What do Stretched Market Valuations in 2025 Mean for Portfolio Returns?

The S&P 500’s Unprecedented Rally

Since the start of 2023, the S&P 500 has surged more than 50%, building on a remarkable rally of over 150% from its March 2020 pandemic low. These gains have delivered record highs and lifted portfolios, but they’ve also pushed valuations into historically stretched territory. The

S&P 500 now trades at over 21 times its projected earnings for the next 12 months which is a level reminiscent of the late-1990s tech bubble or the post-COVID recovery, when interest rates hovered near zero.

What does this mean for investors? Should you celebrate the recent rally or pause to consider what’s next? While today’s valuations might be cause for concern, recent market experience raises another important question: how can you stay disciplined in a volatile environment?

The fact is that exiting the market during uncertain times or taking on unnecessary risk can lead to costly mistakes. Instead, a balanced, long-term investment strategy remains essential for navigating today’s unique challenges while staying aligned with your financial goals.

Valuations: A Historical Perspective

Nevertheless, a key question that that we’re trying to answer with today’ analysis is, “how often do we see markets trade at such elevated levels, and what does it mean for portfolios?”

Upon inspection, there is no doubt that the current valuation of the S&P 500 is rare, with broad market indices trading at over 21 times forward earnings which is a figure not commonly seen outside exceptional periods.

And why does this matter? Because while valuations may not dictate short-term performance, they play a critical role in shaping long-term returns. But put more simply, understanding how valuations work can help you as an investor by setting realistic expectations for the years ahead.

Short-Term vs. Long-Term: The Role of Starting Valuations

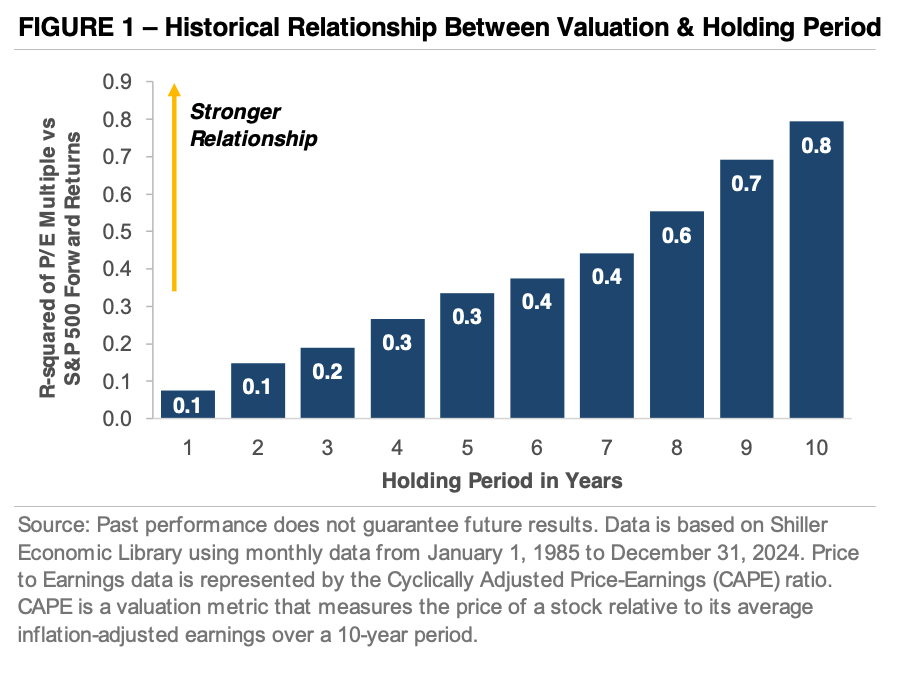

Indeed, figure 1 helps illustrate why starting valuations matter. It tracks the relationship between the S&P 500’s starting valuation and future returns over various holding periods. The horizontal axis shows the length of the holding period in years, while the vertical axis highlights the R-squared (R²) measure, which quantifies how much one variable explains another.

But what does that mean in practical terms? Well, for example, an R² of 0.40 means 40% of changes in one variable can be linked to the other, with the remaining 60% due to randomness or other factors. This means that in the short term, valuations don’t explain much because there’s a low R² for holding periods of just a few years. But over longer time frames, the relationship strengthens. Because by the 10-year mark, starting valuations explain roughly 80% of return variability, underscoring their importance for patient, long-term investors.

What the Numbers Tell Us: Figures That Matter

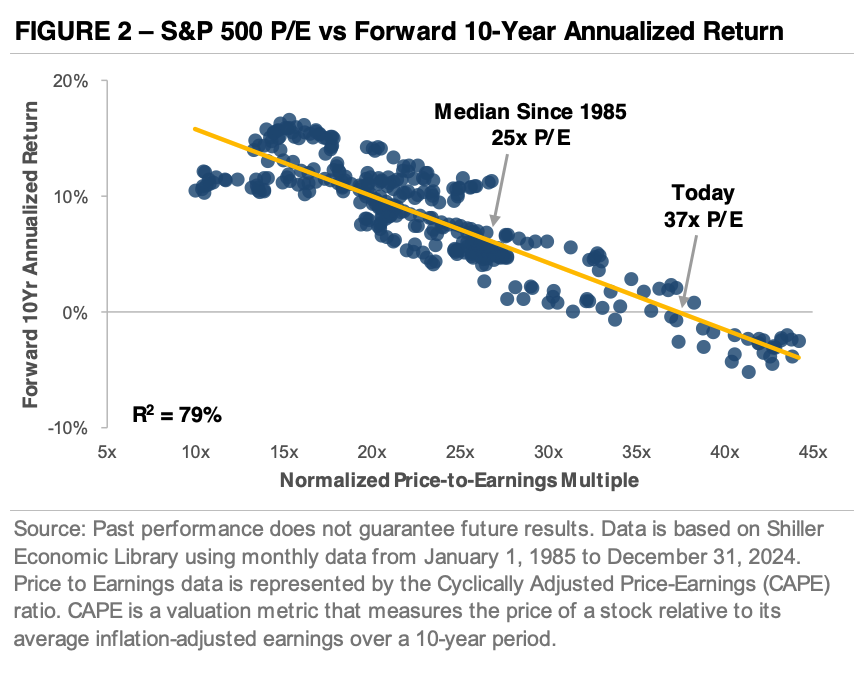

Now, if we zoom out and look at valuations and their impact on longer-term returns we see a different picture. Figure 2 shows how the S&P 500’s starting valuation impacts its next 10 years of annualized returns. This is represented by the normalized price-to-earnings (P/E) ratio, which averages inflation-adjusted earnings over the past decade to smooth out short-term noise.

So then, do higher starting valuations always mean lower returns? Historically, yes. The chart slopes downward, revealing that as valuations increase, forward returns tend to decrease. With today’s normalized P/E ratio sitting at 37, which is an extreme level by historical standards, the S&P 500 could deliver low single-digit annualized returns over the next decade.

Balancing Risk in a Stretched Market

Should you be worried about these numbers? The insights are sobering, but they must be placed in context. While history is an invaluable guide, it’s not a crystal ball. Indeed, figure 1 makes it clear that valuations alone don’t predict short-term results, and markets can stay expensive longer than expected. However, when setting expectations for the years ahead today’s valuations be part of the conversation.

Staying the Course: A Strategy for Long-Term Success

To be sure, current market conditions are a clear signal that it’s prudent to avoid taking on unnecessary risk in today’s market environment. Yet, if the past five years have taught us anything, it’s also the importance of steadiness and staying steadfast to your plan.

Because exiting the market during uncertain times or overreacting to short-term fluctuations can jeopardize your long-term financial planning goals. That’s why now, more than ever, it’s essential to strike the right balance and acknowledge today’s risks while staying committed to a disciplined, long-term investment strategy that aligns with your long-term financial plan.

2025 Economic & Market Outlook

Key Updates on the Economy & Markets

There was no shortage of market-moving events in Q4. The stock market opened the quarter with a slow start in October, but the outcome of the presidential election triggered a broad rally in November.

The rally faded as the year ended, although the S&P 500 trades only a few percentage points below its all-time high. The credit market was equally active in Q4, with the Federal Reserve cutting rates by another -0.50%. However, the major development was the changing 2025 outlook.

The Fed and the market both now expect fewer rate cuts in 2025 compared to the end of Q3, which resulted in a sharp rise in Treasury yields in Q4. This letter recaps the fourth quarter, looks back on the 2024 stock market rally, provides an update on the economy and the Fed’s rate-cutting cycle, and looks ahead to 2025.

Looking Back on the 2024 Stock Market Rally

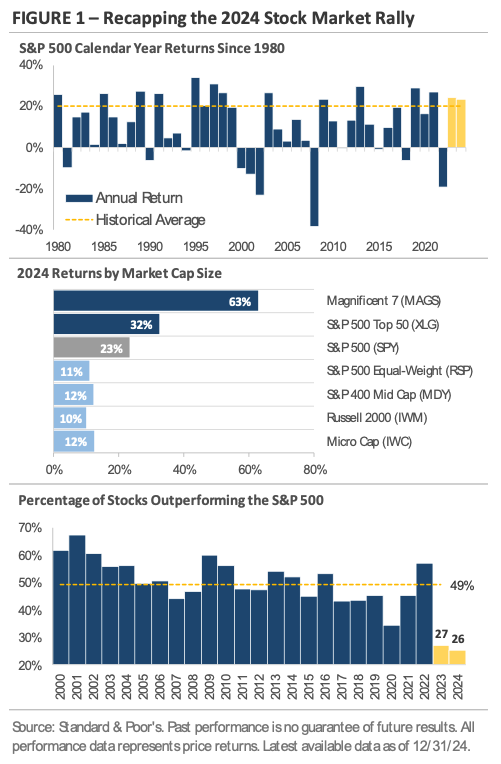

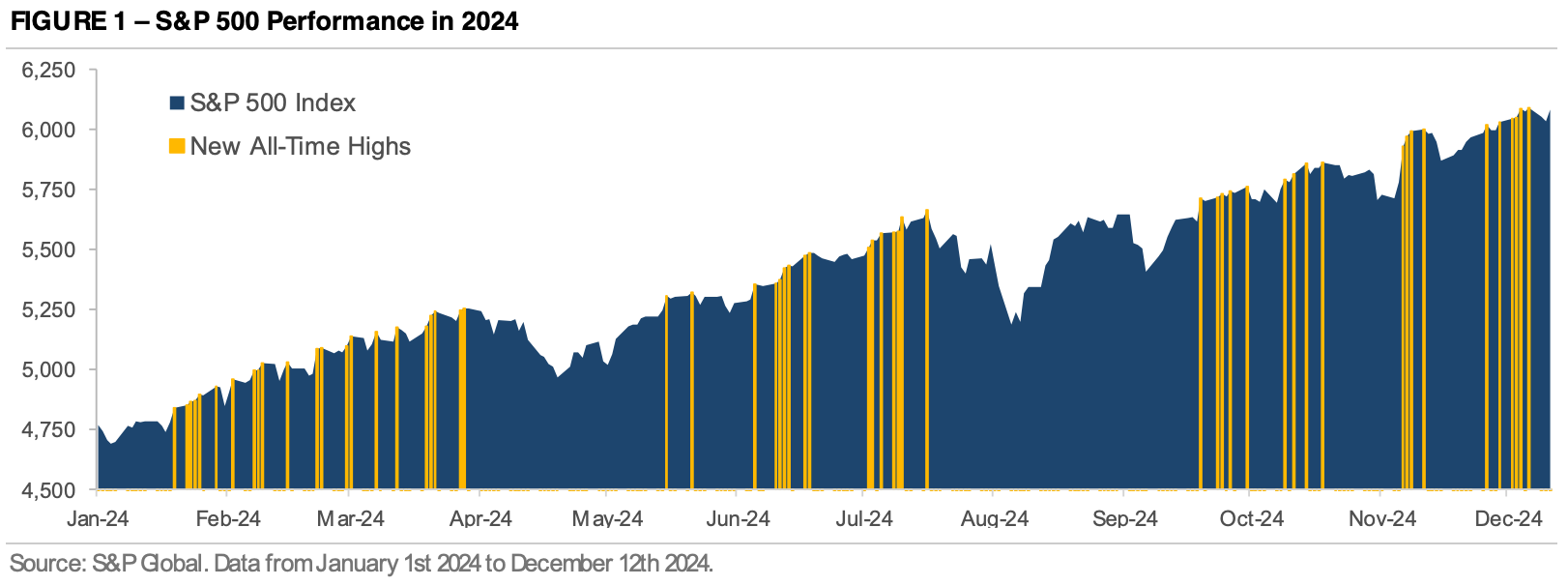

The past two years have been remarkable for investors, with the S&P 500 delivering strong returns in back-to-back years. The three charts in Figure 1 take a closer look at the stock market’s rally in 2024, a year in which the S&P 500 set more than 55 new all-time highs.

The top chart, which graphs the S&P 500’s return for each calendar year since 1980, shows the index posted gains of over +20% in 2023 and 2024. It marked the first time since the 4-year stretch from 1995 to 1998, and like the late 1990s, large-cap technology stocks played a major role in the S&P 500’s gains.

The middle chart shows the 2024 price returns of seven ETFs, each reflecting exposure to companies of different market cap sizes. The chart reveals a significant gap between the returns of large-cap and small-cap stocks in 2024. The top bar tracks the Magnificent 7, a group that includes Microsoft, Apple, Alphabet, Meta, Amazon, Nvidia, and Tesla. These seven companies, which now account for more than 33% of the S&P 500, returned over +60%.

When the group expands from the Magnificent 7 to the 50 largest S&P 500 stocks, the return falls to +32%, still impressive but around half of the Magnificent 7’s return. Broadening the group further to include all S&P 500 companies reduces the index return to approximately +23%, and weighting companies equally rather than by market capitalization lowers the return to +11%.

The key takeaway is that the largest companies contributed a significant portion of the S&P 500’s return in 2024. Smaller companies delivered solid returns around +10%, but they underperformed on a relative basis. An index of mid-cap stocks returned +12%, while small-cap and micro-cap stocks returned +10% and +12%, respectively.

The concentrated stock market rally, which was driven by the outperformance of the largest companies, led to an unusual outcome. The bottom chart tracks the percentage of S&P 500 companies that outperformed the index during each calendar year. For the second consecutive year, fewer than 30% of S&P 500 companies beat the index in 2024. This is significantly below the average of 49% since 2000 and highlights the dominance of the largest companies in 2024.

Data Highlights the U.S. Economy’s Resiliency

The U.S. economy has consistently defied expectations of a slowdown since the Fed started raising interest rates in March 2022. Economists and market participants initially expected growth to slow as the Fed raised interest rates. However, it has now been nearly three years since the Fed’s first rate hike, and the economy continues to grow at an above-trend rate. While higher rates have slowed housing demand and weighed on business investment, the U.S. economy has managed to defy expectations with solid GDP growth.

The top chart in Figure 2 shows the U.S. economy grew at a +3.1% annualized pace in 3Q24, marking the third quarter in the past four with growth above +3%.

The bottom two charts show key drivers of economic growth since early 2022. The middle chart tracks the contribution of personal consumption expenditures (i.e., consumer spending) to U.S. GDP growth. Despite high interest rates, consumer spending has remained a steady driver of growth in recent quarters. Multiple factors have increased household net worth and bolstered consumers’ financial strength, including record-high stock prices, rising home values, and solid wage growth.

Additionally, many borrowers locked in low interest rates during the pandemic, which has made the U.S. economy less sensitive to rising interest rates this cycle.

The bottom chart shows the surge in manufacturing-related construction in recent years. For a long time, manufacturing construction was relatively modest, as most activity was outsourced to China, Mexico, and elsewhere. However, that changed in late 2021, around the time Congress passed trillions in new spending on infrastructure, green energy, and subsidies to incentivize U.S. manufacturing.

These spending bills have been extremely supportive of the U.S. economy and created a boom in the manufacturing of semiconductors, electric vehicles, batteries, and solar panels. The result is a surge in manufacturing-related construction, the largest on record, as companies build new warehouses, industrial facilities, and semiconductor plants. The artificial intelligence industry’s emergence has provided another catalyst, as companies like Microsoft, Amazon, and Meta spend billions on data centers, information processing equipment like semiconductors, and energy production to meet growing power demand.

Economic growth is forecast to slow but remain solid next year, driven by the Trump administration’s pro-growth policies. The new administration’s policy agenda focuses on extending the 2017 tax cuts, reducing regulations across industries, and boosting domestic manufacturing through targeted incentives. These measures have the potential to stimulate capital expenditures, expand manufacturing capacity, and attract foreign investment to the U.S.

An Update on the Fed’s Interest Rate-Cutting Cycle

The Fed continued its rate-cutting cycle in Q4, lowering interest rates by -0.25% at both the November and December meetings for a total of -0.50%. The two -0.25% rate cuts were well telegraphed by the Fed and widely expected, but the big development in Q4 was the changing outlook for 2025.

Despite the two rate cuts, Fed Chair Jerome Powell and other Fed presidents indicated they are not in a hurry to cut rates further. The change in tone follows the U.S. economy’s recent strength, which has caused the Fed to re-examine the need for additional rate cuts.

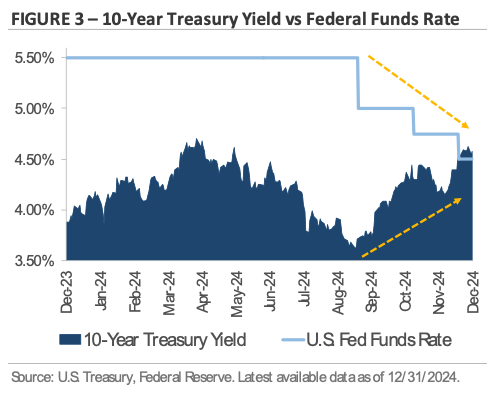

Recent economic strength has also led the market to re-evaluate its rate cut forecast. This dynamic can be seen in the bond market, where longer-maturity Treasury yields have risen sharply since the first rate cut in September.

Figure 3 graphs the 10-year Treasury yield against the federal funds rate, which is the interest rate the Fed adjusts to set monetary policy. Since the first rate cut in September, the federal funds rate has decreased by -1.00%. While the Fed controls shorter-maturity interest rates, the market has more control over longer-maturity interest rates. Over the same period, the 10-year Treasury yield has had the opposite reaction: rising by nearly +1.00%.

What caused Treasury yields to rise as the Fed cut interest rates? Two key data points contributed to the Fed’s decision to start cutting rates in September: falling inflation and rising unemployment. Inflation declined from 3.3% in July 2023 to 2.6% in August 2024, while unemployment rose from 3.5% to a high of 4.3%. The two trends caused the Fed to shift its focus from lowering inflation to supporting the labor market.

However, since the Fed started cutting, the trends have reversed. Inflation progress has stalled since September, and unemployment has declined to 4.2%. Heading into 2025, the Fed and the market have similar rate cut expectations: approximately -0.50% in cuts for the entire year. The question is whether they are placing too much emphasis on recent trends and underestimating the need for rate cuts. As both the Fed and the market saw in 2024, forecasting Fed policy is difficult, especially this cycle.

Equity Market Recap – Stocks End the Year Higher

The stock market ended Q4 higher, but the path included periods of volatility. In October, the S&P 500 ended its five-month winning streak, with most of the equity market finishing slightly lower. The sluggishness occurred as Treasury yields rose after the Fed’s first rate cut in September, suggesting the sharp rise in yields may have played a role in October’s market action. However, stocks rebounded in subsequent months.

In November, the quick and decisive election outcome became a tailwind for stocks. Investor enthusiasm fueled the post-election rally, with stocks trading higher in anticipation of tax cuts, deregulation, and U.S.-focused trade policies aimed at benefiting U.S. companies. Small caps led the way during the broad market rally, with the Russell 2000 rising +11% in November to set a record high.

Bank stocks were another popular post-election trade as investors priced in expectations for financial deregulation and strong economic growth. Industrial stocks saw broad-based strength in anticipation of the Trump administration’s pro-growth policies and protectionist policies, which could spark an industrial renaissance in the U.S. By the end of November, the S&P 500’s year-to-date return surpassed +26%, putting the index on track for consecutive gains of more than +20%.

In December, the market’s excitement cooled, with the S&P 500 trading sideways and ending the month lower. Beneath the surface, a familiar trend from earlier in the year impacted returns, with smaller companies underperforming larger ones by a wide margin.

The Russell 2000 Index was hit hardest, falling -8.4% and giving back most of its post-election gains. Value stocks also traded lower in December, with the Russell 1000 Value Index declining by -6.8%. In contrast, the Magnificent 7 stocks discussed earlier gained more than +5%.

Shifting focus to global markets, international stocks underperformed U.S. stocks in Q4. The MSCI Emerging Market Index returned -7.2%, while the MSCI EAFE Index of developed market stocks returned -8.3%.

Both major international equity indices underperformed the S&P 500 by nearly -10% due to currency headwinds (i.e., a stronger U.S. dollar) and the outperformance of U.S. mega-caps. Looking ahead to 2025 for international markets, the potential for tariffs under the Trump administration is creating significant uncertainty across several global regions.

Credit Market Recap – Bonds Trade Lower as Interest Rates Rise Throughout the Quarter

The sharp rise in Treasury yields weighed on bond returns in Q4. The biggest differentiator within the bond market was duration, or the sensitivity of a bond’s price to interest rate movements.

High-yield corporate bonds produced a total return of -0.1% due to their lower sensitivity to rising interest rates and higher absolute yields. In contrast, investment-grade bonds returned -4% as rising yields had a bigger impact on their longer maturities. Excluding interest received and only looking at price returns, an index of investment-grade corporate bonds posted its biggest quarterly loss since Q3 2022.

Full-year credit returns highlight the key themes that shaped the bond market throughout 2024. Higher-quality bonds like U.S. Treasuries, corporate investment-grade, and mortgage-backed securities underperformed as the market debated and ultimately lowered its rate-cut expectations. In contrast, lower-quality bonds outperformed as economic growth and corporate fundamentals remained solid.

Corporate credit spreads, which measure the difference in yield between two bonds with a similar maturity but different credit quality, steadily tightened throughout the year. This provided a boost to lower-quality bonds in 2024 but has left credit spreads near their lowest levels in decades. For context, the U.S. high-yield corporate credit spread is near its lowest level since 2007, which means investors are receiving less yield in return for taking credit risk.

2025 Outlook – Key Themes to Watch

The S&P 500’s steady climb in 2024 reflects the market’s growing confidence. Investors are optimistic about the artificial intelligence industry’s growth potential. The U.S. economy outperformed expectations, growing at an above-trend rate in three of the past four quarters despite high interest rates.

The stock market rally intensified after the election in November, as investors focused on the incoming administration’s policy agenda. Expectations for tax cuts, deregulation, and energy production are fueling hopes for stronger economic growth.

The bond market echoes the equity market’s confidence, and corporate high-yield credit spreads are near their lowest levels in over 15 years.

However, the equity market rally has made broad market indices like the S&P 500 more concentrated and more expensive. The question on many minds is whether the momentum can continue in 2025.

The S&P 500 currently trades at nearly 22x times its next 12-month earnings estimate, a level not seen outside of periods like the late-1990s tech boom and the recent post-COVID recovery, when interest rates were near zero.

Investors have shown a willingness to pay higher multiples, but with valuations now at extremes, earnings growth will likely play an important role in determining the stock market’s path in 2025.

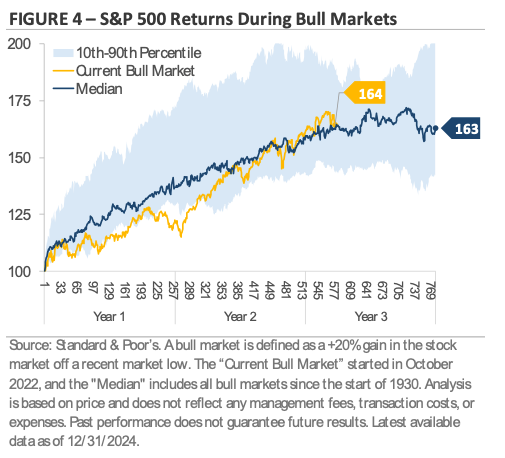

Figure 4 tracks the current bull market, which started in October 2022 and is now in its third year.

The current bull market has performed in line with historical norms, but the chart shows that returns often moderate as bull markets mature. This suggests that the market’s focus could shift to fundamentals and earnings as the next catalyst to push markets higher. 2025 is shaping up to be a year where companies will need to deliver on investors’ expectations to justify their high valuations.

The Bull Market's Unstoppable Momentum in 2024

The past two years have been remarkable for investors, with the S&P 500 posting back-to-back gains of over +20%.

The chart below takes a closer look at 2024’s price movement and uses yellow shading to mark the days when it closed at an all-time high. At the start of this year, the S&P 500’s previous all-time high was set in January 2022.

It took over two years to reclaim the prior high, but once the index broke through in late January 2024, it set more than 50 new highs this year.

The list of all-time highs illustrates the current bull market’s strength and persistence and could grow by year-end.

Large-cap technology stocks, such as Nvidia, Meta, Amazon, and Tesla, have posted strong returns and played a major role in driving the index’s gains. The S&P 500’s record-setting performance is part of a broader cross-asset rally that has lifted stocks, bonds, and commodities.

The stock market’s steady climb this year speaks to investors’ growing confidence. Investors are optimistic about the artificial intelligence industry’s growth potential. The economy has outperformed expectations driven by robust consumer spending, growing at an above-trend rate in Q2 and Q3 despite high interest rates. After the November election, the stock market rally intensified as investors focused on the incoming administration’s policy agenda.

Expectations for tax cuts, deregulation, and energy production are fueling hopes for stronger economic growth. The bond market echoes the confidence in equity markets, and corporate high-yield credit spreads are at levels not seen since May 2007.

The question on many minds is whether the momentum can continue in 2025. The S&P 500 currently trades at over 22x its next 12-month earnings estimate, a level not seen outside of periods like the late-1990s tech boom and the post-COVID recovery. Investors have shown a willingness to pay higher multiples, but with valuations at extremes, earnings could play an important role in determining the stock market’s next move.

The current bull market, which started in October 2022, is now in its third year, and it’s common to see investors shift focus to fundamentals as the bull market matures.

2025 is shaping up to be a year where companies will need to deliver on markets’ expectations to justify their high prices and investors likely will need to remain mindful about taking on more risk than necessary at this point in the market cycle.

Market Reaction: Stocks Post New Highs Post Election

Monthly Market Summary

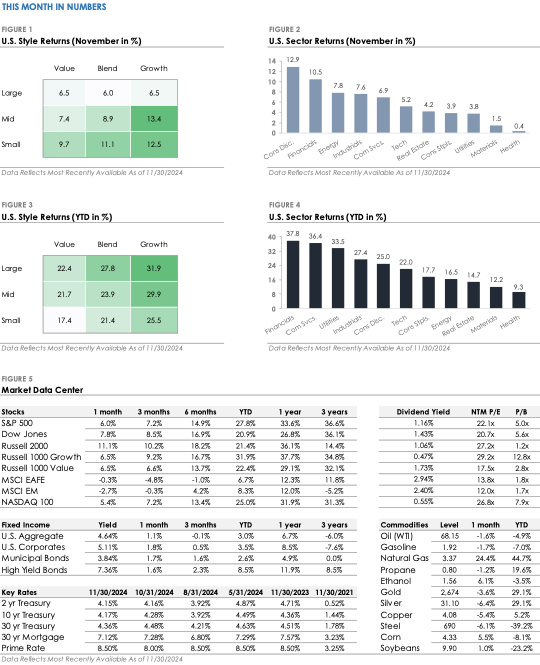

- The S&P 500 Index returned +6.0% but underperformed the Russell 2000 Index’s +11.1% return. All eleven S&P 500 sectors traded higher, with Consumer Discretionary and Financials gaining more than +10%. In contrast, defensive sectors, such as Health Care, Utilities, and Consumer Staples, underperformed the S&P 500.

- Corporate investment-grade bonds produced a +1.8% total return as Treasury yields declined, marginally outperforming corporate high-yield’s +1.6% total return.

- International stocks traded lower for a second consecutive month. The MSCI EAFE developed market stock index returned -0.3%, while the MSCI Emerging Market Index returned -2.7%.

Markets Set New All-Time Highs in November’s Post-Election Rally

The U.S. presidential election results fueled November’s stock market rally, as investors focused on the incoming administration’s policy agenda and its implications. The S&P 500 gained +6.0%, its biggest monthly return since November 2023.

The index traded above the key 6,000 level and set a new all-time high, bringing its year-to-date return to +27%. Smaller companies took center stage during the broad market rally, with the Russell 2000 surging +11.1% to set a record high.

In the bond market, Treasury yields rose after the election due to concerns about increased fiscal spending, tax cuts, and large fiscal deficits under the next administration.

However, later in the month, yields reversed lower, and bonds posted positive returns. With Republicans taking control of the White House, Senate, and House in January, the following section discusses key policy areas to watch, along with the potential market and economic impacts.

Key Policies to Watch in the Next Administration

Investors are monitoring two key areas: tax policy and trade.

The administration is expected to focus on extending the tax cuts passed during President Trump’s first term. This could stimulate economic growth and boost corporate profits, although it could widen the fiscal deficit.

On trade, the administration plans to use tariffs to advance U.S. interests in international affairs and renegotiate trade deals. However, in the near term, tariffs could disrupt supply chains, slow economic growth, and squeeze profit margins.

Other critical policies include immigration and deregulation. There are concerns that tariffs, stricter immigration policies, and expansionary fiscal policy could combine to keep inflation high. If so, the Federal Reserve might need to keep interest rates higher for longer.

Elsewhere, there is an expectation that deregulation could create new growth opportunities in the financial and energy sectors, while relaxed antitrust enforcement could lead to more mergers and acquisitions. Economic growth and corporate earnings will remain important long-term drivers, but in the short term, markets may be sensitive to shifting policy headlines as the new administration takes office.

Trump Wins: What it Means for Your Money

We are likely entering a period of familiar uncertainty. Former President Donald Trump's victory in Wisconsin early this morning clinched his victory and set the stage for a second term as the country's president.

Market Implications

So, what does this mean for the markets, the economy, and your money? Well, as we pointed out in last month's note heading into this week's election, long-term investment data since 1953 shows that markets tend to grow irrespective of the sitting president's party, with a $10,000 investment growing to over $2.1 million if invested continuously, compared to much lower returns if one invested only when Republican or Democratic administrations were in office.

This analysis highlights the benefit of sticking to a disciplined, long-term investment strategy instead of trying to time investments based on political cycles.

Economic Implications

Now, with respect to Trump's second term, the effects of his economic policies could have long-term implications on your savings and spending decisions, given the potential for higher inflation in the coming years and higher taxes once he's out of office.

How so?

First, Trump vowed to renew his trade war with China and begin imposing tariffs shortly after taking office. Although often discussed in geopolitical terms, tariffs on China's exports ultimately function as taxes on US consumers, which can lead to higher prices for goods consumed.

Effects of Tax Cuts

Second, Trump has proposed a host of tax cuts, including extending the 2017 Tax Cuts and Jobs Act (TCJA), eliminating income taxes on Social Security benefits, and reducing corporate tax rates.

Tax cuts provide extra disposable income for households. And when people have more money to spend, consumer demand for goods and services typically increases.

If this increased demand outpaces the economy's ability to supply these goods and services, it can lead to higher prices and contribute to inflation. This point is crucial because a combination of rising import costs, fiscal stimulus, and easy money policies from the Federal Reserve could stoke the embers of inflation.

Higher Taxes Down the Road

Finally, all these tax cuts need to be paid somehow.

As it stands, the US government is spending more than it brings in by the tune of $1.8 trillion in 2024. According to a study by Wharton, this deficit could balloon to $5.8 trillion over the next ten years.

And so, while spending cuts are one way to tackle future deficits, policymakers will likely find ways to raise taxes down the road to cover these debts.

The Big Takeaway

We are headed into a period of familiar uncertainty as it relates to economic policy.

So then, proactive financial planning is prudent now more than ever because higher inflation and higher taxes later are likely a reality we'll all face.

Loose fiscal and monetary policy, along with a renewed trade war, could lead to higher levels of inflation and a rising cost of living over the long term.

At the same time, ballooning government deficits cannot be ignored indefinitely, so spending cuts and higher taxes will be necessary to address the current plight.

Now's the Time to Reevaluate Your Financial Plan

Therefore, reevaluating potentially overly optimistic inflation assumptions in your retirement plan could help you mitigate the effects of a rising cost of living and avoid savings/spending misalignment down the road.

At the same time, tax planning is essential now more than ever because regardless of which tax bracket you're in now, there's a good chance that years from now, your retirement distributions could be facing higher tax rates.

That's why, while your portfolio may grow steadily in this changing political environment, now's the time to begin planning for higher costs and evaluating strategies to keep more of your savings when it's time to take distributions.

As we navigate this period of economic uncertainty, it's crucial to actively review and adjust your financial plan. Doing so not only prepares you for potential inflation and tax changes but also positions your wealth to capitalize on opportunities that arise during fluctuating economic cycles.

WANT TO ENSURE YOU'RE PREPARED FOR INFLATION AND DIAL IN YOUR TAX STRATEGY?

>>> CLICK HERE TO SCHEDULE AN INTRODUCTORY ZOOM CALL! <<<

What Does a 50 Basis Point Cut Really Mean?

Did you know that in a significant move, the Federal Reserve just reduced the fed funds rate by 50 basis points, bringing it down to a range of 4.75 – 5.00%?

This is the first cut since the early days of 2020, marking an end to what has been the most intense period of rate hikes in over four decades.

Why such a decisive cut, you might wonder?

Well, while some might see this as a signal of concern from the Fed about the economy, let’s dig a little deeper. Despite a slight uptick in unemployment and a slowdown in job growth, most indicators suggest that the economy is still expanding.

Even Fed Chief Powell has echoed this sentiment, providing a bit of reassurance to investors. He's betting on a smooth adjustment—a so-called economic soft landing.

Powell’s Perspective: Playing It Safe?

During his latest press conference, Powell maintained that the economy is "in good shape."

But, he hinted that this larger rate cut is more of a precaution—an "insurance" against potential slowdowns. It’s about reinforcing the job market now while it’s strong, not when layoffs start hitting the news.

Think of it as a balancing act. If the Fed waits too long or moves too slowly, it risks a recession. Move too quickly, and it could overheat the economy, sparking inflation. It’s a delicate line to walk, and today, everyone's tuned into how they're managing it.

Market Reactions and Long-term Strategies

Either way, the response from the markets has been generally positive given that it finally got what it’s wanted for years: a Fed Pivot.

Indeed, with profit growth stabilizing, inflation moderating, and interest rates either stable or falling, conditions are ripe for investment. Just this September, both the Dow and S&P 500 reached new heights, a reassuring move given the initial underestimation of inflation by the Fed.

Here’s a quick snapshot of the latest index performances:

- Dow Jones Industrial Average: 1.8% month-to-date, 12.3% year-to-date

- NASDAQ Composite: 2.7% MTD, 21.2% YTD

- S&P 500 Index: 2.0% MTD, 20.8% YTD

Now, it’s worth noting that while strong market performance can stir investor enthusiasm, it also brings with it the temptation for risk-taking. This is where a disciplined investment strategy comes into play.

You see, it’s not just about chasing returns; it’s about managing risks and ensuring you have a portfolio that balances both risks and returns.

The Big Takeaway

So, why should this matter to you?

Well, this situation underscores the critical lesson of diversification—not just in types of investments but also in understanding market movements and central bank strategies.

You see, while markets have rallied strongly this year, recent volatility is a stark reminder that market conditions can change on a whim, so it’s essential to be prepared and not take more risk than necessary.

That’s why, by diversifying your investments, you not only shield yourself from unforeseen market shifts but also position yourself to capitalize on various global opportunities. This kind of strategic positioning ensures that your portfolio captures potential gains while distributing risks, allowing you to focus on what truly matters.

So, as we think on the Fed's recent move, consider this: Is your investment portfolio as diversified as it should be, or are you relying too much on certain assets?

Remember, a disciplined investment strategy isn’t just about picking stocks—it’s about preparing for whatever the future holds while ensuring that your financial foundation is as solid as it can be.

From PE Ratios to Discounted Cash Flows – Which Valuation Method is Best?

Are your holding onto employer stock that’s over- or under-valued?

Well, you've likely tried to read reports, blog posts, or talked to colleagues about the value of your company's stock.

And so, when you're faced with evaluating whether to hold your company stock for the long run or cut your holdings, the road ahead can seem fraught with a number of complex choices.

But you know, getting the answer to your question about the value of your company stock is actually simpler than you think.

That's because when it comes down to it, there are two methods that professionals use to determine whether the price of a company's stock is fairly valued or not.

And that's the absolute valuation and relative valuation methods.

How do these approaches differ?

So, how do these approaches differ?

Well, an absolute valuation model like the Discounted Cash Flow (DCF) method looks at what's called a stock's intrinsic value.

This method forecasts expected future cash flows and adjusts for risk and time value of money—much like estimating all future earnings of a company and converting them into today's dollar value.

On the other hand, relative valuation methods involve comparing a company to its industry peers.

Here, what we're doing is using ratios such as Price-to-Earnings (P/E) so you can get a market-based perspective on whether what you're holding is cheap or expensive.

The Strategic Advantage of a Dual Valuation Approach

So, which one should you use when it comes to valuing your equity compensation?

Well, consider both.

Because here's the thing: if you're a tech professional receiving equity as part of your compensation, then understanding both absolute and relative valuation methods will empower you to make informed, nuanced investment choices.

For example, when looking at absolute valuations, what you're doing is isolating a stock's value based on its internal potential and risks. In other words, does the price of the stock reflect the company's future earnings potential?

In contrast, relative valuation situates a stock within the landscape of its peers, offering you a market-relative perspective on whether it's time to hold or sell. In other words, is the dollar of earnings you're paying for higher or lower compared to industry peers?

Why not just use one versus another?

And so, each method gives you a different lens to look through.

So then, why not use one versus another?

Well, by applying solely an absolute valuation approach, you're potentially at risk of evaluating your company's stock in a vacuum based on expected profits and risks.

However, by adding in relative valuation into the mix, what you're doing is measuring how your company's stock stacks up against similar companies. This approach ensures that you're not just holding onto a high-flyer but also getting a good deal compared to its peers.

In fact, a study by the CFA Institute reveals that over 80% of successful equity fund managers use both techniques to build their portfolios.

They seek out stocks that are not only fundamentally solid but also attractive within their sector, striking a balance between intrinsic worth and extrinsic factors.

The Big Takeaway

Either way, when it comes down to it, this approach can help you assess your company's stock's true value and strategically decide when to hold or sell your equity stakes, which is crucial in a sector where innovations and market shifts often happen at a moment's notice.

With that said, however, it's worth noting that each method comes with its own challenges.

That's because absolute valuations hinge heavily on the accuracy of your future earnings projections and discount rates, which can be highly subjective and vary with market conditions.

At the same time, relative valuations, while useful for contextual analysis, might lead you astray if the broader market is distorted by speculative bubbles or volatile investor sentiments.

That's why merging these valuation strategies offers you a holistic view that reduces the risks associated with relying on a single method.

Nevertheless, staying informed and flexible in your approach can allow you to make smarter, more stable investment choices and position you for a more disciplined approach to managing a key component of your wealth.

Tech is Selling Off, Now What?

Markets are selling off. What should you do?

Well, you might feel the urge to sell, and that's normal.

Because when stocks fall, your first instinct is to do something, right?

But let's talk about what doing something can look like without making decisions you'll later regret:

Step #1: Anchor Yourself to Your Financial Plan

Before you follow the crowd into selling, take a deep breath and revisit your financial plan.

Now, this plan is the rock on which your investment decisions should stand, especially when the markets are falling.

Ask yourself: "What am I investing for, and according to my plan, what should my next step be?"

Now's a great time to reassess your current strategy and ensure it still aligns with your long-term goals.

Remember, a well-crafted plan keeps you looking ahead, no matter what's going on in the markets.

Step #2: Evaluate Your Cash Reserves

If you're retired or depend on your investments for daily living, market drops can feel especially frightening.

That's why it's crucial to ensure you have enough liquidity on hand to cover your immediate needs without compromising your investment strategy.

To this end, ask: "How much cash on hand do I need to keep the lights on for the next six months?"

Then, check your cash reserves. Are they sufficient?

If not, and you absolutely need to sell, do so strategically.

Sell just enough to cover your short-term expenses. This way, you can leave room for your assets to recover and grow over time.

Step #3: Limit Your Exposure to Market Noise

Finally, it's easy to get glued to financial news, but too much noise can lead to stress and poor decisions.

So then, take a few moments and ask: "Am I consuming too much media, and is it affecting my investment choices?"

Often, the wisest action is inaction.

If your financial plan is in order and your cash needs are met, consider stepping back from the media frenzy.

Markets go up and down but remember, this isn't new, especially given the tech sector's rally this year.

Ultimately, success is about not letting the herd mentality sway you. Stick to your plan, keep calm, and carry on investing wisely.

Remember, it's about staying sane, solvent, and strategically set for the future.

Why Does the Market Care About FOMC Meetings?

Why does the market care about FOMC meetings?

And more importantly, why should you care?

Well, the short answer is that the decisions made by the Fed can influence the economy, can influence business earnings, and, hence, can influence the direction of the markets.

You see, the Fed was created by Congress well over a hundred years ago.

The Federal Reserve's Role in the Economy

And today, it has two main mandates: the first is to ensure maximum employment and the second is to maintain price stability.

In other words, the Fed’s role is to ensure that inflation remains in check and that unemployment doesn’t get too far out of control for too long.

So then, at regular intervals throughout the year, during these Federal Open Market Committee (or FOMC) meetings, policymakers assess whether they’re doing what’s necessary to stick to their commitment.

Now, there’s only so much that any one institution can do to control what businesses charge for goods or services or whether they’re prepared to keep hiring.

How Interest Rates Affect the Economy

However, the one thing that the Fed does have control over is short-term interest rates.

And so, you likely know that when the interest rate on your credit cards, or your auto loan or your mortgage goes up, your willingness to spend likewise goes down, right?

Well, in a similar way, the Fed sets its policy rate so that it’s more expensive for businesses to borrow when inflation is getting out of control.

And when inflation is stabilizing, and jobless claims are on the rise, then policymakers consider cutting rates to incentivize borrowing and boost economic activity.

Put a different way, it’s all about the way that money flows through the economy.

When the tap is open and money is flowing freely, the economy is typically humming, but inflation tends to take off as well.

Why You Should Pay Attention to FOMC Meetings

Alright, so with all that said, why does the market care about FOMC meetings?

Well, when the Fed begins raising or lowering rates, it’s typically part of a broader trend. Here again, when interest rates are set to fall, businesses could benefit from lower borrowing costs, and potentially lead to increased profitability and therefore support higher stock prices over the long-term.

So then, why should you care about what the Fed is doing?

Well, when the Fed does something in line with market expectations, this often translates into a higher portfolio value for your retirement savings.

What’s more, understanding the Fed’s decisions can help you make better spending choices, especially if you plan to finance a big-ticket purchase like buying a new home.

At the same time, it can also help you determine whether it’s a prudent time to go out and find that new job.

That’s because when the Fed starts cutting rates, it can signal that a potential economic slowdown is underway and suggest that the job market might soon tighten.

So then from this perspective, it's crucial to approach job changes with caution when the Fed is preparing to cut rates.

Either way, staying on top of the Fed’s latest policy rate decision, and more importantly, understanding why markets respond the way they do, will likely help you make better financial decisions and at the same time, help you make career choices that ultimately set you up for success.

Changing AI Leadership, Trade War 2.0 and Market Volatility

Monthly Market Summary

Changes in Market Leadership

One month into the new year and markets have continued to rally; however, renewed geopolitical uncertainties could pose challenges to solid market gains. Indeed, after a strong showing in 2024, stocks traded higher to start 2025, but the factors driving the rally took on a different character in the past month than we have seen over the past year. For example, the segment of stocks that powered the recent market gains, Large Cap Value stocks, had lagged over the past year but outperformed Large Cap Growth by more than 2.5% in January.

At the same time, the Dow Jones Industrial Average climbed back toward its all-time high in early December after closing last year on a weaker note. Meanwhile, growth stocks, as measured by the Nasdaq 100 and the Technology sector in general, which led markets higher for most of 2024, underperformed the broader index for the month.

This shift was largely driven by AI-related developments in China, which raised concerns about U.S. dominance in the sector and broader market trends. What this means is that while tech stocks powered last year's gains, other sectors may take the lead in 2025, especially if geopolitical risks remain contained. This kind of shift in leadership is not uncommon following strong market years, as investors look to rebalance portfolios and identify opportunities in areas that were previously overlooked.

Are Tech Stocks Out of Steam?

So then, is tech as a driving force of the current rally down for the count this year? It might be too soon to tell. Indeed, January saw a major shake-up in artificial intelligence (AI), with ripple effects across U.S. markets. That's because Chinese startup DeepSeek introduced an AI model that claims to be able to compete with top U.S. platforms like ChatGPT but at a fraction of the cost. The model was allegedly developed using less advanced and cheaper chips, challenging the assumption that leading AI models require heavy investment in high-performance computing. If this approach catches on, it could significantly alter the industry and affect U.S. leadership in AI.

That's why markets reacted quickly, and the impact was significant, leading to a selloff in U.S. tech stocks, especially those that had seen strong gains on AI growth expectations. That's because the prospect of lower-cost AI development raised concerns about the demand for high-end chips. So then companies like Nvidia, a key supplier of advanced AI hardware, saw its market capitalization fall by nearly $600 billion, which was one of the most significant single-day losses for a U.S. company.

At the same time, the selling pressure extended to Microsoft, Alphabet, and Meta, as investors reassessed what appears to be rich valuations in the AI space. And this market response likely reflects broader worries that progress in the AI space may not be as capital-intensive in the future as once believed, which could challenge the dominance of companies that have benefited from high investment requirements in AI-related infrastructure.

Even so, what's notable here is that although the initial market decline was concentrated in a handful of companies, their heavy weighting in the S&P 500 dragged the broader index lower. Nevertheless, investor sentiment is rarely one-sided, and after the initial selloff, markets stabilized coming into February as some investors viewed the pullback as a buying opportunity, particularly in areas of the market that may benefit from AI-driven cost efficiencies. Still, given AI's significant role in market performance, markets will be keen to keep a close eye on developments in the sector while rebalancing to other market opportunities.

Trade War 2.0 Developments

Changes in trade policy also added another layer of market uncertainty after a solid start to the year. That's because, on February 1, 2025, President Trump announced new tariffs as part of what some are dubbing "Trade War 2.0": 25% on imports from Mexico and Canada (with a 10% levy on Canadian energy products) and 10% on Chinese imports. The move is positioned as an effort to address trade imbalances and immigration concerns and prompted immediate responses from major trading partners. Even so, Canada and Mexico secured temporary delays while committing additional resources to combat organized crime and drug trafficking.

But, China responded swiftly, imposed tariffs on U.S. coal, liquefied natural gas, crude oil, and agricultural machinery while launching an antitrust probe into Alphabet. The reaction in financial markets was immediate, with major indices dropping over 1% and the U.S. dollar reaching a 20-year high against the Canadian dollar. Markets have since recovered modestly since the initial selloff, but the surge in the dollar could have additional implications for U.S. multinational companies, as a stronger currency can weigh on exports by making American goods and services more expensive overseas.

These developments reinforce the risks of an escalating trade war, which could lead to higher inflation, supply chain disruptions, and slower economic growth in affected regions. And while markets have endured trade-related tensions in the past, the unpredictability of policy responses are likely to keep investors on edge, especially as incoming data suggests that economic growth is moderating.

Looking Ahead

So, what does this mean for your portfolio? Well, over the next few months, investors will be watching trade policy developments, AI innovation, and Federal Reserve decisions for signals on market direction. While the broadening of market leadership suggests a more balanced rally, geopolitical and macroeconomic risks remain a central headwind to any potential market rally.

Here's the big takeaway: This complicated environment makes it especially important for investors to avoid reacting too strongly to short-term headlines.

Indeed, it's essential to remember that markets don't move in a straight line, and with AI disruptions and trade tensions shaping 2025, staying committed to your long-term plan will be key. Because the question isn't just how these forces play out, it's how you position yourself in response.

Therefore, taking a proactive approach to portfolio positioning, especially rebalancing your investments rather than being swayed by short-term volatility, will be critical to navigating market volatility.

Either way, how political and economic events unfold will shape the market's trajectory. But for now, the best strategy is to focus on your disciplined investment strategy, ignore the noise, and ensure your financial plan is positioned to give you clarity, confidence, and peace of mind as you move through another period of economic and market uncertainty.