Why Your Investments Might Thrive in 2021

This past year has been a period in history that many of us would like to simply forget. Concerns about our communities' wellbeing led to a seismic shift in the way that we work, educate our children, socialize, and go about our daily routines. Without a doubt, 2020 has been a year that has tried our livelihoods, finances, health, relationships, and most importantly, our patience. Indeed, the one word that might best characterize an experience that happened to us is: survival.

Nevertheless, chances are good that the negative factors that have forced us to hunker down are likely to ease into the year ahead, enabling many of us to thrive once again. More specifically, widescale distribution of a coronavirus vaccine and a return to a seemingly normal political environment likely will foster greater business and household confidence in the months ahead. Such outcomes could support labor market improvements and a rise in business earnings. At the same time, accommodative central bank policy may provide much-needed support to the economy and boost financial market sentiment.

Even so, while government spending and money printing were a boon to financial markets in 2020, investing likely won't be as simple as following the latest trading fad. Liquidity-induced momentum trades that provided handsome gains this year could be harder to come by in 2021. That's why as we look into the year ahead, the key to thriving financially for investors with a long-term savings orientation could be as simple as sticking to the basics and focusing on fundamentals.

Climbing Out of a Hole

The healthcare crisis response dealt a blow to the US economy, but there are ample reasons to be optimistic. Nationwide lockdowns during the first half of 2020 led to one of the sharpest economic contractions in history. A record 24.9 million people had claimed jobless benefits this year as businesses closed to help stem the spread of the coronavirus outbreak. During this time, some economists expected a V-shaped economic recovery fueled by historic government spending and central bank money printing.

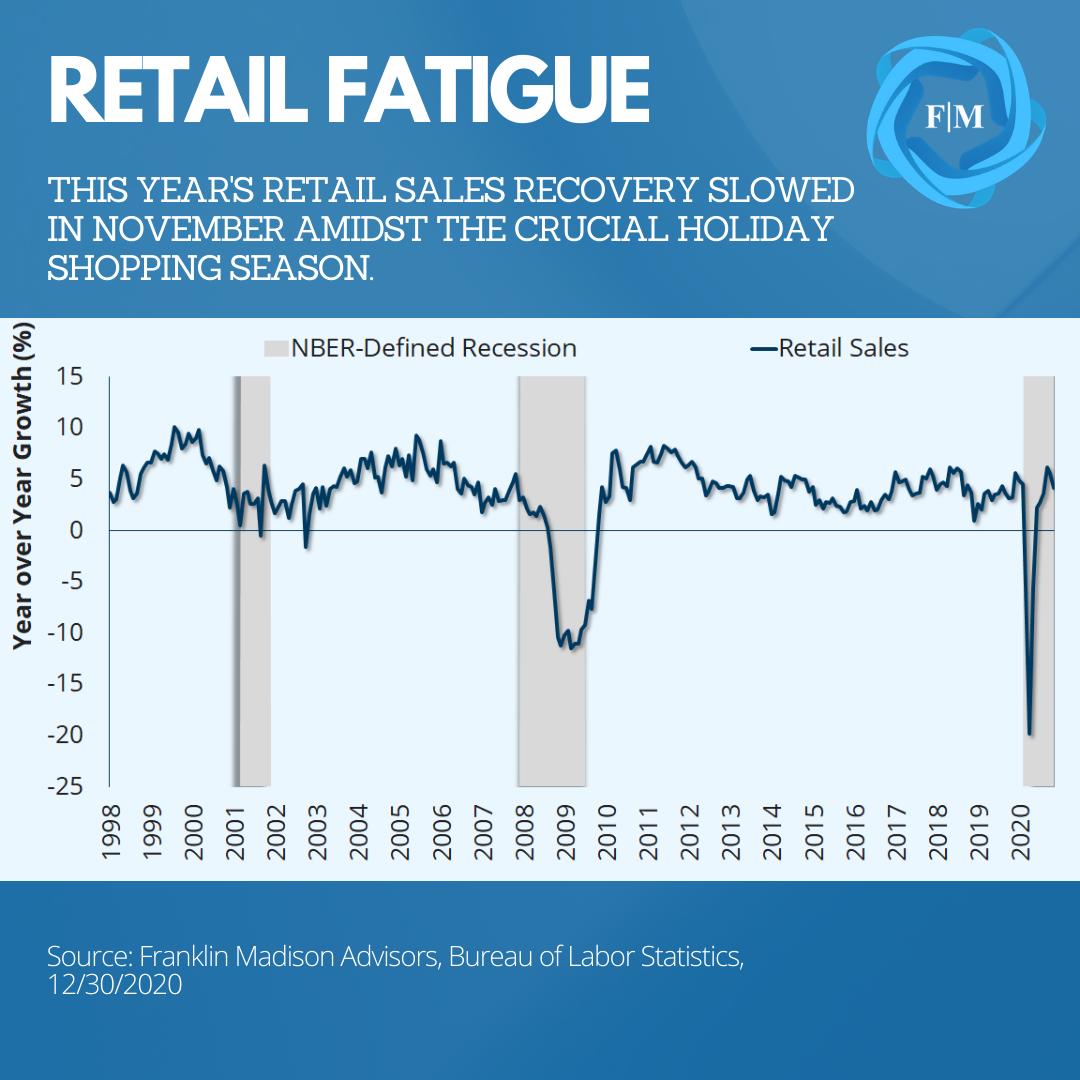

Indeed, while growth improved in 2020, the gains that some people had hoped for failed to materialize. And as 2020 ends, the healthcare crisis has again intensified, leading to a new round of stay-at-home orders, business closures, and a rise in unemployment. While the housing market certainly benefited as more individuals worked from home, much anticipated pent-up demand in consumer spending fizzled out into the holiday season. And while it appears that the economy is now losing steam, a couple of factors may pave the way for greater economic resilience in the coming year.

So why should we be optimistic? Well, to start, we now have several vaccines that put us miles away from where we were just a few months ago. These injections may eventually help mitigate the spread of COVID infections and enable society to return to some semblance of normalcy sooner rather than later. Certainly, news of a vaccine was greeted with optimism by the markets in November.

And as vaccination efforts kick off this month, there is a reason for optimism as social distancing orders are likely to ease at some not-too-distant point. Indeed, a recent CFO Survey from the Richmond Fed showed that business executives are more optimistic about the future than last quarter as they looked past pandemic risks.

Besides vaccines, another likely reason for rising confidence heading into 2021 is greater political certainty. With another chaotic election season behind us, Capitol Hill leaders are likely to focus on introducing policies that further support economic growth. While a $900 billion stimulus package was approved in December, slowing retail sales and rising jobless claims likely opens the door for another round of government spending during the first half of next year.

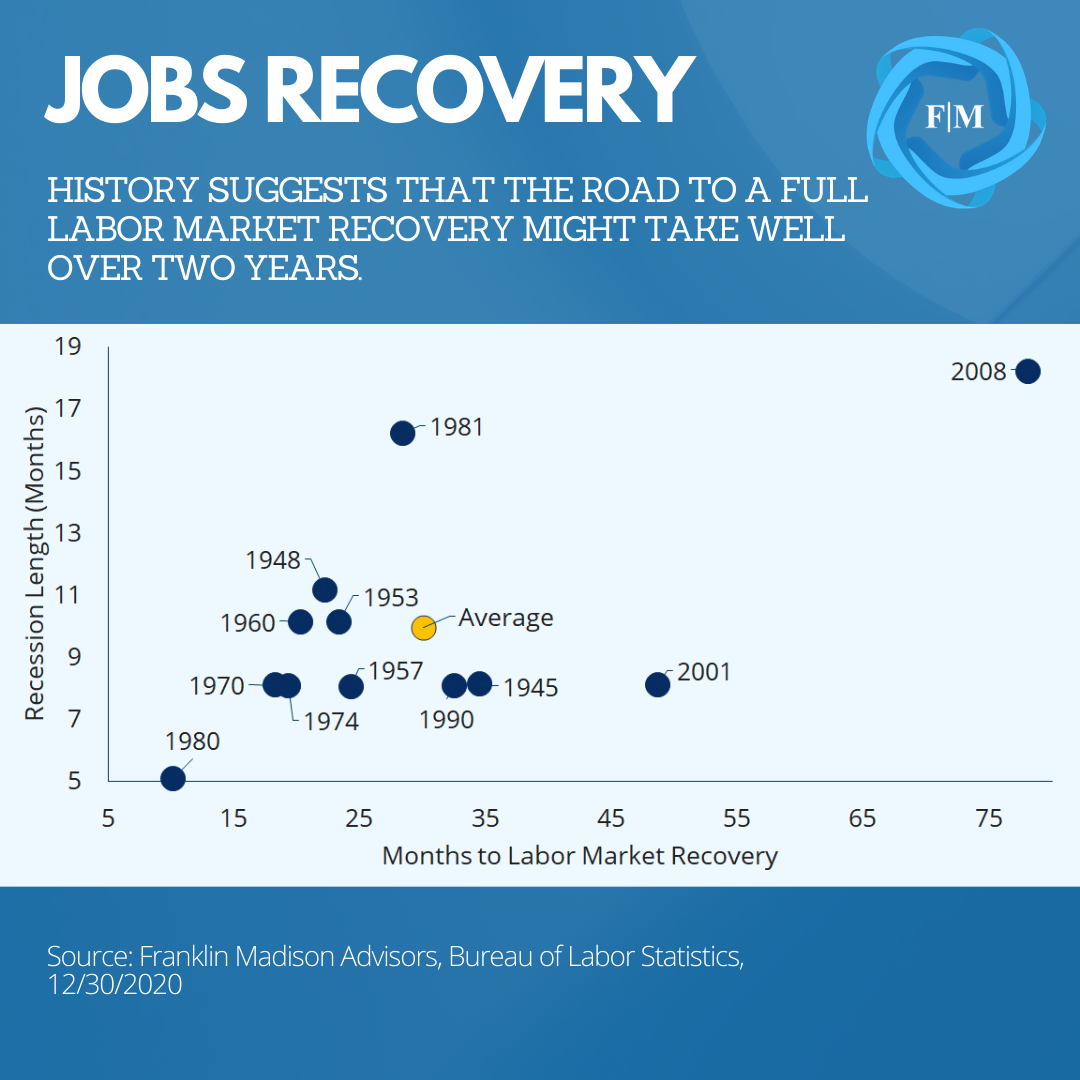

Make no mistake; the road to recovery will take some time. History has shown that, on average, recessions tend to last about three quarters. From there, it takes on average two and a half years for the labor market to return to its previous high-water mark. These data points suggest that the US economy has a deep hole to climb out of, so vaccination efforts and decisions made by Congress will be essential to the recovery pace in the months ahead.

The Markets Are Not the Economy

Let's consider this economic outlook in the context of the markets. Now, there seemed to be a disconnect between financial markets and the economy in 2020. While household spending slowed and employment conditions declined, major stock market indices closed the year positively. To be sure, a repeated mantra reflecting this sentiment has been that the markets are not the economy. So why did markets perform so well amid a global pandemic? Well, without a doubt, global central bank policies played a crucial role in buoying risk asset prices.

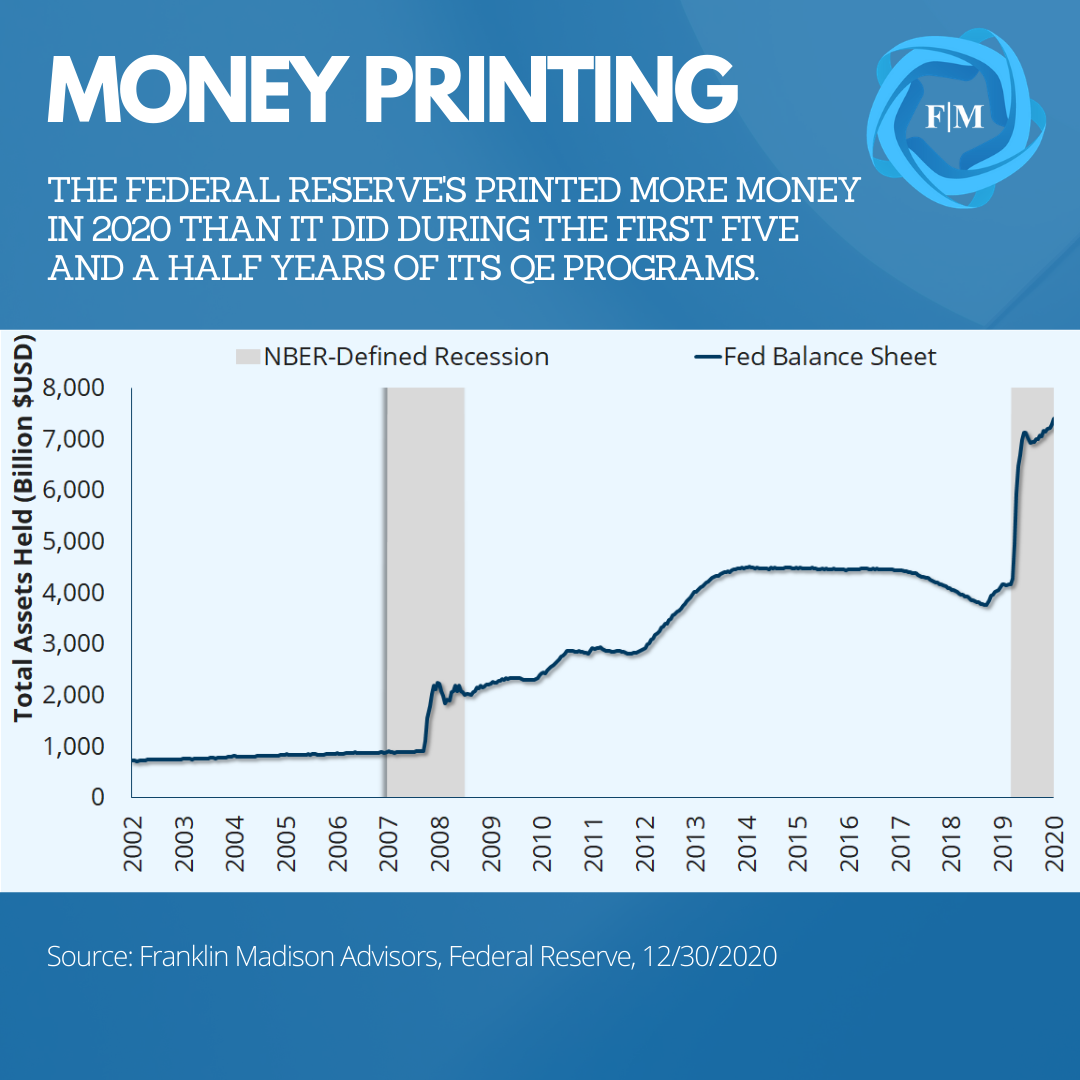

During the height of the pandemic outbreak, the Federal Reserve (Fed) introduced a historic asset purchased program that dwarfed its previous money printing efforts. For example, in 2020, the Fed added $3.3 trillion worth of assets to its balance sheet. To put this figure into perspective, from the height of the Global Financial Crisis in 2008 and three rounds of Quantitative Easing thereafter, it took the Fed over five and a half years to purchase the same amount of assets. What's more, the Fed, European Central Bank, and Bank of Japan bought a combined total of $8 trillion of assets this year, a feat that took eight years during the Global Financial Crisis. Arguably, this massive injection of cash into the financial markets contributed to stellar market performance in 2020.

Newly Minted Investors

Another contributor to the strong market performance was greater participation from individual investors. An analysis prepared by JP Morgan Securities suggests that individuals opened more than 10 million new brokerage accounts in 2020. Add in the rise of a cottage industry of social media investing gurus, the fact that some apps have arguably gamified investing and brokerages flush with cash offering attractive margin loans, and you have a recipe for exuberance in certain corners of the markets. This sentiment was particularly evident in the tech sector, which saw outsized performance as work-from-home and healthcare stocks benefited from Fed-induced liquidity and newly minted day traders.

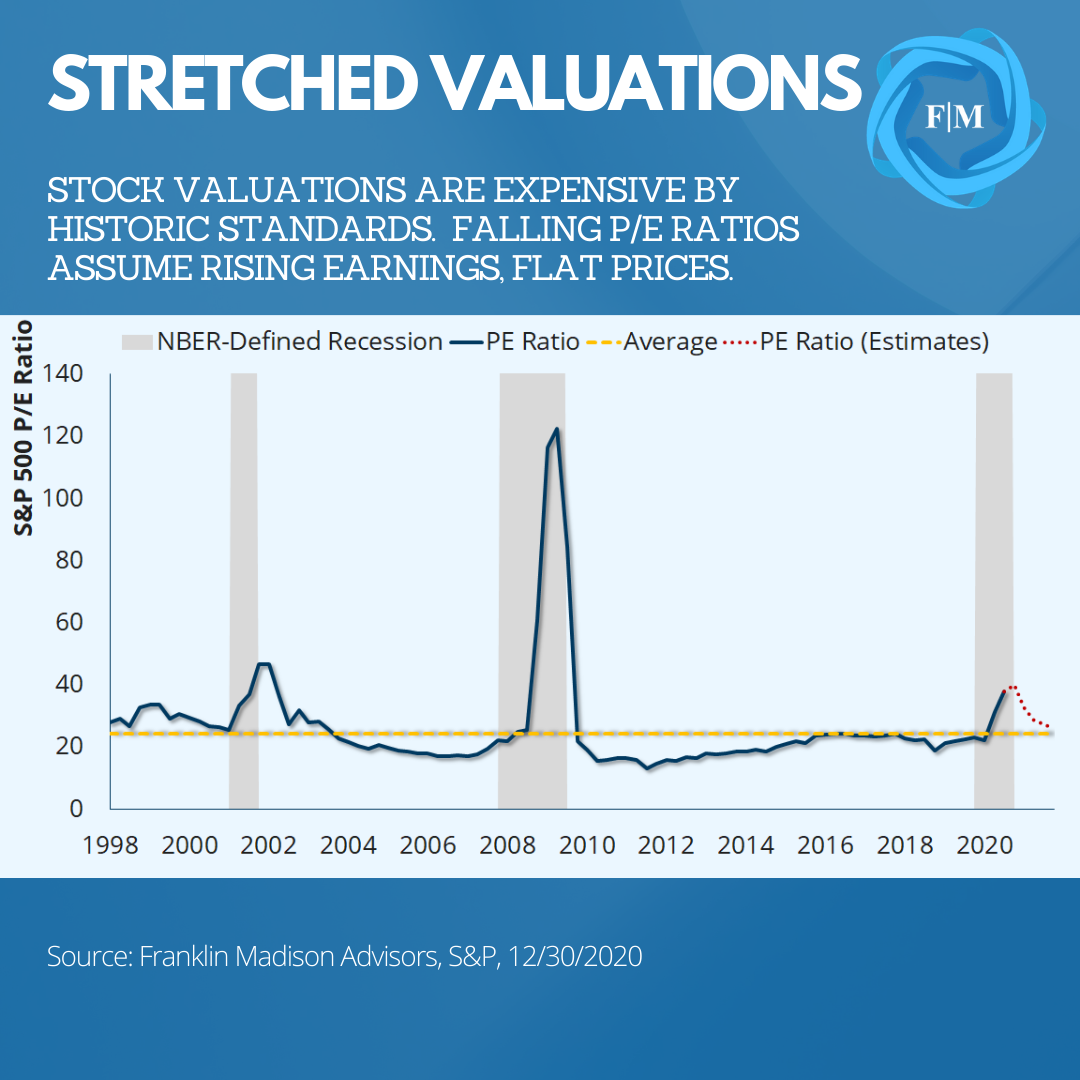

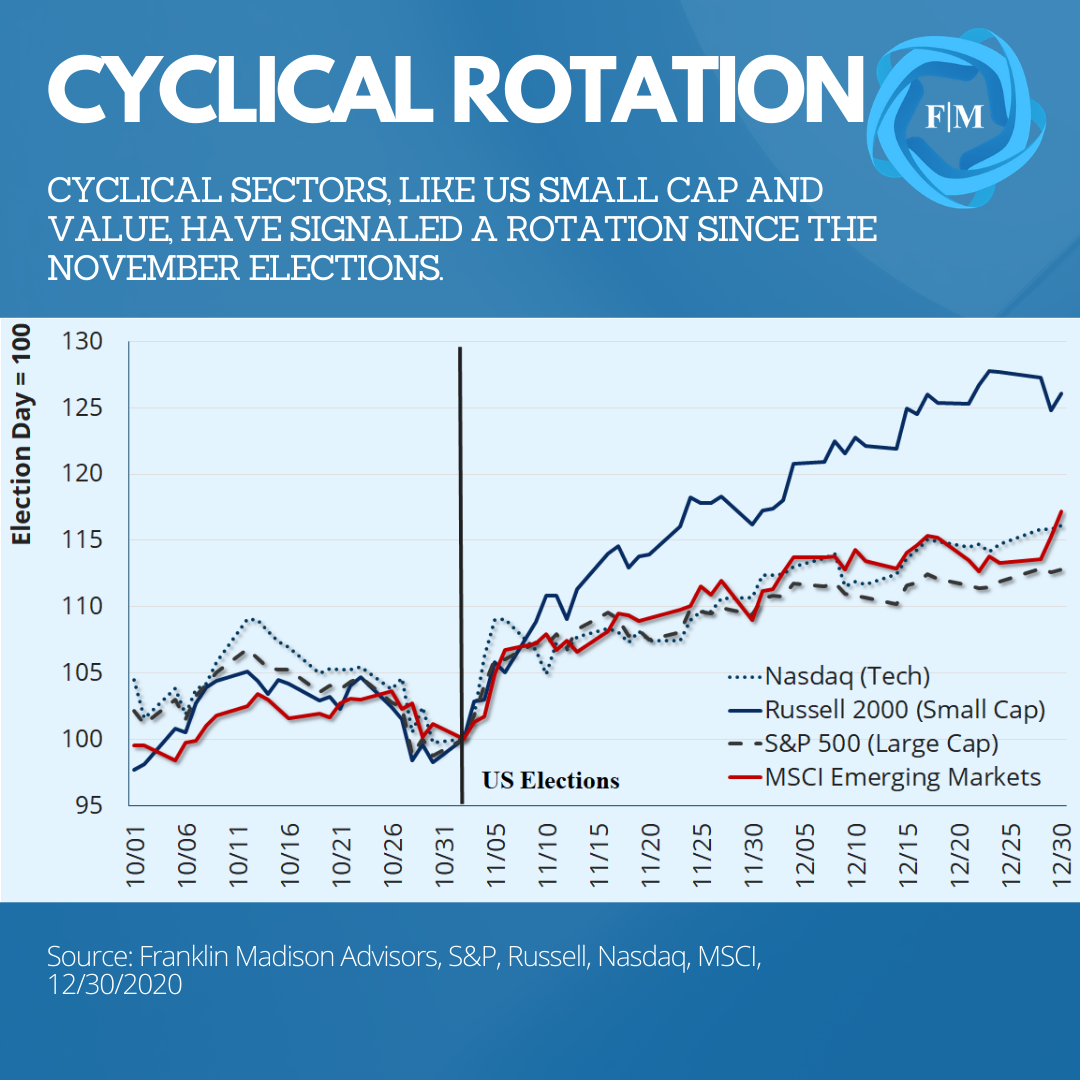

Today, however, there's some indication that this popular market approach may be losing steam. The momentum trade that had supported strong asset performance has subsequently led to stretched valuations. Such excesses have been exhibited more acutely in tech, which is up well over 40% compared to 16% for large caps. This preference for stocks poised to benefit from social distancing and work from home themes has come under pressure as a return to normal appears on the horizon.

Certainly, this perspective has not been lost on market participants. It has been exhibited in a rotation away from the liquidity-induced momentum trade towards more traditional cyclically oriented risk-on segments of the market. This shift in sentiment has also been evident in small-cap and emerging market stocks outperforming tech and a decline in the US dollar demand during the fourth quarter of the year.

Less Tech, More Cyclicals

Looking ahead into 2021, this sector rotation toward cyclical, risk-positive parts of the market could continue ahead of a recovery in the global economy. Even so, market optimism likely will be dependent on positive pandemic developments and a propensity for more fiscal spending.

More specifically, there is a risk that logistical and administrative issues related to vaccinations could lead to slower than anticipated uptake. For example, so far, only 3 million shots have been distributed and 11 million doses shipped – well below the Trump Administration's goal of 20 million vaccinations before year-end.

Now, there is a potential that the bottlenecks contributing to the weak uptake in vaccinations could be resolved in the coming weeks. With that said, the longer it takes to inoculate the population, the longer that pandemic related risks will linger and put downside pressure on economic growth and corporate earnings. This point is important because market expectations seem to be pricing in significant improvements in the pandemic narrative by mid-2021, paving the way for a strong second-half economic recovery. Unfavorable developments that lead to a substantial deviation from this outlook could break sentiment and lead to bouts of heightened market volatility should the market narrative.

What's more, there is a risk that a divided Congress could lead to more gridlock on Capitol Hill, potentially delaying plans for additional fiscal stimulus. Assuming that Democrats fail to pick up gains in the Georgia Senate runoff election, incoming President Joe Biden's plans for a third round of stimulus checks could face a substantial roadblock. For example, the US fiscal deficit as a share of GDP is now at its highest levels since World War II. Fiscally conservative Republicans could derail plans for another stimulus package. Should this happen amidst an already weakening economic backdrop, we could see a rise in investor uncertainty and a bout of price weakness in an already stretched market.

Positioning Your Investments to Thrive in 2021

Without a doubt, the road to recovery from the Pandemic of 2020 will be fraught with many challenges. Even so, we could see a sustained recovery in employment conditions, household spending, and economic growth assuming inoculation efforts accelerate and policymakers remain supportive of more fiscal spending next year.

Such improvements likely would sustain higher corporate earnings growth and support investor demand for cyclically oriented portions of the markets. While following the trend has been an attractive way to play pandemic uncertainty, investors positioning themselves to thrive in 2021 likely would be best served by sticking to the basics and focusing on fundamentals.

For example, markets are arguably mean reverting by nature. This behavior implies that what has performed well in the past is not as likely to perform as well in the future. From this perspective, evaluate which positions in your investment portfolio have outperformed in 2020 (especially if those positions are tech-oriented) and consider whether it's time to take some gains off the table.

Next, look over your overall investment plan and consider the composition of your holdings. As we transition away from economic survival and towards recovery, now may be the time to evaluate whether your portfolio is strategically aligned with your long-term savings goals.

Finally, get your savings plans back on track if this year's survival strategy included avoiding contributions to your retirement plan. With prices at historic highs in certain portions of the markets, it may be tempting to wait for an attractive entry point before getting back into the markets. Even so, trying to time your way back into the markets could lead to missing out on long-term opportunities. That's why dollar-cost averaging back into the markets might help you thrive financially in 2021.

Are Emerging Markets the Right Investment for You?

Should emerging markets have a place in your investment portfolio? In today's low yield, low growth environment, some investors are looking outside of the US to generate extra returns on their savings. For some individuals, emerging markets appear attractive on the surface, given their historically robust economic growth rates and higher bond yields. Indeed, there's a strong fundamental case to be made for investing in emerging markets.

Yet the task of finding the right opportunities can seem daunting, given the overwhelming differences between markets and risks in this space. Given these issues, you might be asking yourself if emerging markets are right for you. Well, finding the right opportunities likely won't be easy. Even so, if you have a long investment time horizon, a higher tolerance for risk, and a willingness to learn more about this increasingly relevant part of the world, then investing in emerging markets might be one way to diversify your investment portfolio.

Not Your Father's Emerging Markets

Emerging markets have experienced a significant transformation over the past two decades. One simple way to think about the change is in terms of a business startup. Decades ago, many of the world's emerging markets were seen as metaphorical economic startups that produced low-cost textiles and were a source of the world's commodity exports.

Indeed, manufacturing offshoring, foreign direct investment, and exporting activity were critical to emerging market growth early on. With the help of early investors and a host of governance changes, many of these countries have today become vital influencers in the global consumer and technological marketplace.

Like a startup business, this rising success has delivered to its population higher levels of financial wealth. That's why today, a young demographic and higher levels of wealth are likely poised to spur the next leg of growth in the emerging market story.

Why Demographics Matter

So why does the age of a population matter? A young, wealthy population is inclined to spend more on goods and services than one that is aging. According to the economic life cycle hypothesis, young individuals typically focus their early working years on growing earnings while they build up to a certain level of consumption on goods and services. Theoretically, these same individuals will use their savings later on in life to maintain an even-level of spending throughout retirement.

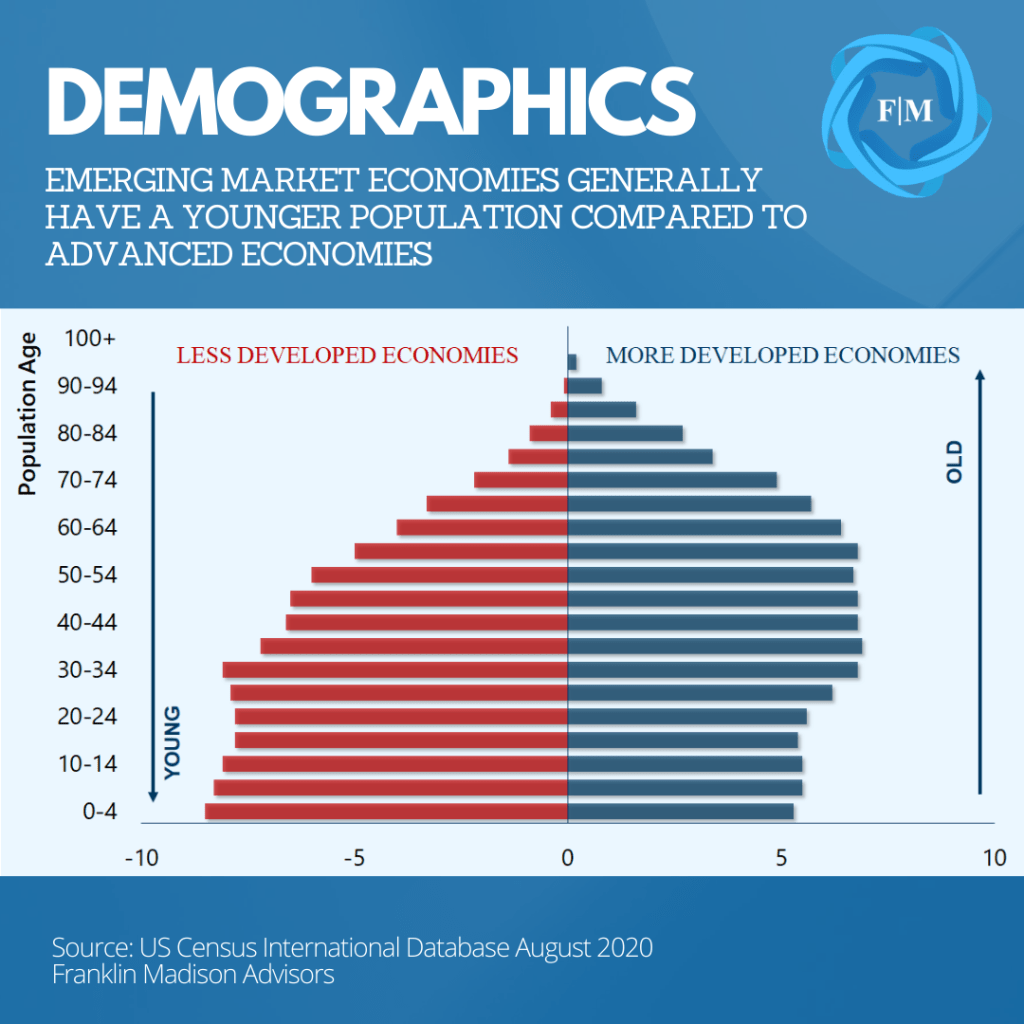

Outside of a purely theoretical framework, we can think of events like getting married, starting a family, and planning for the future as reasons why some younger individuals are more inclined to spend on goods and services than their older counterparts. This spending pattern is also one reason why consumption is likely to play an increasingly crucial role in emerging market growth over the coming years as more developed economies continue to age. How different are the demographics in emerging markets relative to more advanced economies?

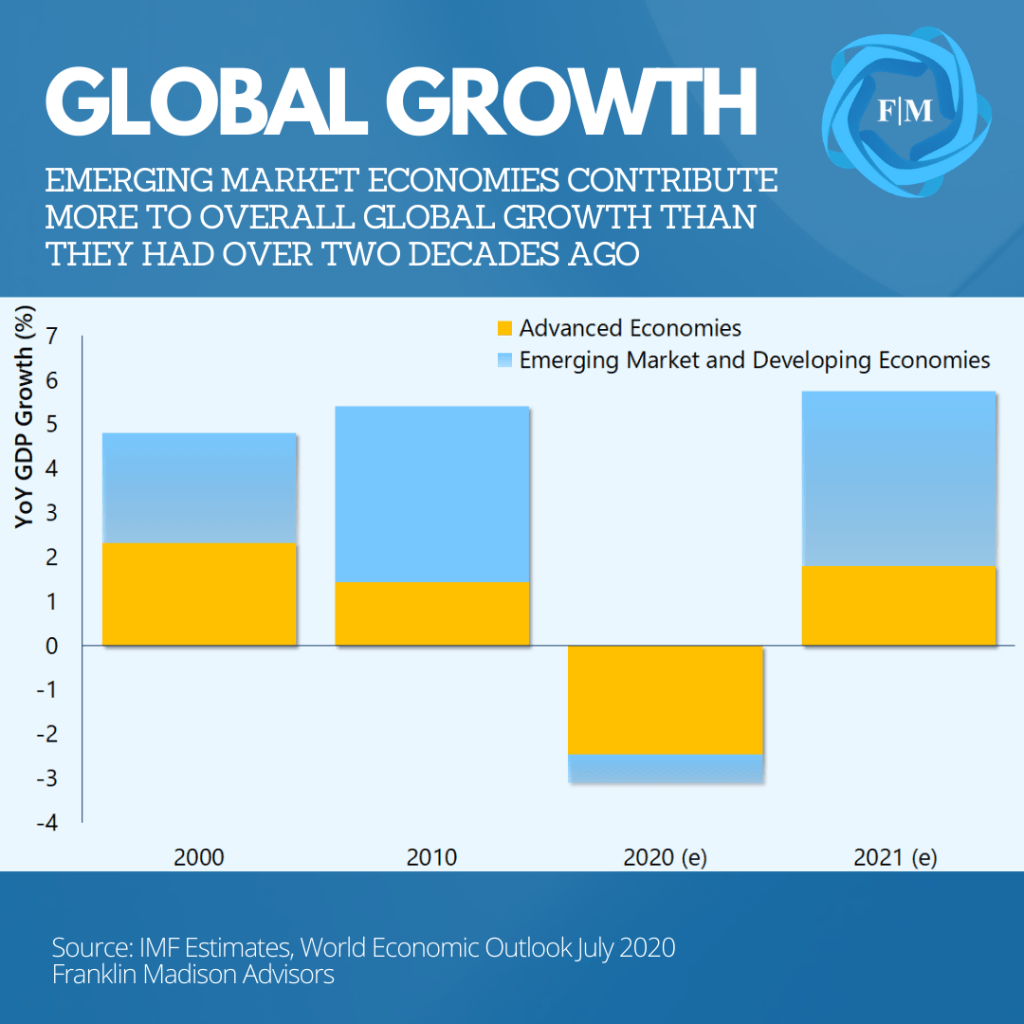

Today, over 6.4 billion people live in developing economies, compare to 1.3 billion in more advanced countries. Among many emerging market populations, the median age is now in the low 30's. In India, for example, over half of its population is below the age of 30. And how does this compare to more advanced economies?

Well, in Japan, the median age is 49 years old, with only 26% of its population below 30. While the US is generally younger than Japan, only a little more than a third of the population is under 30 compared to 50% for India. And considering that India has four times as many people as the US, you can quickly see how this young, consumption-oriented growth narrative in emerging markets might be primed to accelerate.

Now, it's not enough to say that a young population can drive economic growth alone. Take Afghanistan, for example. While not an emerging market economy, this impoverished country illustrates how having one of the youngest populations is not the ticket to wealth. What's missing? A young country poised for growth needs a predictable political, legal, and investment base to provide income opportunities for its growing population. And it's these critical factors that are missing in Afghanistan but have led to rising wealth in some emerging market countries over the past twenty years.

When Reforms Lead to Structural Improvements

While we talk about emerging markets as a single unit, much of the past growth in this part of the world has been driven by Asia. For decades, countries across Asia have built up wealth by stabilizing their political environments, cutting bureaucratic red tape, and introducing predictable and enforceable rules of law.

These actions have arguably underpinned the startup phase of economic growth we mentioned earlier. And these initial efforts resulted in a rise in foreign firms establishing a local presence that brought in billions of dollars in foreign capital investment to emerging market countries.

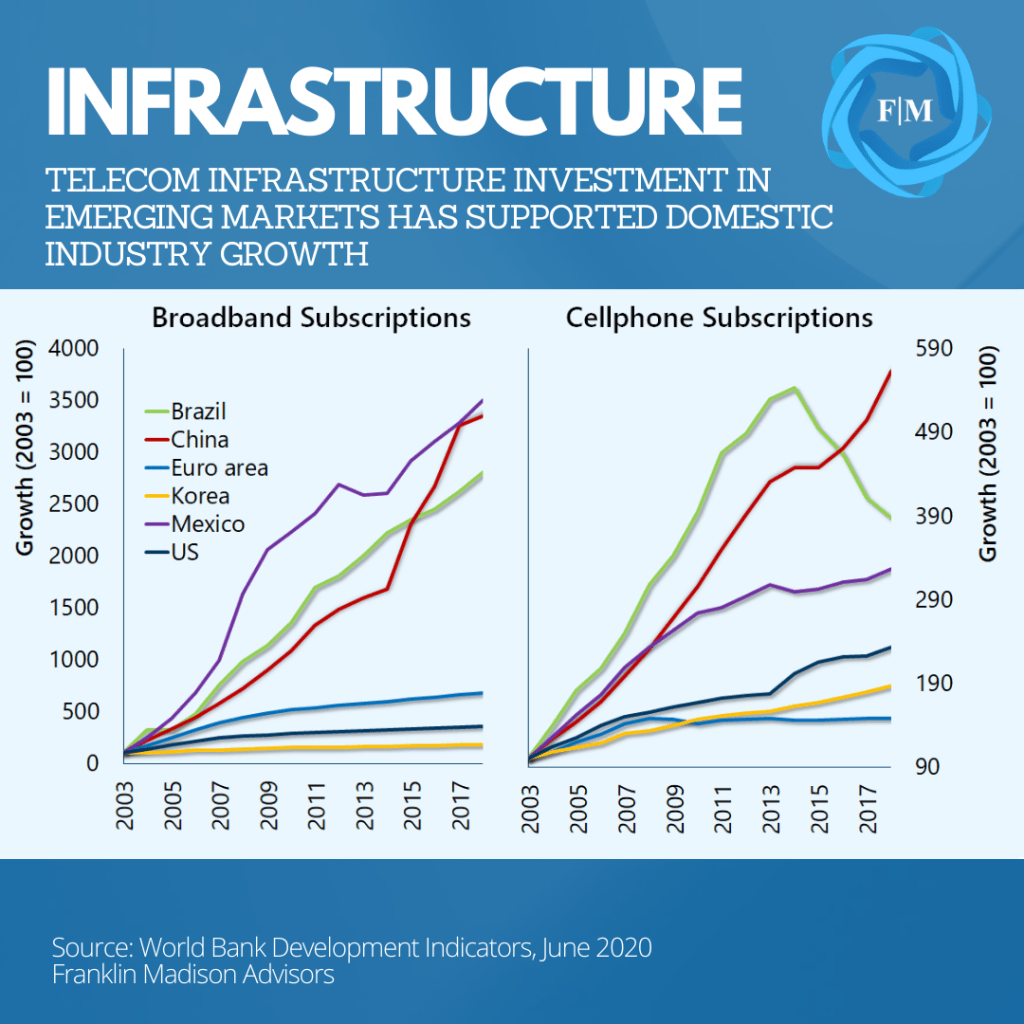

At the same time, leaders made a deliberate effort to reinvest their new-found tax base back into their local economies. These reinvestments included building infrastructure and making it easier for individuals to start small businesses that have given rise to firms that today compete on a global scale. And when we think about economic reforms in emerging markets, China is the most prominent example of this positive outcome.

Policy changes by Chinese leader Deng Xiaoping in the 1970s led to an opening up of the country's economy and ushered in a foreign investment flood. At the same time, policies enacted to reform state-owned enterprises, improving telecommunications infrastructure, and championing its private sector enabled China to create a base for its economic ascendance. And while China's development is significant, it should be noted that this growth miracle isn't isolated to China alone.

Singapore (essentially a small city-state) went from a developing country just a couple of generations ago to an essential part of the Asian economy. And today, it stands as a vital global financial center. South Korea is yet another development success story in the region.

Reforms allowed local names like Samsung, Hyundai, and others to flourish on the global stage. Today, policy changes in countries like India, Vietnam, and Thailand and efforts among ASEAN nations are paving the way for a new cohort of rising economies and increased wealth for a young population ready to spend.

Broadening Investment Opportunities

Having moved past the startup phase and well into expanding growth, firms in emerging market countries increasingly need more capital as they shift their focus from selling goods and services abroad to their own domestic markets. Funding this expansion through bank loans can be costly and is one reason why business leaders look to capital markets to issue stocks and bonds as a more affordable way to fund operations.

It’s crucial to note that foreign investors play an essential role in these markets. Continued governance improvements and other systemic reforms increasingly make emerging markets an attractive investment destination for outside investors. While some foreign investors might consider the markets small or illiquid, here are two points you should know about capital markets in these countries.

First, while the US remains the single largest financial market globally, emerging markets have become a critical part of the global investment landscape. Today, emerging market stocks represent nearly a quarter of global market capitalization compared to less than 5% at the turn of the century. What’s more, the amount of debt in these countries has risen to 25% of total global debt outstanding, with an investible universe of nearly $12 trillion in debt securities.

The second thing to consider is that investing in emerging markets isn't just about materials, industrials, or financials anymore. Rather, sectors oriented toward consumer spending, technology and healthcare are quickly taking a rising share of emerging market investment opportunities and tracking the economic transformations we've discussed.

The point here is that demographic fundamentals are driving a need for emerging market capital investment. A young and increasingly affluent population combined with growing global capital market influence is likely to broaden the set of emerging market investment opportunities available to you in the coming years.

Finding the Right Investment

Up to now, we've laid out the fundamental growth story and capital market opportunities for emerging market investors. And if you're like many investors, you're probably asking yourself how you can get started.

While it's tempting to think of emerging markets as one homogenous group, the reality is that emerging market investing is not like investing in the US. In fact, this universe comprises 27 separate countries that make up emerging markets, each with their varying composition of stocks and bonds, exposure to state-owned and private sector securities, and other factors like company size, sectors, and style. That's why it's essential to consider specific risks in this area, before diving in. Let's begin by taking a look at volatility risk.

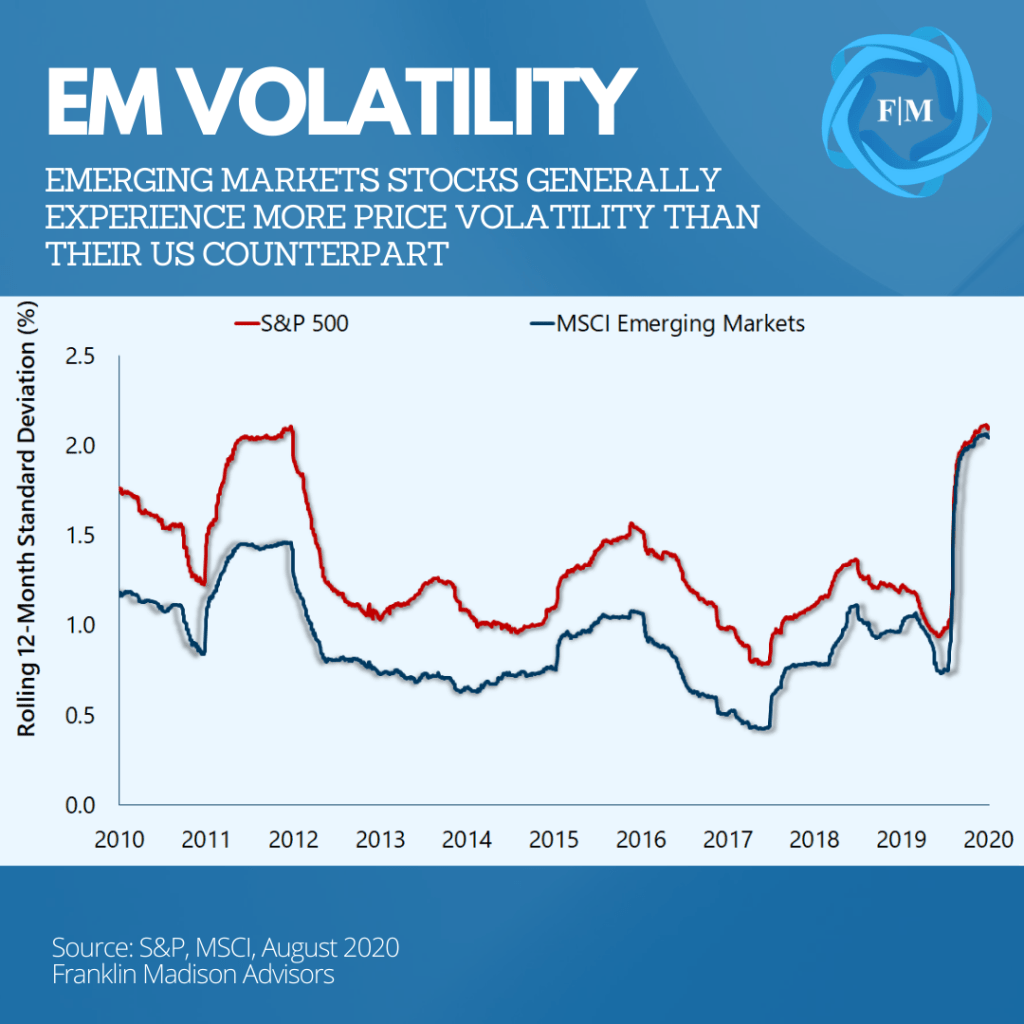

Volatility Risk

Emerging markets have a reputation for being higher risk and higher volatility for a good reason. History shows that over the past decade, emerging markets stocks have exhibited higher levels of price volatility than US stocks.

More specifically, equities making up the MSCI Emerging Markets index returned less than 1% annualized over the past ten years yet had more volatility than the large-cap US stocks. Much of this disparity can be explained by differences in regional equity performance in places like Latin America vs Asia and illustrate that higher risk does not necessarily mean higher returns at a broad level.

Liquidity Risk

Liquidity is another concern for investors in this space. Emerging markets are often influenced by risk-on/risk-off sentiment in global financial markets. In the past, some emerging market governments have welcomed capital inflows during risk-on periods, only to put in place measures to prevent hot capital outflows during times of financial stress.

While some of these liquidity and capital control issues have eased in recent years, this risk nevertheless underscores the point that investing in emerging markets should be done with a long-term view in mind.

Interest Rate Risk

Now when interest rates rise, bond prices fall. This basic fixed income concept illustrates how interest rate risk might be present in emerging markets today. Fluctuating inflation and changes in monetary policy often affect the direction of interest rates in emerging market economies.

One only needs to look at the events in Turkey in recent years to see how political and economic disruptions led to a sharp rise in its central bank policy rate and a rapid decline in bond prices.

Currency Risk

Currency risk is another factor to consider. US-based investors not only need to stay on top of emerging market developments, but they must also be aware of what's happening with the US dollar. When the dollar is weak, investment returns from emerging markets can generally be higher due to currency translation effects.

The opposite is true when the US dollar strengthens. This is notably the case with local currency-denominated debt. How so? Well, it’s because a weaker foreign currency buys fewer dollars when interest payments are brought home. Either way, staying on top of currency market developments is central to emerging market investing.

Political Risk

Finally, political risk is one of the top concerns among emerging market investors. Changes in a political regime or legislative structures within these countries can either quickly lead to economic prosperity or its reversal.

Such risks have been acutely demonstrated in Latin America, where various corruption, legal, and other political issues have created uncertainties for investors. What was the result? Well, these developments have arguably led to Latin American equities mostly underperforming the rest of its peers over the past decade and contributing to investment flat performance for emerging markets as a whole.

The takeaway here is that if you plan to get started with emerging market investing, it's not only essential to understand the narratives that can drive asset prices higher, but also the risks that can move against those opportunities as well.

Getting Educated About Emerging Markets

Navigating complex risks in an ever-changing market environment can be challenging for even the most seasoned investment professional. That's why research is a crucial component of any investing journey. And it only becomes that much harder to sift through overwhelming amounts of data and reports when you're exploring a country or region with little familiarity.

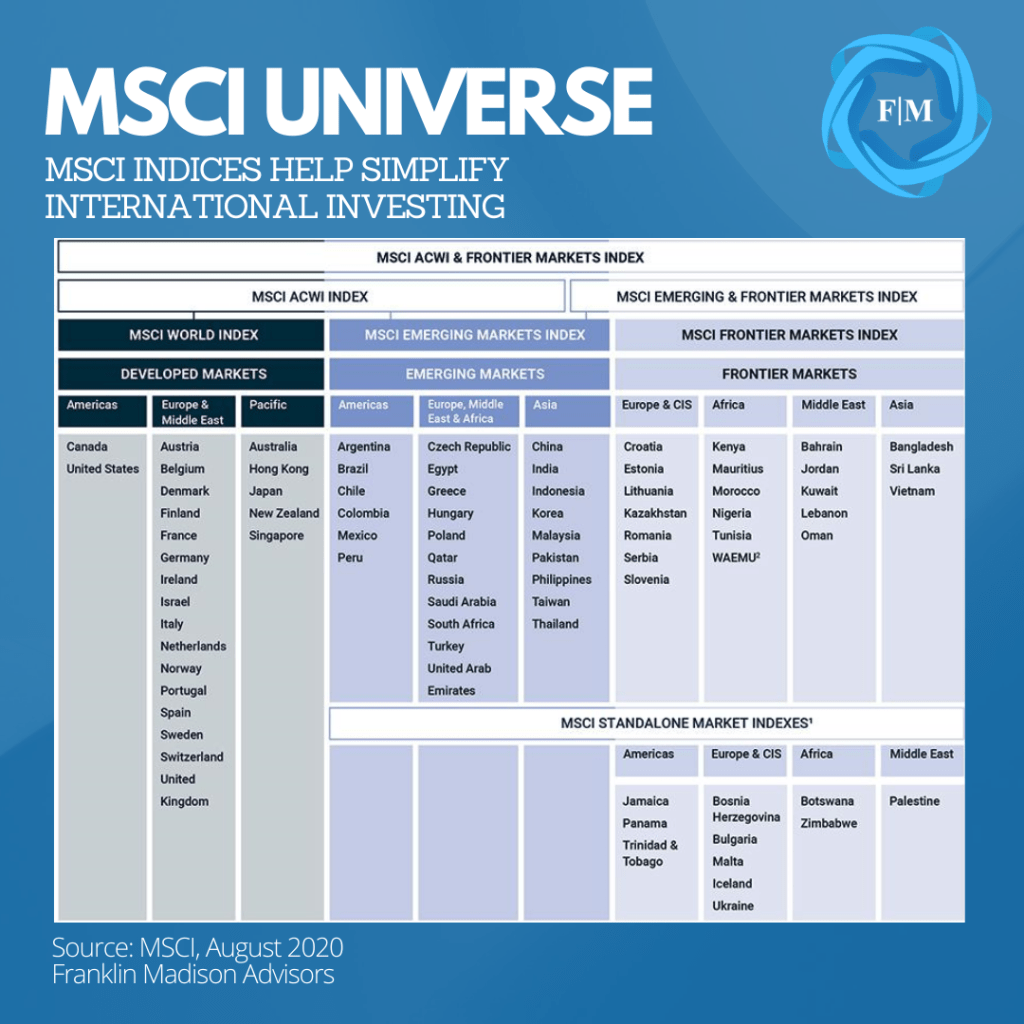

Fortunately, third-party firms have helped simplify the research and security selection process in global markets generally, and emerging markets specifically. One company central to the development of investment strategy within emerging markets is MSCI. MSCI is widely known for its stock market benchmarks. And what's essential to your research process is understanding the methodology MSCI uses to add securities to its indices.

Pages can be written about the tools, techniques, and computations used by MSCI to build its benchmarks. Even so, here are three ways using MSCI's research can help in your emerging market investment journey. First, the firm segments capital markets on many factors like capital controls (mentioned earlier) and market capitalization to differentiate between developed, emerging, and frontier markets.

Second, the indices, in many cases, represent the investible universe available to foreign investors. These factors include free float, which indicates how much of a given company's stock is liquid and available to foreign investors. This process can help take the guesswork out of knowing which firm could experience wide price swings due to low security marketability.

Finally, it's important to note that you cannot invest directly in an index. For this reason, many well-known US-based asset management firms have developed investment vehicles that follow a portfolio construction process to mimic MSCI indices. This fact can simplify the security selection process, especially when emerging market investing is not your primary vocation.

Investment research can be an onerous process. Even so, relying on robust third-party resources and tools can help you shorten the amount of time you spend identifying attractive regions and securities within the emerging market universe.

Are Emerging Markets the Right Investment for You?

Emerging markets are transitioning from being the world's producers of low-cost goods and commodity exporters to high-value, globally relevant investment destinations. These changes have brought wealth to a young population poised to spend, creating a new set of opportunities for global investors. Even with this positive backdrop, is investing in emerging markets right for you?

Well, finding the right opportunities likely won't be easy. Even so, if you have a long investment time horizon, a higher tolerance for risk, and a willingness to learn more about this increasingly relevant part of the world, then investing in emerging markets might be one way to diversify your investment portfolio.

Worried About Inflation? Look Beyond Gold.

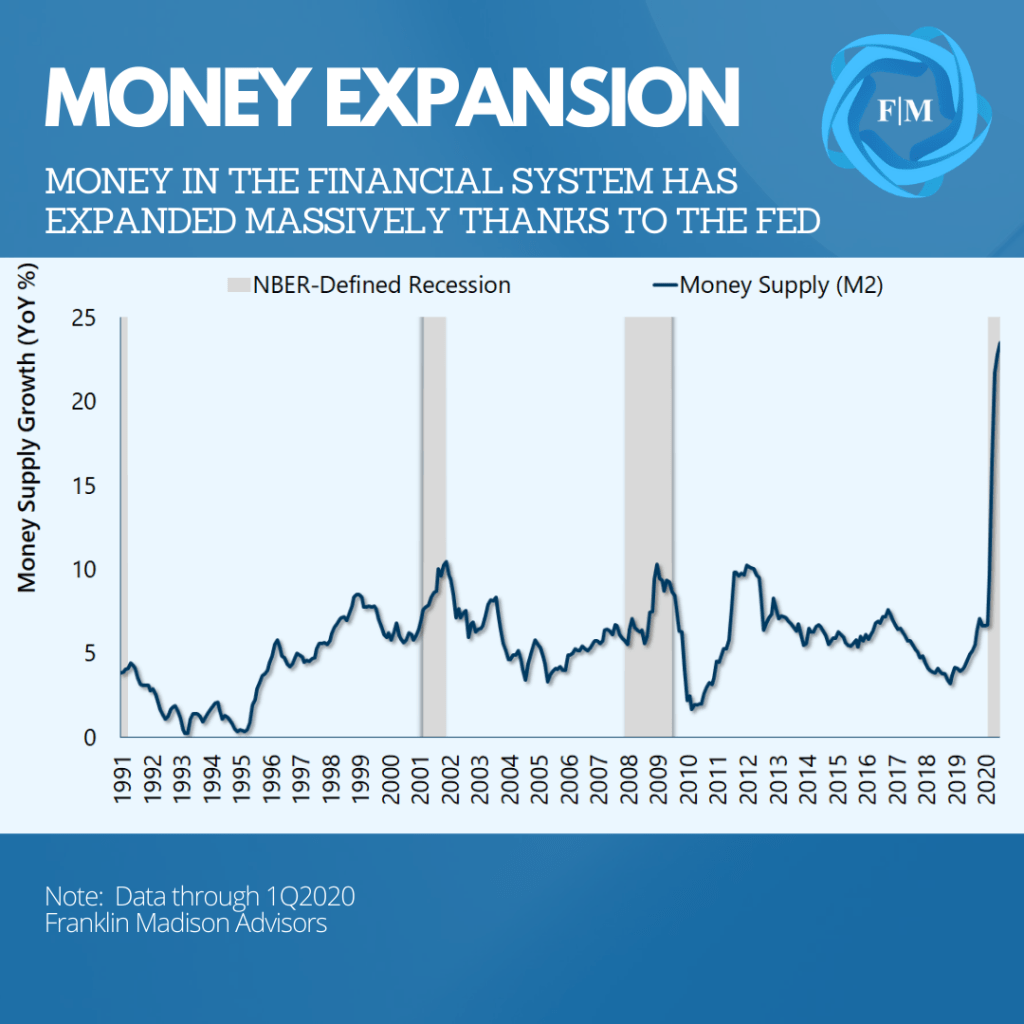

Savers are increasingly looking to gold as a way to address rising inflation and for a good reason. The Federal Reserve's policies in 2020 have massively expanded the supply of money. And more money could lead to higher prices down the road. In anticipation of this concern, some investors are considering gold investments to hedge, or protect against, higher inflation. But a key question for many investors is whether gold is an appropriate way to protect against rising prices.

Our work suggests that relying on gold to protect your savings against inflation may not be optimal. In fact, a survey of historical financial and economic data suggests that assets like stocks and bonds could be better suited to mitigate inflation. More importantly, a diversified portfolio of stocks and bonds provides the benefits of inflation hedging while reducing overall risk to your savings compared to investing in gold alone.

Why Should You Worry About Inflation?

So, what is inflation, and why should you care about it? Well, inflation represents a steady rise in the price of goods and services over time. For example, a can of soda that cost your grandmother ten cents in her youth might now cost you a dollar. And today, inflation is evident in everything from higher housing to education and health care costs.

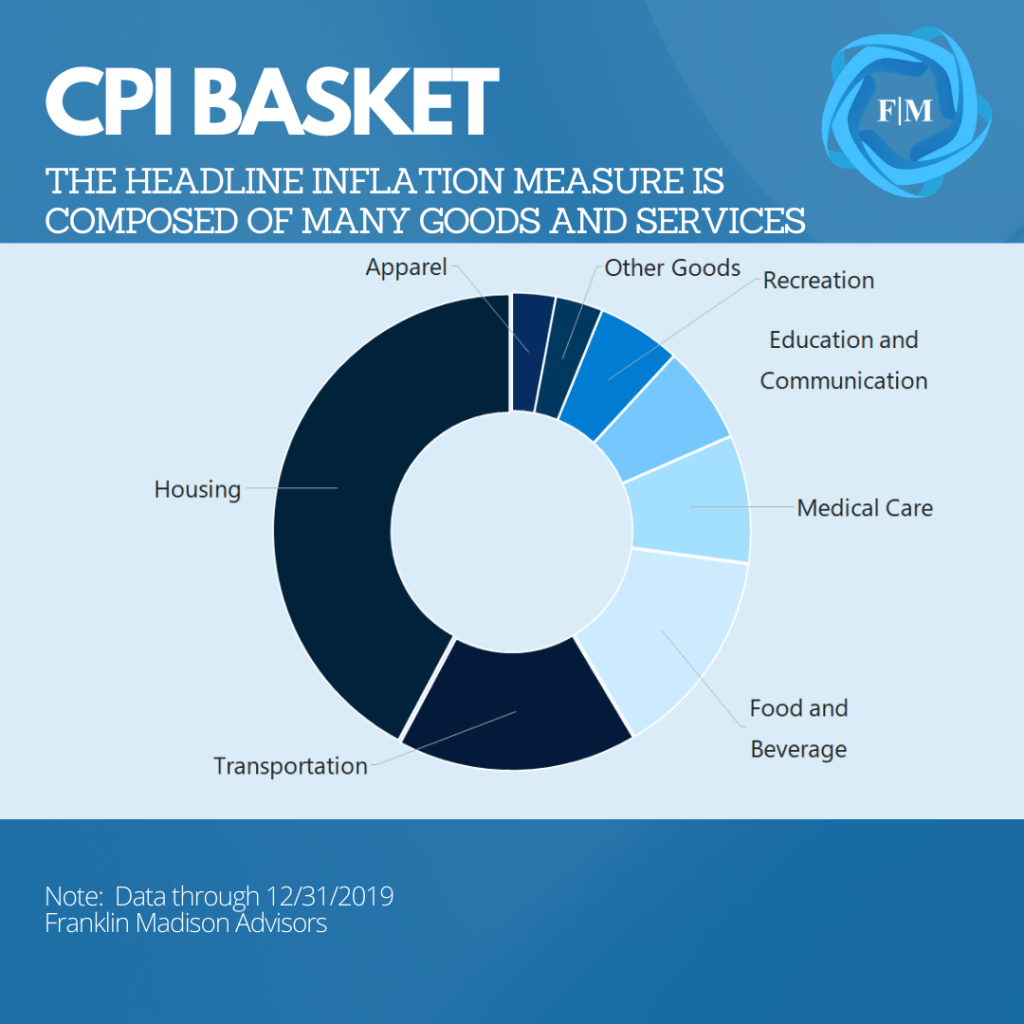

There are many ways to measure inflation. One often-cited inflation measure is the Consumer Price Index (CPI). Every month, government workers survey the prices of hundreds of products and services comprising the CPI basket. The relative importance, or weights, of the items in the CPI basket, is intended to reflect how most Americans spend their paychecks. And while individual prices might ebb and flow from one month to the next, it takes a broad move higher in the basket to signal rising inflation in the economy generally.

Where does inflation come from? Well, there are many schools of thought on the origins of inflation. Ask a Monetarist, and they'll tell you that central banks, with their printing presses, and low-interest rates are the cause of inflation. Ask a Keynesian, and their response might be more nuanced with an emphasis on factors like economic supply and demand and the scarcity of goods or services. Either way you cut it, more money in the financial system and higher levels of future economic growth could lead to faster inflation in the years to come.

Why is inflation important to you? Well, inflation is a vital concept to understand because, when left unchecked, it can erode your purchasing power. That is purchasing power representing the number of goods or services that a dollar saved today can buy you tomorrow. Since 1990, US CPI has risen at an average annual rate of 2.4%. And at this rate, purchasing power is cut in half every 30 years. In other words, while you may have spent $100 on a given good 30 years ago, today, it will cost you $200 thanks to inflation.

This point is notably crucial if you're saving up to buy a home, pay for college, or plan for retirement because not accounting for inflation might leave you short when it comes to paying for these essential financial goals. That's why it's not only enough to just put some away money for the future, it's also vital to grow your money in a way to generate a healthy return that beats inflation.

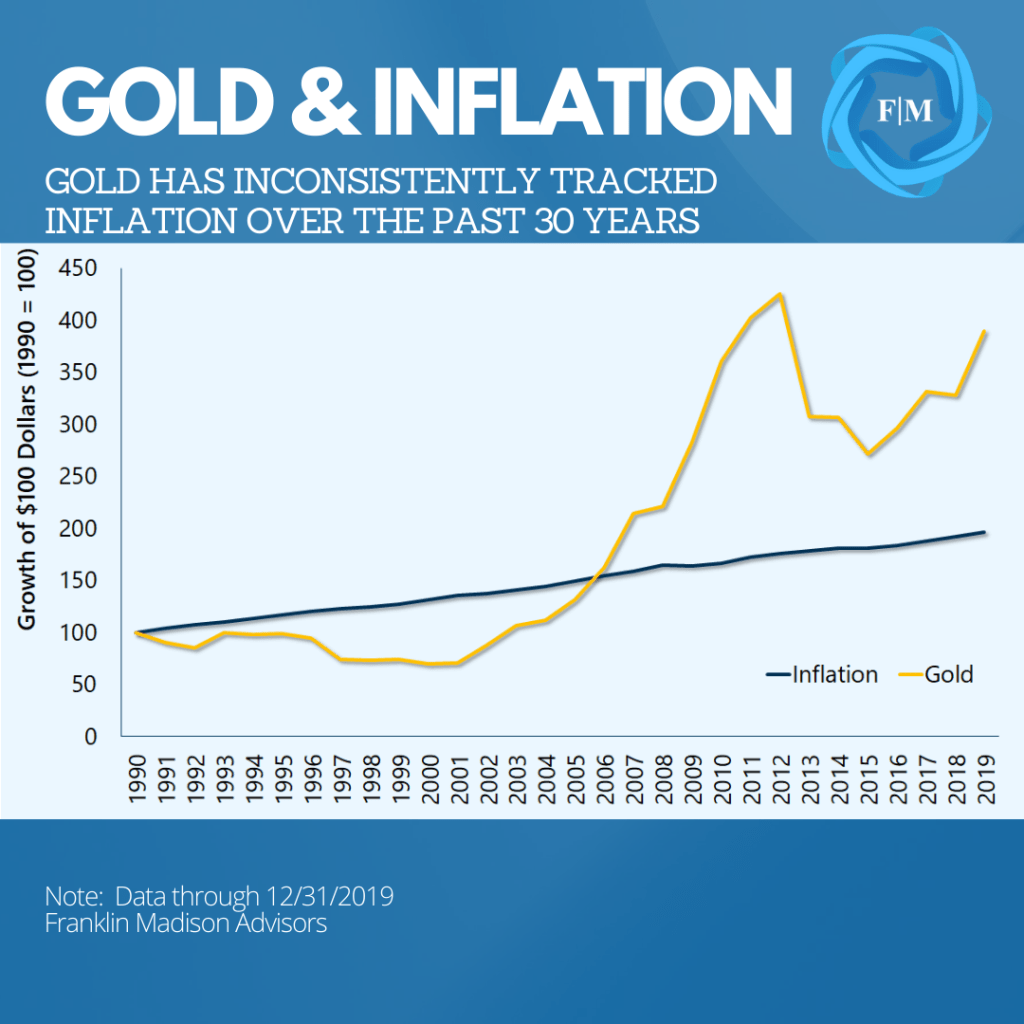

Is Gold an Optimal Inflation Hedge?

For thousands of years, gold has been relied upon as a form of currency and a store of value. Now gold's worth comes mainly due to its scarcity. This precious metal is so scarce that all of the gold mined throughout history could fit into three Olympic-sized swimming pools. Until the 1970s, the value of the US dollar was tied to a gold standard, and today, global central banks are expanding their holdings of the precious metal as part of their currency reserves.

While there are many reasons to view gold as an essential store of value, history has shown that this precious metal is not the best hedge against inflation. For example, since 1990 gold has increased from $391/oz to over $1,500 by the end of 2019, giving it an average annualized growth rate of 4.8%. How does this stack up against inflation? Over this same 30-year period, as mentioned before, inflation has averaged 2.4%. While gold has bested inflation in some respects, the return on gold is lower than what we would find with other financial assets. A point we'll explore in just a moment.

Besides the issue of underperformance versus financial assets, there are other challenges associated with holding gold. First, gold can be costly and cumbersome. Buying, transporting, and storing large amounts of gold comes with various expenses. And while storing gold at home can alleviate some of these inconveniences, doing so can expose your money to potential theft and loss. What's more, many homeowners' policies provide minimal coverage for the loss or theft of gold. So when your gold is gone, it's gone.

Second, when it's time to sell, finding someone to buy your gold, and getting a reasonable price might be difficult. Certainly, many gold dealers are willing and ready to pay cash for your yellow metal. Even so, fluctuations in gold prices can be as volatile as holding stocks, with a price that can fall as quickly as it rises. Therefore, while gold is on a tear today, the price a dealer will pay you tomorrow is less certain. Given its low return, high volatility, and high holding costs, gold may not be an optimal hedge against inflation. If protecting against inflation is a concern, you may want to consider financial assets.

Financial Assets as an Inflation Hedge

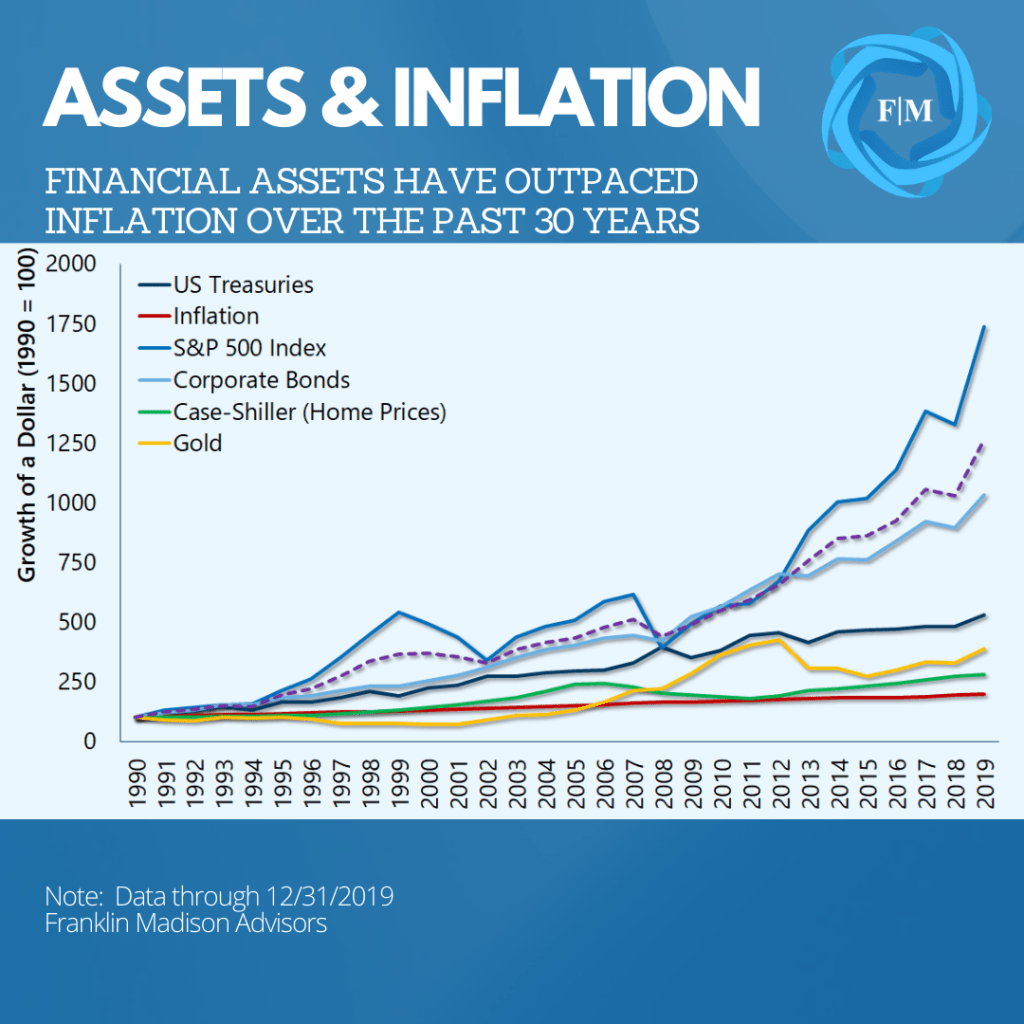

So, how well have financial assets held up against inflation? Well, generally speaking, data have shown that some financial assets, most notably stocks, have handily beaten inflation over the past 30 years. Since 1990, equities (as measured by the S&P 500 index) have appreciated 10.3% per year on a total return basis. This rate of growth has bested gold by a spread of 5.5%.

It's true that many of the same factors that drive stocks higher are evident in gold price movements. Even so, while stock markets are largely seen as driven by supply and demand, the equity gains noted above reflect total returns or the return received with dividends reinvested. This concept of total return is vital because gold does not produce income. Its value is solely based on what an individual buyer or seller thinks the yellow metal is worth.

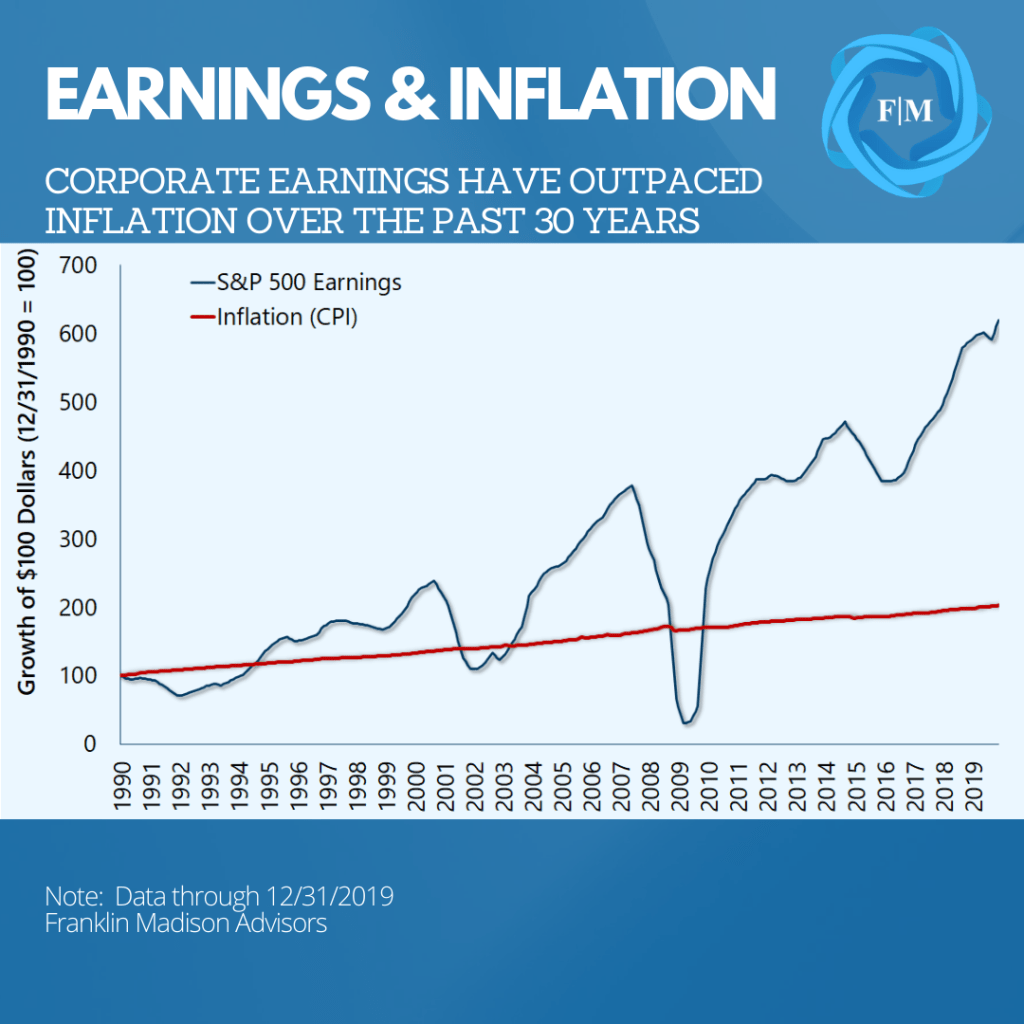

On the other hand, equity prices are driven by market demand for a given security and expectations of a firm's earnings. Market participants are willing to pay increasingly higher prices for a stock in anticipation of a firms' rise in earnings. These earnings typically grow through a combination of competitive advantages and pricing (inflation) adjustments that flow through to a company's revenues and profits.

To this point, over the past 30 years, S&P 500 companies have been able to grow earnings at an annualized rate of 6.7%. From this perspective alone, we find that equities have a natural inflation hedge built-in through their ability to pass along rising prices to their customers. And it's these intrinsic efficiencies that drive value to shareholders.

Other financial assets, like US Treasuries and corporate bonds, have also posted outsized gains against inflation and gold over the past 30 years. Much of this outperformance has been driven by several factors, including falling interest rates, central bank asset purchases, and investors' search for yield. Even so, bond investors not only receive a return on the price of the bonds themselves, in many cases, they get paid interest while they wait.

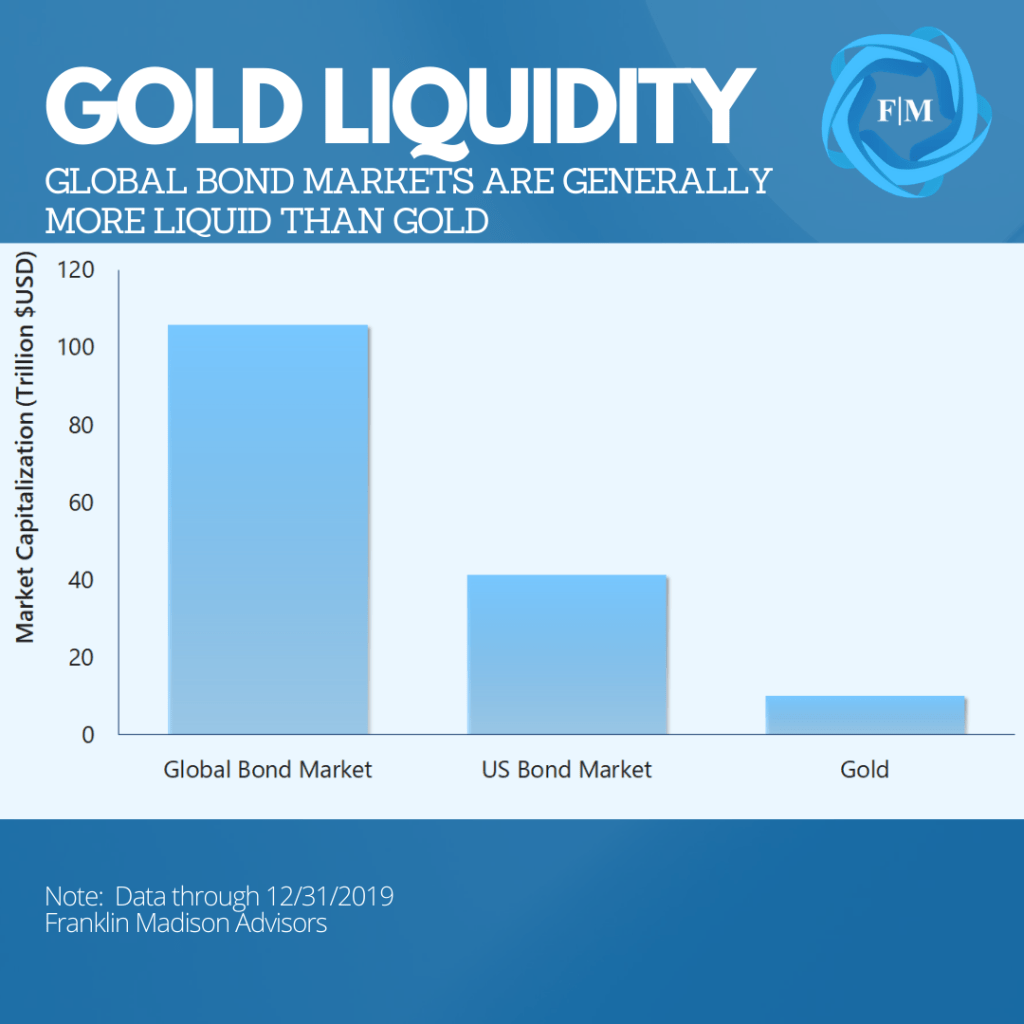

Another thing to consider is that while the total market value of gold globally is around $10 trillion, in the US, total bonds outstanding sat at $46 trillion in the first quarter of 2020. Globally, this figure is well over $100 trillion. And given higher liquidity and marketability, bonds generally have exhibited lower levels of volatility. Add in the earnings power of equities, and historically higher returns, there is a stronger fundamental case for holding financial assets over gold as an inflation hedge.

Getting Paid to Take Risk

One final way to think about the benefits of holding gold versus other assets is to consider how much you're paying to take on investment risk. One standardized measure of this risk-to-reward tradeoff is the Sharpe ratio, a concept we explored in a prior report. From an investment perspective, the Sharpe ratio helps you compare two or more assets to determine whether the return you've received per unit of risk is higher or lower. The higher the Sharpe Ratio, the higher the implied risk-reward tradeoff. How does gold stack up?

Compared to holding large-cap stocks or US Treasuries, gold offers a lower rate of return per unit of risk taken. This observation is notable since gold has returned less than US Treasuries over the past 30 years yet has a volatility measure comparable to stocks.

Even when we expand this measure to include home prices (another poor inflation hedge we'll discuss in a later report), while gold price appreciation beats home values, you're getting paid less on a risk-adjusted basis. Taken together, compared to other investments, gold is likely to pay you less to take on relatively the same amount of risk.

Bringing It All Together

If gold is not an optimal inflation hedge, where should you put your money? How much inflation and when it will arrive is mostly uncertain. What we do know is that when economic uncertainties rise, market volatility often increases as well.

Rather than trying to find one place to invest your money to protect against inflation, you might want to consider holding a diversified basket of stocks and bonds. Doing so might help protect against inflation and help mitigate market volatility when economic uncertainties rise.

As we've written about in the past, diversification is one crucial way to reduce portfolio volatility and smooth out investment returns for the long term. Studies have shown that increasing the number of securities held can reduce overall volatility in an investment portfolio. Therefore, if your goal is to invest for the long term, make an effort to diversify your portfolio across various securities and asset classes to help reduce risk.

Our work suggests that holding a simple 60/40 portfolio of stocks and bonds over the past 30 years protected against inflation, reduced investment risk, and provided generally higher risk-adjusted returns than gold alone.

Worried About Inflation? Gold Alone Might Not Cut It.

Preparing for inflation is a vital concept that all investors should carefully consider. Not accounting for rising prices, particularly at a time of unprecedented central bank policy, could leave you falling short of crucial financial goals. While some investors might look to gold as a way to protect against rising prices, history suggests that the precious metal might not be the best inflation hedge compared to several measures.

In fact, financial assets have a better track record of protecting against inflation. What's more, holding a diversified portfolio of stocks and bonds protects against inflation and can help smooth the ups and downs in the markets. The bottom line here is that if you're looking for a way to hedge against inflation, gold alone might not cut it.

What Are the Essentials of Crafting a Solid Financial Plan?

Many of us know that having a financial plan is a sensible place to start when it comes to achieving essential life goals. But what exactly is a financial plan, and more importantly, what makes for a solid plan? A financial plan is a strategy that lays out a set of actions that you need to take today to achieve your future life goals.

To be sure, a plan identifies a path that aligns available financial resources with your intended life destination. Therefore, the essentials of a solid financial plan should include clearly defined objectives, outcomes relevant to your current life situation and should also thoroughly reflect your entire financial position. Not considering these factors may lead your plans off course and to an unintended destination.

Crystallize Your Goals

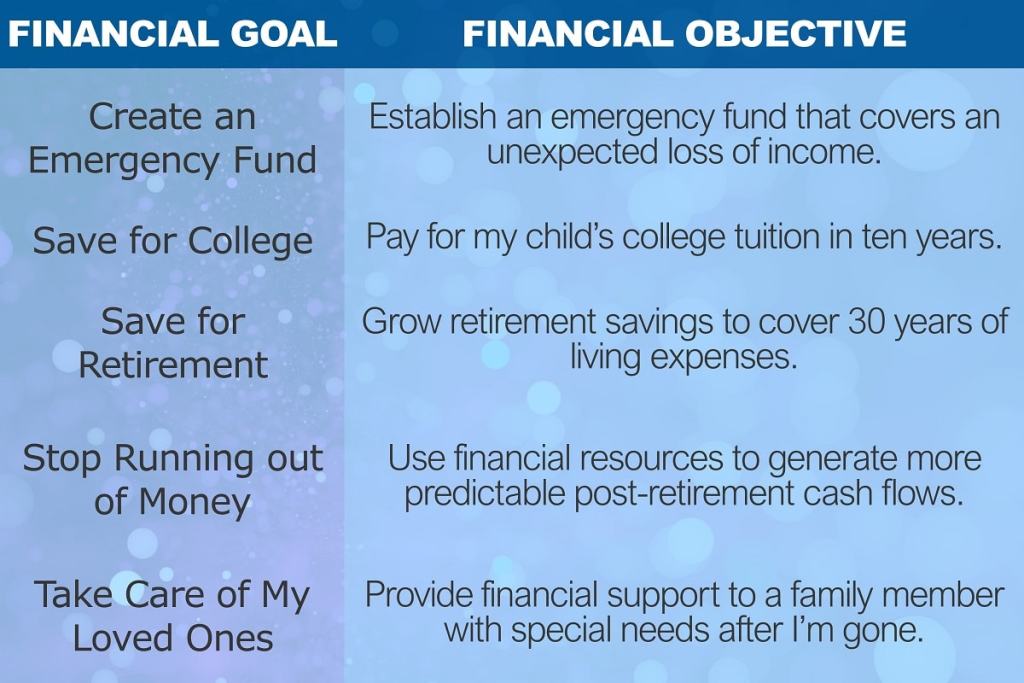

If a financial plan lays out how you can bring about your life ambitions, then being sure about your aim is central to hitting your intended mark. For this reason, the basis of a solid plan often begins with clearly defined financial objectives that align your financial plan with your goals. So, what are financial objectives?

Well, the table below illustrates how clearly defined objectives bring precision to your overall plan. To be sure, financial objectives get at the heart of why your financial plan exists. What's more, they can also be used as a reference point later on down the road to gauge whether your plan recommendations are moving you toward (or away) from your intended target.

Getting Help with Defining Objectives

What can you do if you have a general sense of your goals but are uncertain about articulating your specific objectives? That's where a conversation with a financial advisor can help. For example, let's say that you're a few years away from retiring but don’t know how to start planning for retirement.

During a discussion with your trusted advisor, you may discover that your retirement ambitions may include nuanced intentions like relocating closer to family, traveling the world, or wishing to be more charitable. In this situation, while your overall goal is retirement planning, the objectives that set the course for your plan may include buying a new house, creating a post-retirement travel budget, or evaluating means for engaging in philanthropic endeavors. Either way, financial objectives give direction to and are a crucial first step in creating your financial plan.

Planning Outcomes Should Be Relevant to Your Life Situation

Another essential aspect of creating a solid financial plan is ensuring that your planning objectives are relevant to your current life situation. This is important because irrelevant outcomes in your plan may take you down a path you never intended, leading to wasted time and souring your overall planning experience. When this happens, your perceived value of the planning process may decline along with your desire to put in the work necessary to achieve the other goals contained within your plan.

For example, pursuing a distribution strategy as part of a planning process might not make sense if your retirement date is over a decade away. Similarly, adding a professional asset management objective to your plan when all you want to do is consolidate a few small retirement accounts, might be beyond the scope of your planning engagement.

Comprehensive Shouldn’t Mean Complicated

Along these same lines is the use of a comprehensive financial plan. You might have heard of the term before and asked yourself: what is it, and why do I need one? From a broad perspective, a comprehensive financial plan may include:

- Cash flow planning

- Investment management services and

- Estate planning

Some individuals may find value in looking over all of their money matters in one sitting, particularly ahead of crucial life transitions. For example, let's say that you've amassed substantial savings and are a few years away from retirement. In this case, it might make sense to consider objectives that address investment distributions, ensuring the longevity of savings during your golden years and having an estate plan aimed at leaving behind a legacy.

For many people, however, sitting down with an advisor to talk about investment management or estate and tax planning objectives might not make sense at their given station in life. Even so, a comprehensive financial plan may still be an incredibly useful solution to address your most pressing planning needs. In fact, a comprehensive plan does not need to be complicated to be relevant for your life situation when there's a focus on the basics.

Take another example of a young couple planning to start a family. How might they benefit from a comprehensive financial plan? At this phase in their lives, the family might need to consider 1) adjustments to their current and future expenses, 2) establishing a savings program to pay for their child's education, and 3) reviewing life insurance coverage and preparing a simple will to address unexpected life events.

The point here is that comprehensive shouldn’t mean complicated. What's of more vital concern, however, is whether planning objectives are relevant to your current station in life. In either case, irrelevant planning objectives might prompt buyer's remorse, and derail your entire financial plan. Therefore, be sure to ask yourself early in the planning process, whether your objectives align with what you're ultimately trying to accomplish in your life today.

A Solid Financial Plan Should Be Thorough

How much house can you afford, or how much should you save for retirement? Many resources exist today that can help you calculate answers to these and other important money related matters. In fact, many websites and financial institutions offer free tools that can help you create a savings plan, establish a budget, and track your spending in real-time. But are these simple calculations and means enough to help you create a solid financial plan?

Often what's crucial to the success of your financial plan is not the tool you use, but rather how thoroughly these computations fit into the mosaic that is your life. Therefore, solutions to your financial objectives should reflect your spending and saving decisions as well as your asset and debt circumstances. This is important because some tools only consider one frame of your financial picture and may produce recommendations that fall short of your ideal outcome. And when you make decisions based on incomplete information, it could cost you valuable time and money.

For example, let's assume that your goal is to buy a house. An online calculator may tell you how much you can afford based on your income and living expenses and estimate a purchase price that's consistent with your mortgage. The tool does its job and produces a useful output when you give it some simple inputs. Even so, the estimate may represent a static result and likely not reflect all of the possible outcomes given your dynamic life situation.

Let's take our example a step further. Upon thoroughly reviewing your entire financial situation –spending, savings, assets, and debt – you discover that consolidating credit card debt could free up an extra $500 per month. When you take this information and feed it back into your home buying calculator, what you're likely to find is that 1) you can now afford to buy a more expensive home or 2) shorten the time it takes to save for a down payment.

The point here is that a solid plan should include calculations and estimates that thoroughly consider your entire financial perspective. Even if you intend to address just one objective, broadly understanding the interrelationships across your financial situation can help you craft a solution that fits your unique needs.

Increase Your Chances of Achieving Success

Finally, an essential point to consider is deciding when to create a financial plan on your own and when to bring in a professional. As we mentioned earlier, there are a host of tools available that can help you create your very own plan. From simple calculators to sophisticated smartphone apps and websites, these tools can lay out actions that you need to take today.

What's more, many personalities have authored books and created programs that have helped thousands of people reach their goals. So, when it comes to doing-it-yourself, there are plenty of cost-effective resources that you can utilize today to help you develop a solid financial plan that will move you closer to what's essential in life.

Knowing When It’s Time to Work With an Advisor

Sometimes, working with an advisor might make more sense than going it alone. Think of a financial advisor as a personal trainer. A personal trainer can help you achieve weight loss goals by creating nutrition and work out plans, showing you how to use equipment at the gym, and holding you accountable to your desired outcome. In a similar way, a financial advisor can use the planning process to help you achieve your important financial goals.

When might it make sense to bring an advisor into your planning process? Well, maybe you understand the various planning tools and approaches but have neither the time nor inclination to carry out the analytical and preparation work yourself. Another point where it may make more sense to work with an advisor is when you have a goal but are not quite sure about how to articulate your financial objectives or identify the tasks necessary to pursue that goal. Or maybe you've even tried a canned one-size-fits-all method to managing your finances but find that the approach does not suit your unique situation. If any of these illustrations resonate with you, then it might be time to bring in outside help.

Whether you work with an advisor or decide to go it alone, crystallizing your goals, identifying relevant financial objectives, and utilizing thorough solutions that fit into your life mosaic are essential components to crafting a solid financial plan. Not considering these factors may lead your plans off course and to an unintended destination. Indeed, a financial plan may be just what you need if you're looking for a way to create structure in your life and spend less time worrying about achieving your life's passions and purpose.

Keep Your Money Growing with Two Simple Steps

Growing financial wealth in today’s environment has been a struggle. Whether it’s the wide swings in asset prices that make it hard to decide whether to stay in or get out the markets to the dour economic conditions that have negatively affected business earnings. Finding the right strategy to grow your wealth in a world locked down truly has been a challenge.

So, what can households and investors do to make the right decisions to grow wealth given today’s challenges? Well, we believe that when individuals focus on a process and not an outcome they can create, grow and preserve financial wealth even in this difficult market and economic environment. More to the point, we believe that individuals can still grow their money today by utilizing and staying committed to a systematic wealth management process.

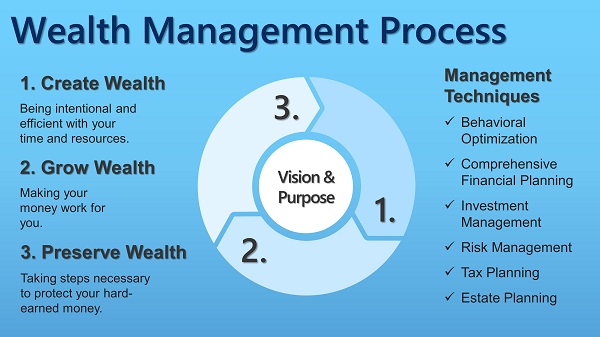

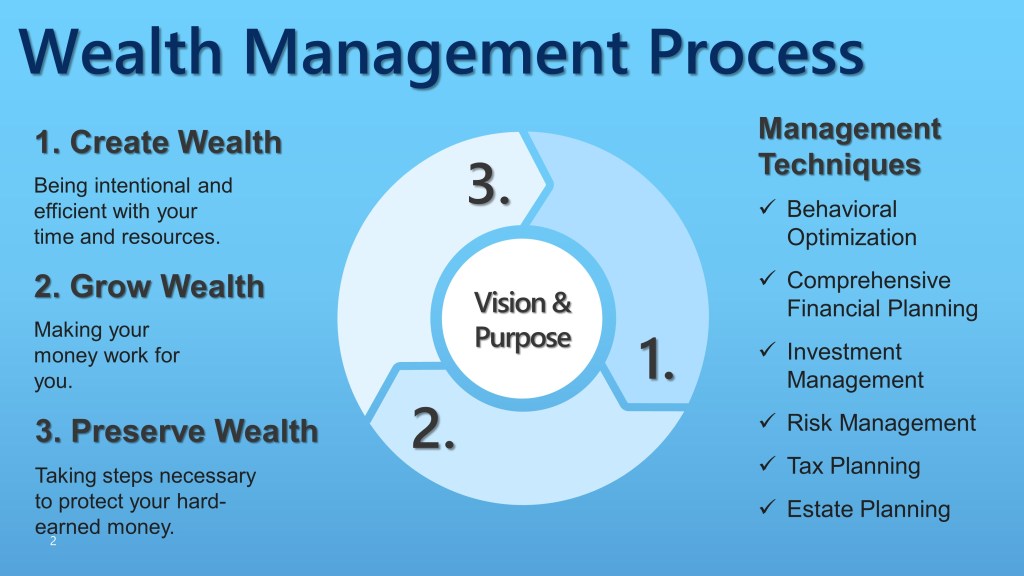

Figure 1: The Wealth Management Process

Growing Wealth Through a Systematic Process

In our report last week, we described how a wealth management process works and how it can help individuals build wealth that can endure the test of time. To recap, our wealth management process focuses on three key points to building enduring wealth:

- Being intentional and efficient with your time and resources

- Making your money work for you and

- Taking steps necessary to protect your hard-earned wealth.

In other words, a process focused on creating, growing, and preserving financial wealth. So why is the process important? Well, we believe it’s important because a process enables us to be consistent in the way that we align our wealth habits with our life’s passions and purpose. A process also provides discipline and being disciplined can help generate the productive assets that we need to pursue the more important things in our lives.

Create Before You Grow

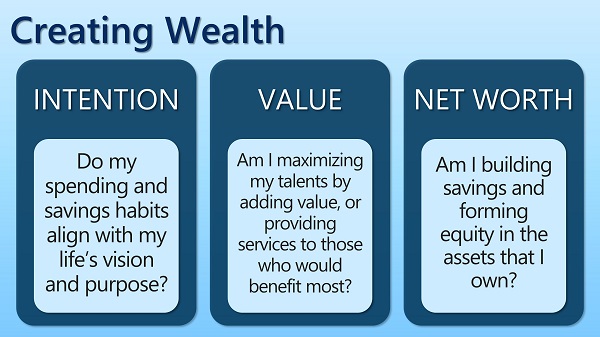

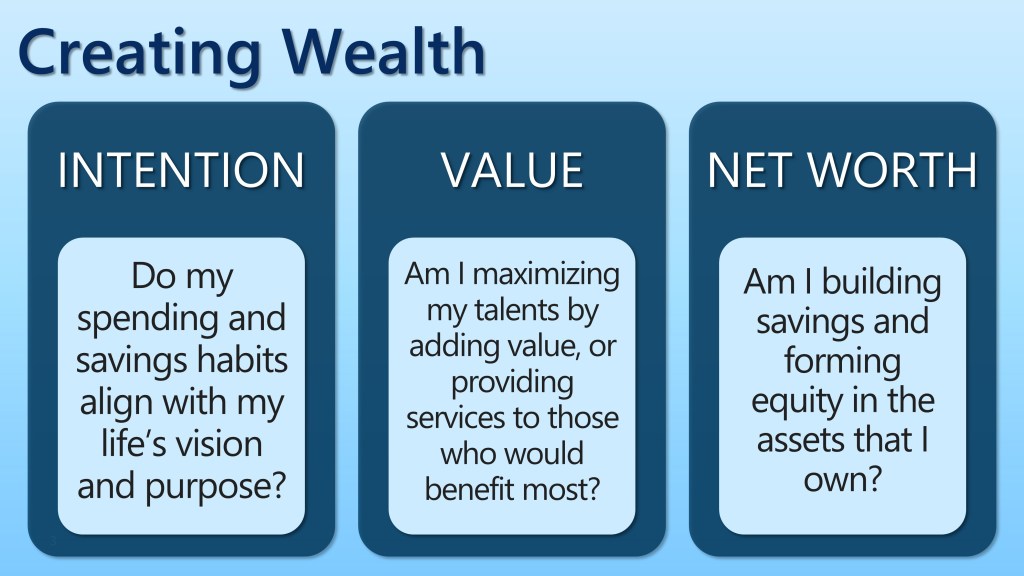

Where to begin? Well, we recommend starting with creating wealth before trying to grow wealth. More specifically, we suggest beginning with the first step in our Wealth Management process. To us, Creating Wealth means:

- Being intentional with your money and identifying your life’s vision and purpose

- Maximizing your value to others to increase your earnings potential and

- Optimizing your net worth so that you have a base of money from which to grow wealth

To be sure, a key reason we stress the importance of the creation process is because it sets the base for generating productive assets that you can use to make money work for you. Crucially, this process enables you to pursue the more important things in your life and in a relatively shorter period of time than you could otherwise.

Figure 2: The Components of Creating Wealth

So, let’s quickly revisit some of the key components of creating wealth that we covered in our report last week, beginning with intention. When we talk about intention what we mean is the way that you align your financial resources with the vision and purpose that you have set out for your life. In other words, intention gives your money a reason for existence. It also means that you may be more inclined to create wealth when your savings and spending plans reflect what matters most to you now and into the future.

Maximizing value is the second wealth creation component that we wrote about last week. That is, using your innate talents to take your career or business to the next level. This means doing the kind of work that gets you up early in the morning, energized and puts you in a state of flow. This is important because, the world tends to exceedingly reward those individuals who are excellent in the things they do and the way they show up to help other.

The third way you can create wealth is by optimizing your net worth. This is done by allocating more of your attention to saving money and by reducing bad debt. Put differently, it means using debt to acquire assets that will appreciate over time or enable you to maximize the value that you provide to others.

Taken together, we believe that these three wealth creation components are key to setting the foundation to building enduring wealth. This is because when followed in a systematic fashion, the components can be used to help generate the crucial financial resources you need to make your money grow over time.

Figure 3: Three Key Components of Growing Wealth

Make Your Money Work for You

So, we’ve just talked about creation and how the first step in our wealth management process provides a base from which wealth can grow. Next, we’ll walk through how you can actually grow your wealth. To start, we’ll need three key components for growing wealth:

- Accumulated savings

- A rate of return

- Time

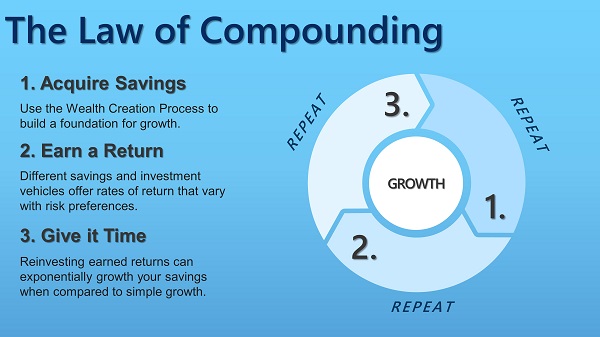

When taken together, you can use the Law of Compounding to grow your money in our current framework. More specifically, we mean earning a return on your savings, then investing that return back into your savings and repeating the process over a given period. Let’s take a closer look at the components necessary to grow wealth.

Figure 4: Law of Compounding

Savings is the first ingredient that you can use to grow wealth. To be sure, it’s primarily through the wealth creation process that we establish a solid foundation for growing financial resources. That is, without some form of savings developed during our creation process we have no base from which to grow money.

Our second growth ingredient focuses on a rate of return. For example, this would be a return that you could get from a savings account at a bank or the expected return from investing in the stock market. Whatever the case, the rate you receive will be either higher or lower depending on a number of factors, including time and the risk characteristics of your savings vehicle.

“…there are no shortcuts to building enduring wealth.”

Finally, to grow wealth you need to allow your returns to accumulate over time. While many of us wish we could grow our money in the quickest way possible, the fact is that there are no shortcuts to building enduring wealth. In fact, some research has shown that growing enduring wealth is typically accomplished through a consistent systematic process and done over an extended period of time. So now that we’ve talk about the three ingredients necessary for growing wealth let’s move on to looking at how this process works in practice.

A Practical Example

So how can you practically make your money work for you? Well, let’s look at an example. And we'll begin by going back to our three ingredients for growing wealth: accumulated savings, a required rate of return and time. In our example here we’ll assume that you’ve accumulated $100,000 in savings through the creation process. More specifically, you’ve done so by being intentional with your money, maximizing your value to others and optimizing your net worth.

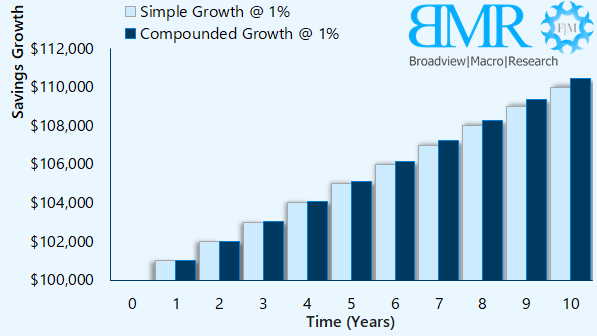

Figure 5: Growth at 1% Over 10 Years

Let’s also assume that your savings is held at a bank and that bank offers you a 1% annual rate of return. So, where does this leave you? Well, in one year, your savings will theoretically grow by $1,000. Therefore, by the end of year one, you would have $101,000 in savings. If you were to repeat this process over a 10-year period, your savings would have grown at a compounded rate by about $10,500 and in excess of $500 more than a simple rate of return.

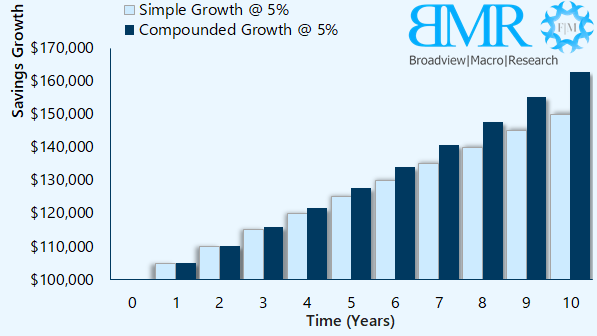

Now let’s assume that we increase your rate of return from 1% to 5%. How would this affect your savings? Well, with $100,000 earning 5% compounded annually the value of your savings would increase to $105,000 after year one and over $110,000 in year two. In fact, after 10 years, the difference between a compounded return and a simple return is nearly $13,000!

Figure 6: Growth at 5% Over 10 Years

What’s more the compounded excess return at 5% is nearly 28x larger than the 1% return when measured over a 10-year period. So, the point here is that with a little time and a decent rate of return you can make your money work for you in a very meaningful way.

Keeping Your Money Growing During Uncertain Times

So, what can you do right now to keep money growing during these uncertain times? Let’s review the two key points we’ve already touched on. For starters, consider your process. It will be increasingly difficult for you to grow and build enduring wealth if you’re undisciplined in the way you create wealth during this time of economic volatility and uncertainty.

If you’re serious about growing wealth, we recommend that you start by taking the time today to gauge your wealth creation habits. You can start by going back and reading our last report. But generally speaking, this includes evaluating the alignment between your wealth habits and intentions, how you’re maximizing value for your employer or clients and the extent to which you are saving and using debt wisely.

“The stock market is a device to transfer money from the impatient to the patient.” –Warren Buffett

The other thing that you can do to grow wealth in today’s environment is to keep in mind that enduring wealth can grow meaningfully when given time and a reasonable rate of return. Financial markets have experienced wide swings in prices lately. And it’s also likely that non-financial assets (like real estate) could see downward pressure in the coming months as well.

Our point here is that there may be a temptation to chase swings in the markets in an attempt to catch an asset while it’s on sale. Well, rather than spending your time and energy trying to time the markets, or looking for a good market entry point we recommend looking for assets that can provide a generally consistent rate of return and that are in alignment with your long-term goals and risk tolerances. With a little time and a decent rate of return, you can make your money work for you in a very important way.

Figure 7: Time and A Reasonable Return Go a Long Way

In short, we believe it’s still possible to grow wealth even in this challenging economic and market environment. You can do this by sticking to a disciplined wealth management process. This begins by systematically creating wealth and then using the law of compounding to make your money work for you. No matter your current circumstances, we believe that people from all walks can start building enduring wealth today simply by following a few key steps to create, grow and preserve their financial wealth.

The First Step to Thriving Financially: Creating Wealth Today

What can individuals do during this downturn to thrive financially and build, or in many cases, rebuild wealth that has been lost in the past few weeks? By many measures, U.S. economic activity continues to grind to a halt on account of the COVID-19 containment efforts. This is evidenced in various data releases published this week. And it’s also a key reason why some Governors are eager to reopen their state economies.

But the reality is that returning to normal will take time, regardless of how quickly the economy fully reopens. Until then, the fact is that there are no quick fixes to undo the financial damage that has already been done. Yet, we believe that purpose driven individuals can, over time, rebuild wealth regardless of their current circumstances. This can be done by taking the first step in a disciplined, systematic process to create enduring wealth. So, how does this process work?

The Wealth Management Process: Creating Wealth

Let’s begin by level-setting our definition of wealth. To us, wealth means more than simply money taken home from a job or material possessions owned. Rather, wealth represents the financial resources we use today to make happen what matters most in our lives. Put differently, we view wealth as a means to an end rather than an end in and of itself.

Riches do not consist in the possession of treasures, but in the use made of them. –Napoleon Bonaparte

So, when we refer to rebuilding wealth, we are not talking about striving to get back lost income or material possessions. Our efforts, instead, are centered on adhering to a wealth process rather than focusing on a wealth outcome. The aim of this process is to help us generate productive assets that can be used to pursue our life’s passions and purpose.

Figure 1: The Wealth Management Process

To be sure, we believe that individuals from all walks of life can amass the financial resources they need to build enduring wealth. This wealth management process includes three ongoing phases: 1) being intentional and efficient with your time and resources, 2) making your money work for you and 3) by taking steps necessary to protect your hard earned wealth. In other words, creating, growing, and preserving financial wealth. We’ll come back to our second and third points in future reports. For now, let’s focus on the first step in our wealth management process: creating wealth.

Components of the Creation Process

Creating enduring wealth involves being intentional with your money, maximizing your value to others and optimizing your net worth. Let’s explore these points in more detail, beginning with intention. A simple way to explain the concept of being intentional with your money is to consider how two families, the Adams and Bakers, use their financial resources.

Assume for a moment that the Adams family earns a million dollars and they spend a million dollars per year without saving a dime. We could deduce that the Adams family’s intention is centered squarely around consumption. What about the Bakers? They earn a hundred thousand dollars per year, yet they only spend fifty thousand and the rest goes into savings. In this case, holding all things constant, the Bakers have amassed more wealth than the Adams. It can also be safely assumed that preparing for future needs might be a key priority for the Baker family.

Figure 2: Components of Creating Enduring Wealth

From this vantage point, we can see that the way in which money flows through your hands represents the physical manifestation of your closely held intentions. That’s pretty deep, right? Well, the point here is not to wax philosophical but to drive home a crucial point: creating wealth is ultimately rooted in the plan or purpose you lay out for your life. Consequently, you can limit your wealth creation ability when you spend or manage money in a manner that is not in alignment with your life priorities.

Intentional – Definition: done with a plan or purpose

That’s why we believe that the very first step in creating enduring financial wealth begins with being intentional – understanding the vision and purpose you have for your own life. With this understanding in hand, you can then evaluate the ways in which your financial habits align with your internal intentions. Opportunities to create wealth therefore occur when you find reasons to address misalignments between your financial habits and your life purpose. Put differently, you may be more apt to create wealth when your savings and spending plans reflect what matters most to you now and into the future.

The second way you can create wealth is by maximizing your value to others. We believe that you can build enduring wealth by using your innate talents to take your career or business to the next level. That is, adding value, or doing what you are best at for those who need it the most. Gay Hendricks, author of “The Big Leap”, describes this level of performance as the “Zone of Genius”.

And simply put, it’s the kind of work that you do that gets you up early in the morning, excited and in a state of flow. This step matters because it is one important way to increase your potential earning power and thereby build enduring wealth. Indeed, we find that the world tends to reward those individuals who are excellent in the things they do, the unique experiences they provide and how well they show up to help others.

Finally, we create wealth when we accumulate savings and quickly build equity in the assets that we own. Typically, we do this through increasing savings and optimizing net worth. Today, the opportunity to save money has never been easier. It’s true that few households have substantial emergency savings. In some cases, building an emergency savings fund is hard. However, we believe that intention and value maximization can increase nearly anyone’s ability to set aside a portion of their income. Savings is crucial to acquiring productive assets. And these assets can help you grow your wealth and make your money eventually work for you over time.

Equally important to acquiring assets is minimizing unnecessary liabilities. This is crucial because having too much of the wrong kind of debt can leave you in a position that creates wealth for your lender and not for yourself. In creating wealth, your focus should be on using good debt to acquire assets that are expected to hold their value, appreciate, or contribute positively to your future earnings potential.

Creating Wealth in the Current Environment

So how can you create wealth in this challenging economic environment? Well, we recommend that you take time to consider whether your financial priorities are in alignment with your life purpose. The stay-at-home orders have clearly given some of us time to think about what matters most in our lives. It has also forced us to reevaluate the things we can and cannot do without.

Therefore, now may be an opportune time to identify mismatches between your spending and savings habits and your life’s vision and purpose. The easiest way to start is by pulling up your last few bank statements. Then, look for patterns in your spending habits and ask yourself if those patterns align with what’s most important in your life right now. Any misalignment between priorities and purchases may be an opportunity for you to create wealth in your life.

Another thing that you can do to create wealth is to think about how you’re utilizing your talents right now and what you can do to create the most value for your employer or clients. With rising unemployment and business bankruptcies, the current economic environment will undoubtably increase your competition as business leaders and consumers have greater hiring and purchasing power.

Every man, even the most blessed, needs a little more than average luck to survive in this world. –Vance Bourjaily

There is no question that you will need to step up your game if you’re going to compete in the current environment and certainly, take your earnings game to the next level. Therefore, we believe that now is an opportune time to invest in yourself and your business with a goal for increasing your unique value offering. This may include looking at MOOCs or other certification processes to brush up on key skills and firm up your talents if you are a working professional. For business owners, the world has fundamentally changed and so finding ways to pivot your business model to efficiently serve clients in a changed world could help give you a competitive advantage and increase your wealth creation ability.

Figure 3: Building Enduring Wealth Begins with a Process

Finally, another way to create wealth is to put money away in savings and to pay down unproductive debt. If your employer offers a 401(k) or other matching retirement savings accounts, look for ways to max out your contributions. The tax, time and other employer benefits can lead to greater wealth creation (notably as financial asset prices have pulled back from recent highs) than compared to a simple savings account.

Also use this quiet period to evaluate how efficiently the assets you own are either helping or hindering your equity position. More specifically, pull up your credit report and take a look at how much good vs. bad debt are on the books. Before paying off any debt, however, it’s important to note during this time of economic uncertainty that cash and credit can both serve as important financial lifelines. For example, should you experience a loss of income you could tap your savings or line of credit to pay bills or meet immediate financial needs.

Therefore, take the time to evaluate your debt situation carefully. If you have experienced reduced or a loss of income, partner quickly with your lenders to find a way to accommodate your present situation. Otherwise, work on developing a debt payoff plan that produces an appropriate balance between quickly reducing debt while preserving an adequate cash buffer.

Get Started Today

We believe that purpose driven individuals can, over time, build wealth regardless of their current circumstances. This can be done by taking the first step in a disciplined, systematic process to create enduring wealth. The steps that we have outlined are simple. But make no mistake, they are not easy and will require constant discipline and consistency to achieve long-term success. Even so, the sooner you get started the closer you can get to achieving important financial goals and ultimately pursuing your life purpose.

When will they shut the markets?

Global risk assets continued to move lower on Monday, pushing the current selloff well into bear market territory and on pace with a level of volatility not seen since the market crash of 1987. To be sure, the S&P 500 index shed over 12% in another unpredictable day of trading and follows the surprise FOMC meeting on Sunday that slashed the fed funds rate by 100 basis points and saw the restart of its asset purchase programs.

What has become clear to many market participants and investors is that the precautionary measures used to slow the spread of the coronavirus (social distancing) will have broad and deep economic implications that are still not well understood. It can further be argued that today’s market activity reflects a sentiment that policymakers lack the tools to mitigate the economic pain that is likely to arise in the coming months.

Market closures in context

Considering the seeming failure of current policy to support sentiment, some market participants are now asking whether more direct measures can be taken to halt the selloff. More specifically, it has been suggested that financial markets could be shut altogether to help cooler heads prevail.

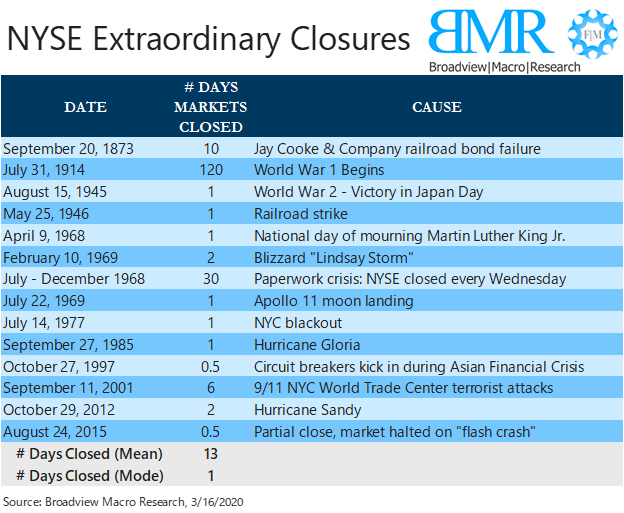

History, nevertheless, has shown that for more than 100 years, closures have sparingly been used to ease market routs. As illustrated in figure 1, there have been a few events over the past century that have led to market closures for more than a day. Some of those events include Hurricane Sandy, the 9/11 terrorist attacks, a Paperwork Crisis in the 60’s and the start of World War 1.

These periods reflect a handful of events that have occurred alongside numerous epidemics, wars, global recessions and financial crises over the same period. Therefore, what the data suggest is that there is little historical precedent for policymakers to outright halt trading in U.S. securities markets for more than a day at a time. What’s more, even during periods of heightened volatility, markets remained opened and largely in normal functioning order.

Figure 1: Days when the New York Stock Exchange was unexpectedly closed

When will they shut the markets?

An argument could be made that closing the markets for even a week or two could preserve household wealth while giving policymakers time to prepare a robust solution set that would help businesses and households navigate what is likely to be a tumultuous economic landscape in the coming months. Nonetheless, what has become clear to us is that the financial markets today act as an important signaling mechanism to policymakers.

For example, indicating a lack of liquidity and other systemically important market dislocations in the case of the Fed, and a lack of confidence in the currently coronavirus policy response to the White House. To shut the markets entirely, therefore, would mean cutting off the feedback mechanism that has helped guide and refine policy as events surrounding the spread of the coronavirus have unfolded. Besides closing the markets, what else can be done to ease market selling pressures?

To be sure, a number of tools exist today that can help prevent negative market sentiment from completely overwhelming asset prices. The New York Stock Exchange, for example, utilizes circuit breakers that halt trading at three different times throughout the trading day: 15 minutes when the S&P 500 index falls 7% and then again after 13% from its previous day’s close; and a complete halt in trading when prices fall more than 20% during the day.

Another tool used by policymakers to stem a market rout is a ban on short selling. This approach was utilized in 2008 to halt speculative selling pressures in financial stocks. And, this approach is being used today in a number of markets outside of the U.S.

In short, after weeks of policy disappointments, investors are eagerly awaiting some catalyst to quickly stop the bleeding and potentially set the stage for a move higher in the markets. While it’s very well possible that market closures could take place in the weeks ahead, their importance as a signaling mechanism suggest such an outcome would be a last resort among a number of other tools.

What this means is that events like today are likely to remain with us until it is evident that the fight against the coronavirus has reached a turning point. Until then, we provide a number of recommendations that households can take to weather this period of heightened market volatility and uncertainty.

Cut costs to increase investment returns

Cutting costs may be one of the most effective ways to increase investment returns this year.

To be sure, some investors have been riding a wave of positive market momentum over the past year as lower central bank policy rates have broadly boosted asset prices and seemingly contributed to easy investment returns.

While monetary policy could be supportive of risk assets in 2020, we expect prices to remain susceptible to quick reversals as markets remain near historic highs.

Market Volatility on the Rise

In fact, this was illustrated last week as news of the coronavirus’s global spread caused a pullback in financial markets.

We believe that last week’s market selloff also serves as an important reminder to investors that the momentum that had contributed to easy market gains are likely to be challenged this year by weaker economic fundamentals, softer earnings and already stretched valuations.

In such an environment, we believe that investors have a better chance of increasing their returns by managing fees and managing risks in their investment portfolios.

Addition by Subtraction

So how can managing fees improve investment returns?

Well, simply put, the higher the fees charged to an investment account, the lower the base from which a portfolio can appreciate.

Or put differently, fees tend to reduce the amount of money that can be put to work and compounded over time. To illustrate this point, we compare the performance of two hypothetical portfolios that have varying fee structures.

For example, two portfolios valued at $250,000, each compounding monthly at a hypothetical annual rate of 5%, but with different fee levels.

Annual product fees in Portfolio 1 average 1.0% and have asset management fees of 1.5%. This compares with annual product and asset management fees each of 0.5% for Portfolio 2.

In aggregate, this is 1.5% less than the first portfolio. So how do they compare?

Performance Divergences

Additionally, a notable divergence in the value of Portfolio 2 over its peer across our 10-year test period.

More specifically, the gains attributed to lower product and management fees added up to over $52,000 over the test period and made for a difference of 16.2% between the two portfolios.

This suggests that not only do lower fees contribute to higher compounded returns, they also reduce the amount of time it takes to achieve financial goals.

To this point, we know that it took 10 years for Portfolio 2 to increase from $250,000 to a value of $372,000.

How much longer would it take Portfolio 1 to achieve this value given the same sort of assumptions in our previous example?

At higher fee levels, Portfolio 1 would need to compound at its current rate and fee structure for six additional years to attain the value that Portfolio 2 had achieved in 10 years.

That’s arriving at a financial goal six years sooner and illustrates the rules of exponential growth applied to savings goals.

Ways to Manage and Reduce Investment Fees

So then what steps can investors take to cut costs and increase investment returns in their portfolios?

Well, we suggest that they begin by looking at how much they’re being charged by the products held in their investment portfolios.

We have found that actively managed mutual funds tend to charge higher fees than passively managed exchange traded funds (ETFs).

This is important because active managers have had a track record of underperforming their benchmarks over the past decade. And from this perspective, investors may be better served by paying for indexing than by paying to time the markets.

Evaluate Third Party Fees

Beyond managing product costs, we recommend that investors take a close look at the fees they are paying to their asset managers.

These fees, typically charged on an asset under management (AUM) basis, vary widely among asset management firms and can rise or fall based on the size of an investment portfolio.

Therefore, we recommend comparing your AUM fees against industry averages, and pay particular attention to the breakpoint levels that may qualify you for a lower fee if your portfolio has appreciated in recent years and your AUM fee remains unchanged.

Is There Value Add?

If the fees you are being charged are above average and your asset management firm cannot clearly articulate the value-add of their higher management fee, then we recommend evaluating potential alternatives.