What should you know about the SECURE Act?

If you are preparing for retirement, are currently retired, or own a small business chances are you’ve probably heard something about the SECURE Act. So what is it? Simply put, the SECURE Act is a law that makes it easier for small business owners to offer attractive retirement savings opportunities to a population of workers largely underserved by retirement savings options. In this week’s blog post, we explore a high-level overview of the SECURE Act and its implications for businesses owners and employees alike.

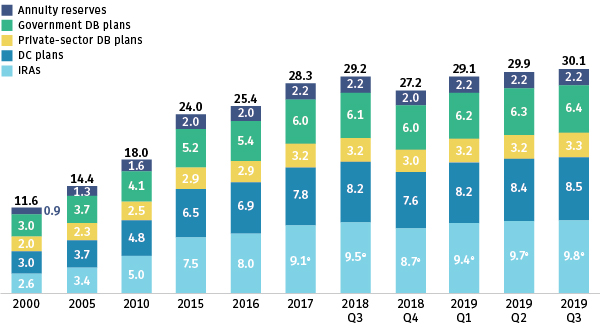

Figure 1: U.S. total retirement market assets

The SECURE Act: a brief overview

For years Congress has been exploring ways to make it easier for Americans to save for retirement, particularly at a time when Social Security is expected to go broke. Last May, the House passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act with the hope of helping more people save for retirement. Around the same time, the Senate introduced their own bill, the Retirement Enhancement and Savings Act of 2019. And after some negotiations between the two chambers of Congress, various features from both bills were ultimately amended into an appropriations bill and signed into law on December 20, 2019. So, what exactly does this law achieve?

Well, while a host of individual changes were adopted by the SECURE Act, the new law arguably accomplishes three key ends:

- It creates incentives for more small business owners to offer 401(k) plans;

- Opens up savings opportunities for a larger portion of the U.S. workforce and;

- Notably alters required minimum distribution (RMD) rules for traditional IRAs

Impact on small business owners

At its core, the SECURE Act incentivizes small businesses to establish tax advantaged retirement plans (like a 401(k)) for their employees. This is important because for some small business owners, establishing and administering a 401(k) plan presents high costs and onerous regulatory tasks, particularly if there are few employees eligible to participate in the plan. So why are 401(k) plans a key part of the SECURE Act?

With a maximum contribution limit of $19,500 for 2020, a 401(k) plan remains one of the most advantageous ways for employees to save pre-tax dollars in collaborative way with their employers. While it’s true that Simplified Employee Pension (SEP) plans allow up to $52,000 in annual contributions, employees (other than owners) typically cannot contribute to a SEP and this limits the plan’s use as a retirement savings vehicle among small business owners with employees. Given the legislation’s goal to incentivize individual retirement savings, a focus on greater adoption of 401(k) plans across a wider swath of companies makes more sense.

While 401(k) plans remain an attractive option, how do business owners get past the cost and administrative burdens of providing a savings benefits to their employees? Enter the Multiple Employment Plan (MEP). In its simplest form, an MEP allows firms to pool together 401(k) resources and share in the administrative burdens with other business owners of running a retirement plan. Under prior laws, MEPs (now called Pooled Employer Plans) were mostly limited to firms in the same industry or geographic location.

The SECURE Act loosens some of these restrictions, enabling unrelated small businesses from different industries and from different places around the U.S. to expand retirement offerings to their employees. The benefits of such an arrangement include 1) reduced fiduciary responsibility for small business owners, 2) transfers the administrative burden of approving loans and hardship withdrawals away from the business owner to the MEP and 3) increases purchasing power and reduces costs of certain investment vehicles. What’s more, the legislation provides a tax credit to firms of between $500 and $5,000 to help defray costs of setting up a 401(k) plan. Taken together, the new law creates more incentives for small business owners to offer an important savings tool to their employees.

...there are some 20 million small businesses in the U.S. that employ fewer than 20 employees – a key group underserved by retirement savings plans.

Impact on workers

Another benefit of the SECURE Act is that could provide more workers with more options to save for retirement. According to data from the Small Business Administration, approximately 47.5% of the U.S. workforce is employed by firms with less than 500 workers. In fact, there are some 20 million small businesses in the U.S. that employ fewer than 20 employees – a key group underserved by retirement savings plans. Assuming that more small businesses owners adopt 401(k) plans, workers could benefit in a couple of ways.

First, the SECURE Act provides tax credits to plan administrators that automatically enroll eligible employees in a company’s 401(k) plan. This would reduce administrative burden on an employee to enroll in their savings plan and, more importantly, get employees (particularly younger workers) saving for retirement sooner and generating more wealth. Second, the new law eliminates the 1,000-hour rule which expands 401(k) participation to more part-time workers. Under the new law, an employee who has worked at least 500 hours a year for three years is now eligible to participate in an employer’s 401(k) plan.

Taken together, these benefits could allow savers, once excluded from qualified plans, to increase their savings rates by between 10% and 37% as earnings are put to work on a pre-tax basis. What’s more, in cases where employers offer dollar-for-dollar matching contributions, some participants could effectively see a 100% return on their savings simply by being able to participate in a 401(k) plan. As we pointed out in a recent post, having more money to put to work early on in the savings process has an exponential effect on wealth creation over time.

Finally, there are a few added benefits that employees should be aware of, beginning with the ability to select an annuity as a savings vehicle. That is, the SECURE Act reduces some of a business owner’s liability related to offering annuities in 401(k) plans and increases the portability of an annuity from one retirement plan to another. Additionally, employees can now contribute as much as 15% (up from 10%) of their pre-tax earnings to their 401(k) (maximum $19,500 annually). And, for those workers concerned about the solvency of their employer’s retirement plan (particular to startup firms), certain provisions in the law provide for retirement accounts to automatically roll into an IRA should an employer’s plan become insolvent, thus offering better protection to worker’s savings.

Figure 2: Retirement assets by type

Too good to be true?

While the SECURE Act will in many ways benefit employers and employees, someone has to pay for these benefits. Between 2020 and 2029, it is estimated that the SECURE Act will cost taxpayers approximately $15 billion. To defray these costs, the new law closes the loophole on the stretch feature available in traditional IRAs.

What this means is that for those individuals who leave behind IRA savings after death, non-marriage beneficiaries will now have only 10 years to liquidate an inherited IRA. This compares to previous laws of the land that allowed a beneficiary to “stretch” minimum required distributions (RMDs) out over their lifetime. The idea here is to expedite the collection of taxes that typically occurs when withdrawals are made from traditional IRAs. What’s more, the new rules change the RMD date from 70 ½ for traditional IRAs to 72, giving some participants who have yet to retire extra time to accumulate savings in their retirement accounts.

Some key takeaways

Time will tell whether more small business owners ultimately will choose to sponsor 401(k) plans (or other qualified plans) as a result of the SECURE Act. With that said, the more businesses that expand retirement benefits to employees, the greater the potential that more people that get to participate in an extremely important tax advantaged savings account. If you’re a small business owner, there are now more opportunities to attract, retain and reward talent to your firm over the long-term. Indeed, lower costs and risk sharing available through PEPs coupled with tax credits that help defray startup costs simply make it that much easier to provide an important benefit to your employees.

For households, increased access to qualified retirement plans could help close the gap on generating a substantial nest egg. Access to a 401(k) plan, particularly one where employers offer dollar-for-dollar matching and automatic enrollment could help build greater wealth and at a faster pace compared. While one downside to the SECURE Act is the elimination of the stretch feature related to inherited IRAs, individuals using IRAs to save for retirement will have a couple more years to see their savings grow before RMDs kick in. Either way, if your employer offers it and you haven’t yet enrolled, the SECURE Act serves as a friendly reminder of how valuable a retirement savings vehicle a 401(k) can be.

Why the coronavirus is relevant to your finances

It’s getting harder and harder to ignore the potential financial fallout from the novel coronavirus (nCoV-2019) outbreak underway. Some of this fallout was evidenced in the global stock selloff on Friday and futures (as of this writing) point to a weaker start at Monday’s open. Indeed, the concerns surrounding the ongoing spread of nCoV is likely to weigh on market sentiment for weeks. But why is nCoV relevant from a financial perspective?

Well, in our opinion, the quickening spread of the coronavirus illustrates how fast unexpected events can alter near term economic assumptions and upend best laid financial plans, notably at a time when the U.S. economy is primed for a recession. Amidst the potential for outbreak-related market and economic volatility, we provide a few recommendations that households can use to increase their financial preparedness as Wall Street and Main Street worries potentially intensify in the weeks ahead.

It’s going to get worse before it gets better

Coming into the year we expected several key events (like geopolitics, central bank policies and elections) to raise uncertainties and simply make getting ahead in life financially harder for some households in 2020. In last week’s post, we wrote about one strategy investors can use to increase portfolio returns as economic growth falls and market volatility picks up.

We’ll talk about some additional financial strategies that can be used to help mitigate uncertainties later, but before we do that we need to highlight two key reasons why we think the coronavirus is important to consider from a financial perspective.

First, reports on the spread of nCoV and the subsequent global response suggest that the outbreak is likely to get worse before it gets better. While Beijing has stepped up its efforts to quarantine suspected infected zones, other governments, like Russia and Singapore have sealed their borders with China while countries like the U.S. have put up their own restrictions on travel to-and-from China amidst the outbreak.

This comes as the World Health Organization (WHO) declared a “public health emergency of international concern” last week. To be sure, the rapid spread of nCoV compared to other coronaviruses like SARS suggests that the current outbreak has the potential to only get worse before it gets better. Barring a rapid de-escalation of current events, what this likely means is that discretionary international travel is poised to slow in the coming weeks not just into and out of China, but potentially among countries that are seeing infections rise and more importantly as deaths outside of China begin to increase in number as well. This brings us to our second point.

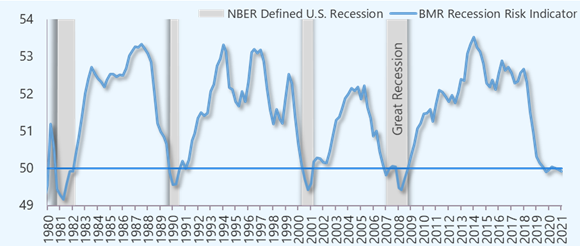

Figure 1: U.S. recession risks are elevated in 2020

U.S. economy primed for a slowdown

The restriction on travel and closing of borders could very well aggravate a downturn in a U.S. economy already primed to slow this year. As we’ve written about in past posts, we believe that the risks related to a U.S. recession remains elevated this year as business spending and hiring activity declines. And while discretionary household spending supported the U.S. economy in 2019, last week’s fourth quarter GDP print remained soft even as the Fed primed its quantitative easing pump during the last three months of the year.

And from this perspective, we expect corporate earnings growth to remain subdued in 2020, challenging already stretched financial valuations. In other words, risky assets have broadly had a strong run in recent months, but now appear expensive on historical basis. And this fact increases the chances that already expensive risky assets could come under increased selling pressure as some sudden shock causes the recent bullish euphoria in the markets to fade. Today, the economic implications of nCoV are only likely to complicate the current market backdrop.

Assuming the uncertainty surrounding nCoV is not reversed quickly, there is a potential that growth in the world’s second largest economy (China) could slow to a rate below current year estimates, contributing to broadly weaker global growth in 2020. This could happen if a further spread of the nCoV outbreak expands quarantine zones and halts economic activity across Chinese provinces as the movement of people and goods grinds to a halt.

What’s more, demand for goods and services globally are likely to fall as people stay home and consume less, impacting exports of goods and services in affected regions and slowing commerce between China and its key trade partners. For the U.S., such uncertainties are likely to only galvanize the willingness of business leaders to postpone discretionary hiring and spending this year. While it is still too soon to tell how the U.S. economy would be affected, the risks related to a U.S. recession are likely to increase in a scenario where global trade declines, business hiring and spending falls and consumers stay home. This leads us to our point about financial preparation.

Coronavirus: how to prepare financially

Without being overly alarmist, we believe that it is important for households to use current events surrounding the novel coronavirus as a reason to take a few steps to ensure financial preparedness as economic and market volatility rise in the coming weeks. This is important because as the economy slows, plentiful jobs may become harder to find when unemployment rises and the ability to borrow money becomes harder as banks tighten lending conditions. So, what steps can households take to increase their financial preparedness?

First, we recommend households look for ways to increase net cash flows. This includes reducing discretionary (or non-essential) spending and finding ways to advantageously use today’s low interest rate environment to refinance high-cost debts. We also suggest maxing out employer-matching retirement savings contributions, putting off big-ticket spending and using excess cash flows to build up emergency savings. We believe that these steps can better prepare households for unexpected life events, particularly as labor market conditions show signs of weakening in the coming months.

Figure 2: Strategies to help financially prepare for the unexpected

Second, for investors oriented towards asset growth, we recommend trimming exposure to higher-beta, lower quality investments and broadly ensuring that aggregate portfolio holdings across all investment accounts reflect long-term goals. While volatility exposes risks in the markets, it is also likely to present opportunities. And this is one reason why we believe that investors should rebalance portfolios, not only to align allocations with long-term goals, but also to generate cash that can be deployed opportunistically as market volatility creates favorable buying prospects.

Finally, for households preparing to take distributions from their investment, we recommend rebalancing accounts to long-term investment objectives and reduce unnecessary risk taking. As we pointed out last week, we investors can increase overall returns (without increasing risks) by trimming unnecessary expenses in their portfolios. Further, we recommend ensuring that cash positions are adequate to meet 6-12 months of living expenses. This is intended to avoid forced selling at depressed prices when market volatility increases.

Cut costs to increase investment returns

Cutting costs may be one of the most effective ways to increase investment returns this year.

To be sure, some investors have been riding a wave of positive market momentum over the past year as lower central bank policy rates have broadly boosted asset prices and seemingly contributed to easy investment returns.

While monetary policy could be supportive of risk assets in 2020, we expect prices to remain susceptible to quick reversals as markets remain near historic highs.

Market Volatility on the Rise

In fact, this was illustrated last week as news of the coronavirus’s global spread caused a pullback in financial markets.

We believe that last week’s market selloff also serves as an important reminder to investors that the momentum that had contributed to easy market gains are likely to be challenged this year by weaker economic fundamentals, softer earnings and already stretched valuations.

In such an environment, we believe that investors have a better chance of increasing their returns by managing fees and managing risks in their investment portfolios.

Addition by Subtraction

So how can managing fees improve investment returns?

Well, simply put, the higher the fees charged to an investment account, the lower the base from which a portfolio can appreciate.

Or put differently, fees tend to reduce the amount of money that can be put to work and compounded over time. To illustrate this point, we compare the performance of two hypothetical portfolios that have varying fee structures.

For example, two portfolios valued at $250,000, each compounding monthly at a hypothetical annual rate of 5%, but with different fee levels.

Annual product fees in Portfolio 1 average 1.0% and have asset management fees of 1.5%. This compares with annual product and asset management fees each of 0.5% for Portfolio 2.

In aggregate, this is 1.5% less than the first portfolio. So how do they compare?

Performance Divergences

Additionally, a notable divergence in the value of Portfolio 2 over its peer across our 10-year test period.

More specifically, the gains attributed to lower product and management fees added up to over $52,000 over the test period and made for a difference of 16.2% between the two portfolios.

This suggests that not only do lower fees contribute to higher compounded returns, they also reduce the amount of time it takes to achieve financial goals.

To this point, we know that it took 10 years for Portfolio 2 to increase from $250,000 to a value of $372,000.

How much longer would it take Portfolio 1 to achieve this value given the same sort of assumptions in our previous example?

At higher fee levels, Portfolio 1 would need to compound at its current rate and fee structure for six additional years to attain the value that Portfolio 2 had achieved in 10 years.

That’s arriving at a financial goal six years sooner and illustrates the rules of exponential growth applied to savings goals.

Ways to Manage and Reduce Investment Fees

So then what steps can investors take to cut costs and increase investment returns in their portfolios?

Well, we suggest that they begin by looking at how much they’re being charged by the products held in their investment portfolios.

We have found that actively managed mutual funds tend to charge higher fees than passively managed exchange traded funds (ETFs).

This is important because active managers have had a track record of underperforming their benchmarks over the past decade. And from this perspective, investors may be better served by paying for indexing than by paying to time the markets.

Evaluate Third Party Fees

Beyond managing product costs, we recommend that investors take a close look at the fees they are paying to their asset managers.

These fees, typically charged on an asset under management (AUM) basis, vary widely among asset management firms and can rise or fall based on the size of an investment portfolio.

Therefore, we recommend comparing your AUM fees against industry averages, and pay particular attention to the breakpoint levels that may qualify you for a lower fee if your portfolio has appreciated in recent years and your AUM fee remains unchanged.

Is There Value Add?

If the fees you are being charged are above average and your asset management firm cannot clearly articulate the value-add of their higher management fee, then we recommend evaluating potential alternatives.

In this increasingly commoditized business, some alternatives would include firms with a lower cost AUM structure or those that charge a flat asset management fee.

Either way, in an environment where market volatility could potentially rise in the months ahead, we believe that investors are best served by managing risk in their investment portfolios.

This is done by rebalancing allocations to their long-term investment objectives.

From the perspective of managing fees and increasing investment returns, the act of addition by subtraction, that is, reducing the amount of money flowing out of a portfolio, we believe can contribute to higher overall portfolio values and reduce the time it takes to grow assets to a target level.