Three Things to Know About Paying a Financial Advisor

Did you know that not all financial advisors get paid the same way? And while compensation does not make the financial advisor, how they're paid can influence the advice you receive and potentially the outcomes of your financial goals. What's more, if you don't understand what your own financial goals are, you may end up paying for products or services that you don't necessarily need.

Knowing where your hard-earned money goes should be your top priority when it comes to working with a financial advisor. This understanding is essential because your ability to make smarter decisions with your money rises when you know what you're paying for and how your advisor gets paid. And when you make smart money decisions, you increase the chance of achieving important long-term financial goals.

Not All Financial Advisors Get Paid the Same Way

One of the first things to know before you go out and spend on a financial advisor's services is that there are some critical differences in how their firms earn money. In general, when engaging with a financial advisor, you are likely to pay either 1) a commission, 2) an asset under management (AUM) fee, or 3) an hourly or flat-rate fee.

![]()

Commission-based Fees

When you work with a commission-based financial advisor, the commitment typically is transactional. For example, a transaction occurs when you complete a securities trade with an advisor's assistance, or they help you buy/sell assets in your investment portfolio. Specifically, you're likely to meet a commissioned-based advisor when you buy a product like an annuity or a mutual fund.

Typical fees for annuity commissions and mutual fund loads can be as high as 8% of the product sold. At an 8% fee, for every $100,000 you allocate to an annuity or mutual fund, the advisor's broker-dealer will keep $8,000 of your money and split it with your advisor.

AUM-based Fees

Size matters for advisors who operate under an asset under management (AUM) basis. Assets under management represent the dollar value of investment accounts for which a financial advisor is responsible. The industry average AUM fee hovers around 2% of investible assets but varies from one advisory firm to the next. Such firms typically have AUM minimums (many around $250,000).

This minimum comes from the fact that firm compensation is commensurate with the amount of assets managed. Typically paid quarterly and in advance, a 2% fee on a $250,000 investment comes out to around $5,000 per year and could be paid directly out of your investment account.

The fee-for-service model is the third way you may pay for a financial advisor's services. For instance, fee-for-service financial advisors typically charge for financial planning or investment management services using an hourly rate, a retainer, or a fixed fee approach. Hourly rates can average $250 and are useful for project-based work like creating a debt payoff plan. Similar to the way many legal firms charge their clients, a retainer fee is paid to an advisor's firm in advance and billed against the time you use to speak to or work with your financial advisor.

A fixed-rate fee is typically associated with a robust suite of services that include comprehensive financial planning, or flat-rate investment management services all for one price. Fixed rates usually average $3,000 per engagement, and you'll likely pay this fee directly to your financial advisor's firm.

Another distinction is a fee-based advisor, who may charge a fee for their service and yet receive a commission for selling you insurance or securities products. Fee-only advisors, on the other hand, typically sign a fiduciary oath (more on fiduciary later) and pledge not to receive commissions.

Compensation Can Influence Your Experience and Outcome

The incentives used by your financial advisor's employer may also influence your experience and overall financial results. Indeed, firms that hire financial advisors (banks, broker-dealers, insurance companies, registered investment advisors) have developed compensation structures meant to drive outcomes for their organizations.

Put simply, an organization's leaders will incentivize (pay) financial advisors to hit sales, asset, or client acquisition goals. What this means to you is that there may be a fine line between whether your financial advisor is looking out for your, their own, or their firm’s best interests.

Sales-based goals

The organizational goal of a commission-based advisor is generally to drive product and insurance sales for their firm. Commission-based advisors are typically associated with a broker-dealer or insurance company. The eat-what-you-kill culture of a commission-based environment may be enough to drive the sales goals of an advisory firm.

Even so, some business leaders have implemented quotas stipulating that an advisor must meet rising dollar or product sales targets to remain employed with their firm. Therefore, if it's the end of the quarter and your financial advisor hasn't met their quota, guess which product or service they're going to recommend to you?

Accumulating more assets is a crucial organization goal of AUM-centric advisory firms. Such companies may be associated with a bank, broker-dealer, or registered investment advisor (RIA). Because client assets tend to move from one firm to another over time, advisors have an incentive to bring in new clients to make up for lost revenue.

At the same time, the percent-relative nature of the AUM model naturally leads to higher firm revenue (and advisor pay) as assets under management rise. Indeed, a financial advisor could receive the same compensation by working with a single million-dollar client as they would with ten $100,000 clients. If an advisor's compensation rises with AUM, and their time is limited, what type of client do you think they'll want to work with most?

Client-acquisition goals

A primary goal of fee-for-service oriented companies is to increase the number of clients that come in through the firm's door. Banks, broker-dealers, and RIAs may employ a fee-for-service model. Yet, registered investment advisors are increasingly leading the way on fee-based and fee-only offerings.

However, some low-cost, fee-for-service offerings may require a financial advisor to work with a large number of clients to achieve the organization's revenue targets. What does this mean to you? Well, there are only so many hours in a day. Think about a financial advisor who has hundreds of clients that they're servicing. How much time, care, and attention do you think your financial priorities will receive when it's your turn to talk about your goals.

Suitability vs. Fiduciary Standard

Understanding the difference between suitability vs. fiduciary standards may influence your financial advisor experience. Simply put, one standard is more legally rigorous as it relates to the kind of advice a financial advisor provides.

For example, let's say that you want to add an index fund to your investment portfolio. Under the suitability standards, your financial advisor must ensure that a fund they recommend suits your needs, goals, and objectives. So far, so good, right? Not so fast. There's nothing to say that an advisor can't recommend a higher load, a-share mutual fund when a lower-cost exchange-traded fund (ETF) would do the job for you just as well.

Under fiduciary rules, however, a financial advisor is legally bound to serve your best interests. This standard is similar to those required of accountants, doctors, and lawyers. In the case of our example, an advisor must find a suitable solution for you. Still, if a lower-cost product like an ETF is in your best interest, then by fiduciary rules, your advisor is required to recommend the product that is in your best interest.

So, to whom does a suitability standard apply? This standard typically applies to commission-based advisors associated with broker-dealers and insurance companies. The fiduciary standard, on the other hand, usually refers to bank- and RIA-based advisors. What's important to note here is that an advisor can be simultaneously associated with both a broker-dealer and a bank or RIA. If a fiduciary standard is important to you, you should ask your advisor how much time they spend in a fiduciary role.

Buyer Beware: You Get What You Pay For

A final point about paying a financial advisor is ensuring you have a clear understanding of what you're trying to accomplish. There are a host of reasons (we wrote about ten of them here) why you might set out to work with a financial advisor. However, a mismatch between the kinds of services that you're looking for and the advisor you ultimately hire may lead you to subpar outcomes and a lower chance of achieving your financial goal.

For example, if your reason for seeking out an advisor is to develop a process that creates wealth, like increasing cash flows or paying down debt, then working with an AUM-based advisor may or may not be a good match. Even if you meet an advisor's asset minimums, you may end up paying for investment services that you otherwise may not need.

Alternatively, an insurance-based financial advisor may or may not be the best person to speak with if you are planning for a retirement that's still 10-20 years out. Why? You could end up purchasing an expensive insurance product that does not keep pace with your lifestyle or evolving risk tolerance or financial goals.

The point here is that each advisor brings their kind of value to the table, so be sure to clearly understand what services you need and shop around before committing to a single financial advisor.

Knowledge is Power

It's important to understand that compensation does not always make the advisor. For example, some commission-based advisors provide excellent service, seek to put their clients in the lowest cost, most suitable products, and ultimately help their clients achieve critical financial goals. In contrast, a fee-for-service advisor may deliver an inadequate financial plan because they failed to hear their client's needs, leading to poorly understood or improperly defined planning objectives.

Even so, knowing where your hard-earned money goes should be your top priority when it comes to working with a financial advisor. This understanding is vital because your ability to make smarter decisions with your money rises when you know what you're paying for and how your advisor gets paid. And when you make smart money decisions, it improves your overall financial planning and investing experience and increases your chances of achieving important long-term financial goals.

Ten Signs it's Time to Find a Financial Advisor

Having a firm grasp of your finances is a critical part of reaching your financial goals. With money being a very personal matter for each of us, knowing when you might need help can be a real struggle. Even so, changing circumstances and life events could be an early indication that you may benefit from a financial professional's assistance. Indeed, here are ten signs that now may be an opportune time to speak with a trusted financial advisor:

1. You’ve just come into a large sum of money.

Have you become suddenly wealthy or come into a small windfall? Whether by inheritance, legal settlement, bonus, or other means, a key concern after the money comes in is, "what should I do now?" Knowing what to do with a large sum of money can be a challenge for many people. Undoubtedly, friends, family, and a host of other souls may offer you well-meaning advice. But the real question is: what do you want to do with your money?

More money can bring more opportunities. When you work with a financial advisor, they can help you narrow down and prioritize what you'd like to do with your money. They can also create a plan to align your spending and investing decisions with what matters most to you now that you have more opportunities. Doing so can help preserve the longevity of your money or ensure that you're not spending in a way that you may otherwise regret.

2. You once enjoyed staying on top of the markets and your investments but would rather spend your time pursuing other interests.

Has investing lost its excitement to you? Losing interest in managing your investments can happen for many reasons. Maybe you were the type of person that got excited about tuning in to CNBC or daily reading the Wall Street Journal—even running the latest Zacks screens to find undervalued securities to add to your investment portfolio. Today, however, you would rather spend your time doing other things that interest you.

What about the financial goals set when you had initially opened that brokerage account? They may nevertheless be within reach. And did you know that a financial advisor can help manage the very account that you once managed on your own? Indeed, one job of a financial advisor is to stay on top of developments in the markets and economy and determine whether and what actions they need to take in their clients’ portfolios so that you don’t have to.

3. You’re not sure what to do about the investments you have overlooked for far too long.

Do you have three or four retirement savings account sitting with a former employer? When’s the last time you rebalanced your 401(k) or checked your brokerage account performance? If you’re not sure how to answer any of these questions, it may be a good time to check in with a financial advisor.

A financial advisor can help you make a plan to consolidate your investments, determine when and how often to rebalance your investment accounts, and show you where and why your investment performance may have deviated from the market. Simply put, a financial advisor will help your investments get back on track and help you keep an eye on its performance.

4. You’ve decided to retire and need help to manage your savings to ensure it lasts through retirement.

After planning for retirement, what’s the next most important financial decision you’ll make? Deciding on how and when to draw down your retirement savings. This decision is vital because your withdrawal choices during times of market volatility can have a significant effect on your savings’ ability to provide during your golden years.

For example, a withdrawal strategy that generally assumes calm markets can derail even the best-laid retirement plans when your investments significantly fall in value. A financial advisor can work with you to understand your liquidity needs and tailor a withdrawal strategy that produces an adequate amount of cash to weather a market downturn while keeping your money invested for the long term.

5. You have reached a meaningful life or career milestone and financial need a plan chart your next course.

Did you just get married (or divorced), buy a house, or get a promotion? It may now be an excellent time to speak with a financial advisor. The reason being is that your spending and savings patterns are likely to be affected by various crosswinds during this time of change.

More importantly, individual and family goals can shift as a result of these milestone events. A financial advisor can take the time to help you refine your priorities, create a financial plan, and provide tools that can help you align your spending and savings with your new financial priorities.

6. You’ve experienced career or personal change, and you’ve had to put off taking care of important financial decisions.

Has life come at you so fast that you’ve lost track of important financial goals? Whether you now realize that you haven’t saved enough for retirement or you have a child preparing for college, it’s never too late to save for retirement or any other consequential financial goal that you may have.

Financial advisors typically have access to sophisticated planning tools. And when applied appropriately, an advisor can create financial projections based on many model assumptions and inputs to show you with varying degrees the time and cost it may take to get your savings goals back on track.

7. Your financial goals are not as straightforward as they used to be, and you need some help realigning priorities.

Do you know what your financial priorities are? Understanding your financial priorities and objectives is essential because they are fundamental components of a solid financial plan. In fact, without clearly defining your goals, your financial plan is likely not to be as effective as it otherwise could be. So how can you clarify goals that once seemed straightforward? Talk it out.

The hallmark of a trustworthy financial advisor is in their ability to understand who you are as a person, listen to what you want from your life and help guide you toward a more specific vision of your financial intentions. What’s important to keep in mind during this process, however, is that your priorities match your values, or what’s important to you. The reason being is that if you can’t buy into the financial priorities outlined by your advisor, chances are you won't buy into your financial plan.

8. You’ve tried the one-size-fits-all books, seminars, or planning solutions and are looking for a plan custom-tailored to your unique lifestyle needs.

Have you ever met someone that taught themselves how to play the piano by ear? Or how about that neighbor that knows how to fix just about everything only by Google searching an article or watching a YouTube video? If this speaks to you, chances are you probably have your financial and investment house in order but are looking for a way to take your process to the next level.

If these scenarios do not speak to you, you’re likely inclined to want someone to help guide you along your planning and investing journey. In either case, a financial advisor can look at your unique background, experience with planning and investing, and create bespoke solutions to meet your financial needs, goals, and objectives.

9. You want a more comprehensive solution to your financial needs.

When was the last time you heard of an electrical or roofing company take on the task of single-handedly building a house? It’s not likely as specialist contractors generally tend to stay in their swim lanes of expertise. That’s where a general contractor comes in. They broadly oversee the construction of a home, from the foundation up to the roof and everything in between, calling in specialists as needed.

When it comes to your financial life, one sign that you need a financial advisor is that you’ve worked with a specialist (an insurance- or investment-oriented advisor) and now want someone to help you out across all aspects of your financial life. As with a general contractor, a fee-only financial advisor offering comprehensive financial planning and investment management services will consider your financial priorities, create a plan, call in the specialists and walk you through each step of the implementation process.

10. You want objectivity in the financial advice you receive and not sure that a commission-based advisor can deliver that outcome.

Did you know that not all financial advisors receive compensation the same way? For example, a commission-based advisor typically earns an income when they sell you an insurance or investment product. Therefore, the more products an advisor can sell, the more revenue they make. When you pay a fee-only advisor directly for service, you receive advice that is in your best interest, free of any competing considerations for selling a product or moving your investments over to their firm. When this happens, it could increase your confidence in the motivation driving the advice you receive and turns the focus toward developing a long-term relationship.

What’s more, when you pay a fixed fee, whether upfront or ongoing, it is clear how much you are paying. A fee-only advisor typically has no complicated fee structures to explain or potential “hidden” fees that may lead to confusion. Through this approach, the benefit to you may be greater trust in your advisor. At the same time, it may reframe financial planning services as another normal part of your financial life, rather than an excessive extra.

Are you ready to speak with a financial advisor?

You may have your reason for wanting to work with a financial advisor not included in this list. The reality is that individuals each have their personal reasons for seeking a financial professional’s services.

Whatever the case may be, if you’re considering your financial future and have experienced a significant change in your life, want more time for other pursuits or entirely not sure where to start, now may be time to speak with a financial advisor.

Adjusting to Seismic Shifts

In the blink of an eye the coronavirus has fundamentally changed our world in more ways than we can imagine. While it seems like an eternity ago, it only has been a matter of days since Pennsylvania Governor Tom Wolf issued his first stay-at-home order for a few counties in the state.

This week, the Governor expanded his order to all counties throughout the Commonwealth and for a period of at least 30 days. In recent weeks, many states have enacted their own stay-at-home measures being it necessary to mitigate the spread of the COVID-19 virus. Unprecedented times call for unprecedented measures.

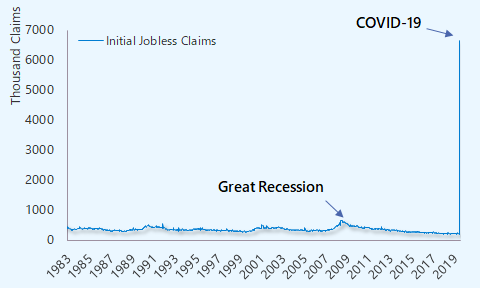

It is needless to say that from a financial perspective, social distancing and self-isolation have created a seismic shift in the economy, in financial markets and in many people’s personal financial plans. Data this week showed that over 6 million people applied for unemployment benefits adding to last week’s catastrophic 3.2 million initial jobless claims.

Figure 1: A 50-fold increase in jobless claims

And to put this number into perspective, the 4-week average just prior to the virus outbreak was sitting at around 200,000 initial claims. That’s a fifty-fold increase in less than two weeks and at no time in post-war history have we seen so many people lose their jobs in such short order.

And so it goes: most people today know someone that has been fundamentally affected – whether it’s in their physical or mental health, finances or otherwise – by the coronavirus outbreak. Without a doubt the unexpected event has fundamentally changed the plans that nearly every single American has laid out for themselves this year and for years to come.

While a number of measures are underway to mitigate the financial fallout from the pandemic, many households and business owners are still struggling to grasp the gravity of the changes underway. With that said, during this time of change, we believe that the best way to rebound from a financial setback is by setting yourself up with a plan to navigate a world that has just gone through a seismic shift.

Government loosens its purse strings

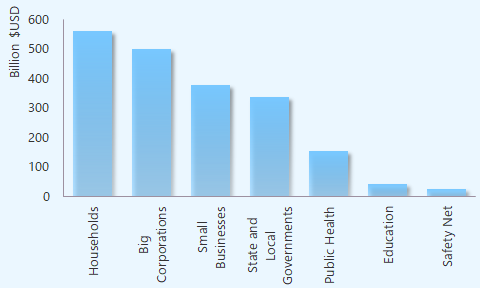

So, what exactly has the government done to address the economic and financial fallout from social distancing measures? Well, in response to and anticipation of further virus mitigation efforts, the government has taken unprecedent actions to shore up the economy. For instance, on March 27, Congress passed the Coronavirus Aid, Relief, and Economic Security (or CARES) Act. This fiscal stimulus package provides more than $2 trillion in aid to individuals and businesses of all sizes and across the United States.

Such a dollar amount is certainly hard to grasp on its own, but in comparison to past stimulus measures, the CARES package is more than twice the size of the American Recovery and Reinvestment Act passed during the Obama administration back in 2009. In terms of what went into the CARES package, there are a number of items geared to help households and businesses. These measures include:

- A one-time cash payment to taxpaying households

- Allowances for certain tax-free withdrawals from retirement savings accounts

- Exclusion of payments for certain federally subsidized student loans

- Increases in unemployment insurance benefits

- A delay of employer payroll taxes and taxes paid by certain corporations and;

- Other changes to the tax treatment of business income and net operating losses

Figure 2: The government will borrow $2 trillion to support households and businesses

Overall, about a quarter of the money from this package will go directly to households, 40% will go to help businesses and roughly a third of the money will go to state and local governments and health and education institutions.

Fed pulls out all the stops

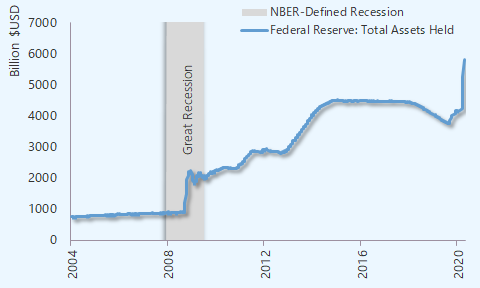

Now on the monetary side, the Federal Reserve has pulled out all the stops to support the proper functioning of the financial system and carry out its dual mandate of price stability and full employment. Put a different way, the Fed today is doing everything it can to support the financial system (and the economy) like it did back in 2008. In reality, under Jay Powell, the Fed is doing much more than it did a decade ago when Ben Bernanke was at the helm.

To this point, early last year the Fed signaled that it would stop raising interest rates, and pivot away from tightening monetary policy and toward easing as economic growth back then started to show signs of fraying. What’s more, in September, the Federal Reserve restarted its asset purchase program after certain events exposed issues in the Treasury market. At that time, the central bank had begun purchasing assets at a rate of $10-20 billion per month.

In March of this year, the Federal Open Market Committee (FOMC) surprised markets when it cut its target policy rate to around zero percent. What this means is that the Federal Reserve wants interest rates to go back to the same level that they were during the height of the Global Financial Crisis a decade ago.

Figure 3: Fed Assets Up Over $2 Trillion in Less Than 7 Months

Also last month, the Fed committed to purchasing corporate and local government debt, it increased the rate of its asset purchases up to $90 billion per day and committed to adding an unlimited amount of assets to its balance sheet for an indefinite period of time. Taken together, the actions from the Fed signal a willingness to get ahead of what is likely to be a very serious downturn in the U.S. economy.

A “V” shaped recovery not likely in the cards

So how do these measures relate to economic expectations? Well, a national poll released on Friday showed that less than half of respondents surveyed believe that the economy will return to normal by the month of June. What this suggests is that the majority of a sample of the American population do not believe that the economy will recover quickly and that the effects of the coronavirus will linger for longer than many policymakers are communicating to the public.

To be sure, we’ve been writing about the fact that global pandemics historically have come in three waves, each with their own recovery period. And so how does this apply today? Well, not only are we right now dealing with the first phase of the outbreak here in the U.S., there are now signs that the outbreak has returned to Asia where – until recently – many countries had thought they contained the coronavirus.

What this means is that social distancing measures in the U.S. are likely to remain in place for longer than most people expect. This also means that businesses may not reopen as quickly as some people anticipate and it means that more workers will likely remain unemployed for longer.

Figure 4: “V” Shaped Recoveries Tend to be Shorter Than “U” Shaped Recoveries

From this perspective, it’s possible that the U.S. and global economy will experience a prolonged “U” shaped rebound and not a “V” shaped recovery as hoped by many economy watchers. Indeed, this view is held by researchers at PIMCO, a widely known asset management firm, who estimate that stability in economic growth could take as long as 12 months to form.

We believe that the reason it could take longer for the economy to recover is because the virus will take longer to contain. And, until a vaccine or significant level of immunity is developed across the global population, the deadly effects of the virus will continue to hamper economic growth. The result is that many firms will simply not be able to restart operations as quickly as some people had hoped.

Adding insult to injury, we have yet to see whether the current fiscal and monetary support packages will be enough to mitigate a broad swath of corporate bond defaults that are now waiting in the wings. To be clear, there is a group of companies that for years have been sitting on the cusp of bankruptcy, if not for the support of the Fed’s money printing operations.

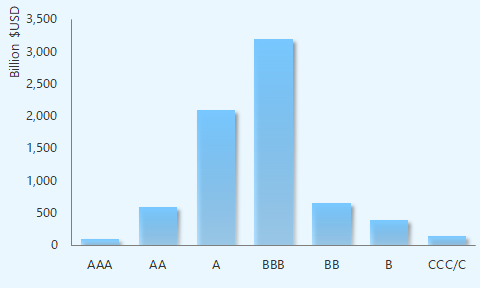

Figure 5: More than 50% of Investment Grade Debt is One Notch Above Junk

What this means is that, in addition to the COVID-19 related risks, the economy and financial markets could get yet another shock from a backlog of ailing companies now filing for bankruptcy protection. In such a scenario, it’s hard for us to see how household spending and business investment could rebound in short order without a sudden drop in new coronavirus cases globally.

"Nimble thought can jump both sea and land."

![]()

William Shakespeare

Setting up for a rebound

In terms of how we should be relating to these financially important events, it’s our belief that people should look for the silver linings whenever possible. Without a doubt the spread of the coronavirus has derailed life and financial plans for many people. While the devastation is unique and personal to each one of us, it is also worth noting that the current events provide a unique opportunity to stop and reassess. That is, to take a hard look at what’s really important in each one of our lives.

Illness has a way of naturally slowing us down and forcing us to reevaluate our current life priorities. Sometimes we get so fixated on a goal, or an outcome in our lives, that we lose sight of the really important things that are going on around us. And from a financial perspective, what may have been a priority or an important goal just a few weeks ago may no longer matter as much in light of the current circumstance. In other ways, the current developments may have taken away people and opportunities that have left us feeling lost and disorientated.

“…in life it doesn’t matter what happened to you or where you came from. It matters what you do with what happens and what you’ve been given.”

![]()

Ryan Holiday

In his book, “The Obstacle is the Way”, author Ryan Holiday tells us that, “…in life it doesn’t matter what happened to you or where you came from. It matters what you do with what happens and what you’ve been given.” From this perspective, we believe that the best way to rebound from a financial setback is by setting yourself up with a plan to navigate a world that has just gone through a seismic shift.

A Dutch proverb tells us that “he who is outside his door already has a hard part of his journey behind him.” Therefore, whatever the case may be regarding our financial circumstances, one of the most important things that we can do in the coming weeks and months is to simply do something about our financial circumstances.

This can begin by simply reprioritizing expenses to shore up emergency cash reserves to holistically reevaluating financial priorities, taking stock of resources and developing a plan to align financial resources with a new set of life goals. Whatever the case may be, we believe that one key to getting ahead in life financially in the coming weeks, months and years is to take action today.

Personal financial playbook: your path to getting ahead

-

Households will face many near- and long-term financial market complexities and economic uncertainties in the years to come. A personal financial playbook can help people get ahead despite these challenges.

-

We believe that a flexible and adaptable personal financial playbook should include three important elements: 1) a well-defined statement of financial purpose, 2) prioritization of financial outcomes and 3) a financial operating plan.

-

Partnering with a trusted advisor can also potentially multiply your chances of achieving your financial goals and getting ahead in 2020.

Certainly, when it comes to getting ahead financially, households will face many near- and long-term financial market complexities and economic uncertainties in the years to come. And as we have noted in prior posts, the strategies for financial success that had worked in the past are not as effective as they once were, leaving many households financially insecure and unprepared for economic shocks. So, how can you prepare for the unexpected and position yourself to get ahead in life financially?

We believe that getting ahead financially means letting go of the notion of a traditional financial playbook, rules-of-thumb and other one-size-fits-all money solutions. We believe that taking an active role in creating a personal financial playbook tailored to allow for flexibility and adaptability can, over time, help you reduce money-related stresses, provide greater peace of mind and most importantly increase the likelihood of achieving life goals.

We believe that a flexible and adaptable personal financial playbook should include three important elements: 1) a well-defined statement of financial purpose, 2) prioritization of financial outcomes and 3) a financial operating plan.

Figure 1: Components of a flexible and agile personal financial playbook

A vision and purpose for your money

To the first point, a statement of financial purpose effectively helps to define the role that money will play in your life. More specifically, it articulates a clear “why” to your money habits and lays the foundation for developing strategies that help you acquire, save and spend financial resources prudently.

Formation of a financial purpose statement begins with a vision for how events would ideally unfold throughout the course of your life, beginning with your final moments and working your way back toward the present. One way to go about this is to answer questions like, “how do I want to be remembered by those closest to me?” or “what sort of legacy would I like to leave behind.” There are no easy answers to these questions by any means, yet the visualization process used to answer these and other similar questions can help crystalize the role that money will play in helping you navigate important life transitions.

Moreover, the process of vision clarification helps to prioritize financial outcomes and identifies the types of opportunities, strategies and tactics for use in achieving your financial goals. Taking the time today to develop a well-defined financial purpose statement has other long-term benefits as well, like creating a sense of financial stability by anchoring expectations during times of increasing economic and financial market uncertainty. Indeed, a quick reference of your financial purpose statement during a time of financial instability or market volatility can help to calm nerves and potentially alleviate a desire to tap long-term savings at inopportunely.

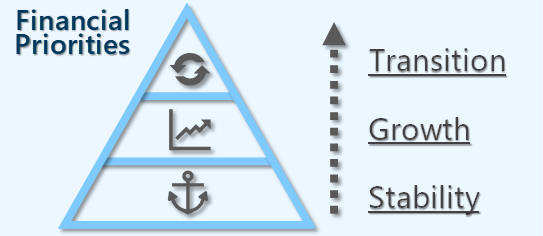

Prioritizing financial outcomes and developing financial strategies

Should you increase savings or reduce spending and if so by how much and when? Prioritization can help answer questions like these by identifying financial strategies relevant to three key financial outcomes: stability, growth and transition. The first outcome, financial stability, utilizes establishes everyday habits and leverages financial strategies that lay the foundation for financial asset growth by working to secure income, managing cash flows and becoming financially prepared when the unexpected strikes.

Figure 2: Key outcomes of financial prioritization

The next phase, financial growth, includes developing financial strategies that aligning practical financial outcomes with passions identified in your financial purpose statement. This can include developing strategies that maximize tax advantaged workplace benefits, increasing your earning potential, and acquiring and growing financial and other non-financial assets. These strategies can be used to fund goals like buying a house, paying for childhood education expenses or funding retirement goals.

In terms of prioritizing transitions, the third phase, we simply refer to the process of drawing down saved assets in a way that balances achieving your financial goals with capital preservation. While the definition is simple, the process is not always easy. Various considerations should be given to the transition outcome, including timing, magnitude and to whom assets are distributed, receiving income during periods of financial market volatility and various tax consequences of early retirement and leaving money behind to family.

Bringing the playbook together: a financial operating plan

The final piece necessary in putting together a flexible and adaptable financial playbook is creating a financial operating plan. Simply put, a financial operating plan outlines the actions necessary to bring together the passions defined in your financial purpose statement with the practical strategies outlined in your financial priorities. Developing a financial operating plan should begin with a thorough inventory of your financial affairs, including data from legal, tax, insurance and bank statements to measure typical cash flows, exposures to risk and an evaluation of assets and liabilities.

A financial operating plan should also include a projection of future or anticipated expenses associated with the vision, goals and habits defined in your financial purpose statement. This could begin with a set of ideal monthly cash flow projections and expand out to savings and growth needs to achieve long-term goals like saving for a child’s education, buying a house, starting a business or retiring comfortably.

Some analytical work will be necessary in the next step of your financial operating plan which includes evaluating your financial inventory against your financial projections. The objective here is to compare activities in your current and ideal financial states in order to select financial and lifestyle strategies that close the current-ideal gap and move you closer toward your desired life and financial goals.

One way a household may choose to close this gap, for example, is in freeing up more money for savings by downsizing lifestyle choices after having adhered to a conservative cash flow strategy. Others may choose to postpone retirement to increase benefits and look to supplement retirement savings with additional sources of savings or income. Whatever the strategies and actions defined in your personal financial playbook, the success of a personal financial playbook is only as good as its use and the degree to which the strategies outlined in it are followed through to completion.

Multiplying your chances of success with the help of a trusted advisor

Indeed, monitoring progress and making needed adjustments to your financial playbook throughout time is critical to ensuring long-term financial success. Yet, life often has a way of diverting our attention away from the things that should be done as more pressing needs arise in the present. Therefore, having the support of a trusted advisor can help keep you on track when the unexpected arises, ensuring that you execute on your financial playbook and increasing your chances of getting ahead in life financially.

Partnering with a trusted advisor has a few additional benefits: first, an advisor can identify financial lifestyle blind spots, like spending above one’s means, that you otherwise may not have been aware of. This unbiased outside perspective from an advisor can help get you back on track when certain financial habits or unexpected life events upset well laid financial plans. Next, working with a trusted advisor can bring a level of objectivity that can help during periods of uncertainty. For example, a trusted advisor can serve as an emotional buffer that keeps your savings plans on track when financial markets are experiencing increased levels of volatility.

Finally, working with a trusted advisor can increase your chances of financial success is by being your accountability partner, ensuring that you are taking the actions necessary today to see your personal financial playbook through to completion. A trusted advisor does this by lending their expertise in guiding you through the process of drawing out your long-term vision, goals and ideal financial habits as well as helping you establish priorities and strategies to get ahead financially.

Who is a trusted advisor?

A trusted advisor is also someone who meets with you regularly, setting up time to review your personal financial playbook progress, cheering you on, holding you accountable and helping you make necessary adjustments to your financial plans to ensure that you get ahead financially.

It is also important to note that not all trusted advisors are cut from the same cloth. So, what is a trusted advisor? Simply put, they have your best interests at heart and more often than not found in a fiduciary relationship. For example, doctors, lawyers and accountants are held to a fiduciary standard, meaning that they must always act in the best interest of their clients. To this point, not all financial advisors are held to a fiduciary standard, a fact that is determined by the type of firm that an advisor works for.

Another point to consider is that compensation can be an adverse motivator for financial advice when it leads to the sale of a security or insurance product. This can create conflicts of interest and potentially bias the advice that an advisor provides to their client. A bias in advice is not only limited to commissions on product sales but also includes asset under management (AUM) fees when an advisor’s compensation is based on the value of assets that he is overseeing. Either way care should be taken when selecting an advisor you can trust.

This post is an excerpt from our report, Getting Ahead Financially in 2020. You can download this report in its entirety by visiting franklinmadisonadvisors.com.

Important Disclosures

Broadview Macro Research is a division of Franklin Madison Advisors, Inc (“FMA”). The commentary provided on this website is limited to the dissemination of general information pertaining to Franklin Madison Advisors’ investment advisory services and general economic market conditions and are subject to change without notice. The information contained herein is not intended to be personal legal, investment or tax advice or a solicitation to buy or sell any security or engage in a particular investment strategy. For additional information about FMA, including fees and services, please contact FMA or refer to the Investment Adviser public disclosures.

Franklin Madison Advisors, Inc., is registered investment adviser firm with its registration and principal place of business in the Commonwealth of Pennsylvania. Registration of an investment adviser does not imply a certain level of skill or training. FMA is in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which FMA maintains clients. FMA may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Any subsequent, direct communication by FMA with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For additional information about FMA, including fees and services, please contact FMA or refer to the Investment Adviser Public disclosures. Please read the disclosure statement carefully before you invest or send money.

To learn more, visit us at http://www.franklinmadisonadvisors.com

Getting ahead isn't what it used to be

-

Various economic and market indicators suggest the U.S. economy is in a better spot today than a decade ago.

-

While some are more well off today, the traditional life playbook for getting ahead has seemingly failed many households.

-

Looking ahead, we believe that the key to households getting ahead financially will be for households to customize their own personal financial playbooks.

By many measures the U.S. economy is in a better spot today than it was a decade ago. In ten short years the size of the U.S. economy has expanded by $4 trillion, unemployment has fallen to a near 50-year low and household wealth is on the rise as stock market prices and home values have surpassed pre-Great Recession levels.

Yet, the improving economic and financial market landscape has left some people behind. In fact, the Great Recession has disrupted traditional financial playbooks and left in its wake many individuals and households who are finding it increasingly difficult to use today’s financial resources to make tomorrow’s important life transitions happen.

A traditional financial playbook and the broken path to success

For some individuals, a traditional financial playbook might have served as a guide to success in finances and life that included going to college, finding a good job, getting married, starting a family, putting some money away in savings and maybe envisioning a few comfortable decades in retirement thanks to a comfortable pension. Along the way they could buy a house, a car or two and spend modestly on home furnishings, personal luxuries and maybe a vacation once or twice per year.

Yet the reality for many is that college has become more of a financial burden than a ticket to financial security. What’s more, planning for retirement has become complicated by households’ increasing need to simultaneously support both younger and older generations all the while lower investment rates of return and increased financial market distortions have complicated traditional retirement savings strategies.

At the same time, a groundswell of geopolitical uncertainties and rising social unrest globally have generated more economic worries in the near term. This has led to a rise in job insecurity as business leaders curb discretionary spending and has reduced hiring activity. Moreover, financial market distortions, debt traps and rising political concerns have challenged the strategies contained in many people’s traditional financial playbooks.

Figure 1: The U.S. economy is $4 trillion larger today than in 2009

The need to redefine a traditional financial playbook

Looking ahead, simple rules-of-thumb and one-size-fits-all strategies that had helped many people get ahead financially decades ago are less likely to cut it in today’s economic and financial market environment. Indeed, navigating important life transitions in a time of increasing complexity and uncertainty likely means that many households will need to tailor a personal financial playbook to suit their own unique purposes and priorities, selecting strategies and developing plans that accommodate a household’s ever changing wants, needs and goals.

To this point, getting ahead financially will require households to become increasingly financially agile. Broadly speaking, this means incorporating creative strategies into their personal financial playbook that balance a suitable quality of life today with the need to build long-term savings for tomorrow.

More specifically, we believe that financially successful households will need to take a more functional role in crafting their personal financial playbook. This includes more actively defining a purpose for their money, prioritizing its use and developing processes used to test, monitor and alternate financial strategies that utilize today’s financial resources in preparation for expected and unexpected life events and to accommodate various life transitions.

In our next post we’ll look at some of the factors that have, in recent years, prevented some households from getting ahead.

This post is an excerpt from our report, Getting Ahead Financially in 2020. You can download this report in its entirety by visiting franklinmadisonadvisors.com.

Important Disclosures

Broadview Macro Research is a division of Franklin Madison Advisors, Inc (“FMA”). The commentary provided on this website is limited to the dissemination of general information pertaining to Franklin Madison Advisors’ investment advisory services and general economic market conditions and are subject to change without notice. The information contained herein is not intended to be personal legal, investment or tax advice or a solicitation to buy or sell any security or engage in a particular investment strategy. For additional information about FMA, including fees and services, please contact FMA or refer to the Investment Adviser public disclosures.

Franklin Madison Advisors, Inc., is registered investment adviser firm with its registration and principal place of business in the Commonwealth of Pennsylvania. Registration of an investment adviser does not imply a certain level of skill or training. FMA is in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which FMA maintains clients. FMA may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Any subsequent, direct communication by FMA with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For additional information about FMA, including fees and services, please contact FMA or refer to the Investment Adviser Public disclosures. Please read the disclosure statement carefully before you invest or send money.

To learn more, visit us at http://www.franklinmadisonadvisors.com

How to Stay Sane when the Markets are Going Crazy

Let’s face it, no one wants to be the one person that missed out on what seems to be a once-in-a-generation investment opportunity simply because you’re trying to do the right thing. This decision is especially difficult at a time when making money in the markets seems so easy. Without a doubt, the fear of missing out on a great opportunity is so powerful that in the past it had encouraged otherwise rationale investors to put money into worthless tech companies in 2000 and prompted hairdressers in Florida during the housing boom to purchase three or four rental homes they just couldn’t afford. Even so, as Jeremy Grantham puts it, “there’s nothing more irritating than seeing your neighbors get rich.”

There’s no doubt that, in certain segments of the markets today, individuals are experiencing phenomenal returns in their holdings of tech, bitcoin, penny stocks and by participating in the options market. For example, the NASDAQ 100 index gained 96 percent from the market bottom in March 2020. Bitcoin, also, has gone from a price of $8,880 twelve months ago to well over $34,000. Names of penny stock companies (stocks that trade for less than $5 per share) have doubled or even trebled in a matter of weeks and months and now account for a growing share of trading activity. With results like this, it’s hard not to feel like you’re missing out on something spectacular when you’re watching from the sidelines.

And it becomes increasingly difficult to remain on the sidelines when these seemingly effortless opportunities to make money are minting new affluent lifestyles every day. To make matters worse, today’s mainstream media is increasingly caught up in reporting on the ease with which amateur investors are turning their stimulus checks into thousands of dollars in gains. Likewise, social media is blowing up with content from amateur investors promising fast returns by following simple rules for speculating in the markets.

To many of us, it’s easy to look at what’s going on today and call it for what it is: it’s market speculation. Even so, with seemingly everyone partying and making money hand over fist, the psychological pressure may grow to the point where you begin to ask yourself: “am I missing out on a great opportunity?” Even when you know that this latest investing craze completely flies in the face of your disciplined savings and investment plans.

So, what can you do when going against the crowd feels increasingly uncomfortable and to the point where fear of missing out is eroding your willpower to remain committed to a disciplined investment strategy? During times like these, it’s crucial to remember that what’s going on today has happened before, and it will likely happen again. That’s why gaining some perspective and reminding yourself why you became an investor and what you have to lose is essential to staying grounded when you feel tempted to follow the crowd and are potentially setting yourself up for failure. So how exactly did we get here?

It’s Happened Before, and It’ll Happen Again

Well, it’s vital to recall that much of the gains in some portions of the markets have been fueled by easy money policies and individual investor euphoria and not sound fundamentals. Recall that skyrocketing unemployment caused by a devastating global healthcare crisis last year led to trillions of dollars being pumped into the financial system and the economy. Fueled by access to cash and success in the early 2020 rally, some individuals today have shifted their focus to the highly speculative market segments we mentioned earlier. In many cases, price action in these parts of the market have little, if any, relationship to company value, revenue, or earnings growth.

Rather, market action in these cases appears to be solely based on speculation of what the asset’s price might be tomorrow, next week or next month. And to this point, one mantra driving participant behavior is “prices can only go up.” Ultimately, we could say that the Greater Fool Theory is driving the markets. More specifically, this theory states that an asset’s value is driven solely by price expectations and not some fundamental underlying factor.

The Greater Fool Theory

Now, if you’re not familiar with the Greater Fool Theory, it goes something like this: I know that the price I’m paying for this asset today doesn’t make much sense, but that doesn’t matter. The market is hot, and there’s so much demand for a given investment that there will almost certainly be a buyer sometime soon. Therefore, I’m going to buy today hoping that I can flip this asset to the next newly minted naïve investor.

This mindset has become so pervasive that it’s spread across discussion groups that were once personal finance strongholds for the disciplined do-it-yourself investor. For instance, White Coat Investor recently shut down a Facebook group after becoming a hotbed for bitcoin speculators and hot-stock tip discussions. In another example, Bogleheads community members have increasingly become divided on whether individuals should take out a personal loan or use their credit card to purchase shares of already high-priced tech stocks. Does what’s going on today at all sound familiar to you?

Recall that skyrocketing US home values in 2006 and 2007 didn’t happen because of a baby boom. They happened because interest rates were low, and mortgage lenders and house flippers believed that prices would rise forever. This sentiment became pervasive throughout the media and government policy and led to many TV shows and seminars devoted to getting rich in real estate. When the music stopped, however, the finances of millions of individuals were devastated. While it’s still too soon to establish how our story will play out, there’s a good chance that the asset bubbles forming today likely won’t end with a soft hiss but with a loud bang.

What’s Your Motivation?

Sometimes having a rational understanding of the facts may not enough for you to shake that uncomfortable feeling that something good might be passing by. If you find yourself in this situation, you’ll likely need to dig deeper to gain a clearer perspective and stay grounded in your long-term plans. And this begins with setting aside some time to consider your core motivation for saving and investing before you get caught up by what’s happening in the markets today. To this point, you’ll need to ask yourself if your primary motivation for investing is to keep up with the Joneses or to carve out your own definition of financial independence.

You’ll likely recall that individuals like you have achieved financial independence by saving prudently, earning a steady rate of return on their investments, and making their money work for them. More often than not, individuals on the path to financial independence are focused on systematically creating, growing or preserving their wealth and care less about what others are doing with their money. So, if you’re tempted to participate in the current market exuberance, now may be the time to ask yourself if the choices you’re considering align with behaviors that lead to long-term success.

If your priority is to generate a steady rate of return over the long run, then making incremental, short-term bets on what appears to be an outsized financial gain may not cut it.

Indeed, history has shown that a disciplined investment strategy, adhered to over a long period, can lead to exponential savings growth. Various academic studies have also illustrated how asset allocation and not stock selection or market timing have been the most significant determinant of investment returns.

How will it Feel to Lose?

By now, the various facts and arguments discussed here may not be enough to convince you to stay the course. You might be considering allocating just a small portion, rather than all of your savings, to these highly speculative segments of the market. If this speaks to you, then you’ll need to think hard about your pain tolerance. In a recent note to investors, UBS warned that some of today’s speculative assets could see their prices fall to zero. And to this point, a key risk in today’s markets is that few individuals remember what it’s like to lose money when winners are created seemingly every day.

If you’re tempted to dabble in parts of the markets where sentiment is hot, ask yourself how you’ll respond emotionally should that investment go to zero. Academic research has shown that the negative emotions that an individual feels by losing a new gain is more potent than not having made money in the first place. What’s more, taking your focus off your long-term investment strategy during a time of emotional turmoil might leave you open to questioning your overall investment process. When the music eventually stops, and the party is over, there will be a rush to the exits, and that’s not the time you want to be figuring out what to do with your investments, especially when emotions are running high.

Don’t be the Bagholder

Finally, don’t be the bagholder. Make no mistake: bubbles do eventually burst. And a bagholder is an individual who holds on to their declining speculative investment, hoping that prices will eventually recover. Whether we’re talking about the Tulip Mania, South Sea Crisis, Tech Bubble or Housing Crisis, they all start, grow and end the same way.

No one can say for sure, in our current situation, whether that moment will come next week or next month.

Either way, rather than trying to time the market, we recommend looking ahead to long-term investment opportunities positioned to perform well at this stage in the economic cycle. Many indicators suggest that the US economy could experience a strong recovery in 2021.

And from this perspective, yesterday’s winners can quickly become tomorrow’s losers. That’s why it’s vital now more than ever to spread your investments across high quality, uncorrelated assets that offer high relative risk-adjusted returns.

As we’ve discussed in previous reports, we believe that a market rotation is currently underway. Value names, small-cap and emerging market stocks are well-positioned as the US and global economy recovers. A key risk to this outlook, however, is predicated on accelerated COVID vaccination rates. Without this, a return to normal may not happen as soon as the second half of this year.

Even so, accommodative fiscal and monetary policies are likely to support higher growth levels into the coming year. Make no mistake, there are no easy answers to the powerful psychological forces of going against the crowd. But by looking past the latest investing craze, reminding yourself of your financial independence goals, digging deep to figure out what you have to lose, and staying committed to a long-term, disciplined investment strategy, you might just be able to maintain your sanity when it seems like the markets are going crazy.