Inflation: An Insidious Threat Your Financial Independence Journey

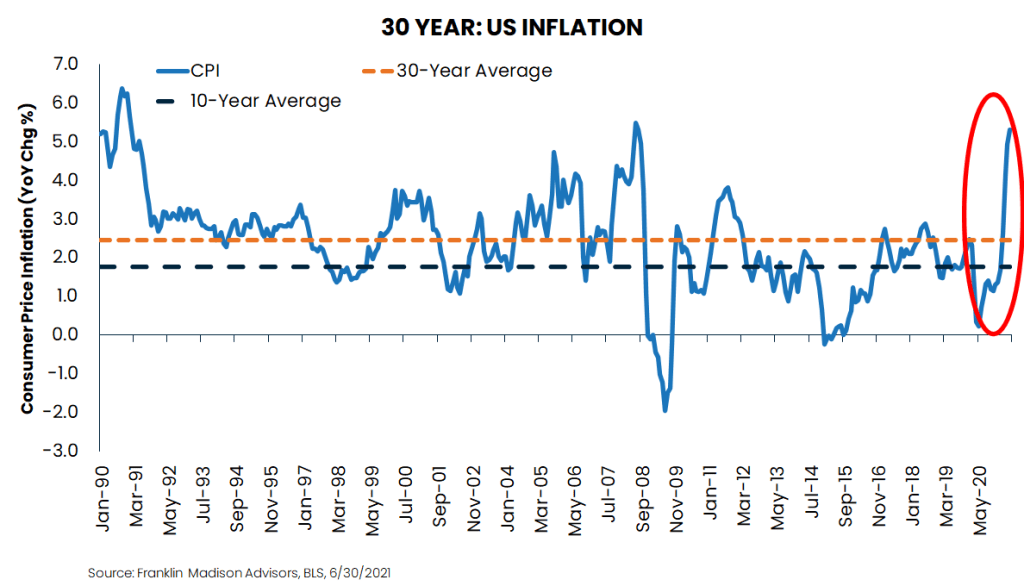

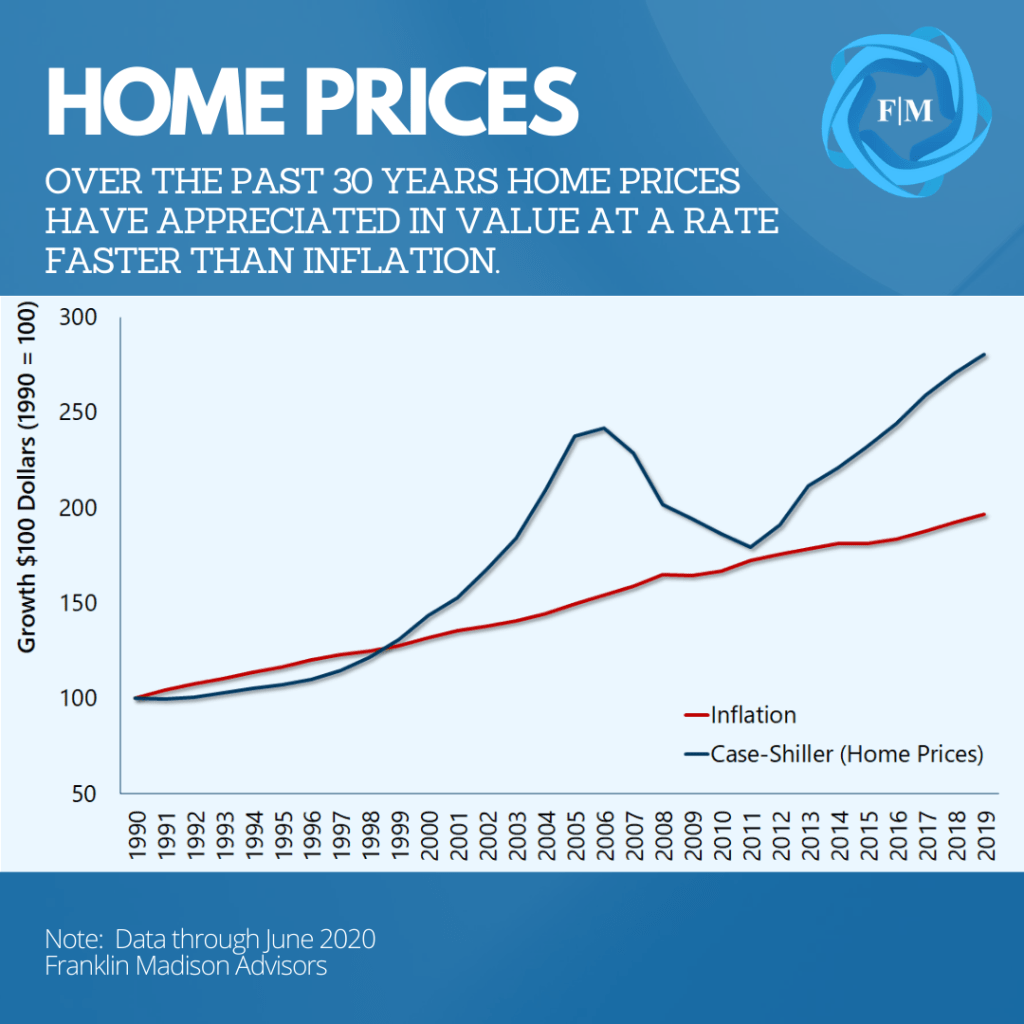

Financial independence plans are coming under threat from inflation's insidious rise. According to a government report, prices paid for everyday household items rose by 4.9% in May compared to a year earlier. Even when stripping out volatile components, like food and energy, prices were up 3.9% over the same period – the fastest in over three decades.

While these statistics might seem arbitrary at face value, it's essential to understand the context. For example, the latest inflation figure comes in stark contrast to its 2.5% average over the past 30 years. Indeed, the reality of rising prices is evident whether you're filling up the gas tank, shopping at the grocery store, getting ready to buy your next house, or decorating the home you just purchased.

Permanent or Transitory?

Today, many economists, market watchers, and to be sure, households look at the recent price spikes and ask, "Is today’s higher inflation a fluke or new reality?"

A Case for Lower Near-Term Inflation

Certainly, there's a case to be made that inflation is likely to ease in the coming months. How so? Well, households globally today are spending faster than expected, and global distributors are struggling to keep up with demand. Last year's global economic shutdown and ongoing COVID restrictions have created gridlock in the global supply chain. These bottlenecks have made it harder to ship certain goods from international producers to US warehouses, crimping supply on store shelves and naturally putting upward pressure on prices.

For example, according to one report, container ships responding to the post-COVID consumer spending surge found it challenging throughout June to unload their goods at the Port of Los Angeles (one of the busiest ports in North America). In fact, some ships were anchored in a holding pattern for five days outside of the port, given logistics backlogs. In normal circumstances, foreign cargo ships typically don't have to wait to enter the port and can unload their cargoes right away.

Why is this story significant? Well, what makes shipping into the Port of LA important is that these freighters carry household goods and manufacturing components that affect all aspects of the US economy. Now, this logistics gridlock story is not unique to the Port of LA as it's happening in ports all around the world. And these delivery slowdowns have led to a global supply chain crunch, giving way to higher near-term prices for a host of goods.

From this perspective, it could be argued that today's high inflation is only transitory. Once global logistics issues are fully resolved, near-term inflationary pressures might ease as the supply of goods finally meet the rising pressure from pent-up global consumer demand.

A Case for Higher Longer-Term Inflation

Now, while there's a case to be made for lower near-term inflation, it's also worth considering the potential factors that might lead to higher prices in the decades ahead. Indeed, the Federal Reserve has flooded the economy with $5 trillion from the start of last year. Combine this excess money printing with trillions in government stimulus, and there's a potential that excess household savings (coupled with a higher propensity to consume) might cause inflation to run hot for longer than what many economists anticipate.

To this point, researchers at Bank of America recently published a report noting that over the next four years, US inflation could average between 2-4%. If we look back through history, this estimate compares to average annual price gains, of around 3% over the past 100 years, 2% in the 2010s, and 1% in 2020. According to this report, analysts believe that a key contributor to faster inflation likely could come from Americans sitting on trillions of dollars in unspent savings. As COVID restrictions ease and the economy rebounds, this savings could make its way back into the economy in the form of higher consumption and wage growth.

Another long-term inflationary point to consider is China's evolving relationship with the rest of the world. Chinese factories have, until recently, been low-cost producers of the world's goods, arguably contributing to low inflation in developed market economies for the past two decades.

Nevertheless, geopolitical tensions remain elevated between Western nations (notably the US) and China. What's more, Beijing is pushing policies that would enable China's economy to become more domestically reliant while expanding its political influence globally. From this perspective, it's very well possible to see higher-priced goods here at home should Beijing's policy changes reduce China's export of deflation to the rest of the world.

Why Does Inflation Matter?

So, what's the big deal if prices rise faster than expected? In other words, what role might higher inflation play in your ability to navigate your financial independence journey? Well, at face value, persistently elevated inflation could result in your spending down retirement savings at a faster than expected rate. How so? Well, a simple example here might help.

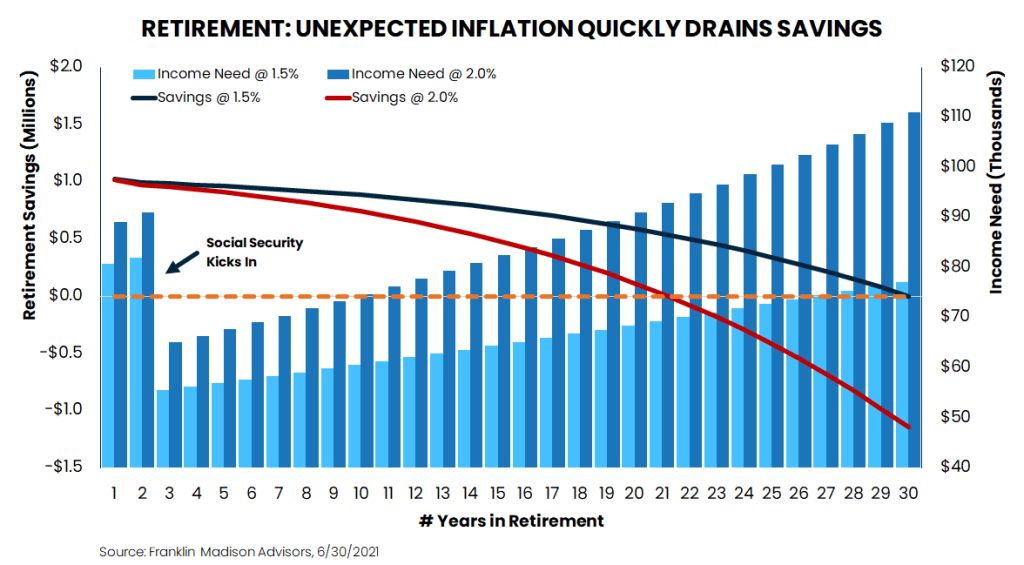

Let's suppose that you're planning to retire in 20 years with a lifestyle need of $60,000 per year in today’s dollars. Assuming a modest Social Security benefit, you'll likely need to have saved about $1 million to cover inflation-adjusted living expenses over the next 30 years. This figure is based on a widely held industry assumption that inflation may average 1.5% over the long term.

So, what happens when the 1.5% average inflation assumption used in calculating your $1 million savings turns out to be 2.0%? Holding our earlier assumptions constant, a half-percentage point cost of living increase could lead to a savings shortfall of over $1 million throughout retirement. Put differently, $1 million of retirement savings might only cover about 20 years of living expenses should inflation average 2% instead of 1.5% in your original plan.

Inflation and Your Financial Independence Journey

So, are higher prices here to stay? And more importantly, is the 1.5% inflation assumption used by many in the financial industry overly optimistic? Well, some argue that once supply constraints ease and the low base effects pass, inflation could return to the low levels we've seen in the last 10-year.

The truth is that in the period following the Global Financial Crisis, economists have had a terrible track record of predicting inflation. Certainly, easing logistics bottlenecks likely will reduce inflationary pressures somewhat in the coming months, but long-term risks remain.

To be sure, many structural changes are afoot, which argue against a return to "normal" inflation. The effects of Trade War tensions and China's growing push for global political influence likely will have some impact on the country's willingness to remain a low-cost producer of the world's goods. Add to this the uncertainty surrounding trillions of dollars in US fiscal and monetary stimulus, and it's likely that inflation will not fall back to 1% over the long-term.

Make no mistake; inflation is so insidious that even a seemingly minor change can have an outsized impact on your achieving (and maintaining) financial independence. When not adequately accounted for, it will slowly and subtly erode the purchasing power of your retirement savings.

Certainly, while inflation is likely to ease in the near term, it would nevertheless be prudent to evaluate whether your long-term inflation assumptions are overly optimistic and if they are, to make adjustments accordingly. Doing otherwise may just end up cutting short your journey to financial independence.

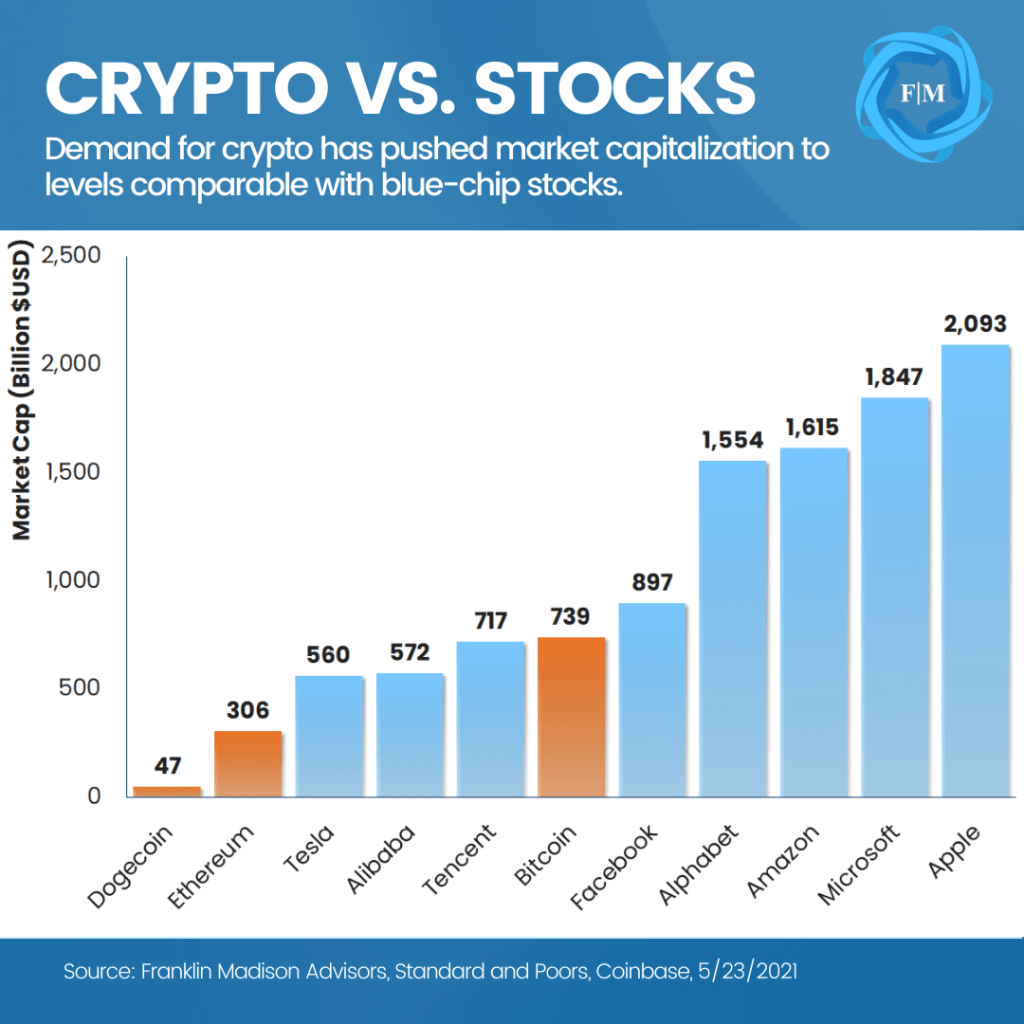

Does Crypto Belong in Your Retirement Portfolio?

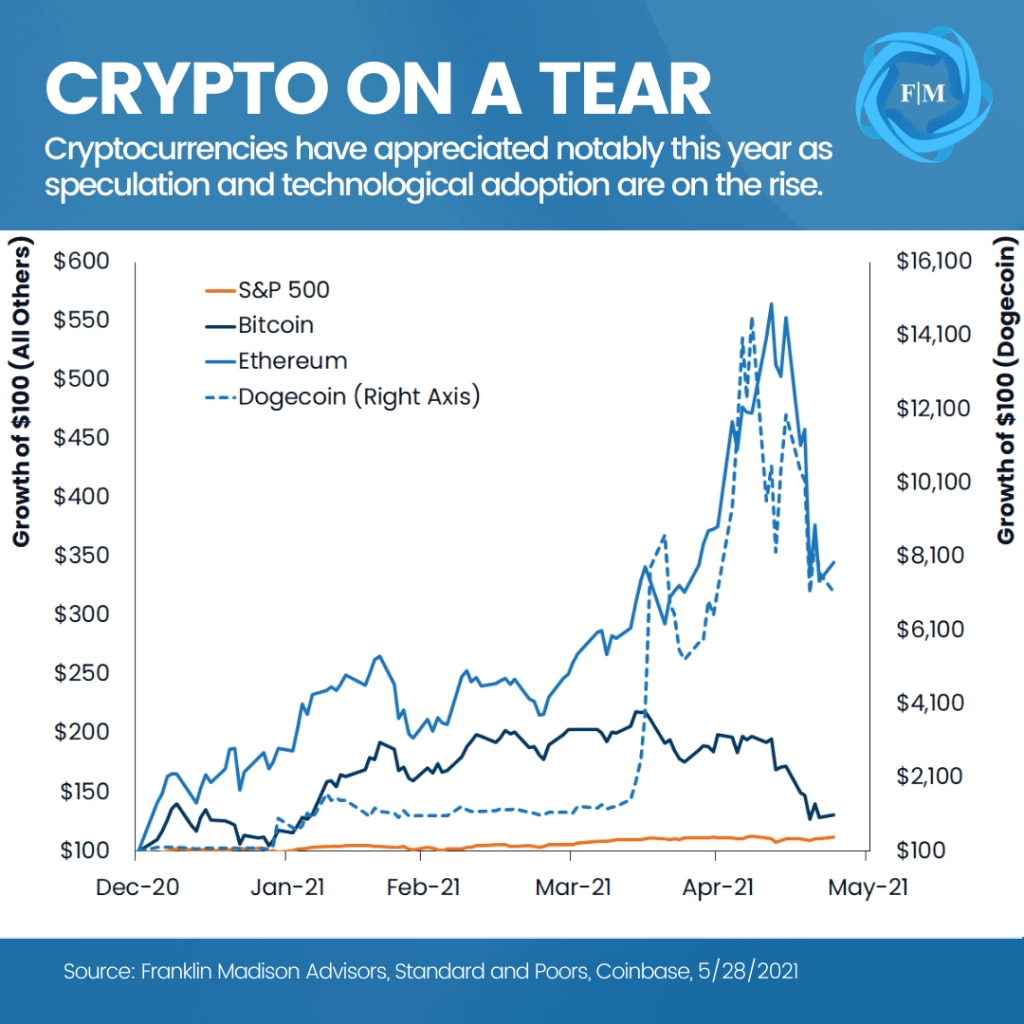

Life changing money. That's what happened to John Ratcliff. In 2013 the software developer from Colorado purchased 150 Bitcoin. Today, his $15,000 bet is worth millions as the price of cryptocurrencies (crypto) skyrocketed. Another individual who also came into life-changing money this year is Vitalik Buterin. The 27-year-old college dropout and co-founder of Ethereum is now the world's youngest crypto billionaire as Ether went from $130 in 2020 to over $4,000 in 2021.

Stories like Ratcliff's and Buterin's have led to a crush of demand for the popular new asset class. To be sure, rapid price appreciation in crypto over the past year has prompted heightened media attention and arguably is fueling frenzied behavior among some market participants in tokens like Bitcoin, Ethereum, and even Dogecoin for fear of missing out.

But what exactly are cryptocurrencies? And more importantly, do they belong in a retirement portfolio?

What is crypto?

Merriam-Webster defines crypto as "any form of currency that only exists digitally, that usually has no central issuing or regulating authority but instead uses a decentralized system to record transactions and manage the issuance of new units, and that relies on cryptography to prevent counterfeiting and fraudulent transactions." In other words, crypto is created by a collection of independent actors rather than a central government.

So, where does crypto come from?Well, in many cases, these virtual currencies are produced out of thin air by computers that solve cryptographic puzzles. This activity called is called mining. As more puzzles are solved, the more crypto an individual or collective earns as payment for their mining efforts on various blockchain networks.

Another essential point to understand about crypto is that they're unregulated and don't flow through traditional financial channels like the euro, yen, or U.S. dollar. Rather than being stored in a bank, these virtual assets are stored in digital wallets, currently limiting their use in the broader economy.

Is crypto just a lot of hype?

For many disciplined investors, it's hard not to see what's happening in the crypto space and ask whether another Tulip Mania, South Sea Bubble, Dot-Com Frenzy, or Housing Bubble is in the works. Even so, various indicators suggest this technology is more than a passing fad as blockchain technologies are increasingly seeing mainstream adoption in both public and private sector applications.

For example, the Federal Reserve announced in May that the central bank will publish a paper exploring the potential for its own Central Bank Digital Currency (CBDC). Meanwhile, the People's Bank of China is already testing a digital Yuan.

From the private sector perspective, Visa, Mastercard, Paypal, and Apple have recently expressed their intent to actively participate in the virtual currency space. So, it's safe to say that crypto, for the time being, may be more than simply a flash in the pan.

What's the outlook for cryptocurrencies?

While blockchain networks have been around for over a decade, the technology remains in its infancy. Even so, a key potential use for blockchain technology and crypto is in Decentralized Finance (DeFi). More specifically, crypto could be used to transform the way large transactions are settled between institutions and private individuals.

For example, a traditional high-dollar international wire can take several days to complete. Blockchain technologies supporting digital currency transfers, however, could offer a means to settle large transactions in minutes instead of days and at a substantially lower cost. For payment processors, this is big news and a key reason why Visa and Mastercard have entered the space.

To be sure, blockchain adoption might also find its way into widespread merchant payment processing services. Whereas banks and other intermediaries often charge around 2% to settle merchant card transactions, blockchain technologies might promote greater payment processing competition, leading to lower fees and higher profits for small and large businesses alike.

Does crypto belong in your retirement portfolio?

There's a case to be made for the blockchain technology but does crypto belong in your retirement portfolio? While rapidly appreciating tokens have led to life changing money for some individuals, we believe that disciplined investors should view crypto as a long-term speculative investment that could go to zero for two key reasons.

First, the jury is still out on long-term token adoption. While Bitcoin remains the largest network, Ethereum is gaining mainstream popularity. That’s because Ethereum’s network is about to dramatically lower its energy usage, increase processing capacity and potentially end Bitcoin’s blockchain dominance. Either way, leadership in the space is likely to change a number of times in the coming years, making it that much harder to pick a winning cryptocurrency in the short-term.

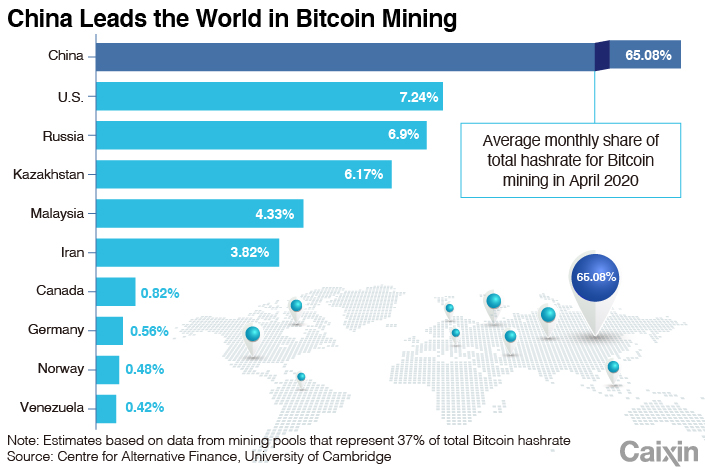

Regulatory risk is another reason we view crypto as speculative near-term investments. Recently, the Chinese government enacted measures to curb bitcoin mining. This is important because the country accounts for 65% of the world’s Bitcoin mining hashrate. Similarly in May, U.S. policymakers hinted at the need for more crypto regulation. What’s more, central banks globally are in the process of developing their own digital currencies.

To be sure, crypto token investor should be comfortable with the idea of their investments going to zero. Nevertheless, blockchain likely will play a transformative role in finance, presenting a long-term thematic investment opportunity. From this perspective, we view a diversified allocation to traditional companies that facilitate blockchain adoption as an attractive component of a retirement portfolio.

From Six Figures and Broke to Financial Independence Master

When Frank began practicing bankruptcy law, his average client earned between $8 to $9 an hour. A decade later, his clients increasingly earn six-figure incomes. And Dave and Beth were one of Frank's high-earning clients. At one point, the couple had amassed over $100,000 in credit card debt and were tapping their home equity line of credit to pay for a lifestyle their family simply couldn't afford. Dave's six-figure annual bonus was enough to cover a large part of his outstanding credit card balances, but the debt kept piling up, and they had little choice but to seek out Frank's services. But it wasn't always like this for the couple.

Dave and Beth had once lived a frugal lifestyle. Beth came from a working-class family that valued making a dollar go as far as it could. One night, Dave offered to take Beth out to Olive Garden for dinner, but Beth insisted that she stop by the grocery store and prepare a meal for the couple instead. Early on in their relationship, Beth drove a car she received in high school and refused to buy herself a new one until Dave paid off his car. So, what changed over the years? Well, their financial issues began shortly after Dave was transferred to Florida after receiving a big promotion.

Following their move, the couple purchased a four-bedroom home in an affluent, gated Orlando community. Their purchase was more significant than anticipated, yet their house was one of the smallest in the neighborhood. Soon enough, Dave and Beth found themselves surrounded by highly educated, ambitious professionals and entrepreneurs who lived in larger homes, drove nicer cars, were members of the local country club, and sent their kids to private schools.

The couple's desire to fit into their new community, coupled with an anticipation of rising future income, led to a spending spiral to keep up with their neighbors. Dave had hoped that by using his annually granted stock options and bonuses, he would maintain his family's spending habits. However, after a short while, Dave and Beth realized that their consumption habits weren't sustainable, and the couple found themselves stuck in a cycle of spending that led them to Frank's office.

When Financial Literacy isn't Enough

By the time Dave and Beth met with their attorney, Frank, they barely made the minimum payments on their credit cards and were facing the courts taking control of their family's spending. How did this educated, high-earning couple go from humble means and sound financial stewardship to earning six figures and broke?

A lack of financial literacy wasn't necessarily their problem. Recall that Beth had once embodied the value of stretching a dollar and minimizing unnecessary debt. Even so, she and Dave ended up charging $2,000 per month on clothes their family didn't need.

Dave and Beth's situation is an extreme example of a condition plaguing many high-earning households. You might know someone in a similar situation or maybe have found yourself in the same spot. Either way, this phenomenon is not new. Call it keeping up with the Joneses or hedonic adaptation. Addressing such challenges related to money management and wealth-building has been covered in volumes of books and seminars and are the frequent talking points of tv and radio financial gurus.

Quick fixes like cutting back on that five-dollar cup of coffee, avoiding debt altogether, or putting your savings on autopilot are often cited, no-brainer remedies to such spend-thrift behavior. Create a budget, develop a financial plan, and stick to it. Simple, right?

Well, many individuals, especially those well-versed in essential financial literacy topics, continue to find their financial wellbeing rising from a level of financial security up to financial freedom and then back down again to living paycheck to paycheck. Something must be missing from the equation for Dave and Beth and millions of other families just like theirs struggling to take back control of their financial situation. But what's missing?

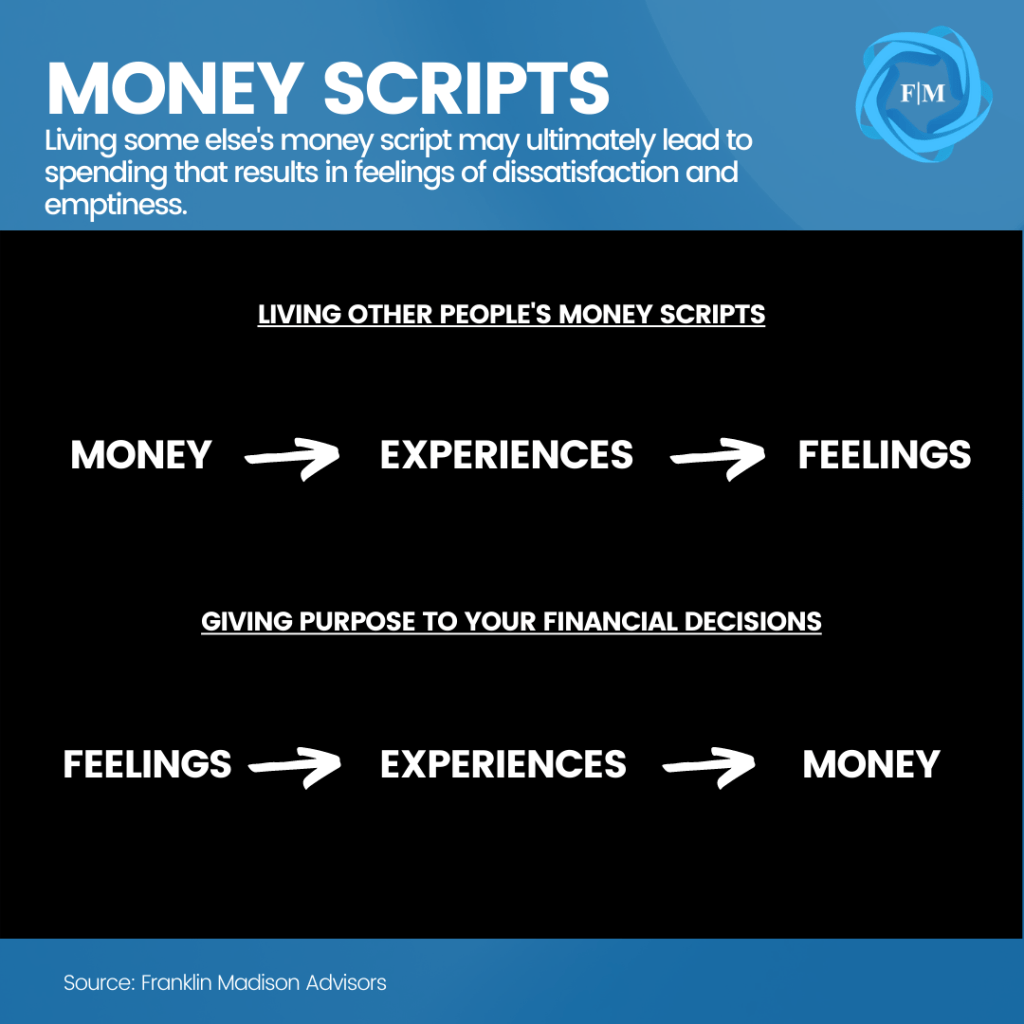

Living Some Else's Money Script

Often, individuals trying to break free of this vicious financial cycle spend too much time trying to master their money without having a conscious understanding of whose life they're living and how they want their money to make them feel. Indeed, many individuals unconsciously make financial decisions based on money scripts handed down to them by family, friends, or society at large.

Go to college, get a high-paying job, buy a house, earn more money, join this club, upgrade your car, live in this neighborhood (not that one) and then buy a bigger house. These outcomes, or milestones, represent expectations about how we might feel once specific experiences materialize due to our earning and spending decisions.

In Dave and Beth's case, their financial choices were dictated by their newly chosen community members' money scripts. Their seemingly fleeting unconscious desire for feelings of love, peace, aliveness, and freedom led them to pour money down a black hole because they were living someone else's money script.

There's nothing wrong with wanting to live in a big house, driving a nice car, or joining a prestigious club. More to the point, what Dave and Beth's story illustrates is that trying to feel emotionally satisfied by chasing someone else's expectations can prove to be a goal as elusive as trying to rid yourself of the pernicious gopher encountered by Bill Murray's character in Caddyshack.

Feelings Give Purpose to Your Financial Decisions

Here again, Dave and Beth's issues didn't revolve around knowing the proper money management techniques. Instead, their challenges came down to finding the right set of experiences that satiated deeply held emotional cravings. By this point, you're probably asking yourself, "why are we talking about feelings?" Well, the truth is that nearly every financial decision we make is based on a desire to satisfy a complex set of feelings.

There's no doubt that money can make you feel secure when you use it to pay your rent or mortgage. You likely feel comfortable when you stock your refrigerator and pantry with groceries. Buying your friends a round of drinks at the local pub likely makes you feel accepted. At its core, money represents stored potential to elicit certain feelings through the experiences afforded.

In the book "Your Money or Your Life," author Joe Dominguez writes how "money… is life energy, or something you trade the hours of your life for… and …is like a mirror that allows [you] to see [yourself]." This truth about money is why many high-earning individuals struggle with growing their wealth for the long-term. Why?

When financial problems crop up, these individuals are focused on trying to solve the wrong set of problems. Often, the solution to their money problems focuses on learning about new money management techniques. On the contrary, in Dave and Beth's situation, developing a conscious awareness of the kinds of experiences that align with their desired feelings, then crafting a money script around those set of experiences could have helped them master their money.

The reality is that few individuals are inclined to think or talk about their feelings. It's easier to look at what's worked for other individuals and try to emulate their lives. While some successful people may appear content from the outside, they may be struggling with as much financial discontentment as Dave and Beth. That's why it's essential to start with the end in mind: understand how you want your money to make you feel and identify the kinds of experiences that will get you there. So how do you determine the fitting types of experiences to pursue?

Which Experiences Matter Most to You?

The first step is understanding what matters most in your life. To this end, George Kinder built his life planning program around answering three vital questions:

- If you had enough money to take care of your needs now and into the future, how would you live your life?

- If you had five years to live, what would you do with your time?

- If you only had 24 hours to live, what did you miss in life, who did you not get to be, what did you not get to do?

Answering questions like these have helped many individuals identify vital life experiences worth pursuing, and at the same time, gain control over their finances and live more rewarding lives.

Why does this approach work? Science has shown that intrinsically oriented goals, or those that come from within, are more likely to be achieved and produce long-lasting emotional satisfaction. On the other hand, extrinsic pursuits focus on goals like getting a promotion, buying a new car, or losing ten pounds. Studies have shown that while such reward-pursuing behavior can produce results in the near-term, their value tends to diminish over time and turns up the speed on the hedonic treadmill.

Indeed, pursuing experiences with the intent of eliciting a specific set of feelings that matter most to you is, by its very nature, an intrinsic goal. So, how can you make an experiences-oriented approach applicable to your life? Spending time with Kinder's three questions is one way to start. What's more helpful, however, is developing a framework in which to put your thoughts, actions, and choices into a broader context. One approach to consider is becoming the master of your financial independence journey.

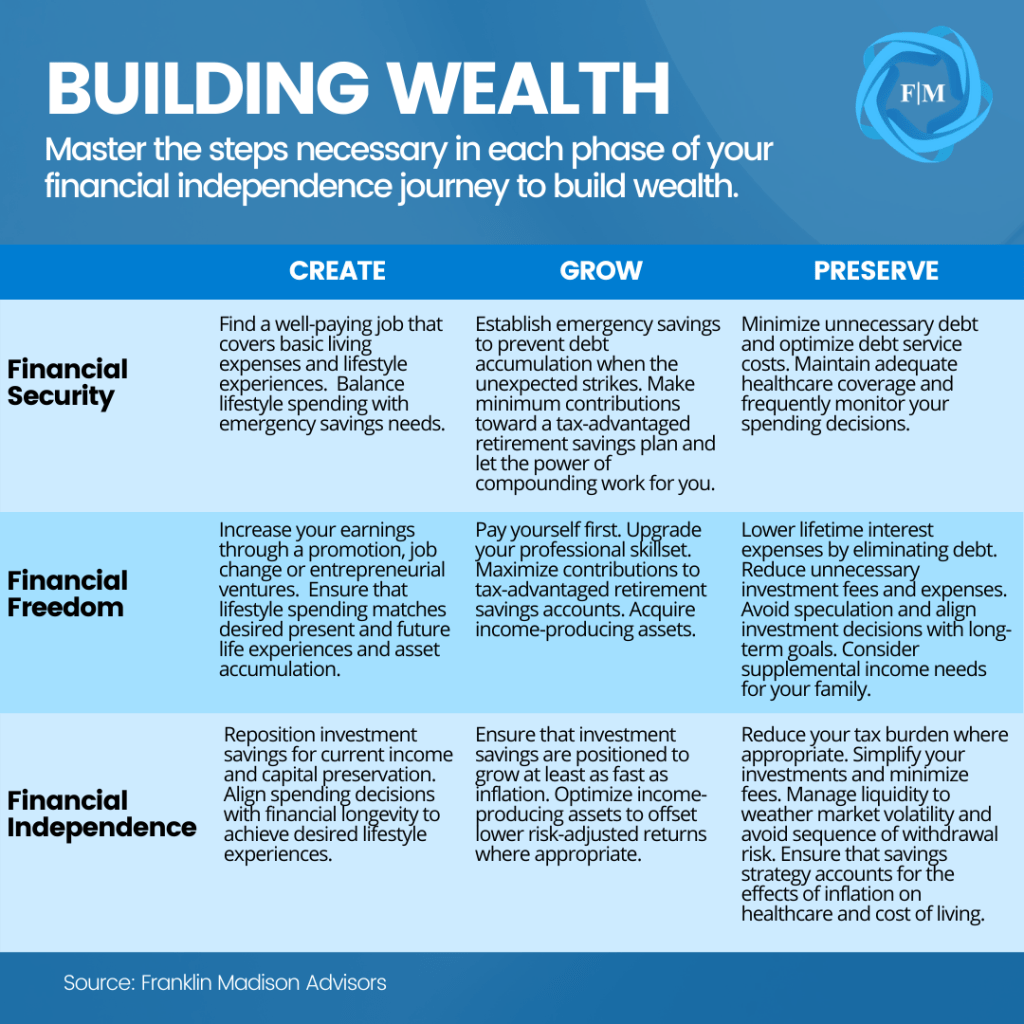

Become the Master of Your Financial Independence Journey

In the simplest terms, financial independence represents a state of financial wellbeing where you have enough money to pursue experiences that are of utmost value to you. Unless you're already retired or anticipating a financial windfall, becoming financially independent requires a daily discipline of creating, growing, and preserving financial wealth.

Considering the journey itself, the path to mastery (financial independence) forces you to think outside of the constraints of the money scripts presented to you by other people. Indeed, pursuing those experiences that satisfy feelings core your value system can activate higher levels of intrinsic motivation and potentially reduce the yo-yo effect of unconscious spending.

What's more, the journey itself becomes transformative. For example, each step in the wealth-building process (creating, growing, and preserving wealth) serves an explicit role in helping you move toward financial independence.

Each of these steps requires you to learn disciplines that enable you to build wealth for the long-term. And because the knowledge your gaining serves an intrinsically defined purpose, its application likely will have a more profound impact on your achieving financial independence than learning money management techniques simply for the sake of knowledge.

When it comes down to it, many individuals see their financial choices as discrete win/lose outcomes. And more often than not, people play the game of life simply not to lose: settling for comfort rather than striving for a goal they may fail. They're looking for quick fixes, temporary relief to get them through their day.

While this approach may work initially, a deliberate lack of understanding of what intrinsically motivates you might leave you feeling stuck in a perpetual cycle of earning and spending more but making little headway towards long-term financial goals.

Whether you’re earning six figures and broke like Dave and Beth, or simply trying to take control of your finances, learning a new financial management technique, determining your "retirement number" or some material outcome may not be the approach you need. What might suit your situation better is reframing your relationship with money, rewriting your money scripts and becoming the master of your financial independence journey.

Indeed, endeavoring to master your financial independence journey sets the stage for defining the kinds of essential experiences in your life. Better yet, the journey might ultimately transform you into a fitter financial steward with less stress than you had imagined.

6 Ways to Stay Financially Fit in 2021

The new year is here and your resolutions are probably well underway. While you have may set goals to get more physically fit, it is also important to consider your financial fitness going into the new year as well. If your finances are not where you want them to be, or maybe they are in need of a little tune-up, consider the six tips below to get your financial health fit this year as well.

1. Trim the Fat

One of the first steps toward a more healthy financial future is spending less. If you take the time to take a hard look at your budget, odds are you can find some excess that you can easily trim off without feeling the pinch. Start with spending items such as clothing, groceries, and entertainment and see if smart shopping or more date nights at home can help free up some extra money each month. Next, look at your utility bills and find ways that can reduce them. Start with your non-essentials such as cable and phone. Do you really need the extra movie channels and data? When was the last time you shopped around to price compare? Finally, discipline yourself to follow good energy saving tips to reduce the overall cost of your energy bills.

2. Tone Up Your Debt

Odds are the holidays have increased your credit card bills. Don't let that debt snowball higher than it needs to with accruing interest. Start with your highest interest rate card and set a larger payment in your budget to begin lessening that total. Once it is paid off, use that same payment to start tackling your next high-interest debt ball and so on. A critical thing to remember is that when paying only your minimum payment, it will take you ten years and a significant amount of interest to pay off your card so always pay more than the minimum if you are looking to pay off debt.

3. Whip Your Credit Into Shape

Your credit score can affect you in many aspects of your financial life. Whether you are looking to buy a house, a car, or to take out a loan to start a business, your credit score will be used to determine how much interest you will pay and how likely you are to even get your funds. Unfortunately, many people neglect their score until they need it, and at that point, it can be difficult to improve in enough time. Keep your credit card balance far from the limits, be sure to make payments on time, and monitor your score for negative marks.

4. Load Up of Savings

Once you have trimmed the fat off your budget, you will want to put some of that into savings. One thing to start saving for immediately is an emergency fund. Surprise repairs, medical bills, and layoffs can damage your financial health if you are not prepared for them. Having this fund available for these times can lessen the blow and help you stay on top of your bills, so you don't fall behind.

5. Put Retirement Savings in Your Routine

Saving for retirement is critical so that you can retire. Many people do not save enough for their retirement or wait so long that it stresses their budget to meet their goals. Make it a point this year to focus on your retirement goals and find extra funds that you can put into your account so that it has the necessary time to grow as it should. Find out if your company matches contributions and if so try to put in as close to how much they will match as possible.

6. Start a New Investing Routine

Investing is the quickest way to grow your wealth, but many people are afraid to enter the world of investing because they are afraid of losing their money. Others are under the misconception that you have to invest a lot of money when the truth is you can begin your investment journey with as little as $100. Start small so you can get the hang of it and if you have more money to invest consider meeting with a financial advisor who can help you pick a mix of funds based on your risk tolerance.

Get your finances healthy this year and set attainable goals to help you grow your wealth and get started on a secure financial future.

Five Ways to Free Up Cash When You Have Little in the Bank

Cash is king. During times of uncertainty, having cash on hand can make the difference between financial stability and the host of issues that come with insolvency. That's why regardless of your current financial situation, having cash options can not only help keep you solvent, they can also ensure that you stay on track right toward your crucial life goals. So, what can you do to raise cash if you have little money in the bank?

Without a doubt, there are many tools and techniques that you can utilize to generate cash and boost your emergency reserves. Today, we'll outline five practices that you can apply to come up with a few hundred or a few thousands of dollars when you need it. It's crucial to note that each option has its own set of benefits and tradeoffs. Even so, keeping track of the resources available to you before you need them can help ensure that your finances stay on track, no matter what issues life throws your way.

#1 Cut Back on Non-Essential Household Spending

One of the quickest ways to come up with cash is to cut back on non-essential household spending. For many, this suggestion seems like a no-brainer. Yet more often than not, this challenging yet straightforward approach is often one of the most underutilized ways to raise extra cash. Certainly, finding a tradeoff between consuming today and saving for tomorrow is hard. So, where should you begin?

To start, you'll want to get a sense of trends in your monthly household spending. To do this, begin by pulling up two months of your latest bank statements. Then go through your expenses, item by item, categorizing each as either essential (like housing, utilities, personal care) or non-essential (like takeout, app subscriptions, shopping). Then, tally up the non-essential items and decide what you can do without for a season while you come up with needed cash and make a plan for reducing these expenses.

Certainly, there are more streamlined methods for this approach. Apps like Mint and Quicken make it easy to link your bank accounts electronically, identify spending categories, and create a budget on the fly. However, the point here is to become accustomed to the way that money is entering and leaving your bank account each month to identify savings opportunities more clearly. To be sure, it's crucial to look at each individual expense to identify opportunities, rather than relying on generic spending categories offered by these apps.

Whichever method you choose, be sure that you're comfortable with how you go about cutting expenses. Dieting research has shown that sudden changes in eating habits often trigger a stress response that can lead to a crash diet. And that's why any changes to your financial spending should be done in a stepwise and systematic fashion. And while budgets are an essential part of a solid financial plan, the approach we're advocating here is short-term adjustments to address an immediate cash need, rather than a long-term lifestyle change.

#2 Reduce your Debt Service Costs

Another approach to coming up with extra cash is to reduce the number of debt accounts that you service every month. On average, Americans carry credit card balances of $6,200 and make minimum payments of $120 per month. Volumes have been written about the dangers of consumer debt and the cost of carrying credit card balances. Indeed, eliminating credit card debt is one way to free up extra cash for the long term.

And prioritizing debt repayment, paying down smaller accounts first, and refinancing are some ways to grow money in your bank account. Let's start by taking a look at paying down your debt.

Make a Budget, Prioritize Debt Repayment

What gets measured, get managed. As mentioned earlier, knowing where your money is going every month can help you identify ways to reduce or eliminate spending and free up cash. You can multiply this effect by using this freed up cash to eliminate credit card debt and thus giving your financial savings another boost.

How does it work? Well, this approach includes reallocating spending away from non-essential matters and toward making extra debt payments for a time. Again, like a diet, this method requires commitment. Yet, the short-term sacrifice of prioritizing debt repayment could lead to a lifetime of financial gain. Where should you start?

Pay Down Smaller Debts First

Consider focusing your efforts on paying off your smallest balances first if you have multiple credit cards. To be sure, prioritizing the elimination of your lowest balances can help free up cash from those payments to be used toward your next higher balances.

Here, the idea is to quickly pay off debts with low balances and then apply the extra monthly cash flow to pay down your next smallest account balance, repeating until your credit cards are completely paid off.

Consider a Personal Loan

Another thing to consider is that interest rates have fallen considerably over the past year. With personal loan rates well below 10%, refinancing higher interest credit card debt might help lower your monthly payments. You can then use the money saved on your monthly payments to pay down your loan faster. How so? Let's look at an example:

Assume you have an outstanding credit card balance of $10,000, for which you are charged an annual percentage rate of 21%. Making the minimum payment of $200 per month would take roughly ten years to pay off your debt. Now, if you refinanced into a fixed-rate 10-year personal loan at 7.5%, your payment could be as low as $118 per month. Applying the extra $82 per month toward your principal amount could lead to your account being paid off five years sooner.

While not necessarily a short-term fix to coming up with cash, the process of reducing credit card debt can help you identify ways to trim expenses, eliminate one more financial burden, and put you on track to building emergency reserves for the long-term.

#3 Judiciously Tap Your Home Equity

Now for many people, a home will be their largest lifetime purchase and source of wealth. A time will come when you have little choice but to borrow money. If you own a home and have a sufficient amount of equity, some lenders may allow you to borrow against your home. You'll have to choose between a home equity loan or a line of credit in this situation.

What's the difference between the two? Well, a home equity loan is a fixed-rate loan, paid off over a set time. On the other hand, home equity lines of credit are like a credit card whose rate and repayment period can fluctuate over time.

When should you borrow against your home? If you plan to sell your home soon and need a way to raise some extra cash, borrowing against your home equity might make sense, assuming stable price conditions in your local real estate market. While you should find ways to reduce non-essential expenses and raise cash first, borrowing against your home equity can be cheaper than using a credit card. Now, here's a word of caution against using home equity loans or lines of credit.

Borrowing against your home's value can help you meet near-term financial needs but should be done so judiciously. Borrowing against your home during a time of financial stress can put you and your home on the line. For example, a bank can force a foreclosure if you stop making regular payments on a home equity loan or line of credit. Therefore, taking on additional debt during a period of financial stress might lead to losing your home. This is one reason why borrowing against your home to come up with extra cash comes with its own set of risks.

#4 Relocate to Lower Your Housing Expense

If your cash need extends beyond addressing non-essential spending or borrowing prudently just won’t cut it, then it might be time to reassess your current living situation. For many people, housing can make up between 30-50% of their overall monthly expenses. And moving to a lower cost part of town or state to reduce this expense is one way to free up extra cash.

This trend is evident today in stories of Silicon Valley tech workers abandoning high cost rents of the San Francisco Bay Area, for more affordable options in places like Austin, Texas. So, what are the financial benefits of relocation?

Right off the bat, moving to lower your housing expense might enable you to finally accumulate savings that can later be used to pay for unexpected costs. At the same time, reducing a large part of your housing expense can give you more lifestyle flexibility compared to cutting back non-essential spending altogether.

In fact, while reducing non-essential expenses can work in the short term, like dieting, your spending is largely determined by your lifestyle priorities. That's why reducing housing expenses can set you up for a long-term gain without having to sacrifice the things that are important to you today. And if you own a home and have built up equity, then you can use that cash as a way to pay for significant one-time expenses if you decide to purchase a cheaper home in a more affordable part of town.

The downside of this approach means moving. Besides paying for boxes, packing supplies, and movers, there are other expenses to account for. If you're a homeowner, you probably know that there will be closing costs associated with selling your home and again when you buy your next home. That's why this option makes the most sense for individuals who have either 1) lived in their home for longer than five years or 2) have seen rapid home price appreciation. The bottom line here is to make sure that the savings benefits you anticipate outpaces moving costs.

#5 Access Retirement Savings Prudently

A final way to come up with extra cash is to tap your retirement savings. Now using your retirement savings to address a short-term need should always be a last resort. Fortunately, there are ways to access your retirement savings if you need cash in a pinch. While borrowing against your retirement savings is one option, let's talk about cash withdrawals.

The CARES Act passed earlier this year allows individuals affected by COVID-19 related conditions to draw down 401k and IRA savings and in many cases do so penalty-free. Under the old rules, penalty-free withdrawals from these accounts were limited to individuals over the age of 59 ½, those experiencing financial hardship or first-time home buyers.

What's more, prior laws applied a 10% penalty for withdrawals on individuals not meeting these criteria. In the case of the CARES Act, you can cash out your retirement plan in a more favorable way. Let's take a closer look.

According to the IRS's interpretation, the CARES Act allows individuals to withdraw up to $100,000 from their retirement accounts penalty-free. Because pre-tax money went into the accounts, money coming out will be considered ordinary income with taxes due. Fortunately, the CARES Act allows employers to forego the standard 20% estimated tax at withdrawals for 401ks and enables individuals to spread out tax payments over three years.

Just because you can take out the money doesn't mean you should. And that’s because taking money out of retirement savings can reduce your investments' future lifetime growth. And while doing so might help you meet a near-term need, the cost of foregoing your savings' future compounded growth should be carefully considered before choosing this option.

Coming Up with Cash When You Have Little in the Bank

A time likely will come where you need to raise cash to meet near- or long-term needs. Depending on your circumstance, finding extra cash may come down to simply cutting back on lifestyle expenses or tapping your retirement savings when a big emergency crops up.

Either way, knowing your options and having a plan in place might help you avoid costly mistakes when your need for cash arises. Even so, keeping track of the resources available to you right now before you need them can help ensure that your finances stay on track, no matter what issues life throws your way.

How Can You Rebuild a Broken Retirement Three-Legged Stool?

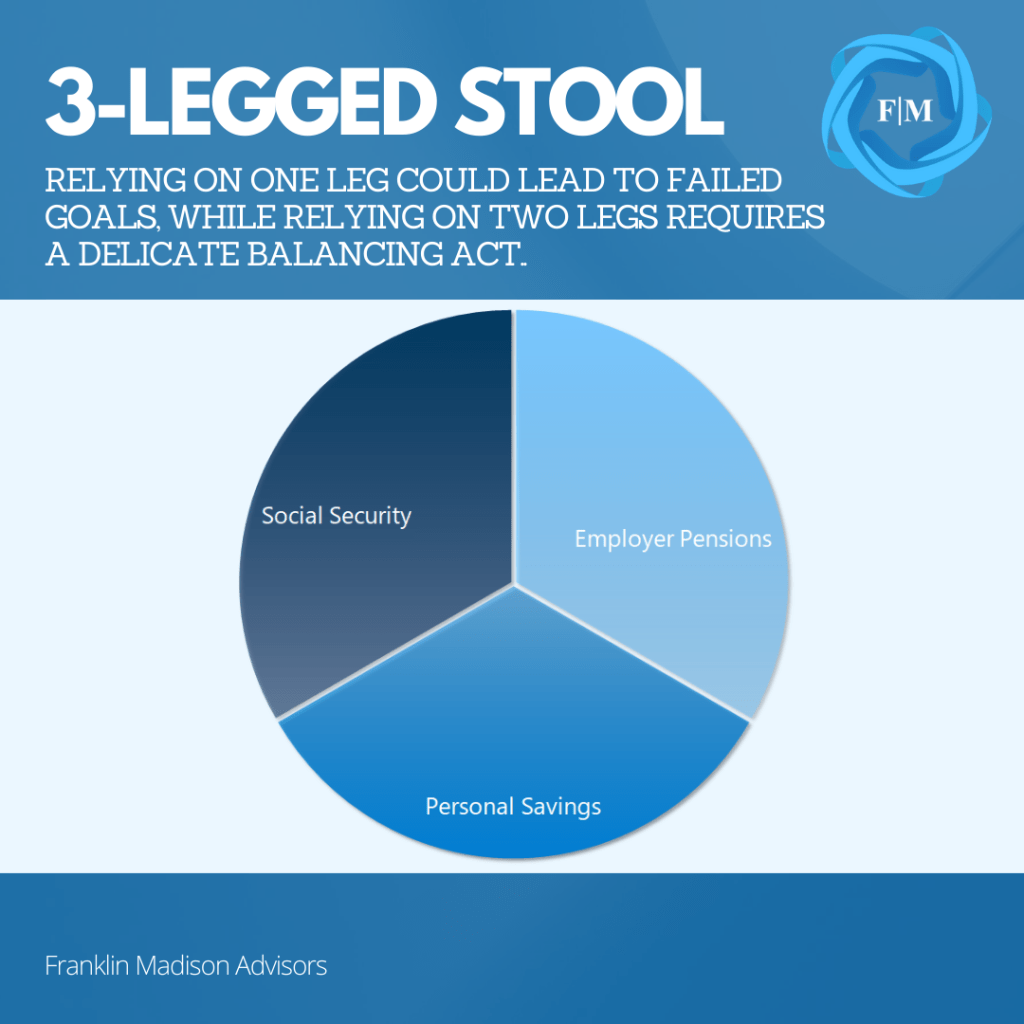

The road to retirement is not as straightforward as it used to be. There was a time when simple metaphors, like the three-legged stool of retirement, captured how you could achieve retirement security with ease. This concept illustrated how securing a good pension, obtaining a solid return on your savings, and relying on social security might have paved the way for financial comfort in your golden years. Relying on just one leg could lead to failed retirement goals, while relying on two legs requires a delicate balancing act.

Unfortunately, for many individuals, this seemingly secure approach to retirement planning has all but disappeared. And today, few simple metaphors exist to describe an easy path toward retirement security, leaving many people scrambling to figure out how to plan for their future thoughtfully. Now, with a little extra work and some creativity, you might be able to repurpose the components of the simple three-legged stool framework to suit your individual goals in this complex and challenging economic environment.

How the Three-Legged Stool Has Changed

When the three-legged stool concept was first introduced generations ago, many employers provided pension benefits to their employees, banks offered healthy returns on savings, and social security was seen as a solid base from which to structure retirement planning. Yet the foundation upon which this concept was developed has materially changed in the past few decades.

Complex Retirement Planning

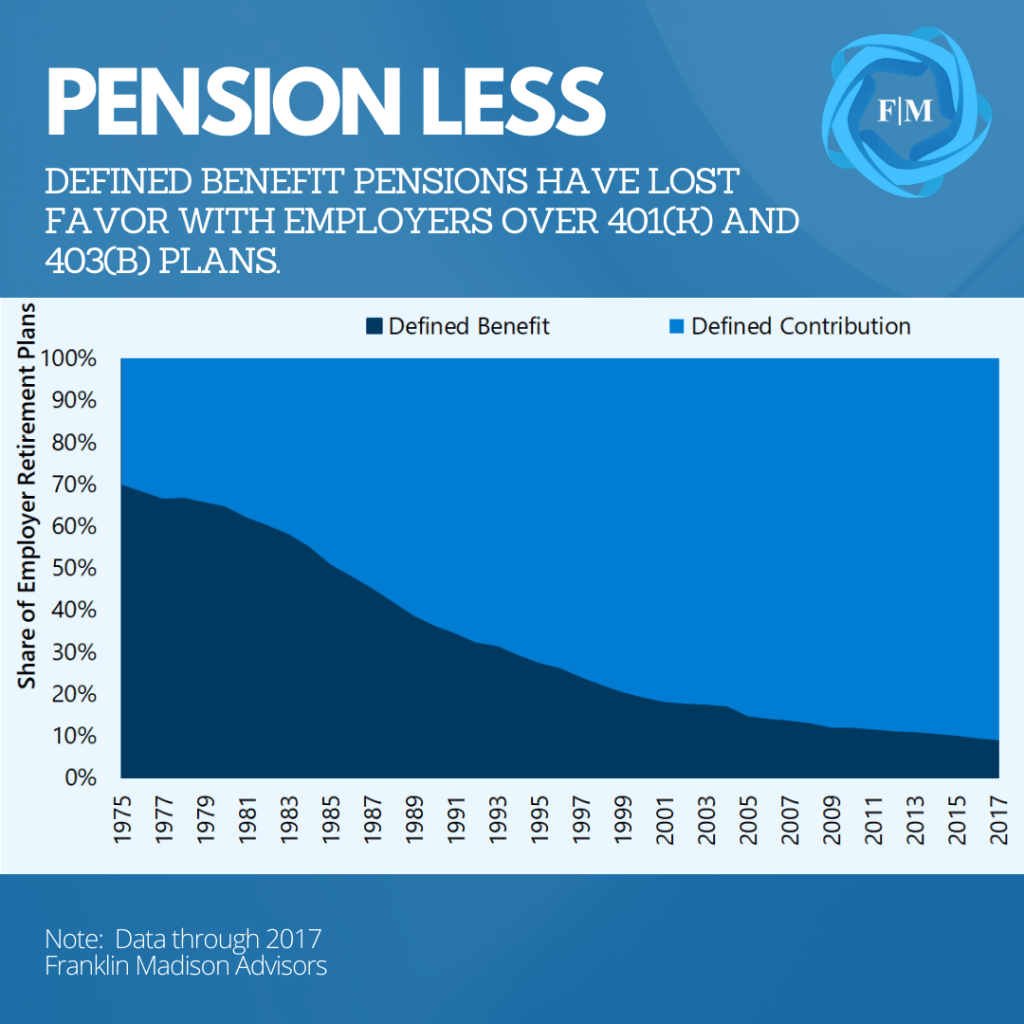

For example, defined benefit pension plans used to be a key component of the three-legged retirement stool. Pensions accounted for 70% of retirement plans in 1975 for companies with 100 or more employees. By 2017, this figure fell to 9% and remains in decline as employers increasingly shift their preference toward defined contribution options like 401(k) and 403(b) plans.

This change means that individuals workers are increasingly responsible for navigating sophisticated investment options, determining appropriate contribution amounts, and working through tax consequences and their crucial distribution choices. It goes without saying that planning for retirement is much more complicated than it used to be.

Source: Broadview Macro Research

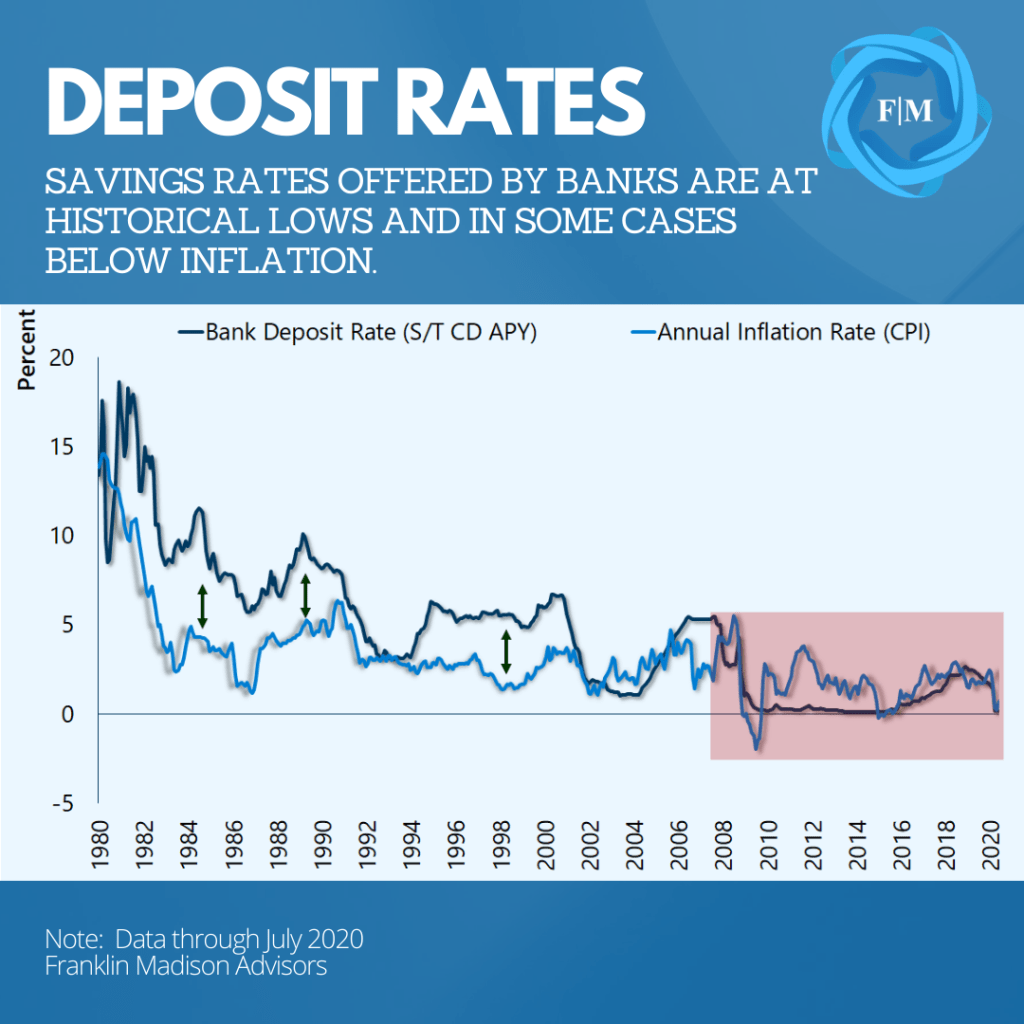

More Challenging to Grow Your Money

In terms of saving for the future, changes in the financial system have made it challenging to grow your money through a simple bank deposit. From 1980 through the start of the Global Financial Crisis, bank deposit rates averaged 6.5%. Since then, the amount of annual interest that your savings might accumulate through a bank account has fallen to less than 1%. Without a doubt, using a simple savings account to shore up your retirement is more challenging.

For example, at the current average deposit rate of 0.5%, it will take you 144 years to double money held in a savings account compared to just 11 years a few decades ago. Taking into consideration the detrimental effects of inflation, if you rely on a standard bank account alone to grow your wealth, there's a good chance that a dollar saved today likely won't go as far in the future.

Social Security is Less Secure

Finally, it will likely come as no surprise that expected future social security benefits are increasingly coming under pressure. Social Security was once seen as the most solid leg of the retirement planning stool. Yet, by some estimates, the government's reserves needed to pay old age, survivor, and disability insurance (OASDI) benefits for Americans likely will be depleted by 2035. This outlook is according to a report from the Social Security Trustees themselves.

What's clear is that Congress must act soon to prevent the Social Security program from going bankrupt. While this entitlement program surely remains an important political debate topic, the program we know today might likely look much different in the future. This view underscores yet another set of uncertainties about how income benefits will be calculated for individuals paying into the program today to draw down benefits decades from now.

Given this backdrop, you can likely see how the three-legged stool that had helped many individuals secure retirement in the past is now less secure for future generations. So, what can you do to secure your retirement plan in light of this crumbing three-legged stool?

While the task at hand will not be easy, there are a few things that you can do to repurpose some of the original intent behind the three-legged stool to overcome today's retirement planning obstacles. Let's start by examining how you can maximize the benefits of your employer retirement plan.

Source: Broadview Macro Research

From Pension to Self-Directed Retirement

As discussed earlier, companies are increasingly offering their workers retirement benefits through defined contribution plans, like 401(k) and 403(b) accounts. These plans require substantially more involvement from their workers. And because defined contribution plans put the retirement savings onus in your court, one of the most vital things you can do to rebuild this critical component of the retirement stool is to begin saving as soon as possible.

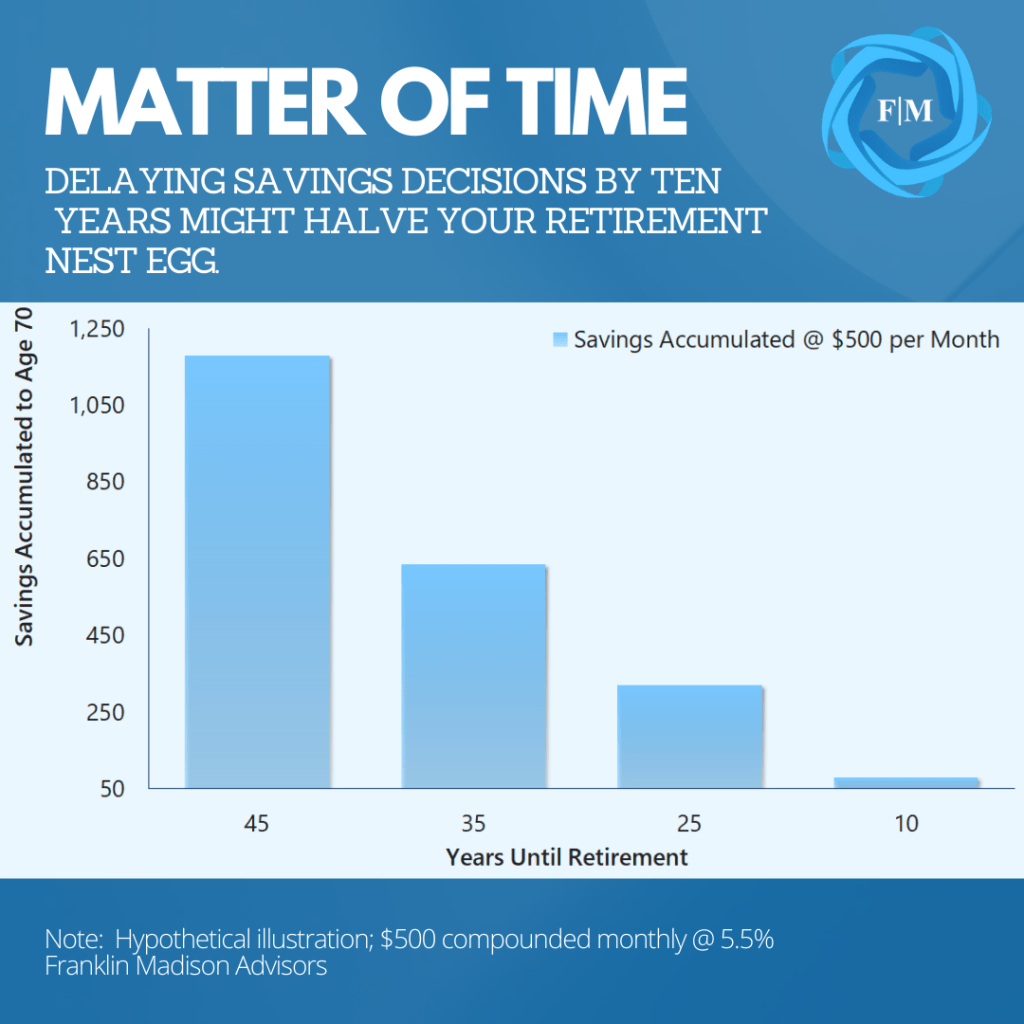

In a previous report, we showed how a steady contribution rate, a modest return, and little time could help you grow your savings for the long term. So, what difference can a few years make? And why should you get started early? Rather than telling you about the benefit, let's look at an illustration that lays out the opportunity cost of delaying retirement savings.

Let's assume that you contribute $500 per month towards your defined contribution account, starting at the age of 25 with a plan to retire at 70. Earning an average return of 5.5% compounded monthly, by the time you retire at the end of 45 years, you could end up with nearly $1.2 million in savings.

Less than a quarter of this amount, just $270,000, is the original principal that you've saved over time. What this means is that that much of your gains over 45 years have come from compounding returns. How does this situation look if you decided to delay retirement savings by a decade?

Source: Broadview Macro Research

Well, if you decided to delay your retirement contributions by ten years, using the same assumptions as before, you could end up with almost half the amount saved compared with starting ten years sooner. This illustration shows that you might accumulate $600,000 instead of having $1.2 million if you had started saving at 35 instead of 25. In fact, if we continued this illustration by delaying savings in ten-year increments, we find that the amount saved continues to decline at a precipitous rate.

The point here is that if you're looking for a simple act to get you on the right track toward retirement security, start by saving early. To be sure, the power of compounding requires three simple components: a contribution rate, a return, and time. Of these three factors, the decision to begin your savings journey is the easiest one to control and is an important reason why starting now is crucial to rebuilding the first leg of your retirement savings stool.

Saving Outside of an Employer Plans

Establishing savings outside of an employer plan is another essential leg of the retirement planning stool. Now, as we pointed out before, merely parking your money in a bank account won't generate the kinds of savings benefits that may have been available decades ago.

In fact, allowing your money to accumulate in a bank account alone over the past ten years might have left you worse off financially when accounting for inflation's effects. So, where else can you store your money for growth while preserving the purchasing power of your savings? Consider real estate.

Ownership Builds Inflation-Protected Savings

Everyone needs a place to live. There are indeed many tradeoffs between renting and owning a home. On the one hand, renting means little to no maintenance costs and gives you the option of relocating when your life circumstances change. On the other hand, rent payments are effectively a 100% loss on financial savings.

Indeed, there are some costs associated with homeownership. Even so, the fact is that each month a portion of your mortgage payment goes toward building equity that you can use in the future. And the longer you pay down your mortgage, the higher the part of your payment goes toward building up your savings.

While the housing market has experienced price volatility over the years, history has shown that at a national level, home values generally rise over time and at a rate that outpaces inflation. This means that making the simple decision to own versus rent might enable you to build savings that are preserved against the ravages of inflation. How can homeownership specifically benefit you in retirement?

Well, assuming your mortgage is paid off by the time you retire, a couple of benefits tend to accrue. First, you will need a place to live during retirement, and owning your home outright is a way to ensure against rising housing costs over time. In fact, owning a home and paying off your mortgage as you enter retirement could lead to household expenses that are between 20-30% lower depending on the size of your pre-retirement mortgage payment.

Another retirement benefit of ownership is the value stored up in equity. For example, you might choose to downsize your family home in retirement. And if you decide to purchase a less expensive home, the difference between your sale and purchase can lead to cash available for retirement savings.

As of 2020, the IRS allows married couples filing jointly to avoid paying taxes on gains of up to $500,000 on the sale of a primary home. This potential tax-free gain illustrates how homeownership is another way to shore up a crucial leg of your retirement planning stool, notably in a low-interest-rate environment.

Delay Your Social Security Benefits

Social security is the final but foundational leg of the retirement planning stool. As discussed earlier, this government program is likely to face several challenges in the years to come. While some individuals argue social security will eventually fail, a possible outcome is that Congress will act in some way to change this vital program by reducing future benefits, increasing taxes, or some combination of the two.

So, what can you do to make the most of this critical part of your retirement plan in light of the ongoing uncertainties surrounding this entitlement program?

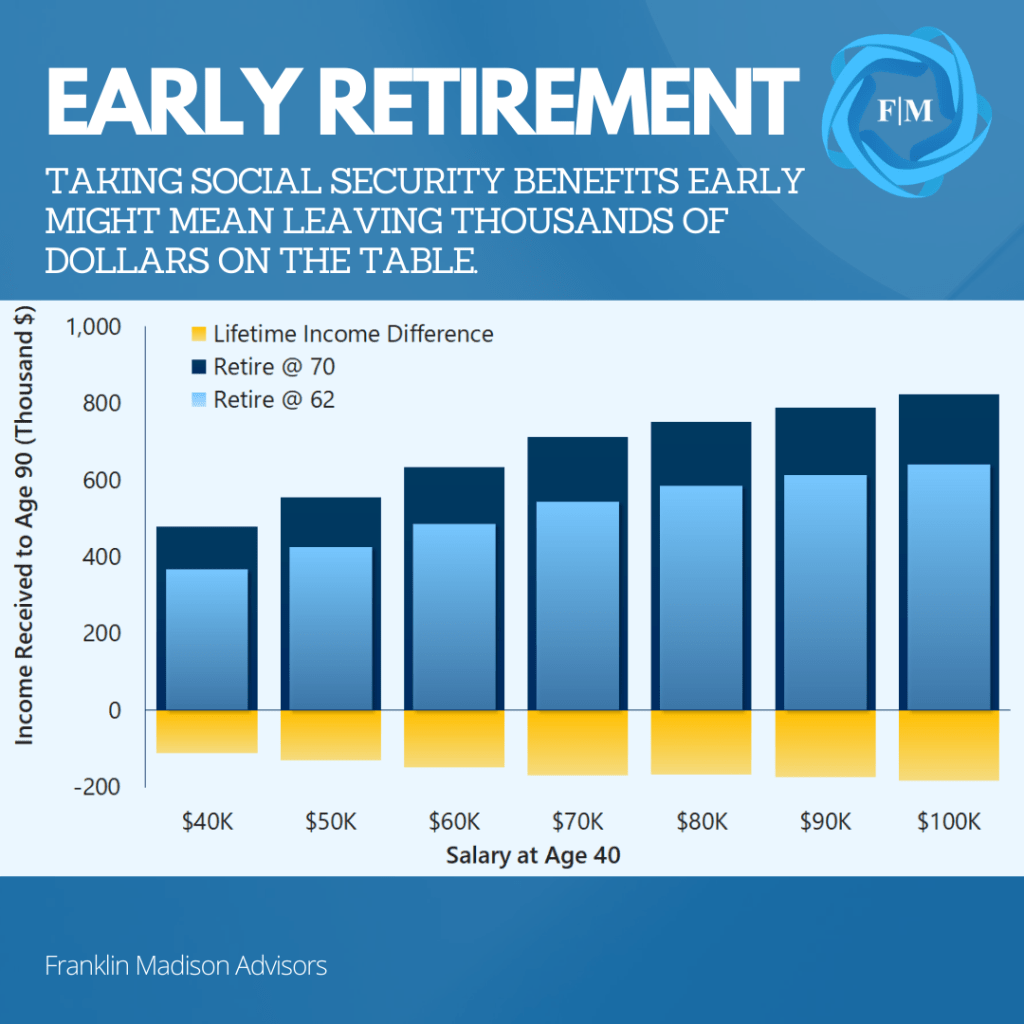

First, it's vital to note that the choice you make between taking Social Security benefits sooner rather than later can mean the difference of thousands of dollars in lifetime income.

As of 2020, the Social Security full retirement age (FRA) is between 66 and 67, depending on what year you were born. FRA represents the age at which you may receive your full benefits based on your income history.

Now, the Social Security Administration allows you to begin taking benefits as early as 62 so long as you meet specific criteria. However, taking social security before your full retirement age means that you'll receive less of a benefit than you otherwise would be entitled to.

For example, compared to waiting until the age of 70, taking retirement benefits at 62 could mean the loss of lifetime income of over $180,000. This outcome assumes that your salary at age 40 is $100,000 per year and that you receive retirement benefits until age 90.

The point here is that if you plan to incorporate social security benefits as part of your retirement plan, then a simple act you can take to shore up this foundational part of retirement planning stool is to delay taking benefits for as long as possible.

Rebuilding the Broken Retirement Stool

The road to retirement is not as straightforward as it used to be. There was a time when the simple concept of the three-legged stool of employer, financial institution, and government support could ensure individual financial comfort throughout retirement. By many measures, the structures making up the legs of this metaphoric stool are broken.

Today, establishing a sense of retirement security has increasingly become the responsibility of individuals over once trusted institutions. If you want to rebuild the retirement planning stool, then you'll need to start by taking a more active role in your employer retirement plan, and crucially beginning your contributions sooner rather than later. And while bank deposit rates are meager today by historical standards, responsibly using your home as a way to store up inflation-protected value might provide you with a useful cash resource as you near retirement.

Finally, social security benefits aren't likely to go away, but you can make the best of an uncertain system by maximizing the benefits available to you throughout retirement. Either way, taking some simple steps today can help you rebuild the broken retirement stool to suit your individual needs in this complex and challenging economic environment.

How Fast Can You Break Free from Student Loans?

Eliminating student loan debt can put you on the fast-track to achieving your essential life goals. If you’re one of the millions of Americans struggling with this vital issue, you know first-hand the challenges of student loan debt. As student loan balances continue to balloon from one year to the next, what can you do to conquer this overwhelming debt load? Well, many people are waiting for an act of congress to make their student loans disappear.

Yet, chances are that it will be on you to forge a path toward financial liberation. If you’re serious about freeing yourself from student loan debt, you’ll need to take steps that you might not have considered before. These actions include evaluating how much minimum payments on your student loans cost you, curbing unnecessary interest expenses, and finding simple ways to come up with extra cash to pay down loan principal. Making these steps a priority might enable you to eliminate debt sooner and give you the ability to focus your efforts on your most essential life goals.

The Burden of Student Loan Debt

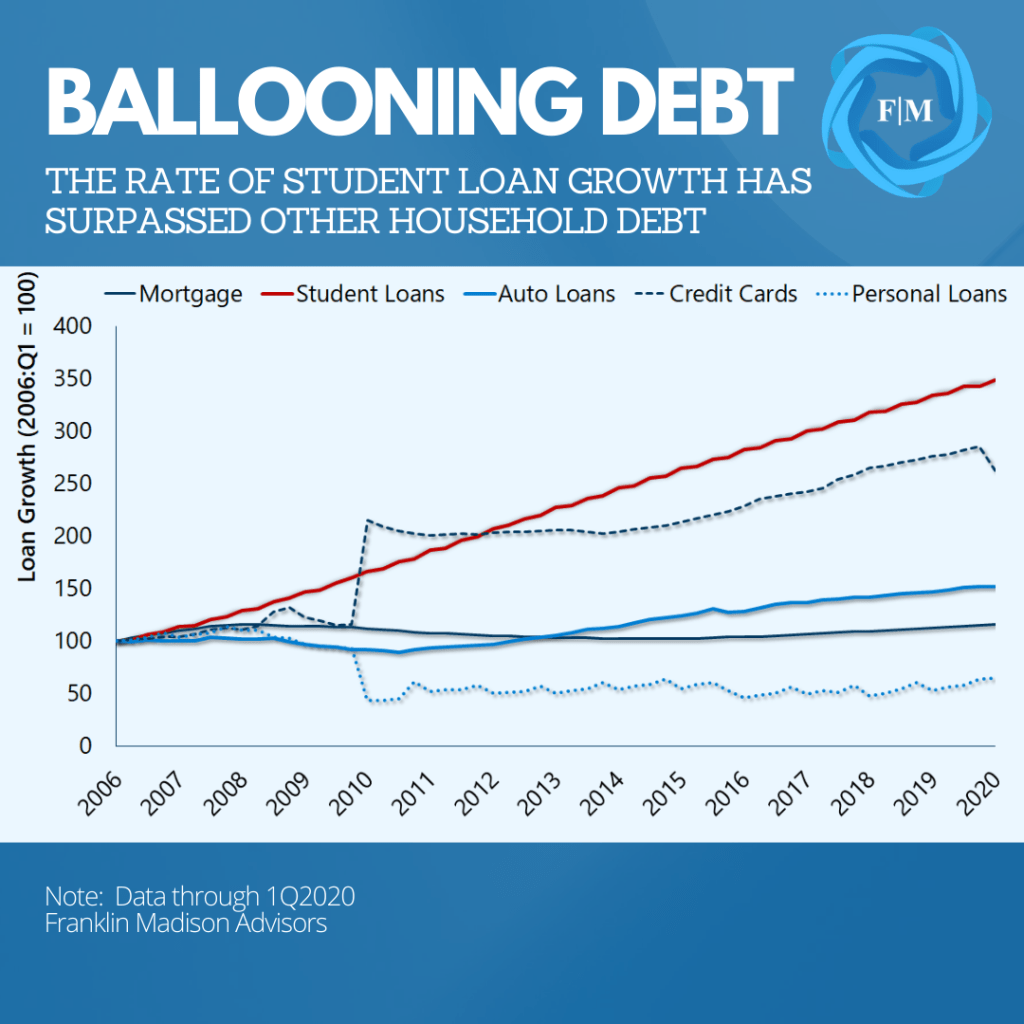

Student loan debt issuance has skyrocketed over the past decade. Government data out in the first quarter showed that total student loan debt outstanding reached $1.7 trillion. Of the amount outstanding, three-quarters were federal direct loans. This ownership share suggests that if you have a student loan, then there’s a good chance that Uncle Sam owns it. And if you feel like your debt burden is unreasonable today, you’re not alone.

Balances outstanding now average $35,000 for the nearly 40 million individuals who have federal student loans -- a figure that has doubled since 2007. And while the number of borrowers has increased by 40% over the past seven years, loan default rates have nearly tripled. If you want to pull yourself out of your student loan debt trap and forge a path to financial liberation, you’ll need to make decisions about your student loans that different than what most people are doing right now.

Relief in Times of Uncertainty

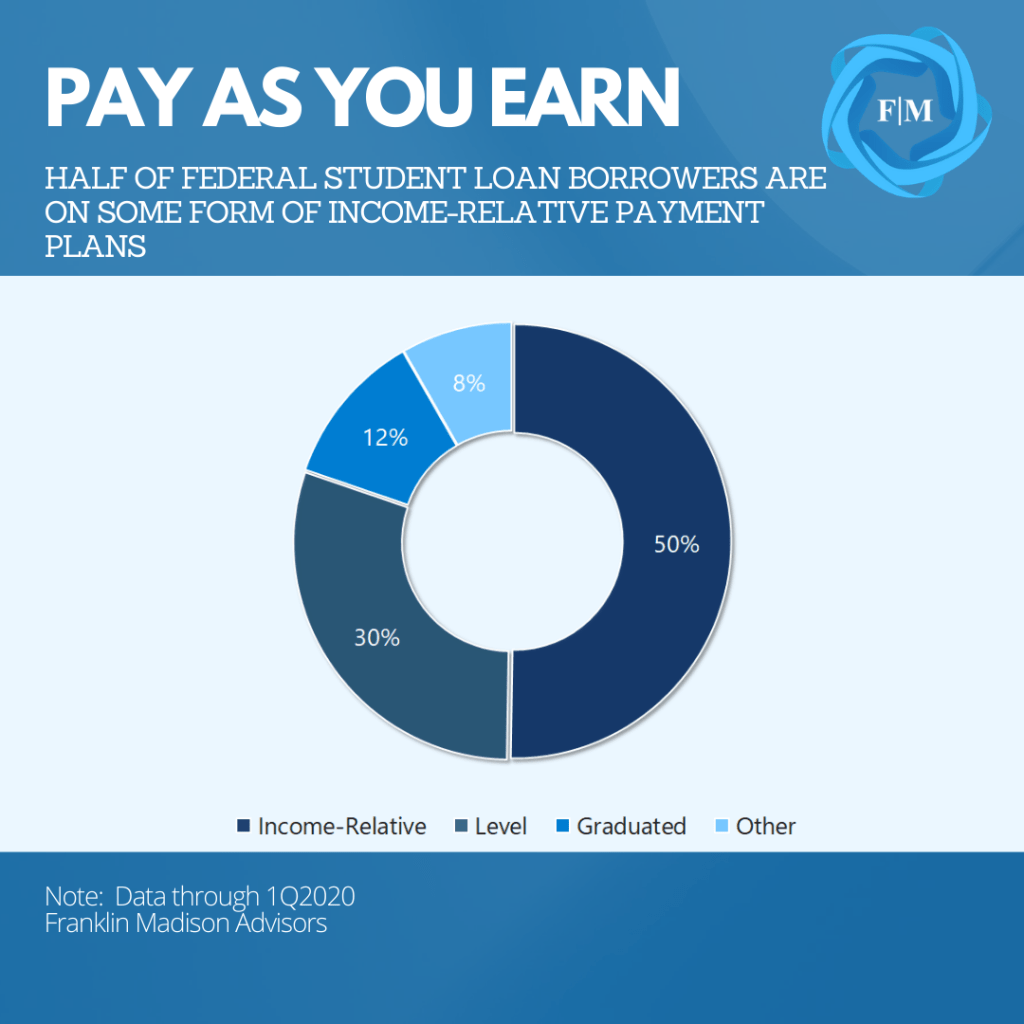

Many college students assume that money borrowed to finance education costs can be reasonably paid back over ten years. This seemingly short payback period is one reason some individuals choose to take on student loans in the first place. By the time they graduate, however, many students accumulate so much debt that they find it challenging to make their standard level payment. That’s when some borrowers choose to utilize income-relative repayment programs.

According to government data, over half of federal direct loans are in some form of an income-relative repayment as of the first quarter of 2020. These programs include Pay as You Earn (PAYE), Revised Pay as You Earn (REPAYE), Income-Based (IBR), and Income-Contingent (ICR) Repayment. The common thread running through these programs is that your monthly student loan payments are based on how much you take home per year rather than a level, amortized loan amount.

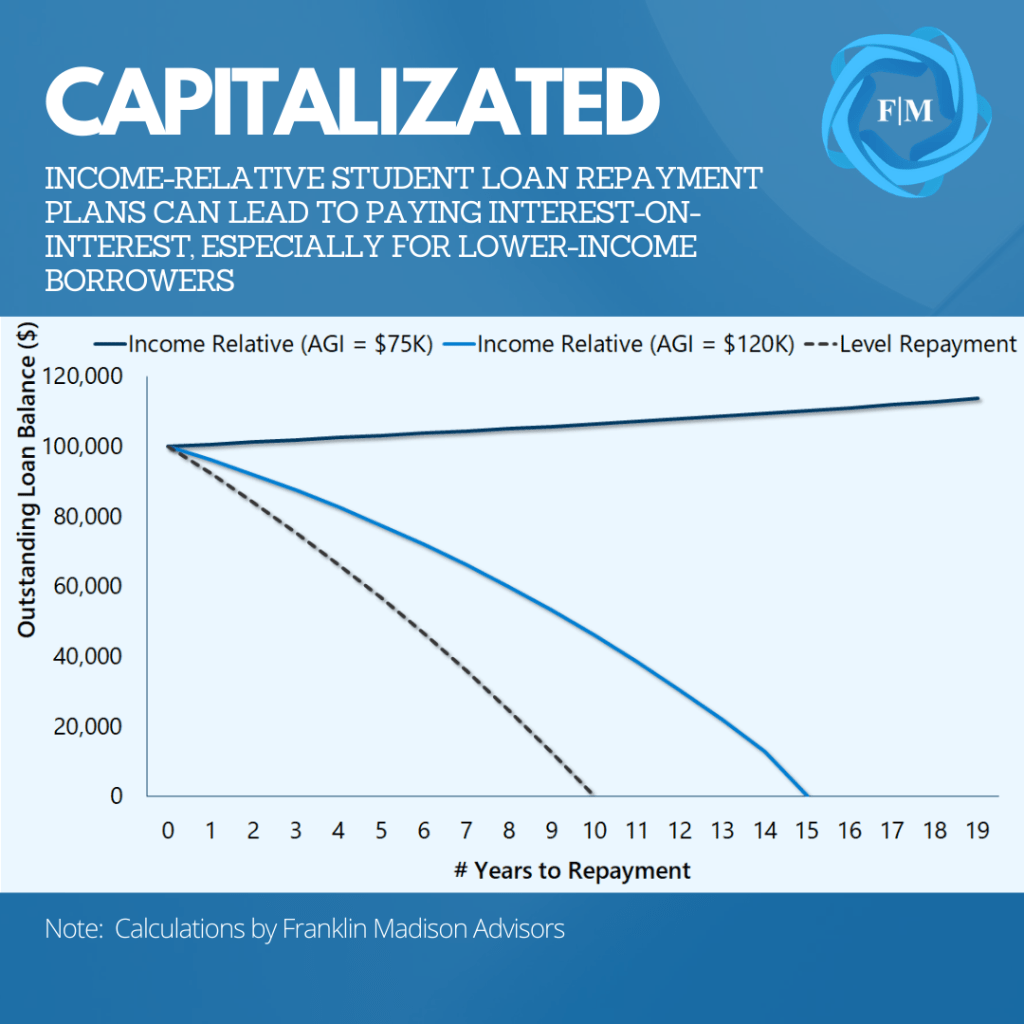

Income-Relative Plans: Not a Long-Term Fix

For example, consider a couple with an adjusted gross income (AGI) of $120,000 per year and $100,000 in student loan debt. Under an income-relative plan, the couple might pay an extra $18,000 in interest expense over the lifetime of their loan compared to level repayment. This difference is due to the fact that it would take 16 years to repay the debt compared to 10 years under a level repayment plan, therefore accumulating more interest.

The drawbacks of an income-relative plan become more evident as we move down the income scale. For a similar household with an AGI of $75,000 instead of $100,000, lifetime interest payments would be nearly $84,000 higher than compared to a level plan. What’s more, because monthly payments barely cover interest expenses in this scenario, the unpaid interest is capitalized or, in other words, added back to the principal amount of the loan.

The effect is that the borrower’s total loan outstanding rises over time rather than being paid down. While many income-relative plans allow for loan forgiveness after 20 or 25 years, these borrowers are not completely off the hook. Debt forgiven is, in some cases, considered taxable income. Therefore, the remaining balance might lead to a tax bill of $23,000 for this couple at the end of 20 years.

It is crucial to understand that income-relative repayment plans are an expensive way to pay down your student loan debt. While useful for addressing short-term challenges to your financial situation, these programs should not be relied upon as a long-term approach to paying down debt. If you’re participating in an income-relative repayment program, and are serious about conquering your student loan debt, it might be time to examine what this payment program is costing you.

Avoid Capitalizing Interest

If you’ve ever experienced hardship as a student loan borrower, you probably know how payment forbearance can help you manage obligations during times of financial uncertainty. Forbearance programs allow you to delay making payments on federal direct (and some other loans) for up to 12 months at a time. And today, there are approximately 3.8 million direct loan borrowers in forbearance with outstanding balances that are growing at a rapid rate.

While beneficial in the short-term, this program can undo the progress made on paying down your loans and, in some cases, leave you with a higher balance than with what you started. As noted earlier, capitalizing interest expenses is the quickest way to derail your student loan repayment plans. While income-relative programs might lead to higher debt levels for certain individuals, participating in a forbearance program will almost certainly cause your outstanding loan balance to rise. Let’s use an example to demonstrate this point.

The Cost of Forbearance

Recall the earlier illustration of a couple with a household AGI of $120,000 and $100,000 in student loan debt. Under an income-relative repayment plan, they might pay off their student loans in about 15 years, costing them about $152,000 over the lifetime of their loan. Now, what would happen if we introduced forbearance into the picture?

Assuming that this couple used forbearance to delay payments by 36 months, their student loan would cost over $191,000 by the time the debt is paid off and $40,000 more than had they avoided forbearance. Capitalized interest increases the outstanding loan balance and leads to paying interest on top of interest. What’s more, in this scenario, the payback period for the loan goes from 15 years to more than 20, leading to a hefty tax bill when the loan is forgiven.

And how does forbearance affect level repayment plans? Well, $100,000 in student loan debt amortized over ten years at 5.5% interest will accumulate about $33,000 in interest expense. Placing their loans into forbearance for 36 months, the couple would end up doubling interest expense. Because the borrowers are now making up for lost time when payments were postponed and paying interest on top of interest, it might take 15 years to repay their level loan versus the 10 years had the borrowers avoided forbearance.

The point here is that while forbearance is a useful tool that can help you navigate times of financial stress, when possible, it should be used only as a last resort. More to the point, if you do come upon tough financial times, prioritizing interest payments can help you avoid capitalization. Indeed, if your goal is to quickly conquer student loans and pay down your debt, then not paying interest on top of interest is crucial to this aim.

A Little Extra Goes a Long Way

Income-relative repayment plans can lengthen the time it takes to repay your student loans, while forbearance can lead you to pay interest on top of interest. If your aim is to eliminate student loan debt, consider alternatives to income-relative payment plans, and avoid forbearance. Then, create a strategy to make additional principal payments on your student loans.

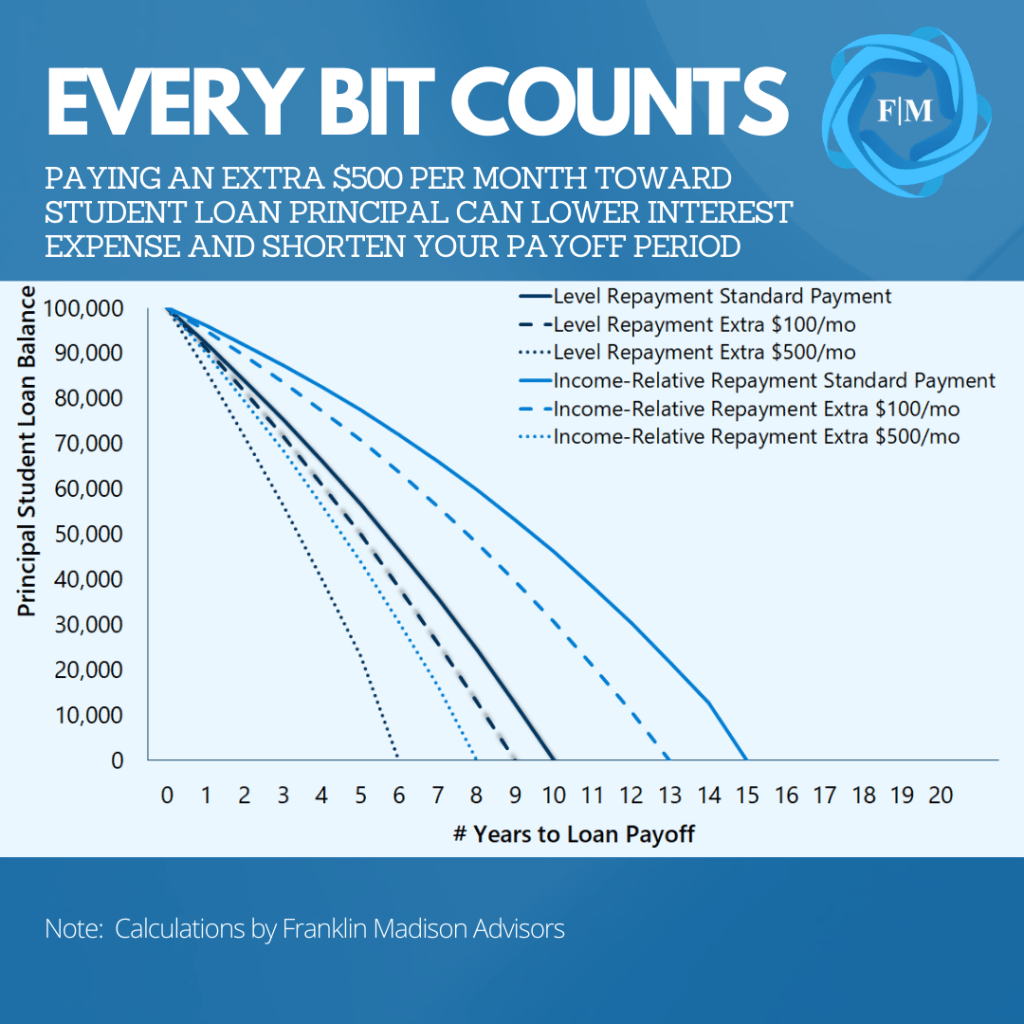

Indeed, whatever your chosen repayment program might be, every extra payment you can make on your loans can shorten the time it takes to pay off your debt and reduces interest expenses. For example, finding a way to pay an extra $100 per month on a $100,000, 10-year level repayment student loan can modestly reduce interest costs and cut your student loan payoff period by a full year.

How does this apply to income-relative payment plans? When using some of the same assumptions as before, making an extra $100 payment on your student loans can result in even more significant financial savings and shorten your payback period. Recall that for a couple with an AGI of $120,000 and $100,000 in debt, it might take them just over 15 years to pay down their student loans. By paying down an additional $100 in principal per month, they can eliminate debt in 13 years and save over $8,000 in interest expenses.

Taking this example one step further, let’s look at increasing principal payments from $100 to $500 per month. In our 10-year level payment scenario, committing $500 per month to principal reduction would reduce the repayment period to just over six years and lower interest expenses by a third. For the income-relative scenario, a similar contribution could cut lifetime interest costs and the repayment period in half. The point here is that every dollar that you can commit to paying down principal puts you one step closer to student loan debt liberation.

How to Eat an Elephant

Desmond Tutu was once quoted as saying that the only way to eat an elephant is a bite at a time. In the case of student loans, paying down your debt won’t happen overnight. However, as we just illustrated, finding ways to commit even a little extra money to pay down student debt principal can shorten your payback period and minimize interest expenses.

Even so, finding an extra $100 or $500 per month might seem like a daunting feat for some individuals. What can you do to come up with extra money to pay down your student loan debt faster? Here are a few suggestions:

- Make a Budget, Prioritize Debt Repayment– What gets measured, get managed. Knowing where your money is going every month can help you identify ways to reduce or eliminate spending and free up cash that can be applied to paying down student debt. The short-term sacrifice of prioritizing debt repayment by reallocating spending away from non-essential matters and toward paying down your debt for the next few years might lead to a lifetime of financial gain.

- Pay Down Smaller Debts First – If you have multiple student loans, prioritizing the payoff of your smallest balances can help free up cash to pay down your higher balances. The idea here is to quickly pay off debts with low balances and then apply the extra monthly cash flow to pay down your next smallest account balance, repeating until your student loans are paid off. Applying this same principle to credit card balances is another way to free up some extra cash. On average, Americans carry credit card balances of $6,200 and make minimum payments of $120 per month. Paying off your small credit card balance then applying those payments to your student loans is another way to reduce your student debt quickly.

- Consider Refinancing – Interest rates have fallen considerably over the past year. With student loan rates as low as 3.5%, refinancing higher interest student loan debt can lower your monthly payment. You can then use the money saved on your monthly payments to pay down principal . However, keep in mind that certain benefits afforded to federal student loans (like forgiveness) may not apply if refinanced with a private lender.

- Use Windfalls to Pay Down Debt – You’re likely to come into some financial windfalls during the year. For example, many people receive a bi-weekly paycheck yet pay expenses monthly. This means that twice a year, you’ll have “extra” checks coming your way. If your budget allows for it, consider using these additional paychecks to pay down student loan balances. Also, consider applying other windfalls, like a tax refund or your stimulus check toward your principal loan balance.

Student Loan Debt Liberation Begins with You

What could you do with an extra few hundred or thousand dollars per month right now? For some individuals, this additional cash might make the difference between buying a bigger house or a newer car. It could even mean getting closer to critical financial goals like funding a college savings plan for their children or shoring up retirement savings.

While many people are waiting on an act of congress to make their student loans disappear, you will likely need to forge your own path toward financial freedom. This includes limiting the use of costly income-relative repayment plans and avoiding capitalized interest. To be sure, taking a measured approach to paying off your student loans may liberate you from seemingly impossible debt and put you on the fast-track to achieving your essential life goals.

What Are the Essentials of Crafting a Solid Financial Plan?

Many of us know that having a financial plan is a sensible place to start when it comes to achieving essential life goals. But what exactly is a financial plan, and more importantly, what makes for a solid plan? A financial plan is a strategy that lays out a set of actions that you need to take today to achieve your future life goals.

To be sure, a plan identifies a path that aligns available financial resources with your intended life destination. Therefore, the essentials of a solid financial plan should include clearly defined objectives, outcomes relevant to your current life situation and should also thoroughly reflect your entire financial position. Not considering these factors may lead your plans off course and to an unintended destination.

Crystallize Your Goals

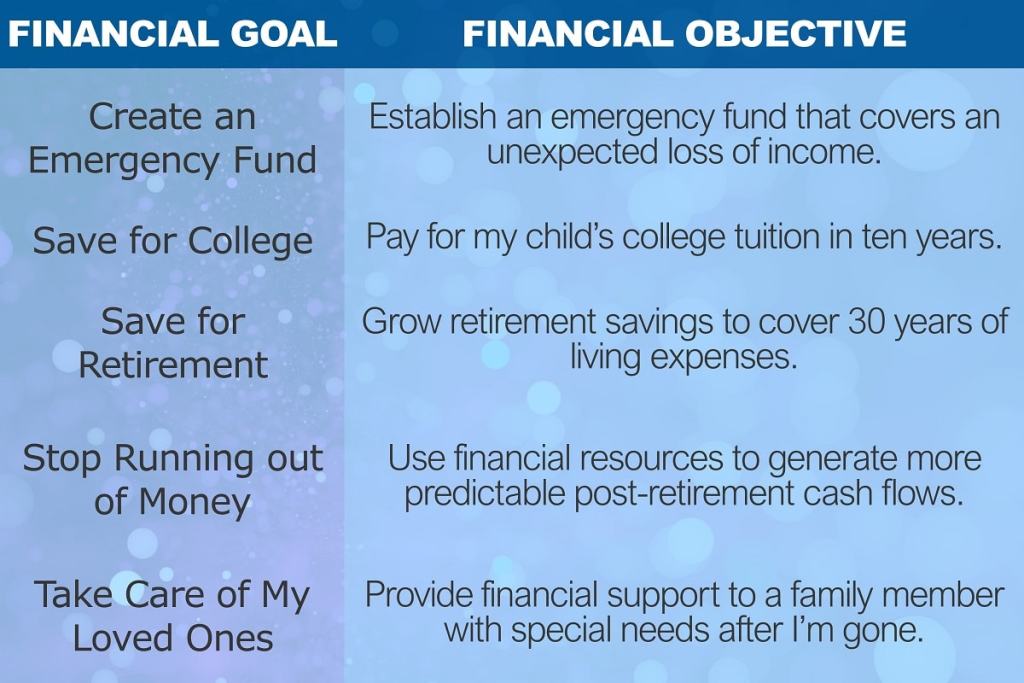

If a financial plan lays out how you can bring about your life ambitions, then being sure about your aim is central to hitting your intended mark. For this reason, the basis of a solid plan often begins with clearly defined financial objectives that align your financial plan with your goals. So, what are financial objectives?

Well, the table below illustrates how clearly defined objectives bring precision to your overall plan. To be sure, financial objectives get at the heart of why your financial plan exists. What's more, they can also be used as a reference point later on down the road to gauge whether your plan recommendations are moving you toward (or away) from your intended target.

Getting Help with Defining Objectives

What can you do if you have a general sense of your goals but are uncertain about articulating your specific objectives? That's where a conversation with a financial advisor can help. For example, let's say that you're a few years away from retiring but don’t know how to start planning for retirement.

During a discussion with your trusted advisor, you may discover that your retirement ambitions may include nuanced intentions like relocating closer to family, traveling the world, or wishing to be more charitable. In this situation, while your overall goal is retirement planning, the objectives that set the course for your plan may include buying a new house, creating a post-retirement travel budget, or evaluating means for engaging in philanthropic endeavors. Either way, financial objectives give direction to and are a crucial first step in creating your financial plan.

Planning Outcomes Should Be Relevant to Your Life Situation

Another essential aspect of creating a solid financial plan is ensuring that your planning objectives are relevant to your current life situation. This is important because irrelevant outcomes in your plan may take you down a path you never intended, leading to wasted time and souring your overall planning experience. When this happens, your perceived value of the planning process may decline along with your desire to put in the work necessary to achieve the other goals contained within your plan.

For example, pursuing a distribution strategy as part of a planning process might not make sense if your retirement date is over a decade away. Similarly, adding a professional asset management objective to your plan when all you want to do is consolidate a few small retirement accounts, might be beyond the scope of your planning engagement.

Comprehensive Shouldn’t Mean Complicated

Along these same lines is the use of a comprehensive financial plan. You might have heard of the term before and asked yourself: what is it, and why do I need one? From a broad perspective, a comprehensive financial plan may include:

- Cash flow planning

- Investment management services and

- Estate planning

Some individuals may find value in looking over all of their money matters in one sitting, particularly ahead of crucial life transitions. For example, let's say that you've amassed substantial savings and are a few years away from retirement. In this case, it might make sense to consider objectives that address investment distributions, ensuring the longevity of savings during your golden years and having an estate plan aimed at leaving behind a legacy.

For many people, however, sitting down with an advisor to talk about investment management or estate and tax planning objectives might not make sense at their given station in life. Even so, a comprehensive financial plan may still be an incredibly useful solution to address your most pressing planning needs. In fact, a comprehensive plan does not need to be complicated to be relevant for your life situation when there's a focus on the basics.

Take another example of a young couple planning to start a family. How might they benefit from a comprehensive financial plan? At this phase in their lives, the family might need to consider 1) adjustments to their current and future expenses, 2) establishing a savings program to pay for their child's education, and 3) reviewing life insurance coverage and preparing a simple will to address unexpected life events.

The point here is that comprehensive shouldn’t mean complicated. What's of more vital concern, however, is whether planning objectives are relevant to your current station in life. In either case, irrelevant planning objectives might prompt buyer's remorse, and derail your entire financial plan. Therefore, be sure to ask yourself early in the planning process, whether your objectives align with what you're ultimately trying to accomplish in your life today.

A Solid Financial Plan Should Be Thorough

How much house can you afford, or how much should you save for retirement? Many resources exist today that can help you calculate answers to these and other important money related matters. In fact, many websites and financial institutions offer free tools that can help you create a savings plan, establish a budget, and track your spending in real-time. But are these simple calculations and means enough to help you create a solid financial plan?

Often what's crucial to the success of your financial plan is not the tool you use, but rather how thoroughly these computations fit into the mosaic that is your life. Therefore, solutions to your financial objectives should reflect your spending and saving decisions as well as your asset and debt circumstances. This is important because some tools only consider one frame of your financial picture and may produce recommendations that fall short of your ideal outcome. And when you make decisions based on incomplete information, it could cost you valuable time and money.

For example, let's assume that your goal is to buy a house. An online calculator may tell you how much you can afford based on your income and living expenses and estimate a purchase price that's consistent with your mortgage. The tool does its job and produces a useful output when you give it some simple inputs. Even so, the estimate may represent a static result and likely not reflect all of the possible outcomes given your dynamic life situation.

Let's take our example a step further. Upon thoroughly reviewing your entire financial situation –spending, savings, assets, and debt – you discover that consolidating credit card debt could free up an extra $500 per month. When you take this information and feed it back into your home buying calculator, what you're likely to find is that 1) you can now afford to buy a more expensive home or 2) shorten the time it takes to save for a down payment.

The point here is that a solid plan should include calculations and estimates that thoroughly consider your entire financial perspective. Even if you intend to address just one objective, broadly understanding the interrelationships across your financial situation can help you craft a solution that fits your unique needs.

Increase Your Chances of Achieving Success

Finally, an essential point to consider is deciding when to create a financial plan on your own and when to bring in a professional. As we mentioned earlier, there are a host of tools available that can help you create your very own plan. From simple calculators to sophisticated smartphone apps and websites, these tools can lay out actions that you need to take today.

What's more, many personalities have authored books and created programs that have helped thousands of people reach their goals. So, when it comes to doing-it-yourself, there are plenty of cost-effective resources that you can utilize today to help you develop a solid financial plan that will move you closer to what's essential in life.

Knowing When It’s Time to Work With an Advisor

Sometimes, working with an advisor might make more sense than going it alone. Think of a financial advisor as a personal trainer. A personal trainer can help you achieve weight loss goals by creating nutrition and work out plans, showing you how to use equipment at the gym, and holding you accountable to your desired outcome. In a similar way, a financial advisor can use the planning process to help you achieve your important financial goals.

When might it make sense to bring an advisor into your planning process? Well, maybe you understand the various planning tools and approaches but have neither the time nor inclination to carry out the analytical and preparation work yourself. Another point where it may make more sense to work with an advisor is when you have a goal but are not quite sure about how to articulate your financial objectives or identify the tasks necessary to pursue that goal. Or maybe you've even tried a canned one-size-fits-all method to managing your finances but find that the approach does not suit your unique situation. If any of these illustrations resonate with you, then it might be time to bring in outside help.

Whether you work with an advisor or decide to go it alone, crystallizing your goals, identifying relevant financial objectives, and utilizing thorough solutions that fit into your life mosaic are essential components to crafting a solid financial plan. Not considering these factors may lead your plans off course and to an unintended destination. Indeed, a financial plan may be just what you need if you're looking for a way to create structure in your life and spend less time worrying about achieving your life's passions and purpose.

Three Things to Know About Paying a Financial Advisor