Why Diversification Feels Broken Right Before It Works

Diversification can feel like a mistake when one part of the market is doing all the work.

That's the part investors don’t always appreciate.

Diversification is easy to believe in when everything's working. It's much harder to believe in when a narrow group of stocks is carrying the market higher and the rest of your portfolio feels like dead weight.

That's when the questions start.

Why own bonds?

Why own value stocks?

Why own international stocks?

Why own anything other than the part of the market that's clearly winning?

Those are fair questions. They're also the exact questions that tend to show up right before diversification matters most.

In our portfolio work, we don’t treat diversification as a prediction tool. It's a risk-management discipline. It's not there because we know exactly which part of the market will lead next. It's there because we don’t.

Diversification Isn’t Supposed to Feel Good All the Time

The purpose of diversification isn’t to beat the hottest asset class every year.

It's not designed to make every part of your portfolio look smart at the same time. It's not designed to keep up perfectly with whatever corner of the market is leading today. And it's not designed to eliminate frustration.

In fact, a diversified portfolio almost always owns something that feels disappointing.

That's not a flaw. That's the tradeoff.

If every part of your portfolio is working at the same time, there's a good chance your portfolio isn’t as diversified as you think. You may simply own different versions of the same risk.

True diversification means owning investments that behave differently under different conditions.

Some may lead when growth stocks are in favor.

Some may help when interest rates fall.

Some may provide stability when stocks are under pressure.

Some may become useful when market leadership broadens beyond the same small group of winners.

But because those investments behave differently, they won’t all work at once.

That's what makes diversification frustrating.

It's also what makes it valuable.

Diversification doesn’t guarantee a profit or protect against loss. No portfolio strategy can do that. But it can reduce the risk that one market segment, one economic outcome, or one investment theme determines the entire result of your plan.

That distinction matters.

The Problem Starts With Comparison

The hardest part of diversification isn’t the math.

It's the comparison.

When large-cap growth stocks lead for a long stretch of time, a balanced portfolio can feel too cautious. When a handful of companies are responsible for most of the market’s gains, anything outside of those companies can feel unnecessary. When the index keeps moving higher and your portfolio is moving more slowly, discipline starts to feel like a drag.

That's usually when investors begin to second-guess the plan.

At first, it's just an observation.

Then it becomes a question.

Then it becomes frustration.

And eventually, it can become action.

That's where investors get into trouble.

Because the decision to abandon diversification rarely feels reckless in the moment. It often feels rational. It feels like responding to the evidence. It feels like finally admitting what's been obvious for a while.

Why own the laggards when the winners are right there?

But that line of thinking can quietly turn a long-term investment plan into a performance chase.

And performance chasing has a way of showing up late.

Market Leadership Doesn’t Last Forever

The problem with chasing what's working now is that market leadership changes.

It doesn’t always change quickly. It doesn’t always change when valuations suggest it should. And it doesn’t always change in a way that feels obvious ahead of time.

But it changes.

That's why diversification exists in the first place.

It's not an admission that returns don’t matter. It's an acknowledgment that the future is uncertain.

Think about a period when large-cap growth stocks have led the market for several years. In that environment, a portfolio that also owns value stocks, small caps, international equities, or high-quality bonds may lag the most visible market benchmark.

The investor may look at the portfolio and feel like too many pieces aren’t pulling their weight.

Then conditions shift.

Interest rates move.

Earnings leadership broadens.

Valuations begin to matter again.

The economy slows, reaccelerates, or changes in a way investors didn’t expect.

Suddenly, the parts of the portfolio that looked unnecessary may become the source of stability, income, or return.

That doesn’t mean every diversifying asset will work perfectly. It doesn’t mean a diversified portfolio will avoid losses. And it doesn’t mean diversification will protect against every bad outcome.

But it does mean the portfolio isn’t dependent on one narrow market outcome continuing forever.

That's the point.

A concentrated portfolio feels best when the concentrated bet is working.

A diversified portfolio can feel less exciting during narrow leadership.

But when leadership changes, the difference matters.

Concentration Risk Often Feels Best Right Before It Matters

One of the reasons diversification is so difficult is that concentration risk can feel rewarding for a long time.

That's what makes it dangerous.

When one asset class, sector, or stock keeps leading, concentration doesn’t feel like risk. It feels like confirmation. The investor feels rewarded for having more exposure to the winners and less exposure to everything else.

This can be especially challenging for investors with concentrated company stock, equity compensation, or large positions that have appreciated over many years. The position may have created meaningful wealth. It may still be a high-quality company. It may still have a strong long-term story.

I worked with a client recently who was heading into retirement with a large share of their net worth sitting in company stock. They'd watched that stock grow across their entire career. Selling any of it felt like betting against their own success story.

I told them about a group of people I met years ago when I worked in Saint Louis. Most were former employees of Wachovia, and many were approaching retirement in 2008. Like my client, a large portion of their retirement savings sat in company stock. When the financial crisis hit and Wachovia collapsed, their savings went with it. Years of disciplined saving disappeared in a matter of months, not because they'd done anything wrong, but because their financial future depended entirely on one company continuing to succeed.

That story isn’t meant to scare anyone away from company stock. It's meant to separate two different questions. The first is, “Has this position performed well?” The second is, “What happens to my retirement plan if it stops?” My client’s stock may still have a bright future. But their retirement plan shouldn’t require it to.

For a deeper look at how to evaluate whether you’re sitting on a concentrated position and what to do about it, see Don’t Keep All Your Eggs in One Basket.

But none of that eliminates concentration risk.

A great company can still become an oversized position.

A strong sector can still become overowned.

A successful investment can still become too important to the family’s financial future.

That's why diversification isn’t just an investment concept. It's a planning concept.

The question isn’t simply, “What has performed best?”

The better question is, “How much of my financial life depends on this one thing continuing to work?”

That's a different question.

And for high-net-worth families, retirees, and investors with concentrated wealth, it's often the more important one.

The Risk Isn’t Just Losing Money

The risk isn’t simply that the market pulls back.

The bigger risk is that investors make a permanent decision based on a temporary environment.

That matters because most families aren’t investing for entertainment, ego, or quarterly bragging rights.

They're investing to support a retirement income plan.

To fund education.

To manage concentrated stock exposure.

To preserve liquidity.

To reduce the risk of being forced to sell at the wrong time.

To keep their broader financial life moving in the right direction.

For those investors, the portfolio has a job.

Its job isn’t to win every short-term comparison.

Its job is to support the plan.

That means some parts of the portfolio may look unnecessary for a while. Some may lag. Some may feel boring. Some may be hard to appreciate when the market’s favorite trade is working.

But every allocation should have a purpose.

Growth assets are there for long-term appreciation.

Defensive assets are there for stability and liquidity.

Income-producing assets are there to support cash flow.

Diversifying assets are there because the future doesn’t always look like the recent past.

The question isn’t whether every piece is outperforming today.

The question is whether the total portfolio is built to survive different market environments.

Diversification Has to Be Judged Against the Plan

A diversified portfolio shouldn’t be judged only against the market’s current favorite.

It should be judged against the plan it was built to support.

That includes the investor’s time horizon, spending needs, withdrawal strategy, tax situation, liquidity needs, risk tolerance, and ability to stay invested when markets become uncomfortable.

For an accumulator, diversification may be about avoiding overdependence on one source of return.

For a retiree, it may be about managing sequence-of-return risk and maintaining enough stability to support withdrawals during difficult markets.

For an executive with equity compensation, it may be about reducing the risk that career income, company stock, and long-term wealth are all tied to the same business outcome.

For a family stewarding generational wealth, it may be about preserving flexibility across market cycles rather than maximizing exposure to the latest winner.

The right portfolio isn’t the one that looks best in hindsight.

It's the one the investor can actually live with, fund goals from, and stick with when the environment changes.

That's where diversification earns its place.

Not because it always feels good.

Because it helps keep the plan from depending on one version of the future.

Don’t Confuse Frustration With Failure

There will always be moments when diversification feels broken.

There will always be a stock, sector, asset class, or theme that makes the disciplined portfolio look dull by comparison.

And there will always be investors who are tempted to simplify the portfolio around whatever's worked best recently.

But temporary frustration isn’t the same thing as strategic failure.

Sometimes diversification feels broken because one part of the market has dominated for a long period of time.

Sometimes it feels broken because the benefit hasn’t been needed yet.

Sometimes it feels broken because the thing it's designed to protect against hasn’t happened.

That doesn’t make it useless.

It makes it easy to underappreciate.

The real test of diversification doesn’t come when the market’s current favorite is still leading. It comes when leadership changes, when expectations shift, when volatility returns, or when investors are reminded that no single trade works forever.

By then, it may be too late to rebuild the portfolio without paying a price.

So don’t judge diversification by whether it keeps up with the market’s current favorite.

Judge it by whether your portfolio can survive a change in leadership.

Because by the time diversification feels obvious again, the opportunity to stay disciplined may have already passed.

Here's the Cost of Moving to the Sidelines

Markets rarely tempt investors to make bad decisions when things feel calm.

They tempt investors when the headlines are loud, losses are fresh, and moving to cash feels less like panic and more like prudence.

That is what made the first quarter so difficult.

From its late-January high through the end of March, the S&P 500 fell nearly 10% as the U.S.-Iran conflict pushed oil prices more than 60% higher. Headlines about the Strait of Hormuz, rising energy costs, and the potential economic fallout created the kind of environment where investors naturally begin asking a very human question:

Should I get out before this gets worse?

Market Timing Rarely Feels Like Market Timing

That question is understandable. It is also dangerous.

The problem with market timing is that it rarely feels like market timing in the moment. It feels like caution. It feels like discipline. It feels like protecting what you have built.

But getting out is only half the decision.

You also have to know when to get back in.

And that second decision is often the harder one.

When ceasefire talks emerged in late March, markets quickly began to recover. Investors who moved to the sidelines during the selloff were then faced with a new question:

Do I get back in now, after the market has already bounced, or do I wait until things feel calmer?

That is where many investors get hurt.

By the time the environment feels safe again, the market has often already moved. The recovery does not usually announce itself ahead of time. It often begins while the headlines are still uncomfortable, while the outcome is still uncertain, and while investors are still waiting for confirmation.

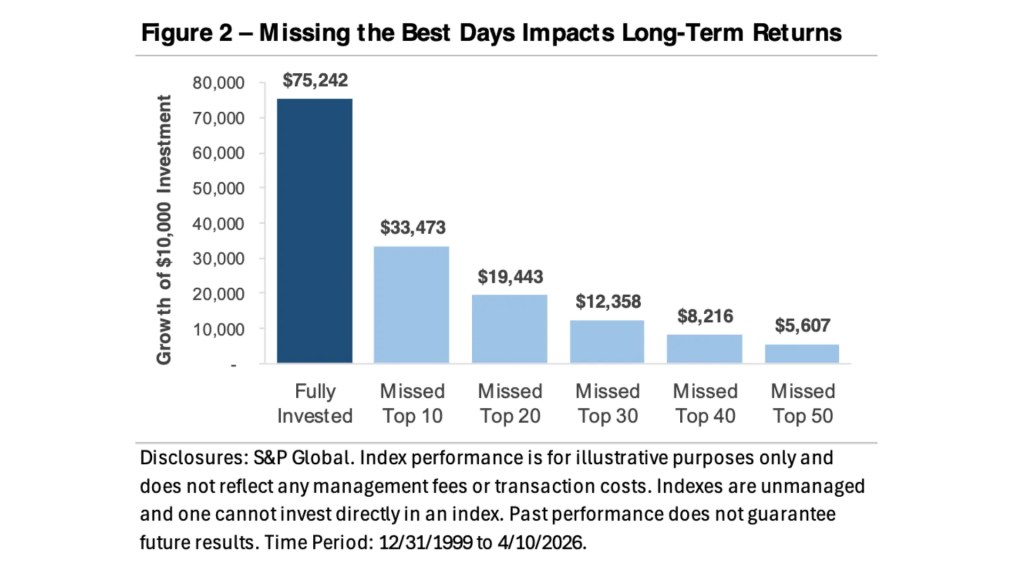

The Best and Worst Days Arrive Together

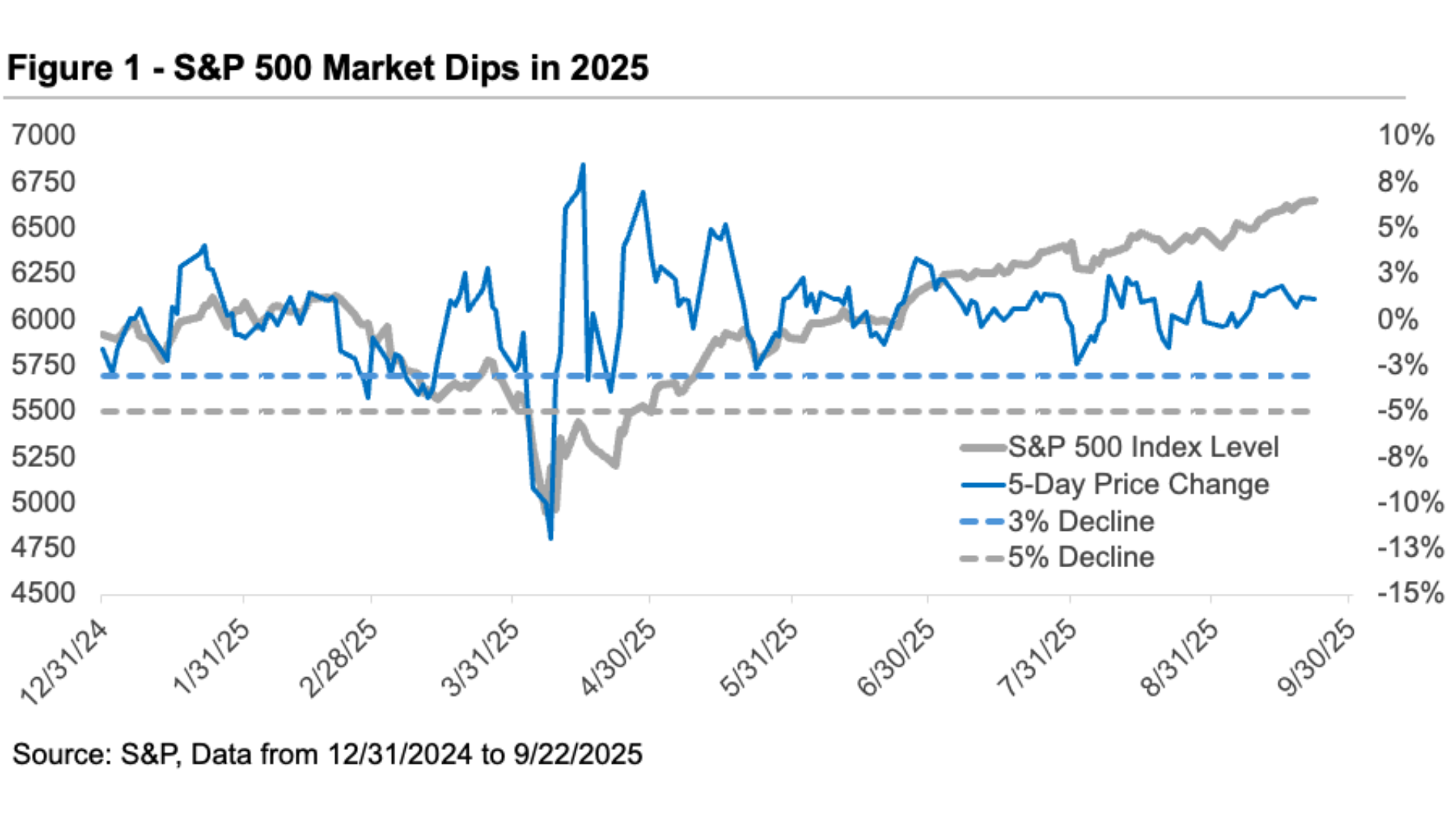

That is why the best and worst days in the market tend to arrive close together.

Figure 1 illustrates this pattern. The chart shows the S&P 500's daily returns over the past 26 years and highlights an important truth: the market's largest moves tend to cluster. The biggest selloffs do not happen in isolation. They are often surrounded by some of the strongest rallies.

We saw this during the 2008 financial crisis. We saw it during the 2020 pandemic. We saw it during the tariff-driven volatility of 2025. And we saw it again during the recent U.S.-Iran volatility, when the S&P 500 posted its strongest daily return since April 2025 on optimism around a possible ceasefire, only days after escalating tensions had pushed stocks lower.

That is the uncomfortable reality of investing through uncertainty.

The same environments that produce sharp selloffs often create the conditions for sharp recoveries.

Missing a Few Days Can Cost You Decades

Figure 2 puts a dollar amount on that lesson. A $10,000 investment in the S&P 500 on December 31, 1999, would have grown to $75,242, despite a period that included the dot-com bust, the global financial crisis, the pandemic, inflation shocks, rising rates, wars, and political uncertainty.

That result did not come from avoiding every downturn.

It came from staying invested through them.

Missing just the 10 best trading days would have reduced the ending value to $33,473, less than half the fully invested result. Missing the 20 best days would have lowered it to $19,443. Missing the 30 best days would have brought it down to $12,358. And missing the 50 best days would have turned the original $10,000 into just $5,607.

In other words, an investor could have lived through a period when the market created substantial wealth, yet still lost money by missing too many of the right days.

That is what makes market timing so costly.

You do not have to be wrong all the time. You only have to be wrong at a few critical moments.

Bottom Line

This year's volatility may feel unsettling, but it reinforces one of the most important principles of long-term investing: the plan has to be built before the panic arrives.

A well-constructed financial plan does not assume markets will always cooperate. It assumes there will be downturns. It assumes there will be recessions. It assumes there will be geopolitical shocks, energy price spikes, scary headlines, and stretches of time when discipline feels uncomfortable.

That is why cash reserves matter.

That is why diversification matters.

That is why rebalancing matters.

And that is why your investment strategy should be connected to your broader financial plan, not just to your feelings about the latest headline.

Selling during a decline may provide temporary emotional relief, but it also locks in losses and creates a difficult re-entry problem. Staying invested does not mean ignoring risk. It means managing risk through a plan rather than reacting to fear.

What the Market Actually Rewards

The market does not reward perfect timing.

It rewards patience, discipline, and the ability to stay anchored when the headlines are loud.

And as the first quarter reminded us, missing just a few of the market's best days can come at a very high cost.

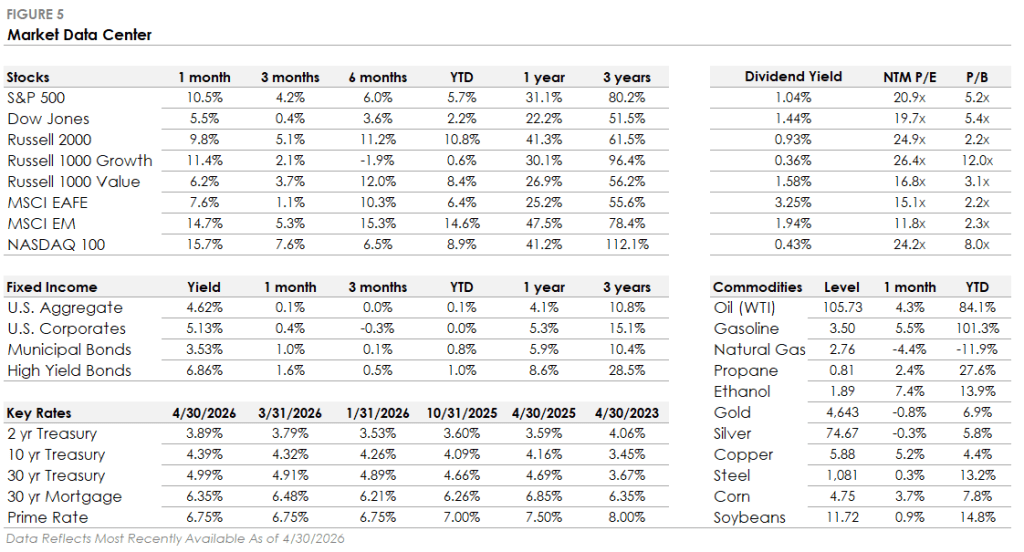

1Q26 Market & Economic Recap & 2Q26 Outlook

Key Updates on the Economy & Markets

The first quarter of 2026 was one of those periods that reminded investors why markets don't move in a straight line.

Stocks started the year on solid footing with January modestly positive, February quiet, and then March arriving with a jolt. The escalation of geopolitical tensions in the Middle East, including the closure of the Strait of Hormuz, sent oil prices surging and rattled markets in ways that few anticipated heading into the year.

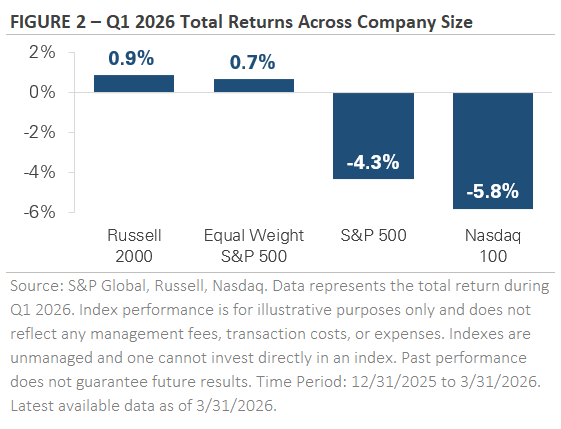

By the time the quarter closed, the S&P 500 was down -4.3%, with the bulk of that decline concentrated in a single month. And if you looked only at that headline number, you might walk away with a grim picture.

But the quarter was more nuanced than the index suggests, and I think it's worth taking a step back to understand what actually happened and what it means for your portfolio going forward.

Higher Oil Prices Changed the Rate Cut Conversation

Indeed, to understand why March felt so disruptive, you have to start with oil.

Crude prices had already been moving higher before tensions escalated with supply concerns tied to Venezuelan output pushing prices up nearly 13% in January, and climbing another 4% in February as geopolitical risks continued to build.

Then March arrived.

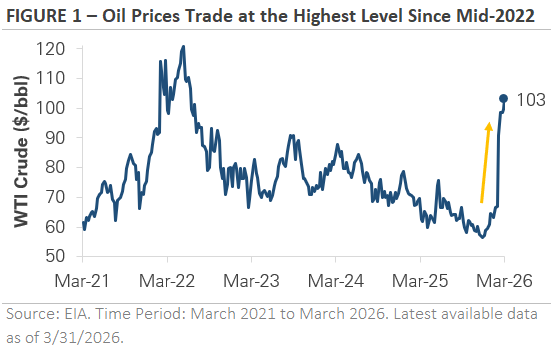

The conflict between the U.S. and Iran intensified, and the closure of the Strait of Hormuz, a waterway that carries roughly 20% of the world's oil, sent crude prices surging nearly 50% in a single month. For the full quarter, oil prices rose more than 70%, reaching levels not seen since mid-2022.

And why does that matter for your portfolio?

Because oil prices don't exist in a vacuum. Higher energy costs flow through to what consumers and businesses pay for goods and services. And as a matter of fact, you've likely already noticed it at the pump, as gasoline prices have risen nearly a dollar per gallon since late February.

And this is happening at a moment when inflation was already showing signs of firming before the conflict began. The Federal Reserve's preferred inflation measure, Core PCE, remains near 3%, and producer prices have been trending higher.

So then, coming into 2026, the market expected the Federal Reserve to cut interest rates two to three times by year end.

That expectation quietly eroded as the quarter progressed.

And by the time March ended, those rate cuts had been priced out entirely, and there was even early discussion about whether a rate hike might come back into the conversation.

The situation is still evolving.

The Strait of Hormuz remains closed as of quarter-end, negotiations are ongoing, and oil is trading near $100 per barrel, a signal that the market expects the disruption to persist for some time.

The April and May inflation reports will be the first data to fully reflect the energy price surge, and they'll go a long way toward shaping the Federal Reserve's next move. In the meantime, headlines out of the Middle East are likely to continue influencing how both stocks and bonds behave in early Q2.

Diversification Quietly Did Its Job

Now, one of the most important, and most overlooked, stories of Q1 was what happened beneath the surface of the S&P 500.

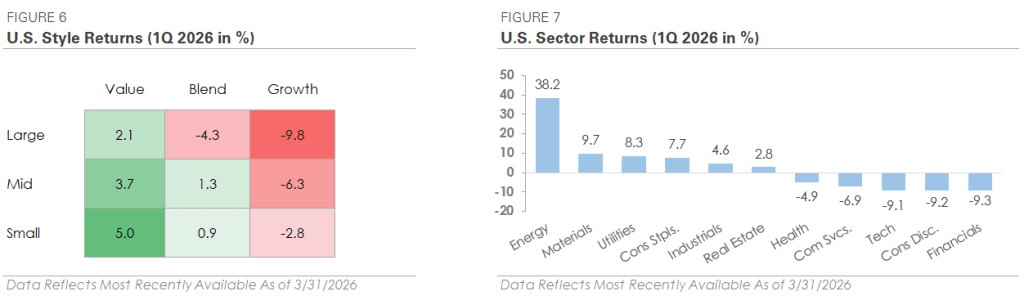

The S&P 500 is a market-cap weighted index, meaning the largest companies carry the most influence over the index's return. When those large companies, particularly those in the technology sector, sold off, the headline number felt worse than what most diversified investors actually experienced.

To put it in perspective, the average S&P 500 stock outperformed the broad index by nearly 5% in Q1. Small-cap stocks, as measured by the Russell 2000, actually gained nearly 1%. And international stocks finished the quarter with a gain of nearly 1% as well, outperforming the S&P 500 by more than 5 percentage points.

And what drove that gap? Well, there were two competing forces at work.

The first was a rotation away from mega-cap tech stocks. For the past two years, a handful of the largest companies drove the majority of the market's gains.

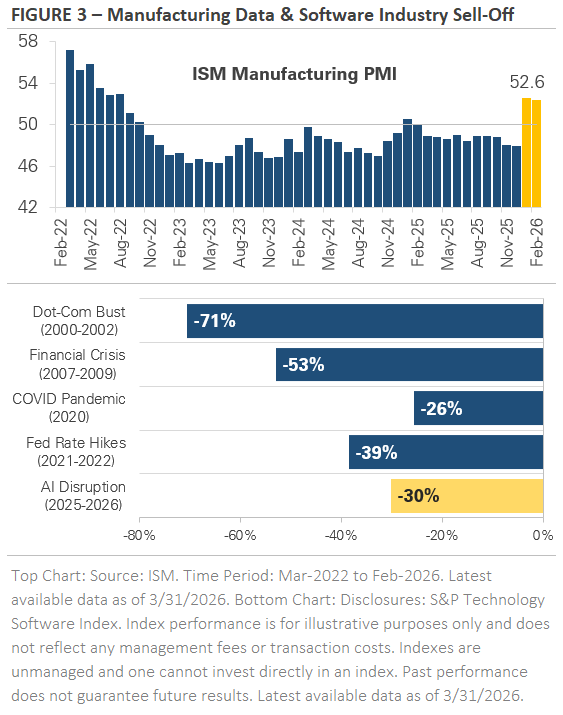

In January, investors started moving away from that concentrated trade. The rotation accelerated in February when concerns about artificial intelligence disruption spread through the software sector, and markets began to price AI not just as a productivity enhancer, but as a potential replacement for entire categories of professional services.

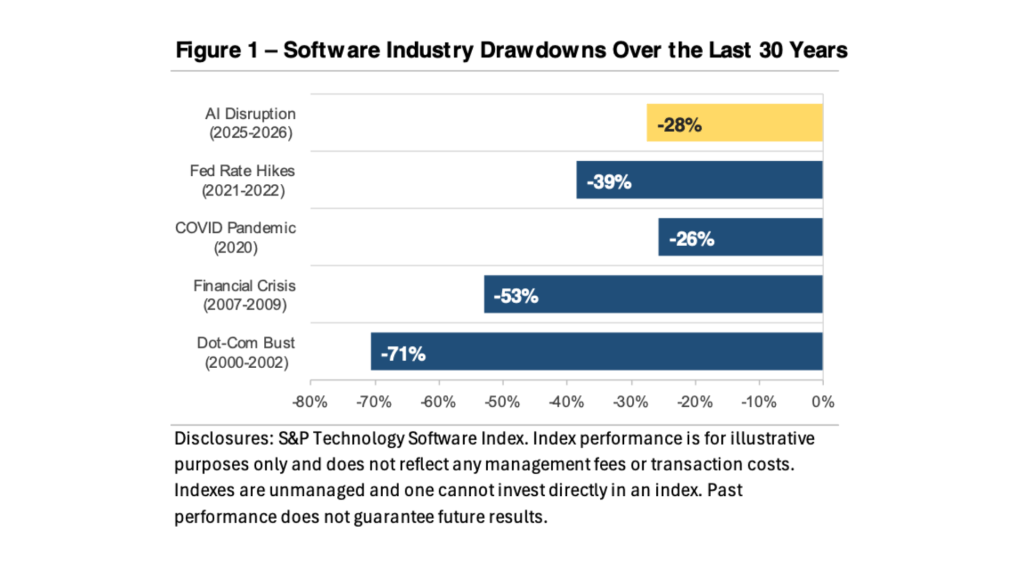

The software sector has now declined nearly 30% from its peak last October, one of the largest non-recessionary drawdowns in over 30 years.

The second force was a genuine improvement in manufacturing activity. After spending nearly a year in contraction, the ISM Manufacturing Index crossed into expansion territory in February and held there in March.

That's a meaningful sign for the economy and potentially for corporate earnings.

Indeed, the manufacturing sector had been a soft spot in the economy since 2022, and the data suggested it was gaining real traction before the conflict began. Industrials was one of the few sectors to set a new all-time high during the quarter.

Across the broader equity market, six of the eleven S&P 500 sectors outperformed the index, a sharp contrast to recent years when gains were driven by just a few names. Energy led everything with a 38% return as oil surged.

Materials, Utilities, and Consumer Staples each gained more than 7.5%. On the other end, Technology, Consumer Discretionary, and Financials each declined more than 9%.

The gap between the best and worst sectors was wide. But for investors with diversified exposure across company sizes, sectors, and geographies, the quarter felt more moderate than the S&P 500 return alone would suggest.

Diversification didn't eliminate the volatility. It helped manage it, and that's exactly what it's designed to do.

Bonds Navigated a Volatile Quarter

The bond market had its own version of the quarter's turbulence.

Interest rates rose in January as tariff concerns resurfaced, then fell sharply in February as growth worries, particularly around AI disruption, pulled investors toward safer assets.

March reversed that move quickly.

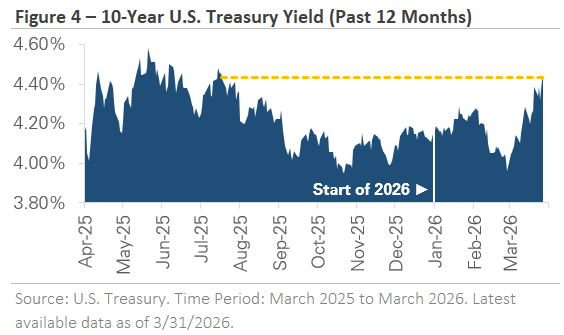

And as oil prices spiked and rate cut expectations faded, yields climbed again. The 10-year Treasury yield ended the quarter near 4.32%, its highest level since mid-2022. The 2-year yield rose nearly 0.35% for the quarter, reflecting how quickly rate cut expectations shifted.

The Bloomberg U.S. Aggregate Bond Index finished the quarter flat, a meaningful step down from the 1% or better returns it produced in each of the prior four quarters. Corporate bonds modestly underperformed higher-quality Treasuries, and credit spreads widened to their highest levels since early 2025.

That widening reflects caution, not crisis, with corporate spreads remaining well below the levels reached during past recessions and financial dislocations.

And what are we to take of all this data?

Well, the bond market is telling us that investors are being careful, but it's not telling us something is broken yet.

What to Watch in Q2

As we move into the second quarter, the central story remains the same: the Middle East, oil prices, inflation, and what the Federal Reserve does next.

Progress toward resolving the Strait of Hormuz closure would ease energy costs and give the Fed more room to maneuver on rates. However, a prolonged disruption means higher oil prices have more time to work through to consumers and businesses, keeping inflation elevated and leaving the Fed in a difficult position.

From a data perspective, the April and May inflation reports are the ones to watch. They'll be the first readings to capture the full impact of higher energy costs, and they'll shape the rate outlook for the rest of the year.

While you're watching those headlines, I want to offer some perspective on the bigger picture.

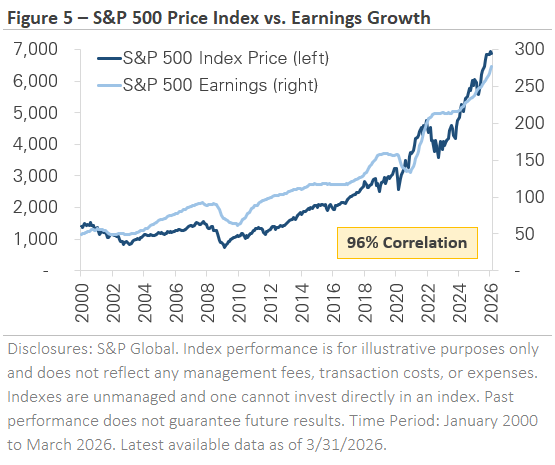

Over the past 26 years, corporate earnings and stock prices have moved together with a 96% correlation.

When earnings rise, prices generally follow.

When earnings deteriorate, as they did in 2001, 2008, and 2020, prices tend to fall with them. What's notable about today's environment is that earnings estimates have continued to rise even as the S&P 500 has pulled back.

Analysts still expect earnings growth in the coming quarters, and profit margins to remain healthy.

Put differently, the market's decline in Q1 was driven by uncertainty around oil, inflation, and Federal Reserve policy, not by a deterioration in the underlying fundamentals that drive stock prices over time.

And that distinction matters.

Certainly, uncertainty is uncomfortable, but it's different from a breakdown in the economic foundation.

The quarter also reinforced something I believe deeply in that staying invested, staying diversified, and keeping a long-term perspective is one of the most effective strategies available to investors. The areas of the market that led over the past two years underperformed in Q1.

Investors with broad exposure across company sizes, styles, and geographies experienced a meaningfully different quarter than the headlines suggested.

When it comes down to it, markets will work through the uncertainty in the Middle East. The data will come in, the Fed will respond, and conditions will shift, as they always do.

In the meantime, your plan was built for periods like this one, and I remain confident in the approach we have in place.

Here’s Why Concentration Risk Matters

Lately, investors have had no shortage of headlines to process. Geopolitics, interest rates, and questions about the economy have all competed for attention. Those stories matter, and they can certainly move markets in the short run.

But beneath those headlines, another shift has been taking place. And that’s that market leadership has been changing in a subtle way.

And this change is worth paying attention to because leadership changes are often where concentration risk gets exposed. That’s because the stocks and sectors that led in one environment do not always lead in the next. And when the market begins to reassess those winners, the repricing can happen quickly.

This is one reason diversification still matters, especially in a year like this.

A Reminder From Software Stocks

One of the clearest examples has come from the software industry, which has fallen nearly 30% from its peak since last October. The move makes it one of the largest non-recessionary drawdowns in the group in more than 30 years.

And that historical context matters because the two biggest software drawdowns before this one happened during recessions, in the dot-com bust and the 2008 financial crisis, when earnings were under pressure and businesses were pulling back on spending.

Now, it’s worth noting that the 2022 decline was different because that selloff was driven by the Federal Reserve’s aggressive rate-hiking cycle, and software stocks fell nearly 40%.

This time, however, the catalyst appears to be different. The market is not primarily reacting to recession fears or rising rates. Rather, it appears to be reacting to uncertainty around artificial intelligence and what it could mean for future business models as we’ve discussed in previous reports.

What Changed Earlier This Year

The selloff in software picked up speed in January and February after a series of AI product launches suggested that general-purpose AI tools may be able to handle tasks that had previously required specialized software, often at a lower cost.

That mattered because it changed the market’s framing.

For the past two years, AI had largely been viewed as a productivity tool, something that could help existing businesses become more efficient. But earlier this year, investors began asking a different question: what if AI does not simply improve some business models, but starts to pressure or replace parts of them?

Software stocks felt that shift first. Then the concern spread into other areas, including financial data providers, commercial real estate services, and logistics companies.

In other words, this was not just about one corner of the market having a bad stretch. It was a broader reminder that when investors begin to question the durability of future earnings, yesterday’s leaders can suddenly look much more vulnerable.

Where Things Stand Now

By late February, some of the more extreme fears around AI disruption began to cool, and markets started to stabilize. Analysts pushed back on the most aggressive replacement narratives, and the conversation became more measured.

The question shifted from whether AI would replace entire industries to which businesses are genuinely vulnerable, and which may be able to adapt, defend their position, or even strengthen it.

Since then, some of the hardest-hit stocks have rebounded. Even so, the software industry remains down more than 25%, and the broader question is still unresolved. AI is likely to remain a force that shapes leadership across markets, especially in software and other professional-service-oriented industries.

What This Means for Your Portfolio

For investors, the lesson is not that every new innovation requires a major portfolio change.

The lesson, rather, is that market leadership can shift quickly, and concentrated positions can become more vulnerable when the narrative changes. Even strong, well-established businesses can be repriced in a short period of time when the market starts applying a different set of assumptions to future earnings.

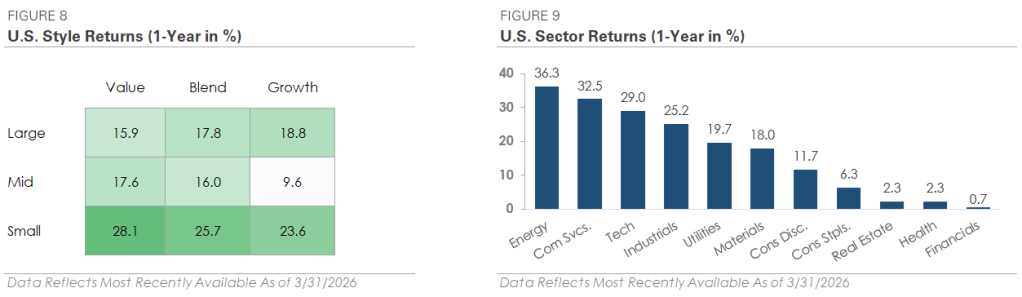

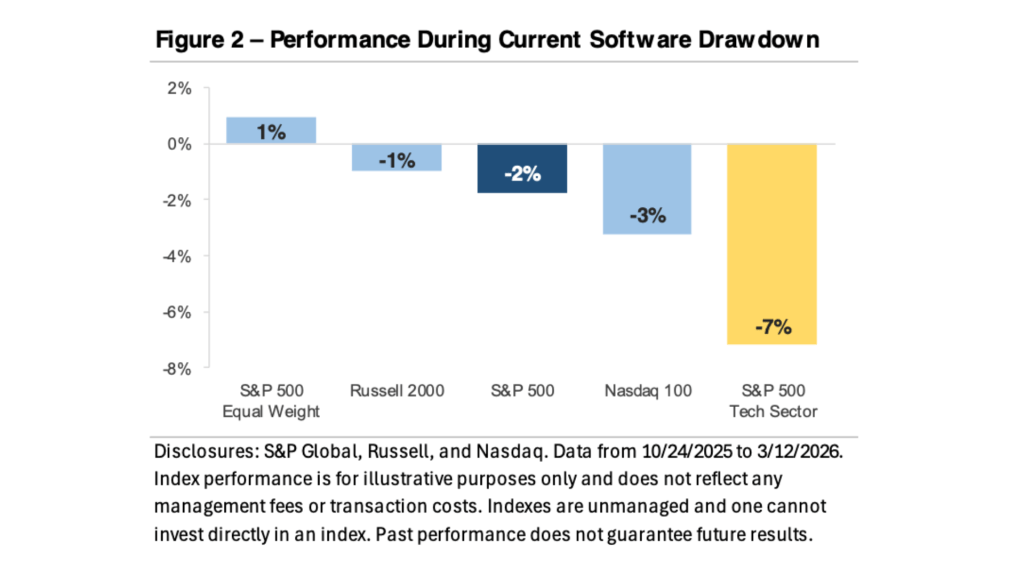

At the same time, this period has also been a useful reminder of why diversification works. The pressure has been meaningful in some concentrated parts of the market, but much more limited for diversified investors. International stocks and the average S&P 500 stock have posted gains, while small caps, the broader S&P 500, and the Nasdaq 100 are each down only modestly.

That does not remove uncertainty. But it does reinforce an important principle.

A disciplined portfolio is built not just for the trends we expect, but for the leadership changes we do not. And in an environment like this, diversification across sectors and asset classes remains one of the most practical ways to manage risk without losing sight of long-term goals.

Market Volatility – Here’s What to Do About It…

After what feels like nearly a year of markets going straight up, even a modest pullback can feel like a personal hit.

One week you’re checking your account balances with a little extra confidence. And then the next week, when risk assets are sliding and headlines are loud it can feel like the mood shifts fast, right?

So here’s the real question: Should you be worried about market volatility, or should you be expecting it?

Why volatility feels worse after a long rally

Well, while I can tell you that market volatility is a natural part of any market cycle, you’re likely to feel differently these days.

That’s because when markets grind higher for months, we get used to it. That steady climb starts to feel normal and it starts to feel earned.

And when the market finally takes a breather, it can like something broke and make you want to put your money into something “safe”.

The fact is, however, that markets do not move up in a straight line, even when the market and economic backdrop is strong. To be sure, routine pullbacks are part of healthy markets, and part of what keeps longer-term uptrends from overheating.

Even so, minor pullbacks could feel like a sign of a bigger impending move for some individuals.

So, what do you do if you’re feeling this way?

Well, the first step is a simple reframe.

Why this pullback feels different: AI disruption and shifting leadership

Indeed, one reason this bout of volatility feels so intense is that it isn’t only about prices. It’s also about narratives, or the stories that drive market behavior.

Lately, markets have been reacting sharply to AI-related news, including concerns that rapid innovation and shifting leadership can pressure yesterday’s winners and accelerate competitive disruption.

For example, law professionals used to rely on expensive software to give them an edge in their practice. Today, AI can do what the attorneys and software do at a fraction of the cost.

This matters because investors often underestimate how quickly a “winner” stock can turn into a “why is this selling off?”

Because here’s the thing: AI is not merely a theme. It’s a force that can reshape profit pools.

What seemed like an mere augment to business processes is now demonstrating, in real-time, how quickly the innovation can displace earnings potential in more legacy parts of the tech industry.

And when that happens, the market rarely reprices politely over years. More often, it reprices in weeks. And that volatility is what we’re seeing today.

So yes, news about AI being disruptive, including to seasoned incumbents, can absolutely be a catalyst for volatility. The risk is not that the AI story disappears.

The risk is that markets get ahead of themselves, timelines disappoint, competition shows up faster than expected, and leadership rotates while investors are still anchored to the last set of winners.

Nevertheless, time and time again, markets have shown how quickly sentiment can change when the market decides the future arrived sooner than expected.

Markets participation is broadening, and that's not a bad thing

There’s another dynamic worth paying attention to and that’s that market participation is broadening, even as the overall indices chops around.

In other words, it isn’t just the same ten stocks pushing the markets higher. Lately, investors are paying more attention to broader areas of the market, which is a theme we’ve highlighted in recent months, including meaningful moves in small caps.

Now, broadening isn’t a bad thing because it can be a sign of a healthier market structure. But, it does comes with a tradeoff.

That’s because when leadership rotates and participation broadens, dispersion increases. In other words, some sectors rally while others stall out or drop. And this increased disparity can make the market feel more volatile even if the index level does not look dramatic.

So, if you’re looking at your portfolio and thinking, “Why does this feel worse than the headlines suggest?” it’s because the market movements more uneven these days.

The cycle is later, but that does not mean recession is imminent

Another reason we’re likely seeing more market volatility is that we’re likely later in the economic cycle.

Indeed, the latest read on fourth quarter GDP and softening labor market data suggest that economic growth is slowing. This is leading to more economic surprises and frankly, markets are more sensitive to surprises than they were earlier in the cycle.

But “late cycle” does not automatically mean “recession is imminent.”

To be sure, in one of our previous reports, we described an environment where growth remained positive even as the economy softened, with the narrative focused on slowing without slipping into recession.

We have also framed the current data backdrop as modest economic growth, while acknowledging that policy mistakes could change the path.

So yes, the cycle is later.

But the base case is still slower growth, not collapse.

How often does volatility happen?

So then, should we be worried about volatility?

Well, once you understand the frequency of market moves, you’re more likely to stop treating volatility like an emergency.

Because the fact of the matter is that pullbacks happen a lot.

Indeed, in our published work last year, we noted that market dips around 3% have historically happened about seven times per year on average, and declines of 5% or more occur roughly three times annually.

That didn’t happen in 2025.

So, if you’ve felt like you’ve been living through a year with no pullbacks, you’ve been waiting for something that simply feels like it does not show up very often.

Zoom out even further and the point gets even clearer.

For example, in our 2Q25 market update, we shared that since 1928 the S&P 500 has experienced an intra-year decline of at least 5% in the vast majority of calendar years, with the median intra-year drop around 13%.

So volatility is not rare, it’s routine.

The truth is that big down days are rarer, but they still get the headlines.

And that’s the trap, isn’t it?

The scary days are memorable. The normal days are forgettable. And the market uses that to mess with your confidence.

Because the truth is that corrections are not an “if,” they’re a “when.”

When it comes down to it, some investors like a clean framework like, “Markets are due for corrections every 18 to 24 months.”

Whether you like that cadence or not, the core conclusion holds either way.

Smaller pullbacks happen multiple times per year. And, history has shown that a 5% drawdown typically happens in almost every calendar year.

So the takeaway is straightforward: Corrections are not an “if,” they’re a “when.”

What do we do when uncertainty shows up?

So what should you do when market volatility picks up? Well, this is where most investors go wrong.

They spend most of their energy trying to predict what happens next instead of focusing on what they control.

And the one thing you can control is whether you react or respond.

#1: Stick to Your Discipline

Because in moments like this, the winning move is often boring. It’s about sticking to a disciplined investment strategy.

It’s staying diversified.

It’s staying committed to a process built for markets that occasionally misbehave. It’s dollar cost averaging into your portfolio and rebalancing regardless of what the markets are doing.

It’s a point we have made consistently in our updates, including the idea that trying to sidestep volatility through timing can mean missing the best days in the markets, potentially costing you thousands, while staying invested gives compounding room to work.

#2: Review Your Cash Management Process

The other thing you can control is whether you are forced to sell investments at an inopportune time.

That’s where cash management comes in.

The simplest way to avoid panic-selling is to remove the need to sell. Indeed, over the years, we’ve reinforced the use of a cash as a buffer to help you avoid selling at the wrong time, and holding cash reserve ranges that are often appropriate depending on whether you’re working or approaching retirement.

It’s about creating your “sleep-well number,” or the level of cash that lets you stay committed to your strategy when headlines get uncomfortable.

#3: Stick to Your Plan

And finally, you can control how well you’re sticking to your broader financial plan when markets start to feel uncontrollable.

Keep doing the work outlined in your plan, because we’ve already planned for moments like these.

In the short term, markets can feel like a voting machine. In the long term, they act more like a weighing machine.

Pullbacks help reset expectations, cool overheated parts of the market, and set the stage for future gains.

Historically, markets have recovered over time, even through major crises.

So the question is not, “Will this feel uncomfortable?”

It will.

The better question is, “Do I have a plan that assumes discomfort shows up from time to time?”

Bottom line

Should you be worried about market volatility?

Not if you’re prepared for it.

Because the fact is that volatility l is not a surprise guest, it’s part of the ticket to achieving your long-term goals.

So if you’re feeling unsettled right now, then it’s time to get back to the basics. That involves staying disciplined, knowing your sleep-well cash number and keeping your focus on the long-term plan.

That’s how you move through uncertainty without letting it drive the bus.

New Highs, Old Lessons: Staying Invested and Diversified in an AI-Driven Market

It has not felt like a normal year in markets.

Between headlines about trade tensions, elections, and interest rates, many investors describe this year as "uncertain" or even "uncomfortable." Yet when you step back from the day-to-day noise and simply look at the scoreboard, you see something very different:

The stock market is quietly having another record-setting year.

A Market that Keeps Finding New Highs

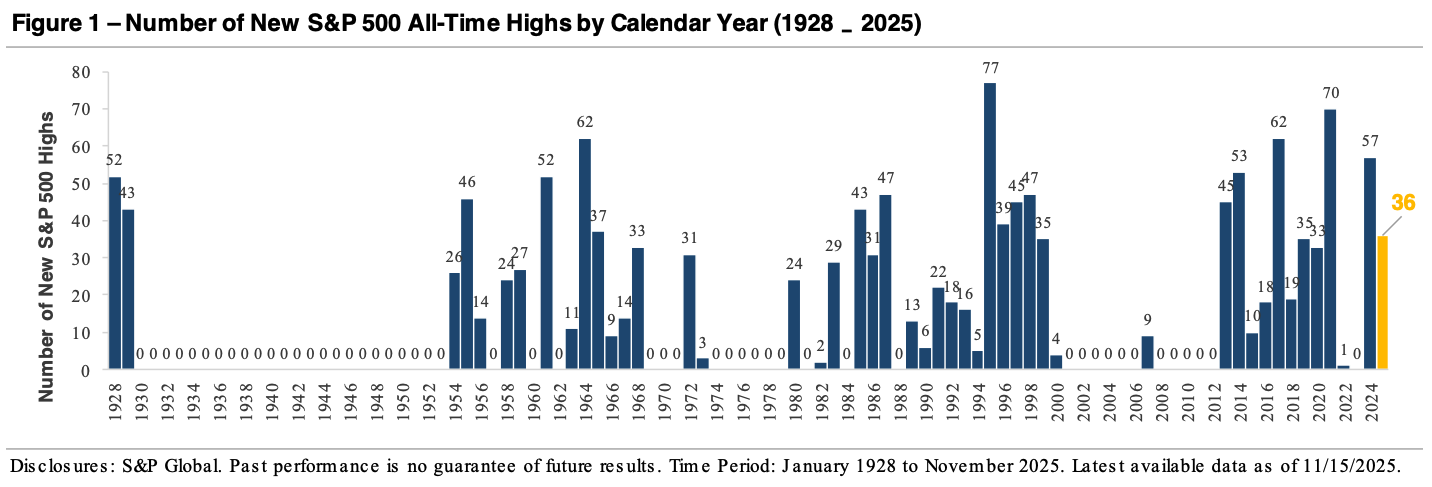

So far this year, the S&P 500 has set 36 new all-time highs. And while that's fewer than last year's pace, it still ranks 18th out of the past 98 years. In other words, this is not an ordinary year, it's a year in which the market has spent a lot of time in record territory.

And it is not just one index. The S&P 500's strength is part of a broader pattern across major equity markets. For example, the Nasdaq composite index has logged 36 new highs, the Dow has posted 17, and even the small-cap Russell 2000 index, which spent years stuck below its 2021 peak, and has now recorded six new highs after finally breaking through that old ceiling.

So then, if you only checked your account periodically, you might simply see "up double digits" and move on. But, the more interesting story lives beneath those numbers: what is driving these gains, and how healthy is this advance?

The AI Boom: Powerful Tailwind, Narrow Leadership

And so, what's been driving this year's rally? Well, the clearest theme this year has been artificial intelligence (AI).

That's because companies are spending hundreds of billions of dollars to train AI models, to build and cool data centers, and to secure the power needed to run it all. To this point, Nvidia recently became the first company to reach a market value above $5 trillion. At the same time, large technology firms such as Microsoft, Amazon, Alphabet, and Meta are reporting strong growth that is directly tied to demand for their cloud and AI-related services.

And as capital flows into this theme, AI-linked stocks have moved sharply higher. Because many of these companies are very large, their gains have an outsized effect on the indices they belong to. That's one reason the broad market can look very strong at the index level even while many individual companies are treading water or declining.

Indeed, you can see this in the Russell 1000 Index, which tracks a wide universe of large and mid-sized U.S. companies. For example, on a market-cap-weighted basis, the Russell 1000 is up about +14% year-to-date, which is a number you are most likely to see in headlines.

However, if you give every stock an equal weight, the return is closer to +6%. And if you line up all the individual companies and look at the one in the middle, the median stock is up only about +2%. Put differently, nearly half the companies in the index are actually negative for the year, with 462 names in the red.

What this tells us is simple: A relatively small group of very large companies, powered by the AI theme, is doing a lot of the heavy lifting. With this narrow leadership, the average stock is not enjoying the same party the indices suggest.

Beyond AI: the Fed, the Economy, and Earnings

With all that said, while AI is getting the headlines, it's not the only driver of this market.

That's because after a nine-month pause, the Federal Reserve restarted its rate-cutting cycle in September. And over the past two months, the Fed has lowered interest rates by a total of 0.50%. This is important because lower borrowing costs help ease pressure on consumers and businesses alike. And they also support higher valuations for risk assets like stocks. On top of that, markets tend to look ahead. Expectations for additional cuts in the coming year have created a tailwind for equities.

At the same time, the U.S. economy has proven more resilient than many expected as it has continued to grow while navigating a long list of headwinds, including trade policy and tariffs, geopolitical tensions, political noise, and even a government shutdown. And make no mistake, none of those issues are trivial, and yet the economy has continued to move forward.

At the same time, corporate earnings tell a similar story. Profit growth remains solid, and third-quarter earnings came in ahead of expectations. This is imporant because over long periods of time, stock prices tend to follow earnings. And while it doesn't mean that they move in a straight line, what it does mean, is that healthy, growing profits provide a fundamental foundation underneath the price action we see.

Put together, you have a powerful combination of an economy that is bent but not broken, a central bank that has shifted from "higher for longer" to modest cuts, and a highly visible growth theme in AI that is attracting both capital and optimism.

The Emotional Challenge: Good Markets, Bad Headlines

For many investors, this year has not felt like a year in which the S&P 500 returned nearly +15% and notched 36 new highs.

The reason is that the emotional experience of investing rarely matches the outcome in the numbers.

Because here's the thing: if you had known the headlines in advance at the start of the year, you might have assumed the market would struggle with trade tensions, policy uncertainty, geopolitical flare-ups, a government shutdown, and elections on the horizon.

In that environment, it would have been very easy to say, "I will step aside until things calm down."

The problem is that markets often climb a wall of worry.

By the time the news feels "safe," a significant portion of the returns is already behind you. So then, stepping aside means you not only have to decide when to get out, you also have to decide when to get back in. That is the essence of market timing, and history shows that it is extremely difficult to do consistently.

This year has been another reminder that trying to outguess the market based on headlines can be costly. Missing just a handful of strong days or weeks can put your long-term goals at risk.

The Planning Lesson: Stay Invested, then Stay Diversified

Every year offers a different lesson for investors.

And this year has underscored the value of staying invested through periods of uncertainty. That's because investors who allowed headlines to push them to the sidelines risked missing out on meaningful returns and the long list of new highs.

Looking ahead, the next lesson may focus on a different lesson: diversification.

When a relatively small group of AI-linked stocks is carrying much of the market's gains, it can be tempting to chase what's working and load up on whatever has gone up the most. And that approach may feel smart in the moment, especially when everyone is talking about the same names.

But here's the thing: true diversification is less exciting. It means owning parts of the market that are not currently in the spotlight. It means keeping exposure to areas that have lagged, even when the story feels old or uninspiring. It means remembering that the goal is not to win every short-term race, but instead to finish the marathon.

If 2025's lesson is that staying invested matters, then 2026 may remind us that how we stay invested matters just as much. That's where a portfolio that is thoughtful, diversified, and aligned with your financial plan is better positioned to weather changes in leadership, economic surprises, and policy shifts.

Bringing it Back to Your Plan

As always, the most important market is the one that lives inside your own financial plan.

The question is not, "Can I predict the next 36 new highs?" The better questions are:

- Are my investments aligned with the goals I want to accomplish?

- Is my portfolio diversified across different asset classes, sectors, and regions, or is it overly dependent on a single theme?

- Am I relying on headlines to make decisions, or am I following a clear, disciplined process?

Our work together is designed to keep you anchored to that process. Markets will continue to move from one narrative to another: AI, interest rates, elections, something else after that. Your plan should remain the steady reference point that guides how we respond.

If you have questions about how this year's market dynamics are affecting your portfolio, or if you are wondering whether your diversification is where it needs to be, let us talk. The goal is the same as always: to pursue returns in a way that supports your long-term purpose and provides clarity, confidence, and peace of mind along the way.

Staying Grounded in a Soft-Landing Market

Markets carried their strong momentum from Q2 into Q3, with the S&P 500, Nasdaq, and small-cap stocks each hitting new highs. Investor sentiment remained optimistic despite soft labor market data and mixed economic signals, and stocks traded higher due to strong corporate earnings, the Federal Reserve’s pivot toward rate cuts, and easing trade tensions.

The technology sector remained an important contributor, as artificial intelligence (AI) companies reported strong earnings growth. At the same time, improving market breadth added fuel to the rally, and small-cap stocks finally broke above their 2021 highs.

A Quarter of Transition in the Economy

The quarter opened on solid footing. Economic activity had recovered from the tariff-driven volatility earlier in the year, and incoming data pointed to steady consumer and business demand. Job growth was solid, consumers continued to spend, and business surveys showed sentiment was improving. The stock market traded higher in July, driven by confidence that the economy could withstand high interest rates and trade uncertainty without slipping into a recession.

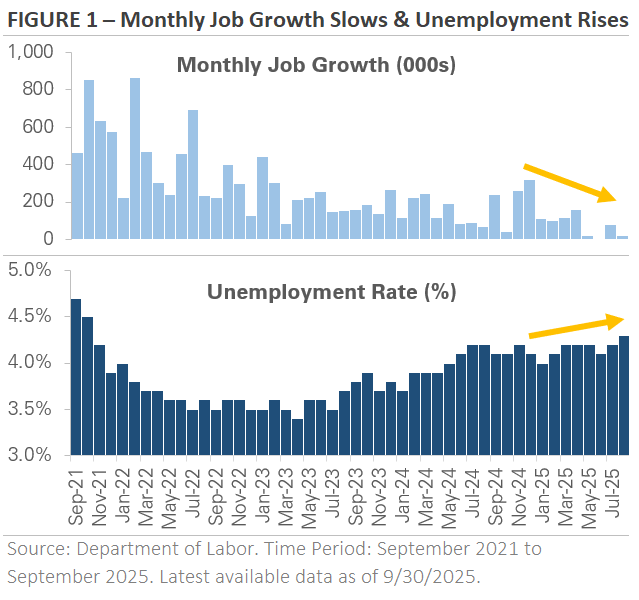

By late summer, cracks began to emerge in the labor market. Figure 1 shows job growth slowed sharply starting in May, with two consecutive months of weak job growth in July and August and negative revisions to prior months. The unemployment rate rose to 4.3%, the highest since 2021. While the labor data raised concerns about an economic slowdown, separate data showed consumer spending remained solid. Economic growth was still positive, but the economy was softening.

The shift in the economic backdrop was significant because it changed the conversation around Federal Reserve policy. As labor market data softened, the market adjusted its forecast to price in a more accommodative Fed and multiple interest rate cuts before year-end. In the market’s view, slowing job growth wasn’t a recession signal but rather a catalyst for the Fed to resume its rate-cutting cycle.

The question was when, not if, the Fed would deliver its next cut.

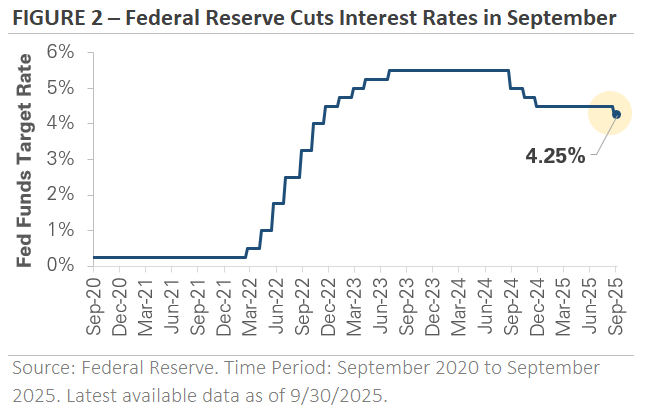

Fed Cuts Interest Rates After a 9-Month Pause

The Federal Reserve held interest rates steady at its late-July meeting, citing a solid labor market and lingering inflation risk. However, the outlook changed two days later when the July jobs report missed expectations.

In his Jackson Hole speech a few weeks later, Fed Chair Jerome Powell laid the groundwork for a September rate cut. He noted that monetary policy appeared restrictive and said softening labor market data might justify a rate cut, despite inflation still above target. Powell’s remarks reinforced expectations for a September cut and marked a clear shift from fighting inflation to supporting the labor market.

As expected, the Fed delivered a -0.25% rate cut in September, ending its 9-month pause (Figure 2). In his press conference, Fed Chair Powell framed the move as a “risk management” cut, describing it as a proactive step to keep the economic expansion on track rather than concern about a recession. The central bank updated its policy forecast to include two more rate cuts before year-end, with the potential for more in 2026. The revised forecast and Powell’s remarks signaled a measured and gradual rate-cutting cycle rather than an aggressive one.

The market initially celebrated the Fed’s decision, with stocks climbing to record highs and interest-rate-sensitive sectors outperforming. However, sentiment cooled in late September after a batch of stronger-than-expected data suggested the economy may need fewer rate cuts. New home sales rose sharply, Q2 GDP growth was revised higher, and consumer spending remained solid. The data caused investors to dial back their rate cut expectations, and by quarter-end, the market was pricing in a slower pace of cuts.

Artificial Intelligence Theme Dominates Headlines

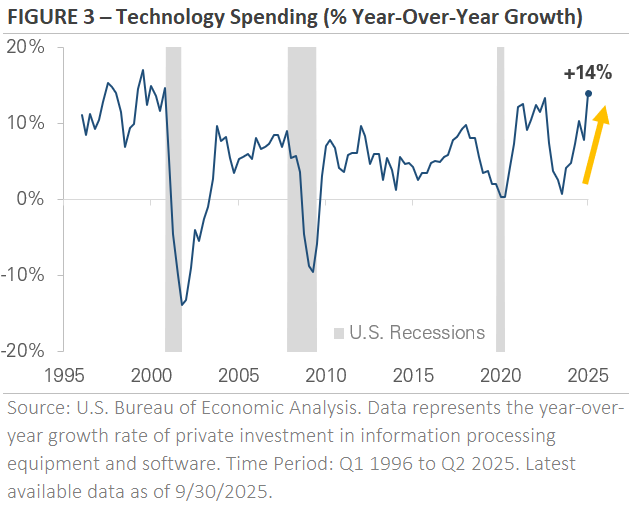

Artificial intelligence continued to be a top market theme during the quarter. Figure 3 shows technology-related investment grew +14% year-over-year in Q2, the second consecutive quarter and the fastest pace since the late 1990s. The spending is tied to the AI industry buildout, with billions being spent on high-performance computer chips, cloud architecture, data center construction, and the power and cooling needed to run it all.

The spending boom has become a significant contributor to economic growth and helped offset softness in rate-sensitive areas, such as housing, manufacturing, and non-AI business investment.

Management teams across the AI supply chain continue to report strong demand. Spending plans measure in the hundreds of billions, and order backlogs span years, not quarters, into the future. The commentary and scale of investment reinforce the market’s belief that AI will drive capex budgets in the coming years, and investors see AI infrastructure spending as a durable theme with room for growth.

In the equity market, AI enthusiasm has fueled outsized gains in specific technology and semiconductor stocks, creating a wide divide between AI-infrastructure leaders and the broader market.

While investors view AI as a multi-year investment cycle rather than a one-off spending burst, a more balanced conversation around AI is also taking place. Some question whether spending is outpacing potential revenue growth, and early studies have questioned whether the productivity gains from the new technology justify the high level of investment. These concerns have triggered periodic volatility, but they haven’t derailed the broader narrative that AI will continue to be a key driver of corporate earnings growth, economic growth, and market returns.

Equity Market Recap: Stocks Rally to New Highs as Market Leadership Broadens

Stocks climbed to new highs in Q3, boosted by the Fed’s rate cut, resilient earnings, and continued enthusiasm around AI.

The Fed’s rate cut marked a shift toward policy support and fueled optimism for a “soft landing”, a scenario whereby the economy slows but avoids a recession. Trade policy was another tailwind, and progress on deals with major trading partners reduced the near-term risk of escalation.

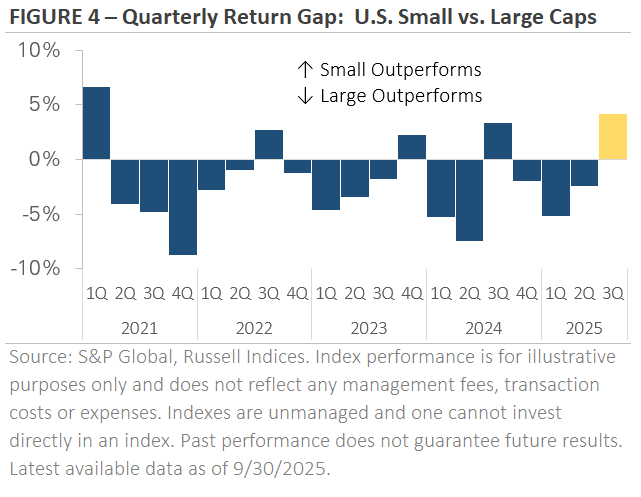

The S&P 500 gained more than +8% in Q3, bringing its year-to-date return to over +14%. Technology stocks remained a key driver, but broader market leadership also provided a tailwind. Small-cap stocks rallied sharply in anticipation of the Fed’s rate cut.

The Russell 2000 surpassed its previous high from 2021 and returned nearly +12% as investors bet that rate cuts would benefit smaller companies. Figure 4 shows small caps posted their biggest quarter of outperformance over the S&P 500 since Q1 2021. In another sign of the market’s optimism, cyclical sectors broadly outperformed their defensive counterparts.

International stocks performed in line with the S&P 500 in Q3, but headline results masked significant divergence beneath the surface. Emerging markets outperformed U.S. stocks, driven by renewed stimulus efforts in China and strong gains from AI-related companies in Asia.

The Fed’s decision to resume its rate-cutting cycle provided another tailwind, as emerging markets, like U.S. small caps, are often viewed as more sensitive to rate cuts and shifts in global financial conditions. In contrast, developed markets underperformed U.S. stocks. European equities ended the quarter modestly higher as they consolidated gains from earlier this year.

Despite the quarter’s mixed returns, both emerging and developed markets have gained more than +25% year-to-date. The two indices are each outperforming the S&P 500 by more than +10% since the start of 2025.

Credit Market Recap: Bonds Trade Higher as the Fed Resumes Its Rate-Cutting Cycle

Interest rates fluctuated in Q3 but ended the quarter lower. Treasury yields rose in July as stronger-than-expected economic data pushed back the expected timing of Fed rate cuts. However, yields reversed sharply lower in August after the soft labor market data and Chair Powell’s speech. Treasury yields declined further in early September after the weak August jobs report, but they ticked higher later in the month as economic data stabilized.

The decline in Treasury yields caused bonds to trade higher. Longer-maturity bonds outperformed due to their higher sensitivity to falling interest rates, while shorter-maturity bonds underperformed. This outperformance extended to corporate bonds, where investment-grade outperformed high-yield as the combination of falling interest rates and credit spread tightening produced gains.

Corporate credit spreads remain tight by historical standards. Investment-grade and high-yield spreads are at their tightest levels in decades, a reflection of investor confidence in corporate earnings growth and the economic outlook. While spread tightening has supported corporate bond returns recently, it means valuations are no longer cheap.

Corporate bonds offer compelling yields for income-focused investors, but they also come with important trade-offs. When credit spreads are this tight, there’s less margin of safety if earnings or economic growth disappoint. If either of these scenarios occur, Treasury bonds could outperform corporate bonds despite their lower yields.

Staying Grounded in a Soft-Landing Market

As we move into Q4, the outlook for the economy remains positive yet cautious. Growth is moderating but still positive, inflation continues to ease, and the Federal Reserve has shifted from tightening to gradual rate cuts. Together, these dynamics have fueled renewed optimism across equity and credit markets.

Yet, history reminds us that markets rarely move in straight lines. Even in strong years like this one, pullbacks of 3% to 5% are normal and often healthy. They serve as natural pauses in longer-term uptrends, helping to reset expectations and valuations.

Now is an ideal time to stay grounded, reaffirming liquidity reserves, reviewing portfolio allocations, and preparing to take advantage of opportunities when markets inevitably take a breather. Maintaining 6–9 months of cash reserves for working investors and 12–18 months for retirees helps avoid selling assets at unfavorable times.

Market dips also present planning opportunities. Declines in asset prices can create favorable conditions for tax-aware strategies such as Roth conversions, portfolio rebalancing, and tax-loss harvesting, all of which strengthen long-term after-tax outcomes. While short-term volatility will always be part of investing, the key is not to fear it but to plan for it.

Remaining disciplined, maintaining liquidity, and using volatility as an ally, not an adversary, ensures investors can participate fully when the next leg of the rally begins.

As always, I’ll continue to monitor market developments and stand ready to help you navigate what’s ahead, keeping your plan aligned with clarity, confidence, and peace of mind.

Here’s How to Prepare for the Next Market Dip

Who doesn’t love a good market rally? It’s the time when investment account balances continue to move higher and retirement options continue to solidify.

Market Rallies and the Reality of Pullbacks

But we know that markets don’t move up in a straight line, despite what we’ve seen over the past few months. According to Ned Davis Research, market dips of around 3% happen about seven times per year on average, and corrections of 5% or more occur roughly three times annually.

In other words, pullbacks aren’t unusual, they’re a normal part of the investing landscape that investors should anticipate even when the backdrop is strong.

And here’s the thing: since April’s selloff, the S&P 500 index has not experienced a sustained market dip greater than 3% and that’s worth noting.

What goes up, must come down, right? Maybe for a bit, then often right back up. That’s the mindset we want to focus on: enjoy the rally, yet be ready for the routine setbacks that come with healthy markets.

Staying Grounded is Essential

That’s why now, more than ever, is the right time to stay grounded and position your portfolio for an inevitable bout of market volatility. Now, preparation doesn’t necessarily mean pessimism, but rather it’s how you participate in the upside while keeping your footing when markets take a breather.

Because if you don’t, you could end up leaving money on the table when the market pulls back.

How so?

Well, the fact of the matter is that there are two key areas that you'll want to be prepared for when the markets eventually take a turn.

First, not giving up gains unnecessarily by avoiding mistakes that leave money on the table.

Second, not missing out on potential tax planning opportunities when asset prices do pull back.

Taken together, these help you stay constructive and benefit across cycles.

Let's take a look at this more closely.

What the Current Market Is Telling Us

So far this year the S&P 500 index is up over ten percent. And while this double-digit return for domestic stocks is quite notable, it's also worth noting that international stocks are up well over 20% so far this year.

There's a case to be made for the ongoing rally in international stocks and risk assets in general, especially as interest rates fall and the dollar continues to weaken.

Even so, while risk assets continue to rally higher on expectations that the Federal Reserve cutting interest rates will make it more favorable for risk assets to rally, the very backdrop that prompts policymakers to cut rates suggests U.S. economic growth could still face headwinds.

And while the U.S. economy has been generally steady in 2025, there’s a very real potential that any incoming data pointing to fractures in the solid growth story could give investors reason for pause, leading to a market pullback.

That kind of pause is consistent with history and with the Ned Davis data on frequent, modest setbacks, not a reason to abandon a long-term plan.

Why Cash and Taxes Matter Most

In anticipation of this market pullback, there are two things to consider doing before the market actually turns, and some actions you can take when the markets are actually in a pullback.

To start, cash is king when it comes to periods of heightened market volatility. That’s why now is the time to evaluate your cash management plan and make sure that your reserves are properly topped up to cover the unexpected.

This means that if you're still in your working years, make sure you have between 6 to 9 months of cash on hand or liquid assets available just in case to cover unexpected expenses.

And if you're already retired or approaching retirement, now would be the time to make sure that you have between 12 and 18 months of liquid cash reserves available to cover your living expenses. The last thing that you want to do during a market downturn is sell assets at an inopportune time and lock in losses.

Think of cash as both a defensive buffer and an offensive enabler that lets you avoid forced selling and gives you flexibility to act on opportunities when others can’t.

The second approach to take and consider when the inevitable market pullback does come is to think about how you're positioning yourself from a tax perspective. More specifically, one of the big things that we focus on during periods of market weakness is taking advantage of Roth conversions.

That's because market sell-offs temporarily lower asset values, giving us an opportunity to realize lower taxable amounts when moving money from qualified accounts like IRAs or 401(k)s into a Roth IRA and positioning those assets for future tax-free growth and withdrawals. This is a clear example of not leaving money on the table: using normal volatility to improve your after-tax outcomes.

Staying Grounded with Cautious Optimism

When it comes down to it, nobody wants to be the person who washes away a market rally by thinking about or talking about the potential for a pullback.

Nevertheless, history has shown repeatedly that all good things include periodic setbacks. And when they do, they often happen without warning, happen suddenly, and lead to regret for the unprepared.

Acknowledging that reality is part of being cautiously optimistic: we respect the risks so we can stay invested for the rewards.

While there's a case to be made for assets to continue to rally in the months ahead, there's no better time than the present to practice prudent portfolio management.

Sticking to a disciplined investment strategy, keeping appropriate cash reserves, using volatility-aware tax strategies like Roth conversions, and rebalancing your portfolio help ensure you're not leaving money on the table and not paying Uncle Sam any more than his fair share.

That’s how you remain grounded and prepared for when the markets eventually rally once again.

Two Quarters, Two Stories: A Market That Came Full Circle

The first half of 2025 delivered a tale of two very different quarters.

After stumbling out of the gate with a sharp selloff in the first quarter of the year, markets found their footing in the second quarter.

Indeed, what began as a year marked by caution, driven by rising policy uncertainty, slower growth concerns, and questions surrounding the durability of the AI boom, sentiment shifted dramatically as headlines softened, tariffs proved less disruptive than feared, and corporate earnings came in stronger than expected.

And yet, for all the twists and turns, markets ended the first six months surprisingly close to where they began.

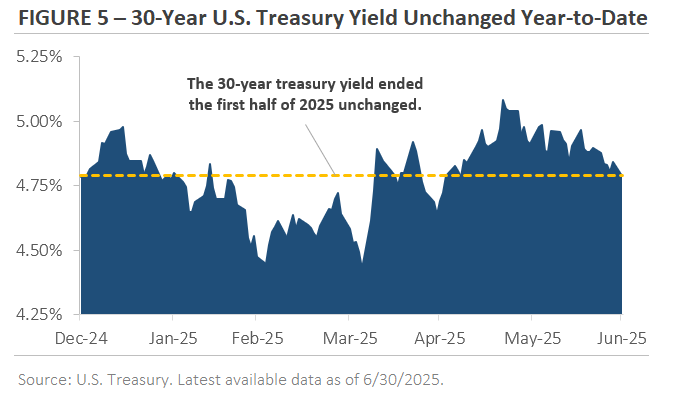

The S&P 500 returned a gain of 6.1% through June, which is a notable rebound from being down more than -15% earlier in the year. Long-term interest rates told a similar story with the 30-year U.S. Treasury yield swinging widely between 4.40% and 5.10%, but finished June just a touch below where it started, near 4.80%.

To the casual observer, it may seem like little has changed. But under the surface, the story is far more nuanced, and still worth watching as we head into the second half of the year.

Markets Ride a Wave of Policy Whiplash

Now, if there’s one word that’s defined the first half of 2025, it’s “whiplash.”

And trade policy was at the center of it all. That’s because what started as a steady drumbeat of tariff escalation early in the year gave way to a flurry of de-escalation efforts just weeks later which left businesses, investors, and global partners scrambling to make sense of the shifting landscape.

As you’ll likely recall, the escalation phase took hold in February and March, with sweeping tariffs targeting imports from China, Canada, Mexico, and broader categories like steel, aluminum, and autos.

Then, just as tensions peaked in early April with the announcement of tariffs on nearly all imports, the tone reversed. A week later, the Trump administration paused reciprocal tariffs for every trading partner except China. And by early May, a new trade agreement with China signaled further cooling.

Yet, despite this pivot, the uncertainty still hasn’t gone away.

Because in late May, a U.S. trade court ruled the sweeping tariff measures unconstitutional, and by June, the administration was already signaling the possibility of reinstating certain tariffs. With July and August deadlines looming for tariff exemptions, we’re entering another chapter of policy ambiguity.

So then, for markets and businesses alike, the story that we’re tracking is not just the tariffs themselves, it’s the pace and unpredictability of change that’s creating the most friction.

And until clarity returns, volatility may remain part of the ride in the months ahead.

Tariff Talk Hits the Economy, But Not How You Might Expect

Now, one of the more surprising outcomes of this year’s trade drama is how quickly it filtered into the economic data and not through slowdown as we had expected, but through acceleration.

How so?

Well, in the first quarter, businesses and consumers raced to front-run potential price increases by pulling forward purchases. Imports of consumer goods and industrial supplies spiked, while vehicle sales surged in March and April, reflecting a scramble to buy ahead of expected tariffs.

These moves weren’t part of a typical economic activity, it was a strategic move by business and consumers. It was less about improving demand and more about beating the clock on higher prices.

And this kind of behavior can distort short-term data. Because what might look like strength may simply be a shift in timing. And that makes it harder to assess the true underlying trend.

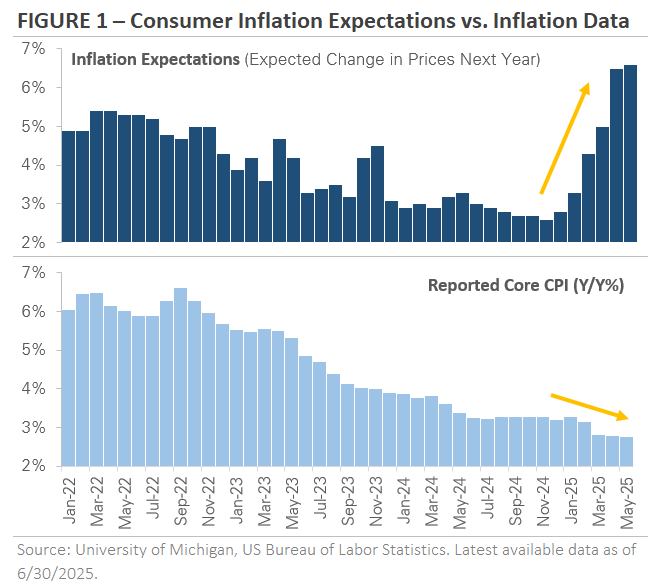

Another dynamic worth watching is inflation, specifically, the growing gap between what consumers expect and what’s actually showing up in the data. As shown in Figure 1, consumer inflation expectations have surged, even as official inflation readings, like the Consumer Price Index, continue to trend lower.

It’s a disconnect that speaks volumes because while prices haven’t materially risen yet, consumers are clearly bracing for what might come next.

Whether those expectations become reality remains to be seen because of different factors.

For example, some economists warn that inflation could pick up as tariffs ripple through supply chains over time, just as they had during the pandemic.

Yet others argue companies may absorb the cost increases to stay competitive. And the earnings season may offer early insight, particularly into how businesses are adjusting their pricing strategies and how much of the tariff story is already baked into forward guidance.

For now, however, the hard data remains calm. But expectations are restless. And in markets, that’s often where the story begins.

The Fed Stays Put While Markets Wait for Clarity

Now, uncertainty doesn’t just spook investors, it complicates policymaking as well. And for the Federal Reserve, this year’s shifting trade landscape has added a new layer of complexity to an already delicate balancing act.

On one hand, policymakers are contending with the fact that tariffs could ignite inflation.

On the other, tariffs might slow the economy if higher costs start to weigh on consumer demand and business investment.

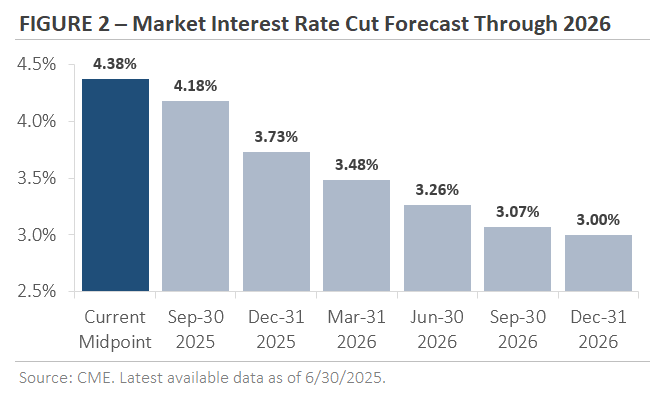

So then, caught between those risks, the Fed held rates steady at both its May and June meetings, signaling that it needs more data before making its next move.

In other words, it’s a time for patience, which is now playing out in the markets.

Indeed, figure 2 illustrates the market’s evolving expectations for interest rates. The Fed’s current target range stands at 4.25% to 4.50%.

However, futures markets are now pricing in a gradual path of rate cuts beginning in September, with momentum picking up into 2026.

In other words, by the end of that year, investors expect the Fed to lower rates by approximately -1.25% from current levels.

That forecast reflects a kind of economic middle ground of inflation risks persisting, but the damage from tariffs appears contained for now. Still, as always, the path forward is highly dependent on what comes next.

Markets are adjusting their expectations in real time and so is the Fed. Therefore, any shift in inflation trends, labor market strength, or trade policy could quickly rewrite the script which is what we’re keeping an eye on.

But for now, the message is clear: until the dust settles, both the Fed and the market are content to wait.

Valuations Bounce Back as Sentiment Shifts

So, how has this trade and central bank policy affected the stock market? Well, after a rocky first quarter, investors seemed to flip the script in the second quarter.

That’s because, despite lingering uncertainty around trade and interest rates, the stock market staged an impressive rebound. And this came not because earnings surged, but because investors became more willing to pay up for the earnings already expected.

In other words, valuations (the price investors are willing to pay) not profits (earnings that support those prices) did the heavy lifting.

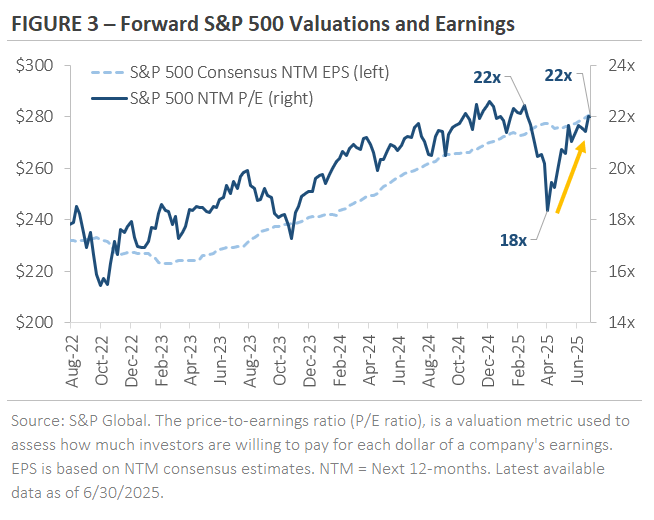

Figure 3 tells this story. The dashed light blue line tracks Wall Street’s 12-month earnings forecast for the S&P 500. The darker navy line shows the index’s price-to-earnings (P/E) ratio, or the multiple investors assign to those expected earnings.

And at the end of 2024, the S&P 500 traded at roughly 22-times forward earnings. You’ll recall that at that time there was optimism around AI and pro-growth policies supported those higher valuations. But as trade tensions escalated in early April, sentiment cracked, and the P/E multiple fell to 18x almost overnight.

And at the end of 2024, the S&P 500 traded at roughly 22-times forward earnings. You’ll recall that at that time there was optimism around AI and pro-growth policies supported those higher valuations. But as trade tensions escalated in early April, sentiment cracked, and the P/E multiple fell to 18x almost overnight.

Here it wasn’t earnings that changed, it was mood.

But then came the rebound. As tariff concerns cooled and companies delivered better-than-expected first-quarter results, confidence returned. By late June, the P/E ratio had climbed back to where it started the year at just above 22x.

This kind of valuation whiplash is a reminder of how quickly investor sentiment can swing and why trying to time your way into (and out of the market) can be disadvantageous.

It also underscores the importance of understanding what’s driving market moves, not just earnings, but how much investors are willing to pay for them.

And so, with earnings season ahead, the focus now shifts to whether companies can meet or exceed the expectations embedded in these renewed valuations.

From Flight to Risk to Return to Risk-On

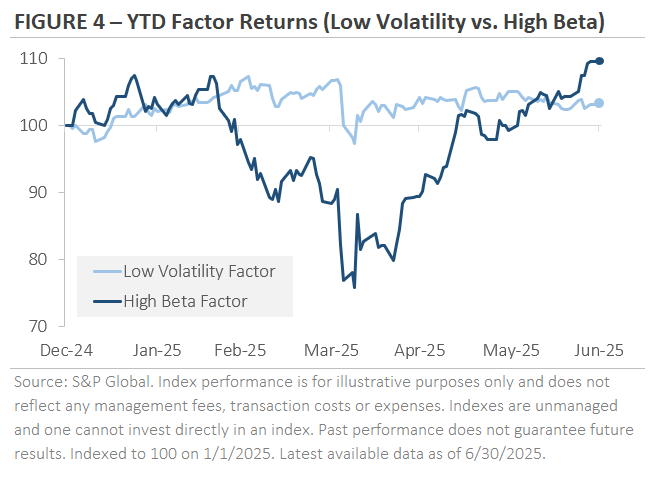

Now, we know that markets have rebounded, but it’s essential to also note that the players that previously led market moves higher (and lower) have changed hands this year.

Indeed, the first half of 2025 saw a dramatic rotation in market leadership, one that played out almost like two separate market cycles in rapid succession.

That’s because in the first quarter, uncertainty dominated and defensive stocks outperformed.

How so?

Well, during the uncertain times, investors sought stability in low-volatility names like utilities and healthcare, while higher beta, economically sensitive sectors lagged behind.

Then things changed on a dime in the second quarter.

As policy tensions cooled and growth fears receded, risk appetite returned in force. Figure 4 highlights the shift by tracking the performance of low-volatility versus high-beta stocks.

In the first quarter, low volatility led by nearly 20%. And in the second quarter, high volatility outpaced low volatility by over 25% which fully erased its earlier underperformance.

That reversal extended beyond factors to asset classes and sectors.

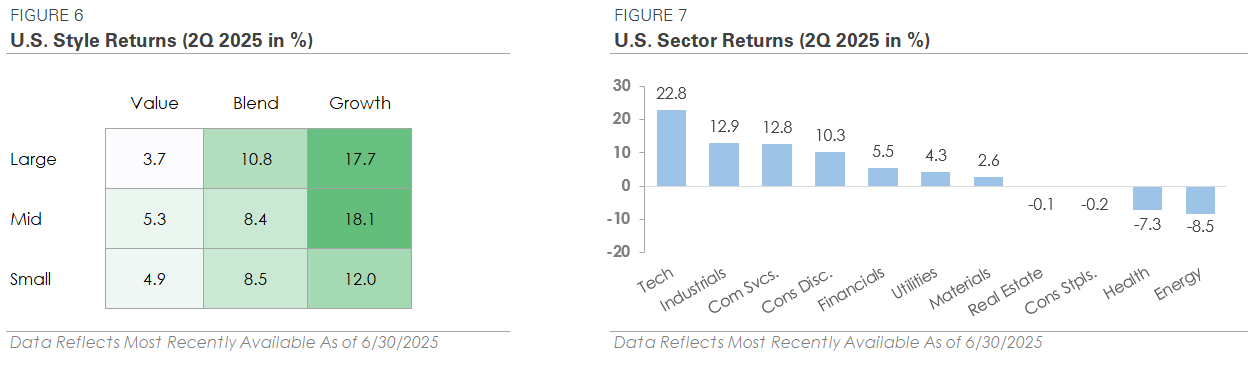

- The S&P 500 rose 10.8% in Q2 after falling -4.3% in Q1.

- Small caps, which had been hit hard early in the year, bounced 8.5% in Q2.

- Growth stocks reclaimed leadership: the Nasdaq 100 rallied 17.8%, and the Russell 1000 Growth Index surged 17.7%.

- The “Magnificent 7” tech giants, down -15.7% in Q1, came roaring back with a 21.0% return in Q2.

Meanwhile, value stocks posted more modest gains, as measured by the Russell 1000 Value Index which rose just 3.7% and is a reflection of the market’s clear tilt back toward risk and momentum.

International markets also quietly delivered another standout quarter. For example, developed and emerging market equities returned over 11% in Q2, outpacing U.S. stocks for a second straight quarter. However, it’s essential to note that much of that performance has been currency-driven, as a weaker dollar, pressured by tariff uncertainty and a shift in global flows, provided a tailwind for non-U.S. assets.

So then, if the first quarter was a flight to safety, then the second quarter was a return to growth and a powerful reminder of just how quickly market leadership can change.

Bonds Caught Between Calm and Concern

And what about the bond market?