A Playbook for the Prudent Speculator

Being a prudent speculator is like trying to "act natural", or being "clearly confused", or listening to the "deafening silence".

They're all things that typically don't go together.

Even so, it is possible to become a prudent speculator if you approach it the right way.

And why would you want to be a speculative investor?

Certainly, don't we all know that disciplined investing is the surefire way to achieving and maintaining financial independence?

Well, let's face it: For many of you out there, taking big bets is what's allowed you to achieve the level of success in your career or business that you're living today.

Indeed, you know all too well what it feels like to go all-in on yourself, and to see those efforts rewarded in many multiples of your initial time and financial outlay.

Now, while it's true that you've likely experienced some big professional wins in the past, a common mistake that many high achievers make is to extrapolate expertise in one domain by trying their hand at beating the markets.

And you know, all too often, this move rarely works.

That's because, all it takes is one wrong move in the markets, and you could see your years of hard work wiped out in short order, which is why a disciplined investment strategy works for the long-term.

Even so, if you're going to try your hand at speculative investing, there is a way to have your cake and eat it too, so long as you approach this act from a place of self-knowledge, order, and prudence.

Do You Have What it Takes?

So then, before we go into talking about how to get into speculative investing, the first thing we’ll need evaluate is whether you have what it takes to get started.

And what are we talking about here?

Well, image that you've got an extra $100,000 lying around, and you want to put it to work in the markets.

And by now, you've likely come across various so-called experts promising different ways to turn just a little bit of money into your ticket to financial independence.

So now, the big question here is, "do you have what it takes to put that money on the line?"

The Emotional Journey of Speculative Investing

Well, while the answer to that question might seem like an obvious "yes", given your professional success, the truth is that speculative investing introduces a different kind of emotional situation that you likely haven’t faced in your professional circumstances.

You see, while a disciplined investor puts their money to work by allowing time, a reasonable rate of return from their investments, and the power of compounding to produce gains, speculators tend to take big bets hoping that the price of an asset will rise AND that there will be a buyer at the other side of the table when it's time to sell.

Make no mistake, just as you might feel a rush when a new product takes off or a project succeeds, the potential gains in speculative investing can be exhilarating.

On the other hand, the lows can be profound, as has been the case for many "meme" stock and NFT speculators in recent years, because, unlike a product that can be tweaked or a business strategy that can be adjusted, investments can sometimes plummet with little warning.

So then, the question here is, are you emotionally equipped to handle this high level of volatility and uncertainty?

And why is this question relevant?

Well, as much as you might think you're ready to take speculative bets, it's essential to gauge your emotional resilience and ensure that you're not just chasing the highs associated with following the crowd but are indeed making informed decisions.

The Role of Self-awareness in Investment Decisions

To be sure, in your professional journey, you've likely honed your instincts and now trust them to guide you through complex decisions.

However, in the world of speculative investing, instincts can sometimes be clouded by personal biases. Now, these biases might stem from past experiences, current market trends, or even societal pressures.

And what are we talking about here?

Well, for example, you might be inclined towards a particular tech stock because you're familiar with its products or have an affinity for its CEO.

But you’ve got to ask yourself, “is this fact alone a sound reason to invest?”

The point here is that recognizing such biases is the first step in assessing your readiness for speculative investing.

Then, the next step is to actively challenge your biases to ensure that every investment decision is rooted in research and reason and not just personal preference or emotion.

Indeed, Michael Mauboussin, who is a financial strategist and author known for his work on decision-making, valuation, and behavioral finance, is frequently cited for his insights into the intersection of psychology and finance.

And in his work, he's described this concept known as the "outside view."

And what is the "outside view?"

Well, simply put, holding an outside view means stepping back from the specifics of a situation and instead looking at the broader set of similar situations to make a more informed prediction or decision.

In other words, instead of relying solely on your specific experience or the details of the current problem, you should consider how things generally turned out in comparable situations.

And why is this important?

Well, by taking this approach, you're likely to make more accurate assessments of your investments and avoid common biases that come from being too narrowly focused on the present situation.

The Ever-evolving Landscape of Speculative Investing

Now, another thing to consider as you evaluate whether you've got what it takes to be a speculative investor is that, just like the rapid changes we see in the tech industry, the speculative investment world is also in constant flux.

That's because new trends and opportunities arise, and old ones fade as market dynamics shift. So then, to successfully navigate this everchanging landscape, you need to be constantly in the know.

Now, this doesn't just mean staying up-to-date with the latest market news. Rather, it involves having a deeper understanding of market mechanics, global economic factors, and even behavioral finance.

Here again, it means taking a step back and looking at all of the factors that could influence the price movement, one way or another, of your speculative position.

That's why you'll have to put in the additional time and effort so that every investment decision you make is backed by a robust dataset, ensuring that you're not just reacting to market movements but getting ahead of them.

The Importance of the Right Tools and Resources

Finally, if you're going to engage in speculation, you've got to have the right tools at your disposal. Now, in your professional life, you already know the value of having the right tools, like the latest apps for product development or analytics for market research.

In a similar way, in speculative investing, the right tools can make all the difference. This might mean leveraging advanced analytics software for evaluating market trends or having access to high-quality research from financial experts who can provide insights beyond raw data.

And while having all of these tools at your disposal is a good start, the real magic is in your ability to use them effectively. To be sure, just as you wouldn't rely solely on one data point to make a business decision, you shouldn't base an investment decision on a single piece of analysis before pulling the trigger.

Indeed, as a tech professional or business owner, you likely possess a unique skill set in identifying value opportunities that can be invaluable in speculative investing.

But the real question here is, "do you have what it takes to be a prudent speculator?"

Make no mistake, it's crucial to approach this practice with the same diligence, self-awareness, and thirst for knowledge that has driven your professional success.

And why is this important?

Well, by recognizing and challenging biases, continuously learning, and leveraging the right tools, you can have a better chance at successfully navigating speculative investing without losing your shirt.

Is Your Financial House in Order

Alright, so now that you've done the work to determine whether you have the intestinal fortitude to engage in speculative behavior, the next thing you'll want to do before getting started is to ensure that your financial house is in order.

Now, this might sound like basic work, but listen up, because this step is essential for ensuring that you have the ability to stay in the game.

The Importance of a Financial Foundation

Now, throughout your career, you've likely built products, services, or entire companies from the ground up. So then, you likely understand the importance of a strong foundation.

In a similar way, when it comes to money, before you can explore the volatile world of speculative investing, it's crucial to have a solid financial base in place so you can bounce back from setbacks.

To be sure, as you know, speculative investments are high-risk by nature, and while they offer the potential for high returns, they also come with a greater likelihood of loss.

So then, if your basic financial needs, like emergency savings, debt management, and retirement funding, are not yet secure, then you risk jeopardizing your long-term financial health by engaging in speculative activities.

Indeed, having a solid financial foundation gives you the freedom to take calculated risks without endangering your or your family's overall financial well-being.

Now, this point is essential because, without this foundation, a single bad bet could have disastrous consequences, potentially setting you and your family back years and adding a host of various stresses to your life.

So, then, before you venture into the world of high-risk, high-rewards, make sure you've secured your basic financial needs so that you can weather potential losses without derailing your long-term goals or lifestyle.

Strategic Use of Windfalls

Now, in your professional life, sudden successes like a product going viral, a business deal exceeding expectations, or your company going public are events that bring along big windfalls that you might want to immediately put back to work and double or even triple your windfall.

But before you speculate with such a big gain, it's crucial first to consider your strategic opportunities.

And what do we mean here?

Well, when you experience a sudden windfall, it's tempting to see it as a ticket to the high-risk, high-reward pace of speculative investing. You've got to double your money, right?

Well, before you do, take a pause and consider the bigger picture.

In many ways, a windfall is a chance to solidify your financial position. Indeed, it's an opportunity to address areas in your life you might have previously neglected or as a way to accelerate your financial goals.

This could involve reducing or eliminating debt, which can save you significant interest costs over time. Or, your windfall could help bolster your savings and provide greater financial security and flexibility.

Either way, by addressing these financial needs first, what you're doing is ensuring that any venture into speculative investing is done from a position of prudence and strength, rather than on a hope and a prayer.

The Role of an Emergency Fund in Risk Management

And finally, think about your emergency fund.

Now, you're likely familiar with the importance of backups and redundancies or even understand the value of contingency plans in the business world. Now, these same concepts translate to your financial life, and underscore the importance of having a solid cash reserve in place before you engage in speculative activity.

Now, what we're talking about here isn't just about having money set aside for a rainy day.

Indeed, what we're talking about here is risk management.

And so, why is this important?

Well, can you imagine having all of your liquid cash tied up in a speculative position, and then having a sudden financial need come up in your life, like a healthcare emergency or job loss, and now you can't tap into your money?

That’s why with a robust emergency fund, or cash management strategy, you're free to explore speculative investing with the knowledge that, even if things don't go as planned, you still have a safety net when you need it.

Now, here again, it's crucial to note that this fund should be separate from your speculative investments, and contain enough liquid assets to cover living expenses from between 3 to 9 months, depending on your income and asset levels.

This way, you can ensure that market volatility doesn't directly impact your immediate financial security because, ultimately, it's about having the freedom to take calculated risks, knowing that you've mitigated the impacts from potentially disastrous events.

Become a Risk Manager

Alright, so now that you understand the emotional costs of engaging in speculative behavior and have taken the steps necessary to ensure that your finances are in order, let's take some time to talk about risk management.

Now, while speculative investing is about hoping that an opportunity will provide you with a high return in the future, risk management is a process that ensures you can stay in the game long enough to see that outcome come to pass.

And why is this approach important?

Well, speculative investments, by definition, are more volatile and uncertain than traditional investments. That's because they often involve assets or strategies that have a higher chance of rapid price fluctuation in short periods of time.

And these price moves could be due to various reasons, such as limited historical data, external macro or market factors, or the speculative nature of the asset itself.

Put differently, there are many more unknowns to account for when it comes to speculation. And even in situations where you might know everything about the market you're betting on, there might be outside events that you just can't control.

For example, a new tech startup's stock might be considered speculative because it doesn't have a long track record, and its success might hinge on factors like long-term market adoption of a product.

Or, in the case of real estate speculation, there's no guarantee that, when interest rates continue to creep higher, that the next buyer will want to pay a higher price than their neighbor.

Indeed, while risk management is essential for all forms of investing, its importance is magnified in when it comes to speculative behavior.

Alright, so now that we understand the importance of risk management, how does one actually go about becoming a risk manager?

Understanding Position Sizing

Well, when it comes to becoming a risk manager as it concerns speculative investing, the first thing you'll want to think about is sizing.

Now, from a risk management perspective, market traders (who are often known for their short-term speculative bets) talk about position sizing. And what they're referring to here is the amount of capital you allocate to a specific trade relative to your overall portfolio.

And why is this important?

Well, sizing is crucial because it's a way for you to effectively manage risk.

How so? Well, by determining the right position size, what you're doing is ensuring that even if a trade doesn't go in your favor, the loss won't be devastating to your overall finances.

At it's core, it's about deciding how much to invest in a particular trade or asset, so you can both maximize potential returns and limit potential losses in a manner consistent with your risk tolerance.

Either way, when you consider position sizing, just know that it's more than just a numerical decision. It's a reflection of your understanding of your financial situation and your comfort with risk.

The Imperative of a Clear Exit Strategy

Alright, so now that we've talked about one prudent way to enter a speculative position, let's talk about using a prudent risk management technique and setting your exit strategy.

Now, as you might well already know, venturing into speculative investments without a clear exit strategy is like sailing into stormy seas without a compass. That's because no matter how enticing the potential rewards are, without a plan to navigate the challenges, you risk being swept away and having your ship sunk.

Indeed, an exit strategy outlines the conditions under which you'll sell or otherwise exit your position, either to lock in profits or to your cut losses.

And so, by setting these parameters ahead of time, what you're doing is not leaving your decision to the heat of the moment, where emotions like fear or greed can cloud your judgment.

Ultimately, having an exit strategy allows you to enter speculative positions with a clearer sense of what you're aiming to achieve and what you're willing to risk.

At the same time, it helps you maintain discipline and helps ensure that you'll make decisions based on logic and strategy rather than purely on emotion.

Adopting a Gambler's Mindset

And finally, when it comes to risk management, the last thing you'll want to consider is adopting a gambler's mindset.

And what exactly are we talking about here?

Well, adopting a gambler's mindset can help you make better investment decisions by emphasizing risk management and probabilistic thinking in your approach.

And how's that possible?

Well, that's because in gambling, just like in speculative investing, the outcomes are uncertain, but the odds can often be quantified.

And so, by thinking like a gambler, what you're doing is becoming more attuned to assessing the probabilities of different outcomes, which allows you to better weigh potential risks against potential rewards.

Another reason to adopt this mindset is that gamblers who succeed in the long run know the importance of sticking to a strategy, setting limits on losses, and not chasing after bad bets.

In a similar way, a prudent approach to speculative investing, like knowing when to enter and exit positions and adhering to your risk management plan, can increase your likelihood of success over the long term.

A Playbook for the Prudent Speculator

You know, when it comes down to it, navigating the tumultuous waters of speculative investing is not for the faint of heart.

That’s because it demands a blend of courage, strategy, and self-awareness because, when not approached prudently, it can quickly wipe you out financially.

With that said, by understanding when to push forward, when to hold back, and most importantly, when to exit, you ensure that you're not just participating in the race, but that you have the chance to actually finish it.

In the end, the prudent speculator's voyage is not just about financial gains, it's about growth, learning, and resilience so you can take one step closer to becoming the master of your own financial independence journey.

Don't Keep All Your Eggs in One Basket

All it takes is just one stock to go to the moon, and that's it, you're set for life, right? Well, if it were only that simple. You see, concentrated investing, or keeping your eggs in one basket, seems to work until it doesn't.

Now, make no mistake, concentrated investing isn't all that bad. In fact, notable investor Warren Buffett is known to have made lots of money decade after decade because he takes big bets.

Even so, concentrated investing isn't for everyone.

In fact, if you were to personally ask the Oracle of Omaha for investment advice, he'd likely tell you to buy a diversified basket of stocks that tracks the S&P 500 index and simply hold on to your investments for the long haul!

And why would a sage investor give such seemingly conflicted advice?

Well, that's because Buffett knows that concentrated investing cuts both ways. You see, on the one hand, you could score big under the right circumstances or find yourself desperately holding onto a failing position that wipes away your life savings when fate turns against you.

Indeed, whether you've intentionally placed all your eggs in one basket or are simply trying to figure out what to do with your restricted stock or stock options, then having a plan is essential to preventing unfavorable outcomes.

And this approach starts with checking for concentrated holdings, assessing your risk tolerance to manage such a position, and then understanding how to rebalance away or hedge risk when necessary.

Understanding Concentrated Investment Positions

So then, how can you tell if you're holding on to a concentrated position in your portfolio or otherwise? Well, there are several straightforward methods to figure this out.

The first approach involves evaluating your portfolio's asset allocation. And, as you'll likely recall, your asset allocation refers to the mix of stocks and bonds, US and International holdings you might hold in your investment portfolio.

Now, a portfolio heavily weighted towards a single investment or a given sector or industry is typically indicative of a concentrated position. For example, a general rule of thumb is that if more than 20% of your portfolio is allocated to one stock or sector, then that's likely considered a concentrated investment.

Now, this sort of concentration typically happens when you have restricted stock units (RSUs) that vest, and you haven't decided what to do with your equity, so you just let it sit in your employer's stock plan account. Or, it can happen when you decide to exercise and hold your stock options but don't have a strategy in place for your equity now that you own it.

Now, another method for evaluating whether or not you have a concentrated investment position involves reviewing your exposure to a single asset or sector relative to a benchmark index.

And, what are we talking about here?

Well, let's say your portfolio has 30% invested in the tech sector while your equity benchmark has a 20% weighting in the sector itself. In this situation, you're likely to find yourself with a concentrated position from the perspective of owning more of a sector than you would otherwise like.

And finally, when it comes to determining whether you have a concentrated investment position, you should look at your holdings from the perspective of a worst-case scenario. For example, heading into the Global Financial Crisis, many employees of Wachovia Bank had their retirement savings stored up in company stock, which ultimately led to an unfortunate outcome.

That's because, when the bank failed, the value of their holdings was effectively wiped out, which canceled the retirement plans of many of the bank's former employees. So then, the moral of the story here is that if the failure of a single investment would lead to a significant loss that would severely affect your future financial plans, then you likely have a concentrated position.

Evaluating Your Risk Tolerance for Concentrated Investments

Alright, so now that you understand what it means to have a concentrated investment holding, the big question now is, "do you have what it takes to hold on to that concentrated position for the long-haul?"

And this question is so essential because, as you likely very well know, the road of investing is long and winding, with pitfalls and windfalls alike. It's like a journey where your risk appetite can significantly influence the trajectory and the destination of your investment returns.

And so, what do we mean here by risk tolerance?

Well, to be clear, risk tolerance refers to your ability and willingness to bear losses in exchange for potential gains, especially when a large portion of your net worth is potentially ebbing and flowing with the whims of the markets.

So then, for those of you out there considering or already maintaining concentrated positions, it's essential to have a deep understanding of not only your concentrated holdings, but also of how these investments are affected by market trends, narratives, and principles alike.

And why's that?

Well, it's one thing to know everything about your company stock. But to understand what Mr. Market might also think is a powerful money management skill. Indeed, financial acumen, paired with a disciplined approach, is often what separates successful investors from those who experience significant losses.

To be sure, for those of you out there who have studied market cycles or have simply lived through them, you likely already understand that downturns are inevitable and, more often than not, unpredictable.

Now, if you're a seasoned investor with a high tolerance for risk, then you're likely to remain steadfast in your investment strategy during periods of heightened market volatility because you understand the broader economic and market factors at work and anticipate the longer-term investment play at hand.

With all of that said, holding onto a concentrated position in market ups and downs isn't always as simple as understanding the technical of market or economic factors.

And why's that?

Well, that's because investing can, and often is, an emotional journey. To be sure, when market volatility picks up, and your net worth starts swinging to and fro, it can bring about strong emotional responses, like fear during downturns and euphoria during market rallies.

So then, within the context of investment risk tolerance, your emotional fortitude is a crucial trait to consider in these scenarios. Indeed, in these situations, you have to be able to resist reactive decision-making and stick to your long-term investment plan no matter what's ahead of you.

This approach is especially true when a large portion of your wealth is tied up in your company's stock, and so you'll need to be able to hold on without panicking during periods of negative news or poor earnings performance.

So then, how can you tell if you're fit for holding concentrated investment positions? Well, the first thing you'll want to do is to evaluate your inclination towards maintaining your financial acumen in your given investment holding.

More specifically, you'll need to ask yourself not only whether you're well-versed in the intricacies of a given sector of the market or your company's financials but also whether you have the mental bandwidth and time to stay on top of all the changes in both.

Remember, more often than not, all it takes is one lousy report to send an investment plummeting, so you'll need to stay on top of key developments so you can make wise decisions.

Next, you'll want to assess whether you have the intestinal fortitude to deal with a single large holding and its potential impact on your wealth. More specifically, you'll need to determine whether you can endure periods of market turbulence without making rash decisions. For example, if you're tempted to sell investments or simply move to the sidelines entirely during periods of heightened market volatility, then managing a concentrated position may not be the right fit for you.

And, when it comes to evaluating your risk tolerance within the context of managing a concentrated investment holding, you'll want to consider your broader financial position. More specifically, you'll want to look beyond your investments and evaluate your entire balance sheet.

That's why it's essential to take some time to ask yourself whether you have the ability to absorb potential losses when markets go against your holdings without it impacting your lifestyle or financial goals. And, if you don't have the financial flexibility to weather market downturns, then managing a concentrated position may not be for you.

Strategies for Managing Concentrated Investment Risk

Alright, so now that you understand what a concentrated position looks like, and have evaluated your own risk tolerance, what else can you do if you have concentrated investment risk that you can’t just walk away from, but you need to address in the present?

Well, managing concentrated investment risk often requires a strategic, multi-faceted approach that draws on a range of financial tools and principles to grow your wealth in a mindful way.

Indeed, when it comes to managing a concentrated position, you'll need to consider several factors, from complex things like tax consequences to finding the right trade-off between risk and reward to make prudent choices with your holdings.

Diversification, Asset Allocation and Rebalancing to Manage Risks

And so, how do you go about managing these risks?

Well, to start, let's come back to the first principles of diversification. Indeed, history has shown that, over the long term, you can reduce the overall risk in an investment portfolio when you spread your money across multiple holdings. To be sure, by investing in a broad range of assets, you reduce the risk associated with the poor performance of any one single investment.

And so, how do you achieve this outcome? Well, that's where a solid asset allocation strategy comes into play.

Remember, diversification is achieved by adding different asset classes (like stocks and bonds) to your portfolio, by investing in different sectors or countries, or by utilizing mutual funds or exchange-traded funds (ETFs) that offer instant diversification.

Now, asset allocation, on the other hand, involves determining how much to allocate to these various investments, and more often than not, will be determined by your investment goals, risk preferences, and time horizon.

Alright, with all that said, a common question that typically comes up with respect to diversifying a concentrated position is whether you should sell all of your holdings at once and just be done with it or whether to do so over an extended period of time?

Well, you could sell everything today, but there's a host of factors at play, including tax consequences and the potential for missing out on investment gains to consider as well.

And so, depending on your situation, this is where portfolio rebalancing comes into play.

Now, portfolio rebalancing is a proactive risk mitigation strategy that involves periodically buying or selling assets in your portfolio to maintain your desired asset allocation.

And, in your situation, this could mean reducing a concentrated position by selling some of your investment holdings and then using the proceeds to invest in other underrepresented sectors or asset types.

So then, by taking this approach, what you’re doing is preventing your portfolio from becoming overly concentrated in a single investment while ensuring it aligns with your investment goals and risk tolerance.

Okay, so now that you understand that to reduce concentration risk, you'll need to spread it out across various assets, the next question is, "over what time period?"

Well, if you have a long enough investment horizon, meaning that you don't need to tap into the proceeds from your concentrated position for quite some time, then you might be able to bear the short-term volatility associated with a concentrated position with the expectation of higher returns in the long run as you begin diversifying away this position.

With that said, however, if your investment horizon is short, meaning that you'll need to tap into those investments sooner rather than later for, let's say, a home purchase or for your early retirement, then an extended diversification strategy might be too risky since you likely won't have sufficient time to recover from a potential market downturn when unexpected volatility hits.

Hedging as a Way to Manage Risks

Now, outside of rebalancing as a way to mitigate the risk of a single investment holding, another way to deal with a concentrated position involves hedging.

And what do we mean here?

Well, hedging involves a rather deliberate process of making intricate investment decisions to transfer the risk of adverse price movements in a concentrated asset.

You're still with me, right?

Well, to put this process more simply, to achieve your desired outcome, what you're going to do more often than not is use financial derivatives like options and futures to transfer risk (or hedge against) a potential decline in the value of your concentrated position.

Now, this concept can get pretty technical rather quickly, so let me give you an example to explain here.

Let's assume that you anticipate that the value of your company stock is likely to decline in the months ahead for any number of reasons. Well, in this situation, you could enter into a contract to buy put options, which gives you the right (but not the obligation) to sell a portion of your concentrated position at a locked-in price in the future.

It's like an insurance policy if the value of your concentrated position falls significantly, but it comes with its own set of costs and trade-offs and is helpful in specific situations.

Either way, when it comes to managing a concentrated investment position, you have several options to consider. And so, what's critical to take away here is that if you do decide to hold onto a large position for the long-term, it's essential to find a strategy that works for you and ultimately stay committed to it.

Don't Keep All Your Eggs in One Basket

You know, when it comes down to it, the road to successful investing, especially when it involves concentrated positions, requires a mix of self-awareness, emotional resilience, and strategic execution. Indeed, managing a concentrated investment position is like trying to balance on a high wire where the rewards may be as significant as the risks.

Make no mistake, however, managing a concentrated investment position is often a full-time job, and likely one reason why Warren Buffett encourages individual investors to buy a diversified basket of investments early and often.

Even so, the risks are far from impossible, so long as you're armed with the right tools and strategies, like knowing when you're in a concentrated investment position and appreciating the risks and potential rewards of such positions.

And when it comes to successfully managing your concentrated investment position, understanding your investment horizon, portfolio rebalancing, and hedging strategies can help guide you through the often turbulent seas of investing.

To be sure, with these tools in hand, you'll not only be better equipped to navigate the often stressful but many times rewarding path of investing, you'll also be able to take one step closer to becoming the master of your own financial independence journey.

Train Your Brain, Build Your Fortune: The Power of Mental Rehearsal

When was the last time you mentally rehearsed how you're going to make your financial goals a reality?

Well, whether you're a skeptic or a die-hard proponent of mental rehearsal, you can take a lesson from Craig, who used this approach to fast-track his financial progress toward his essential life goals.

Now, Craig had a decent job as a middle manager in a tech company and was making good money, but not the kind of money where he could call himself rich. Even so, Craig had big dreams. And his goal was to hit a net worth of $10 million before the age of 50.

Sounds like a tall order, right?

Well, this was especially the case given that he was already halfway through his thirties and only had a fraction of that amount saved.

That's when Craig realized that he needed a financial game changer, something totally different from what he was currently doing to reach his lofty goal.

Now, you know how sometimes the craziest ideas come from the most unlikely places? Well, a friend told Craig about a book that he was reading and it was all about the power of mental rehearsal.

More specifically, it described how one's mind often can't tell the difference between the mental world and the physical world, and so developing a practice of mental rehearsal could help him better realize his dreams.

Now, it's essential to note here that this approach wasn't some sort of pie-in-the-sky wishful thinking.

In fact, the book discussed three concrete steps that Craig needed to focus on to realize his dreams, and these included: 1) clarifying his goals, 2) developing a mental rehearsal routine, and 3) overcoming limiting beliefs.

Sounds too good to be true, right?

Well, Craig thought so at first, but he ultimately decided to give it a shot.

And, so, how did he do it?

Well, he started with the basics and got clear about what he wanted and that was: a $10 million net worth by age 50. Then, he wrote his goal down, big and bold, and stuck it to his kitchen wall.

Now, you might wonder, does this approach really help? But think about it this way: seeing that number daily reminded Craig of his dream and kept him motivated regardless of what was going on that day.

Next, Craig got real about his expectations. He knew that just seeing a number wouldn't cut it. That's because he had to make this dream feel as real as possible. So, what did he do?

Well, Craig made a list of what his $10 million goal would look like to him.

For Craig, this meant a house in Hawaii, being able to travel the world, and funding scholarships for underprivileged children. And so, to make the list more real, he attached pictures representing his goals to each one of the items.

Now, stay with me here because this is more than simple daydreaming. That's because the pictures of his goals made the outcome real and tangible to Craig so that he knew exactly what his financial decisions would help him accomplish.

Finally, Craig got serious about his visualization practice, and that's where the magic started to happen. That's because Craig started visualizing his desired outcomes every single day. Now, can you imagine how powerful it would be to be so focused on what you want from your life that you don't lose focus of it regardless of what’s going on in your life?

Well, by doing so, Craig could almost taste the life he was dreaming of, and it drove him to push even harder toward his financial goals.

And, so, what happened?

Well, as he spent more time mentally rehearsing the life he wanted, Craig noticed he was more willing to take more risks.

He asked for that promotion he'd been eyeing, he got serious about his disciplined investment strategy, and even began exploring side hustles to diversify his income. And wouldn't you know it, his net worth started to climb faster than he ever thought was possible.

And here's the kicker: just after his 48th birthday, Craig hit his goal a full two years earlier than planned. And at that point, he was standing in his beachfront home, traveling the world and giving scholarships to needy kids. But the best part? It wasn't just about the money. Craig found that the real magic was in the journey and the incredible power of mental rehearsal that got him there.

The Power of Mental Rehearsal

Now, while Craig's story may sound too good to be true, the fact is that our mindset and how we view our life goals have a lot of sway on whether or not we achieve our desired life goals.

And at this point, it's critical to note here that the kind of visualization we're talking about is not necessarily one associated with the Law of Attraction, or the "Name it and Claim It" prosperity gospel.

To be sure, while the jury is out on whether thinking good thoughts about what we want from life will actually manifest them, what we're talking about here is the proven method of priming our brains for a desired life outcome so that we can better do the work, rather than simply wishing our desires into existence.

Indeed, looking at mental rehearsal from the perspective of sports, psychologist Aidan Moran has been known to say that "sports are played with the body and won in the mind."

And, so what does this mean?

Well, the saying suggests that winning in sports goes beyond mere physical dominance. That's because athletes who can harness the power of their minds by channeling their mental strength, visualizing success, setting goals, and employing effective strategies are more likely to achieve ultimate victory.

And so, what does sports have to do with money? Well, the truth is that top-performing athletes often acknowledge that their opponent isn't the person staring at them from the other side of the court, but rather, it's often the person staring at them from the other side of the mirror.

That's why when it comes to mental rehearsal in performance training, Jim Afremow, the author of "The Champion's Mind," has some valuable insights for upping your game when it comes to mastering your journey to financial independence.

Goal Setting

To start, you need to consider the fact that mental rehearsal plays a vital role in goal setting. And why's that? Well, that's because visualization helps you take obscure or ethereal desires and turn them into something you can touch, taste and smell.

For example, have you ever visualized yourself living in a new house while touring homes with your real estate agent? Or how about imagining your child's experience at a new school during an open house? Could you recall how you felt in those moments?

Well, if you can, then you've likely already experienced the power of visualization when it comes to setting your goals. To be sure, to make the practice successful for you, Afremow suggests frequently visualizing yourself accomplishing your desired outcomes, whether it's winning a competition, attaining personal financial milestones, or achieving financial freedom through your savings goals.

Indeed, by consistently envisioning your success, you enhance your focus, motivation, and belief in your ability to achieve those objectives. To be sure, when engaging in vivid mental imagery or visualization, the brain can activate similar neural networks and pathways as it does during actual experiences. This activation can lead to physiological and psychological responses similar to those experienced in real-life situations.

What's more, visualizing yourself in your desired financial state will not only help you set goals, it can also boost your motivation and focus your energy towards achieving those highly desired life goals. Now, these outcomes typically happen because you're using the power of your imagination to generate positive emotions and feelings of accomplishment to get a taste of what achieving that goal might feel like.

Again, this mental rehearsal process will help keep you motivated during challenging times, help you remain focused on your objectives, help you avoid distractions, and, most importantly, help you avoid making impulsive financial decisions that could derail your financial independence journey.

Develop a Mental Rehearsal Practice

Alright, so once you have a clear idea of which objectives you want to pursue, the next step in using visualization to fast-track your financial goals is to mentally rehearse your desired life outcomes.

And, so, how do you do this?

Well, start by visualizing the satisfaction and joy you'll experience once you achieve your goals. As in Craig's case, this could include tapping into the feeling of cruising up the driveway of your house in Hawaii, experiencing the awe and wonder of visiting a new country or seeing the joy in a child's face when they realize that you've helped them pay for college.

Now, naturally, on the surface, constantly thinking about your desired financial goals might seem a little like daydreaming.

But, the truth is that mental rehearsal is much more than daydreaming because it's a way to prime your brain for the outcome that you want to achieve. In fact, mental rehearsal is an approach used by the soccer great Pele, Olympic swimmer Michael Phelps, Muhammad Ali, Tiger Woods, and many other well-known athletes to prime their minds for the outcomes they desire before actually doing the work.

Now, when it comes to applying this concept to your finances, you'll likely want to make the outcome more than just about achieving your life goals but also about the actions you need to take to achieve those outcomes. For example, take the time to visualize what your typical week or month looks like when it comes to how you're handling your finances.

For example, imagine your ideal financial situation and visualize specific milestones, such as paying off debts, saving a targeted amount of money, or acquiring assets that can produce income later on in life. And by creating a clear mental image of what you need to do to hit your life goals, you can develop a long-term roadmap along with short-term actionable steps that you can touch, taste and feel to reach them more efficiently.

To be sure, can you vividly imagine how you would feel checking your bank statements to see how your spending and savings are aligned with your overall life goals? And how do you want to feel knowing that your savings balances are growing consistently or that they're solid enough to cover your lifestyle goals until you die, thanks to the choices that you're currently making?

That's the power of mental rehearsal and visualization.

Again, it's essential to note here that we're not talking about wishful thinking. To be sure, the field of neuroscience has a lot to say about how neurons that fire together wire together, and that's a discussion for another time. But when it comes down to it, what you should know is that mental rehearsal helps improve connections in your brain that link effort to outcome.

Remember, the mind is, for the most part, a lazy member of our physiological system. It prefers habits and novelty and tends to focus on things you're good at or generally enjoy doing. So then, from this perspective, mental rehearsal allows you to prime your brain and body for future habits and desired outcomes by pairing images and scenarios of success with a physiological outcome that links potential achievement with positive emotions.

Indeed, through visualization, you can mentally rehearse the daily choices you'll need to make with your money with utmost clarity. And by creating detailed mental images, you are effectively training your brain to simulate the actual physical experience associated with that work.

Overcome Limiting Beliefs

The last point we'll cover when it comes to mental rehearsal is how it's a great way to overcome limiting money beliefs and how it can help you build confidence in your financial abilities. Now, if you're having trouble being consistent with doing the work to hit your financial goals, like sticking to your budget, it may have something to do with your belief in your ability to achieve these goals.

And that's where mental rehearsal can help out.

That's because visualization allows you to rehearse those behaviors necessary to achieve your life goals while helping you identify blindspots and potential derailers to create potential solutions.

And, so, how do you go about doing this work?

Well, to start, identify any negative beliefs or doubts you may have about your financial potential and replace them with empowering imagery. This could include imagining yourself finally overcoming those bad habits or derailers that have been holding you back, and what it would feel like to finally attain your measure of financial success.

To be sure, this visualization practice will not only help you challenge your limiting beliefs but also help you develop a confident mindset, enabling you to take bold actions such as investing, starting a business, or negotiating for better financial outcomes in your life.

Use Mental Rehearsal to Fast-track Your Financial Goals

Now, if you're still not sure where to begin with all this mental rehearsal work, consider this: what would your dream life look like, and how would achieving your financial goals bring this vision to life? Can you feel the excitement bubbling within as you step into your dream home, or experience the pride coursing through your veins as you fund your child's college education without any debt?

That's the power of mental rehearsal kicking in.

Now, drawing on Craig's story, reflect on the impact of visualization in your life. Picture the confidence you would feel asking for a deserved promotion or the thrill of discovering a new investment opportunity that aligns perfectly with your financial goals. At the same time, imagine the satisfaction of seeing your savings grow steadily or the relief in realizing that you're financially prepared for your post-employment years no matter what comes at you.

To be sure, your dreams aren't as far-fetched or unachievable as you might think. In fact, it's quite the contrary. Your financial dreams are within your grasp, and it starts with mentally rehearsing how your life will look when you achieve that outcome.

Indeed, just like in sports, the battlefield is in your mind, and victory starts there. And by frequently visualizing your desired financial state, you'll find an increase in your focus, motivation, and belief in your ability to reach your goals, but most importantly, you'll be taking one step closer to becoming the master of your own financial independence journey.

Why Linear Thinking Won't Get You Exponential Results

Have you ever wondered why some people seem to achieve enormous growth, whether in mastering new skills or building wealth, while others appear stuck in a state of static complacency?

Exponential growth might just be the hidden answer.

Now, before you write off this seemingly abstract concept, let's take a moment to think about this concept in simpler terms.

To do this, picture yourself standing at the foot of a towering mountain of opportunity. Now, the peak is barely visible because it's shrouded in the clouds of potential.

Even so, this mountain represents the concept of exponential growth, a potent yet often misunderstood principle that has the power to rapidly accelerate your life and financial goals.

So, where does exponential growth fit in?

Well, you can think of exponential growth as a small snowball at the top of the mountain. As it begins to roll down the mountain, it gathers more snow, growing in size and speed.

Now, imagine this snowball is your initial $10,000 savings investment. Initially, it might not seem substantial, but once you give it a bit of time and the right conditions, you'll likely be looking at an avalanche of progress and prosperity.

So, what can you do to tap into this power to fast-track your progress to financial independence?

Well, the first step is to get out of the trap of thinking about your money in a linear fashion. That's because once you truly grasp how exponential growth works, you can then take advantage of two critical financial concepts to 1) save less to reach your financial independence goals and 2) have more money set aside each month to enjoy your life instead of worrying about the future.

Now, outside of winning the lottery or coming into a sizeable windfall, there's no shortcut on your path to financial independence. It's a little like running a marathon. It requires patience, consistency, and the willingness to start even if the benefits aren't immediately apparent.

But you'll likely have the motivation you need once you have a firm grasp of how small actions today can influence your big financial goals tomorrow.

Beyond a Linear Mindset: Exponential Growth

Now, to fully grasp the concept of exponential growth you need to understand its essence.

And what is exponential growth?

Well, exponential growth or decay refers to a constant rate of increase or decrease. And one of the simplest ways to think about this phenomenon is compound interest.

How so?

Well, consider the growth of $10,000.

If you put that money to work today, earning a 5% growth rate, at the end of the first year, your investment will have grown to $10,500. In the second year, the 5% growth rate is not only applied to your initial $10,000 but also to the $500 you earned in interest, resulting in a total of $11,025. This pattern of accumulation continues, becoming increasingly dramatic over time.

In fact, if you took $10,000, invested it at a 5% growth rate and left it alone for 50 years, you’d have nearly $115,000!

So then, it’s this pattern of growth starting off small and slow, and then rapidly rising that characterizes exponential growth.

Now, it’s important to note that exponential growth is not confined to the realm of abstract concepts. That’s because it manifests in various facets of everyday life. A prime example is the evolution of technology, which adheres to the principle of exponential growth, as demonstrated by Moore's Law. According to this law, the number of transistors on a microchip doubles approximately every two years, propelling technological progress forward at an astonishing pace.

Nature, too, abounds with instances of exponential growth. Bacterial growth serves as a classic example, where under optimal conditions, a single bacterial cell can divide and multiply, giving rise to two, then four, eight, sixteen, and so forth, in an astonishingly short period.

Roadblocks to Exponential Thinking

Now, despite its ubiquity, many individuals struggle to comprehend the true nature of exponential growth.

And why’s that?

Linear Thinking

Well, to start, humans naturally tend to think linearly, perceiving relationships as straightforward and proportional. For instance, if I walk for an hour, I cover a certain distance, right?

And if I double the duration to two hours, I cover twice that distance. In this situation, linear thinking hinges on constant rates.

Even so, however, exponential growth operates differently, involving a rate of change that intensifies over time. And because this rate of change evolves over time, this non-linear nature can be counterintuitive and challenging for many to grasp.

Time Frame

Another reason many individuals struggle with understanding exponential growth is because it often starts slowly, only to suddenly surge forward.

And it’s this initial period of gradual growth that can lull people into a false sense of security, causing them to underestimate the profound long-term effects of the process.

And where is this applicable?

Well, we typically see this pattern of thinking observed in the context of epidemics, when reported infections are low, but transmission ability is high or financial investments, when an individual is just starting out their savings journey.

Mathematical Complexity

And when it comes to truly getting a grasp of exponential growth, some individuals may find the mathematical concept behind process simply daunting. That’s because it demands an understanding of multiplication and powers, which are concepts that may be unfamiliar or intimidating to some people.

Even so, by delving into the depths of exponential growth and unraveling its intricacies, we can unlock its immense potential. Indeed, from fostering personal growth to harnessing financial gains, the mastery of this concept opens doors to a world of possibilities.

Exponential Growth in Personal Development

Now, while exponential growth has the potential to transform your finances, it also has an incredible capacity to propel your personal growth. That's because daily habits, even small positive changes, when consistently practiced, can yield substantial progress over time.

It's like the compounding effect of interest. Let's say that you're interested in learning a new language and give it just 15 minutes each day worth of practice. While this approach may seem small and insignificant at first, over the span of a year, this modest commitment amounts to over 90 hours of practice which is an impressive investment that can foster considerable advancement.

Now, this concept extends beyond learning a new language. Indeed, learning new skills, enhancing your physical well-being, and nurturing personal relationships can all experience exponential growth through the accumulation of tiny, consistent adjustments. That's because every minuscule change, when compounded over time, possesses the potential to catalyze remarkable personal development.

Use Exponential Growth to Calculate Your Nest Egg Need

Alright, so now that you understand how essential exponential growth is for your personal and financial life, let's take a deeper dive and talk about how we can apply this concept from a financial perspective to determine how much you need to save to meet your essential life goals.

Now, when considering complex savings goals, like saving for post-employment living expenses, it's tempting to settle on a round number, say $1 million, as your financial independence savings target.

But how can you be certain this figure will support your lifestyle for the remainder of your life? That's where the concept of exponential growth enters the picture to help you calculate your financial independence number.

And how do we calculate this figure?

Well, to calculate how much you need to save for retirement or your post-employment living expenses, you must consider your savings journey in two distinct phases.

Two Phases for Financial Independence

The first phase, referred to as the accumulation phase, starts today and ends when you attain your definition of financial independence. This could be 10, 20, 30 years, or even more in the future.

The second phase, known as the distribution phase, covers the period between when you achieve financial independence and your eventual passing. In simpler terms, it represents the duration for which you plan to live off your savings.

Now, the big question you're probably asking is, "how much should I save today to meet my financial independence goals?" The answer is, "It depends." That's because, before you can accurately determine how much to save during your accumulation phase, you must understand how much you intend to spend during your distribution phase.

Consider this analogy. If you're planning a cross-country road trip, how much fuel will you need? The answer depends on a few factors, such as your vehicle's fuel efficiency and your chosen route. Are you planning a direct journey or do you anticipate detours to scenic spots?

The same principle applies to your journey toward financial independence. Just as you'd calculate your road trip's distance and fuel consumption, you need to estimate your retirement spending and income's saving potential to figure out how much to save today.

And how do you go about doing this work?

Well, let's illustrate these concepts with an example. Suppose your goal is to save enough money to supplement your lifestyle by $40,000 per year in today's dollars, and you plan to maintain this lifestyle throughout a 30-year retirement. Your goal is to save annually for the next 25 years before reaching your financial independence date.

So, how much do you need to save?

Exponential Growth of Inflation

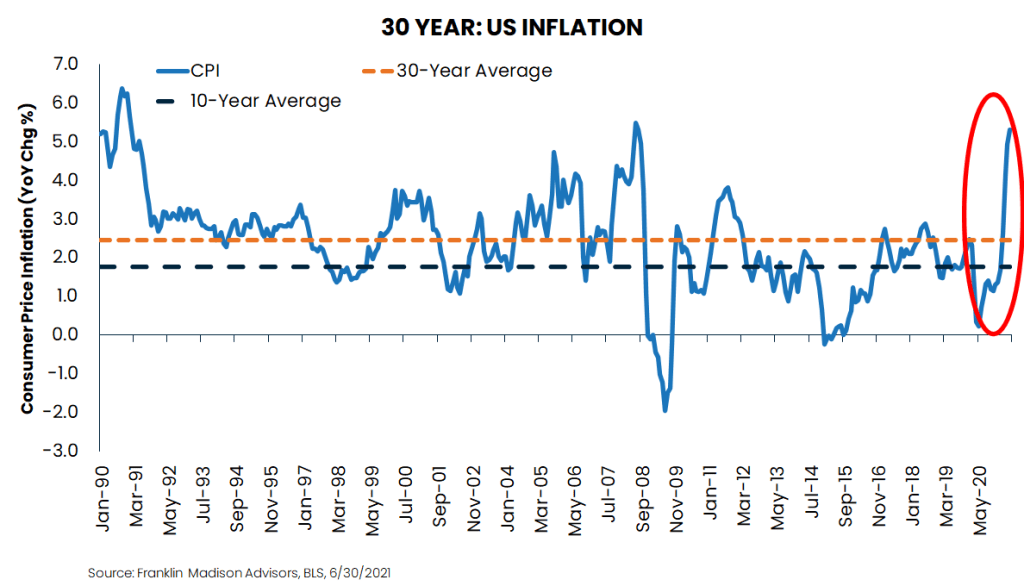

Well, while it might be tempting to simply multiply $40,000 by 30 years to calculate your retirement nest egg need, you'd likely end up with a linear result that could jeopardize your financial independence goals. That's because, as you’ll recall from our discussion earlier, exponential growth works both ways.

Not only can it boost your savings, exponential growth in expenses, like inflation, can eat away at your future purchasing power. Indeed, history has shown that inflation tends to increase at an exponential rate as price growth compounds year over year.

Indeed, when we incorporate inflation into our hypothetical lifestyle expenses projection, assuming an average inflation rate of 3%, you'd need to spend $83,751 in 25 years to buy the same goods and services you can today with $40,000. What's more, that $40,000 lifestyle expense today will likely rise to over $200,000 by the time you pass away in 55 years.

So, given an annual inflation assumption of 3%, how much money would you need to have saved by your financial independence date in 25 years? Well, when taking inflation into consideration, you'd likely need just over $4.1 million to cover your rising lifestyle expenses!

Exponential Growth of Investment Returns

Now, before you get worried about the large savings figure, you can take comfort in knowing that you can use exponential growth during your distribution years to lower your overall savings need. That's because while inflation is an exponential factor that works against your savings, a compounding investment return can help mitigate your overall savings need.

How does this work?

Let's suppose that you decide to keep your savings invested throughout retirement, and your investments grow at about 5.5% annually. You might be thinking, "Isn't that small investment return barely offsetting my average inflation rate?"

Well, at first glance, it might seem that way, but let's examine how the numbers pan out over the long term.

Now, you'll recall that without any investment return and just saving enough to cover 30 years' worth of inflation-adjusted expenses, you'd need to have saved around $4.1 million. However, if your investments grow 5.5% per year in your post-employment years with inflation at 3%, you'd likely only need to save around $1.7 million, which is less than half the original figure!

Why?

Well, that modest growth rate applied to your retirement savings acts as a buffer or a cushion, that offers growth of your savings even as you're drawing down on the principal balance. And when your money has the opportunity to grow at a modest rate over a long period of time, it means that you need less money to start at retirement to fund your living goals.

From this perspective, you can think of exponential growth of your retirement savings like a fruitful orchard. Just as a tree steadily grows and bears fruits year after year, your savings, growing at a modest rate over time, acts as a resilient tree that continues to produce new fruit even as you pluck some of the ripe ones. And in our case, the growth of your savings serves as a cushion, ensuring that your retirement nest egg keeps expanding even as you withdraw from it.

Now, it’s crucial to bear in mind that these calculations are based on estimates and averages, and actual inflation rates and investment returns can vary. Therefore, it's vital to regularly review your financial plan, make necessary adjustments, and seek personalized advice from a financial planner who can guide you based on your specific situation and goals.

Use Exponential Growth to Figure Out Your Savings Need

Now, when it comes to planning for your financial independence, it's crucial to have a clear understanding of how much you need to save to achieve your goals. In our previous discussion, we explored the concept of exponential growth and its role in helping you understand your future savings needs. Now, let's shift our focus to determining the actual amount you should save today to meet your future financial goals.

And, as you’ll recall, we can break down your journey toward financial independence into two phases: the accumulation phase and the distribution phase. And, given our hypothetical example earlier, we've already discussed how to calculate your savings need for when you need it in the future.

So, now, let's tackle the fundamental question: "How much do I need to set aside today to reach my post-employment savings goal?"

Pitfalls of Linear Thinking to Fund Savings Goals

Well, to illustrate how to calculate your current savings plan, we'll continue with the same example and draw upon the concept of exponential growth. And you’ll recall that, assuming an inflation rate of 3% during your retirement and an average investment return of 5.5% over 30 years, you’d likely need to save $1.7 million over the next 25 years.

So far, so good, right?

Now, if we divide $1.7 million by 25, we find that you would need to set aside approximately $68,000 annually to reach your goal, assuming you're starting with no savings. It's understandable if this figure seems daunting, considering the various financial obligations and priorities you have in your life right now.

The Power of Exponential Growth and Your Savings

However, there's a way to use the power of exponential growth to your advantage, that can help reduce this annual savings need. And by doing so, you'll have more flexibility to enjoy your present while increasing your chances of achieving your financial independence goals.

So, how can you achieve this outcome?

Let's consider a scenario where you invest your annual savings and let it grow at an average rate of 6.5% until you need it in 25 years. Using a time value of money calculation, we find that you would only need to set aside around $29,000 annually to reach your savings target of $1.7 million, which is a lot lower than our earlier linear estimate of $68,000!

And how is this possible?

While your principal contributions would amount to approximately $750,000 at this rate, the power of compounding would contribute to the growth of your investments to the tune of around $950,000 by the end of 25 years.

The key takeaway here is that the power of compounding not only increases the amount of money you can save but, more importantly, it reduces the necessary savings over a given period of time. This enables you to strike a balance between enjoying your life today and preparing for a financially secure future.

Regular Review and Personalized Advice

Now, it's crucial to note that financial planning involves various uncertainties and variables. Factors like changing economic conditions, personal circumstances, and investment performance can impact your savings goals. Therefore, it's crucial to regularly review your plan and seek personalized advice to ensure it remains aligned with your evolving needs.

Either way, by understanding the concept of exponential growth and leveraging the power of compounding, you can gain a clearer perspective on your savings journey and work towards achieving your financial independence with confidence. Remember, financial planning is a dynamic process, and by staying informed and proactive, you can make the most of your financial resources both now and in the future.

Harnessing the Potential of Exponential Growth

Alright, so now that you have a grasp of the concept of exponential growth and its implications lets talk about strategies for leveraging its power to expedite our life and savings goals.

Laying the Foundations Early

Now, one of the most crucial things you can do to take advantage of exponential growth is to start early. To be sure, starting early is a golden rule when it comes to leveraging exponential growth.

It’s like setting out on an adventure, and the sooner you embark, the more time you have to explore and experience later on down the road. So, whether it's honing a new skill, establishing a fitness routine, or investing your hard-earned money, the trick is to dive in as early as possible.

You might not notice the benefits immediately, much like planting a seed doesn't yield a tree overnight. Yet, with the passage of time, these small steps start to pile up, multiply and just like that, you've made some significant strides towards your goals.

Consistency: Your Trusted Companion

Another crucial consideration when it comes to exponential growth is to think of consistency as your reliable travel buddy on this journey.

That’s because regular contributions, whether it's to your knowledge bank, health goals, or investment portfolio, lay the groundwork for considerable growth over time.

Indeed, just like a disciplined athlete achieves personal bests when they practice, your consistent efforts towards learning new skills or saving for the future can usher in an era of significant personal and financial growth.

Small Steps, Giant Leaps and Patience

A final point to consider when leveraging exponential growth to your advantage is to take small steps, giant leaps and leverage patience.

And what are we talking about here?

Well, let's consider the humble power of incremental improvements. Imagine improving just 1% each day for a year, that would lead to a whopping 37 times improvement due to the magical compounding effect! So, from this perspective, don't underestimate the impact of even the smallest positive changes because every bit counts.

And when you’re applying the concepts of exponential growth, it’s essential to remember to be patient! That’s because exponential growth is a bit like watching a pot boil, it may seem slow at first, but before you know it, it's bubbling away.

In a similar way, patience plays an instrumental role in this process. It's all about appreciating that growth isn't always instantly visible, but when compounding kicks in, it takes off like a rocket!

Linear Thinking Won't Get You Exponential Results

Make no mistake, having a firm grasp of the power of exponential growth can be a game-changer for your personal and financial journey. And by making a shift away from linear thinking and embracing exponential thinking, you can likely achieve incredible results over time.

It's just like a small snowball rolling down a mountain. Your initial investments and daily habits can gather momentum and lead to an avalanche of progress and prosperity. So then, the key is to start today and remain consistent in your efforts because even the smallest positive changes can have a significant impact when compounded over time.

Remember, when it comes to using exponential growth to calculate your savings needs, you'll need to be mindful of both the accumulation and distribution phases of your financial journey. And by using the principles of exponential growth and the power of compounding, you can determine how much you need to save today to meet your future goals.

In the end, you have the power to tap into the awe-inspiring force of exponential growth and to unlock limitless personal and financial changes in your life. So, get after it with confidence, and watch as your small steps transform into giant leaps on your path to mastering your financial independence journey.

Asset Location vs. Asset Allocation: The Winning Formula for Wealth

Have you ever wondered why your savings aren't growing even though you're contributing to an investment account? It may be because you haven't set your investment strategy.

That's what happened to Mariam.

Now, Mariam knew the importance of investing and that her bank account wouldn't cut it when it came to satisfying her long-term financial independence goals. But, like many uninitiated investors, Mariam misunderstood the concept of investing and believed that simply opening an investment account would guarantee high returns.

Sound familiar?

Well, in Mariam's case, she opened a Roth IRA, because that's what she's heard she's supposed to do. In fact, Mariam believed that her Roth IRA was all she needed, not realizing that the account itself was just a vessel for her investment strategy.

And how many of us have ever made that same mistake?

Well, everything changed when Mariam discovered that her Roth IRA wasn't performing as well as she had hoped. And it turns out that her account was all sitting in cash and not actually invested. That's when she realized that she had focused too much on the account itself and not enough on the underlying investment strategy.

So, what did she do?

Well, frustrated with her situation, Mariam took the time to track down resources and professional assistance that helped her discover that focusing solely on her Roth IRA may not have been a solid strategy from the start.

To be sure, Mariam discovered that the key to a solid investment strategy begins with putting her savings not only in suitable buckets, but also in choosing an ideal mix of stocks, bonds, and other assets that align with her near- and long-term life and savings goals.

Now, with a renewed sense of confidence, Mariam implemented her new investment strategy. And it was at that point that she knew she was making informed decisions and using all available savings vehicles, like her brokerage, employer retirement plan, and her IRA in an orderly manner.

So, what's the moral of the story here? Well, to build real wealth, it's essential to not just put money in an investment account, but also to understand the difference between asset location (that's the types of investment accounts) and asset allocation (or your investment strategy) and use them effectively within your overall financial plan.

Understand Your Investment Account Options

Indeed, understanding the difference between asset location and asset allocation is just as crucial as knowing which type of account to stash your cash in and how to make that money work for you once it's saved.

Account Asset Location

So, what is asset location? Well, this approach refers to placing your savings contributions into different savings buckets, or types of accounts based on their tax treatment. Now, these accounts might include taxable accounts, tax-deferred accounts (like a 401k and traditional IRA), and tax-free accounts (like a Roth IRA).

And, what's the whole point of asset location? Well, the point of asset location is to maximize the tax efficiency of your investment portfolio. And while you're likely aware of some of the immediate tax benefits of putting your money into these various accounts, the real focus should be on how your investments will be taxed when the money comes. That's because not being aware of your tax location could mean having less money to cover your living expenses when you need it the most.

So then, how does asset allocation differ from asset location? Well, asset allocation is the art of spreading your investments across various asset classes like stocks, bonds, cash, and other investments. The goal here is to build a balanced and diversified portfolio that vibes with your risk tolerance, time horizon, and financial goals.

Indeed, a well-diversified portfolio keeps your overall risk in check since your investments are spread across different assets, which react differently to market ups and downs. Now, before we talk about how to invest your savings, let's discuss the various savings buckets, or account types, and what they're typically used for.

Brokerage Accounts

Let's begin by taking a look at brokerage accounts. Now, a brokerage account is the most basic type of investment account that you'd open at a firm like Schwab, Fidelity, or Vanguard. And you can think of a brokerage account as your flexible platform for chasing various financial goals, like growing your wealth, saving for retirement, or funding major life expenses.

These accounts let you buy and sell various assets, like stocks, bonds, mutual funds, and ETFs, which promotes portfolio diversification and long-term growth.

Now, unlike retirement accounts such as 401ks and IRAs, brokerage accounts don't offer tax-deferral benefits. This means that you fund these accounts with after-tax dollars, and you'll likely have to pay taxes on your capital gains, dividends, and interest in the year they are earned. Now, it's possible to reduce these tax burdens through various investment strategies, but we'll save that discussion for a future report.

For now, what's essential to note here, though, is that while brokerage accounts don't have the same tax perks as other tax-advantaged accounts, they still allow you to put your savings to work for the long-term while giving you the flexibility to pull your money out penalty-free anytime you need it.

Retirement Accounts (401k, 403b, IRA)

Now, retirement accounts like 401ks, 403bs, and IRAs are tailor-made to help you save for your golden years. Now, when it comes to retirement accounts available through your employer, what’s essential to note is that in most cases these account types allow you to make contributions on a pre-tax basis, which means that you're putting more money to work before Uncle Sam gets his share of your earnings.

And in the case of Traditional IRAs, after-tax contributions can be tax deductible in certain circumstances. Either way, money in these accounts grow tax-free until you’re ready to take the money out.

Sounds good so far, right? What's the catch, you ask?

Well, the catch is that you typically can't access these accounts penalty-free until age 59 1/2, and when you do, you'll likely be taxed at ordinary income tax rates. Even so, because more money is going in on a pre-tax basis in the early years as far as your contributions are concerned, the more money you're putting to work and allowing to compound over time.

Now, one caveat to note here when it comes to retirement accounts is the Roth IRA. A Roth IRA is an account that you typically set up with a brokerage firm (or Roth 401k if your employer offers it), and is funded with after-tax dollars. While you generally can't access the funds penalty-free until age 59 1/2, the benefit of a Roth IRA is that the money grows tax free, and you typically pay no tax when you take the money out.

Education Savings Accounts (529 Plans)

Now, education savings accounts, like 529 Plans, are another kind of savings bucket designed to help families save for future education expenses. And they're useful because these accounts offer a tax-advantaged way to invest and grow funds for educational purposes.

That's because earnings in a 529 Plan grow tax-free, and withdrawals for qualified education expenses don't get hit with federal income tax. What's more, some states offer tax deductions for 529 Plan contributions, which make them a compelling savings vehicle in certain situations.

Health Savings Accounts (HSAs)

And finally, health savings accounts (or HSAs) allow you to save and pay for qualified medical expenses while offering some nice tax advantages.