The Tax Items Congress Wants, But Probably Won’t Pass Yet

Most months, there isn’t much new tax law to report. This is one of those months.

No major tax rules have changed. But there’s still a useful update worth sharing, because what Congress is debating now can tell us something about where tax policy may be headed, even when nothing has changed yet.

The Short Version

Republicans are working on another budget reconciliation bill before the midterm elections.

Reconciliation is the procedural workaround that lets the Senate pass certain budget-related legislation with a simple majority instead of the usual 60-vote threshold. It’s how last year’s major tax bill became law on a strictly partisan vote, and it’s the most likely vehicle for any significant tax legislation between now and then.

GOP taxwriters would like to see tax provisions included in this next bill. Their wish list includes priorities that didn’t make it into last year’s bill, a framework for taxing digital assets, changes to health savings accounts, easings to the corporate alternative minimum tax, and reforms to refundable credits.

That’s the wish list. The problem is that the vehicle for carrying it may not be available this time.

The next reconciliation package now looks likely to be narrow. The current direction from the White House and congressional leadership is to limit the bill to funding for two Department of Homeland Security agencies, Immigration and Customs Enforcement and Customs and Border Protection.

The administration wants the bill enacted by June 1, which puts pressure on lawmakers to move quickly and reduces the appetite for expanding the package.

In other words, taxes probably aren’t in the next bill. But the wish list itself is still informative.

What We’re Watching, and Why

When tax provisions are debated and then deferred, it’s tempting to file the news away as not relevant yet.

We treat it differently.

The items being discussed today are often the items that resurface when the next legislative opportunity appears. The planning value of knowing what may be coming is highest before the rules are final, not after.

A few specific items are on our watch list.

Digital Assets

A clear federal framework for taxing cryptocurrency and other digital assets has been on the wish list for years and keeps getting pushed.

When it does pass, it could create new reporting obligations and may affect how gains, losses, and transactions are documented. Clients with meaningful digital asset positions should expect this issue to land eventually.

Health Savings Accounts

Proposed changes generally aim to expand who can contribute and how the funds can be used.

HSAs are already one of the most tax-efficient accounts in the code. Any expansion could create new planning opportunities for clients who qualify, especially those trying to coordinate healthcare costs, retirement planning, and long-term tax efficiency.

Refundable Credits

Reform here usually means tightening eligibility and increasing verification.

That connects directly to the broader IRS enforcement story we wrote about separately. The trend is toward more scrutiny of these credits, whether through legislation, enforcement, or both.

Corporate Alternative Minimum Tax

Most individual clients aren’t directly affected by the corporate alternative minimum tax.

But executives, business owners, and investors with exposure to companies affected by the rule may still care about how changes could flow through to valuation, cash flow, compensation, or transaction planning.

The Big Takeaway

None of these tax changes appear imminent.

But they’re still worth watching, because tax legislation tends to move in long pauses punctuated by short bursts of activity. The pauses are when planning happens. The bursts are when the rules change.

We watch the legislative calendar so that when something does move, we already know what it means for the clients it affects. More importantly, we’ve already had the conversations that need to happen.

If any of the items above touch your situation and you’d like to talk through the implications, we’re glad to do that.

A Smaller IRS, a Different Kind of Enforcement

The IRS is meaningfully different than it was eighteen months ago. The agency has lost more than a fifth of its workforce since the start of 2025, its budget has been cut, and most of the funding boost it received from the 2022 Inflation Reduction Act has been clawed back.

What this adds up to isn't just a smaller IRS. It's a different IRS.

The agency is reshaping what it enforces, how it enforces it, and which taxpayers are most likely to hear from it. That story is worth understanding, both because it's genuinely consequential and because the practical implications for taxpayers aren't what you might first assume.

The numbers behind the change

Congress set the IRS's fiscal year 2026 budget at $11.2 billion, about 9% below FY25. House appropriators are pushing for a further cut to $10.2 billion in FY27. The agency has lost more than 20% of its workforce since January 2025 through deferred resignations and layoffs, with additional departures expected this year.

The Trump administration's FY27 budget request includes an 18% reduction in enforcement activity and projects an enforcement workforce below 25,000. Within that already shrunken enforcement arm, some of the largest losses have hit the examination and collection groups, and many of those who left were experienced agents and managers carrying years of institutional knowledge that won't be easy to replace.

In plain English, the IRS has fewer people, fewer experienced reviewers, and less capacity to conduct traditional enforcement the way it once did.

Fewer audits, especially at the top

The audit rate for individuals has been well below 1% for several years, and we expect it to keep falling, at least over the next few years.

Audits of individuals with $10 million or more of income, which numbered 6,786 in FY25, dropped to 2,264 in FY26. Partnership audits fell from 3,174 to 2,932 over the same period. The agency forecasts further declines in both categories in FY27.

For clients in higher income brackets, who historically faced disproportionate audit attention, the near-term picture is meaningfully different than it was even two years ago. The headline probability of a traditional audit appears lower.

But that doesn't mean enforcement risk has disappeared. It means the nature of that risk is changing.

The odds of a traditional audit may be lower, but the audits that remain are less likely to be random noise. They're more likely to be tied to something specific in the return, such as a mismatch, an anomaly, a complex transaction, or an item that doesn't reconcile cleanly with third-party data.

What's replacing the lost capacity

That's the headline. The more interesting story is what's replacing the lost capacity.

IRS leadership has said publicly that fewer audits will be paired with more targeted ones, and the mechanism for that targeting is increasingly data analytics and artificial intelligence. The agency has been investing in software that mines taxpayer data to surface anomalies, flag suspicious activity, and identify cases for review.

Even with reduced funding, the direction of travel is clear: the IRS is leaning harder on technology because it no longer has the same human capacity. The intent is to compensate for the loss of human reviewers by being more precise about who gets reviewed in the first place.

We'll see how well it works in practice. But the direction is clear: less of the broad coverage that audit rates traditionally measured, and more of the targeted attention those same rates fail to capture.

Where enforcement is concentrating

Two areas in particular look like they'll absorb a disproportionate share of the enforcement capacity that remains.

The first is refundable credits, where the IRS estimated improper payments of $21.4 billion in FY24 alone. The earned income credit, the American Opportunity credit, and the premium tax credit are all on this list, and all are well-suited to algorithmic review.

For many higher-income households, refundable credit reviews may not be the primary concern. But they illustrate the broader enforcement shift. The IRS is favoring areas where software can flag returns quickly and where discrepancies can be identified without a large team of experienced agents.

For you, the more relevant version of that same shift is income matching.

The IRS's automated underreporting program compares the W-2s, 1099s, and other third-party tax forms it receives against what taxpayers report on their returns. Significant mismatches generate a CP2000 notice, which is computer-driven and doesn't require an experienced agent to produce.

This matters for households with brokerage accounts, equity compensation, retirement income, business income, K-1s, real estate activity, charitable giving, or multiple sources of income. The more moving pieces there are, the more important it becomes that the return tells a clean and consistent story.

Traditional enforcement may shrink, but automated enforcement can still expand because it requires fewer experienced agents to initiate. As enforcement leans further into automation, expect more of this kind of correspondence, not less.

What it means for you

For you, this all means a few things.

First, the headline audit risk for high-income clients is genuinely lower than it was. That's a real shift, and it's worth naming rather than dismissing. But it isn't a license for casual recordkeeping.

The audits that do occur will be more precisely chosen. That means the cases that get pulled are more likely to be cases where something genuinely doesn't reconcile. Clean books, good documentation, and coordinated reporting matter at least as much in this environment as they did before, possibly more.

Second, the surface area for automated correspondence is growing.

CP2000 notices, refundable credit reviews, and other algorithm-driven inquiries don't feel like audits and may not show up in the headline audit statistics. They may not require the same scope of work as a full audit, but they still require careful review, documentation, and a timely response.

If you receive one, the worst thing to do is ignore it. The deadlines on these notices are real, and the IRS's response to silence is rarely favorable.

Third, the shape of the agency is going to keep changing.

Budget proposals are still being debated, workforce attrition is ongoing, and the technology is still maturing. What looks like a settled picture today may shift again over the next year or two.

That's part of why we follow this closely. Tax planning is most useful when it accounts for where the enforcement environment is going, not just where it is.

Why coordination matters more now

This is also why tax planning and wealth planning shouldn't live in separate silos.

The more complex your income, investments, retirement withdrawals, equity compensation, business interests, or estate planning becomes, the more important it is that the tax return tells the same story as the financial plan.

A smaller IRS may conduct fewer traditional audits. But a more automated IRS may still notice when the pieces don't line up.

That's why tax planning isn't just about finding deductions or reacting before year-end. It's about making sure decisions are coordinated before they show up on a return. Investment decisions, retirement income decisions, Roth conversion decisions, charitable giving decisions, and estate planning decisions can all create tax consequences. The goal is to understand those consequences ahead of time rather than explain them after the fact.

The Big Takeaway

None of this changes the fundamentals of what we do for clients.

We aim to file accurately, document thoroughly, and structure things so that when the IRS does ask a question, the answer is already on the shelf.

That discipline mattered when audit rates were higher, and it matters now, even as the agency asking the questions becomes smaller, more automated, and more selective.

The goal hasn't changed: clarity in your filings, confidence in your position, and the peace of mind that comes from knowing the work was done right the first time.

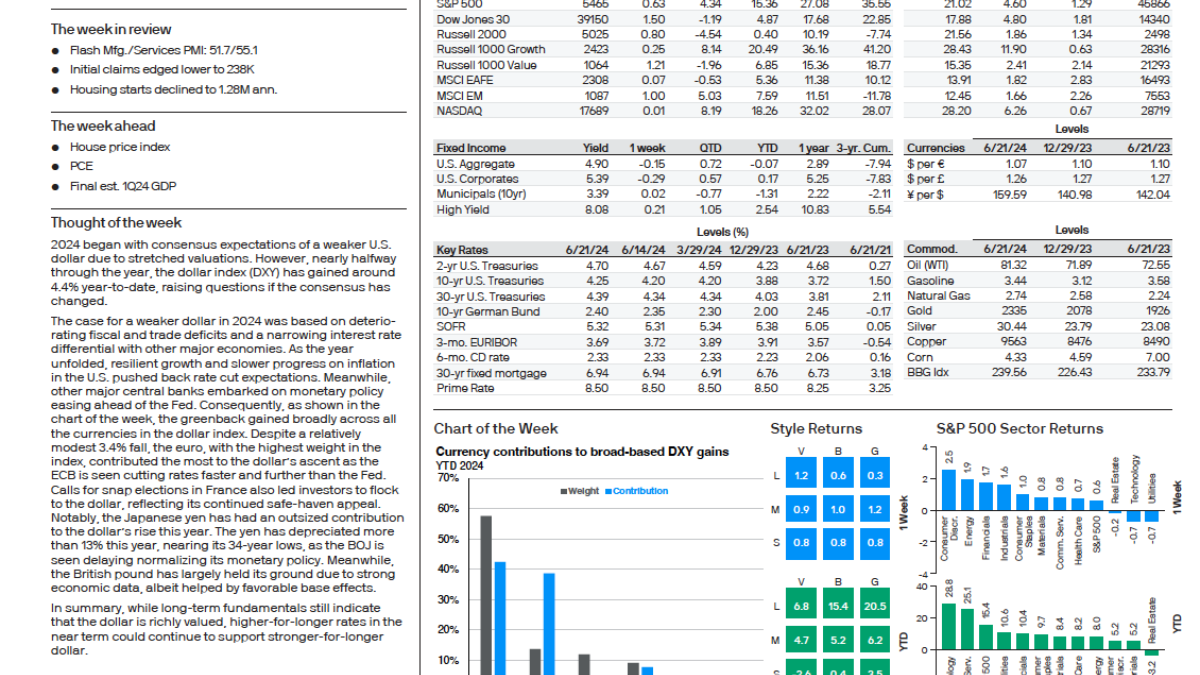

Analysts Corner: 06/25/2024 – Mid Year Economic Outlooks

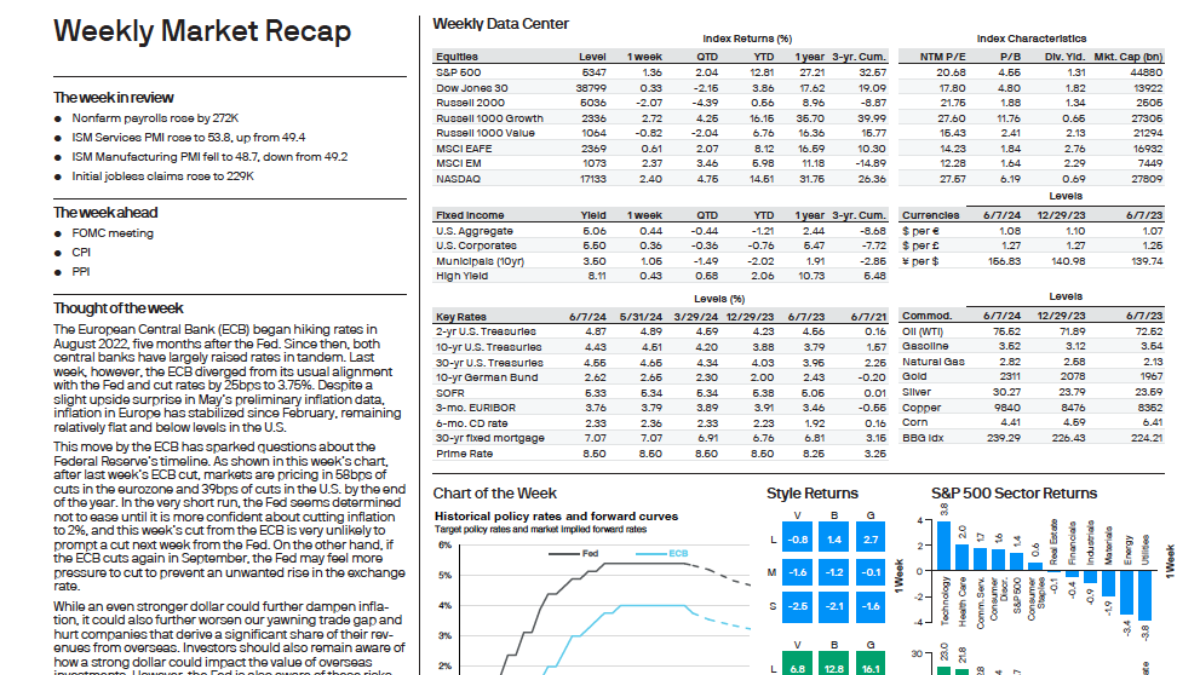

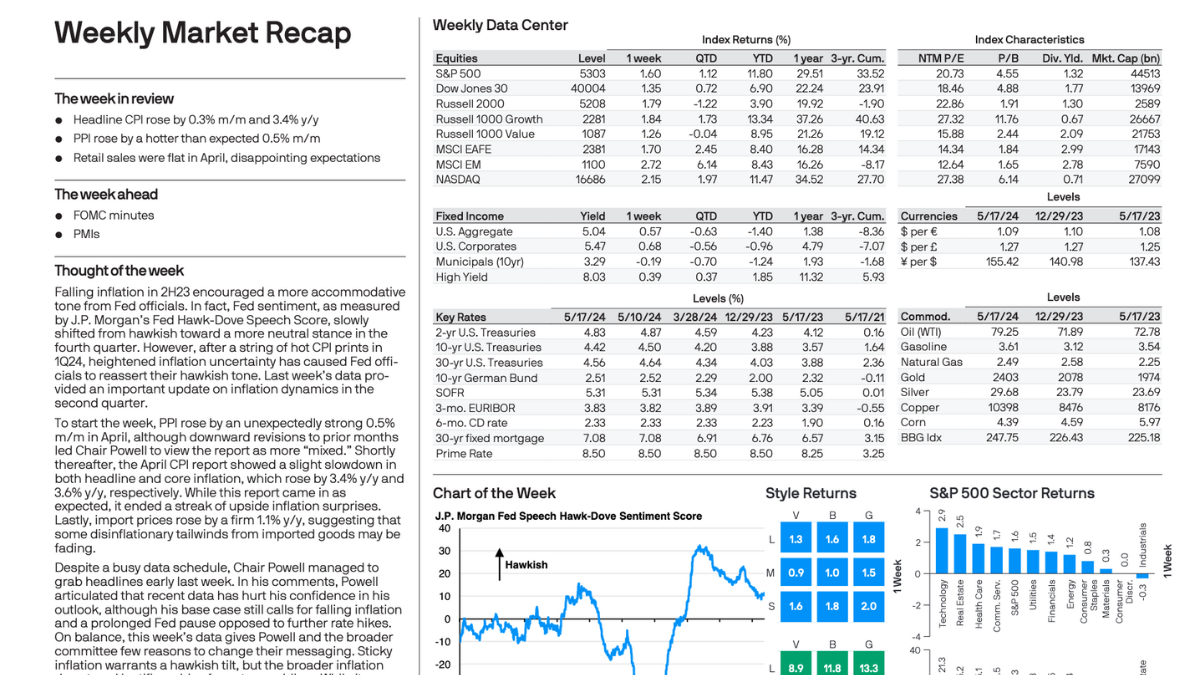

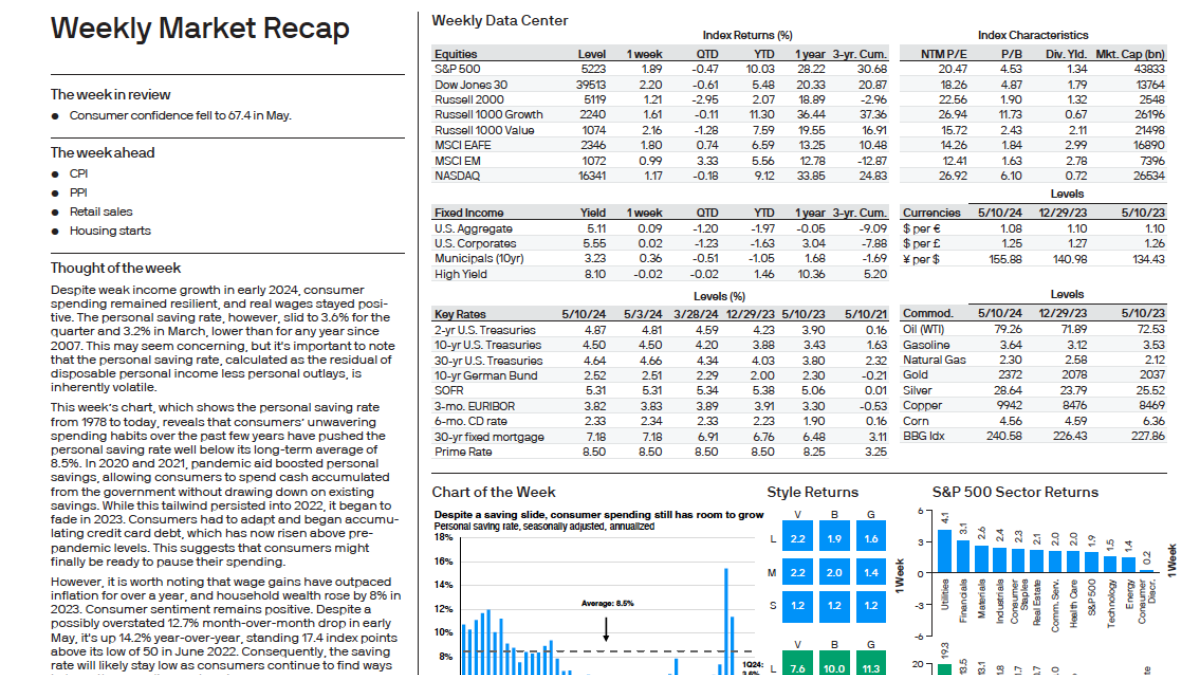

Weekly Market Recap

A look back at the financial markets over the past week and a look ahead at key economic developments this week.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/06/weekly_market_recap_20240624.pdf

Source: JP Morgan Asset Management

Weekly Macro Recap

A look back at key macroeconomic and geopolitical developments that help us contextualize the current investing landscape.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/06/weekly_macro_recap_20240624.pdf

Source: Luke Gromen, FFTT

Opportunities Amidst Divergence

A significant risk that markets are overly positive and have not fully priced in potential problems. Given the positive macro backdrop, an overweight to risky assets is favored but keep risks tightly controlled, as very tight valuations limit the upside for risky assets.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/06/Opportunities-Amidst-Divergence.pdf

Source: Invesco

Renewed Growth, New Challenges

Despite improvements, many investors are likely to be distracted by increasing noise as November’s US election draws near. This election is significant, but we believe it is unlikely to change the direction of the world economy and markets. That said, there are many other risks, including potential inflationary shocks and unpredictable geopolitical flareups.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/06/Renewed-Growth-New-Challenges.pdf

Source: Citi

From Stability to Agility: Nine Implications for a New Investment Landscape

The underlying assumptions that have driven many investment strategies over the last 40 years must be reexamined. This paper explores nine implications that can help empower investors with the agility needed to navigate the uncertainties of the new economic environment.

Source: Nuveen

Analysts Corner: 06/18/2024 – More Economic Data Needed

Weekly Market Recap

A look back at the financial markets over the past week and a look ahead at key economic developments this week.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/06/weekly-market-recap-20240617.pdf

Source: JP Morgan Asset Management

Weekly Macro Recap

A look back at key macroeconomic and geopolitical developments that help us contextualize the current investing landscape.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/06/weekly-macro-recap-20240618.pdf

Source: Luke Gromen, FFTT

Goldilocks, for Now

The US economy has recently experienced the benign combination of steady growth and slowing inflation; a sort of renewed ‘Goldilocks’. The volatility in economic data since the pandemic, however, suggests the situation is unlikely to last. We expect growth to slow modestly in the quarters ahead, with core inflation remaining comparatively high.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/06/Goldilocks-For-Now.pdf

Source: BNP Paribas

Fed Policy: One Month of Good Data Is Not Enough

Good news on U.S. inflation in May did not sway the Federal Reserve to signal interest rate cuts could come sooner.

Source: PIMCO

What to Watch in 2024 Elections

Over half the world's population goes to the polls in 2024. Governments and candidates have limited solutions to key financial issues for voters.

Source: Blackrock

Analysts Corner: 06/11/2024 – Risk Asset Rally is Broadening Globally

Weekly Market Recap

A look back at the financial markets over the past week and a look ahead at key economic developments this week.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/06/weekly-macro-recap-20240611.pdf

Source: JP Morgan Asset Management

Weekly Macro Recap

A look back at key macroeconomic and geopolitical developments that help us contextualize the current investing landscape.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/06/weekly-macro-recap-20240611.pdf

Source: Luke Gromen, FFTT

Stock Market Sector Update

The hunt for positive growth momentum and attractive valuations is starting to shift investors’ focus away from the U.S. and towards more regionally diversified exposure, where the scope for catch up appears greater.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/06/European-Elections-Whats-At-Stake.pdf

Source: JPAM

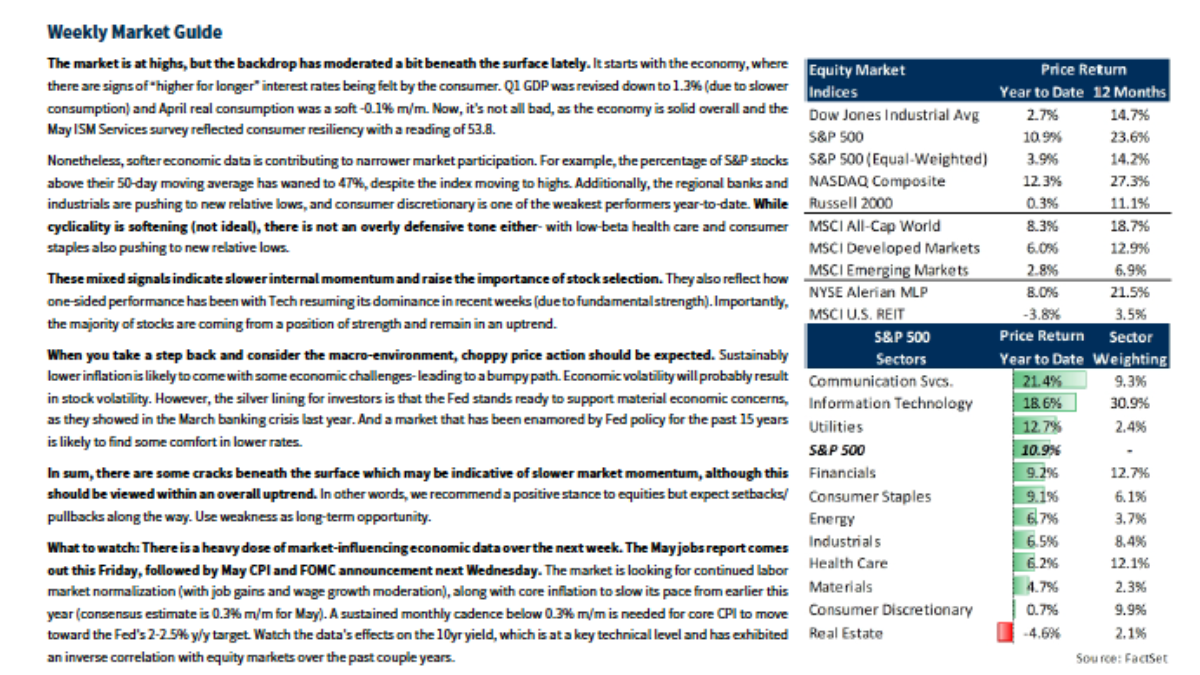

Equity Market Guide

A solid Q1 earnings season supported the uptrend in equities; and importantly, forward estimates have held steady at healthy growth rates (i.e. double-digit S&P 500 earnings growth expectations for 2024 and 2025).

https://franklinmadisonadvisors.com/wp-content/uploads/2024/06/equity-market-guide.pdf

Source: Raymond James

European Elections: What’s At Stake

Europe might be losing international competitiveness, but in the coming days it will return to the global centre stage with three major events: the ECB’s rate cut decisions, European elections and, of course, the European Football Championship.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/06/European-Elections-Whats-At-Stake.pdf

Source: ING

Analysts Corner: 06/04/2024 – Slower Growth and Rate Cut Optimism Fuel Market Rally

Weekly Market Recap

A look back at the financial markets over the past week and a look ahead at key economic developments this week.

Source: JP Morgan Asset Management

Weekly Macro Recap

A look back at key macroeconomic and geopolitical developments that help us contextualize the current investing landscape.

Source: Luke Gromen, FFTT

Not Your Typical Rate Cutting Cycle

The ECB is set to start easing before the Fed, but a wider policy gap between them will be temporary, even if a Fed hike is not impossible.

Source: Blackrock

Market Drivers Insights Report

Risk appetite recovers on easing financial conditions but drives US 12m forward PE to more than one standard deviation above the 10-year average.

Source: Wilshire Indexes

Currency Volatility: Will US Dollar Strength Continue?

In light of improving global growth and repricing of Fed expectations, will the U.S. dollar sustain its strength in 2024? And what’s the outlook for other major currencies?

Source: JPM

Analyst's Corner: 05/28/2024 – Startups Paying Out Less in Equity Comp

Weekly Market Recap

A look back at the financial markets over the past week and a look ahead at key economic developments this week.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/05/weekly-market-update-20240527.pdf

Source: JP Morgan Asset Management

Weekly Macro Recap

A look back at key macroeconomic and geopolitical developments that help us contextualize the current investing landscape.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/05/weekly-macro-recap-20240528.pdf

Source: Luke Gromen, FFTT

Startups are hiring fewer workers and paying out less in equity comp

The Equity Podcast is about the business of startups, where they unpack the numbers and nuance behind the headlines.

https://techcrunch.com/podcast/startups-are-hiring-fewer-workers-and-paying-out-less-in-equity-comp/

Source: Tech Crunch

Challenges remain but IPO outlook brightens

Global IPO markets have had a comparatively positive start to 2024 after a challenging year. Investors and IPO candidates hope that stable interest rates and pent-up demand will support an increasing flow of IPO activity in the months ahead.

https://www.whitecase.com/insight-our-thinking/global-ipos-2024-outlook-brightens

Source:White & Castle

Negotiating Stock Options And Restricted Stock Units: 7 Points To Consider Before You Try

Depending on your professional clout and the company’s need, you may be able to negotiate your equity compensation when you are hired or get promoted.

Source: Forbes

Analysts Corner: 05/21/2024 – Stay Diversified As Markets Diverge

Weekly Market Recap

A look back at the financial markets over the past week and a look ahead at key economic developments this week.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/05/weekly-market-recap-20240521.pdf

Source: JP Morgan Asset Management

Weekly Macro Recap

A look back at key macroeconomic and geopolitical developments that help us contextualize the current investing landscape.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/05/weekly-macro-recap-20240521.pdf

Source: Luke Gromen, FFTT

Global Financial Stability Report 2024

Near-term risks to global financial stability have receded as disinflation is entering its last mile but medium-term vulnerabilities are mounting.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/05/Global-Financial-Stability-Report.pdf

Source: IMF

When Markets Diverge, Opportunities Emerge

Shifting dynamics among global economies and markets present a range of opportunities for multi-asset portfolios.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/05/When-Markets-Diverge-Opportunities-Emerge.pdf

Source: PIMCO

3 Assets That Might Not Diversify as Well as You Think

Real estate, high-yield bonds, and cryptocurrency don’t always live up to their reputation as portfolio diversifiers.

https://franklinmadisonadvisors.com/wp-content/uploads/2024/05/3-Assets-That-Might-Not-Diversify-as-Well-as-You-Think-Morningstar.pdf

Source: Morningstar

Analysts Corner: 05/13/2024 – Can the Economy Avoid Stagflation?

Weekly Market Recap

A look back at the financial markets over the past week and a look ahead at key economic developments this week.

Source: JP Morgan Asset Management

Weekly Macro Recap

A look back at key macroeconomic and geopolitical developments that help us contextualize the current investing landscape.

Source: Luke Gromen, FFTT

Watching for Mean Reversion, Technology Diffusion, and the Next Inflection Point

Is there still a case for small caps? Head of Multi-Asset Strategy Adam Berger and Peter Carpi, a small- and micro-cap manager, consider the evidence and the asset allocation implications

Source: Wellington

Monthly Market Viewpoint – Delayed Landing

One might have thought that four years after the start of the pandemic, investors might have some confidence in the outlook for economic growth and inflation. Unfortunately, that is not the case.

Source: BNP Paribas

Do We Now Need to Worry About Stagflation?

Jerome Powell, Chair of the U.S. Federal Reserve, offered a memorable antidote to the gloomy sentiment at his last press conference on May 1: “I don’t see the ‘stag’ or the ‘flation’.”

Source: Beuberger Berman

Weekly Market Update: May's Record Rally Runs on a Short Leash

May was a month of records, though the rally's foundation was narrower than the headlines suggested. The S&P 500, Nasdaq, Dow, and Russell 2000 all set new all-time highs, powered almost entirely by technology and semiconductor stocks. The gains came despite a genuine rate scare: back-to-back hot inflation readings put a Federal Reserve rate hike back on the table and pushed long-term Treasury yields sharply higher. The pressure faded when oil prices fell more than 13%, taking inflation fears with them and clearing the way for the AI trade to reassert itself.

Beneath the surface, the picture was more complicated. Technology gained nearly 20% on the month; strip it out, and the remaining sectors were slightly negative in aggregate. Only three of the eleven sectors finished higher. Bond markets reflected the same tension, with shorter-term yields rising while longer maturities ended roughly flat. In credit, spreads generally tightened, though the riskiest tier of high-yield bonds diverged and widened. Oil fell 13.2% as the geopolitical risk premium unwound, dragging the broader commodity complex down more than 5%. Corporate earnings offered a bright spot: first-quarter blended growth came in at 28.6% against a 13.1% estimate, with profit margins reaching a record 14.8%. But like the rally itself, the earnings strength was concentrated in a handful of large semiconductor and mega-cap names.

The month also brought a change at the Federal Reserve. Jerome Powell's term expired in mid-May, and Kevin Warsh was confirmed as the new chair. Warsh inherits a complicated environment: the base case points to a rate hike by December if the Strait of Hormuz disruption keeps oil prices elevated, the administration has expressed a preference for lower rates, and inflation remains above the 2% target. Markets will need to adjust to a new communication style just as the Fed's independence faces heightened scrutiny.

The economic backdrop offers a similarly mixed read. The labor market has firmed after softening last fall, and manufacturing has returned to expansion territory. The consumer, however, is moving the other way, with income growth slowing and confidence near record lows by some measures. What has kept households spending is balance-sheet strength from elevated home values and a rising stock market. That support, as long as it holds, keeps the expansion intact. Whether it holds is the central question heading into the summer.

Key Takeaways

Records Built on Narrow Leadership

May's market gains were real, but the breadth underlying them was not. Technology accounted for nearly all of the S&P 500's advance, and most sectors finished negative. The Dow, Russell 2000, and equal-weight S&P each returned between 2% and 3%, a fraction of the Nasdaq's performance. Momentum and high-beta factors led; defensive and dividend-oriented stocks lagged.

Why it matters: An index sitting at all-time highs on such concentrated leadership is more fragile than the scoreboard implies. Any shift in sentiment around AI and semiconductors would leave most of the market without a catalyst to offset the pressure.

Oil Was the Swing Factor

WTI crude fell 13.2% in May as the geopolitical risk premium tied to the Strait of Hormuz unwound. That decline did the critical work of easing inflation pressure mid-month, pulling Treasury yields lower and giving equities room to recover. The broader commodity complex fell more than 5% in sympathy.

Why it matters: The rally's trajectory is directly tied to oil. The Strait of Hormuz remains functionally closed, and the physical supply disruption is unresolved. If oil prices move higher again, the inflation and rate-hike risk that rattled markets mid-month returns with it.

A New Fed Chair Adds Policy Uncertainty

Kevin Warsh replaced Jerome Powell as Federal Reserve chair in mid-May, inheriting an environment with inflation above target, a December rate hike increasingly priced in, and an administration publicly favoring lower rates. Futures markets, which began the year expecting cuts, now assign meaningful odds to a hike by year-end.

Why it matters: A leadership transition at the Fed introduces communication uncertainty at a moment when policy expectations are already shifting. Markets priced in cuts and got a possible hike. How Warsh navigates that gap, and the political pressure that surrounds it, will shape rate expectations for the remainder of the year.

Earnings Growth Is Strong but Concentrated

First-quarter blended earnings growth came in at 28.6%, well above the 13.1% estimate entering the quarter, with profit margins reaching a record 14.8%. Analysts have continued to raise forecasts, with upgrades outpacing downgrades by roughly two and a half to one.

Why it matters: Strip out the largest semiconductor names and technology's growth rate is cut roughly in half. The same concentration that defines the price rally defines the earnings beneath it. As estimates keep rising, the bar future quarters must clear keeps rising with them.

The Consumer Is the Key Risk to Watch

The labor market has firmed and manufacturing has returned to expansion, but consumer confidence is near a record low by at least one closely watched measure, and income growth continues to slow. Households have stayed spending largely because elevated home values and a rising stock market support balance-sheet health.

Why it matters: Several years of consumer-led growth have kept the expansion intact. If the asset-price support that underlies household spending begins to weaken, reduced consumer outlays could translate into slower economic growth at the same moment the Fed may be tightening rather than easing.