6 Things to Know About a Robo-Advisor

If you’ve considered buckling down and getting serious about your portfolio, it’s likely you’ve come across the term “robo-advisor” before. What is a robo-advisor exactly, and how do you know if one is right for you? We’ve got your answers below.

What Is a Robo-Advisor?

A robo-advisor is also known as an automated investing service or online advisor. Instead of having an individual, such as yourself or an advisor, build and manage an investment portfolio, a robo-advisor does so using algorithms and computer software.

Robo-advisors typically include limited interaction with an advisor, and they can be set up quickly (often in just a couple of minutes).

Common Questions About Robo-Advisors, Answered

Below we’ve rounded up our answers to the most common questions we hear about robo-advisors.

1. What Are the Advantages of Using a Robo-Advisor?

One of the most prominent advantages of using a robo-advisor is the account minimum requirements. Some have no minimums at all, while others will let anyone start investing with just a few thousand dollars. This can be an appealing alternative for investors (such as young professionals) who have not yet acquired the assets needed to hire an investment advisor (since many advisors have minimum AUM, or Asset Under Management, requirements to work with them).

Robo-advisors can help reduce the chance of human error or behavioral bias. They’re automated and use algorithms to invest, making it hard for an investor to make a mistake or gut reaction on their end. It takes the emotional response to market changes out of the equation. While you may be inclined to change your strategy based on what you see on the news, a software program isn’t.

Robo-advisors are also an ideal way to simply “set it and forget it.” They’re typically programmed to automatically rebalance, without a need for you to take any action.

2. What Are the Disadvantages of Using a Robo-Advisor?

Robo-advisors really can’t replace the one-on-one, tailored advice and strategies of an investment advisor. If your investment needs are more complex, or you’re looking to integrate your portfolio into the rest of your financial plan, a robo-advisor may not offer what you’re looking for.

If you have multiple accounts, like a company 401(k) plan, a robo-advisor also may not be able to accommodate these different investment accounts. If you need to integrate these various accounts, you’ll likely want to work with an advisor directly.

3. Who Primarily Uses Robo-Advisors?

Robo-advisors could be considered a “happy medium” between DIY investing on your own and hiring a professional financial advisor. It can be a big time saver and cost-effective option for those who have a simple investment strategy and/or are just looking to automate their investments. In addition, robo-advisors are advantageous for young investors who don’t have the assets or net worth needed to hire an investment advisor, but still would like to get started building a portfolio.

4. What Does a Robo-Advisor Cost?

Robo-advisors vary in cost, but the fee structure is similar across the board. Most robo-advisor services charge a percentage of the assets under management. This is typically anywhere between 0.25 percent and 0.50 percent, but some providers could charge more.

In addition, you may have to pay any fees associated with the investments themselves (such as an expense ratio).

Some providers may offer robo-advisor services as a flat fee for users, rather than a percentage of the assets under management.

5. What Services Does a Robo-Advisor Offer?

Robo-advisors are available through a number of providers, and the services they offer may differ. Common services to look for include:

- Automatic rebalancing of your portfolio (or rebalancing set at regular intervals)

- Tools you can use for other financial planning services (such as a retirement calculator)

- Tax-loss harvesting

6. What Are the Alternatives to Using a Robo-Advisor?

If you’re interested in investing but don’t believe a robo-advisor is a good fit for your needs, you primarily have two options to choose from.

You can work one-on-one with an investment or financial advisor to develop a customized, tailored portfolio. This is a much more personalized approach, and it involves utilizing the expertise and guidance of an industry professional. Some advisors now incorporate robo advisor platforms into their own offerings, allowing them to work with younger clients (or those who don't yet meet their asset minimums).

The other option is to take an entirely do-it-yourself (DIY) approach to your investments. This would include researching and selecting all of your investments (stocks, bonds, real estate, etc.) on your own. Some investors choose to work with a financial planner to build a comprehensive financial plan, but choose to take an entirely DIY approach to their portfolio.

Selecting a robo-advisor, especially if you’re investing with a smaller amount upfront, can be an opportune way to begin building your portfolio. If you’re unsure of whether one is right for you or not, start by comparing and contrasting robo-advisors on the market. And if you’re currently working with an advisor, they may be able to help you decide what would work best for your unique investment needs.

Does Dollar Cost Averaging Still Work?

One of the biggest fears of any new or seasoned investor is losing money. This fear can actually inhibit some people from ever investing at all, and it might also lead to selling preemptively or opting for the lower risk investment option time and again. To minimize the fear of losing money, investors sometimes choose to go with a risk-reduction strategy, such as Dollar Cost Averaging (DCA).

Despite the fact that the majority of academic research has shown that dollar cost averaging may help to manage risk, but that on average it just reduces returns (and therefore is inferior to lump-sum investing), the popularity of DCA remains high among practitioners and the investing public.

However, given that research has shown that the pain of losses is more severe than the joy of gains for investors1, risk-averse investors may prefer to dollar cost average simply to minimize the potential regret of not doing so and seeing markets decline shortly thereafter.

What is DCA?

DCA is an investment tactic in which a fixed amount of money is invested at regular intervals. The intended goal of DCA is to provide the investor with a lower average cost of shares over time. Since the investment amount will be the same at each interval, the idea is that more shares will be purchased when the price is low, while fewer will be purchased when the price is more expensive.

Those who support the use of DCA claim that it can provide a lower average purchase price for a risky asset, proposing that purchases of assets (that are higher risk) with DCA when prices are declining will provide better returns than lump-sum investing.

What are the Proposed Benefits of DCA?

Risk Mitigation

By only investing a portion of your lump sum, price drops will not impact your portfolio as heavily had you invested a larger portion or your entire sum. Dollar-cost averaging is meant to mitigate the risks involved in lump-sum investing through which an investor could face major losses if the market crashes or prices fall drastically. Risk-aversive individuals may, therefore, prefer to use DCA.2

Managing Emotions

Market fluctuations and losses can greatly affect an individual’s emotional well-being. Further, emotional responses to these ebbs and flows, such as overconfidence or panic, can affect future investment decisions.3 Since only part of a sum is exposed to the market, losses may not be as drastic. Therefore, many individuals may experience a duller emotional reaction than if all of their sums were to be affected, decreasing the likelihood of their making emotionally-driven investment decisions in the future.4

As such, DCA may be good option for those looking to minimize the impact of emotion on their investment choices.

What are the Critiques of DCA?

Missing Out On Gains

When employing dollar-cost averaging, portions of your money sit uninvested. The main argument against DCA is that these portions are not given the chance to accumulate any return at all. As a result, some investors and financial professionals may prefer another strategy such as lump-sum investing, which exposes a larger portion of your funds to the market.

Lump-Sum Investing vs. DCA

In lump-sum investing, a larger portion of your money is given the chance to make gains sooner rather than later. However, investing a significant portion of your money also means that you may experience more pronounced losses in a vacuum. Over time, however, you can make up for these losses. This long-term thinking also supports the idea behind dollar-cost averaging. Ultimately, the decision to use either tactic will depend on your unique situation.

When to Consider Using DCA

Investors might choose to employ dollar-cost averaging for a variety of different reasons, including for investments that are historically more volatile. DCA is also a way to potentially regulate emotional responses. Dollar-cost averaging might be used in the following circumstances:

- Volatile investments

- Other long-term investments, such as 401(k)’s or IRA’s

- A time in life where any volatility is not feasible and may cause immediate ramifications (i.e. nearing retirement)

- Individuals who are risk-aversive

- Individuals who do not have the funds for a lump-sum investment

The alleged benefit of dollar-cost averaging is that it encompasses the unpredictability of the market yet intends to lower the cost of your shares as a result. When choosing how to invest, it is wise to seek the counsel of a financial advisor, who can help you make the best choice for your circumstances and future goals.

- https://www.apa.org/science/about/psa/2015/01/gains-losses

- https://www.onefpa.org/journal/Pages/OCT15-Dollar-Cost-Averaging-The-Trade-Off-Between-Risk-and-Return.aspx

- https://www.aeaweb.org/articles?id=10.1257/jep.29.4.61

- https://www.onefpa.org/journal/Pages/FEB18-Using-a-Behavioral-Approach-to-Mitigate-Panic-and-Improve-Investor-Outcomes.aspx

Is Income a Missing Component to Securing Your Financial Independence?

The old adage, “it’s not about how much you make, but how much you keep…” is often applied to the concept of spending and saving prudently. But, what if spending wisely and prudently managing your savings was just a part of securing your path to financial independence?

Make no mistake, managing your cash flows is essential to mastering your path to financial independence. That’s because without a firm grasp of this critical process, having the money you need to accomplish your life goals likely just won't happen.

However, maximizing your take-home pay is another essential financial planning task often overlooked by many individuals.

Indeed, whether you’re still in your earning years or already retired, many individuals, whether their income comes from a paycheck or savings distributions, end up leaving thousands of dollars on the table each year.

So, what are some ways to increase your take-home cash flows?

Well, one way to increase your income is to pay no more tax than necessary.

That's why it's vital to have a plan in place to ensure that you take advantage of all the tax savings opportunities available to you while paying yourself first, as you make smart financial decisions from one month to the next.

Maximize Employer Retirement Plan

One of the most advantageous ways to minimize your taxes is to maximize your pre-tax retirement savings contributions to an employer-sponsored plan. That's because the money contributed to these accounts goes in on a pre-tax basis or before taxes are taken out.

Compared to after-tax contributions, this approach maximizes the amount of money that can grow in your savings over the long term.

For example, let's assume for a moment that your current employer-sponsored retirement account has $250,000 in it. Then each year, you contribute $20,000 to your account on a pre-tax basis that earns 6% annually. At the end of ten years, your portfolio could have grown to $730,000 when making pre-tax contributions.

Now, let's assume for a moment that you made those same contributions on an after-tax basis. Assuming an effective tax rate of 30%, this time around, you’ll only be able to contribute $14,000 after Uncle Sam gets his fair share of your income. Using the same assumptions as before, at the end of ten years, you'd likely have saved around $650,000.

That's a difference of $80,000 just by making a simple choice to prioritize pre-tax versus after-tax contributions. And keep in mind that this difference could be even larger if your employer offers matching contributions to your employer-sponsored plan.

Now, some individuals will set aside some money to their 401k or 403b and then make additional contributions to their IRA, hoping to get an extra tax break. The issue here is that if you're not maxing out your 401k before your IRA, you're likely only getting a fraction of the tax benefit compared to prioritizing all of your contributions on a pre-tax basis.

This is especially the case for high-earning households, as the tax deductibility of IRA contributions is phased out over certain income limits. In contrast, 401k contributions are only limited by the annual amount you can put in, making them a no-brainer choice when it comes to tax-advantaged savings options.

Create Your Own Retirement Plan

Now, for those of you out there who are self-employed or running a small business and maxing out IRA contributions, consider setting up your own employer-sponsored retirement savings plan. While the thought of setting up your own retirement plan can seem onerous, there are straightforward options available that would allow you to make tax-advantaged contributions.

For example, if you're relying on an IRA to fund your retirement savings, then you're missing out on a big opportunity.

For example, options like a Solo 401k, SIMPLE, or SEP IRA allow you to contribute multiples more than an IRA on a tax-advantaged basis and help reduce your overall tax burden. Which one is right for you will come down to the structure of your business. And when it comes to administration, many custodians today make it easy to manage a retirement plan for your business without having to deal with all of the administrative red tape.

Adjust Your W4

Another way to increase your take-home pay is to adjust how much tax is withheld from each paycheck. This approach may be more relevant if you receive a tax refund from one year to the next. Remember, while a refund may seem like a windfall when you receive it, at the end of the day, it's an interest-free loan that you're making to Uncle Sam throughout the course of the year.

To this point, to reduce your odds of a tax refund and increase the amount of cash available to you each pay period, you'll want to adjust your withholding exemptions through form W4. By lowering your exemptions, you can reduce how much money is withheld from your paycheck. Now, before you go out and begin changing your exemptions willy-nilly, be sure to check out the IRS's Tax Withholding Estimator.

This tool will help you get a gauge the ideal number of withholdings to elect on your W4. And when you're ready to make adjustments, be sure to reach out to your HR department or your payroll services provider to make the necessary adjustments.

Maximize Your Equity Compensation

Now, for you tech professionals out there, you'll likely receive incentive compensation in the form of stock options or restricted stock units (RSUs) as part of your total pay package. However, many tech professionals do not fully understand the value and potential of their equity compensation benefits, which can result in missed financial opportunities.

So, if you are the recipient of equity compensation, what are some things you should watch out for to maximize your income?

First, you'll need to understand that equity compensation is tied to your company's overall performance and can increase in value over time as your company grows and its stock price rises. If you're a tech professional who receives equity compensation and yet you're not paying attention to the details of your equity award, you may miss out on the opportunity to sell your stock at a higher price, potentially resulting in a significant financial loss.

Second, there may be restrictions or deadlines associated with equity compensation that you may need to be aware of. For example, RSUs typically vest over a period of time and may be subject to forfeiture if you leave your company before the vesting period is over. Stock options, like ISOs may also have expiration dates, meaning that they become worthless after a period of time. So staying on top of those vesting periods is essential.

Third, tax implications of equity compensation should also be considered. Tech professionals need to understand the tax implications of exercising stock options or selling RSUs, such as ordinary income tax on the difference between the exercise price and the stock price at the time of exercise, as well as potential capital gains tax on the sale of the stock.

Now, it's easy to leave your stock award aside and do nothing with it. That’s why you’ll likely benefit from last month’s discussion on equity compensation housekeeping. You can find resources in the FI|Mastery Journey to review best practices for managing your awards. But at the very least, get to know your equity award and check to make sure that you're taking advantage of opportunities where they're available.

Pre-tax Spending Needs

Another effective way to maximize your income is to pay for regular expenses on a pre-tax basis. A couple of tools available through your employer may include health savings accounts, or HSAs, and Flexible Spending Accounts, or FSAs.

If you have a high deductible health plan (HDHP), for example, HSAs allow you to make pre-tax contributions that can be later used to pay for medical expenses. This account type also has an investment component built into it that allows your savings to grow over the long term.

Another way to spend on a pre-tax basis is to utilize a Flexible Spending Account or FSA. These accounts are typically a use-it-or-lose-it type of account. And this means that any contribution you make during the course of the year must be spent, or you'll lose that money by the end of the year.

Even so, these types of accounts still offer some advantages.

For example, let's assume for a moment that you spend $10,000 per year on childcare expenses. If your employer offers a dependent care FSA, a household is allowed to contribute $5,000 annually to this account on a pre-tax basis. Assuming that your effective tax rate is 24%, your $5,000 gives you a savings of $1,500 annually on that contribution towards your childcare expenses that you may have otherwise paid for on an after-tax basis.

Review Your Employer's Group Life Coverage

Another way to keep more money in your pocket is to evaluate how you're paying for life insurance. Now, whether you have a family or are just getting started, life insurance is often a cheap way to transfer financial risk should something happen to you.

And if you have an individual life insurance policy but are not taking advantage of your employer's group policy, you may be paying more for that individual policy than what's available to you through your employer's group benefit.

Renegotiating Your Pay

Finally, consider asking your employer or clients for more money. This may include having an awkward conversation that could end up netting you a few extra thousand dollars per year. This approach could involve either asking for raise or negotiating an off-cycle increase in your incentive compensation, such as a bonus or off-cycle equity grant.

And if you're self-employed, now may be the time to evaluate the fees charged to your clients. Given the recent cost of living increases, now may be an opportune time to raise your prices to reflect the value of your services and rising overhead costs.

Increasing the take-home income component of your cash flows can help ensure that you achieve your spending and savings goals for the year. While earning more money is certainly one way to accomplish these goals, being more tax-efficient with your cash flows is a more controllable approach to bringing home more money from one pay period to the next.

Maximize Your Post-Employment Income

Now, if you've already achieved your financial independence goals and are living off retirement savings, then finding ways to maximize your take-home salary may seem less relevant to you.

Even so, while fine-tuning your earnings ability was a key consideration during your accumulation years, focusing on the income-producing capabilities of your savings nest egg will be essential to staying strong financially in retirement.

Now, while some rules of thumb will guide you on how much you should safely withdraw from your portfolio from one year to the next, the fact is that a disciplined investment process will be essential to preserving the value of your potential lifetime retirement income.

To this end, there are two approaches you should consider when it comes to maximizing the potential retirement income generated by your investment portfolio this year: 1) your investment strategy and 2) your cash management strategy.

Let's take a look at how ways you can maximize the income-producing ability of your retirement savings:

Diversify Your Investments

First, one of the most important steps you can take to maximize the sustainable income from your investment portfolio is to diversify your investments. To do this, ensure that you're spreading your assets across various types of investments, including stocks and bonds, US and international investment assets. This approach will help reduce your portfolio's overall risk and ensure a reliable income stream throughout your retirement.

Indeed, setting an appropriate mix of stocks and bonds, US and international assets, is essential for preserving the income-producing capabilities of your retirement savings. And the degree to which you allocate between various asset classes influences your investment rate of return.

For example, a larger allocation to historically riskier assets could generate a higher rate of return for your investment portfolio compared to allocations to typically conservative assets like government bonds.

So, how much should you contribute to each mix? Well, start by evaluating your risk tolerance and preparing your investment policy statement to find the right mix for you. This approach will be essential to crafting and sticking to a disciplined investment process in the years ahead.

Consider Passive Investment Strategies

Next, consider allocating your savings to passive investment strategies, such as exchange-traded index funds (or ETFs). These vehicles are often lower cost and easier to manage than actively managed portfolios. This can help you maximize the income from your investment portfolio by reducing the amount of money you need to spend on fees and expenses.

Consider Tax-Efficient Sources of Income

Another way to maximize the income from your investment portfolio involves understanding how that income is taxed. For example, capital gains, dividends, and interest income can all be taxed at different rates. Therefore, if your portfolio composition, or the allocation to a particular security or asset class, is heavily weighted towards taxable income, you could be giving away more of your income to Uncle Sam than necessary.

Therefore, one way to produce tax-efficient income for your portfolio is through munis. Municipal bonds, also known as munis, are debt securities issued by state or local governments to finance public projects such as infrastructure, schools, and hospitals.

In a retirement investment portfolio, municipal bonds can serve as a source of stable, tax-free income. Since the interest earned on munis is often exempt from federal and state taxes, they can be especially attractive for individuals in higher tax brackets who are looking for ways to reduce their tax liability.

Munis can also add diversification to a portfolio, as their performance is often uncorrelated with stocks and other bonds. However, it's essential to consider the credit risk of the issuer, as well as the market risks associated with bonds, before adding munis to a retirement portfolio.

Reduce Your Future Tax Liability

Another way to increase your retirement income is by reducing how much tax you're paying to Uncle Sam. To achieve this outcome, you'll want to evaluate the tax efficiency of your portfolio. If you expect your taxable income to rise after retirement, especially when required minimum distributions (or RMDs) kick in, consider ways to reduce your future tax liability.

In some cases, evaluating the benefit of a Roth Conversion might make sense. A Roth conversion is the process of moving money from a traditional individual retirement account (IRA) to a Roth IRA. By converting a traditional IRA to a Roth IRA, a retired individual may be able to reduce their future tax liabilities by establishing a source of tax-free withdrawals, reducing or eliminating RMDs, and generally putting them in a lower overall tax bracket.

Rebalance Your Portfolio Regularly

Another way to maximize income over the long-term is to potentially mitigate near-term losses in your portfolio through regular rebalancing. As markets fluctuate, your portfolio's asset allocation may change, which can impact the sustainable withdrawal rate you can generate from your investments. To avoid this, consider rebalancing your portfolio regularly to ensure that your desired asset allocation is maintained.

Consider Inflation-Protected Investments

Now, if you're reliant on your retirement savings to cover your living expenses, you'll need to be mindful of the effects of inflation. Inflation is a natural part of the economy, but over time it can erode the purchasing power of your investment portfolio. To combat this, consider whether investing in inflation-protected investments, such as Treasury Inflation-Protected Securities (TIPS), can help preserve your purchasing power over the long term.

Have an Adequate Cash Management Plan

And finally, another critical component to preserving your spending ability when drawing down assets is having an adequate cash management plan in place. This means having enough cash on hand within your portfolio to cover 12-18 months' worth of living expenses.

Why so much cash on hand?

Well, after a year like 2022 in the markets, the last thing that you want to be doing is selling securities in a down market to cover your living expenses.

Either way, finding ways to maximize your income from your investment portfolio is vital to ensuring that you don't go broke in your post-employment years.

Addressing this concern begins by having an investment strategy and mix of assets that fit your overall risk tolerance, goals, and objectives. Then, allocating to low-cost, tax-efficient investments likely will ensure that you're keeping more of your money by paying only what is necessary.

And finally, have a cash management plan in place may allow you to weather the ups and downs in the markets without having to sell securities at an inopportune time.

Pay Yourself First

Now that we've discussed ways to maximize your income, whether that's from earned income or retirement income, let's take a few minutes and explore the concept of paying yourself first.

So, what do we mean when we say to pay yourself first?

Well, we're talking about setting aside a portion of your monthly income for savings and investments before paying bills and spending on other expenses. This approach may help you prioritize your financial goals and build wealth over time.

Paying yourself first includes funding your cash management or emergency savings fund and allocating your money to suitable financial accounts.

How to Pay Yourself First

Now, a cash management or emergency savings fund is an essential component of a solid financial plan. It is a savings account that is set aside for unexpected expenses, such as a car repair, medical bill, or job loss. Indeed, having an emergency savings fund can provide peace of mind and financial security in times of crisis.

Evaluate Your Emergency Savings Target

So, how much should you have saved in your emergency savings fund?

Well, one rule of thumb is saving between 3-6 months of household living expenses. Depending on your situation, your financial planner will define this number for you as part of your specific financial plan. Either way, know your number and commit to it.

In terms of where to save that money, here are some options:

High-yield Savings Account

A high-yield savings account is a type of savings account that offers a higher interest rate than a traditional savings account. This means that your money will grow faster, and you will earn more interest over time.

Certificates of Deposit (CD)

A CD is a type of savings account that allows you to deposit money for a fixed period, typically from 3 months to 5 years. CDs usually offer a higher interest rate than savings accounts, but they also have penalties for early withdrawal.

Roth IRA

Roth IRA is a type of retirement account that allows you to invest money after tax, and withdrawals in retirement are tax-free. If you are young and in a low tax bracket, this might be a good option to consider.

Whichever account type you choose to leverage as your savings vehicle, it's always worth considering some best practices to maximize your emergency savings.

Order of Savings Operations

Now that we've talked about ways to fund your emergency savings, where should your money go when it comes to longer-term savings?

Make no mistake, it can be confusing to know which accounts to contribute to first and in what order. As you begin paying yourself, you should contribute to various retirement and taxable investment accounts that give you the most significant tax bang for your buck.

Employer-sponsored retirement plans

The first step in saving for retirement should be taking advantage of your employer-sponsored retirement plan, such as a 401(k) or 403(b) plan. These plans offer significant tax benefits, including the ability to contribute pre-tax dollars. Additionally, many employers provide matching contributions, which is free money and a 100% return on your retirement contributions.

IRA Accounts

After you have maximized your contributions to your employer-sponsored retirement plan, you should consider contributing to an individual retirement account (IRA). Traditional IRA contributions are tax-deductible, and the money grows tax-free until withdrawal. Roth IRA contributions are made with after-tax dollars, but withdrawals in retirement are tax-free.

Taxable Investment Accounts

Once you have maximized your contributions to your employer-sponsored retirement plan and your IRA, you can begin contributing to taxable investment accounts. These are investment accounts that are not tax-advantaged, such as a regular brokerage account. The benefit of these accounts is that you can withdraw money at any time without penalty.

Health Savings Account (HSA)

If you are enrolled in a high-deductible health plan, you may be able to open a Health Savings Account (HSA). The benefit of these types of accounts is that contributions to an HSA are typically made on a pre-tax basis, the money grows tax-free, and withdrawals for qualified medical expenses are also tax-free.

College Savings Plan

And if you have children, consider contributing to a college savings plan, such as a 529 plan. These plans offer some tax benefits including the ability to take tax-free withdrawals for qualified education expenses.

Now, it's important to note that some of these accounts have contribution limits, and it's essential to check the limits and rules to avoid penalties. Additionally, you should consider your overall financial situation and goals when deciding how much to contribute to each account.

Ultimately, the most important thing is to find an account that works for you, that you are comfortable with, and that you can access easily in case of emergency.

Setting up a savings plan, tracking your spending and cutting back on unnecessary expenses are all effective ways to build an emergency savings fund. Remember, it's never too late to start building your emergency savings fund, which is necessary to achieve financial stability.

The Missing Component to Achieving Financial Independence: Maximize Your Income

By taking steps like maximizing pre-tax retirement contributions, creating a self-employed retirement plan, and adjusting your W4, you can minimize your tax burden and in many cases maximize your income.

And the result is more money in your pockets and a secure financial future.

But it doesn't stop there. Maximizing the income from your investment portfolios is crucial for a strong and sustainable retirement. Diversifying our investments across stocks, bonds, US and international assets, and allocating your savings to passive investment strategies like index funds, can reduce overall portfolio risk and increase your retirement income. Plus, by finding tax-efficient sources of income, reducing future tax liabilities, and investing in inflation-protected investments, you can take control of our financial future.

But it all starts with a disciplined investment process, a deep understanding of the tax implications of your portfolios, and a careful consideration of all the factors that impact your retirement income. With the right strategies in place, financial independence is well within your reach.

Finally, the key to maximizing your income is to avoid letting it be diverted to the inevitable financial setback. By establishing a solid cash management or emergency fund, you can secure your financial stability in times of crisis. Whether it's through a high-yield savings account, CD, Roth IRA, or other options, the key is to evaluate our emergency savings target, choose the right savings vehicle, and contribute to it regularly.

The sacrifices may be temporary, but the peace of mind and financial security will last a lifetime. Indeed, taking theses steps will not only allow you to maximize your income, but they’ll also take get you one step close to becoming the master of your own financial independence journey.

Hold Tight in this Financial Meltdown

US equity markets have officially erased their summer gains. The Dow Jones Industrial Average is back in bear market territory, and the S&P 500 is on pace for its worst year-to-date start in recent history. Adding insult to injury, rising US Treasury yields have pushed borrowing costs to seemingly unsustainable levels as mortgage rates in some markets are now above 7% from around 3% just months ago.

It feels like the financial system is about to break.

The fact is that we’ve been here before. In many ways, today’s financial environment is similar to the one that played out during the height of the Global Financial Crisis in 2008.

And I’m taken back to the early years of my career when our Chief Investment Officer held weekly calls for our advisors to help them navigate the market volatility.

If you’ll recall, at the time, Countrywide was handed over to Bank of America months earlier, while Lehman Brothers and Washington Mutual had just gone under. Money markets had just “broken the buck”, AIG was getting bailed out, and Wachovia was pushed into the arms of its competitor for pennies on the dollar.

Fourteen years ago this week, the financial system was melting down in front of my very own eyes.

Understandably, our clients (and team of advisors), were panicking. The floor was falling out from under many individuals’ retirement plans and overall financial well-being. At the time, market participants and households alike were looking for simple answers to a challenging situation.

Now, our weekly calls involved hundreds of investment professionals, and many of them felt like they needed to do something. Some advisors wanted to implement exotic derivative strategies to stem the losses in client portfolios. Others suggested buying specific stocks or sectors amidst the selloff. And other advisors were doing everything they could to stop themselves from simply getting out of the markets altogether.

So, what was the advice from our Chief Investment Officer?

Hold tight.

The advice offered then still holds merit today, and here’s why.

Why You Should Hold Tight

As the financial system was coming unglued in fall of 2008, few individuals knew what the path forward would look like. Investors were desperately looking for a catalyst to drive financial assets higher, but a positive market narrative was nowhere to be found.

The old rules of how the financial system should function in many ways no longer applied during that time.

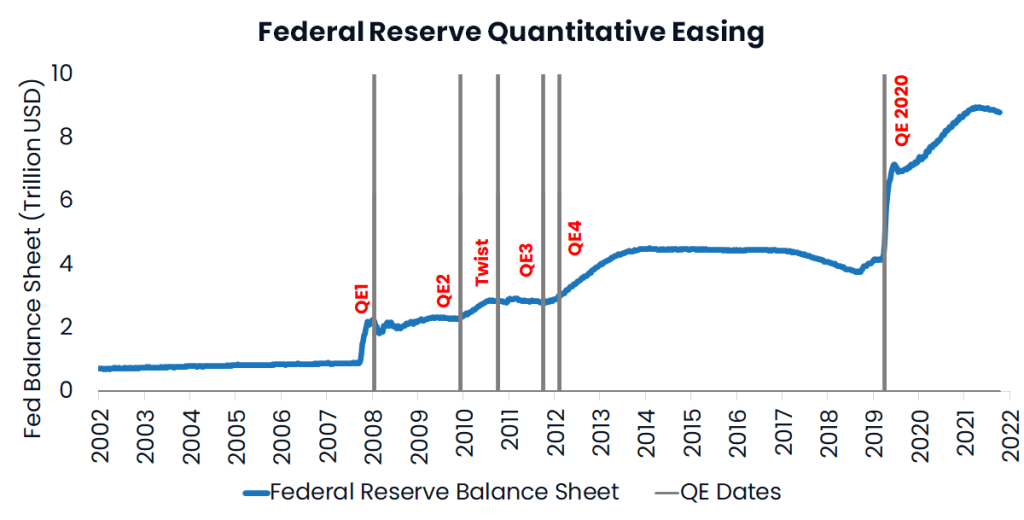

Even so, policymakers stepped in with creative approaches to undergird the financial system. As you’ll recall, in October 2008, the US government introduced the Troubled Asset Relief Program (TARP) to prevent other financial institutions from failing.

In November of the same year, the Federal Reserve launched a historic quantitative easing program aimed at buying up bad debt and restoring confidence in the financial system by showing that policymakers had “tools in the toolbox” to address the market dysfunction. The central bank also introduced a number of measures to support global central banks that had been experiencing stresses in international markets.

By March 9, 2009, market participants were finally convinced that the right set of tools were in place to avoid any further catastrophic collapse in the financial system, and risk assets susbequently rallied.

In the year that followed the March 2009 lows, the S&P 500 index would nearly double in value and then rise by around 600% through December of last year.

Now, there are some individuals whose investment experience was far worse than the broader market. It was those individuals who got out of the markets in January 2009, waiting on the sidelines for an “all-clear” signal before putting their money back to work.

Keep Moving Forward

The point here is that when it seems like the world is crumbling around you and the path forward appears ambiguous, the best course of action may be to simply hold tight and keep moving forward.

Indeed, three fundamental principles apply here when it comes to managing your finances in times of uncertainty:

- Focus on what you can control

- Try not to get caught up in the emotions of the day, and;

- Stay in the present moment

What You Should Focus On

To the first point, there is only so much that we can control when it comes to managing our lives or our money. During times like today, I’m often reminded of an illustration from Carl Richards over at the Behavior Gap. It’s a Venn Diagram with two circles.

In the left circle are the “things that matter.” And in the right circle are the “things you can control.”

When you bring the things that matter, and things you can control together, what you find is that there are only a few items in life that you should be focused on when the economy or markets are in decline.

These areas should include reminding yourself of the long-term financial purpose that you’ve defined for your wealth, and the plan you’ve put in place to address times like these when the markets go south.

These actions could include reevaluating your investment strategy to ensure that your holdings are aligned with your long-term goals. It can also mean ensuring that you have a cash management strategy in place to avoid having to sell investments at an inopportune time.

Stay Objective

The next component to holding steady in times of uncertainty is to remain objective and avoid getting caught up in emotions when the markets are gyrating up and down.

Now, it’s been said that watching the stock market every day is like watching someone play with a yo-yo while riding up a moving escalator.

You’re likely to feel a high degree of stress if you focus on the yo-yo rather than where the escalator is headed.

If you find yourself worried about the markets and glued to financial media desperately seeking out answers, now may be a good time to turn off the TV and go for a walk.

There’s no better time than the present to remind yourself that over the long-term, financial markets have historically rallied after periods of extreme volatility. Remember, the role of financial media often is to sell emotion and rarely to provide any meaningful advice.

And if you find yourself stressed and still looking for answers, now may also be a great time to reach out to your trusted advisor to get an objective opinion on your options.

Stay in the Present

Finally, it’s vital to stay present in uncertain times like these. John Kabat-Zinn had a saying that “wherever you go, there you are.” What this means is that the one constant we have throughout our experience with money (or life in general) is how we deal with the present moment.

There’s nothing we can do about the past and very little we can do about future events outside of our control.

That’s why during these times of economic and market uncertainty, it’s essential to focus on what you need to do right now. Not sure what to do? Then go back to your financial plan and remind yourself what you need to do now to make your goals a reality.

Don’t have a plan?

Well, there’s no better time than the present moment to put one together. Either way, avoiding rumination on past or upcoming financial decisions begins with staying focused on what needs to be done right now in the present.

Where to from Here?

Make no mistake, the events unfolding in financial markets today feel ominously similar to the events that took place fourteen years ago this week. Equity markets at home and abroad seem to feel like they’re in some sort of freefall. The US dollar’s strength is squeezing international financial markets while bond yields are heading relentlessly higher and stocks are moving lower.

And the key reason that markets are behaving the way they are today is mainly due to uncertainty around what appears to be a self-inflicted wound from policymakers: a desire to inflict pain in order to tame inflation expectations.

It’s scary out there, and it feels like things can only get much worse.

But here’s what’s key: we’re going to get through this market dislocation just like we did during the Global Financial Crisis, Savings and Loan Crisis, Energy Crisis of the ’70s, and so many other crises from the past.

The solution to today’s high government debt and experiment in money printing likely will require a solution that hasn’t been presented yet.

For now, policymakers appear to be out of tools that address historically high inflation while avoiding a crash in the economy and financial markets.

What history has shown, however, is that when it seems like it can’t get any worse and there’s seemingly no way out, a solution eventually finds a way, allowing risk assets to breathe a sigh of relief and rally higher.

Until then, hold tight.

Eight Minutes that Derailed the Bull Market

By some measures, Fed Chair Jerome Powell derailed the fledgling bull market rally in U.S. and global risk assets last Friday. In eight short minutes, the central bank governor drove home the point that the Federal Reserve would do everything within its power to halt inflation, including bringing economic “pain” to U.S. households and businesses alike.

For the markets, it was a halting realization given the fact that the recent market rally had been predicated, at least in part, on the Fed pausing rate hikes and giving the economy some breathing room as various data points have shown that a U.S. recession is looming on the horizon.

But not anymore.

On Friday, Jay Powell briefly laid out a case explaining why it’s essential for the Fed to focus first on inflation, not the economy or the markets. To that end, he ended his speech with a determination to bring inflation back to normal by stating that:

“We are taking forceful and rapid steps to moderate demand so that it comes into better alignment with supply, and to keep inflation expectations anchored. We will keep at it until we are confident the job is done.”

- Federal Reserve Chairman Jerome Powell, Jackson Hole, August 26, 2022

The Narrative Shift

So, where does this put the markets now? Has the temporary bear market rally finally given way to a broader selloff that could last for months? Or are we experiencing the birth pains of a broad rally in global risk assets?

Well, to recognize where markets may be headed, we often need to understand what can drive prices either higher or lower on a day-to-day and week-to-week basis. And more often than not, markets are driven by a balance between fundamentals and narratives.

So, what’s the difference here? Well, fundamentals look at how the underlying top-down economy could affect corporate earnings and hence, an investor’s overall return on their investments.

When markets are driven by narratives, on the other hand, investors are mainly betting on expectations that fiscal or monetary policies or broad geopolitical developments could affect the overall market direction despite what’s going on in the corporate earnings or the broader economic environment.

Now, while fundamentals are important, it’s likely today that markets are being driven by a broad market narrative.

So, what narrative is driving the markets today? Well, up until Friday, the critical narrative being watched by investors here in the U.S. and around the world was whether the Federal Reserve’s aggressive monetary policy would give way to a more accommodative stance next year. Some have dubbed this the “Powell Pivot.”

Certainly, headline inflation has increased this year, and the Federal Reserve has made some efforts to hike policy rates to curb rising prices. The idea here is that as businesses and households spend less, there will be less demand for goods and services, and hence, prices and inflation could subsequently fall.

So far, the Fed has raised rates four times this year and is expected to do so again at its three remaining meetings in September, November, and December. After that, market expectations had been that policymakers could “pivot”, or stop raising rates and keep them steady, maybe even start cutting interest rates in response to what’s expected to be a recession later this year or early next year.

Now, it’s essential to note that financial markets are in many ways a forward discounting mechanism. As Warren Buffet once put it, “in the short run, the market is a voting machine, but in the long run, it is a weighing machine.”

The rally that we had seen in U.S. risk assets up until last Friday likely had to do with the notion that investors were betting that, even as the economy slows and likely heads into a recession this year, policymakers would likely pivot to a more accommodative stance (like stable or lower interest rates in the coming months).

It’s this narrative-effect that arguably led to the March 2020 rally during the height of the pandemic and also helped juice risk asset prices in 2009 during the Global Financial Crisis, which led to multiple rounds of Quantitative Easing (QE).

So, will they or won’t they?

By some measures, Friday’s Jackson Hole speech was not only disappointing, it in many ways it derailed what had been a time-tested narrative that the Fed would adjust policy to support an ailing economy and hence provide a boost to financial markets. The key takeaway from Jay Powell’s Friday speech is that rescuing the economy is not a priority for policymakers this time around.

Why?

Well, keep in mind that the Fed failed to catch the early signs of inflation when it first started accelerating last year. Since then, policymakers have been heavily criticized for calling inflation transitory when in fact, it was more persistent than expected.

From this perspective, Powell and the Fed are trying to save face and make up for a series of policy missteps from last year. Put differently, it appears that policymakers would rather err on the side of being too aggressive and tamp down inflation at the expense of economic growth rather than stopping too soon to save the economy, only to prolong its battle with inflation for years to come. For now, the expectation is that the Federal Reserve will continue to raise interest rates until the end of this year.

So, when will the pain end?

How long rate hikes continue and the magnitude of which will be dependent on incoming economic data. And of significance will be inflation data, and not just headline inflation, but namely the Fed’s preferred measure of inflation, which is PCE inflation, as well as producer prices, energy prices, import prices, and the like.

Put simply, inflation data will be essential to the Fed policy narrative and market direction in the coming months. With headline inflation seemingly turning a corner in July, all eyes will be on the August inflation report due out mid-September to evaluate whether the trend of slowing inflation has some legs.

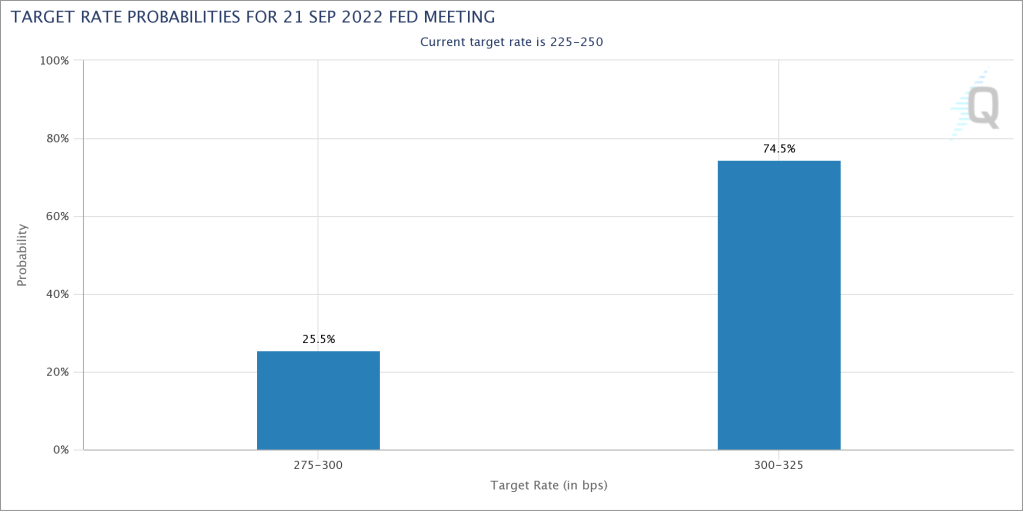

As it stands today, however, markets still expect the Fed to raise interest rates by 75 basis points at its September 21st meeting and another 75 basis points by the end of the year, bringing the top-end of the Fed Funds rate to four percent!

This rate expectation reflects a more hawkish stance from the Fed combined with the Biden administration’s recent decision to forgive nearly half a trillion dollars’ worth of student loan debt.

Easing Inflation and Shallow Recession Essential to Market Sentiment

So, what does this mean for your investments?

Well, the difference between a short-lived bear market rally and the start of a new bull market likely will come down to how inflation plays out and how resilient the U.S. economy can remain in light of higher interest rates over the coming months.

One area that we’re closely watching as it relates to inflation is housing. Home prices have played a critical role in inflation this year.

For example, shelter makes up nearly a third of the overall CPI basket, and these prices were up nearly 6% on a year-over-year basis in July.

Higher interest rates have nevertheless contributed to weakness in the housing market, which could be a positive development for inflation down the road. For example, existing home sales are down 5.9% from where they were a year earlier, with sales declining for a sixth consecutive month in July. And some real estate firms like Redfin and Zillow are increasingly reporting homes selling for less than asking.

New home inventories have also spiked to levels not seen since 2009 as new home sales have plunged 39% over the past year. In other words, cooling housing market activity could ease rent pressures and subsequently help reduce this key measure of inflation.

At the same time, if energy prices continue to stabilize, agriculture production remains robust and geopolitical tensions in Eastern Europe ease, we could see further positive developments in the inflation story. For now, Friday’s post-Jackson Hole selloff was likely an excuse for traders to take profits after a strong run risk asset rally over the past month.

Nevertheless, we’re likely in for another choppy few weeks in the markets as investors parse through economic data leading up to the September FOMC meeting. At that point, we’ll have a better picture of how pleased policymakers are with the pace of inflation moderation and their willingness to once again support the economy and the markets in the months ahead.

However you cut it, Powell’s eight-minute speech derailed the market’s pivot narrative last week. What investors need now is another broad narrative to support their reason to invest in this uncertain market. Until they do, expect market conditions to remain volatile in the weeks and months ahead.

A Systematic Process for Navigating Market Uncertainty

That’s why it’s essential now more than ever to rely on a disciplined investment process to navigate this period of market uncertainty.

So, what do we mean by investment process? Simply put, we suggest 1) choosing the right mix of assets for a portfolio that aligns with your risk tolerances and objectives, 2) putting money to work in the markets in a disciplined manner, 3) rebalancing portfolios at regular intervals, and 4) finally having a cash management process in place.

Diversify your portfolio

Now, a systematic investment process begins with understanding your own tolerance for risk and adding a set of assets to an investment portfolio that that vary with your overall goals and objectives. What does this look like? Well, for investors with a low tolerance for market swings and a near-term need for access to their assets, a conservative allocation would likely reflect a bias toward more bonds and less stocks.

On the other hand, a more aggressive asset allocation framework could be appropriate for investors who can tolerate wide swings in the markets and have a longer investment horizon. Either way, a solid investment process begins with understanding your preference for risk and your overall investment horizon.

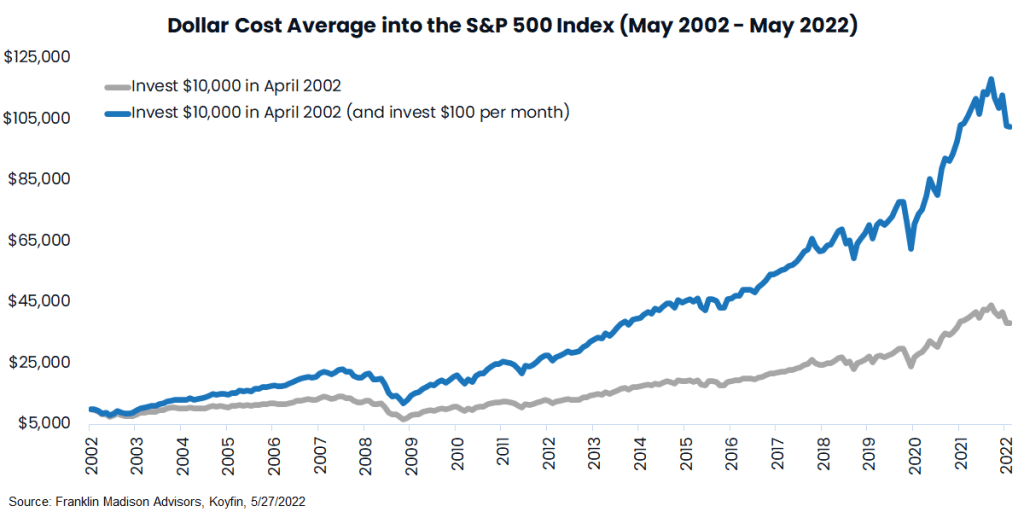

Dollar-cost averaging

The next part of the systematic investment process involves being disciplined with committing capital to an investment portfolio at regular intervals. As we pointed out earlier, trying to time the best and worst days of the markets might have an adverse effect on overall investment performance. To avoid such issues, we recommend dollar cost averaging, or more simply, committing a set sum of money to your investment portfolio on a regular basis.

What does this look like?

If you participate in an employer-sponsored retirement plan, this could involve setting up automatic payroll deductions and having capital committed to your portfolio every pay period regardless of market conditions. Or, a similar approach can be used for after-tax contributions or lump-sum transfers by scheduling cash allocations to your IRA or taxable investment account on a pre-defined schedule. Either way, putting capital to work at set intervals can help reduce cognitive load, simplify decision-making during periods of market volatility and keep your savings goals on track.

Rebalance your portfolio

Another step in the systematic investment process is portfolio rebalancing. Now, rebalancing is essential because, over time, the values of various assets within a portfolio will drift away from their initial allocations as markets move up and down. The purpose, then, of rebalancing is to realign portfolio holdings with their target allocations.

So, when should you rebalance?

Rebalancing can occur 1) on a set schedule, 2) when asset values drift by a certain threshold, or 3) in a combination of the two. For example, rebalancing on a set schedule could involve evaluating portfolio holdings quarterly, partially selling positions that have appreciated, and adding to allocations that have underperformed during that period.

Alternatively, using a threshold to rebalance could involve using a decision rule that prompts a rebalance only when the value of a specific asset class is a set percentage above or below its target allocation. This process could lead to less frequent rebalancing during flat markets but more rebalancing during periods of heightened market volatility.

Cash Management

Finally, if you're in the distribution phase of your investment journey, or in other words, dependent on your savings to pay for your living expenses, then cash management is essential for navigating market volatility without missing out on the best days in the market.

Now, a solid cash management technique ensures that you have access to enough liquid assets in your retirement portfolio to cover between 12-18 months of living expenses. Such investments can include money market mutual funds, and the purpose of this approach is to give your savings enough of a runway to avoid having to sell assets at an inopportune time when the markets begin to sell-off.

Bottom line

When it comes down to it, the Federal Reserve and indeed, many central banks around the world have committed to tamping down inflation and doing so at the cost of the economy at large. This means that we’re likely to see heightened economic and market volatility in the months ahead. Put differently, few individuals know which way the economy or markets will be headed in the next week, month or year.

That's why during times like the present, we challenge investors to ask themselves whether the decisions they are making are aligned with a systematic investment process. This approach includes committing to a target asset allocation framework, deploying capital to the markets in a disciplined manner, rebalancing as appropriate, and having a solid cash management process in place.

Whether you're looking to buy securities at a discount or avoid losses altogether, there's rarely a right time to get into the markets. Nevertheless, we believe that staying committed to a disciplined investment process and using techniques to manage uncertainty during periods of heightened market volatility could help you increase the odds of achieving your lifestyle goals regardless of market conditions and keep you on track to mastering your financial independence journey.

How Age Impacts Your Investment Decisions

Your mindset and goals continually evolve over time. At age 25, you might be focused on paying off student loans and saving up for your first home. Your career is just getting started, and post-work years are well into the future. At 50, however, you’re starting to imagine a time when the career hustle won’t be a part of your life anymore — and neither will your usual income setup. Just as your life changes, your investment decisions may develop as well.

If you’re taking the same risky investment approach at age 50 as you did at 25, you may decide to pump the breaks. And for those who are conservative with decades left until your golden years, you could be leaving money on the table. As you move into new life chapters, it can be worthwhile to re-evaluate your investment decisions.

Investment Risks Over Time

Generally speaking, the younger you are, the riskier you may decide to make your investment portfolio. Earlier in life, many feel comfortable with a high-risk strategy because they won’t be withdrawing for years — they have time to recover and recoup from any losses from incidents such as a sudden market downturn.

Someone who's a few years away from retirement, however, won’t have as much time to recover from a plunge in the markets and may decide to maintain a low-risk strategy. If their portfolio relies too heavily on stocks, their entire retirement strategy could be jeopardized. They may not recoup their losses and could easily drain their other resources while trying to accommodate for this loss of income.

Investing At Various Ages

Along with risk tolerance, your age can also be an essential factor when deciding how much to invest and what types of vehicles to invest in. For example, the higher the percentage of stocks you invest in, the more volatile your portfolio may be. Many may choose to minimize risk and focus on more steady sources of income as they get closer to retirement.

Investing In Your 20s and 30s

After gaining some stability in your life and career, you may be ready to move your money out of a savings account and into a more active role through investments. With 30-plus years ahead of you before retirement, your intention might be focusing on growth over time. For those planning on retiring at least 30 years out (past your 50s), it’s common to have between 70 and 80 percent of your portfolio in stocks. For ambitious savers who are interested in retiring early (age 50 or sooner), you might decide to keep that percentage a bit lower to make room for more steady and conservative options. During your 20s and 30s, other common investment options include real estate, employer 401(k) plans and/or IRAs.

Investing In Your 40s

As you’re inching closer to those peak earning years, your 40s can be an opportune time to double down on steadier investment options. If your employer offers contribution matches to 401(k) plans, contributing the maximum amount now could create a promising payout through retirement. In general, how you invest in your 40s will vary greatly depending on the types of investment options (if any) were made in your younger years, how close you are to retiring and your risk tolerance. In general, most people begin shifting their asset allocation to a more conservative strategy in their forties, with stock allocations closer to 60 or 70 percent.

Investing In Your 50s

How you choose to invest in your 50s will greatly depend on how your current financial picture aligns with your upcoming retirement goals. Take a look at your current income level, nest egg, taxes and projected retirement income. This could help you determine how aggressive your portfolio should remain throughout your 50s. Why? Because now’s the time to focus on creating income for you and your spouse throughout retirement. Depending on when you plan to retire, today’s 50-year-old man is expected to live an additional 31.9 years, while women can expect an additional 35.3 years.1 Incorporating an appropriate amount of risk into your portfolio can help you and your spouse prepare to experience the kind of retirement you want.

How you may decide to invest throughout your career can be based on a number of factors, but it’s always important to take your age and proximity to retirement into account. As you’re analyzing your portfolio’s asset allocation, diversifying and protecting your future retirement income is essential. Reflecting on your investment strategies can create peace of mind as you get closer to retirement age.

How Self Directed IRAs Work: Everything You Need to Know

When it comes to saving for your retirement, there are several options available. It’s important to remember, however, that the best option for you will always depend on your unique preferences and goals. IRAs — or individual retirement accounts — are a popular type of retirement accounts offered in a variety of forms. Keep reading to learn more about the difference between self-directed IRAs and regular IRAs.

What Is a Self-Directed IRA?

A self-directed IRA is a type of traditional or Roth IRA that someone can choose to invest in non-traditional investments with. A regular IRA is typically for those interested in common investment vehicles, such as stocks and bonds. A self-directed IRA, on the other hand, differs in this way. This type of account may be beneficial for those looking to own different kinds of assets in their account — such as real estate, a privately held company or any other endeavor a custodian will agree to.

Self-Directed IRAs: Rules and Limitations

As of 2019, your self-directed IRA total contributions cannot exceed $6,000. However, if you’re 50 or older, you can contribute up to $7,000.1 According to the IRS, this limit does not apply to rollover contributions or qualified reservist repayments.1 A rollover happens when funds are distributed from one retirement account (such as an IRA) and deposited into the same — or a different — account.

Under the SECURE Act’s new rules, there is no age cap for contributing to an IRA or self-directed IRA. In addition, the required minimum distribution age has been adjusted from 70½ to 72 in an effort to match longer expected life expectancies.2

Advantages of Self-Directed IRAs

If you’re someone who prefers having more options, a self-directed IRA could be a good fit for you. That’s because with a self-directed IRA, you can invest in a variety of companies, properties and operations.

If you’re passionate about a certain field or industry, a self-directed IRA offers the opportunity to put your knowledge to the test. Instead of investing in things you know nothing about, you’re able to go after investments you actually have an interest in, which can make the experience much more enjoyable. For example, you could invest in real estate, precious metals, or a privately held company. It’s important to note that regardless of the type of IRA you have, you’re going to need to have a person or company hold the account for you.

Regarding a self-directed IRA’s tax advantages, your contributions could either be fully or partially tax-deductible, depending on a variety of factors. Oftentimes, both the earnings and gains in your IRA are not taxed until they are distributed. Sometimes, this money may not be taxed at all.3 However, if your spouse has a retirement plan at work and your income level exceeds a certain amount, your total tax deduction may be reduced.1

Disadvantages of Self-Directed IRAs

When exploring the possibility of contributing to a Self-Directed IRA it’s also important to consider the amount of responsibility required. Because your custodian will be passive — as in they will simply hold the account without providing investment advice — you will need to educate yourself on investment best practices if you want to generate consistent, positive returns. Additionally, you’ll be in charge of managing paperwork and transactions, which requires ongoing dedication.

In some ways, a self-directed IRA can be seen by some as a part-time job, so you want to think carefully about your own capabilities and time before you make the commitment. For some people, a self-directed IRA may be appealing because of the dedication and commitment it requires to stay focused on changes in the economic environment. Neglecting to do so means running the risk of losing a considerable amount of money. A self-directed IRA is a good fit for people who enjoy the challenge of investing and are eager to learn and grow as the market fluctuates. If this doesn’t sound like you, a traditional or Roth IRA may be a more suitable option.

- https://www.irs.gov/retirement-plans/retirement-plans-faqs-regarding-iras-contributions

- https://www.congress.gov/116/bills/hr1994/BILLS-116hr1994rds.pdf

- https://www.irs.gov/publications/p590a

Is now the right time to get into the markets?

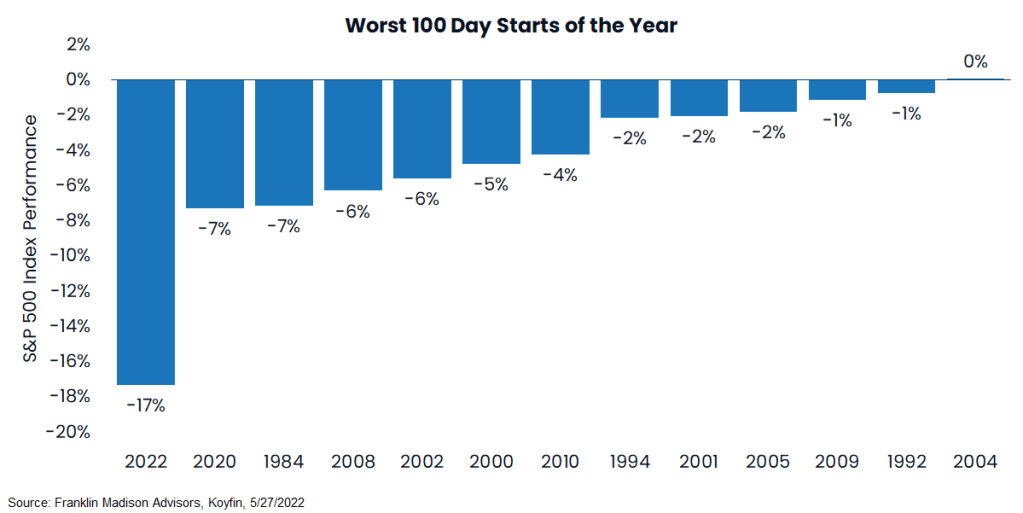

With risk assets having pushed into bear market territory in May, some investors are asking whether now is the right time to get into the markets. On one side of this debate is a group of investors who look at the recent pullback as an opportunity to buy securities at a discount. On the other side is a set of investors concerned that prices will only move lower from here. Make no mistake, this question is relevant to investors today not only because of the magnitude but also because of the breadth of recent market declines.

For example, if we consider year-to-date performance for the S&P 500 index, what we find is that the first one hundred days of this year's market performance have been brutal. Indeed, through the end of May, the data show that U.S. Large Cap stocks have had their worst year-to-date decline in the past forty years. Adding insult to injury, investors have had little place to hide given the fact that stocks and bonds across U.S. and international asset classes have all posted losses this year.

So, why are markets selling off across the board? Well, the reasons behind this seemingly correlated selloff across major asset classes are manifold. But at its core, persistently high inflation and the prospects for an impending U.S. recession given ongoing logistics issues, healthcare concerns, and the war in Eastern Europe have made market participants more sensitive to the effects of less favorable central bank policy and the weaker corporate earnings outlook.

Now, in the past, market participants could look to policymakers to bolster the economy and markets when similar weak or uncertain macroeconomic conditions were present as they did back in 2020. But today, that story has changed. With headline inflation well above 8% this year, Federal Reserve policymakers are keen to continue raising interest rates, even if that means forcing the U.S. economy into a recession.

At the same time, businesses likely will find it increasingly challenging to keep passing along rising prices to consumers as wage growth has failed to keep up with inflation and household pocketbooks become increasingly stretched.

With the economic backdrop poised to weaken, and asset prices declining across the board, is now the right time to get into the markets? Well, with market sentiment being driven by the macro narrative, it can be argued that current economic conditions depend on many factors for which we yet have little clarity. For example, can the world avoid massive food shortages this year and next with a war raging in Ukraine? And, has inflation peaked, and if so, when will it stabilize enough for the Fed to stop pushing borrowing costs higher and higher?

While the answers to these questions are debatable, what is clear is that market participants have a host of broad-based macroeconomic concerns that still need to be worked out. And from this perspective, the prospect of continued volatility across asset classes suggests that timing market entry points (whether that's buying at a discount or avoiding the markets altogether) may be challenging for even the most seasoned investors.

Therefore, in the current environment, we believe that the question investors should be most concerned about is not how to time the markets but rather whether they have an investment process in place to withstand this period of heightened market uncertainty.

Missing the best days in the markets

Indeed, some investors may be enticed to use timing techniques or other short-term strategies in a bid to boost overall returns or to avoid losses completely. Such approaches involve exiting risk assets in anticipation of market moves lower and ratcheting risk back up as market sentiment improves. While such an approach sounds reasonable, getting the timing wrong could be more costly than beneficial.

How so?

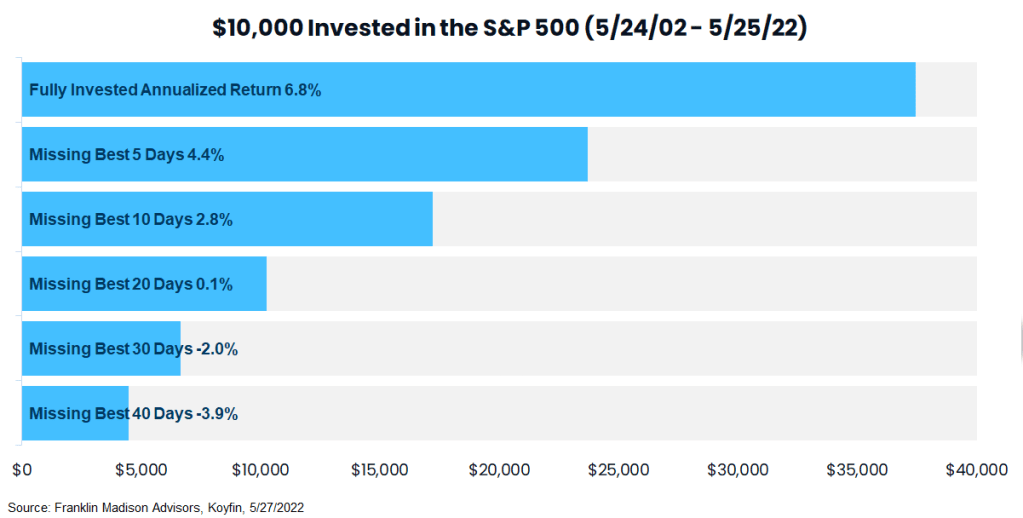

Well, one analysis shows that over a 20-year period, missing even the 10-best days in the market would have led to returns of more than half the rate of those made by investors who stayed committed to the markets during up and down periods.

How is this possible?

Well, history shows that some of the best days in the markets typically follow the worst selloffs. This insight means that investors who had taken money out of the market in fear of a move lower could miss the beginning of a long-term rally. This reality was evident as recently as the COVID-induced market pullback in early 2020 and the subsequent risk asset rally through the end of 2021.

So, what's the point?

Well, unless you have the time, inclination, and experience, getting the timing right on a trade in your portfolio because you're debating whether you should (or shouldn't) get into the markets may cost you more than it is ultimately worth over the long run.

Finding the winning trade

This timing discussion also raises the question about trying to spot winning and losing trades. This attempt to time the market is especially tempting when yesterday's winners are beaten down and appear to be deep value opportunities or a bargain-buy.

Another temptation during the market selloff is chasing what appear to be winning asset classes and avoiding those asset classes that appear to be losing trades. The problem with trying to separate winners from losers, notably during a time of heightened market volatility, is that investor sentiment can shift on a dime, leaving many a portfolio in disarray.

Indeed, some data show that today's best-performing asset class could be tomorrow's laggard and vice versa.

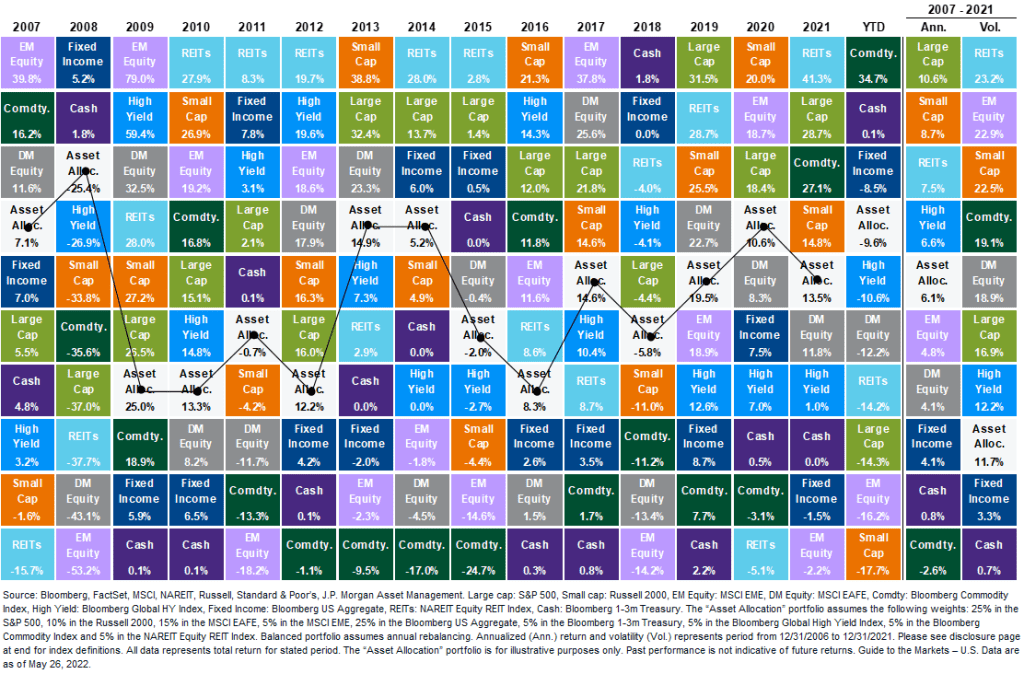

What's more, the variability between stocks and bonds and even domiciles like the U.S. versus international investments tend to vary in performance from one year to the next. That's why an investment portfolio utilizing a diversified asset allocation framework and rebalanced at regular intervals tends to perform more consistently and avoids the wide swings associated with staking a claim in any one asset class. This finding leads us to our final point: a systematic investment process can add more value over time than trying to time the markets.

A systematic process for navigating market uncertainty

To be sure, even some of the best asset managers have had a hard time beating the markets over the past decade, which underscores the importance of a solid investment process. What do we mean by investment process? Simply put, we suggest 1) choosing the right mix of assets for a portfolio that aligns with an investor's risk tolerances and objectives, 2) putting money to work in the markets in a disciplined manner, 3) rebalancing portfolios at regular intervals, and 4) finally having a cash management process in place.

Diversify your portfolio

Now, a systematic investment process begins with understanding your own tolerance for risk and adding a set of assets to an investment portfolio that that vary with your overall goals and objectives. What does this look like? Well, for investors with a low tolerance for market swings and a near-term need for access to their assets, a conservative allocation would likely reflect a bias toward more bonds and less stocks.

On the other hand, a more aggressive asset allocation framework could be appropriate for investors who can tolerate wide swings in the markets and have a longer investment horizon. Either way, a solid investment process begins with understanding your preference for risk and your overall investment horizon.

Dollar-cost averaging

The next part of the systematic investment process involves being disciplined with committing capital to an investment portfolio at regular intervals. As we pointed out earlier, trying to time the best and worst days of the markets might have an adverse effect on overall investment performance. To avoid such issues, we recommend dollar cost averaging, or more simply, committing a set sum of money to your investment portfolio on a regular basis.

What does this look like?

If you participate in an employer-sponsored retirement plan, this could involve setting up automatic payroll deductions and having capital committed to your portfolio every pay period regardless of market conditions. Or, a similar approach can be used for after-tax contributions or lump-sum transfers by scheduling cash allocations to your IRA or taxable investment account on a pre-defined schedule. Either way, putting capital to work at set intervals can help reduce cognitive load, simplify decision-making during periods of market volatility and keep your savings goals on track.

Rebalance your portfolio

Another step in the systematic investment process is portfolio rebalancing. Now, rebalancing is essential because, over time, the values of various assets within a portfolio will drift away from their initial allocations as markets move up and down. The purpose, then, of rebalancing is to realign portfolio holdings with their target allocations.

So, when should you rebalance?

Rebalancing can occur 1) on a set schedule, 2) when asset values drift by a certain threshold, or 3) in a combination of the two. For example, rebalancing on a set schedule could involve evaluating portfolio holdings quarterly, partially selling positions that have appreciated, and adding to allocations that have underperformed during that period.

Alternatively, using a threshold to rebalance could involve using a decision rule that prompts a rebalance only when the value of a specific asset class is a set percentage above or below its target allocation. This process could lead to less frequent rebalancing during flat markets but more rebalancing during periods of heightened market volatility.

Cash Management

Finally, if you're in the distribution phase of your investment journey, or in other words, dependent on your savings to pay for your living expenses, then cash management is essential for navigating market volatility without missing out on the best days in the market.

Now, a solid cash management technique ensures that you have access to enough liquid assets in your retirement portfolio to cover between 12-18 months of living expenses. Such investments can include money market mutual funds, and the purpose of this approach is to give your savings enough of a runway to avoid having to sell assets at an inopportune time when the markets begin to sell-off.

Bottom line

When it comes down to it, asking whether now is the time to get into the markets often misses the point of what it means to be a long-term investor. To be sure, trying to time the markets and hoping to find the next "fat pitch" or winning trade are demeanors often associated with speculative behavior. And, as we have pointed out earlier, such behavior can lead to unfavorable investment outcomes over the long term.

That's why during times like the present, we challenge investors to ask themselves whether the decisions they are making are aligned with a systematic investment process. This approach includes committing to a target asset allocation framework, deploying capital to the markets in a disciplined manner, rebalancing as appropriate, and having a solid cash management process in place.