How to Avoid Financial Stress During the Holidays

Depending on who you ask, the holidays are either a season full of celebration and connecting with family and friends, or they’re a seasonal burden that adds to the never-ending stresses of life. A recent survey found that 88% of people believe the holidays are the most stressful time of the year and 56% say that financial strain brought on by the holidays is their largest source of anxiety.1

We’ve identified a few ways to manage stress, keep your budget in line, and experience the joy of giving in a tax-advantageous way.

Sticking to a Budget

Everyone understands the past year has been tough, and while the economy is recovering, we’re not out of the woods yet. American balance sheets are in better shape, but it’s easy for the end-of-year festivities to blow a holiday-shaped hole in any budget. American Express reports that 86% of millennials spent more than they had planned to during the holidays last year.2 With ‘buy now, pay later’ services on the rise, it may be even more challenging to keep spending to a limit.

One way to keep holiday spending manageable is by setting a budget. It’s never been easier to compare prices online to figure out where the best deals are, so before hitting the mall or scrolling through Amazon, have an idea of what you’re able to spend. Take some time to list out your gift buying. Planning your purchases ahead of time will help you avoid impulse buying and overspending.

Another strategy is to use a separate card or account for holiday spending so you can easily see how much you’ve spent. It may even help to download a budgeting app, such as Mint or You Need a Budget, for the holidays so you can set limits on spending and get notified when you’re close to hitting them.

But remember, memories and experiences are worth more than the number at the bottom of a receipt. Don’t overextend yourself and add more stress to your plate when gifting this holiday season.

Practicing Gratitude & Prioritizing Mental Health

Practicing gratitude is a good habit no matter what season it is, but it feels more significant during the holidays. Oftentimes, the focus around this time of year is on gifts, but the holidays are more than spending money and exchanging presents. They can be a time of reflection and a chance to spend time with family. Many studies have shown a direct correlation between practicing gratitude and increased levels of happiness and reduced stress.

Overall, we tend to take little things for granted. It’s easy to get caught up in the day-to-day stresses of life, but don’t forget to take some time to be thankful and grateful for the positive aspects of life, the blessings you have, and the time you may get to spend with loved ones.

The past year has taken a toll and mental health conversations are at the forefront. In addition, many Americans struggle with seasonal depression as the holidays can trigger a variety of different feelings. One way to help reduce negative feelings is by being proactive and recognizing triggers and symptoms. This can allow you to plan ahead to avoid certain situations or at the very least, be aware that actions need to be taken to help cope.

During the holidays we may feel obligated to do certain things or act certain ways around family or friends and it’s not always healthy. Setting boundaries is important in any relationship. Without them, you may end up in uncomfortable or undesirable situations, leading to more stress and frustration. By setting boundaries, even with those you love, you’re laying out guidelines for yourself to determine what works for you and what doesn’t. This can be challenging to do but overall, but it can lead to healthier relationships.

The Season of Giving

Giving back is a great way to ground yourself and find purpose during the holiday season. It’s a time of giving and right now, the world needs more of it. Giving can come in many forms and also doesn’t have to be monetary. Spending time in your community and volunteering at a food kitchen or charity both have an impact and volunteers often report having higher personal satisfaction and gratitude than those who don’t. Additionally, you may also be able to deduct volunteer expenses if you purchased any supplies or had significant travel costs.

Don’t forget about the local businesses when you’re shopping. Small businesses keep money in the local economy, may not have the same supply chain issues as the big stores, and may participate in a lot of giving back to the community. They’re often the local sponsors for sports teams and arts clubs, and they often support food banks and sponsor charitable drives.

Tax-Advantaged Giving

Of course, there are direct donations to charities and other organizations as well. This may be easier to do and it can also come with tax benefits. Depending on the type of organization you donate to and how the donation is made, you may be able to deduct the full donation amount.

Setting up a trust is a classic option when it comes to charitable giving, but depending on your circumstances, a donor-advised fund may be simpler and achieve your goals. According to the National Philanthropic Trust, DAF contributions exceeded $38 billion in 2019, an 80% increase since 2015. DAFs allow you to donate highly appreciated stock and assets, receive an immediate tax deduction, but rather than select a charity immediately, the funds can be invested in the DAF, left to grow over time, and distributed at a later date.

Donating appreciated stock is advantageous because it can allow you to donate more than if you sold investments and donated cash. When charities receive appreciated stock, they’re not required to pay capital gains upon liquidation. As long as requirements are met, you receive a tax deduction for the full market value of the assets.

Those over age 70 1/2 can use a qualified charitable distribution strategy that allows donations of up to $100,000 directly to a charity from an IRA instead of taking RMDs. This can help reduce taxes because you avoid taking income, which could mean staying in a lower tax bracket, and potentially lowering the amount of RMDs in future years.

The Takeaway

The holidays bring out a variety of different emotions, and we often focus on others during this time, but don’t forget to take care of yourself. If you typically feel overwhelmed during the holidays, taking appropriate steps can help you spend more of the season enjoying the festivities. With a little planning, the holidays can be a time to unwind and spend much-needed time with loved ones.

1. Anderer, John. Jingle Bell Crock: 88% Of Americans Feel The Holiday Season Is Most Stressful Time Of Year. Study Finds. December 21, 2019.

2. White, Alexandria. 86% of Millennials Overspent on Holiday Gifts Last Year—Here’s How to Avoid the Same Mistakes. CNBC. August 17, 2021.

Inflation: An Insidious Threat Your Financial Independence Journey

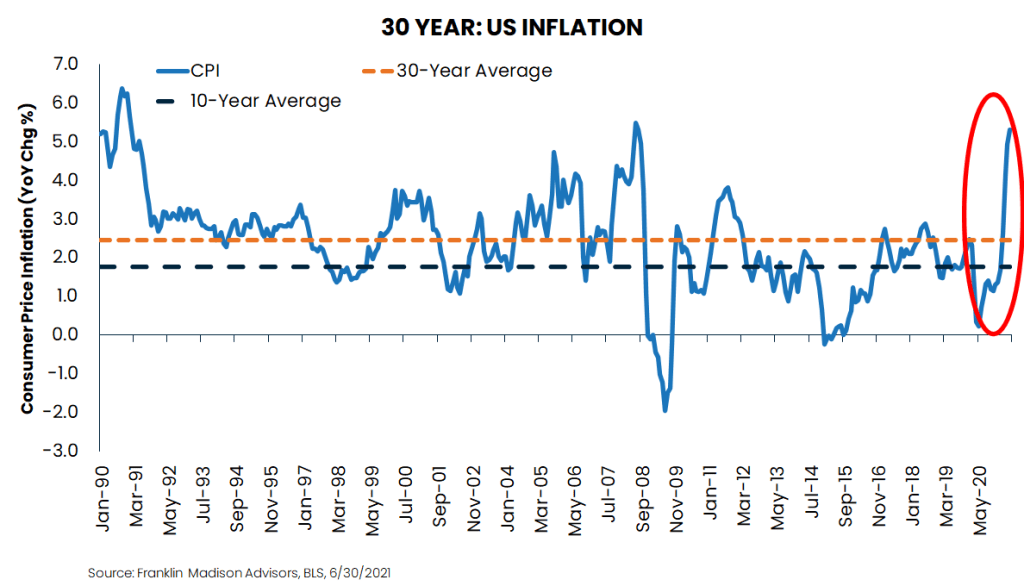

Financial independence plans are coming under threat from inflation's insidious rise. According to a government report, prices paid for everyday household items rose by 4.9% in May compared to a year earlier. Even when stripping out volatile components, like food and energy, prices were up 3.9% over the same period – the fastest in over three decades.

While these statistics might seem arbitrary at face value, it's essential to understand the context. For example, the latest inflation figure comes in stark contrast to its 2.5% average over the past 30 years. Indeed, the reality of rising prices is evident whether you're filling up the gas tank, shopping at the grocery store, getting ready to buy your next house, or decorating the home you just purchased.

Permanent or Transitory?

Today, many economists, market watchers, and to be sure, households look at the recent price spikes and ask, "Is today’s higher inflation a fluke or new reality?"

A Case for Lower Near-Term Inflation

Certainly, there's a case to be made that inflation is likely to ease in the coming months. How so? Well, households globally today are spending faster than expected, and global distributors are struggling to keep up with demand. Last year's global economic shutdown and ongoing COVID restrictions have created gridlock in the global supply chain. These bottlenecks have made it harder to ship certain goods from international producers to US warehouses, crimping supply on store shelves and naturally putting upward pressure on prices.

For example, according to one report, container ships responding to the post-COVID consumer spending surge found it challenging throughout June to unload their goods at the Port of Los Angeles (one of the busiest ports in North America). In fact, some ships were anchored in a holding pattern for five days outside of the port, given logistics backlogs. In normal circumstances, foreign cargo ships typically don't have to wait to enter the port and can unload their cargoes right away.

Why is this story significant? Well, what makes shipping into the Port of LA important is that these freighters carry household goods and manufacturing components that affect all aspects of the US economy. Now, this logistics gridlock story is not unique to the Port of LA as it's happening in ports all around the world. And these delivery slowdowns have led to a global supply chain crunch, giving way to higher near-term prices for a host of goods.

From this perspective, it could be argued that today's high inflation is only transitory. Once global logistics issues are fully resolved, near-term inflationary pressures might ease as the supply of goods finally meet the rising pressure from pent-up global consumer demand.

A Case for Higher Longer-Term Inflation

Now, while there's a case to be made for lower near-term inflation, it's also worth considering the potential factors that might lead to higher prices in the decades ahead. Indeed, the Federal Reserve has flooded the economy with $5 trillion from the start of last year. Combine this excess money printing with trillions in government stimulus, and there's a potential that excess household savings (coupled with a higher propensity to consume) might cause inflation to run hot for longer than what many economists anticipate.

To this point, researchers at Bank of America recently published a report noting that over the next four years, US inflation could average between 2-4%. If we look back through history, this estimate compares to average annual price gains, of around 3% over the past 100 years, 2% in the 2010s, and 1% in 2020. According to this report, analysts believe that a key contributor to faster inflation likely could come from Americans sitting on trillions of dollars in unspent savings. As COVID restrictions ease and the economy rebounds, this savings could make its way back into the economy in the form of higher consumption and wage growth.

Another long-term inflationary point to consider is China's evolving relationship with the rest of the world. Chinese factories have, until recently, been low-cost producers of the world's goods, arguably contributing to low inflation in developed market economies for the past two decades.

Nevertheless, geopolitical tensions remain elevated between Western nations (notably the US) and China. What's more, Beijing is pushing policies that would enable China's economy to become more domestically reliant while expanding its political influence globally. From this perspective, it's very well possible to see higher-priced goods here at home should Beijing's policy changes reduce China's export of deflation to the rest of the world.

Why Does Inflation Matter?

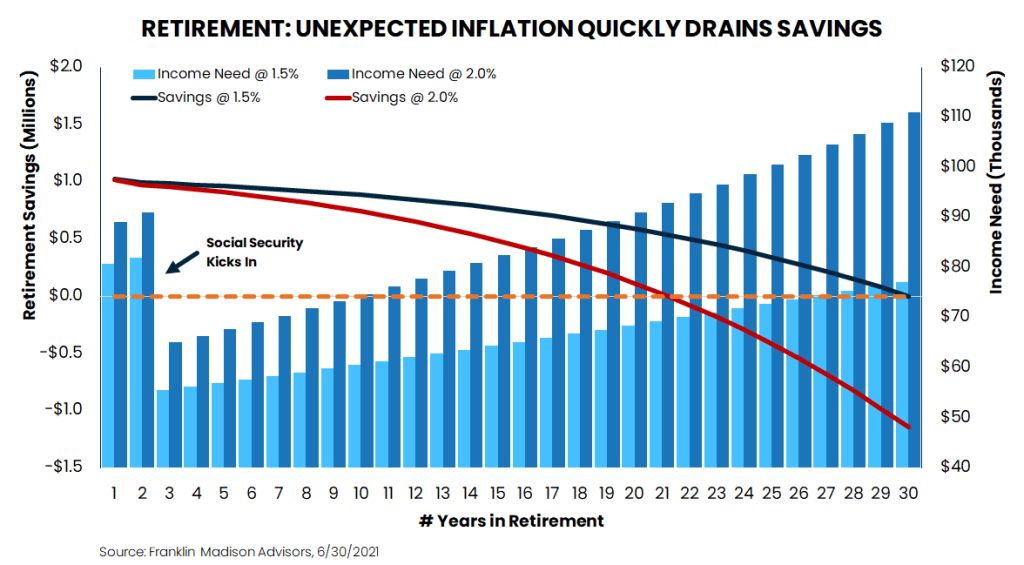

So, what's the big deal if prices rise faster than expected? In other words, what role might higher inflation play in your ability to navigate your financial independence journey? Well, at face value, persistently elevated inflation could result in your spending down retirement savings at a faster than expected rate. How so? Well, a simple example here might help.

Let's suppose that you're planning to retire in 20 years with a lifestyle need of $60,000 per year in today’s dollars. Assuming a modest Social Security benefit, you'll likely need to have saved about $1 million to cover inflation-adjusted living expenses over the next 30 years. This figure is based on a widely held industry assumption that inflation may average 1.5% over the long term.

So, what happens when the 1.5% average inflation assumption used in calculating your $1 million savings turns out to be 2.0%? Holding our earlier assumptions constant, a half-percentage point cost of living increase could lead to a savings shortfall of over $1 million throughout retirement. Put differently, $1 million of retirement savings might only cover about 20 years of living expenses should inflation average 2% instead of 1.5% in your original plan.

Inflation and Your Financial Independence Journey

So, are higher prices here to stay? And more importantly, is the 1.5% inflation assumption used by many in the financial industry overly optimistic? Well, some argue that once supply constraints ease and the low base effects pass, inflation could return to the low levels we've seen in the last 10-year.

The truth is that in the period following the Global Financial Crisis, economists have had a terrible track record of predicting inflation. Certainly, easing logistics bottlenecks likely will reduce inflationary pressures somewhat in the coming months, but long-term risks remain.

To be sure, many structural changes are afoot, which argue against a return to "normal" inflation. The effects of Trade War tensions and China's growing push for global political influence likely will have some impact on the country's willingness to remain a low-cost producer of the world's goods. Add to this the uncertainty surrounding trillions of dollars in US fiscal and monetary stimulus, and it's likely that inflation will not fall back to 1% over the long-term.

Make no mistake; inflation is so insidious that even a seemingly minor change can have an outsized impact on your achieving (and maintaining) financial independence. When not adequately accounted for, it will slowly and subtly erode the purchasing power of your retirement savings.

Certainly, while inflation is likely to ease in the near term, it would nevertheless be prudent to evaluate whether your long-term inflation assumptions are overly optimistic and if they are, to make adjustments accordingly. Doing otherwise may just end up cutting short your journey to financial independence.

Take these 5 Back-to-the-Basics Steps when Markets Move Against You

Market volatility can have a way of derailing your best-laid investment strategy. So, what can you do to reduce risk when markets move against you? Stay invested and get back to the basics. As with most life situations, when circumstances put up roadblocks to your goals, your first response may be to double down on your current approach instinctively. However, doing more of what you already have done may not only deplete your resources, it may also exacerbate an already untenable situation.

That's why when markets start moving against you, one of the best things you can do from an investment perspective is to focus on the essentials. While it may be tempting to get out of the markets altogether, fine-tuning some components of your investment strategy could otherwise set you up for long-term success. These steps include evaluating your exposure to market risk, focusing on higher-quality investments, reducing leverage, and diversifying your portfolio. To be sure, taking these actions may enable you to stay in the game for the long-run and improve your odds of achieving your financial goals.

Source: Broadview Macro Research

Step 1: Evaluate Your Market Risk Exposure

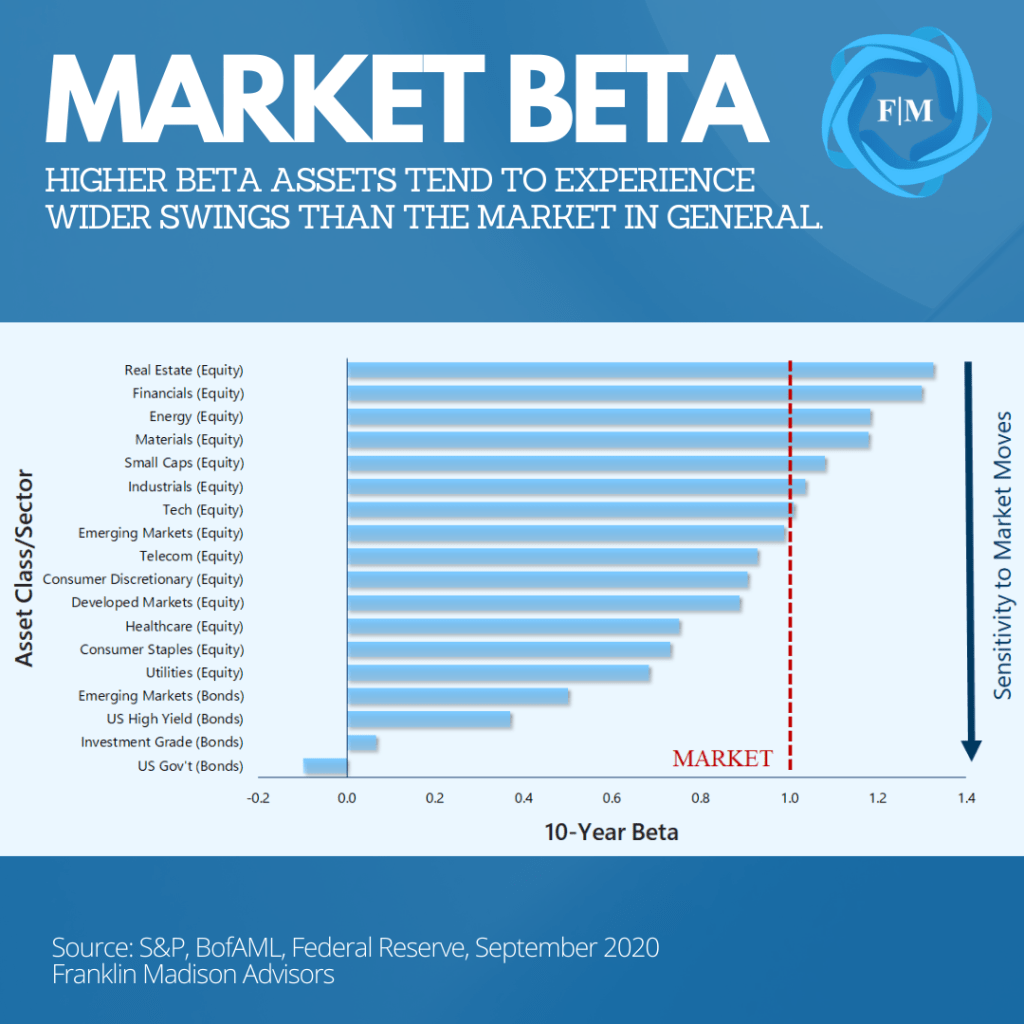

The first essential step you should take when markets start moving against you is to evaluate your exposure to market risk. Beta is one way to quantify this risk, and reducing exposure to it may help you better navigate sharp market swings. Why? Investments with high beta tend to experience outsized moves relative to the broader market when risk assets rally or decline. So, what is beta?

Well, beta is a statistical representation of the movements between a security and a broad measure of the financial markets, like the S&P 500 index. A positive value suggests that a security might move in tandem with the broader markets. Assets with a negative beta tend to move in the opposite direction of the broader markets, while a zero beta suggests little affect in its price relative to the broader markets. And which assets are more prone to move with sharp swings in the markets? Let's look at an example.

History tells us that cyclically oriented equity sectors, like financials, energy, and materials, tend to follow the broader market's moves higher (and lower). On the other hand, fixed income assets like Investment Grade and US Government bonds are less inclined to follow the direction of the broader markets and, in some cases, move in the opposite direction.

Beta is particularly useful when uncertainty rises, and your priority is to reduce the level of swings within your investment portfolio. Holding too many high-beta securities can leave your savings exposed to unnecessary risks and increases the likelihood that you'll fall short of your financial goals when risk assets suddenly decline in value. That's why when market volatility picks up, identifying an appropriate mix of high- and low-beta investments in your portfolio may be vital to reducing investment risk, particularly as you near your savings goals.

Source: Broadview Macro Research

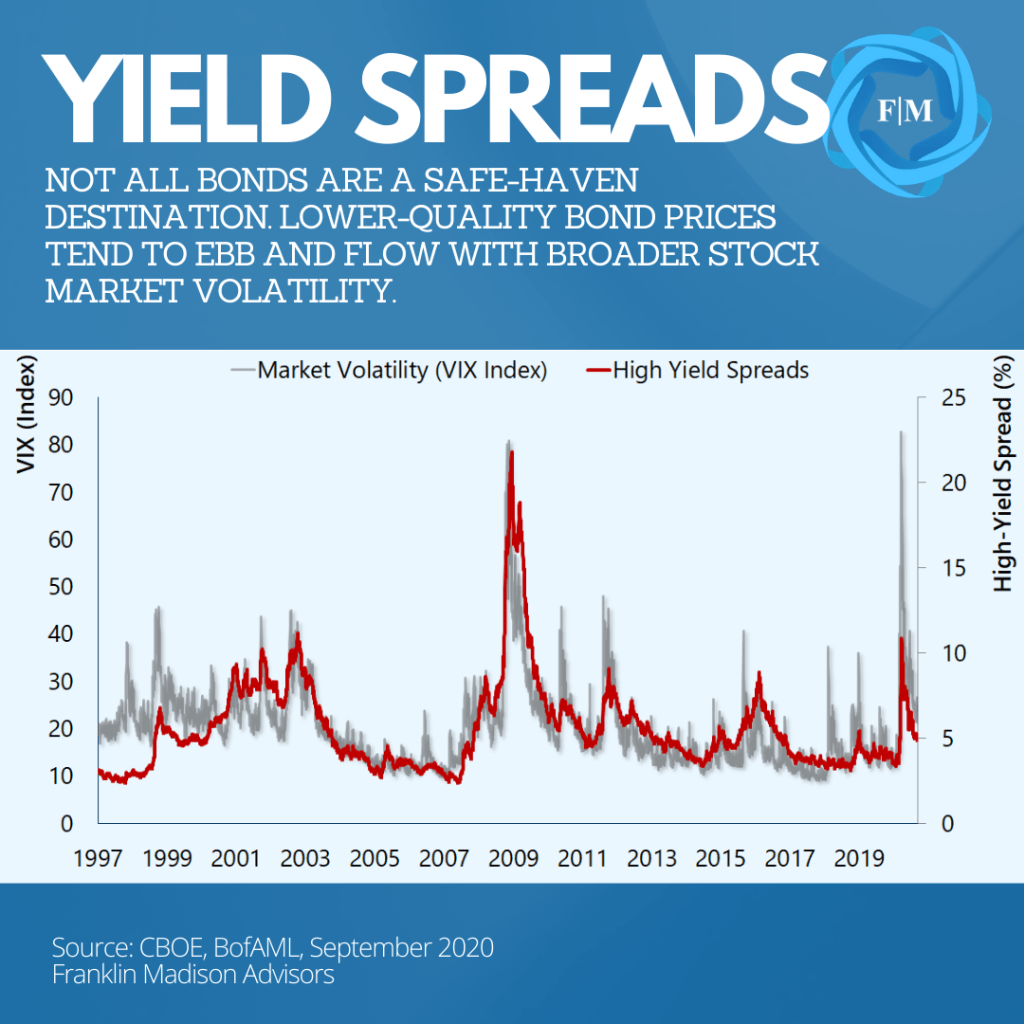

Step 2: Move Up in Credit Quality

The next step you should take in getting back to investing basics is evaluating your bond exposure and consider moving up in credit quality. Assuming that merely having exposure to bonds in your investment portfolio is a way to hedge against volatility could be a recipe for disappointment. To be sure, not all bonds offer safety from market swings.

This point is evident in how yield spreads of low-quality bonds tend to rise during periods of heightened market volatility. Historical data show that when the VIX (a measure of market volatility) rises, the price of lower quality bonds falls, and yields move higher relative to higher-rated fixed-income assets, like government bonds.

In fact, history has shown that the spread between high yield and US government bonds can widen by as much as 20% during periods of heightened market volatility. For example, during the market selloff in early 2020, spreads went from less than 4% in January to 11% in March. Such price behavior not only reflects lower risk appetite among market participants, but it also represents a desire among some investors for higher compensation to take on additional risk. This is notably the case for assets that may have a higher degree of financial uncertainty when economic conditions underpinning the securities deteriorate.

As noted earlier, higher beta fixed income assets, like high yield bonds and emerging market debt, tend to move in the same direction as risk assets, like stocks. Indeed, while bonds might be perceived as a more conservative investment, the truth is that certain cash flow, industry, or country characteristics can make them higher-risk investments and susceptible to market ebbs and flows. That's why if you've been using bonds as a way to gain additional yield in your portfolio, you may want to consider higher quality and lower beta fixed-income assets as a way to reduce investment risk.

Source: Broadview Macro Research

Step 3: Consider Cheaper Stock Alternatives

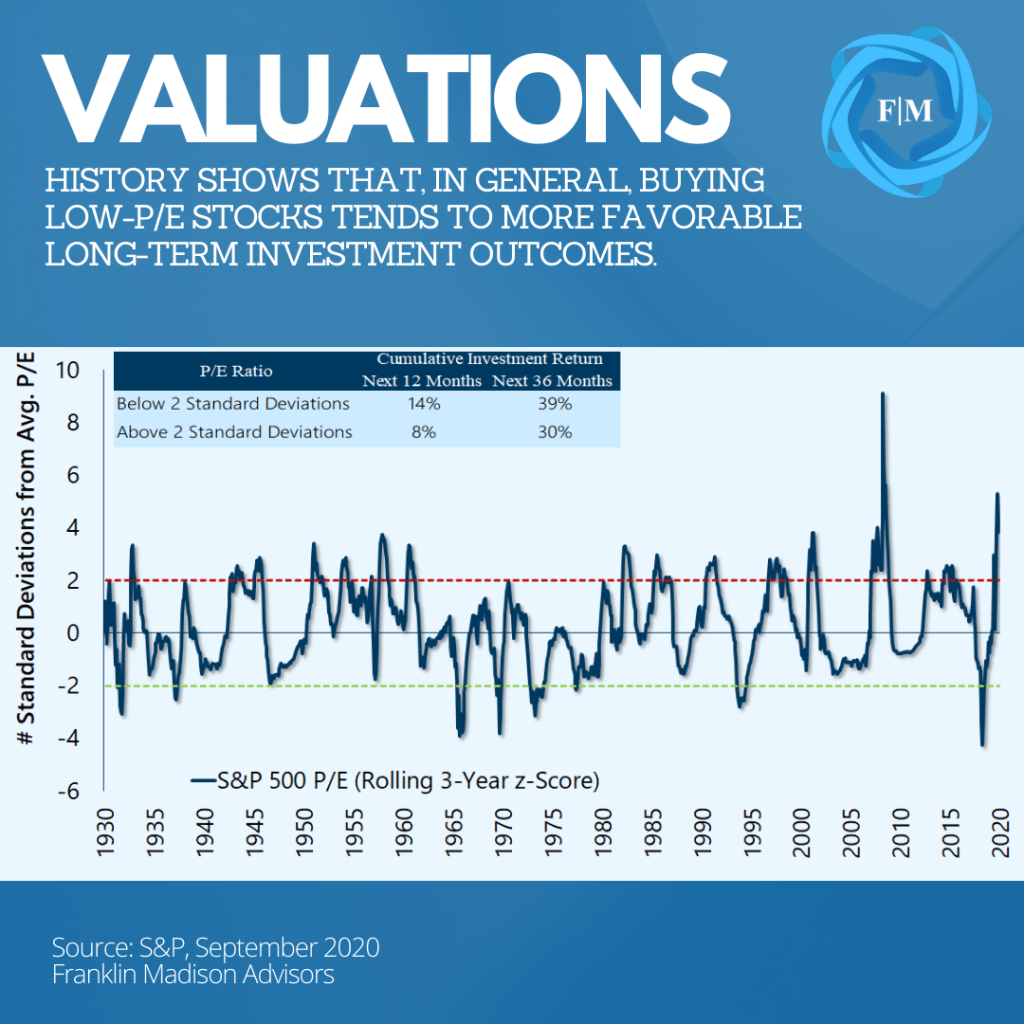

After you've evaluated risk exposure and the credit quality of your bonds, the next thing you might want to think about during a market pullback is whether you're paying too much for stocks. It might go without saying that buying low and selling high is vital to long-term investing success. And while momentum, or recent price action can be an informative value indicator, you may want to consider valuation factors like price-to-earnings (P/E) ratios to determine whether you're paying too much for a given asset.

Why do valuations matter? While it's true that even some high P/E growth stocks can provide investors with positive returns, history suggests that lower P/Es are often associated with more favorable investment outcomes. To evaluate how well this relationship holds, we looked at the historical relationship between P/E ratios for the S&P 500 and subsequent returns over a one-year period. What did we find?

Well, with data going back to the 1930s, our work shows that if you held a portfolio tracking the S&P 500 index when its P/E ratio fell two standard deviations below its mean, you could have received an average annual return of 14%. And how does this compare with purchasing a similar basket of stocks when P/E's are excessively high? Well, buying stocks when they're expensive generated an average 8% returns in the following one-year period.

While our analysis shows that buying high P/E stocks also produced positive returns, the simple truth is that lower P/E stocks tend to outperform over time. The point here is that when the market begins to move against you, one way to set yourself up for a favorable investment outcome is to consider cheaper stock alternatives than what you may already be holding. This includes keeping an eye on high quality, low valuation opportunities.

Source: Broadview Macro Research

Step 4: Reduce Portfolio Leverage

For some investors, trending market behavior presents an opportunity to use borrowed money to boost investment returns. This strategy can work well when prices are moving higher but can amplify losses during a pullback. That's why when markets start moving against you, another critical factor to consider is reducing leverage in your portfolio. Let's take a closer look at how this works.

Leverage usually involves opening a margin account with your brokerage firm, depositing 50% of the value you wish to borrow (this is called initial margin), and hoping that the asset you purchased continues to appreciate. Simple enough, right?

Well, while the value of your portfolio may rise and fall with the markets, the loan you received typically stays fixed. What's more, your broker will also require that your levered investment maintain an equity-to-debt ratio above a certain threshold (maintenance margin). This approach might work well as markets head higher, but when they fall, a time might come when you'll need to raise cash to bring your equity position above the maintenance margin requirement or sell some of your stock to make your broker whole.

And it goes without saying that being forced to sell during a downturn to cover a margin call can amplify losses. That's why overseeing leveraged positions and avoiding a margin call is crucial to managing investment risk during uncertain times. To help illustrate the point, consider the performance of two portfolios that bought on margin heading into a market downturn.

Example: Margin and a Downturn

Let's say that you decide to invest $100,000 into ABC company using $70,000 cash, and $30,000 borrowed from your broker. In this situation, we'd say that your portfolio is 30% leveraged. After initially gaining in value, your portfolio experiences a 40% drawdown over two weeks. While your portfolio avoided a margin call, your net return after accounting for the loan is -48%. To put this number into context, the loss on an all-cash portfolio during this time could be -33%.

And how would this situation look if you had borrowed more money from the start? Well, let's assume that you use $100,000 to purchase the same security, this time with 50% of your broker's money. During the same market downturn, your net return after accounting for the margin loan declines -67%. This two-thirds decline is amplified by a broker's margin call, theoretically leaving you with a more significant hole to climb out of.

The key takeaway here is that if you're using leverage to gain an investing edge, then one of the first steps you should take when the markets are moving against you is to evaluate your use of margin. While this resource can undoubtedly help boost returns when markets are trending higher, it can also open you up for excessive losses during periods of heightened market volatility.

Step 5: Diversify Your Portfolio

A final but crucial step to reducing investment risk during times of uncertainty is to diversify. Diversification can help smooth out investment returns and, more importantly, lessen volatility when the markets begin to move against you. Why is diversification important?

Well, few individuals can predict with certainty which investments will perform well in any given year. In fact, history has shown that an outperforming sector or asset class one year often loses favor with market participants the following year.

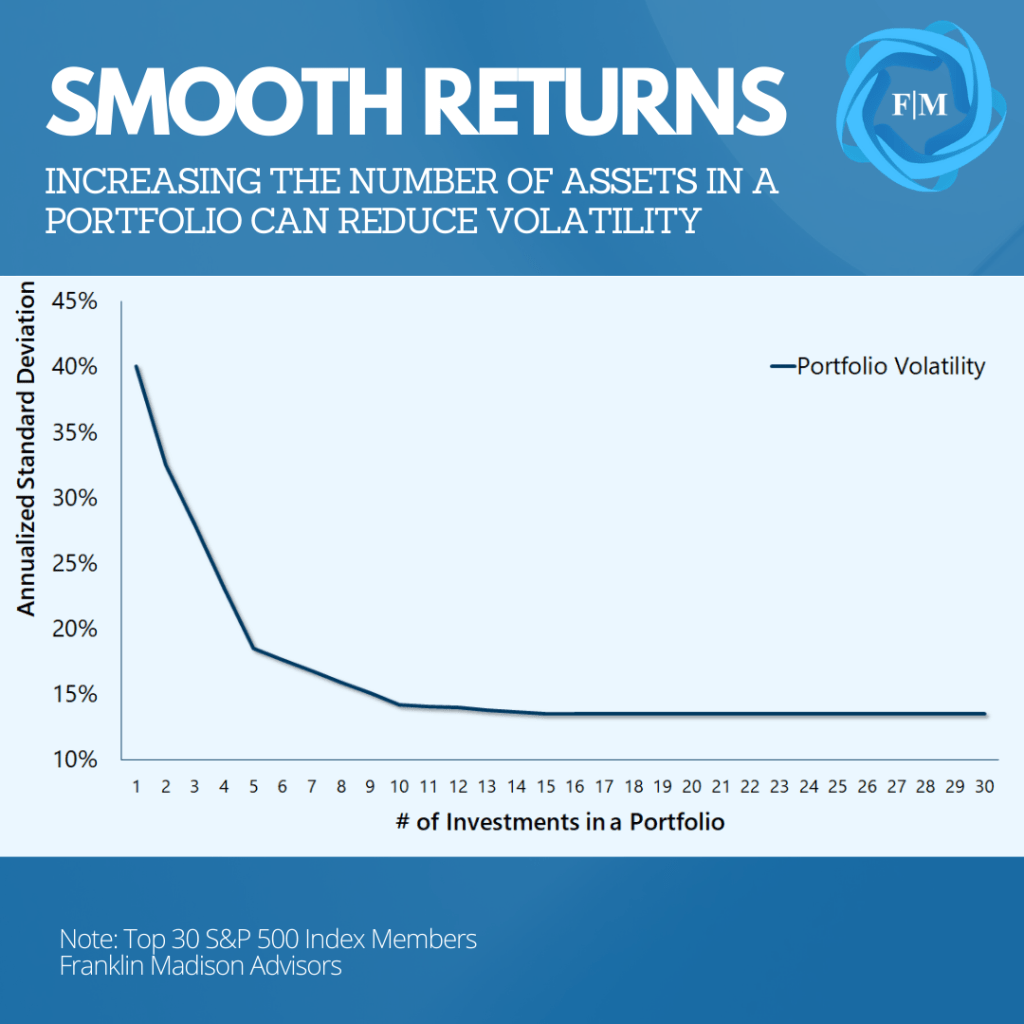

For example, if you held one of the largest names in the S&P 500 index, what you're likely to have experienced over the past few decades is annualized volatility as high as 40%. Put differently, while your stock might have an average return of 10% in a given year, that value could swing between a 30% loss, a 50% gain from one year to the next.

This varying performance can be problematic if you're near a critical savings goal and is how diversification comes help. A simple analysis shows that combining just five stocks from the S&P 500 index could cut your portfolio volatility in half from 40% to 18%. In fact, adding 30 stocks to your portfolio might reduce volatility by two-thirds.

The point here is that diversifying your portfolio lets you gain exposure to market returns without having to pick a winner while taking excessive risk rather than trying guess which investment might do well from one year to the next. When paired up with assets of varying correlations, diversification has historically demonstrated its ability to reduce volatility and smooth out portfolio returns.

Get Back to Investing Basics When Markets Move Against You

As with most life situations, when circumstances put up roadblocks to accomplishing your goals, your first response may instinctively be to double down on your approach as a way to achieve success. Doing more of what you already have done, however, may not only deplete your resources, it may also even exacerbate an already untenable situation.

That's why when markets start moving against you, one of the best things you can do from an investment perspective is to focus on the essentials. While it may be tempting to get out of the markets altogether, shifting your investment strategy could be a better set up. These steps include evaluating your exposure to market risk, focusing on higher-quality investments, reducing leverage, and diversifying your portfolio. Taking these actions may enable you to weather a downturn, stay in the game for the long-run, and improve your odds of achieving financial success.

These Two Techniques May Help You Avoid Gambling with Your Financial Future

How certain are you that you'll achieve your crucial financial goals? Even if you've had the most basic experience preparing for the long-term, you likely know that having the right financial target in mind for retirement, financial independence, or a big-ticket purchase is vital to a successful planning outcome. But did you know that basing your financial allocation decisions on a static, unchanging view of the world might leave you gambling with your financial future?

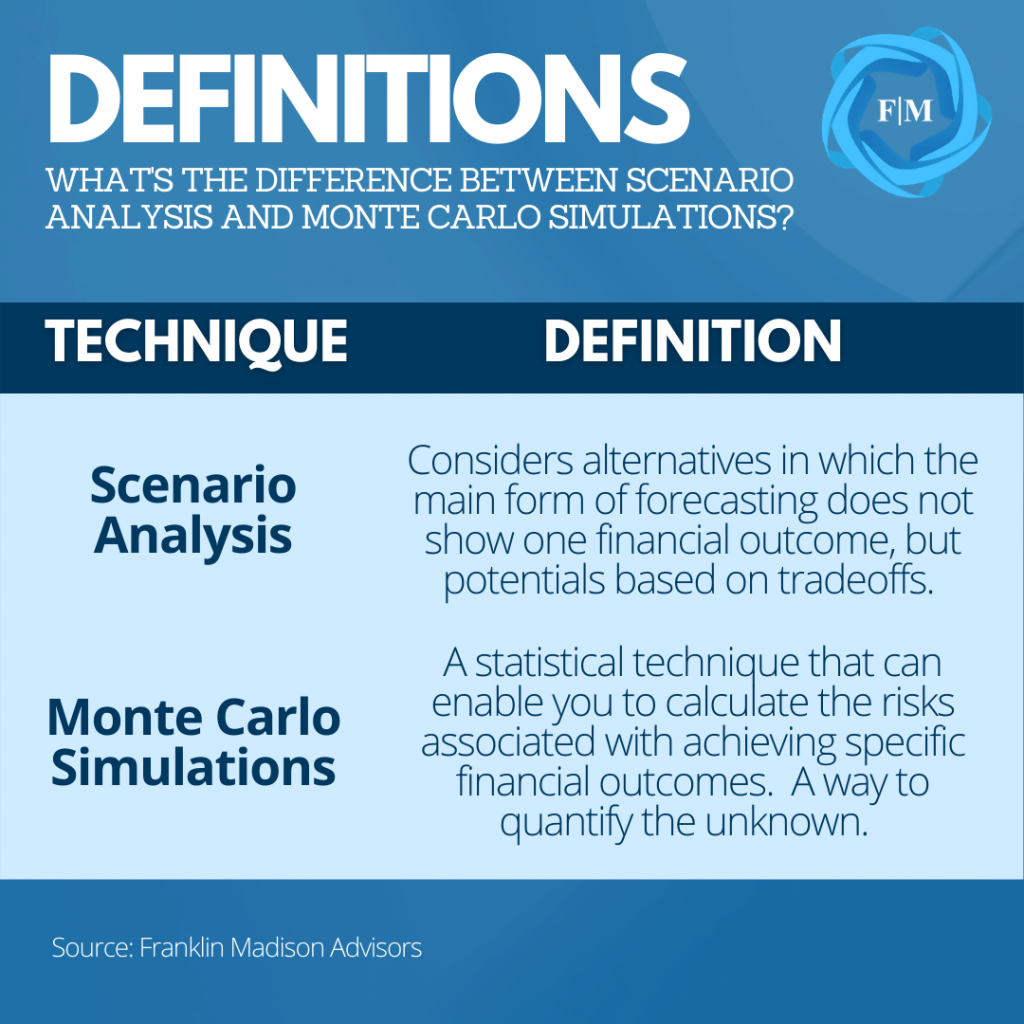

Indeed, understanding how your financial target may rise or fall based on shifting financial and economic conditions or varying lifestyle preferences is vital to the success of achieving your long-term goals. So, how can you sift through these varying factors and identify the right savings target for you? That's where two techniques – scenario analysis and Monte Carlo simulations – play critical roles. Rather than coming up with one fixed solution, you can use these tools to choose from a host of possible outcomes, enabling you to make more informed planning decisions and likely increase your chances of success as you prepare for the future.

Scenario Analysis: Evaluating Tradeoffs

A savings discipline, a modest rate of return, and time can help you achieve your financial goals. Simple enough, right? Well, how can you be sure that you're not saving enough (or too much) if your financial needs rise or fall in the future? What if your financial priorities change? And how can you be sure that your assumed modest rate of return will help you reach your savings goal? Incorporating scenario analysis and Monte Carlo simulations into your financial planning process can help you tackle these and similar questions. Let's take a look at each in a little more detail.

A scenario analysis acknowledges that no one perfect answer exists to fulfill a given set of desired planning outcomes. Indeed, identifying one result to meet your financial goals would be the most straightforward approach. Even so, every savings decision will have its own unique set of costs and benefits. An example here may help illustrate this point.

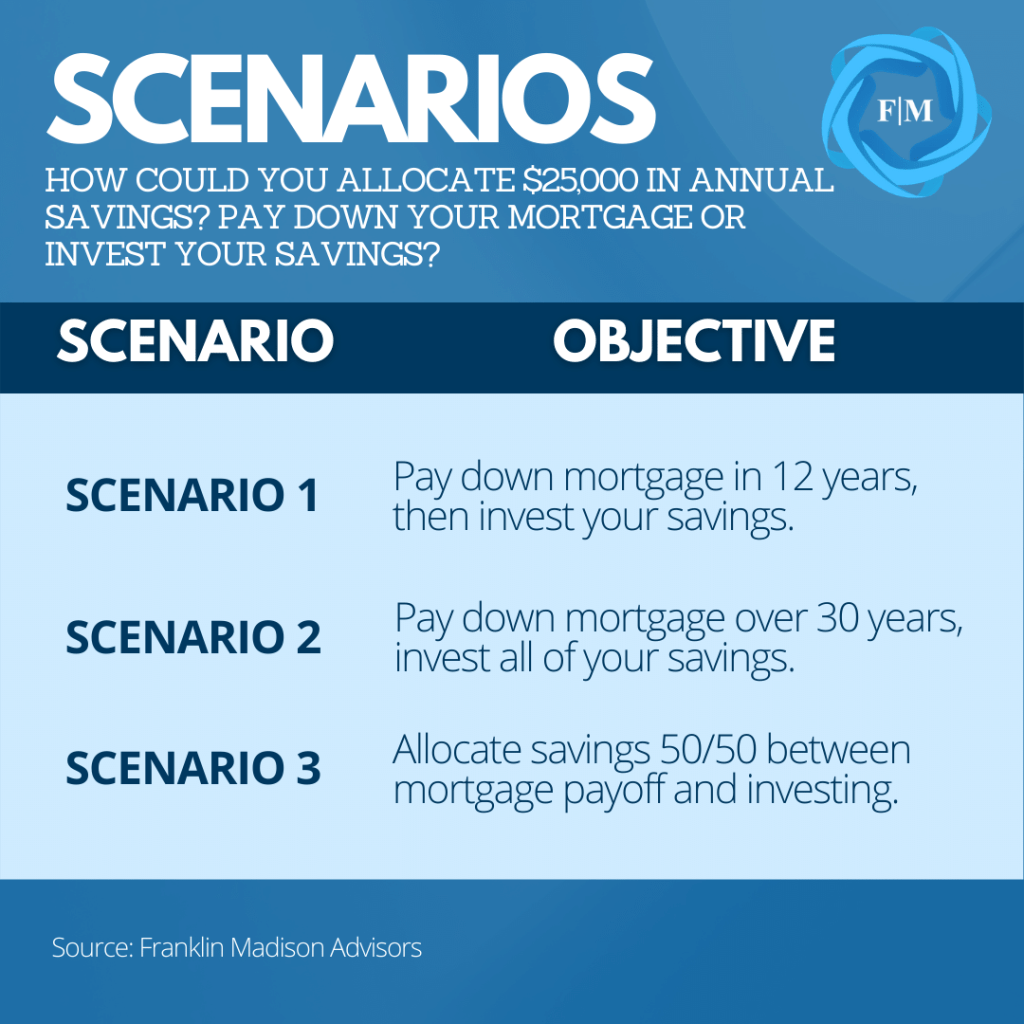

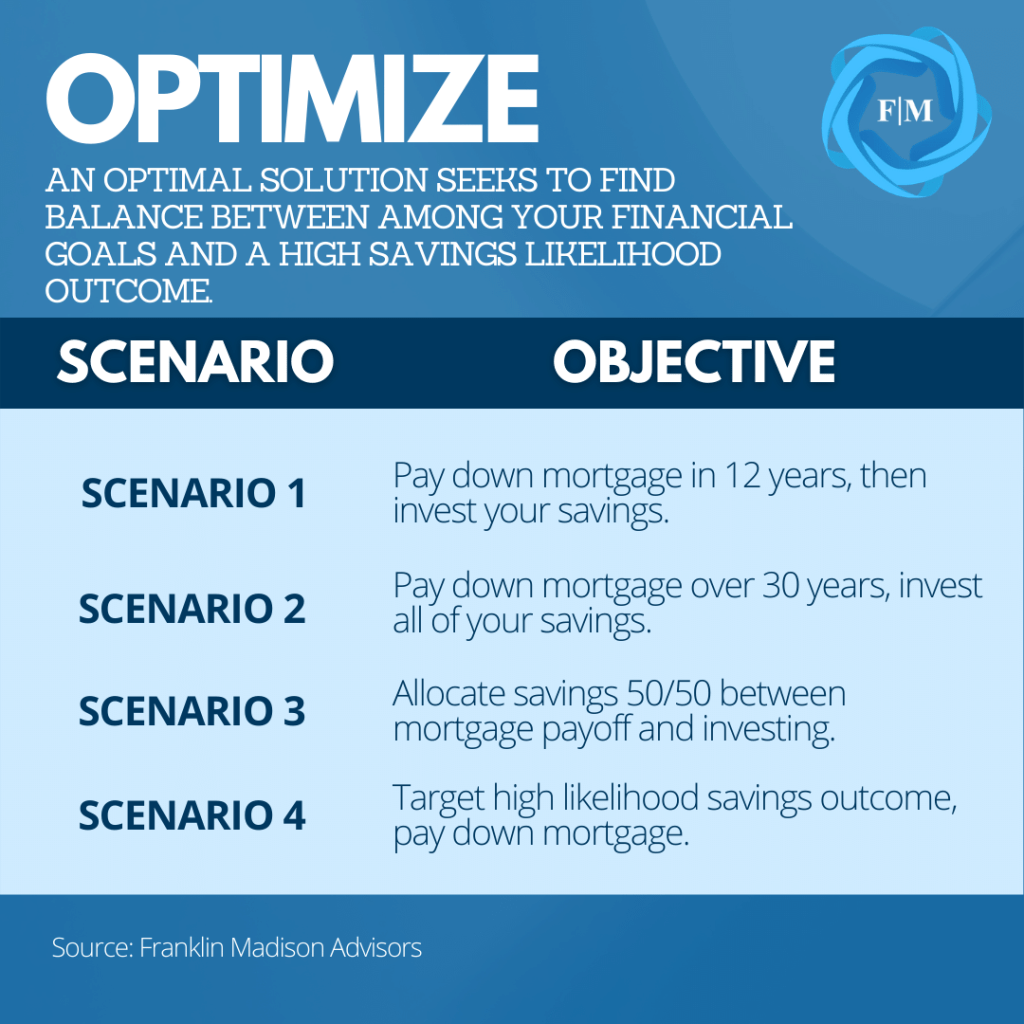

Assume that you can save $25,000 per year. Maybe you'd like to use this money to pay down your $500,000 mortgage, but you'd also like to accumulate $500,000 for a big-ticket purchase in 20 years. We can evaluate the tradeoffs between paying down the mortgage and building up savings from a scenario analysis approach. So, should you pay down the mortgage first or concentrate your efforts on investing your savings? Let's take a look at what would happen if you paid down your mortgage first.

Source: Broadview Macro Research

Scenario Analysis Example

Assuming that you have 30 years left on your mortgage and you use all of your annual $25,000 savings to make additional principal payments, you might be able to pay off your mortgage in 12 years and reduce your lifetime mortgage interest by $230,000. With your house paid off in 12 years, you could then apply what would have been regular mortgage payments to your extra savings. Invested over 8 years with a 5% return, your savings could grow to $529,000. So far, so good, right? Now let's consider an alternative.

What would this situation look like if you invested $25,000 over 20 years instead of waiting to pay off your mortgage? Assuming that you achieved your investment return rate consistently over this period, you'd likely have accumulated $826,000 for your big-ticket purchase. Even if we consider the opportunity cost associated with mortgage interest savings, your savings' end value is notably higher than in the first scenario. Here, you could surmise that you'd be better off investing your savings from the start. Such a conclusion, however, misses a crucial point.

While building savings is vital, paying down your mortgage as you move toward financial independence might still be an essential lifestyle value to consider when allocating your financial resources. Is there a way to have the best of both worlds? One compromise between the two alternatives is to apply half your savings toward investing and the other toward paying down your mortgage. What's the result? Well, at the end of 20 years, not only have you paid off your mortgage, but you're likely to have also accumulated $552,000 for your big-ticket purchase.

These three situations illustrate how scenario analysis can help you evaluate tradeoffs between two or more competing financial priorities. This iterative process is extremely useful in assessing the cost and benefit of selecting an ideal outcome to come up with an optimal solution for prioritizing your financial resources. Even so, one crucial factor to consider is that your simple growth rate may not account for market volatility. To address such uncertainties, you'll likely want to incorporate Monte Carlo simulations into your process to ensure that your plan stays on the right track.

Source: Broadview Macro Research

Monte Carlo Simulations: Evaluating Risks

So, what exactly is a Monte Carlo simulation? Simply put, it's a statistical technique that may enable you to calculate the risks associated with achieving specific financial outcomes. In other words, it's a way to quantify the unknown.

Earlier, we showed several scenarios in which you might grow $25,000 to $500,000 in 20 years using a 5% return rate. But how certain can you be that you'll receive precisely 5% per year, mainly if your return is based on investing in financial markets that vary in performance from one year to the next? In other words, how can you ensure that you're saving the right amount to account for a potential savings shortfall in any given year? Monte Carlo simulations can help.

Indeed, a Monte Carlo simulation is a computer model that, given a set of assumptions – like risk and return – produces thousands of random return observations within the parameters specified. The process not only tells you what might happen, but it also gives you a way of quantifying the likelihood of your desired outcome. Let's demonstrate how this works with our previous mortgage payoff, big-ticket purchase example.

Monte Carlo in Practice

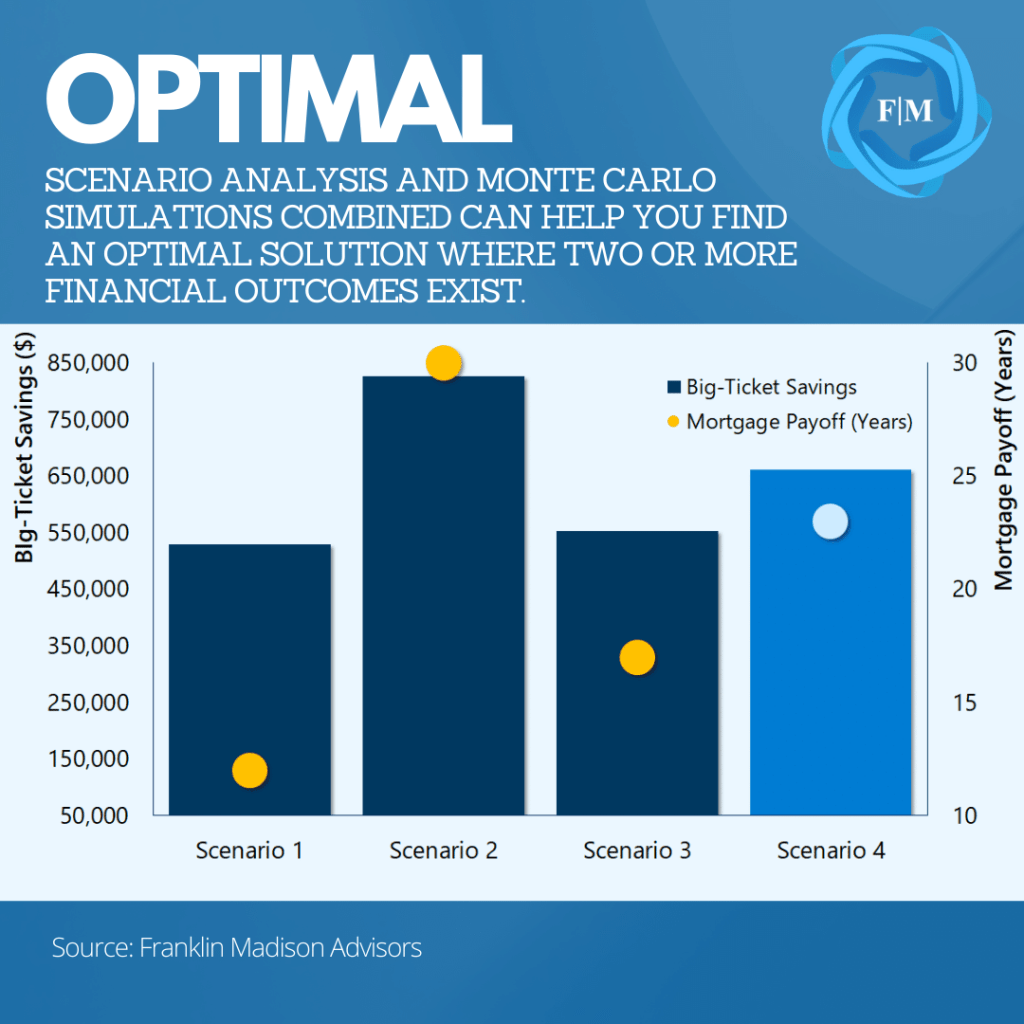

You'll recall that the three scenarios aimed to answer how to apply annual savings of $25,000 best: 1) pay off your mortgage first, then invest 2) invest all of your savings from the start or 3) a 50/50 split between mortgage payoff and investment savings. Each of these outcomes exceeded the $500,000 threshold we set for a big-ticket purchase through investment growth. Even so, what's the probability that each of these outcomes will occur?

In the first scenario, while savings are projected to grow to $529,000, our Monte Carlo simulations tell us that there's only a 60% chance that your savings will be higher than your $500,000 threshold. How so? It all comes down to volatility. In fact, over a third of the 10,000 simulated investment portfolios fall short of this goal, ranging in value between $400,000 to $500,000. How did the other two portfolios perform?

In the third scenario, an even split of savings between mortgage payoff and investment savings over 20 years led to only a marginally higher probability of meeting or exceeding the savings benchmark. However, the Monte Carlo simulations for the second scenario, where we committed all savings to investments, showed a 95% likelihood of achieving or exceeding the $500,000 savings threshold. While a positive solution, you have to consider a critical point: is this the most optimal outcome? Put differently, the mortgage still hasn't been paid off. Let's see how the combination of scenario analysis and Monte Carlo simulations can help.

Source: Broadview Macro Research

Optimal Outcome: Combined Monte Carlo Analysis

Each of the three scenarios discussed has its benefits and drawbacks. Pay off a mortgage sooner and accept a lower likelihood of achieving your savings goal, or up your savings goal and pay off your debt as scheduled. Let's consider a fourth alternative: optimize. Here, our goal is to optimize cash flows to find a balance between paying down your mortgage and accumulating savings with a higher success rate of reaching its threshold. How exactly?

First, we ask the Monte Carlo simulation to identify a value that meets or exceeds our threshold with an 80% certainty level. After another 10,000 iterations, the software tells us that the target value should be $661,000. When we run this figure through our scenario analysis again, we find that the split between saving and debt payoff changes to 80/20 from 50/50 savings vs. mortgage payments in scenario 3. And while you won't pay off your mortgage in 12 years as in scenario 1, this new outcome may shave seven years off of your payments and save you about $90,000 in lifetime mortgage interest expenses.

At this point, you might be asking yourself, why not go for 100% certainty that you'll achieve the $500,000 threshold? Remember, your goal here is to achieve an "optimal", not "maximum" outcome. Increasing your probability might lead to saving more money than you need.

To be sure, Monte Carlo simulations aim to help you evaluate the tradeoff between how much risk you're willing to take to achieve to reach a given effect. Considering all four scenarios, the analysis as a whole tells us that if you're willing to accept that the probability of your big-ticket savings outcome is somewhere around 80%, you could allocate more savings while still eliminating your debt sooner. At the end of the day, it really comes down to evaluating which tradeoffs are more important to you.

Are You Gambling with Your Financial Future?

The Monte Carlo method gets its name from a popular casino in Monaco. The irony of its name is that this technique can actually help you increase your odds of financial success when paired with a concrete scenario analysis framework.

Indeed, if you have two or more financial objectives that you're trying to evaluate then using a Monte Carlo Analysis is one way to help you find an optimal balance between your lifestyle needs and financial goals. More importantly, however, if you're not using a disciplined, quantitatively-based process to assess the likelihood of reaching your financial goals, then you might be gambling with your financial future.

Four Ways to Prepare for Heightened Market Volatility

Many investors know that managing volatility is central to achieving essential financial goals. But how much should you worry about volatility, and what can you do to prepare for it? Volatility represents the ups and downs of asset prices over time. And quite often it’s not the volatility that you should be worried about as it is periods of heightened market volatility.

What’s more, human expectations about the future tend to influence asset price movements. And it's during periods of changing expectations and uncertainty that asset prices swing wildly. Being aware of the narratives driving the markets and having a plan in place before they change is central to financial success. The bottom line is that if you're unprepared for periods of heightened volatility, you might be exposing your savings to unnecessary losses.

#1 Become Familiar with Volatility

Volatility is a normal part of investing. Asset prices do not move up in a straight line but tend to ebb and flow as they appreciate over time. Volatility is the price that you pay to earn a return on your investment. Indeed, what should be at the top of your list of in terms of investing concerns is not volatility itself, but periods of heightened volatility. Before diving deeper into the topic, let's explore some basic concepts.

One way to quantitatively measure volatility is through a mathematical standard deviation of an asset's return. This measure describes the historical tendency for prices to swing up or down versus their long-term average. The higher the standard deviation, the higher the volatility. This understanding is essential because the wider the swings in price returns relative to their long-term average, the less certainty you may have about future returns from one period to the next. And less certainty tends to go hand in hand with higher investment risk.

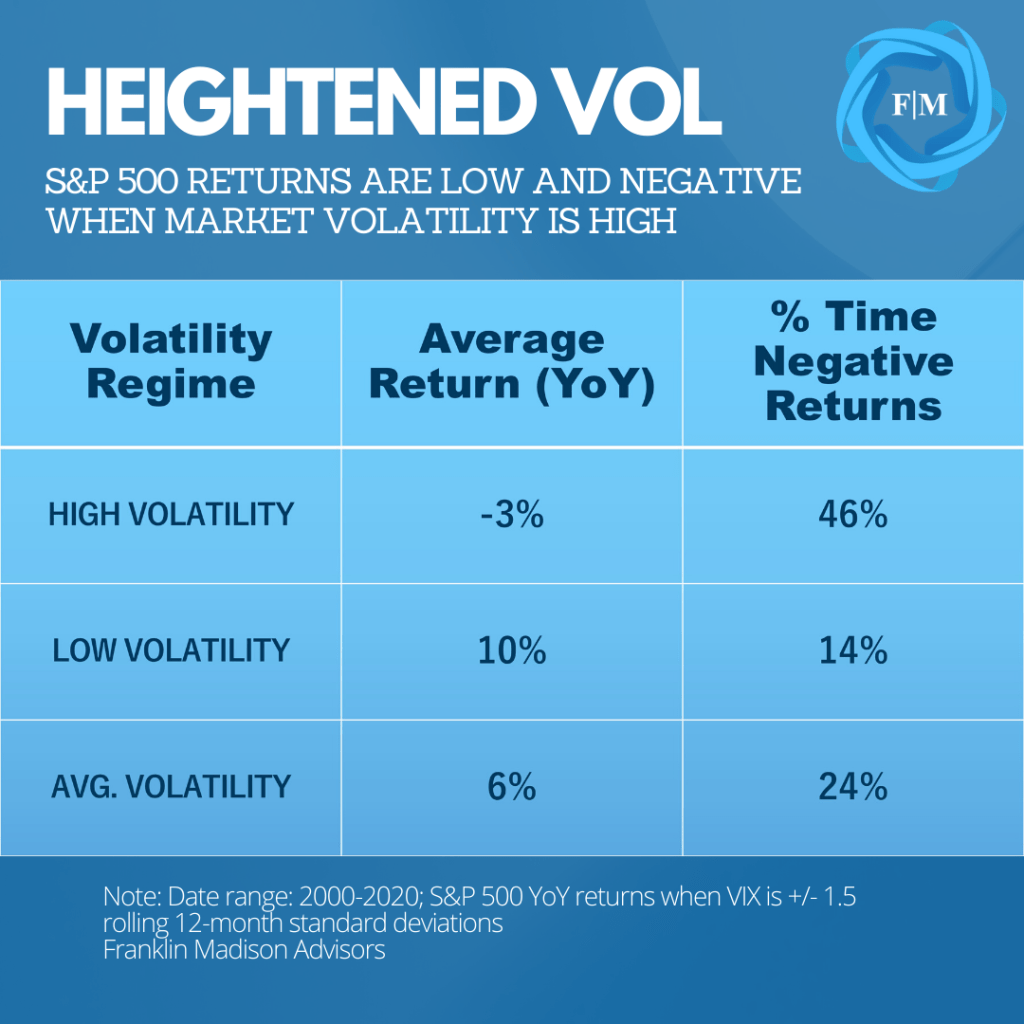

Let's look at an example. From the turn of the century, the S&P 500 index has averaged a modest yearly gain of about 5.3%. This average return, however, masks some of the sharp market moves over the past two decades. If we looked at periods when market volatility was elevated during this time, the S&P 500 returned an average year-over-year loss of -3.3%. However, periods of lower volatility were associated with a higher average annual gain of around 10%.

The takeaway here is that volatility can be used to generate investment returns, mainly when it is low. More crucially, however, history tells us that sudden moves higher in volatility can detract from those returns. Therefore, awareness of the potential impact of a sudden rise in market volatility is vital to improving your investment outcomes.

Source: Broadview Macro Research

#2 Understand Volatility Trends

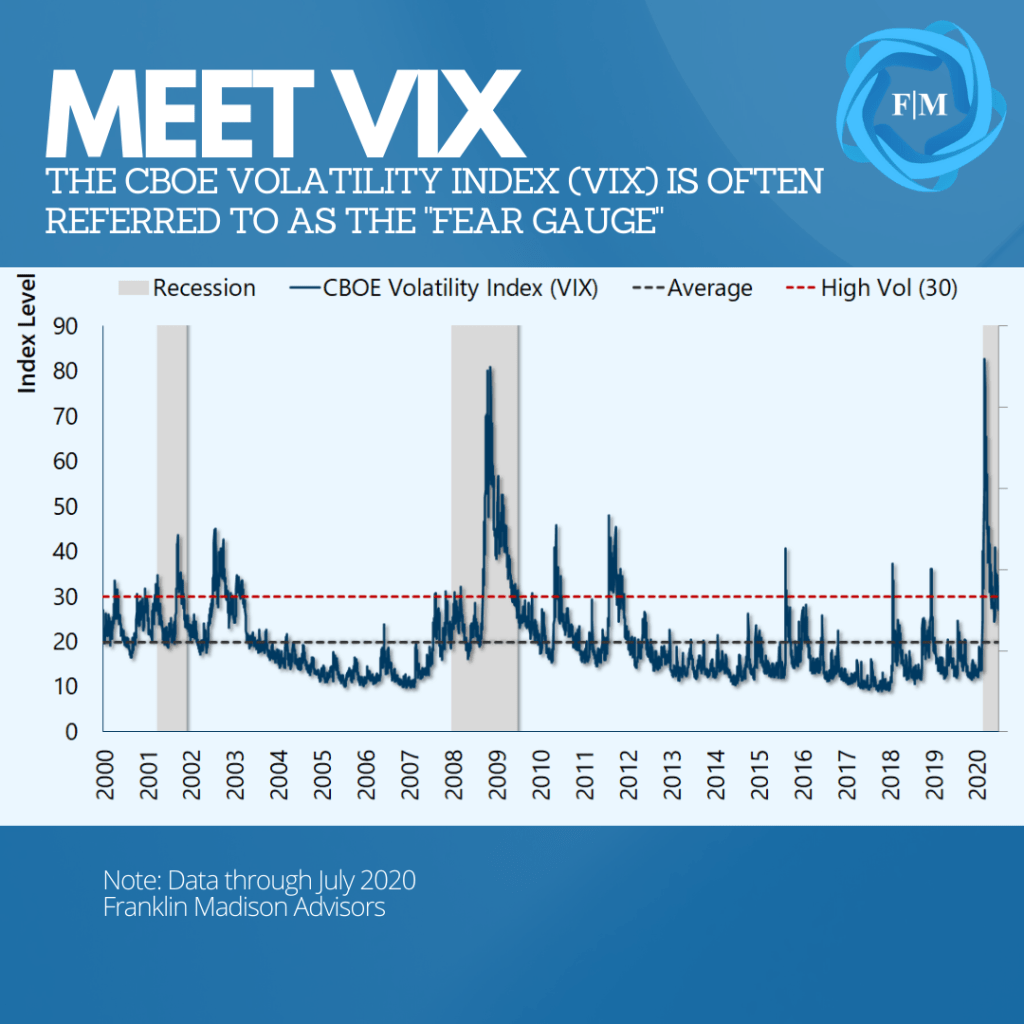

Another way to look at volatility is through market participants' expectations about the future. One widely tracked measure of such expectations is the VIX. The CBOE Volatility Index (VIX) uses a sophisticated method to express the future implied moves of the S&P 500 index. Often referred to as a "fear gauge," sudden moves higher in the VIX are often associated with periods of uncertainty and heightened market volatility.

Compared to the backward-looking statistical measure of volatility mentioned earlier, the VIX is forward-looking. It is also based on investor's directional expectations of the S&P 500 in the month ahead expressed through options market activity. A higher reading generally reflects greater pessimism about the expected direction of the markets.

Over the past two decades, the reading on the VIX has averaged a level of around 20. During the height of the Global Financial Crisis, VIX shot up to a level of 80 and, more recently, bested in February by the uncertainties related to the COVID19 pandemic. Historically speaking, a level below 20 has been consistent with favorable market conditions. A reading above 30 tends to occur during down moves in the market. Why is VIX important?

If you don't know where you are, then it becomes that much harder to figure out where you might be heading. From a volatility perspective, VIX offers a simple way to know how much uncertainty might be priced into the markets at a given time. This understanding is useful before making investment decisions, particularly when history has shown that higher levels of volatility are associated with the potential for lower returns.

Source: Broadview Macro Research

#3 Anticipate Changing Narratives

While financial markets are often viewed as a singular entity, the truth is that they are composed of thousands of assets, each with a host of participants. While algorithmic (computer-based) trading plays an increasingly essential role in the markets, the value of an asset is primarily driven by what human buyers and sellers think it's worth.

Investors are more inclined to bid up prices when they feel confident about the future. For example, when there is certainty about a company's earnings prospects, the policy environment, and the economy's health, asset prices tend to grind steadily higher, and volatility remains low. However, during times of uncertainty about these factors, investors are less willing to pay more for an asset, prices fall, and volatility rises.

One way to measure broad expectations about the economic and policy environment and its potential impact on earnings is by evaluating work compiled by researchers at Northwestern, Stanford, and the University of Chicago. Their Economic Policy Uncertainty Index brings together three components that track 1) news about the economy, 2) tax policy changes and 3) economic forecasts. Their research aims to provide a quantitative measure of what is often a qualitative event (feeling uncertain).

When comparing this measure against the VIX, the data confirm what we know intuitively from a historical perspective: market volatility tends to rise during times of heightened economic uncertainty. From an investment perspective, when uncertainty rises, market participants often change their expectations about the future. And it's during this time of shifting expectations when the price of an asset that may have otherwise seemed reasonable an hour, day or week ago comes into question.

Look for Changes in the Narrative

These periods of uncertainty are driven by a catalyst that often takes time to develop, and that's why measures like the Economic Policy Uncertainty index can help. We only have to look back to the events in February to see how this relationship between uncertainty and heightened volatility played out. Coming into 2020, concerns about a recession had been on the rise, yet many economists expected only softer overall US growth.

In February, however, this hopeful view on the economy changed as Chinese provinces were under lockdown amid a healthcare crisis while the US began reporting rising COVID19 infection rates. As large parts of the US went into lockdown, prospects rose of a deep economic downturn, fueling a volatility spike by late February and ushering in one of the sharpest market selloffs in history.

The point here is that market sentiment is regularly driven by a broad story that is often evident in many quantitative indicators. When factors that support the dominant narrative are challenged, market participants that had been prepared for one set of developments may suddenly change their market positioning to re-evaluate their investment thesis.

When the story changes, the market direction will likely go along with it. Being aware of the narrative driving market sentiment, potential inconsistencies in the story, and how individual market participants might respond can help you better anticipate periods of heightened market volatility.

#4 Know What You Own

Another vital point to understand about volatility is that not all financial assets behave the same way when volatility rises. During periods of heightened market volatility, assets with higher risk levels tend to see wider price swings.

To this point, it is generally understood that stocks are riskier than bonds. This is because equity holders often share in the benefits of company ownership, like stock price appreciation and earnings paid out in dividends. During times of financial distress, like a bankruptcy, however, bondholders are often first in line to be paid back while equity holders might lose a sizeable share of their investment.

Other factors, like the type of issuer (government vs. private sector), company size, market characteristics, and country of domicile, all affect an asset's risk characteristics. Taken together, the higher the likelihood that these factors might expose an investor to a loss, the higher an asset's level of expected risk.

When uncertainties rise and market volatility spikes, individuals holding riskier investments are likely to experience wide swings in asset prices. How do we know this? Well, take, for example, the March market selloff. During the first quarter, the S&P 500 experienced a historic price drop of 20%. At the same time, US government bonds rallied nearly 8% as market participants shed risk assets in preference for perceived safe havens.

The critical takeaway here is that higher-risk assets tend to underperform when uncertainties arise and volatility spikes. If you're anticipating higher market volatility levels, then it's vital to know what you own. Understanding your risk exposures may enable you to trim less favorable holdings and align your investments with your long-term goals ahead of a rise in market volatility.

Source: Broadview Macro Research

Improve Your Volatility Preparedness

We've addressed the various characteristics of volatility and its impact on the markets and investing. So, what can you do to help mitigate the effects of heightened market volatility in your investment portfolio?

Here are three suggestions:

First, don't put your eggs in one basket. As we've written about recently, diversification is one crucial way to reduce portfolio volatility and smooth out investment returns for the long term. Studies have shown that increasing the number of securities held can reduce overall volatility in an investment portfolio. Therefore, if your goal is to invest for the long term, be sure to diversify your portfolio across various securities and asset classes to help reduce risk.

Second, build situational awareness. It's easy to get caught up in the market's daily price action or stay focused on a particular asset when your investments are doing well. Even so, markets are often driven by one or more underlying stories that can evolve. And it's at those turning points in market narratives where volatility tends to spike. That's why it's critical to stay informed about broadly relevant market topics so that you don't get caught unprepared when they change.

Finally, have a plan and act accordingly. Start with knowing what you own. Then, try to anticipate how those assets might perform during wild market swings and adjust your holdings accordingly. Heading into a period of heightened market volatility, it's also vital to have a higher level of cash on hand. Doing so accomplishes two ends. One, it reduces the likelihood that you'll need to sell an investment at an inopportune time to pay for necessary expenses. And two, it may allow you to have dry powder on hand for an opportunity to add discounted assets to your investment portfolio.

Volatility is a normal part of investing. It's the price you pay to earn an investment return. That's why what should be at the top of your list in terms of investing concerns is not volatility itself, but periods of heightened market volatility.

Whether you measure it using backward- or forward-looking means, the fact is that spikes in volatility are often drive by changing human expectations about the future and associated with lower investment returns. Being aware of the narratives driving the markets and having a plan in place before they change is central to investing success. The bottom line is that if you're unprepared for periods of heightened volatility, then you might be exposing your savings to unnecessary losses.

What’s the Best Way to Protect Your Hard-Earned Wealth?

What’s the best way to protect your hard-earned wealth? That’s the million-dollar question that’s on a lot of people’s minds right now. The fact is that the coronavirus has demonstrated in absolute terms how an unexpected event can quickly take away your earnings ability and deplete your life savings.

Events surrounding the coronavirus have also demonstrated how life’s surprises can come at you from all directions. And when they do, your ability to build enduring wealth can evaporate in the blink of an eye. So how can you protect your hard-earned wealth today?

Figure 1: Our Risk Management Process

Source: Broadview Macro Research

Well, we believe that one way to prepare for life’s unexpected events is to incorporate a disciplined risk management process into your wealth management framework. This involves identifying outstanding risks, using tools to mitigate these threats and monitor for evolving challenges to your wealth.

Risks to Creating, Growing and Preserving Enduring Wealth

Before we dive into our discussion on the methods you can use to protect your wealth. Let’s take a closer look at some of the ways that risks may come your way.

Risk – a situation involving exposure or danger

The word “risk” can mean many things to many people, so we’ll frame our discussion on the topic within the context of our wealth management framework. As you’ll recall from our previous reports, the wealth management framework focuses on the actions you need to take today to build enduring wealth over time.

Figure 2: Our Wealth Management Framework

Source: Broadview Macro Research

This includes: 1) being intentional and efficient with your time and resources, 2) making your money work for you and 3) the topic of today’s discussion: taking steps necessary to protect your hard-earned money from both expected and unexpected events.

Indeed, the wealth management framework is just one tool you can use to build wealth. But the reason we believe that it's important is that it’s a disciplined process that can help you create, grow, and preserve financial wealth for the long-term.

Being Risk Aware: Creating Wealth

The aim of our wealth creation process centers on steps necessary to generate a productive source of financial savings. These actions include being intentional with your money, maximizing your value to others and optimizing your net worth.

Your goals during this time should be to hone your innate talents and abilities and leverage a systematic, disciplined process to build a solid financial base. Now, what would you do if your ability to create wealth became impaired? For some people, COVID-19 has done just that.

Many of us spend a lot of time thinking about various ways we can get ahead and produce results. And often we do this without really giving much thought to what could derail our efforts or take us out of the game completely.

As of this today's publishing date, Coronavirus infections continue to rise across the US. And there’s no doubt that the outbreak has impacted many lives in many different ways. The current events also illustrate the kind of risk awareness you must have if your goal is to produce enduring wealth during the creation process.

Figure 3: U.S. Unemployment Rises to a Post-War Record

Source: Broadview Macro Research

More specifically at this stage, your awareness should focus on identifying risks that can impede your ability to earn an income and address hazards that can impair the value of assets you use to grow wealth. So, what are some of these risks?

Well, we’re talking about events that could lead to short term or long-term disability, property damage, lawsuits, and in some cases, death. We’ll talk about measures you can take to protect yourself against such events in just a moment. But the point here is that you need to develop an awareness of the risks that could derail your ability to create wealth before they even happen.

Being Risk Aware: Growing Wealth

Sustaining your disciplined wealth creation habits and then using 1) your base of savings, 2) a rate of return, and 3) some time to make your money work for you are the goals of the growing wealth process.

The obvious risks to growing wealth are financial market volatility and other losses related to investing. With that said, there more insidious threats working against you as you’re growing your wealth.

These are menaces waiting to separate you from your hard-earned money – one basis point at a time. These factors include excess fees eating into your investment rate of return and the IRS taking a bigger bite of your earnings. So, what exactly do we mean here?

Figure 4: Excess Fees Can Reduce Potential Long-term Returns

Source: Broadview Macro Research

Well, here are a couple of examples. First, let’s think about fees charged on investment products for a moment. Did you know that a one-percent investment management fee difference can lead to more than $400,000 in wealth forgone on a million dollars invested over 20 years?

What about taxes? As it relates to investing, you could have income on the same two savings vehicles taxed at many different rates simply based on the structure of one savings vehicle versus another.

The takeaway here is that if you’re not careful with how you put your money to work, you may be growing your money, but at a much slower rate than you otherwise could during your growth phase.

Being Risk Aware: Preserving Wealth

Seeing through important life goals like retirement or even leaving behind a legacy is the aim of the wealth preservation process. During this time, you’ll need to ensure that the money that you’ve spent time accumulating and growing is still around to pay for your important life goals years from now.

And not only that, but that there’s enough left over to pass along to people or charities closest to your heart if that’s important to you. The risk here is that there won’t be enough money to meet your retirement needs or the needs of your loved ones.

This can occur, for example, when financial markets experience a sharp sell-off just as you’re preparing to enter retirement. There's no question, this year’s financial market volatility has acutely illustrated how a sudden and deep pullback in the markets can derail even the best-laid retirement plans.

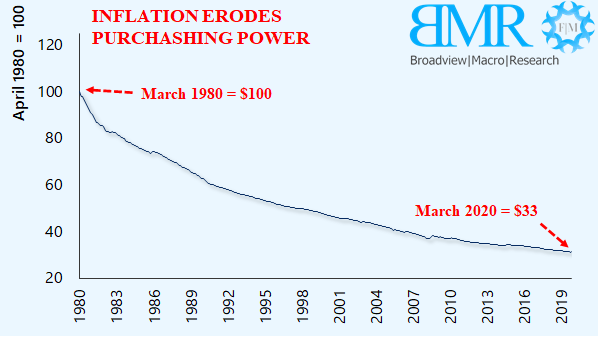

Figure 5: Inflation Erodes Purchasing Power

Source: Broadview Macro Research

Another risk to wealth longevity is having your purchasing power reduced over time by inflation. For example, did you know that when inflation is running at around 2% per year, it takes about 36 years to cut your purchasing power in half?

Or put differently, a million dollars today may only buy half that amount of today’s goods or services in less than two generations when inflation is present. Taken together, the important point here is that at each phase of the wealth management process there are risks that could prevent you from building enduring wealth.

Protect Your Wealth Today

So, what steps can you take to protect your hard-earned wealth today? Well, one way to prepare for life’s unexpected events is to incorporate a disciplined risk management process into your wealth management framework. Let’s take a look at some examples of how this risk management process applies as we create, grow, and preserve financial wealth.

Risk Management: Creating Wealth

Events that hamper your ability to use your innate talents to produce income and generate savings are key risks during the wealth creation process. One way to protect your wealth during this time is to utilize insurance as a tool to protect against financial loss.

The key to preserving your wealth during this time is ensuring you have the right amount of insurance coverage to meet every one of your financial needs. For example, COVID-19 has reminded us all of our mortality. At the same time, it has served as an important reminder that life insurance can be a useful way to create financial wealth.

This is especially true if you experience unexpected tragedy in your own life before you’ve had a chance to build the kind of wealth that will leave your loved ones protected. In a similar vein, now’s also the time to take a look at your disability coverage. More specifically, you should consider whether the limits on your disability insurance policy are sufficient to cover your living expenses should you become injured and can no longer work.

The point here is that if your goal is to build enduring wealth, you will need a method to defray some of the risks if life’s curveballs threaten to take you out of the game. In our case, insurance provides a way to defray some unknown risks and immediately creates a financial source of wealth in case of an unexpected tragedy.

Risk Management: Growing Wealth

Fees and taxes are factors that can hinder your ability to quickly build enduring wealth during the growing wealth process. Your goal during the growth process should be to maximize your risk-to-reward ratio. And one way to do this is to reduce unnecessary investment fees.

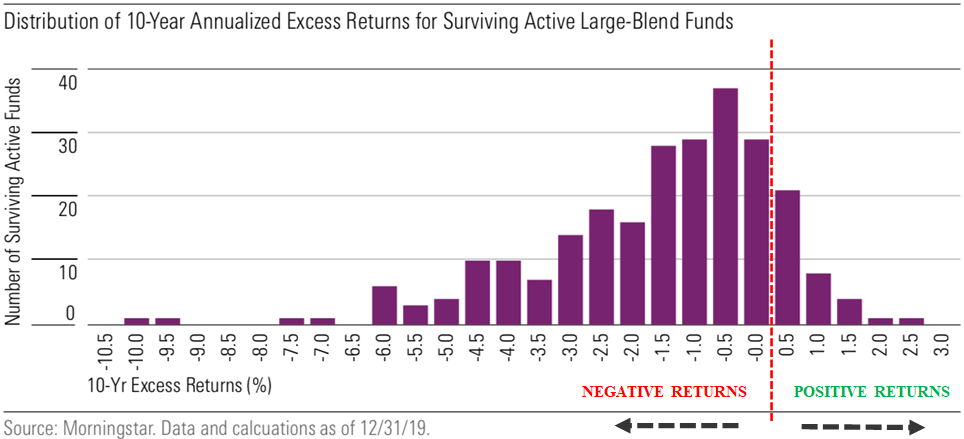

Figure 6: Active Management Has Largely Underperformed

For instance, actively managed investment funds tend to charge a premium when compared to passive funds. Therefore, now’s a good time to look at the performance of these funds and consider whether what you're paying for active management is worth the premium. This is notably important at a time when active managers in some cases have underperformed their passive benchmarks.

Addressing unnecessary taxes is another way to cut your losses during the growing wealth process. This is especially true if your investments produce income and you’re not yet retired.

For example, you can minimize the taxes that you pay by making sure that income producing investments are held in tax deferred vehicle like a 401k or IRA rather than a brokerage account which is taxable.

Risk Management: Preserving Wealth

If you are planning on taking distributions from your retirement within the next year or expect to leave a legacy, protecting wealth at this phase is important now more than ever. You’ve put in the hard work to grow your money, so now’s a critical time to protect it as you move from accumulating wealth to distributing wealth.

We mentioned earlier how a sudden drop in markets can derail even the best-laid retirement plans. That’s why you’ll want to have a distribution strategy in place that addresses how retirement assets will be liquidated during periods of heightened market volatility.

For example, giving more distribution weight to an asset that is less sensitive to sharp moves in the markets and ensuring you have an adequate level of cash on hand to weather volatility is one way to prepare for such times. When it comes to leaving a lasting legacy, having a solid estate plan is where it all starts.

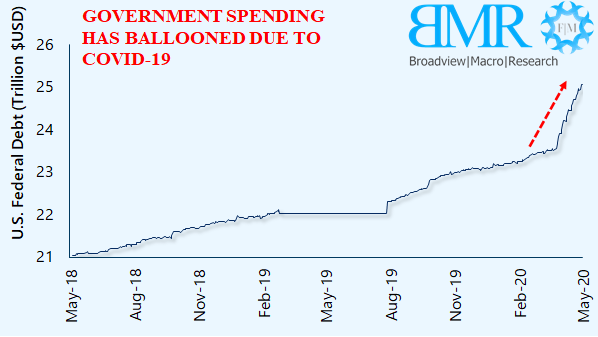

Figure 7: Federal Debt Has Ballooned Due to COVID-19

Also, you’ll want to make sure that your long-term investment management process reflects the realities of inflation. Remember, purchasing power can be cut in half in less than two generations when inflation is running at around 2% per year.

With government debt issuance ballooning by $3 trillion and Federal Reserve assets growing at an exponential rate, you’ll want to make sure that how your legacy assets are managed align with today's inflation expectations. This is important because doing so will help ensure that your wealth can adequately serve generations now and into the future.

Protecting Wealth Begins with a Process

The coronavirus certainly has exposed our varying levels of financial risk preparedness. Even so, we believe that you can take some especially important take steps right now to protect your wealth, starting with being risk-aware.

This means identifying the kinds of threats that may crop up at various life phases and then preparing for those threats as part of a disciplined risk management process. There's no doubt that when it comes to building enduring wealth it’s important to think about the steps you need to take today to create and grow your money over the long term.

However, another important step is taking the time to protect yourself against the threats that are waiting to separate you from your hard-earned wealth. Some of these steps include utilizing tools like insurance, tax and cost-efficient investing vehicles, and a solid investment, estate, and distribution plan to protect your money.

Finally, be sure to manage risks for the long term. This involves continuously evaluating the current economic and market environment to identify evolving threats to your wealth. Then use some of the tools that we’ve discussed to help mitigate those risks.

We believe that incorporating an active risk management process into your wealth management framework could ensure that your wealth endures for the long-term no matter what surprises life throws your way.

Three quick steps to help manage financial anxieties during uncertain times

If the coronavirus, recession angst or elections are keeping you up at night or have generally increased your level of anxiety, you can take comfort in knowing that what you’re feeling is natural. In fact, our brains are primed for an anxiety response during times of heightened uncertainty. At least that’s according to one research paper published in the journal Nature. And as the researchers point out, higher levels of uncertainty disrupt our ability to assign clear probabilities of success to our desired life plans and goals. When this happens, chemical messengers tend to activate the same centers that control the “fight or flight” response in our brains. The result?

When anxieties build to the point that a fight or flight response is activated, panic can ensue, leading to a set of decisions and actions that may appear irrational in hindsight, yet seeming rational in the moment. From a financial perspective, panicked behavior can include anything from hoarding resources or doubling down on losing bets to selling fundamentally sound investments during a bout of financial market and economic volatility. And while anxiety may build during periods of uncertainty, panic may not be a foregone conclusion during these times. To be sure, the solution may lie in the act of exposure, desensitization and acceptance. So what exactly do we mean here?

Who me, worry?

Well, the idea is that repeated exposure to the things that trouble us the most can, over time, desensitize our brain to our concerns, reduce anxiety and dull our innate panic response and generally increasing one’s ability to constructively deal with highly uncertain events. While this approach is more actively utilized in treating patients with certain phobias like fears of animals or insects, the process can be useful in reducing financial anxieties at a broad level. How so? Well, this can be accomplished by actively embracing the potential for a negative outcome, putting the possible consequence in context and developing tangible action steps to help mitigate their expected negative effects.

Let’s revisit what could go wrong from a financial perspective as a result of the coronavirus outbreak. In brief, we believe that the coronavirus has had both direct and indirect impacts on the global economy that are yet to be determined. Either way, in the most affected parts of the world, like China, the direct effects have been lower consumer spending and business activity resulting from mandatory quarantine and self-isolation on account of the coronavirus. One of the indirect effects of the outbreak has been supply chain disruptions that are making it harder for firms in less affected countries (like the U.S.) to get the products they need to do business.

What this means is that global economic growth is likely to suffer in the coming months as household spending and business activity fall (assuming that a solution to the outbreak is not found soon). While risk assets have in recent days bounced in response to global monetary and proposed fiscal support, the fact is that corporate earnings growth is likely to slow in the months ahead, making assets like stocks more expensive. And as the risk of a U.S. recession rises, we expect economic and financial market volatility to remain elevated for quite some time. So, what can households and investors do to prepare amidst increasing uncertainties?

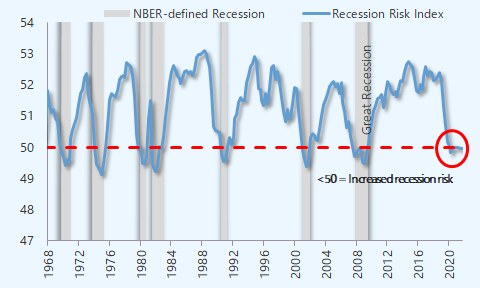

Figure 1: U.S. recession risks remain elevated

Gain some perspective

For starters, gain some historical perspective and keep an eye on the future. While the coronavirus has not yet been characterized as a pandemic by the World Health Organization (WHO), it could be on track to be more disruptive than the H1N1 virus of 2009. Even so, what’s important to note amidst today’s developments is that in some ways we’ve been here before.

In fact, as a civilization we dealt with a host of health epidemics in the 20th and 21st century, in the last 100 years the global economy has weathered 30 major military conflicts and six global recessions since 1970. During this time, we’ve also witnessed the rise and fall of various political and economic systems and yet, by some measures, global wealth has steadily risen, and poverty levels have fallen. What’s the point?

The point is that despite the concerns surrounding the coronavirus, state of the economy or potentially disruptive nature of elections this year, over the long term economic and financial market conditions are more likely than not to rise in the future. While market volatility and uncertainty can generate uncomfortable feelings in the near term, it is also helpful to remember is that similar events have come and gone over the years. Therefore, revisiting and staying committed to long term goals could help even the most anxious households and investors better navigate near-term uncertainties.

Take action today

Besides gaining some perspective and staying focused on long term goals, what are some tangible actions that households and investors can take to navigate short term economic and financial market volatility? First, build up your cash reserves to help prepare for the unexpected. This includes boosting cash flows by reducing non-essential household spending and lowering interest expenses by refinancing high cost debts. This is important because we expect employment conditions to become less solid should economic uncertainty increase in the months ahead. Therefore, having enough cash on hand to cover 6-12 months of living expenses will be key to bridging disruptive life events.

Next, we recommend investors avoid trying to time the market bottom or, alternatively, selling everything and going to cash. Rather, at this juncture our advice for investors is to keep an attitude toward investing that is rooted in fundamentals and maintaining broad exposure to the markets. This begins with ensuring that portfolio allocations are strategically aligned with long-term goals. And with the market poised to move lower in the near term, we believe that now is the time to look for investment opportunities in solid defensive names, like consumer staple companies, that are positioned to weather periods of sustained market volatility.

Finally, when the economic and market outlook begins to feel out of control, we recommend embracing radical acceptance. That is, accepting life as it is and not resisting what can’t be changed. To be sure, there are arguably more topics of great consequence today creating angst than there has been in years. And while it may be tempting to take a passive posture towards today’s uncertainties, we believe that now more than ever is the time to begin taking proactive steps to preserve long-term goals. This includes educating (exposing) yourself about the potential effects of today’s events, staying rooted in a historical perspective and taking proactive steps to ensure that you can weather near term economic volatility to achieve your long-term goals.

Why the coronavirus is relevant to your finances

It’s getting harder and harder to ignore the potential financial fallout from the novel coronavirus (nCoV-2019) outbreak underway. Some of this fallout was evidenced in the global stock selloff on Friday and futures (as of this writing) point to a weaker start at Monday’s open. Indeed, the concerns surrounding the ongoing spread of nCoV is likely to weigh on market sentiment for weeks. But why is nCoV relevant from a financial perspective?

Well, in our opinion, the quickening spread of the coronavirus illustrates how fast unexpected events can alter near term economic assumptions and upend best laid financial plans, notably at a time when the U.S. economy is primed for a recession. Amidst the potential for outbreak-related market and economic volatility, we provide a few recommendations that households can use to increase their financial preparedness as Wall Street and Main Street worries potentially intensify in the weeks ahead.

It’s going to get worse before it gets better

Coming into the year we expected several key events (like geopolitics, central bank policies and elections) to raise uncertainties and simply make getting ahead in life financially harder for some households in 2020. In last week’s post, we wrote about one strategy investors can use to increase portfolio returns as economic growth falls and market volatility picks up.

We’ll talk about some additional financial strategies that can be used to help mitigate uncertainties later, but before we do that we need to highlight two key reasons why we think the coronavirus is important to consider from a financial perspective.

First, reports on the spread of nCoV and the subsequent global response suggest that the outbreak is likely to get worse before it gets better. While Beijing has stepped up its efforts to quarantine suspected infected zones, other governments, like Russia and Singapore have sealed their borders with China while countries like the U.S. have put up their own restrictions on travel to-and-from China amidst the outbreak.

This comes as the World Health Organization (WHO) declared a “public health emergency of international concern” last week. To be sure, the rapid spread of nCoV compared to other coronaviruses like SARS suggests that the current outbreak has the potential to only get worse before it gets better. Barring a rapid de-escalation of current events, what this likely means is that discretionary international travel is poised to slow in the coming weeks not just into and out of China, but potentially among countries that are seeing infections rise and more importantly as deaths outside of China begin to increase in number as well. This brings us to our second point.

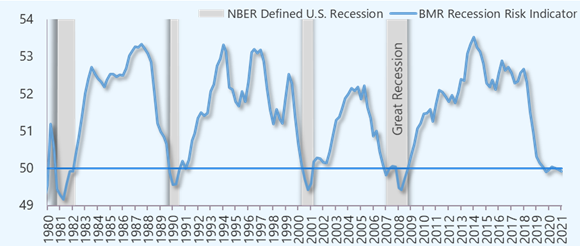

Figure 1: U.S. recession risks are elevated in 2020

U.S. economy primed for a slowdown

The restriction on travel and closing of borders could very well aggravate a downturn in a U.S. economy already primed to slow this year. As we’ve written about in past posts, we believe that the risks related to a U.S. recession remains elevated this year as business spending and hiring activity declines. And while discretionary household spending supported the U.S. economy in 2019, last week’s fourth quarter GDP print remained soft even as the Fed primed its quantitative easing pump during the last three months of the year.

And from this perspective, we expect corporate earnings growth to remain subdued in 2020, challenging already stretched financial valuations. In other words, risky assets have broadly had a strong run in recent months, but now appear expensive on historical basis. And this fact increases the chances that already expensive risky assets could come under increased selling pressure as some sudden shock causes the recent bullish euphoria in the markets to fade. Today, the economic implications of nCoV are only likely to complicate the current market backdrop.

Assuming the uncertainty surrounding nCoV is not reversed quickly, there is a potential that growth in the world’s second largest economy (China) could slow to a rate below current year estimates, contributing to broadly weaker global growth in 2020. This could happen if a further spread of the nCoV outbreak expands quarantine zones and halts economic activity across Chinese provinces as the movement of people and goods grinds to a halt.

What’s more, demand for goods and services globally are likely to fall as people stay home and consume less, impacting exports of goods and services in affected regions and slowing commerce between China and its key trade partners. For the U.S., such uncertainties are likely to only galvanize the willingness of business leaders to postpone discretionary hiring and spending this year. While it is still too soon to tell how the U.S. economy would be affected, the risks related to a U.S. recession are likely to increase in a scenario where global trade declines, business hiring and spending falls and consumers stay home. This leads us to our point about financial preparation.

Coronavirus: how to prepare financially

Without being overly alarmist, we believe that it is important for households to use current events surrounding the novel coronavirus as a reason to take a few steps to ensure financial preparedness as economic and market volatility rise in the coming weeks. This is important because as the economy slows, plentiful jobs may become harder to find when unemployment rises and the ability to borrow money becomes harder as banks tighten lending conditions. So, what steps can households take to increase their financial preparedness?

First, we recommend households look for ways to increase net cash flows. This includes reducing discretionary (or non-essential) spending and finding ways to advantageously use today’s low interest rate environment to refinance high-cost debts. We also suggest maxing out employer-matching retirement savings contributions, putting off big-ticket spending and using excess cash flows to build up emergency savings. We believe that these steps can better prepare households for unexpected life events, particularly as labor market conditions show signs of weakening in the coming months.

Figure 2: Strategies to help financially prepare for the unexpected

Second, for investors oriented towards asset growth, we recommend trimming exposure to higher-beta, lower quality investments and broadly ensuring that aggregate portfolio holdings across all investment accounts reflect long-term goals. While volatility exposes risks in the markets, it is also likely to present opportunities. And this is one reason why we believe that investors should rebalance portfolios, not only to align allocations with long-term goals, but also to generate cash that can be deployed opportunistically as market volatility creates favorable buying prospects.

Finally, for households preparing to take distributions from their investment, we recommend rebalancing accounts to long-term investment objectives and reduce unnecessary risk taking. As we pointed out last week, we investors can increase overall returns (without increasing risks) by trimming unnecessary expenses in their portfolios. Further, we recommend ensuring that cash positions are adequate to meet 6-12 months of living expenses. This is intended to avoid forced selling at depressed prices when market volatility increases.

How to Stay Sane when the Markets are Going Crazy

Let’s face it, no one wants to be the one person that missed out on what seems to be a once-in-a-generation investment opportunity simply because you’re trying to do the right thing. This decision is especially difficult at a time when making money in the markets seems so easy. Without a doubt, the fear of missing out on a great opportunity is so powerful that in the past it had encouraged otherwise rationale investors to put money into worthless tech companies in 2000 and prompted hairdressers in Florida during the housing boom to purchase three or four rental homes they just couldn’t afford. Even so, as Jeremy Grantham puts it, “there’s nothing more irritating than seeing your neighbors get rich.”

There’s no doubt that, in certain segments of the markets today, individuals are experiencing phenomenal returns in their holdings of tech, bitcoin, penny stocks and by participating in the options market. For example, the NASDAQ 100 index gained 96 percent from the market bottom in March 2020. Bitcoin, also, has gone from a price of $8,880 twelve months ago to well over $34,000. Names of penny stock companies (stocks that trade for less than $5 per share) have doubled or even trebled in a matter of weeks and months and now account for a growing share of trading activity. With results like this, it’s hard not to feel like you’re missing out on something spectacular when you’re watching from the sidelines.