How Smart Investors Profit from Tax Loss Harvesting

It's that time of the year again, and apple picking and pumpkin patches not only usher in traditional fall routines, they also signal that it's time for an annual review of potential tax losses you can harvest from your investment portfolio.

And you know, just as farmers come together to bring in the fall harvest before winter kicks in, prudent investors should take the time to review their portfolios for opportunities to harvest tax losses this season.

Now, for some of you out there, the idea of "harvesting" losses might seem counterintuitive.

That's because when we think of harvests, we tend to think of taking gains, not losses, right?

Well, while this point may be relevant in most situations, the truth is that a harvest can also happen when you act to avoid leaving money on the table.

Indeed, the key to growing and preserving your wealth isn't just about how much you make, it's also how much you keep.

That's why, just as farmers harvest their crops to reap the benefits of their sewing efforts, investors "harvest" losses to minimize tax expenses.

And so, by realizing (or "harvesting") losses, you can offset taxable gains elsewhere in your portfolio and avoid paying Uncle Sam any more than his fair share.

With that said, this process isn't just about selling all your losses. Indeed, it involves making sure that you’re harvesting losses in the right accounts, being methodical in your approach, and avoiding common and costly pitfalls that could derail all of your tax-savings efforts.

What is Tax Loss Harvesting?

Alright, so now that you understand that tax loss harvesting is a crucial component of your journey to financial independence, let's talk a little more about what it is.

What is Tax Loss Harvesting

Now, at its core, tax loss harvesting is a sophisticated financial maneuver that allows you to turn the tables on your investment losses. You can think of it as a silver lining to the occasional cloud of a poorly performing investment.

That's because, instead of merely accepting an investment loss when market volatility picks up, you can use it to your advantage.

How so?

Well, imagine for a moment that you've invested in a promising growth sector in the market, but because of some macro or micro concerns, the value of your investment has declined. While this position is undoubtedly disappointing, tax loss harvesting allows you to sell that investment and realize, or "harvest," that loss.

Now, this strategy shines because you can use the loss from this sale to offset capital gains from other investments. And remember, there's no free lunch in the world of investments, so then the profit you make when you sell an investment for more than you paid, which is called a capital gain, comes with a tax liability.

So then, by offsetting these gains with your harvested losses, you can effectively manage and potentially reduce the amount of taxes you owe to the IRS.

So far, so good, right?

Well, good news doesn't stop there.

You see, the added benefit here is that for someone in a high tax bracket, like many of you tech professionals and business owners out there, this strategy can be especially beneficial because the money you save on taxes can be reinvested, allowing your wealth to compound more efficiently over time.

At the same time, if your harvested losses exceed your capital gains in a given year, you can typically use some of your excess losses to reduce your ordinary taxable income.

And if there's still a remaining loss after that? You can carry it forward to offset gains in future years.

What Tax Loss Harvesting Isn't

Now, as we dive deeper into the topic of tax loss harvesting, it's crucial to clear up some common misconceptions about this strategy.

And to start, it's essential to note here that tax loss harvesting isn't a luxury reserved only for the ultra-wealthy.

In fact, while it might seem like a strategy tailored to those with only the biggest portfolios, the truth is that you can harness its benefits to manage your tax liabilities even if your investments are more modest than the typical billionaire.

Another misconception to consider here is the belief that tax loss harvesting offers a permanent tax reduction.

Now, while this process can indeed offset your capital gains in the current year, this approach is more about deferring taxes due to a future date. In other words, you can think of it as a strategic pause that gives you more control over when you'll face certain tax implications.

And finally, there's more to this process than simply the benefit of its tax-saving powers.

To be sure, beyond the tax benefits, tax loss harvesting is a gateway to portfolio rebalancing. And this approach is crucial to your investment strategy because, by offloading certain assets, you're not just optimizing for tax, you're also creating an opportunity to realign your investments with your long-term goals and vision.

And so, don't fall into the trap of thinking of tax loss harvesting as a one-time strategy, or something to be pulled out of the toolbox only during a particularly turbulent market year.

At the end of the day, it's a dynamic approach that can be woven into your annual financial rituals, allowing you to consistently manage and potentially reduce tax liabilities year after year.

To be sure, when you boil it down to its core, tax loss harvesting is about making the best out of a less-than-ideal situation. And, even when the market doesn't move in your favor in a given year, you still have this proactive strategy in place to mitigate the impact of a pullback.

Why Tax Loss Harvesting is a Game-Changer

Alright, so now that we've discussed what tax loss harvesting is and isn't, let's take a few minutes and talk through why you specifically would want to implement this approach in your portfolio.

Optimized Tax Management

Now, as someone who's achieved significant financial success over the years, you're likely no stranger to the hefty tax liabilities that often accompany significant capital gains.

In fact, as your earnings have grown over the years, you've likely looked at your tax bill with resentment and scorn as the government seems to keep an evergrowing share of your hard-earned wealth.

And so, if this is you, then tax loss harvesting might be your secret weapon here.

Indeed, by strategically selling off those investments that haven't performed as expected throughout the year, you can use those losses to offset the gains from the thriving assets in other parts of your investment portfolio.

What's more, in a situation where your losses surpass your gains, you have the added advantage of offsetting up to $3,000 of your ordinary income. Now, this might not seem like much, but every cent counts when it comes to minimizing taxes.

What's more crucial, however, is that this approach offers you flexibility during tax season and could position you in a more favorable tax bracket, ensuring that you're not paying Uncle Sam more than his fair share.

Strategic Financial Planning and Rebalancing

Now, another benefit to consider is that beyond the immediate tax season, tax loss harvesting is your ally for long-term financial prosperity.

To be sure, the ability to carry forward losses means that you're equipped with a tool to mitigate potential tax impacts in the years ahead.

But there's another layer to this strategy that you may want to consider.

For example, when you decide to offload those underperforming assets, you're not just cutting losses. What you're also doing is freeing up capital, that can be reinvested in opportunities that better align with the current market conditions and your financial goals.

A Proactive Approach to Setbacks

And finally, when it comes to reasons why you may want to consider this approach, you can think of it as a reset button to your overall investment strategy.

How so?

Well, think about it for a minute. In your own journey to professional success, you've likely faced challenges and setbacks that have forced you to stop what you're doing and evaluate the choices you're making in life.

In a similar way, the process of tax loss harvesting offers you a fresh perspective on setbacks in your portfolio. Indeed, instead of viewing them as mere losses, you can now see them as strategic levers, ones that can be pulled to optimize your financial outcomes.

And so, knowing that you can use the losses from an investment or trade that has moved against you might be the salve you need to move on from a position that may have never been a good fit in your portfolio, to begin with.

To be sure, this approach doesn't just offer peace of mind, it empowers you. It ensures that even when the market throws you a curveball, that you have a well-thought-out strategy in place which allows you to turn potential challenges into tangible opportunities.

In essence, tax loss harvesting isn't just a financial tool, it's a mindset, or a way for you to continuously adapt, innovate, and thrive in the ever-evolving financial markets around you.

The Mechanics of Tax Loss Harvesting

Alright, so now that we've talked about tax loss harvesting and how you might benefit from this approach in your investment portfolio, let's walk through how you actually go about the process and cover some common pitfalls to avoid along the way.

Spotting the Decline

Now, the initial step in this strategy is like debugging code in a piece of software that you're writing. But in our situation, the work involves meticulously scanning your portfolio, and not for bugs, but for investments that have depreciated in value.

Now, it's essential to remember here again that this process isn't about labeling certain investments as failures. Instead, this approach is about recognizing the inherent volatility of the market and using it to your advantage.

Here again, by identifying assets that have fallen in value, what you're doing is not admitting defeat, but rather, you're positioning yourself to leverage these declines for potential future tax benefits.

Indeed, just like a savvy software engineer might use a software glitch as a learning opportunity, tax loss harvesting allows you to use market downturns as a chance to optimize your tax situation.

So then, as you review your portfolio, remember that spotting the decline isn't about dwelling on what went wrong. It's about forward-thinking, about understanding that in the markets, challenges can be turned into opportunities.

Cashing in on the Downturn

Alright, so now that you've spotted positions in your portfolio that have declined in value, the next move isn't to lament or second-guess your choices.

Instead, it's to cash in on the downturn. Now, as you cash in on this process, there are a few definitions that you'll want to keep in mind.

First, you'll want to take a loss on a position that has fallen in value relative to its cost basis.

And what is cost basis?

Well, simply put, cost basis refers to how much an asset was worth when you legally received it. This could be the value when your restricted stock vested, when you exercised your stock options, or when you initially purchased a security.

Now, another term you’ll want to get familiar with is understanding the difference between short-term or long-term capital-losses in your portfolio.

And what are we talking about here?

Well, when you sell an asset that you've held for one year or less and you get less than what you paid for it, you incur a short-term capital loss.

And to calculate this value, what you do is simply subtract the sale price from the purchase price. If the result is negative, that's your short-term capital loss.

On the other hand, if you sell an asset that you've held for more than one year and the sale price is less than the purchase price, then you have a long-term capital loss.

Again, what you'll do is subtract the sale price from the purchase price to determine the amount of the loss. Here again, if the result is negative, then that's your long-term capital loss.

So then, by selling these assets, what you're doing is taking a proactive step to "realize" the loss.

Now, in the financial lexicon, to "realize" a loss means to officially acknowledge it for tax purposes.

And so, by selling and realizing the loss, what you're doing is essentially turning a paper loss into a tangible tax benefit. Indeed, it's a way to harness the market's inherent volatility, transforming potential setbacks into strategic opportunities.

Staying in the Game

Now, after you've made the decision to sell and realize your losses, it's crucial to remember that the cash now sitting in your account isn't meant to just sit there and gather dust until the markets turn around.

And why's that?

Well, that cash is your ticket to staying in the game.

How so?

Well, imagine that you're at a farmer's market, and there before you are two fruit baskets.

Now, one basket contains apples you bought recently at a higher price, but due to unforeseen circumstances (maybe a sudden influx of apples in the market), the value of your apples has fallen.

And what about the second basket? Well, the other basket is empty, but it represents the potential for new investment opportunities.

Now, let's say that a vendor at the local farmers market offers to buy your apples but at a lower price than you had initially paid. Here, you realize that if you sell now, you'll be realizing a loss.

But here's the twist, right next to this guy who wants to buy your apples is another vendor selling oranges at a rather attractive price, and you believe that the demand for oranges will rise soon.

So then, you decide to sell your apples and take your "loss." With that said, however, instead of walking away with just cash, you immediately buy the oranges and put them in your second basket with the money you received from the apple sale.

Are you still following along?

Ultimately, what you've done here is swapped apples for oranges, and redeploying your capital at a given price level.

And so, what happens next?

Well, a week later, you return to the market and find that the demand for oranges has indeed skyrocketed. So then, you can either hold onto your gains or sell your oranges at a profit that not only covers the loss from your apples but also provides for additional gains.

And, what's the key takeaway here?

Well, the takeaway is that you didn't "lock in" a loss when you sold the apples, but rather you strategically redeployed your capital.

And the truth is that you likely won't be able to make up your investment losses in a week.

However, by focusing on the price level at which you're redeploying rather than the loss you incurred, what you're doing is you're positioning yourself for potential future gains.

Navigating the "Wash Sale" Rule

Now amidst all this repositioning, there are some regulations that you'll want to keep in mind as you consider tax loss harvesting, and that's the IRS's "wash-sale" rule.

And what is the "wash-sale" rule?

Well, let's say that you've just offloaded a stock that hasn't been performing so well.

Now, if this were a software glitch, you'd quickly patch it and move on, right?

Well, when it comes to investing, if you rush to buy a stock that's "substantially identical" to the one you just sold, either 30 days before or 30 days after the sale, then you're potentially running up against the wash-sale.

And why is this rule even here in the first place?

Well, the IRS, in its bid to ensure fair playing field, set up this rule to prevent investors from gaming the system.

Essentially, it stops you from selling a stock to claim a tax loss only to immediately buy it back in anticipation of a rebound.

And why does this matter to you?

Well, understanding the nuances of this rule is crucial to effectively leveraging tax loss harvesting. You see, it's not just about recognizing a loss, it's about strategically navigating the aftermath of that decision.

In fact, if you run afoul of the wash-sale rule, then all those losses that you've so meticulously cashed in on could be considered worthless, leaving your harvest a fruitless one.

So then, what can you do to avoid running afoul of the wash-sale rule?

Well, the first thing you can do after selling a security at a loss is to wait at least 31 days before repurchasing that same security. This will ensure you're outside the 30-day window that the IRS monitors for wash sales.

And if you don't plan on purchasing that same investment or if you're eager to reinvest the proceeds from the sale immediately, then consider investing in a different security that isn't what's considered "substantially identical" to the one you sold.

For example, if you sold a specific company's stock, you might invest in another company within a different sector or in a broad-based index fund. This way, you're still putting your money to work, but without violating the wash-sale rule.

And the last thing to consider here is that you'll likely want to be cautious with automatic investment plans, like Employee Stock Purchase Plans (ESPP) and dividend reinvestment plans (DRIP) during this period.

That's because, if these plans purchase a "substantially identical" security within the 30-day window, it could inadvertently trigger the wash-sale rule.

That's why it might be wise to temporarily halt these automatic purchases or ensure they're directed towards different securities as you go about your tax-loss harvesting this season.

How to Profit from Tax Loss Harvesting

Now, as the leaves turn color and the crispness of fall reminds us of nature's ever-changing cycles, it's essential to remember that seasons aren't the only things that undergo perpetual change.

Indeed, the markets, much like your chosen profession, is in a constant state of flux.

But with change comes opportunity, and just as farmers meticulously tend to their crops, awaiting the right moment to harvest, you too have the power to harness the fluctuations in your investment portfolio.

Remember, tax loss harvesting isn't merely a financial maneuver, but rather, it's about recognizing that in every downturn, there's a hidden path for growth.

So then, as you stand at the beginnings of another seasonal change, remember that the essence of prudent money management isn't just about the gains you make but also about ensuring that with every decision you make when the market twists and turns, you're always one step closer to becoming the master of your financial independence journey.

Plan Your Way into Tax-Free Income

Let’s face it, no one likes paying Uncle Sam more than his fair share. But what if there was a way to take advantage of financial planning techniques to not only grow your savings, but also help protect your family and transfer wealth tax-free?

Sounds too good to be true, right?

Well, it’s more possible than you think. And as a highly driven individual, you likely have multiple streams of income to consider, like your salary, bonuses, stock options, and perhaps even revenue from a side hustle or business.

And with these multiple income streams and your high earnings, you’re likely setting yourself and your family up for an even higher tax liability in the years ahead unless you do something about it today.

That’s where tax planning comes in.

Now, tax planning is essential because it provides a structured approach to minimize the taxes you owe. And without adequate tax planning, you could end up paying more to Uncle Sam than necessary, which reduces the amount of wealth available to you and your family.

To be sure, the financial decisions you make today can have significant tax implications on your future wealth. That’s why understanding how to harness techniques to gain tax-free income can help you avoid paying thousands to the IRS, leave more to your family, and to ultimately make more informed financial decisions.

Understanding Legit Ways to Produce Tax-Free Income

Alright, so, when you hear tax planning you might think to yourself, “isn’t creative tax planning what got Al Capone put away in jail?” Well, the truth is that the US tax code, as complex as it is, has features written into it that gives certain advantages to those individuals with the time and patience to see them through, like sidestepping taxes on income.

To be sure, tax-free income is like a treasure that’s hidden in plain sight. It's income you or your loved ones receive that, as the name suggests, is free from obligation to the IRS. And what this means is that every dollar you receive stays a dollar, without a portion being reduced by what you would otherwise owe to Uncle Sam.

Now, it’s essential to keep in mind that we all earn income under a progressive tax system here in the United States. And what does this mean? Well, a progressive tax system means that the more money you make, the more you will owe Uncle Sam because your tax rate rises, or progresses, with your rising income.

And this rising tax rate doesn’t apply just to your wage income. In fact, in many cases it also applies to your interest and investment income applied towards the substantial savings you’re likely to receive now and into retirement as well. That’s why it’s essential, now more than ever, for you to understand some of the basic techniques of creating tax-free income so you can substantially boost your wealth while legally mitigating your future tax liability.

And, so, what are those techniques?

Well, when it comes to reducing your future tax obligations, there are generally three ways to produce tax-free income for yourself and your family. The first is putting money away in a tax-free investment account. The second option is to purchase securities or insurance products that offer tax-free income now and into the future. And, finally, you can mitigate a significant tax liability through the decisions you make about your home, when you gift money to loved ones and the decisions you make before you pass away.

Tax-Free Investment Accounts: Vehicles to Hold Taxable Investments

Alright, so let’s talk about some ways to use investment accounts to mitigate your tax liability. Now, before diving deep down this rabbit hole, let’s take a moment to make a distinction here between tax-free investment accounts and tax-free investment products.

And why is this important?

Well, it’s important because investment accounts and financial products are in many ways entirely different beasts. For example, tax-free investment accounts, like Roth IRAs, 529 Plans and HSAs act as shelters or holding containers, that allow a range of otherwise taxable investments within them to grow tax-free.

On the other hand, tax-free securities or insurance products like municipal bonds or life insurance, offer tax advantages inherent to the instrument itself, regardless of the account they're housed in. Indeed, another way to think about this is that tax-free accounts shelter holdings from future tax liabilities, while tax-free products inherently sidestep income tax altogether.

Ok, so then with this distinction in mind, let's explore tax-free investment accounts in greater detail.

Roth IRA – Tax-Free Lifestyle Savings

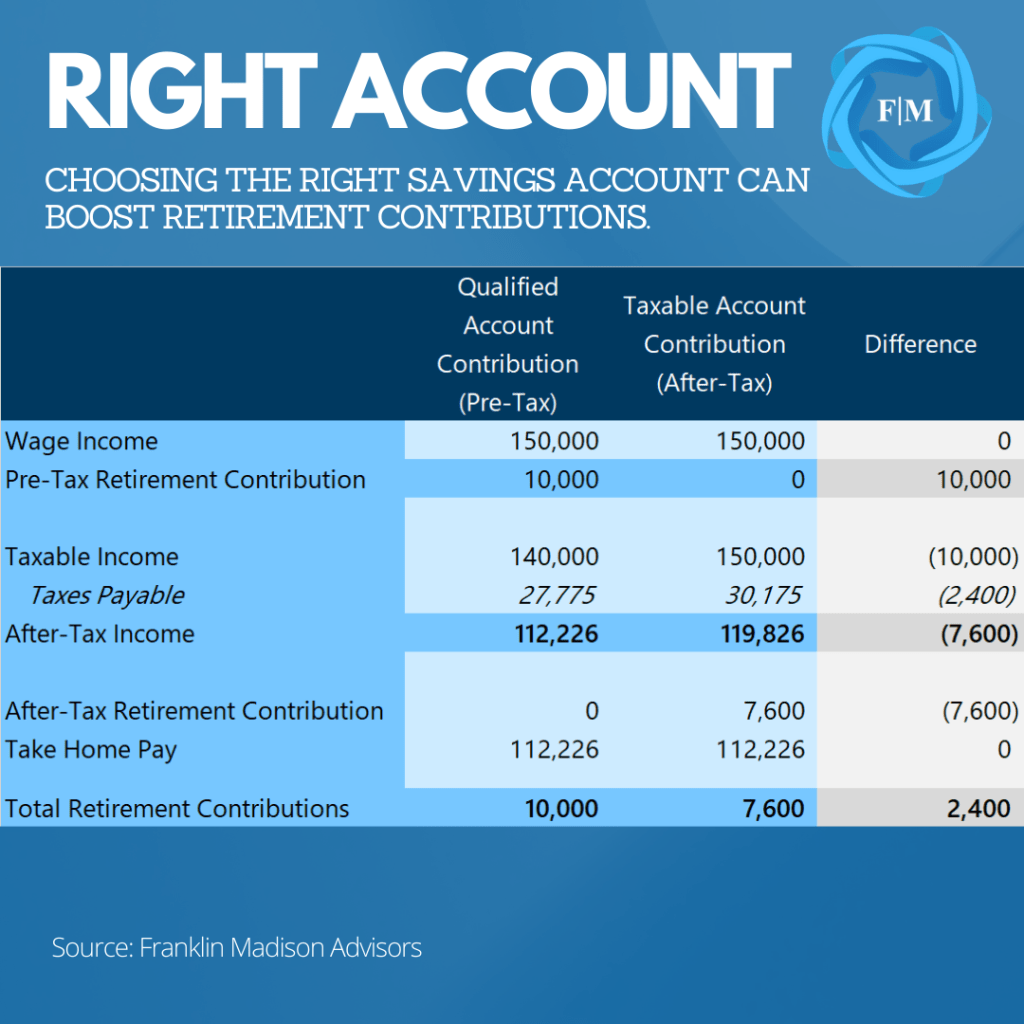

More specifically, let's start with the Roth IRA. Now, a Roth is an individual retirement account and acts like a container that offers specific tax breaks for the otherwise taxable investments you hold inside. And the way it works is that you put money into a Roth IRA using after-tax, take-home dollars.

And now while you don’t get an immediate tax break for your contributions to this account, the magic happens as your investments grow and when you start to withdraw your funds later in retirement. That’s because all the withdrawals, including earnings from the investments, are received tax-free if you meet certain conditions.

529 Plan – Tax-Free Education Savings

Another investment account that allows you to earn tax-free returns is a 529 Plan.

Now you may have heard of a 529 Plan before.

But if you haven’t, a 529 plan is an education savings program designed to encourage you to save for your or your children’s future education costs. Now, these plans operate in much the same way as a Roth IRA, meaning that you fund them with money you've already paid taxes on.

And while there's no federal tax deduction on the front-end for these contributions, the investments still grow tax-free so that when it’s time to use these funds for qualified education expenses, the withdrawals often come out without owing a cent to the IRS.

HSA Savings – Tax-Free Healthcare Savings

And finally, when discussing tax-free investment accounts, we can’t forget about Health Savings Accounts, or HSAs. Now, these accounts are a little different from Roth and 529 accounts in several ways.

How so?

Well, for starters, these accounts allow you to set aside money on a pre-tax basis before Uncle Sam gets a cut of your pay. What’s more, the contributions you make to this account grow tax-free, meaning you don’t pay taxes on dividends, interest or capital gains and for an added benefit, the money comes out tax-free when it’s time to spend your savings.

Therefore, an HSA creates tax-free income by providing a tri-fold tax benefit which is pre-tax contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

Tax-Free Considerations

So then, with all this discussion about tax-free income from these various investment accounts, you might be asking yourself, “these benefits all sound great, what the catch?” Well, while each of these accounts offer tremendous benefits, there are some things that you’ll want to consider.

For example, in most cases, you can’t money out of a Roth until you’re at least 59 ½ (or have a qualifying event) and there are limitations about when and how much you can put into the account. Now, there are ways around these limits, but that’s a discussion for another time. Even so, if you expect to be in a higher tax bracket by the time you reach retirement age, then looking into Roth contributions might be worth your time.

As for 529 and HSA accounts, there are a few things you’ll want to consider before you start putting money into these accounts. For starters, while you can begin taking money out of the accounts almost immediately after making contributions, you need to keep in mind that to qualify for tax-free status on those withdrawals, the money must be used for qualifying expenses.

Either way, the big takeaway here is that if you’re looking to put money to work now so you can fund your future lifestyle, education or healthcare expenses in a tax-free manner, then you should consider looking into a Roth IRA, 529 or HSA account.

Unlocking the Hidden Gems: Tax-Free Financial Products and Securities

Alright, so now that we’ve talked about certain tax-free investment account types out there, let’s talk about financial products and securities that offer similar tax advantages.

Here again it’s essential to make the distinction between accounts and products or securities. Remember, accounts are like baskets that hold all kinds of investments and shelter them from taxes.

And when it comes to securities and financial products, on the other hand, they can exist either inside or outside of a financial account and offer tax-free income.

Insurance Products: Tax-Free Income and Financial Security

For example, insurance products, like disability, long-term care and life insurance can be purchased directly from an insurer, or through your employers group coverage, without opening a specific type of financial account. That’s because these types of products are more like contracts between you and the insurer, rather than purchasing an investment security in the open market that needs to be held in an account.

And so, how does the tax-free aspect of these products factor in? Well, imagine that you decide to purchase a disability insurance policy. Essentially, what you're doing is entering into a contract with an insurance company to safeguard your income against the potential risk of being unable to work due to illness or injury.

Alright, now, fast forward to a situation where you unfortunately become disabled and start receiving benefits from this policy. In this situation, these benefits typically would come to you tax-free if you've paid the premiums with after-tax dollars.

And when it comes to long-term care insurance, this type of coverage operates in a similar way, except that it helps defray future costs associated with extended medical care with the benefits paid out from such a policy generally coming to you tax-free.

Now, life insurance is another insurance product that offers tax-free income, but this time not to you specifically, but to your loved ones instead. Here an insurance company offers what’s called a death benefit to your designated beneficiaries upon your passing. And, typically, this death benefit is like a gift received tax-free by your beneficiaries.

With all of this said, it’s essential to keep in mind that there are some situations where insurance payouts could be taxable. For example, in certain situations, if policy premiums are paid by your employer, then you could find a portion of your disability or long-term care proceeds taxable. And on the life insurance side, if your estate is the beneficiary of your policy, then you could find yourself paying estate tax on the state side, or federal tax if that life insurance policy pushes your estate above certain exemption limits.

Financial Securities: Exploring Tax-Free Investments

Ok, so now that we’ve talked about insurance products, let’s take a few minutes to talk about tax-free securities. Here again, whereas an insurance policy is a contract between you and the insurance company, purchasing a tax-free security, like a municipal bond, often times means holding the security in a financial account.

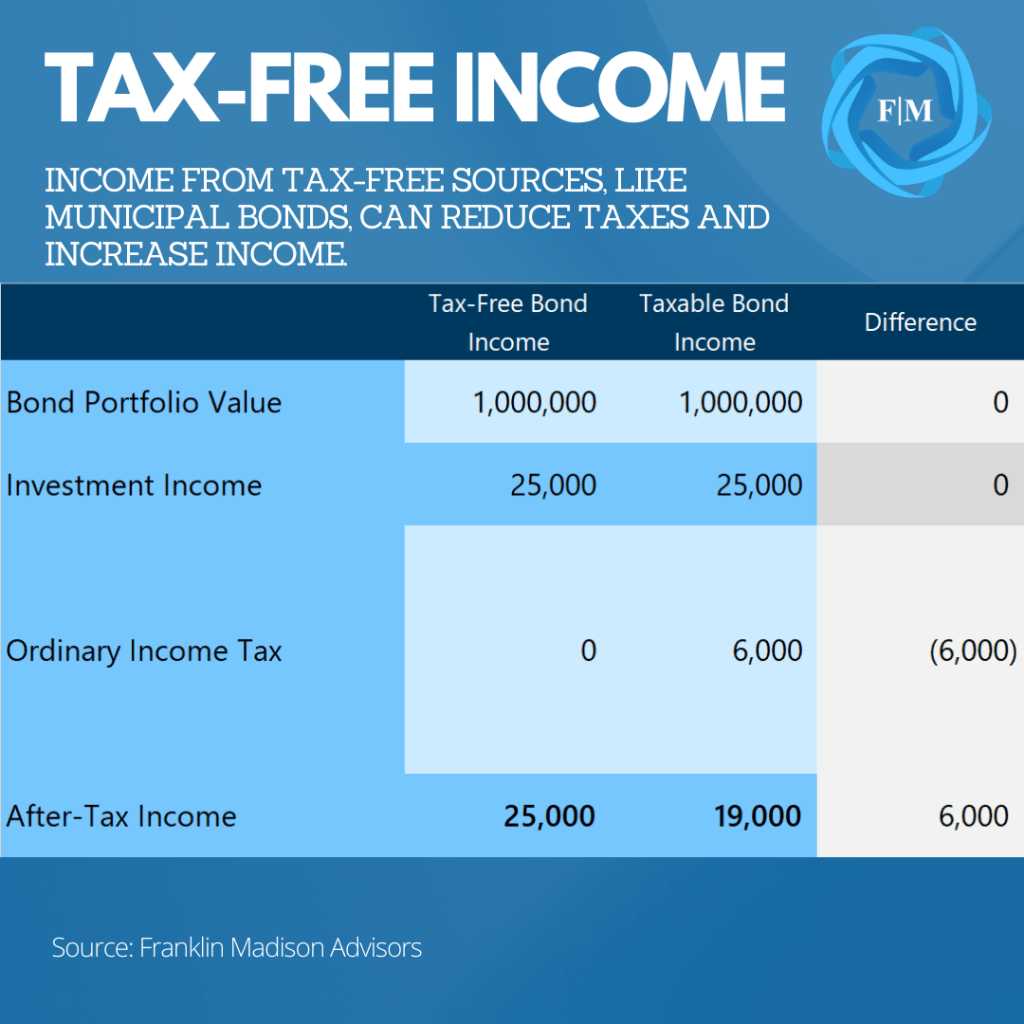

Now, municipal bonds, also known as "munis," are certain investments where you’re lending money to a municipality, such as a city, county, or state. And these entities often borrow money from investors to finance public projects, like building schools, highways, or sewage systems.

And here's where the tax-free part comes into play.

The borrowers pay you interest for lending them money, and, because of laws that are currently in place for these muni bonds, the interest income that you earn is typically exempt from federal income taxes. So, instead of giving a portion of your investment returns to the government, in many ways, you're allowed to keep all of your earnings.

What’s more, depending on the specifics of the bond and where you live, your interest income might also be free from state and local income taxes. And so, as a result, investing in municipal bonds from your own state could provide an even greater tax advantage and offer a completely tax-free source of income in some instances.

Now, when it comes to investing in tax-free securities like munis, there are some key caveats to keep in mind. For example, munis may offer lower interest rates than other bonds, so it’s crucial to evaluate whether the tax exemption makes them more attractive on an after-tax basis relative to taxable bonds.

And another thing to keep in mind is that while the income you receive from munis is often tax-free, you’re still likely to pay capital gains tax from selling a municipal bond before maturity. And finally, it’s crucial to keep in mind that you don’t get a double benefit from holding a muni in a tax-sheltered investment account like an IRA, 529 or HSA account, so that’s something to keep in mind as well.

Real Estate and Estate Planning: Strategies for Tax-Free Asset Transfers

Alright, so now that we’ve talked about how various financial accounts and products can help you navigate the tax man in the present, let’s talk about how navigating real estate and estate planning can also lead to tax-free asset transfers for yourself and your loved ones.

Tax-Free Income from Real Estate: Capitalizing on Home Sales

To start, let’s focus on how you can generate tax-free income from the sale of your home. Now, when you sell real estate, you’re likely to make a capital gain if the sales price is higher than what you originally paid for it. For example, if you bought your house for $500,000 and you sell it for $750,000, then your potential capital gain is $250,000.

Now, imagine that you've decided to sell your home in a high-cost part of the country so that you can move to a more affordable cost-of-living state. So, to go about this approach, you make your preparations and after the sale, you find that you've got a capital gain of $250,000. And because you met the necessary criteria, the entire amount is exempt from taxes, leaving you with a sizable sum of money you can now use however you want.

Now, it’s crucial to keep in mind that in order to make this all work you must meet certain criteria to be eligible for this exclusion. The first requirement is that you have owned the property for at least two years during the five-year period ending on the date of the sale. This is what’s known as the ownership test. The second condition is that the home must have been your primary residence for at least two years during that same five-year period, also known as the use test.

And finally, you’re not allowed to have excluded the gain from the sale of another home during the two-year period prior to the sale of your current home. That’s because this rule ensures that you’re not flipping homes and constantly taking advantage of this tax benefit over and over. Even so, if you meet all of the criteria to get the exclusion, you could tap your home as a source of tax-free income as a way to hasten your journey to financial independence.

Gifting Tax-Free Income: Sharing Wealth While Reducing Taxes

Alright, so now that we’ve talked about using real estate to generate tax-free income, let’s take a few moments to talk about gifting and estate planning to set your loved ones up for tax-free income in the future.

Now, some individuals may feel overwhelmed by the mere mention of the term estate planning. And if that’s you, that’s ok because we recently published a post on how to navigate the complexities of estate planning to make it work for you, so be sure to check out that resource.

But for now, let’s talk about a few ways that you can transfer assets to your loved ones without paying income tax. The first way is through gifting. Now, when you gift assets or money to someone while you’re still alive, it can potentially allow them to avoid giving a portion of that money to Uncle Sam.

How so?

Well, that’s because when you’re gifting an asset, what you’re doing is essentially passing on the responsibility for any income generated by those assets to the recipient. And, if the recipient falls within a lower tax bracket than you or if they have deductions or credits that offset the income, they may end up paying little or no tax on the gifted income.

Let’s look at an example to explain this a little better. Now, let's say that you have investments that generate significant income each year, and you’re in a high tax bracket. By gifting some of those investments to a family member or loved one who is in a lower tax bracket, any income generated from those investments may be taxed at a lower rate or possibly not taxed at all, which can result in tax savings for the receiver. Now, while we’ve talked about transfers of assets, this approach also applies to cash gifts.

Now, cash gifts are a little different than asset transfers, it's crucial to note here that there are specific rules and limitations surrounding gifting for tax purposes. For instance, there is an annual gift tax exclusion that allows you to give a certain amount to an individual each year without triggering gift tax consequences, which is currently $17,000 or $34,000 for a couple.

Tax-Free Inheritance: Step-Up in Basis and Its Wealth-Building Potential

Alright, while gifting allows you to provide tax-free income to your loved ones while you’re still alive, inheritance planning allows you to offer tax-free income after you pass away, and one way this is done is through a set-up in basis.

And how does this work?

Well, let's say you inherit a million-dollar investment property from your wealthy uncle Frank who recently passed away. Now, the trouble is that Uncle Frank has depreciated that property over the years, and it now has a low cost-basis. Normally, if you were to sell that asset, you would have to pay taxes on the capital gains.

However, with a step-up in basis, what happens is that the cost-basis of the inherited asset is adjusted to its fair market value at the time of the Uncle Frank’s death. In other words, the cost basis for tax purposes is "stepped up" to its current value, erasing any potential capital gains that may have accrued during Frank’s lifetime.

Now, when it comes to bequeathing, or transferring your assets, this step-up in basis can come as a substantial advantage for individuals who inherit assets with significant appreciation. That’s because it allows them to potentially sell the asset and realize a profit without owing capital gains taxes on the appreciation that occurred before the inheritance.

So then, from an estate planning perspective, thinking about which assets you want to gift now and which ones you want to leave as an inheritance is a critical component of creating tax-free income through the estate planning process.

Plan Your Way into Tax-Free Income

Indeed, by now, you’ve likely come to realize that tax planning is a cornerstone of a sound wealth management strategy. In many ways, it's the unsung hero that safeguards your hard-earned wealth, curtails tax liabilities, and unearths the chance for tax-free income. And by mastering these techniques and tactics, you can sail through the labyrinth of the US tax code and harness many strategies to create wealth that lasts a lifetime.

To be sure, tax-free income can come from tax-advantaged investment accounts like Roth IRAs, 529 Plans, and HSAs. That’s because they offer tax-free growth of otherwise taxable investments, and, eventually, tax-free withdrawals for specific purposes like funding your lifestyle, healthcare, or education expenses.

Beyond investment accounts, certain financial products and securities carry their weight in gold when it comes to tax-free income. That’s because insurance policies like disability, long-term care, and life insurance can serve up tax-free benefits under certain situations, which ensures that your income is secure and offers financial protection for you and your loved ones. And, at the same time, investments in tax-free securities like municipal bonds can provide you a tax edge, which can exempt the interest income from federal, state, and even local income taxes.

And, as we just discussed a moment ago, it’s essential to remember that real estate and estate planning can be a real game-changer in generating tax-free income. Indeed, by decoding various tax strategies and deploying them effectively, you can take one step closer to becoming the master of your own financial independence journey.

Is a Roth Conversion Right for You?

A Roth conversion is a critical consideration for many high-earning tech professionals and business owners, but is it right for you?

To be sure, as you delve into the work of planning for your financial independence journey, it's essential to understand the intricate dance between taxable and tax-free retirement accounts. And as we've pointed out in recent articles, with a strategic approach, you can make the most of your hard-earned money and ensure a comfortable retirement that aligns with your aspirations.

But, now, at what point should you consider a Roth conversion?

Well, picture this: You're diligently setting aside a portion of your earnings in a traditional 401k or a similar taxable retirement account. It's a tried-and-true method, offering immediate tax benefits, but there are long-term implications that you may not have considered.

For example, as your savings grow, so does the potential tax liability. From this perspective, then, the question arises, "how can you strike a balance between receiving tax advantages today and dealing with a future tax burden?"

That's where tax-free retirement savings vehicles like Roth IRAs come into play.

That’s because with a Roth IRA, you pay taxes on your contributions upfront, but the growth and withdrawals are entirely tax-free in retirement. It's like planting seeds today that will blossom into a tax-smart future.

But, again, the big question here is is this the right strategy for you? Should you maximize your 401k contributions to take advantage of immediate tax benefits? Or would it be wiser to prioritize Roth IRA contributions, offering tax-free growth potential. So then, how do you navigate these choices and find your optimal balance?

Now, make no mistake, retirement planning is rarely a one-size-fits-all endeavor because it's about crafting a strategy that suits your unique circumstances. That’s why as you embark on the journey of maximizing your retirement savings, understanding the interplay between taxable and tax-free accounts is paramount.

By strategically considering your order of operations, leveraging 401k contributions, evaluating your traditional and Roth IRA options, and even delving into the realm of Roth conversions, you can lay a solid foundation for a financially secure future.

Understand the Difference Between Tax-Deferred (Taxable) and Tax-free Retirement Accounts

Now, as you embark on your journey towards financial independence, it is crucial to grasp the distinction between taxable and tax-free retirement savings contributions. This understanding likely will empower you to make informed decisions about your savings options, optimize tax efficiency, and potentially enhance the longevity of your retirement savings.

Now, to achieve these objectives, one powerful tool at your disposal is a Roth conversion. Before delving into its benefits, let's explore the concept of taxable retirement savings options like the 401(k) and Traditional Individual Retirement Account (IRA), as well as tax-free options such as the Roth IRA. That’s because by understanding these choices and how they differ, you can strategically plan for your future in a more thoughtful manner.

Tax-Deferred (Taxable) Retirement Savings

So, what exactly is a taxable retirement account? In simple terms, it refers to savings accounts like 401(k)s and Traditional IRAs, where contributions grow without tax consequences in the present, but future withdrawals are subject to ordinary income taxes.

401(k) Plans

And how does this work with a 401(k)?

Well, as you’ll recall, these types of accounts are employer-sponsored retirement savings programs enabling you to allocate a portion of your pre-tax earnings towards your retirement fund.

Now, one notable benefit of these accounts is that the contributions you make are not taxed in the year that the income is earned. This reduces your taxable income, allowing your savings to grow tax-deferred and potentially reducing your overall income tax liability. Furthermore, any employer matching contributions effectively yield a 100% return on your own savings.

However, when it comes time to withdraw funds from your 401(k), these distributions are treated as ordinary income and subject to taxation. This makes 401(k)s tax-deferred accounts, as all distributions are typically taxed either upon withdrawal or when required minimum distributions (RMDs) become mandatory.

Traditional IRA

Now, let's shift our focus to the tax-deferred cousin of the 401(k): the Traditional IRA. Similar to a 401(k), a Traditional IRA allows you to defer taxes on contributions made with after-tax income.

Contributions to this type of account are typically tax-deductible, reducing your taxable income for the year. Like a 401(k), capital gains, dividends, and interest earned within a Traditional IRA remain untaxed until you start withdrawing funds.

Even so, upon withdrawal or when RMDs are required, the distributions are taxed as regular income, with the tax bracket in retirement determined by your total annual income.

Tax-Free Retirement Savings

Alright, now that we’ve explored tax-deferred accounts, let's now turn our attention to tax-free retirement savings options. These include accounts like the Roth IRA, where contributions are made with after-tax dollars, and withdrawals are completely tax-free.

Roth IRA

And how does a Roth IRA work?

Well, as we mentioned earlier, a Roth IRA is funded with after-tax income, meaning you contribute to the account using your take-home pay. And while this may seem less advantageous compared to pre-tax contributions, the real benefit lies in tax-free withdrawals during retirement.

That’s because, as long as the Roth IRA has been open for at least five years, and you are at least 59 ½ years old, any distributions you make from this account will be entirely tax-free.

And this makes the Roth IRA a compelling choice if you anticipate being in a higher tax bracket during retirement, expect future tax rate increases, or simply want to avoid mandatory distributions altogether.

Now, after exploring the differences between taxable and tax-free accounts, the question remains, “how do you decide which type of account to fund?” Well, the answer depends on several factors.

Current vs. Future Tax Bracket

If you anticipate being in a lower tax bracket during retirement compared to your current situation, sticking with a 401(k) or Traditional IRA may be advantageous. That’s because by deferring taxes now and paying a lower tax rate upon withdrawal, you can potentially minimize your overall tax burden.

However, if you expect to be in a higher tax bracket in retirement, a Roth IRA becomes a more appealing option. That’s because paying taxes upfront allows you to enjoy tax-free withdrawals later, effectively sidestepping potentially higher taxes in the future.

Now, it's crucial to note that you don't have to choose one account type exclusively. In fact, a mix of both taxable and tax-free retirement savings accounts can provide optimal flexibility and tax diversification. This approach allows you to manage taxable income in retirement and hedge against future changes in tax rates.

Indeed, understanding the differences between taxable and tax-free retirement savings options is a crucial step when considering a Roth conversion. Both types of accounts offer unique advantages and disadvantages, and the right choice depends on your individual circumstances, including your current income, expected future income, and retirement goals.

Consider Your Order of Operations

Alright, now that we've discussed the differences between taxable and tax-free accounts, let's review your order of operations when it comes to savings contributions. Just like solving a complex math equation, there's an ideal way to put your income to work before fully converting your savings to a Roth IRA.

Maximizing Your 401k Contributions

So, then, where should you put your money to work first?

Well, when it comes to saving for retirement, your employer-sponsored retirement plan, such as a 401k, can be a potent resource. That’s because these plans offer unique advantages that significantly enhance your long-term savings strategy.

And as we’ve mentioned before, one of the biggest benefits is the potential for an employer match. Now, this happens when your employer contributes additional money to your 401k based on how much you contribute in the first place.

And it's essentially free money, providing an immediate 100% return on your investment that you can't get through most other retirement savings strategies. And the fact is that many people leave money on the table every year by not taking full advantage of the employer match.

And so, why is an employer match so important?

Let's consider an example to illustrate why matching is so important. Suppose your employer offers a 100% match on your contributions up to 6% of your salary. If you contribute 6%, your employer adds an additional 6% (i.e., 100% of your 6% contribution). That’s why failing to contribute that 6% in the first place means missing out on that extra 6% from your employer, effectively leaving money on the table.

So then from this perspective, the first step in maximizing your retirement savings should always be to contribute at least enough to your employer-sponsored retirement plan to fully capture your employer's matching contribution.

Now, it’s also worth noting that the Internal Revenue Service (IRS) sets limits on how much you can contribute to these types of retirement accounts each year. As of 2023, the maximum contribution limit for a 401k, 403(b), or TSP is $22,500. And if you're aged 50 or older, you can contribute an additional $7,500 per year. And this catch-up contribution is designed to help individuals who are closer to retirement age bolster their savings.

So then, if your financial situation permits, consider maximizing your contributions to these accounts up to their limits. Doing so not only allows you to take full advantage of the tax benefits these plans offer but can also significantly enhance your long-term savings due to the power of compounding on a pre-tax basis.

Taking Advantage of Traditional IRA Contributions

Alright, so now that you’ve taken full advantage of your employer's 401k match or reached your contribution limit, another smart strategy to consider is funding a Traditional IRA. A Traditional Individual Retirement Account (IRA) offers numerous advantages that can help you grow your retirement savings more effectively and efficiently.

And the primary advantage of a Traditional IRA is the tax deductibility of contributions. That’s because any money you contribute to a Traditional IRA can be deducted from your income for a given tax year, effectively reducing your taxable income. This means you'll owe less income tax, freeing up more of your money for saving or investing.

And as of 2023, the contribution limit for a Traditional IRA is $6,500 per year. And this contribution limit applies collectively to all of your IRAs, including both Traditional and Roth accounts.

While the tax benefits of a Traditional IRA are notable, it's crucial to be aware of certain limitations that apply if you or your spouse have a retirement plan through work. The IRS imposes income limits that can reduce or even eliminate your ability to deduct your Traditional IRA contributions if you or your spouse are covered by a workplace retirement plan.

For example, in 2023, if you're covered by a retirement plan at work, the deduction for contributions to a Traditional IRA is phased out for singles and heads of household with modified adjusted gross incomes (MAGI) between $73,000 and $83,000.

For married couples filing jointly, where the spouse making the IRA contribution is covered by a workplace retirement plan, the income phase-out range is $116,000 to $136,000. If you're not covered by a workplace retirement plan but your spouse is, the deduction is phased out if your combined income is between $204,000 and $214,000.

Now, it’s important to note that these income ranges are subject to change and can vary from year to year, so it's essential to verify the current ranges with the IRS before making a contribution.

So then, if you're eligible, it's wise to contribute the maximum amount to your Traditional IRA each year. Doing so provides you with an immediate tax deduction and allows your savings to grow tax-deferred over time. This means you won't owe taxes on your investment earnings until you start taking distributions in retirement, enabling your money to compound more effectively.

Prioritizing Roth IRA Contributions

Now, once you've maximized your contributions to your 401k and Traditional IRA, the next logical step in your retirement savings journey is to consider a Roth IRA. While Roth IRA contributions don't provide an immediate tax deduction like Traditional IRA contributions, they offer several unique benefits that make them a valuable part of a balanced retirement savings strategy.

Now, before we talk about these benefits, let’s take a step back and recap what makes a Roth different from a Traditional IRA or employer-sponsored plan.

Unlike 401k and Traditional IRA accounts, contributions to a Roth IRA are made with after-tax dollars. This means you pay income tax on the money before contributing it to the account. While this might seem like a disadvantage compared to tax-deductible contributions, it still offers a significant payoff down the line in the form of tax-free withdrawals.

To be sure, with a Roth IRA, both your contributions and the earnings on those contributions can be withdrawn tax-free during retirement, provided the withdrawals meet certain qualifications. This means the money you invest in a Roth IRA today could grow substantially over time, and all of that growth will be yours to keep when you retire.

Now, as of 2023, the Roth IRA contribution limit is the same as that of a Traditional IRA which is $6,500 per year and $7,500 for those aged 50 or older. Even so, with a Roth IRA it’s essential to note that certain income restrictions can limit your ability to put money into these accounts.

For those filing single and head of household, the ability to contribute to a Roth IRA begins to phase out at a modified adjusted gross income (MAGI) of $129,000 and is eliminated entirely at $144,000. For married couples filing jointly, the phase-out range is between $204,000 and $214,000.

Put simply, if you make too much money, more often than not you likely can’t make a direct contribution to a Roth IRA.

Even so, the Roth IRA is a powerful retirement savings tool because it allows you to pay taxes now in exchange for tax-free income later. This can be particularly beneficial if you anticipate being in a higher tax bracket in retirement than you are currently or if you believe that tax rates are likely to increase in the future.

And by contributing to a Roth IRA, you're essentially locking in your current tax rate. This could result in substantial tax savings in the long term, as you won't owe taxes on the growth of your investments when you start taking distributions.

Additionally, Roth IRAs aren't subject to required minimum distributions during the account owner's lifetime, unlike Traditional IRAs and 401ks. This flexibility allows you to manage your retirement savings and withdrawal strategy on your terms.

Calculate the Benefit of a Roth Conversion Using the NPV Approach

Alright, so what if you find yourself in a position where you’ve maximized your contributions to your employer-sponsored plan, and taken full advantage of your Traditional IRA but make too much money to contribute to a Roth IRA? Well, you could consider doing a Roth conversion.

And what is a Roth conversion?

Well, a Roth conversion is the process of transferring assets from a traditional IRA or 401k into a Roth IRA. Now, as we’ve mentioned before, this is a strategic financial decision that can offer significant tax benefits, enabling you to maximize your retirement savings. However, like any financial decision, it entails complexities and requires careful consideration.

Indeed, understanding the benefits of a Roth conversion is just one aspect of the puzzle. To determine if it is the right move, you need to compare the cost of the conversion which is essentially the taxes you would have to pay now versus the potential benefits which is mainly the tax-free withdrawals in the future.

And how do you do this comparison? Well, this is where the net present value (NPV) approach comes into play.

The NPV approach is a financial calculation used to determine the present value of an investment while taking into account the time value of money. In essence, it calculates the worth of future cash flows in today's dollars.

And when applied to a Roth conversion, the NPV calculation helps compare the current tax cost of the conversion with the present value of future tax-free withdrawals. And so, how do we determine if the NPV is good or bad?

Well, if the NPV is positive, it suggests that the present value of the future benefits of a Roth IRA outweighs the immediate tax cost, indicating a beneficial conversion. Conversely, a negative NPV suggests that the conversion may not be advantageous.

How to Calculate NPV for a Roth Conversion

To calculate the NPV for a Roth conversion, several variables need to be estimated:

- Current Tax Cost: This represents the tax amount you would pay if you converted your traditional Individual Retirement Account (IRA) to a Roth IRA today. For example, if you have a traditional IRA worth $100,000, and your current tax rate is 25%, the tax cost of converting to a Roth IRA would be $25,000.

- Future Tax Savings: This estimates the value of the tax you would save on distributions from a Roth IRA in the future. Unlike traditional IRAs, Roth IRA withdrawals are tax-free during retirement. To calculate this, you need to estimate your future tax rate and the expected annual withdrawal amount. For instance, if you anticipate withdrawing $50,000 per year from your Roth IRA in retirement and expect your tax rate to be 25% at that time, your annual tax savings would amount to $12,500.

- Discount Rate: This is an estimate of the rate of return you could expect to earn on your investments if you didn't convert to a Roth IRA. For example, if you expect your investments to earn an average of 6% per year, this would be your discount rate.

- Investment Horizon: This refers to the number of years until you plan to start withdrawing money from your retirement account. If you intend to retire in 20 years, your investment horizon would be 20 years.

Once you have estimates for these variables, you can use the following formula to calculate NPV:

NPV = (Future Tax Savings / (1 + Discount Rate)^Investment Horizon) - Current Tax Cost

The result of this calculation will provide you with the net present value of your Roth conversion in today's dollars. A positive NPV suggests that the conversion is likely a good financial decision, while a negative NPV suggests that you may be better off not converting to a Roth IRA.

Considerations When Using the NPV Approach

Make no mistake, the Net Present Value (NPV) approach is a powerful tool in the decision-making process when considering a Roth IRA conversion. With that said, this approach is not without its complexities, that’s because this approach relies on several estimates and assumptions that can significantly influence the results.

The Impact of Changes in Tax Law

Now, one fundamental assumption in an NPV calculation is that current tax laws will remain constant. However, tax laws are subject to political forces and can change over time.

For example, future changes could affect the tax benefits associated with Roth IRAs, such as tax-free distributions, or modify the tax rates applicable to Traditional IRA distributions. If income tax rates were to decrease in the future, the tax savings from a Roth conversion would be less than what you might have estimated using current rates.

Predicting Your Future Tax Rate: A Not-So-Certain Exercise

Another factor to consider when conducting conversion analyses is that the trajectory of your future specific tax bracket is largely unknown. Indeed, while determining your current tax rate is relatively straightforward in the present, estimating your future tax rate can be much more challenging. That’s because numerous factors can influence this rate, many of which are difficult to predict accurately.

And these factors can include changes in your income, whether from employment, investments, or retirement distributions, which can significantly impact your future tax bracket. And even your personal circumstances, like a change in marital status, can also alter your future tax liabilities.

The Role of the Assumed Rate of Return

And, finally, another key assumption in the NPV calculation to take into consideration is the discount rate, which represents the assumed rate of return on your investments. This rate plays a pivotal role in determining the present value of future tax savings or costs.

Now, while history is typically a useful indicator of market direction, predicting the rate of return can be challenging due to the variability of market conditions and investment performance. And this uncertainty is a key consideration when performing an NPV analysis because the rate of return significantly influences the results of the NPV calculation.

That’s because a higher assumed rate of return reduces the present value of future tax payments, making a Roth conversion appear less attractive. Conversely, a lower rate increases the present value of these future tax savings, potentially favoring the conversion.

Either way, using the NPV approach to evaluate a Roth IRA conversion is a powerful method for understanding the potential long-term financial impact of this decision. However, it's important to remember that this calculation relies on estimates and assumptions that are subject to change. That’s why it’s essential to consider multiple scenarios and work with a professional who can provide personalized advice based on your specific circumstances.

Is a Roth Conversion Right for You?

Taken together, in the ever-evolving landscape of preparing for financial independence, the thing that remains constant is the need for a strategic and informed decision-making process. And, as high-earning tech professionals and business owners, you possess the power to shape your financial destiny and secure a measure of financial independence that reflects your purpose and values.

Remember, the path to financial freedom is as unique as your fingerprint. That's why it's essential to understand the intricacies of balancing taxable and tax-free accounts, strategically leveraging your 401k contributions, and making informed choices regarding traditional and Roth IRA contributions.

And by calculating the net present value of a Roth conversion, you can gain a clearer understanding of the potential benefits and make decisions that align with your long-term goals and help ensure that you're making a decision that's right for you.

Indeed, by understanding the various tradeoffs, considering the order of operations, and harnessing the power of Roth conversions, you'll be well-equipped to make confident and informed decisions about your wealth. Even more crucial, doing so will take you one step closer to becoming the master of your own financial independence journey.

Manage Your Tax Anxiety and File Your Returns with Confidence

Is tax anxiety causing you to wait until the last minute to file your tax returns? If so, then you’re in good company.

According to one survey, over thirty percent of respondents said they waited until the tax filing deadline to prepare their returns last year.

Now, if you’re one of these individuals, there’s likely many reasons why you’ve chosen not to file your taxes yet.

Maybe you anticipate owing money to the government this year and you’re using every last moment to wait to pay Uncle Sam his owed money. Or, you might find the process to file your returns complicated and it just stresses you out. Or maybe, you haven’t found the time to sit down and complete your returns and you just need to put it on your to do list.

Whatever your case may be, you should know that the April 18 deadline to file your tax returns is just a few weeks away. And while it may seem like you have enough time to get the work done, in some instances, the longer you delay, the more it could cost you.

Indeed, for many individuals, filing your taxes is just a process of sitting in front of your computer, entering your tax documents into planning software and either choosing how you want to receive your tax refund or cutting a check to the IRS.

So, what can you do if you find yourself paralyzed by indecision and hesitant to prepare your returns?

Well, the truth is that you can overcome the anxiety that comes with filing your returns by following a simple process to get the job done. Indeed, knowing what you should do before, during and after you file could give you the motivation to finally complete your returns sooner rather than later.

And, at a basic level, using a stepwise approach to navigating your returns process may help you reduce your anxiety levels and avoid some costly mistakes commonly associated with procrastination and avoidance this tax season.

What to do Before You File Your Returns

Now, depending on your situation, one of the first things that you'll likely want to do before filing your returns is to evaluate whether you should file your returns on your own or take the time to go about hiring a professional to help complete your returns.

If you're still trying to determine which route you should take, be sure to take a moment to review our recent article where we discuss the criteria for evaluating when to go it alone and when hire a tax pro.

Either way, before you begin calculating your tax for the year, you’ll likely want to make sure that you have gathered all the proper documents to complete your tax return. Doing so will ensure that you’re accurately accounting for all income received, and not missing out on potential tax penalties or opportunities down the road.

And, so, how do you know whether you've gathered all the necessary information to complete your return?

Well, start by creating a checklist of all the documents and forms needed to complete your tax return, such as W-2s, 1099s, and receipts for charitable donations, medical costs, and other deductible expenses.

And if you need help figuring out where to start with your checklist, take a moment to review last year's tax returns. Indeed, by reviewing last year's return, you can identify the documents and forms that were required to complete your return and can help ensure that you have not overlooked any necessary paperwork.

Another option for ensuring that you have all the necessary documents to file your return is to log in to online portals for your current and former employers, financial institutions, and other organizations that may be required to provide tax documents, such as W2s, 1099s, mortgage or interest statements.

And finally, you can complete a tax organizer to ensure that you have gathered all of the documents necessary to prepare your return.

And, so, what is a tax organizer?

Well, a tax organizer is a tool that is used by tax professionals to help individuals gather and organize the information needed to prepare an accurate tax return. It typically includes a list of questions and prompts to help you identify and provide all the necessary information to complete your return, as well as worksheets to organize and summarize the data.

And when in doubt, completing your organizer can facilitate better communication between you and your tax professional, ensuring that all necessary information is obtained and questions are answered promptly.

Either way, before you get started with filing your returns, be sure to organize all tax-related documents in a secure and easily accessible location, such as a dedicated digital vault or online storage service.

And if you’re not sure how to go about this process, be sure to check out our FI|Mastery January action items for tips on ideal storage locations for critical documents and how tax organizers work.

Which institutions should I contact if I have problems?

Now, it's vital to note that reporting institutions can and do make errors in the tax documents they send to you. These errors can be as simple as omitting a taxpayer ID number to something as costly as reporting the wrong cost basis on a 401k rollover that could potentially cost you thousands of dollars in taxes due.

So, what can you do if you discover an error in one of your tax documents?

Well, first things first, contact the issuer of the tax document, such as your employer or the financial institution that sent you the tax form, and inform them of the error as soon as you discover it. Then, explain the nature of the error and provide any supporting documentation if necessary.

Next, request that the issuer provide a corrected tax document as soon as possible. In most cases, they’re required to provide a corrected form by January 31st, but, given that we’re past that deadline now, it will likely take a week or two to receive the updated document so plan accordingly.

That’s why getting started on your taxes sooner rather than later can help you avoid the anxiety related to working against a tight deadline. And when you do receive the corrected tax document, take a moment to review it to ensure that the error has been corrected and that all other information is accurate.

Now, keep in mind that if you discover an error on a tax document after you've already filed your return, you have the option to file an amended tax return to correct the error. With that said, the amended return must be filed within three years from the original filing deadline or two years from the date the tax was paid.

Overall, however, as you’re working to get your tax documents corrected, keep records of all communications with the document issuer regarding the error, as well as copies of the original and corrected tax documents and any other relevant paperwork.

These records may be necessary if the error is not corrected or if the IRS questions your returns down the road. And when in doubt or if the error is complex and you're unsure how to proceed, you may need to seek the assistance of a tax professional or accountant.

Finally, before you begin the process of preparing your returns, you’ll likely want to evaluate whether you should make a prior year contribution to an IRA before the tax filing deadline. This approach makes the most sense if you want to take advantage of a traditional IRA tax deduction for the prior year if you have the cash to do so.

For instance, if you didn't reach the annual contribution limit for the previous tax year, or came into windfall income in 2023, such as a bonus or inheritance, you have the option of using your current income to make a prior year IRA contribution.

Now, it's critical to note that the contribution limits and tax benefits associated with IRAs can vary depending on several factors, such as your income level, age, and marital status. Therefore, carefully consider your specific situation to see if it makes sense to make a prior year IRA contribution.

Things to Consider as You File Your Returns

Alright, now that you've organized your documents, gathered all of the necessary data, and tied up loose ends on contributions, it's time to begin filing your returns. As you do, however, there are a few critical tax choices you'll likely need to consider as you begin filing your return, including your filing status, understanding the difference between tax credits and deductions, knowing when to itemize, and being mindful of considerations for reporting cryptocurrency assets to the IRS.

Determine Your Filing Status

Now, determining your filing status is often as simple as evaluating whether you're single or married. If you're single and have no children, then your filing status can be rather straightforward. But what if you're unmarried, paid more than half the cost of keeping up your home for the year, and you have a qualifying person living with you, such as a dependent?

Well, in this case, claiming the "head of household" filing status could make sense. Why would you choose this route? Well, compared to the standard deduction of $13,850 for a single filer in 2023, an individual filing as head of household could qualify for the higher standard deduction of $20,800 so long as you meet the qualifying requirements.

And for you married folks out there, more often than not, it makes sense to simply file as "married filing jointly". But how do you know when it might make sense to choose the "married filing separately" route?

Well, here are a few situations where it might make sense to take the filing separately route, and so let’s look at a few examples.

High Itemized Deductions

First, if one spouse has a significant amount of itemized deductions, such as medical expenses or charitable donations, these can only be claimed if they exceed a certain threshold. Depending on your income level and unique situation, filing separately may result in a larger tax benefit in this instance.

Separate Finances

Next, if each spouse has separate finances and wants to be responsible only for their own tax liability, filing separately may work for you. This approach is common in situations where a couple is recently married and one spouse has significant tax liabilities or unpaid taxes from previous years.

Income-based Deductions or Credits

Now, being able to claim certain tax deductions or credits, such as the Earned Income Tax Credit or the Child and Dependent Care Credit may also be another reason to file separately. That’s because these credits have income limits, and so in some situations, it can be more advantageous for married couples to split their financial situation to claim the credit rather than filing jointly and missing out on the benefit altogether.

Student Loan Payments

And finally, if one spouse has significant student loan payments and is enrolled in an income-driven repayment plan or a Public Service Loan Forgiveness Program (PSLF), filing separately can result in lower monthly payments and improve qualification criteria to receive loan forgiveness.

Now, with all that said, in many cases, if you’re married, filing jointly can result in a lower tax liability overall, as it allows you to take advantage of certain tax deductions and credits that are not available to those filing separately.

Either way, it's critical for you married couples out there to carefully consider your options and consult with a tax professional to determine the most advantageous filing status for your specific situation.

What's the difference between a tax credit and tax deduction?

Another critical concept to understand as you're filing your returns is the difference between a tax credit and a tax deduction.

So, what is a tax credit?

Well, a tax credit is a dollar-for-dollar reduction of the amount of tax owed. For example, if you owe $5,000 in taxes and are eligible for a $1,000 tax credit, your tax bill could be reduced to $4,000.

What’s more, tax credits can either be refundable or nonrefundable. For instance, refundable tax credits can result in a refund if the credit exceeds the amount of tax owed, while nonrefundable tax credits can only reduce the amount of tax owed to zero.

Now, a tax deduction, on the other hand, reduces the amount of income that is subject to taxation. Deductions are subtracted from your gross income to arrive at your taxable income, which is then used to calculate the amount of tax owed.

For example, if you earned $150,000 and were eligible for a $20,800 deduction, your taxable income would be reduced to $129,200, which would result in a lower tax liability.

Either way, when planning for future taxes, it's essential to consider both tax credits and tax deductions to determine the most effective tax strategy. This may involve maximizing deductions to reduce taxable income, while also taking advantage of available tax credits to further reduce your tax liability.

Indeed, understanding the difference between these two tax concepts can help you make informed decisions about your tax planning strategies and ultimately reduce your overall tax burden this return season.

Itemize or Standard Deduction?

Another point to consider as you’re preparing your returns is whether to itemize or take the standard deduction for the year. And in the current environment, more often than not, it makes more sense to take the standard deduction than to itemize.

Indeed, fewer and fewer individuals have itemized their deductions since the Tax Cuts and Jobs Act (TCJA) was passed in 2018. That's because this legislation provided a significant boost to the standard deduction, and in 2019, this figure nearly doubled for single filers from $6,500 to $12,000 and from $13,000 to $24,000 for married filers.

And this change in policy was so effective that the number of itemized deductions filed in the year after this change in legislation was introduction fell by nearly half as individuals chose the higher standardized deduction.

Now, while the standard deduction is generous, there are still several reasons why you may want to consider itemizing deductions on your tax return this year.

For example, there are certain deductions that are only available if you choose to itemize, such as charitable contributions, medical expenses, and state and local taxes. If you don't itemize, you won't be able to take advantage of these deductions, even if they would result in a lower tax liability.

Itemizing your deductions can also provide greater flexibility in your tax planning. For example, if you have a large number of deductible expenses in one year and few deductible expenses in another year, itemizing allows you to maximize your deductions in the year when you have the most expenses.

And while the TCJA limited the amount of state and local tax (SALT) deductions that taxpayers can take, if you live in a high-tax state or have significant property taxes, your SALT deductions may still exceed the standard deduction, making it beneficial to itemize.