Don't Pay the Price by Doing the Work Twice

Have you ever hired someone for help around the house, and you immediately regretted it?

You know, I've had my fair share of unhelpful helpers over the years.

In fact, I remember a time when I hired cleaners that didn't leave my house as clean as they promised.

You see, my family is pretty good about keeping our home tidy.

But, every once in a while, we'll hire someone to come out and take care of the deep cleaning we sometimes can't get to.

You know, it's the stuff like wiping down the baseboards, dusting in high places, cleaning the ovens, and otherwise getting into those deep nooks and crannies.

Well, one day, we needed help cleaning, and having recently moved to Pennsylvania, we were looking for a new crew.

And so, after doing our research online and calling around, three nice ladies showed up at our home one afternoon and offered to give us a "deep clean" for what seemed like a reasonable price.

Well, as they got to work, it immediately became clear that they wouldn't be able to get the job done in the time they had allotted for the work.

And how did I know this?

Well, they didn't have the same hustle or focus on their work as other professionals that we had hired in the past.

And wouldn't you know it, as soon as I left to pick up the kids from school, the crew took off.

And you know the biggest disappointment in all of this was that I could have done the work myself.

But, I just wanted to use my money to buy back some of my time so I could spend it with the family.

And because of this bad hire, I was left paying the price for the same work twice.

Have you ever found yourself in a similar situation?

Have you ever hired someone to help you out, but they didn't meet your expectations?

Well, having lived in different parts of the country and having hired plenty of contractors, here's one of the biggest lessons I learned when it comes to hiring help:

If you want to achieve your desired outcome and effectively buy back your time, then it's crucial to have a clear set of expectations and a personal definition of success for your project before you get started.

That's because having clarity not only prevents common pitfalls like cost overruns, unnecessary complications, and potential disappointments.

It also ensures that you can devote more of your time to what truly matters: like family, close relationships, and developing your passion pursuits.

So then, by clearly defining your success criteria and selecting help wisely, you'll be able to optimize the cost and quality of the service you receive.

But more importantly, by taking this approach you’re likely setting yourself up to effectively buy back more of your time in the future.

Buying Back Your Time

So, why should you even care about who or why you're hiring around your house in the first place?

Well, simply put, it's because you have better things to do with your time.

Here's the thing: given where you're at in your career, you've likely earned the ability to buy back your time.

In fact, you're likely in a position where you're juggling the demands of a high-earning career, nurturing your family, and starting to focus on what your legacy looks like, right?

So then, given all the responsibilities on your plate, you very well know that making the most of every single minute of your day is essential.

That's why it's crucial to think about hiring help around the house, whether that's cleaners, gardeners, nannies, contractors, or personal assistants, not just as an expense but as a strategic investment in your future.

You see, as Joe Dominguez points out in his book, "Your Money or Your Life," time is one of our most precious assets.

Because here's the thing: you can't buy any more of it.

But, you can use your wealth to delegate tasks to people who can help you get your time back.

In fact, by delegating daily chores and maintenance tasks on the regular, what you're doing is effectively, you guessed it, buying back your time.

So then, you can use this bought-back time to do the things that add more value to your life and that move you closer to your long-term goals.

But, it's one thing to hire out the work.

And it's another to actually get someone to show up who will actually take things off your plate in a way that adds value over the long term.

That's why what I'm talking about here is more than just getting help.

Instead, it's about creating more room in your life so you can thrive in the areas that matter most to you.

So then, when you approach the act of hiring help around the house as an investment in your quality of life rather than just another cost, it becomes a powerful tool to enhance your life and ultimately help you manage your busy lifestyle more effectively.

The Costs of Not Knowing What You Want

Alright, so now that you know that you need to be mindful about how you hire help, you’re all set, right?

Well, not so fast.

Because, here's the thing: without a clear plan or a clear understanding of what you want to have accomplished, you could end up with projects that are over budget on costs, under-delivered in terms of quality, and inefficient in terms of time management.

How so?

Well, let me tell you another story.

It's a story about a family, maybe much like yours or mine, who decided to build an addition on to their home.

In fact, this was no ordinary addition.

This family had planned on adding a whole new floor to the top of their house.

Now, the head of this household was Tom.

And Tom was a skilled builder but already had a lot on his plate.

So then, Tom teamed up with a contractor friend named Brian to help tackle this big project.

Now, at first, things seemed to get off to a good start.

That's because Tom's family started with intangible dreams and translated them into tangible blueprints.

And so, they thought they had done all the right things to prepare for a beautiful transformation.

Well, construction got underway, and Tom's family was excited to see how the structure of a new second floor was taking shape.

They were talking about how, in just a matter of months, they'd finally have the home they'd been dreaming about for so long.

But before they could get to the finishing touches, Tom began noticing something odd as the bills started coming in.

Something just didn't add up.

The numbers, the costs, they were off, and by a lot.

Now, Tom was keen to keeping a close eye on building expenses and noticed charges for materials that never made it to their house.

In fact, these were charges for materials that they didn't even need and that certainly weren't being used in their renovation.

So, Tom did what any other reasonable person would do, and he brought this up with contractor, Brian.

Now, Tom expected a simple explanation.

But instead of clarity, Tom received defiance.

That's because Brian insisted that everything his crew ordered was used in the build.

But, having been a builder himself, Tom knew this just wasn't true.

Well, push came to shove, and Brian eventually walked away from the job, leaving the family with an unfinished home and a looming legal battle.

But ultimately, in court, it came out that the contractor's crew had been ordering extra materials on Tom's dime that they were using for their own side projects.

So then, eventually, the judge ruled in the family's favor about the unused materials.

But, Tom's family was left with an unfinished home, including no electrical, no plumbing, and no roof: just a shell of what was supposed to be.

Now, what's the point of this story?

Well, while Tom clearly laid out his expectations about how the addition was supposed to be built, he fell short in the selection of his contractor.

You see, Tom placed too much trust in Brian without first establishing the right sort of expectations for how they'd work together.

It was his friend, right?

Well, there's a good reason they say you shouldn't mix business with pleasure.

Because ultimately for Tom, it led to Brian's crew taking advantage of his family and also led to a failed home improvement project.

You know, when it comes down to it, you don't want to pay the price for the same work twice.

What Happens if You Don't Know What You Want

So then this brings us to our next point about hiring help and that's hiring for the right fit.

Because here's the thing: if you don't step into this decision with a clear idea of how you want your helpers to work with you, then you might find yourself facing not just a logistical mess but with an emotional one too.

How so?

Well, what I'm talking about here involves more than just dissatisfaction with unfinished or poorly done tasks.

No, what I'm talking about here gets at your and my core need to feel in control, to feel secure, and to feel like we're capable of making the right choices, right?

Now, up to now, you've likely prided yourself on your ability to smoothly manage things in your professional or personal life.

You've got your daily calendar dialed in, and you likely always start your week by planning out your schedule to ensure you're making the most of your time.

But this week, things aren't going as planned.

That's because the help you hired is not meeting your expectations.

In fact, now you're spending more time managing the helpers than focusing on what you were supposed to use that extra time for, right?

So what happens now?

Well, deep down, I'm guessing that you're feeling a mix of frustration and disappointment.

And there's this nagging thought that maybe, maybe you could have done the job better yourself than to have hired the help in the first place.

So then, the issue isn't just about the financial cost.

No, it's about feeling like you've failed at something as personal as creating the right environment for your family because you really weren't able to buy back your time.

And you know, the truth is that you likely had an implicit expectation that hiring this individual should have made your life easier and more enjoyable, right?

So then, when it doesn't happen as expected, it can feel like a personal setback.

How so?

Well, let me tell you what I mean here.

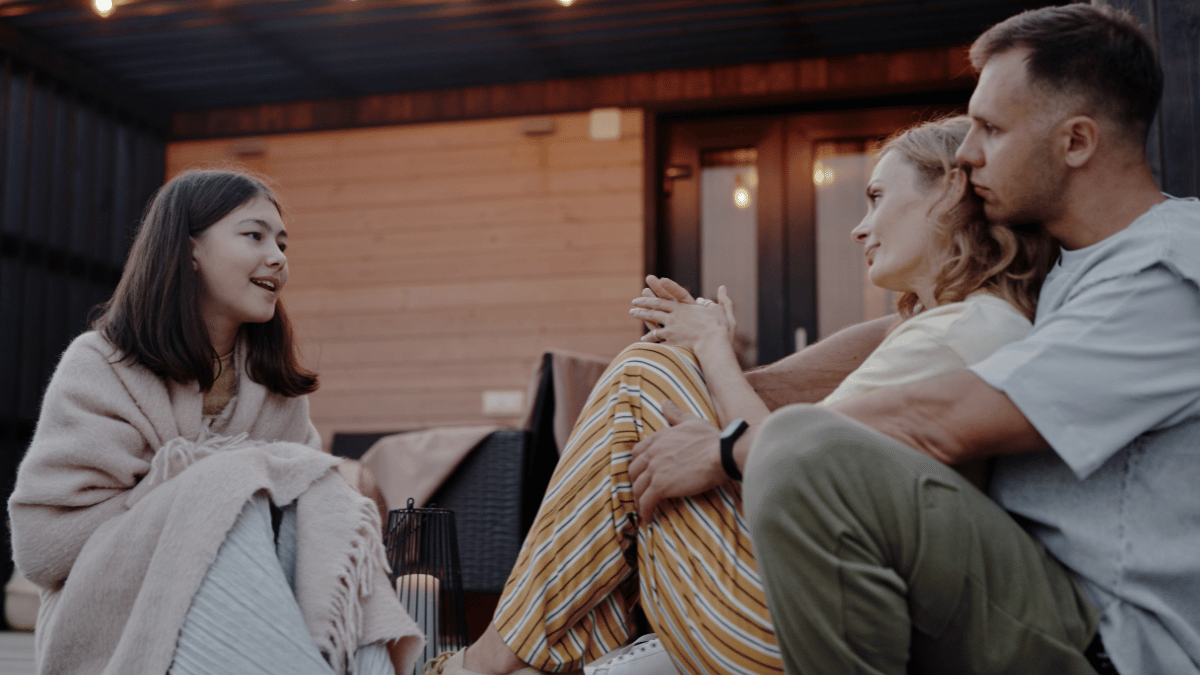

So last spring, I decided to hire a landscaper to help out around the house.

Now, this is work that I'd typically do myself, like mowing, edging, pruning, and generally keeping the yard around the house looking neat and tidy.

In fact, it's work that I generally enjoy doing, but I decided that it was time to buy back my time.

That's because with several changes taking place in my life, I knew that I could really use a few extra hours per week all to myself to relax and recharge.

But ultimately, hiring this help gave me peace of mind knowing that someone was going to come by at a set time each week to take this work off my hands.

Now, this wasn't the first time I hired a landscaper.

In fact, years ago, just after my oldest was born, I hired a landscaper to help out around the house in anticipation of spending more time with my newborn baby.

And back then, I got lucky because the people I hired nailed the work without me saying much about it at all.

They cut the grass, and edged the lawn.

They took care of the weeds growing between the cracks in my walkway without my saying anything about it.

And, they even cleaned the flowerbeds and carried away the leaves instead of filling up my garbage cans.

This crew took care of everything in a way like they were reading my mind.

But you know, back then, I must have simply been lucky or something.

Because last year, I didn't have the same experience.

In fact, I had to call the landscaper back out to my house multiple times to finish mowing the lawn because they missed a few spots.

I even patiently and carefully described what needed to be done, but the poor guy still couldn't get it.

And you know, the way this crew was set up, there was one guy who would come by to mow, and another guy would come by days later to edge the lawn.

It even got to the point where I didn't know when this crew would show up.

Some weeks, the lawn was taken care of, but other would go by, and I'd be staring at an overgrown lawn.

It got to the point that driving by my own home was stressing me out.

It got to the point that I wanted to mow my own lawn, but I felt frustrated because I was already paying someone to do the work, you know?

Well, long story short, I ended up parting ways with this crew and going back to taking care of business around the house.

So, what's the point?

Well, the point here is that this bad hire led to an emotional toll.

That's because the discomfort of dealing with subpar work or the need to micromanage work around the house reminded me of earlier times in my life when I felt out of control or when my financial decisions didn't pan out despite my best efforts.

In essence, the negative experience wasn't so much about the cost, as it was about the emotional toll it had taken on my life.

It was about how my attempt to buy back my time actually backfired and cost me more than it was worth.

So for you then, the lesson here from my experience is that not hiring the right fit can lead to unnecessary frustrations.

That's why getting your hiring decisions right the first time is so crucial.

It's not just about efficiency.

It's also about maintaining your emotional balance and ensuring that your home remains a sanctuary, not a source of stress.

How to Avoid Paying the Price Twice

Alright, so then, what can you do to ensure that you're hiring the right help and not paying the price for the same work twice?

Step #1: Clearly Define Success

Well, you can start by clearly defining success.

Now, this work involves gaining clarity on what you want to have accomplish before you actually go out and hire help.

You see, without a clear vision of what success looks like, the work that your helpers show up to do can become disjointed and ineffective.

But, with clear goals, you get clear actions, which in turn result in clear outcomes.

That's why, one of this first things that I do when I go looking for help is to start by defining what success looks like to me.

What I'm doing here is aligning all my efforts and resources toward achieving that defined objective.

And so, where do you begin?

Well, what I typically do is ask myself, "What specific outcomes do I expect to see once the project is complete?"

Here, you're not focused on "how" the work is supposed to be done.

Instead, you're turning your attention to the "what," or more specifically, what you want to see this individual or crew bring into reality.

Now, defining clarity might involve researching similar projects, getting to know industry standards, or even consulting with experts so you can set appropriate expectations.

Either way, what you'll want to do is to prioritize your non-negotiables.

Then, be ready to articulate your vision clearly and effectively once you start engaging with potential service providers.

Step #2: Hire for Outcomes, Not Cost

Now, one of the biggest mistakes I’ve made in the past is to base my hiring decisions solely on price alone.

That's because, more often than not, those low-cost providers are likely focused on quantity instead of quality.

And, you know, going with a low-cost provider is likely to turn you into another job that they simply rush through instead of focusing on you a highly valued client.

That's why when you're hiring for outcome, what you're doing is ensuring that the quality of work meets your needs and expectations and that it aligns with the goals you've meticulously set out in step one.

And so here, when I'm getting ready to hire help, one of the things I ask is, "Is my intended hire truly committed to my defined outcome?"

In other words, are they willing to go the extra mile to give me what I want, or am I just another job that they need to get through?

So then, to figure this out, what I've found works best is to have candidates describe what the end results will look like. But what I’m listening for is not how they’re doing the work, but what their vision for the work will look like.

In other words, instead of telling them how they should do their job, I'll go back to step 1 and articulate what success looks like to me.

So then, if they can reiterate back to me my own vision, then I know that we’re likely on the same page.

Remember, you don't want to pay the price by doing the same work twice.

Step #3: Have a Backup Plan in Place

Finally, when it comes to hiring effectively, I want to ensure that I have a backup plan in place to deal with the inevitable hiccup.

Whether it's a house that isn't cleaned to your standards, a garden that's neglected, or a home repair that's incomplete, these letdowns can disrupt your routine at best and cost you all the time you thought you had bought back at worst.

That's why being prepared for these eventualities is crucial in maintaining the smooth operation of your household and helps ensure that your family's well-being is taken care of.

So then, the number one question I ask of a service professional before I hire them is, "How will you make the situation right if the work goes wrong?"

Here, what I look for is someone to tell me more than, "we'll take care of you" or "you have nothing to worry about…"

Because the truth is that a lot has changed in recent years, so yes, I do have a lot to worry about.

That's why you'll want to ensure that your contract or service agreement includes clauses that address non-delivery or non-performance and how those situations might be resolved.

Don't Pay the Price by Doing the Work Twice

You know, when it comes down to it, hiring help in your personal life is one of the most effective ways of buying back your time.

At the same time, it could very well turn into a fruitless effort if you don't approach hiring it from a place of intention.

That's why I take the time to first clearly define what success means to me.

Then, as I'm screening candidates, I communicate these goals clearly to my helpers and have a backup plan just in case things don't work out.

Remember, your ability to get the most out of your service provider starts with you.

That's because if you don't clearly communicate your expectations when you hire them, you could end up with problems that go beyond money.

Indeed, without a clear plan, you could risk facing projects that cost too much, you could experience subpar service, or you could wake up with even less time on your hands than when you started.

But think for a moment how your life would change if you ended up getting it right.

Imagine what you could do with an extra 5, 10, or 20 hours per week if you just took a few minutes now to define exactly what you need and what you expect from those you invite into your home to help.

That's why, if you're in the market to hire help, it's essential to start with clarity and purpose in what you want accomplished.

Because by doing so, you're not only buying back your time, you're taking one step closer to becoming the master of your own financial independence journey.

If You Don't Write Your Story, Someone Else Will

"How do I want to be remembered?"

You know, the older I get, the more I linger on this question.

And it's not because I'm intentionally looking for ways to gain notoriety.

Instead, I've come to realize that I only have a finite amount of time to get done what I was put on this earth to do.

The reality is that, over time, my priorities have changed.

You know, the motorcycle life that I once was so fond of in my youth is now long gone.

And today, when I think about working out, it's more about staving off heart disease than it is toning down my waistline.

But when it comes to how I want to be remembered, I'm reminded of a truly impactful quote that I recently came across that said, "In 100 years, no one will remember who you are."

It's shocking to think about, right?

In a way, I'm sure you likely already knew that intuitively.

I mean, can you remember your great-grandfather's name without looking it up or asking a relative?

I start getting depressed just thinking about it!

But here's the thing: instead of looking at this quote as being a cause for disappointment, I've used it as my inspiration to purposefully write my life's story.

You see, in 100 years, few people will care about what corporate title I earned, how much money I made, the square footage of my home , or all the toys I've owned.

But they'll likely be interested in my legacy, or rather, the story of what I did with my life.

Have you thought about your legacy lately?

Have you thought about what folks will say about you in 100 years?

And no, I'm not talking about the monetary inheritance that you could leave behind.

Instead, your legacy is the story that you want people tell about you when you’re not here to tell it yourself

But here's the thing though: your legacy can only be as solid as the vision for the ideal world that you're trying to bring into reality in the right here and now.

It's something that you can make happen right now; it's not something that magically happens in the future.

That's why, if you want to create a story worth remembering, then you need to prioritize daily activities that are aligned with your legacy-building vision.

Because if you don't, in 100 years, someone else will write your story.

What's Keeping You from Writing Our Story

So then, what does it look like when someone else writes your story?

Well, consider the story of Nikola Tesla.

Now, as you'll likely recall, Tesla was an inventor and engineer known for his contributions to the development of many things you use today.

These include things like alternating current (AC) electricity, wireless communication, and a number of other innovations that you can look up on the web.

Here's the thing, though: Tesla's legacy has been shaped by historians in ways that emphasize certain aspects of his life while leaving out others.

How so?

Well, many times, historians will portray Tesla as an eccentric genius who struggled financially and was overshadowed by Thomas Edison.

In other words, he failed because he didn't get rich like Edison, right?

Now, the trouble here is that this portrayal of Tesla's legacy has created a narrative that often focuses on his rivalry with Edison and his financial difficulties instead of his genuine passion for science and innovation.

That's because, by many accounts, Tesla was deeply dedicated to advancing technology for the betterment of humanity.

And this dedication is evident in his numerous patents and contributions to various fields, including electricity, radio, and wireless communications.

Ultimately, Tesla had a visionary approach to his inventions and was more focused on their potential societal impact than his own personal gain.

In other words, he wasn't as concerned about the money as he was about the work, but the story that was written about him put the emphasis on money.

And that likely came from the comparison between him and Edison.

Now, had Tesla been able to shape his narrative more effectively, he might have been remembered differently.

He might have been remembered not only for his scientific genius but also for his integrity and commitment to making the world a better place through his inventions.

Maybe, had Tesla been a little more thoughtful with his finances, he'd have been better known today as a visionary who made a big impact, instead of the guy that got beat out by Edison, right?

Indeed, your legacy goes beyond how you want to be remembered. It's about the impact you make through every little daily choice you make today.

Daily Distractions

Now, the trouble is that so many of us want to do good.

We want to make an impact in our families, in our communities, and in the world around us.

And now, certainly, you likely want to make an impact and do the right thing on a daily basis, right?

The trouble is that outside obstacles often distract you from focusing on your long-term goals.

Indeed, in the context of building a legacy, you'll likely face a host of daily distractions like emails, social media notifications, and urgent but not important tasks that compete for attention.

And these distractions tend to pull you away from activities that would otherwise contribute meaningfully to your vision for the future.

In fact, these external distractors are relentless and seemingly everywhere.

And you know, the trouble is that they make it very hard for you to stay focused on what truly matters because your attention is constantly being pulled from one fire that you need to put out to another.

You're doing busy work, but you're not making any progress.

And so, all those well-intentioned plans that you had laid out with your family or the time you planned to contribute to your local non-profit are once again put on the back burner.

Now, here's the thing: this constant tug-of-war between the immediate demands of life and your long-term goals can lead to a disconnect.

That is, it inflames those feelings of frustration and a sense that the demands of everyday life are diluting your efforts.

But, where you give your time and energy is your choice.

Because, if you don't write your story, someone else will.

Internal Struggles

Now, oftentimes, those daily distractions aren't a cause but an effect.

In other words, what if you're staying busy because you want to avoid thinking about the bigger picture of life?

Let me tell you what I'm talking about here: You see, in the early 1970s, there was this psychologist by the name of Wayne Oates, who found himself grappling with his own relentless compulsion to work.

He found himself distracted by external things, or so he thought.

Now, this wasn't just about being sucked into the nine-to-five grind.

In reality, Oates was dealing with an internal struggle and he couldn't understand his compulsion to work so much.

Have you ever felt this way? Have you ever felt the need to be the one to turn out the lights in the office at night?

And so, he did some digging. He looked internally and used his own professional observations to eventually give a name to his struggles, which he called "workaholism."

And so, as part of this discovery process, Oates ended up writing a book called, "The Confessions of a Workaholic: The Facts About Work Addiction."

Now, the book starts off with an account of Oates' own life experiences and offers an inside look at how his work consumed his life, including how it cost him his personal relationships and his health.

But here's why this all matters. Oates helps give us a modern-day definition of workaholism.

He helps us understand how our own internal struggles often manifest as external issues that distract us from doing the essential things in life.

Now, you likely already have your own definition of workaholism.

But let's go back to the original definition as Oates describes it, because it's quite telling.

Now, Oates defines workaholism as an uncontrollable need to work incessantly, where an individual is internally compelled to work hard, often exceeding what is required.

But the big question here is, "why?"

What would compel an individual to behave this way, right?

Well, that's what Oates talks about in his book.

And so, Oates goes on to talk about how traits like perfectionism, a need for control, and fear of emotional intimacy can drive a person deeper into the arms of their work.

But the big takeaway here is that the struggles that individuals face internally, often lead them to mask their problems with external solutions.

That's why, ignoring the internal struggles of doubt and uncertainty when it comes to writing your life story can result in a lack of decisive action towards building your legacy.

So what happens if you don't do anything?

What if you think you're doing something, but in reality, you're just engaging in busy work?

Well, there's a cost.

And the emotional toll can include a persistent sense of dissatisfaction and the haunting question of "what if?" when it's too late, like:

What if I had started that side hustle?

What if I made it to my kid's ball games more often?

What if I took more time with that precious relationship?

What if?

What if...

You know, if you don't write your story, someone else will.

How to Write Your Own Story

So then, what can you do to move past the internal and external struggles and get to a place where you can begin write your own story and building a legacy you want to leave behind?

Step #1: Identify Your Values

Well, the first thing you'll want to do is to take the time to identify and get to know your values. Now, you'll likely recall that your values are not the things you aspire to be, but rather, they're the things that are important to you right now.

Now, this distinction between aspiration and actuality is crucial because aspirations are often externally influenced, while what you really value is often something internally important to you.

In other words, you're born with it.

Indeed, these are things that you would genuinely care about if no one was standing around watching what you're doing.

But for now, what you need to know is that gaining clarity on what is truly essential allows you to filter out the noise and focus on what genuinely matters to you and to the legacy you're creating.

And so, by defining your core values and the ultimate impact you want to leave behind, you can prioritize the actions and decisions that align directly with your life's purpose.

And how exactly do you go about doing this work?

Well, you can start by asking yourself, "Do I truly understand what's essential in my life, and if not, how can I find out?"

One thing you can do here is to take the time to complete a values assessment.

At the very least, review resources like James Clear's Core Values List.

Either way, I've covered the topic of values discovery in previous posts and episodes, so be sure to check out those resources at https://legacygenone.com.

But doing this work will give you a solid base from which to make your decisions.

Step #2: Practice Deathbed Meditation

Now, the next thing you'll want to do visualize what happens in your world after you’re gone.

And one helpful approach to this end is to practice Maranasati meditation or otherwise known as deathbed meditation.

And what exactly is Maranasati meditation, you ask?

Well, Maranasati meditation is a type of meditation that helps you not only think about but also accept the idea of death.

And so, why would you want to take the time to think about dying?

Well, this kind of meditation encourages you to think about how death is a natural part of life and to appreciate how everything in life is truly temporary.

That's because, when practicing Maranasati meditation, you might imagine what happens when you die or think about the process of your body getting older and eventually not working at all.

The goal here isn't to make you scared but to help you value life more fully and to worry less about minor problems.

So then, by frequently thinking about death in a calm way, what you're actually doing is giving yourself the ability to enjoy your life even more.

And how exactly is this possible?

Well, that's because you start to learn how to live in the moment and not get too upset about things that are impermanent or simply don't matter.

Ultimately, this meditation can help you feel more at peace and ready to handle whatever life throws your way.

So then to do this, start by asking yourself, "In my final moments, who will I be surrounded by and how will they remember me?"

Then, consider all of the values you've identified in the previous step and find a quiet space to reflect on your life as if in your final moments.

Consider the alignment between your current path, or the daily choices you're making today, and your deepest values.

Then, use this reflection to set intentions or goals that bring you closer to your ideal life vision, and keep track of these insights for future guidance.

Step #3: Take Daily, Incremental Steps

Now, the last thing that you'll want to consider as you're intentionally writing your story is to focus on your most important actions.

These are the things that you want to be doing each and every day to get you on your path and move you closer to your ideal version of your life story.

And so, what does this look like?

Well, consider the story of Mike Flint.

Now, Flint was Warren Buffett's personal pilot.

And you remember Buffett, right?

The Oracle from Omaha?

The billionaire investor?

Well, before working for Buffett, Flint had flown for four U.S. Presidents.

And so, by many measures, he was an accomplished pilot. But he was looking for more.

So then, as Flint tells it, one day, he approaches Buffett looking for advice on furthering his career.

So, what did Buffett do?

Well, Buffett asked Flint to list his top 25 career goals and then circle the top five most important ones.

At this point, Flint thought that he would work on his top five goals immediately and then focus on the remaining 20 when he had free time, right?

Well, it didn't work out that way.

That's because Buffett gave Flint a surprising instruction: He told Flint he should avoid the 20 uncircled items at all costs until he had achieved his top five goals.

These uncircled items, Buffett explained, are not just distractions but also potential traps that could divert his energy and focus away from his most critical objectives.

Now, this isn't a one-size-fits-all solution.

Not everyone can have a single-minded focus and achieve the top things in their life at the cost of other priorities.

But, Buffett's advice not only highlights the importance of focusing on your highest priorities and also underscores the necessity of avoiding less critical tasks that can impede significant progress.

That's why you'll want to take the time now to think about the small steps you need to take each and every day to move you closer to the story you want to write.

With that said, I'm not talking about doing work for work's sake.

More specifically, you'll want to make sure that you match your actions to your values.

It's about taking intentional daily steps.

It's like making sure each puzzle piece fits so you can see the big picture of your dream life coming true.

So then, to begin, you'll want to take the time to ask yourself, "What do I need to do today to live in alignment with my values?"

Then, every day, try to do one small thing that shows you what's really important, whether that's being more kind or more helpful to others.

Remember, it's okay to make mistakes; the most essential part here is to keep trying to live by your own value system, not what you think others want for you.

Ultimately, the point here is to do one thing today that moves you closer to where you want to go.

So then, don’t let another day pass you by.

Go grab a pen, outline your vision, and commit to one small step today that brings you closer to the legacy you dream of.

If You Don't Write Your Story, Someone Else Will

Remember, the story of your life is yours to write.

If you're anything like me, you'll likely want to be proud to hear what your family or loved ones have to say when they tell it.

That's because if you don't take charge and define the legacy you want to leave behind, you risk allowing life's daily hustle and others' agendas to shape your path and the steps you take.

Remember, each day spent without aligning your actions to your true purpose is a missed opportunity to forge a meaningful legacy.

Ultimately, the world will remember you not just for your good intentions but for what you did with your time.

So then, you'll likely want to make sure it's a reflection of your true aspirations. Because if you don't write your story, someone else will.

But, what if you do end up writing your story the way you want it to be read?

Imagine what could unfold in your life today if you decided to prioritize what truly matters.

Picture a future where, each day, you commit to small, deliberate actions that align seamlessly with your deepest values and aspirations.

That's why it's crucial to not wait for another year to wonder what could have been.

Start now, start today so you can not only begin defining what’s truly important to you, but so you can write your own story by taking one step closer to becoming the master of your own financial independence journey.

Torchbearers: Raising Kids Who Care About Your Legacy

Who will tell your great tales and your family's story when you're gone?

Now, if your first inclination is to say, "I hope it's my children," then your situation might not be as definitive as you think.

The truth is that in about three generations, you will be forgotten without a proactive approach to keep your story alive.

You see, the fact is that a lot of work goes into passing along your family's legacy.

To be sure, Native American cultures, who are known for their oral storytelling traditions, put a great deal of forethought into raising up the next generation of storytellers, which often starts from childhood.

Now, sure, you can keep a journal, write a memoir, or even produce a family legacy video to preserve and share your story.

But here's the thing: you'll still need an interested party to engage with the content you create.

And the thing is that people want to hear from people.

So then, who will pass along your family's story for generations to come?

That's where your torchbearers come into play.

These individuals will be responsible for keeping your family's story alive and carrying along your family's traditions.

However, to effectively pass your legacy from one generation to the next, you'll want to ensure that your family has a shared set of values from the start.

You'll also need to identify the right person in your family to carry your family's story, and then you need to do the work to raise up the next generation of torchbearers.

Indeed, this approach is not just about ensuring that your memory lasts well beyond your passing; when done right, it will provide a living guide that influences decision-making, instills values, and ensures the continuity of your family's legacy in an ever-changing world.

Ultimately, this work is about giving your family a head start so that future generations don't have to constantly reinvent the wheel so they can pursue their own measure of happiness.

Instilling Ideals and Values

Alright, so one of the first things that you'll want to do when it comes to raising up your family's torchbearer is to start with your family's values.

Indeed, building a legacy that lasts the test of time is about much more than just the wealth you accumulate, it's about the values and ideals you instill in your family.

That's why, as you're starting out as a first-gen wealth builder, your journey starts by embedding a strong foundation of core values that guide every action and decision your family makes.

Identify Your Core Family Values

And, you can think of your family's core values as the guiding stars for your collective journey.

Now, these aren't just abstract concepts but the principles that you live by every day.

Whether it's the importance of honesty in all dealings, the commitment to giving back to the community, or the relentless pursuit of excellence, these values define who you are as a family.

It's your family's DNA and is passed on from one generation to the next.

That's why creating a family values statement is a powerful way to articulate these ideals.

Now, we've discussed a number of formal and informal ways to identify your family's values in past articles.

But for now, you could start as simply as sitting down with your entire family and discussing what each person believes is most important.

Here, you've got the chance to listen, understand, and come together to craft a statement that reflects the collective heart of your family.

This process not only clarifies your family's values but also strengthens your tribe's bond together.

That's why getting everyone involved in defining and expressing these values is crucial.

So then, while creating a basic values statement is a good start, you'll also want to consider organizing regular family retreats where you can dive deeper into these discussions.

These retreats can become a sacred time for your family to connect, reflect, and align on your shared values.

It's about ensuring everyone, from the youngest to the oldest, understands and feels connected to these guiding principles.

It's a way to go back to your values statement and ensure that it reflects your family's story and that you haven't missed any crucial points about what makes your family unique.

Identifying and Supporting Torchbearers

Alright, once your family's foundation of ideals and values is firmly in place, the next critical step is identifying and supporting the torchbearers within your family.

Now, it's crucial to note here that these individuals don't just serve as scribes or reporters.

That's because they'll become the living embodiment of your family's values and, thus, need to be motivated and capable of leading in a way that sustains your family's legacy.

Defining Leadership Roles

Indeed, torchbearers are those within your family who naturally take the initiative, show a deep commitment to your collective values, and possess the leadership qualities necessary to guide others.

So then, identifying these individuals involves looking beyond age or birth order to recognize who genuinely demonstrates these traits and how they can embody this crucial role.

That's why these individuals might be the niece who organizes family volunteering events, reflecting a commitment to community service, or the cousin who always steps up to mediate and resolve conflicts, showcasing leadership and a commitment to family unity.

Either way, identifying who will carry on your story involves more intention because recognizing potential torchbearers is a nuanced process.

Indeed, it's about observing not just what family members say but what they do, how they act in family and external activities, and how they lead by example.

Preparing for Responsibility

Now, once you've identified your torchbearer, this recognition shouldn't result in a formal coronation but a natural acknowledgment of their roles and contributions to the family.

Indeed, it's about highlighting the values and behaviors that led you to choose this individual in the first place, while enabling the rest of the family to see how this individual exemplifies and supports the family's overall vision, mission, and values.

At the same time, celebrating these qualities and actions publicly within your family encourages these behaviors and signals to others the value placed on leadership and service to the family's legacy.

Now, supporting your identified torchbearers is crucial for their development and continuing your legacy.

You can't just tell them how great they are and expect them to perpetuate your family's story.

They need ongoing support.

Now, this support can take many forms, from targeted education opportunities that align with their interests and the family's values to leadership roles within family enterprises or philanthropic efforts.

And so, how does this work?

Well, if a family member shows a keen interest in the arts and your family values cultural contributions, then supporting their education in art history or museum studies and involving them in the family's art foundation could be a way to nurture their passion and align it with the family legacy.

Mentorship is another way to support your family's up-and-coming torchbearer and plays a key role in preparing torchbearers for their responsibilities.

That's why pairing them with seasoned family members or even external mentors who can share wisdom, experiences, and guidance is crucial to their long-term development.

Now, this mentorship should ideally be structured like a coaching relationship. One that's built on a two-way exchange where questions are encouraged and learning is mutual.

This approach ensures that you have full buy-in from your chosen leader, and allows you to optimize your approach when viewed with a fresh set of eyes.

Either way, by identifying and supporting your family's torchbearers, you're not just preparing individuals to carry on a legacy, you're ensuring that the family's future leaders are ready and able to navigate the challenges and opportunities ahead.

It's a step that reinforces the importance of individual contribution within the context of the family's collective mission, ensuring that the torch of your family's legacy burns brightly for generations to come.

Keeping the Torch Lit

Alright, so we discussed why it's crucial to build your family's story around values that you want to pass along and how a torchbearer can be crucial to this end.

But the next big question here is, "Who will train the trainers?"

To be sure, it's one thing as a first-gen wealth builder to raise up your torchbearer to carry along your family's story.

And it's another to ensure that future generations will continue the same process and keep your family's torch lit.

That's why training the next generation of torchbearers is a dynamic process and one that ensures the continuity and growth of your family's legacy.

Indeed, it's about creating a culture of teaching by actively engaging younger family members, immersing them in the family's core values, and equipping them with the skills and knowledge they need to thrive as future leaders.

So then, assuming that you already have your torchbearer identified, how do you go about creating a teaching culture?

Engaging with the Rising Generation

Well, you can start by creating opportunities for the younger generation to deeply connect with the family's core values and legacy.

This engagement should be interactive and meaningful, and allow them to experience firsthand the impact of these values in action.

For instance, you can involve them in family philanthropy projects that align with your values, or include them in discussions about the family business, highlighting how these ventures reflect the family's mission.

This hands-on approach not only strengthens their understanding of the family's values but also fosters a sense of responsibility and pride in carrying these forward.

And the best thing is that you can start this process early because the work is about exposing family members to your family's values in living action and allowing them to learn through osmosis, at least initially.

Development Programs

Now, as children in the family get older, you'll likely want to consider developing formal training programs tailored to your family's legacy, to help build their skills and knowledge in being potential torchbearers.

Now, this approach could include workshops on financial literacy, leadership retreats, or internships within the family business.

And the goal here is to provide a structured yet flexible learning environment that caters to their interests and developmental needs.

For example, if your family values environmental stewardship, a summer internship with a green technology firm could provide practical experience and inspire innovative thinking about how to integrate these values into the family's investments and philanthropic efforts.

Mentorship and Transition

Here again, mentorship is also crucial in the training process, and serves as a bridge between generations.

That's why it's crucial to establish structured mentorship relationships that pair potential torchbearers in gen-three, gen-four and so on with contemporaneous leaders who exemplify the family's values and have successfully navigated the challenges of stewarding the family's legacy.

This mentorship approach can also facilitate a smoother transition of roles, and ensure that when the time comes, the next generation is prepared not just to take the reins but to lead with vision and purpose.

It's about passing on not just the tools for success but the wisdom to use them wisely, ensuring that your family's legacy continues to evolve and flourish in the hands of each new generation of torchbearers.

Indeed, by engaging, educating, and empowering the next generation in this way, you do more than prepare them to inherit a legacy, you're inspiring them to become conscientious custodians of a rich heritage that transcends financial wealth, imbuing them with the values, skills, and vision to lead your family into the future with confidence and integrity.

Torchbearers: Raising Kids Who Care About Your Legacy

You know, when it comes down to it, crafting a legacy is more than a testament to one's achievements, it's a deliberate and thoughtful process that ensures your family's values, stories, and aspirations are preserved and passed down through generations.

That's why, if you're in the throes of building first-generation wealth, this work is not merely about financial success but about embedding a culture of values, leadership, and legacy within your family that lasts for generations to come.

It's about identifying those who will carry the torch of your family's legacy, supporting them, and ensuring the continuity of your family's story in a way that resonates with both the present and future generations.

Indeed, the essence of your legacy lies in the impact it has on the lives it touches and the future paths it paves.

It's about making intentional choices now that will empower your children and their children after them to build upon the foundation you've laid, guided by the principles and values that define your family's identity, and, ultimately, help future generations become the masters of their own financial independence journey.

How to Pass on a Healthy Money Mindset Legacy

Many well-meaning parents want to raise children with wise money habits.

Who doesn't want their kids to be good financial stewards, right?

Well, what some end up doing, however, is unknowingly passing along money beliefs that limit their children financially, often for far too long than necessary.

Indeed, some parents may unintentionally transfer their own financial anxieties and insecurities to their children, perpetuating a generational cycle of financial fear and avoidance where children grow up feeling anxious about money because they've absorbed their parents' fears.

And so, what tends to happen then is that children raised with a limiting financial mindset end up lacking the confidence to make informed financial decisions.

That's because these individuals may either become overly conservative, missing out on beneficial financial opportunities, or too reckless with their savings because they don't understand the value of prudent financial planning.

Ultimately, if children don't learn to manage money wisely, building and maintaining generational wealth becomes challenging.

That's because, without the ability to navigate investing, save intelligently, and spend judiciously, you're going to face an uphill battle when it comes to passing along your financial legacy.

So then, what can you do to ensure that you're not passing along limiting money beliefs to your kids?

Well, you can start by first taking some time for introspection and getting to know your own money scripts, or money belief system. Then, you'll want to make a conscious effort to move beyond your own limiting beliefs by cultivating a growth mindset and then, most importantly, sharing what you've learned with your family and involving them in your wealth-building process.

Indeed, by uncovering your own money beliefs and shifting towards a growth mindset, what you're doing is not only reducing the chance of transmitting limiting money beliefs to your kids, you'll also pave the way for them to make smarter financial decisions and share those new habits with their own children.

Recognize and Understand Your Money Scripts

So then, at the core of first-gen wealth building lies a critical yet often overlooked challenge, and that's identifying and challenging limiting money beliefs.

And so to start, you're likely asking, "what is a money script?"

Definition and Origin

Well, the idea of money scripts is a concept introduced by financial psychologist Brad Klontz.

And based on his own professional experience and observation, what he's trying to describe are the subconscious beliefs about money that shape our financial perspectives and the way we behave with money.

Now, more often than not, these scripts are typically formed in childhood, and rooted in our earliest observations and experiences related to money within our family and societal context.

Whether it's the belief that "money is the root of all evil," "you have to work hard to get wealthy," or "money doesn't buy happiness," these scripts play a pivotal role in our financial lives, often without your conscious awareness.

If you think about it long enough, you could probably identify some unique situation or experience in your family of origin that defined how you act around money today.

Identification

Indeed, identifying your own limiting money beliefs is the first crucial step toward overcoming them, and ensuring that you don't pass them down to your kids.

Now, this process involves introspection and reflection on your financial decisions and understanding the emotions tied to those decisions.

How so?

Well, consider moments when you've felt anxious about spending or investing, or times when you've avoided financial planning altogether.

At the time, it might have felt like simple procrastination or analysis paralysis.

Nevertheless, these reactions can be clues to underlying, subcoscious money scripts borne in childhood that are guiding your behavior today.

For example, if you find yourself hesitating to invest in the stock market, even though, logically, you know its potential for long-term growth, then you could be holding on to a deep-seated belief that investing is too risky, which is reflective of a script that can hinder wealth accumulation.

Impact Analysis

To be sure, the impact of these limiting beliefs on not just your personal wealth, but also your family wealth dynamics can't be overstated.

And that's why, As James E. Hughes Jr. points out, these scripts not only affect how individuals manage their own finances but also how they communicate about money within the family, potentially perpetuating harmful financial behaviors across generations.

How so?

Well, a parent who subconsciously believes that talking about money is taboo may fail to educate their children about financial literacy, leaving them ill-prepared to manage or grow family wealth in the future.

That's why recognizing and understanding your money scripts is a vital first step in breaking free from the cycle of limiting financial beliefs.

So then, by bringing these subconscious beliefs to light, you can begin the process of challenging and transforming them, setting the stage for more empowered financial decisions that pave the way for generational wealth and prosperity.

And this journey of financial self-awareness is not just about enhancing your own money management skills, it's about ensuring that your legacy, one that's full of knowledge, empowerment, and financial well-being, can be passed on to future generations.

Break the Cycle and Cultivate a Growth Mindset

Alright, so once you've identified your money script and the impact that it's having on your family, the next step is to create a new set of beliefs that align with where you want your family to go.

Now, it's often easier to say what you want to do than actually doing it. That's why, to bring these new beliefs to reality, you'll also need to cultivate a growth mindset.

Indeed, breaking the cycle of limiting money beliefs and cultivating a growth mindset is a transformative first step towards personal financial success and the fostering of generational wealth.

Now, this transformative phase is about challenging those deep-seated scripts that have governed your financial decisions and behaviors for so long, and reshaping them into empowering beliefs that open the door to wealth and prosperity.

You're not eliminating or erasing these beliefs, but editing them and rewriting them to suit the lifestyle you've envisioned for yourself and your family.

Challenging Limiting Beliefs

So then, where do you start?

Well, the journey begins by confronting your limiting money scripts head-on.

Indeed, as Klontz points out in his book, "Wired for Wealth," you can start by questioning the validity of these beliefs and evaluating whether they're truly reflective of your reality, or whether they're echoes of past circumstances.

Now, this questioning approach is so crucial because it can often unravel some loosely held, yet still detrimental scripts, allowing you to see them for what they are: outdated narratives that no longer serve you well.

For example, if you've been held back by the belief that "you have to work hard to get wealthy," and have given yourself time to enjoy your family or your wealth, then you can challenge this belief by defining your own measure of "enough", and considering investment opportunities that can grow your wealth without the constant need to exchange your time for money.

Here, it's about recognizing that while hard work is valuable, defining your own level of satisfaction and evaluating smart financial strategies can also lead to prosperity.

Growth Mindset Development

The next thing you'll want to do is to cultivate a growth mindset.

Now, cultivating a growth mindset towards wealth means embracing the idea that your financial capabilities are not fixed but can be developed through dedication and learning.

It's seeing mistakes not as failures but as valuable learning opportunities.

Indeed, what this approach is ultimately about is fostering a healthy mental lifestyle.

You can think about it as if you've decided to train for a marathon.

Simply going to the gym a few times a week or getting in a few 5Ks per month isn't going to cut it.

If you're going to accomplish this feat, you'll need to consider how you're sleeping, your rest cycle, how often you're training, and so forth.

Your entire health lifestyle shifts to accommodate this new goal.

In a similar way, developing a growth mindset to challenge limiting money beliefs includes developing an approach that values perseverance, adaptability, and the continuous pursuit of knowledge.

Practical Application

And so, how do you go about doing this work?

Well, to start, it's essential to acknowledge these limiting beliefs as they come up, just as you would when overhearing a familiar but outdated song in your mind.

You can recognize it, yet don't feel compelled to accept them as truths.

What you need to do is challenge these beliefs by questioning their validity, and you can do this by asking yourself whether they are indeed accurate reflections of your capabilities or simply echoes of past constraints.

Now, this process isn't about dismissing your experiences but rather considering new financial possibilities. It's by going back to the start of those limiting beliefs and identifying ways to reimagine them to suit your current life and family goals.

Then what you'll want to do is leverage your inherent love for learning and self-improvement and apply this enthusiasm towards enhancing your financial literacy.

This could involve exploring resources like books, podcasts, or seminars that broaden your understanding of managing your money.

You can also try engaging with the narratives of individuals who have successfully navigated financial transformations. Try on their experiences, walk a mile in their shoes, and learn if their approach could help you as well.

This isn't approach isn't just about accumulating knowledge, it's about exposing yourself to diverse financial philosophies and recognizing the breadth of options you have available to you.

Finally, embrace the concept of small wins and experimentation.

Now, chances are that you're likely in a unique position where you can afford to take some calculated risks.

Try out new investment strategies on a small scale, or allocate a portion of your wealth to support causes you care about, and observe what you learn from these experiences.

It's like training for a marathon: you don't start by running the full distance on day one.

You build up to it, learning and adjusting your strategy as you go.

Celebrate each success, no matter how minor it may seem, and use setbacks as learning opportunities, not evidence of failure.

Educate and Involve Your Family in Wealth Building

Alright, so we've talked about identifying limiting money scripts and developing a growth mindset to move beyond them.

The next thing you'll want to do to ensure that you're setting the stage for your children to develop healthy money habits is to teach your children what you've learned.

And why would you want to do this?

Well, teaching what you've learned is crucial for breaking limiting money beliefs and nurturing a growth mindset because it reinforces your understanding and challenges you to clarify your thoughts.

Indeed, as you explain your financial insights to others, you deepen your own grasp and commitment to these ideas and distance yourself from outdated beliefs.

In fact, the act of sharing fosters a cycle of continuous learning and self-improvement, making you both a learner and a mentor and propelling you further away from those limiting scripts.

At the same time, educating and involving your family in wealth-building marks a pivotal step towards not only managing your money effectively but also ensuring its growth and sustainability across generations.

Family Financial Education

So then, when it comes to sharing your knowledge with your family, you can start by integrating financial education into your family's weekly and monthly routine.

The objective here is to demystify money matters and make financial discussions a regular part of your family's life.

Now, you can start this knowledge sharing with basic concepts like earning, saving, and spending for younger members and gradually introduce more complex topics like investing, taxes, and estate planning as they grow.

Either way, what you'll want to do is ensure that the tools and resources you discuss are tailored to different age groups so you can make learning engaging and relevant and set a solid foundation for engagement.

Wealth Transfer Planning

Then, as you've moved through the basics of money management and have a solid process in place for transferring knowledge, you can begin incorporating weightier topics like wealth transfers to ensure a solid base for legacy building.

Now, involving your family in wealth transfer planning discussions is crucial for preparing them to manage and preserve your family's wealth for generations to come.

This could include conversations about estate planning, philanthropy, and legacy preservation.

And so, by making these discussions inclusive and starting early, what you're doing is ensuring that your wealth transfer aligns with your family's values and goals and that each member understands their role in the continuity of the family's financial legacy.

For example, discussing the creation of a family foundation can be a way to involve everyone in philanthropy because it allows each member to contribute to decisions about charitable giving.

This approach not only helps in passing on financial wealth but also instills a sense of purpose and responsibility towards the wider community.

Modeling Positive Financial Behaviors

Finally, it's one thing to tell your family to do as you say. And it's another for them to do as you do.

That's why, as a parent or guardian, modeling positive financial behaviors is perhaps the most influential tool in your arsenal for instilling a healthy financial mindset in your children.

And what does this look like?

Well, this means making transparent financial decisions, openly discussing financial successes and setbacks, and showing how challenges can be navigated through informed decision-making and resilience.

At the same time, encouraging open communication about money removes the taboo surrounding financial discussions, making it easier for family members to express their views, ask questions, and share their aspirations.

Indeed, educating and involving your family in wealth building is a transformative step that not only enhances your family's financial literacy and preparedness but also cements a legacy of shared values, collective responsibility, and enduring prosperity.

So then, by taking proactive steps to educate, plan, and model positive behaviors, what you're doing is laying the groundwork for a future where your family's wealth is not just preserved but flourishes and, more importantly, is supported by a foundation of knowledge, unity, and purpose.

How to Pass on a Legacy of a Healthy Money Mindset

When it comes down to it, it's clear that the desire to raise children who are wise with money is a noble and common goal among many parents.

Nevertheless, this outcome requires introspection to ensure that we don't pass onto our children our own belief systems that limit their financial abilities.

Indeed, the journey from recognizing and understanding your own limiting money beliefs to breaking these cycles and cultivating a growth mindset is no small feat.

It requires reflection, dedication, and a willingness to embrace change, not just for yourself but for the sake of your children and the generations that follow.

Remember, educating your children about money, involving them in the wealth-building process, and modeling positive financial behaviors are not just strategies, they are gifts you're giving that pay dividends for generations to come.

Indeed, these gifts equip your children with the knowledge, skills, and mindset necessary to make informed financial decisions, manage wealth wisely, and, importantly, become the masters of their own financial independence journey.

Having the Talk: Kids and Money

Opening up and starting conversations about how to handle money and finances with your kids may seem overwhelming, but it doesn’t have to be. As a parent, it is your role to serve as a positive influence in their lives to get them on the right financial track. Here are five things to consider as you embark on helping your children understand the importance of being responsible with their finances.

Start Simply, When They Are Young

Start discussing money with even the littlest ones by including by including them in everyday activities, such as grocery shopping or budgeting. This allows money to become a tangible concept and not some abstract thing that they cannot see. You can also ask them questions such as "We have 5 dollars to buy a treat, would you pick ice cream or cookies?". These types of conversations help children to understand that their are trade-offs to any decision, and that money is not infinite.

Be Truthful

Being honest with your kids is a great first step to opening the door to discussing finances. You can share the family budget for items like groceries or entertainment, and explain remind them of this limit when they ask for items that don't fit within it.

Additionally, If there are things in your financial past, such as going into debt, that you are not proud of, share that with your kids. Honest moments with your kids are very valuable and will help build trust. Keep in mind that the more open and honest you are with your kids, the more open they will be with you, so being truthful about your own finances is a great place to start.

Talk About Values

Encourage your kids to consider what is important to them for their future. Start by asking questions such as "Do you want to own a house or rent when you grow up? or "What splurges would you like to be able to make when you grow up (travel, cars, etc)?".

Helping kids to visualize what they want for the future is a crucial component to talking to kids about money and financial goals. Talking about what they value and hope to have in their future allows them to take a long-term view, which is critical to the concepts of saving, budgeting, and paying down debts.

Establish Family Goals

As a family, talk about your budgeting methods and set specific goals together. For instance, perhaps you set a weekly grocery limit of $150. Take your children to the store with you when you shop and have them help look for sales or clip coupons to keep your cart under budget. Involving your children however you can with the family finances is a great hands-on way to educate them and give them a chance to see real-life examples of how their financial habits will impact them in the future.

Lead By Example

There may be certain financial topics that you are not as knowledgeable about, and that’s okay! Take the opportunity to learn with your kids. Showing your kids that you are interested in growing your understanding of financial topics will heighten their interest in it as well.

Talking to your kids about money may seem like a daunting conversation to have if you don’t know how to approach it properly. However, broaching the subject sooner rather than later will reap many benefits for you and your kids. Ultimately, you want your kids to have the knowledge and skills they need to handle their own finances responsibly as they grow up. As a parent, it’s your job to instill this knowledge in them and to open the door to an often taboo subject so that you can help them get off on the right foot with their finances. Financial habits are formed young, so it’s critical that you start early and start the conversation today. Make your kids feel comfortable to talk about finances with you by using these tips.

The Family that Plans Together Stays Together

Some say that the family that plays together stays together.

And the simple reason this saying holds true is because unstructured time well-spent together creates stronger social and emotional ties within the family unit.

You're literally bonding together.

Now, when it comes to talking about money, some families find the opposite to be true.

That's because discussions around money often repel members.

And so, the more you try to talk about money, especially how it's supposed to be used, the greater the tension that are likely to arise.

But here's the rub: most individuals know that achieving life and financial goals often requires planning for the future.

This work involves starting with the end in mind, identifying the resources you have today, and then creating a strategy for bridging the gap between where you're at today, and where you want to be in the future.

It's simple, right?

Well, sure, this approach to planning is simple, but it's not easy.

This is especially true when you're trying to get your family’s spending and savings habits on the same page.

That's because it's one thing to plan for a singular vision for your life or your life with your partner. And it's another to agree on a plan that your kids or other family members can buy into.

So then, what can you do to create a financial framework for your wealth that involves your family and helps you achieve your broader legacy goals while improving your family’s togetherness?

Well, you can start by creating a unified family wealth strategy.

This approach involves creating a shared family vision for your wealth, identifying easy-to-achieve goals that your family can rally around, and developing principles to foster effective communication to ensure everyone's voice is heard.

Establishing a Shared Values System

Alright, now, when it comes to creating a unified family wealth strategy, especially if you’re a first-generation wealth builder, you need more than just sharing what you know when it comes to talking to your family about money.

You need a common money language.

In other words, for your family to get on the same page when it comes to money, you need a singular reference point to ensure that you're all singing from the same hymnal.

And so, that's where establishing a shared values system comes into play.

Indeed, this approach allows your family's money decisions to be filtered through the same lens and ensures that every financial decision reflects your family's core principles.

Defining Family Values

So then, where do you start?

Well, the process begins with first defining your family's values.

Now, this is a topic that we've written about in the past, so be sure to check out our recent resources.

Either way, to facilitate this first step and actually identify your family values, you can utilize exercises and workshops designed to help your family articulate and align its values.

Now, these approaches can be as simple as discussing what values each family member believes are collectively important, to something more structured like a workshop with a professional facilitator.

Either way, the key here is to ensure that every family member's voice is heard and that the values chosen truly reflects the collective goals of the family.

And if you're still not sure where to start, James Clear in his book, "Atomic Habits" has some great exercises to choose from.

You can also visit one of my favorite tools, the life values inventory online, available at lifevaluesinventory.org to get started.

Either way, by clearly defining and integrating your family's values into your financial planning approach, what you’re doing is ensuring that the way you and your family talk about money isn’t just about growing assets but about building a legacy that reflects what's truly important to you collectively.

Doing so not only aligns your financial decisions with your ethical and moral beliefs, it also strengthens your family's bonds by uniting everyone behind a common purpose.

Crafting a Family Financial Plan

Alright, now after establishing a shared values system with y our family, the next crucial step in creating a unified family wealth strategy, and finding harmony when it comes to talking to your family about money is crafting a financial plan that aligns with your family's values.

Now, earlier you heard that the family that plays together, stays together.

Well, when it comes to money, the truth is that the family that plans together, stays together.

You see, it’s one thing to create a vision for where you should go.

It’s another to execute on that vision, and move your family, collectively, toward that purpose.

And that’s where a family financial plan comes into play.

And why’s that?

That's because a financial plan serves as a roadmap to guide your family towards achieving its financial goals, all while staying true to its core values and principles.

Setting Collective Goals

So then, where do you begin?

Well, you can start by setting clear, collective financial goals for the next year, five years, twenty years, and 100 years.

Get your family to think big!

This process involves a collaborative discussion where each family member shares their personal goals, and together, you identify common objectives that align with your collective values.

Whether it's saving for your kids' education expenses, planning for family vacations, imagining what your retirement will look like for your family, or setting aside funds to support the learning goals of generations down the road, these goals should reflect your family's shared values.

Setting Tangible Financial Milestones

Now, once you've set your shared values and goals, it's time to bring them to life with some real, hard timelines you can get behind.

You can think of these as your family's financial milestones.

Now, the beauty of setting these firm, hard dates is that they give you something tangible to work towards, and it motivates everyone in the family to stay on track.

So, how do we get there?

Well, imagine you've decided to fully fund your great grandchildren’s education so that they don’t have to lean on student loans.

It's a big goal, right?

Well sure, it might be, but we can simplify it by breaking down the goal, starting with a date.

For example, let’s say that you want to have a million dollars saved in an educational trust by 2070.

This means that your family will need to figure out how much to set aside each month starting today, and stay committed to that savings goal as a family until your milestone is reached.

Indeed, having a big, tangible savings goal like setting money aside for future generations and benefits the entire family can help get everyone get energized and on the same page.