Revitalize Your Retirement Savings with a Mid-Year Checkup

Making regular contributions to an employer-sponsored plan can supercharge your journey to financial independence.

But, you already knew that, right?

And, you likely already know about the benefits of "free money" that you could receive from your employer match and how pre-tax contributions to a qualified retirement account like a 401k, 403b or other employer-sponsored account can give your financial independence savings goals a major boost.

But, did you know that there are things you need to do periodically throughout the year besides putting money into your employer-sponsored plan to ensure that your financial independence goals are on the right track?

To be sure, some of you may be asking yourself, "isn't contributing to a 401k, 403b, or other employer-sponsored plan account enough to secure my retirement?

Well, the short answer is: no.

That's because getting money into a retirement account is a crucial first step toward securing your path to financial freedom, but it's not the only step.

Indeed, throughout the year, there are some specific actions that you should take to 1) ensure that you're putting your money to work in the most efficient way possible, 2) that you're not taking more risk than necessary, and 3) that you're not leaving any money on the table.

So then, with the mid-year upon us, there's no better time than the present to log into your employer plan website and follow along as we review key factors that can help or hinder your financial independence goals.

Check Your Asset Allocation

According to various studies out there, asset allocation is one of the most crucial decisions you can make when it comes to growing and preserving your retirement savings for the long-term. And to put it simply, asset allocation refers to the mix between stocks, bonds, and real estate held in your portfolio.

Now, when we think of asset allocation, we tend to think of it in terms of aggressive versus conservative. And what do we mean here?

And an aggressive asset allocation could hold a higher weighting to stocks, while a more conservative portfolio holds more bonds. Aggressive allocations tend to take more risk, but also tend to get higher returns over the long-run. On the other hand, a conservative portfolio tends to take less risk, but also receives a lower return over the long-term.

To be sure, growing and preserving your savings has less to do with timing the markets or choosing the best performing security or mutual fund. Rather, it has to do with ensuring that you’re putting your money to work in a way that matches your risk tolerance, investment goals and time horizon.

The Risk of Being too Conservative

And why does this matter? Well, let’s assume that you’re still saving for retirement and have about 15 years to go before you’re ready to walk away from your job. If your asset allocation is too conservative, meaning that you’re not taking enough risk, you could end up saving less than you had initially planned.

For example, let’s assume that you have half a million dollars saved in your employer sponsored plan. We’ll also assume that you’re maxing out your contributions, and, to simplify our illustration, we’ll leave out any employer matching for the time being. If you have an aggressive investment profile, you could assume to expect to receive an investment return of around 6.5% under normal circumstances. Given this set of assumptions, your portfolio could grow to $1.9 million by the time you’re ready to walk away from your job.

Alright, so far, so good, right? Well, what happens if we keep all of the assumptions the same, but this time, we change the return assumption to be more consistent with a conservative investment portfolio that is expected to return 3.5% annually over the long term. Well, in this case, your portfolio would still grow, but at the end of 15 years, you’d have $1.3 million saved, which is nearly half a million dollars less than in the aggressive asset allocation profile!

This illustration shows how essential it is to ensure that your asset allocation aligns with your tolerance, goals and time horizon. And the truth is that, all too often, individuals who have the room to take more aggressive stances in their retirement portfolios play it too safe, which ends up costing them over the long-run.

So then, if you have well over a decade before you need to begin drawing down on your savings, you may want to take a moment to ensure that you’re not being too conservative with your asset allocation.

The Risk of Being too Aggressive

Another critical moment to check your investment allocation is if you’re five or fewer years away from needing to take distributions from your retirement savings. And why’s that? Well, what we’re trying to do is get ahead of what we call sequence of return risk. Now, sequence of returns risk is particularly important to individuals who are less than five years away from retirement because it directly impacts the value of your retirement savings during a critical period.

Here again, this risk refers to the order and timing of investment returns, which can significantly affect the overall portfolio performance and the sustainability of retirement income. In fact, here's why sequence of returns risk is of concern to individuals nearing retirement.

First, when you’re transitioning to retirement, you’ll typically start relying on your investment portfolios to provide regular income. Now, if there's a sequence of poor investment returns early in retirement, it can deplete your portfolio faster than expected, leaving fewer funds available for the remainder of your retirement. This situation is particularly detrimental because, if you choose not to return to work, you’ll likely have limited time to recover from significant losses.

Next, if you’re approaching retirement, you have a shorter time frame to replenish your savings compared to those who are earlier in their careers. So then, if you experience a series of negative investment returns just before or during retirement, you may not have the opportunity to recover those losses through additional savings or a prolonged investment horizon.

That’s because the compounding effect of investment returns becomes less impactful as your retirement approaches. In fact, even small losses in the final years leading up to your retirement can have a substantial impact on your overall retirement nest egg, as there is less time for the compounding effect to work in your favor.

Now, another point to consider is that, as you’re nearing retirement, you may have already made decisions about your retirement income strategy, such as setting up systematic withdrawals. Now, if poor investment returns coincide with the initiation of these income streams, the negative impact can be long-lasting, potentially leading to lower income throughout retirement.

Indeed, the impact of sequence of returns risk is more pronounced for if you’re close to retirement because you have fewer years to recover from a market downturn. Again, a significant loss in the final years before retirement may force you to delay retirement or make drastic adjustments to your planned lifestyle.

So how do you get around this? Well, again, this is where your asset allocation strategy comes into play. And at this point, you may want to consider gradually shifting towards a more conservative investment allocation to minimize the potential impact of market volatility. And you’ll also want to take a second look at your comprehensive financial plan to help you manage your savings effectively during the transition into retirement.

Regardless of whether you’re in the accumulation stage and have years to save, or nearing the distribution stage and are preparing to draw down on your savings in just a few short years, the first thing you’ll want to do as you’re reviewing your employer-sponsored savings plan is ensure that your investment holdings align with your overall asset allocation decisions.

Choosing the Right Investments

Alright, now that you have a good understanding of why it’s essential to know how much you should have allocated between various asset classes, let’s talk about where you should be putting your money to work.

The fortunate thing is that in a world of tens of thousands of investment options, your employer sponsored plan may limit your available investment options to less than a few dozen choices. Now, while its’s arguable whether this limitation is a good thing or not, it does reduce the analysis paralysis aspect of putting your money to work once you’ve identified your ideal asset allocation framework.

Asset Class Purity

So, where should you start when it comes to evaluating your investment options? Well, first things first, take time to ensure that the funds held in your retirement savings account align with the asset classes defined in your asset allocation strategy.

For example, let’s say that your goal is to allocate a quarter of your retirement savings to large cap stocks. And let’s also say that your employer has given you the option of a Total Stock Market Index Fund and an S&P 500 Index fund. Which should you go with? Well, if you decided to choose the total stock market fund, you would not only gain exposure to large cap stocks, but also to mid and small caps at the same time.

Now, while this may not seem like a big deal on the surface, the point here is that if you’re serious about adhering to a disciplined asset allocation approach, then you need to choose funds whose investment profiles match the asset class that you’re selecting them for. We call this using asset class purity.

Now, when you, select funds that are "asset class pure," it means that you choose funds that focus exclusively on a specific asset class or category. Here again, asset classes refer to different types of investments, such as stocks, bonds, real estate, commodities, or cash equivalents.

By opting for asset class pure funds, your aim is to maintain concentrated exposure to a particular asset class, rather than investing in a diversified fund that includes multiple asset classes. This approach allows for a targeted investment strategy and can be beneficial if you have a strong conviction about a specific asset class or want to align your investment choices with a particular investment theme or strategy.

For example, if you believe that the stock market will outperform other asset classes in the near future, you may choose to allocate funds exclusively to equity-focused funds, which primarily invest in stocks. By doing so, you concentrate your investments in a single asset class, potentially maximizing returns if your prediction proves accurate.

Now, it's important to note that investing in asset class pure funds carries certain risks because when your portfolio is concentrated in a single asset class, it may be more susceptible to fluctuations and volatility specific to that asset class. And that’s why diversification across multiple asset classes is a common strategy to mitigate risk and smooth out investment performance over time. Therefore, selecting asset class pure funds should be carefully considered and aligned with your risk tolerance, investment objectives, and overall portfolio diversification strategy.

Now, if you’re not sure which asset class a particular fund tracks, you can always look up the benchmark that the fund is measuring itself against in the fund prospectus, or you can go online and use a tool like Morningstar.com to evaluate the asset class style for that particular fund.

Fees and Expenses

Another point to take into consideration when choosing which funds to hold in your retirement account is fees and expenses. Here again it comes back down to the old adage of it’s not how much you make, but how much you keep.

Now, not all employer sponsored retirement plans are created alike. Therefore, the fees and expenses you’re likely to pay will vary depending on your program, but the three main expenses you’ll want to pay attention to are individual service fees, administration fees and investment fees.

Of these fees, you’ll want to pay particular attention to the investment fees related to your fund holdings. And why do investment fees matter? Well, let’s assume for a moment that you’re considering three funds that track large cap stocks, and they all seem like reasonable investments.

Now, if you’re not paying attention, you could be giving away much more of your investment returns in the form of fees than you expected. Indeed, depending on your situation, investment fees in your employer sponsored retirement account can range between 0.5% to 2.0% per year!

Now, at face value, this might not seem like a lot, but a half percent difference on a half million dollar portfolio invested over 15 years could mean forgoing over $100,000. And in the case where the fee is 2% for a given fund, that could cost you well over $400,000 in potential returns. That’s why, when you’re choosing between various fund options, your best bet is to go with the fund that is the lower cost option given your specific asset class constraints.

Putting Away Enough Money

Alright, now that you’ve ensure that you’ve dialed in your asset allocation decisions to your risk tolerance, and have chosen low-cost, asset class pure investments to go along with those allocations, one last thing that you’ll want to do is to ensure that you’re setting aside enough money in your retirement account.

But, now, how much is enough? Well, because everyone’s situation is unique and there is no one right answer, here are some general guidelines to consider as you go about putting your money to work:

Take Advantage of Your Employer Match

First, many employers offer to match a percentage of your 401k contributions up to a certain limit. And in many ways, when your employer matches your contribution, it's essentially free money being added to your retirement savings.

In fact, this is an immediate return on your investment, which is something few other investment opportunities can offer. And is a sense, not taking advantage of this match would be like turning down a pay raise.

What’s more, the employer match can accelerate the growth of your retirement savings. That’s because this extra contribution not only increases the principal amount being invested but also compounds over time, which could significantly increase the total amount you have saved by the time you retire.

Again, what we’re talking about here is essentially free money and provides an immediate return on your investment. That’s why if your employer provides this benefit, you should consider contributing at least up to the maximum matching limit.

Balanced Contribution Amount

Next, it's crucial to strike a balance between saving for the future and maintaining a reasonable quality of life in the present. That’s because your ability to contribute to your retirement savings account will be influenced by your current income and your ongoing living expenses.

Now, as it stands today, the contribution limit for employees who participate in 401k, 403b, and other employer sponsored plans is $22,500. And if you’re over the age of 50, you have an option to drop in another $7,500 annually as a catch-up contribution.

So then, as you go about considering how much to contribute to your employer sponsored plan, maxing out your contributions should be your priority in most cases. That’s because most contributions to employer sponsored plans are made on a pre-tax basis, which allows you to put more of your money to work before Uncle Sam gets his fair share of your earnings.

Targeted to Your Retirement Goals

Alright, so as you’re evaluating your contributions, if you’re making the bare minimum to take advantage of your employer’s match, but not willing to max out your pre-tax contributions, then what should your do to find the right balance?

Well, if you find yourself in this situation, then your likely focus should be on setting aside enough money to cover your projected lifestyle expenses in retirement. Here again, how much you need to save will largely depend on the kind of retirement lifestyle you want. That’s why you should consider factors like where you want to live, what kind of activities you want to participate in, and potential healthcare costs.

Now, in previous posts, we spent some time discussing how to use exponential returns to calculate your retirement need. But if don’t have a financial plan and are looking for a quick and easy way to figure out your savings need, then online calculators and retirement planning tools can help you estimate how much you'll need to save to meet your retirement goals.

Consider Auto Escalation

Now, as you’re going about reviewing your employer-sponsored plan, another option to consider is setting up your plan contributions to automatically rise each year as you earn more money. Now, automatically increasing your contribution each year is often called "auto-escalation," which could work in your favor in several ways. For starters, it's a straightforward and effortless method to regularly boost your savings.

To be sure, since the contribution increases happen automatically, you don't have to remember to make the adjustments yourself every year, which means there's less chance you'll forget or keep delaying it.

Another benefit to consider is that as your salary grows over time, there's a tendency for spending to increase along with it. This is known as "lifestyle inflation." If you're automatically increasing your contributions every year, you're effectively channeling some of the extra income that might have gone into spending, into your savings instead.

And, naturally, by contributing more to your employer-sponsored plan, you're speeding up the growth of your retirement savings. Indeed, every incremental increase in your yearly contribution accelerates this process, potentially allowing you to reach your retirement savings goal much sooner than expected.

The bottom line is that while these annual increases might seem insignificant in the short term, they can significantly impact your total savings over time, thanks to the power of compounding.

Either way, as you’re reviewing your employer sponsored plan, you’ll want to make sure that you’re contributing enough to take advantage of your employer’s match. And, if you can, max out your pre-tax contributions to enable your savings to grow for maximum effort. And, when possible, turn on auto-escalation within your plan to make higher contributions much more effortless.

Revitalize Your Retirement Savings with a Mid-Year Checkup

No matter where you are in your journey to financial independence, ensuring that your retirement savings are on the right track requires more than just contributing to an employer-sponsored plan. While it is a crucial first step, there are additional measures you need to take on a regular basis to maximize the efficiency of your savings and minimize unnecessary risks.

Indeed, when it comes down to it, managing your employer-sponsored retirement account involves three key aspects. First, you should assess your asset allocation to align it with your risk tolerance, investment goals, and time horizon. This will help you strike the right balance between risk and return, ensuring your savings grow optimally.

Second, carefully evaluate the investment options available within your retirement account. Consider the concept of asset class purity, selecting funds that correspond to your desired asset classes. By doing so, you maintain a focused investment strategy and potentially capitalize on specific asset class performance.

Additionally, pay close attention to fees and expenses associated with your fund holdings. Even seemingly small differences in fees can significantly impact your long-term returns. That’s why, when you can, opt for lower-cost options that align with your asset allocation decisions to preserve more of your investment returns.

Lastly, make sure you're contributing enough to your retirement account. Take advantage of any employer match offered, as it is essentially free money that can boost your savings. Strive to maximize your pre-tax contributions and consider utilizing auto-escalation to gradually increase your savings over time. By finding the right balance between saving for the future and your current lifestyle, you can ensure a more secure retirement over the long run.

And by addressing asset allocation alignment, investment selection, fee management, and contributions you can ensure that you’re taking one step closer to becoming the master of your own financial independence journey.

Is Income a Missing Component to Securing Your Financial Independence?

The old adage, “it’s not about how much you make, but how much you keep…” is often applied to the concept of spending and saving prudently. But, what if spending wisely and prudently managing your savings was just a part of securing your path to financial independence?

Make no mistake, managing your cash flows is essential to mastering your path to financial independence. That’s because without a firm grasp of this critical process, having the money you need to accomplish your life goals likely just won't happen.

However, maximizing your take-home pay is another essential financial planning task often overlooked by many individuals.

Indeed, whether you’re still in your earning years or already retired, many individuals, whether their income comes from a paycheck or savings distributions, end up leaving thousands of dollars on the table each year.

So, what are some ways to increase your take-home cash flows?

Well, one way to increase your income is to pay no more tax than necessary.

That's why it's vital to have a plan in place to ensure that you take advantage of all the tax savings opportunities available to you while paying yourself first, as you make smart financial decisions from one month to the next.

Maximize Employer Retirement Plan

One of the most advantageous ways to minimize your taxes is to maximize your pre-tax retirement savings contributions to an employer-sponsored plan. That's because the money contributed to these accounts goes in on a pre-tax basis or before taxes are taken out.

Compared to after-tax contributions, this approach maximizes the amount of money that can grow in your savings over the long term.

For example, let's assume for a moment that your current employer-sponsored retirement account has $250,000 in it. Then each year, you contribute $20,000 to your account on a pre-tax basis that earns 6% annually. At the end of ten years, your portfolio could have grown to $730,000 when making pre-tax contributions.

Now, let's assume for a moment that you made those same contributions on an after-tax basis. Assuming an effective tax rate of 30%, this time around, you’ll only be able to contribute $14,000 after Uncle Sam gets his fair share of your income. Using the same assumptions as before, at the end of ten years, you'd likely have saved around $650,000.

That's a difference of $80,000 just by making a simple choice to prioritize pre-tax versus after-tax contributions. And keep in mind that this difference could be even larger if your employer offers matching contributions to your employer-sponsored plan.

Now, some individuals will set aside some money to their 401k or 403b and then make additional contributions to their IRA, hoping to get an extra tax break. The issue here is that if you're not maxing out your 401k before your IRA, you're likely only getting a fraction of the tax benefit compared to prioritizing all of your contributions on a pre-tax basis.

This is especially the case for high-earning households, as the tax deductibility of IRA contributions is phased out over certain income limits. In contrast, 401k contributions are only limited by the annual amount you can put in, making them a no-brainer choice when it comes to tax-advantaged savings options.

Create Your Own Retirement Plan

Now, for those of you out there who are self-employed or running a small business and maxing out IRA contributions, consider setting up your own employer-sponsored retirement savings plan. While the thought of setting up your own retirement plan can seem onerous, there are straightforward options available that would allow you to make tax-advantaged contributions.

For example, if you're relying on an IRA to fund your retirement savings, then you're missing out on a big opportunity.

For example, options like a Solo 401k, SIMPLE, or SEP IRA allow you to contribute multiples more than an IRA on a tax-advantaged basis and help reduce your overall tax burden. Which one is right for you will come down to the structure of your business. And when it comes to administration, many custodians today make it easy to manage a retirement plan for your business without having to deal with all of the administrative red tape.

Adjust Your W4

Another way to increase your take-home pay is to adjust how much tax is withheld from each paycheck. This approach may be more relevant if you receive a tax refund from one year to the next. Remember, while a refund may seem like a windfall when you receive it, at the end of the day, it's an interest-free loan that you're making to Uncle Sam throughout the course of the year.

To this point, to reduce your odds of a tax refund and increase the amount of cash available to you each pay period, you'll want to adjust your withholding exemptions through form W4. By lowering your exemptions, you can reduce how much money is withheld from your paycheck. Now, before you go out and begin changing your exemptions willy-nilly, be sure to check out the IRS's Tax Withholding Estimator.

This tool will help you get a gauge the ideal number of withholdings to elect on your W4. And when you're ready to make adjustments, be sure to reach out to your HR department or your payroll services provider to make the necessary adjustments.

Maximize Your Equity Compensation

Now, for you tech professionals out there, you'll likely receive incentive compensation in the form of stock options or restricted stock units (RSUs) as part of your total pay package. However, many tech professionals do not fully understand the value and potential of their equity compensation benefits, which can result in missed financial opportunities.

So, if you are the recipient of equity compensation, what are some things you should watch out for to maximize your income?

First, you'll need to understand that equity compensation is tied to your company's overall performance and can increase in value over time as your company grows and its stock price rises. If you're a tech professional who receives equity compensation and yet you're not paying attention to the details of your equity award, you may miss out on the opportunity to sell your stock at a higher price, potentially resulting in a significant financial loss.

Second, there may be restrictions or deadlines associated with equity compensation that you may need to be aware of. For example, RSUs typically vest over a period of time and may be subject to forfeiture if you leave your company before the vesting period is over. Stock options, like ISOs may also have expiration dates, meaning that they become worthless after a period of time. So staying on top of those vesting periods is essential.

Third, tax implications of equity compensation should also be considered. Tech professionals need to understand the tax implications of exercising stock options or selling RSUs, such as ordinary income tax on the difference between the exercise price and the stock price at the time of exercise, as well as potential capital gains tax on the sale of the stock.

Now, it's easy to leave your stock award aside and do nothing with it. That’s why you’ll likely benefit from last month’s discussion on equity compensation housekeeping. You can find resources in the FI|Mastery Journey to review best practices for managing your awards. But at the very least, get to know your equity award and check to make sure that you're taking advantage of opportunities where they're available.

Pre-tax Spending Needs

Another effective way to maximize your income is to pay for regular expenses on a pre-tax basis. A couple of tools available through your employer may include health savings accounts, or HSAs, and Flexible Spending Accounts, or FSAs.

If you have a high deductible health plan (HDHP), for example, HSAs allow you to make pre-tax contributions that can be later used to pay for medical expenses. This account type also has an investment component built into it that allows your savings to grow over the long term.

Another way to spend on a pre-tax basis is to utilize a Flexible Spending Account or FSA. These accounts are typically a use-it-or-lose-it type of account. And this means that any contribution you make during the course of the year must be spent, or you'll lose that money by the end of the year.

Even so, these types of accounts still offer some advantages.

For example, let's assume for a moment that you spend $10,000 per year on childcare expenses. If your employer offers a dependent care FSA, a household is allowed to contribute $5,000 annually to this account on a pre-tax basis. Assuming that your effective tax rate is 24%, your $5,000 gives you a savings of $1,500 annually on that contribution towards your childcare expenses that you may have otherwise paid for on an after-tax basis.

Review Your Employer's Group Life Coverage

Another way to keep more money in your pocket is to evaluate how you're paying for life insurance. Now, whether you have a family or are just getting started, life insurance is often a cheap way to transfer financial risk should something happen to you.

And if you have an individual life insurance policy but are not taking advantage of your employer's group policy, you may be paying more for that individual policy than what's available to you through your employer's group benefit.

Renegotiating Your Pay

Finally, consider asking your employer or clients for more money. This may include having an awkward conversation that could end up netting you a few extra thousand dollars per year. This approach could involve either asking for raise or negotiating an off-cycle increase in your incentive compensation, such as a bonus or off-cycle equity grant.

And if you're self-employed, now may be the time to evaluate the fees charged to your clients. Given the recent cost of living increases, now may be an opportune time to raise your prices to reflect the value of your services and rising overhead costs.

Increasing the take-home income component of your cash flows can help ensure that you achieve your spending and savings goals for the year. While earning more money is certainly one way to accomplish these goals, being more tax-efficient with your cash flows is a more controllable approach to bringing home more money from one pay period to the next.

Maximize Your Post-Employment Income

Now, if you've already achieved your financial independence goals and are living off retirement savings, then finding ways to maximize your take-home salary may seem less relevant to you.

Even so, while fine-tuning your earnings ability was a key consideration during your accumulation years, focusing on the income-producing capabilities of your savings nest egg will be essential to staying strong financially in retirement.

Now, while some rules of thumb will guide you on how much you should safely withdraw from your portfolio from one year to the next, the fact is that a disciplined investment process will be essential to preserving the value of your potential lifetime retirement income.

To this end, there are two approaches you should consider when it comes to maximizing the potential retirement income generated by your investment portfolio this year: 1) your investment strategy and 2) your cash management strategy.

Let's take a look at how ways you can maximize the income-producing ability of your retirement savings:

Diversify Your Investments

First, one of the most important steps you can take to maximize the sustainable income from your investment portfolio is to diversify your investments. To do this, ensure that you're spreading your assets across various types of investments, including stocks and bonds, US and international investment assets. This approach will help reduce your portfolio's overall risk and ensure a reliable income stream throughout your retirement.

Indeed, setting an appropriate mix of stocks and bonds, US and international assets, is essential for preserving the income-producing capabilities of your retirement savings. And the degree to which you allocate between various asset classes influences your investment rate of return.

For example, a larger allocation to historically riskier assets could generate a higher rate of return for your investment portfolio compared to allocations to typically conservative assets like government bonds.

So, how much should you contribute to each mix? Well, start by evaluating your risk tolerance and preparing your investment policy statement to find the right mix for you. This approach will be essential to crafting and sticking to a disciplined investment process in the years ahead.

Consider Passive Investment Strategies

Next, consider allocating your savings to passive investment strategies, such as exchange-traded index funds (or ETFs). These vehicles are often lower cost and easier to manage than actively managed portfolios. This can help you maximize the income from your investment portfolio by reducing the amount of money you need to spend on fees and expenses.

Consider Tax-Efficient Sources of Income

Another way to maximize the income from your investment portfolio involves understanding how that income is taxed. For example, capital gains, dividends, and interest income can all be taxed at different rates. Therefore, if your portfolio composition, or the allocation to a particular security or asset class, is heavily weighted towards taxable income, you could be giving away more of your income to Uncle Sam than necessary.

Therefore, one way to produce tax-efficient income for your portfolio is through munis. Municipal bonds, also known as munis, are debt securities issued by state or local governments to finance public projects such as infrastructure, schools, and hospitals.

In a retirement investment portfolio, municipal bonds can serve as a source of stable, tax-free income. Since the interest earned on munis is often exempt from federal and state taxes, they can be especially attractive for individuals in higher tax brackets who are looking for ways to reduce their tax liability.

Munis can also add diversification to a portfolio, as their performance is often uncorrelated with stocks and other bonds. However, it's essential to consider the credit risk of the issuer, as well as the market risks associated with bonds, before adding munis to a retirement portfolio.

Reduce Your Future Tax Liability

Another way to increase your retirement income is by reducing how much tax you're paying to Uncle Sam. To achieve this outcome, you'll want to evaluate the tax efficiency of your portfolio. If you expect your taxable income to rise after retirement, especially when required minimum distributions (or RMDs) kick in, consider ways to reduce your future tax liability.

In some cases, evaluating the benefit of a Roth Conversion might make sense. A Roth conversion is the process of moving money from a traditional individual retirement account (IRA) to a Roth IRA. By converting a traditional IRA to a Roth IRA, a retired individual may be able to reduce their future tax liabilities by establishing a source of tax-free withdrawals, reducing or eliminating RMDs, and generally putting them in a lower overall tax bracket.

Rebalance Your Portfolio Regularly

Another way to maximize income over the long-term is to potentially mitigate near-term losses in your portfolio through regular rebalancing. As markets fluctuate, your portfolio's asset allocation may change, which can impact the sustainable withdrawal rate you can generate from your investments. To avoid this, consider rebalancing your portfolio regularly to ensure that your desired asset allocation is maintained.

Consider Inflation-Protected Investments

Now, if you're reliant on your retirement savings to cover your living expenses, you'll need to be mindful of the effects of inflation. Inflation is a natural part of the economy, but over time it can erode the purchasing power of your investment portfolio. To combat this, consider whether investing in inflation-protected investments, such as Treasury Inflation-Protected Securities (TIPS), can help preserve your purchasing power over the long term.

Have an Adequate Cash Management Plan

And finally, another critical component to preserving your spending ability when drawing down assets is having an adequate cash management plan in place. This means having enough cash on hand within your portfolio to cover 12-18 months' worth of living expenses.

Why so much cash on hand?

Well, after a year like 2022 in the markets, the last thing that you want to be doing is selling securities in a down market to cover your living expenses.

Either way, finding ways to maximize your income from your investment portfolio is vital to ensuring that you don't go broke in your post-employment years.

Addressing this concern begins by having an investment strategy and mix of assets that fit your overall risk tolerance, goals, and objectives. Then, allocating to low-cost, tax-efficient investments likely will ensure that you're keeping more of your money by paying only what is necessary.

And finally, have a cash management plan in place may allow you to weather the ups and downs in the markets without having to sell securities at an inopportune time.

Pay Yourself First

Now that we've discussed ways to maximize your income, whether that's from earned income or retirement income, let's take a few minutes and explore the concept of paying yourself first.

So, what do we mean when we say to pay yourself first?

Well, we're talking about setting aside a portion of your monthly income for savings and investments before paying bills and spending on other expenses. This approach may help you prioritize your financial goals and build wealth over time.

Paying yourself first includes funding your cash management or emergency savings fund and allocating your money to suitable financial accounts.

How to Pay Yourself First

Now, a cash management or emergency savings fund is an essential component of a solid financial plan. It is a savings account that is set aside for unexpected expenses, such as a car repair, medical bill, or job loss. Indeed, having an emergency savings fund can provide peace of mind and financial security in times of crisis.

Evaluate Your Emergency Savings Target

So, how much should you have saved in your emergency savings fund?

Well, one rule of thumb is saving between 3-6 months of household living expenses. Depending on your situation, your financial planner will define this number for you as part of your specific financial plan. Either way, know your number and commit to it.

In terms of where to save that money, here are some options:

High-yield Savings Account

A high-yield savings account is a type of savings account that offers a higher interest rate than a traditional savings account. This means that your money will grow faster, and you will earn more interest over time.

Certificates of Deposit (CD)

A CD is a type of savings account that allows you to deposit money for a fixed period, typically from 3 months to 5 years. CDs usually offer a higher interest rate than savings accounts, but they also have penalties for early withdrawal.

Roth IRA

Roth IRA is a type of retirement account that allows you to invest money after tax, and withdrawals in retirement are tax-free. If you are young and in a low tax bracket, this might be a good option to consider.

Whichever account type you choose to leverage as your savings vehicle, it's always worth considering some best practices to maximize your emergency savings.

Order of Savings Operations

Now that we've talked about ways to fund your emergency savings, where should your money go when it comes to longer-term savings?

Make no mistake, it can be confusing to know which accounts to contribute to first and in what order. As you begin paying yourself, you should contribute to various retirement and taxable investment accounts that give you the most significant tax bang for your buck.

Employer-sponsored retirement plans

The first step in saving for retirement should be taking advantage of your employer-sponsored retirement plan, such as a 401(k) or 403(b) plan. These plans offer significant tax benefits, including the ability to contribute pre-tax dollars. Additionally, many employers provide matching contributions, which is free money and a 100% return on your retirement contributions.

IRA Accounts

After you have maximized your contributions to your employer-sponsored retirement plan, you should consider contributing to an individual retirement account (IRA). Traditional IRA contributions are tax-deductible, and the money grows tax-free until withdrawal. Roth IRA contributions are made with after-tax dollars, but withdrawals in retirement are tax-free.

Taxable Investment Accounts

Once you have maximized your contributions to your employer-sponsored retirement plan and your IRA, you can begin contributing to taxable investment accounts. These are investment accounts that are not tax-advantaged, such as a regular brokerage account. The benefit of these accounts is that you can withdraw money at any time without penalty.

Health Savings Account (HSA)

If you are enrolled in a high-deductible health plan, you may be able to open a Health Savings Account (HSA). The benefit of these types of accounts is that contributions to an HSA are typically made on a pre-tax basis, the money grows tax-free, and withdrawals for qualified medical expenses are also tax-free.

College Savings Plan

And if you have children, consider contributing to a college savings plan, such as a 529 plan. These plans offer some tax benefits including the ability to take tax-free withdrawals for qualified education expenses.

Now, it's important to note that some of these accounts have contribution limits, and it's essential to check the limits and rules to avoid penalties. Additionally, you should consider your overall financial situation and goals when deciding how much to contribute to each account.

Ultimately, the most important thing is to find an account that works for you, that you are comfortable with, and that you can access easily in case of emergency.

Setting up a savings plan, tracking your spending and cutting back on unnecessary expenses are all effective ways to build an emergency savings fund. Remember, it's never too late to start building your emergency savings fund, which is necessary to achieve financial stability.

The Missing Component to Achieving Financial Independence: Maximize Your Income

By taking steps like maximizing pre-tax retirement contributions, creating a self-employed retirement plan, and adjusting your W4, you can minimize your tax burden and in many cases maximize your income.

And the result is more money in your pockets and a secure financial future.

But it doesn't stop there. Maximizing the income from your investment portfolios is crucial for a strong and sustainable retirement. Diversifying our investments across stocks, bonds, US and international assets, and allocating your savings to passive investment strategies like index funds, can reduce overall portfolio risk and increase your retirement income. Plus, by finding tax-efficient sources of income, reducing future tax liabilities, and investing in inflation-protected investments, you can take control of our financial future.

But it all starts with a disciplined investment process, a deep understanding of the tax implications of your portfolios, and a careful consideration of all the factors that impact your retirement income. With the right strategies in place, financial independence is well within your reach.

Finally, the key to maximizing your income is to avoid letting it be diverted to the inevitable financial setback. By establishing a solid cash management or emergency fund, you can secure your financial stability in times of crisis. Whether it's through a high-yield savings account, CD, Roth IRA, or other options, the key is to evaluate our emergency savings target, choose the right savings vehicle, and contribute to it regularly.

The sacrifices may be temporary, but the peace of mind and financial security will last a lifetime. Indeed, taking theses steps will not only allow you to maximize your income, but they’ll also take get you one step close to becoming the master of your own financial independence journey.

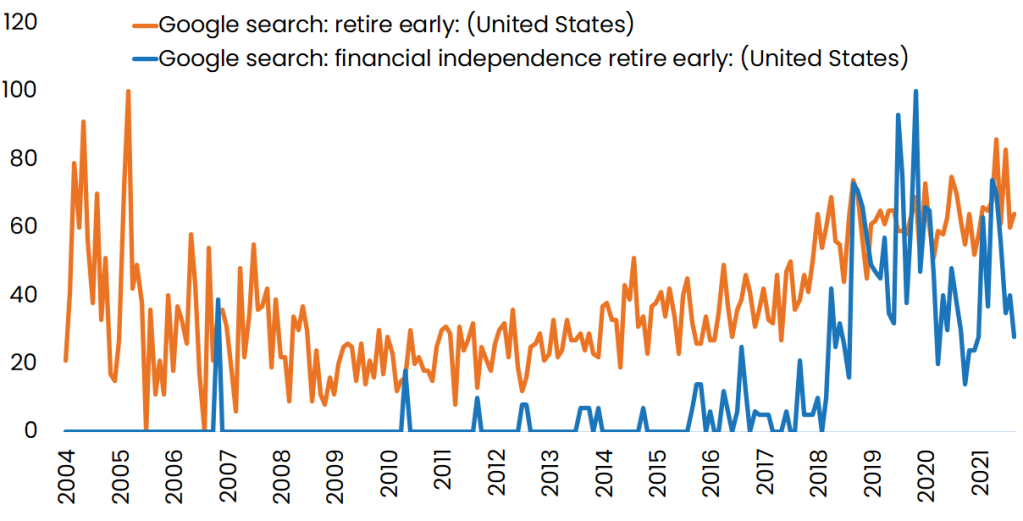

Early Retirement: Don’t Make these Five Mistakes

Handing in a resignation letter and walking away from an unfulfilling career may be one of the most satisfying acts in an individual's life. By some measures, there are an increasing number of satisfied people in the world today. Indeed, recent accounts increasingly show that people are leaving their jobs in droves. These developments are evident in articles about quit and vacancy rates and even rising Google Search trends for early retirement. To be sure, one study found that COVID has prompted a growing wave of early retirements, especially for people who had not planned to quit their jobs but are now thinking of doing so. Can you relate?

Maybe your investments have performed solidly over the past 18 months, and now you have the financial resources and confidence you need to pull the trigger and finally step into financial independence. Maybe your company has recently gone public, and you've come into a large financial windfall that has set you up for early retirement. Or, perhaps you've had time to consider whether the work you're doing today truly aligns with what matters most to you in your life.

Whatever the case may be, now could finally be the time for you to take the next steps towards early retirement. But before you walk into your boss's office and hand in that resignation letter, you'll likely want to consider some potential pitfalls that might derail your financial independence early retirement plans. Indeed, not thinking through some crucial early retirement mistakes could leave your financial goals falling short.

Here are five financial mistakes that you'll likely want to avoid as you take your next step towards becoming the master of your financial independence journey:

Mistake #1: Underestimating your retirement cash flow needs

Let's assume that you're 45 years old, have saved one million dollars, and are now ready to pull the trigger on early retirement. If this is you, I'd like to give you a round of applause because, according to a study from Fidelity, the average 401k balance for an individual in their forties is roughly $93,000. So, if you've accumulated one million dollars by this age, you're well ahead of your peers. But will this savings be enough to cover your lifestyle expenses if you decide to retire tomorrow?

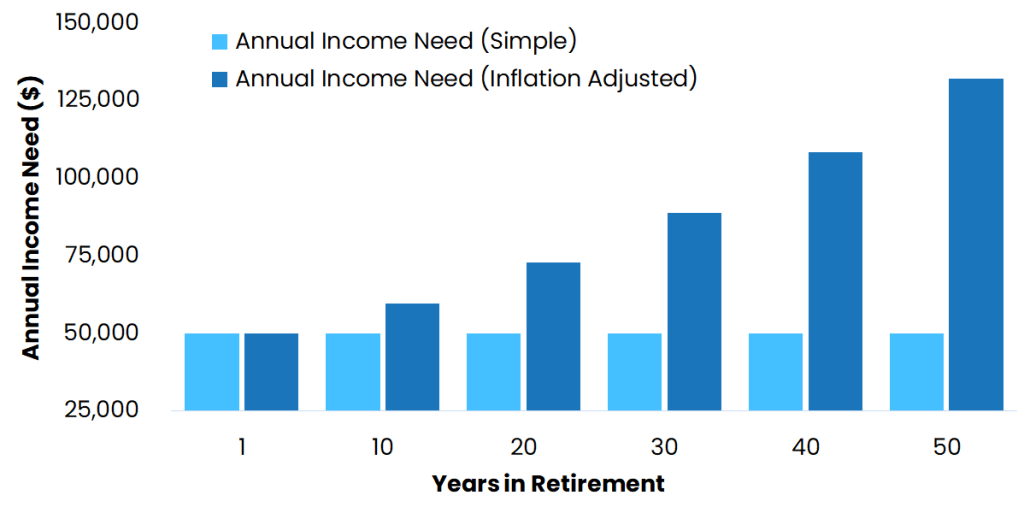

Let's take a look at an example to understand when a million dollars may not cut it when it comes to covering your retirement cash flow needs. First, if we assume that you'll need $50,000 per year to keep the lights on and allow you to enjoy your current lifestyle and your investments grow by about five percent annually, you should be fine, right?

Well, one problem with this assumption is that your living expenses will stay fixed at $50,000 annually over the next half-century. Realistically, however, your cost of living is likely to creep higher by an average of 2% per year. Rising inflation means that the lifestyle that costs you $50,000 today could well rise to over $130,000 in 50 years. At this rate, your million-dollar savings could be wiped out well into retirement if specific lifestyle changes aren't made today.

Therefore, if you're trying to determine whether a million dollars or any amount for that matter is enough to retire early, start by figuring out what your inflation-adjusted household expenses may be throughout retirement.

This analysis involves developing realistic expectations for your lifestyle spending in the years ahead, evaluating the effects of inflation on your annual income needs, and setting some realistic expectations about your investment return rate. Only then can you determine with some certainty whether the nest egg you have today is enough to cover your living expenses for the rest of your life.

Mistake #2: Relying solely on your 401k or IRA for early retirement

Another mistake that some early retirees make is concentrating their savings in qualified accounts and not putting enough away in taxable investment accounts. Why is this a problem? Well, with some exceptions, money in a qualified account, like a 401k or IRA, won't be available penalty-free until you reach age 59 ½.

So, if you're 45 years old, ready to retire early, and have all of your savings tied up in a 401k, your options likely will be limited when it comes to using your savings to cover everyday expenses. That's because tapping your qualified savings early could lead to a host of penalties that could otherwise derail your best laid financial plans. How can you ensure that you're prepared for early retirement without incurring unnecessary costs?

One option is to save enough money in a taxable account to cover your living expenses until you can begin safely drawing down money from a 401k or IRA at 59 ½. So, how much money should you have saved up in each type of account?

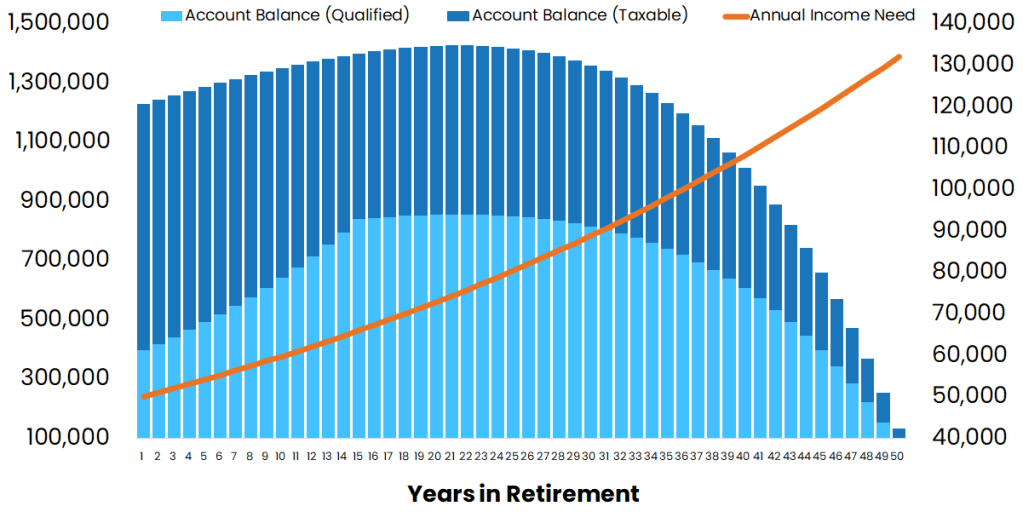

Well, let's assume that you're 45 years old and plan to spend $50,000 per year on living expenses, inflation-adjusted over the next 50 years. Based on several simplified assumptions, you'll likely need to have saved 1.3 million dollars before you quit your job. Two-thirds of that amount (or about $830,000) should be in a taxable account to pay for day-to-day expenses.

The remaining amount of your retirement savings (about $400,000) should be spread across qualified accounts like 401ks or IRAs. As you draw down your taxable account early in retirement, your qualified accounts likely will continue to appreciate, untouched but for periodic contributions or rebalancing, hypothetically appreciating to a level of $850,000 by the time you reach age 59 ½. At that point, you can begin spreading living expenses between both taxable and qualified accounts.

Complex calculations aside, the key takeaway here is that the farther out you are from retiring at age 59 ½, the more of your retirement savings you'll need to have allocated to a non-qualified savings account. Not anticipating this mistake could derail your early retirement goal for quite some time.

Mistake #3: Dismissing social security benefits entirely

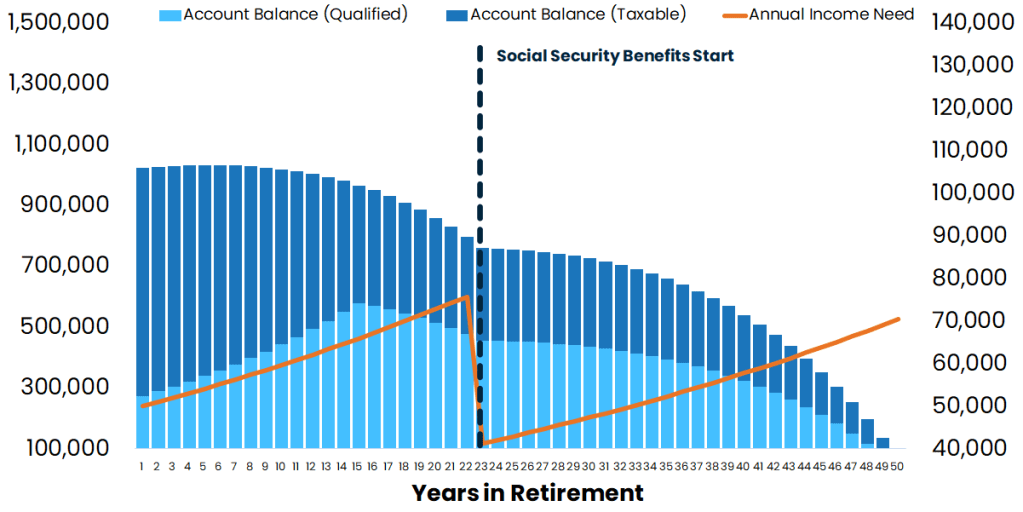

One financial planning component that many financial independence retire early (FIRE) proponents often overlook is social security's effects on how much you'll need to have saved for early retirement. For example, recall from our previous example that an individual might need $1.3 million to cover lifestyle expenses of $50,000 (inflation-adjusted) over fifty years. A $36,000 annual social security income benefit could reduce your investment savings need by about $200,000 starting at age 45 and put you closer to that $1 million savings target.

How? Let's take a closer look.

You'll recall that between various retirement savings accounts, we estimate that an individual with an income need of $50,000 per year, retiring at 45, would likely need about $830,000 in taxable accounts and $400,000 in their qualified accounts. Factoring in social security benefits starting at age 67, this same individual would likely need about $750,000 in their taxable account and $274,000 in their qualified accounts. The added social security benefit lowers the amount of money drawn down from retirement savings in later years, naturally reducing the total amount of money that needs to be saved before quitting their job.

The good news is that making one million dollars work for retirement is feasible, so long as the savings are spread across the proper accounts, and social security benefits kick in as expected. So, how can you determine the social security benefit amount to use in your financial projections? One of the simplest ways to obtain this number is to visit https://ssa.gov/myaccount. Here you'll be able to get a copy of your social security benefit statement, which outlines your projected future benefits based on what you've already paid into the system.

But what if you're 45 years old today, and you expect that social security will go broke by the time you start drawing down benefits twenty years from now? This concern certainly is legitimate. Even so, it's possible that being such a politically sensitive topic, lawmakers won't let the social security program die entirely. Even so, the further you are away from receiving projected social security benefits, the more of a discount you'll likely want to apply to projected future income benefits as a way to account for uncertainty related to the program.

Mistake #4: Forgetting to factor in healthcare expenses

So, you're 45 years old, in good health, and doing everything right to take care of your body and mind. You exercise regularly, eat a balanced meal, and take your vitamin supplements daily. You don't have any health concerns right now and expect to live a long life. Why should you care about potential healthcare expenses?

Well, what happens if your health situation unexpectedly changes somewhere down the road, say in 10 years or so. Indeed, the events of 2020-2021 have taught many of us that our health, no matter how hard we try, can be drastically affected by circumstances entirely out of our control.

Add to this the fact that the cost of medical care has been outpacing the average level of inflation for years. From this perspective, if you're not building in rising healthcare costs into your financial independence early retirement plans, you could be setting yourself up for a big disappointment in the years ahead.

So, how do you know whether you're accounting for the right amount of healthcare spending?

To answer this question, you'll need to take time to think through the kind of care you will need in old age and account for their related costs. While medical expenses (like paying for insurance premiums) may only constitute a sixth of your early retirement income need at age 45, by the time you reach age 70, those expenses could rise to a third of your income needs. And depending on your living situation, these numbers could increase to over half of your spending by your late 80's when considering expenses related to assisted or long-term care needs.

So, if we take a simple 6% appreciation in medical costs from age 45 and extrapolate it out through retirement, how does that affect our earlier projections? Recall that with social security benefits, your financial independence retire early savings need would be about 1 million dollars spread across taxable and qualified accounts at age 45.

When factoring in rising medical costs, you'd likely need to have saved an extra $300,000 at age 45 even after factoring in the bump from social security benefits. When accounting for rising medical costs, this time around, you'd likely need $870,000 in taxable accounts and $420,000 in qualified accounts compared to $750,000 and $274,000 in our previous example when you begin early retirement.

Again, the key consideration here is ensuring that you'll have enough saved to cover unexpected medical expenses when you're healthy while being prepared for the unexpected over the long term. Without employer medical coverage, you'll need to be prepared for private healthcare coverage, which you can purchase in your state's insurance marketplace. You can visit healthcare.gov to get a better sense of the options available to you. Either way, no matter how healthy you are today, don't make the mistake of being unprepared for some form of medical care that you'll likely need in the decades ahead.

Mistake #5: Not giving your money a purpose

One final but a fundamental mistake that some individuals who retire early make is not having a purpose for their money. These individuals often have one goal, and it's simple: save money so you can quit your job. But then what? If your goal has been to live frugally and save every penny so you can leave the workforce but don't have a purpose for life after that, then what's this journey been about?

For many of us with financial independence retire early (FIRE) aspirations, these qualitative, squishy questions may seem irrelevant at face value. You may say, "I already know how much I intend to spend." Or "I'm content with my life today; nothing will change." But honestly, how can you be so sure? Many of us don't know where our lives will take us a year from now, let alone a decade or half-century from now.

One analogy that we use when discussing an individual's finances is to think about it as a home divided into two parts. The right-hand side of the house defines the financial resources and tactics used to make retirement a reality. In other words, it encompasses a lot of the items that we discussed here today: tactics.

However, the left-hand side of the home defines your values, your relationship with money, and your life goals in retirement. In order words, it contains the elemental component: strategy. It represents, "where is my life headed, and what's all this money for?"

The point here is to spend time thinking about the general direction you'd like your life to go. One analogy that we often share is that of taking a flight from Los Angeles to New York. A pilot's five-degree navigation error at the start of the journey could put the plane thousands of miles off course when it reaches the East Coast.

Giving your money purpose will take some deep thought, and at times involve having uncomfortable conversations and thinking through some harsh realities. But in the end, the outcome produces greater clarity and direction for your money's use. At the same time, if you do plan to retire at age 45, it can help you define exactly how much savings you'll need to cover your lifestyle expenses over the next 50 years.

Avoiding Early Retirement Mistakes

Before we wrap things up, we need to talk about one of the biggest mistakes individuals aspiring for financial independence retire early make: blindly following the four-percent rule. A lot has changed since this concept was introduced nearly 30-years ago, and, quite frankly, this approach to calculating how much money you need to retire early is likely outdated.

To be sure, financial markets, central banks, and government policies have fundamentally changed since the four-percent rule was introduced in 1994. So, what can you do to ensure that you've saved the right amount of money for retirement to maximize your chances of avoiding a savings shortfall? First, start by spending the time to think through what you want your post-career years to look like. Ultimately, answer the question, "what is this money for?"

Next, think about how you expect your lifestyle spending to change over the coming years and decades while being mindful that inflation will create a greater demand on your savings. Here again, you'll want to ensure that your financial plan is realistic regarding income needs as prices rise, even if you don't anticipate a significant change in lifestyle spending today.

Then, be sure that you've put enough money away in savings accounts that you can access today. Recall that qualified accounts, like a 401k and IRAs, aren't accessible penalty-free until age 59 ½. Therefore, you'll want to have money socked away in taxable investment accounts to cover living expenses before tapping your retirement savings.

Finally, consider how social security benefits and medical costs will impact your overall income drawdowns, and more broadly, your retirement savings needs for the long-term. Recall that factoring social security benefits into your income projections could cut your retirement savings need at age 45 by hundreds of thousands of dollars. At the same time, not preparing for unforeseen healthcare concerns could leave you with unexpected medical expenses not accounted for in your savings plan.

Are you ready to quit your job and live life on your own terms? While you might think you have enough money saved today, one way to ensure that your retirement savings are on the right track is by avoiding some common early retirement mistakes. While calculating your retirement need is no simple task, it nevertheless highlights a key reason why developing a financial plan is an essential component of early retirement preparation. Indeed, doing the work today could maximize your chances of success for the long term and help you finally become the master of your financial independence journey.

Four Ways to Set Your Retirement on FIRE

Retiring early is an aspiration that many individuals can get excited about. Vicki Robin and Joe Dominguez, in their best-selling book, “Your Money or Your Life”, arguably introduced the concept of early retirement to the mainstream culture decades ago. Today, thousands of individuals are actively pursuing their goal of becoming financially independent and quitting their nine-to-five grind.

According to one Gallup study, individuals in their early 20’s were generally optimistic about their ability to save for retirement before age 60. However, those same individuals curbed their early retirement enthusiasm when later surveyed in their 30’s as savings and other lifestyle realities made it increasingly clear that early retirement might just be an elusive goal.

Even so, data from Hearts & Wallets suggests that one out of every six Americans surveyed by the group expects to retire before the age of 55 - ten years sooner than the standard retirement age of 65.

This data illustrates one key point when it comes to the concept of retirement: individuals across all walks of life increasingly want to start the journey to become financially independent and retire early, rather than walking down the path of a traditional retirement later on in life. To be sure, retiring early has become so popular that it’s even earned its own name: the FIRE movement.

So, what is FIRE? Well, the acronym FIRE stands for ‘financial independence, retire early,’ and the goal is to create an opportunity where you can stop chasing an unfulfilling career and live life on your terms without being tied down to the demands of a full-time job. Many individuals have accomplished this goal by living frugally through their working years, carefully planning out their finances, and prioritizing saving and investing over other frivolous lifestyle activities.

Does becoming financially independent and retiring early sound appealing to you? And how would it feel to hand your boss a resignation letter today, knowing that you would be financially set to live your best life however you choose tomorrow? If you’re in the camp that’s excited about early retirement but not sure that you can commit to a restrictive savings plan, you can take heart knowing that there are several options for achieving FIRE. Certainly, the idea of retiring early may seem like a pipe dream to some individuals. Still, with proper planning and the determination to make it happen, early retirement may be closer than you think.

Understanding the FIRE Movement

Now some individuals might get the impression that in order to achieve FIRE, one must live a spartan lifestyle and disown nearly all earthly pleasures. While such an approach may work for some individuals, the truth is that we all have varying degrees of tolerance for postponing consumption today so that we can save for tomorrow. That’s why over the past couple of decades, some individuals have developed a few different ways to achieve financial independence. These include traditional FIRE, LeanFIRE, FatFIRE, and Barista FIRE.

Let’s first talk about traditional FIRE.

Traditional FIRE

So, what is traditional FIRE? Well, it’s the most basic way to achieving financial independence and retiring early. The concept is simple: identify your early retirement goals, calculate your financial independence number, then save as much of your income as possible. Traditional FIRE is centered on the idea of acquiring enough income-producing assets, like financial investments or rental property to produce a steady stream of income to cover living expenses for the rest of an individual’s life.

Achieving FIRE along this path often involves living a somewhat traditional lifestyle while finding ways to save a large portion of money received from a traditional job. An individual pursuing a traditional FIRE journey often has already achieved contentedness with their current lifestyle. That’s why their goal is to focus their financial efforts on building up a nest egg that will help them maintain their current lifestyle for the rest of their lives.

LeanFire

Another way to retire early is by LeanFIRE. Its very name suggests that this approach takes a more modest, frugal path to early retirement and requires living with a bare minimum budget in your current lifestyle, as well as in retirement. Many households in this camp earn six-figure paychecks but spend only a fraction of their income to cover living expenses. LeanFire is a genuine commitment and takes a different kind of mindset compared to the traditional FIRE path.

In fact, individuals pursuing this path often develop a minimalist mindset, finding ways to live off of less than $40,000 per year while developing a savings strategy centered around their financial retirement number. For example, Joshua Fields and Ryan Nicodemus, who dub themselves “The Minimalists”, claim to have helped over 20 million people live meaningful lives by choosing to reevaluate their relationship with material wealth.

Now, this path to FIRE may not be for everyone because it requires an individual to challenge their emotions and mindset to live a life well below their potential means. Nevertheless, LeanFIRE is still an attractive option because it provides one of the most accessible and quickest paths to early retirement.

FatFire

Next up, we have FatFire. How is FatFire different from LeanFire? Well, in many ways, FatFire is the opposite of LeanFire. FatFIRE might be appealing for those individuals who can appreciate the finer things in life and would like to use their savings to experience a more extravagant retirement lifestyle. Retirement income goals for individuals in this space typically start at around $100,000 per year. Individuals taking the FatFire path are often high earners who spend their early years balancing quick career progression, a commitment to a disciplined savings strategy with acquiring that house by the lake or all the toys they’d like to enjoy in retirement while having the opportunity to travel when they’re finally able to quit their jobs.

This approach typically requires more time to attain FIRE, but can make early retirement more enjoyable than LeanFIRE, which generally requires living on the bare necessities. The idea here is to acquire financial and lifestyle assets that produce an income capable of covering your minimum living expenses while allowing you some room for additional spending as your lifestyle permits.

Barista FIRE

Now, similar to LeanFIRE, Barista FIRE focuses on living a minimalist lifestyle, acquiring revenue-producing assets, and counting on a side hustle to supplement your lifestyle income. With Barista FIRE, there’s less pressure to save money like a minimalist. Additionally, one often overlooked need for individuals on their journey to financial independence, and early retirement is covering the cost of healthcare. While insurance marketplaces have improved accessibility, paying for medical coverage, especially for a family on the FIRE path, can be rather expensive.

One thing that makes Barista FIRE attractive is the ability to work a less demanding job while having access to affordable medical coverage available through an employer-sponsored benefits plan. Additionally, this path can help ensure individuals earn the 40 Social Security credits they need to become eligible for government retirement benefits, like Medicare and Medicaid. Barista Fire is increasingly becoming a more common alternative to LeanFire, given that the idea is to have enough money saved and invested that you can quit your full-time job all the while working a less demanding side hustle that can help you cover some monthly expenses.

Planning for Early Retirement

Whether you want to live lavishly or are comfortable living a spartan lifestyle, the path of financial independence and the FIRE movement essentially comes down to living life on your terms without being tied down to an unfulfilling job. And achieving this end almost always requires a little bit of planning.

So which path to FIRE is right for you? Well, just like planning for retirement at age 65, to achieve FIRE it’s essential to define your near- and long-term lifestyle goals while at the same time having a clear understanding of your current financial situation. Doing so will help you determine what steps need to happen first and what actions you need to prioritize.

The most significant difference between planning for traditional retirement and planning for FIRE is the time horizon. This means that to retire early, savings rates and investment contributions need to be maximized as soon as possible so you have enough money invested to draw income from.

Now, determining how much money you need to have saved can be a challenge. That’s why in 1994, retired financial advisor William Bengen established a savings guideline called the 4% rule. This rule suggests that if you have 25x your annual living expenses saved, you can withdraw 4% from the portfolio and not run out of money for 30 years.

So, for example, if you need $75,000 per year to cover your lifestyle expenses in retirement, you’d need approximately $1.9 million saved and invested. This $1.9 million is what many in the movement would consider your financial independence number.

Now, rules of thumb are a good place to start. Realistically, however, you’ll likely need to make some modifications to the 4% rule. For example, you’ll likely need to account for a retirement time horizon greater than 30 years, varying inflation levels, life expectancy changes, variable spending, and rising medical costs as part of inputs to calculate a more accurate financial independence number. That’s why it’s essential to develop a plan that’s tailored for your unique goals, values, and desired life outcomes.

Outside of being able to retire early, one of the most significant benefits of planning for FIRE is that it requires you to think about the kind of life you want to live. That’s what makes Vicki Robin’s and Joe Dominguez’s work so appealing for so many people. Too often, we fail to dream big and think about our future, but the exercise of planning for a post-employment life creates an opportunity to honestly think about what goals and experiences you want to accomplish in life.

Being able to retire early really comes down to asking yourself a few questions:

- What would my life look like if I didn’t have to work again?

- How soon do I want to be able to live such a life?

- What’s my financial independence number?

- What has to change in my life today to achieve this goal?

Once you get solid answers to these questions, you can begin working backward to determine the necessary savings rates and the action items needed to achieve FIRE.

How to Make It a Reality

While your lifestyle needs will play a significant role in deciding which FIRE path is appropriate for you, keeping expenses as low as possible while still maintaining a quality way of life is generally what makes FIRE possible. Based on the financial independence number you discovered in your planning sessions, you can then determine how much money needs to be saved each month and each year to hit that savings goal.

Even so, saving money is only a start to your financial independence journey. Investing is the most crucial piece of the FIRE puzzle because you need to put your money to work today so that it can quickly grow tomorrow. Depending on your situation, it’s generally recommended to make annual 401(k) contributions that at least qualify you for your employer match to take advantage of free money. At the same time, keep in mind that if you do plan to retire early, you’ll need a source of savings to draw on to avoid penalties from the IRS.

Being as debt-free as possible is also crucial to keeping expenses low and simplifying your lifestyle while in FIRE. Remember, investment income is a reward you pay yourself for being a diligent saver. Interest on debt is income you pay to someone else for lending you their savings.

Even so, if you find yourself needing additional income, working a side hustle during your years of accumulation can help supercharge your savings and may also prove to be a fallback source of income after taking a step off the corporate ladder.

The Takeaway

Whether we’re talking about LeanFIRE, FatFIRE or BaristaFIRE, the common denominator among these early retirement paths is to take cash earned today and convert it into future cash flows for tomorrow. Being financially independent with the ability to retire early is a dream that many people have. Even if you don’t desire to retire early, everyone can benefit from the fundamentals of the FIRE movement.

Planning out your future, being intentional with your spending, and investing for retirement are essential steps to evaluate whether you want to retire early or retire at the traditional age of 65. And that’s why working with the right financial planner can help you work through the numbers and build a plan to live life on your own terms, a reality.

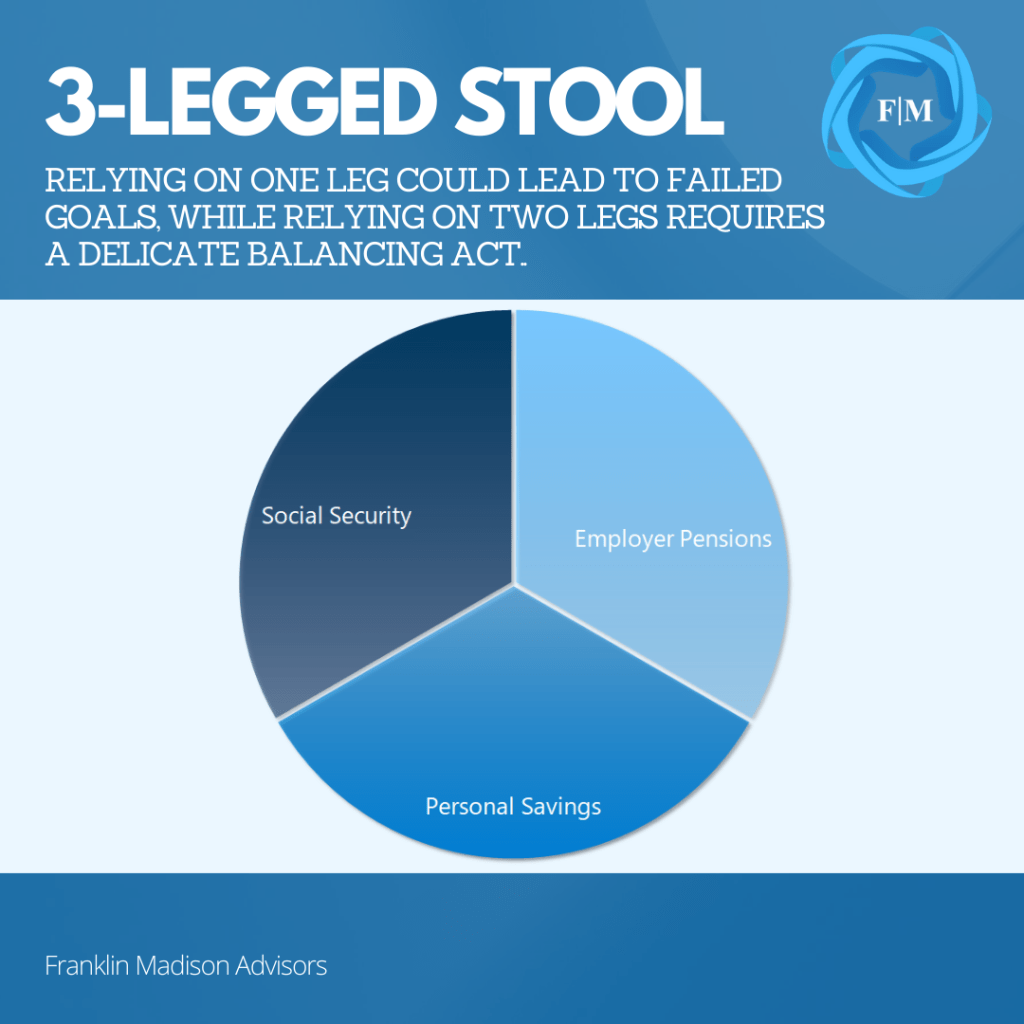

How Can You Rebuild a Broken Retirement Three-Legged Stool?

The road to retirement is not as straightforward as it used to be. There was a time when simple metaphors, like the three-legged stool of retirement, captured how you could achieve retirement security with ease. This concept illustrated how securing a good pension, obtaining a solid return on your savings, and relying on social security might have paved the way for financial comfort in your golden years. Relying on just one leg could lead to failed retirement goals, while relying on two legs requires a delicate balancing act.

Unfortunately, for many individuals, this seemingly secure approach to retirement planning has all but disappeared. And today, few simple metaphors exist to describe an easy path toward retirement security, leaving many people scrambling to figure out how to plan for their future thoughtfully. Now, with a little extra work and some creativity, you might be able to repurpose the components of the simple three-legged stool framework to suit your individual goals in this complex and challenging economic environment.

How the Three-Legged Stool Has Changed

When the three-legged stool concept was first introduced generations ago, many employers provided pension benefits to their employees, banks offered healthy returns on savings, and social security was seen as a solid base from which to structure retirement planning. Yet the foundation upon which this concept was developed has materially changed in the past few decades.

Complex Retirement Planning

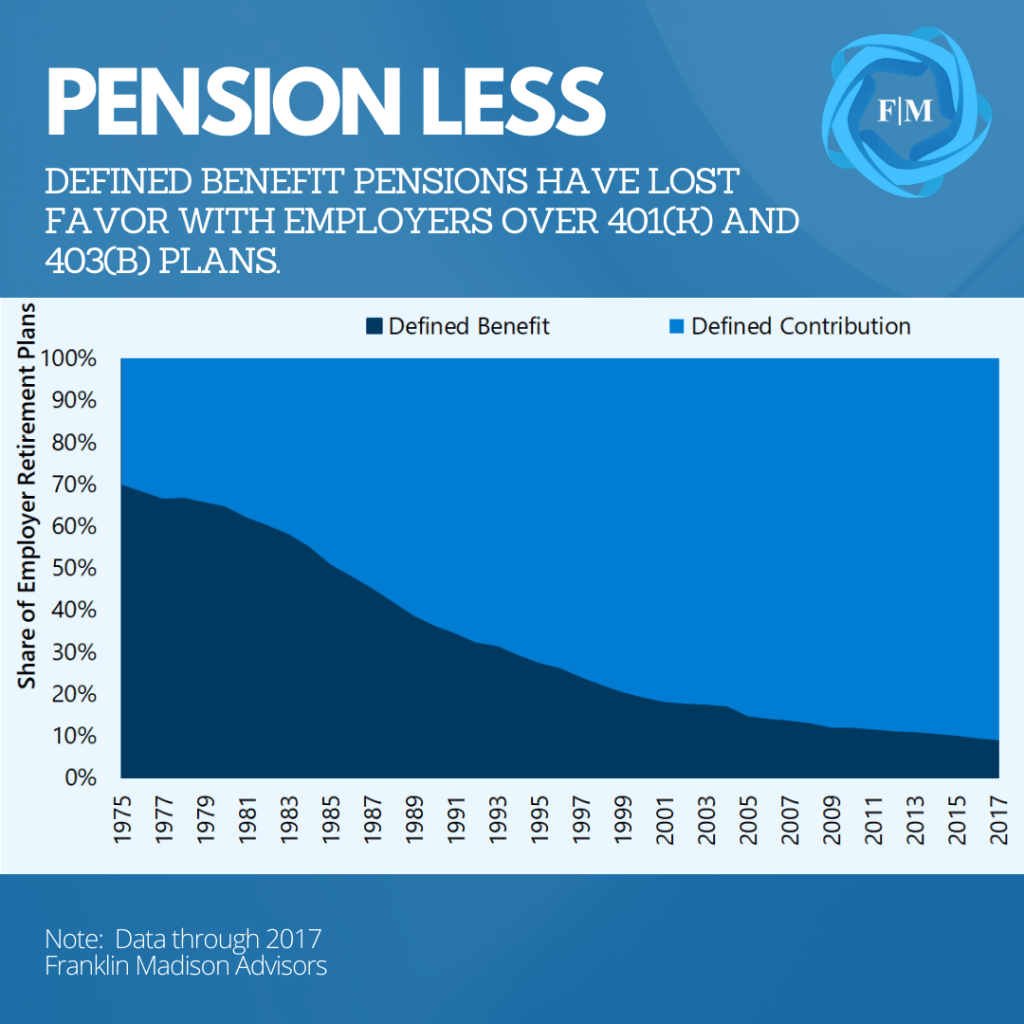

For example, defined benefit pension plans used to be a key component of the three-legged retirement stool. Pensions accounted for 70% of retirement plans in 1975 for companies with 100 or more employees. By 2017, this figure fell to 9% and remains in decline as employers increasingly shift their preference toward defined contribution options like 401(k) and 403(b) plans.

This change means that individuals workers are increasingly responsible for navigating sophisticated investment options, determining appropriate contribution amounts, and working through tax consequences and their crucial distribution choices. It goes without saying that planning for retirement is much more complicated than it used to be.

Source: Broadview Macro Research

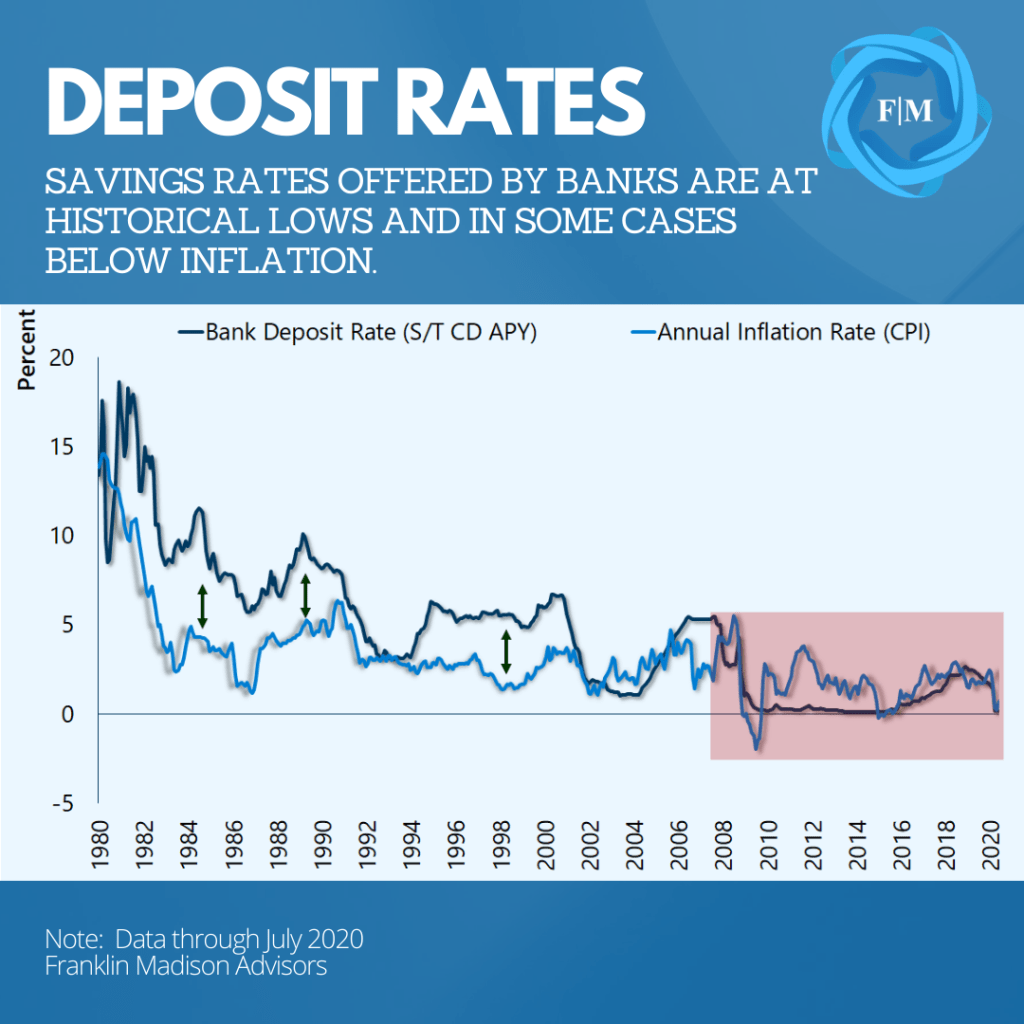

More Challenging to Grow Your Money

In terms of saving for the future, changes in the financial system have made it challenging to grow your money through a simple bank deposit. From 1980 through the start of the Global Financial Crisis, bank deposit rates averaged 6.5%. Since then, the amount of annual interest that your savings might accumulate through a bank account has fallen to less than 1%. Without a doubt, using a simple savings account to shore up your retirement is more challenging.

For example, at the current average deposit rate of 0.5%, it will take you 144 years to double money held in a savings account compared to just 11 years a few decades ago. Taking into consideration the detrimental effects of inflation, if you rely on a standard bank account alone to grow your wealth, there's a good chance that a dollar saved today likely won't go as far in the future.

Social Security is Less Secure

Finally, it will likely come as no surprise that expected future social security benefits are increasingly coming under pressure. Social Security was once seen as the most solid leg of the retirement planning stool. Yet, by some estimates, the government's reserves needed to pay old age, survivor, and disability insurance (OASDI) benefits for Americans likely will be depleted by 2035. This outlook is according to a report from the Social Security Trustees themselves.