Mid-Year Financial Check-In: Are You On Track To Reach Your Year-End Goals?

The summer season is winding down and fall is fast approaching. And whether you’re excited for the cooler months ahead or still holding on to the last bits of summer, mid-year is officially here. Now is a great time to slow down and take stock of your entire financial picture and how it’s lining up with your year-end goals. Below are a few ways in which you can check-in with your financial health as summer comes to a close.

Check-In #1: Evaluate Current Debt

Holiday retail sales hit a staggering $719 billion last year, meaning our spending won’t be slowing down anytime soon as we head into the holiday season.1 In fact, people expect to spend around $800 on Christmas presents alone - that doesn’t include holiday parties, decorations, travel, etc.2 With your spending likely to increase towards the end of the year, now is a great time to evaluate any current debt you may have accumulated throughout the year.

You may want to write down all debt currently owed including credit cards, student loans, mortgages and car payments. Be sure to also keep track of the minimum payment amounts and due dates. Once you have everything laid out and organized in one place, you can begin focusing on how to minimize or eliminate certain debts. For example, if you’ve been making regular payments to your credit card company, you could try negotiating a lower interest rate or look into transferring the debt to another company. Seeing all your debt in one place may sound stressful, but it’s an important first step in taking control and minimizing what you can.

Check-In #2: Check Your Credit Score

Can you remember the last time you checked your credit score? It’s possible (and likely) that your credit score is really only thought about when it’s time to apply for a new credit card, take out a loan or make any other large purchases. If you haven’t given it a good look in a while, now’s the time. Your credit scores can give you a decent overview of how your financial health is doing. In addition, it can help make you aware of any potential red flags such as missed payments or unauthorized use of your credit cards and identity theft.

Check-In #3: Readjust Your Retirement Fund

If you contribute to an employer-sponsored retirement fund such as a 401(k) or 403(b), take some time to check in with your account. This is especially important if you set automatic deposits a year or two ago and haven’t thought about it since. In fact, it is especially important to revisit your retirement fund in 2019 because the IRS raised the maximum contribution limit from $18,500 to $19,000 a year for those under 50.3 If you’re heading towards retirement and trying to make the most out of your employer-sponsored plan, you now have the opportunity to save even more in your account.

Check-In #4: Refill Your Savings

With family vacations, weekend trips and summer concerts, enjoying the warmer weather can cost quite a bit. The temptation to tap into your savings is strong, and if you did - you’re not alone. But as we gear up for the holidays, now’s the perfect time to work on filling it right back up. And if you set a savings goal for the year, do a quick progress report. Have you nearly reached your goal? Then you may want to challenge yourself to save even more. And if you’re nowhere near it, focus on adjusting your spending habits to better support your savings goal.

Check-In #5: Rethink Your Goals

Think back on everything that’s happened this year. It’s likely some unexpected events occurred, isn’t it? From unfortunate events like divorce, death or property damage to exciting celebrations like proposals or births, moments large and small can have a significant impact on your financial standings and goals. Revisit the goals you made at the beginning of the year and make sure they are still well-aligned with your current standings. If not, take some time to look at your entire financial picture and future needs, and create new goals that better reflect them.

With a bit of time to prepare, you can enter the second half of the year feeling financially confident and on track to meet your goals. As vacations wind down and school starts back up, find some time to yourself to readjust, reevaluate and rethink as needed to stay on track for the rest of the year.

- https://www.statista.com/statistics/243439/holiday-retail-sales-in-the-united-states/

- https://www.statista.com/statistics/246963/christmas-spending-in-the-us-during-november/

- https://www.irs.gov/newsroom/401k-contribution-limit-increases-to-19000-for-2019-ira-limit-increases-to-6000" rel="noopener noreferrer

6 Step Guidebook to Setting Achievable Financial Goals

We won’t sugar coat it — achieving your financial goals isn’t always easy. But if you don’t create a plan based on your goals, you’re only making it harder on yourself. In fact, American’s with a plan in place are more likely to make positive progress towards achieving their financial goals. In a recent survey, 56 percent of people with a plan in place reported making good or excellent progress towards their savings needs, compared to only 24 percent of those who didn’t.1 As you look to find financial well-being, we’re offering six steps you can follow in creating achievable financial goals.

Step 1: Give Your Goals a “Why”

When it comes to numbers, it can be hard to evoke an emotional response. That’s why it’s important to give your goals a “why” when you can. Placing a reason behind the numbers can be a big motivator in achieving your financial goals. Think about the difference between “I want to pay my student loans off faster” and “I want to pay off my student loans faster so my wife and I can buy a house and start our family.” Remembering why you’re passing up on those concert tickets this month can help make your sacrifices a little easier to make.

Step 2: Make Your Goals Measurable

Ambiguity won’t be your friend as you work to set financial goals. Focus on being as specific as possible instead, your goals should have a measurable and definitive finish line. This will help you track your progress and feel a sense of accomplishment once you achieve your goals. For example, if you have a goal to save money for a down payment on a new car, choose a number. While you may not know exactly what car you want or how much it’ll cost yet, put an estimate to your goal. Instead of saying “I want to save some money and buy a new car next year,” try “I will put $250 in a separate savings account for the next 12 months that will be used as a down payment for a new car.” This provides a clear, definitive goal that you can track month after month.

Step 3: Be Reasonable

You can follow every step in this guide, but if your goal simply isn’t reasonable — you likely won’t attain it. As you look to set a goal, you must evaluate your current financial standings in comparison with your desired financial picture. If you’d like to accumulate a certain amount of wealth by the end of your 30’s, you need to figure out how it can be done. If your current saving and spending habits support this goal, then you’re likely on the right track. But if you’re often spending more than you’re saving, then you may need to either adjust your goal or adjust your current spending habits.

Step 4: Set a Budget

While we mentioned it in step three, evaluating your spending habits is a tip worth repeating. If your spending habits don’t support your goals, you’re likely fighting a losing battle. Create a monthly budget that supports your future financial goals and current needs. A popular budget breakdown is 50/30/20:

- 50 percent on needs (groceries, rent/mortgage, utilities)

- 30 percent on wants (shopping, eating out)

- 20 percent on savings and debt repayment

For example, if your income after tax each month is $4,000, you’d spend $2,000 on necessities like your car payment, electric bill and rent or mortgage, $1,200 on date nights, clothes shopping and weekend trips and $800 would go toward your student loans and savings account. While everyone’s financial circumstances and current needs differ, this ratio can be a great place to start as you look to draft a budget.

Step 5: Balance Short-Term Needs and Long-Term Goals

Money is nothing more than a tool. The reason you set financial goals in the first place isn’t to simply accumulate more money, it’s to accomplish something that’s pertinent to you and your happiness. And while your future happiness is important, it’s crucial to strike a balance between your long-term goals and your needs or wants for today. You shouldn’t be passing on all trips, vacations, home renovations, car buys or celebrations now because you’re saving for retirement 30 years down the line. Yes, your retirement savings is important. But you need to remember to enjoy what you have today as well. And, of course, the same goes for the other way around. Spending all your wealth today could leave you in a tough spot later down the line.

Step 6: Higher Income Doesn’t Equal Success

Are you ever surprised when you hear of celebrities declaring bankruptcy or pro-athletes having to sell their house? It makes sense to think that a higher income level means more wealth and financial success. But whether you make $40,000 or $400,000 a year, it often doesn’t matter how much your income is. Your wealth and the success of your financial goals is dependent, rather, on what you do with it instead. If you make $400,000 a year but spend $500,000 on frivolous expenses, you’re not building wealth or finding financial success. But if you’re making $40,000 and putting a sizeable portion away in savings each year, your wealth is building over time. As you look to set financial goals, remember that it’s not always about how much you have, it’s about what you do it with it that determines your success.

If you have a financial milestone you’d like to start preparing for, it’s important to begin with a plan. Evaluate your current needs and spending habits to develop a realistic goal and plan of action based on your unique financial picture.

Three Things You Can Do About Inflation

Inflation is on a lot of people's minds right now.

And for a good reason.

While we tend to hear about inflation in terms of percent changes in government reports, chances are, you've likely experienced its natural effects in everything from higher prices at the grocery store, gas pump, restaurants, and utility bills.

Prices change constantly, so why should you care about inflation now?

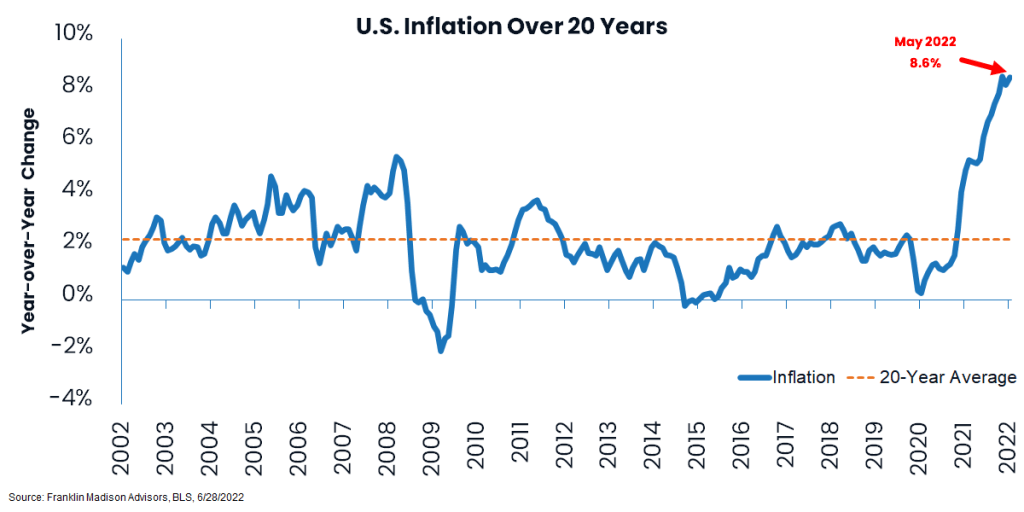

Well, other than the fact that inflation is at a 40-year high, it's crucial to understand that when inflation stays high for a long time, it can potentially erode your ability to secure your future financial independence goals if you do nothing to prepare for it today.

What is inflation?

So, what is inflation? Simply put, inflation measures the rate at which prices change for goods and services you spend money on.

For example, if a pound of apples costs $1.05 today, when it was $1.00 twelve months ago, we can say that inflation has caused the price of apples to change by 5% over the past year.

Inflation is the rate of change, or speed, at which prices rise over time.

Whether you're aware of it or not, inflation is always around. The price you pay for the things you need or want is constantly in flux. It can rise and fall daily, weekly, or monthly.

It's like a car traveling down a highway.

Sometimes, inflation moves along steadily for months or years, like it's on cruise control traveling at the highway speed limit. It can also suddenly speed up over days and weeks when something causes the gas pedal to hammer down.

What truly makes it a matter of concern now is how quickly inflation has sped up and how long it has remained in high gear.

How does inflation affect purchasing power?

Inflation matters because the longer it remains in high gear, the fewer goods or services your money will buy tomorrow.

Economists call this declining purchasing power.

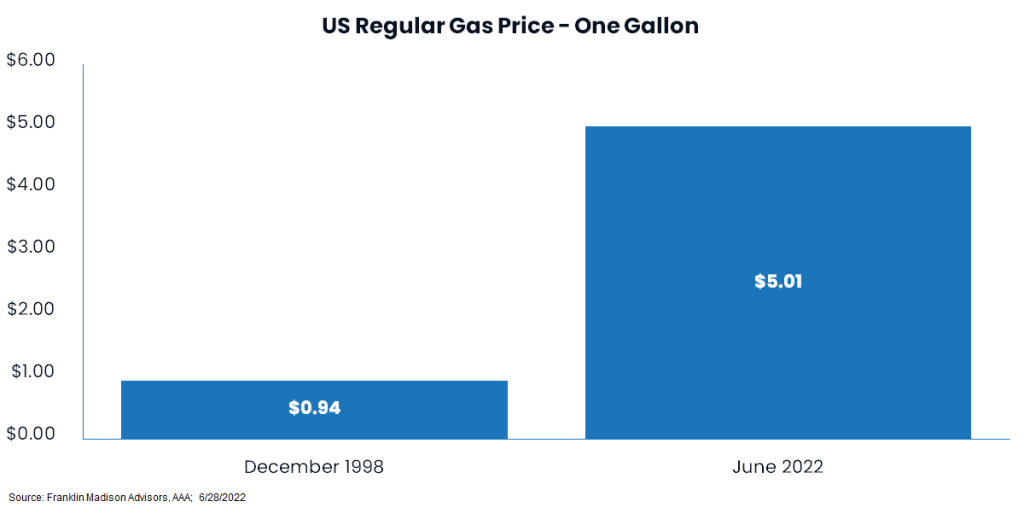

For example, a dollar in the late 1990's purchased one gallon of gasoline. Today, with gas prices around $5.00 per gallon, a dollar today has a fifth of the purchasing power it did over two decades ago!

A dollar is still a dollar, but it doesn't go as far as it used to. At least for gasoline.

And when inflation takes off, you need more dollars to buy the same product compared to a month or year ago.

That's why if you're setting money aside for a big-ticket purchase or plan to live off your savings sometime in the future, you need to be able to anticipate rising prices.

Indeed, understanding purchasing power is essential whether you're socking money away in a 401k to retire later in life or dependent on your savings now to cover retirement living expenses.

When inflation goes up, and purchasing power goes down, you'll likely need to either save more money today, spend less in the future or do a bit of both. Otherwise, you could find your financial independence plans falling short.

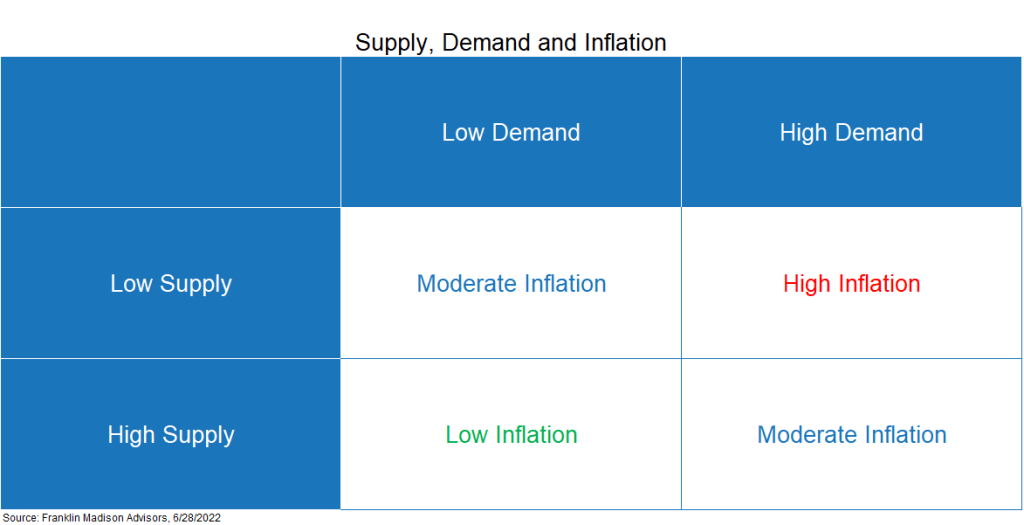

What causes inflation to speed up?

Just like a car needs gas to power its engine and a driver to raise or lower their foot on the gas pedal, no one factor causes inflation to accelerate or decelerate.

Inflation is an interplay between supply (amount of gas in the tank) and demand (driver's willingness to push down on the accelerator).

A full gas tank (supply) won't make a car go fast with a cautious driver (demand) at the wheel.

Likewise, an aggressive driver can only go so far with fumes in the tank.

Let's look at gasoline prices as an example. While some may argue that high prices at the pump are related to oil company profits, there's more at play than pure greed.

From a supply perspective, the fact is that economic sanctions on Russia has led to oil shortages in the West.

At the same time, key oil refiners have shut down because of fires, needed repairs, or maintenance.

From a demand perspective, summer is the travel season. And as more cars get out on the road and air travel picks up, so does oil usage.

When supply is limited, and demand is high, prices tend to go up.

Buying a house is another example. Demand for new homes increased nationally during the pandemic as individuals moved to the suburbs to work from home.

It typically takes about a year or so to build a new home, making supply an issue when thousands of individuals are looking to buy a home simultaneously.

Again, when demand is high, and supply is limited, prices tend to go up.

What role does government money play in inflation?

Now, some people will blame the government for today's high prices.

They'll argue that if the Federal Reserve (Fed) hadn't increased the money supply by printing trillions of dollars, or if it had raised rates sooner and the Treasury didn't send out stimulus checks, we wouldn't be dealing with high rates of inflation today.

To a certain extent, this is a valid argument.

Easy central bank policies arguably made it easier for banks to lend money, thus increasing demand from individuals willing and able to make large expenditures, like a new home or car.

Stimulus checks also made it easier for people to purchase goods or services they otherwise may not have needed during the pandemic, thus increasing demand at a time when economic lockdowns constrained global supply chains.

While this argument makes for a simple explanation, the truth is that the story is much more nuanced than can be explained by any one government policy.

That's because the rise in food and energy prices today arguably has less to do with interest rates or government stimulus than it has to do with supply. While government policies have added to the demand side of the equation, the supply of raw materials and finished goods sourced from around the world is still in short supply.

It's not just the government's fault. To be sure, today, we're dealing with a perfect storm of artificially too much money chasing artificially too few goods.

What can be done about inflation?

So, if inflation is seemingly speeding out of control, can't someone stop it? The truth is, there's only so much the government can do to halt inflation.

The Federal Reserve has raised its policy rate in a bid to slow down demand by making money more expensive to borrow and thus slowing the economy. But with war raging in Ukraine, ongoing Covid lockdowns in China, and other challenges, supply-side challenges likely will keep inflation elevated until those issues are resolved.

Fortunately, some businesses have raised wages to help workers offset higher living costs. However, most firms are not entirely altruistic, making up for higher wages by raising the price of their goods and services. This behavior could introduce an entirely new complexity to the inflation discussion. But, that's a topic for another day.

Three things you can do about inflation

For now, inflation matters because it can affect your ability to maintain your standard of living now and into the future.

There's not a lot we can do to affect the declining purchasing power of a dollar. However, you can mitigate its effects by:

1) holding just enough cash to help you sleep well at night,

2) putting excess cash to work in assets that move with inflation and

3) ensuring that you're saving and growing enough money today to make up for a declining purchasing power in the future.

Hold just enough cash to sleep well at night

Setting cash aside during this time of economic uncertainty is essential to weathering a financial setback.

However, keeping too much cash on hand could leave you with a reduced purchasing power of your savings.

For example, let's assume that you have $10,000 in a savings account that pays you interest of 1.00% per year. We'll also assume that inflation averages 5.00% over the year.

How much purchasing power do you have at the end of the year? If you said $10,100 you'd be wrong.

While you earned $100 in interest, inflation reduced your purchasing power by $500, with inflation running at 5% during the year.

That's why if you want to preserve the inflation-adjusted value of your savings, you'll need to put it to work in assets that can protect your purchasing power.

Put your money to work in productive assets

Where else can you put your money if a savings account alone won't protect against inflation? Consider your investments.

A diversified investment portfolio has historically been shown to be a hedge against inflation. Why?

Well, a key reason being is that the price paid for a stock today is often in anticipation of the underlying company's future earnings potential. And with firms increasingly passing rising costs on to consumers, corporate earnings have the potential to rise with inflation over the long term.

At the same time, bondholders demand a return on their investment that will compensate them for their time, investment risk, and inflation.

While stocks and bonds offer a degree of inflation protection, consider holding a mix of these assets in a diversified portfolio to reduce investment risk.

Ensure that you're saving enough to account for inflation

Finally, to our earlier point, inflation could leave your retirement savings goals falling short if not adequately accounted for. Indeed, if you want to secure your future financial independence when inflation is on the rise, you'll likely need to evaluate whether you need to save more money, reduce your spending or do a little of both.

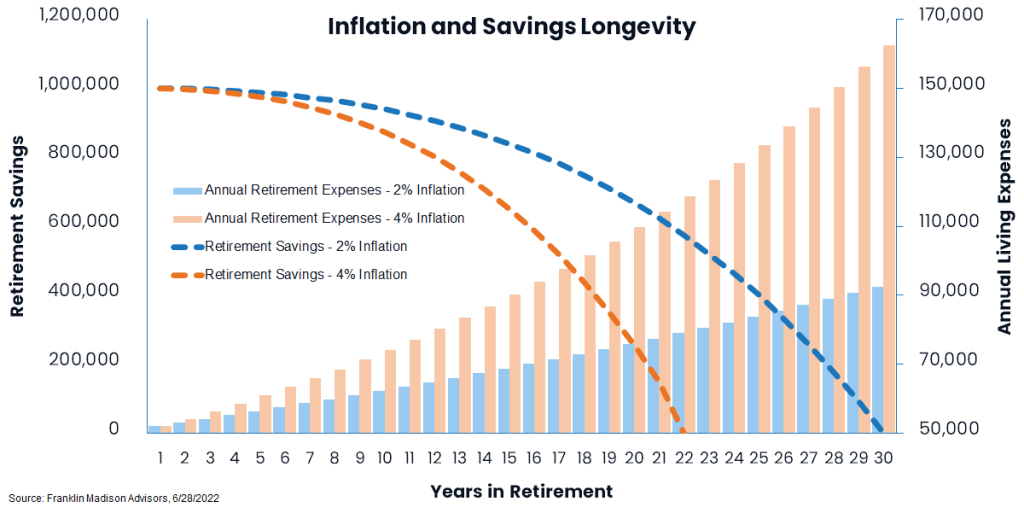

Let's look at an example of how higher than expected inflation could alter the size of your retirement savings nest egg:

We'll start with a base set of assumptions that at retirement, you'll need roughly $50,000 per year to cover living expenses for the next 30 years. We further assume 2.0% average inflation and 5.5% average portfolio returns throughout retirement. At this rate, you'll likely need to have saved one million dollars to cover your costs.

What happens if inflation comes in faster than 2.0%? Well, if inflation turned out to average 4.0% instead of 2.0% over your 30 years in retirement, your million-dollar nest egg could go to zero in just over twenty years instead of thirty years.

To overcome this shortfall, you'd likely need to save an extra $280,000 before retiring, reduce your retirement spending by $10,000 annually or delay retiring by six years.

That's why periodically revisiting your financial plan and clearly understanding the effects of inflation on your expected future income need is essential to maintaining your standard of living and not running out of money in retirement.

Make no mistake, inflation can be a serious threat to your financial independence plans as it reduces the purchasing power of your savings.

Understanding the effects of rising inflation, putting your money to work in productive investments, and formulating a game plan to address declining purchasing power is essential to securing financial independence.

If you do nothing to mitigate this inflation threat, you could find your savings falling short of your desired standard of living later in life.

What is Lifestyle Creep + 4 Ways to Avoid it

Lifestyle creep is something that’s simple to define, easy to see, yet hard to avoid. Especially prevalent amongst young professionals, lifestyle creep is a hurdle many face in saving for their short- and long-term goals, like retirement. Below we’ll discuss what exactly lifestyle creep is and four ways you can work to avoid it.

What Is Lifestyle Creep?

Lifestyle creep is the idea that as your income rises, so does your spending. It’s often a naturally occurring financial issue, typically taking place gradually over long periods of time.

For example, if someone’s yearly salary rises from $40,000 to $50,000, they may be inclined to eat out more, take an extra vacation, update their wardrobe, move to a new apartment, etc. The problem with lifestyle creep is the lack of putting that extra income toward retirement and spending it all instead. That means that while someone is earning more, they’re not saving more.

Four Ways to Avoid Lifestyle Creep

If you’ve fallen victim to lifestyle creep, you’re not alone. And there are ways in which you can work to combat this financial phenomenon year-after-year.

Way #1: Compare Your Personal Inflation Rate to the CPI

An effective way to figure out if you’ve succumbed to lifestyle creep is to figure out your personal inflation rate and compare it to the Consumer Price Index (CPI), which is the inflation rate set by the government.

Take a look at your spending from last year. Say, for example, that you spent around $60,000 last year, and this year you spent around $65,000. Your personal inflation rate from last year would be 8.2 percent. If the inflation rate from last September to this September was 1.5 percent, we can easily see your spending is well beyond simple inflation adjustments. That’s a pretty big sign that you’ve experienced lifestyle creep.

Way #2: Make a Budget

The big thing to understand about lifestyle creep is that it’s different for everyone because it’s all relative to how much you make versus how much you keep. If you’re increasing your spending significantly but still putting a sufficient amount away towards your savings and retirement, then you aren’t outspending your earnings. A good way to do this and avoid lifestyle creep is to make a budget. Building a budget and tracking your spending is an eye-opening way to see where all the money is going and how easily small purchases can turn into significant spending.

Way #3: Plan For Your Next Promotion

Seeing your paycheck increase significantly after a promotion or salary increase is exciting and exhilarating. But if you go into a significant salary increase without a plan, that extra cash could start burning a hole in your bank account. Before temptation strikes, come up with a game plan for your new earnings. Decide what percentage of your increase you’ll be putting directly into savings and how much you’ll be leaving as new discretionary income. Move forward with your plan as soon as the increase goes into effect, making the transfer into savings automatic if possible. This way, you won’t even have to decide month after month whether to save or spend.

Way #4: Don’t Forget to Enjoy Your Earnings

You work hard for promotions and salary increases, and you should get to reap the reward of your efforts. Don’t try to deprive yourself completely when you receive a pay increase, especially when you’re creating a new budget that’s adjusted for your new salary. Give yourself a little wiggle room to spend, and practice spending with intention. For example, instead of making a couple of impulse purchases here and there, save that extra money to spend on a weekend trip with your loved one.

Lifestyle creep can occur so effortlessly that you don’t even know you’ve experienced it until you look back and assess your previous spending. And while receiving more money month-after-month is exciting, the key is to focus on saving what you need to for retirement and other large financial goals before spending your extra earnings.

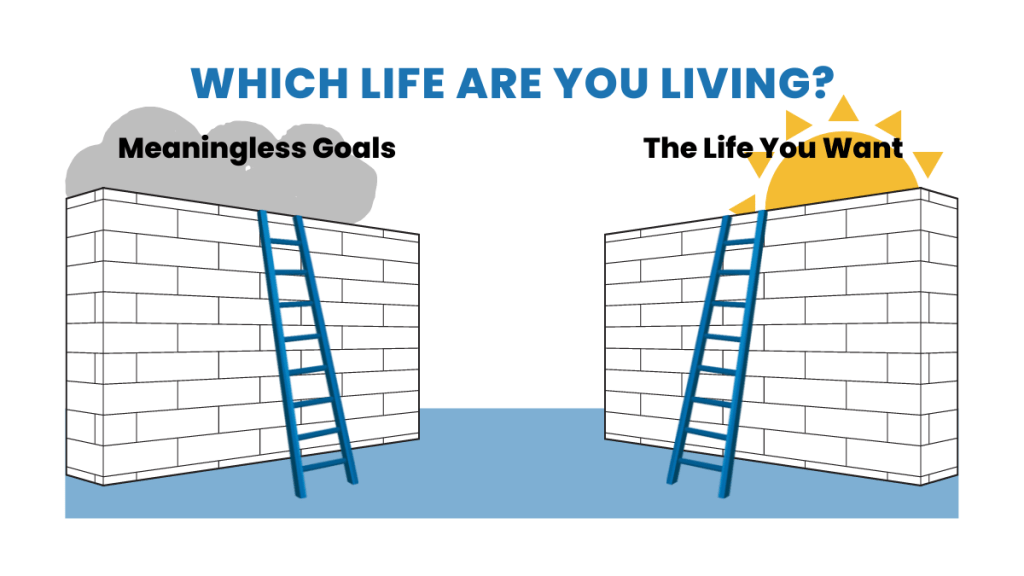

Are Your Financial Goals Meaningless?

Most driven individuals on their path to financial independence mastery know that you need goals to get to the next stage in life. And when it comes to money, many individuals have plans to increase their earnings ability, improve their lifestyle or save for long-term financial security. Nevertheless, even the most ambitious individuals quite often find that their goals fail within weeks or months into their endeavor. Why? Because they set meaningless goals.

So, what is a goal? A goal is a future or the desired result that you envision, plan for and commit to achieving. Many well-intentioned individuals set specific, measurable, actionable, realistic, and timebound (or SMART) goals. And goal-setting can be as simple as striving to wake up at 4 am each morning to exercise for 15 minutes so you can lose five pounds in a month or as ambitious as starting a business from the ground up.

When viewed in isolation, a well-defined financial goal may appear virtuous or valid on its surface. But, when it's out of context with what's essential to you, your goal likely will become meaningless and fail because it's not aligned with what matters most in your life. Certainly, determination to achieve an objective may initially propel you towards your aim, but soon enough, willpower fatigue likely will set in, and you'll probably end up reverting to old financial habits.

Alternatively, you could push toward your financial goals on willpower alone, mistaking effort and progress as measures of success as you propel forward only to find that the object of your intention is hollow or unappealing once you've attained it.

Goals in and of themselves are meaningless. They're simply a means to an end. What gives a goal meaning is its transformative power to shape and change who you are so that you can have the resources you need to experience a life worth living.

Why Do People Set Meaningless Goals?

So, why would someone set out to pursue a meaningless goal? Well, some individuals attain disappointing outcomes because they fail to take the time to understand what they want from life before creating and getting after their dreams. Thomas Merton, an American Trappist Monk, once said that "people may spend their whole lives climbing the ladder of success only to find, once they reach the top, that the ladder is leaning against the wrong wall." In a similar vein, Steven Covey was quoted to say that "if the ladder is not leaning against the right wall, every step we take just gets us closer to the wrong place faster."

In his book, The Second Mountain, David Brooks uses the analogy of climbing a mountain to pursue goal fulfillment. Some individuals start out in life intending to scale a mountain summit to reach some level of material wealth, comfort, or simply to be "happy". After speaking with hundreds of people from all walks of life and studying philosophy, religion, psychology and sociology, Brooks' findings show how even the most accomplished athletes, artists, business leaders and many others struggle with drugs, alcohol or other vices to make up for the hollowness of their lives even after acquiring status or wealth that many in society today would yearn for.

Whether you view goal setting as climbing a ladder or summiting a mountain, the fact is that if you haven't clearly defined why you're pursuing the goals you've set out for yourself, a time likely will come when you end up with frustration and regret. Indeed, a time could come where everything you have achieved will seem as though it were for nothing. And to be sure, society today is littered with broke lottery winners, miserable millionaires, and accomplished actors and musicians who have ended their lives in desperation.

The truth is that many well-intentioned individuals chase meaningless goals not because they're sadistically pursuing failure. More often than not, this outcome has to do with the fact that their goals were not their own. They're just doing what seemingly everyone around them is doing or wants them to do.

This behavior typically occurs when we live a financial script handed down from family or culture early on in life, like going to school, getting a good job, buying a house, getting married, having kids, and saving for retirement. It's keeping up with the Jonses or living the American Dream, right? Well, when you're setting goals to live someone else's financial scripts, there's a good chance that you could wake up lost, disappointed, or simply unfulfilled. So how can you set meaningful financial goals?

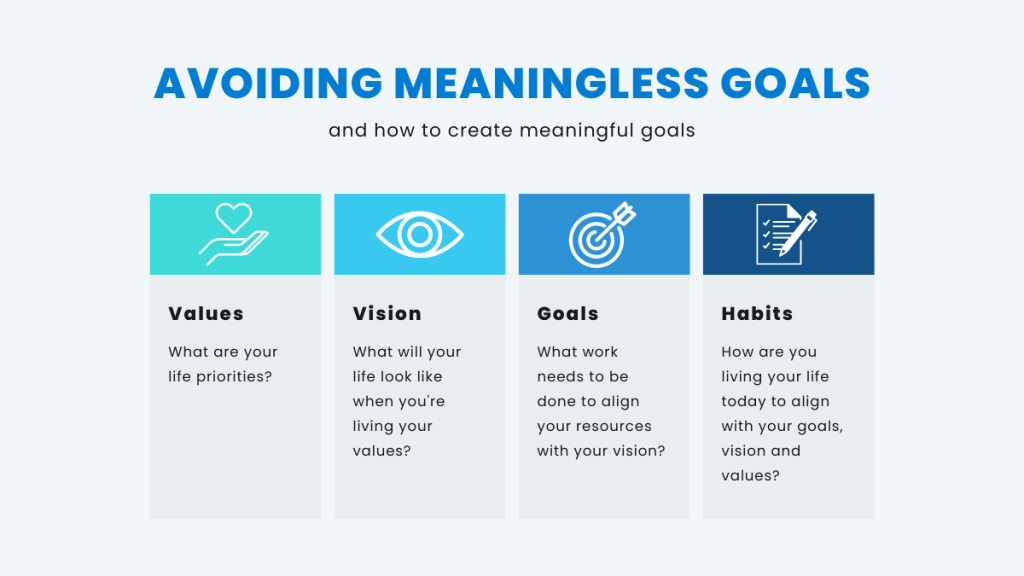

The Antidote for Meaningless Goals

First, start by understanding what's essential in your life, define a vision that aligns with your values, and then create goals that align with your vision. Isn't this all fluff when we should be talking about making money? The short answer is no.

Make no mistake, the word "vision" seems like another fancy buzzword because it's become so overused in today's culture. That's why when you hear the word "vision", you might think of business leaders who are intent on using ten-dollar words like "vision statements" to represent ten-cent ideas or self-help gurus who espouse having vision as a panacea for overcoming personal or professional underperformance.

But the truth is that in its simplest form, the word vision represents a picture or a snapshot of your desired life destination. It's the creative process of developing a mental movie of your future potential life outcome. Vision is about being clear about where you're heading; goals are how you get there. That's why without vision, goals are meaningless.

Now, you may be asking: "Isn't vision and goal the same thing?" You might even ask, "I envision myself having saved more money in ten years than I have today; isn't that a vision." Well, vision is different from goals because it marks what happens after you've crossed the finish line. If your goal is to have more money in ten years, how would you use that money? What would change in your life as a result of having acquired more wealth? A goal, like saving more money in the coming ten years, sets out a specific set of tasks necessary to accomplish that outcome. The vision, on the other hand, is what you will do with that money and how your life will change once you have that money in your hands.

What Does Vision Look Like?

If you're still trying to wrap your head around the concept of vision as it relates to your finances, take an example from Pele. Now, Pele is arguably one of the greatest soccer players in the world. And he attributes his success to the practice of visualization. If creating a vision is imagining your future life outcome, then visualization is the active practice of rehearsing that story in your mind. That's why one hour before each game, Pele would go through his own mental movie, starting with when he was a child to his current moment right before a game, recalling how he felt playing soccer as a child and how he needed to play his next match as a way and to evoke positive emotions and mentally prepare himself for success on the field.

Thinking more long-term, some individuals find it helpful to create vision boards by physically laying out pictures of places, people, or destinations they'd like to see take place in their lives. Now, to be clear, we're not talking about the "law of attraction" or positive thinking type of board here. Simply put, it's a physical board filled with a collage of pictures representing how you'd like to see your career, family, health, travel, or social situation play out in the future. The collage itself is a physical representation of your intentions. It's there to remind you why you're getting up in the morning. You're still going to have to get at it and do the work to make that vision a reality!

At first glance, your initial response may be to say, "What's the point in all of this? I'm not looking for some path to enlightenment here. All I want is to save enough money to buy a house, put my kids through college and ensure that there's enough money to cover my needs for the rest of my life." Now, this is a valid point, but how much money is enough? Let's assume for a moment that you've accomplished these goals. Then what? Well, take a tip from Disney. No, not Walt Disney. We're talking about his brother Roy.

When we think of Disney, more often than not, we think of its founder, Walt Disney, the creative mind behind the media company. Few people know, however, that it was Roy who was the operations genius that turned the company into a profitable empire. And Roy once said that "when your values are clear to you, making decisions becomes easier." Put differently, when you're clear about where you're going and understand what the destination looks like, you instinctively know what goals need to be set and the resources you'll need to achieve that result.

Intention: It's What You Need to Create Your Vision

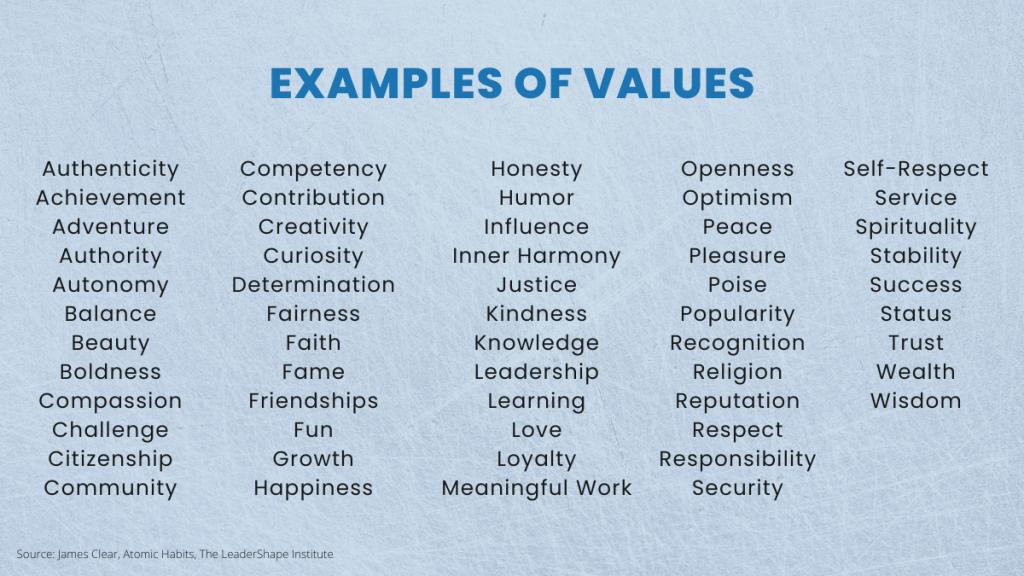

So, how do you create your life vision? To know what you want your life to look like, you'll first need to take the time to understand what's important to you and how you want to spend your time. This journey begins by identifying your top core values. In his book, Atomic Habits, author James Clear shares a list of values he prepared in collaboration with the LeaderShape Institute.

In his book, Clear describes how he identifies five core values to focus on and then prioritizes the short-list. After that, he aligns his daily practices to align his life with his values. Once you've identified which values you want to give your time to, then take the time to create a vision for how your life will change in the future as you begin to focus on your priorities.

Again, vision represents a picture, or a snapshot of your desired life destination. It's the creative process of developing a mental movie of your future potential life outcome. Vision is about being clear about where you're heading, goals are how you get there. This brings us to our final point: setting your goals.

Goal setting is the process of identifying what work needs to be done, the financial resources you need, and who you need to become to close the gap between where you are today and your ideal life vision. When approached correctly, this goal-setting process should withstand the ebbs and flows of near-term uncertainties when they're grounded in your vision and values.

When it comes down to it, spending the time to create your vision is an act of intentionally designing your life. The truth is that few individuals want to take the time to be introspective. They want a quick fix or rely on others to tell them how to do it. But if you want to avoid pursuing meaningless financial goals, you'll have to start by doing the work to understand who you are, what's essential to you and then creating a vision for how you want your life to unfold. Doing so will naturally lead to creating meaningful goals and move you further down the path to mastering your financial independence journey.

Finances: The No. 1 Reason Americans are More Anxious Than Ever Before

As we get older, more and more expenses end up on our plate. From mortgages to car repairs, it can feel like there are endless bills to pay. And as we all know, with more bills, comes more pressure, anxiety and stress. In fact, the American Psychological Association found that money is Americans’ number one stressor.1 Finances have remained at the top of the list since the survey began in 2007.2

When it comes to stress, the numbers don’t lie. The Proceedings of the National Academy of Sciences conducted a study that evaluated heart health changes before, during and after a recent financial crisis and found that during the recession, both blood pressure and blood glucose levels increased in respondents, signaling a worsening in heart health.3

While many of us dream of being financially secure, most of us can agree that traditional education in our public schools does not properly equip us with the knowledge and resources necessary to be effective financial decision-makers. There seems to be a growing gap between financial literacy and our population, causing many people to lose hope and get trapped in a deeper hole of debt. However, when it comes to money, there are four ways you can more effectively manage your finances so you remain in control of your spending habits.

Tip #1: Automate Your Savings

It can be difficult to set aside money every month, especially after you’ve been anxiously awaiting to get your paycheck. If you’re someone who struggles with putting money away, consider setting up an automatic transfer from your checking account to your savings account each month to make sure that no matter what, you’re continuously growing your nest egg. Whether you want to be prepared for any emergencies that may come up or have a dream of buying a house one day, adding money to your savings account every month — even if it’s only $100 — can get you closer to the financial stability you need to feel confident about your future.

Tip #2: Stay Away from Impulse Purchases

With so many products out there — ranging from new gadgets to the latest must-have accessories — it can be difficult to put a cap on your spending habits. Instead of putting yourself right in front of your guilty pleasures, consider putting your money towards experiences, rather than material items. If your favorite past-time is going to the mall, swap window shopping with a picnic out in the park or a day out at your local museum (some museums offer discounted prices over the weekend). While retail therapy may seem like the solution to your problems, oftentimes, you end up feeling worse than if you had spent your time making memories instead. With these memories, your craving for consumerism may gradually die down, leaving you with more time to enjoy the simple pleasures in life.

Tip #3: Focus on What You Can Control

While it’s difficult to effectively plan ahead for every single expense we’re going to have, you can at least have an initial game plan for where your money is going to go. Theoretically, every month, you know you’re going to have to pay rent or a mortgage, buy groceries, pay other utility bills and fill up on gas a few times. So, after you get your paycheck, subtract all of these expenses from your total amount. This will give you a clear idea of how much “fun” money you have to spend each month. And, if you plan to put some money into your savings account, you’ll want to make a note of that too. The purpose of this exercise is to make yourself more mindful of the money you’re spending each month. When you know — without a doubt — certain specific expenses are going to come up, you can start planning ahead to make sure you’re not spending more money than you have.

Tip #4: Be More Goal-Oriented

For some people, the thought of having a goal can be terrifying as it means there is a chance they might fail. However, if you never set goals for yourself, you’ll never have complete control over your financial life. To get started, begin with a realistic goal that can ideally be achieved in less than five years, such as paying off your credit card debt or student loans. Once you’ve identified what you want to accomplish, write it down.

Oftentimes, the simple act of writing down your goals can make it feel more real, therefore making you more accountable. Next, create a rough timetable of how you are going to achieve your objectives. This timetable could include information such as how much money you’re going to save every month, as well as milestones for each payment you’re going to make. Over time, you’ll begin to gain more confidence about your finances, in turn leaving you feeling more in control — and capable — of managing your money on your own.

- https://www.apa.org/news/press/releases/2015/02/money-stress

- https://www.marketwatch.com/story/one-big-reason-americans-are-so-stressed-and-unhealthy-2018-10-11

- https://www.pnas.org/content/115/13/3296

6 Financial To-Do's for New Parents

Having a new baby is a much-anticipated event. While growing a larger family brings added joy and love to your household, it can also wreak havoc on your finances if you don't properly plan. Being prepared financially can go along way to reducing stress and allowing you to enjoy the new life that you are bringing into the world. To help you get started, below are six financial to-do's that new parents should consider.

1. Figure Out Your Health Insurance Coverages and Processes

Even if you have good health insurance coverage, the bill for having a baby can be an expensive one to pay. When you find out you are expecting, contact your insurance company and get a basic framework for what portions of the physician and hospital costs are covered and which ones you will need to pay out-of-pocket. Even though the determined amount is only a ballpark figure, it can help you set a goal to save, so that you don't get underwater with medical bills after your new bundle of joy arrives. If you have a health savings account, be sure to adjust it so that you will have as much as possible towards your medical costs while enjoying the tax break on your paycheck. When contacting your health insurance company, it may also be a good time to determine the process to add your new little one to your policy as well.

2. Create a Baby Budget

Even if you have a fairly well-laid out budget, you will need to make changes to it to account for the additional cost of your newborn. If you plan on making payments for medical expenses, you will need to include that in your new budget as well as diapers, feeding supplies, clothing, and doctor visit costs. You may also want to consider starting your budget when you find out you are expecting and including a section where you work in the expenses of high-cost baby items such as a stroller or crib. If you plan to return to work, you will need to estimate your child care expenses as well.

3. Make Any Necessary Insurance Adjustments

If you have a life insurance policy, you will probably need to increase the value to have enough for the care of your child in the event something unexpected occurs. If you don't have a policy, now is the time to get one so that you can ensure your family is protected if you are no longer around. It is also a good time to address any other policies, such as disability insurance, checking all of the amounts to make sure that you and your new family are fully covered.

4. Make a Financial Plan

Find out what your employer covers for maternity or paternity leave and make sure to include savings in your budget so that you will have the amount of lost income during this time saved up. This will help you alleviate any strain to your budget after your little one arrives. If you don't plan to return to work, or plan to work only part-time after your leave, you will need to create an adjusted budget and make other adjustments to bridge the gap that your loss of income will have.

5. Start an Education Fund

While it may seem like college is a long way away, it can sneak up on you in a financial sense. College tuition is one of the largest expenses that families will face when raising their child and all too often savings fall short because many parents don't get started until later on in life. Starting early will help your money grow faster, reducing the amount that you will have to put into the account in the end.

6. Start or Increase Your Emergency Fund

It is always critical to have an emergency fund. This way if you suffer a loss in income, an expensive event, or unexpected major repair, you will have the funds to cover it without having to fall behind in bills or borrow against your assets. If you currently have an emergency fund, you will probably want to increase it as your financial need will be greater with a new baby.

Get your financial house in order before your little one arrives, so you can relax and enjoy your new addition without having to stress over your monthly bills.

Sole Income Earner: Tips to Surviving the Pressure

So you're not a "DINK." If you aren't familiar with that phrase, it means "dual income no kids." Those types of families are some of the most financially stable because obviously they have two steady incomes coming into the household and they also don't have the financial responsibility of having children to take care of. Sounds pretty ideal, right? But...

If it's just you as the sole income earner in your life, you can easily thrive and succeed with some key pieces of advice. Because honestly being a sole income earner means that all the bills, debt, monthly expenses and anything else miscellaneous you might need falls on your shoulders. That can be a pretty heavy burden to stress over at times.

Let's take a look at, regardless of your circumstances, how to survive as a sole income earner with these five best tips for feeling more financial secure in your life.

Tip #1: Have a Detailed Monthly Budget Set

People tend to slack on budgets, mainly because they don't like seeing the facts and figures written on paper in black and white. Makes that five dollar Starbucks Latte each day look like a high expense when you write out the monthly cost, right? Having a detailed monthly budget set out actually helps you focus on what's coming in and what you spend. If you're not making one out each month, you should. Granted things are going to be on there every month, like rent or mortgage payments, utilities, your smartphone, and any student debt you might have, but sitting down each month and factoring in additional things that you know are coming up will help you stick to your budget so that you don't run out of funds.

Tip #2: Share Expenses Where You Can

This is a great tip. Even though you are a sole income earner that doesn't mean you can't share expenses where you can with friends or family. That monthly Netflix bill? Split it with a buddy and save yourself seven bucks. Up to four different people can use the same account. Little things you can save on add up at the end of the month so don't underestimate splitting the cost of things when you can.

Tip #3: Have an Emergency Fund

This is very important in case you become ill or other life events pop up. You want to ideally have at least six months of expenses saved in the bank. If that's too overwhelming aim for at least three months of expenses.

Tip #4: Pick Up Gig Work

It's a gig economy now folks and the best part is that for sole income earners there are always extra ways to make more money. Become a dog walker on the weekends, play out with a band, do some contract or freelance work within your field of expertise. The point is that by using your skills you can always figure out a way to make additional funds.

Tip #5: Relax!

Money is stressful. Bills are stressful. Life is stressful. You get the point. Try to relax and know that you are a fiscally capable person. You can be a sole income earner and survive. If you find that money troubles are on your mind a lot talk to a financial planner that can help to set you on the right path.

Crush Your Financial Resolutions by Becoming Rather than Doing

Who doesn’t like a fresh start? The beauty of New Year’s Resolutions is that we all have an opportunity to fully commit to losing weight, getting organized, or finally saving more money at the turn of the calendar year.

In fact, resolving to change one’s life for the better is a tradition that goes back millennia, starting with the ancient Babylonian 12-day New Year’s celebration. During the Akitu festival, Babylonians promised the gods to return borrowed items and pay down their debts. In more recent developments, some historians note clippings from an 1813 Boston newspaper documenting what could be considered the first contemporary use of the “New Year’s Resolution”:

“And yet, I believe there are multitudes of people, accustomed to receive injunctions of new year resolutions, who will sin all the month of December, with a serious determination of beginning the new year with new resolutions and new behavior, and with the full belief that they shall thus expiate and wipe away all their former faults.”

Whatever the origin of this tradition, the fact is that many of us will create financial resolutions in the coming days only to find those well-intentioned goals falling short soon after they’re conceived. One study from sports company Strava, using over 800 million user-logged activities in 2019, found that individuals are likely to give up on their fitness goals by January 19 – less than three weeks into the start of the New Year.

Another study from Scranton University found that only roughly 19% of individuals keep their resolutions for the year. The data go on to show that the majority of New Year’s resolutions are abandoned by mid-January, confirming findings from many different studies.

Whether you want to admit it or not, the chances are that the work you’re about to put into one or more of your financial resolutions this year likely will soon end in frustration and disappointment. So, what can you do to ensure that your financial resolutions stay on the right track heading into the New Year? Well, one way is to focus your goals on “becoming” rather than “doing.”

Becoming Rather than Doing

Let’s face it: the past two years have derailed many of our New Year’s resolutions and life goals as we’ve rightfully focused on doing everything necessary to keep ourselves and our loved ones safe. Even so, heading into year three of this healthcare crisis, many of us have a choice to set our sights on a bigger goal of thriving financially rather than surviving in day-to-day uncertainty.

While external circumstances can be a reason for goal failure, they can also be an excuse for not getting to the heart of what’s preventing long-term success with your financial plans. And quite often, that roadblock is being focused on “doing” the work necessary to achieve a goal, rather than first taking the time to understand who you need to “become” to make your New Year’s Resolution a reality.

Indeed, some individuals will suggest that the way to improve your odds of achieving your resolution is to ensure that you’re defining SMART goals (Specific, Measurable, Achievable, Relevant, and Time-Bound). While SMART goals are important, more often than not, what many well-intentioned individuals miss is what needs to happen before specific goal setting begins. And that is asking yourself: “who do I need to become this year to make my financial resolutions a reality?”

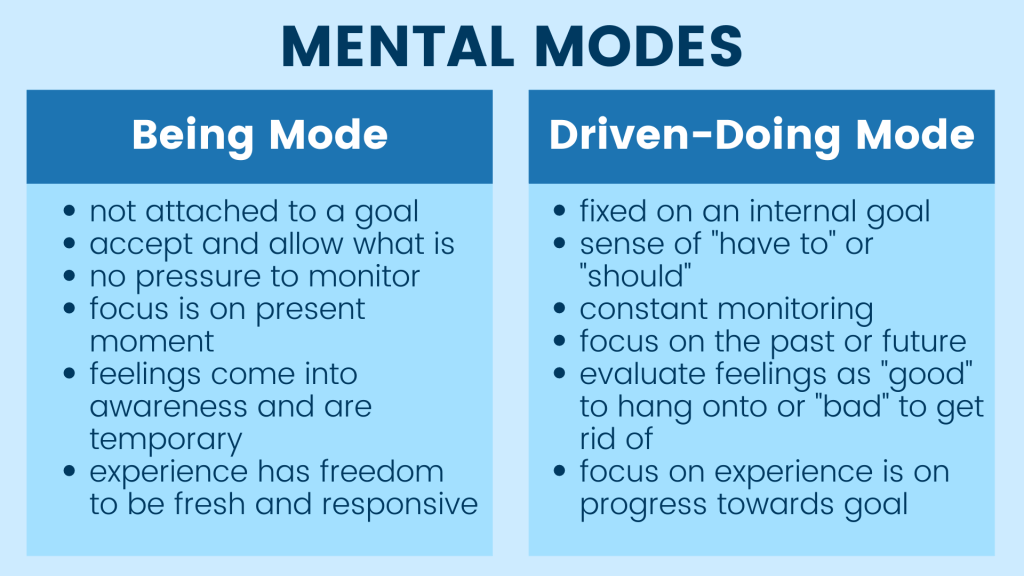

One school of thought suggests that individuals operate in two modes: “Doing” and “Being”. The Doing Mode individual is focused on explicitly defining a goal, then developing a system to monitor their progress and striving for the future outcome they’re attempting to achieve. Whether it’s a reward that you plan to give yourself for accomplishing the goal – or a threat, like the potential shame experienced from friends and family – quite often, this carrot and stick approach sets the stage for a possible resolution failure.

When you shift your approach to accomplishing resolutions from Doing Mode to Being Mode, there’s a broader sense of aligning your daily actions, choices, and behaviors with who you are as an individual. When you approach your goals from a Being Mode, saving more money or investing in a disciplined manner isn’t a task, it’s a way of life – you’re simply doing what’s natural for who you are as an individual. When positive developments or setbacks occur, they’re viewed as part of the natural process of being rather than a good or bad outcome.

This approach to Being is essential because when your New Year’s resolution is at odds with who you believe yourself to be, you’re more likely to experience self-sabotage and reject the “new” habits you’ve identified for yourself. Such a disconnect often leads to what psychologists call cognitive dissonance or the mental anguish of holding two competing thoughts simultaneously. Fortunately, becoming the person who does the desired behaviors is one way to overcome this resistance.

Dealing with Resistance

At first glance, many individuals will dismiss the notion of “becoming” and state that what’s needed is focus, discipline, and a firm commitment to accomplishing goals. While there’s some truth to this notion, again, the reality is that your subconscious mind does not like to engage in habits or behaviors that conflict with your identity.

...once you’ve identified who you want to become, achieving your New Year’s Resolution continues to progress by aligning your daily habits with the outcomes necessary to become the person you need to be.

For example, a New Year’s resolution to become more disciplined with your household spending could quickly become derailed if you don’t intrinsically believe that you’re a good steward of your finances. Indeed, your first misstep after setting a financially prudent resolution likely could prompt negative internal dialogue like, “I’m not good with money” or “I’ll never be good with money, so what’s the point of trying to save.” When this disconnect arises, it potentially could lead you to abandon a worthwhile goal for the coming year.

So, how can you overcome this negative self-talk and self-sabotaging behavior? Well, one way to overcome cognitive dissonance is to either 1) change your thoughts, 2) change your behavior, or 3) justify your behavior by adding new thoughts. In his book, Atomic Habits, James Clear points out how we are likely to meet resistance when we start new habits inconsistent with our self-image.

For example, a couch potato could have an ambitious goal of completing a marathon in the coming year. Certainly, willpower and self-discipline likely will lead to some progress initially, that is, until that individual begins to experience setbacks, like an injury or scheduling conflict, naturally leading them to give up on their goal to run a marathon.

Cast differently, if your goal is to become a runner (rather than accomplishing a running feat, like a marathon), then the daily one-percent improvements that Clear outlines in his book naturally will lead you to get in the kind of shape you need to compete in a marathon.

From this perspective, once you’ve identified who you want to become, achieving your New Year’s Resolution continues to progress by aligning your daily habits with the outcomes necessary to become the person you need to be. How is this accomplished?

Well, Clear refers to the work necessary as the Four Laws of Behavior Change:

- Make it Obvious – list all the steps that need to happen to make your new habit a reality

- Make it Attractive – link your new routine with behaviors that you already enjoy doing

- Make it Easy – simplify your environment to make your new habit easy to accomplish

- Make it Satisfying – create intrinsic rewards when you complete behaviors that align with your identity

Starting with this approach could help you overcome resistance as you put in the work to become the person you want to be this year and accomplish essential life goals. Now it’s easy to say that an individual who wants to run a marathon should focus on becoming a runner first.

So, who does an individual need to become to save more money or become a more disciplined investor? From this perspective, consider becoming the master of your financial independence journey.

Becoming the Master of Your Financial Independence Journey

In the simplest terms, financial independence represents a state of financial well-being where you have enough money to pursue experiences of utmost value. Unless you’re already retired or anticipating a financial windfall, becoming financially independent requires a daily discipline of creating, growing, and preserving financial wealth.

...a deliberate lack of understanding of what intrinsically motivates you might leave you feeling stuck in a perpetual cycle of earning and spending more but making little headway towards long-term financial goals.

Considering the journey itself, the path to mastery (financial independence) forces you to think outside of the constraints of the money scripts presented to you by other people. Indeed, pursuing those experiences that satisfy feelings core your value system can activate higher levels of intrinsic motivation and potentially reduce the yo-yo effect of unconscious savings and spending decisions.

What’s more, the journey itself becomes transformative. For example, each step in the wealth-building process (creating, growing, and preserving wealth) serves an explicit role in helping you move toward financial independence.

Each of these steps requires you to learn disciplines that enable you to build wealth for the long term. And because the knowledge you’re gaining serves an intrinsically defined purpose, its application likely will have a more profound impact on your achieving financial independence than learning money management techniques simply for the sake of knowledge or to mark off a completed resolution for the year.

Many individuals see their financial choices as discrete win/lose outcomes when it comes down to it. They think of their behaviors as things that need to be done. And more often than not, people play the game of life not to lose: settling for comfort rather than striving for a goal for which they may fail. They’re looking for quick fixes, temporary relief to get them through their day.

While this approach may work initially, a deliberate lack of understanding of what intrinsically motivates you might leave you feeling stuck in a perpetual cycle of earning and spending more but making little headway towards long-term financial goals.

Whether you’re earning six figures and broke, or simply trying to take control of your finances, doing the work of learning a new financial management technique, determining your “retirement number” or achieving some material outcome may not be the approach you need.

What might better suit your situation and help you stay committed to and crush your New Year’s resolution is reframing your relationship with money, rewriting your money scripts, and becoming the master of your financial independence journey.

Worried About Ukraine and Your Money? Consider these Six Things.

Words seem to fail when attempting to describe the horrors of war currently faced by the people of Ukraine. Since last Thursday, millions of innocent Ukrainians have been displaced and hundreds killed following Russia's invasion of an Eastern European democracy.

Indeed, world leaders have since responded by providing Ukraine with financial and military support while imposing heavy economic and financial sanctions on Russian President Vladimir Putin and his cronies. Today, much of the world looks on with bated breath, hoping for a quick and triumphant victory for the Ukrainian people.

How and when this war ends remains largely unknown. It could end tomorrow or persist for weeks to come. Indeed, we're hopeful that delegates from Ukraine and Russia can find a way to end this war diplomatically. Even so, as we pointed out in last week's note, a seismic shift in the geopolitical status quo could lead to economic spillover effects that likely will impact US households for months or even years to come.

So, this leaves many asking, what do these developments mean for my finances, and is there anything I should do right now to protect my wealth? Well, here are six points you may want to consider when it comes to guarding your money during periods of uncertainty:

#1 Expedite big-ticket purchases

Inflation is likely to stay elevated for months to come as a result of this conflict. If your emergency fund is already topped up (see point #3 below) and you have adequate means to buy a new car, house, or anticipate any other big-ticket cash expenditures later this year, you may want to consider purchasing those items now before they become more expensive later.

While a military confrontation currently is limited to Russian and Ukrainian, globally imposed sanctions could, directly and indirectly, affect imported goods and compound supply chain issues that have recently contributed to inflation's rise to multi-decade highs. That's why front-loading spending within your means today may help you avoid potentially higher prices tomorrow.

#2 Revisit your lifestyle spending and savings plan

While inflation's rise likely will mean higher costs for big-ticket spending, you can also expect to pay more on everyday living expenditures not only over the coming months but also potentially for years. Not accounting for these rising costs could leave your retirement nest egg falling short. Indeed, uncertainty surrounding the implications of sanctions and global supply chain efficiency could broadly affect the cost of keeping the lights on at home, filling up your gas tank, eating out, or even buying everyday staples.

In isolation, these higher expenditures may seem manageable in the near term. However, not accounting how these expenses could remain at elevated levels over the long-term could potentially derail your overall financial independence journey when not considered within the context of your broader lifestyle spending goals. That's why now's a good time to reset future cost of living expectations in the face of higher inflation, recalculate your traditional/early retirement total savings need, and make necessary adjustments today to your lifestyle spending or savings contributions to ensure that your everyday financial decisions keep you aligned with your path to financial independence.

#3 Top up your emergency savings fund

The US labor market remains favorable for workers and job seekers alike by many measures. Indeed, while jobs in specific sectors of the economy are plentiful and wages continue to rise, the fact is that US economic growth is slowing and faces headwinds from ambiguous central bank policy, systemic financial instability, and global military conflict.

While an economic recession is not baked into economists' GDP forecast of 3.5% this year, a policy misstep by the Federal Reserve, a shock to the global financial system or a global military escalation could put downward pressure on US economic activity. That's why if you don't have 6-9 months-worth of cash to cover living expenditures, now may be the time to reconsider big-ticket spending decisions along with how much you spend on non-essential goods and services, so that you can increase your monthly savings or reduce needed distributions from your retirement savings.

#4 Prepare for a smaller employer bonus or limited equity award payout

Even if you feel like your job is secure and your emergency savings are topped off, relying on an employer bonus or equity award payout to cover living expenses may lead to financial disappointment later this year. Generally speaking, firm bonuses are tied to corporate earnings. As evidenced during the Covid-induced recession, when economic conditions soften and earnings decline, employers tend to cut back on incentive compensation in a given year.

Present expectations of weaker economic conditions, combined with many of the risks we’ve already mentioned, likely could weigh on risk asset prices this year. That's why if you're the recipient of equity awards and dependent on ISOs or RSUs to cover a portion of your lifestyle spending needs, you may be in for a disappointment should stock prices decline in the months ahead. Put simply, you may want to reevaluate how much of your household outlays are funded by once-per-year windfalls and consider adjusting your lifestyle spending today.

#5 Avoid timing the markets & increase your home country bias

When it comes to your investments, how markets respond to Russia's war with Ukraine likely will depend on day-to-day developments. As such, we expect market volatility to ebb and flow with the news cycle. Indeed, there are times when you may be tempted to make changes in your investment portfolio when it appears that the news is about to get bad.

Nevertheless, during these times of uncertainty, astute investors stick to their disciplined investment process. Rather than trying to identify an inflection point in stock prices or trying to time the next move in the markets, you'll likely be best served by ensuring that your portfolio is aligned with your long-term goals over the coming years, rather than responding to near-term uncertainties by trying to pick the right securities to buy or sell over the coming days and weeks.

#6 Rebalance international risk exposure

Finally, the Russia-Ukraine war coupled with the potential for further confrontations with China has some investors concerned about holding securities tied to these countries in their investment portfolios. While we continue to advocate for investing internationally, we also believe that now may be a good time to reevaluate your investment exposure to countries where the rule of law or the potential for escalating military conflict may lead to downside investment risks.

We're evaluating the current situation more opportunistically, particularly as it relates to international vs. domestic exposure. Indeed, while Russian securities make up a small portion of emerging market stock and bond benchmarks, China's dominance in traditional EM indices likely may argue for a tactical rebalance from traditional asset class benchmark guidelines. We'll provide further guidance and clarification to our active clients in the coming weeks.

For now, only time will tell whether the current situation will escalate to a broader conflict or settle more amicably. Our hope is that substantial financial and economic sanctions coupled with a solid political resolve from Western leaders will convince Putin to end his military incursion in Ukraine. Until then, we anticipate market volatility to ebb and flow with the news cycle. For now, avoiding the noise, evaluating the six items we covered today and committing to your long-term financial plan will not only give you peace of mind during this time of uncertainly, it may also enable you to continue your journey toward financial independence mastery.