Three Things You Can Do About Inflation

Inflation is on a lot of people's minds right now.

And for a good reason.

While we tend to hear about inflation in terms of percent changes in government reports, chances are, you've likely experienced its natural effects in everything from higher prices at the grocery store, gas pump, restaurants, and utility bills.

Prices change constantly, so why should you care about inflation now?

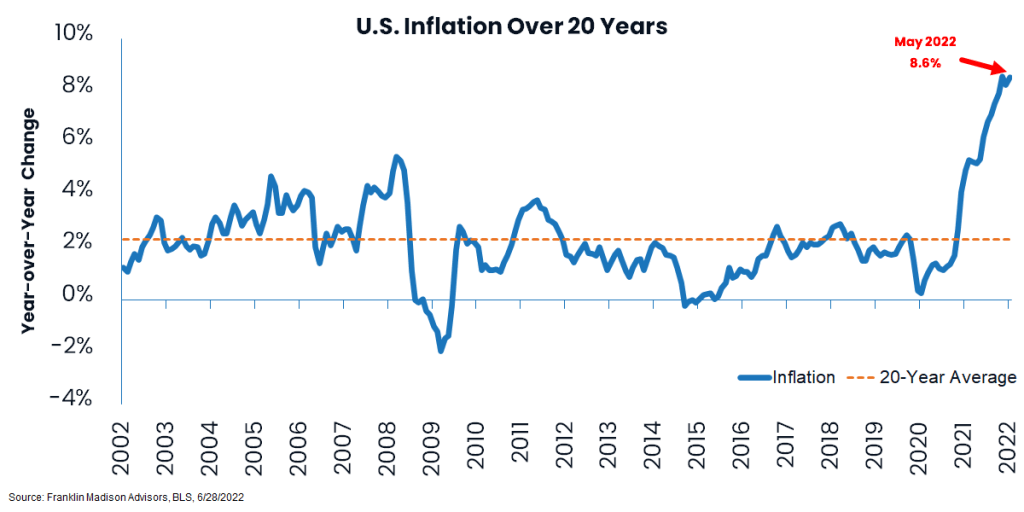

Well, other than the fact that inflation is at a 40-year high, it's crucial to understand that when inflation stays high for a long time, it can potentially erode your ability to secure your future financial independence goals if you do nothing to prepare for it today.

What is inflation?

So, what is inflation? Simply put, inflation measures the rate at which prices change for goods and services you spend money on.

For example, if a pound of apples costs $1.05 today, when it was $1.00 twelve months ago, we can say that inflation has caused the price of apples to change by 5% over the past year.

Inflation is the rate of change, or speed, at which prices rise over time.

Whether you're aware of it or not, inflation is always around. The price you pay for the things you need or want is constantly in flux. It can rise and fall daily, weekly, or monthly.

It's like a car traveling down a highway.

Sometimes, inflation moves along steadily for months or years, like it's on cruise control traveling at the highway speed limit. It can also suddenly speed up over days and weeks when something causes the gas pedal to hammer down.

What truly makes it a matter of concern now is how quickly inflation has sped up and how long it has remained in high gear.

How does inflation affect purchasing power?

Inflation matters because the longer it remains in high gear, the fewer goods or services your money will buy tomorrow.

Economists call this declining purchasing power.

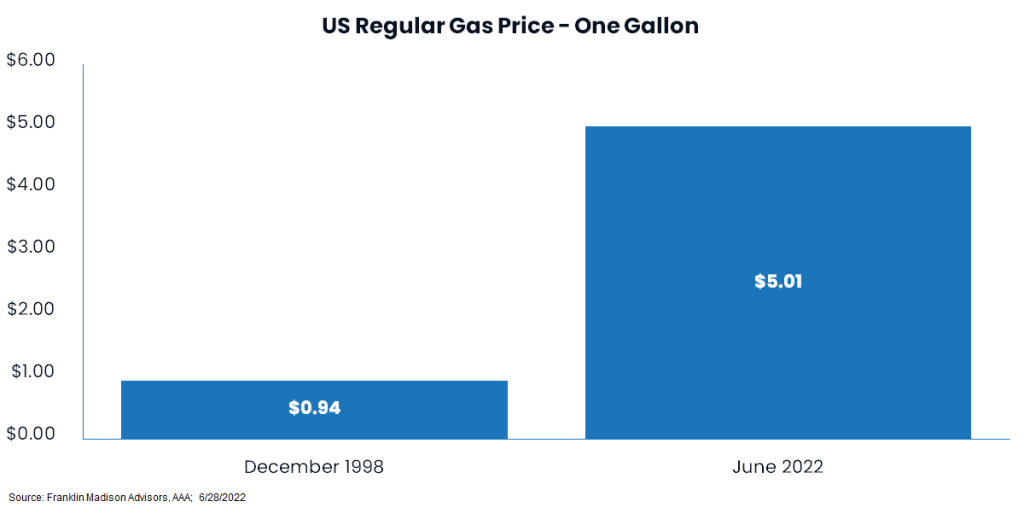

For example, a dollar in the late 1990's purchased one gallon of gasoline. Today, with gas prices around $5.00 per gallon, a dollar today has a fifth of the purchasing power it did over two decades ago!

A dollar is still a dollar, but it doesn't go as far as it used to. At least for gasoline.

And when inflation takes off, you need more dollars to buy the same product compared to a month or year ago.

That's why if you're setting money aside for a big-ticket purchase or plan to live off your savings sometime in the future, you need to be able to anticipate rising prices.

Indeed, understanding purchasing power is essential whether you're socking money away in a 401k to retire later in life or dependent on your savings now to cover retirement living expenses.

When inflation goes up, and purchasing power goes down, you'll likely need to either save more money today, spend less in the future or do a bit of both. Otherwise, you could find your financial independence plans falling short.

What causes inflation to speed up?

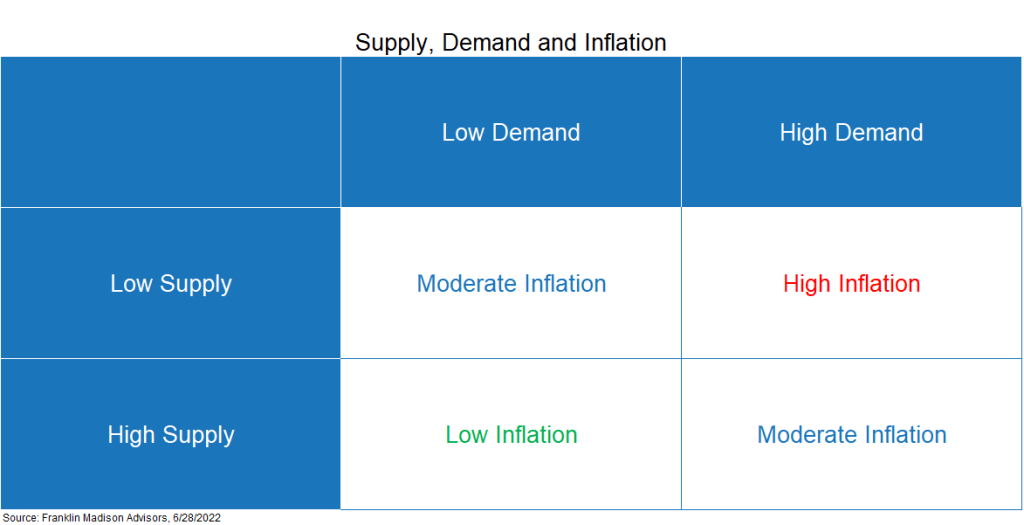

Just like a car needs gas to power its engine and a driver to raise or lower their foot on the gas pedal, no one factor causes inflation to accelerate or decelerate.

Inflation is an interplay between supply (amount of gas in the tank) and demand (driver's willingness to push down on the accelerator).

A full gas tank (supply) won't make a car go fast with a cautious driver (demand) at the wheel.

Likewise, an aggressive driver can only go so far with fumes in the tank.

Let's look at gasoline prices as an example. While some may argue that high prices at the pump are related to oil company profits, there's more at play than pure greed.

From a supply perspective, the fact is that economic sanctions on Russia has led to oil shortages in the West.

At the same time, key oil refiners have shut down because of fires, needed repairs, or maintenance.

From a demand perspective, summer is the travel season. And as more cars get out on the road and air travel picks up, so does oil usage.

When supply is limited, and demand is high, prices tend to go up.

Buying a house is another example. Demand for new homes increased nationally during the pandemic as individuals moved to the suburbs to work from home.

It typically takes about a year or so to build a new home, making supply an issue when thousands of individuals are looking to buy a home simultaneously.

Again, when demand is high, and supply is limited, prices tend to go up.

What role does government money play in inflation?

Now, some people will blame the government for today's high prices.

They'll argue that if the Federal Reserve (Fed) hadn't increased the money supply by printing trillions of dollars, or if it had raised rates sooner and the Treasury didn't send out stimulus checks, we wouldn't be dealing with high rates of inflation today.

To a certain extent, this is a valid argument.

Easy central bank policies arguably made it easier for banks to lend money, thus increasing demand from individuals willing and able to make large expenditures, like a new home or car.

Stimulus checks also made it easier for people to purchase goods or services they otherwise may not have needed during the pandemic, thus increasing demand at a time when economic lockdowns constrained global supply chains.

While this argument makes for a simple explanation, the truth is that the story is much more nuanced than can be explained by any one government policy.

That's because the rise in food and energy prices today arguably has less to do with interest rates or government stimulus than it has to do with supply. While government policies have added to the demand side of the equation, the supply of raw materials and finished goods sourced from around the world is still in short supply.

It's not just the government's fault. To be sure, today, we're dealing with a perfect storm of artificially too much money chasing artificially too few goods.

What can be done about inflation?

So, if inflation is seemingly speeding out of control, can't someone stop it? The truth is, there's only so much the government can do to halt inflation.

The Federal Reserve has raised its policy rate in a bid to slow down demand by making money more expensive to borrow and thus slowing the economy. But with war raging in Ukraine, ongoing Covid lockdowns in China, and other challenges, supply-side challenges likely will keep inflation elevated until those issues are resolved.

Fortunately, some businesses have raised wages to help workers offset higher living costs. However, most firms are not entirely altruistic, making up for higher wages by raising the price of their goods and services. This behavior could introduce an entirely new complexity to the inflation discussion. But, that's a topic for another day.

Three things you can do about inflation

For now, inflation matters because it can affect your ability to maintain your standard of living now and into the future.

There's not a lot we can do to affect the declining purchasing power of a dollar. However, you can mitigate its effects by:

1) holding just enough cash to help you sleep well at night,

2) putting excess cash to work in assets that move with inflation and

3) ensuring that you're saving and growing enough money today to make up for a declining purchasing power in the future.

Hold just enough cash to sleep well at night

Setting cash aside during this time of economic uncertainty is essential to weathering a financial setback.

However, keeping too much cash on hand could leave you with a reduced purchasing power of your savings.

For example, let's assume that you have $10,000 in a savings account that pays you interest of 1.00% per year. We'll also assume that inflation averages 5.00% over the year.

How much purchasing power do you have at the end of the year? If you said $10,100 you'd be wrong.

While you earned $100 in interest, inflation reduced your purchasing power by $500, with inflation running at 5% during the year.

That's why if you want to preserve the inflation-adjusted value of your savings, you'll need to put it to work in assets that can protect your purchasing power.

Put your money to work in productive assets

Where else can you put your money if a savings account alone won't protect against inflation? Consider your investments.

A diversified investment portfolio has historically been shown to be a hedge against inflation. Why?

Well, a key reason being is that the price paid for a stock today is often in anticipation of the underlying company's future earnings potential. And with firms increasingly passing rising costs on to consumers, corporate earnings have the potential to rise with inflation over the long term.

At the same time, bondholders demand a return on their investment that will compensate them for their time, investment risk, and inflation.

While stocks and bonds offer a degree of inflation protection, consider holding a mix of these assets in a diversified portfolio to reduce investment risk.

Ensure that you're saving enough to account for inflation

Finally, to our earlier point, inflation could leave your retirement savings goals falling short if not adequately accounted for. Indeed, if you want to secure your future financial independence when inflation is on the rise, you'll likely need to evaluate whether you need to save more money, reduce your spending or do a little of both.

Let's look at an example of how higher than expected inflation could alter the size of your retirement savings nest egg:

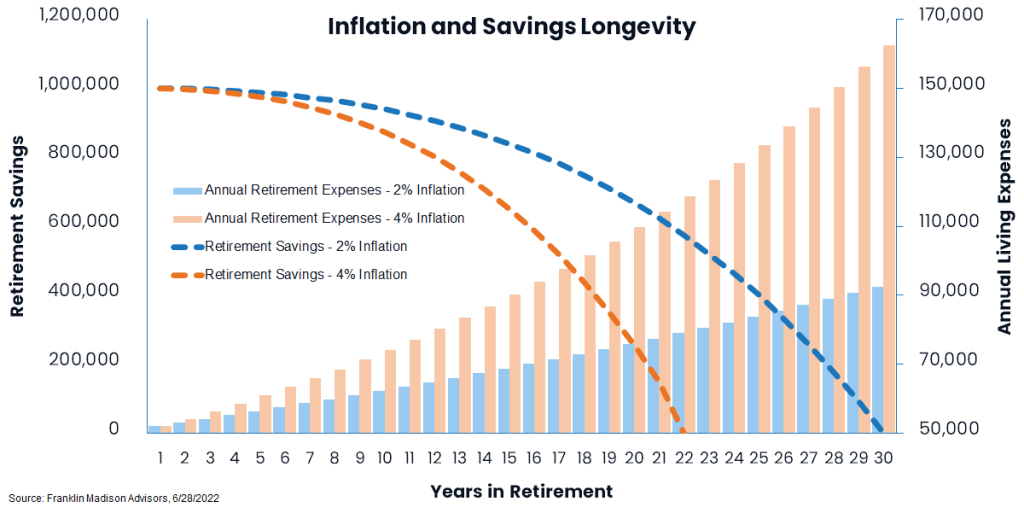

We'll start with a base set of assumptions that at retirement, you'll need roughly $50,000 per year to cover living expenses for the next 30 years. We further assume 2.0% average inflation and 5.5% average portfolio returns throughout retirement. At this rate, you'll likely need to have saved one million dollars to cover your costs.

What happens if inflation comes in faster than 2.0%? Well, if inflation turned out to average 4.0% instead of 2.0% over your 30 years in retirement, your million-dollar nest egg could go to zero in just over twenty years instead of thirty years.

To overcome this shortfall, you'd likely need to save an extra $280,000 before retiring, reduce your retirement spending by $10,000 annually or delay retiring by six years.

That's why periodically revisiting your financial plan and clearly understanding the effects of inflation on your expected future income need is essential to maintaining your standard of living and not running out of money in retirement.

Make no mistake, inflation can be a serious threat to your financial independence plans as it reduces the purchasing power of your savings.

Understanding the effects of rising inflation, putting your money to work in productive investments, and formulating a game plan to address declining purchasing power is essential to securing financial independence.

If you do nothing to mitigate this inflation threat, you could find your savings falling short of your desired standard of living later in life.

Should You Invest When the Market is High?

Some investors today are worried. They're asking, "is now the right time to get into the markets?" Their primary concern is putting money to work at the top of the market, only to see their precious savings decline in a selloff. And they have good reason to be concerned. Volatility in certain parts of the financial markets remains elevated while asset prices continue to drive higher and, by many measures, are disconnected from fundamentals. So, what should an investor do to avoid losses associated with investing at the wrong time in such an environment?

Maybe you're sitting on cash and asking whether you should put your money to work now or wait until conditions settle down a bit? Truth be told, not investing at market highs is a fallacy because there is generally no wrong time to invest in the markets. More specifically, the right time to be putting money to work in the markets is when your investment strategy balances your income needs with capital appreciation and other savings goals.

In fact, staying out of the markets at an inopportune time might cost you in terms of growth over the long-term for the benefit of avoiding a loss in the short-term. To be sure, the key to navigating financial markets during periods of uncertainty is to avoid market timing altogether. When it comes down to it, investing isn't so much about divining market direction. It is about adhering to a strategy that enables you to achieve and maintain financial independence regardless of where you are in the market cycle.

Remaining Disciplined when Markets Are Uncertain

Our last article discussed methods for staying sane and avoiding unnecessary risk-taking when it appears the market is going crazy. There's little doubt that those principles remain relevant today. Nevertheless, some individuals are sitting on the sidelines, worried about losing money in today's frothy markets and unsure what to do next.

Before we discuss why and how you could invest your savings, let's address a critical anxiety-provoking issue facing many disciplined investors: signs of a market top. By various measures, price action in certain parts of the markets makes little sense today. Some traditional investing theory suggests that an asset's value depends on its future earnings, cash flows, or potential store of value discounted at today's price. Therefore, the value of an asset can be explained, at least in part, by a rational understanding of the underlying factors, or fundamentals, underpinning the directional move in an asset's price.

As we pointed out last month, however, markets are also be fueled by periods of irrational social dynamics rather than logical fundamental analysis. One of the key concepts we previously highlighted to this point was the Greater Fool Theory. And this theory suggests that asset prices will rise solely because some individuals believe that others will be around to bid prices higher in the future. And it's this very phenomenon that has underpinned notable historical asset price bubbles that seem to pop up once or twice a decade. Presently, the gyrations in "meme" and high-flying tech stocks and bitcoin underscore the disconnect between rational decision making and price action.

So how long will the current craziness last? The truth is that no one can divine where the market is heading in the near-term. Still, certain developments would suggest that higher price momentum for questionable assets is coming under pressure. This view has become evident in heightened volatility among penny stocks and cryptocurrencies and rising yields, and other dislocations in the bond markets themselves. Under current conditions, there's little doubt that having money in the market, notably, if you're dependent on that money to cover lifestyle needs in the near-term, is disconcerting at the moment.

Timing the market Isn't an Efficient Investment Strategy

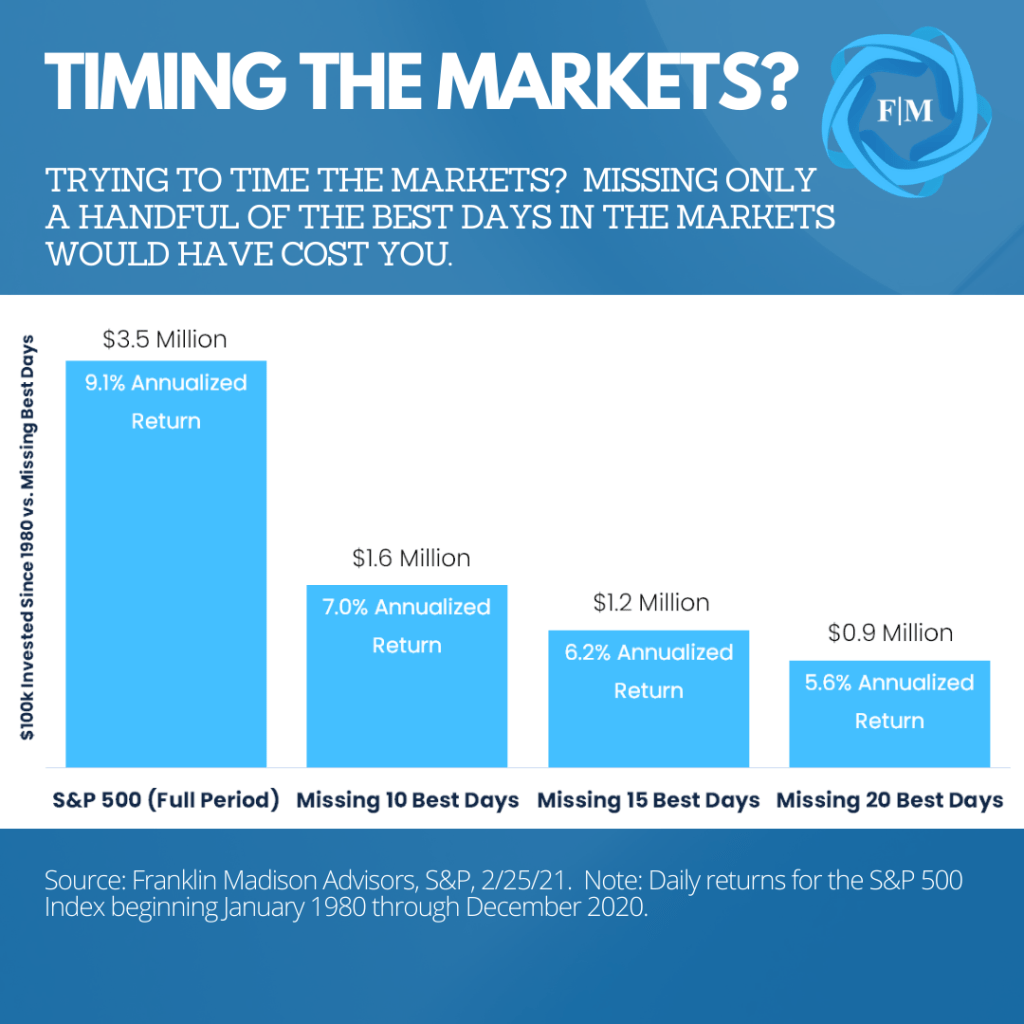

Certainly, there's a sense of comfort that comes from sitting on cash in anticipation of what seems to be an imminent end to an otherwise irrational period in the financial markets. Trying to time the markets, or waiting on the sidelines until the craziness ends, may not, however, be in your best interest. Why? Well, how certain can you be about the timing of a highly anticipated market pullback, and what's the cost of getting the timing wrong? Well, history has shown that missing some of the best days in the markets can cost you significantly, depending on your savings horizon.

For example, over the past 50 years, investors missing out on the ten best days in the markets might have had a portfolio value half the size of those who remained fully invested. On the flip side, you could argue that staying out of the markets during a time of uncertainty could help you avoid losses during a sharp market pullback. While this sentiment may be true to a certain extent, again, you'll need to be able to answer a few key questions to make this approach work: First, when will the selloff begin? Second, how long will the next selloff last? And finally, when should you get back into the market? Will you wait one day, a week, or month for an all-clear sign to reinvest your savings?

The challenge here is that the longer you wait to answer these questions, the more it may cost you as you miss out on periods of critical market rallies that are essential to fueling compounded growth of your savings over the long-term. To understand this concept with a little more clarity, let's consider hypothetical investment performance following sharp market pullbacks.

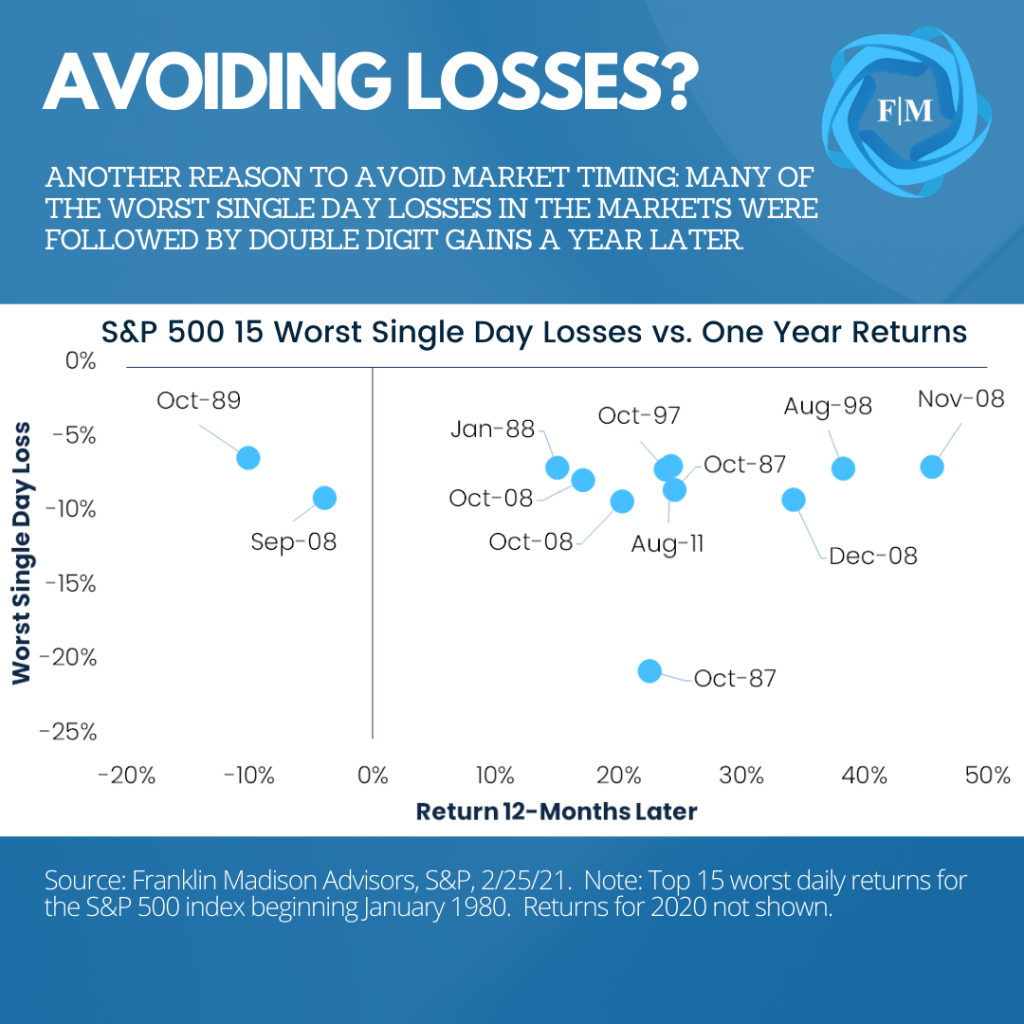

Now, if we gather data for the ten worst single-day selloffs in the S&P 500 index over the past 50 years and evaluate performance a year later, what does history tell us? Well, the data shows us that during these historic down days in the S&P 500, the index fell an average of 8.8% in a single day. So how did it perform a year later? The same data set showed that the sharp selloff was followed by an average gain of 24% in the following twelve months. The takeaway here is that avoiding the markets altogether could cost you in terms of lost appreciation and compounded growth if you happen to make decisions based solely on market timing.

A Prudent Approach to Investing in Uncertainty: Manage Risk, Stay Disciplined

So, is now the right time to get into the markets? Should you wait until the markets settle before putting your money to work? Well, rather than concerning yourself with the next move, higher or lower in the market, now may be the time to evaluate how you're positioning your investments in the current environment. More importantly, it would help if you considered whether your portfolio is appropriately balanced to meet your short-term living needs and long-term capital appreciation goals.

While the answer to this question will vary from one individual to the next, let's consider how you might be able to approach the market from the perspective of an investor with varying capital distribution and appreciation needs.

The Already Retired Investor

Suppose you're already retired and dependent on your investment savings for income. In this case, your primary concern might be to find an optimal balance between income needs to weather a market selloff in the short-term and continued investment growth to avoid the harmful effects of inflation over the long-run. So how much money should you set aside in your portfolio? While the amount of cash you should have on hand will vary depending on your unique circumstances, one rule of thumb if you're already retired is to have enough cash on hand to cover two to three years' worth of lifestyle needs.

The benefit of this approach is twofold. First, having a few years of cash on hand will enable you to preserve your wealth for the long-term without worrying about the periodic ups and downs in the markets. To be sure, rather than selling all of your investments during a period of uncertainty, remaining fully invested in the markets while holding a higher allocation to cash might enable you to address lifestyle needs without being forced to sell investments at an inopportune time.

Compared to a cash-only portfolio, the second benefit is that allowing a portion of your savings to maintain market exposure might provide continued investment appreciation while avoiding a shortfall should you live longer than expected. Price inflation or a rising cost of living can be detrimental to your retirement plans, especially if you outlive your savings. Even so, history has shown that the longer you invest your savings and allow the power of compounding to work, the less likely you are to experience a cost-of-living shortfall should you live longer than you had planned.

Soon to be Retired Investor

Now, what if you're not yet retired but plan to leave your job in the next few years? Well, one challenge faced by some soon-to-be retirees is the need to reposition their portfolios from a high concentration in stocks or riskier assets to a more diversified, preservation-oriented allocation. During seasons of heightened market uncertainty, you might be tempted to go to an all-cash portfolio when a market pullback seems imminent, and your retirement is just a few years away.

Nevertheless, when it comes to preparing your savings to address long-term retirement needs, going to cash may not be the most optimal approach. In fact, one of the most effective strategies you can consider is to evaluate your income needs during your first few years of retirement, set aside that amount of money, and stick to a disciplined rebalancing plan.

Like individuals who are already retired, having enough cash to cover 2-3 years of retirement expenses might help you avoid selling investments at an inopportune time. More importantly, having the optimal amount of cash on hand might ease your anxiety during periods of market uncertainty, especially as you transition into your post-employment years.

Next, ensure that your investment portfolio is diversified across several uncorrelated asset classes as a means to reduce the time it takes to come back from a market selloff. To be sure, history has shown that, even when you're invested at a market top, a diversified portfolio might recover from losses months and even years sooner than a highly concentrated portfolio as illustrated in the post-Global Financial Crisis period.

Not Retiring Anytime Soon Investor

Finally, what should you do if you don't plan to retire anytime soon but are still concerned about investing near a market top? Well, if your plan for retirement is more than five years away, then one of the most important things you can do today is to ensure that you remain invested for the long-term and stay committed to a disciplined dollar-cost-averaging strategy.

It's vital to recall that riding through periods of euphoria and despair, fear and greed are the cost of admittance to participating in financial markets. If you have a long-term investment horizon, your primary goal should be to allow the power of compounding to make your money work for you, rather than spending your time trying to divine the next move higher or lower in the markets.

To be sure, our earlier example of missing the ten best days in the markets is notably relevant to individuals with a long-term savings horizon. Therefore, rather than trying to figure out whether you should be in or out of the market, take the time to evaluate whether your strategy matches your risk tolerance and investment objective and commit to making the power of compounding work for you.

Should You Invest When the Market is High?

So, with some indices having hit all-time highs, is now the right time to get into the markets? Well, the idea of not investing when indices are near all-time highs suggests a prime time to put money to work. And the fallacy here is that there is no right or wrong time to be invested in the financial markets.

In fact, staying out of the markets at an inopportune time might cost you in terms of growth over the long-term for the benefit of avoiding a loss in the short-term. To be sure, the key to navigating financial markets during periods of uncertainty is to avoid market timing altogether.

When it comes down to it, investing isn't so much about divining market direction. It is about adhering to a strategy that enables you to achieve and maintain financial independence regardless of where you are in the market cycle.

Worried About Ukraine and Your Money? Consider these Six Things.

Words seem to fail when attempting to describe the horrors of war currently faced by the people of Ukraine. Since last Thursday, millions of innocent Ukrainians have been displaced and hundreds killed following Russia's invasion of an Eastern European democracy.

Indeed, world leaders have since responded by providing Ukraine with financial and military support while imposing heavy economic and financial sanctions on Russian President Vladimir Putin and his cronies. Today, much of the world looks on with bated breath, hoping for a quick and triumphant victory for the Ukrainian people.

How and when this war ends remains largely unknown. It could end tomorrow or persist for weeks to come. Indeed, we're hopeful that delegates from Ukraine and Russia can find a way to end this war diplomatically. Even so, as we pointed out in last week's note, a seismic shift in the geopolitical status quo could lead to economic spillover effects that likely will impact US households for months or even years to come.

So, this leaves many asking, what do these developments mean for my finances, and is there anything I should do right now to protect my wealth? Well, here are six points you may want to consider when it comes to guarding your money during periods of uncertainty:

#1 Expedite big-ticket purchases

Inflation is likely to stay elevated for months to come as a result of this conflict. If your emergency fund is already topped up (see point #3 below) and you have adequate means to buy a new car, house, or anticipate any other big-ticket cash expenditures later this year, you may want to consider purchasing those items now before they become more expensive later.

While a military confrontation currently is limited to Russian and Ukrainian, globally imposed sanctions could, directly and indirectly, affect imported goods and compound supply chain issues that have recently contributed to inflation's rise to multi-decade highs. That's why front-loading spending within your means today may help you avoid potentially higher prices tomorrow.

#2 Revisit your lifestyle spending and savings plan

While inflation's rise likely will mean higher costs for big-ticket spending, you can also expect to pay more on everyday living expenditures not only over the coming months but also potentially for years. Not accounting for these rising costs could leave your retirement nest egg falling short. Indeed, uncertainty surrounding the implications of sanctions and global supply chain efficiency could broadly affect the cost of keeping the lights on at home, filling up your gas tank, eating out, or even buying everyday staples.

In isolation, these higher expenditures may seem manageable in the near term. However, not accounting how these expenses could remain at elevated levels over the long-term could potentially derail your overall financial independence journey when not considered within the context of your broader lifestyle spending goals. That's why now's a good time to reset future cost of living expectations in the face of higher inflation, recalculate your traditional/early retirement total savings need, and make necessary adjustments today to your lifestyle spending or savings contributions to ensure that your everyday financial decisions keep you aligned with your path to financial independence.

#3 Top up your emergency savings fund

The US labor market remains favorable for workers and job seekers alike by many measures. Indeed, while jobs in specific sectors of the economy are plentiful and wages continue to rise, the fact is that US economic growth is slowing and faces headwinds from ambiguous central bank policy, systemic financial instability, and global military conflict.

While an economic recession is not baked into economists' GDP forecast of 3.5% this year, a policy misstep by the Federal Reserve, a shock to the global financial system or a global military escalation could put downward pressure on US economic activity. That's why if you don't have 6-9 months-worth of cash to cover living expenditures, now may be the time to reconsider big-ticket spending decisions along with how much you spend on non-essential goods and services, so that you can increase your monthly savings or reduce needed distributions from your retirement savings.

#4 Prepare for a smaller employer bonus or limited equity award payout

Even if you feel like your job is secure and your emergency savings are topped off, relying on an employer bonus or equity award payout to cover living expenses may lead to financial disappointment later this year. Generally speaking, firm bonuses are tied to corporate earnings. As evidenced during the Covid-induced recession, when economic conditions soften and earnings decline, employers tend to cut back on incentive compensation in a given year.

Present expectations of weaker economic conditions, combined with many of the risks we’ve already mentioned, likely could weigh on risk asset prices this year. That's why if you're the recipient of equity awards and dependent on ISOs or RSUs to cover a portion of your lifestyle spending needs, you may be in for a disappointment should stock prices decline in the months ahead. Put simply, you may want to reevaluate how much of your household outlays are funded by once-per-year windfalls and consider adjusting your lifestyle spending today.

#5 Avoid timing the markets & increase your home country bias

When it comes to your investments, how markets respond to Russia's war with Ukraine likely will depend on day-to-day developments. As such, we expect market volatility to ebb and flow with the news cycle. Indeed, there are times when you may be tempted to make changes in your investment portfolio when it appears that the news is about to get bad.

Nevertheless, during these times of uncertainty, astute investors stick to their disciplined investment process. Rather than trying to identify an inflection point in stock prices or trying to time the next move in the markets, you'll likely be best served by ensuring that your portfolio is aligned with your long-term goals over the coming years, rather than responding to near-term uncertainties by trying to pick the right securities to buy or sell over the coming days and weeks.

#6 Rebalance international risk exposure

Finally, the Russia-Ukraine war coupled with the potential for further confrontations with China has some investors concerned about holding securities tied to these countries in their investment portfolios. While we continue to advocate for investing internationally, we also believe that now may be a good time to reevaluate your investment exposure to countries where the rule of law or the potential for escalating military conflict may lead to downside investment risks.

We're evaluating the current situation more opportunistically, particularly as it relates to international vs. domestic exposure. Indeed, while Russian securities make up a small portion of emerging market stock and bond benchmarks, China's dominance in traditional EM indices likely may argue for a tactical rebalance from traditional asset class benchmark guidelines. We'll provide further guidance and clarification to our active clients in the coming weeks.

For now, only time will tell whether the current situation will escalate to a broader conflict or settle more amicably. Our hope is that substantial financial and economic sanctions coupled with a solid political resolve from Western leaders will convince Putin to end his military incursion in Ukraine. Until then, we anticipate market volatility to ebb and flow with the news cycle. For now, avoiding the noise, evaluating the six items we covered today and committing to your long-term financial plan will not only give you peace of mind during this time of uncertainly, it may also enable you to continue your journey toward financial independence mastery.