Market Reaction: Stocks Post New Highs Post Election

Monthly Market Summary

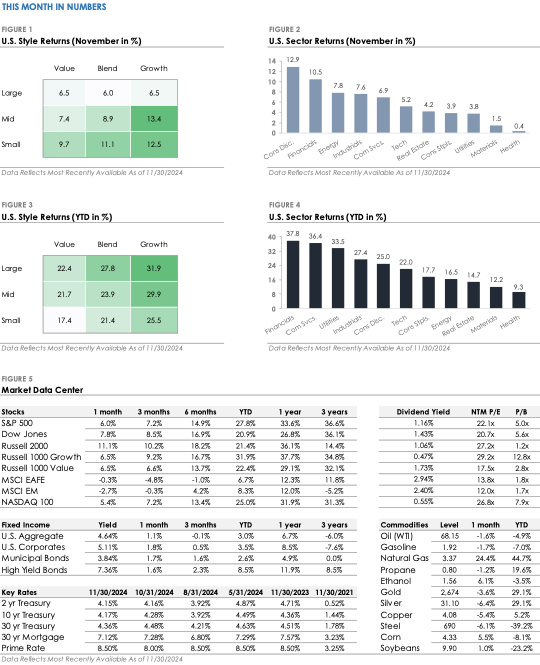

- The S&P 500 Index returned +6.0% but underperformed the Russell 2000 Index’s +11.1% return. All eleven S&P 500 sectors traded higher, with Consumer Discretionary and Financials gaining more than +10%. In contrast, defensive sectors, such as Health Care, Utilities, and Consumer Staples, underperformed the S&P 500.

- Corporate investment-grade bonds produced a +1.8% total return as Treasury yields declined, marginally outperforming corporate high-yield’s +1.6% total return.

- International stocks traded lower for a second consecutive month. The MSCI EAFE developed market stock index returned -0.3%, while the MSCI Emerging Market Index returned -2.7%.

Markets Set New All-Time Highs in November’s Post-Election Rally

The U.S. presidential election results fueled November’s stock market rally, as investors focused on the incoming administration’s policy agenda and its implications. The S&P 500 gained +6.0%, its biggest monthly return since November 2023.

The index traded above the key 6,000 level and set a new all-time high, bringing its year-to-date return to +27%. Smaller companies took center stage during the broad market rally, with the Russell 2000 surging +11.1% to set a record high.

In the bond market, Treasury yields rose after the election due to concerns about increased fiscal spending, tax cuts, and large fiscal deficits under the next administration.

However, later in the month, yields reversed lower, and bonds posted positive returns. With Republicans taking control of the White House, Senate, and House in January, the following section discusses key policy areas to watch, along with the potential market and economic impacts.

Key Policies to Watch in the Next Administration

Investors are monitoring two key areas: tax policy and trade.

The administration is expected to focus on extending the tax cuts passed during President Trump’s first term. This could stimulate economic growth and boost corporate profits, although it could widen the fiscal deficit.

On trade, the administration plans to use tariffs to advance U.S. interests in international affairs and renegotiate trade deals. However, in the near term, tariffs could disrupt supply chains, slow economic growth, and squeeze profit margins.

Other critical policies include immigration and deregulation. There are concerns that tariffs, stricter immigration policies, and expansionary fiscal policy could combine to keep inflation high. If so, the Federal Reserve might need to keep interest rates higher for longer.

Elsewhere, there is an expectation that deregulation could create new growth opportunities in the financial and energy sectors, while relaxed antitrust enforcement could lead to more mergers and acquisitions. Economic growth and corporate earnings will remain important long-term drivers, but in the short term, markets may be sensitive to shifting policy headlines as the new administration takes office.

Trump Wins: What it Means for Your Money

We are likely entering a period of familiar uncertainty. Former President Donald Trump's victory in Wisconsin early this morning clinched his victory and set the stage for a second term as the country's president.

Market Implications

So, what does this mean for the markets, the economy, and your money? Well, as we pointed out in last month's note heading into this week's election, long-term investment data since 1953 shows that markets tend to grow irrespective of the sitting president's party, with a $10,000 investment growing to over $2.1 million if invested continuously, compared to much lower returns if one invested only when Republican or Democratic administrations were in office.

This analysis highlights the benefit of sticking to a disciplined, long-term investment strategy instead of trying to time investments based on political cycles.

Economic Implications

Now, with respect to Trump's second term, the effects of his economic policies could have long-term implications on your savings and spending decisions, given the potential for higher inflation in the coming years and higher taxes once he's out of office.

How so?

First, Trump vowed to renew his trade war with China and begin imposing tariffs shortly after taking office. Although often discussed in geopolitical terms, tariffs on China's exports ultimately function as taxes on US consumers, which can lead to higher prices for goods consumed.

Effects of Tax Cuts

Second, Trump has proposed a host of tax cuts, including extending the 2017 Tax Cuts and Jobs Act (TCJA), eliminating income taxes on Social Security benefits, and reducing corporate tax rates.

Tax cuts provide extra disposable income for households. And when people have more money to spend, consumer demand for goods and services typically increases.

If this increased demand outpaces the economy's ability to supply these goods and services, it can lead to higher prices and contribute to inflation. This point is crucial because a combination of rising import costs, fiscal stimulus, and easy money policies from the Federal Reserve could stoke the embers of inflation.

Higher Taxes Down the Road

Finally, all these tax cuts need to be paid somehow.

As it stands, the US government is spending more than it brings in by the tune of $1.8 trillion in 2024. According to a study by Wharton, this deficit could balloon to $5.8 trillion over the next ten years.

And so, while spending cuts are one way to tackle future deficits, policymakers will likely find ways to raise taxes down the road to cover these debts.

The Big Takeaway

We are headed into a period of familiar uncertainty as it relates to economic policy.

So then, proactive financial planning is prudent now more than ever because higher inflation and higher taxes later are likely a reality we'll all face.

Loose fiscal and monetary policy, along with a renewed trade war, could lead to higher levels of inflation and a rising cost of living over the long term.

At the same time, ballooning government deficits cannot be ignored indefinitely, so spending cuts and higher taxes will be necessary to address the current plight.

Now's the Time to Reevaluate Your Financial Plan

Therefore, reevaluating potentially overly optimistic inflation assumptions in your retirement plan could help you mitigate the effects of a rising cost of living and avoid savings/spending misalignment down the road.

At the same time, tax planning is essential now more than ever because regardless of which tax bracket you're in now, there's a good chance that years from now, your retirement distributions could be facing higher tax rates.

That's why, while your portfolio may grow steadily in this changing political environment, now's the time to begin planning for higher costs and evaluating strategies to keep more of your savings when it's time to take distributions.

As we navigate this period of economic uncertainty, it's crucial to actively review and adjust your financial plan. Doing so not only prepares you for potential inflation and tax changes but also positions your wealth to capitalize on opportunities that arise during fluctuating economic cycles.

WANT TO ENSURE YOU'RE PREPARED FOR INFLATION AND DIAL IN YOUR TAX STRATEGY?

>>> CLICK HERE TO SCHEDULE AN INTRODUCTORY ZOOM CALL! <<<

Elections: Why You Shouldn’t Mix Politics and Your Portfolio

Investing based on political preferences can be bad for your portfolio.

As the 2024 presidential election approaches, Americans are preparing to vote in what polls forecast to be a tight race. And, like many investors, you may wonder how the election outcome could affect financial markets and whether your investment strategy should change should one party take office over another.

Well, while elected leaders can influence economic growth by enacting laws and regulations, data suggests that who occupies the White House has little to no impact on investment performance.

Fundamentals Matter More

That’s because fundamental factors like corporate earnings growth and valuations impact the stock market far more than political headlines. And while politicians make many promises during election years, more often than not these often go unfulfilled because of the government’s system of checks and balances.

Moreover, the economic outcomes of policies are less predictable than officials think, with the economy more influenced by factors like job growth, interest rates, and inflation.

Missing Out on Growth

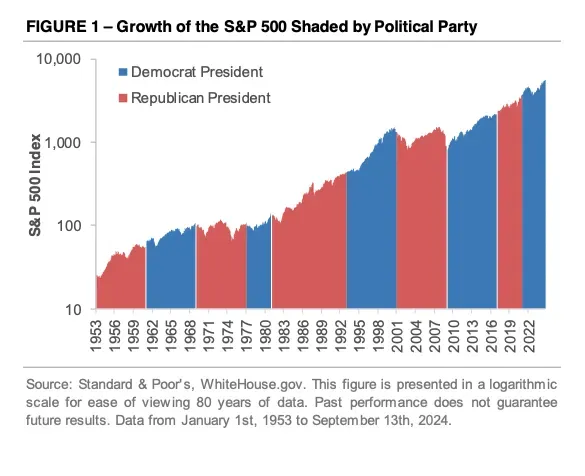

To this point, the charts below illustrate the financial impact of allowing political beliefs to influence investment decisions. The chart below (figure 1) graphs the S&P 500 Index starting with Dwight Eisenhower’s presidency in 1953 and is color-coded by political party.

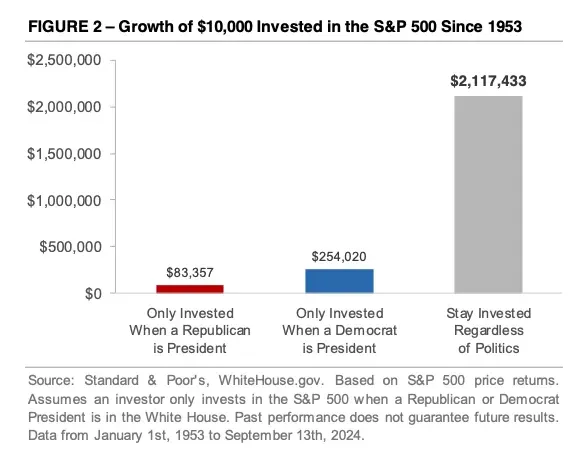

The graph below (figure 2) compares the investment performance of portfolio decisions made based on political affiliation.

If an investor only invested in the stock market when a Republican was President, $10,000 would have grown into $83k today, excluding dividends. On the other hand, investing only when a Democrat was President would have returned $254k.

And while the gap may seem wide at first glance, the reality is that if an investor ignored the president’s political party and remained invested for the long-term, $10,000 would have grown to over $2.1 million.

The Big Takeaway

Political views can stir strong emotions but making investment choices based on those feelings can lead to poor portfolio outcomes. Instead, it’s better to focus on a time-tested disciplined investment strategy and avoid letting politics influence your long-term strategy.

The U.S. economy’s success, growth, and resiliency don’t change with each new election, and neither should your investment strategy.

That’s why it’s best to express political opinions at the ballot box, not in your portfolio.

What Does a 50 Basis Point Cut Really Mean?

Did you know that in a significant move, the Federal Reserve just reduced the fed funds rate by 50 basis points, bringing it down to a range of 4.75 – 5.00%?

This is the first cut since the early days of 2020, marking an end to what has been the most intense period of rate hikes in over four decades.

Why such a decisive cut, you might wonder?

Well, while some might see this as a signal of concern from the Fed about the economy, let’s dig a little deeper. Despite a slight uptick in unemployment and a slowdown in job growth, most indicators suggest that the economy is still expanding.

Even Fed Chief Powell has echoed this sentiment, providing a bit of reassurance to investors. He's betting on a smooth adjustment—a so-called economic soft landing.

Powell’s Perspective: Playing It Safe?

During his latest press conference, Powell maintained that the economy is "in good shape."

But, he hinted that this larger rate cut is more of a precaution—an "insurance" against potential slowdowns. It’s about reinforcing the job market now while it’s strong, not when layoffs start hitting the news.

Think of it as a balancing act. If the Fed waits too long or moves too slowly, it risks a recession. Move too quickly, and it could overheat the economy, sparking inflation. It’s a delicate line to walk, and today, everyone's tuned into how they're managing it.

Market Reactions and Long-term Strategies

Either way, the response from the markets has been generally positive given that it finally got what it’s wanted for years: a Fed Pivot.

Indeed, with profit growth stabilizing, inflation moderating, and interest rates either stable or falling, conditions are ripe for investment. Just this September, both the Dow and S&P 500 reached new heights, a reassuring move given the initial underestimation of inflation by the Fed.

Here’s a quick snapshot of the latest index performances:

- Dow Jones Industrial Average: 1.8% month-to-date, 12.3% year-to-date

- NASDAQ Composite: 2.7% MTD, 21.2% YTD

- S&P 500 Index: 2.0% MTD, 20.8% YTD

Now, it’s worth noting that while strong market performance can stir investor enthusiasm, it also brings with it the temptation for risk-taking. This is where a disciplined investment strategy comes into play.

You see, it’s not just about chasing returns; it’s about managing risks and ensuring you have a portfolio that balances both risks and returns.

The Big Takeaway

So, why should this matter to you?

Well, this situation underscores the critical lesson of diversification—not just in types of investments but also in understanding market movements and central bank strategies.

You see, while markets have rallied strongly this year, recent volatility is a stark reminder that market conditions can change on a whim, so it’s essential to be prepared and not take more risk than necessary.

That’s why, by diversifying your investments, you not only shield yourself from unforeseen market shifts but also position yourself to capitalize on various global opportunities. This kind of strategic positioning ensures that your portfolio captures potential gains while distributing risks, allowing you to focus on what truly matters.

So, as we think on the Fed's recent move, consider this: Is your investment portfolio as diversified as it should be, or are you relying too much on certain assets?

Remember, a disciplined investment strategy isn’t just about picking stocks—it’s about preparing for whatever the future holds while ensuring that your financial foundation is as solid as it can be.

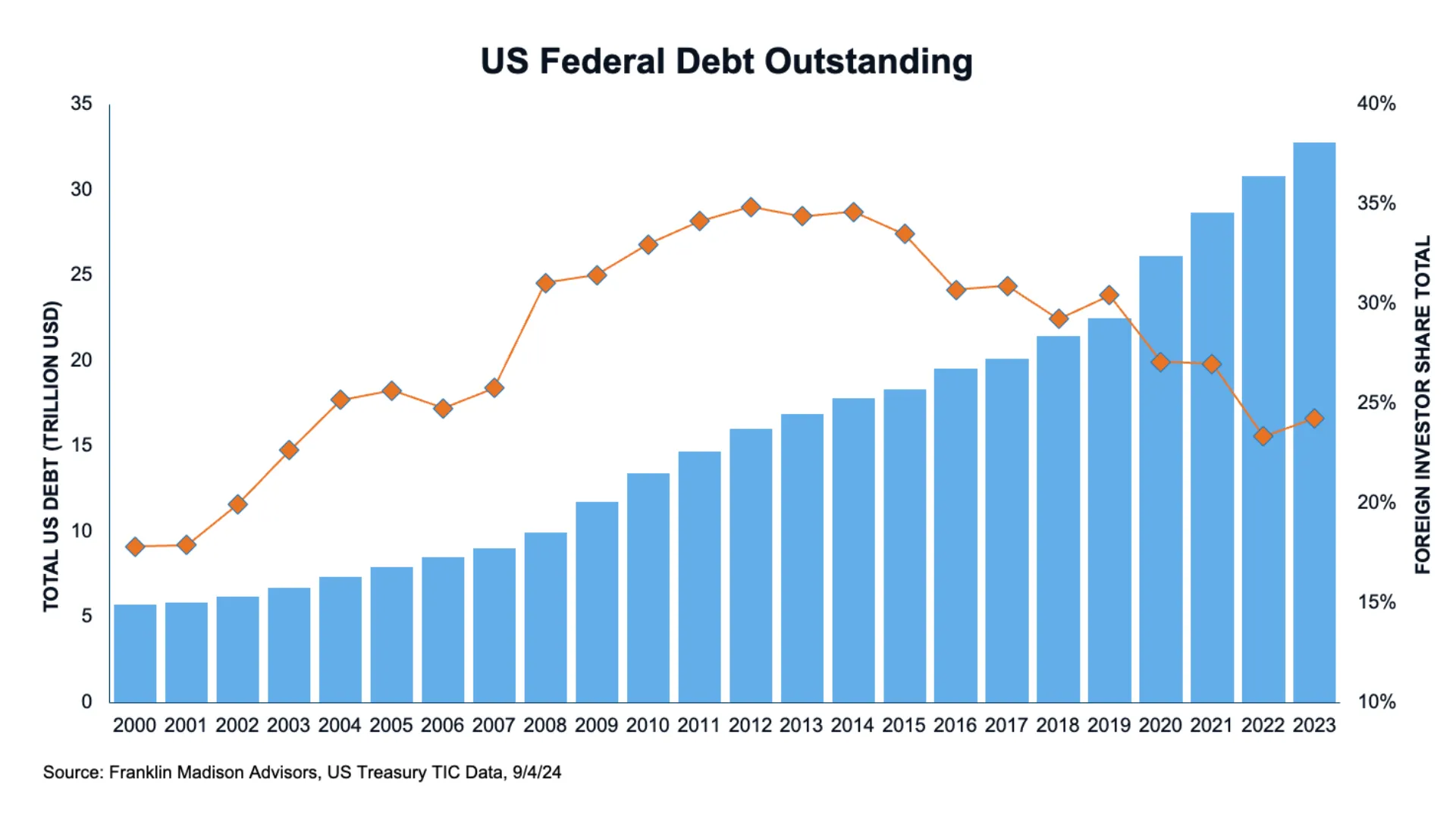

What Can We Learn from Big Government Bond Investors?

Did you know that nearly a quarter of all US government debt outstanding is held by foreign investors?

And, what if I told you that this number has been falling in recent years?

In fact, This figure was at a peak of 35% in 2014 but has declined to 24% as of the end of 2023.

Well, this shift might remind you about concerns about the US dollar's dominance, right?

The Decline in Foreign Holdings: A Sign of Shifting Trends

Well, as a high-achieving professional, you likely understand that these global movements can provide valuable insights into managing your own investment portfolio.

And you see, this market development actually highlights a critical lesson in financial wisdom: the importance of diversification.

How so?

The Real Story: Global Asset Diversification

Well, while some may argue that fewer foreign investors holding Treasuries reflects a decline in US dollar dominance, the fact is that the USD is still the world's preeminent reserve currency.

So then, the decline in foreign holdings must be attributed to something else, right?

So, what's really happening?

Well, it looks like what we're seeing is a broader trend towards global asset diversification as global economic and financial conditions have evolved over the past decade.

The Evolution of Foreign Investment in US Debt

In fact, recent research from the Treasury Department shows that the percentage of US debt held by foreigners has started to decline from its peak in 2015, signaling a shift towards a more diversified global investment strategy.

You see, at the turn of the century, treasuries held by foreign investors accounted for about 18% of total federal debt outstanding, which is a figure that’s substantially less than it is today.

Think about this: after surging during events like the Global Financial Crisis and the European Debt Crisis, when US treasuries were the go-to safe haven, the percentage of US debt held by foreigners has begun to moderate.

Why?

Because as markets stabilize, investors start looking for opportunities beyond the US. It's like they're spreading their bets rather than putting all their eggs in one basket.

Case Study: The European Debt Crisis and Its Aftermath

For example, during the European Debt Crisis, investors flocked to US treasuries as a safe haven, which spiked the percentage of US debt held by foreigners.

But once the dust settled and global markets got back on their feet, these investors started diversifying their portfolios with a mix of assets, showing a savvy approach to investment that we can all learn from.

So then, the main takeaway here is not just that diversification is wise; it's a necessary strategy in today’s interconnected financial landscape.

Personal Portfolio Implications

Why should you, as a tech professional with significant earnings, care about this?

Well, diversification isn't just a practice for institutional investors. It’s equally crucial for your personal portfolio.

By diversifying your investments, you’re not only protecting yourself from unforeseen market shifts but also positioning yourself to take advantage of various global opportunities.

And this kind of positioning ensure that your portfolio captures upside potential while spreading out risk even as you spend your precious little time on things that truly matter to you.

Evaluating Your Investment Strategy

So then, take a lesson from foreign investors and ask yourself, “is my portfolio truly diversified, or am I relying on a single big position to carry my retirement and financial independence goals?”

Remember, building a disciplined investment strategy is not just about picking stocks or sectors; it’s about preparing for the future, wherever it might lead.

So then, take this opportunity to make sure your investments are as globally savvy as you are.

The Bull Market's Unstoppable Momentum in 2024

The past two years have been remarkable for investors, with the S&P 500 posting back-to-back gains of over +20%.

The chart below takes a closer look at 2024’s price movement and uses yellow shading to mark the days when it closed at an all-time high. At the start of this year, the S&P 500’s previous all-time high was set in January 2022.

It took over two years to reclaim the prior high, but once the index broke through in late January 2024, it set more than 50 new highs this year.

The list of all-time highs illustrates the current bull market’s strength and persistence and could grow by year-end.

Large-cap technology stocks, such as Nvidia, Meta, Amazon, and Tesla, have posted strong returns and played a major role in driving the index’s gains. The S&P 500’s record-setting performance is part of a broader cross-asset rally that has lifted stocks, bonds, and commodities.

The stock market’s steady climb this year speaks to investors’ growing confidence. Investors are optimistic about the artificial intelligence industry’s growth potential. The economy has outperformed expectations driven by robust consumer spending, growing at an above-trend rate in Q2 and Q3 despite high interest rates. After the November election, the stock market rally intensified as investors focused on the incoming administration’s policy agenda.

Expectations for tax cuts, deregulation, and energy production are fueling hopes for stronger economic growth. The bond market echoes the confidence in equity markets, and corporate high-yield credit spreads are at levels not seen since May 2007.

The question on many minds is whether the momentum can continue in 2025. The S&P 500 currently trades at over 22x its next 12-month earnings estimate, a level not seen outside of periods like the late-1990s tech boom and the post-COVID recovery. Investors have shown a willingness to pay higher multiples, but with valuations at extremes, earnings could play an important role in determining the stock market’s next move.

The current bull market, which started in October 2022, is now in its third year, and it’s common to see investors shift focus to fundamentals as the bull market matures.

2025 is shaping up to be a year where companies will need to deliver on markets’ expectations to justify their high prices and investors likely will need to remain mindful about taking on more risk than necessary at this point in the market cycle.