Set Financial Boundaries and Gain Peace of Mind

Are you good at setting boundaries? If you’re not, then rest assured that many individuals struggle with setting and enforcing boundaries.

And what kind of boundaries are we talking about here?

Well, imagine for a moment that a school’s playground is situated so close to a highway that you could reach out and touch the passing cars. In fact, there are no fences surrounding the playground and cars zip right by at 80 miles per hour, unimpeded.

Now, understandably, when it’s time for recess, both the teachers and children face an overwhelming amount of stress and anxiety as they head out to play. For the kids, their concern is getting too close to the edge of the highway, so they play in the center of the yard for fear of the vehicles passing by at high speeds.

And for the teachers, their anxiety comes from the constant worry about a rogue child leaving the playground and wandering onto the highway, which could ultimately lead to a tragic outcome. It then goes without saying that in this situation, recess is not an enjoyable experience for either the children or the teachers. That’s because they spend their free time huddled up in the center of the schoolyard, each vigilant for their own reasons, instead of enjoying the present moment.

Now, let’s say that the city puts up a reinforced concrete wall to separate the highway from the playground. How do you think this outcome would change the recess experience? Certainly, with a solid fence in place, the children can utilize the entire playground, and run right up to the wall, without worrying about all of the high-speed traffic on the other side of the barrier.

At the same time, the teachers would likely be less anxious because they can rest assured that the newly constructed barrier will prevent a wayward child from wandering on to the highway.

Now, if you’re a parent out there, how would you feel knowing that your child was playing near a busy highway with nothing standing between them and the cars? Well, too often, that’s what happens when we set about managing our money without setting prudent financial boundaries.

Like a protective wall separating a school playground, boundaries tell others where they end and you begin. While on the surface setting boundaries seems to look like a form of restriction or control, this practice involves setting limits on how much emotional energy and time we give to others and ourselves and has the benefit of clarifying expectations, demonstrating self-esteem, fostering trust and encouraging mutual respect.

And when it comes to money, financial boundaries are intended to set a wall around how you use your life energy to manage your finances.

To be sure, financial boundaries are essential for maintaining a healthy relationship with not only our money, but also with your friends and family. And by embracing financial boundaries, you can likely experience increased financial stability and harmony in both personal and relationship contexts, and more importantly, make essential financial decisions while protecting your emotional and mental well-being.

Understand How Boundaries Can Help You

So, how can setting financial boundaries improve the money relationships you have with yourself and others?

Clarifying Expectations

Well, let’s look at it from the perspective of clarifying expectations.

By outlining the limits of acceptable behavior and communicating these limits effectively, you help others understand what you expect from them.

For instance, in the book, Boundaries, by Henry Cloud and John Townsend, they describe scenarios where someone like Bob, for example, frequently shows up unannounced at Tom’s home, expecting to be welcomed in at any time, without regard for Tom's schedule or needs.

By setting a boundary, Tom would communicate to Bob that while he values their friendship and wants to spend time together, Bob needs to call or schedule a visit in advance, so that Tom can prepare and make time for him. This act of setting boundaries helps to clarify expectations and set mutual respect for each other's time and space.

And without a boundary in place, Bob may continue to show up unannounced, causing stress and resentment in the relationship. That’s why by setting a clear boundary, both parties know what is expected and therefore they can maintain a healthier, more respectful relationship going forward.

Self-Respect

Another benefit of establishing boundaries is that it demonstrates self-respect to ourself and others. That’s because when we communicate our needs and expectations, it signals that we value ourselves and our well-being.

In Nancy Levin’s book, “Setting Boundaries will Set You Free,” the author gives us an example of someone like Michelle, who has a pattern of always saying "yes" to her boss's requests, even if it means sacrificing her own needs and personal time.

And by setting a boundary and saying "no" to certain requests, Michelle demonstrates that she values her own time and energy, and that her needs are important too. And this act of self-respect can lead to a greater sense of empowerment and self-worth.

What’s more, Levin argues that when we establish healthy boundaries, we show ourselves and others that we are worthy of respect and consideration. And by setting limits on what we are willing to tolerate, we communicate that our needs and feelings matter, and we create a foundation for healthy relationships built on mutual respect and understanding.

Fostering Trust

Now, setting clear boundaries can also fosters trust because when we’re open about our needs and expectations, we show our reliability and trustworthiness.

For example, in her book "Daring Greatly," Brene Brown shares a story about a woman like Gretchen, who was struggling the relationship she had with her mother-in-law. Now, Gretchen felt like her mother-in-law was constantly criticizing and interfering in her life, and she was having trouble setting boundaries.

With time, Gretchen learned to set clear boundaries with her mother-in-law, telling her that she could not tolerate the constant criticism and interference in her life. As a result, this specific relationship improved and Gretchen felt more respected and valued.

Now, Brene suggests that setting boundaries in this way fosters trust because it establishes clear communication and mutual respect. And when we’re able to communicate our needs and expectations effectively, we show that we are reliable and trustworthy, which builds stronger relationships and fosters a sense of trust in our personal lives as well as our professional ones.

Mutual Respect

Finally, establishing our limits while also honoring other people’s boundaries leads to more rewarding and mutually beneficial relationships through mutual respect.

For example, in the Boundaries book, Cloud and Townsend share a story about a woman like Sarah who was constantly being taken advantage of by her friends. That’s because Sarah was always available to listen to their problems and offer support, but when she needed help, Sarah’s friends were nowhere to be found.

Over time, Sarah learned to set clear boundaries with her friends and communicate her needs and limitations. In fact, Sarah stopped being the "go-to" person for everyone's problems and started focusing on her own needs and goals.

As a result, Sarah’s relationships with her friends improved, and they learned to respect her boundaries and limitations. What’s more, Sarah was able to establish a more balanced and mutually beneficial relationship with herself and her friends.

Indeed, Townsend and Cloud suggest that when we are able to communicate our needs and limitations effectively, we create a space for others to do the same, which leads to a healthier and more balanced relationship for everyone involved.

To be sure, setting boundaries is crucial for fostering healthy, fulfilling, and respectful relationships. And by clarifying expectations, showing self-respect, building trust and fostering mutual respect, we can create a strong foundation for effective communication and more importantly, financial and emotional well-being.

Set Financial Boundaries with Yourself

Alright, so now that we have a baseline for what healthy boundaries are, let’s look at this approach from the context of how you deal with your own money.

Indeed, while boundaries often tell others where they end and you begin, when it comes to setting financial boundaries, we often need to start with focusing on ourselves.

And what does this mean?

Well, psychologist Anne Katherine in her book "Boundaries: Where You End and I Begin," explains that setting boundaries with yourself involves recognizing your limits, being aware of your emotional and physical needs, and asserting those needs to maintain a healthy balance in your life.

That’s because setting boundaries with yourself can help you avoid burnout, manage stress, and cultivate a sense of self-worth. And without this healthy baseline in place, you can’t expect others to support or respect the boundaries you plan to set with them.

Indeed, when it comes to financial boundaries, Anne Katherine's insights can be applied in a similar fashion. Based on her book, Anne likely would emphasize the importance of understanding your financial needs and limits, setting clear guidelines for spending, saving, and investing, and practicing self-discipline to adhere to those guidelines.

Boundaries and Giving Your Money Purpose

So, then, how do you go about doing the work of setting financial boundaries with yourself?

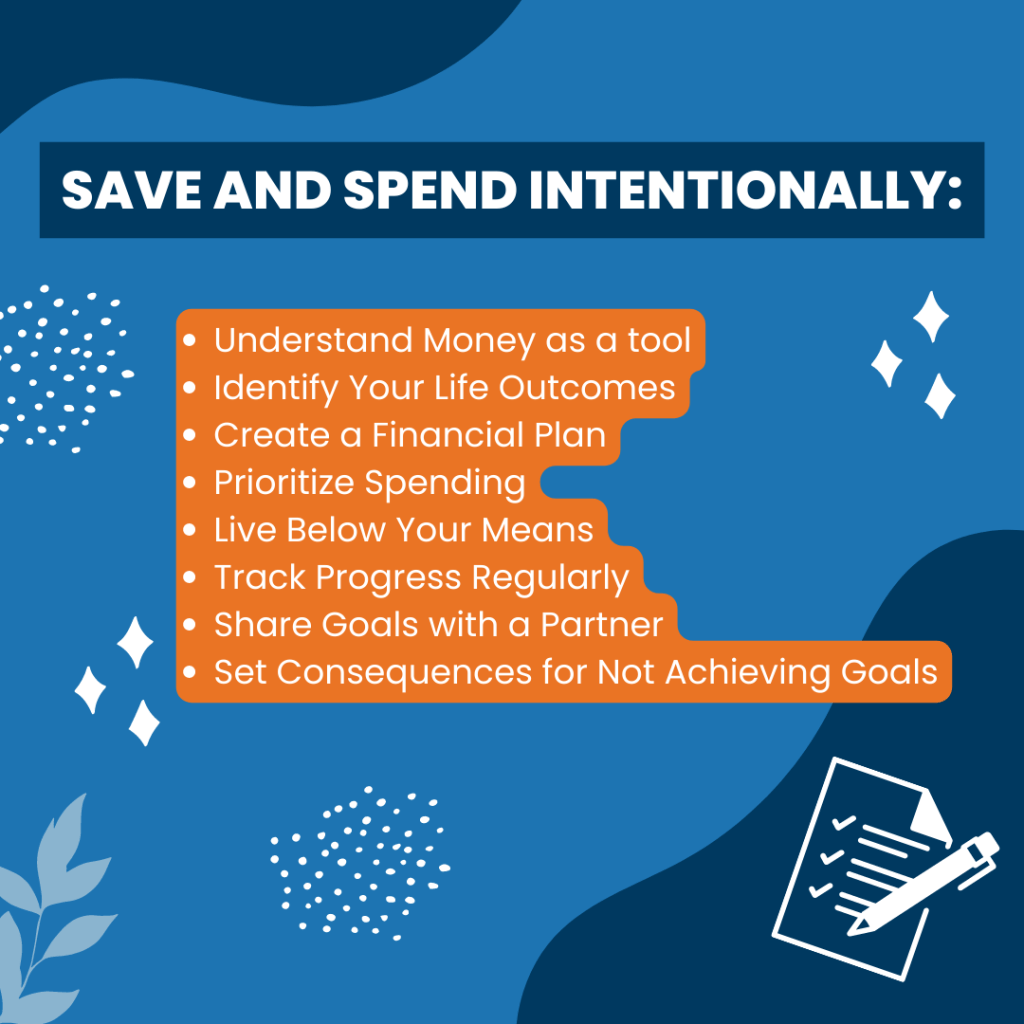

Well, to start, setting financial boundaries with yourself involves identifying a purpose for your money, and then aligning your own spending, saving, and investing habits with your broader values and purpose. This approach can help you establish a sense of control over your finances and financial future and ultimately help reduce your financial anxiety.

Indeed, creating a financial plan that includes a solid cash management process, allocating a certain percentage of your income towards savings and investments, and avoiding unnecessary expenses are all forms of setting clear boundaries about your money.

For example, consider Samantha’s story. Now, Samantha is a 38-year-old software engineer, who recently received a significant salary increase after her promotion. Now, despite her newfound financial success, she found herself feeling out of control and anxious about her financial future, as she struggled to maintain healthy financial boundaries.

Without a purpose for her money, Samantha was unsure how to allocate her income wisely. She had no idea how much of her salary should be set aside for savings and investments, and her spending habits had become increasingly impulsive. Now, this lack of control over her personal finances also affected her financial boundaries with others. That’s because she often found herself lending money to friends and family without considering the impact on her own financial stability.

And Samantha’s anxiety intensified when she realized that her lack of a solid cash management process left her with minimal emergency funds, making her vulnerable to unexpected expenses. What’s more, her inability to track her spending meant she was often surprised by her credit card bills at the end of each month.

So what did Samantha do? Well, to regain control, Samantha put in the work to identify her personal values and what she ultimately wanted to get out of her life, and created a financial plan that would finally give her money purpose.

And by doing this work, Samantha was able to establish a monthly budget that included allocating a certain percentage of her income towards savings and investments, as well as setting limits on discretionary spending. What’s more, Samantha started using her cash management process to track her expenses, which helped her avoid unnecessary costs and gain more financial confidence.

Boundaries to Reduce Emotional Spending

Another way to set financial boundaries with yourself is to become more aware of your propensity to spend impulsively or emotionally. And doing so can help prevent purchases outside of your budget or not aligned with your values or the purpose that you’ve defined for your money.

Remember, a boundary is a decision about how and where you give your emotional energy. And from this perspective, Bari Tessler, the author of "The Art of Money," emphasizes the importance of establishing emotional boundaries as a tool for overcoming impulsive spending.

Indeed, Tessler believes that impulsive spending is often a response to emotional triggers such as stress, anxiety, or a desire for instant gratification. And by setting financial boundaries, you can learn to identify and manage your emotions in healthier ways, which can reduce the urge to engage in impulsive spending.

So, how do you establish boundaries in this arena? Well, Tessler suggests several ways to establish emotional boundaries to overcome impulsive spending, and the first of which is to develop awareness of your emotional triggers.

From this perspective, if you have trouble with setting boundaries on emotionally driven or impulsive spending, Tessler recommends keeping a journal to track your emotional responses and subsequent spending habits. Doing so can help you identify patterns and triggers that lead to impulsive spending, and potential ways to address them.

Then, once you have identified your emotional triggers, Tessler suggests setting limits on your emotional responses. For example, if you find that stress triggers impulsive spending, you can set a boundary to take a break or engage in a stress-reducing activity before you pull the trigger on that next regretful purchase.

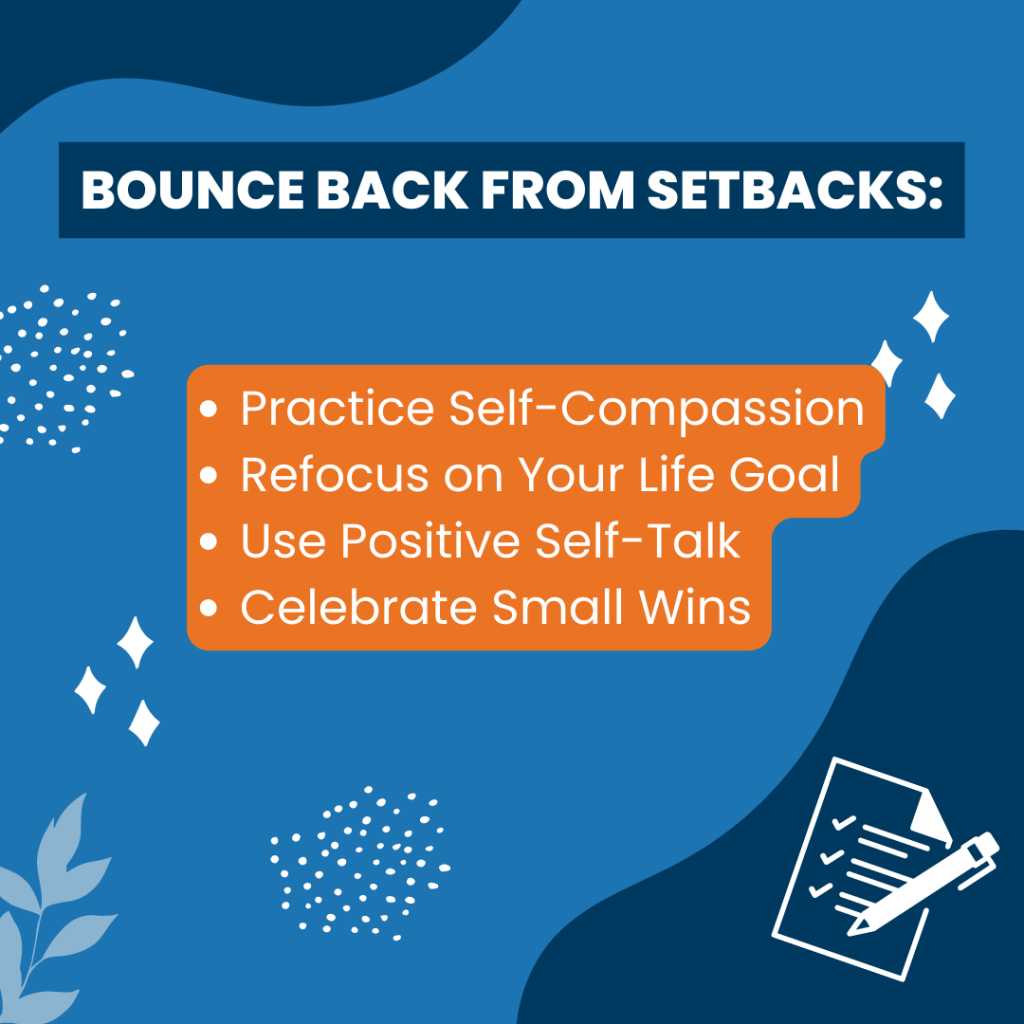

Tessler also emphasizes the importance of practicing self-compassion when establishing financial boundaries to curtail emotional spending. This means being kind and understanding with yourself, even when you make mistakes or struggle to avoid impulsive spending. Indeed, self-compassion can help you stay motivated and avoid feeling discouraged or overwhelmed.

Boundaries to Foster Healthy Financial Habits

Lastly, setting clear financial boundaries can help you develop sustainable money habits. Remember, the act of setting boundaries with yourself is about deciding where you will (and won’t) devote your time and energy.

Indeed, Mark Manson the author of, "The Subtle Art of Not Giving a F*ck," argues that people often have a limited amount of time, energy, and attention to devote to different areas of their life. And, so, when it comes to your money, three areas where you give your energy are founded in your values, responsibilities, and control.

So, then, from this perspective, the first thing you’ll want to focus on to develop sustainable financial habits is to set boundaries on your values and priorities.

What does this mean?

Well, let's say that one of your core values is to be financially independent. When your choices are driven by this value, you’ll likely prioritize saving money each month and avoid overspending on non-essential items, such as eating out or buying expensive clothes. And, by aligning your spending habits with your values, you can create a sense of purpose and motivation for sticking to your financial habits.

And, so, how do you go about doing this?

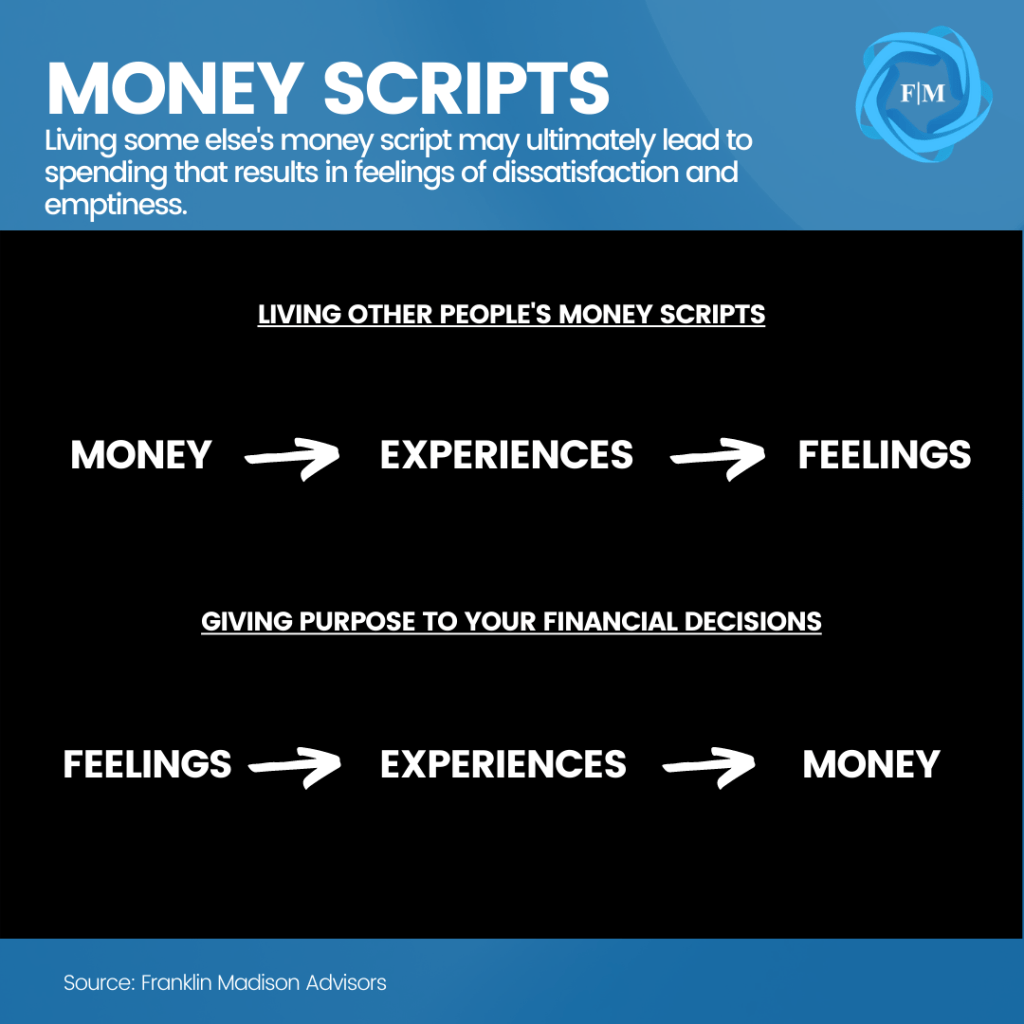

Well, take some time to reflect on your beliefs, attitudes, and behaviors around money and evaluate whose money script you’re living.

Remember, a money script is a set of thoughts, beliefs and attitudes you have about money that, more often than not, are influenced by the people around you. If you’re not sure whose script you’re living, then be sure to check out our recent posts on Money Scripts so that you can get some much needed guidance in this area.

Next, set boundaries to be more responsible. Now, responsibility refers to your obligation to take care of yourself and your finances. And so, setting financial boundaries involves taking responsibility for your financial rituals. For example, let's say that you have a habit of ignoring your bills and not keeping track of when they are due because you’re dealing with financial procrastination.

Naturally, this can lead to missed payments, late fees, and damage to your credit score. Therefore, taking self-responsibility in this situation, would involve identifying emotional triggers that are leading to your willingness to procrastinate.

At the same time, it may also involve taking the time to review your bills each month and checking your bank statements for errors or discrepancies to ensure that you’re not leaving money on the table. Either way, setting responsibility boundaries can help you stay focused on what needs to be done, and help develop sustainable habits.

Finally, set boundaries around what you do and don’t have control over. Remember, you can’t control where the markets are headed, but you can control your investment strategy. You can’t always control when you or a loved one will pass away, but you can control how you’ll prepare financially for just such an event. You can’t control whether you’ll lose your job, but you can be prepared if it happens.

Indeed, Franklin Covey, in his book, “Seven Habits of Highly Effective People,” suggests that if you want to use your life energy wisely, you’ll need to have a clear understanding of what you can and can’t control. Covey refers to this as the circle of influence.

And what does this mean?

Well, according to Franklin Covey, there are three areas of the circle of influence:

- Circle of Concern: This includes all the things that an individual is concerned about, but has little or no control over, such as the weather, political events, or other people's behavior.

- Circle of Influence: This includes all the things that an individual can impact including their own behavior, thoughts, and emotions, as well as their relationships and work.

- Circle of Control: This includes all the things that an individual has complete control over, such as their own actions, choices, and attitudes.

Now, when it comes to choosing where to give your energy, Covey emphasizes the importance of focusing on the circle of influence and circle of control, rather than expending energy on things in the circle of concern that cannot be changed. That’s because by focusing on what can be controlled, you can create sustainable habits and make progress towards your financial independence goals.

The big takeaway here is that personal financial boundaries are about deciding who and what gets your emotional energy when it comes to your money. And by creating boundaries around your money’s purpose, emotional spending, and habits, you can create mental and emotional space to concentrate on pursuing your long-term life and financial goals.

Setting Financial Boundaries with Others

And now, the final point that we’ll discuss when it comes to financial boundaries is those we set with other people. Now it's crucial to set boundaries around money when dealing with other people, and here’s why.

First and foremost, if you don't set boundaries, you might end up giving away, lending or spending more money than you can afford, which could put you in a tough spot. Now, imagine if money issues started causing problems in your relationships with friends or family. That wouldn't be great, would it? Well, setting boundaries helps avoid misunderstandings and keeps things from getting awkward or causing conflicts.

You might wonder, how can setting financial boundaries help others? Well, by setting effective financial boundaries with others, you encourage them to be responsible with their own money. This way, they learn how to manage their finances and become more independent, rather than relying on you when they fall short in their own financial habits.

Indeed, when you set appropriate financial boundaries, you can help reduce your own stress and guilt because you won't constantly feel like you have to help others financially.

Let me explain what I mean here by telling you a story about, Lisa.

Now, Lisa is a successful marketing executive who's really smart about her money. But there was a time, however, when she found herself in a bit of a financial predicament, all because of social pressures.

You see, Lisa's friends loved going out for fancy dinners, taking expensive vacations, and basically, just living the high life. And Lisa, not wanting to feel left out or seem stingy, would simply go with the flow, even though she knew it wasn't the best choice for her finances.

What was the result?

She was constantly stressed about money and struggling to save for her future.

Then, one day, Lisa decided she'd had enough. She knew she needed to set some financial boundaries and be more open about her money matters with her friends and family.

So, what did she do?

Well, the next time her friends invited her on a luxury weekend getaway, Lisa took a deep breath and said, "Guys, I appreciate the invite, but I've got to be honest with you—I'm trying to be more responsible with my money, and this trip is out of my budget right now."

Now, to her surprise, a few of her friends admitted they were feeling the same way! They'd been silently struggling with keeping up with their own social pressures, but were too embarrassed to say anything.

In fact, Lisa's honesty sparked a conversation about finances among her friends, and they started brainstorming ways to have fun without blowing their budgets.

Now, Lisa and her friends have a new tradition: once a month, they get together for a potluck dinner at someone's house instead of going out to an expensive restaurant. They still have a great time, and the best part? Everyone's a lot less stressed about money.

So, what's the big takeaway? Don't be afraid to assert your financial boundaries and talk openly about money with your friends and family. That’s because you might just find that others are in the same boat, and you'll all be better off for it.

By this point you might be thinking to yourself, “the approach sounds simple, but how do you actually make this happen?”

How to Set Boundaries with Friends and Family

Well, in the book "Set Boundaries, Find Peace," author Nedra Tawwab discusses the importance of setting financial boundaries with friends and family. She emphasizes that money can be a sensitive and emotionally charged topic, so setting boundaries around finances is crucial for maintaining healthy relationships.

But how do you set these boundaries with friends and family?

First things first, know your own financial goals and limits. This understanding comes from the work you did in setting your own personal financial boundaries and can help you more clearly articulate your own financial expectations and goals before engaging in conversations with friends and family about money. Then, use what you’ve learned about your own financial boundaries to communicate to others what you’re willing and unwilling to do when it comes to your money.

For example, let’s say that you’re considering co-signing on a loan with a friend or family member. In this case, take the time to review your own financial goals and the purpose that you’ve defined for your money. This will help you determine whether co-signing is a good fit for your own financial situation and whether you can afford the risk.

Next, be clear and consistent in your communication. More specifically, when discussing money with loved ones, it's important to be clear about your boundaries and consistent in enforcing them so that you can avoid blame or miscommunications.

For example, if you've established a boundary with a family member, and they’re still hassling you to lend them money, then you might need to remind them of the boundary, and learn to use "I" statements to express your own needs and concerns.

And what if you have to say "no"? Well, truth be told, setting financial boundaries often involves saying "no" to requests for money or financial assistance. But remember that saying "no" is not a rejection of your loved ones, but rather a way to prioritize your own financial well-being.

For example, if a friend asks to borrow money and you're not comfortable with the request, say "no" in a firm but respectful manner. Here, you can explain that you're not in a position to provide financial support, but you're happy to help in other ways if possible.

Also, if you’re unwilling to say “no” outright, try thinking through some alternatives, such as helping your loved ones find other sources of financial support or offering to provide non-financial assistance.

For example, if a family member asks for a loan that you're not comfortable providing, you can offer to help them find other sources of financial support, like connecting them with local financial resources or recommending job opportunities. Alternatively, you can provide non-financial assistance, like helping them move or offering emotional support.

Finally, take care of your emotional well-being. Setting financial boundaries can be emotionally challenging, so prioritize your own well-being throughout this process is essential. And what does this look like? Well, taking care of your emotional well-being might involve seeking support from a professional, practicing self-care, and being patient with yourself as you navigate this process.

For example, if setting financial boundaries with loved ones is causing you emotional stress, seek support from a therapist or trusted friend. You can also practice self-care activities, like meditation or exercise, to help manage stress and maintain a sense of well-being. Overall, be patient with yourself as you navigate this process and prioritize your own emotional needs.

Remember, social pressures can heavily influence your own financial decisions, making it crucial to assert financial boundaries with friends and family. And by establishing clear guidelines and openly discussing money matters, you can navigate social expectations and emotional pressures while maintaining your financial well-being.

Set Financial Boundaries and Gain Peace of Mind

When it comes down to it, financial boundaries play a pivotal role in achieving your long-term life and financial goals by enabling you to stay emotionally disciplined when you’re tempted to do otherwise.

Indeed, by taking the time to assess and tweak your boundaries, you're giving yourself the opportunity to respond to life's inevitable ups and downs with flexibility and resilience.

But what's the ultimate outcome of embracing financial boundaries? The answer is simple: increased harmony, stability, and overall well-being in both your personal life and your relationships. Indeed, when you actively engage with your finances in a thoughtful, proactive manner, you're not only setting yourself up for success but also fostering healthier, more fulfilling connections with those around you. But most importantly, doing the work of setting healthy financial boundaries ultimately takes you one step closer to becoming the master of your own financial independence journey.

What's the Cost of Too Many Financial Accounts?

Did you know that having too many financial accounts can actually be more counterproductive than being useful? To be sure, while some individuals view having multiple financial accounts as making them better stewards of their finances, the truth is that being overbanked can lead to serious financial problems.

And that's what happened to Brian. Now, Brian is an ambitious entrepreneur with a passion for personal finance. And Brian believed that the more accounts he had, the better he could manage his finances and grow his wealth.

Even so, little did Brian know that his obsession with opening and managing various financial accounts would take a toll on his mental health and cost him dearly.

And, that's not because Brian didn't know how to manage his money. In fact, Brian had always been a high achiever. He graduated at the top of his class from a prestigious business school and quickly climbed the corporate ladder, earning a six-figure salary enabling him to make the leap and start his own business.

As his wealth grew, so did his appetite for diversification. So much so that Brian believed that opening multiple bank accounts, credit cards, and investment accounts would provide him with better financial security and opportunities for growth.

And, over the years, Brian accumulated several dozen bank accounts, credit cards, and investment accounts. Even so, Brian meticulously tracked the balance, interest rates, and fees for each account, ensuring that he maximized his returns. In fact, he spent countless hours poring over spreadsheets and statements, monitoring his cash flows, and making complex transactions between accounts.

Now, at first, Brian's strategy seemed to work. His wealth grew, and he felt a sense of accomplishment from his financial prowess. But as Brian brought on new clients and his business grew, so did the complexity of his financial situation.

And as his finances became more complex, Brian's stress level started to rise. Indeed, whenever a statement arrived in the mail, or an email notification popped up on his phone from a financial institution, Brian felt a wave of anxiety wash over him. The truth is that the sheer volume of information related to his finances was so overwhelming that he struggled to keep track of all the financial details.

The turning point came when Brian missed a credit card payment deadline. He had always prided himself on his financial responsibility, but the oversight led to a hefty late fee and a hit to his credit score. And it was that incident that shook Brian to his core, forcing him to question whether his financial strategy was really working.

Nevertheless, despite the warning signs, Brian stubbornly refused to simplify his finances. He believed that his system, while complex, was still the best way to manage his money, and this decision came at a steep cost. That's because the stress from managing so many accounts at once led to more oversights and errors, resulting in additional fees and penalties. As this happened, his stress levels skyrocketed, which affected his work performance and personal relationships.

So, what happened?

Well, Brian's once-pristine credit score plummeted, making it difficult for him to secure cheap funding to keep his business afloat. What's more, his investment accounts suffered, as he was unable to give each account the attention it required. Eventually, Brian's professional and personal life began to suffer as a result of his financial struggles.

And, only when Brian hit rock bottom did he finally recognize that something needed to change. At that point, he realized that his finances had become unmanageable, leading him to admit that he needed to simplify his financial life.

Now, as Brian began working to simplify his financial life, he noticed a significant decrease in his stress levels. In fact, he no longer spent countless hours poring over financial statements or worrying about missing important details. And as a result, his professional performance improved, and he gradually repaired his relationships with friends and family.

The Mental and Financial Costs of Too Many Financial Accounts

In the end, Brian learned a valuable lesson: sometimes, less is more. His pursuit of financial complexity had limited his ability to remain financially flexible, ultimately costing him far more than it had earned. By embracing simplicity, however, Brian was able to regain control of his finances and, more importantly, his life.

Can you relate to Brian?

The truth is that many individuals today are overbanked or have too many financial accounts spread across various financial institutions, and it's costing them their ability to manage everyday stresses and to remain resilient to one-time shock events.

The Mental Costs of Being Overbanked

In turn, these complex processes for managing their finances quickly spiral out of control, leading to unnecessary financial costs and setbacks.

Indeed, there are many costs associated with being overbanked, and it all starts with cognitive overload.

So, what is cognitive overload?

Well, cognitive overload is when you become so stressed that you don't know what to do next. And this typically happens when your brain cannot process and handle the overwhelming amount of information it's receiving because there are so many things coming at you at one time.

Now, Eldar Shafir has a lot to say about cognitive overload. That's because Shafir is a cognitive psychologist whose work focuses on how cognitive limitations, such as cognitive overload, can affect decision-making and behavior in various life domains. And Shafir, along with other behavioral economists studied how your mental resources can become scarce when you're faced with income challenges, time pressures, or other demanding situations.

According to Shafir, when you experience cognitive overload due to resource scarcity, it can lead to a phenomenon called "tunneling." Tunneling occurs when you focus your attention on the immediate problem at hand, forcing you to neglect other important aspects of your life. And, as a result, you may struggle to make sound decisions or engage in effective problem-solving when it comes to your money.

Indeed, in a study conducted by Shafir and his colleagues, participants were given a challenging financial decision to make, with some participants facing a high-pressure situation that simulated financial scarcity while others faced a low-pressure situation. Those in the high-pressure condition experienced cognitive overload, leading them to make suboptimal financial decisions compared to those in the low-pressure condition.

What this study illustrates is that when you're overbanked, and your financial management process becomes so complex that it takes up too much of your attention, it leaves little room for other essential professional and personal life obligations, especially when sudden life changes take place.

When this happens, you may feel mentally exhausted, find it difficult to focus on tasks, and struggle to make critical decisions. In turn, "tunneling" can affect your productivity, creativity, and overall well-being because your mental resources are committed to solving one complex problem. And more often than not, that's worrying about your finances. It can also cause additional stress and anxiety, leading to burnout and decreased life satisfaction.

Moreover, when your brain is preoccupied with one domain of your life, like staying on top of managing your various financial accounts, it may be less able to switch gears and focus on other tasks. This situation can lead to reduced creativity and problem-solving ability, as well as increased risk of errors or oversights in other parts of your life, like staying on top of your workload or managing essential relationships.

Now, maybe you're in a situation where you have various deposit, credit, and investment accounts spread across various financial institutions and are doing just fine managing all of them.

The Financial Costs of Being Overbanked

The trouble is that while you may have a well-oiled process right now to manage all of the complexity, all it takes is one overwhelming life event to put a kink in your complex financial process, ultimately leading to cognitive overload and potentially costly financial mistakes down the road.

And what are these costs?

Well, having multiple deposit accounts, like checking and savings accounts, can lead to increased fees and expenses if you become distracted by other pressing personal or professional matters in your life.

That's because when you're managing several accounts spread across different institutions, it's easy to overlook minimum balance requirements, which might result in monthly maintenance fees. And if you're using three, four or five deposit accounts to pay various expenses, chances are that you might encounter the occasional overdraft charge if you forget to make a transfer from one account to the other as expenses come through.

Now, at this point, you may be tempted to believe that, when times get tough, you can just put your expenses on your credit cards to avoid those potential bank charges. But, when it comes to your credit cards, managing multiple cards can make it more challenging to track your spending and pay off your balances on time, leading to interest charges and potential late payment fees when the inevitable road bump or pothole comes along in your journey to financial independence.

What's more, having too many accounts can not only affect your propensity to spend wisely, it can also negatively impact your credit score. For example, each time you apply for a new card, there is a hard inquiry on your credit report, which can lower your overall score and make it more expensive to borrow money in the future.

And finally, when it comes to your investment accounts, there is such a thing as having too much of a good thing. Indeed, when it comes to investment accounts, managing multiple accounts can lead to inefficiencies, including a suboptimal asset allocation and paying too much in performance fees.

That's because when you have too many investment accounts, tracking each account's performance and combined allocations can become time-consuming, making it harder to maintain a well-diversified portfolio. What's more, with so many accounts to manage, you'll likely be less inclined to evaluate the fees that you're paying for various investment products, leading to overall lower returns over the long-term.

So, when it comes down to it, being overbanked or having too many financial accounts can be mentally and emotionally taxing and lead to unnecessary fees and expenses that can delay or even derail your journey to financial independence. That's why it may not always be beneficial to have many accounts spread across various institutions when it comes to your financial accounts.

The Benefits of Financial Simplicity

So, what can you do if you find yourself in Brian's position where you're overbanked, and it's beginning to tax your time and cost you money?

The short answer is to simplify.

Why simplify? Well, other than the obvious reason that it can reduce the complexities in your life, simplifying your financial account management can have many near- and long-term benefits.

For example, in the book, "Your Money or Your Life," authors Vicki Robin and Joe Dominguez emphasize the importance of simplicity and intentionality when it comes to managing your finances. In fact, the authors drive home the point that being overbanked can often lead to confusion and unnecessary complexity in your financial life.

What's more, Robin and Dominguez emphasize the importance of understanding the true value of money in terms of life energy. By simplifying your finances, you are more likely to gain a clearer perspective on your spending habits and the amount of time and energy you invest in acquiring material possessions. This awareness can lead to more intentional and meaningful use of your financial resources, ultimately improving your overall quality of life.

Indeed, embracing simplicity can allow you to cultivate a more fulfilling and purpose-driven life. That's because by reducing physical and financial clutter, you can focus on the activities, relationships, and experiences that truly bring you joy and satisfaction.

Sure, managing a complex financial framework can, at times, make you feel empowered and like you're a good steward of your money. At the same time, however, simplifying your life can help you identify and prioritize your values and help you align your spending habits with your life goals, ultimately leading to a more content and purposeful existence.

Another take on the idea of simplicity comes from the world of home organization. Marie Kondo, known for her KonMari method of tidying and organizing, offers valuable insights on how you may want to consider decluttering the number of financial accounts you have, which can help simplify your financial life.

Now, Kondo believes that decluttering and simplifying your surroundings can profoundly impact your mental and emotional well-being. That's because by only keeping items that "spark joy" in your life, you cultivate an environment filled with positivity and happiness. When you do, you'll likely experience less stress and anxiety, and as a result, your mind will be clearer and more focused.

How does this work? Well, the KonMari method encourages you to be more mindful of your possessions and their value. By focusing on simplicity, you develop a deeper understanding of what truly matters to you. As you carefully consider each of your financial accounts and determine whether or not its management sparks joy, you become more conscious of your consumption habits and learn to appreciate how you spend your life energy.

How to Simplify by Aligning Account Management with Your Money's Purpose

So, now that we've discussed the emotional and financial costs of being overbanked, and how simplifying your life and finances can help you cut stress and achieve peace of mind, how do you actually go about the process of reducing the number of accounts you manage?

One approach to simplifying your financial management is to align your financial accounts with your money's purpose.

And what exactly does this mean?

Well, you'll likely recall that in recent articles, we discussed how essential it is to identify your values, crystallize your life purpose and align your money with these priorities. So then, from this perspective, if your values and life purpose guide how you use your money, then how you manage your financial accounts is an extension of making your life goals a reality.

Indeed, when you take the time to examine your financial accounts, you may discover that some of them no longer serve a clear purpose or align with your current financial goals. Remember, this clutter can lead to cognitive overload and stress, making maintaining a healthy relationship with money challenging.

Alright, so where do you begin once you're ready to simplify and declutter your financial house?

Well, you can start by reflecting on your near- and long-term financial goals and the values that drive them. Ask yourself: "What do I truly want to achieve over the next one, three, five, and ten years and how will my money help me get there?"

Then, review each of your financial accounts, including bank accounts, credit cards, and investment accounts. Consider whether each account serves a specific purpose that supports your defined financial goals. If you find an account that no longer aligns with your objectives or creates unnecessary complexity, consider closing or consolidating it.

Ultimately, the goal is to simplify your financial life and make it easier to manage your money. By reducing the number of bank accounts you have, you can streamline your finances and make it easier to keep track of your spending, savings, and investments. This, in turn, can help you achieve greater clarity and control over your financial future.

What's more, as you simplify your financial household, you may notice a positive shift in your mental state. The process of aligning your accounts with your money's purpose can bring clarity and focus to your financial decision-making, reducing anxiety and stress. That's because when you clearly understand the life goals you are working towards, and how your money supports your goals, it becomes easier to make intentional choices that promote financial well-being.

Moreover, this newfound sense of financial order can free up mental space and energy for other aspects of your life. To be sure, when you are no longer weighed down by financial clutter, you can devote more time and attention to nurturing your personal and professional relationships, pursuing your passions, and moving you one step closer to becoming the master of your financial independence journey.

Is Financial Procrastination Derailing Your Life Plans?

What do Willie Nelson, MC Hammer, and Allen Iverson have in common? Well, what their life situations have in common is that it doesn't matter how much you make, but how much you keep.

To be sure, these individuals came into vast fortunes, only to see their wealth dwindle in a short period of time. And certainly, it's hard to believe that these individuals didn't have trusted advisors who urged them to take actions that could help them preserve their fortunes.

But the truth is that there are likely many reasons why these individuals found themselves in their situations, and one reason likely has to do with financial procrastination.

Now, when you hear the word procrastination, you might immediately think of a pejorative, like a bad word or something with negative intent. But the truth is that procrastination simply reflects a subconscious (or sometimes conscious) decision to delay or postpone something you know you should be doing.

Indeed, you've likely experienced a moment where you've procrastinated on crucial financial work, like paying an important bill, balancing your checkbook, or taking care of some financial obligation, and these delays have likely cost you in lost time or money.

And the unfortunate truth is that in our society today, people who procrastinate are often viewed as lazy or unmotivated, which is why so few of us want to talk about this uncomfortable topic. But the fact is that there are many valid reasons why an individual may choose to put off doing an important task, especially when it comes to their money.

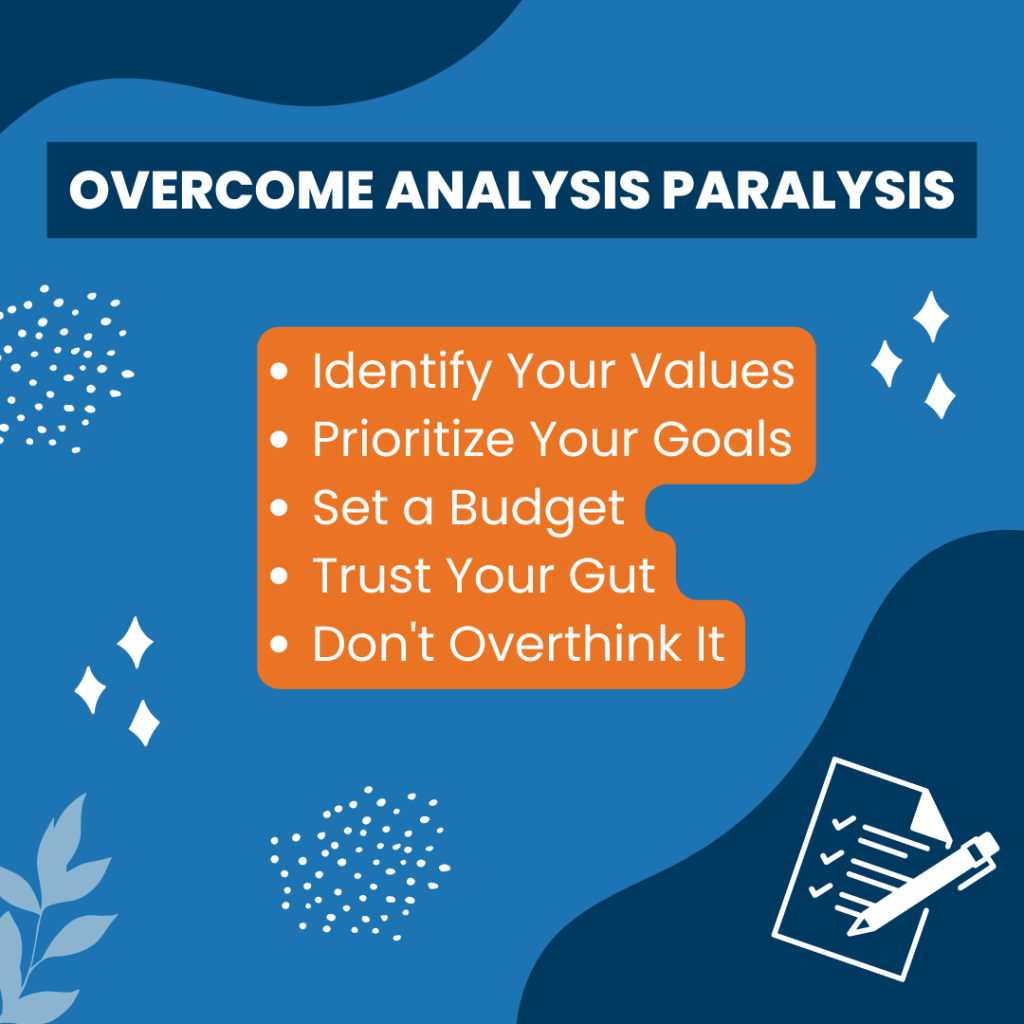

Do you or someone you know struggle with financial procrastination? Do you ever wonder why some people are really good at managing their finances while others get stuck in analysis paralysis and indecision or procrastination?

Well, even if you only occasionally struggle with putting off paying your bills, gaining some insight into this underlying behavior, understanding how to rebound after a setback, and doing the work to maintain your positive momentum can help you stay the course on your path to mastering your financial independence journey.

Some Common Causes of Financial Procrastination

So then, what causes procrastination when it comes to money?

Well, while there are many reasons why someone may be a financial procrastinator, generally speaking, this act could be related to 1) your thought processes, 2) a struggle for instant gratification, or 3) your body's signal that something is just not right.

So as we dive deeper, let’s start by taking a look at your mindset’s role in financial procrastination.

Procrastination and Self Efficacy

Now, when it comes to your mindset, Henry Ford was known to have said that, "whether you can, or you can't, you're right." That's because when it comes to finding the motivation to do what we know we're supposed to do, self-efficacy, or the internal belief we have about our ability to accomplish a task or goal, plays a significant role in our ability to get started on essential tasks.

Indeed, when we have high self-efficacy, we are more likely to take on challenging tasks and persist in the face of obstacles. Conversely, when we're dealing with low self-efficacy, we may be more likely to avoid or delay tasks, particularly those that we perceive as challenging or complex.

That's why in her book, "Mindset: The New Psychology of Success," Carol Dweck discusses how self-efficacy and mindset can influence procrastination.

Dweck explains that individuals with a growth mindset tend to have higher levels of self-efficacy. Indeed, these individuals are more likely to view setbacks and failures as opportunities to learn and grow rather than as a reflection of their own innate abilities. As a result, they are less likely to procrastinate, as they have confidence in their ability to succeed.

On the other hand, individuals with a fixed mindset tend to have lower levels of self-efficacy and are more likely to procrastinate. These individuals may avoid tasks or challenges they perceive as difficult or beyond their abilities because they fear failure and negative feedback.

Therefore, if you find yourself procrastinating, ask yourself if your mindset is holding you back from taking the next steps toward what you know you should be doing next.

The Struggle for Instant Gratification

Another factor to consider when you're trying to identify the underlying factor causing your procrastination is time inconsistency.

So, what is time inconsistency?

Well, have you ever made plans to get up early in the morning, only to find yourself struggling to get out of bed when your alarm goes off? Or how about the last time you made plans to get to the gym on the regular, only to find yourself with other obligations coming up when it's time to go?

If you've found yourself in this situation, then you're likely already familiar with the concept of time inconsistency and how it can influence procrastination.

Now, time inconsistency is a psychological concept that describes people's tendency to make present decisions that conflict with their long-term goals. This means that people often make more favorable choices in the short-term, but that can be detrimental to their long-term interests.

For example, imagine an individual who has a long-term goal of improving their credit score but struggles with time inconsistency when it comes to paying bills on time. They may have the intention to pay their bills when they're due and understand the importance of doing so for their long-term financial goals, but when the time comes to complete their task, they may simply put off the payment in exchange for a short-term reward such as spending money on leisure activities or delaying the discomfort of paying their bills.

Indeed, when it comes to procrastination, time inconsistency can cause people to delay tasks or critical decisions vital to achieving their long-term goals, even if they know that delaying the task will have negative consequences. This likely happens because the immediate rewards of avoiding the task (such as short-term pleasure or relief from anxiety) can be more compelling than the potential long-term benefits of completing the task.

Either way, time inconsistency is just a fancy way of saying that we prefer the immediate benefit of instant gratification over long-term rewards. And when it comes down to it, procrastination can be a coping mechanism for time inconsistency, as an individual delays essential tasks to avoid the immediate discomfort of starting important work. Even so, while it may seem harmless at first, when left unchecked, this behavior can negatively affect their long-term goals and financial well-being.

The Body Relation

One last potential cause for procrastination that we'll explore is looking at what's going on in the body. That's because, in some situations, procrastination, or the act of putting off what we know we should be doing, is often the body's way of telling us that something bigger is going on behind the scenes.

Indeed, psychologist Dr. Stephen Porges, in his Polyvagal Theory, suggests that procrastination is a form of self-protection when viewed in the context of the body's nervous system. Now, what this theory suggests is that inside our bodies, we have a special nerve called the vagus nerve that helps us respond to stress and danger. It has three parts, and each part helps our body react in different ways.

The first part, the ventral vagal, or "rest" state, helps us feel safe and calm. When we feel safe, our bodies can “rest and digest” and give us the confidence to take on challenges and meet new people.

The second part, the sympathetic nervous system, or "fight/flight" state, helps us prepare to fight or run away when we feel threatened. This part of the nerve helps us become more alert and ready to act quickly to protect ourselves. When our minds are in this state, we are more likely to take care of our finances from a place of panic, fear, and anxiety as we realize that a bill is past due.

The third part of the nerve, the "freeze" state, is like a last resort. That’s because when we feel like we can't fight or run away from danger, our bodies can shut down and become very still and quiet. In this state, we're more likely to feel shame, a sense of helplessness, hopelessness, or utterly trapped. In this state, we have an inability to focus and actually get work done.

Indeed, when the nervous system is dysregulated or underactive, we may experience difficulties in social interactions and have a reduced ability to cope with stressors, leading our bodies to physically shut down and produce what looks like procrastination.

Therefore, if you typically have a growth mindset and rank low in terms of impulsive behaviors but still occasionally struggle with financial procrastination, then take a moment to listen to your body and evaluate what's going on in your life.

If there are other things going on, like problems at work, challenges in your personal relationships, health issues, or other situations that are increasing your levels of anxiety, then these factors likely will inhibit your ability to take care of money issues until these matters are addressed.

Steps to Move Past Procrastination

So, now that you understand what might be driving your inclination towards procrastination, the next step to actually moving out of this state and towards your desired financial outcomes involves identifying ways to adapt whether your mindset, instant gratification, or your nervous system are causing you to procrastinate.

Shifting Your Mindset

And what can you do when you find yourself procrastinating on managing your finances and paying your bills because you are dealing with self-doubt? Well, recall that self-efficacy is the belief in one's ability to achieve a specific goal or outcome. When someone experiences self-doubt, they question their ability to succeed or feel uncertain about their competence in a particular area, but there are some things you can do to improve your self-belief and get your finances back on track.

First, you can start by educating yourself about the particular financial matter where you might be struggling. This could involve reading books, articles or taking online courses on topics such as budgeting, investing, and debt management. By learning more about the financial topics that give you anxiety, you can better understand how to manage your money effectively and improve your self-confidence in areas where you might be struggling.

Next, consider whether you're approaching your situation from a growth or fixed mindset. Remember, individuals with a fixed mindset believe that there’s little they can do to change their present circumstances, and are more inclined towards procrastination. And, what can you do if you find yourself in this situation? Well, to develop a growth mindset, you can take several steps based on Carol Dweck's book.

Well, to start, embrace challenges and view them as opportunities for growth and learning. Rather than shying away from complex tasks or new experiences, welcome them as chances to develop your skills and abilities. At the same time, recognize that setbacks and failures are a natural part of the learning process and can provide valuable feedback for future efforts.

Then, cultivate a love of learning and approach challenges with a sense of curiosity and a desire to gain new knowledge and skills. Indeed, take the time to focus on the effort and hard work you put into achieving your goals rather than attributing success or failure to innate abilities or talent.

As you go about this work, you'll also want to be kind and supportive to yourself, even when you encounter setbacks or failures. Dweck points out that developing a growth mindset can be a challenging process, and it's essential to be kind and compassionate to oneself during this journey. That's why she suggests you practice self-compassion by treating yourself with the same kindness and support you would offer a close friend or, if you're a parent, your own child.

Indeed, Dweck goes on to point out that self-criticism and negative self-talk can be detrimental to one's self-esteem and motivation, and can ultimately hinder growth and progress and undermine a growth mindset. That's why replacing negative thoughts with more positive and realistic ones that emphasize your strengths and potential is essential to building a growth mindset. At the same time, be open to constructive criticism, and actively seek out feedback from a trusted advisor and use it as an opportunity to learn and grow so you can improve your ability to prudently manage your finances.

Finally, surround yourself with individuals who encourage and support your growth mindset. This approach could include seeking out mentors and role models who exemplify a growth mindset and can provide guidance and support as you work to develop this mindset for yourself.

Dealing with Instant Gratification

Now, let’s take a moment to talk about dealing with instant gratification.

Earlier, we discussed the trouble with time inconsistency and how it can lead individuals to favor a present bias over difficult long-term decisions.

So then, what can you do if you find that you identify with instant gratification as a leading cause of your procrastination? Well, take a page from James Clear.

In his book "Atomic Habits," Clear provides proven methods for developing healthy habits and overcoming a present bias. And in his book, Clear focuses on creating a system for building habits that are sustainable and effective.

One key takeaway from Atomic Habits is that it's not about making big changes all at once but about making small, consistent improvements over time. This approach means focusing on small changes to your daily routines that will help you gradually move toward your goals.

For example, if you have a hard time getting started with paying your bills or even reviewing your finances on the regular, then set aside a thirty-minute block of time and do as much as you can within that window. Then, take a break and return to your task if you still have work that needs to be done. This approach can help you tackle a big task that might otherwise seem overwhelming in small, bite-sized pieces.

Another point emphasized by Clear is the importance of focusing on the habit-building process rather than just making the outcome the end-all-be-all. Clear emphasizes that building a habit is not just about achieving a goal but creating a system of actions that will help you consistently achieve your goals over time. That's why if you procrastinate when it comes to paying your bills, you may want to reframe this task as a ritual that is performed rather than a task that's marked off a to-do list.

Clear also emphasizes the importance of creating a supportive environment for building habits. This means surrounding yourself with people who will support your goals and help create an environment that makes it easier to stick to your habits.

For example, if you're trying to be more prudent with your finances, then spending time with individuals who like to talk about how much money they make or spend could tempt you to make poor choices and set you back from your financial goals. While you may not need to find new friends (or maybe you do), at the very least, be mindful of how others can affect your own decision-making process.

Lastly, Clear emphasizes that habits are not just about what you do but about who you become. By building habits that align with your values and goals, you can transform yourself into the person you want to be. To be sure, overcoming a present bias, or desire for instant gratification, means consistently evaluating the long-term benefits of achieving your financial goals and why it’s essential to keep your house in order at all times.

So then, from this perspective, ask yourself, “who do I want to become?” How will your life change if you commit to making this new habit of being disciplined with your money and doing what needs to be done at the right time? More importantly, how will people's perceptions of you change, and how would that make you feel?

Support Your Nervous System

Finally, if your financial procrastination is tied to life stressors that are putting your body into a freeze state, then you can take a few suggestions from Stephen Porges to get you moving forward.

Now, you'll recall that according to the Polyvagal Theory, our nervous system exists in three states, 1) rest and digest, 2) fight or flight, and 3) freeze. When we experience trauma or stress, our body's natural response is to activate the sympathetic nervous system, which can result in feelings of fear or anxiety to act or eventually activate the parasympathetic system, leading to a freeze or shutdown when the situation becomes untenable.

This state of dorsal shutdown can feel overwhelming and paralyzing, but there are ways to help our body transition to a more regulated parasympathetic, or "rest and digest" state.

So then, to move out of a frozen state, what you'll need to do is activate your fight/flight system, which is responsible for mobilizing your body to respond to stress and danger. Now, at this point you might be asking, why are we going to a stress response if we're trying to get to the "rest and digest" state?

Well, recall that the nervous system has a primal function to keep us safe. It's like those moments in a National Geographic episode when a gazelle trapped in the mouth of a lion. With nowhere to go, the gazelle goes into freeze mode as a way to cope with the trauma that it’s about to face. But the moment that the lion gets distracted and lets go, the gazelle can snap back into fight mode in its bid to break free and get to safety.

In other words, the gazelle goes into freeze mode to stay safe, but then it first snaps into fight/flight to get away from the lion before it can eventually return to life as normal in the rest and digest phase.

And, so, how do we move between these states?

Well, one way to activate this system is through physical activity or exercise, which can increase your heart rate and respiration, release adrenaline and other stress hormones, and promote feelings of alertness and energy. For example, going for a brisk walk, heading to the gym, or dancing to music can help stimulate the sympathetic nervous system and promote a sense of activation and help move you out of shutdown mode.

Another way to move out of a dorsal vagal state is through social engagement and connection. Polyvagal theory suggests that social engagement, such as eye contact, facial expressions, vocal tone, and touch, can help regulate the autonomic nervous system and promote feelings of safety and connection.

For example, calling a friend, joining a group activity, or participating in a social event can help stimulate the ventral vagal system, which is responsible for social engagement and connection, and promote a sense of safety and belonging. And if you're in a place where you'd rather not engage with others, getting out into the public to people-watch can be a safe way to reset your nervous system as well.

Finally, breathing exercises and meditation can also help move out of a dorsal vagal state by promoting relaxation and reducing stress. Slow, deep breathing can stimulate the vagus nerve and promote feelings of relaxation and calm.

Keep the Momentum Going

Alright, so now that we've identified potential factors that could be causing your financial procrastination and have offered some suggestions for overcoming them, let's talk about a few things you can do to build momentum to avoid going off the tracks again.

Create a Conducive Environment

So, what can you do to keep the positive momentum of prudently managing your finances going for the long-term?

Well, to start, consider your environment and how it might affect how you deal with your finances. Marie Kondo, an expert in the art of tidying up and creating a joyful home, believes that your physical environment has a powerful impact on your habits and behaviors. So then, from a financial perspective, here are a few tips from Marie on ideally designing your physical environment to establish new financial habits, such as consistently paying your bills and prudently managing your finances.

First, create a dedicated financial management space in your home. You can do this by designating a specific area in your home for managing your money like a desk or a corner of your living room. And this space should be clean and organized, with all the tools and documents you need to manage your money easily accessible.

Next, use visual cues to remind yourself to pay bills, review financial statements, rebalance investments or take care of other essential financial tasks. You can do this by placing a brightly colored sticky note or a decorative object in your financial management space to remind you of when it’s time to take care of the essentials, and make these habits more automatic.

Also be sure to make it a pleasant experience by playing music, lighting a candle, or sipping a cup of your favorite drink while you take care of your finances. This way, paying bills doesn't have to be a chore, and you may even come to look forward to the experience.

Create New Habits, But Start Small

Now, earlier, we discussed James Clear's take on how habits can help overcome procrastination. Another take on habits comes from Charles Duhigg, who emphasizes the importance of starting small in his book "The Power of Habit." And Duhigg suggests that the key to forming new habits is to focus on small wins that give you a sense of progress and accomplishment.

For example, if you're trying to build a habit of going to the gym regularly, start by committing to just 10 minutes of exercise each day. In a similar way, if you have trouble with paying your bills or staying on top of your financial accounts, try paying one bill or reviewing one financial account per day.

The idea here is that once you've established the habit, you can gradually increase the amount of time you spend on it. This way, you're starting small, but you're building towards a larger goal.

Another key principle of habit formation is the habit loop, which consists of three parts: the cue, the routine, and the reward. The cue is the trigger that sets off the habit, the routine is the behavior or action that follows, and the reward is the positive outcome that reinforces the habit.

To establish a new habit of paying your bills on time, for example, you may want to consider creating a new habit loop. To accomplish this outcome, start by identifying a cue that will trigger you to pay your bills. This could be something as simple as setting a reminder on your phone or marking your calendar with the due date of your bills.

Then, once you have a cue in place, establish a routine for paying your bills. This could involve setting aside a specific time each week to pay your bills or automating your bill payments to automatically deduct them from your account.

Finally, make sure you reward yourself for paying your bills on time. This reward system could be something as simple as treating yourself to a favorite snack or taking a few minutes to relax and enjoy a cup of your favorite drink after you've paid your bills.

By creating a new habit loop for paying your bills, you can establish a new habit that will help you stay on top of your finances and avoid late fees and other financial penalties. With practice and persistence, you can make this new habit a permanent part of your life and enjoy the benefits of better financial management.

Treat Yourself

Finally, make sure you don't miss out on the earlier point about rewarding yourself for the progress you're making. Indeed, in "18 Minutes: Find Your Focus, Master Distraction, and Get the Right Things Done," Peter Bregman emphasizes the importance of incorporating rewards into the habit-creation process as a way to reinforce positive behavior.

According to Bregman, when we engage in a behavior that we find rewarding, we are more likely to repeat that behavior in the future. Therefore, he suggests that we identify specific rewards that we can give ourselves for completing a desired behavior or task.

For example, if your goal is to review your bank account transactions once a week, you might reward yourself with a pizza delivery or takeout from your favorite restaurant. Alternatively, if your goal is to balance your checkbook by a specific deadline, you might reward yourself with a night on the town or a big-ticket purchase once you've finished your work.

Bregman also emphasizes the importance of making the rewards tangible and immediate. Indeed, rather than waiting for a long-term goal to be achieved, he suggests that we reward ourselves for making progress along the way. Again, it's the small wins on a daily and weekly basis that move us closer to our long-term financial goals.

By incorporating rewards into the habit-creation process, Bregman believes that we can create positive habits that are sustainable and enjoyable rather than feeling like a chore. Additionally, he suggests that we track our progress and celebrate our successes, which can also serve as a form of reward and motivation to continue positive behaviors.

Is Financial Procrastination Putting Your Life Plans Off Track?

Make no mistake, financial procrastination can significantly impact your money and relationships if left unchecked. It can lead to missed payments, late fees, and even ruin relationships. And while there are many reasons why people procrastinate, understanding the underlying causes can help you take steps to overcome this behavior.

These approaches include addressing mindset, working to avoid instant gratification, and by listening to your body, you can start to break free from the cycle of financial procrastination and take control of your finances. Remember, it's never too late to start taking action and making positive changes in your financial life.

Indeed, by shifting towards a growth mindset, developing sustainable habits, and supporting your nervous system, you can overcome the barriers that are preventing you from taking action and moving towards your desired financial outcomes.

Remember, sometimes all it takes is small, consistent steps and being kind and compassionate towards yourself during this process to make sustainable gains. And, with a little patience and persistence, you can take one step closer to becoming the master of your financial independence journey.

Is Credit Your Superpower or Kryptonite?

Is credit a good thing or bad thing?

Well, it all depends on your perspective.

When used correctly, credit can supercharge your life and help you level up financially in a shorter time than you would have if you relied on savings alone. That's why Dale Carnegie, in his book, "The Gospel of Wealth," wrote that debt could be a powerful force for good if used productively.

Now, the trouble with debt is that, just like any other financial tool out there, it has been misused by lenders and borrowers alike, leading its use to be largely villainized by society. Make no mistake, in the wrong applications, debt can be a form of bondage. That's why in some cultures, its use is forbidden and why some individuals have mortgage payoff parties instead of retirement savings celebrations.

Make no mistake, however, when used prudently, credit can boost your earnings ability, enable you to acquire appreciable or income-producing assets, and help keep you from going broke when life throws you a curveball bigger than your savings account.

Even so, a Scottish historian and author, Niall Ferguson, wrote, "credit is like a looking glass. Once cracked, it can never be the same again, and the more we use it, the more fragile it becomes…"

Indeed, these perspectives from Carnegie and Ferguson show how on the one hand, the wise use of credit can dramatically enhance your current financial situation. On the other hand, debt can leave your finances in a precarious position when not managed properly.

Certainly, much has been written about the trouble with credit and how too much debt can be a trap. Before we discuss the drawbacks of credit, let's take a look at why you would want to use debt to lever up your current financial situation.

Why Credit Can Be a Force for Good

Credit as a Force Multiplier

When used the right way, credit can be a force multiplier. It can help you accomplish things in your life that you otherwise may not have been able to do on your own financially.

Now, the term force multiplier is often used in the military to describe a factor, such as better positioning or equipment, that can increase a unit's combat potential, allowing it to fight on a par with a more significant fighting force.

For instance, in World War II the development and use of radar technology arguably changed the course of the war in favor of the Allies. As you'll recall, radar is a detection system that uses radio waves to determine the location, speed, and direction of objects.

Now, radar served as a force multiplier for the Allies by providing them with a significant advantage in air and naval combat. With radar, the Allies could detect incoming enemy aircraft and ships at a much greater distance than the enemy could detect them. This tool allowed the Allies to prepare their defenses and launch counterattacks more efficiently and accurately.

For example, radar played a critical role in the Battle of Britain, in which the Royal Air Force (RAF) used radar to detect incoming German aircraft and direct their own fighters to intercept them. Using radar allowed the RAF to defend against the German bombing campaign more effectively and played a crucial role in their eventual victory.

So, from this perspective, credit can act as a force multiplier by taking the financial resources you have today and amplifying them to achieve a broader victory in your life.

How so?

Well, the first way it can benefit you is by enhancing your future earnings ability by allowing you to borrow money in the present so that you can improve your skills and get credentials that can help you break into a new field or raise you to a higher earnings level in your current role. And while the topic of college education, and more specifically college debt, is hotly debated today, the statistics still argue in favor of a college degree.

Now, according to data from the Bureau of Labor Statistics' most recent Occupational Outlook Handbook, the data show that those jobs with the fastest industry growth rates and median pay of at least $100,000 all require a college degree. Indeed, according to the same government data, there is a growing earnings gap between individuals holding a college degree and those without.

For example, government data show that the average 25-year-old full-time worker with a bachelor's degree made a median annual wage of around $55,000, compared with $30,000 for full-time workers of the same age group with just a high school diploma. And when we look at the earnings gap over a lifetime, it continues to increase. Here again a study from the Department of Education shows that an individual with a high school diploma is likely to earn a median income of around $1.9 million over their lifetime.

However, an individual with a bachelor's degree could earn $3.4 million over their lifetime, while a top-earning professional degree could bring in nearly $6.5 million. So, then, even if we assume that it costs an individual $160,000 to obtain and pay off their debt over ten years, the costs associated with the college debt would still net an extra $1.3 million or a multiplier of eight times of what a non-college graduate could earn over their lifetime.

So, then, from this perspective, we can say that credit can act as a force multiplier to enhance an individual's inherent knowledge and increase their earnings power.

A Lever for Wealth Building

Another way that credit can dramatically change your financial situation is by giving you leverage to use a little bit of money to create a lot of wealth. Now, for many individuals, purchasing a home is one way to create wealth. Certainly, arguments have been and continue to be made for and against the wealth-building attributes of home ownership. Even so, the long-term benefits become evident once you look past the short-term costs of home ownership versus renting.

Now, one way homeownership builds wealth is through the appreciation of the value of your home over time. Historically, home values have tended to appreciate over the long term, sometimes resulting in significant wealth gains to homeowners. And while you may be only putting down five- ten-, or twenty-percent towards the purchase of a home, you gain access to the full value of the appreciated equity in your home over time when you borrow against or sell it.

What's more, homeownership can help you build wealth through the process of forced savings. That's because the longer you make mortgage payments, the more principal you pay down, which is essentially putting money into a savings account each month, assuming home values remain stable. And this approach can help you build wealth over time, even if the cost of homeownership is slightly higher in the short term than that of renting.

Another way that credit can help turn a little bit of money into a lot of money is by starting a business. Now, the internet is filled with stories of individuals who borrowed money to achieve wildly successful outcomes. And one rags-to-riches entrepreneur who used debt to start their business is John Paul DeJoria, the co-founder of John Paul Mitchell Systems, the haircare company.