Manage Your Tax Anxiety and File Your Returns with Confidence

Is tax anxiety causing you to wait until the last minute to file your tax returns? If so, then you’re in good company.

According to one survey, over thirty percent of respondents said they waited until the tax filing deadline to prepare their returns last year.

Now, if you’re one of these individuals, there’s likely many reasons why you’ve chosen not to file your taxes yet.

Maybe you anticipate owing money to the government this year and you’re using every last moment to wait to pay Uncle Sam his owed money. Or, you might find the process to file your returns complicated and it just stresses you out. Or maybe, you haven’t found the time to sit down and complete your returns and you just need to put it on your to do list.

Whatever your case may be, you should know that the April 18 deadline to file your tax returns is just a few weeks away. And while it may seem like you have enough time to get the work done, in some instances, the longer you delay, the more it could cost you.

Indeed, for many individuals, filing your taxes is just a process of sitting in front of your computer, entering your tax documents into planning software and either choosing how you want to receive your tax refund or cutting a check to the IRS.

So, what can you do if you find yourself paralyzed by indecision and hesitant to prepare your returns?

Well, the truth is that you can overcome the anxiety that comes with filing your returns by following a simple process to get the job done. Indeed, knowing what you should do before, during and after you file could give you the motivation to finally complete your returns sooner rather than later.

And, at a basic level, using a stepwise approach to navigating your returns process may help you reduce your anxiety levels and avoid some costly mistakes commonly associated with procrastination and avoidance this tax season.

What to do Before You File Your Returns

Now, depending on your situation, one of the first things that you'll likely want to do before filing your returns is to evaluate whether you should file your returns on your own or take the time to go about hiring a professional to help complete your returns.

If you're still trying to determine which route you should take, be sure to take a moment to review our recent article where we discuss the criteria for evaluating when to go it alone and when hire a tax pro.

Either way, before you begin calculating your tax for the year, you’ll likely want to make sure that you have gathered all the proper documents to complete your tax return. Doing so will ensure that you’re accurately accounting for all income received, and not missing out on potential tax penalties or opportunities down the road.

And, so, how do you know whether you've gathered all the necessary information to complete your return?

Well, start by creating a checklist of all the documents and forms needed to complete your tax return, such as W-2s, 1099s, and receipts for charitable donations, medical costs, and other deductible expenses.

And if you need help figuring out where to start with your checklist, take a moment to review last year's tax returns. Indeed, by reviewing last year's return, you can identify the documents and forms that were required to complete your return and can help ensure that you have not overlooked any necessary paperwork.

Another option for ensuring that you have all the necessary documents to file your return is to log in to online portals for your current and former employers, financial institutions, and other organizations that may be required to provide tax documents, such as W2s, 1099s, mortgage or interest statements.

And finally, you can complete a tax organizer to ensure that you have gathered all of the documents necessary to prepare your return.

And, so, what is a tax organizer?

Well, a tax organizer is a tool that is used by tax professionals to help individuals gather and organize the information needed to prepare an accurate tax return. It typically includes a list of questions and prompts to help you identify and provide all the necessary information to complete your return, as well as worksheets to organize and summarize the data.

And when in doubt, completing your organizer can facilitate better communication between you and your tax professional, ensuring that all necessary information is obtained and questions are answered promptly.

Either way, before you get started with filing your returns, be sure to organize all tax-related documents in a secure and easily accessible location, such as a dedicated digital vault or online storage service.

And if you’re not sure how to go about this process, be sure to check out our FI|Mastery January action items for tips on ideal storage locations for critical documents and how tax organizers work.

Which institutions should I contact if I have problems?

Now, it's vital to note that reporting institutions can and do make errors in the tax documents they send to you. These errors can be as simple as omitting a taxpayer ID number to something as costly as reporting the wrong cost basis on a 401k rollover that could potentially cost you thousands of dollars in taxes due.

So, what can you do if you discover an error in one of your tax documents?

Well, first things first, contact the issuer of the tax document, such as your employer or the financial institution that sent you the tax form, and inform them of the error as soon as you discover it. Then, explain the nature of the error and provide any supporting documentation if necessary.

Next, request that the issuer provide a corrected tax document as soon as possible. In most cases, they’re required to provide a corrected form by January 31st, but, given that we’re past that deadline now, it will likely take a week or two to receive the updated document so plan accordingly.

That’s why getting started on your taxes sooner rather than later can help you avoid the anxiety related to working against a tight deadline. And when you do receive the corrected tax document, take a moment to review it to ensure that the error has been corrected and that all other information is accurate.

Now, keep in mind that if you discover an error on a tax document after you've already filed your return, you have the option to file an amended tax return to correct the error. With that said, the amended return must be filed within three years from the original filing deadline or two years from the date the tax was paid.

Overall, however, as you’re working to get your tax documents corrected, keep records of all communications with the document issuer regarding the error, as well as copies of the original and corrected tax documents and any other relevant paperwork.

These records may be necessary if the error is not corrected or if the IRS questions your returns down the road. And when in doubt or if the error is complex and you're unsure how to proceed, you may need to seek the assistance of a tax professional or accountant.

Finally, before you begin the process of preparing your returns, you’ll likely want to evaluate whether you should make a prior year contribution to an IRA before the tax filing deadline. This approach makes the most sense if you want to take advantage of a traditional IRA tax deduction for the prior year if you have the cash to do so.

For instance, if you didn't reach the annual contribution limit for the previous tax year, or came into windfall income in 2023, such as a bonus or inheritance, you have the option of using your current income to make a prior year IRA contribution.

Now, it's critical to note that the contribution limits and tax benefits associated with IRAs can vary depending on several factors, such as your income level, age, and marital status. Therefore, carefully consider your specific situation to see if it makes sense to make a prior year IRA contribution.

Things to Consider as You File Your Returns

Alright, now that you've organized your documents, gathered all of the necessary data, and tied up loose ends on contributions, it's time to begin filing your returns. As you do, however, there are a few critical tax choices you'll likely need to consider as you begin filing your return, including your filing status, understanding the difference between tax credits and deductions, knowing when to itemize, and being mindful of considerations for reporting cryptocurrency assets to the IRS.

Determine Your Filing Status

Now, determining your filing status is often as simple as evaluating whether you're single or married. If you're single and have no children, then your filing status can be rather straightforward. But what if you're unmarried, paid more than half the cost of keeping up your home for the year, and you have a qualifying person living with you, such as a dependent?

Well, in this case, claiming the "head of household" filing status could make sense. Why would you choose this route? Well, compared to the standard deduction of $13,850 for a single filer in 2023, an individual filing as head of household could qualify for the higher standard deduction of $20,800 so long as you meet the qualifying requirements.

And for you married folks out there, more often than not, it makes sense to simply file as "married filing jointly". But how do you know when it might make sense to choose the "married filing separately" route?

Well, here are a few situations where it might make sense to take the filing separately route, and so let’s look at a few examples.

High Itemized Deductions

First, if one spouse has a significant amount of itemized deductions, such as medical expenses or charitable donations, these can only be claimed if they exceed a certain threshold. Depending on your income level and unique situation, filing separately may result in a larger tax benefit in this instance.

Separate Finances

Next, if each spouse has separate finances and wants to be responsible only for their own tax liability, filing separately may work for you. This approach is common in situations where a couple is recently married and one spouse has significant tax liabilities or unpaid taxes from previous years.

Income-based Deductions or Credits

Now, being able to claim certain tax deductions or credits, such as the Earned Income Tax Credit or the Child and Dependent Care Credit may also be another reason to file separately. That’s because these credits have income limits, and so in some situations, it can be more advantageous for married couples to split their financial situation to claim the credit rather than filing jointly and missing out on the benefit altogether.

Student Loan Payments

And finally, if one spouse has significant student loan payments and is enrolled in an income-driven repayment plan or a Public Service Loan Forgiveness Program (PSLF), filing separately can result in lower monthly payments and improve qualification criteria to receive loan forgiveness.

Now, with all that said, in many cases, if you’re married, filing jointly can result in a lower tax liability overall, as it allows you to take advantage of certain tax deductions and credits that are not available to those filing separately.

Either way, it's critical for you married couples out there to carefully consider your options and consult with a tax professional to determine the most advantageous filing status for your specific situation.

What's the difference between a tax credit and tax deduction?

Another critical concept to understand as you're filing your returns is the difference between a tax credit and a tax deduction.

So, what is a tax credit?

Well, a tax credit is a dollar-for-dollar reduction of the amount of tax owed. For example, if you owe $5,000 in taxes and are eligible for a $1,000 tax credit, your tax bill could be reduced to $4,000.

What’s more, tax credits can either be refundable or nonrefundable. For instance, refundable tax credits can result in a refund if the credit exceeds the amount of tax owed, while nonrefundable tax credits can only reduce the amount of tax owed to zero.

Now, a tax deduction, on the other hand, reduces the amount of income that is subject to taxation. Deductions are subtracted from your gross income to arrive at your taxable income, which is then used to calculate the amount of tax owed.

For example, if you earned $150,000 and were eligible for a $20,800 deduction, your taxable income would be reduced to $129,200, which would result in a lower tax liability.

Either way, when planning for future taxes, it's essential to consider both tax credits and tax deductions to determine the most effective tax strategy. This may involve maximizing deductions to reduce taxable income, while also taking advantage of available tax credits to further reduce your tax liability.

Indeed, understanding the difference between these two tax concepts can help you make informed decisions about your tax planning strategies and ultimately reduce your overall tax burden this return season.

Itemize or Standard Deduction?

Another point to consider as you’re preparing your returns is whether to itemize or take the standard deduction for the year. And in the current environment, more often than not, it makes more sense to take the standard deduction than to itemize.

Indeed, fewer and fewer individuals have itemized their deductions since the Tax Cuts and Jobs Act (TCJA) was passed in 2018. That's because this legislation provided a significant boost to the standard deduction, and in 2019, this figure nearly doubled for single filers from $6,500 to $12,000 and from $13,000 to $24,000 for married filers.

And this change in policy was so effective that the number of itemized deductions filed in the year after this change in legislation was introduction fell by nearly half as individuals chose the higher standardized deduction.

Now, while the standard deduction is generous, there are still several reasons why you may want to consider itemizing deductions on your tax return this year.

For example, there are certain deductions that are only available if you choose to itemize, such as charitable contributions, medical expenses, and state and local taxes. If you don't itemize, you won't be able to take advantage of these deductions, even if they would result in a lower tax liability.

Itemizing your deductions can also provide greater flexibility in your tax planning. For example, if you have a large number of deductible expenses in one year and few deductible expenses in another year, itemizing allows you to maximize your deductions in the year when you have the most expenses.

And while the TCJA limited the amount of state and local tax (SALT) deductions that taxpayers can take, if you live in a high-tax state or have significant property taxes, your SALT deductions may still exceed the standard deduction, making it beneficial to itemize.

Even if you believe that your standard deduction will be higher than their itemized deductions, it is still essential to consider itemizing your deductions if you're a high-income earner, have had significant medical expenses recently, or have made considerable gifts or charitable contributions in the past year. Indeed, itemizing can provide greater flexibility and access to certain deductions, potentially resulting in a lower tax liability.

Cryptocurrencies and Your Taxes

And finally, don’t forget about Cryptocurrencies as you prepare to file your taxes this year. This topic is especially salient if you have bought or sold cryptocurrencies because the IRS treats crypto as property for tax purposes, which means that gains or losses from buying, selling, or exchanging crypto are all taxable.

Along these lines, it's critical to keep accurate records of all cryptocurrency transactions, including the date, value, and purpose of the transaction. This information will be needed to calculate any capital gains or losses for the tax year.

And when calculating gains or losses, you'll need to determine the cost basis of your cryptocurrency, which is the amount you paid for the crypto, including any fees or commissions and the cost basis which is used to calculate the gain or loss when the cryptocurrency is sold.

And if you think that your crypto is anonymous and you can avoid reporting your transactions for the year, think again. The IRS has recently introduced steep penalties for individuals who try to hide their cryptocurrency dealings, which, more often than not, can be discovered through a simple audit should you be subject to one. Either way, when in doubt, consult with your tax pro to evaluate the best path forward for reporting taxes on this speculative asset class.

Wrapping Up Your Returns

Now that you've gone through the process of collecting your tax documents and making critical elections for your returns, there are likely a few loose ends that you should consider as you wrap up your return filings, including whether to make estimated payments or prepay next year's tax from your return, evaluating tax planning opportunities or even deciding whether to file for an extension if you need more time to prepare your return.

Now, if you've filed your taxes and find that you owe Uncle Sam a considerable amount of money this year, you will likely understand the sting of the IRS's underpayment penalty. One way to avoid this same sting next year is to begin making estimated tax payments this year.

Indeed, if you owed a substantial amount to the government this year, then you may need to make estimated quarterly tax payments if you anticipate the same circumstances that led to your high tax liability last year to persist this year.

And, generally speaking, you are required to make estimated quarterly tax payments if:

You expect to owe at least $1,000 in tax for the year after subtracting your withholding and refundable credits, or if you expect your withholding and refundable credits to be less than 90% of the tax you owe for the current year, or 100% of the tax you owed in the previous year.

If either of these conditions apply, then you likely must make estimated quarterly tax payments to avoid underpayment penalties and interest.

It's also critical to note that in certain instances, you can simply adjust the withholding on your W4 form to increase the amount of tax withheld from your paychecks throughout the year to ensure that you’re paying enough tax and to avoid having to make estimated quarterly tax payments altogether.

Now, another option for avoiding an underpayment penalty next year is prepaying your tax liability for the coming year from your tax refund, if you received one this year. Indeed, applying a tax refund to an anticipated tax liability for next year can have several benefits.

For example, it can help reduce your future tax liability by paying some of the taxes owed in advance. This approach can help you avoid coming up with a large lump sum payment should you have taxes due next year and also reduces your risk of owing additional penalties and interest.

Applying a tax refund to an anticipated tax liability the coming year can also simplify your tax planning. Indeed, by knowing in advance that you have already paid some of your taxes owed, you can more accurately plan your cash flow, budgeting, and financial decisions.

Reviewing Tax Planning Opportunities

And, along these same lines, now may also be a good time to evaluate your tax planning opportunities for the coming year now that you have a better understanding of your current tax situation.

So, how do you go about the tax planning process?

Well, to start, review the amount of taxes withheld from your paychecks or other income sources to ensure that you’re paying no more or no less than needed based on your tax liability for the prior year.

If necessary, adjust your withholding by filing a new W4 form with your employer to ensure that you're paying just the right amount of tax for the coming year. And if you’re not sure how to adjust your withholdings, the IRS has a tool on their website that you can use to evaluate whether you’re withholding the right amount of money, so be sure to check that out.

And if you're not maximizing your retirement savings, now may be the time to consider increasing your contributions to an employer-sponsored retirement plan such as a 401k or 403b, or a traditional IRA as a way to reduce your future taxable income.

Also, if you participate in a High Deductible Health Plan (HDHP), now’s a great time to review your current health savings account (HSA) contributions and consider increasing this amount during your next benefits election cycle if you’re not already maxing out your contributions. Doing so can help reduce taxable income and provide a tax-free source of funds for medical expenses down the road.

Finally, reviewing your investment strategy is also a key component of tax planning. Here, you'll want to evaluate the kind of income produced by your investment portfolio to ensure that the right assets are located in the appropriate tax-advantaged accounts, and to evaluate ways to optimize income-producing assets for your particular tax bracket.

When to File an Extension

Now, if your anxiety has gotten the best of you and you’ve put off filing your returns for too long, you may finally come to realize that you need more time to prepare your returns. This situation may apply if you have incomplete tax paperwork, an unexpected life event, or you simply need more time to make a strategic tax decision.

And if you begin filing your returns and find yourself in this situation, before you stress out, consider filing an extension.

Indeed, if you need more time to file your federal income tax return, you can request an extension from the IRS by obtaining Form 4868, or the Application for Automatic Extension.

This form is available on the IRS website or can be obtained from a tax professional. And you can submit the form electronically using the Free File service online or by mailing a paper form to the IRS.

Finally, once the request is processed, the IRS will grant an automatic six-month extension, moving the filing deadline from April to October. And it’s worth noting that no explanation or documentation is necessary to receive the extension.

It's also important to note that filing an extension only extends the time to file the tax return, not the time to pay any taxes owed. You should work with your tax filer to estimate the amount of taxes owed and make a payment by the original due date to avoid penalties and interest. If you fail to pay the full amount owed on time, then you may be subject to penalties and interest on the unpaid balance.

Manage Your Anxiety and File Your Taxes with Confidence

If you're feeling anxious about filing your tax returns and tend to procrastinate, just know that you're not alone. However, delaying filing your taxes could end up costing you more in the long run than you had initially planned. The good news is that you can overcome your tax anxiety by following a simple process to complete your returns.

This approach may involve evaluating whether to file your taxes on your own or with the help of a professional, organizing your documents, understanding tax credits and deductions and deciding whether to itemize or take the standard deduction.

Once you've filed your returns, it's important to evaluate tax planning opportunities for the coming year and make adjustments to your withholdings as necessary. And if you find that you need more time to file your returns, consider filing for an extension.

Either way, don't let your tax anxiety get the best of you.

Indeed, by taking control of your finances and filing your tax returns with confidence, you can take one step closer to becoming the master of your financial independence journey.

3 Essential Steps to Start a Stress-Free Tax Season

Most individuals can't stand preparing their taxes. It's often a complex, confusing process that leaves many fearing the dreaded audit from the IRS.

And according to the latest data from the IRS, 1.8% of tax filers with reported total positive income between $1 and $5 million received an audit letter from the IRS in 2021.

While this number seems low, it certainly is higher than your chances of winning the Powerball lottery (currently 1 in over 292 million) and a key reason to have all of your ducks in a row before you file your returns this year.

Audits aside, being adequately prepared to complete your returns this tax season is essential to a stress-free and smooth filing season, especially if you have a complex financial situation.

Indeed, waiting until the April deadline to file your taxes this year could leave you with a last-minute scramble and the potential for lost opportunities (or unnecessary penalties) without proper preparation.

To be sure, the deadline for filing your taxes is months away, and you likely haven't received all of your critical tax documents from your employer and financial institutions yet. However, you can still do several things right now to prepare for the tax filing season.

This month, we'll cover a few essential items to consider as we head into the tax season, including what you should do with your tax documents, whether to file on your own or hire out help, and some key deadlines to consider ahead of the filing season.

To begin, let's take a look at one approach to efficiently organizing your tax return documents.

Establish a Place to Secure Your Return Documents

Now, whether you're filing your returns on your own or working with a tax professional, organizing all your essential tax documents in one place will simplify the process of completing your returns and shorten the time it takes to complete the task.

Over the coming weeks, you'll likely receive copies of your W2s, 1099s, and other essential documents, either digitally or in hard copies, by mail.

Many individuals who receive these documents in the mail set the envelopes aside in a kitchen drawer without taking a look at what they've received until it's time to file and then scramble to find all the necessary paperwork days before the filing deadline.

So, what should you do when you receive these tax documents?

Well, when you receive your tax documents, open the envelope or visit your financial institution's website and take a moment to review the records immediately. Believe it or not, it's common for financial institutions to make reporting errors.

Indeed, in several instances, we've had some clients receive 1099s with cost-basis errors on transferred securities and rollovers that could have cost them tens of thousands of dollars in taxes if we didn't catch the error early.

So, be sure to review those tax documents before you file them away.

Another big question when the emails or tax documents begin rolling in through the mail is, "where do I store these documents?"

The simple answer here is: digitize your documents. Even if you enjoy working with paper, take a few moments to take a quick picture of your tax document with your phone and email it to yourself. Doing so right away can ensure that you capture this critical paperwork correctly before you begin your filing prep.

And when it comes to storing digital copies of documents, some individuals prefer to store these documents on their computer or phone.

Now, while this approach works, consider saving these essential documents to a secure cloud-based server or digital vault like the one offered through your financial planning website.

Why?

Well, here are a few benefits to storing your essential tax documents on the cloud:

First, your documents will remain safe if something happens to your computer or phone.

This fact is especially salient if data is not recoverable from your computer or phone. It could also prevent essential documents from being inadvertently deleted or overwritten as many cloud providers offer backup services.

What's more, if you inadvertently download malware or ransomware, a fraudster could gain access to your computer, steal your personal information, or hold it hostage until you can pay them a ransom.

Another benefit to using a cloud-based approach to store your tax documents is that it likely will give you access to your records when you're away from your computer.

For example, suppose you're working with a CPA to prepare your returns and, for whatever reason, your professional has not received a critical document from you. In this case, having followed the simple steps we outlined earlier, you could simply log in to your cloud and send it to your tax professional without waiting until you get back to your computer.

To Do: Establish a Place to Secure Your Return Documents

So, what are your options for storing your tax return documents on the cloud? Well, some noteworthy options include Apple's iCloud service, Microsoft OneDrive, Google Drive, and Dropbox, to name a few.

Another alternative for storing your tax return documents securely is using the digital vault in your personal financial planning website provided to you by your financial planner. This approach offers the same conveniences as a cloud-based solution and also ensures that all of your critical financial documents are stored in the same place.

Whichever approach you choose during this year's tax season, be sure to take a look at your tax documents to catch errors early, grab a picture of your documents and store them in a cloud-based solution to avoid losing critical paperwork ahead of key filing deadlines.

Determine Who Will Prepare Your Return

Now that we've talked about organizing your paperwork, another essential component to being prepared this tax season is determining who will file your returns.

Now, whether you decide to file your own tax returns or work with a professional, knowing where you stand now will save you time and headaches down the road.

What to consider when self-preparing returns

If you have a simple financial situation and typically file a 1040EZ, then it likely would make sense to prepare your taxes on your own using online services like H&R Block or TurboTax.

If you've used services like these before, great! You're likely familiar with their features and benefits.

Either way, be sure to log in now, update your personal information, and familiarize yourself with any changes to the providers' products, services, and processes as you wait for your income and financial documents.

Doing so likely will make your tax preparations straightforward this year.

Another key consideration for many of you self-filers out there is, of the two biggest prepares out there (H&R Block and TurboTax), which would should you use? Well, when it comes down to it, most online services use similar approaches and get the job done.

H&R Block, however, is in many ways a lower cost option overall, and I've used their service personally for simple and complex returns over the past two decades without issue. Again, many of the major online tax prep services offer the same features and benefits. Which one you choose likely will come down to a matter of preference.

Either way, take time to evaluate your options and familiarize yourself with the various self-filing options out there. That way, you're not changing service providers a week or two before the April deadline and scrambling to learn a new system under the pressure of teh filing deadline.

When to hire a professional to complete your returns

Now, if you've had significant life changes in 2022 or your financial situation is more complex, then you're likely best served working with a professional.

So, if you decide to hire out the work and still need to find an accountant, you had better get looking sooner rather than later.

Make no mistake, it's getting harder to find qualified tax pros in recent years.

Indeed, given recent changes to the tax code, retirements, and other structural challenges, there has been a need for more qualified tax preparers.

And if you're in the market to have your taxes prepared for you, then you had better act now, as CPA bookings are filling up quickly.

So, what should you look for when hiring out your tax prep work? Well, as you go about looking for someone to prepare your taxes, consider asking the following questions before hiring a professional:

Ask about their specialization: CPAs (Certified Public Accountant) and EAs (Enrolled Agents) can specialize in many accounting areas, including business, government, and forensic accounting, as well as tax preparation. For preparing and filing your taxes, consider finding a professional specializing in individual income tax returns or business returns. If you have stock options, restricted stock, or other forms of stock awards, make sure your preparer is familiar with the tax consequences of these income sources.

Ask whether they're licensed: Believe it or not, there are some bad apples out there taking advantage of the accountant shortage and holding themselves out as CPAs when they're not. That's why it's essential to know that the state licenses CPAs, so before hiring one, you can search their records with your state's board of accountancy. Most states offer CPA databases that allow you to search by name and find important information on a CPA's license status, issue, expiration dates, and disciplinary actions and suspensions.

Ask if your preparer is experienced: While all CPAs are credentialed before offering their services, CPAs with several years of experience will more likely have a deeper understanding of the tax code than a newly certified individual. Surprisingly, not all professionals understand the tax consequences of equity compensation.

Ask if your preparer will sign your returns: Verify that your CPA or EA will sign your tax return and represent you before the IRS for any tax matter related to your return. If not, consider finding a professional who will.

Ask if they offer tax planning advice: A good tax CPA or EA will not only prepare and file your return for the current tax year, but they can also offer year-round tax planning advice to help you maximize your tax savings for years to come.

Ask how much they charge: CPAs and EAs can charge by the hour, flat fee, or other payment options based on the complexity of your taxes. This includes how many schedules and supporting forms you'll need to file with your return. Also, be sure to find out if their fees include federal, state, and local filing. Finally, CPAs generally are not allowed to base their fees on a percentage of your tax refund, so you may want to avoid this type of pay arrangement.

Ask if your preparer will file your returns electronically: The IRS lists several reasons why you should e-file your federal tax return. Chief among them is to ensure better accuracy and completeness for your return, but also because it adds safety and security for your information and results in faster refunds if you're due one. What's more, the IRS requires tax preparers who file 11 or more tax returns per year to provide e-filing services, so if a CPA or EA does not offer e-filing, they may not be very experienced.

Finally, ask how your preparer will support you if you get audited: No one wants to get audited, but they still happen, as we mentioned earlier. In that event, you'll want a qualified tax professional like a CPA to represent you before the IRS or Tax Court. They can gather your documentation to prepare your return and deal with the IRS directly if you authorize them to do so on your behalf. Having a licensed CPA discuss your tax return with the IRS is likely a better option than you doing it alone.

Taken together, if you're self-preparing your returns this year, be sure to identify your online tax prep service if you haven't already.

And if you're looking for help to file your returns this year, acting sooner rather than later may ensure that you find a qualified preparer before they get overbooked.

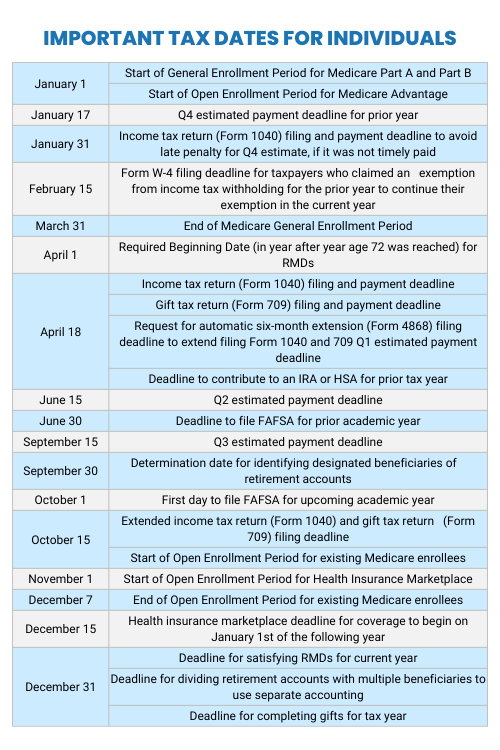

Stay Ahead of Key Deadlines & Milestones

Finally, as you secure a safe place for your return documents and settle on a service to prepare your taxes, you'll also want to ensure that you stay on top of crucial filing deadlines for the year.

To Do: Stay Ahead of Key Deadlines

Certainly, April 18, 2023, is likely the critical deadline you'll want to pay the most attention to this year.

But there are also other events leading up to and following the individual filing dates:

It's Not Too Early to Begin Preparing for Tax Season

While the April 15 deadline is still months away, there are still many things you can do right now to prepare for what is likely to be another hectic tax filing season in 2023.

This includes 1) taking a quick look at your tax documents and making a digital copy immediately upon receipt, 2) determining whether to self-prepare or hire out your tax returns this year, and 3) staying informed about key tax deadlines to avoid missing out on planning opportunities or tax penalties this year.

In our other posts, we cover essential life changes and events that could affect your taxes and last-minute tips to consider before filing your returns.

Either way, taking these first steps to prepare to file your returns could set you up for a stress-free tax season. But more essentially, doing the work now to get your financial house in order likely will put you one step closer to mastering your journey to financial independence.