Let the good times roll: the beginning of the end?

Stock market prices continued to grind higher as economic data releases surprised to the upside this week. Indeed, a host of indicators suggest to some that growth in the U.S. may in fact be improving after a softer showing in 2019 which has supported a rally in risk assets not just in the U.S. but globally this year. A key question for investors and savers now, however, is whether the good times are just getting started or the data mark the beginning of the end of good economic times.

We have argued that 2020 is likely to mark the beginning of the end for U.S. economic buoyancy and financial market resilience. Indeed, longer term indicators point to a rising risk of economic and market disappointment this year with recession related risks remaining elevated and not decreasing even as Fed policymakers would otherwise like people to believe.

What this means is that households should increasingly prepare for higher levels of economic and market volatility in 2020. This includes taking efforts to increase net positive cash flows, building up emergency reserves, rebalancing investment risk exposures and generating cash in investment portfolios to cover an extended period of retirement living expenses as market volatility increases.

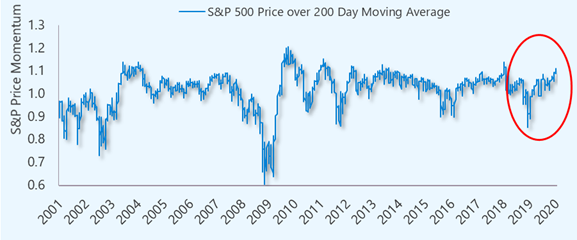

Figure 1: Market momentum near 2-year high

Why so glum?

Key data releases hailed by the financial markets this week included seemingly robust retail sales and housing market data. The reports pointed to generally better than expected activity in December and capped a strong finish to an otherwise lackluster year for both sectors. Indeed, government data showed that December retail sales grew at its fastest year-over-year pace (+5.8%) since August 2018. This compares to a meager 1.6% rate in December 2018 and contrasts a period of general economic malaise in the fourth quarter of 2018.

Similarly, reports on building permits, housing starts, mortgage applications and builder confidence all trended higher in the month of December, pointing to a rebound in housing market activity. Building permits, for example, were up 11.4% year-over-year at the end of the fourth quarter of 2019 compared to a decline of -1.8% in 2018. What’s more, builder sentiment rose to its highest level in over 20 years as mortgage rates remained low all the while December UofM Michigan Consumer Sentiment rose to its highest level since May 2019. Taken together, these developments have given financial markets a reason to keep pushing higher this year.

To be sure, market participants have been heartened by the seemingly positive economic data and the S&P 500 is now up over 3% in January, making new all-time highs in 10 out of the first 12 trading days of the year. Year-to-date, riskier international equities are in some cases outpacing the U.S. with China up 5%, Mexico up 6% and Turkey up 7.3%. These developments come even after the threat of war between Iran and the U.S. and ongoing impeachment proceedings on Capitol Hill. So why are we so pessimistic on the market and economic outlook?

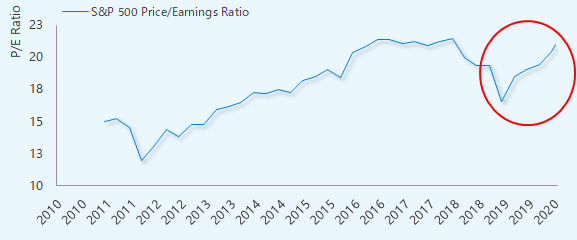

Figure 2: Stretched equity market valuations

No so fast...

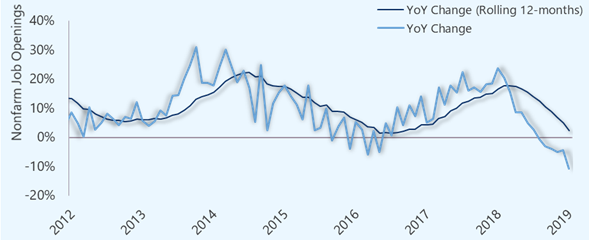

While it is tempting to extrapolate positive near-term developments into the future, the truth is that cyclical factors that we track suggest that economic and market conditions may be more fragile than the recent historical data suggest. Take, for example, the latest labor market data. While December payrolls bested estimates, the trend in new job growth remains biased to the downside. This is evidenced in the latest nonfarm job openings data, an important leading indicator of labor market developments. To be sure, the rate of employers putting out ads to hire new workers declined -10.8% in November and is on track for their worst rolling 12-month pace of growth since 2017.

This is important because, if labor market conditions continue to deteriorate, and business sentiment weakens as our projections suggest, then growth in the U.S. economy is likely to remain weak in the first half of 2020. Such a development would put downward pressure on corporate revenues, leading to earnings disappointments in the year and giving market participants a reason to step back from their expensive positions in stocks. What’s more, a continued decline in labor market conditions, weaker economic sentiment and increased financial system instability could lead to a rising risk of a U.S. recession in 2020.

Figure 3: Labor market conditions waning

Juicing the markets

To be sure, equity prices have been on a tear since the Federal Reserve quietly restarted its asset purchase program, increasing the size of its balance sheet by 11% since August 2019 even as Chairman Powell asserts that the Fed has not restarted quantitative easing (QE). Better near-term economic data aside, this form of money printing has arguably boosted risk asset prices all the while corporate earnings growth has slowed and the economic outlook remains weak.

The effect of central bank supported rising prices and stagnant earnings growth has contributed to stretched valuations in the equity market. In other words, U.S. stocks, as measured by the S&P 500 are now more expensive than they have been in the past two years when measured by its trailing and forward-looking P/E ratio. And these stretched valuation measures have also been showing up in other parts of the equity market, particularly in the growth style of large, mid and small cap U.S. stocks as a whole.

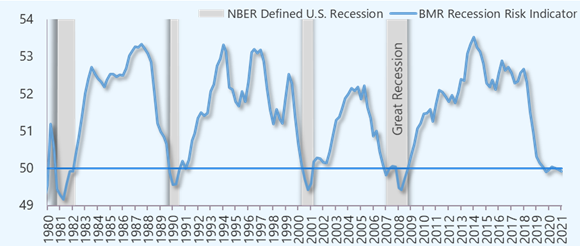

Figure 4: Recession risks remain elevated

Preparing for economic and market uncertainties

The fact that risk asset prices continue to push higher even as geopolitical risks linger and economic fundamentals remain subdued has given us reason for pause. To be sure, we believe that the current rally in risk assets has more to do with the Fed’s unsustainable easy money policies which could set the stage for a pullback in prices this year. While central bank asset purchases have been supportive of lower borrowing rates and provided a near-term boost to housing market sentiment, we are hard pressed to find positive catalysts that would support a sharp economic rebound this year and hence underpin the financial market rally.

In fact, we believe that global easy money policies have contributed to systemic excesses, and are providing a lifeline to firms that otherwise should no longer be in business. History has shown that such excesses do not continue in perpetuity, and when combined with our latest business cycle work, suggest that risk of an economic downturn and heightened market volatility is likely to increase this year. Taken together, we believe that recent market exuberance could be marking the beginning of the end to this economic and market cycle.

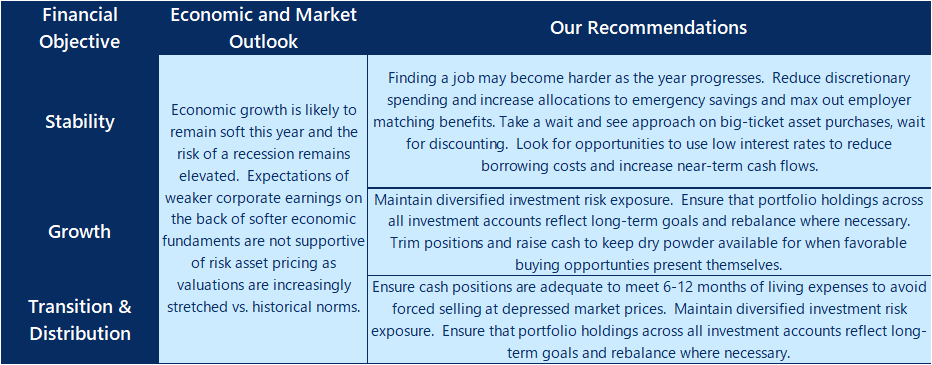

With the economic outlook set to weaken this year and financial market volatility likely on the rise, we recommend households take some constructive steps to remain prepared for the unexpected. First, we recommend households take a step back and reevaluate the vision and purpose for their money as they look ahead into 2020 and beyond and determine whether their plans are in alignment with current economic and market conditions.

Next, we recommend preparing for rising uncertainties by increasing net cash flows by reducing discretionary spending and finding ways to refinance debts given today’s lower interest rate environment. We also suggest reevaluating big ticket spending decisions, topping off emergency savings and ensuring employer-matching contributions are maxed out. We believe that these steps will better prepare households for unexpected life events, particularly as labor market conditions show signs of weakening in the coming months.

For investors oriented towards asset growth, we recommend maintaining a diversified investment exposure and stepping back from riskier investments. Further, households would be best served by ensuring that aggregate portfolio holdings across all investment accounts are in alignment with their long-term goals. This includes rebalancing portfolios to target allocations and trimming winning positions to raise cash to keep as dry powder for when market volatility creates favorable buying opportunities.

Finally, for households taking distributions from investment, we recommend rebalancing accounts to long-term investment objectives and reduce unnecessary risk taking. Further, we recommend ensuring that cash positions are adequate to meet 6-12 months of living expenses. This is intended to avoid forced selling at depressed prices when market volatility increases.

Figure 5: Preparing for the unexpected

Is now the right time to get into the markets?

With risk assets having pushed into bear market territory in May, some investors are asking whether now is the right time to get into the markets. On one side of this debate is a group of investors who look at the recent pullback as an opportunity to buy securities at a discount. On the other side is a set of investors concerned that prices will only move lower from here. Make no mistake, this question is relevant to investors today not only because of the magnitude but also because of the breadth of recent market declines.

For example, if we consider year-to-date performance for the S&P 500 index, what we find is that the first one hundred days of this year's market performance have been brutal. Indeed, through the end of May, the data show that U.S. Large Cap stocks have had their worst year-to-date decline in the past forty years. Adding insult to injury, investors have had little place to hide given the fact that stocks and bonds across U.S. and international asset classes have all posted losses this year.

So, why are markets selling off across the board? Well, the reasons behind this seemingly correlated selloff across major asset classes are manifold. But at its core, persistently high inflation and the prospects for an impending U.S. recession given ongoing logistics issues, healthcare concerns, and the war in Eastern Europe have made market participants more sensitive to the effects of less favorable central bank policy and the weaker corporate earnings outlook.

Now, in the past, market participants could look to policymakers to bolster the economy and markets when similar weak or uncertain macroeconomic conditions were present as they did back in 2020. But today, that story has changed. With headline inflation well above 8% this year, Federal Reserve policymakers are keen to continue raising interest rates, even if that means forcing the U.S. economy into a recession.

At the same time, businesses likely will find it increasingly challenging to keep passing along rising prices to consumers as wage growth has failed to keep up with inflation and household pocketbooks become increasingly stretched.

With the economic backdrop poised to weaken, and asset prices declining across the board, is now the right time to get into the markets? Well, with market sentiment being driven by the macro narrative, it can be argued that current economic conditions depend on many factors for which we yet have little clarity. For example, can the world avoid massive food shortages this year and next with a war raging in Ukraine? And, has inflation peaked, and if so, when will it stabilize enough for the Fed to stop pushing borrowing costs higher and higher?

While the answers to these questions are debatable, what is clear is that market participants have a host of broad-based macroeconomic concerns that still need to be worked out. And from this perspective, the prospect of continued volatility across asset classes suggests that timing market entry points (whether that's buying at a discount or avoiding the markets altogether) may be challenging for even the most seasoned investors.

Therefore, in the current environment, we believe that the question investors should be most concerned about is not how to time the markets but rather whether they have an investment process in place to withstand this period of heightened market uncertainty.

Missing the best days in the markets

Indeed, some investors may be enticed to use timing techniques or other short-term strategies in a bid to boost overall returns or to avoid losses completely. Such approaches involve exiting risk assets in anticipation of market moves lower and ratcheting risk back up as market sentiment improves. While such an approach sounds reasonable, getting the timing wrong could be more costly than beneficial.

How so?

Well, one analysis shows that over a 20-year period, missing even the 10-best days in the market would have led to returns of more than half the rate of those made by investors who stayed committed to the markets during up and down periods.

How is this possible?

Well, history shows that some of the best days in the markets typically follow the worst selloffs. This insight means that investors who had taken money out of the market in fear of a move lower could miss the beginning of a long-term rally. This reality was evident as recently as the COVID-induced market pullback in early 2020 and the subsequent risk asset rally through the end of 2021.

So, what's the point?

Well, unless you have the time, inclination, and experience, getting the timing right on a trade in your portfolio because you're debating whether you should (or shouldn't) get into the markets may cost you more than it is ultimately worth over the long run.

Finding the winning trade

This timing discussion also raises the question about trying to spot winning and losing trades. This attempt to time the market is especially tempting when yesterday's winners are beaten down and appear to be deep value opportunities or a bargain-buy.

Another temptation during the market selloff is chasing what appear to be winning asset classes and avoiding those asset classes that appear to be losing trades. The problem with trying to separate winners from losers, notably during a time of heightened market volatility, is that investor sentiment can shift on a dime, leaving many a portfolio in disarray.

Indeed, some data show that today's best-performing asset class could be tomorrow's laggard and vice versa.

What's more, the variability between stocks and bonds and even domiciles like the U.S. versus international investments tend to vary in performance from one year to the next. That's why an investment portfolio utilizing a diversified asset allocation framework and rebalanced at regular intervals tends to perform more consistently and avoids the wide swings associated with staking a claim in any one asset class. This finding leads us to our final point: a systematic investment process can add more value over time than trying to time the markets.

A systematic process for navigating market uncertainty

To be sure, even some of the best asset managers have had a hard time beating the markets over the past decade, which underscores the importance of a solid investment process. What do we mean by investment process? Simply put, we suggest 1) choosing the right mix of assets for a portfolio that aligns with an investor's risk tolerances and objectives, 2) putting money to work in the markets in a disciplined manner, 3) rebalancing portfolios at regular intervals, and 4) finally having a cash management process in place.

Diversify your portfolio

Now, a systematic investment process begins with understanding your own tolerance for risk and adding a set of assets to an investment portfolio that that vary with your overall goals and objectives. What does this look like? Well, for investors with a low tolerance for market swings and a near-term need for access to their assets, a conservative allocation would likely reflect a bias toward more bonds and less stocks.

On the other hand, a more aggressive asset allocation framework could be appropriate for investors who can tolerate wide swings in the markets and have a longer investment horizon. Either way, a solid investment process begins with understanding your preference for risk and your overall investment horizon.

Dollar-cost averaging

The next part of the systematic investment process involves being disciplined with committing capital to an investment portfolio at regular intervals. As we pointed out earlier, trying to time the best and worst days of the markets might have an adverse effect on overall investment performance. To avoid such issues, we recommend dollar cost averaging, or more simply, committing a set sum of money to your investment portfolio on a regular basis.

What does this look like?

If you participate in an employer-sponsored retirement plan, this could involve setting up automatic payroll deductions and having capital committed to your portfolio every pay period regardless of market conditions. Or, a similar approach can be used for after-tax contributions or lump-sum transfers by scheduling cash allocations to your IRA or taxable investment account on a pre-defined schedule. Either way, putting capital to work at set intervals can help reduce cognitive load, simplify decision-making during periods of market volatility and keep your savings goals on track.

Rebalance your portfolio

Another step in the systematic investment process is portfolio rebalancing. Now, rebalancing is essential because, over time, the values of various assets within a portfolio will drift away from their initial allocations as markets move up and down. The purpose, then, of rebalancing is to realign portfolio holdings with their target allocations.

So, when should you rebalance?

Rebalancing can occur 1) on a set schedule, 2) when asset values drift by a certain threshold, or 3) in a combination of the two. For example, rebalancing on a set schedule could involve evaluating portfolio holdings quarterly, partially selling positions that have appreciated, and adding to allocations that have underperformed during that period.

Alternatively, using a threshold to rebalance could involve using a decision rule that prompts a rebalance only when the value of a specific asset class is a set percentage above or below its target allocation. This process could lead to less frequent rebalancing during flat markets but more rebalancing during periods of heightened market volatility.

Cash Management

Finally, if you're in the distribution phase of your investment journey, or in other words, dependent on your savings to pay for your living expenses, then cash management is essential for navigating market volatility without missing out on the best days in the market.

Now, a solid cash management technique ensures that you have access to enough liquid assets in your retirement portfolio to cover between 12-18 months of living expenses. Such investments can include money market mutual funds, and the purpose of this approach is to give your savings enough of a runway to avoid having to sell assets at an inopportune time when the markets begin to sell-off.

Bottom line

When it comes down to it, asking whether now is the time to get into the markets often misses the point of what it means to be a long-term investor. To be sure, trying to time the markets and hoping to find the next "fat pitch" or winning trade are demeanors often associated with speculative behavior. And, as we have pointed out earlier, such behavior can lead to unfavorable investment outcomes over the long term.

That's why during times like the present, we challenge investors to ask themselves whether the decisions they are making are aligned with a systematic investment process. This approach includes committing to a target asset allocation framework, deploying capital to the markets in a disciplined manner, rebalancing as appropriate, and having a solid cash management process in place.

Whether you're looking to buy securities at a discount or avoid losses altogether, there's rarely a right time to get into the markets. Nevertheless, we believe that staying committed to a disciplined investment process and using techniques to manage uncertainty during periods of heightened market volatility could help you increase the odds of achieving your lifestyle goals regardless of market conditions and keep you on track to mastering your financial independence journey.