Is Financial Procrastination Derailing Your Life Plans?

What do Willie Nelson, MC Hammer, and Allen Iverson have in common? Well, what their life situations have in common is that it doesn't matter how much you make, but how much you keep.

To be sure, these individuals came into vast fortunes, only to see their wealth dwindle in a short period of time. And certainly, it's hard to believe that these individuals didn't have trusted advisors who urged them to take actions that could help them preserve their fortunes.

But the truth is that there are likely many reasons why these individuals found themselves in their situations, and one reason likely has to do with financial procrastination.

Now, when you hear the word procrastination, you might immediately think of a pejorative, like a bad word or something with negative intent. But the truth is that procrastination simply reflects a subconscious (or sometimes conscious) decision to delay or postpone something you know you should be doing.

Indeed, you've likely experienced a moment where you've procrastinated on crucial financial work, like paying an important bill, balancing your checkbook, or taking care of some financial obligation, and these delays have likely cost you in lost time or money.

And the unfortunate truth is that in our society today, people who procrastinate are often viewed as lazy or unmotivated, which is why so few of us want to talk about this uncomfortable topic. But the fact is that there are many valid reasons why an individual may choose to put off doing an important task, especially when it comes to their money.

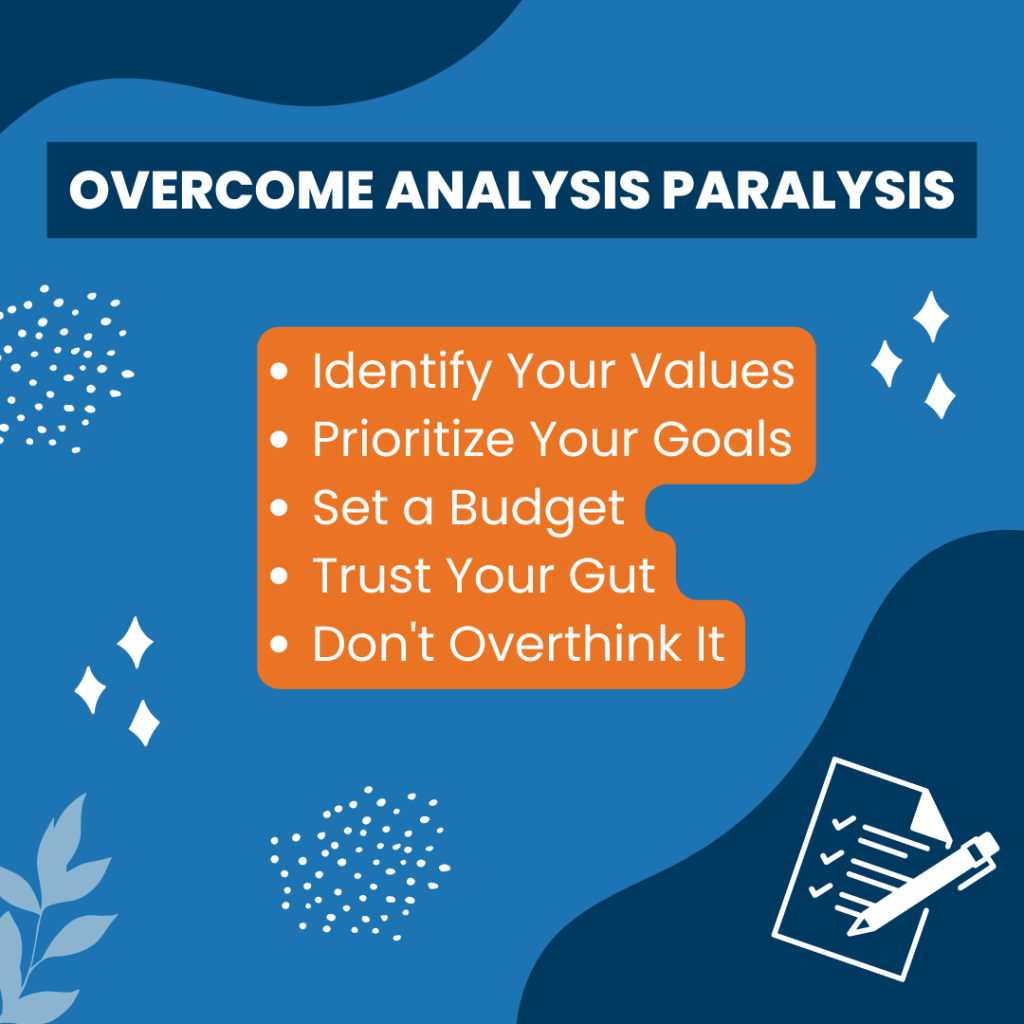

Do you or someone you know struggle with financial procrastination? Do you ever wonder why some people are really good at managing their finances while others get stuck in analysis paralysis and indecision or procrastination?

Well, even if you only occasionally struggle with putting off paying your bills, gaining some insight into this underlying behavior, understanding how to rebound after a setback, and doing the work to maintain your positive momentum can help you stay the course on your path to mastering your financial independence journey.

Some Common Causes of Financial Procrastination

So then, what causes procrastination when it comes to money?

Well, while there are many reasons why someone may be a financial procrastinator, generally speaking, this act could be related to 1) your thought processes, 2) a struggle for instant gratification, or 3) your body's signal that something is just not right.

So as we dive deeper, let’s start by taking a look at your mindset’s role in financial procrastination.

Procrastination and Self Efficacy

Now, when it comes to your mindset, Henry Ford was known to have said that, "whether you can, or you can't, you're right." That's because when it comes to finding the motivation to do what we know we're supposed to do, self-efficacy, or the internal belief we have about our ability to accomplish a task or goal, plays a significant role in our ability to get started on essential tasks.

Indeed, when we have high self-efficacy, we are more likely to take on challenging tasks and persist in the face of obstacles. Conversely, when we're dealing with low self-efficacy, we may be more likely to avoid or delay tasks, particularly those that we perceive as challenging or complex.

That's why in her book, "Mindset: The New Psychology of Success," Carol Dweck discusses how self-efficacy and mindset can influence procrastination.

Dweck explains that individuals with a growth mindset tend to have higher levels of self-efficacy. Indeed, these individuals are more likely to view setbacks and failures as opportunities to learn and grow rather than as a reflection of their own innate abilities. As a result, they are less likely to procrastinate, as they have confidence in their ability to succeed.

On the other hand, individuals with a fixed mindset tend to have lower levels of self-efficacy and are more likely to procrastinate. These individuals may avoid tasks or challenges they perceive as difficult or beyond their abilities because they fear failure and negative feedback.

Therefore, if you find yourself procrastinating, ask yourself if your mindset is holding you back from taking the next steps toward what you know you should be doing next.

The Struggle for Instant Gratification

Another factor to consider when you're trying to identify the underlying factor causing your procrastination is time inconsistency.

So, what is time inconsistency?

Well, have you ever made plans to get up early in the morning, only to find yourself struggling to get out of bed when your alarm goes off? Or how about the last time you made plans to get to the gym on the regular, only to find yourself with other obligations coming up when it's time to go?

If you've found yourself in this situation, then you're likely already familiar with the concept of time inconsistency and how it can influence procrastination.

Now, time inconsistency is a psychological concept that describes people's tendency to make present decisions that conflict with their long-term goals. This means that people often make more favorable choices in the short-term, but that can be detrimental to their long-term interests.

For example, imagine an individual who has a long-term goal of improving their credit score but struggles with time inconsistency when it comes to paying bills on time. They may have the intention to pay their bills when they're due and understand the importance of doing so for their long-term financial goals, but when the time comes to complete their task, they may simply put off the payment in exchange for a short-term reward such as spending money on leisure activities or delaying the discomfort of paying their bills.

Indeed, when it comes to procrastination, time inconsistency can cause people to delay tasks or critical decisions vital to achieving their long-term goals, even if they know that delaying the task will have negative consequences. This likely happens because the immediate rewards of avoiding the task (such as short-term pleasure or relief from anxiety) can be more compelling than the potential long-term benefits of completing the task.

Either way, time inconsistency is just a fancy way of saying that we prefer the immediate benefit of instant gratification over long-term rewards. And when it comes down to it, procrastination can be a coping mechanism for time inconsistency, as an individual delays essential tasks to avoid the immediate discomfort of starting important work. Even so, while it may seem harmless at first, when left unchecked, this behavior can negatively affect their long-term goals and financial well-being.

The Body Relation

One last potential cause for procrastination that we'll explore is looking at what's going on in the body. That's because, in some situations, procrastination, or the act of putting off what we know we should be doing, is often the body's way of telling us that something bigger is going on behind the scenes.

Indeed, psychologist Dr. Stephen Porges, in his Polyvagal Theory, suggests that procrastination is a form of self-protection when viewed in the context of the body's nervous system. Now, what this theory suggests is that inside our bodies, we have a special nerve called the vagus nerve that helps us respond to stress and danger. It has three parts, and each part helps our body react in different ways.

The first part, the ventral vagal, or "rest" state, helps us feel safe and calm. When we feel safe, our bodies can “rest and digest” and give us the confidence to take on challenges and meet new people.

The second part, the sympathetic nervous system, or "fight/flight" state, helps us prepare to fight or run away when we feel threatened. This part of the nerve helps us become more alert and ready to act quickly to protect ourselves. When our minds are in this state, we are more likely to take care of our finances from a place of panic, fear, and anxiety as we realize that a bill is past due.

The third part of the nerve, the "freeze" state, is like a last resort. That’s because when we feel like we can't fight or run away from danger, our bodies can shut down and become very still and quiet. In this state, we're more likely to feel shame, a sense of helplessness, hopelessness, or utterly trapped. In this state, we have an inability to focus and actually get work done.

Indeed, when the nervous system is dysregulated or underactive, we may experience difficulties in social interactions and have a reduced ability to cope with stressors, leading our bodies to physically shut down and produce what looks like procrastination.

Therefore, if you typically have a growth mindset and rank low in terms of impulsive behaviors but still occasionally struggle with financial procrastination, then take a moment to listen to your body and evaluate what's going on in your life.

If there are other things going on, like problems at work, challenges in your personal relationships, health issues, or other situations that are increasing your levels of anxiety, then these factors likely will inhibit your ability to take care of money issues until these matters are addressed.

Steps to Move Past Procrastination

So, now that you understand what might be driving your inclination towards procrastination, the next step to actually moving out of this state and towards your desired financial outcomes involves identifying ways to adapt whether your mindset, instant gratification, or your nervous system are causing you to procrastinate.

Shifting Your Mindset

And what can you do when you find yourself procrastinating on managing your finances and paying your bills because you are dealing with self-doubt? Well, recall that self-efficacy is the belief in one's ability to achieve a specific goal or outcome. When someone experiences self-doubt, they question their ability to succeed or feel uncertain about their competence in a particular area, but there are some things you can do to improve your self-belief and get your finances back on track.

First, you can start by educating yourself about the particular financial matter where you might be struggling. This could involve reading books, articles or taking online courses on topics such as budgeting, investing, and debt management. By learning more about the financial topics that give you anxiety, you can better understand how to manage your money effectively and improve your self-confidence in areas where you might be struggling.

Next, consider whether you're approaching your situation from a growth or fixed mindset. Remember, individuals with a fixed mindset believe that there’s little they can do to change their present circumstances, and are more inclined towards procrastination. And, what can you do if you find yourself in this situation? Well, to develop a growth mindset, you can take several steps based on Carol Dweck's book.

Well, to start, embrace challenges and view them as opportunities for growth and learning. Rather than shying away from complex tasks or new experiences, welcome them as chances to develop your skills and abilities. At the same time, recognize that setbacks and failures are a natural part of the learning process and can provide valuable feedback for future efforts.

Then, cultivate a love of learning and approach challenges with a sense of curiosity and a desire to gain new knowledge and skills. Indeed, take the time to focus on the effort and hard work you put into achieving your goals rather than attributing success or failure to innate abilities or talent.

As you go about this work, you'll also want to be kind and supportive to yourself, even when you encounter setbacks or failures. Dweck points out that developing a growth mindset can be a challenging process, and it's essential to be kind and compassionate to oneself during this journey. That's why she suggests you practice self-compassion by treating yourself with the same kindness and support you would offer a close friend or, if you're a parent, your own child.

Indeed, Dweck goes on to point out that self-criticism and negative self-talk can be detrimental to one's self-esteem and motivation, and can ultimately hinder growth and progress and undermine a growth mindset. That's why replacing negative thoughts with more positive and realistic ones that emphasize your strengths and potential is essential to building a growth mindset. At the same time, be open to constructive criticism, and actively seek out feedback from a trusted advisor and use it as an opportunity to learn and grow so you can improve your ability to prudently manage your finances.

Finally, surround yourself with individuals who encourage and support your growth mindset. This approach could include seeking out mentors and role models who exemplify a growth mindset and can provide guidance and support as you work to develop this mindset for yourself.

Dealing with Instant Gratification

Now, let’s take a moment to talk about dealing with instant gratification.

Earlier, we discussed the trouble with time inconsistency and how it can lead individuals to favor a present bias over difficult long-term decisions.

So then, what can you do if you find that you identify with instant gratification as a leading cause of your procrastination? Well, take a page from James Clear.

In his book "Atomic Habits," Clear provides proven methods for developing healthy habits and overcoming a present bias. And in his book, Clear focuses on creating a system for building habits that are sustainable and effective.

One key takeaway from Atomic Habits is that it's not about making big changes all at once but about making small, consistent improvements over time. This approach means focusing on small changes to your daily routines that will help you gradually move toward your goals.

For example, if you have a hard time getting started with paying your bills or even reviewing your finances on the regular, then set aside a thirty-minute block of time and do as much as you can within that window. Then, take a break and return to your task if you still have work that needs to be done. This approach can help you tackle a big task that might otherwise seem overwhelming in small, bite-sized pieces.

Another point emphasized by Clear is the importance of focusing on the habit-building process rather than just making the outcome the end-all-be-all. Clear emphasizes that building a habit is not just about achieving a goal but creating a system of actions that will help you consistently achieve your goals over time. That's why if you procrastinate when it comes to paying your bills, you may want to reframe this task as a ritual that is performed rather than a task that's marked off a to-do list.

Clear also emphasizes the importance of creating a supportive environment for building habits. This means surrounding yourself with people who will support your goals and help create an environment that makes it easier to stick to your habits.

For example, if you're trying to be more prudent with your finances, then spending time with individuals who like to talk about how much money they make or spend could tempt you to make poor choices and set you back from your financial goals. While you may not need to find new friends (or maybe you do), at the very least, be mindful of how others can affect your own decision-making process.

Lastly, Clear emphasizes that habits are not just about what you do but about who you become. By building habits that align with your values and goals, you can transform yourself into the person you want to be. To be sure, overcoming a present bias, or desire for instant gratification, means consistently evaluating the long-term benefits of achieving your financial goals and why it’s essential to keep your house in order at all times.

So then, from this perspective, ask yourself, “who do I want to become?” How will your life change if you commit to making this new habit of being disciplined with your money and doing what needs to be done at the right time? More importantly, how will people's perceptions of you change, and how would that make you feel?

Support Your Nervous System

Finally, if your financial procrastination is tied to life stressors that are putting your body into a freeze state, then you can take a few suggestions from Stephen Porges to get you moving forward.

Now, you'll recall that according to the Polyvagal Theory, our nervous system exists in three states, 1) rest and digest, 2) fight or flight, and 3) freeze. When we experience trauma or stress, our body's natural response is to activate the sympathetic nervous system, which can result in feelings of fear or anxiety to act or eventually activate the parasympathetic system, leading to a freeze or shutdown when the situation becomes untenable.

This state of dorsal shutdown can feel overwhelming and paralyzing, but there are ways to help our body transition to a more regulated parasympathetic, or "rest and digest" state.

So then, to move out of a frozen state, what you'll need to do is activate your fight/flight system, which is responsible for mobilizing your body to respond to stress and danger. Now, at this point you might be asking, why are we going to a stress response if we're trying to get to the "rest and digest" state?

Well, recall that the nervous system has a primal function to keep us safe. It's like those moments in a National Geographic episode when a gazelle trapped in the mouth of a lion. With nowhere to go, the gazelle goes into freeze mode as a way to cope with the trauma that it’s about to face. But the moment that the lion gets distracted and lets go, the gazelle can snap back into fight mode in its bid to break free and get to safety.

In other words, the gazelle goes into freeze mode to stay safe, but then it first snaps into fight/flight to get away from the lion before it can eventually return to life as normal in the rest and digest phase.

And, so, how do we move between these states?

Well, one way to activate this system is through physical activity or exercise, which can increase your heart rate and respiration, release adrenaline and other stress hormones, and promote feelings of alertness and energy. For example, going for a brisk walk, heading to the gym, or dancing to music can help stimulate the sympathetic nervous system and promote a sense of activation and help move you out of shutdown mode.

Another way to move out of a dorsal vagal state is through social engagement and connection. Polyvagal theory suggests that social engagement, such as eye contact, facial expressions, vocal tone, and touch, can help regulate the autonomic nervous system and promote feelings of safety and connection.

For example, calling a friend, joining a group activity, or participating in a social event can help stimulate the ventral vagal system, which is responsible for social engagement and connection, and promote a sense of safety and belonging. And if you're in a place where you'd rather not engage with others, getting out into the public to people-watch can be a safe way to reset your nervous system as well.

Finally, breathing exercises and meditation can also help move out of a dorsal vagal state by promoting relaxation and reducing stress. Slow, deep breathing can stimulate the vagus nerve and promote feelings of relaxation and calm.

Keep the Momentum Going

Alright, so now that we've identified potential factors that could be causing your financial procrastination and have offered some suggestions for overcoming them, let's talk about a few things you can do to build momentum to avoid going off the tracks again.

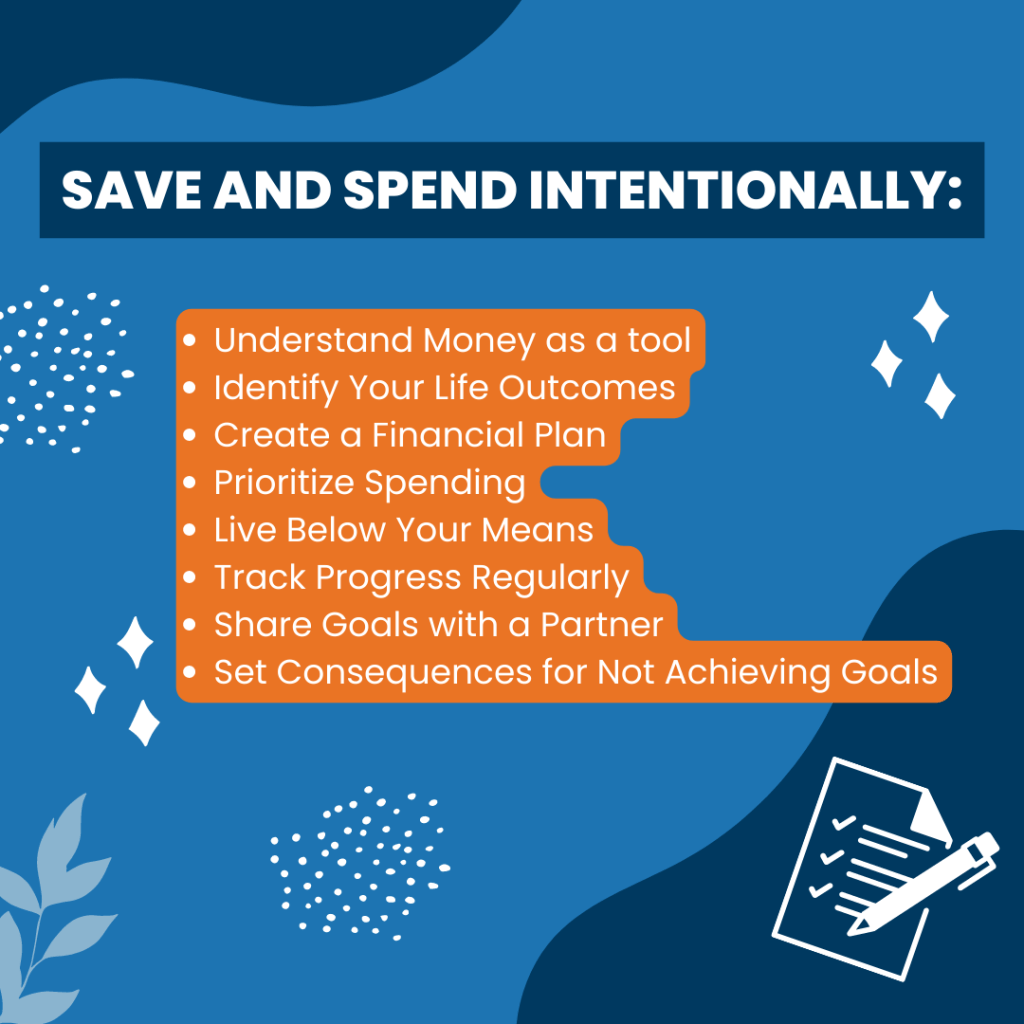

Create a Conducive Environment

So, what can you do to keep the positive momentum of prudently managing your finances going for the long-term?

Well, to start, consider your environment and how it might affect how you deal with your finances. Marie Kondo, an expert in the art of tidying up and creating a joyful home, believes that your physical environment has a powerful impact on your habits and behaviors. So then, from a financial perspective, here are a few tips from Marie on ideally designing your physical environment to establish new financial habits, such as consistently paying your bills and prudently managing your finances.

First, create a dedicated financial management space in your home. You can do this by designating a specific area in your home for managing your money like a desk or a corner of your living room. And this space should be clean and organized, with all the tools and documents you need to manage your money easily accessible.

Next, use visual cues to remind yourself to pay bills, review financial statements, rebalance investments or take care of other essential financial tasks. You can do this by placing a brightly colored sticky note or a decorative object in your financial management space to remind you of when it’s time to take care of the essentials, and make these habits more automatic.

Also be sure to make it a pleasant experience by playing music, lighting a candle, or sipping a cup of your favorite drink while you take care of your finances. This way, paying bills doesn't have to be a chore, and you may even come to look forward to the experience.

Create New Habits, But Start Small

Now, earlier, we discussed James Clear's take on how habits can help overcome procrastination. Another take on habits comes from Charles Duhigg, who emphasizes the importance of starting small in his book "The Power of Habit." And Duhigg suggests that the key to forming new habits is to focus on small wins that give you a sense of progress and accomplishment.

For example, if you're trying to build a habit of going to the gym regularly, start by committing to just 10 minutes of exercise each day. In a similar way, if you have trouble with paying your bills or staying on top of your financial accounts, try paying one bill or reviewing one financial account per day.

The idea here is that once you've established the habit, you can gradually increase the amount of time you spend on it. This way, you're starting small, but you're building towards a larger goal.

Another key principle of habit formation is the habit loop, which consists of three parts: the cue, the routine, and the reward. The cue is the trigger that sets off the habit, the routine is the behavior or action that follows, and the reward is the positive outcome that reinforces the habit.

To establish a new habit of paying your bills on time, for example, you may want to consider creating a new habit loop. To accomplish this outcome, start by identifying a cue that will trigger you to pay your bills. This could be something as simple as setting a reminder on your phone or marking your calendar with the due date of your bills.

Then, once you have a cue in place, establish a routine for paying your bills. This could involve setting aside a specific time each week to pay your bills or automating your bill payments to automatically deduct them from your account.

Finally, make sure you reward yourself for paying your bills on time. This reward system could be something as simple as treating yourself to a favorite snack or taking a few minutes to relax and enjoy a cup of your favorite drink after you've paid your bills.

By creating a new habit loop for paying your bills, you can establish a new habit that will help you stay on top of your finances and avoid late fees and other financial penalties. With practice and persistence, you can make this new habit a permanent part of your life and enjoy the benefits of better financial management.

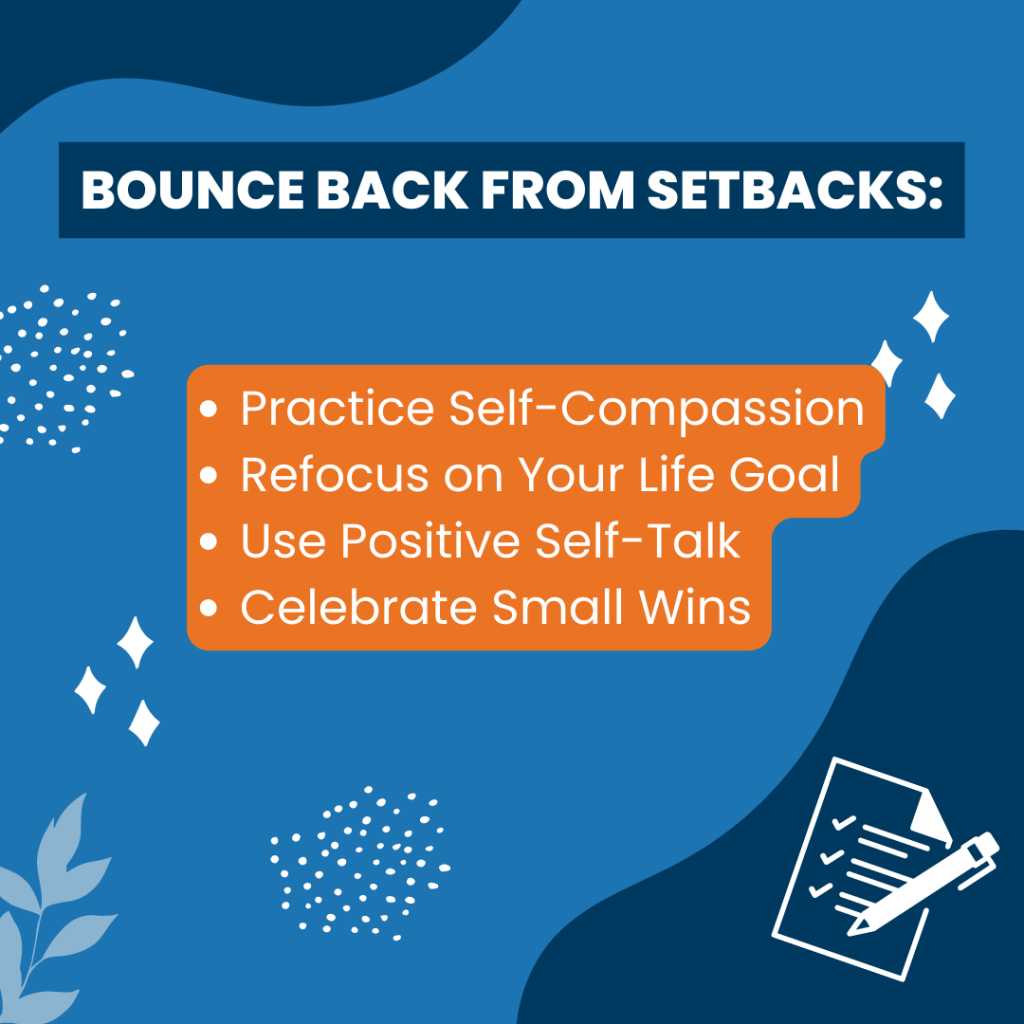

Treat Yourself

Finally, make sure you don't miss out on the earlier point about rewarding yourself for the progress you're making. Indeed, in "18 Minutes: Find Your Focus, Master Distraction, and Get the Right Things Done," Peter Bregman emphasizes the importance of incorporating rewards into the habit-creation process as a way to reinforce positive behavior.

According to Bregman, when we engage in a behavior that we find rewarding, we are more likely to repeat that behavior in the future. Therefore, he suggests that we identify specific rewards that we can give ourselves for completing a desired behavior or task.

For example, if your goal is to review your bank account transactions once a week, you might reward yourself with a pizza delivery or takeout from your favorite restaurant. Alternatively, if your goal is to balance your checkbook by a specific deadline, you might reward yourself with a night on the town or a big-ticket purchase once you've finished your work.

Bregman also emphasizes the importance of making the rewards tangible and immediate. Indeed, rather than waiting for a long-term goal to be achieved, he suggests that we reward ourselves for making progress along the way. Again, it's the small wins on a daily and weekly basis that move us closer to our long-term financial goals.

By incorporating rewards into the habit-creation process, Bregman believes that we can create positive habits that are sustainable and enjoyable rather than feeling like a chore. Additionally, he suggests that we track our progress and celebrate our successes, which can also serve as a form of reward and motivation to continue positive behaviors.

Is Financial Procrastination Putting Your Life Plans Off Track?

Make no mistake, financial procrastination can significantly impact your money and relationships if left unchecked. It can lead to missed payments, late fees, and even ruin relationships. And while there are many reasons why people procrastinate, understanding the underlying causes can help you take steps to overcome this behavior.

These approaches include addressing mindset, working to avoid instant gratification, and by listening to your body, you can start to break free from the cycle of financial procrastination and take control of your finances. Remember, it's never too late to start taking action and making positive changes in your financial life.

Indeed, by shifting towards a growth mindset, developing sustainable habits, and supporting your nervous system, you can overcome the barriers that are preventing you from taking action and moving towards your desired financial outcomes.

Remember, sometimes all it takes is small, consistent steps and being kind and compassionate towards yourself during this process to make sustainable gains. And, with a little patience and persistence, you can take one step closer to becoming the master of your financial independence journey.

10 Basic Truths of Financial Independence

Financial independence can be defined in a number of ways. However, when most think of financial independence they dream of a time in their lives when they are generating enough income to cover the essential expenses so that they never have to work again.

For some, financial independence is far off into the distance, for others it's within close reach. Wherever you fall on the spectrum, here are 10 financial rules to never break if you want to achieve full financial independence someday:

1. Earn More Money Than You Spend

You obey this principle by always living below your means. Follow this simple rule, no matter what your income and everything else will fall into place. As your income goes up, so will the extra money for savings and investment.

2. Make a Budget and Stick to It

You cannot live within or below your means without knowing what your expenses are and where you can start cutting. The path to that higher knowledge is a budget. There are dozens of free budget templates online. Fill in the template blanks and you’ll learn some rather eye-opening facts about where your money is going. Follow that budget and see how spending discipline give you an immediate leg up on financial independence.

3. Eliminate Unnecessary Living Expenses

Take a critical look at your budget. Are you spending over $100 for cable TV, for example? Cut the cable and save an extra $1,200 a year. Look everywhere and be ruthless.

4. Get Into Daily Financial Awareness Habits That Result in Wealth Accumulation

If your daily habits include a stop at Starbucks for that $5 latte, you are spending $100 a month — another $1,200 a year. Make your own frothy caffeinated beverage from the mixes on sale at your grocery store. Look for ways to save costs and expenses through coupons and sales. Keep track of your monthly bills and look for ways to cut down on energy expenses, for example.

5. Concentrate on Doing Well at and Keeping Your Job

You cannot obey financial rule number one without the income from your present employment. There is a correlation between job satisfaction, promotion and ever-increasing earnings. If you are bored, unchallenged and unhappy with your work, you need to take steps to resolve the matter or you will be stuck in a financial rut.

6. Avoid Money-Making Schemes and Scams

No matter what the slick infomercials and bombastic websites shout out, there is no shortcut to wealth. Anyone who advertises that buying their plan or paying to attend their seminar is manly only interested in making money from you. That meets their financial goals, but detracts from yours.

7. Pay off Your Debts

If you are bogged down in heavy debt and your monthly expenditures are beginning to leapfrog your income, it may be time to consolidate your debts. There are many pathways to debt consolidation. Check around on the web. There is help out there.

8. Pay Your Monthly Credit Card Bill on Time

If you’re carrying a monthly balance on your credit card, you’re swimming upstream in your quest to get out of debt. Consider instead using a bank debit card, or at least get into the habit of paying off your monthly credit card balance.

9. Pay Down Your Mortgage

Your budget will show that your monthly mortgage payment is one of your biggest expenses. Paying off your mortgage early takes discipline and can eat into those excess funds you will begin accumulating through following steps one through eight. However, once your home is free and clear, you have the true wealth of the worth of your home’s market value. When the mortgage payments go away, you likewise have the income excess that becomes a powerful savings and investment resource.

10. Begin a Savings and Investment Plan

Start slow if you must, but save something each month. You’re in this for the long term and your goal is to be debt-free and to accumulate real wealth (i.e., to be financially independent). The savings and investment plan that is best for you depends on your age, situation and how much you need for a comfortable retirement. Again, look around. There are financial experts and expertise out there ready to help.

Is Credit Your Superpower or Kryptonite?

Is credit a good thing or bad thing?

Well, it all depends on your perspective.

When used correctly, credit can supercharge your life and help you level up financially in a shorter time than you would have if you relied on savings alone. That's why Dale Carnegie, in his book, "The Gospel of Wealth," wrote that debt could be a powerful force for good if used productively.

Now, the trouble with debt is that, just like any other financial tool out there, it has been misused by lenders and borrowers alike, leading its use to be largely villainized by society. Make no mistake, in the wrong applications, debt can be a form of bondage. That's why in some cultures, its use is forbidden and why some individuals have mortgage payoff parties instead of retirement savings celebrations.

Make no mistake, however, when used prudently, credit can boost your earnings ability, enable you to acquire appreciable or income-producing assets, and help keep you from going broke when life throws you a curveball bigger than your savings account.

Even so, a Scottish historian and author, Niall Ferguson, wrote, "credit is like a looking glass. Once cracked, it can never be the same again, and the more we use it, the more fragile it becomes…"

Indeed, these perspectives from Carnegie and Ferguson show how on the one hand, the wise use of credit can dramatically enhance your current financial situation. On the other hand, debt can leave your finances in a precarious position when not managed properly.

Certainly, much has been written about the trouble with credit and how too much debt can be a trap. Before we discuss the drawbacks of credit, let's take a look at why you would want to use debt to lever up your current financial situation.

Why Credit Can Be a Force for Good

Credit as a Force Multiplier

When used the right way, credit can be a force multiplier. It can help you accomplish things in your life that you otherwise may not have been able to do on your own financially.

Now, the term force multiplier is often used in the military to describe a factor, such as better positioning or equipment, that can increase a unit's combat potential, allowing it to fight on a par with a more significant fighting force.

For instance, in World War II the development and use of radar technology arguably changed the course of the war in favor of the Allies. As you'll recall, radar is a detection system that uses radio waves to determine the location, speed, and direction of objects.

Now, radar served as a force multiplier for the Allies by providing them with a significant advantage in air and naval combat. With radar, the Allies could detect incoming enemy aircraft and ships at a much greater distance than the enemy could detect them. This tool allowed the Allies to prepare their defenses and launch counterattacks more efficiently and accurately.

For example, radar played a critical role in the Battle of Britain, in which the Royal Air Force (RAF) used radar to detect incoming German aircraft and direct their own fighters to intercept them. Using radar allowed the RAF to defend against the German bombing campaign more effectively and played a crucial role in their eventual victory.

So, from this perspective, credit can act as a force multiplier by taking the financial resources you have today and amplifying them to achieve a broader victory in your life.

How so?

Well, the first way it can benefit you is by enhancing your future earnings ability by allowing you to borrow money in the present so that you can improve your skills and get credentials that can help you break into a new field or raise you to a higher earnings level in your current role. And while the topic of college education, and more specifically college debt, is hotly debated today, the statistics still argue in favor of a college degree.

Now, according to data from the Bureau of Labor Statistics' most recent Occupational Outlook Handbook, the data show that those jobs with the fastest industry growth rates and median pay of at least $100,000 all require a college degree. Indeed, according to the same government data, there is a growing earnings gap between individuals holding a college degree and those without.

For example, government data show that the average 25-year-old full-time worker with a bachelor's degree made a median annual wage of around $55,000, compared with $30,000 for full-time workers of the same age group with just a high school diploma. And when we look at the earnings gap over a lifetime, it continues to increase. Here again a study from the Department of Education shows that an individual with a high school diploma is likely to earn a median income of around $1.9 million over their lifetime.

However, an individual with a bachelor's degree could earn $3.4 million over their lifetime, while a top-earning professional degree could bring in nearly $6.5 million. So, then, even if we assume that it costs an individual $160,000 to obtain and pay off their debt over ten years, the costs associated with the college debt would still net an extra $1.3 million or a multiplier of eight times of what a non-college graduate could earn over their lifetime.

So, then, from this perspective, we can say that credit can act as a force multiplier to enhance an individual's inherent knowledge and increase their earnings power.

A Lever for Wealth Building

Another way that credit can dramatically change your financial situation is by giving you leverage to use a little bit of money to create a lot of wealth. Now, for many individuals, purchasing a home is one way to create wealth. Certainly, arguments have been and continue to be made for and against the wealth-building attributes of home ownership. Even so, the long-term benefits become evident once you look past the short-term costs of home ownership versus renting.

Now, one way homeownership builds wealth is through the appreciation of the value of your home over time. Historically, home values have tended to appreciate over the long term, sometimes resulting in significant wealth gains to homeowners. And while you may be only putting down five- ten-, or twenty-percent towards the purchase of a home, you gain access to the full value of the appreciated equity in your home over time when you borrow against or sell it.

What's more, homeownership can help you build wealth through the process of forced savings. That's because the longer you make mortgage payments, the more principal you pay down, which is essentially putting money into a savings account each month, assuming home values remain stable. And this approach can help you build wealth over time, even if the cost of homeownership is slightly higher in the short term than that of renting.

Another way that credit can help turn a little bit of money into a lot of money is by starting a business. Now, the internet is filled with stories of individuals who borrowed money to achieve wildly successful outcomes. And one rags-to-riches entrepreneur who used debt to start their business is John Paul DeJoria, the co-founder of John Paul Mitchell Systems, the haircare company.

Now, DeJoria was raised in a low-income family and faced financial difficulties throughout his life. In fact, in 1980, when he decided to start John Paul Mitchell Systems with his partner, Paul Mitchell, DeJoria was homeless and living out of his car. Even so, he borrowed $700 to launch the company and personally went door-to-door selling their first hair care products. And through perseverance and hard work, DeJoria managed to grow the business into a multi-billion dollar empire, making him one of the most successful entrepreneurs in the world.

Help You Stay Solvent

A final way that credit can be a valuable tool in your financial toolbox is that it can help you stay solvent even when you're short on cash. This point is especially salient should you have an unexpected home or auto emergency, an unforeseen medical expense, or suddenly find yourself without a job.

Now, make no mistake, when it comes down to it, an emergency fund or a solid cash management strategy is a prudent way to help mitigate these financial risks.

Even so, a time likely will come when using credit can help you stay solvent enough to keep your priorities straight and stay on track to your journey to financial independence. That's because if you're facing an unexpected one-time big-ticket expense, such as a large medical bill or a significant home repair, instead of drawing down on your savings or liquidating your investments, you can use credit to cover the expense to preserve your financial security.

Indeed, by using credit responsibly, you can, over time, spread out the cost of a large one-time expense. And why not just use cash savings to pay down the debt? Well, if you draw down your cash reserves too much, you risk putting yourself in a position where you'd be unable to handle uneven cash flow situations or potentially limit your optionality when other unforeseen expenses come your way as they inevitably do.

What's more, using credit to cover unexpected expenses can also help you achieve financial freedom in the long term. Now, while this may sound counterintuitive, this works because by avoiding the need to liquidate your investments or tap into your savings, you can preserve your wealth and allow your money to compound over time.

So, when it comes down to it, credit can be a force for good when it's used the right way. Indeed, credit can act as a force multiplier when it comes to your earnings ability, and it can serve as a lever to help acquire assets that might build long-term wealth and a means to help buy time and stay solvent so you can keep fighting in the game.

Give Your Credit a Good Purpose

Now, when it comes to the prudent use of credit, what trips up a lot of individuals is not necessarily gaining access to credit but needing a clearly defined purpose for how they'll use the credit itself. At that point, credit becomes a problem because, without a clearly defined purpose for your money, you may end up relying on credit to live someone else's money script., or, as Will Rogers puts it, spending money you haven't earned, to buy things you don't need, to impress people you don't like.

Indeed, this topic is essential and one we spent time on in a broader discussion about giving your money purpose in past articles. And as you'll likely recall, giving your money purpose means knowing…

- why you work in a chosen profession

- where you are spending and what you are spending my money on

- why you are saving money for the future

- how you will feel when you can use your money to make critical life change

- that your kids won't have debt burdens when they go to school

- that you are leaving something behind for future generations to enjoy

- that you can spend money without feeling guilty

- that no matter what happens in the economy or markets that, your financial situation is secure

- that you can help out a friend or family member when the financial need arises

- that you have the resources you need to pursue your hobbies and passions

- that you have the time to do what you want when you want

- that you have options to make life changes

- that no job or relationship will ever control your ability to live a fulfilling life

- that you can give your family life experiences that they can treasure

So, what purpose does your money have?

Take a moment to consider the values and purpose that you defined for your life. Then, think about the near- and long-term life priorities that you've defined for your life journey.

Now, ask yourself, "how can I use my credit as a force multiplier, leverage to acquire productive assets, or to ensure that I have an adequate last-resort backstop?"

Put differently, if you plan to use credit to amplify your future earnings potential, ask yourself if your chosen profession on vocation and the credential you're planning to borrow for is genuinely something that aligns with your values and the purpose that you've defined for your life. If not, then carefully consider whether borrowing for this education goal is something you might regret if it's not moving you closer to your intended life.

Tim Kasser, a psychologist who has written extensively on the psychological consequences of materialism and the pursuit of wealth, emphasizes the importance of aligning one's chosen vocation with their values and life purpose. And Kasser argues that people who pursue careers solely for the sake of money and status are more likely to experience adverse psychological outcomes, such as anxiety, depression, and a lack of fulfillment.

That's why Kasser suggests that individuals who choose a career that aligns with their values and life purpose are more likely to experience a sense of meaning and purpose in their work. This, in turn, can lead to greater intrinsic motivation, satisfaction, and overall well-being, but more importantly, a genuinely prudent use of credit.

As it relates to borrowing to acquire an asset like a home or car, here again, the question you want to ask yourself is whether the purchase you make will move you further down your path to financial independence or whether it's simply serving as a means to satisfy someone else's money script.

To be sure, Horstein Veblen, a prominent economist and social theorist, believed that people often engage in conspicuous consumption, or the spending of money on items solely to display wealth and social status, in order to signal their social status and impress others. In his book "The Theory of the Leisure Class," Veblen argued that people engage in this behavior as a way of demonstrating their superiority over others in their social circles.

So before you go out and borrow to buy a new house or car, ask yourself if your motivation is based on moving you closer to your intended life purpose or simply to live someone else's money script.

And when it comes to relying on credit as a stop-gap for emergencies, remember that cash should be your primary means for addressing one-time big-ticket spending needs.

An emergency savings fund can serve as your financial safety net, ensuring that you stay on track with your financial goals and avoid setbacks when unforeseen expenses arise. When you have this reserve in place, you're able to cope with unexpected events, such as medical emergencies, car repairs, or job loss, without dipping into your long-term savings or incurring debt.

Either way, giving your money purpose is the first step in getting off the hedonic treadmill of mindlessly borrowing more money simply to chase after outcomes or spend it to impress others. Alternatively, it can give you the push you need to begin spending more intentionally if you're a natural saver and worry too much about overspending.

How Much is Too Much of a Good Thing?

Now that we've talked about how credit can fast-track your path to financial independence and how aligning its use with your money's purpose can help you make wise borrowing decisions, let's take a moment to discuss why too much credit can be too much of a good thing.

Now, it's common sense that we all need to borrow money within reason. Most, if not all, financial professionals out there argue against accessing credit, and the truth is, you likely know individuals in your own life who have had their financial plans derailed because of unmitigated borrowing and spending choices.

In fact, Suze Orman, the well-known personal finance expert, struggled with debt early in her life, which impeded her ability to achieve her financial goals. That's because Suze grew up in a middle-class family in Chicago, and while she was always interested in finance, she didn't have the best financial habits.

As a young adult, Suze worked as a waitress and later as a financial advisor, but she was living beyond her means and accumulating debt. At one point, she had over $20,000 in credit card debt and owed money to the IRS. Despite making a decent income, Suze struggled to make ends meet and could not save for her future.

It wasn't until Suze hit rock bottom that she realized she needed to take control of her finances. That's when she made a plan to pay off her debt, cut back on her spending, and start saving for her future. She even took a job as a financial advisor in California to learn more about managing money and building wealth.

Over time, Suze's financial situation improved, and she was eventually able to achieve her financial goals. Despite her early struggles with debt, however, Suze's experiences taught her valuable lessons about the importance of managing money wisely and avoiding the pitfalls of debt. She has since become an advocate for financial education and empowerment, helping others take control of their finances and achieve their financial goals.

Now, as you think about the possibilities that borrowed money can open up in your life, it's easy to forget that your debt will need to be serviced. That's why when you're not paying attention to how much you're borrowing or who you're borrowing from, you could find yourself in a position where you're earning an income simply to pay off your creditors. And when you do, it becomes a form of bondage.

This is because you could find yourself in a position where a large portion of your income is going towards paying off your debts, leaving you with little money to spend on the things you want or need. You may also find yourself needing help to make ends meet, unable to save for the future, or even struggling to pay for unexpected expenses.

Additionally, having excess debt can also limit your options and control over your life. For example, you may be unable to change jobs or start a business because you need a steady income to service your high debt load. You may also have to put off major life milestones, like buying a house or starting a f amily, because you simply cannot afford it.

The stress and anxiety that come with being in debt can also take a toll on your mental and emotional well-being. You may feel trapped and hopeless, constantly worrying about how you will make ends meet or how you will ever pay off your debts.

And, when taken together, servicing too much debt can be a form of bondage because it limits your options, control, and ability to live the life you want. It can be a constant source of stress and anxiety, leaving you feeling trapped and unable to break free.

Setting the Right Levels

So, what is an ideal amount of debt to carry? Let's take a look at some ideal borrowing limits for key consumer debt categories, starting with your home.

Mortgage

Now, when it comes to borrowing to purchase a home, Clark Howard, author of the book," Living Large in Lean Times," believes that limiting your monthly mortgage payments to no more than 28% of your gross monthly income is important because it can help you avoid taking on more debt than you can comfortably afford to repay. That's because when you take on too much mortgage debt, you risk becoming "house poor" and not having enough money to meet other financial obligations or save for the future.

In his book, Clark further explains that your mortgage payment should consider the principal and interest on your loan as well as the property taxes, insurance, and any homeowners association fees. That's why he recommends that you calculate the total cost of owning a home before making a purchase, taking into account all of these expenses as well as any maintenance or repair costs that may arise.

For example, Howard suggests that if you earn $5,000 per month before taxes, your total monthly mortgage payment should not exceed $1,400 (28% of $5,000). If your mortgage payment is higher than this amount, he recommends that you consider finding a less expensive home or waiting until you have saved up a larger down payment to reduce your monthly payment.

Auto Loans

And when it comes to buying a new car, what's a reasonable amount to borrow? Well, in "Your Money: The Missing Manual," J.D. Roth recommends that you should keep your auto loan debt to a minimum and aim to pay cash for your vehicles whenever possible. However, if you need to take out an auto loan, he suggests limiting your monthly car payments to no more than 10% of your take-home pay.

Roth believes that taking on too much auto loan debt can be a financial burden and limit your ability to achieve other financial goals, such as saving for retirement or emergencies. He suggests that you should choose a used car instead of a new car, as they are often more affordable and can provide good value for your money.

Roth also recommends that you shop around for the best auto loan rates and terms before making a purchase and suggests that you should avoid dealer financing and consider getting pre-approved for an auto loan from a credit union or bank before shopping for a car.

Credit Cards

According to government data, many Americans carry a balance of at least $1,000 on their credit cards. That's why in her best-selling personal finance book "The Money Class: How to Stand in Your Truth and Create the Future You Deserve," Suze Orman recommends that you aim to keep your credit card debt to no more than 30% of your available credit limit.

What's more, Suze argues that you should aim to pay off your credit card balances in full each month to avoid high-interest charges and long-term debt. In her book, Orman goes on to explain that carrying a balance on your credit card can be costly, as interest charges can quickly add up over time.

Student Loans

And finally, when it comes to student loan debt, how much should you aim to borrow for yourself or for your children? Well, in "Making the Most of Your Money Now," Jane Bryant Quinn recommends that you should limit your total student loan debt to no more than your expected annual salary after graduation. This means that if you expect to earn $40,000 per year after graduation, you should aim to limit your total student loan debt to $40,000 or less.

Quinn emphasizes the importance of minimizing student loan debt as much as possible by exploring alternatives such as grants, scholarships, work-study programs, and part-time jobs. She also suggests that you should choose a less expensive college or university, attend community college before transferring to a four-year institution, and take advantage of programs that allow you to earn college credit while still in high school.

The Costs of Poor Debt Management

Now, as we mentioned earlier, being able to stick to a disciplined use of credit can help you avoid running afoul of common borrowing issues. That's because when your borrowing gets out of hand, it can lead to unfavorable situations that 1) limit your optionality and creates missed opportunities and 2) creates more emotional stress and anxiety in your life.

Make no mistake, when managed wisely, credit can help you fast-track your path to financial independence by acting as a force multiplier for your earnings ability, providing you with the leverage you need to acquire appreciable assets and keeping you solvent in times of emergency.

Too Much Debt: Missed Opportunities

Even so, taking on too much debt can limit your ability to jump on financial opportunities that may come your way.

How so? Well, let me tell you about Frank.

Frank is an entrepreneur who used his stellar credit to borrow money to start a business. However, one afternoon, Frank found himself sitting at the kitchen table, sifting through a pile of bills he had accumulated from his startup. Now, Frank had always been a responsible person, but a series of unexpected events with his startup had left him struggling to keep up with his financial obligations.

And, a few weeks ago, a close friend approached Frank with a promising business opportunity. They needed a partner to help expand their thriving local storefront into a chain of stores, and they believed Frank had the skills and experience to make it a success. The potential for lucrative returns was undeniable, but the required initial investment was substantial.

Frank spent countless nights analyzing the opportunity and dreaming of the financial freedom it could bring him and his family. This opportunity could be his ticket out of debt, a way to secure a comfortable future. But as he sat down to create a detailed plan, he realized that his current debt situation made it impossible to take on the additional financial risk.

His mortgage, car loans, and credit card balances had snowballed into a mountain of debt that was suffocating his finances. The monthly payments were barely manageable, and he knew that adding another significant obligation could easily push him into a downward spiral.

Frank hesitated for days, trying to figure out a way to make it work. He considered taking on a second job, selling some assets, or even asking for a loan from family members. But deep down, he knew that none of these options would be enough to keep his head above water if the venture didn't go as planned.

With a heavy heart, Frank picked up the phone to tell his friend that he couldn't join them in the business venture. He could hear the disappointment in their voice, but they understood his situation and wished him well.

Now, as he sat at the kitchen table, he knew that it was time to face his financial reality head-on. He would need to develop a plan to tackle his debt, cut back on expenses, and work towards a more secure financial future. The missed opportunity served as a reminder of the importance of managing his finances responsibly and staying on top of his obligations.

Though the thought of what could have been stung, Frank understood that he must focus on overcoming his current challenges before he could chase after new opportunities. He was determined to learn from this experience and ensure that the next time an incredible opportunity came knocking, he would be ready to answer the door.

Too Much Debt: Financially Fragile

Certainly, taking on too much debt may limit your choices when lucrative financial opportunities come your way. What's more, while credit can act as a lifeline for one-off, big-ticket purchases, borrowing too much money can leave you financially fragile and unable to bounce back if you get hit with another unexpected life event.

And that's what happened to Maria.

Now, Maria had always been prudent with her money, living frugally and saving for the future. However, she couldn't have anticipated the series of events that would unfold and leave her in a financially fragile position.

A few years ago, however, she decided to take the plunge and purchase her dream home, with a picturesque view and a spacious backyard for her growing family. She took out a sizable mortgage that was at the top end of her budget, but with her steady income and careful budgeting, she felt confident that she could manage the monthly payments.

Life carried on smoothly for a while, and Maria made consistent progress towards paying down her mortgage. However, unforeseen challenges began to arise. Her partner lost their job due to company downsizing, and although they actively searched for a new position, it took months for them to secure another job, leading them to burn through their emergency savings because her partner's unemployment benefits weren't enough to cover their share of the household expenses, leaving Maria to shoulder the burden alone.

To make matters worse, she was hit with an unexpected medical emergency that required surgery and a lengthy recovery. While her insurance covered most of the costs, she was still left with significant out-of-pocket expenses. This event also forced her to take extended leave from her job, which impacted her income further as her long-term disability only covered a portion of her regular income.

To stay afloat, Maria reluctantly turned to credit cards to cover the mounting expenses. Soon, however, the minimum payments on her credit card balances began to pile up, adding to her already strained budget.

Just when she thought things couldn't get any worse, a leak in her home's roof led to water damage and costly repairs. Desperate to address the issue before it worsened, she took out a home equity line of credit, hoping to pay it off once her financial situation improved.

Unfortunately, the combined weight of the mortgage, credit card debt, and the home equity line of credit left Maria struggling to keep her head above water. With each passing month, she found it harder to make ends meet, and the stress began to take a toll on her physical and mental well-being.

Maria never imagined that her pursuit of a dream home could lead to such a financially fragile position, but the combination of unforeseen challenges and mounting debt became an overwhelming burden. Nevertheless, this was her “rock bottom” moment, and now she's focused on finding a way to overcome this difficult situation and regain control of her financial future.

The takeaway here is that while credit can be helpful, too much of a good thing can act as kryptonite, holding you back from potential opportunities or leave you financially fragile if you overstretch your borrowing budget.

That's why it's crucial to understand that debt isn't always the enemy when you're working towards financial independence. Indeed, if used wisely, credit can be a superpower, amplifying your future earning potential, providing leverage for purchasing valuable assets, and offering a safety net during tough times.

However, it's vital to remain true to your core values and the purpose you've assigned to your money. Be introspective and ask yourself whether a debt-related purchase aligns with your financial goals or if it's merely catering to someone else's expectations. This mindfulness will help you avoid overconsumption and ensure your credit works for you, not against you.

And finally, think of managing your credit as an essential skill, much like spending and saving judiciously. Overwhelming debt can lead to lost opportunities and financial fragility in the face of life's unpredictable events. Nevertheless, by adopting a balanced approach, you're well on your way to crafting a stable, prosperous future—one in which you're moving one step closer to mastering your path to financial independence.

Don't Confuse Budgets and Cash Flows

Cash is the lifeblood of your finances. Without it, you would be hard-pressed to pay your debts, cover your living expenses and prepare for essential savings decisions.

With cash flows being a critical component of household finances and the primary path to securing financial independence, various surveys suggest that between half and three quarters of Americans don't have a process for keeping track of their cash flows!

What's more, the data show that about half of working Americans are living paycheck to paycheck, and about that same number can't cover a $1,000 emergency expense.

Make no mistake, many of us are well aware of how essential staying on top of our cash flows from one month to the next is to maintaining financial health.

And while the rigor of sticking to a budget may not be for everyone, the truth is that you need to have some way to track and manage your cash flows if you want to increase your chances of securing your path to financial independence sooner rather than later.

Certainly, you’ve likely heard that a budget is useful in helping you keep your finances in order, but a cash management plan is also a vital component of a well-crafted financial plan.

Cash Flow Management vs. Budgeting

Now, it's critical to make a key distinction between budgeting and cash flow management. A budget is an estimate of what you believe you will spend and save over a given period of time. Cash flow management, on the other hand, is the process of allocating your cash resources to spending and savings decisions.

So, what's the difference between the two?

Well, a budget is a static measure of where your money ideally should go over a week, month, or year. Cash flow management, on the other hand, is a dynamic process that involves actively deciding where your money goes in real time. What's essential to note here is that budgeting and cash flow management are not mutually exclusive. And the two often go hand-in-hand, with a budget providing a benchmark of where your money should go, and cash flow management is how you allocate your money accordingly.

Now, the trouble with cash flow management and budgeting is that what you should do is often tied to black-and-white logical thinking, while our emotions largely influence how we spend money. Indeed, many studies over the years have demonstrated a psychological connection between our money choices and our current emotional states.

And with cash being so important to getting the things we need throughout our life, staying on top of where your money is going is critical to achieving your goals. That’s because an inevitable emergency, like a furnace that needs replacing, the need for a new car, or a last-minute visit from out-of-town family members, can derail a budget. But a proper cash management plan can help you decide the best course of action when unexpected events arise.

Defining Your Cash Flow Management Strategy

That's why when it comes to managing your money, focusing on your cash flow management process should likely take priority over your budget. Indeed, a well-defined cash flow management process should include a few critical components, including:

- How often you review your financial accounts

- Which financial accounts you need to check

- The time and place that you're reviewing your cash flows

- Understanding your savings and spending decisions

What You Should Track

Now, at its most basic level, your cash management plan should give you an idea of how you spend your income from one pay period to the next. And while a casual glance at your bank account balance can be helpful, not understanding what that balance represents, especially if you anticipate further expenses or spending to come through in between pay periods, can quickly put you off track.

That's why you should evaluate your cash flows, at the very least, on a weekly basis. For most individuals, this process can take just a few moments to less than 30 minutes per week. But the benefit of taking this step is immediately gaining peace of mind knowing where you stand financially.

Another step you can take to stay on track of your bank account balances is to take advantage of your financial institution's text, email, and app alerts. Many financial institutions will send you daily updates on the available balances in your various bank accounts. Receiving these alerts can provide you a way of keeping track of changing balances from one day to the next without having to take the time to log into your accounts.

This approach is extremely useful should you see a sudden change in one of your daily cash balances, as it will allow you to get ahead of potential cash flow issues well in advance of them becoming a more significant problem down the road.

So with that said, which accounts should you keep track of?

Well, to begin, you'll likely want to take a step back and determine your primary sources of spending. For example, ask yourself if most of your essential regular spending is flowing through your bank accounts or credit cards? If there's a mix of cash and credit card spending that is paid off at the end of the month, what does that mix of spending look like?

While we'll have more to say about the benefits and drawbacks of using credit cards to fund your daily spending decisions, for now, we'll focus on your cash bank accounts. That's because while credit spending can be a helpful stopgap in the near term, a shortfall in your cash accounts could have a cascade effect on your overall savings and spending decisions over the long term.

Remember, it's the nickels and dimes that will get you.

So, as you log in to your bank accounts and look over your current transactions, your eyes likely will be drawn to large dollar transactions. While it's vital to stay on top of total dollar spending, take a moment to review the frequency of spending, not just from day to day but also from vendor to vendor perspective. What you want to do here is get a feel for the trends to understand not just where you're spending your money, but also how often you’re spending at those specific locations.

After a time evaluating your expenditures, you should have an intuitive sense of whether your spending trends from the past week are higher or lower than expected. For example, are you spending more than usual this past Wednesday compared to last week? If so, what changed? Was it that business trip or an unexpected visit from a friend or family member? Maybe work is stressing you out, and you needed to spend a little extra this week to compensate.

Whatever the case may be, look for trends in the frequency of your spending, and take some time to evaluate why you may have spent more money on a given day or with a particular vendor, and if so, understand what may have triggered those expenditures.

Finally, take some time to review your finances in a place that is conducive to the review. As we mentioned in a previous post, your environment plays a critical role in how you relate psychologically to the process of evaluating your finances.

Indeed, reviewing your money can be emotionally stressful because it may remind you of the sometimes less than ideal choices you may have made in the past.

That's why priming your mind for a financial review is essential to getting a handle on your cash flows and to avoid becoming emotionally activated or emotionally shutting down altogether.

To do this, find a quiet time and place to complete your weekly cash flow management review. If you have children, ideally, this time could be in the early morning before they wake up or late in the evening after putting your kids to bed.

Either way, align your positive ideation with the process of reviewing your finances. And if your stress related to your financial review is coming from a place of shame or guilt, your best course of action is to practice self-compassion and self-forgiveness before you begin reviewing your numbers.

And finally, stick to the process no matter how uncomfortable it might feel. While procrastination can give you a sense of bliss, you'll likely find that the very act of simply looking at your accounts can immediately reduce your stress levels because now you know what you have to deal with, rather than worrying about what could potentially be waiting for you when you come back to it.

Spending within Your Means

So, now that you’ve prepared yourself to review your cash flows and understand what to look for from a transactional perspective, you need to give your review a purpose. And so, from this perspective, a key question you'll likely need to answer here is whether you're spending within your means.

Now, if you make a lot of money and are not sure where it all goes each month, then this approach will likely help you identify in short order where exactly your money is going. Put simply, ask yourself if your total expenses are less than your take-home pay each month?

Off hand, you will likely know whether this is the case if you find yourself dipping into savings or resorting to credit cards to supplement your spending on an ongoing basis. With that said, however, an ideal way to determine whether you're consuming within your means is to tabulate your spending and compare it to your paycheck deposits.

You can accomplish this using a spreadsheet, tracking software, pen, and paper or mobile banking tools. The whole point is to group each line-item spending in categories to help better understand where your money is going.

Whatever your preferred tool to track your spending and savings might be, be sure to categorize each spending item consistently each month. This way, you can go back and accurately compare your consumption trends from one month to the next.

And, as you move forward with your spending and savings evaluation, ask yourself if your net consumption is positive, meaning that you spend less than you bring home each month.

If so, congratulations!

The next step here is to evaluate whether you're leaving enough room to pay yourself and fund your savings goals. Now, if there's not enough cash left over at the end of the month to build up that emergency reserve or fund your child's 529 savings plan, now might be a good moment to take a step back and evaluate your spending categories for opportunities to reduce consumption or to increase your savings rate.

And if your net consumption is negative, meaning that you draw down on your savings account or use your credit cards to supplement your spending, take a few moments to evaluate which spending categories are taking up most of your cash flows. Here again, you'll want to not just look at the absolute dollar values of expenditures, but you'll also want to get a good idea of the frequency or how often you spend at a given vendor or in a particular lifestyle category for opportunities to free up cash flows.

Finally, now may be an excellent time to evaluate whether a budget might be a helpful means to managing your money. Now, make no mistake, sticking to a budget can be arduous, and as we pointed out before, it's a static practice that in many ways does not reflect the dynamic nature of our lives. Even so, a budget is a valuable yardstick for evaluating how you're spending and where it goes each month.

And here's the thing: there's no right or wrong way to create a budget. Ultimately, your budget should act as guide to show you how your expenses and savings should net out to zero versus your cash inflows from one pay period to the next.

Know When It’s Time to Create a Budget

And, so, how do you know whether it's time to create a budget for yourself? Well, here are a few ways to tell whether it’s time to create a budget.

First, if you find yourself struggling to make ends meet even when you’re bringing in a lot of money, then a household budget can help you identify areas where you might need to cut back on expenses or save more money. By tracking your spending, you can prioritize your needs over wants and ensure you're putting money toward your financial goals.

Next, if you have you don’t have an emergency fund, then that might be your sign that it’s time to create a budget. Indeed, unexpected expenses can arise anytime, and so it's essential to have a cushion to fall back on when you need that money. And so if you don't have an emergency fund, a household budget can help you save money specifically for that purpose.

Another sign that it’s time to create a budget is when you’re overly reliant on credit cards. That’s because credit card debt can quickly spiral out of control, leading to higher interest charges and fees. And by creating a household budget, you can identify areas to reduce expenses and allocate more money away from credit and to pay off accumulated debt.

If you’re a high earner but don’t have enough money to contribute to your retirement plan, that might be another sign that it’s time to create a budget. Now, it's never too early (or too late) to start planning for retirement. And a household budget can help you find ways to set aside more money for retirement and ensure you're on track to meeting your financial goals.

Finally, if you have no idea where your money is going, then that might be your sign that you need a budget. If you need to figure out where your money is going each month, a household budget can help you identify areas where you may need to spend more wisely. And by creating a baseline against which to tracking your expenses, you can make informed decisions about allocating your money and working towards your financial goals.

Now, creating a household budget may seem like a daunting task, but it doesn't have to be. There are numerous online tools and resources available that can help simplify the process. But remember, once you have a budget in place, it's essential to stick to it. And, when an emergency arises, that’s when you can lean on your cash management process to help navigate life’s inevitable curveballs.

Tools to Create Your Budget

Well, so far, we've discussed how essential it is to track your expenses and why you may want to go about creating a budget. To be sure, a household budget can help you track your income and expenses, identify areas where you can save money, and set financial goals.

But, how should you go about setting a budget?

To begin, you'll want to evaluate the critical components in your budget. You can start by identifying all sources of income, including salary, bonuses, investment income, or side hustles. Be sure to base your budget on your net income or the amount of money you take home after taxes.

Next, identify your fixed expenses. This is the spending that likely will remain consistent each month, such as rent or mortgage payments, car payments, insurance, and utilities.

Then, calculate your variable expenses. These are the costs that fluctuate each month, such as groceries, gas, entertainment, and dining out. These expenses can be more challenging to predict, but it's crucial to have an estimate.

You’ll also want to factor in how much you should be saving each month. Indeed, your savings should reflect how much you’ll need to set aside for emergency savings, retirement, and other big-ticket purchases throughout the year.

And finally, don't forget about your debt payments. Make a list of all the creditors you owe money to, then login to your financial institution’s website and identify your minimum payment due. Now, an important caveat here is that if you’re carrying a credit card balance, your minimum payment may fluctuate from one month to the next. That’s why it’s essential to monitor all of your financial accounts from one month to the next.

Now, as you build out your budget and consider where to allocate your income each pay period, think about it in terms of where your priorities lie. Start by separating out fixed costs from variable costs. Then, figure out how much money to allocate to each category by evaluating your spending over the past three months.

Budgeting Tools

Now, when it comes to actually creating your budget, there are a number of approaches you can take to establish a benchmark for your cash flows, savings and spending goals. However, the process of creating a spending plan can be overwhelming, especially if you're not sure where to start.

Luckily, there are various methods available to help individuals create a spending plan, including the use of spreadsheets, software, mobile banking tools, and handwritten methods. So, let’s take a moment to review each of these approaches and their pros and cons.

Spreadsheets

To start, spreadsheets are an excellent tool for creating a spending plan. They're flexible, customizable, and in many ways are easy to use. By creating a spreadsheet, you can develop a detailed plan that includes your income, expenses, and savings goals on one easy to use page. The added benefit of using a spreadsheet is that you can create formulas to calculate your spending and savings goals automatically.