Creating Work-Life Balance When You're "Always On"

Work is a vital part of daily life. You get an education so that you can obtain employment which will provide you with the security you need to live throughout your life. Even though making money is one of the most important reasons to have a job or career, it is not the only factor that should be considered. Your employment should not only serve your financial needs but your emotional ones as well.

This means that being successful in your career should involve more than the financial reward and it should never take precedence over your well being, both physical and emotional. To achieve this, you need to find a way to create a balance between your work and home life even when your job requires your attention after hours. Below are three ways to help to achieve a balanced work and home life even for careers where you are "always on."

1. Accept the Fact That There is No Perfect Balance

Even though creating a work-life balance is the goal, it is crucial to be realistic in your expectations or you may find yourself becoming more frustrated with the process or feel as though you are in some way failing yourself or your family. Most people start by coming up with a strict schedule that can incorporate everything you have to do and want to do in your day. Unfortunately, these regimented schedules often leave little time for the curveballs that life may throw at you, and when they do occur, it may cause you unnecessary stress. Instead, try and create a basic schedule with things that you have to do and things you would enjoy doing if you have time. You need to remember that a balance means creating a balance over time not necessarily every day.

2. Always Make Your Health a Priority

Always remember that achieving your goals can be difficult if your health is not up to par. This includes not only your physical health but your mental well-being too. If your job creates a lot of stress or anxiety, or you suffer from depression, addressing these issues is important, or they can lead you to the possibility of breakdowns, sleep deprivation, or other problems that can lead to physical ailments and burn out. When you suffer from physical illness, it is better to take time off to get the rest you need for your body to repair itself, or you will end up struggling with the symptoms for longer. You also should make time to get in some exercise, even if it is taking a walk or sneaking in a spin class. Remember that being healthy will also make you a more productive employee and in a better mood when you are home.

3. Don't Be Afraid to Unplug Once in Awhile

The ability to stay connected is a great way to stay socially engaged as well as be able to complete work even when you are away from the office. Even though this ability to connect through technology is a great convenience, it can also create stress and keep your mind in work mode the entire time you are away from the office. Sometimes a short unplugged vacation can be as relaxing and refreshing as a long vacation and a great way to de-stress and refocus even if it is for a few hours. Always remember that the world continued to function before the advent of such technology and unplugging yourself once in a while is not the end of the world. If your technology is a crucial tool for your work, you can set designated times when you are off-hours and will not use or respond to your device.

Taking time away from your work, or work-related devices, and focusing on forgotten hobbies or even relaxing and doing nothing at all is important to preventing job burnout and allowing you to recharge and revitalize so that you can be at your best when you need to be. Remember finding that work-life balance is its own journey but an extremely rewarding one once it has been achieved.

6 Tips to Prioritizing Finances for the Self-Employed

So, you have decided to become self-employed. You’re probably aware of the costs it will take to get started. However, you should keep in mind the potential of rocky terrain on your road to riches — 6.3 percent of Americans were self-employed in 2017.1 If the past is prescient, a third of those who have their own business will have closed up shop within two years. We don’t know how many who were in the gig economy will have returned to a day job. If your endeavor is to survive, you should plan your finances to account for the ups and downs of being in business for yourself.

1. Save on Startup Costs

You may be tempted to purchase everything you need all at once before starting your self-employment phase, and buy the best and buy it at retail prices. You may be in an endeavor that doesn’t demand that kind of capital expenditure at the beginning. See if you can purchase assets in a good used condition. Look into sharing workspace with another entrepreneur, or even work out of your home if possible. If you need to advertise, focus on using free social media or getting coverage from a local news organization for press. Place a priority on what comes after the startup, running your business efficiently and successfully.

2. Organize a Budget

While you’re budgeting to save on startup costs, plan a budget for the next six months. Take a good survey of your situation and estimate your income. Be realistic about what you’re going to take in and what you can spend on your business and personal life. Because at the beginning, you’re likely to experience volatility in your income levels, it’s best to think what you might make on average. It may be difficult to gauge. Ask other people in your line of work how they’ve done to get an idea.

Your budget should include considerations of:

- Tax liability

- Health care and insurance costs

- Your debt

- A retirement plan or college fund if you have those.

- Expected business expenditures

Of course, you should pocket enough of your own money to survive each month. This may not be an issue for those in the gig economy. For those who have a business, there may be employees or vendors to satisfy as well. You want to prioritize yourself as you are the engine of your income, you’re the most important asset you have.

3. Separate Personal and Business Expenses

Track your personal spending separately from your business expenses. This may become important during tax time when you are making deductions. If you use your car in your side hustle, track how much gas you use for business as well as how much gas you’re using for personal errands.

4. Prioritize Saving

Because of the uncertainty surrounding self-employment, those involved may be tempted to keep their earnings in a checking account so they can easily grab it when they need it. You may want to do the opposite. Consider prioritizing saving rather than putting it on the back burner. Double the amount you put into your retirement accounts and section off a reasonable portion of your income for an emergency fund.

5. Don’t Forget Your Day-to-Day Life

While you may be enmeshed in the battle to become financially independent, you may still have other obligations that you have to account for. If you have kids, they need to be fed and clothed, and they will often need money for school supplies and field trips. You’ll have auto maintenance, dry cleaning and other personal expenses to consider. It’s easy to lose track of these when you’re focused on dominating your field.

6. Get Good Advice

Before stepping into the self-employment arena, talk to people who can give good advice. For your business concerns, talk to people who have already experienced what you’re about to go through. For concerns about savings, debt management and other financial issues, talk it over with a trusted financial advisor.

5 Top Traits Best-Performing CEOs Have in Common

Becoming a successful CEO takes considerable time and effort. If you think about some of the top CEOs today - Sundar Pichai, Elon Musk, Jeff Bezos - you may notice that they have a few traits in common. Whether you’re a CEO at your company now or aspiring to be one, here are five traits that high-powered CEOs have in common - and you can strive for too.

Trait #1: Strong Communication Skills

It should come as no surprise that one of the top traits shared by CEOs is great communication skills. As a CEO, you act as the face of the company, meaning you need to be able to communicate what you want effectively. Whether you’re looking to motivate your employees, address an issue within the company or express your gratitude, effective communication is key. The best CEOs communicate in a strong and clear fashion, which leads to action.

Trait #2: Willingness to Take Risk

The best CEOs wouldn’t be where they are today if they weren’t willing to take risks. This trait is perhaps one of the key elements of being a CEO. You need to be able to embrace uncertainty and not be afraid to fail. When we take risks, we grow and step outside of our comfort zones. Similarly, in order to drive business growth and discover new paths, CEOs tend to take risks that allow them to propel their businesses to the next level.

Trait #3: Realistic Optimism

The best CEOs dream big - but they dream realistically. In order to make things happen, it’s important that you see the line between possible and impossible. Having too much ambition as a CEO can hurt you as you spend money, energy and resources on a goal that is very unlikely to be met.

Therefore, the most successful CEOs take the high road if they know there is some potential. This may seem counterproductive to the previous trait of taking more risks. However, there is a difference between taking a risk, despite knowing you will fail, and taking a risk where you simply don’t know what the outcome will be.

Trait #4: Ability To Learn From The Past

Remember the phrase, “learn from your mistakes?” CEOs have the ability to see failure in a positive light as they learn what they did wrong, and they make sure they don’t do it again. There are those who can’t bounce back after failure, there are those that bounce back after failure but repeat the same mistakes over and over again, and then there are those who bounce back and change for the better. Top-performing CEOs tend to be the latter.

Trait #5: Approachability

We often think of CEOs as intimidating people, making us afraid to approach them. But if you think about it, successful CEOs wouldn’t be successful if people were afraid of them, right? The top CEOs are, in fact, highly approachable, and they make sure to let people know this. Some ways that CEOs build their approachability factor is by being physically present at the company facilities, interacting with their employees one-on-one, sending emails out regularly, etc.

Being a top-level CEO requires a key bundle of traits. Behind this big title, there is a special type of person with unique characteristics that help make them successful. For those aspiring to reach this high-level position, these traits can be learned and always improved upon. If you want to be the next most successful CEO, ask yourself if you have each of the above-mentioned traits. If you don’t think you do, now’s the time to work on building them one by one.

5 Bedtime Habits of Highly Successful CEOs

Want in on the most successful CEO's bedtime habits? From Mark Zuckerberg to Ron Rudzin, you may think these busy bigwigs get about three hours of sleep a night. Surprisingly, they prioritize sleep just like you and me, and their bedtime habits serve as a key to their success!

Mark Zuckerberg And Sundar Pichai Spend Time With Their Families

Mark Zuckerberg, CEO of Facebook, and Sunday Pichai, CEO of Google, like to be with their respective families before bedtime. Specifically, they both get home at night in time to tuck their kids into bed. Mark Zuckerberg said, “I am reminded of a prayer ‘Mi Shebeirach,’ that I say whenever I face a big challenge.” “...That I sing to my daughter, thinking of her future when I tuck her in at night.”

Richard Branson Relaxes

Richard Branson, CEO of Virgin Group, goes to a quiet area before going to sleep. Branson said, “If I have some time to spare, I’ll read for a bit or perhaps watch a documentary, to help me relax and put me in a great frame of mind to get a good night’s sleep.”

Elon Musk Eliminates Caffeine

We love caffeine to get us through the day and so does Elon Musk, CEO of Tesla. He used to drink eight cans of diet coke and two cups of coffee a day. However, he now strays away from any caffeine six hours before going to sleep.

Bill Gates Reads Books

Do you read before going to bed? If you do, you should know that Bill Gates, the previous CEO of Microsoft, does too! Bill Gates said, “I read an hour almost every night. It's part of falling asleep.” In fact, Bill Gates is a power reader, getting through a new book every week.

Oprah Winfrey Meditates

Racing mind keeping you up at night? Take a tip from media mogul, Oprah Winfrey, and meditate before hitting the hay. Oprah reportedly practices transcendental meditation every morning and night to promote lower stress levels, improved cognitive functioning, creative thinking and productivity and even improved physical health. This form of meditation is practiced for 20 minutes twice per day sitting still with your eyes closed.

If you’re looking to switch up your bedtime routine to be more energized and ready to take on the next day try adopting a tip or two from these ultra-successful CEOs and let us know how your life changes!

Are Your Finances Impacting Your Health?

Health care costs have been rising for years. The issue is one that concerns most people and is one of the most influential when it comes to voters making political decisions. We’re concerned about how much it costs to be healthy, but could being unhealthy financially be making us sick?

The evidence suggests that it’s true. An American Psychological Association study showed that financial stress reduces life expectancy.1 Financial stress can cause a range of symptoms, from migraine headaches to clogged arteries.

Real Problems Cause Real Problems

So then, being worried about our financial state can cause us physical harm. It’s also true that actually experiencing financial distress can cause poor health. A study from the Economics Policy Institute showed that the richer we are, the healthier we are.2 Men with a higher income simply live longer.

People with a lower income are more likely to suffer various maladies, similar to those caused by financial stress. This is often because of a lack of access to adequate health care, as one survey of health care statistics indicates.3 Also, people with less disposable income may be less likely to make regular visits to a doctor or dentist, eat a healthy diet or have the time to get regular exercise. All of these things can lead to poor overall health.

Poor Coping Mechanisms Makes Things Worse

Poor or not, worrying about finances can lead us to attempt to cope with the stress. We often go for the easiest method of relief, such as:

- Sitting in front of a TV or computer screen for hours, living a sedentary lifestyle

- Binge eating

- Drinking alcohol in excess

- Maladaptive behavior in our interpersonal relationships

- Lacking proper sleep

As you might guess, these behaviors can have negative consequences for our physical and mental health. We can put on excess weight, experience poor circulation, lack important nutrients and exacerbate stresses by having conflicts with family members.

The Psychology of Scarcity

An interesting study revealed the raw mental impact of financial stress on those with lower incomes.4 The participants were shown two car repair bills, one large and one small. They were asked to work out several questions. The idea wasn’t to test math skills, but other cognitive abilities. The lower-income subjects performed poorly when presented with the large car bill. The effect, called the “psychology of scarcity,” showed that people are less capable when lacking something important in their lives.

Working Your Way Out

So then, financial stress can affect our health. The easy answer it seems would be to remove the financial stress. Of course, it isn’t always that easy. Sometimes we have to ride out the rough times while finding healthy strategies for dealing with the physiological and psychological aspects.

One way, perhaps a little painful for those going through a rough patch, would be to take stock of where you are and look to make a plan to get out of it.

- Make a budget

- Talk with family members who may have experienced similar situations

- Look for ways to increase income without increasing stress, like turning a hobby into a side hustle.

- Get help from family or friends if possible

- Talk to a financial advisor

You can also engage in healthier activities to act as a buffer between your financial stress and your health.

- Start an exercise plan

- Get a healthy diet

- Spend more time with family or friends instead of sitting alone weighed down with worry

- Visit a doctor if you are feeling poorly, don’t wait for something serious to go wrong

It’s clear that financial stress can negatively affect your health. However, it doesn’t have to. While you work your way out of your financial trouble, take time to apply some self-care for your health care.

1 https://www.apa.org/news/press/releases/stress/2017/state-nation.pdf

2. https://www.epi.org/publication/webfeatures_snapshots_20080116/

3. https://newsinteractive.post-gazette.com/longform/stories/poorhealth/1/

4. https://www.apa.org/monitor/2014/02/scarcity.aspx

Running a Business? Listen to These Podcasts for the Best Ideas on How to Scale

Are you trying to accelerate your growth? If you are running a business or thinking of starting one soon, then you probably have a long list of business books you want to read. But it can be hard to find the time to read like you know you should.

Podcasts are a great way to keep learning during your morning commute or during those pockets of the day when your hands are busy but you have the bandwith to listen, like when you are making dinner or waiting in the school pickup line.

Here's 10 business podcasts to get you started:

1. HBR IdeaCast by Harvard Business Review

HBR IdeaCast is hosted by senior editors at Harvard Business Review. The podcast covers as many topics as the print publication by bringing in leading thinkers in all areas of business and management for each episode.

2. How I Built This

How I Built This with Guy Raz tells the stories of how some of the best-known companies got started. Even if you never see your business becoming a global company, it's still interesting to see how the big names got there, and many of their early steps are things you can replicate as you build towards your own goals.

3. Masters of Scale

LinkedIn co-founder Reid Hoffman hosts Masters of Scale. This podcast also examines large growth companies with an emphasis on how they went from tiny ideas to the companies they are today. Each episode features different industry leaders explaining and challenging the theories behind fast growth.

4. The Tim Ferriss Show

Tim Ferriss got his start with the book The 4-Hour Workweek. If you're trying to learn about time management and how to increase your productivity, this is the podcast to tune into. The show also covers other ways to boost your success in sports, arts, and business.

5. Entrepreneurial Thought Leaders

Entrepreneurial Thought Leaders is part of the Stanford Speaker Series. If you miss the days of guest speakers on your college campus, this is the place to go. Stanford follows the same format bringing in entrepreneurs and innovators to tell their stories of how they launched and grew their businesses.

6. Startups for the Rest of Us

Startups for the Rest of Us is by software developers for software developers. If you're building an app or are launching a software product, this is where you want to go to learn from people who did it before you.

7. Smart Passive Income

The theme behind Smart Passive Income is doing a little work now to have a regular income stream coming in with almost no future work. If you're trying to build a side hustle or would rather spend your time out on the golf course, the marketing tips in this podcast will help you get there.

8. Youpreneur

When your company is small, you are the company. Youpreneur dives into how to build your personal brand and establishing yourself as an authority to give yourself the credibility to take on industry giants.

9. Online Marketing Made Easy

If you want to launch a business in today's economy, online marketing is essential. Online Marketing Made Easy is an educational series covering the basics including social media, content marketing, and branding.

10. As Told By Nomads

Hosted by digital marketing specialist, Tayo Rockson, As Told By Nomads shares a variety of insights for entrepreneurs looking to leverage digital marketing to really make an impact in the business world. If you're in need of some creative inspiration and out-of-the-box digital marketing ideas this is a podcast to add to your listen list.

The Executive Way: Treat Your Career Like a Sport

When thinking about your career, it might seem odd to make comparisons to a sport. But when you zoom out and look at the similarities, they’re more closely related than you may think. For example, a common problem many people face as they end their careers and enter retirement is a loss of purpose and a feeling of emptiness because the thing that consumed eight hours a day for the past 40 years is now gone.

Athletes face these same struggles, but a lot sooner in life. However, some athletes find themselves thriving in life after sports because they’ve learned many valuable lessons and picked up traits from their sport that can translate into many other areas of life.

Derek Jeter, former Yankees shortstop and first-ballot Hall of Famer, is now CEO and part-owner of the Miami Marlins and co-founded the media company, The Players’ Tribune. Hall of Fame defensive end Michael Strahan took his talents and football knowledge to live TV and has co-hosted Fox NFL Sunday, $100,000 Pyramid, and even Good Morning America.

While your career may not lead to headlines and TV gigs, there are a few ways that you can treat your career like a sport to set yourself up for long-term success.

The 10,000 Hour Rule

In his book, The Outliers, Malcolm Gladwell claims that it takes roughly 10,000 hours of work to master a skill. While the specific number of hours has been challenged by many, the principle will always make sense: to be great at something, you must put in the work.

Athletes dedicate years, sometimes decades, to their craft to be the best that they can be, and we shouldn’t treat our own careers too different. Over the course of your working career, you’re most likely going to put 10,000 hours of work in by just showing up. However, if you’re intentional about the work that’s being put in, you can begin to propel your career.

For example, this may be getting additional certifications or a graduate degree that allows you to move up in the ranks of your profession. Also, putting in the work of connecting with like-minded people on the same path as you or growing your skillset to make a career change that provides higher potential income.

When you put in the work, it’s hard not to make progress.

Be Prepared for Uncertainty

Just like athletes devote time to be mentally and physically prepared for competition, an effective way to level up in your career is by being prepared. Whether you’re interviewing for a new job or giving a presentation to your team, preparation is critical and impacts how you perform the given task.

When you’re prepared, you’re more confident. The stress that comes with uncertainty disappears when you’ve prepared appropriately, and with that, the likelihood of achieving the desired result is increased.

Be Accountable in Your Work

Being accountable is a trait that impacts many areas of life, even outside of your career. When things don’t go right, which is bound to happen many times over your career, it’s easy to blame other people or external factors. However, by taking ownership of your work, you’ll stand out from other workers, and you begin to build trust with the people around you.

While being accountable to others is excellent, it doesn’t stop there. It’s also important to be responsible for yourself and your goals. For example, if you want to get promoted over the next year and you’ve laid out the steps needed to make it happen, stick to them. Too often, we set goals for ourselves, like New Year’s Resolutions, and end up leaving them behind when life gets in the way.

Embrace Your Team

In both the workplace and sports, being successful almost always requires good teamwork.

The backbone of a championship team usually consists of two essential factors: cohesion and communication. But one doesn’t come without the other. Cohesion is formed through effective and consistent communication. These two traits then begin to form a solid foundation of trust, leading to better, more efficient work.

Having a good relationship with a team or coworkers can create healthy competition, and a great example of this is the sales profession.

Imagine being a salesperson who works alone, didn’t have a team to fall back on, and didn’t know how the rest of the team was performing. They might get discouraged or lose sight of the end goal. So, there’s a reason that most sales teams operate together - it can create a healthy competitive atmosphere, increases engagement, and keeps everybody’s motives and goals aligned.

Aside from the performance aspect, embracing your team and having an enjoyable workplace makes work that much easier, and the foundation is built through being reliable, offering help to others, and being a good teammate.

The Takeaway

In our careers, it’s easy to lose sight of an end goal and feel like we’re not making progress. But when you treat your career like a sport and strive to get better, it starts to feel like a natural part of your life, not just another task to check off the list each weekday.

4 Creative Ways to Reduce Business Expenses During Coronavirus

In the era of COVID-19, the consumer market has been anything but normal, causing many businesses to scramble in response. Even as time has progressed, a survey of CFOs indicated that the financial impacts of coronavirus have consistently been a top concern.1

If your company needs to contain costs in order to achieve financial stability - during a time of extreme instability - these four strategies can be used to help consolidate your spending and protect the longevity of your business.

Way #1: Switch to Remote Work

Over 60 percent of employees have transitioned to working from home as a result of the coronavirus.2 Remote work has experienced a huge surge in popularity, and for good reason; it can be a big saver when it comes to resource expenses, and it often goes hand-in-hand with implementing flexible work schedules and, as a result, different payroll procedures.

If your business is in a position where it can adapt to remote work, take the opportunity to do so. This will drastically reduce employee-related expenses and can also serve as a segue into other cost-saving actions.

Other Employment Options

No one wants to be forced into the position of letting employees go. If COVID-19 puts your specific industry in a tight financial situation, or if you currently can’t conduct substantial business remotely or in-person, consider saving jobs by suspending benefits or adjusting some employees to part-time.

Way #2: Eliminate Unnecessary Expenses

If your company has made significant adjustments, such as transitioning to remote or partly-remote, chances are there are a lot of expenses you don’t need to be paying for anymore.

Office Supplies

Don’t let the excuse of “stocking up” stop you from cutting costs on office resources. This includes everything from office equipment or space to simple expenses, such as toiletries or paper supplies.

Office Services

Make a point to round up all of your regular service expenses and decide what you need and what you can forgo, at least for the time being. Think about necessary utilities such as heat, water and electricity, but also don’t overlook other recurring subscriptions you may have, such as internet, phone or recreational services.

Travel or Parking

For most industries, travel expenses are already way down. Take further advantage of this by reducing parking expenses for parking spots you may not be utilizing. If you’re still having employees travel, it might be time to evaluate if it’s really necessary or not.

Way #3: Take Advantage of Flexible Billing

Many suppliers, banks and landlords are being flexible and understanding during this time. It may be worth it to at least reach out and ask what options may be available to you. They may allow you to delay certain payments or take out a loan until your business is in a better financial position.

If you take this route, be sure that you fully understand the terms of your agreement. The last thing you want is to get stuck in a worse financial position down the road.

Way #4: Rework Your Marketing

84 percent of marketers have been improvising new marketing strategies in response to COVID-19.3 You should try to reduce marketing expenses that no longer offer an advantage, such as an advertisements at large in-person events. This doesn’t mean, however, that you need to sacrifice or abandon your marketing efforts.

Get creative and dive into digital marketing. More people are on the internet now than ever, and if you leverage it correctly, you may just build your company’s presence and generate some more revenue.

Don’t lose hope if your company’s financial outlook is unclear. Simply continue to focus on your growth, find new ways to market your product or service and cut costs where you can.

- https://www.pwc.com/us/en/library/covid-19/pwc-covid-19-cfo-pulse-survey.html

- https://news.gallup.com/poll/311375/reviewing-remote-work-covid.aspx

- https://cmosurvey.org/results/

In 2020, The World Went Virtual. But Should Your Financial Planner Still Live in Your Area?

In early 2020, governments around the globe took drastic measures to slow the spread of Covid-19. As a result, we saw a major shift in the way we work, interact with others and go about our daily lives. While working with an advisor virtually is nothing new, the relevance of virtual advising has increased significantly amidst the global pandemic.

Money is one of the most personal and important aspects of your life, meaning you may feel more comfortable trusting someone you can get to know in-person. But with today’s technology and ongoing need to continue social distancing, now’s the perfect time to consider whether working with a local advisor is really a necessity or not. Instead of physical location, it may be more prudent to consider other factors, such as designations and certifications, years of experience, areas of expertise and more.

As you consider whether or not to work with someone in your area or beyond, ask yourself the following questions.

Am I Comfortable Utilizing Technology?

Virtual advisors will likely want to meet with you face-to-face over video chat, whether through Skype, Zoom, Facetime or other video conferencing tools. They’ll likely want to share their screen with you, go over important documents and even have you virtually sign paperwork. When you’re not meeting virtually face-to-face, you’ll likely have access to view your portfolio and other financial information online.

It’s likely your advisor will work with you to try to make your experience as comfortable as possible. They can provide instructions for using their tools and answer any questions you may have to help ease your concerns. But if you’re still uncomfortable with building a technology-heavy relationship with your advisor, working with someone local may be better.

What Services Do I Need?

The type of services you’re looking for from an advisor may shape the type of relationship you’re looking to build. If you’d prefer to remain fairly hands-off or you have a demanding schedule, working together virtually may be much more preferred than meeting in-person during office hours. On the other hand, if you prefer to work together closely with your advisor, drop by their office to ask a question or check-in often, you may be more comfortable working with an advisor within driving distance.

Do I Need an Advisor With Certain Expertise?

Another important consideration is experience and credentials. If you’re in need of someone with a specific niche (such as handling student loan debt for medical professionals), there may not be an advisor who specializes in this in your area. If that’s the case, it may be worth working with someone virtually who can provide the expertise you’re looking for.

In a world that’s gone virtual, working with an advisor simply because they are local is no longer a necessity. The technology to build a well-developed relationship virtually is there, and it’s being utilized by thousands of advisors, brokers and agents around the globe. The important thing is to determine what you’re comfortable doing when it comes to your money and finding a partner who will be compatible and capable of helping you reach your goals.

Franklin Madison Advisors, Inc. (“FMA”), is a registered investment adviser firm with its registration and principal place of business in the Commonwealth of Pennsylvania. Registration of an investment adviser does not imply a certain level of skill or training. FMA is in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which FMA maintains clients.

This commentary and forecasts are limited to the dissemination of general information pertaining to Franklin Madison Advisors’ investment advisory services and general economic and market conditions and are subject to change without notice. The information contained herein is not intended to be personal, legal, investment or tax advice or a solicitation to buy or sell any security or engage in a particular investment strategy. For additional information about FMA, including fees and services, please contact FMA or refer to the Investment Adviser Public disclosures.

FMA may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Any subsequent, direct communication by FMA with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For additional information about FMA, including fees and services, please contact FMA or refer to the Investment Adviser Public disclosures. Please read the disclosure statement carefully before you invest or send money.

How Fast Can You Break Free from Student Loans?

Eliminating student loan debt can put you on the fast-track to achieving your essential life goals. If you’re one of the millions of Americans struggling with this vital issue, you know first-hand the challenges of student loan debt. As student loan balances continue to balloon from one year to the next, what can you do to conquer this overwhelming debt load? Well, many people are waiting for an act of congress to make their student loans disappear.

Yet, chances are that it will be on you to forge a path toward financial liberation. If you’re serious about freeing yourself from student loan debt, you’ll need to take steps that you might not have considered before. These actions include evaluating how much minimum payments on your student loans cost you, curbing unnecessary interest expenses, and finding simple ways to come up with extra cash to pay down loan principal. Making these steps a priority might enable you to eliminate debt sooner and give you the ability to focus your efforts on your most essential life goals.

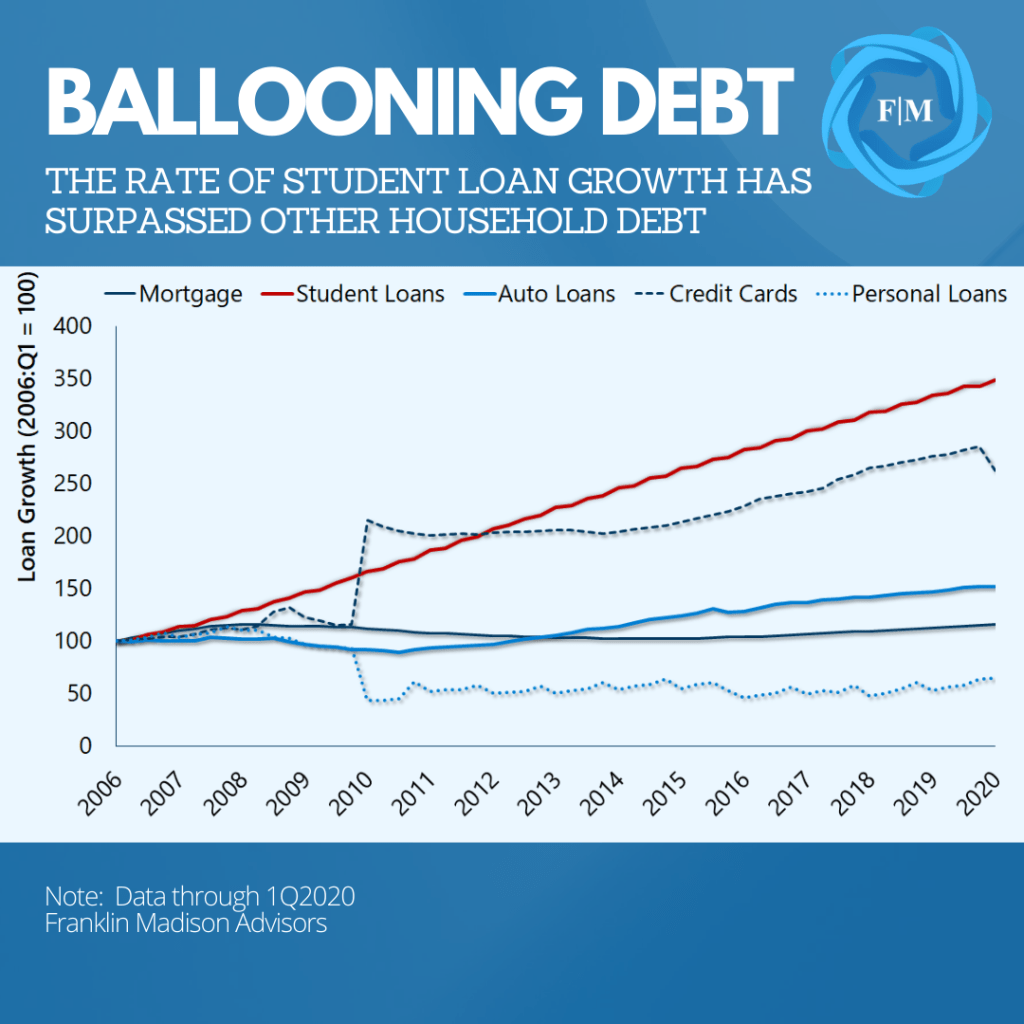

The Burden of Student Loan Debt

Student loan debt issuance has skyrocketed over the past decade. Government data out in the first quarter showed that total student loan debt outstanding reached $1.7 trillion. Of the amount outstanding, three-quarters were federal direct loans. This ownership share suggests that if you have a student loan, then there’s a good chance that Uncle Sam owns it. And if you feel like your debt burden is unreasonable today, you’re not alone.

Balances outstanding now average $35,000 for the nearly 40 million individuals who have federal student loans -- a figure that has doubled since 2007. And while the number of borrowers has increased by 40% over the past seven years, loan default rates have nearly tripled. If you want to pull yourself out of your student loan debt trap and forge a path to financial liberation, you’ll need to make decisions about your student loans that different than what most people are doing right now.

Relief in Times of Uncertainty

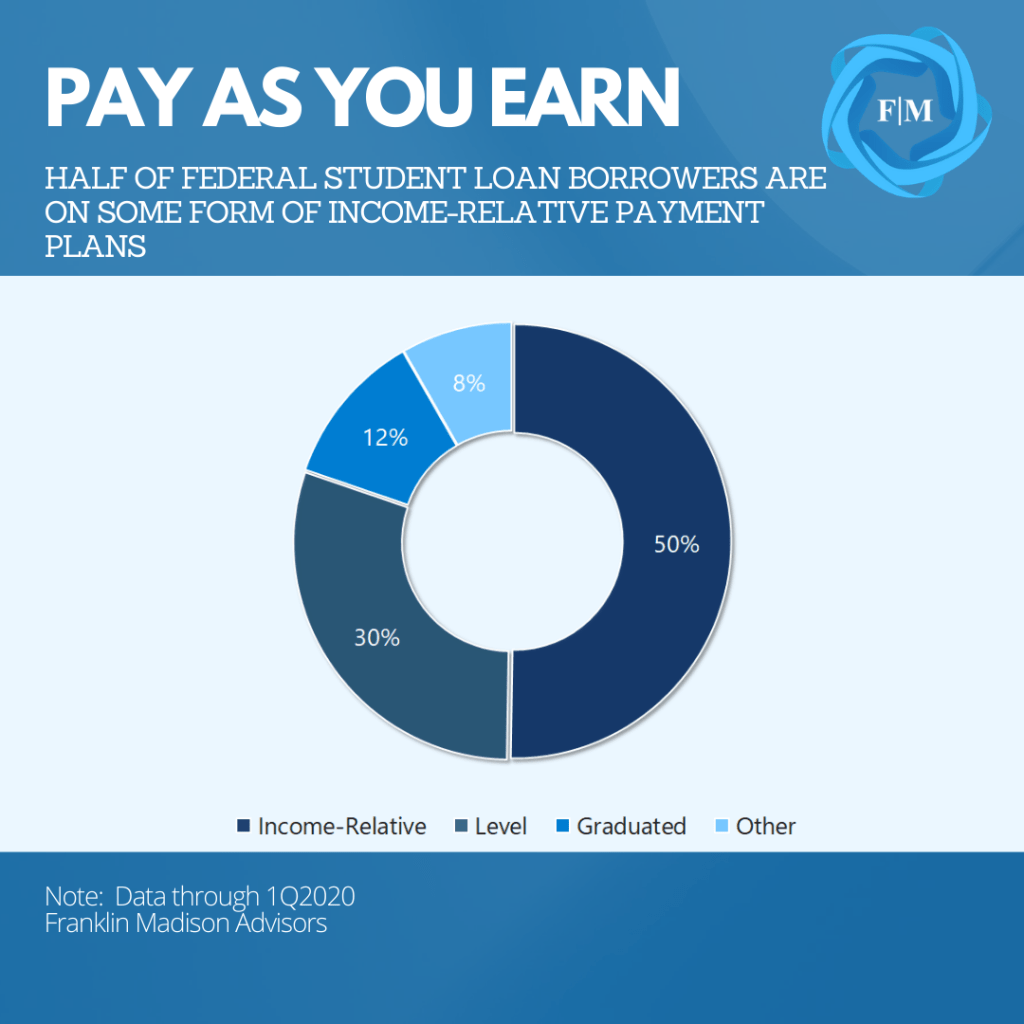

Many college students assume that money borrowed to finance education costs can be reasonably paid back over ten years. This seemingly short payback period is one reason some individuals choose to take on student loans in the first place. By the time they graduate, however, many students accumulate so much debt that they find it challenging to make their standard level payment. That’s when some borrowers choose to utilize income-relative repayment programs.

According to government data, over half of federal direct loans are in some form of an income-relative repayment as of the first quarter of 2020. These programs include Pay as You Earn (PAYE), Revised Pay as You Earn (REPAYE), Income-Based (IBR), and Income-Contingent (ICR) Repayment. The common thread running through these programs is that your monthly student loan payments are based on how much you take home per year rather than a level, amortized loan amount.

Income-Relative Plans: Not a Long-Term Fix

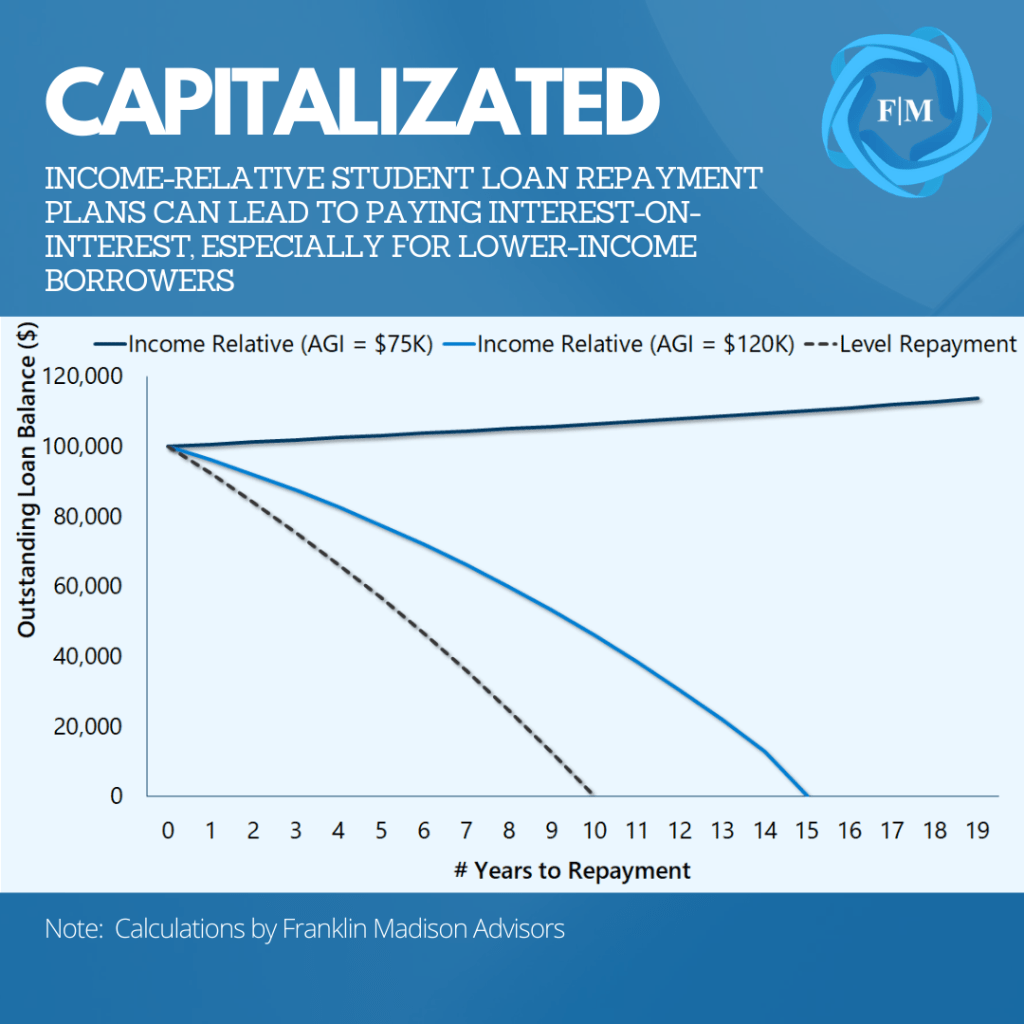

For example, consider a couple with an adjusted gross income (AGI) of $120,000 per year and $100,000 in student loan debt. Under an income-relative plan, the couple might pay an extra $18,000 in interest expense over the lifetime of their loan compared to level repayment. This difference is due to the fact that it would take 16 years to repay the debt compared to 10 years under a level repayment plan, therefore accumulating more interest.

The drawbacks of an income-relative plan become more evident as we move down the income scale. For a similar household with an AGI of $75,000 instead of $100,000, lifetime interest payments would be nearly $84,000 higher than compared to a level plan. What’s more, because monthly payments barely cover interest expenses in this scenario, the unpaid interest is capitalized or, in other words, added back to the principal amount of the loan.

The effect is that the borrower’s total loan outstanding rises over time rather than being paid down. While many income-relative plans allow for loan forgiveness after 20 or 25 years, these borrowers are not completely off the hook. Debt forgiven is, in some cases, considered taxable income. Therefore, the remaining balance might lead to a tax bill of $23,000 for this couple at the end of 20 years.

It is crucial to understand that income-relative repayment plans are an expensive way to pay down your student loan debt. While useful for addressing short-term challenges to your financial situation, these programs should not be relied upon as a long-term approach to paying down debt. If you’re participating in an income-relative repayment program, and are serious about conquering your student loan debt, it might be time to examine what this payment program is costing you.

Avoid Capitalizing Interest

If you’ve ever experienced hardship as a student loan borrower, you probably know how payment forbearance can help you manage obligations during times of financial uncertainty. Forbearance programs allow you to delay making payments on federal direct (and some other loans) for up to 12 months at a time. And today, there are approximately 3.8 million direct loan borrowers in forbearance with outstanding balances that are growing at a rapid rate.

While beneficial in the short-term, this program can undo the progress made on paying down your loans and, in some cases, leave you with a higher balance than with what you started. As noted earlier, capitalizing interest expenses is the quickest way to derail your student loan repayment plans. While income-relative programs might lead to higher debt levels for certain individuals, participating in a forbearance program will almost certainly cause your outstanding loan balance to rise. Let’s use an example to demonstrate this point.

The Cost of Forbearance

Recall the earlier illustration of a couple with a household AGI of $120,000 and $100,000 in student loan debt. Under an income-relative repayment plan, they might pay off their student loans in about 15 years, costing them about $152,000 over the lifetime of their loan. Now, what would happen if we introduced forbearance into the picture?

Assuming that this couple used forbearance to delay payments by 36 months, their student loan would cost over $191,000 by the time the debt is paid off and $40,000 more than had they avoided forbearance. Capitalized interest increases the outstanding loan balance and leads to paying interest on top of interest. What’s more, in this scenario, the payback period for the loan goes from 15 years to more than 20, leading to a hefty tax bill when the loan is forgiven.

And how does forbearance affect level repayment plans? Well, $100,000 in student loan debt amortized over ten years at 5.5% interest will accumulate about $33,000 in interest expense. Placing their loans into forbearance for 36 months, the couple would end up doubling interest expense. Because the borrowers are now making up for lost time when payments were postponed and paying interest on top of interest, it might take 15 years to repay their level loan versus the 10 years had the borrowers avoided forbearance.

The point here is that while forbearance is a useful tool that can help you navigate times of financial stress, when possible, it should be used only as a last resort. More to the point, if you do come upon tough financial times, prioritizing interest payments can help you avoid capitalization. Indeed, if your goal is to quickly conquer student loans and pay down your debt, then not paying interest on top of interest is crucial to this aim.

A Little Extra Goes a Long Way

Income-relative repayment plans can lengthen the time it takes to repay your student loans, while forbearance can lead you to pay interest on top of interest. If your aim is to eliminate student loan debt, consider alternatives to income-relative payment plans, and avoid forbearance. Then, create a strategy to make additional principal payments on your student loans.

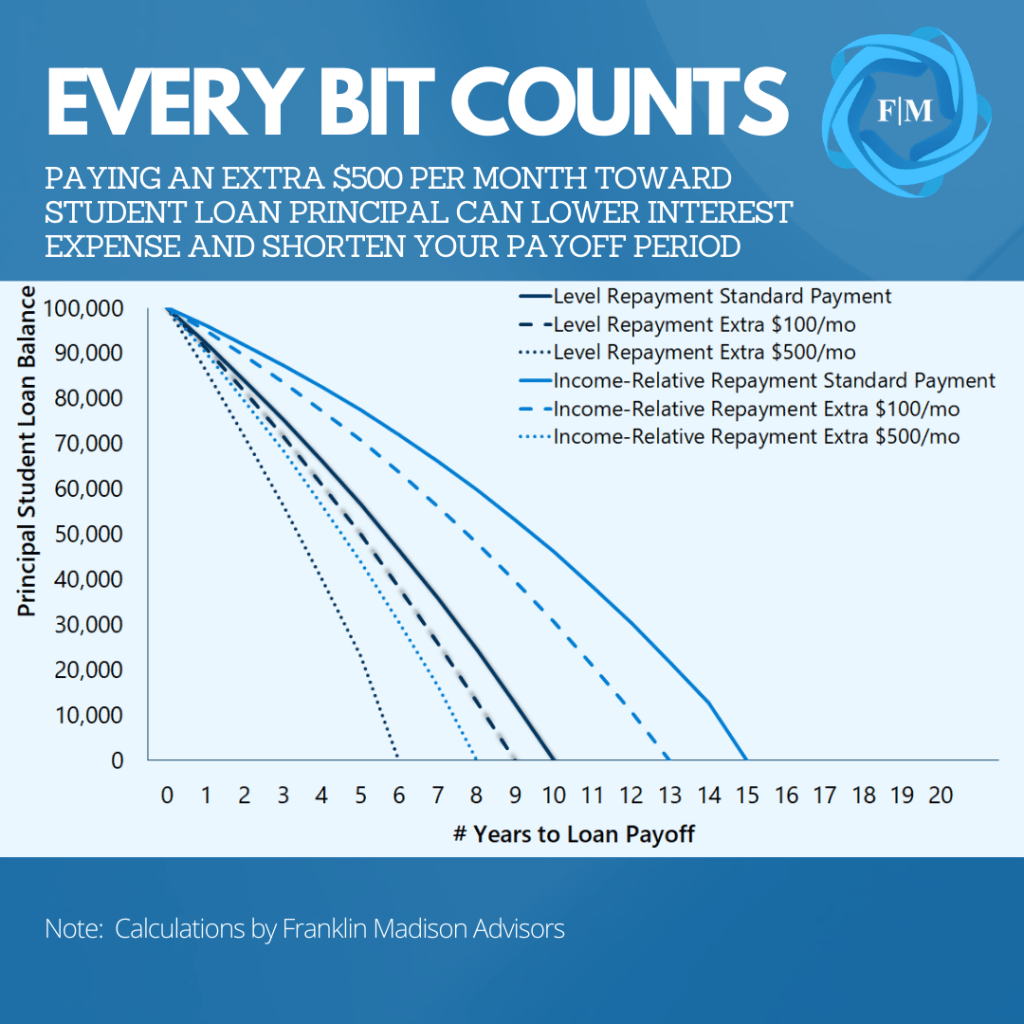

Indeed, whatever your chosen repayment program might be, every extra payment you can make on your loans can shorten the time it takes to pay off your debt and reduces interest expenses. For example, finding a way to pay an extra $100 per month on a $100,000, 10-year level repayment student loan can modestly reduce interest costs and cut your student loan payoff period by a full year.

How does this apply to income-relative payment plans? When using some of the same assumptions as before, making an extra $100 payment on your student loans can result in even more significant financial savings and shorten your payback period. Recall that for a couple with an AGI of $120,000 and $100,000 in debt, it might take them just over 15 years to pay down their student loans. By paying down an additional $100 in principal per month, they can eliminate debt in 13 years and save over $8,000 in interest expenses.

Taking this example one step further, let’s look at increasing principal payments from $100 to $500 per month. In our 10-year level payment scenario, committing $500 per month to principal reduction would reduce the repayment period to just over six years and lower interest expenses by a third. For the income-relative scenario, a similar contribution could cut lifetime interest costs and the repayment period in half. The point here is that every dollar that you can commit to paying down principal puts you one step closer to student loan debt liberation.

How to Eat an Elephant

Desmond Tutu was once quoted as saying that the only way to eat an elephant is a bite at a time. In the case of student loans, paying down your debt won’t happen overnight. However, as we just illustrated, finding ways to commit even a little extra money to pay down student debt principal can shorten your payback period and minimize interest expenses.

Even so, finding an extra $100 or $500 per month might seem like a daunting feat for some individuals. What can you do to come up with extra money to pay down your student loan debt faster? Here are a few suggestions:

- Make a Budget, Prioritize Debt Repayment– What gets measured, get managed. Knowing where your money is going every month can help you identify ways to reduce or eliminate spending and free up cash that can be applied to paying down student debt. The short-term sacrifice of prioritizing debt repayment by reallocating spending away from non-essential matters and toward paying down your debt for the next few years might lead to a lifetime of financial gain.

- Pay Down Smaller Debts First – If you have multiple student loans, prioritizing the payoff of your smallest balances can help free up cash to pay down your higher balances. The idea here is to quickly pay off debts with low balances and then apply the extra monthly cash flow to pay down your next smallest account balance, repeating until your student loans are paid off. Applying this same principle to credit card balances is another way to free up some extra cash. On average, Americans carry credit card balances of $6,200 and make minimum payments of $120 per month. Paying off your small credit card balance then applying those payments to your student loans is another way to reduce your student debt quickly.

- Consider Refinancing – Interest rates have fallen considerably over the past year. With student loan rates as low as 3.5%, refinancing higher interest student loan debt can lower your monthly payment. You can then use the money saved on your monthly payments to pay down principal . However, keep in mind that certain benefits afforded to federal student loans (like forgiveness) may not apply if refinanced with a private lender.

- Use Windfalls to Pay Down Debt – You’re likely to come into some financial windfalls during the year. For example, many people receive a bi-weekly paycheck yet pay expenses monthly. This means that twice a year, you’ll have “extra” checks coming your way. If your budget allows for it, consider using these additional paychecks to pay down student loan balances. Also, consider applying other windfalls, like a tax refund or your stimulus check toward your principal loan balance.

Student Loan Debt Liberation Begins with You

What could you do with an extra few hundred or thousand dollars per month right now? For some individuals, this additional cash might make the difference between buying a bigger house or a newer car. It could even mean getting closer to critical financial goals like funding a college savings plan for their children or shoring up retirement savings.

While many people are waiting on an act of congress to make their student loans disappear, you will likely need to forge your own path toward financial freedom. This includes limiting the use of costly income-relative repayment plans and avoiding capitalized interest. To be sure, taking a measured approach to paying off your student loans may liberate you from seemingly impossible debt and put you on the fast-track to achieving your essential life goals.