Common Financial Mistakes High Net Worth Real Estate Investors Make

High net worth individuals (HNWI) is a classification used by the financial services industry to denote an individual or a family with liquid assets above a certain figure. Although there is no exact number, high net worth is generally referred to as those who have liquid assets of $1 million or more. These individuals accrue and grow their wealth by making calculated risks and letting their money work on their behalf. However, wealthy investors can make mistakes too.

Here are four investing mistakes HNWIs (and those who wish to join their ranks) should avoid making.

1. Deciding to Invest Only in the U.S. and the E.U.

As developed countries, the United States and the European Union offer a lot of security when it comes to commercial and residential real estate investments. However, ignoring the opportunities in nations that may be considered riskier excludes higher earnings that often accompany higher risks. For example, some ultra-high-net-worth individuals (classified as those worth more than $30 million) often invest in other parts of the world such as Chile, Singapore and Indonesia. Individual investors or their advisors often can find emerging markets that match up to their investment strategies. Just keep in mind that you also don't want to make the mistake of not thoroughly researching the local market before investing in a property. This research should take into account local information regarding price-per-square-foot comparisons, commercial construction activity, cap rates, zoning regulations and economic growth

2. Playing Lone Ranger

For those looking for wise ways to invest their assets, it's important to also build up a team of trusted professionals. It's fine to act as the point person or to appoint a trusted ally to do so. However, trying to make all the decisions on your own can actually slow you down and cause you to miss out opportunities. Establishing good relationships with a real estate broker, home inspector, appraiser and real estate attorney are essential if you plan to concentrate your investment within a certain area. In addition, finding a lender for personal deals and joint ventures is key to being able to act quickly when opportunities arise.

If your preference is flipping or renting single-family or multi-family units, your team should include reliable, reasonably priced electricians, plumbers, roofers, painters and HVAC contractors, among others. Having other people you can trust lets you concentrate on investing.

3. Not Thinking Outside the Box

Commercial assets don't have to include buildings or complexes. Thinking outside the box can help you diversify your investment portfolio even more. For example, investing in parking garages addresses concerns over the rising unavailability of parking in an urban area. Industrial and warehouse themes are other options that are often overlooked when it comes to diversification, and renting out warehouse space can be quite lucrative near ports and transit hubs. Distressed assets may require a little TLC but they often present opportunities for the highest returns. Following up on the advice to avoid going it alone, these are perfect opportunities to join an investment cohort to mitigate the risks without giving up the potential upside.

4. Forgetting to Save as Well as Make Money

Another common mistake that high net worth investors make is setting unrealistic expectations when budgeting expenses. There's a tendency to underestimate capital expenditures and maintenance costs. A good rule of thumb is to budget 2 percent of the property's value into a reserve fund. This gives you cash on hand when major repairs are needed. Although this mainly applies to commercial assets, such as buildings, it's also important to set aside funds for residential properties. If you're flipping homes, leave some slack in the budget in case problems arise. The older the property, the more can go wrong, so pad your budget accordingly to keep your cash flow liquid and allow multiple investments.

While some of these mistakes may seem rudimentary, many of them arise when you act too quickly or don't properly prepare before jumping into an opportunity that may include some unwelcome surprises.

Dollar-Cost Averaging (DCA): What Is This Investment Strategy and Should You Use It?

One of the biggest fears of any new or seasoned investor is losing money. This fear can actually inhibit some people from ever investing at all, and it might also lead to selling preemptively or opting for the lower risk investment option time and again. To minimize the fear of losing money, investors sometimes choose to go with a risk-reduction strategy, such as Dollar Cost Averaging (DCA).

Despite the fact that the majority of academic research has shown that dollar cost averaging may help to manage risk, but that on average it just reduces returns (and therefore is inferior to lump-sum investing), the popularity of DCA remains high among practitioners and the investing public.

However, given that research has shown that the pain of losses is more severe than the joy of gains for investors1, risk-averse investors may prefer to dollar cost average simply to minimize the potential regret of not doing so and seeing markets decline shortly thereafter.

What is DCA?

DCA is an investment tactic in which a fixed amount of money is invested at regular intervals. The intended goal of DCA is to provide the investor with a lower average cost of shares over time. Since the investment amount will be the same at each interval, the idea is that more shares will be purchased when the price is low, while fewer will be purchased when the price is more expensive.

Those who support the use of DCA claim that it can provide a lower average purchase price for a risky asset, proposing that purchases of assets (that are higher risk) with DCA when prices are declining will provide better returns than lump-sum investing.

What are the Proposed Benefits of DCA?

Risk Mitigation

By only investing a portion of your lump sum, price drops will not impact your portfolio as heavily had you invested a larger portion or your entire sum. Dollar-cost averaging is meant to mitigate the risks involved in lump-sum investing through which an investor could face major losses if the market crashes or prices fall drastically. Risk-aversive individuals may, therefore, prefer to use DCA.2

Managing Emotions

Market fluctuations and losses can greatly affect an individual’s emotional well-being. Further, emotional responses to these ebbs and flows, such as overconfidence or panic, can affect future investment decisions.3 Since only part of a sum is exposed to the market, losses may not be as drastic. Therefore, many individuals may experience a duller emotional reaction than if all of their sums were to be affected, decreasing the likelihood of their making emotionally-driven investment decisions in the future.4

As such, DCA may be good option for those looking to minimize the impact of emotion on their investment choices.

What are the Critiques of DCA?

Missing Out On Gains

When employing dollar-cost averaging, portions of your money sit uninvested. The main argument against DCA is that these portions are not given the chance to accumulate any return at all. As a result, some investors and financial professionals may prefer another strategy such as lump-sum investing, which exposes a larger portion of your funds to the market.

Lump-Sum Investing vs. DCA

In lump-sum investing, a larger portion of your money is given the chance to make gains sooner rather than later. However, investing a significant portion of your money also means that you may experience more pronounced losses in a vacuum. Over time, however, you can make up for these losses. This long-term thinking also supports the idea behind dollar-cost averaging. Ultimately, the decision to use either tactic will depend on your unique situation.

When to Consider Using DCA

Investors might choose to employ dollar-cost averaging for a variety of different reasons, including for investments that are historically more volatile. DCA is also a way to potentially regulate emotional responses. Dollar-cost averaging might be used in the following circumstances:

- Volatile investments

- Other long-term investments, such as 401(k)’s or IRA’s

- A time in life where any volatility is not feasible and may cause immediate ramifications (i.e. nearing retirement)

- Individuals who are risk-aversive

- Individuals who do not have the funds for a lump-sum investment

The alleged benefit of dollar-cost averaging is that it encompasses the unpredictability of the market yet intends to lower the cost of your shares as a result. When choosing how to invest, it is wise to seek the counsel of a financial advisor, who can help you make the best choice for your circumstances and future goals.

- https://www.apa.org/science/about/psa/2015/01/gains-losses

- https://www.onefpa.org/journal/Pages/OCT15-Dollar-Cost-Averaging-The-Trade-Off-Between-Risk-and-Return.aspx

- https://www.aeaweb.org/articles?id=10.1257/jep.29.4.61

- https://www.onefpa.org/journal/Pages/FEB18-Using-a-Behavioral-Approach-to-Mitigate-Panic-and-Improve-Investor-Outcomes.aspx

What to Do When the Market Tanks

You notice over your morning coffee a stern warning emanating from your television as the very serious business reporter notes the Dow opening down one percent. What do you do? If you screamed, “Sell!” or “Panic!” perhaps you should take the advice of some of the world’s savviest investors and turn away from the stock ticker for the rest of the day. You may be envisioning dollar signs flying out of your wallet and you want to get on the phone and sell. You may even see an opportunity to buy. However, most market gurus will say that if you have a wise strategy in place, it's typically best to stay the course.

Billionaire and real estate magnate Warren Buffet told CNBC in 2016 that buying or selling in a rush may not be the best strategy. “If [worried investors are] trying to buy and sell stocks, and worry when they go down a little bit … and think they should maybe sell them when they go up, they're not going to have very good results." Such a panic move could unbalance your portfolio where you are either taking on more or less risk than you should.

1. Keep a Balanced Portfolio

Having a balanced portfolio can help to balance risk and return. Generally speaking, balanced portfolios consist of a 50/50 mixture of stocks and bonds. You can re-balance by selling other assets like bonds or even commodities. Then you can invest in stocks that are down in price. It’s not a panic buy; it’s a strategic move that fits your original investment plan by taking your portfolio back to the ratio of stocks to other assets.

2. Resist Panic Selling

Typically panic selling is triggered by events that may lower the confidence level of investors causing them to sell and when this occurs on such a wide scale sharp declines in pricing tend to occur. Selling in a rush to get out of a down market could have long-term implications and often times cause you to miss out on some big gains when the market corrects.

3. Consider Taking Advantage of Tax Laws

Many financial advisors suggest a strategy to create tax losses to offset capital gains by selling an investment. If your gains are less than your losses, you can claim those losses on your tax return. You can carry over losses greater than the amount you can claim on your annual return to another tax year. This strategy is referred to as tax-loss harvesting.

4. Protect Your Nest Egg

If you’re really worried about things like a college or retirement fund during a downturn in the market there are a few steps you can take to protect these funds.

- Reduce your debt. If you start losing money in the market that threatens to deplete your funds, you don’t want to have to pay creditors while trying to take care of yourself and maintain your accounts.

- Ask your financial advisor about reducing the amount of risk you have. You’ll at least feel more confident about your portfolio if you know that you’ll have a healthy portfolio that is less affected by market fluctuations.

- Don’t invest money you think you may need. This is especially important for retirees who may only have investment income to rely on as they get older.

5. Focus Long-Term

When you start to see headlines of the stock market declining it can be easy to go into panic mode and wait to watch values decline in real-time. However, when you sell investments in a downturn your essentially locking in your losses. When the market eventually stabilizes you'll likely be left chasing much higher prices. It's always a good idea to keep your long-term goals in mind before making any decisions in a downturn and consulting with an experienced financial advisor before making any moves.

Buffet advised taking a look at the earnings sheet to determine whether you have made a good investment, not the market. You can’t judge your investment strategy all of a sudden; you have to look long-term.

How to Stay Sane when the Markets are Going Crazy

Let’s face it, no one wants to be the one person that missed out on what seems to be a once-in-a-generation investment opportunity simply because you’re trying to do the right thing. This decision is especially difficult at a time when making money in the markets seems so easy. Without a doubt, the fear of missing out on a great opportunity is so powerful that in the past it had encouraged otherwise rationale investors to put money into worthless tech companies in 2000 and prompted hairdressers in Florida during the housing boom to purchase three or four rental homes they just couldn’t afford. Even so, as Jeremy Grantham puts it, “there’s nothing more irritating than seeing your neighbors get rich.”

There’s no doubt that, in certain segments of the markets today, individuals are experiencing phenomenal returns in their holdings of tech, bitcoin, penny stocks and by participating in the options market. For example, the NASDAQ 100 index gained 96 percent from the market bottom in March 2020. Bitcoin, also, has gone from a price of $8,880 twelve months ago to well over $34,000. Names of penny stock companies (stocks that trade for less than $5 per share) have doubled or even trebled in a matter of weeks and months and now account for a growing share of trading activity. With results like this, it’s hard not to feel like you’re missing out on something spectacular when you’re watching from the sidelines.

And it becomes increasingly difficult to remain on the sidelines when these seemingly effortless opportunities to make money are minting new affluent lifestyles every day. To make matters worse, today’s mainstream media is increasingly caught up in reporting on the ease with which amateur investors are turning their stimulus checks into thousands of dollars in gains. Likewise, social media is blowing up with content from amateur investors promising fast returns by following simple rules for speculating in the markets.

To many of us, it’s easy to look at what’s going on today and call it for what it is: it’s market speculation. Even so, with seemingly everyone partying and making money hand over fist, the psychological pressure may grow to the point where you begin to ask yourself: “am I missing out on a great opportunity?” Even when you know that this latest investing craze completely flies in the face of your disciplined savings and investment plans.

So, what can you do when going against the crowd feels increasingly uncomfortable and to the point where fear of missing out is eroding your willpower to remain committed to a disciplined investment strategy? During times like these, it’s crucial to remember that what’s going on today has happened before, and it will likely happen again. That’s why gaining some perspective and reminding yourself why you became an investor and what you have to lose is essential to staying grounded when you feel tempted to follow the crowd and are potentially setting yourself up for failure. So how exactly did we get here?

It’s Happened Before, and It’ll Happen Again

Well, it’s vital to recall that much of the gains in some portions of the markets have been fueled by easy money policies and individual investor euphoria and not sound fundamentals. Recall that skyrocketing unemployment caused by a devastating global healthcare crisis last year led to trillions of dollars being pumped into the financial system and the economy. Fueled by access to cash and success in the early 2020 rally, some individuals today have shifted their focus to the highly speculative market segments we mentioned earlier. In many cases, price action in these parts of the market have little, if any, relationship to company value, revenue, or earnings growth.

Rather, market action in these cases appears to be solely based on speculation of what the asset’s price might be tomorrow, next week or next month. And to this point, one mantra driving participant behavior is “prices can only go up.” Ultimately, we could say that the Greater Fool Theory is driving the markets. More specifically, this theory states that an asset’s value is driven solely by price expectations and not some fundamental underlying factor.

The Greater Fool Theory

Now, if you’re not familiar with the Greater Fool Theory, it goes something like this: I know that the price I’m paying for this asset today doesn’t make much sense, but that doesn’t matter. The market is hot, and there’s so much demand for a given investment that there will almost certainly be a buyer sometime soon. Therefore, I’m going to buy today hoping that I can flip this asset to the next newly minted naïve investor.

This mindset has become so pervasive that it’s spread across discussion groups that were once personal finance strongholds for the disciplined do-it-yourself investor. For instance, White Coat Investor recently shut down a Facebook group after becoming a hotbed for bitcoin speculators and hot-stock tip discussions. In another example, Bogleheads community members have increasingly become divided on whether individuals should take out a personal loan or use their credit card to purchase shares of already high-priced tech stocks. Does what’s going on today at all sound familiar to you?

Recall that skyrocketing US home values in 2006 and 2007 didn’t happen because of a baby boom. They happened because interest rates were low, and mortgage lenders and house flippers believed that prices would rise forever. This sentiment became pervasive throughout the media and government policy and led to many TV shows and seminars devoted to getting rich in real estate. When the music stopped, however, the finances of millions of individuals were devastated. While it’s still too soon to establish how our story will play out, there’s a good chance that the asset bubbles forming today likely won’t end with a soft hiss but with a loud bang.

What’s Your Motivation?

Sometimes having a rational understanding of the facts may not enough for you to shake that uncomfortable feeling that something good might be passing by. If you find yourself in this situation, you’ll likely need to dig deeper to gain a clearer perspective and stay grounded in your long-term plans. And this begins with setting aside some time to consider your core motivation for saving and investing before you get caught up by what’s happening in the markets today. To this point, you’ll need to ask yourself if your primary motivation for investing is to keep up with the Joneses or to carve out your own definition of financial independence.

You’ll likely recall that individuals like you have achieved financial independence by saving prudently, earning a steady rate of return on their investments, and making their money work for them. More often than not, individuals on the path to financial independence are focused on systematically creating, growing or preserving their wealth and care less about what others are doing with their money. So, if you’re tempted to participate in the current market exuberance, now may be the time to ask yourself if the choices you’re considering align with behaviors that lead to long-term success.

If your priority is to generate a steady rate of return over the long run, then making incremental, short-term bets on what appears to be an outsized financial gain may not cut it.

Indeed, history has shown that a disciplined investment strategy, adhered to over a long period, can lead to exponential savings growth. Various academic studies have also illustrated how asset allocation and not stock selection or market timing have been the most significant determinant of investment returns.

How will it Feel to Lose?

By now, the various facts and arguments discussed here may not be enough to convince you to stay the course. You might be considering allocating just a small portion, rather than all of your savings, to these highly speculative segments of the market. If this speaks to you, then you’ll need to think hard about your pain tolerance. In a recent note to investors, UBS warned that some of today’s speculative assets could see their prices fall to zero. And to this point, a key risk in today’s markets is that few individuals remember what it’s like to lose money when winners are created seemingly every day.

If you’re tempted to dabble in parts of the markets where sentiment is hot, ask yourself how you’ll respond emotionally should that investment go to zero. Academic research has shown that the negative emotions that an individual feels by losing a new gain is more potent than not having made money in the first place. What’s more, taking your focus off your long-term investment strategy during a time of emotional turmoil might leave you open to questioning your overall investment process. When the music eventually stops, and the party is over, there will be a rush to the exits, and that’s not the time you want to be figuring out what to do with your investments, especially when emotions are running high.

Don’t be the Bagholder

Finally, don’t be the bagholder. Make no mistake: bubbles do eventually burst. And a bagholder is an individual who holds on to their declining speculative investment, hoping that prices will eventually recover. Whether we’re talking about the Tulip Mania, South Sea Crisis, Tech Bubble or Housing Crisis, they all start, grow and end the same way.

No one can say for sure, in our current situation, whether that moment will come next week or next month.

Either way, rather than trying to time the market, we recommend looking ahead to long-term investment opportunities positioned to perform well at this stage in the economic cycle. Many indicators suggest that the US economy could experience a strong recovery in 2021.

And from this perspective, yesterday’s winners can quickly become tomorrow’s losers. That’s why it’s vital now more than ever to spread your investments across high quality, uncorrelated assets that offer high relative risk-adjusted returns.

As we’ve discussed in previous reports, we believe that a market rotation is currently underway. Value names, small-cap and emerging market stocks are well-positioned as the US and global economy recovers. A key risk to this outlook, however, is predicated on accelerated COVID vaccination rates. Without this, a return to normal may not happen as soon as the second half of this year.

Even so, accommodative fiscal and monetary policies are likely to support higher growth levels into the coming year. Make no mistake, there are no easy answers to the powerful psychological forces of going against the crowd. But by looking past the latest investing craze, reminding yourself of your financial independence goals, digging deep to figure out what you have to lose, and staying committed to a long-term, disciplined investment strategy, you might just be able to maintain your sanity when it seems like the markets are going crazy.

Why Your Investments Might Thrive in 2021

This past year has been a period in history that many of us would like to simply forget. Concerns about our communities' wellbeing led to a seismic shift in the way that we work, educate our children, socialize, and go about our daily routines. Without a doubt, 2020 has been a year that has tried our livelihoods, finances, health, relationships, and most importantly, our patience. Indeed, the one word that might best characterize an experience that happened to us is: survival.

Nevertheless, chances are good that the negative factors that have forced us to hunker down are likely to ease into the year ahead, enabling many of us to thrive once again. More specifically, widescale distribution of a coronavirus vaccine and a return to a seemingly normal political environment likely will foster greater business and household confidence in the months ahead. Such outcomes could support labor market improvements and a rise in business earnings. At the same time, accommodative central bank policy may provide much-needed support to the economy and boost financial market sentiment.

Even so, while government spending and money printing were a boon to financial markets in 2020, investing likely won't be as simple as following the latest trading fad. Liquidity-induced momentum trades that provided handsome gains this year could be harder to come by in 2021. That's why as we look into the year ahead, the key to thriving financially for investors with a long-term savings orientation could be as simple as sticking to the basics and focusing on fundamentals.

Climbing Out of a Hole

The healthcare crisis response dealt a blow to the US economy, but there are ample reasons to be optimistic. Nationwide lockdowns during the first half of 2020 led to one of the sharpest economic contractions in history. A record 24.9 million people had claimed jobless benefits this year as businesses closed to help stem the spread of the coronavirus outbreak. During this time, some economists expected a V-shaped economic recovery fueled by historic government spending and central bank money printing.

Indeed, while growth improved in 2020, the gains that some people had hoped for failed to materialize. And as 2020 ends, the healthcare crisis has again intensified, leading to a new round of stay-at-home orders, business closures, and a rise in unemployment. While the housing market certainly benefited as more individuals worked from home, much anticipated pent-up demand in consumer spending fizzled out into the holiday season. And while it appears that the economy is now losing steam, a couple of factors may pave the way for greater economic resilience in the coming year.

So why should we be optimistic? Well, to start, we now have several vaccines that put us miles away from where we were just a few months ago. These injections may eventually help mitigate the spread of COVID infections and enable society to return to some semblance of normalcy sooner rather than later. Certainly, news of a vaccine was greeted with optimism by the markets in November.

And as vaccination efforts kick off this month, there is a reason for optimism as social distancing orders are likely to ease at some not-too-distant point. Indeed, a recent CFO Survey from the Richmond Fed showed that business executives are more optimistic about the future than last quarter as they looked past pandemic risks.

Besides vaccines, another likely reason for rising confidence heading into 2021 is greater political certainty. With another chaotic election season behind us, Capitol Hill leaders are likely to focus on introducing policies that further support economic growth. While a $900 billion stimulus package was approved in December, slowing retail sales and rising jobless claims likely opens the door for another round of government spending during the first half of next year.

Make no mistake; the road to recovery will take some time. History has shown that, on average, recessions tend to last about three quarters. From there, it takes on average two and a half years for the labor market to return to its previous high-water mark. These data points suggest that the US economy has a deep hole to climb out of, so vaccination efforts and decisions made by Congress will be essential to the recovery pace in the months ahead.

The Markets Are Not the Economy

Let's consider this economic outlook in the context of the markets. Now, there seemed to be a disconnect between financial markets and the economy in 2020. While household spending slowed and employment conditions declined, major stock market indices closed the year positively. To be sure, a repeated mantra reflecting this sentiment has been that the markets are not the economy. So why did markets perform so well amid a global pandemic? Well, without a doubt, global central bank policies played a crucial role in buoying risk asset prices.

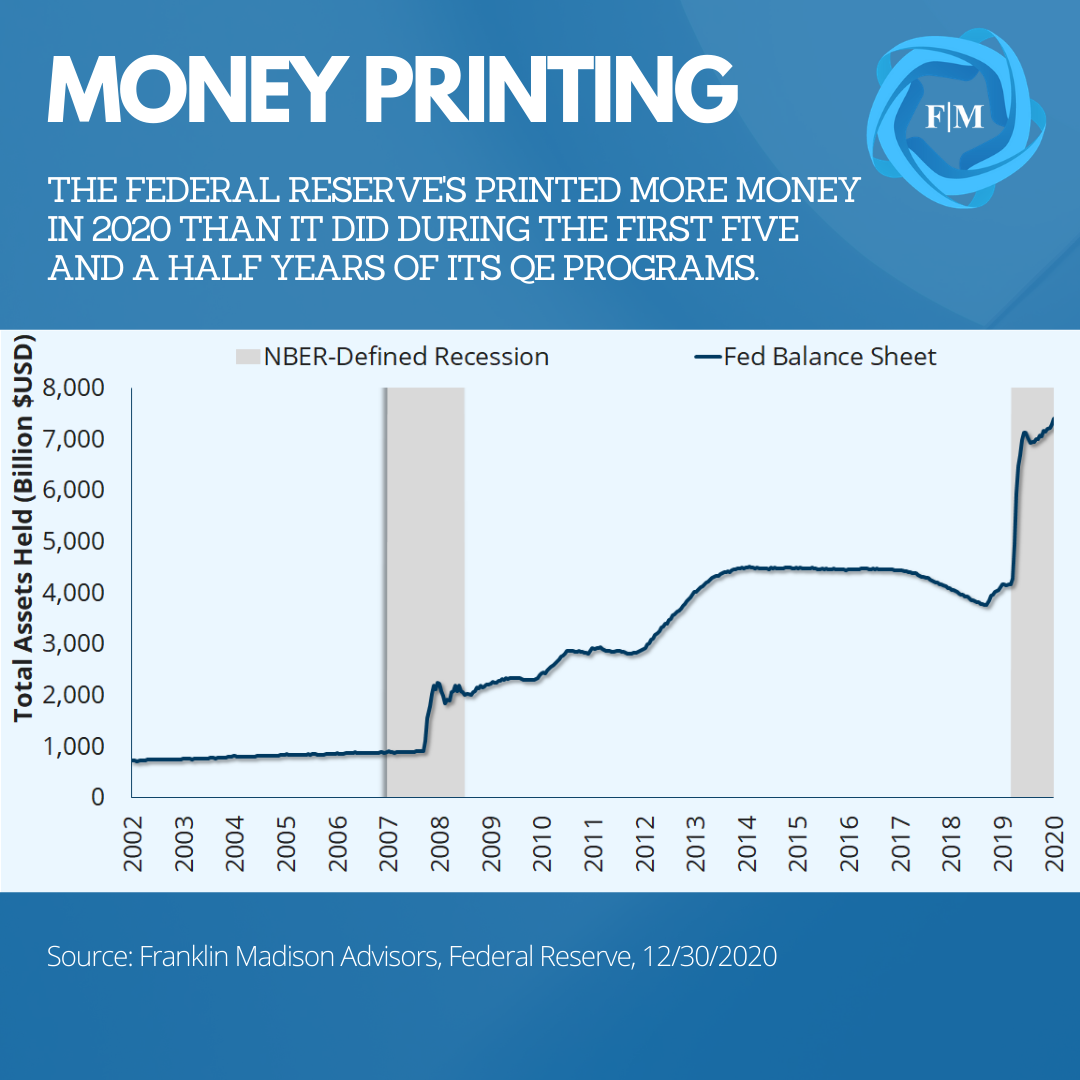

During the height of the pandemic outbreak, the Federal Reserve (Fed) introduced a historic asset purchased program that dwarfed its previous money printing efforts. For example, in 2020, the Fed added $3.3 trillion worth of assets to its balance sheet. To put this figure into perspective, from the height of the Global Financial Crisis in 2008 and three rounds of Quantitative Easing thereafter, it took the Fed over five and a half years to purchase the same amount of assets. What's more, the Fed, European Central Bank, and Bank of Japan bought a combined total of $8 trillion of assets this year, a feat that took eight years during the Global Financial Crisis. Arguably, this massive injection of cash into the financial markets contributed to stellar market performance in 2020.

Newly Minted Investors

Another contributor to the strong market performance was greater participation from individual investors. An analysis prepared by JP Morgan Securities suggests that individuals opened more than 10 million new brokerage accounts in 2020. Add in the rise of a cottage industry of social media investing gurus, the fact that some apps have arguably gamified investing and brokerages flush with cash offering attractive margin loans, and you have a recipe for exuberance in certain corners of the markets. This sentiment was particularly evident in the tech sector, which saw outsized performance as work-from-home and healthcare stocks benefited from Fed-induced liquidity and newly minted day traders.

Today, however, there's some indication that this popular market approach may be losing steam. The momentum trade that had supported strong asset performance has subsequently led to stretched valuations. Such excesses have been exhibited more acutely in tech, which is up well over 40% compared to 16% for large caps. This preference for stocks poised to benefit from social distancing and work from home themes has come under pressure as a return to normal appears on the horizon.

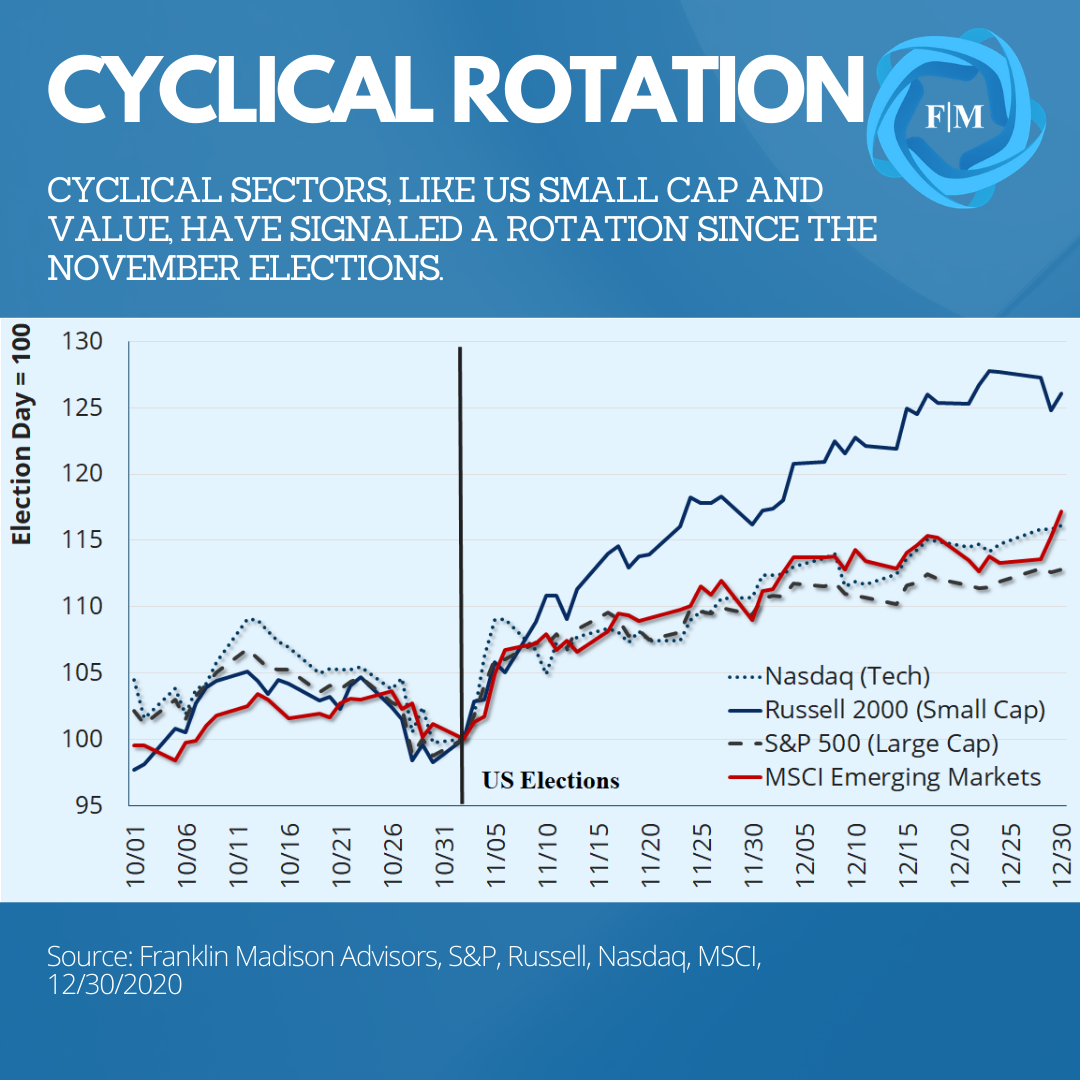

Certainly, this perspective has not been lost on market participants. It has been exhibited in a rotation away from the liquidity-induced momentum trade towards more traditional cyclically oriented risk-on segments of the market. This shift in sentiment has also been evident in small-cap and emerging market stocks outperforming tech and a decline in the US dollar demand during the fourth quarter of the year.

Less Tech, More Cyclicals

Looking ahead into 2021, this sector rotation toward cyclical, risk-positive parts of the market could continue ahead of a recovery in the global economy. Even so, market optimism likely will be dependent on positive pandemic developments and a propensity for more fiscal spending.

More specifically, there is a risk that logistical and administrative issues related to vaccinations could lead to slower than anticipated uptake. For example, so far, only 3 million shots have been distributed and 11 million doses shipped – well below the Trump Administration's goal of 20 million vaccinations before year-end.

Now, there is a potential that the bottlenecks contributing to the weak uptake in vaccinations could be resolved in the coming weeks. With that said, the longer it takes to inoculate the population, the longer that pandemic related risks will linger and put downside pressure on economic growth and corporate earnings. This point is important because market expectations seem to be pricing in significant improvements in the pandemic narrative by mid-2021, paving the way for a strong second-half economic recovery. Unfavorable developments that lead to a substantial deviation from this outlook could break sentiment and lead to bouts of heightened market volatility should the market narrative.

What's more, there is a risk that a divided Congress could lead to more gridlock on Capitol Hill, potentially delaying plans for additional fiscal stimulus. Assuming that Democrats fail to pick up gains in the Georgia Senate runoff election, incoming President Joe Biden's plans for a third round of stimulus checks could face a substantial roadblock. For example, the US fiscal deficit as a share of GDP is now at its highest levels since World War II. Fiscally conservative Republicans could derail plans for another stimulus package. Should this happen amidst an already weakening economic backdrop, we could see a rise in investor uncertainty and a bout of price weakness in an already stretched market.

Positioning Your Investments to Thrive in 2021

Without a doubt, the road to recovery from the Pandemic of 2020 will be fraught with many challenges. Even so, we could see a sustained recovery in employment conditions, household spending, and economic growth assuming inoculation efforts accelerate and policymakers remain supportive of more fiscal spending next year.

Such improvements likely would sustain higher corporate earnings growth and support investor demand for cyclically oriented portions of the markets. While following the trend has been an attractive way to play pandemic uncertainty, investors positioning themselves to thrive in 2021 likely would be best served by sticking to the basics and focusing on fundamentals.

For example, markets are arguably mean reverting by nature. This behavior implies that what has performed well in the past is not as likely to perform as well in the future. From this perspective, evaluate which positions in your investment portfolio have outperformed in 2020 (especially if those positions are tech-oriented) and consider whether it's time to take some gains off the table.

Next, look over your overall investment plan and consider the composition of your holdings. As we transition away from economic survival and towards recovery, now may be the time to evaluate whether your portfolio is strategically aligned with your long-term savings goals.

Finally, get your savings plans back on track if this year's survival strategy included avoiding contributions to your retirement plan. With prices at historic highs in certain portions of the markets, it may be tempting to wait for an attractive entry point before getting back into the markets. Even so, trying to time your way back into the markets could lead to missing out on long-term opportunities. That's why dollar-cost averaging back into the markets might help you thrive financially in 2021.

How Could the Behavior Gap Affect Your Investments During This Time of Market Volatility?

“It turns out my job was not to find great investments, but to help create great investors,” writes Carl Richards, author of “The Behavior Gap.”1 From increasing our budget mindfulness to taking a steadier approach to investing, Richards has drawn attention to the way our unexamined behaviors and emotions can be our detriment when it comes to living a happy and financially sound life.

In many cases, we make poor financial decisions when experiencing panic or anxiety as a result of personal or widespread events. In the past few weeks, the Coronavirus is one such event that has affected nearly every industry and home as people and governments take action to keep themselves and their community safe. The virus continues to evoke fear and panic as the number of affected individuals rises.

The stock market volatility of 2020 began on Monday, March 9, with history’s largest point plunge for the Dow Jones Industrial Average. On March 16, 2020, the Dow hit a new record. It lost 2,997.10 points to close at 20,188.52, demonstrating the financial effect of this health crisis.2

Whether facing a devastating event or an exciting advancement, people frequently make money decisions as a response. Below we discuss the common financial behaviors driven by such circumstances.

The Behavior Gap Explained

Coined by Richards, “the behavior gap” refers to the difference between a smart financial decision versus what we actually decide to do. Many people miss out on higher returns because of emotionally driven decisions, creating a gap — “the behavior gap” — between their lower returns and what they could have earned.

4 Common Emotions that Can Create a Behavior Gap

#1: Excitement When Stocks Are High

Whether in a bull market or witnessing the hype from a product release, many investors may feel tempted to increase their risks or attempt to gain from emerging investments when stocks are high. This can lead to investors constantly readjusting their portfolios as the market itself experiences upswings. An investor who follows such patterns is likely to do the same with declines and may end up trying to time the market time and again amidst its inevitable, unpredictable movement.

#2: Fear When Stocks Are Low

As a response to the Coronavirus, the market has seen losses as many investors feel the need to choose more secure investments and avoid uncertain or seemingly unsafe investments.2 When stocks are low, a common response may be to sell and effectively miss out on potential long-term gains.

#3: Engagement in the Search for Alpha

People yearn to make money and take action to do so. Throughout our lives, this emotional desire is likely a constant one. As such, many seek the help of a financial advisor to procure above-average returns, otherwise known as “alpha.”1 However, in this search for “alpha,” our humanness — our emotions and our behaviors — may lead us astray. Ironically, studies done by DALBAR have calculated the “average investment return” as compared to investor returns and have shown that investor returns are lower.1 The underlying emotional desire and pursuit of money is exactly the recipe for unwise behaviors in response to emotions — but only if left unchecked.

#4: Short-Term Anxiety and Focus

As humans, viewing aspects of our lives through the lenses of current circumstances is normal. One emotional response to any event, however, is letting the moment consume us, especially if faced with grave consequences — from our personal health being compromised to the loss of loved ones. Many may find it difficult in these times to both think long-term and to remember logic. However, making a rash decision can inhibit the long-term benefit that comes from maintaining a balanced perspective without reactionary behavior.

How to Lessen the Behavior Gap for Your Financial Health

At any given point, the market can go up, down or it can remain the same. While many aspects of the virus are out of our control, one thing we can control right now is how we handle our financial strategy.

In the past, the market has recovered in response to epidemics with an average of 17.17 percent over time.3 While no two situations are alike, remembering the likelihood of recovery over time — and the market’s nearly inevitable up-and-down movement — can provide a more logical angle to calm the nerves.

If you’re experiencing financial anxiety in response to the coronavirus, take a breath and also remember the potential for long-term gains. Of course, you can and should always reach out to your advisor for further clarification and advisement.

- https://behaviorgap.com/outperform-99-of-your-neighbors/

- https://www.nytimes.com/2020/03/16/business/stock-market-today-coronavirus.html

- https://www.marketwatch.com/story/heres-how-the-stock-market-has-performed-during-past-viral-outbreaks-as-chinas-coronavirus-spreads-2020-01-22

Franklin Madison Advisors, Inc. (“FMA”), is a registered investment adviser firm with its registration and principal place of business in the Commonwealth of Pennsylvania. Registration of an investment adviser does not imply a certain level of skill or training. FMA is in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which FMA maintains clients.

This commentary and forecasts are limited to the dissemination of general information pertaining to Franklin Madison Advisors’ investment advisory services and general economic and market conditions and are subject to change without notice. The information contained herein is not intended to be personal, legal, investment or tax advice or a solicitation to buy or sell any security or engage in a particular investment strategy. For additional information about FMA, including fees and services, please contact FMA or refer to the Investment Adviser Public disclosures.

FMA may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Any subsequent, direct communication by FMA with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For additional information about FMA, including fees and services, please contact FMA or refer to the Investment Adviser Public disclosures. Please read the disclosure statement carefully before you invest or send money.

6 Ways to Overcome Market Psychology

Market psychology is the reaction to investing. Overcoming market psychology is not easy but learning how the market works can reduce the number of surprises and increase the degree of success. Keep in mind, all assets rise and fall in value, the more extreme the swing, the stronger the sentiment.

For market success, develop your awareness and work with a market professional for sound advice and investment guidelines. Participation in the market has its ups and downs, but when you compare non-participation with the right guidance and mindset the probabilities improve.

1. Equalizing the Costs

Costs include monetary and non-monetary expenses. Monetary is comprised of transaction and brokerage fees. Non-monetary is the time spent learning about the market and understanding the investment process along with managing the shifts between the increase and loss.

Much like the past, today’s modern portfolio needs the assistance and watchful eye of an experienced market professional. It’s not enough to guess or even estimate the changes – planning is necessary to anticipate the wins and the losses.

2. Long-Term and Short-Term

The nature of the market is the volatility of prices rising and dropping. Our emotions share a similar reaction between excitement and depression. Surges of pleasure with favorable uptrends and neurotic negatives with declines.

The long and short of it is about now and the future – both terms play a vital role in learning how the market shifts affect your choice.

- Long-term is noted for continued performance and consistent results.

- Short term focus on temporary boosts during innovative or downturn markets.

3. Market Awareness

Start by figuring out your financial characteristics, and what segment of the market works best for you. It takes an honest assessment of your knowledge, means, and objectives. For this reason, working with an experienced professional is a benefit – they are going to help ease the emotional and financial ups and downs.

There are two noted market trends – bear and bull. They are both related to volume shifts. Bear markets have prices falling accompanied by the urge to sell. Bull markets are steady and confident; prices go up involving rational decisions to buy or sell.

4. Manage and Control

Unfortunately, emotions can be drivers for selling early (short-term) diminishing the significant gains (long-term). As we go through various phases in life so does the market. On the average upswing, markets have a lifespan of five years. It doesn't mean earnings stop entirely – but they could settle in with a slower and more steady growth.

Here, diversity and multiple selections are necessary for a healthy portfolio. Don’t underestimate the value of the entire portfolio, one investment increasing won’t stand alone over time.

5. Move Forward

Get over the past experiences and focus on the future. It's coming with or without your approval – better to be part of the plan and manage the calls so you can reap the benefits. Start slowly and build trustworthy confidence to reduce the risk and the stress, allowing the market to respond back to you - positively.

Questions to ask yourself: are you in the right market? Does your plan have a solid strategy built into it? If you have some concern do yourself a favor and look for help.

6. Change Perspectives

Most individuals don’t always experience success immediately, and our mind begins to associate financial markets with negative emotions. Acknowledge the market is not just about winning and losing – it’s about strategy and duration.

The market will continue to do three things: it goes up, it goes down, or it stays the same. Talking with a market professional helps to manage the market's pluses. Working with one could change your perspectives and broaden the future's outlook.

What Is a Robo-Advisor? 6 Of Your Top Questions Answered

If you’ve considered buckling down and getting serious about your portfolio, it’s likely you’ve come across the term “robo-advisor” before. What is a robo-advisor exactly, and how do you know if one is right for you? We’ve got your answers below.

What Is a Robo-Advisor?

A robo-advisor is also known as an automated investing service or online advisor. Instead of having an individual, such as yourself or an advisor, build and manage an investment portfolio, a robo-advisor does so using algorithms and computer software.

Robo-advisors typically include limited interaction with an advisor, and they can be set up quickly (often in just a couple of minutes).

Common Questions About Robo-Advisors, Answered

Below we’ve rounded up our answers to the most common questions we hear about robo-advisors.

1. What Are the Advantages of Using a Robo-Advisor?

One of the most prominent advantages of using a robo-advisor is the account minimum requirements. Some have no minimums at all, while others will let anyone start investing with just a few thousand dollars. This can be an appealing alternative for investors (such as young professionals) who have not yet acquired the assets needed to hire an investment advisor (since many advisors have minimum AUM, or Asset Under Management, requirements to work with them).

Robo-advisors can help reduce the chance of human error or behavioral bias. They’re automated and use algorithms to invest, making it hard for an investor to make a mistake or gut reaction on their end. It takes the emotional response to market changes out of the equation. While you may be inclined to change your strategy based on what you see on the news, a software program isn’t.

Robo-advisors are also an ideal way to simply “set it and forget it.” They’re typically programmed to automatically rebalance, without a need for you to take any action.

2. What Are the Disadvantages of Using a Robo-Advisor?

Robo-advisors really can’t replace the one-on-one, tailored advice and strategies of an investment advisor. If your investment needs are more complex, or you’re looking to integrate your portfolio into the rest of your financial plan, a robo-advisor may not offer what you’re looking for.

If you have multiple accounts, like a company 401(k) plan, a robo-advisor also may not be able to accommodate these different investment accounts. If you need to integrate these various accounts, you’ll likely want to work with an advisor directly.

3. Who Primarily Uses Robo-Advisors?

Robo-advisors could be considered a “happy medium” between DIY investing on your own and hiring a professional financial advisor. It can be a big time saver and cost-effective option for those who have a simple investment strategy and/or are just looking to automate their investments. In addition, robo-advisors are advantageous for young investors who don’t have the assets or net worth needed to hire an investment advisor, but still would like to get started building a portfolio.

4. What Does a Robo-Advisor Cost?

Robo-advisors vary in cost, but the fee structure is similar across the board. Most robo-advisor services charge a percentage of the assets under management. This is typically anywhere between 0.25 percent and 0.50 percent, but some providers could charge more.

In addition, you may have to pay any fees associated with the investments themselves (such as an expense ratio).

Some providers may offer robo-advisor services as a flat fee for users, rather than a percentage of the assets under management.

5. What Services Does a Robo-Advisor Offer?

Robo-advisors are available through a number of providers, and the services they offer may differ. Common services to look for include:

- Automatic rebalancing of your portfolio (or rebalancing set at regular intervals)

- Tools you can use for other financial planning services (such as a retirement calculator)

- Tax-loss harvesting

6. What Are the Alternatives to Using a Robo-Advisor?

If you’re interested in investing but don’t believe a robo-advisor is a good fit for your needs, you primarily have two options to choose from.

You can work one-on-one with an investment or financial advisor to develop a customized, tailored portfolio. This is a much more personalized approach, and it involves utilizing the expertise and guidance of an industry professional. Some advisors now incorporate robo advisor platforms into their own offerings, allowing them to work with younger clients (or those who don't yet meet their asset minimums).

The other option is to take an entirely do-it-yourself (DIY) approach to your investments. This would include researching and selecting all of your investments (stocks, bonds, real estate, etc.) on your own. Some investors choose to work with a financial planner to build a comprehensive financial plan, but choose to take an entirely DIY approach to their portfolio.

Selecting a robo-advisor, especially if you’re investing with a smaller amount upfront, can be an opportune way to begin building your portfolio. If you’re unsure of whether one is right for you or not, start by comparing and contrasting robo-advisors on the market. And if you’re currently working with an advisor, they may be able to help you decide what would work best for your unique investment needs.

Franklin Madison Advisors, Inc. (“FMA”), is a registered investment adviser firm with its registration and principal place of business in the Commonwealth of Pennsylvania. Registration of an investment adviser does not imply a certain level of skill or training. FMA is in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which FMA maintains clients.

This commentary and forecasts are limited to the dissemination of general information pertaining to Franklin Madison Advisors’ investment advisory services and general economic and market conditions and are subject to change without notice. The information contained herein is not intended to be personal, legal, investment or tax advice or a solicitation to buy or sell any security or engage in a particular investment strategy. For additional information about FMA, including fees and services, please contact FMA or refer to the Investment Adviser Public disclosures.

FMA may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Any subsequent, direct communication by FMA with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For additional information about FMA, including fees and services, please contact FMA or refer to the Investment Adviser Public disclosures. Please read the disclosure statement carefully before you invest or send money.

Take these 5 Back-to-the-Basics Steps when Markets Move Against You

Market volatility can have a way of derailing your best-laid investment strategy. So, what can you do to reduce risk when markets move against you? Stay invested and get back to the basics. As with most life situations, when circumstances put up roadblocks to your goals, your first response may be to double down on your current approach instinctively. However, doing more of what you already have done may not only deplete your resources, it may also exacerbate an already untenable situation.

That's why when markets start moving against you, one of the best things you can do from an investment perspective is to focus on the essentials. While it may be tempting to get out of the markets altogether, fine-tuning some components of your investment strategy could otherwise set you up for long-term success. These steps include evaluating your exposure to market risk, focusing on higher-quality investments, reducing leverage, and diversifying your portfolio. To be sure, taking these actions may enable you to stay in the game for the long-run and improve your odds of achieving your financial goals.

Source: Broadview Macro Research

Step 1: Evaluate Your Market Risk Exposure

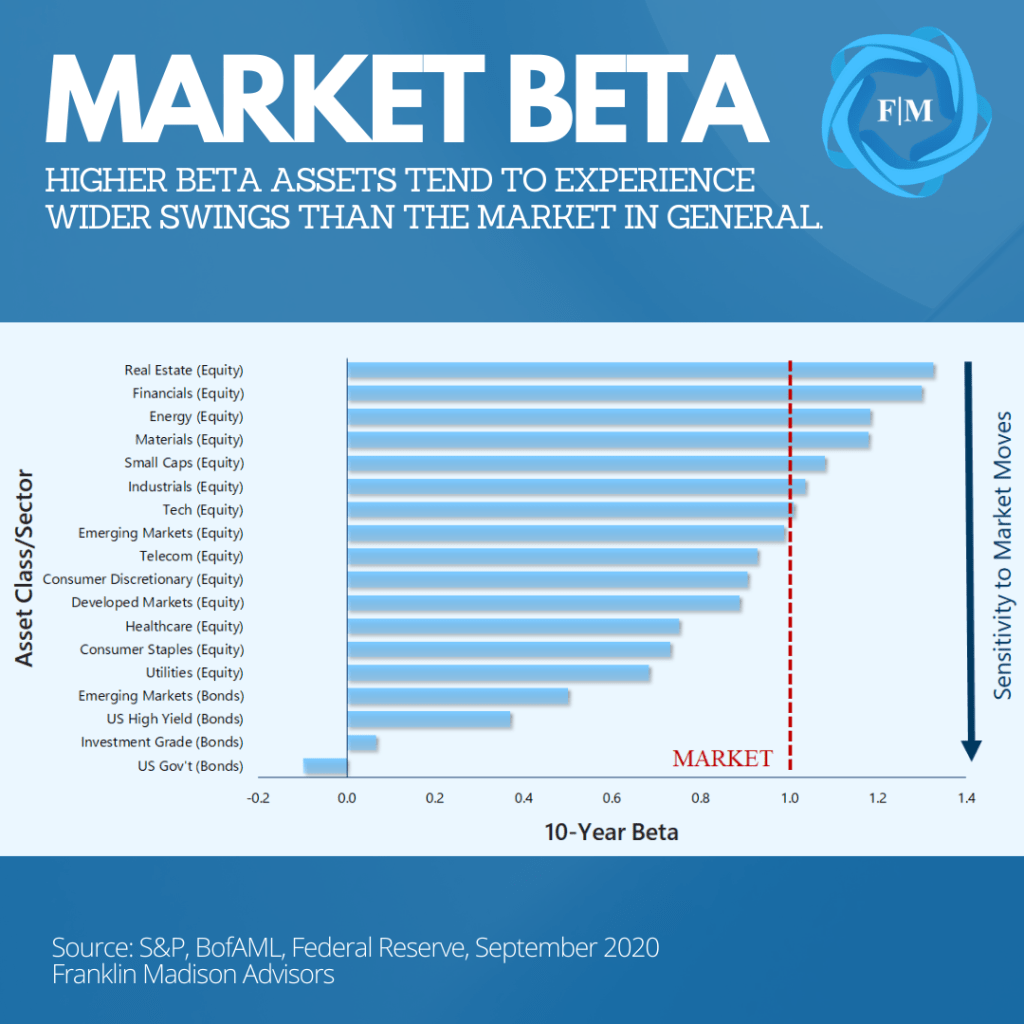

The first essential step you should take when markets start moving against you is to evaluate your exposure to market risk. Beta is one way to quantify this risk, and reducing exposure to it may help you better navigate sharp market swings. Why? Investments with high beta tend to experience outsized moves relative to the broader market when risk assets rally or decline. So, what is beta?

Well, beta is a statistical representation of the movements between a security and a broad measure of the financial markets, like the S&P 500 index. A positive value suggests that a security might move in tandem with the broader markets. Assets with a negative beta tend to move in the opposite direction of the broader markets, while a zero beta suggests little affect in its price relative to the broader markets. And which assets are more prone to move with sharp swings in the markets? Let's look at an example.

History tells us that cyclically oriented equity sectors, like financials, energy, and materials, tend to follow the broader market's moves higher (and lower). On the other hand, fixed income assets like Investment Grade and US Government bonds are less inclined to follow the direction of the broader markets and, in some cases, move in the opposite direction.

Beta is particularly useful when uncertainty rises, and your priority is to reduce the level of swings within your investment portfolio. Holding too many high-beta securities can leave your savings exposed to unnecessary risks and increases the likelihood that you'll fall short of your financial goals when risk assets suddenly decline in value. That's why when market volatility picks up, identifying an appropriate mix of high- and low-beta investments in your portfolio may be vital to reducing investment risk, particularly as you near your savings goals.

Source: Broadview Macro Research

Step 2: Move Up in Credit Quality

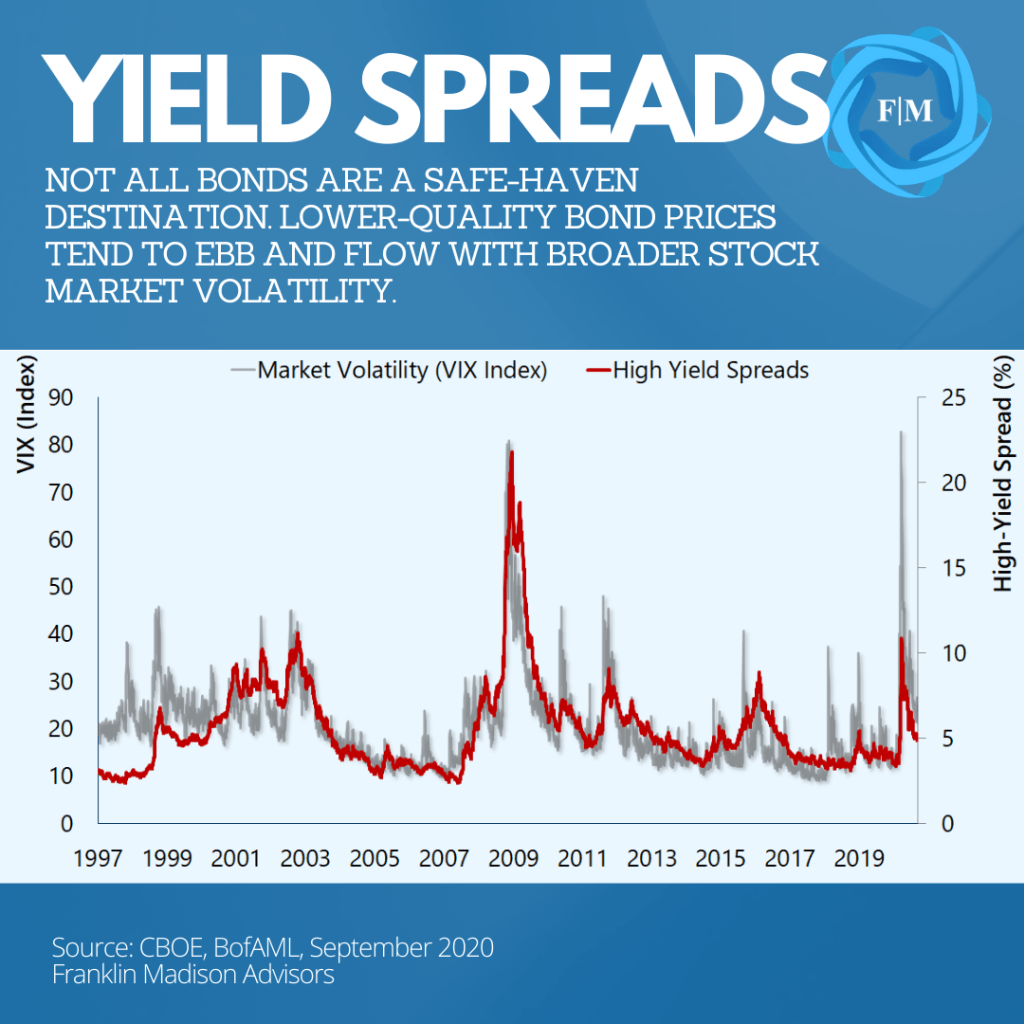

The next step you should take in getting back to investing basics is evaluating your bond exposure and consider moving up in credit quality. Assuming that merely having exposure to bonds in your investment portfolio is a way to hedge against volatility could be a recipe for disappointment. To be sure, not all bonds offer safety from market swings.

This point is evident in how yield spreads of low-quality bonds tend to rise during periods of heightened market volatility. Historical data show that when the VIX (a measure of market volatility) rises, the price of lower quality bonds falls, and yields move higher relative to higher-rated fixed-income assets, like government bonds.

In fact, history has shown that the spread between high yield and US government bonds can widen by as much as 20% during periods of heightened market volatility. For example, during the market selloff in early 2020, spreads went from less than 4% in January to 11% in March. Such price behavior not only reflects lower risk appetite among market participants, but it also represents a desire among some investors for higher compensation to take on additional risk. This is notably the case for assets that may have a higher degree of financial uncertainty when economic conditions underpinning the securities deteriorate.

As noted earlier, higher beta fixed income assets, like high yield bonds and emerging market debt, tend to move in the same direction as risk assets, like stocks. Indeed, while bonds might be perceived as a more conservative investment, the truth is that certain cash flow, industry, or country characteristics can make them higher-risk investments and susceptible to market ebbs and flows. That's why if you've been using bonds as a way to gain additional yield in your portfolio, you may want to consider higher quality and lower beta fixed-income assets as a way to reduce investment risk.

Source: Broadview Macro Research

Step 3: Consider Cheaper Stock Alternatives

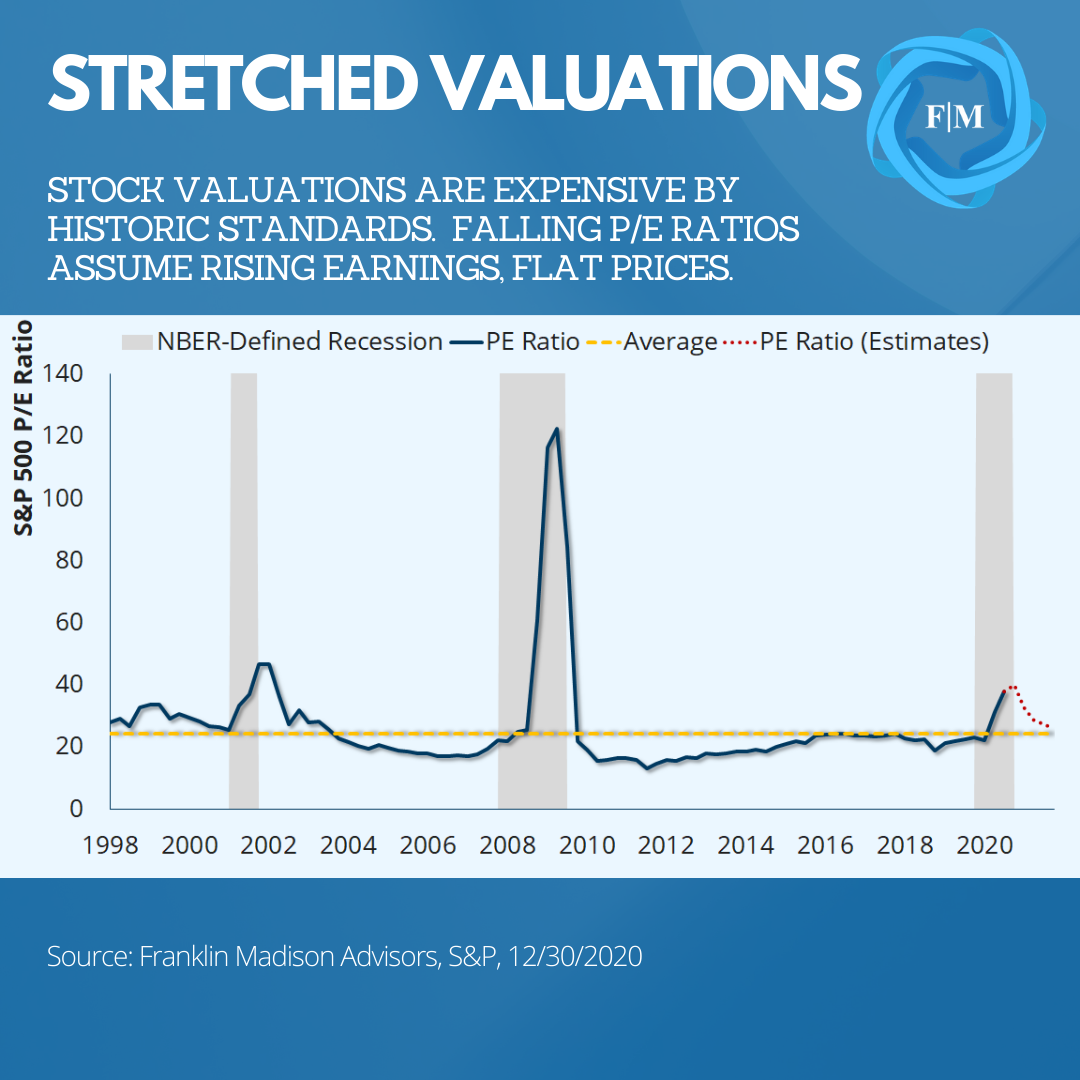

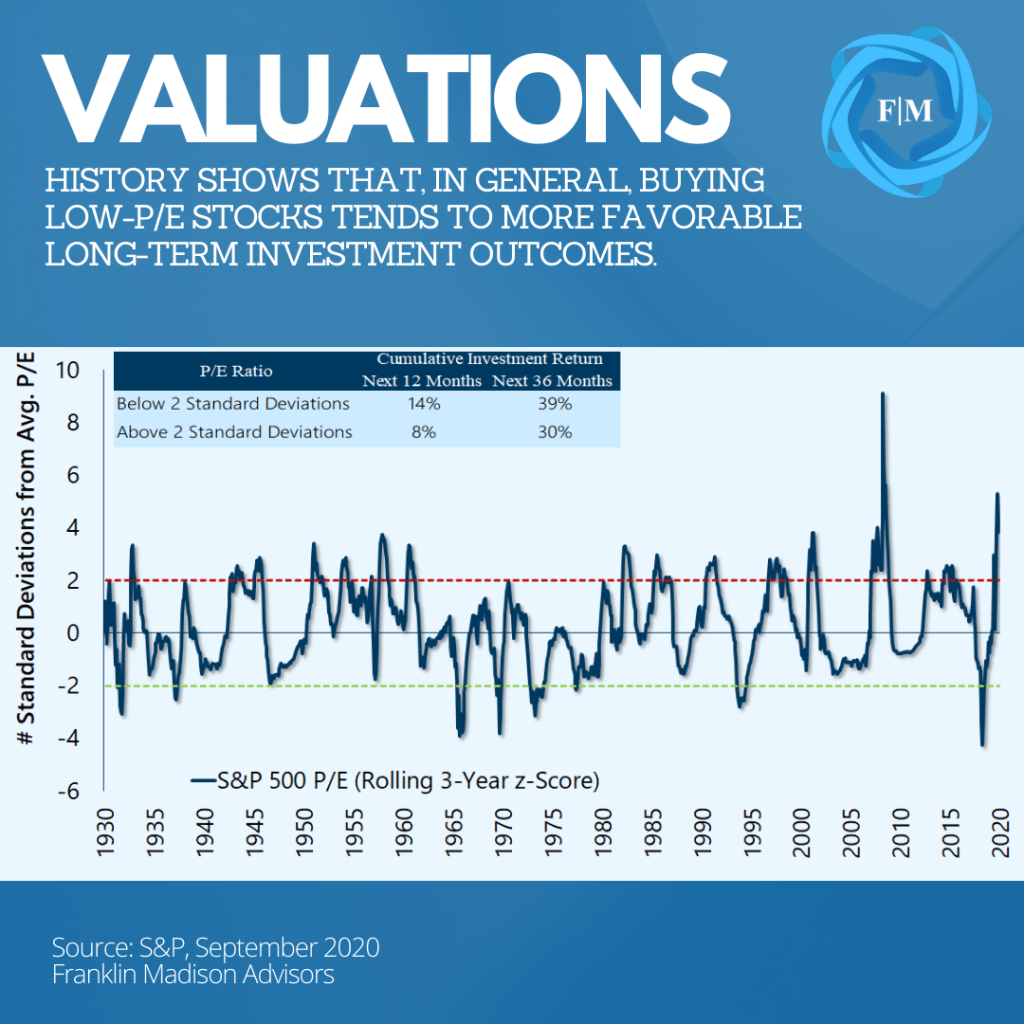

After you've evaluated risk exposure and the credit quality of your bonds, the next thing you might want to think about during a market pullback is whether you're paying too much for stocks. It might go without saying that buying low and selling high is vital to long-term investing success. And while momentum, or recent price action can be an informative value indicator, you may want to consider valuation factors like price-to-earnings (P/E) ratios to determine whether you're paying too much for a given asset.

Why do valuations matter? While it's true that even some high P/E growth stocks can provide investors with positive returns, history suggests that lower P/Es are often associated with more favorable investment outcomes. To evaluate how well this relationship holds, we looked at the historical relationship between P/E ratios for the S&P 500 and subsequent returns over a one-year period. What did we find?

Well, with data going back to the 1930s, our work shows that if you held a portfolio tracking the S&P 500 index when its P/E ratio fell two standard deviations below its mean, you could have received an average annual return of 14%. And how does this compare with purchasing a similar basket of stocks when P/E's are excessively high? Well, buying stocks when they're expensive generated an average 8% returns in the following one-year period.

While our analysis shows that buying high P/E stocks also produced positive returns, the simple truth is that lower P/E stocks tend to outperform over time. The point here is that when the market begins to move against you, one way to set yourself up for a favorable investment outcome is to consider cheaper stock alternatives than what you may already be holding. This includes keeping an eye on high quality, low valuation opportunities.

Source: Broadview Macro Research

Step 4: Reduce Portfolio Leverage

For some investors, trending market behavior presents an opportunity to use borrowed money to boost investment returns. This strategy can work well when prices are moving higher but can amplify losses during a pullback. That's why when markets start moving against you, another critical factor to consider is reducing leverage in your portfolio. Let's take a closer look at how this works.

Leverage usually involves opening a margin account with your brokerage firm, depositing 50% of the value you wish to borrow (this is called initial margin), and hoping that the asset you purchased continues to appreciate. Simple enough, right?

Well, while the value of your portfolio may rise and fall with the markets, the loan you received typically stays fixed. What's more, your broker will also require that your levered investment maintain an equity-to-debt ratio above a certain threshold (maintenance margin). This approach might work well as markets head higher, but when they fall, a time might come when you'll need to raise cash to bring your equity position above the maintenance margin requirement or sell some of your stock to make your broker whole.

And it goes without saying that being forced to sell during a downturn to cover a margin call can amplify losses. That's why overseeing leveraged positions and avoiding a margin call is crucial to managing investment risk during uncertain times. To help illustrate the point, consider the performance of two portfolios that bought on margin heading into a market downturn.

Example: Margin and a Downturn

Let's say that you decide to invest $100,000 into ABC company using $70,000 cash, and $30,000 borrowed from your broker. In this situation, we'd say that your portfolio is 30% leveraged. After initially gaining in value, your portfolio experiences a 40% drawdown over two weeks. While your portfolio avoided a margin call, your net return after accounting for the loan is -48%. To put this number into context, the loss on an all-cash portfolio during this time could be -33%.

And how would this situation look if you had borrowed more money from the start? Well, let's assume that you use $100,000 to purchase the same security, this time with 50% of your broker's money. During the same market downturn, your net return after accounting for the margin loan declines -67%. This two-thirds decline is amplified by a broker's margin call, theoretically leaving you with a more significant hole to climb out of.

The key takeaway here is that if you're using leverage to gain an investing edge, then one of the first steps you should take when the markets are moving against you is to evaluate your use of margin. While this resource can undoubtedly help boost returns when markets are trending higher, it can also open you up for excessive losses during periods of heightened market volatility.

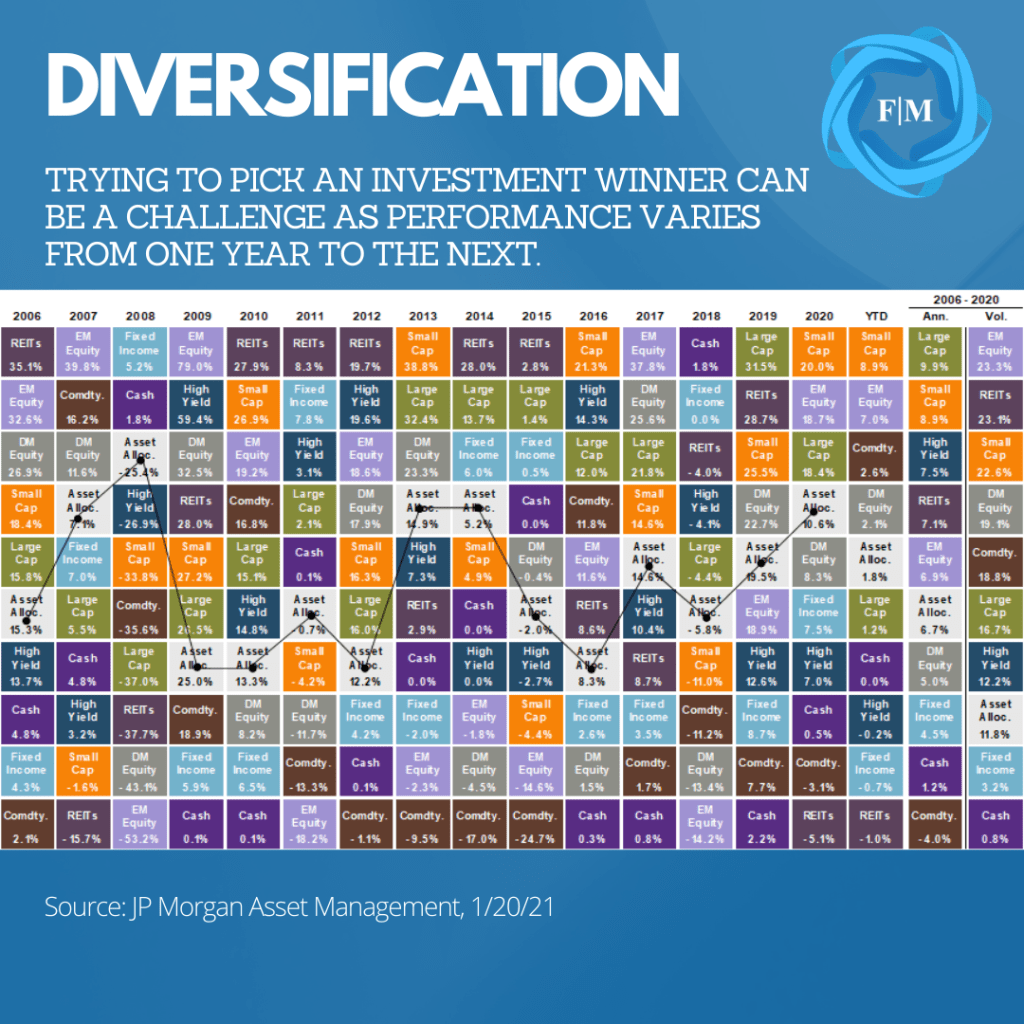

Step 5: Diversify Your Portfolio

A final but crucial step to reducing investment risk during times of uncertainty is to diversify. Diversification can help smooth out investment returns and, more importantly, lessen volatility when the markets begin to move against you. Why is diversification important?

Well, few individuals can predict with certainty which investments will perform well in any given year. In fact, history has shown that an outperforming sector or asset class one year often loses favor with market participants the following year.

For example, if you held one of the largest names in the S&P 500 index, what you're likely to have experienced over the past few decades is annualized volatility as high as 40%. Put differently, while your stock might have an average return of 10% in a given year, that value could swing between a 30% loss, a 50% gain from one year to the next.

This varying performance can be problematic if you're near a critical savings goal and is how diversification comes help. A simple analysis shows that combining just five stocks from the S&P 500 index could cut your portfolio volatility in half from 40% to 18%. In fact, adding 30 stocks to your portfolio might reduce volatility by two-thirds.

The point here is that diversifying your portfolio lets you gain exposure to market returns without having to pick a winner while taking excessive risk rather than trying guess which investment might do well from one year to the next. When paired up with assets of varying correlations, diversification has historically demonstrated its ability to reduce volatility and smooth out portfolio returns.

Get Back to Investing Basics When Markets Move Against You

As with most life situations, when circumstances put up roadblocks to accomplishing your goals, your first response may instinctively be to double down on your approach as a way to achieve success. Doing more of what you already have done, however, may not only deplete your resources, it may also even exacerbate an already untenable situation.

That's why when markets start moving against you, one of the best things you can do from an investment perspective is to focus on the essentials. While it may be tempting to get out of the markets altogether, shifting your investment strategy could be a better set up. These steps include evaluating your exposure to market risk, focusing on higher-quality investments, reducing leverage, and diversifying your portfolio. Taking these actions may enable you to weather a downturn, stay in the game for the long-run, and improve your odds of achieving financial success.

Should You Invest When the Market is High?

Some investors today are worried. They're asking, "is now the right time to get into the markets?" Their primary concern is putting money to work at the top of the market, only to see their precious savings decline in a selloff. And they have good reason to be concerned. Volatility in certain parts of the financial markets remains elevated while asset prices continue to drive higher and, by many measures, are disconnected from fundamentals. So, what should an investor do to avoid losses associated with investing at the wrong time in such an environment?

Maybe you're sitting on cash and asking whether you should put your money to work now or wait until conditions settle down a bit? Truth be told, not investing at market highs is a fallacy because there is generally no wrong time to invest in the markets. More specifically, the right time to be putting money to work in the markets is when your investment strategy balances your income needs with capital appreciation and other savings goals.

In fact, staying out of the markets at an inopportune time might cost you in terms of growth over the long-term for the benefit of avoiding a loss in the short-term. To be sure, the key to navigating financial markets during periods of uncertainty is to avoid market timing altogether. When it comes down to it, investing isn't so much about divining market direction. It is about adhering to a strategy that enables you to achieve and maintain financial independence regardless of where you are in the market cycle.

Remaining Disciplined when Markets Are Uncertain

Our last article discussed methods for staying sane and avoiding unnecessary risk-taking when it appears the market is going crazy. There's little doubt that those principles remain relevant today. Nevertheless, some individuals are sitting on the sidelines, worried about losing money in today's frothy markets and unsure what to do next.

Before we discuss why and how you could invest your savings, let's address a critical anxiety-provoking issue facing many disciplined investors: signs of a market top. By various measures, price action in certain parts of the markets makes little sense today. Some traditional investing theory suggests that an asset's value depends on its future earnings, cash flows, or potential store of value discounted at today's price. Therefore, the value of an asset can be explained, at least in part, by a rational understanding of the underlying factors, or fundamentals, underpinning the directional move in an asset's price.

As we pointed out last month, however, markets are also be fueled by periods of irrational social dynamics rather than logical fundamental analysis. One of the key concepts we previously highlighted to this point was the Greater Fool Theory. And this theory suggests that asset prices will rise solely because some individuals believe that others will be around to bid prices higher in the future. And it's this very phenomenon that has underpinned notable historical asset price bubbles that seem to pop up once or twice a decade. Presently, the gyrations in "meme" and high-flying tech stocks and bitcoin underscore the disconnect between rational decision making and price action.

So how long will the current craziness last? The truth is that no one can divine where the market is heading in the near-term. Still, certain developments would suggest that higher price momentum for questionable assets is coming under pressure. This view has become evident in heightened volatility among penny stocks and cryptocurrencies and rising yields, and other dislocations in the bond markets themselves. Under current conditions, there's little doubt that having money in the market, notably, if you're dependent on that money to cover lifestyle needs in the near-term, is disconcerting at the moment.

Timing the market Isn't an Efficient Investment Strategy

Certainly, there's a sense of comfort that comes from sitting on cash in anticipation of what seems to be an imminent end to an otherwise irrational period in the financial markets. Trying to time the markets, or waiting on the sidelines until the craziness ends, may not, however, be in your best interest. Why? Well, how certain can you be about the timing of a highly anticipated market pullback, and what's the cost of getting the timing wrong? Well, history has shown that missing some of the best days in the markets can cost you significantly, depending on your savings horizon.

For example, over the past 50 years, investors missing out on the ten best days in the markets might have had a portfolio value half the size of those who remained fully invested. On the flip side, you could argue that staying out of the markets during a time of uncertainty could help you avoid losses during a sharp market pullback. While this sentiment may be true to a certain extent, again, you'll need to be able to answer a few key questions to make this approach work: First, when will the selloff begin? Second, how long will the next selloff last? And finally, when should you get back into the market? Will you wait one day, a week, or month for an all-clear sign to reinvest your savings?

The challenge here is that the longer you wait to answer these questions, the more it may cost you as you miss out on periods of critical market rallies that are essential to fueling compounded growth of your savings over the long-term. To understand this concept with a little more clarity, let's consider hypothetical investment performance following sharp market pullbacks.

Now, if we gather data for the ten worst single-day selloffs in the S&P 500 index over the past 50 years and evaluate performance a year later, what does history tell us? Well, the data shows us that during these historic down days in the S&P 500, the index fell an average of 8.8% in a single day. So how did it perform a year later? The same data set showed that the sharp selloff was followed by an average gain of 24% in the following twelve months. The takeaway here is that avoiding the markets altogether could cost you in terms of lost appreciation and compounded growth if you happen to make decisions based solely on market timing.

A Prudent Approach to Investing in Uncertainty: Manage Risk, Stay Disciplined

So, is now the right time to get into the markets? Should you wait until the markets settle before putting your money to work? Well, rather than concerning yourself with the next move, higher or lower in the market, now may be the time to evaluate how you're positioning your investments in the current environment. More importantly, it would help if you considered whether your portfolio is appropriately balanced to meet your short-term living needs and long-term capital appreciation goals.

While the answer to this question will vary from one individual to the next, let's consider how you might be able to approach the market from the perspective of an investor with varying capital distribution and appreciation needs.

The Already Retired Investor

Suppose you're already retired and dependent on your investment savings for income. In this case, your primary concern might be to find an optimal balance between income needs to weather a market selloff in the short-term and continued investment growth to avoid the harmful effects of inflation over the long-run. So how much money should you set aside in your portfolio? While the amount of cash you should have on hand will vary depending on your unique circumstances, one rule of thumb if you're already retired is to have enough cash on hand to cover two to three years' worth of lifestyle needs.

The benefit of this approach is twofold. First, having a few years of cash on hand will enable you to preserve your wealth for the long-term without worrying about the periodic ups and downs in the markets. To be sure, rather than selling all of your investments during a period of uncertainty, remaining fully invested in the markets while holding a higher allocation to cash might enable you to address lifestyle needs without being forced to sell investments at an inopportune time.

Compared to a cash-only portfolio, the second benefit is that allowing a portion of your savings to maintain market exposure might provide continued investment appreciation while avoiding a shortfall should you live longer than expected. Price inflation or a rising cost of living can be detrimental to your retirement plans, especially if you outlive your savings. Even so, history has shown that the longer you invest your savings and allow the power of compounding to work, the less likely you are to experience a cost-of-living shortfall should you live longer than you had planned.

Soon to be Retired Investor

Now, what if you're not yet retired but plan to leave your job in the next few years? Well, one challenge faced by some soon-to-be retirees is the need to reposition their portfolios from a high concentration in stocks or riskier assets to a more diversified, preservation-oriented allocation. During seasons of heightened market uncertainty, you might be tempted to go to an all-cash portfolio when a market pullback seems imminent, and your retirement is just a few years away.

Nevertheless, when it comes to preparing your savings to address long-term retirement needs, going to cash may not be the most optimal approach. In fact, one of the most effective strategies you can consider is to evaluate your income needs during your first few years of retirement, set aside that amount of money, and stick to a disciplined rebalancing plan.

Like individuals who are already retired, having enough cash to cover 2-3 years of retirement expenses might help you avoid selling investments at an inopportune time. More importantly, having the optimal amount of cash on hand might ease your anxiety during periods of market uncertainty, especially as you transition into your post-employment years.

Next, ensure that your investment portfolio is diversified across several uncorrelated asset classes as a means to reduce the time it takes to come back from a market selloff. To be sure, history has shown that, even when you're invested at a market top, a diversified portfolio might recover from losses months and even years sooner than a highly concentrated portfolio as illustrated in the post-Global Financial Crisis period.

Not Retiring Anytime Soon Investor

Finally, what should you do if you don't plan to retire anytime soon but are still concerned about investing near a market top? Well, if your plan for retirement is more than five years away, then one of the most important things you can do today is to ensure that you remain invested for the long-term and stay committed to a disciplined dollar-cost-averaging strategy.

It's vital to recall that riding through periods of euphoria and despair, fear and greed are the cost of admittance to participating in financial markets. If you have a long-term investment horizon, your primary goal should be to allow the power of compounding to make your money work for you, rather than spending your time trying to divine the next move higher or lower in the markets.

To be sure, our earlier example of missing the ten best days in the markets is notably relevant to individuals with a long-term savings horizon. Therefore, rather than trying to figure out whether you should be in or out of the market, take the time to evaluate whether your strategy matches your risk tolerance and investment objective and commit to making the power of compounding work for you.

Should You Invest When the Market is High?

So, with some indices having hit all-time highs, is now the right time to get into the markets? Well, the idea of not investing when indices are near all-time highs suggests a prime time to put money to work. And the fallacy here is that there is no right or wrong time to be invested in the financial markets.

In fact, staying out of the markets at an inopportune time might cost you in terms of growth over the long-term for the benefit of avoiding a loss in the short-term. To be sure, the key to navigating financial markets during periods of uncertainty is to avoid market timing altogether.

When it comes down to it, investing isn't so much about divining market direction. It is about adhering to a strategy that enables you to achieve and maintain financial independence regardless of where you are in the market cycle.