, has offered an ultra-millionaire tax on wealth (rather than income) for the wealthiest 75,000 families in the U.S. Sanders similarly has his own Extreme Wealth Tax, that would require CEOs earnings more than 50x their employees to pay higher taxes as a way to fund spending on his social programs.

Bloomberg, Biden and Buttigieg have focused more on broadly increasing existing taxes rather than singling out any one social class or taxpayer. Bloomberg, for example, would like to roll back some of the TCJA benefits, raising the corporate tax rate back up to 35% from current levels of 21%. Biden would also like to increase revenues by taxing capital gains as ordinary income, raising the corporate tax rate and ending stepped-up basis rules.

Potential economic disruption?

The solutions offered by some of the Democratic candidates are in many ways a departure from current policy and certainly have the potential to be disruptive to the financial markets and economy. Why? On the one hand, an elimination of student debt could act as a massive form of fiscal stimulus, in some cases substantially increasing the amount of disposable income available to younger households who have a greater propensity to spend. Increased certainty over health care, employment and housing could also give households the confidence they need to make long-term spending and saving decisions.

On the other hand, someone will need to pay for the additional costs associated with some of the proposed programs. And while financial markets cheered the TCJA, its effects on the economy, notably as they related to tax cuts, have yet to show major benefits to the overall economy. Nevertheless, reversing some of these benefits, particularly raising corporate taxes, could be perceived negatively by the financial markets as corporate earnings decline as taxes increase. What’s more, business hiring and investment activity could slow in the short-run as business leaders put off spending decisions as policy uncertainties linger.

Assuming a Democrat wins the White House, over the long-run, the outcomes will further depend on a number of factors, including the composition of Congress following elections and the political will to implement some of the large-scale projects. Make no mistake, topics like housing, health care, wages and paying for college are issues that are likely to remain relevant for years and will need to be addressed sooner rather than later.

As for the degree to which candidates’ policies will disrupt the U.S. economy, we believe that the outlook will become clearer as we move past conventions in the summer. Even so, some of the same policies that have gotten us to this point will need to at least be addressed by our political leaders, regardless of whether a Republican or Democratic president is at the helm post-November.

Economic update: Recession risks on the rise

U.S. Growth

Our latest estimates continue to suggest that economic growth in the U.S. will weaken in the coming year while the risk of a recession remains elevated. We expect growth to come in around 2.1% YoY in 2020, slightly weaker than our expectation of 2.2% for 2019.

International Growth

Globally, World GDP is likely to accelerate as emerging market economies (ex China) rebound from markedly low levels of growth in 2019. We expect China’s economy to slow further in 2020 (5.8% YoY) as policymakers balance easy credit conditions with allowing market forces to curb certain lending excesses. Growth in developed market economies is expected to remain soft in 2020 as weaker growth in China and the U.S. put downward pressure on eurozone (1.1% YoY) and Japanese (0.6% YoY) exports.

U.S. Employment

Incoming data show that labor market conditions remain weak and continue to deteriorate, as evidenced in the November double digit job opening decline. These figures continue to support our expectation of a rise in employed workers (3.8% in 2020 vs. 3.7% in 2019) as nonfarm payrolls growth continues to slow and the number of people reporting full-time employment falls.

U.S. Inflation

Inflation is likely to remain soft as a decline in home prices through the first half of 2020 is offset by a rise in transportation costs off of 2019’s low base. Core PCE is likely to fall further in 2020, led on by housing weakness. Decelerating inflationary pressures coupled with slowing economic growth are likely to prompt two further rate cuts by the Fed in 2020.

Click here to download our latest economic forecasts.

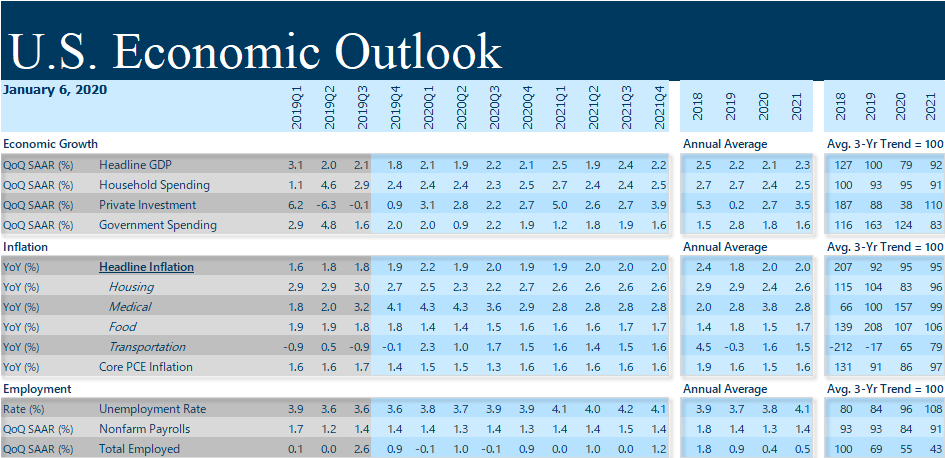

Figure 1: January economic outlook

Let the good times roll: the beginning of the end?

Stock market prices continued to grind higher as economic data releases surprised to the upside this week. Indeed, a host of indicators suggest to some that growth in the U.S. may in fact be improving after a softer showing in 2019 which has supported a rally in risk assets not just in the U.S. but globally this year. A key question for investors and savers now, however, is whether the good times are just getting started or the data mark the beginning of the end of good economic times.

We have argued that 2020 is likely to mark the beginning of the end for U.S. economic buoyancy and financial market resilience. Indeed, longer term indicators point to a rising risk of economic and market disappointment this year with recession related risks remaining elevated and not decreasing even as Fed policymakers would otherwise like people to believe.

What this means is that households should increasingly prepare for higher levels of economic and market volatility in 2020. This includes taking efforts to increase net positive cash flows, building up emergency reserves, rebalancing investment risk exposures and generating cash in investment portfolios to cover an extended period of retirement living expenses as market volatility increases.

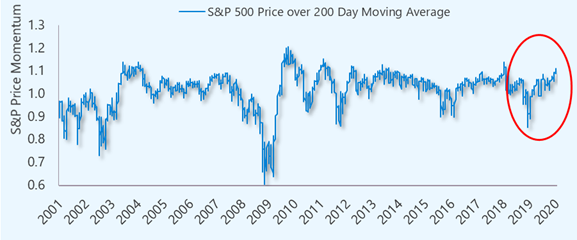

Figure 1: Market momentum near 2-year high

Why so glum?

Key data releases hailed by the financial markets this week included seemingly robust retail sales and housing market data. The reports pointed to generally better than expected activity in December and capped a strong finish to an otherwise lackluster year for both sectors. Indeed, government data showed that December retail sales grew at its fastest year-over-year pace (+5.8%) since August 2018. This compares to a meager 1.6% rate in December 2018 and contrasts a period of general economic malaise in the fourth quarter of 2018.

Similarly, reports on building permits, housing starts, mortgage applications and builder confidence all trended higher in the month of December, pointing to a rebound in housing market activity. Building permits, for example, were up 11.4% year-over-year at the end of the fourth quarter of 2019 compared to a decline of -1.8% in 2018. What’s more, builder sentiment rose to its highest level in over 20 years as mortgage rates remained low all the while December UofM Michigan Consumer Sentiment rose to its highest level since May 2019. Taken together, these developments have given financial markets a reason to keep pushing higher this year.

To be sure, market participants have been heartened by the seemingly positive economic data and the S&P 500 is now up over 3% in January, making new all-time highs in 10 out of the first 12 trading days of the year. Year-to-date, riskier international equities are in some cases outpacing the U.S. with China up 5%, Mexico up 6% and Turkey up 7.3%. These developments come even after the threat of war between Iran and the U.S. and ongoing impeachment proceedings on Capitol Hill. So why are we so pessimistic on the market and economic outlook?

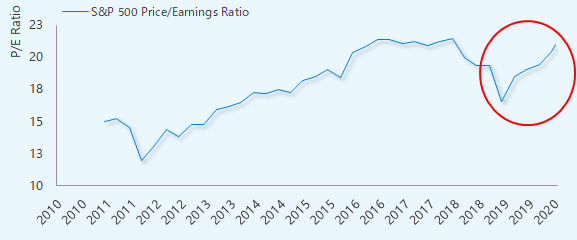

Figure 2: Stretched equity market valuations

No so fast...

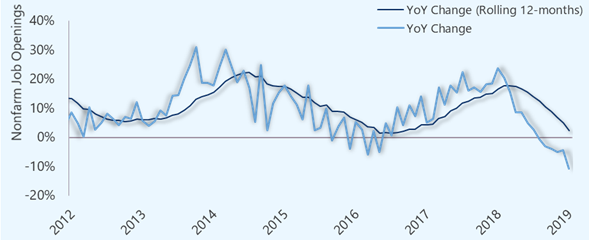

While it is tempting to extrapolate positive near-term developments into the future, the truth is that cyclical factors that we track suggest that economic and market conditions may be more fragile than the recent historical data suggest. Take, for example, the latest labor market data. While December payrolls bested estimates, the trend in new job growth remains biased to the downside. This is evidenced in the latest nonfarm job openings data, an important leading indicator of labor market developments. To be sure, the rate of employers putting out ads to hire new workers declined -10.8% in November and is on track for their worst rolling 12-month pace of growth since 2017.

This is important because, if labor market conditions continue to deteriorate, and business sentiment weakens as our projections suggest, then growth in the U.S. economy is likely to remain weak in the first half of 2020. Such a development would put downward pressure on corporate revenues, leading to earnings disappointments in the year and giving market participants a reason to step back from their expensive positions in stocks. What’s more, a continued decline in labor market conditions, weaker economic sentiment and increased financial system instability could lead to a rising risk of a U.S. recession in 2020.

Figure 3: Labor market conditions waning

Juicing the markets

To be sure, equity prices have been on a tear since the Federal Reserve quietly restarted its asset purchase program, increasing the size of its balance sheet by 11% since August 2019 even as Chairman Powell asserts that the Fed has not restarted quantitative easing (QE). Better near-term economic data aside, this form of money printing has arguably boosted risk asset prices all the while corporate earnings growth has slowed and the economic outlook remains weak.

The effect of central bank supported rising prices and stagnant earnings growth has contributed to stretched valuations in the equity market. In other words, U.S. stocks, as measured by the S&P 500 are now more expensive than they have been in the past two years when measured by its trailing and forward-looking P/E ratio. And these stretched valuation measures have also been showing up in other parts of the equity market, particularly in the growth style of large, mid and small cap U.S. stocks as a whole.

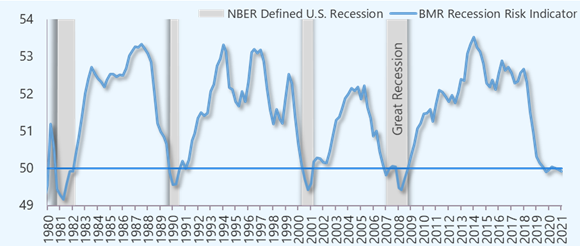

Figure 4: Recession risks remain elevated

Preparing for economic and market uncertainties

The fact that risk asset prices continue to push higher even as geopolitical risks linger and economic fundamentals remain subdued has given us reason for pause. To be sure, we believe that the current rally in risk assets has more to do with the Fed’s unsustainable easy money policies which could set the stage for a pullback in prices this year. While central bank asset purchases have been supportive of lower borrowing rates and provided a near-term boost to housing market sentiment, we are hard pressed to find positive catalysts that would support a sharp economic rebound this year and hence underpin the financial market rally.

In fact, we believe that global easy money policies have contributed to systemic excesses, and are providing a lifeline to firms that otherwise should no longer be in business. History has shown that such excesses do not continue in perpetuity, and when combined with our latest business cycle work, suggest that risk of an economic downturn and heightened market volatility is likely to increase this year. Taken together, we believe that recent market exuberance could be marking the beginning of the end to this economic and market cycle.

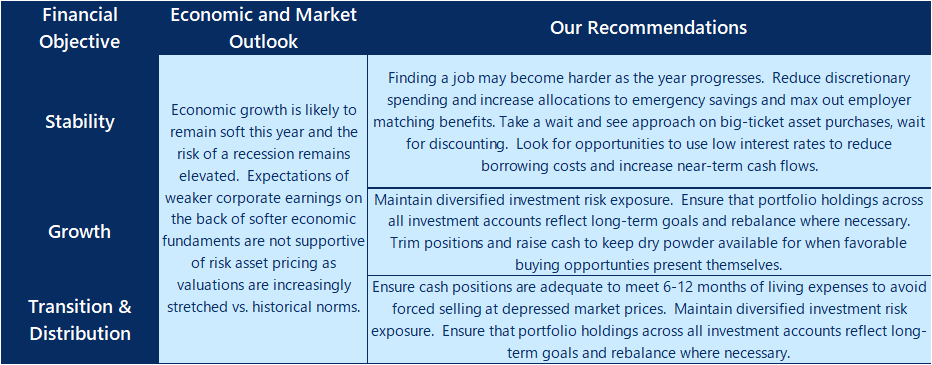

With the economic outlook set to weaken this year and financial market volatility likely on the rise, we recommend households take some constructive steps to remain prepared for the unexpected. First, we recommend households take a step back and reevaluate the vision and purpose for their money as they look ahead into 2020 and beyond and determine whether their plans are in alignment with current economic and market conditions.

Next, we recommend preparing for rising uncertainties by increasing net cash flows by reducing discretionary spending and finding ways to refinance debts given today’s lower interest rate environment. We also suggest reevaluating big ticket spending decisions, topping off emergency savings and ensuring employer-matching contributions are maxed out. We believe that these steps will better prepare households for unexpected life events, particularly as labor market conditions show signs of weakening in the coming months.

For investors oriented towards asset growth, we recommend maintaining a diversified investment exposure and stepping back from riskier investments. Further, households would be best served by ensuring that aggregate portfolio holdings across all investment accounts are in alignment with their long-term goals. This includes rebalancing portfolios to target allocations and trimming winning positions to raise cash to keep as dry powder for when market volatility creates favorable buying opportunities.

Finally, for households taking distributions from investment, we recommend rebalancing accounts to long-term investment objectives and reduce unnecessary risk taking. Further, we recommend ensuring that cash positions are adequate to meet 6-12 months of living expenses. This is intended to avoid forced selling at depressed prices when market volatility increases.

Figure 5: Preparing for the unexpected

Acute threat: a looming U.S. recession

-

The threat of a U.S. recession will add to a number of looming issues contributing to heightened financial market and economic complexities and uncertainties in 2020.

-

While some of the latest economic data suggest that growth in the U.S. economy remains steady, some key market and economic indicators are more consistent with a downturn, like the inverted yield curve.

-

The health of the U.S. consumer is likely to hold the key to the health of the U.S. economy and the potential timing of a U.S. recession.

In addition to the financial market distortions, debt overhangs and democratic challenges to getting ahead financially over the long term, lies the increasingly real potential for a U.S. recession in the near term. The reason an economic downturn is important is because of its immediate and acute effects on households, particularly as it relates to its potential to derail life transitions as emergency savings are put to the test, opportunities to get ahead are stalled by lending and labor market tightness and financial market volatility further complicate aforementioned retirement insecurity.

The making of an economic downturn

What is a recession? On the one hand, a commonly cited definition of a recession is two consecutive quarterly declines in GDP growth. The National Bureau of Economic Research, a highly regarded business cycle dating group, on the other hand, broadly defines a recession as “a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales".

Put in simpler terms, a recession is a crisis of confidence experienced by businesses and consumers that is preceded by a set of events or circumstances (inflation shock, financial market disruption, war, social unrest) leading to a broad slowdown in economic activity. More than ten years have passed since the U.S. experienced its last recession and comes at a time when downturns tend to happen once every 5-7 years[1]. Does this mean that a recession is imminent?

[1] National Bureau of Economic Research, Business Cycle Dating, December 2019

Figure 1: Yield curve inversions lead recessions by 18-24 months

What the recession indicators are saying

While some of the latest economic data suggest that growth in the U.S. economy remains steady, some key market and economic indicators are more consistent with a downturn, like the inverted yield curve. More specifically, the spread, or difference between the yield on 10-year and 3-month U.S. Treasurys is historically consistent with a recession beginning 18 to 24 months after the spread turns negative.

Using history as our guide, an inversion of the yield curve in 2019 suggests that the risk of a recession is likely to increase in mid-to-late 2020. Nevertheless, no one measure can accurately predict a downturn in the economy and so it is important to look to other economic indicators for more confirmation of a likely downturn.

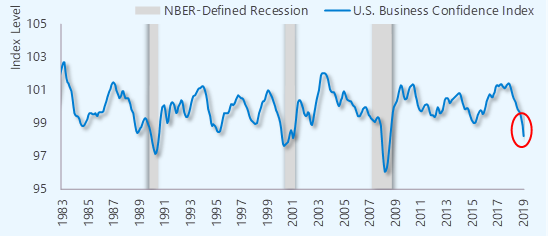

Figure 2: U.S. business confidence in decline on trade uncertainties

To be sure, measures of business and household sentiment are another statistically significant indicator of a potential recession. And lately, business confidence in the U.S. and globally has weakened from its peak in 2018. This comes as the positive effects of the U.S. Tax Cuts and Jobs Act have faded, and the U.S. has raised tariffs on important economic and trading partners like Canada, Mexico, China and Europe.

At the same time, China’s credit-fueled growth continues to slow, putting downward pressure on economic activity at home and among its important trading partners, including the U.S. Taken together, these and other financial market complexities and geopolitical uncertainties are contributing to a greater level of caution among business leaders.

This is important because as businesses lose confidence, they tend to cut back on discretionary spending activity like replacing aging equipment, expanding facilities or adding new jobs. At the same time, businesses tend to pare back on the amount of inventory held in storerooms, putting downward pressure on factory orders and manufacturing activity. Indeed, recent surveys of corporate executives suggest plans to curb capital expenditure and hiring activity in the coming year as corporate earnings growth are expected to slow.[2]

[2] Duke Fuqua School of Business, “Duke CFO Global Business Outlook”, September 2019

Figure 3: Economic growth forecasts downwardly revised

A slowdown is coming, consumers may hold the key

Recession or not, economists have ratcheted down their expectations of global growth and largely expect economic activity to weaken in 2020. Most notably, the International Monetary Fund in October 2019 published revisions to its World Economic Outlook that suggest global GDP growth will slow to levels not seen since the 2008-2009 global financial crisis. And while slower economic growth does not necessarily portend a recession, it does increase an economy’s susceptibility to a downturn, particularly at a time when a few recession indicators are flashing amber.

One factor underpinning positive economic growth and arguably staving off an economic downturn has been the resilience of household spending. U.S. retail spending growth has largely surprised to the upside in 2019. And this followed a rebound in global equity markets and the prospect of falling interest rates earlier in the year, which likely buoyed household sentiment and underpinned household consumption in major economies. A key question today, however, is whether this virtuous trend in spending can continue amidst a host of uncertainties, particularly as elections and trade uncertainties loom in 2020.

Moreover, the buoyancy of consumer sentiment is likely to remain tied to developments in the business sector. As business uncertainties grow, employers are likely to further curb hiring activity. This means that the current slowing pace of job gains is likely to be exacerbated by falling sentiment, making it harder for some people to find work and leaving others worried about their own job prospects and potentially feeding into a cycle of falling discretionary spending and hiring activity.

Either way, with government spending constrained and business spending expected to slow, a decline in household spending could tip the U.S. economy into a recession, leading to a period of heightened economic and financial market volatility and challenging households’ ability to get ahead financially.

In our final post in this series, we discuss how households can get ahead, financially, despite growing financial market and economic complexities and uncertainties.

This post is an excerpt from our report, Getting Ahead Financially in 2020. You can download this report in its entirety by visiting franklinmadisonadvisors.com.

Important Disclosures

Broadview Macro Research is a division of Franklin Madison Advisors, Inc (“FMA”). The commentary provided on this website is limited to the dissemination of general information pertaining to Franklin Madison Advisors’ investment advisory services and general economic market conditions and are subject to change without notice. The information contained herein is not intended to be personal legal, investment or tax advice or a solicitation to buy or sell any security or engage in a particular investment strategy. For additional information about FMA, including fees and services, please contact FMA or refer to the Investment Adviser public disclosures.

Franklin Madison Advisors, Inc., is registered investment adviser firm with its registration and principal place of business in the Commonwealth of Pennsylvania. Registration of an investment adviser does not imply a certain level of skill or training. FMA is in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which FMA maintains clients. FMA may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Any subsequent, direct communication by FMA with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For additional information about FMA, including fees and services, please contact FMA or refer to the Investment Adviser Public disclosures. Please read the disclosure statement carefully before you invest or send money.

To learn more, visit us at http://www.franklinmadisonadvisors.com

Brace for more uncertainties in 2020

-

An undercurrent of seemingly benign financial market and political developments are poised to move both prepared and unprepared households further away from their financial goals in the coming years.

-

These issues include monetary policy-related financial market distortions, a drag from excessive global debt and the rise of geopolitical uncertainties.

-

Households attempting to financially prepare for the future will need to contend with financial market distortions that induce greater risk taking, debt constrained growth that lead to increasingly more expensive investment options and weaker economic activity and political developments that have the potential to batter financial assets.

An undercurrent of seemingly benign financial market and political developments are poised to move both prepared and unprepared households further away from their financial goals in the coming years. Contributing to this outlook includes the fact that the global economic ties that had in recent years contributed to higher standards of living for millions of people globally are at risk of unwinding with the rise of populist politics and social unrest. At the same time, policy responses are forcing some savers into riskier investments and creating unsustainable excesses in debt and equity markets.

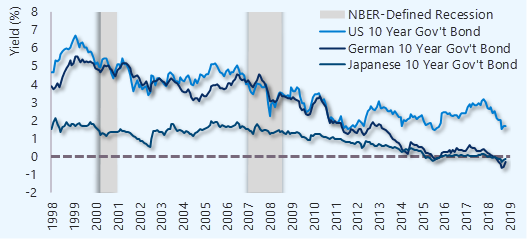

How financial market distortions make it easier to lose money

Central banks, in a bid to reverse slower economic growth and weak inflation, have maintained unconventional monetary policies since the height of the Global Financial Crisis. Doing so has nevertheless led to certain distortions in the global financial system, like extremely low interest rates (negative in places like Europe and Japan), excess liquidity in some corners of the financial system and liquidity shortages in others.

And these policies aren’t likely to go away anytime soon as gross domestic product (GDP) and inflation in the U.S., Europe, Japan and China remain weak, prompting policymakers to remain committed to unconventional monetary policies for the long term.

Figure 1: Major government bond yields remain in decline

This has two important implications for both savers and retirees when it comes to asset accumulation and distribution strategies. First, lower central bank interest rates have put downward pressure on traditional fixed income asset yields. What this means is that individuals and institutions setting aside funds to meet long term obligations will either need to put away more money today to boost saving levels or allocate their savings to high yielding (and often riskier) financial assets to generate higher investment growth rates.

There is no such thing as a free lunch and so the cost associated with higher returns is either the increased time need for more investment due diligence on riskier assets or the need for greater investor risk tolerance for inevitable swings in market prices. Either way, these central bank policies have effectively made it easier for unprepared savers to lose money by incentivizing higher allocations riskier investments.

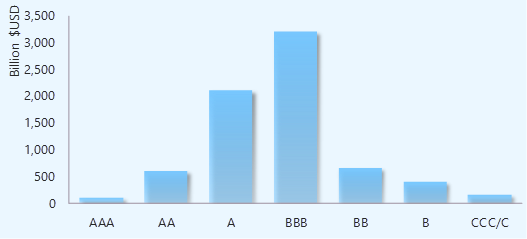

Figure 2: A notch above junk: BBB rated corporate bonds a key market risk

At the same time, the number of firms rated as financially risky has increased as lower borrowing costs provide a support to otherwise structurally uncompetitive firms. Typically, rising interest rates late in the business cycle has the natural effect of weeding out weak firms as revenues typical with selling goods and services dry up and increased borrowing becomes prohibitive. Yet, lower rated firms have been given an artificial lifeline as central banks maintain extremely accommodative policies, keeping borrowing costs lower than usual.

Further, lower rates have pushed up valuations of riskier investments like stocks even as corporate earnings growth has weakened recently. The implications here is that valuations for some stocks and bonds, particularly those of lower quality issues, may become susceptible to outsized price swings when political or economic concerns inevitably lead to bouts of increased market volatility. Lower interest rates have also contributed to a notable rise in the amount of debt outstanding globally.

Figure 3: A rise in global debt will challenge growth for years to come

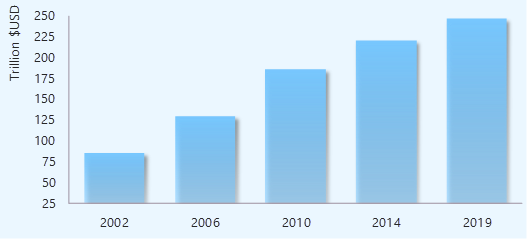

Debt and when a rising tide does not lift all ships

According to the Institute for International Finance, total public and private debt outstanding globally was $246 trillion at the start of 2019, which is 50% higher compared to a decade ago and nearly three times the annual output of the global economy. At some point this debt must be paid back, which becomes increasingly problematic and a rising source of financial market volatility when economic growth rates for major global economies are expected to remain subdued in the near term.

Closer to home, the cost to service debt is actually below where they were prior to the Great Recession in the U.S. Yet, lower interest rates have created an incentive for households to borrow more money, pushing up the value of non-financial assets like home prices and contributed to the ballooning cost of education, crowding out other discretionary spending and in some cases making important life transitions harder to attain.

And while lower interest rates have reduced government debt service costs, Washington has only increased debt-fueled deficit spending and hindering its ability to invest in important growth-oriented infrastructure projects. Taken together, what this means is that households and governments alike increasingly remain constrained in their ability to spend on growth-oriented ventures as balance sheets remain hampered by ballooning debt piles.

Therefore, potential economic growth rates (and rates of corporate earnings growth) are likely to remain subdued in the coming year, further challenging firms’ ability to service growing stockpiles of debt and potentially leading savers to buy investments at a time when asset prices are becoming more expensive and economic and market risks are increasing.

Figure 4: A rise in global policy uncertainties has challenged growth

Reasons to be worried: geopolitics and Main Street uncertainty

And if low interest rates and a debt overhang didn’t already complicate financial strategies for preparing for the future, a rise in geopolitical tensions has contributed to a rise in economic and financial market concerns. This comes as the U.S.’s Trade War with Canada, Mexico, the European Union and China has led to higher prices paid for goods by some households and a simultaneous decline in business confidence. What’s more, the unclear outcome of the 2020 U.S. presidential election is likely to intensify political uncertainties that markets, businesses and households have already contended with in the past year.

From a trade policy perspective, leaders on both sides of the political aisle remain energized to address economic issues caused by past trade policies, particularly as it relates to the U.S.’s seemingly unbalanced relationship with China. And so, the implication here is that while a partial trade deal between the U.S. and China may be secured at some point, tensions between the U.S. and China are likely to remain elevated for years to come irrespective of the 2020 election outcome.

Meanwhile, some U.S. presidential candidates have proposed tax and spend policies that are likely unfavorable for some families and complicate long-term estate planning considerations. Moreover, financial markets – abhorring uncertainty – are likely to become increasingly choppy heading into the 2020 U.S. elections as the potential for notable shifts in trade or economic policies brought about by shifts in the executive or legislative branches are likely to buffet risk asset prices and dampen near term business and consumer confidence.

Taken together, households attempting to financially prepare for the future will need to contend with financial market distortions that induce greater risk taking, debt constrained growth that lead to increasingly more expensive investment options and weaker economic activity and political developments that have the potential to batter financial assets.

Above all, these developments have the potential to raise the risks of a U.S. recession which we cover in our next post.

This post is an excerpt from our report, Getting Ahead Financially in 2020. You can download this report in its entirety by visiting franklinmadisonadvisors.com.

Important Disclosures

Broadview Macro Research is a division of Franklin Madison Advisors, Inc (“FMA”). The commentary provided on this website is limited to the dissemination of general information pertaining to Franklin Madison Advisors’ investment advisory services and general economic market conditions and are subject to change without notice. The information contained herein is not intended to be personal legal, investment or tax advice or a solicitation to buy or sell any security or engage in a particular investment strategy. For additional information about FMA, including fees and services, please contact FMA or refer to the Investment Adviser public disclosures.

Franklin Madison Advisors, Inc., is registered investment adviser firm with its registration and principal place of business in the Commonwealth of Pennsylvania. Registration of an investment adviser does not imply a certain level of skill or training. FMA is in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which FMA maintains clients. FMA may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Any subsequent, direct communication by FMA with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For additional information about FMA, including fees and services, please contact FMA or refer to the Investment Adviser Public disclosures. Please read the disclosure statement carefully before you invest or send money.

To learn more, visit us at http://www.franklinmadisonadvisors.com

Adjusting to Seismic Shifts

In the blink of an eye the coronavirus has fundamentally changed our world in more ways than we can imagine. While it seems like an eternity ago, it only has been a matter of days since Pennsylvania Governor Tom Wolf issued his first stay-at-home order for a few counties in the state.

This week, the Governor expanded his order to all counties throughout the Commonwealth and for a period of at least 30 days. In recent weeks, many states have enacted their own stay-at-home measures being it necessary to mitigate the spread of the COVID-19 virus. Unprecedented times call for unprecedented measures.

It is needless to say that from a financial perspective, social distancing and self-isolation have created a seismic shift in the economy, in financial markets and in many people’s personal financial plans. Data this week showed that over 6 million people applied for unemployment benefits adding to last week’s catastrophic 3.2 million initial jobless claims.

Figure 1: A 50-fold increase in jobless claims

And to put this number into perspective, the 4-week average just prior to the virus outbreak was sitting at around 200,000 initial claims. That’s a fifty-fold increase in less than two weeks and at no time in post-war history have we seen so many people lose their jobs in such short order.

And so it goes: most people today know someone that has been fundamentally affected – whether it’s in their physical or mental health, finances or otherwise – by the coronavirus outbreak. Without a doubt the unexpected event has fundamentally changed the plans that nearly every single American has laid out for themselves this year and for years to come.

While a number of measures are underway to mitigate the financial fallout from the pandemic, many households and business owners are still struggling to grasp the gravity of the changes underway. With that said, during this time of change, we believe that the best way to rebound from a financial setback is by setting yourself up with a plan to navigate a world that has just gone through a seismic shift.

Government loosens its purse strings

So, what exactly has the government done to address the economic and financial fallout from social distancing measures? Well, in response to and anticipation of further virus mitigation efforts, the government has taken unprecedent actions to shore up the economy. For instance, on March 27, Congress passed the Coronavirus Aid, Relief, and Economic Security (or CARES) Act. This fiscal stimulus package provides more than $2 trillion in aid to individuals and businesses of all sizes and across the United States.

Such a dollar amount is certainly hard to grasp on its own, but in comparison to past stimulus measures, the CARES package is more than twice the size of the American Recovery and Reinvestment Act passed during the Obama administration back in 2009. In terms of what went into the CARES package, there are a number of items geared to help households and businesses. These measures include:

Figure 2: The government will borrow $2 trillion to support households and businesses

Overall, about a quarter of the money from this package will go directly to households, 40% will go to help businesses and roughly a third of the money will go to state and local governments and health and education institutions.

Fed pulls out all the stops

Now on the monetary side, the Federal Reserve has pulled out all the stops to support the proper functioning of the financial system and carry out its dual mandate of price stability and full employment. Put a different way, the Fed today is doing everything it can to support the financial system (and the economy) like it did back in 2008. In reality, under Jay Powell, the Fed is doing much more than it did a decade ago when Ben Bernanke was at the helm.

To this point, early last year the Fed signaled that it would stop raising interest rates, and pivot away from tightening monetary policy and toward easing as economic growth back then started to show signs of fraying. What’s more, in September, the Federal Reserve restarted its asset purchase program after certain events exposed issues in the Treasury market. At that time, the central bank had begun purchasing assets at a rate of $10-20 billion per month.

In March of this year, the Federal Open Market Committee (FOMC) surprised markets when it cut its target policy rate to around zero percent. What this means is that the Federal Reserve wants interest rates to go back to the same level that they were during the height of the Global Financial Crisis a decade ago.

Figure 3: Fed Assets Up Over $2 Trillion in Less Than 7 Months

Also last month, the Fed committed to purchasing corporate and local government debt, it increased the rate of its asset purchases up to $90 billion per day and committed to adding an unlimited amount of assets to its balance sheet for an indefinite period of time. Taken together, the actions from the Fed signal a willingness to get ahead of what is likely to be a very serious downturn in the U.S. economy.

A “V” shaped recovery not likely in the cards

So how do these measures relate to economic expectations? Well, a national poll released on Friday showed that less than half of respondents surveyed believe that the economy will return to normal by the month of June. What this suggests is that the majority of a sample of the American population do not believe that the economy will recover quickly and that the effects of the coronavirus will linger for longer than many policymakers are communicating to the public.

To be sure, we’ve been writing about the fact that global pandemics historically have come in three waves, each with their own recovery period. And so how does this apply today? Well, not only are we right now dealing with the first phase of the outbreak here in the U.S., there are now signs that the outbreak has returned to Asia where – until recently – many countries had thought they contained the coronavirus.

What this means is that social distancing measures in the U.S. are likely to remain in place for longer than most people expect. This also means that businesses may not reopen as quickly as some people anticipate and it means that more workers will likely remain unemployed for longer.

Figure 4: “V” Shaped Recoveries Tend to be Shorter Than “U” Shaped Recoveries

From this perspective, it’s possible that the U.S. and global economy will experience a prolonged “U” shaped rebound and not a “V” shaped recovery as hoped by many economy watchers. Indeed, this view is held by researchers at PIMCO, a widely known asset management firm, who estimate that stability in economic growth could take as long as 12 months to form.

We believe that the reason it could take longer for the economy to recover is because the virus will take longer to contain. And, until a vaccine or significant level of immunity is developed across the global population, the deadly effects of the virus will continue to hamper economic growth. The result is that many firms will simply not be able to restart operations as quickly as some people had hoped.

Adding insult to injury, we have yet to see whether the current fiscal and monetary support packages will be enough to mitigate a broad swath of corporate bond defaults that are now waiting in the wings. To be clear, there is a group of companies that for years have been sitting on the cusp of bankruptcy, if not for the support of the Fed’s money printing operations.

Figure 5: More than 50% of Investment Grade Debt is One Notch Above Junk

What this means is that, in addition to the COVID-19 related risks, the economy and financial markets could get yet another shock from a backlog of ailing companies now filing for bankruptcy protection. In such a scenario, it’s hard for us to see how household spending and business investment could rebound in short order without a sudden drop in new coronavirus cases globally.

"Nimble thought can jump both sea and land."

William Shakespeare

Setting up for a rebound

In terms of how we should be relating to these financially important events, it’s our belief that people should look for the silver linings whenever possible. Without a doubt the spread of the coronavirus has derailed life and financial plans for many people. While the devastation is unique and personal to each one of us, it is also worth noting that the current events provide a unique opportunity to stop and reassess. That is, to take a hard look at what’s really important in each one of our lives.

Illness has a way of naturally slowing us down and forcing us to reevaluate our current life priorities. Sometimes we get so fixated on a goal, or an outcome in our lives, that we lose sight of the really important things that are going on around us. And from a financial perspective, what may have been a priority or an important goal just a few weeks ago may no longer matter as much in light of the current circumstance. In other ways, the current developments may have taken away people and opportunities that have left us feeling lost and disorientated.

“…in life it doesn’t matter what happened to you or where you came from. It matters what you do with what happens and what you’ve been given.”

Ryan Holiday

In his book, “The Obstacle is the Way”, author Ryan Holiday tells us that, “…in life it doesn’t matter what happened to you or where you came from. It matters what you do with what happens and what you’ve been given.” From this perspective, we believe that the best way to rebound from a financial setback is by setting yourself up with a plan to navigate a world that has just gone through a seismic shift.

A Dutch proverb tells us that “he who is outside his door already has a hard part of his journey behind him.” Therefore, whatever the case may be regarding our financial circumstances, one of the most important things that we can do in the coming weeks and months is to simply do something about our financial circumstances.

This can begin by simply reprioritizing expenses to shore up emergency cash reserves to holistically reevaluating financial priorities, taking stock of resources and developing a plan to align financial resources with a new set of life goals. Whatever the case may be, we believe that one key to getting ahead in life financially in the coming weeks, months and years is to take action today.