Take these 5 Back-to-the-Basics Steps when Markets Move Against You

Market volatility can have a way of derailing your best-laid investment strategy. So, what can you do to reduce risk when markets move against you? Stay invested and get back to the basics. As with most life situations, when circumstances put up roadblocks to your goals, your first response may be to double down on your current approach instinctively. However, doing more of what you already have done may not only deplete your resources, it may also exacerbate an already untenable situation.

That's why when markets start moving against you, one of the best things you can do from an investment perspective is to focus on the essentials. While it may be tempting to get out of the markets altogether, fine-tuning some components of your investment strategy could otherwise set you up for long-term success. These steps include evaluating your exposure to market risk, focusing on higher-quality investments, reducing leverage, and diversifying your portfolio. To be sure, taking these actions may enable you to stay in the game for the long-run and improve your odds of achieving your financial goals.

Source: Broadview Macro Research

Step 1: Evaluate Your Market Risk Exposure

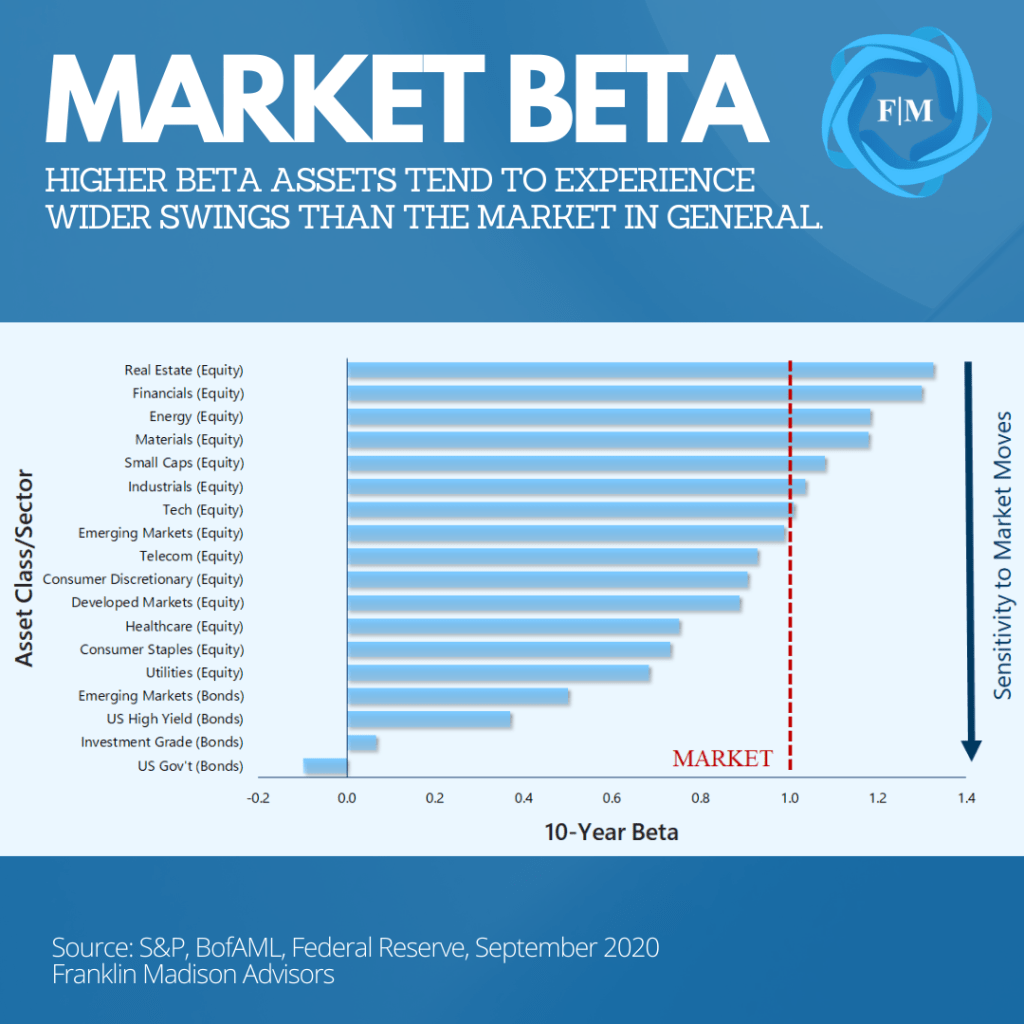

The first essential step you should take when markets start moving against you is to evaluate your exposure to market risk. Beta is one way to quantify this risk, and reducing exposure to it may help you better navigate sharp market swings. Why? Investments with high beta tend to experience outsized moves relative to the broader market when risk assets rally or decline. So, what is beta?

Well, beta is a statistical representation of the movements between a security and a broad measure of the financial markets, like the S&P 500 index. A positive value suggests that a security might move in tandem with the broader markets. Assets with a negative beta tend to move in the opposite direction of the broader markets, while a zero beta suggests little affect in its price relative to the broader markets. And which assets are more prone to move with sharp swings in the markets? Let's look at an example.

History tells us that cyclically oriented equity sectors, like financials, energy, and materials, tend to follow the broader market's moves higher (and lower). On the other hand, fixed income assets like Investment Grade and US Government bonds are less inclined to follow the direction of the broader markets and, in some cases, move in the opposite direction.

Beta is particularly useful when uncertainty rises, and your priority is to reduce the level of swings within your investment portfolio. Holding too many high-beta securities can leave your savings exposed to unnecessary risks and increases the likelihood that you'll fall short of your financial goals when risk assets suddenly decline in value. That's why when market volatility picks up, identifying an appropriate mix of high- and low-beta investments in your portfolio may be vital to reducing investment risk, particularly as you near your savings goals.

Source: Broadview Macro Research

Step 2: Move Up in Credit Quality

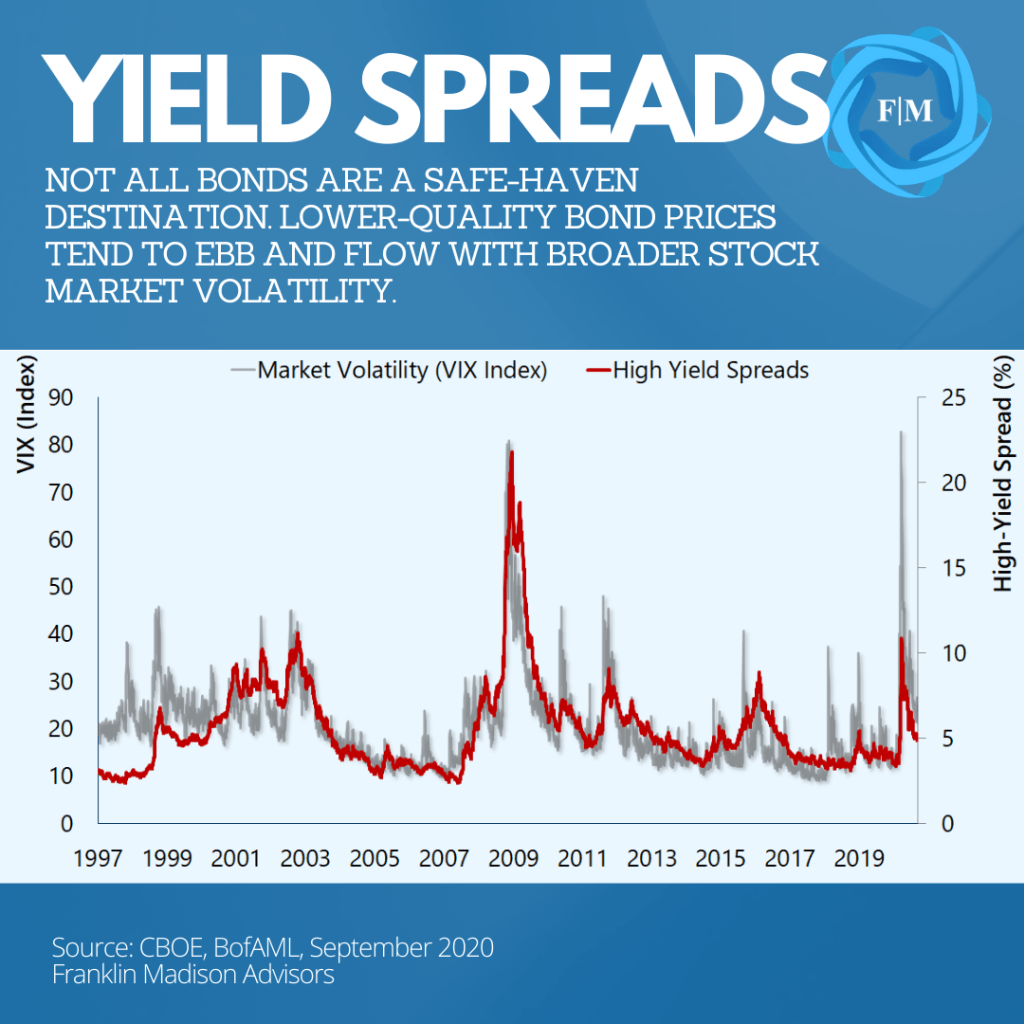

The next step you should take in getting back to investing basics is evaluating your bond exposure and consider moving up in credit quality. Assuming that merely having exposure to bonds in your investment portfolio is a way to hedge against volatility could be a recipe for disappointment. To be sure, not all bonds offer safety from market swings.

This point is evident in how yield spreads of low-quality bonds tend to rise during periods of heightened market volatility. Historical data show that when the VIX (a measure of market volatility) rises, the price of lower quality bonds falls, and yields move higher relative to higher-rated fixed-income assets, like government bonds.

In fact, history has shown that the spread between high yield and US government bonds can widen by as much as 20% during periods of heightened market volatility. For example, during the market selloff in early 2020, spreads went from less than 4% in January to 11% in March. Such price behavior not only reflects lower risk appetite among market participants, but it also represents a desire among some investors for higher compensation to take on additional risk. This is notably the case for assets that may have a higher degree of financial uncertainty when economic conditions underpinning the securities deteriorate.

As noted earlier, higher beta fixed income assets, like high yield bonds and emerging market debt, tend to move in the same direction as risk assets, like stocks. Indeed, while bonds might be perceived as a more conservative investment, the truth is that certain cash flow, industry, or country characteristics can make them higher-risk investments and susceptible to market ebbs and flows. That's why if you've been using bonds as a way to gain additional yield in your portfolio, you may want to consider higher quality and lower beta fixed-income assets as a way to reduce investment risk.

Source: Broadview Macro Research

Step 3: Consider Cheaper Stock Alternatives

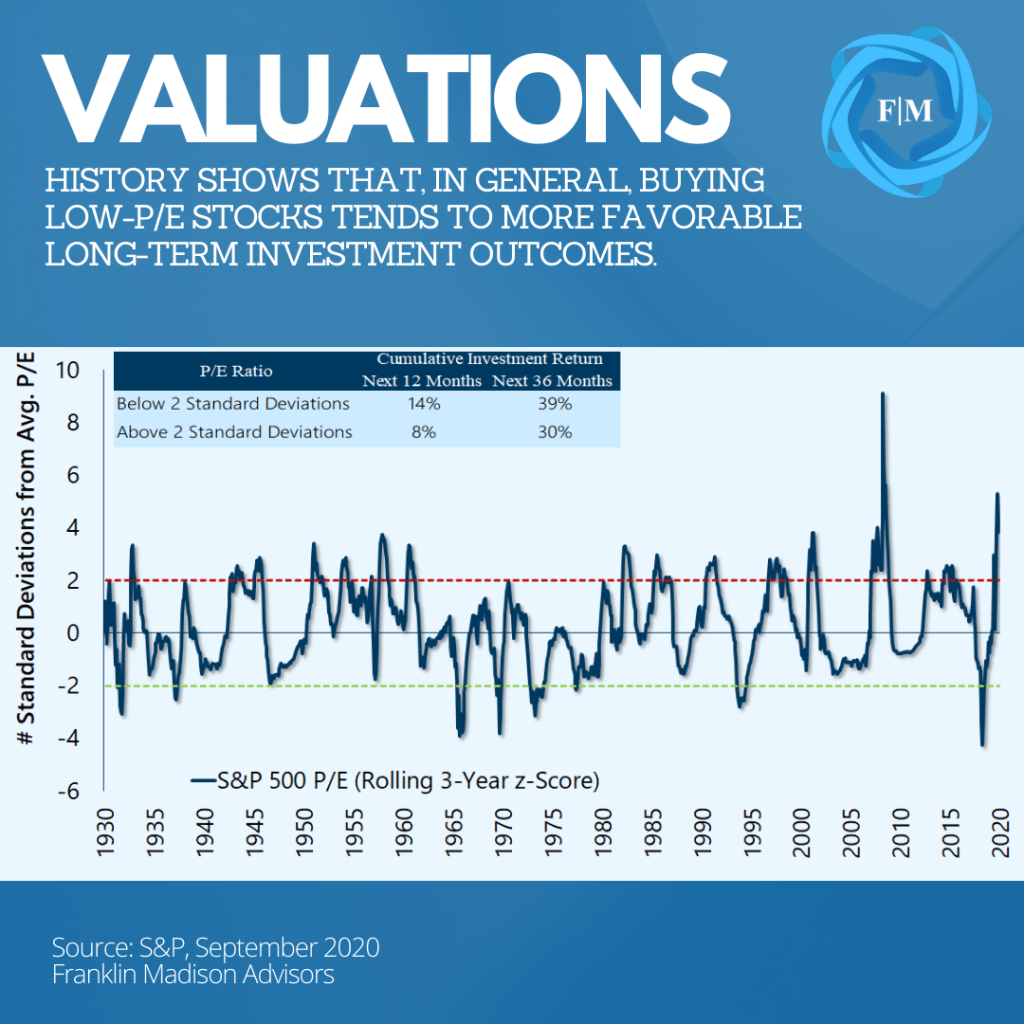

After you've evaluated risk exposure and the credit quality of your bonds, the next thing you might want to think about during a market pullback is whether you're paying too much for stocks. It might go without saying that buying low and selling high is vital to long-term investing success. And while momentum, or recent price action can be an informative value indicator, you may want to consider valuation factors like price-to-earnings (P/E) ratios to determine whether you're paying too much for a given asset.

Why do valuations matter? While it's true that even some high P/E growth stocks can provide investors with positive returns, history suggests that lower P/Es are often associated with more favorable investment outcomes. To evaluate how well this relationship holds, we looked at the historical relationship between P/E ratios for the S&P 500 and subsequent returns over a one-year period. What did we find?

Well, with data going back to the 1930s, our work shows that if you held a portfolio tracking the S&P 500 index when its P/E ratio fell two standard deviations below its mean, you could have received an average annual return of 14%. And how does this compare with purchasing a similar basket of stocks when P/E's are excessively high? Well, buying stocks when they're expensive generated an average 8% returns in the following one-year period.

While our analysis shows that buying high P/E stocks also produced positive returns, the simple truth is that lower P/E stocks tend to outperform over time. The point here is that when the market begins to move against you, one way to set yourself up for a favorable investment outcome is to consider cheaper stock alternatives than what you may already be holding. This includes keeping an eye on high quality, low valuation opportunities.

Source: Broadview Macro Research

Step 4: Reduce Portfolio Leverage

For some investors, trending market behavior presents an opportunity to use borrowed money to boost investment returns. This strategy can work well when prices are moving higher but can amplify losses during a pullback. That's why when markets start moving against you, another critical factor to consider is reducing leverage in your portfolio. Let's take a closer look at how this works.

Leverage usually involves opening a margin account with your brokerage firm, depositing 50% of the value you wish to borrow (this is called initial margin), and hoping that the asset you purchased continues to appreciate. Simple enough, right?

Well, while the value of your portfolio may rise and fall with the markets, the loan you received typically stays fixed. What's more, your broker will also require that your levered investment maintain an equity-to-debt ratio above a certain threshold (maintenance margin). This approach might work well as markets head higher, but when they fall, a time might come when you'll need to raise cash to bring your equity position above the maintenance margin requirement or sell some of your stock to make your broker whole.

And it goes without saying that being forced to sell during a downturn to cover a margin call can amplify losses. That's why overseeing leveraged positions and avoiding a margin call is crucial to managing investment risk during uncertain times. To help illustrate the point, consider the performance of two portfolios that bought on margin heading into a market downturn.

Example: Margin and a Downturn

Let's say that you decide to invest $100,000 into ABC company using $70,000 cash, and $30,000 borrowed from your broker. In this situation, we'd say that your portfolio is 30% leveraged. After initially gaining in value, your portfolio experiences a 40% drawdown over two weeks. While your portfolio avoided a margin call, your net return after accounting for the loan is -48%. To put this number into context, the loss on an all-cash portfolio during this time could be -33%.

And how would this situation look if you had borrowed more money from the start? Well, let's assume that you use $100,000 to purchase the same security, this time with 50% of your broker's money. During the same market downturn, your net return after accounting for the margin loan declines -67%. This two-thirds decline is amplified by a broker's margin call, theoretically leaving you with a more significant hole to climb out of.

The key takeaway here is that if you're using leverage to gain an investing edge, then one of the first steps you should take when the markets are moving against you is to evaluate your use of margin. While this resource can undoubtedly help boost returns when markets are trending higher, it can also open you up for excessive losses during periods of heightened market volatility.

Step 5: Diversify Your Portfolio

A final but crucial step to reducing investment risk during times of uncertainty is to diversify. Diversification can help smooth out investment returns and, more importantly, lessen volatility when the markets begin to move against you. Why is diversification important?

Well, few individuals can predict with certainty which investments will perform well in any given year. In fact, history has shown that an outperforming sector or asset class one year often loses favor with market participants the following year.

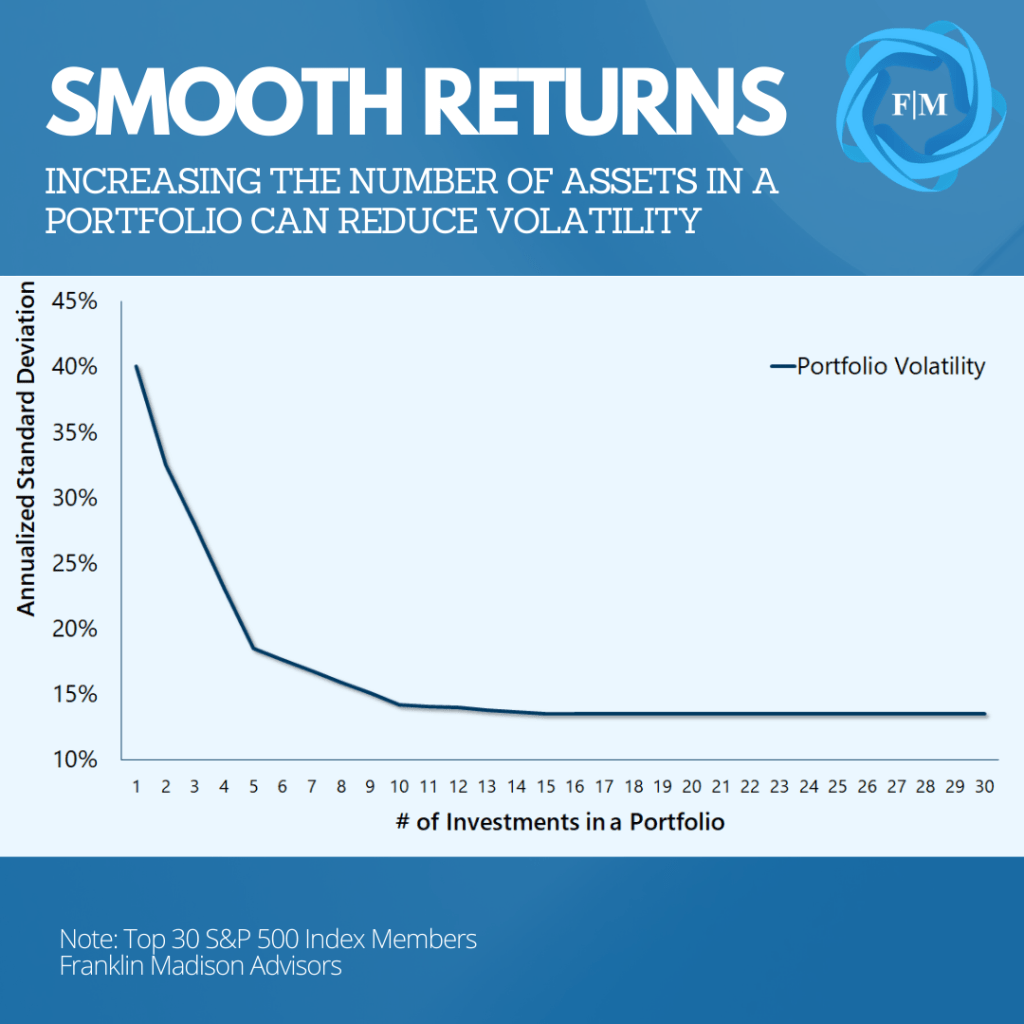

For example, if you held one of the largest names in the S&P 500 index, what you're likely to have experienced over the past few decades is annualized volatility as high as 40%. Put differently, while your stock might have an average return of 10% in a given year, that value could swing between a 30% loss, a 50% gain from one year to the next.

This varying performance can be problematic if you're near a critical savings goal and is how diversification comes help. A simple analysis shows that combining just five stocks from the S&P 500 index could cut your portfolio volatility in half from 40% to 18%. In fact, adding 30 stocks to your portfolio might reduce volatility by two-thirds.

The point here is that diversifying your portfolio lets you gain exposure to market returns without having to pick a winner while taking excessive risk rather than trying guess which investment might do well from one year to the next. When paired up with assets of varying correlations, diversification has historically demonstrated its ability to reduce volatility and smooth out portfolio returns.

Get Back to Investing Basics When Markets Move Against You

As with most life situations, when circumstances put up roadblocks to accomplishing your goals, your first response may instinctively be to double down on your approach as a way to achieve success. Doing more of what you already have done, however, may not only deplete your resources, it may also even exacerbate an already untenable situation.

That's why when markets start moving against you, one of the best things you can do from an investment perspective is to focus on the essentials. While it may be tempting to get out of the markets altogether, shifting your investment strategy could be a better set up. These steps include evaluating your exposure to market risk, focusing on higher-quality investments, reducing leverage, and diversifying your portfolio. Taking these actions may enable you to weather a downturn, stay in the game for the long-run, and improve your odds of achieving financial success.

These Two Techniques May Help You Avoid Gambling with Your Financial Future

How certain are you that you'll achieve your crucial financial goals? Even if you've had the most basic experience preparing for the long-term, you likely know that having the right financial target in mind for retirement, financial independence, or a big-ticket purchase is vital to a successful planning outcome. But did you know that basing your financial allocation decisions on a static, unchanging view of the world might leave you gambling with your financial future?

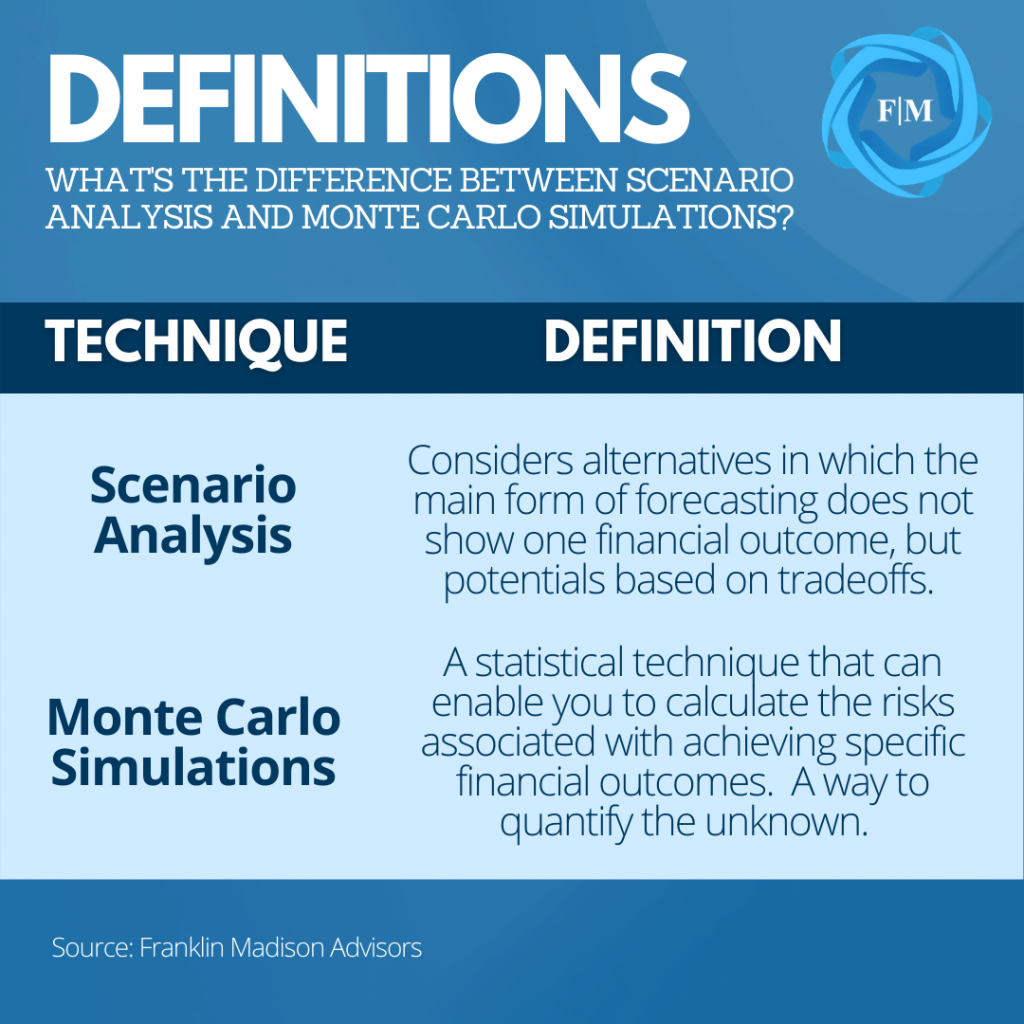

Indeed, understanding how your financial target may rise or fall based on shifting financial and economic conditions or varying lifestyle preferences is vital to the success of achieving your long-term goals. So, how can you sift through these varying factors and identify the right savings target for you? That's where two techniques – scenario analysis and Monte Carlo simulations – play critical roles. Rather than coming up with one fixed solution, you can use these tools to choose from a host of possible outcomes, enabling you to make more informed planning decisions and likely increase your chances of success as you prepare for the future.

Scenario Analysis: Evaluating Tradeoffs

A savings discipline, a modest rate of return, and time can help you achieve your financial goals. Simple enough, right? Well, how can you be sure that you're not saving enough (or too much) if your financial needs rise or fall in the future? What if your financial priorities change? And how can you be sure that your assumed modest rate of return will help you reach your savings goal? Incorporating scenario analysis and Monte Carlo simulations into your financial planning process can help you tackle these and similar questions. Let's take a look at each in a little more detail.

A scenario analysis acknowledges that no one perfect answer exists to fulfill a given set of desired planning outcomes. Indeed, identifying one result to meet your financial goals would be the most straightforward approach. Even so, every savings decision will have its own unique set of costs and benefits. An example here may help illustrate this point.

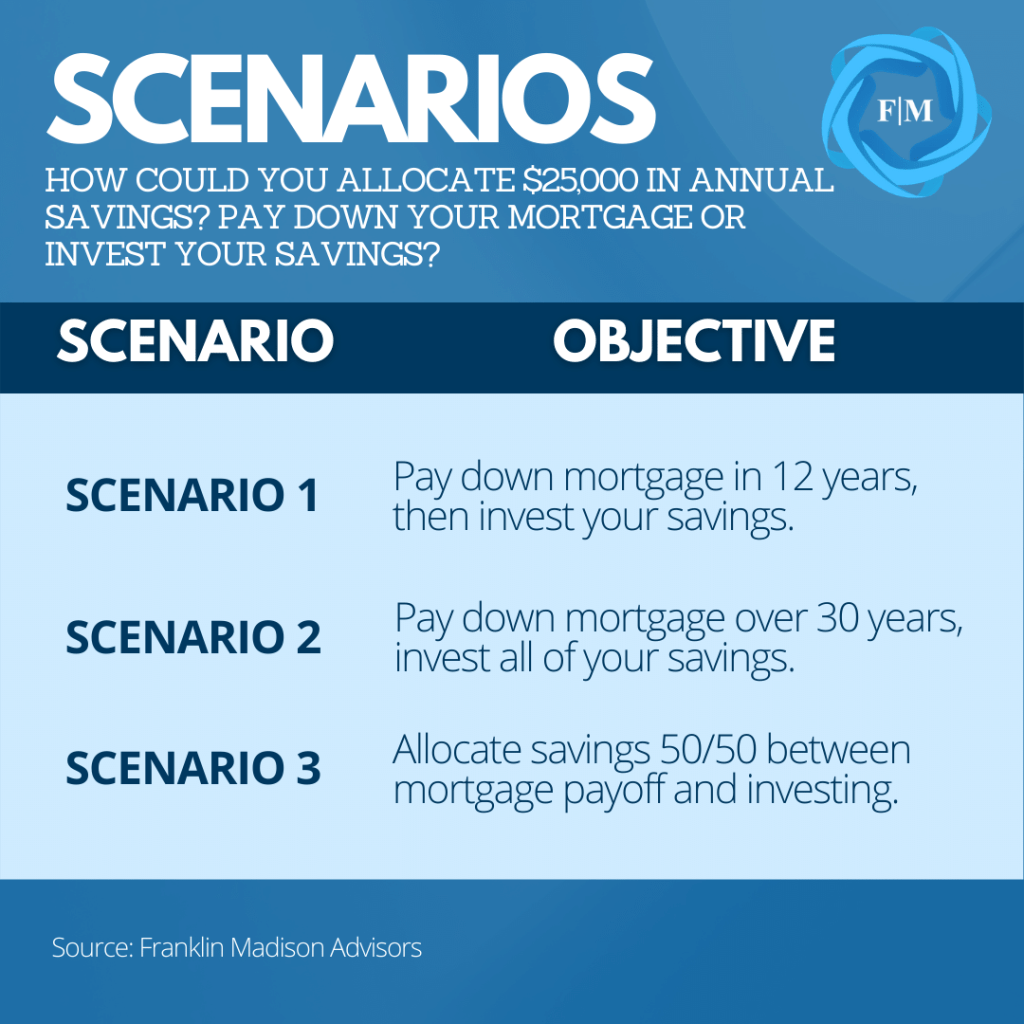

Assume that you can save $25,000 per year. Maybe you'd like to use this money to pay down your $500,000 mortgage, but you'd also like to accumulate $500,000 for a big-ticket purchase in 20 years. We can evaluate the tradeoffs between paying down the mortgage and building up savings from a scenario analysis approach. So, should you pay down the mortgage first or concentrate your efforts on investing your savings? Let's take a look at what would happen if you paid down your mortgage first.

Source: Broadview Macro Research

Scenario Analysis Example

Assuming that you have 30 years left on your mortgage and you use all of your annual $25,000 savings to make additional principal payments, you might be able to pay off your mortgage in 12 years and reduce your lifetime mortgage interest by $230,000. With your house paid off in 12 years, you could then apply what would have been regular mortgage payments to your extra savings. Invested over 8 years with a 5% return, your savings could grow to $529,000. So far, so good, right? Now let's consider an alternative.

What would this situation look like if you invested $25,000 over 20 years instead of waiting to pay off your mortgage? Assuming that you achieved your investment return rate consistently over this period, you'd likely have accumulated $826,000 for your big-ticket purchase. Even if we consider the opportunity cost associated with mortgage interest savings, your savings' end value is notably higher than in the first scenario. Here, you could surmise that you'd be better off investing your savings from the start. Such a conclusion, however, misses a crucial point.

While building savings is vital, paying down your mortgage as you move toward financial independence might still be an essential lifestyle value to consider when allocating your financial resources. Is there a way to have the best of both worlds? One compromise between the two alternatives is to apply half your savings toward investing and the other toward paying down your mortgage. What's the result? Well, at the end of 20 years, not only have you paid off your mortgage, but you're likely to have also accumulated $552,000 for your big-ticket purchase.

These three situations illustrate how scenario analysis can help you evaluate tradeoffs between two or more competing financial priorities. This iterative process is extremely useful in assessing the cost and benefit of selecting an ideal outcome to come up with an optimal solution for prioritizing your financial resources. Even so, one crucial factor to consider is that your simple growth rate may not account for market volatility. To address such uncertainties, you'll likely want to incorporate Monte Carlo simulations into your process to ensure that your plan stays on the right track.

Source: Broadview Macro Research

Monte Carlo Simulations: Evaluating Risks

So, what exactly is a Monte Carlo simulation? Simply put, it's a statistical technique that may enable you to calculate the risks associated with achieving specific financial outcomes. In other words, it's a way to quantify the unknown.

Earlier, we showed several scenarios in which you might grow $25,000 to $500,000 in 20 years using a 5% return rate. But how certain can you be that you'll receive precisely 5% per year, mainly if your return is based on investing in financial markets that vary in performance from one year to the next? In other words, how can you ensure that you're saving the right amount to account for a potential savings shortfall in any given year? Monte Carlo simulations can help.

Indeed, a Monte Carlo simulation is a computer model that, given a set of assumptions – like risk and return – produces thousands of random return observations within the parameters specified. The process not only tells you what might happen, but it also gives you a way of quantifying the likelihood of your desired outcome. Let's demonstrate how this works with our previous mortgage payoff, big-ticket purchase example.

Monte Carlo in Practice

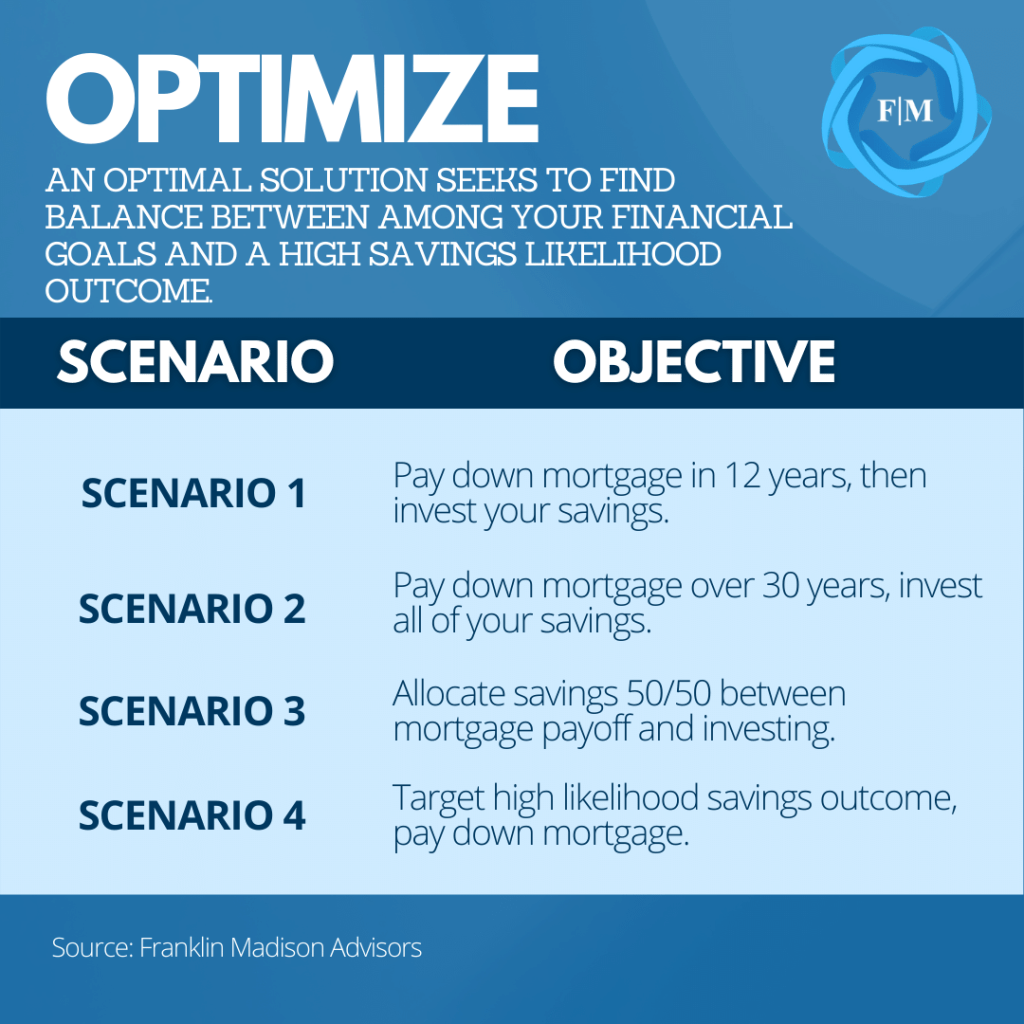

You'll recall that the three scenarios aimed to answer how to apply annual savings of $25,000 best: 1) pay off your mortgage first, then invest 2) invest all of your savings from the start or 3) a 50/50 split between mortgage payoff and investment savings. Each of these outcomes exceeded the $500,000 threshold we set for a big-ticket purchase through investment growth. Even so, what's the probability that each of these outcomes will occur?

In the first scenario, while savings are projected to grow to $529,000, our Monte Carlo simulations tell us that there's only a 60% chance that your savings will be higher than your $500,000 threshold. How so? It all comes down to volatility. In fact, over a third of the 10,000 simulated investment portfolios fall short of this goal, ranging in value between $400,000 to $500,000. How did the other two portfolios perform?

In the third scenario, an even split of savings between mortgage payoff and investment savings over 20 years led to only a marginally higher probability of meeting or exceeding the savings benchmark. However, the Monte Carlo simulations for the second scenario, where we committed all savings to investments, showed a 95% likelihood of achieving or exceeding the $500,000 savings threshold. While a positive solution, you have to consider a critical point: is this the most optimal outcome? Put differently, the mortgage still hasn't been paid off. Let's see how the combination of scenario analysis and Monte Carlo simulations can help.

Source: Broadview Macro Research

Optimal Outcome: Combined Monte Carlo Analysis

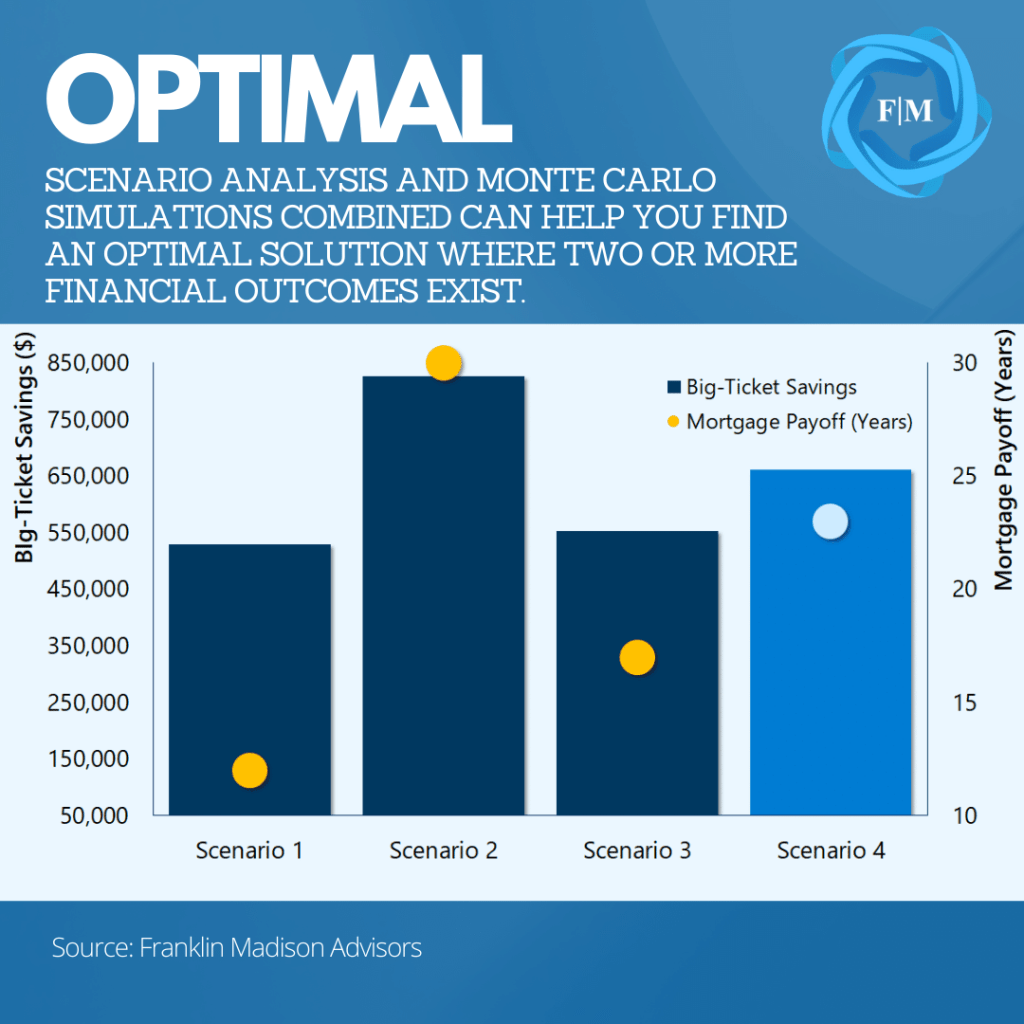

Each of the three scenarios discussed has its benefits and drawbacks. Pay off a mortgage sooner and accept a lower likelihood of achieving your savings goal, or up your savings goal and pay off your debt as scheduled. Let's consider a fourth alternative: optimize. Here, our goal is to optimize cash flows to find a balance between paying down your mortgage and accumulating savings with a higher success rate of reaching its threshold. How exactly?

First, we ask the Monte Carlo simulation to identify a value that meets or exceeds our threshold with an 80% certainty level. After another 10,000 iterations, the software tells us that the target value should be $661,000. When we run this figure through our scenario analysis again, we find that the split between saving and debt payoff changes to 80/20 from 50/50 savings vs. mortgage payments in scenario 3. And while you won't pay off your mortgage in 12 years as in scenario 1, this new outcome may shave seven years off of your payments and save you about $90,000 in lifetime mortgage interest expenses.

At this point, you might be asking yourself, why not go for 100% certainty that you'll achieve the $500,000 threshold? Remember, your goal here is to achieve an "optimal", not "maximum" outcome. Increasing your probability might lead to saving more money than you need.

To be sure, Monte Carlo simulations aim to help you evaluate the tradeoff between how much risk you're willing to take to achieve to reach a given effect. Considering all four scenarios, the analysis as a whole tells us that if you're willing to accept that the probability of your big-ticket savings outcome is somewhere around 80%, you could allocate more savings while still eliminating your debt sooner. At the end of the day, it really comes down to evaluating which tradeoffs are more important to you.

Are You Gambling with Your Financial Future?

The Monte Carlo method gets its name from a popular casino in Monaco. The irony of its name is that this technique can actually help you increase your odds of financial success when paired with a concrete scenario analysis framework.

Indeed, if you have two or more financial objectives that you're trying to evaluate then using a Monte Carlo Analysis is one way to help you find an optimal balance between your lifestyle needs and financial goals. More importantly, however, if you're not using a disciplined, quantitatively-based process to assess the likelihood of reaching your financial goals, then you might be gambling with your financial future.

Has the US Dollar Lost its Dominant Reserve Currency Status?

Is US dollar dominance poised to end, and what might it mean for your finances? Uncertainties surrounding US dollar strength have been top-of-mind for some individuals for many years and for a good reason. A significant decline in our nation's currency could lead to higher prices for the goods and services you consume and make it more expensive to borrow money for big-ticket purchases like a house or a new car.

Today, there is a sensible argument to be made for a diminished worth of the US dollar. Ballooning government borrowing, massive central bank money printing, and the decline of US geopolitical influence suggest to some that the end of the dollar's global dominance may have finally come. Some individuals even point to a near-term rise in gold prices and a falling exchange rate as evidence for such a move.

That being said, the dollar's role is more nuanced than such simple near-term explanations would presume. For now, evidence suggests that the dollar's prominence is likely to remain in place for many years to come. Even so, the growing importance of the euro and Chinese yuan over the long-term could reduce the world's dependence on the dollar. So, what does this mean for your money? A structurally weaker US dollar might lead to higher future living costs and is a vital reason why your savings should account for rising inflation.

Making Sense of Foreign Exchange Market Moves

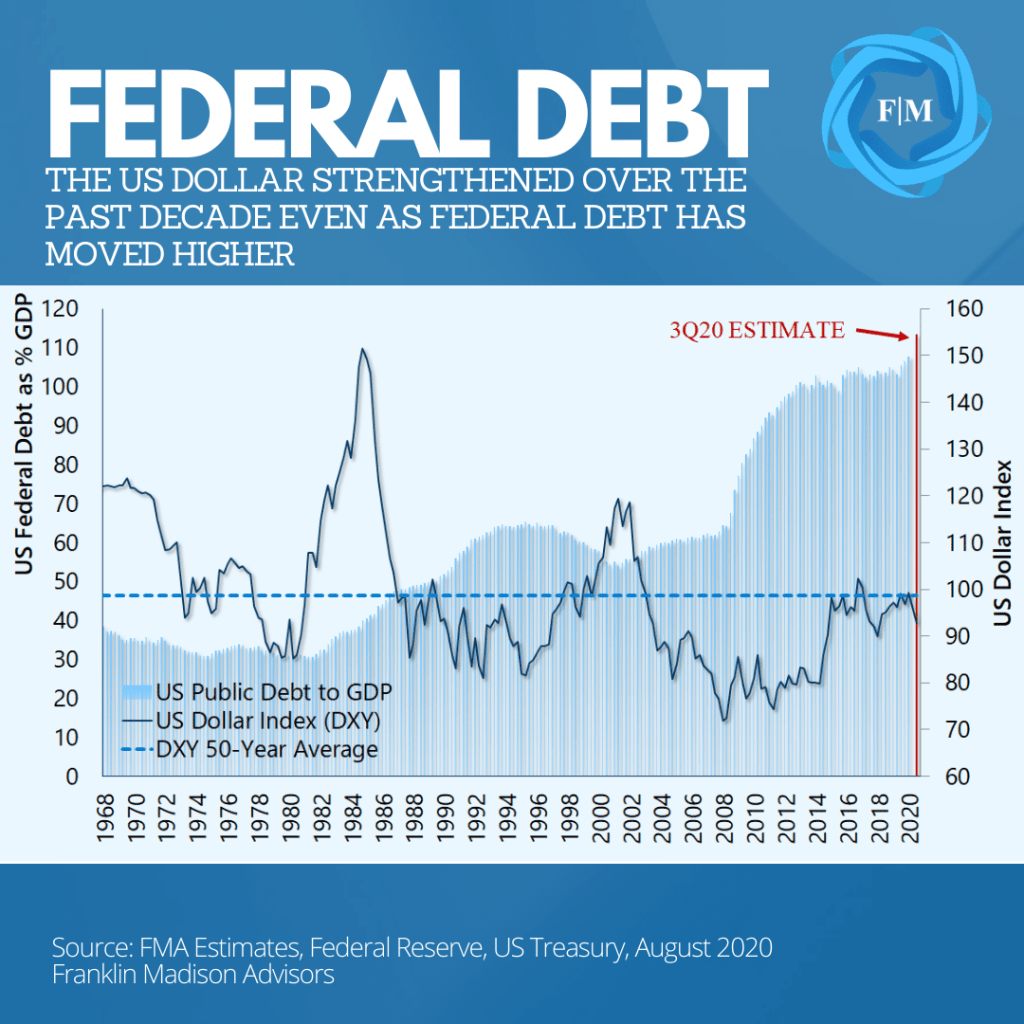

Is the US dollar in decline? One indicator that some individuals use to signal a fall in the dollar is recent foreign exchange market activity. Between March and August of 2020, the dollar, as measured by the US Dollar Index, lost 9% of its value. At the same time, gold prices pushed past record highs. And these combined moves might suggest that something ominous is happening with the US dollar. While it's tempting to extrapolate near-term developments into the future, let's look at what history has to say about the dollar's movements.

From a purely data-driven perspective, history has shown that periods of US dollar weakness are often preceded by strength, especially during crisis times. In the months leading up to its March 2020 highs, the US dollar rose in value versus its key global trading partners. This move occurred as individuals and institutions piled into perceived safe have US assets as coronavirus uncertainties weighed on the global economic outlook.

Certainly, during times of financial stress and economic uncertainties, the US dollar is often sought after as a globally secure destination to park savings. This ebb and flow in value is not unique to 2020. In fact, it is evident in prior crises, like in March 2009, amidst the Great Recession and during the popping of the Tech Bubble in 2001. In fact, after appreciating in 2008 and early-2009, the US dollar gave up 13% of its value in the five months following stock market lows in March. And in 2001, even with the events surrounding September 11, the dollar trimmed 4% of its value during the year.

The point here is that a dollar decline today might coincide with legitimate concerns about massive fiscal and monetary spending. Even so, correlation should not be confused with causation. Instead, one way to look at the recent dollar moves is from the perspective of a safe-haven currency. When economic and geopolitical uncertainties rise, there is greater demand for the safety of the US dollar. Today, it can be argued that movements in the foreign exchange market reflect less demand for US dollars as global market participants look past economic uncertainties.

What Makes a Global Reserve Currency?

If we presume that dollar fluctuations in foreign exchange markets are consistent with near-term risk-on/risk-off trends, what then can we make of the US dollar's role as a preeminent reserve currency? In other words, why wouldn't market participants look to the euro or Chinese yuan as dollar-alternatives during times of uncertainty? In its simplest form, there are generally three factors that make a currency a dominant global reserve: 1) it's used to settle foreign financial obligations, 2) a means to pay for international trade, and 3) as a store of value.

Settling Foreign Obligations (Liquidity)

It's often assumed that central banks print money out of thin air. The fact is that financial institutions are primarily responsible for affecting money supply in circulation. This occurs as banks take in deposits and issue loans. One factor that has propelled the dollar into its global reserve status is how financial institutions outside of the US have issued US dollar-based loans. We refer to these dollar-based foreign obligations as Eurodollars.

While the term was originally coined to represent dollar-based borrowing in a post-World War II Europe, today it applies to US dollar-based obligations in other parts of the world. Experience tells us that interest is often paid back to a lender on top of the principal owed when we borrow money.

Foreign individuals and firms earning money outside of the US might need to convert their own local currencies in exchange for US dollars to make their lenders whole. And by some estimates, today there well over $10 trillion is Eurodollar deposits outside of the $18 trillion in the US financial system. Taken together with loans issued by the International Monetary Fund, the World Bank and Asian Development Bank the dollar is a key source of liquidity for the global financial system.

Use to Settle Global Trade (Size)

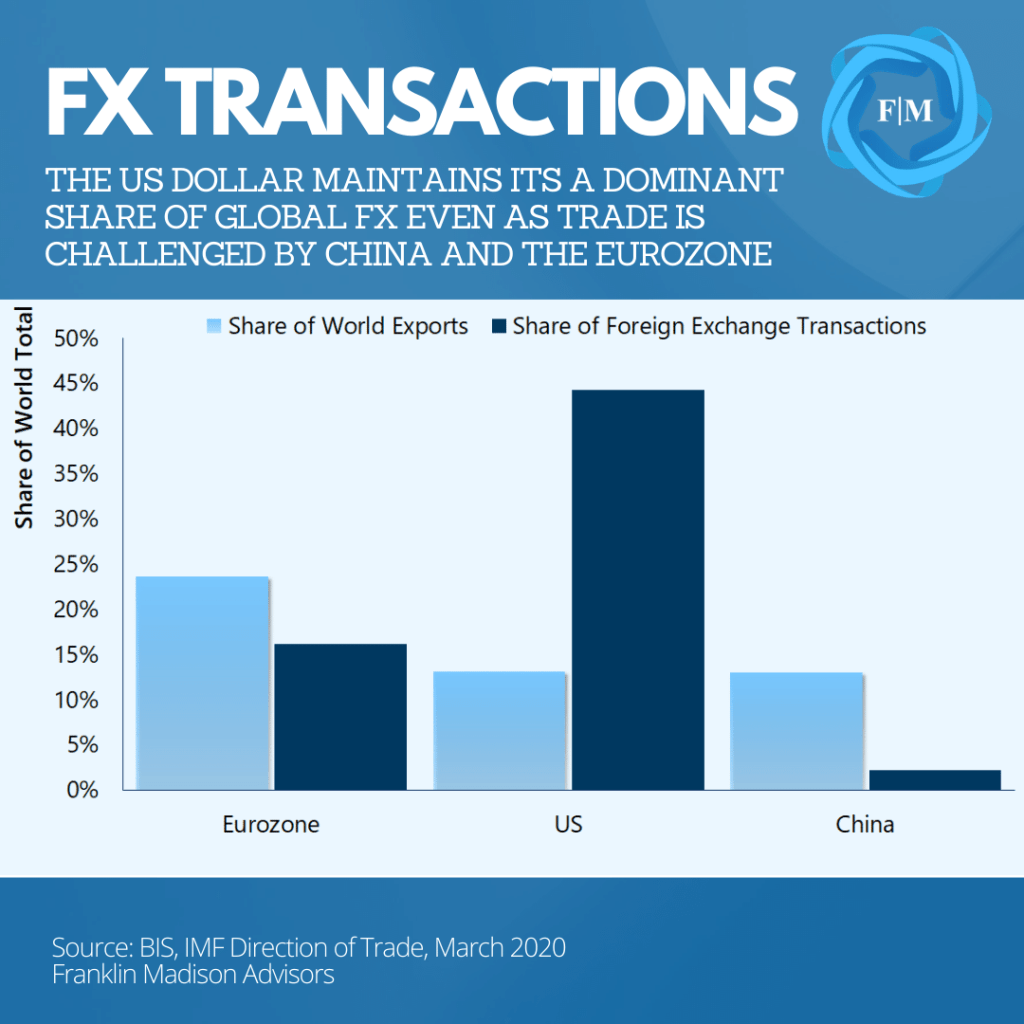

Another factor that distinguishes a global reserve currency is its use to settle trade in international goods and services. In the post-War era, the US was a dominant leader in global trade, given the fact that it was essentially the last major economy standing. In the decades since the Eurozone has become one of the world's largest trading powerhouses and China has risen in prominence as an essential exporter of global goods. Even so, data continue to show that the lion's share of world trade is settled in US dollars.

According to data from the Bank for International Settlements, foreign exchange transactions in US dollars were nearly three times higher than the euro. Indeed, even as China has risen to be a key leader in terms of global trade volumes, the use of the yuan in foreign exchange markets remains a mere fraction compared to the US dollar’s use.

Looking beyond manufactured goods, essential commodity items like gold, oil, and soybeans contracts are largely priced and settled in US dollars. The point here is that buyers and sellers of goods and services globally affect millions of transactions that follow through foreign exchange markets every year and remain overwhelmingly reliant on the US dollar.

Store of Wealth (Stability)

A third factor that makes a global reserve currency is in its perceived ability to store wealth. Put differently, holders of a currency must have a strong belief that its value will remain generally stable over time. Strength in a country's economy, government, and monetary system all contribute to the collective perception of stability underpinning a country's currency.

And despite a number of developments over the past decade, the fundamental factors underpinning the US economy, its government institutions, and monetary system remain on solid footing compared to other global alternatives. To be sure, it's this stability in growth and governance that has led to demand foreign capital flows into US markets and a still outsized demand among foreign central banks for US reserve assets.

For example, US equity and debt markets account for 40% of global market capitalization. This size makes US markets the single largest and most stable investment destination for foreign investors. And while US government debt continues to rise and foreign policy changes have led to more uncertainties lately, China and Japan, remain two of the world's largest holder of US federal debt reflecting ongoing trust in US institutions.

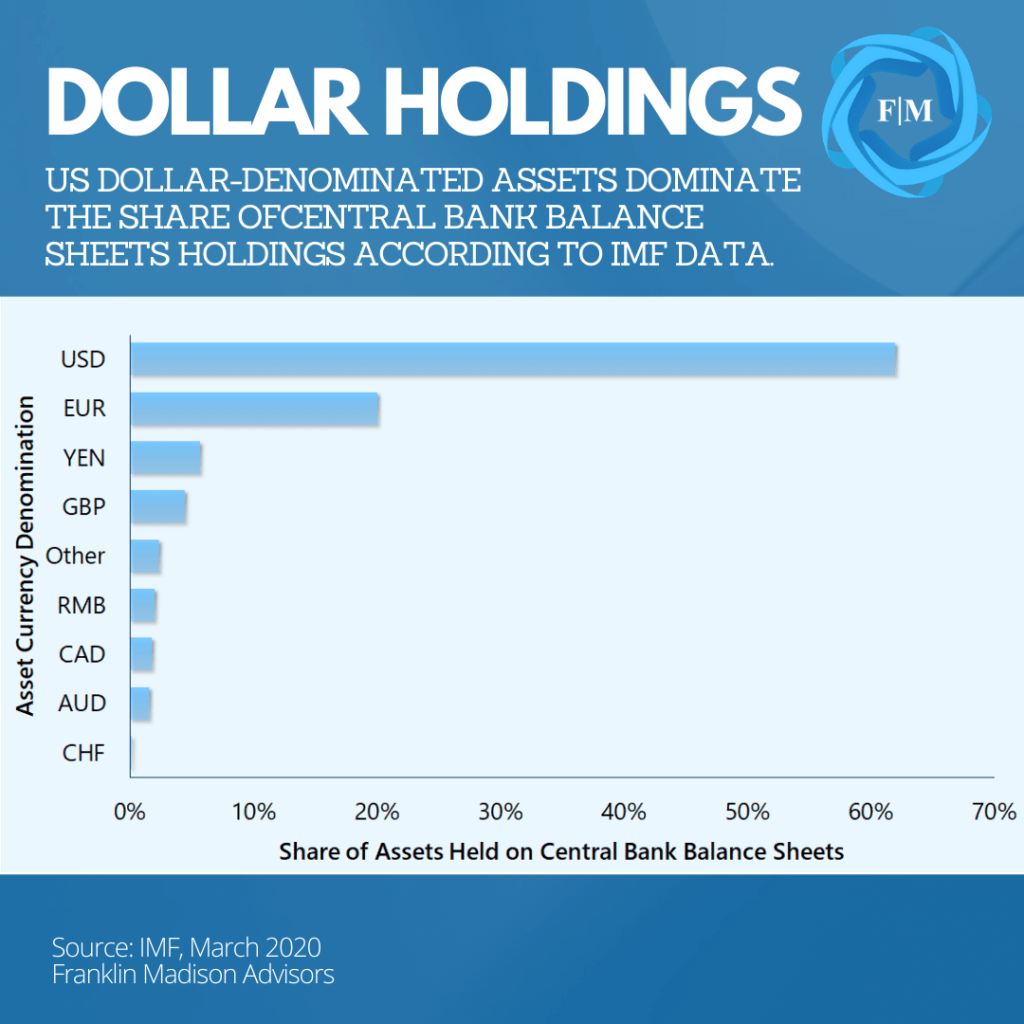

Another factor to consider is that US-dollar denominated holdings make up well over 60% of the world's central banks' assets according to data from the IMF. These assets are used by central banks to help fund obligations in their own domestic financial systems. Indeed, these assets held often reflect a need that banks or institutions in their own country might have for a particular currency. Taken together, this demand for US dollars by foreign individuals, governments, and institutions suggest ongoing faith in the US dollar.

There is No Good Alternative

So far, we've discussed factors that make the US dollar a global reserve currency. Now a key question you might be asking is what could change the US dollar's status. Well, anthropologists have pointed out that when it comes to an individual's choice to migrate from one geography to another, they not only need a desire to leave their current situation but also have a destination to move towards. From a dominant reserve currency perspective, few countries possess the size, liquidity, and stability factors to overwhelmingly support financial transactions, trade, and use as a store of value.

Now, the euro and yuan have often been pointed to as potential alternatives to the US dollar. A key question is whether they meet all three criteria of a dominant reserve currency. In terms of the euro, the currency increasingly benefits from its size and liquidity factors but suffers from uncertainties surrounding its political stability. Consider the Eurozone. It represents a subset of countries within the European Union and its currency, the euro, is largely used to facilitate trade and financial transactions.

Nevertheless, the EU itself remains a confederation of sovereign states and not a single country when compared to federalism in the US. And in recent years, the EU has experienced its fair share of political instability, including the departure of the UK (Brexit) and populism that threatened Greece's EU withdrawal. What about China?

China has undoubtedly made an effort in recent years to internationalize the yuan. It's currency's inclusion in the IMF's Special Drawing Rights basket, lending efforts across the Belt and Road Initiative, easing its peg to the US dollar, and opening up its capital markets have all been aimed at greater foreign adoption of the yuan.

And while China is the world's second-largest economy and accounts for a large portion of global trade, a foreign market for the yuan remains small and illiquid on a global relative basis. In terms of stability, President Xi Jinping's pivot away from Deng and toward Maoist ideology introduces a host of uncertainties related to the rule of law and foreign policy in China.

When it comes to finding a suitable replacement to the dollar as a preeminent reserve currency, the simple fact is that there is no good alternative right now. Until countries like China or the EU step up to address size, liquidity, and stability concerns, the US dollar is likely to remain a dominant reserve currency into the foreseeable future.

Effects of a Structurally Weaker Dollar

Up to this point, we have made a case for a generally stable role for the US dollar as it relates to its status as a dominant reserve currency. However, a moment could come in our lifetimes when the US dollar may lose this coveted status. What might this development mean for your finances?

Well, a slow transition from a dominant role to a second-run reserve currency measured over decades might have little noticeable impact for the average household. Indeed, inflation running at a 4% rate could lead to the cost of living doubling in 18 years compared to 36 years at current inflation rates. Given time, policymakers and business leaders might be able to introduce strategies and technologies that help pivot the economy in light of a changing financial environment.

Indeed, a structurally weaker US dollar could change the economics of US goods manufacturing and lead to higher levels of reshoring and job opportunities at home. At the same time, US firms doing business abroad likely would also see earnings rise as foreign currencies strengthen when US dollars are brought back home.

Sudden Currency Shock

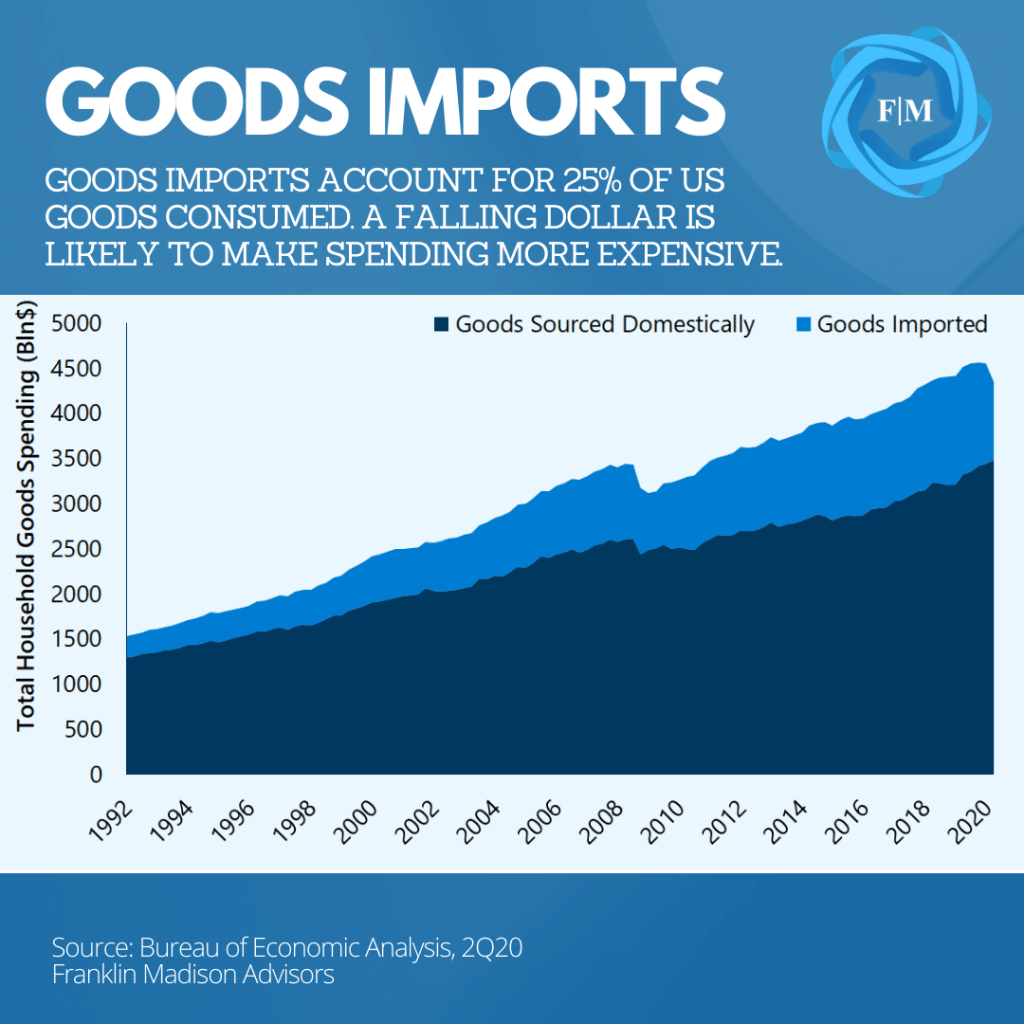

On the other hand, a sudden shock, like war or an unmitigated economic collapse, might lead to a sharp drop in the US dollar and make it more expensive for households to spend or borrow. How so? According to government data, households spent $4.3 trillion on goods at an average annualized rate during the first half of 2020. At the same time, over a quarter of the goods consumed were imported from abroad. This point is important because when the dollar falls, the cost of goods imported rises, leading to higher inflation rates. And a sudden drop in the dollar could lead to noticeably more expensive goods on store shelves.

Another thing that a weaker dollar could do is push up borrowing costs. Should confidence in the US dollar finally wane, the Federal Reserve likely would be forced to raise interest rates to incentivize foreign investors to hold dollars. And when the Fed makes changes to its interest rate policy, it can affect borrowing costs that likely would make spending more expensive.

In fact, rising interest rates might make it more expensive to borrow when it comes to purchases like a house or a new car. At the same time, higher interest rates could lead to stagnating home prices as values are typically inversely related to interest rates. Higher interest rates would also make it more expensive for local and federal governments to borrow, challenging their finances and their ability to fund essential programs like Social Security and Medicare.

The point here is that effect on your finances as it relates to a weaker dollar likely will depend on whether the dollar’s fall from grace occurs over a short or long period of time.

US Dollar Dominance Likely Here to Stay

Today, some individuals point to near-term weakness in foreign exchange markets or the rise of currency alternatives like gold or bitcoin to signal an imminent demise in the US dollar. The fact is that the world remains heavily dependent on the dollar to affect international trade, settle financial transactions, and in its use as a trusted store of value.

And while the impact of a sudden loss in reserve status might lead to higher inflation and borrowing costs, it remains likely that the dollar's fall from grace might occur over an extended period. This potential could give US leaders time to enact policies that could help mitigate the world's shifting preference toward the euro or yuan as a preferred reserve currency.

Even so, as we pointed out in a recent report, if your concern is rising inflation, then history has shown that financial assets are an optimal means for hedging against rising cost of living. Until then, the size, liquidity, and general stability of institutions supporting its use are likely to uphold the US dollar's preeminent status into the foreseeable future.

Are Emerging Markets the Right Investment for You?

Should emerging markets have a place in your investment portfolio? In today's low yield, low growth environment, some investors are looking outside of the US to generate extra returns on their savings. For some individuals, emerging markets appear attractive on the surface, given their historically robust economic growth rates and higher bond yields. Indeed, there's a strong fundamental case to be made for investing in emerging markets.

Yet the task of finding the right opportunities can seem daunting, given the overwhelming differences between markets and risks in this space. Given these issues, you might be asking yourself if emerging markets are right for you. Well, finding the right opportunities likely won't be easy. Even so, if you have a long investment time horizon, a higher tolerance for risk, and a willingness to learn more about this increasingly relevant part of the world, then investing in emerging markets might be one way to diversify your investment portfolio.

Not Your Father's Emerging Markets

Emerging markets have experienced a significant transformation over the past two decades. One simple way to think about the change is in terms of a business startup. Decades ago, many of the world's emerging markets were seen as metaphorical economic startups that produced low-cost textiles and were a source of the world's commodity exports.

Indeed, manufacturing offshoring, foreign direct investment, and exporting activity were critical to emerging market growth early on. With the help of early investors and a host of governance changes, many of these countries have today become vital influencers in the global consumer and technological marketplace.

Like a startup business, this rising success has delivered to its population higher levels of financial wealth. That's why today, a young demographic and higher levels of wealth are likely poised to spur the next leg of growth in the emerging market story.

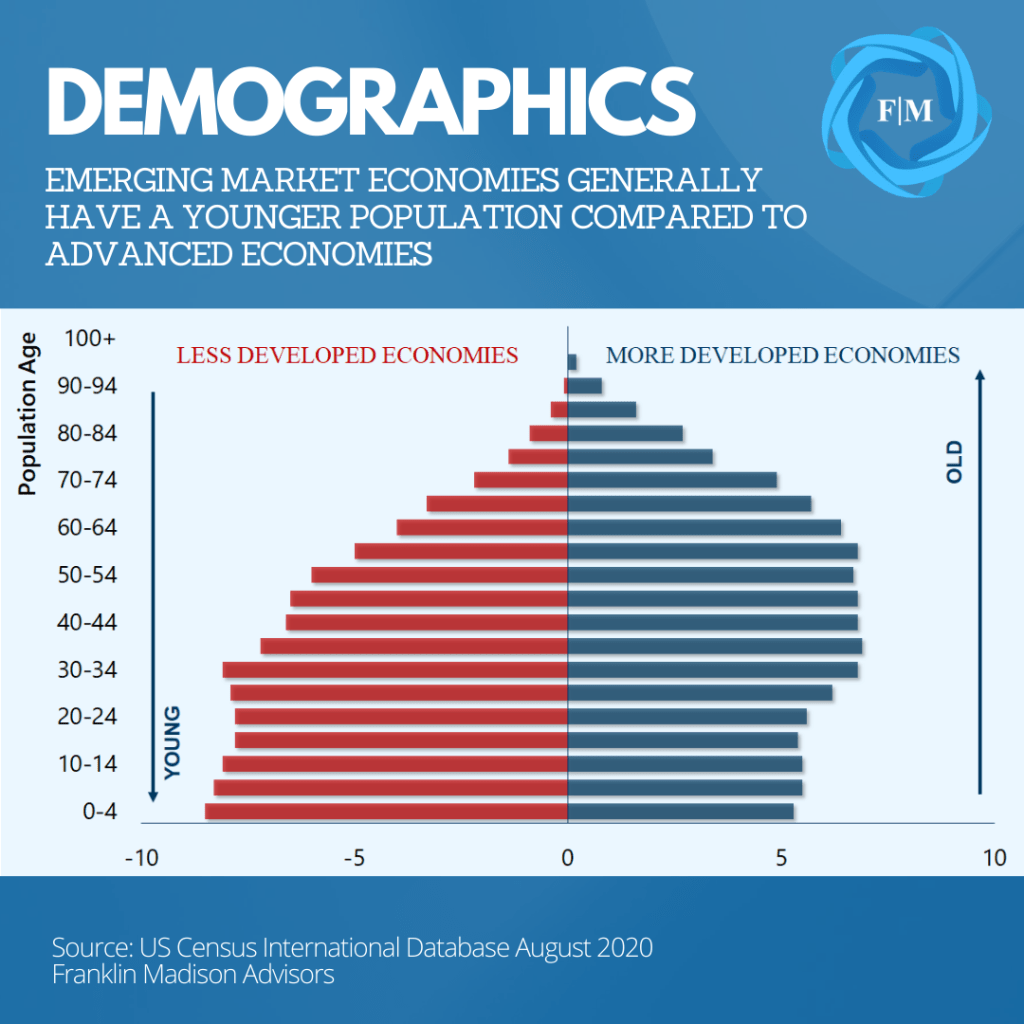

Why Demographics Matter

So why does the age of a population matter? A young, wealthy population is inclined to spend more on goods and services than one that is aging. According to the economic life cycle hypothesis, young individuals typically focus their early working years on growing earnings while they build up to a certain level of consumption on goods and services. Theoretically, these same individuals will use their savings later on in life to maintain an even-level of spending throughout retirement.

Outside of a purely theoretical framework, we can think of events like getting married, starting a family, and planning for the future as reasons why some younger individuals are more inclined to spend on goods and services than their older counterparts. This spending pattern is also one reason why consumption is likely to play an increasingly crucial role in emerging market growth over the coming years as more developed economies continue to age. How different are the demographics in emerging markets relative to more advanced economies?

Today, over 6.4 billion people live in developing economies, compare to 1.3 billion in more advanced countries. Among many emerging market populations, the median age is now in the low 30's. In India, for example, over half of its population is below the age of 30. And how does this compare to more advanced economies?

Well, in Japan, the median age is 49 years old, with only 26% of its population below 30. While the US is generally younger than Japan, only a little more than a third of the population is under 30 compared to 50% for India. And considering that India has four times as many people as the US, you can quickly see how this young, consumption-oriented growth narrative in emerging markets might be primed to accelerate.

Now, it's not enough to say that a young population can drive economic growth alone. Take Afghanistan, for example. While not an emerging market economy, this impoverished country illustrates how having one of the youngest populations is not the ticket to wealth. What's missing? A young country poised for growth needs a predictable political, legal, and investment base to provide income opportunities for its growing population. And it's these critical factors that are missing in Afghanistan but have led to rising wealth in some emerging market countries over the past twenty years.

When Reforms Lead to Structural Improvements

While we talk about emerging markets as a single unit, much of the past growth in this part of the world has been driven by Asia. For decades, countries across Asia have built up wealth by stabilizing their political environments, cutting bureaucratic red tape, and introducing predictable and enforceable rules of law.

These actions have arguably underpinned the startup phase of economic growth we mentioned earlier. And these initial efforts resulted in a rise in foreign firms establishing a local presence that brought in billions of dollars in foreign capital investment to emerging market countries.

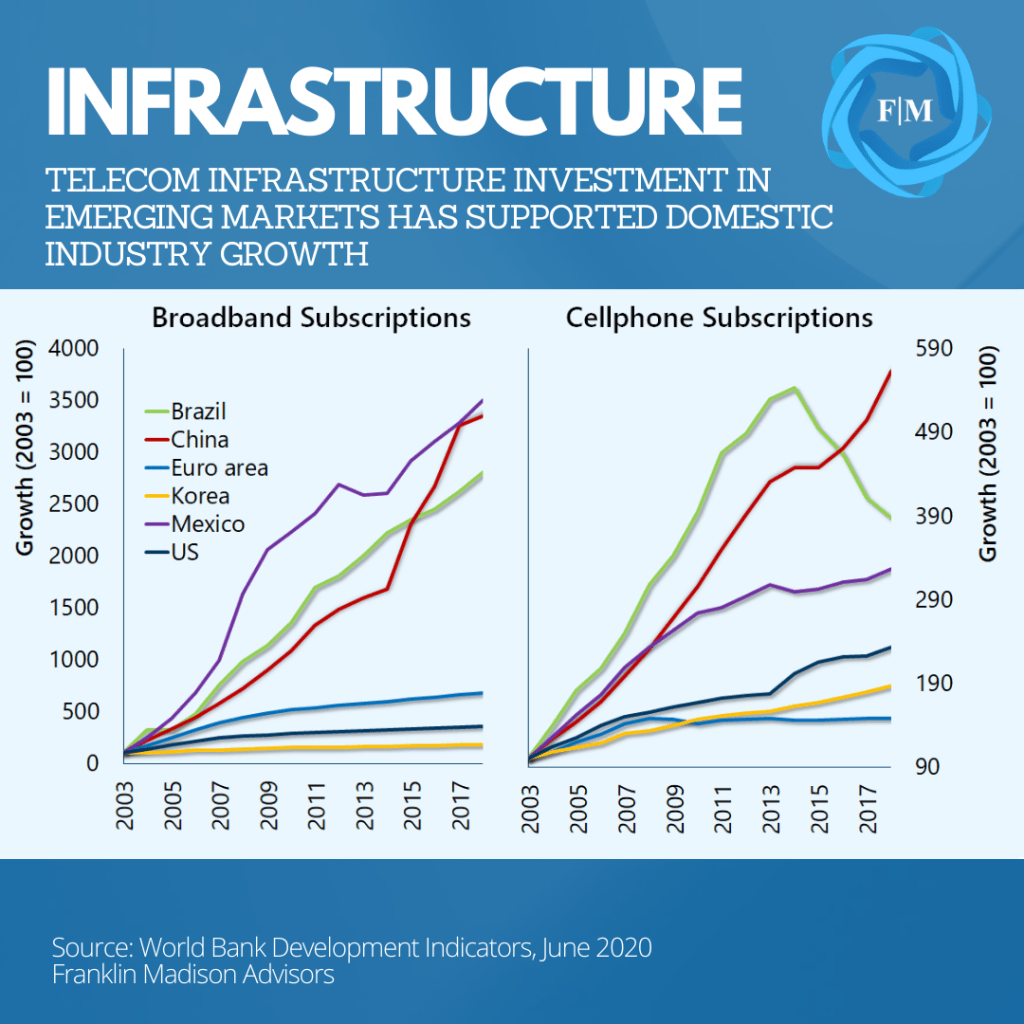

At the same time, leaders made a deliberate effort to reinvest their new-found tax base back into their local economies. These reinvestments included building infrastructure and making it easier for individuals to start small businesses that have given rise to firms that today compete on a global scale. And when we think about economic reforms in emerging markets, China is the most prominent example of this positive outcome.

Policy changes by Chinese leader Deng Xiaoping in the 1970s led to an opening up of the country's economy and ushered in a foreign investment flood. At the same time, policies enacted to reform state-owned enterprises, improving telecommunications infrastructure, and championing its private sector enabled China to create a base for its economic ascendance. And while China's development is significant, it should be noted that this growth miracle isn't isolated to China alone.

Singapore (essentially a small city-state) went from a developing country just a couple of generations ago to an essential part of the Asian economy. And today, it stands as a vital global financial center. South Korea is yet another development success story in the region.

Reforms allowed local names like Samsung, Hyundai, and others to flourish on the global stage. Today, policy changes in countries like India, Vietnam, and Thailand and efforts among ASEAN nations are paving the way for a new cohort of rising economies and increased wealth for a young population ready to spend.

Broadening Investment Opportunities

Having moved past the startup phase and well into expanding growth, firms in emerging market countries increasingly need more capital as they shift their focus from selling goods and services abroad to their own domestic markets. Funding this expansion through bank loans can be costly and is one reason why business leaders look to capital markets to issue stocks and bonds as a more affordable way to fund operations.

It’s crucial to note that foreign investors play an essential role in these markets. Continued governance improvements and other systemic reforms increasingly make emerging markets an attractive investment destination for outside investors. While some foreign investors might consider the markets small or illiquid, here are two points you should know about capital markets in these countries.

First, while the US remains the single largest financial market globally, emerging markets have become a critical part of the global investment landscape. Today, emerging market stocks represent nearly a quarter of global market capitalization compared to less than 5% at the turn of the century. What’s more, the amount of debt in these countries has risen to 25% of total global debt outstanding, with an investible universe of nearly $12 trillion in debt securities.

The second thing to consider is that investing in emerging markets isn't just about materials, industrials, or financials anymore. Rather, sectors oriented toward consumer spending, technology and healthcare are quickly taking a rising share of emerging market investment opportunities and tracking the economic transformations we've discussed.

The point here is that demographic fundamentals are driving a need for emerging market capital investment. A young and increasingly affluent population combined with growing global capital market influence is likely to broaden the set of emerging market investment opportunities available to you in the coming years.

Finding the Right Investment

Up to now, we've laid out the fundamental growth story and capital market opportunities for emerging market investors. And if you're like many investors, you're probably asking yourself how you can get started.

While it's tempting to think of emerging markets as one homogenous group, the reality is that emerging market investing is not like investing in the US. In fact, this universe comprises 27 separate countries that make up emerging markets, each with their varying composition of stocks and bonds, exposure to state-owned and private sector securities, and other factors like company size, sectors, and style. That's why it's essential to consider specific risks in this area, before diving in. Let's begin by taking a look at volatility risk.

Volatility Risk

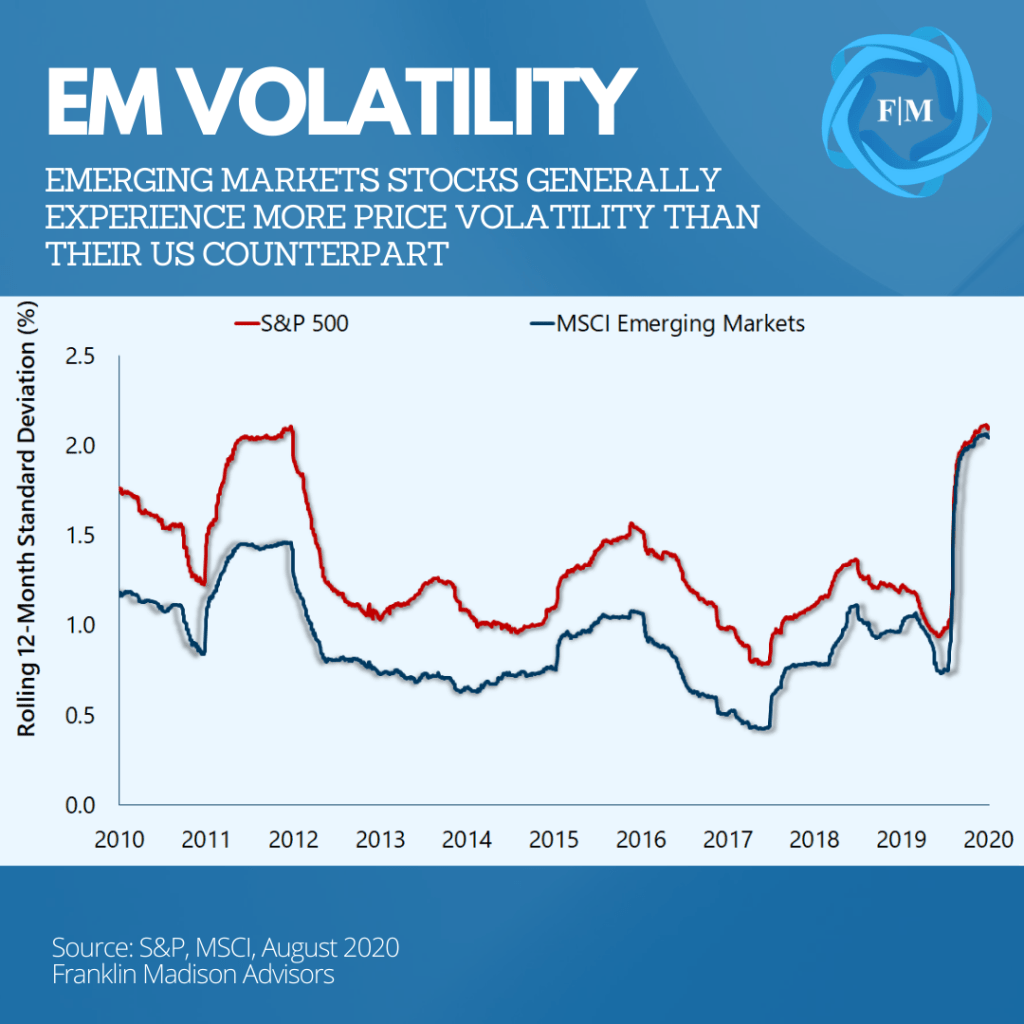

Emerging markets have a reputation for being higher risk and higher volatility for a good reason. History shows that over the past decade, emerging markets stocks have exhibited higher levels of price volatility than US stocks.

More specifically, equities making up the MSCI Emerging Markets index returned less than 1% annualized over the past ten years yet had more volatility than the large-cap US stocks. Much of this disparity can be explained by differences in regional equity performance in places like Latin America vs Asia and illustrate that higher risk does not necessarily mean higher returns at a broad level.

Liquidity Risk

Liquidity is another concern for investors in this space. Emerging markets are often influenced by risk-on/risk-off sentiment in global financial markets. In the past, some emerging market governments have welcomed capital inflows during risk-on periods, only to put in place measures to prevent hot capital outflows during times of financial stress.

While some of these liquidity and capital control issues have eased in recent years, this risk nevertheless underscores the point that investing in emerging markets should be done with a long-term view in mind.

Interest Rate Risk

Now when interest rates rise, bond prices fall. This basic fixed income concept illustrates how interest rate risk might be present in emerging markets today. Fluctuating inflation and changes in monetary policy often affect the direction of interest rates in emerging market economies.

One only needs to look at the events in Turkey in recent years to see how political and economic disruptions led to a sharp rise in its central bank policy rate and a rapid decline in bond prices.

Currency Risk

Currency risk is another factor to consider. US-based investors not only need to stay on top of emerging market developments, but they must also be aware of what's happening with the US dollar. When the dollar is weak, investment returns from emerging markets can generally be higher due to currency translation effects.

The opposite is true when the US dollar strengthens. This is notably the case with local currency-denominated debt. How so? Well, it’s because a weaker foreign currency buys fewer dollars when interest payments are brought home. Either way, staying on top of currency market developments is central to emerging market investing.

Political Risk

Finally, political risk is one of the top concerns among emerging market investors. Changes in a political regime or legislative structures within these countries can either quickly lead to economic prosperity or its reversal.

Such risks have been acutely demonstrated in Latin America, where various corruption, legal, and other political issues have created uncertainties for investors. What was the result? Well, these developments have arguably led to Latin American equities mostly underperforming the rest of its peers over the past decade and contributing to investment flat performance for emerging markets as a whole.

The takeaway here is that if you plan to get started with emerging market investing, it's not only essential to understand the narratives that can drive asset prices higher, but also the risks that can move against those opportunities as well.

Getting Educated About Emerging Markets

Navigating complex risks in an ever-changing market environment can be challenging for even the most seasoned investment professional. That's why research is a crucial component of any investing journey. And it only becomes that much harder to sift through overwhelming amounts of data and reports when you're exploring a country or region with little familiarity.

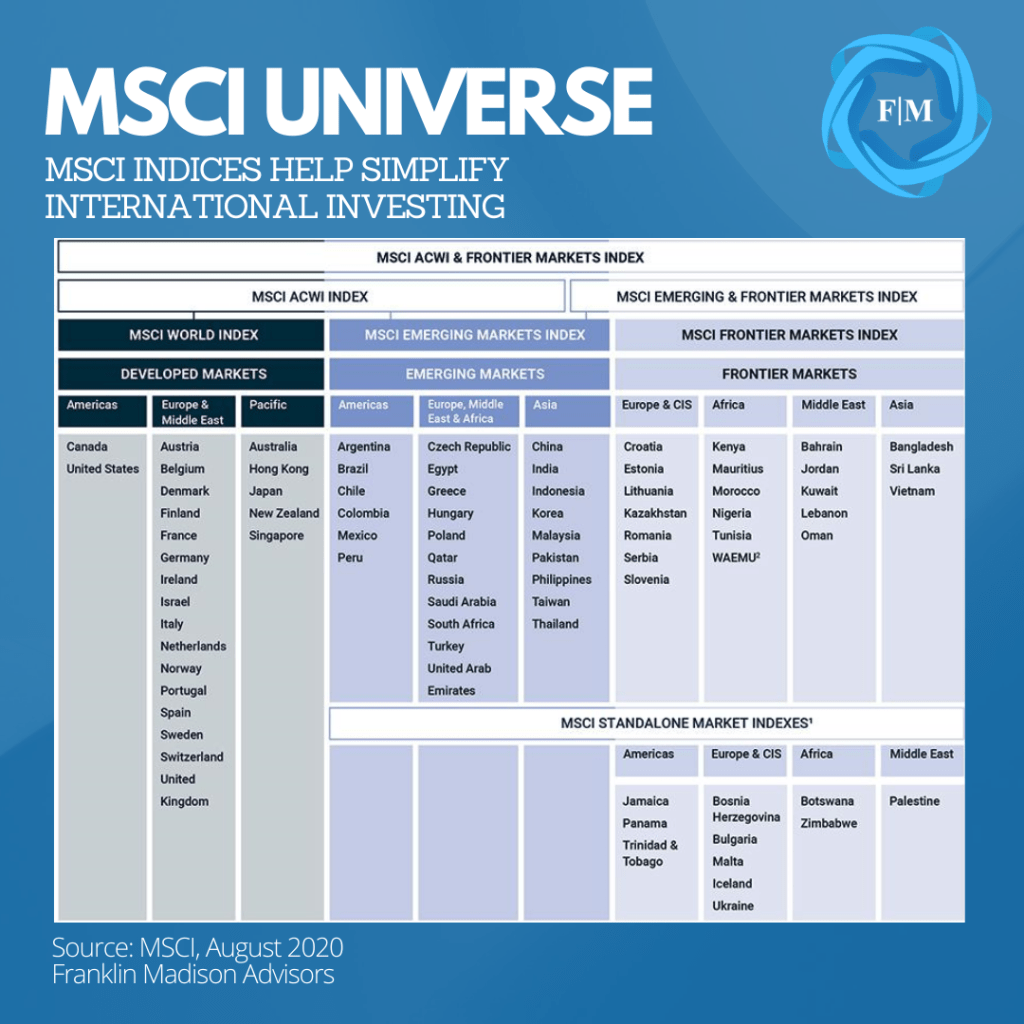

Fortunately, third-party firms have helped simplify the research and security selection process in global markets generally, and emerging markets specifically. One company central to the development of investment strategy within emerging markets is MSCI. MSCI is widely known for its stock market benchmarks. And what's essential to your research process is understanding the methodology MSCI uses to add securities to its indices.

Pages can be written about the tools, techniques, and computations used by MSCI to build its benchmarks. Even so, here are three ways using MSCI's research can help in your emerging market investment journey. First, the firm segments capital markets on many factors like capital controls (mentioned earlier) and market capitalization to differentiate between developed, emerging, and frontier markets.

Second, the indices, in many cases, represent the investible universe available to foreign investors. These factors include free float, which indicates how much of a given company's stock is liquid and available to foreign investors. This process can help take the guesswork out of knowing which firm could experience wide price swings due to low security marketability.

Finally, it's important to note that you cannot invest directly in an index. For this reason, many well-known US-based asset management firms have developed investment vehicles that follow a portfolio construction process to mimic MSCI indices. This fact can simplify the security selection process, especially when emerging market investing is not your primary vocation.

Investment research can be an onerous process. Even so, relying on robust third-party resources and tools can help you shorten the amount of time you spend identifying attractive regions and securities within the emerging market universe.

Are Emerging Markets the Right Investment for You?

Emerging markets are transitioning from being the world's producers of low-cost goods and commodity exporters to high-value, globally relevant investment destinations. These changes have brought wealth to a young population poised to spend, creating a new set of opportunities for global investors. Even with this positive backdrop, is investing in emerging markets right for you?

Well, finding the right opportunities likely won't be easy. Even so, if you have a long investment time horizon, a higher tolerance for risk, and a willingness to learn more about this increasingly relevant part of the world, then investing in emerging markets might be one way to diversify your investment portfolio.

Four Ways to Prepare for Heightened Market Volatility

Many investors know that managing volatility is central to achieving essential financial goals. But how much should you worry about volatility, and what can you do to prepare for it? Volatility represents the ups and downs of asset prices over time. And quite often it’s not the volatility that you should be worried about as it is periods of heightened market volatility.

What’s more, human expectations about the future tend to influence asset price movements. And it's during periods of changing expectations and uncertainty that asset prices swing wildly. Being aware of the narratives driving the markets and having a plan in place before they change is central to financial success. The bottom line is that if you're unprepared for periods of heightened volatility, you might be exposing your savings to unnecessary losses.

#1 Become Familiar with Volatility

Volatility is a normal part of investing. Asset prices do not move up in a straight line but tend to ebb and flow as they appreciate over time. Volatility is the price that you pay to earn a return on your investment. Indeed, what should be at the top of your list of in terms of investing concerns is not volatility itself, but periods of heightened volatility. Before diving deeper into the topic, let's explore some basic concepts.

One way to quantitatively measure volatility is through a mathematical standard deviation of an asset's return. This measure describes the historical tendency for prices to swing up or down versus their long-term average. The higher the standard deviation, the higher the volatility. This understanding is essential because the wider the swings in price returns relative to their long-term average, the less certainty you may have about future returns from one period to the next. And less certainty tends to go hand in hand with higher investment risk.

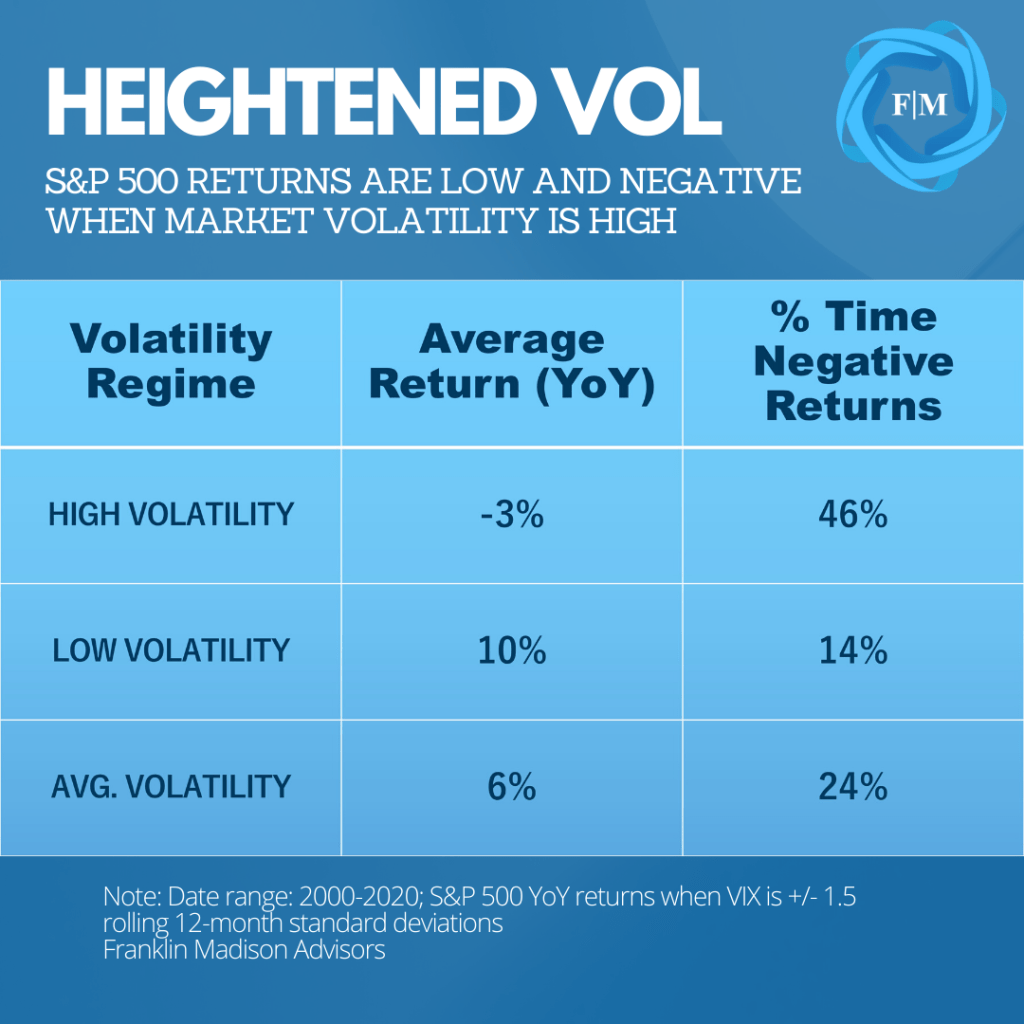

Let's look at an example. From the turn of the century, the S&P 500 index has averaged a modest yearly gain of about 5.3%. This average return, however, masks some of the sharp market moves over the past two decades. If we looked at periods when market volatility was elevated during this time, the S&P 500 returned an average year-over-year loss of -3.3%. However, periods of lower volatility were associated with a higher average annual gain of around 10%.

The takeaway here is that volatility can be used to generate investment returns, mainly when it is low. More crucially, however, history tells us that sudden moves higher in volatility can detract from those returns. Therefore, awareness of the potential impact of a sudden rise in market volatility is vital to improving your investment outcomes.

Source: Broadview Macro Research

#2 Understand Volatility Trends

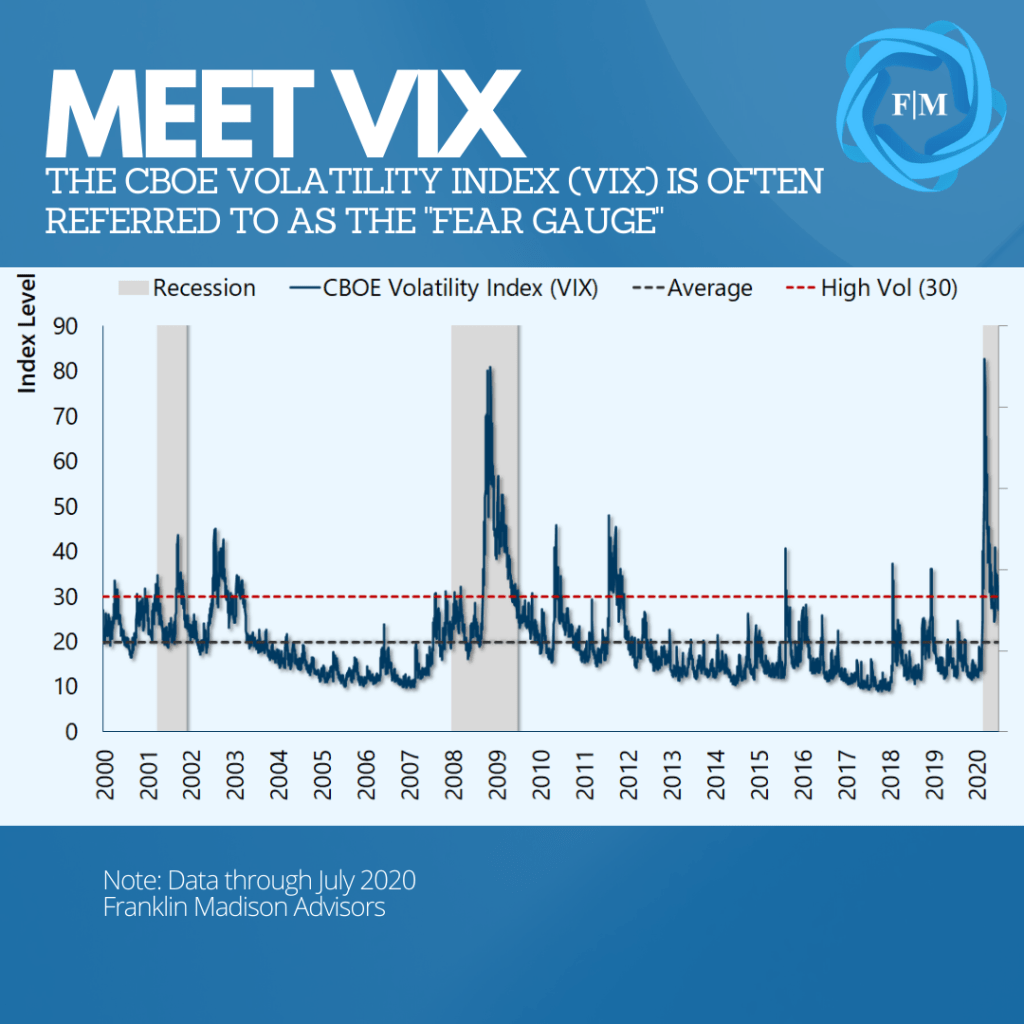

Another way to look at volatility is through market participants' expectations about the future. One widely tracked measure of such expectations is the VIX. The CBOE Volatility Index (VIX) uses a sophisticated method to express the future implied moves of the S&P 500 index. Often referred to as a "fear gauge," sudden moves higher in the VIX are often associated with periods of uncertainty and heightened market volatility.

Compared to the backward-looking statistical measure of volatility mentioned earlier, the VIX is forward-looking. It is also based on investor's directional expectations of the S&P 500 in the month ahead expressed through options market activity. A higher reading generally reflects greater pessimism about the expected direction of the markets.

Over the past two decades, the reading on the VIX has averaged a level of around 20. During the height of the Global Financial Crisis, VIX shot up to a level of 80 and, more recently, bested in February by the uncertainties related to the COVID19 pandemic. Historically speaking, a level below 20 has been consistent with favorable market conditions. A reading above 30 tends to occur during down moves in the market. Why is VIX important?

If you don't know where you are, then it becomes that much harder to figure out where you might be heading. From a volatility perspective, VIX offers a simple way to know how much uncertainty might be priced into the markets at a given time. This understanding is useful before making investment decisions, particularly when history has shown that higher levels of volatility are associated with the potential for lower returns.

Source: Broadview Macro Research

#3 Anticipate Changing Narratives

While financial markets are often viewed as a singular entity, the truth is that they are composed of thousands of assets, each with a host of participants. While algorithmic (computer-based) trading plays an increasingly essential role in the markets, the value of an asset is primarily driven by what human buyers and sellers think it's worth.

Investors are more inclined to bid up prices when they feel confident about the future. For example, when there is certainty about a company's earnings prospects, the policy environment, and the economy's health, asset prices tend to grind steadily higher, and volatility remains low. However, during times of uncertainty about these factors, investors are less willing to pay more for an asset, prices fall, and volatility rises.

One way to measure broad expectations about the economic and policy environment and its potential impact on earnings is by evaluating work compiled by researchers at Northwestern, Stanford, and the University of Chicago. Their Economic Policy Uncertainty Index brings together three components that track 1) news about the economy, 2) tax policy changes and 3) economic forecasts. Their research aims to provide a quantitative measure of what is often a qualitative event (feeling uncertain).

When comparing this measure against the VIX, the data confirm what we know intuitively from a historical perspective: market volatility tends to rise during times of heightened economic uncertainty. From an investment perspective, when uncertainty rises, market participants often change their expectations about the future. And it's during this time of shifting expectations when the price of an asset that may have otherwise seemed reasonable an hour, day or week ago comes into question.

Look for Changes in the Narrative

These periods of uncertainty are driven by a catalyst that often takes time to develop, and that's why measures like the Economic Policy Uncertainty index can help. We only have to look back to the events in February to see how this relationship between uncertainty and heightened volatility played out. Coming into 2020, concerns about a recession had been on the rise, yet many economists expected only softer overall US growth.

In February, however, this hopeful view on the economy changed as Chinese provinces were under lockdown amid a healthcare crisis while the US began reporting rising COVID19 infection rates. As large parts of the US went into lockdown, prospects rose of a deep economic downturn, fueling a volatility spike by late February and ushering in one of the sharpest market selloffs in history.

The point here is that market sentiment is regularly driven by a broad story that is often evident in many quantitative indicators. When factors that support the dominant narrative are challenged, market participants that had been prepared for one set of developments may suddenly change their market positioning to re-evaluate their investment thesis.

When the story changes, the market direction will likely go along with it. Being aware of the narrative driving market sentiment, potential inconsistencies in the story, and how individual market participants might respond can help you better anticipate periods of heightened market volatility.

#4 Know What You Own

Another vital point to understand about volatility is that not all financial assets behave the same way when volatility rises. During periods of heightened market volatility, assets with higher risk levels tend to see wider price swings.

To this point, it is generally understood that stocks are riskier than bonds. This is because equity holders often share in the benefits of company ownership, like stock price appreciation and earnings paid out in dividends. During times of financial distress, like a bankruptcy, however, bondholders are often first in line to be paid back while equity holders might lose a sizeable share of their investment.

Other factors, like the type of issuer (government vs. private sector), company size, market characteristics, and country of domicile, all affect an asset's risk characteristics. Taken together, the higher the likelihood that these factors might expose an investor to a loss, the higher an asset's level of expected risk.

When uncertainties rise and market volatility spikes, individuals holding riskier investments are likely to experience wide swings in asset prices. How do we know this? Well, take, for example, the March market selloff. During the first quarter, the S&P 500 experienced a historic price drop of 20%. At the same time, US government bonds rallied nearly 8% as market participants shed risk assets in preference for perceived safe havens.

The critical takeaway here is that higher-risk assets tend to underperform when uncertainties arise and volatility spikes. If you're anticipating higher market volatility levels, then it's vital to know what you own. Understanding your risk exposures may enable you to trim less favorable holdings and align your investments with your long-term goals ahead of a rise in market volatility.

Source: Broadview Macro Research

Improve Your Volatility Preparedness

We've addressed the various characteristics of volatility and its impact on the markets and investing. So, what can you do to help mitigate the effects of heightened market volatility in your investment portfolio?

Here are three suggestions:

First, don't put your eggs in one basket. As we've written about recently, diversification is one crucial way to reduce portfolio volatility and smooth out investment returns for the long term. Studies have shown that increasing the number of securities held can reduce overall volatility in an investment portfolio. Therefore, if your goal is to invest for the long term, be sure to diversify your portfolio across various securities and asset classes to help reduce risk.

Second, build situational awareness. It's easy to get caught up in the market's daily price action or stay focused on a particular asset when your investments are doing well. Even so, markets are often driven by one or more underlying stories that can evolve. And it's at those turning points in market narratives where volatility tends to spike. That's why it's critical to stay informed about broadly relevant market topics so that you don't get caught unprepared when they change.

Finally, have a plan and act accordingly. Start with knowing what you own. Then, try to anticipate how those assets might perform during wild market swings and adjust your holdings accordingly. Heading into a period of heightened market volatility, it's also vital to have a higher level of cash on hand. Doing so accomplishes two ends. One, it reduces the likelihood that you'll need to sell an investment at an inopportune time to pay for necessary expenses. And two, it may allow you to have dry powder on hand for an opportunity to add discounted assets to your investment portfolio.

Volatility is a normal part of investing. It's the price you pay to earn an investment return. That's why what should be at the top of your list in terms of investing concerns is not volatility itself, but periods of heightened market volatility.

Whether you measure it using backward- or forward-looking means, the fact is that spikes in volatility are often drive by changing human expectations about the future and associated with lower investment returns. Being aware of the narratives driving the markets and having a plan in place before they change is central to investing success. The bottom line is that if you're unprepared for periods of heightened volatility, then you might be exposing your savings to unnecessary losses.

Are Stocks Setting Up for a Second Quarter Repeat?

U.S. stocks had a blockbuster second-quarter. Indeed, both the Dow and S&P 500 have posted their best returns in decades. How long can this outperformance last? With market sentiment still generally positive, some investors are asking whether supportive central bank policies and hope for a rapid economic recovery may be the set up for a third-quarter market surge.

We believe that the dominant narrative that had supported the second-quarter rally is increasingly coming under pressure. Stretched asset valuations and a historical precedent for weaker market returns argue for more caution in the coming quarter. As a result, we recommend that investors use recent market strength to reduce investment risk and raise cash through portfolio rebalancing.

Stocks Had a Stellar Second Quarter – What are the Chances of a Repeat?

Last quarter's rally came on the heels of a sharp market pullback. Efforts to flatten the curve in March led to a massive experiment that had not been tried in well over a century: shut down the economy to curb a pandemic.

Risk assets experienced a sharp selloff in the first quarter on the prospect of weaker economic growth but regained their footing at the start of the second quarter. The rally arguably was fueled by a hope that massive fiscal and monetary stimulus efforts could contribute to a rapid economic rebound.

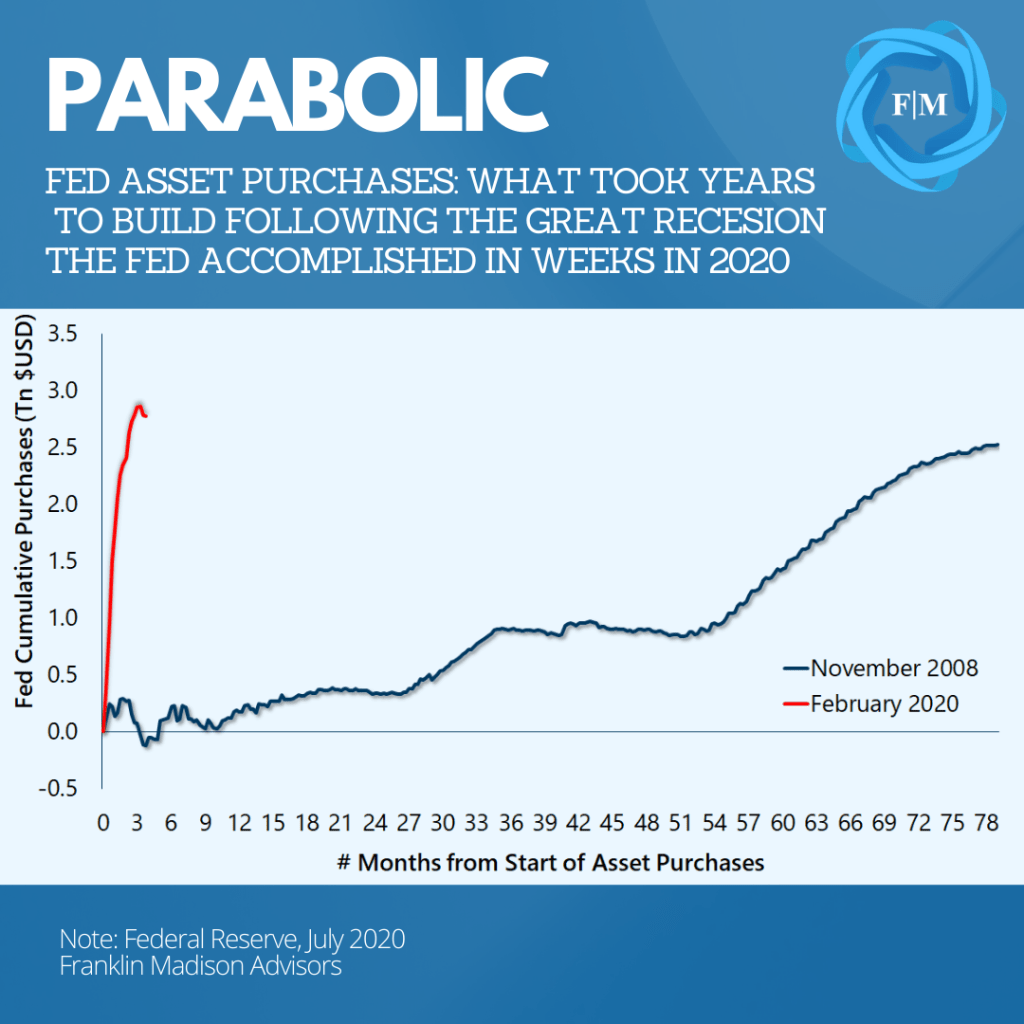

For example, Congress and the Federal Reserve responded to ballooning unemployment and economic uncertainties by launching unprecedented stimulus programs. On the fiscal side, several million businesses in the US received financial support through the Paycheck Protection Program (PPP). The government also issued cash handouts to unemployed workers and households alike.

At the same time, the Fed ramped up purchases of government bonds and mortgage-backed securities. The central bank also launched its Main Street Lending Program to make it easier for small businesses to borrow money. In late June, the Fed began purchasing private firms' bonds through its Secondary Market Corporate Credit Facility (SMCCF). In a matter of weeks, the Fed increased its balance sheet by well over two trillion dollars – a feat that had taken years to accomplish during the Great Recession.

The critical takeaway here is that the second quarter market rally was built upon low price levels and expectations that policy efforts could support a rapid rebound in economic growth. This narrative, however, is increasingly coming into question.

History Suggests Softer Performance

Another important point to consider is that there is little historical precedent for a repeat of second-quarter market performance. We know this because we analyzed data to determine how markets have performed historically following a sizeable rally. Our work suggests that the return on the S&P 500 index in the third quarter could be less than half the 20% realized in the second quarter.

For example, history shows that the S&P 500 rallied 15% in the three months following market lows set in March 2009. How did the index perform in the next quarter? Well, the index gained only 5.5% in the next quarter. And this observation is not limited to just one period in time.

Looking at a distribution of returns going back to 1930, we find that market returns tend to come in between 0-10% in the quarter following a strong market rally at about two-thirds of the time. To be sure, the data showed that market performance on the heels of a massive rally was not only softer in the next quarter, but they were also consistently weaker 98% of the time.

The crucial takeaway here is that, from a historical perspective, strong returns do not beget even higher returns. While the historical data suggest that performance is quite likely to remain positive in the third quarter, from a purely statistical perspective, it's hard to make a case that we'll see even higher returns in the months ahead.

Unmitigated Healthcare Crisis

Finally, it's important to note that the healthcare crisis is not improving, and this will challenge the market's rapid recovery narrative. At the onset of the outbreak, there was a notion that if we locked down the economy and reopened in a deliberate, intentional way (think phase red, yellow, green), we'd be able to contain the coronavirus outbreak, and quickly have life get back to normal.

After initial success in flattening the curve, we're now seeing that COVID19 cases are reaccelerating weeks after much of the US economy has reopened. With vaccine trials still ongoing, and infection rates currently on the rise, there's a real risk that we may end up with a healthcare crisis more severe than the one we had in March.

Such an outcome could lead to delayed household spending and employer hiring decisions, challenging the dominant market narrative that supported second-quarter market performance. Indeed, with more state governors reversing or delaying plans to open their economies, it is becoming increasingly difficult to make a case that markets can continue to rally on hope of a sudden economic recovery.

What Should Investors be Mindful of Heading into the Third Quarter?

Investors should be mindful of the fact that expectations for the future often drive market behavior. Presently, there are arguably two vital expectations supporting market sentiment: 1) policy response will fuel economic growth, and 2) economic growth will quickly recover. Right now, it's unclear whether monetary policy can do more than stabilize economic conditions.

Monetary Policy is not a Panacea

Monetary policy can only do so much to support economic growth. With that said, there is little doubt whether the Fed will pull out all the stops to stabilize growth. The Fed's willingness to support its full employment and inflation mandates is evident in the various programs mentioned earlier. Even so, monetary policy is not a panacea for market-related concerns.

Take, for instance, the Bank of Japan. This central bank has been buying public and private sector stocks, bonds, and real estate for years. It has implemented non-traditional measures such as a negative interest rate policy and yield curve control. Japan's economic growth has nevertheless been weak, and the performance of its markets has lagged its peers. A similar situation is present in the Eurozone.

Anecdotally, history has shown that markets tend to stage an early rally based on expectations of a massive game-changing catalyst, like an election, a rise in government spending, or a favorable change in monetary policy. Today, such expectations are playing out in mantras like "don't fight the Fed." Even so, what we've observed over the past couple of decades is that such rallies tend to wane as market participants eventually reset their expectations to the reality that policy alone does not heal what's ailing a struggling economy.

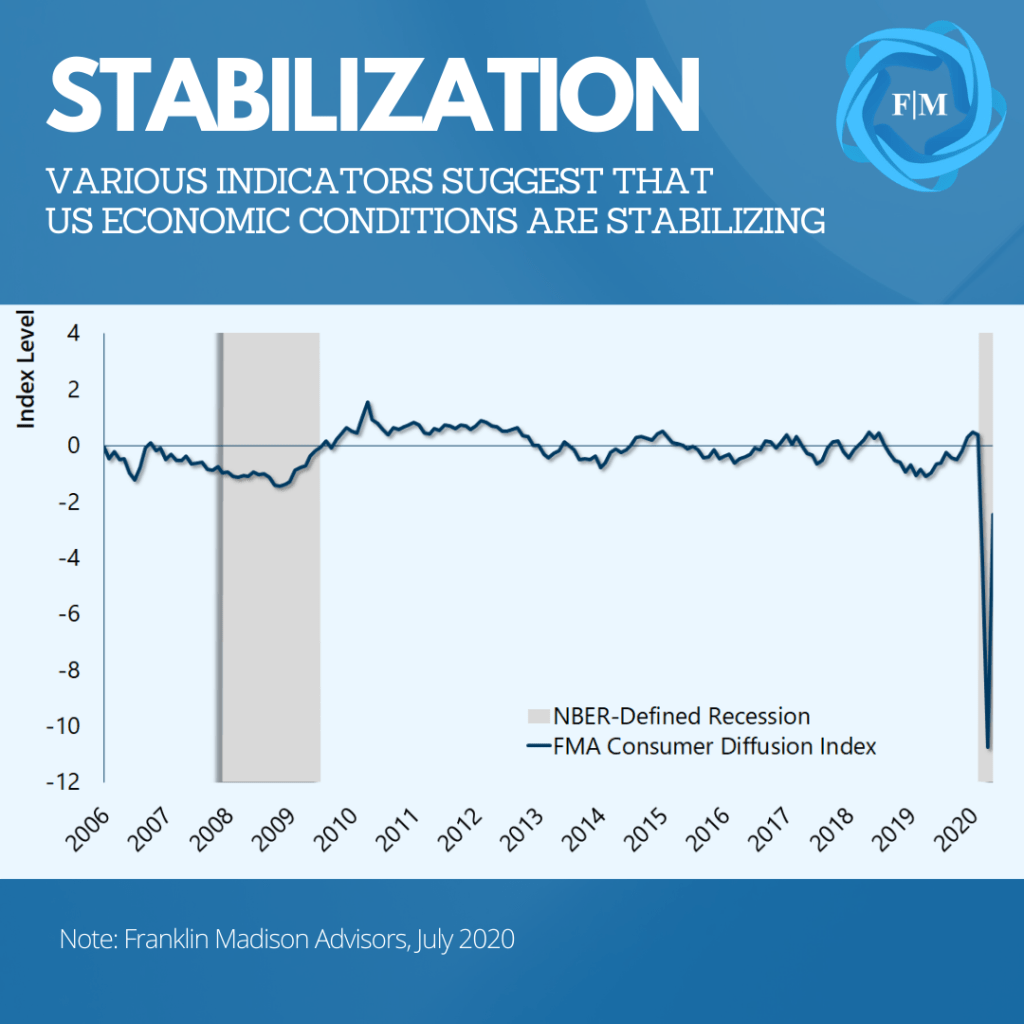

Economy stabilizing, growth likely to struggle

Another issue with which investors must contend in the coming quarter is that weaker growth will challenge market sentiment. While some data have improved, reports are not yet consistent with a robust economic rebound. To this point, the IMF recently downgraded its estimate of a US economic recession from -5% set in April to -8% (consistent with the Great Recession) in June.

This view does not dismiss the fact that by some measures, the economy is stabilizing. Our own consumer and business diffusion indices show that US economic activity is recovering from lows set in April. Even so, these backward-looking indicators need to be reconciled with forward-looking realities: households are increasingly likely to curb spending amid the ongoing healthcare crisis.

A rising number of states are reporting record one-day coronavirus infection rates. The effect of which has led some governors to postpone reopening their economies and others to shut down establishments like bars and restaurants. Prolonging the economic lockdown may curb the recent consumer spending recovery.

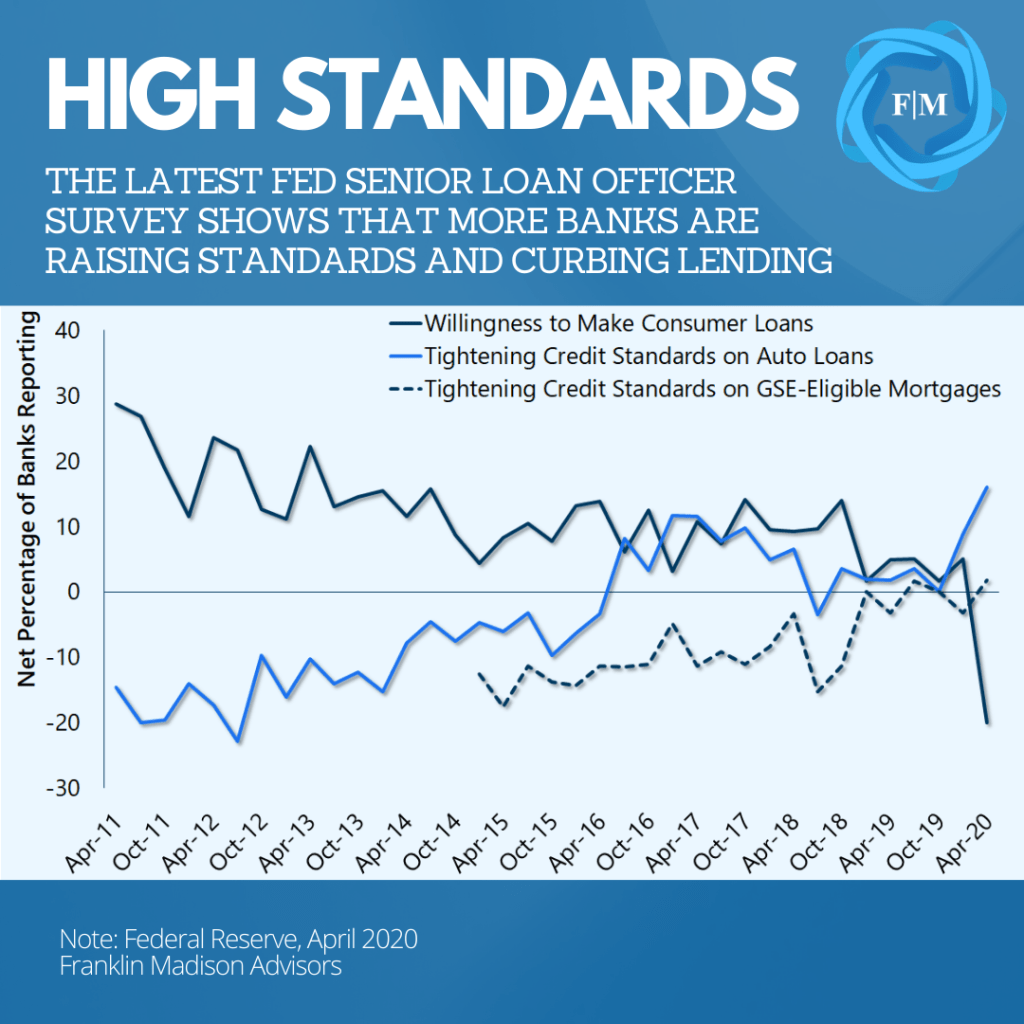

Compounding the problem of lower consumption is the fact that individuals willing and able to spend are finding it harder to borrow money. This issue is evidenced in the Fed's recent Senior Loan Officer Survey. It shows that banks are less willing to lend and that they are also raising lending standards. The implication is that individuals ready to spend, especially on big-ticket items like homes and cars, may find it increasingly difficult to obtain the loan necessary to complete their purchase.

Indeed, there's no question that the US economy is showing signs of having stabilized. Nevertheless, the ongoing healthcare crisis likely will alter household spending behavior and challenge market expectations of a quick economic recovery.

How should investors prepare for lower returns and ongoing uncertainties in the third quarter?

It's important to note that the second quarter rally has led to risk assets becoming expensive when measured by various valuation metrics. The combination of high asset prices and an unmitigated healthcare crisis may contribute to higher market volatility in the months ahead. In anticipation of a market pullback and increased volatility, we suggest that investors pare back recent gains to achieve two ends.

First, during this time of uncertainty, investors need to manage risk and ensure that their portfolios align with their long-term goals. Periods of market strength like we experienced in the second quarter can lead to portfolio drift. Therefore, we suggest that investors use recent market strength to trim winning positions and add to under-allocated holdings. This can be accomplished through portfolio rebalancing that realigns investment holdings with long-term target asset allocations.

Second, we recommend that investors prepare to use market volatility as an opportunity to raise cash. Periods of heightened market volatility may lead to selling assets at inopportune times. This is especially important given the tenable economic environment and ever present need to address unplanned life events. Therefore, we recommend that investors use this period of market strength to bring their portfolios back into alignment with long-term goals through rebalancing while at the same time setting aside some cash to meet unexpected needs.

Feeling Stuck Financially? Hit the Reset Button.

You've been diligent with your money. You've amassed sizable savings. Then life knocks on your door – a once-in-a-lifetime opportunity falls through, work moves you to another state, a family emergency calls, or your primary source of income evaporates. Years of diligent financial progress comes undone in an instant, and now you feel stuck.

Or maybe you're in a position where you've struggled for years to get a handle on your finances, but one disruption after the next keeps you from moving forward. In either case, what can you do when your financial life is stuck? Hit the reset button. Indeed, you can often get your financial life back on track much sooner than you would otherwise by pausing, resetting expectations about your goals, and being methodical in your approach to rebuilding your finances.

Pause and Disconnect

Unplug it and wait a minute. Shutdown your computer. Power down your device. If you've ever encountered a problem with technology, then one of these phrases will likely be the first recommendation you'll receive to correct the problem. While such advice often comes after you've spent many frustrating hours trying to get your router, computer, or phone to do what they're supposed to do, the simple solution often does the trick.

But what do you do if your net worth or savings have declined in value recently? After years of building up your nest egg, what remains today is only a fraction of its once glorious worth after a down move in the markets, a family emergency, or loss of income. During such times it's quite common for feelings of discouragement and negative self-talk to emerge, and you may even feel the temptation to make a big-ticket purchase or have the desire to double down on a loss.

One of the quickest methods, however, to reduce money-related anxieties and regain a sense of financial empowerment in your life during a time of loss or transition is to stop what you are doing, pause and take a break. Doing so may enable you to postpone financial decisions that you may later regret while giving you the ability to assess events that may or may not have been within your control.

What's more, like a project post-mortem or military debrief, the initial act of disconnecting from your financial routine shifts your focus from trying to fix a problem to reviewing lessons learned that might enable you to see opportunities in your new setting. More importantly, pausing and disconnecting may prepare you to rebuild your financial life in a way that is authentic to the present while making room for future growth prospects.

Reset Your Financial Expectations