Is it Possible: Two Recessions in Two Years?

Two recessions in two years. Is it possible? Well, calls for a U.S. recession have been on the rise recently following the Fed's decision to raise rates at its March FOMC meeting. To be sure, given several factors already in play, it's possible that we could see an economic slowdown later this year or even early next year.

While some market watchers have suggested that policymakers could simply stop raising rates if a downturn emerges, the reality is that the Fed's credibility and its playbook are considerably changed from where it was two years ago.

Make no mistake, at this moment, the U.S. economy is doing well. And recent data suggest that growth has been on a solid footing since the COVID-related lockdowns eased last year. Nevertheless, various developments related to monetary policy uncertainty and rising geopolitical tensions suggest that the road to U.S. economic growth likely will face some headwinds in the year ahead.

Indeed, the bond market, typically a canary in the coal mine when it comes to the health of the economy, is now indicative of heightened financial and economic stress as escalating war tensions and rising interest rates have led to yield curve flattening. And too much flattening could be an early indicator of an impending recession.

This outlook has led some investors to ask whether there is anything they should be doing now to avoid downside risks related to a market or economic downturn. The truth is that many investors have been caught flat-footed by trying to time the markets during similar periods of uncertainty.

And that's why during times like these, it’s essential for driven individuals on their path to financial independence mastery to focus on an approach that has worked time and time again: consistently executing on a well-defined financial plan.

Still Solid Economic Growth?

So, how strong is the U.S. economy right now? Well, if you were to look at some recent reports, the data suggest that U.S. economic growth has been robust over the past year. Indeed, government data showed that the U.S. economy grew seven percent on an inflation-adjusted basis in the fourth quarter of 2021. This gain is much faster than the average growth rate between the Great Recession and the pandemic, likely reflecting the positive effects of easy monetary and fiscal policies.

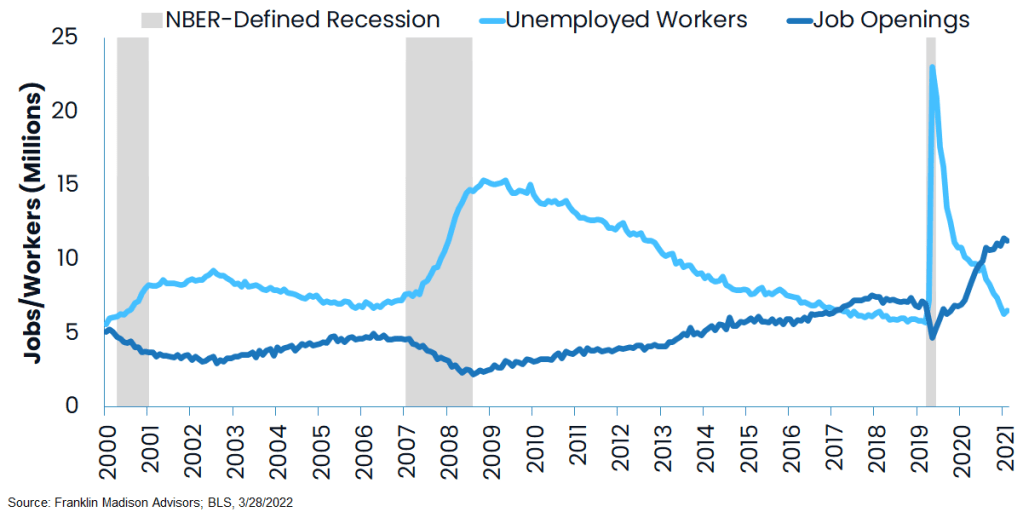

What's more is that recent data shows that the U.S. labor market, another important indicator of economic health, continues to improve significantly. For example, recent initial jobless claims have declined to their lowest level since the pandemic began, and according to some reports, there are more job openings today than there are unemployed workers. So, what does this all mean?

Well, by looking at a solid growth print in the fourth quarter and continued robust labor market data, one could conclude that, at present, growth momentum remains positive. Now, while it's true that labor market shortages and falling unemployment rates are signs of robust economic conditions, what truly drives growth in this environment is business and consumer spending which are poised to decline later this year.

Slowing Growth and Rising Inflation

How can spending decline when labor market conditions have improved? Simply put, households today are likely to face twin headwinds of higher borrowing costs as the Fed raises rates, commodity shortages and ongoing supply chain issues related to Russia's war with Ukraine drive inflation higher. It's important to recall that back in 2020, policymakers unleashed unprecedented amounts of cash into the financial system as the U.S. economy stared into the abyss of Covid-related lockdowns. Back then, trillions of dollars worth of stimulus payments allowed many businesses and households to remain solvent while the U.S. economy effectively shut down.

With COVID lockdowns easing, and individuals returning to their usual spending routines, household consumption has been robust over the past year. Even so, real disposable personal income, which measures how much households have left at the end of the month after paying their obligations, has fallen to its lowest level in nearly two years as the effects of inflation has bid up the prices of goods and services.

Rising inflation has also negatively affected household confidence, falling to its lowest reading in over a decade as measured by the University of Michigan's consumer sentiment index. Indeed, the same survey shows that individuals anticipate inflation to remain above 4.9% over the next twelve months, which is its highest reading since the height of the Great Recession in 2008.

It's important to note that these weaker data points were published before Russia invaded Ukraine. Today's high inflation arguably is tied to legacy supply chain issues coupled with too much money chasing too few goods as a result of pandemic-era stimulus measures. While Covid ground global supply chains to a halt, Russia's war with Ukraine coupled with Western sanctions are likely to exacerbate an already challenging inflationary environment for which we're only beginning to see the early signs.

For example, in some parts of the country today, gasoline prices are at historic highs. According to AAA data, diesel prices were as high as $5.25 per gallon in mid-March, besting the Great Recession peak price of $4.76 in July of 2008 and a pandemic low of $2.37. Add to this the parabolic rise of fertilizer, wheat, industrial metals, and other commodity prices, and the inflation picture could become more challenging in the months ahead. And this matters because households tend to consume less when prices move higher, especially when borrowing costs rise due to the Fed's anticipated tighter policies.

Second Recession Worse than the First

Looking ahead, recent positive economic developments could give way to disappointment in the coming months. Even though a tight labor market has led to higher wages, they're not rising fast enough to compensate households for higher food, housing, or transportation-related costs. At the same time, it's becoming increasingly clear that the U.S. response to Russian aggression is not something that will be resolved in just a few weeks. Indeed, following his meeting with NATO members last week, President Joe Biden indicated that the U.S. and its allies are preparing for a long, drawn-out confrontation with Russia (and potentially China) that could lead to a prolonged high-inflation environment.

So, that leaves us with monetary policy. And one question on some people's minds is will the Fed cut rates as they did in 2020 if the economy begins to slow? While it would be comforting to believe that the Fed could hold back on raising rates if growth slows, the truth is that policymakers likely will continue raising interest rates so long as inflation remains stubbornly high.

Long story short, the Fed made a bad call on inflation in 2020 and waited too long to raise interest rates, so its credibility has suffered. Now, with inflation in the U.S. increasing to 7.9% in February and cruising over five percent for the past nine months, Fed policymakers are playing catchup when supply-side pressures are poised to make their jobs more difficult.

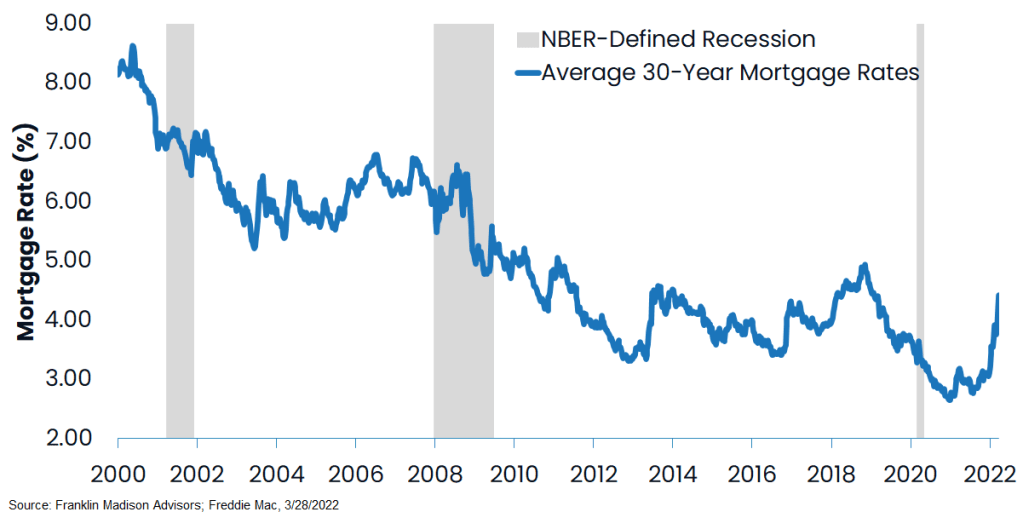

Indeed, during its March meeting, the FOMC raised the Fed Funds rate for the first time since 2018 by one-quarter of a percent, to a rate of one-half of one percent. While this appears to be a small move, the economy is already feeling its effect, with average 30-year mortgage rates now approaching five percent.

What's more, according to the Fed's economic projections, policy rates are likely headed above two percent this year and above three percent in 2023. At this pace, it's very well possible that we've seen the end of zero-percent auto loans and mortgage rates near three percent.

Simply put, if a recession does materialize, what will make it different from 2020 is that there likely won't be broad-based stimulus to prop up growth this time around. You'll recall that during the pandemic-induced slowdown, politicians were willing to dole out stimulus checks to households and businesses, and the Fed cut interest rates and expanded its balance sheet.

This time around, however, the economic slowdown may not lead to the same kinds of bailouts as we saw a couple of years ago, naturally giving way to increased strain on households, businesses, and the financial markets alike.

The truth is that central bank policymakers have lost credibility in their capacity to manage inflation. Their policies either undershot in the years following the Great Recession or overshot during the pandemic. That's why, from their perspective, one way to make that up for the loss of credibility is to allow the economy to fall into a recession, just as the central bank did back in the 1980s during Paul Volcker's time as Fed Chair.

Positioning your Finances for an Economic Slowdown

Taken together, rising interest rates, higher commodity prices and ongoing supply chain issues likely will lead to slower economic growth in the coming year. And this time around, Uncle Same probably won't be doling out cash like he 2020. That's why you need to be prepared financially should a recession appear for the second time in two years.

So how should you position your finances for a potential slowdown and heightened market volatility in the months ahead? Well, if you're an individual focused on mastering your financial independence journey, the short answer is to stay committed to executing on your long-term financial plan.

During times of economic and market uncertainty, for some of us, there's a tendency for our vision to narrow to the present, tempting us to change the way we handle our finances or investment allocations as a way to mitigate what appears to be an immediate financial threat.

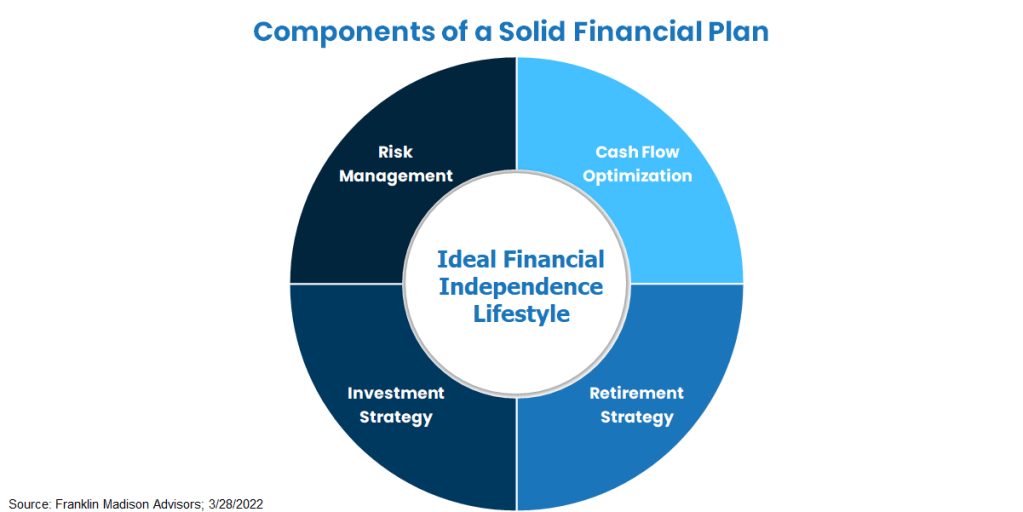

Even so, if you have a well-structured financial plan and a disciplined investment process already in place, then the action that you'll likely need to focus on today is consistently doing the work necessary to execute on your plan. If you have a well-crafted plan, those actions should be defined in your implementation schedule. Otherwise, developing a set of strategies to align your financial resources with your long-term goals should be a priority if you don’t already have a comprehensive financial plan in place.

Indeed, a solid financial plan lays out how to connect the dots between your financial resources and ideal long-term lifestyle goals. At the same time, it identifies predefined strategies and tactics that you can tap into to manage adverse conditions when they inevitably arise in the near-term.

When it comes down to it, various indicators suggest that we’re likely headed for a second recession in two years. And this time around, the government possibly won’t be as accommodating as it has been in the past. That’s why if you're serious about mastering your journey to financial independence, then now's the time to ensure that you have a solid financial plan in place, that your investment strategy is aligned with your long-term plan and that you're effectively executing on your implementation schedule.

Russia Invades Ukraine – What Now?

Russian President Vladimir Putin made good on his promise to invade Ukraine on Thursday. As a result, the S&P 500 Index sold off sharply before bouncing back into the close. Front-month crude oil futures also climbed above $100 per barrel intraday for the first time since 2014 before giving back gains. Market tensions indeed settled after President Biden’s press conference concluded on Thursday, but, on a year-to-date basis, US equities, on the whole, remain near bear market territory.

A New Set of Risks

There’s little doubt that market participants have had a lot to contend with over the past few weeks. More recently, it was the uncertainty surrounding central bank policy and whether the FOMC would aggressively raise rates in March to help stem the tide of higher inflation. Now, investors not only have to make sense of what a Russian invasion in Eastern Europe might mean for corporate earnings but whether military conflict escalates to the point of sparking a world war, as some US politicians have suggested.

Make no mistake, there are many reasons to be concerned about Russia’s assault on Ukraine. For starters, this move has arguably rewritten Russia’s relationship with the West after 30 years of peace following the collapse of the Soviet Union. Certainly, some might suggest that this relationship changed when Russia invaded and took control of Crimea in 2014.

Even so, as President Biden pointed out in today’s press conference, Putin’s ambitions to restore the Soviet Union could lead to further military escalations beyond Ukraine’s borders. Indeed, a Russian confrontation with NATO-allied countries in Eastern Europe could escalate tensions along other territorial fault lines, leading to a broader global conflict.

Potential Conflict Beyond Ukraine

That’s why it’s essential to understand that the events unfolding in Ukraine are just one of many other territorial disputes across the world today. And the most significant source of these disputes is China. Indeed, after dismantling democracy and securing its hold of Hong Kong, China is arguably looking for an opportunity to finally take back control of Taiwan (a country staunchly allied with the US), potentially by force. India has also seen its fair share of confrontations with China as military tensions have centered on the Kashmir border for years.

In Southeast Asia, North Korea, whose economy is mainly dependent on China, continues to agitate its neighbors with threats of military strikes even as its population starves. And more broadly, China has a score to settle with several countries regarding its nine-dash line claims to the South China Sea. Add in political instability and various proxy wars in the Middle East and Central Asia, and you could have the recipe for a broad-based global conflict.

Are We Headed for World War III?

So, is this the start of World War III? Well, we hope that cooler heads prevail in the coming days and weeks, notably following the imposition of significant financial and economic sanctions placed by G7 leadership on the Russian economy. Either way, China likely will be directionally key to broader global tensions. To be sure, Beijing appears to be walking a fine line between appeasing the Kremlin while maintaining decorum with the West, potentially forestalling a broader global conflict. Even so, in the coming weeks these sanctions likely could have a notable impact on the global markets and economy even without a hot war. How is this possible?

Well, long story short, global energy prices are likely to rise as sanctions hit a vital producer of the world’s fossil fuels. Additionally, restrictions on US technology exports to Russia could inadvertently spark a policy tit-for-tat with China and complicate an already strained global supply chain. Indeed, much of inflation’s rise over the past year has been attributed to global supply chain issues resulting from Covid-related economic lockdowns.

Amidst this geopolitical uncertainty, one silver lining seems to have surfaced. And that’s the fact that it could be more problematic for central bank policymakers to raise rates aggressively without potentially pushing the economy into a recession with the threat of war looming. Indeed, this realization among some market participants arguably led to a significant risk asset rally into the market close on Thursday.

What’s the End Game?

So, how will this all end? Well, we don’t have a crystal ball and can’t say with certainty how today’s events will unfold in the weeks and months ahead. Nevertheless, what we do know is that similar geopolitical events have come and gone over the past century, yet global democracy has only become stronger as a result while risk asset prices continue to gain decade over decade.

Now, it goes without saying that Russia’s decision to invade Ukraine could have significant global economic and market implications. So, from this perspective, what should individuals concerned about the prospects of military escalation do to best position their finances during this time of uncertainty?

Well, given the tenuous geopolitical and global economic backdrop, we believe that individuals on the path to mastering their financial independence journey should take a few steps to frame these uncertainties within the context of their portfolios and, more importantly, their broader financial plans.

Dealing with Market Uncertainty

To start, turn off the news and take the time to remind yourself of your long-term financial goals. During times of crises, we often find ourselves consumed with ever-changing news flow and yearning to take some form of action.

Oftentimes, however, the best course of action during times like these is to stay committed to the priorities you’ve set out to achieve for the future. Don’t get distracted by the near-term noise. Indeed, your long-term financial plan and disciplined investment strategy was created to help you navigate times just like these.

Next, try to avoid timing the market where possible. Even after reviewing your financial plan, you may be tempted to make near-term investment decisions in your portfolio that may have adverse consequences over the long term.

For example, if you had sold into the market open on news of Ukraine’s invasion, you likely would have missed the strong rally into the market close. During these times of uncertainty, many investors are best served by managing risk in their portfolio rather than by trying to divine market moves hour-by-hour or day-by-day.

And that brings us to our last and final point: manage investment risk. To manage risk in your portfolio you’ll likely want to focus on two things you can control: 1) having adequate cash on hand and 2) ensuring that your portfolio is properly aligned with your long-term goals. To the first point, consider having enough cash on hand to cover living expenses or other expenditures over the next 9-12 months. Doing so could prevent you from selling securities from your portfolio at an inopportune should market volatility linger for longer.

Second, now may be the time to ensure that your portfolio has an ideal mix of stocks and bonds aligned with your strategic asset allocation framework. Periodically rebalancing your investment can help ensure that you’re taking the ideal amount of risk in your portfolio, given your current stage in life.

At the same time, you may want to ensure that your portfolio holdings reflect a basket of stocks with solid earnings potential while holding higher-quality credit in your bond holdings.

Only time will tell whether the current situation will escalate to a broader conflict or settle more amicably. We hope that substantial financial and economic sanctions coupled with a solid political resolve from Western leaders will convince Putin to end his military incursion in Ukraine. Until then, we anticipate market volatility to ebb and flow with the news cycle. For now, avoiding the noise and committing to your long-term financial plan will not only give you peace of mind during this time of uncertainly, it likely will also enable you to continue your journey toward financial independence mastery.

Don't Call it a Crash (Yet)

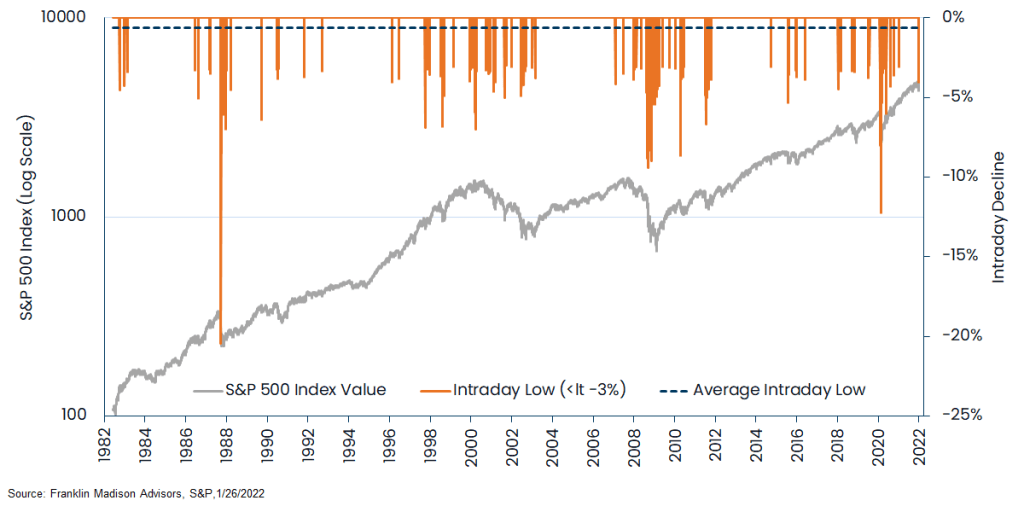

The S&P 500 index fell nearly four percent intraday on Monday, January 24, making for one of its most volatile trading sessions since September 2020. Heading into this period of instability, investors had good reason to believe that the markets were heading for a collapse. Rising inflation, concerns about the Omicron variant, the potential for war with Russia, and a Fed poised to aggressively raise interest rates amidst a clouded U.S. and global economic outlook had seemingly overshadowed any positive catalysts for an upward market move.

S&P 500 Index Intraday Declines Greater than 3%

With so much uncertainty on the rise, and policymakers poised to drain liquidity from the financial markets, a key question for many investors is whether we are on the precipice of a prolonged market selloff. Certainly, some market watchers and prognosticators are making the rounds on financial media and arguing that this week's volatility is setting the stage for lower equity prices ahead.

Anecdotes aside, historical data indeed suggests that a period of market weakness in risk assets is likely on the horizon after this week's moves. That said, however, there's still a case to be made for avoiding panic and remaining committed to a long-term investment strategy amidst solid economic and corporate fundamentals. Indeed, it's during these times of increased market uncertainty that financial independence masters like yourself preserve their wealth by adhering to their disciplined asset accumulation and retirement distribution strategies.

Intraday Decline and Future Market Performance

So, what should we make about Monday's market decline? Well, one way to interpret the selloff is to view the market move in a historical context. To do this, we looked at S&P 500 index data going back to 1982 first to understand the frequency and significance of sharp intraday pullbacks. Second, we evaluated how stocks have performed in the periods following a significant one-day selloff.

What did the data show?

Well, to the first point, history shows that days where the markets declined by at least 3% intraday, like the one we saw this week, have occurred in less than two hundred of the ten thousand trading days over the past forty years, or 2% in total. In fact, the data show that, on average, stocks tended to decline less than one percent in intraday trading over this period. Moreover, our analysis suggests that these sorts of pullbacks are prevalent heading into periods of price weakness, more so when market narratives change.

So, now that we know that what happened this week wasn't just another run of the mill market slump, what does history tell us about how stocks have performed in the weeks and months following such a selloff? Historically speaking, the data suggests that markets more often than not continued sliding an average 8% in the month following a sharp one-day selloff.

And how have stocks performed after three months following a selloff greater than 3%? Well, from this expanded timeline, the data fares somewhat better, with markets down only about a third of the time. And finally, if we look out over a one-year horizon the data suggest that equity prices are down about a quarter of the time over the past four decades. Taken together, one way to interpret Monday's selloff from a historical context is that volatility likely could remain elevated in the near term, with market conditions improving over the long term.

Is it a Crash or Market Correction?

While there's certainly precedent for continued market weakness in the weeks ahead, a key question for some investors is whether we're heading for a market correction or a market crash. First, it's important to clarify that a crash is much different from a correction. A market crash can be characterized as a sudden, steep decline occurring over a matter of days. For example, you'll likely recall that in February 2020, the S&P 500 index declined over 10% in less than a week amidst Covid concerns before dropping the following month precipitously.

On the other hand, Corrections generally extend over weeks and are relatively common. So common, in fact, that corrections have occurred 18 times over the past decade. So, what does all this mean? Well, as we pointed out earlier, while a sharp intraday pullback has been historically consistent with near-term risk asset declines, several catalysts like expectations for positive economic growth and rising corporate earnings this year likely remain supportive of equity prices.

S&P 500 Index Analyst Earnings Estimates

Solid Fundamentals as Tailwinds Fade

Indeed, compared to the outlook driving the market crash of 2020, economic fundamentals today are softening yet remain generally on firmer footing. For example, the government this week reported that U.S. economic growth bested expectations in the fourth quarter and that the economy expanded at its fastest clip in nearly four decades on an inflation-adjusted basis. Data also show that personal income and household balance sheets remain solid as the unemployment rate declines and employers offer higher wages to their workers.

From a business sentiment perspective, the Richmond Fed's latest survey of CFOs shows that optimism among business leaders remained buoyant in the fourth quarter of 2021. Indeed, aside from cost pressures and supply chain issues (which we'll discuss in a moment), positive hiring intentions remain a key indicator of forward-looking business health.

On the earnings front, analysts expect corporate earnings growth to slow compared to last year's post-pandemic rise, but generally are anticipated to remain positive in 2022. This data is vital because heading into the market crash of 2020, corporate CEOs slashed forward guidance, and earnings declined amidst policy-induced economic lockdown measures.

US Average Hourly Earnings

Self-Inflicted Wound

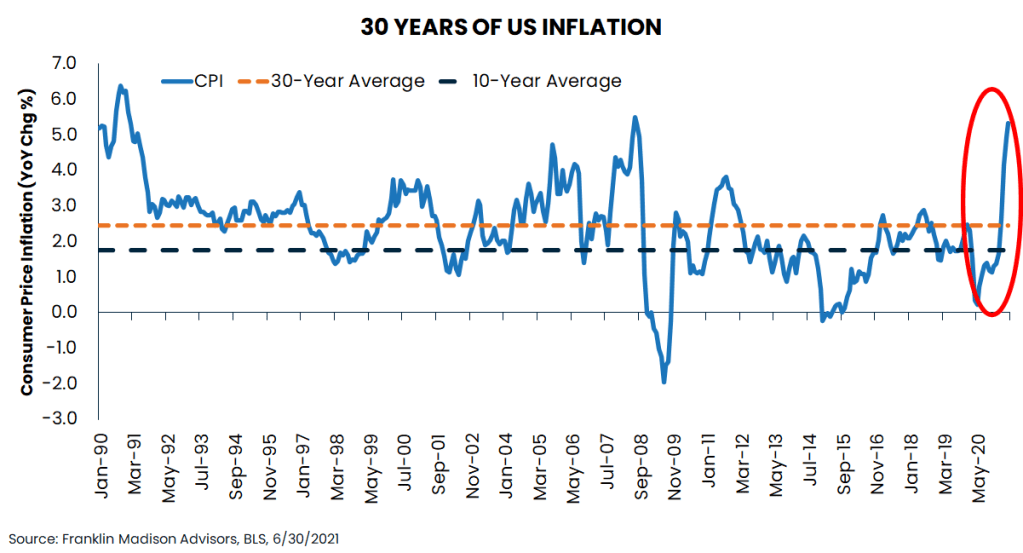

While backward-looking data suggests that the U.S. economy has been on solid footing, forward-looking indicators point to both economic and market headwinds in the months ahead. Top of mind for households, businesses, policymakers and market participants alike is the persistence of stubbornly high inflation. This concern is evidenced in headline inflation coming in at 7.1% in December, its sharpest rise in forty years. At the same time, the core PCE index (the Fed's preferred measure of inflation) came in at 4.9% in December, compared to a pre-pandemic average of 1.6%.

This inflation rise has also been evident in record-high home and auto prices as well as the rising cost of food and gasoline, which understandably has households worrying. Indeed, data out on Friday from the University of Michigan showed that consumer sentiment is at among its lowest level since the start of the pandemic, with survey respondents reporting five-year inflation expectations at their highest level in a decade. At the same time, business surveys indicate that rising input costs are among the top concerns for business leaders.

To address seemingly out of control price increases, Federal Reserve policymakers have announced measures to quickly raise interest rates and have scaled back asset purchases. And it's this aggressive policy response that has caught market participants on the back foot and contributed to recent bouts of market volatility. As it stands, the Fed is ready to raise rates four times this year (likely beginning in March), with some analysts predicting as many as seven hikes this year.

While monetary policy can be used as a tool to slow rising prices, a slowdown in the economy (or even worse, a recession) could result as a self-inflicted wound via Fed policy in 2022, which has some market participants on edge. The reason being is that today's spiraling inflation is in many ways driven by logistics issues over which the Fed has little control.

To be sure, at a macro level, global supply chain issues have contributed to the rising prices of everything from clothing to autos. At a local level, a report from the American Trucking Association suggests that the U.S. is experiencing a shortage of around 80,000 drivers due to illness, retirement, or simply a lack of interest. This shortage of freight delivery drivers and the rising cost of transportation is putting upward pressure on the price of goods on store shelves – something the Fed can’t control.

Freight Costs Growing Fastest in Decades

Don't Call it a Crash (Yet)

While there's a reason for concern among some market participants, it may yet be too soon to call recent market moves the beginning of an outright crash. Indeed, compared to the events of the market crash in 2020, both fiscal and monetary policymakers have greater leeway on addressing impediments to economic growth, which can affect market sentiment.

Nevertheless, with forward-looking indicators pointing to signs of slowing economic growth, market participants need some clarity that aggressive Fed policy won't choke off economic growth and, hence, corporate earnings. Simply put, how the Fed threads the needle of policy tightening while preserving economic growth will determine whether the markets can claw back gains or succumb to a prolonged bear market selloff. This is one reason why incoming forward-looking economic data will be crucial to market sentiment in the coming weeks, confirming whether or not the economy can handle higher rates.

So what's an investor to do during these times of changing market narratives and policy uncertainty?

Whether you're still saving up for your early retirement goals or have already become financially independent, now is the time to carefully consider your investing, savings, and spending strategies for the coming year.

Saving for Financial Independence

If you're still in the accumulation phase of your financial independence journey, now's likely an excellent time to take a second look at how much you'll need to have saved to cover your post-employment lifestyle expenses in the future.

While it's likely that the inflation rate could slow in the months ahead, the truth is that prices of goods and services will potentially remain elevated for years to come. Indeed, the rapid rise in home, auto, and other consumer goods has reset long-term baseline spending needs for some individuals.

From this perspective, your role as an asset accumulator will be to ensure that the baseline financial independence savings goal you've defined for yourself five, ten, or twenty years down the road are consistent with the reality of higher prices today. From there, you'll need to determine if and to what degree your savings needs to increase today to meet your new financial independence number.

Additionally, during these times of uncertainty, you'll likely want to avoid the temptation to shift your investment strategy when markets become volatile.

Unless you have a near-term need to drawdown investment savings, changing your asset allocation, like going to all cash, could be detrimental to your long-term savings plan. Indeed, as we pointed out in a prior report, missing even the ten best days in the market could leave your long-term financial plan falling short.

Missing the Best Days in the Markets

Preserving Your Financial Independence

If you're already financially independent and living off of your savings, being prepared for a bout of market volatility while accounting for higher prices in the years ahead likely will be essential to preserving your wealth. No one has a crystal ball to tell them where the economy or markets are headed. That's why during times of uncertainty, your investment process is vital to ensuring long-term financial success. To this end, we suggest that you take a multi-pronged approach to ensure that your assets are well-positioned to provide savings longevity.

First, as with the accumulators, take the time to reevaluate your long-term income distribution need when factoring in higher levels of inflation and market volatility using Monte Carlo simulations. After completing this analysis, you may find that your financial wealth could fall short of your high-confidence savings projections. If this is the case, now may be the time to adjust your near-term lifestyle spending trends by making minor adjustments to expenses, which can significantly impact your overall savings need.

Second, stay committed to a disciplined investment process. Periods of market uncertainty, like we experienced this week, might tempt you to go to cash in anticipation of a broader market selloff. On the other hand, after reevaluating your savings need, you may be tempted to increase your investment risk exposure to make up for a projected savings shortfall. Either way, when it comes to managing your wealth, focus on what you can control and stay committed to long-term outcomes.

Finally, ensure that you have enough cash on hand in the coming months to navigate periods of market uncertainty. The last thing that you'll want to do is sell portfolio holdings to pay for household expenses when markets are in decline. Selling at inopportune times may lead to disappointment and reduce your likelihood of long-term retirement success, particularly if you're not in a position to add to savings through employment income.

While we may not be headed for a market crash just yet, there's ample fuel for a prolonged market selloff in the weeks ahead. With that said, however, there’s still a case to be made for avoiding panic and remaining committed to a long-term investment strategy amidst solid economic and corporate fundamentals. Indeed, it’s during these times of increased market uncertainty that financial independence masters like yourself preserve their wealth by adhering to their disciplined asset accumulation and retirement distribution strategies.

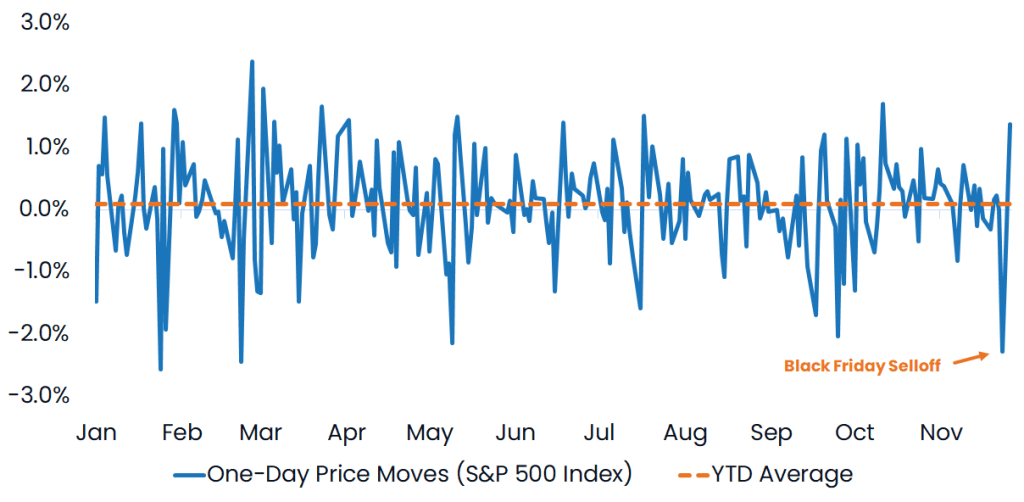

What to Make of the Black Friday Market Selloff?

Some investors cut short Thanksgiving festivities last week as financial markets sold off on renewed Covid concerns. The World Health Organization (WHO) declared the latest Covid strain Omicron a “variant of concern”, leading broad market indices to post their sharpest single-day losses in months.

This latest designation from the WHO reflects the fact that the viral strain contains around 50 mutations, 30 more than the main target of many current Covid-19 vaccines, potentially making the virus more transmissible and existing treatments less effective. While the ongoing healthcare situation has created angst in the markets over the past two years, the virus itself is likely not the primary cause of the Black Friday selloff.

To be sure, shortly after the WHO announcement, the US, along with the Canadian, Japanese, and EU governments, announced travel restrictions on Omicron fears. These actions prompted market concerns about renewed economic lockdowns while, at the same time, leading rallies in some stay-at-home stocks even as broader indices posted sharp declines. After a prolonged risk-asset recovery following March 2020 lows, many investors are asking whether this latest viral development will be the catalyst for a long-awaited bear market selloff.

Uneven Policy Transition

Now, many unknowns are surrounding the healthcare and economic implications of the latest viral outbreak. Ever since Covid was discovered in late 2019, the WHO has designated dozens of outbreaks as “variants of concern”. This ever-changing viral landscape has diminished the prospect of a clean break with the pandemic, leading many experts to conclude that the temporary nature of the healthcare crisis likely will shift into a long-term endemic that society will contend with for some time.

While these suggestions seem simple enough, the authors of the reports concede that such an approach would require what they consider a momentous societal shift where every stakeholder plays an important role...

For many individuals, last week’s outbreak announcement likely came as little surprise, and it’s very well possible that society at large is already accepting the inevitability that this disease will be with us for months, if not years to come. While a transition from pandemic to endemic may seem natural at this juncture in the outbreak, the trouble for markets is that policymakers continue to rely on playbooks that focus on halting a pandemic in the near-term, rather than addressing the reality that closing businesses and shutting down the economy could cause more long-term harm than short-term benefits.

A report from McKinsey & Company suggests that in order to adapt to a new reality surrounding the healthcare crisis, policymakers should focus on a four-point approach that 1) defines the new normal, 2) tracks disease progress, 3) limits illnesses and deaths, and 4) slows transmissions. While these suggestions seem simple enough, the authors of the reports concede that such an approach would require what they consider a momentous societal shift where every stakeholder plays an important role, this includes:

- Governments building consensus on goals, communicating superbly, and setting the right incentives

- Employers taking an elevated role, setting policies for their workplace and helping their employees think through the changes

- Health systems striking the right balance among competing demands and planning for the inevitable outbreaks and surges

- Individuals challenging the convictions they’ve developed in the past 18 months and adopting new behaviors

While such an approach seems ideal, the truth is that policy today remains largely reactionary, as evidenced in the latest travel bans. What’s more, the US Administration’s recently introduced vaccine mandates aimed at halting the viral spread likely will only exacerbate the US supply chain issues that have contributed to higher-priced consumer goods and persistently high inflation over the past few months.

What’s more, governments have relied on central banks to buffer the adverse effects of economic shutdowns and restrictions by increasing the availability of capital. Today, however, this approach shows its limits as supply constraints and labor shortages, coupled with easy money policies, contribute to historic inflationary pressures.

A Bumpy Road to Transition

Looking ahead to 2022, we believe that government and central bank policy will remain a key risk to market sentiment. By many measures, Covid is here to stay for the long-term. Even so, the policies employed to “flatten the curve” during the early months of the outbreak are likely not sustainable. To some degree, easy central bank policies and fiscal spending helped offset the economic impact of shutdown measures early in the pandemic.

Even so, central bank policy is now showing the limits of its effectiveness, and the likelihood of additional monetary and fiscal support next year could be limited should US economic growth begin to stall. That’s why we believe that a critical risk to the markets is continued myopic policy response to a long-term healthcare issue as new Covid variants and strains inevitably materialize.

On the other hand, one potential positive market narrative in the coming year likely could be the introduction of policies that reflect the endemic nature of the healthcare crisis, as outlined earlier in this report. Such an approach could introduce pragmatic ways to live with the virus over the long-term and let go of some policies aimed at the failed hope of stopping Covid in its tracks at the cost of economic growth.

Positioning for Policy Uncertainty

So how should you position your finances during this transition from pandemic to endemic? Well, there is little doubt that the ongoing healthcare crisis has challenged many of our financial independence plans for 2021 and beyond. Whether you’re still saving up for your early retirement goals or have already become financially independent, now is the time to carefully consider your savings and spending strategies for the coming year.

Saving for Financial Independence

If you’re still in the accumulation phase of your financial independence journey, now’s likely a good time to take a second look at how much you’ll need to have saved to cover your post-employment lifestyle expenses in the future. The combined effects of healthcare uncertainty and policies to curb viral spreads have put upward pressure on prices this year.

While it’s likely that the inflation rate could slow in the months ahead, the truth is that prices of goods and services will potentially remain elevated for years to come. Indeed, the rapid rise in home, auto, and other consumer goods has reset baseline spending needs for some individuals. From this perspective, your role as an asset accumulator will be to ensure that the baseline financial independence savings goal you’ve defined for yourself five, ten, or twenty years down the road are consistent with the reality of higher prices today. From there, you’ll need to determine if and to what degree your savings needs to increase today to meet your new financial independence number.

Preserving Your Financial Independence

If you’re already financially independent and living off of your savings, being prepared for a bout of market volatility while accounting for higher prices in the years ahead likely will be essential to preserving your wealth. No one has a crystal ball on where things are headed. That’s why during times of uncertainty, your investment process is vital to ensuring long-term financial success. To this end, we suggest that you take a multi-pronged approach to ensure that your assets are well-positioned to provide savings longevity.

The Black Friday selloff is likely to be the first of many market fits and starts in the coming year following a strong market rally.

First, as with the accumulators, take the time to reevaluate your long-term income distribution need when factoring in higher levels of inflation and market volatility using Monte Carlo simulations. After completing this analysis, you may find that your financial wealth could fall short of your high-confidence savings projections. If this is the case, now may be the time to adjust your near-term lifestyle spending trends by making minor adjustments to expenses can have a significant impact on your overall savings need.

Second, stay committed to a disciplined investment process. Periods of market uncertainty, like we experienced last week, might tempt you to go to cash in anticipation of a broader market selloff. On the other hand, after reevaluating your savings need, you may be tempted to increase your investment risk exposure to make up for a projected savings shortfall. Either way, when it comes to managing your wealth, focus on what you can control and stay committed to long-term outcomes.

Finally, ensure that you have enough cash on hand in the coming months to navigate periods of market uncertainty. The last thing that you’ll want to do is sell portfolio holdings to pay for household expenses when markets are in decline. Selling at inopportune times may lead to disappointment and reduce your likelihood of long-term retirement success, particularly if you’re not in a position to add to savings through employment income.

The Black Friday selloff is likely to be the first of many market fits and starts in the coming year following a strong market rally. Make no mistake, inflation certainly is a concern for households, businesses and market participants alike. Nevertheless, as we look into the coming year, we believe a key risk to market sentiment likely will be policy missteps that ignore the evolving nature of a Covid pandemic to long-term endemic. On the other hand, policies aimed at responding quickly to healthcare concerns while eliminating restrictions that reduce commerce friction could be a positive catalyst for market sentiment.

Mid-Year Outlook: Not Out of the Woods Yet

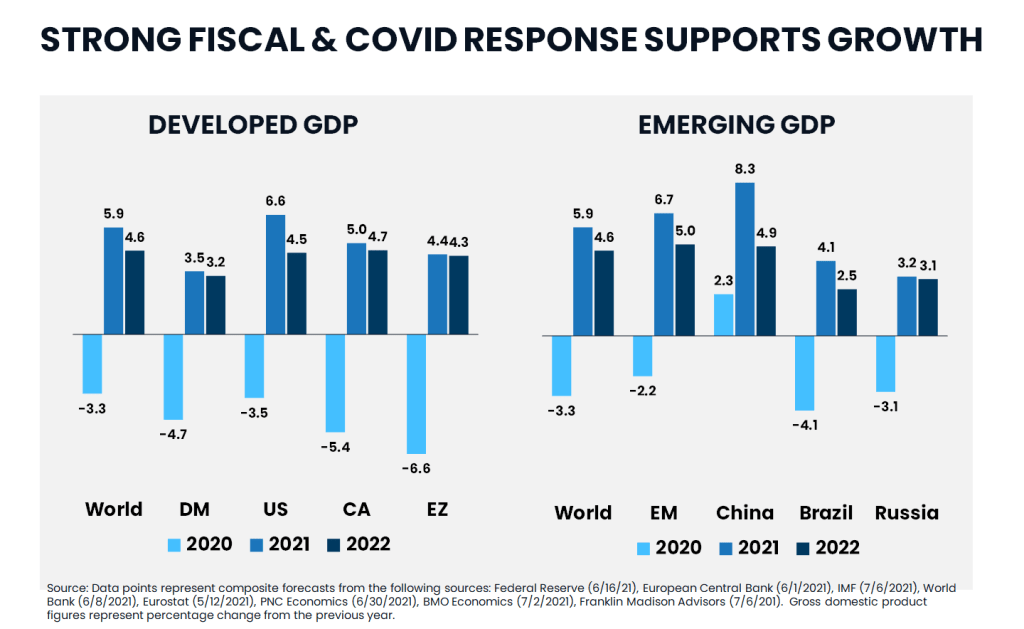

Investors have had good reason to celebrate this year, but is it truly time to let our guards down? Thanks to practical policy guidance, more than half of the US population has received at least one COVID-19 vaccine in 2021. Add to this the boost from a $1.9 trillion fiscal stimulus package introduced in March, and the US economy today is on pace for its most robust recovery in nearly 40 years.

So, how have the financial markets taken these improvements? Well, risk assets have responded to the positive health and economic developments by posting solid gains in the first and second quarters. Looking ahead, however, the market and economic outlook appear less promising. A resurgent COVID variant, accelerating inflation, and a notable lack of bipartisan support for additional fiscal stimulus pose challenges to economic and market momentum in the second half of the year.

Mid-year Review

Now, before discussing likely challenges to the markets and economy in the latter half of the year, let's take a moment to recall how we got here.

Stabilizing Economic Growth

It can be argued that ongoing fiscal and monetary stimulus and easing COVID restrictions led to improving business and consumer sentiment in the first half of 2021. According to government data, the US economy posted a 6.4% gain during the first three months of the year. And by some estimates, the US economic growth is expected to have come in around 8.7% in the second quarter.

For many households, the extra $1,400 per person stimulus checks, coupled with easing social distancing restrictions, likely contributed to this year's spending boom. For example, the latest retail sales data showed that spending at restaurants outpaced pre-COVID levels, rising to a record $67 billion in May.

It's also worth noting that in 2020, approximately 114 million people lost their jobs due to social distancing efforts and the economic downturn. Today, however, labor market conditions are on an upswing. For example, the US unemployment rate as of June was 5.9%, which remains elevated but nevertheless improved from 14.8% last April. Unemployment claims have also fallen back to levels not seen since early 2020 as some businesses have quickly reopened.

Now, one downside to this year's economic boom has been rising inflation. And as we recently wrote about in last month's report, a key reason for higher inflation today is ongoing supply chain disruptions. To be sure, global logistics bottlenecks have had lingering effects on the price of goods used in end-consumer products and manufacturing inputs alike. Add in trillions of dollars in fiscal and monetary stimulus, and a key concern for markets and households is whether inflation will truly be transitory.

We'll discuss this point about inflation more in a moment. But, for now, we can say with some confidence that the recent economic improvements have underpinned positive investor sentiment even as the nearly 16-month market rally shows signs of exhaustion.

Solid Market Performance

In terms of market performance during the first half of the year, the US remained one of the best-performing markets, led higher by small-cap stocks. For instance, the Russell 2000 Index was up over 17% during the first six months of 2021 as cyclicals rallied in anticipation of the US economic recovery. A 14% gain in the S&P 500 Index followed this positive performance along with a 12% move higher in the tech-heavy Nasdaq 100 Index.

Internationally, emerging markets lost momentum during the first half as COVID concerns in Asia and uncertainties surrounding China weighed on overall performance. Even so, the MSCI Emerging Markets Index posted a solid 6% gain during the first six months of the year. Across the pond in Europe, while economic conditions are anticipated to improve this year, ongoing health concerns have limited equity market gains to around 10%.

And while we're talking about risk assets, we would be remiss, not to mention the recent attention given to "meme stocks" and crypto. These highly speculative investments made a splash last year but have seemingly lost their fizzle recently. After peaking early in the second quarter, prices of these assets have given up much of their gains. And these highly volatile price swings are a crucial reason why we view such assets are speculative in nature.

From a fixed income perspective, the bond markets aren't quite so convinced that the US economy is entirely on solid footing. This point has arguably been seen in rising Treasury prices even as inflationary pressures move higher. For example, the yield on US 10-Year Treasurys fell 50 basis points from their April peak even as core and headline inflation surprised to the upside in the first half of the year.

At the same time, however, the low yield environment coupled with investor desire for income led to increased demand for high yield bonds, and thus driving down credit and quality spreads to levels not seen in several years.

On the commodities side, lumber prices have also made headlines with their exponential rise and sharp selloff this year. Even so, prices for real estate and commodities are higher on balance given solid demand for housing and as consumers get out and about in this post COVID world. To this point, the NAREIT All REIT Index gained 21% during the first half of the year, while the S&P GSCI Commodity index was up 30%.

Second Half Outlook: Not Out of the Woods Yet

Certainly, the economy and financial markets have shown solid improvements during the first half of the year. But a key question right now is, "can we let our guards down and rely on the positive developments to carry performance into the latter half of 2021?" The short answer is, possibly not.

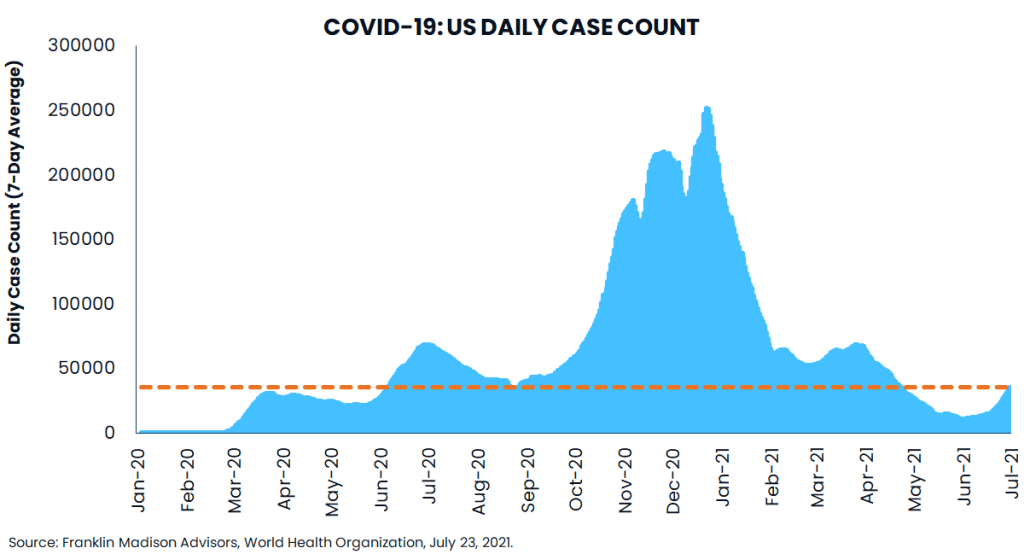

The reason for this caution comes from the fact that market participants, households, and business leaders alike will have many unknowns to contend with during the second half of this year. To be sure, an ascendant COVID Delta variant, accelerating inflation, and policy uncertainties likely will dominate the market and economic narrative over the coming months.

Inflation May be a Drag to Growth

While the US economy has made significant strides this year, it's essential to note that lingering political and healthcare concerns coupled with uncertainties surrounding inflation remain potent headwinds to market sentiment. While we expect the US economy to expand at around 6.5% this year, this estimate reflects a deceleration from solid growth earlier in the year.

Of these issues, rising inflation and, more specifically, how policymakers respond to it will remain top of mind for many market participants. And it's this uncertainty that likely will contribute to ongoing bouts of market volatility in the months ahead. As noted earlier, much of the recent inflationary pressures have come from global supply chain issues related to COVID lockdowns.

Even so, in recent testimony to congressional leaders, Fed Chair Jay Powell indicated that if inflation does not slow down as expected, the "[Fed] will use [their] tools to guide inflation back down." While such language has raised market expectations for a rate hike later this year, the path to that outcome remains highly uncertain and a headwind to positive market momentum in the near term.

Variant Spread a Key Risk to Sentiment

On the healthcare front, an infectious surge in the coronavirus Delta variant globally likely will give market participants reason for pause. Recent reports show that new cases are on the rise again in the US and are at their highest levels since mid-May.

Globally, less prepared economies are struggling to contain this highly contagious variant, which is putting downward pressure on economic growth projections. To this point, even countries that have seemingly overcome COVID, like Australia, have found themselves in lockdown once again.

What's more, a relentless spread of the Delta variant might once again complicate the US economic and market outlook as children return to school in the fall. Should efforts to contain the Delta variant fall short in less prepared economies (and at home), there's a potential for rolling global lockdowns, which could further upset global supply chains and keep prices elevated for an extended period.

Stay on Track to Financial Independence

So, what does this outlook mean for your financial independence journey? Well, while the economy and markets are indeed on the upswing, it's essential to note that we're not out of the woods yet. From a financial markets perspective, positive price action in risk assets this year has primarily been driven by an economic recovery narrative.

Lately, this narrative is coming under pressure as higher than expected inflation and the potential for another economic slowdown are bringing into question whether the Fed will raise interest rates sooner rather than later. The concern behind this approach is that policymakers may try to address inflationary concerns at a time when the economy is slowing, potentially reducing market liquidity and subsequently putting the markets on the back foot.

While Biden's infrastructure plan may offer another fiscal thrust to the economy, the latest iterations of the package may not provide the same impulse that the dual effects of monetary and fiscal stimulus provided early last year. From this perspective, positive market sentiment could begin to wane. Indeed, ongoing healthcare concerns, inflation worries, and policy uncertainties may all contribute to higher levels of market volatility in the months ahead.

So, what can you do to ensure that your plans for financial independence stay on the right track? Well, at this crossroads between still buoyant market sentiment and economic uncertainty, we recommend evaluating your risk management process and giving your attention to two key points of consideration.

Reposition Your Investments for Risk

First, whether you're still building wealth or relying on it to fund your post-employment years, now might be a good time to rebalance your investment portfolio. Sharpen your pencil and position your portfolio to take advantage of potential sales in pro-cyclical investments like emerging markets, small caps, and value stocks if you're in the wealth accumulation phase of your financial independence journey.

For those of you dependent on your wealth to remain financially independent, now may be the time to raise enough cash to meet living expenses in anticipation of a market pullback. This approach might involve taking some of your winning positions off the table, adding to cash to cover near-term lifestyle expenses, and reducing the need to sell at inopportune times if you're already dependent on retirement income.

Now is also a good time to evaluate trimming unnecessary risky positions in your portfolio and focusing on more high-quality, tax-efficient investments. At the same time, you'll want to be sure that your portfolio is closely aligned with your long-term asset allocation objectives. Why? Well, when market volatility does pick up, you'll want to ensure that your retirement nest egg has a fighting chance to quickly recover from a period of heightened market volatility.

Check Your Assumptions

Finally, it's hard not to ignore the rising cost of living. Whether inflation is truly transitory or not is yet to be seen. Either way, inflation rates may be unlikely to return to pre-pandemic levels once global supply chain issues are resolved. To this point, if you haven't already evaluated the inflation assumptions in your financial plan recently, now may be an opportune time to recheck them. The reason being is that higher than anticipated inflation over the long term could result in your spending more than expected in retirement and lead to cutting your financial independence plans short.

That's why it's essential to periodically review assumptions used in your retirement plan, evaluate whether those assumptions are generous considering the changing economic environment, and make necessary adjustments today to ensure that your financial independence journey is on track for the long term.

Biden’s Infrastructure Plan: Will a Deal Get Done?

City streets had been flooded for hours before the hurricane made landfall in Louisiana on the morning of August 29, 2005. Levees all around New Orleans had collapsed, and by 5 a.m., the city's largest canal, the 17th Street Canal, failed.

Over 1,800 souls lost their lives, and billions of dollars in damage was left in the wake of Hurricane Katrina. Scientists predict that once-in-a-generation natural disasters like this one may become more prevalent in the coming years, given the effects of climate change. Even so, President Joe Biden's infrastructure plan intends to address this genuine concern.

The American Jobs Plan

In a speech delivered just outside of Pittsburgh in late March, President Biden introduced the American Jobs Plan. This sweeping initiative would spend over $2 trillion to prevent infrastructure disasters like the one in New Orleans and provide a renewed foundation for businesses and individuals to compete globally in the twenty-first-century marketplace.

To be sure, President Biden's proposal is more ambitious than we've seen in generations. His package includes spending on preventable infrastructure failures while funding traditional bridge and road repairs. Simultaneously, the plan makes provisions for investments in quality-of-life essentials like clean water, quality education, and telecommunications improvements while funding caregiving assistance for an aging population and creating globally competitive U.S. manufacturing jobs.

Proposed Spending on Biden's American Jobs Plan

Following decades of false starts, it appears that the U.S. is finally on the cusp of beginning its most ambitious infrastructure program in years. But will a deal get done? Now, Joe Biden isn't the first president to propose ambitious infrastructure spending. In fact, many infrastructure plans have been introduced in recent years. From Clinton to Bush, Obama and Trump, each administration put forward its ideas to repair bridges, fix roads and future-proof the economy, only to face gridlock on Capitol Hill.

A lack of political will

There's little debate among members of Congress that U.S. infrastructure is in desperate need of repair. From preventable levee failures in New Orleans to a bridge collapse in Minneapolis and bus-swallowing sinkholes in Downtown Pittsburgh, politicians have voiced their concerns about the work that’s needed. Nevertheless, a challenge for previous administrations has been an inability to overcome a lack of political will to get a meaningful infrastructure bill passed through congress. Will the Democratic president’s proposal meet a similar fate?

On the surface, taxes and spending appear to be a central point of contention for some GOP members. To this point, the Biden administration is striving to find middle ground. Even so, a key challenge may be a deep-seated issue of politicians worrying that they'd be unable to defend a trillion-dollar bill to their constituencies who may not see the benefits of the legislation for years to come. So, what's changed that would enable an infrastructure deal to get done this time around?

Impetus for deal making

Well, first, there's the issue with China. Both Republicans and Democrats agree that China’s economic advance has come at a cost for U.S. businesses and workers. While taking on China directly is one approach to the matter, there's little doubt that failing infrastructure is hampering our country’s ability to compete with the world's second-largest economy. Therefore, addressing deferred maintenance and investing in technologically underdeveloped parts of the economy will be essential to responding to economic challengers and preserving our nation’s global leadership.

Second, before COVID-19, arguably few widely relatable examples existed to demonstrate how fundamental education, childcare, and eldercare are to the smooth functioning of the economy. The coronavirus nevertheless laid bare the striking deficit in U.S. social infrastructure. To be sure, many of us have had intimate experiences with the education and healthcare shortfalls amidst the pandemic. Looking ahead, it is difficult to dispute how investments in these vital areas of the economy will be essential to creating and supporting a competitive and productive labor force for generations to come.

And speaking of productivity, the pandemic showed how efficient technological infrastructure can keep some workers engaged and how investments in next-generation technology (like 5G) might further boost worker output. At the same time, however, the healthcare crisis exposed the stark inequalities as many households fundamentally lack access to necessary technological infrastructure. Whether it's for school, work, or to register for a vaccine, the technology divide further reveals economic weaknesses that must be addressed if we are going to promote tools that benefit everyone in all aspects of our lives.

Will a deal get done?

So, will Joe Biden's American Jobs Plan make its way into law this year? Will a deal get done? Well, politics is fraught with uncertainty, and truly anything can happen in the coming months. However, what is certain are the shortcomings in our transportation, technological and social infrastructure amidst rapidly changing natural and geopolitical environments.

Indeed, Katrina exposed the inadequacies of our infrastructure amidst climate change while COVID showed us how a lack of social infrastructure investment might put one of the most technologically advanced economies at risk of leaving its citizens, and truly, the nation as a whole, behind. The implications of these glaring disparities and shortcomings are today harder to ignore and might be reason why, after decades of fits and starts, politicians from both sides of the aisle may defend spending large sums to finally get a deal done.

Are Vaccine Hopes a Shot in the Arm for the Markets?

Financial markets have posted notable gains month to date. And market optimism concerning the US elections has been amplified this week by hopes for a COVID vaccine. A key question for investors now is whether news of a vaccine will be enough to push risk assets higher through year-end, even as accelerating COVID infection rates threaten an already fragile economic recovery.

Without a doubt, the news of a means to quell the spread of this year's deadly virus is a positive development for our healthcare system, our economy, and the markets. However, of particular concern remains production and distribution obstacles related to getting the vaccine out to those who need it most. These enduring questions mean that the healthcare crisis is likely to intensify before it gets better.

Even so, we believe that the recent vaccine news combined with prospects of a concerted national response to the pandemic and potentially trillions of dollars in additional fiscal spending signals that light is beginning to shine at the end of the tunnel. If hope holds out, and the economy largely remains open, then the current market rotation into cyclical sectors could continue ahead of an economic recovery next year.

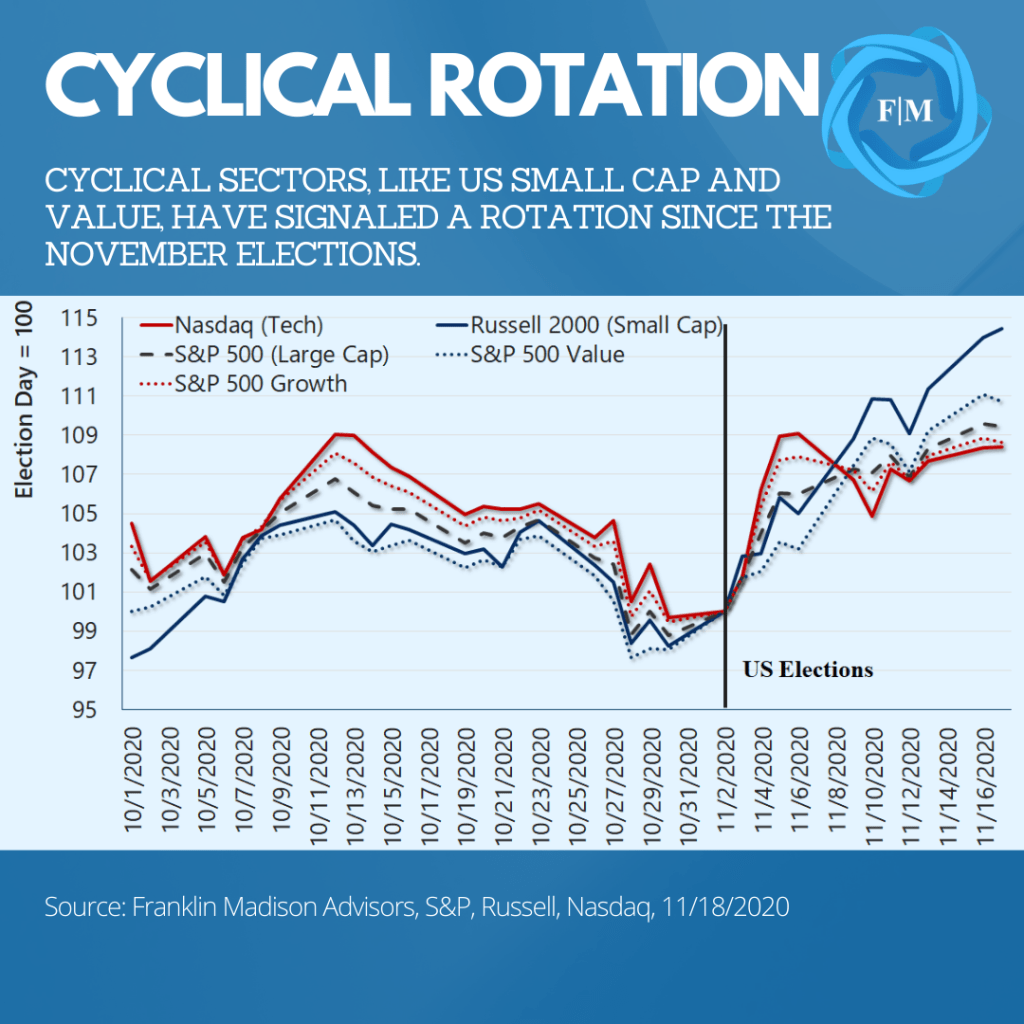

Figure 1: Cyclical Market Sectors Have Benefited in Recent Months

A Rally on Vaccine News

Markets moved higher this week on news of successful COVID vaccine drug trials announced by several large drug companies. These companies reported that their vaccines showed a more than 90% effective rate, which signals that, once the drugs become widely available, the spread of the coronavirus could be curtailed as soon as the second half of next year. With global cases topping 55 million this week, top US healthcare advisors estimate that between 75% to 80% of Americans might need to receive these vaccines to stop the spread of the deadly virus.

Production Issues

While markets indeed have rallied on the vaccine's positive news, the reality is that three key challenges stand between the end to the pandemic and a full-throated economic recovery. First, consider the production issues. One of the large drug companies recently announced that it might have as much as 50 million vaccine doses ready by the end of this year. Now keep in mind that each patient requires two doses of the vaccine to ensure immunization.

And assuming that the other drug companies that have also signaled successful trials can produce a similar quantity, we could see vaccine production reach 100 million doses to treat 50 million individuals every two months. While these production figures are considered optimistic, if we assume that only 80% of Americans need to be vaccinated, then there might be enough of the drug produced to help stem the virus's spread by the summer of 2021.

Distribution Bottlenecks

Now, production is a crucial first step to ending the pandemic, yet the next issue we'll likely contend with is the logistics of getting the vaccines to the right people. To this point, the drugs need to be stored at between negative 1- and negative 100-degrees Fahrenheit to ensure that they'll remain effective. While one company has developed a unique workaround to transport the drug, its solution will likely create a bottleneck in the vaccine's widescale distribution. This limited distribution means that receiving a vaccine probably won't be as simple as walking into your local pharmacy to get a flu shot.

Administration Fatigue

Finally, there's the challenge of handling and administering the vaccine and the potential that mishandlings could affect the stated 90% effective rate. Traditionally, drug testing occurs in highly controlled, structured environments.

However, distribution will take place in real-world settings, where anxiety surrounding the virus remains high, healthcare systems strained, and doctors and nurses burnt out and overwhelmed. Mistakes are likely to occur during vaccine administration, potentially questioning the 90% efficacy rate of the drug treatments. What’s more, while an inoculation rate of 75% to 80% could help stem the COVID spread, polls suggest that a large part of the US population is still unwilling to receive the drug. This fact alone could delay the benefits of administering the vaccine.

Even with these factors in mind, some market participants remain optimistic that the potential issues related to manufacturing, distribution and administration of the vaccine will be overcome. When this happens, social distancing measures likely will ease and struggling businesses could have a fighting chance to stage a comeback. It’s this optimism that arguably appears to be priced into the markets. That is, the potential for a sustained economic recovery, assuming that concerns about COVID begin to fade into the second half of next year.

Figure 2: US Coronavirus Infection Rates Hit Record Highs in November

Market Sentiment Cautious on a Likely Rebound

Make no mistake, markets likely will contend with COVID related issues for the entirety of 2021 and potentially beyond. Of particular concern at the moment is the rapid rise in infection rates taking hold in the US and around the world.

Infections Still a Near-term Economic Concern

This week, data from the Johns Hopkins University showed that daily average infection rates topped 160,000, besting peak infection rates reported during the summer months. This rapid rise in the coronavirus’s spread has recently led to renewed stay at home advisories, school closures, and limits on dining and social gatherings across the US. While a full lockdown of the US economy is not yet in the cards, these measures enacted at the local level could dampen the modest economic recovery that has unfolded over the past few months.

As it relates to infections, the prospects of a harsh winter arguably has been baked into many economists' GDP forecasts for the year. Expectations are set for the US economy to post a gain of roughly 4% in the fourth quarter as consumer spending and construction activity underpin growth.

This positive sentiment is playing out in the markets today. This optimism is arguably evidenced in a rotation away from the market's liquidity-oriented sectors toward a preference for pro-cyclical sectors that historically tend to do well in the early phases of an economic rebound.

Nevertheless, a key risk for the markets now is how quickly the resurgent infection rate can be quelled and what, if any, additional economic impact might come from various stay at home advisories and limited business operating hours.

Looking ahead, an incoming Biden administration focused on broad measures to address the healthcare crisis likely will give business leaders greater confidence in a durable solution to the virus's spread. What's more, the issue of another economic relief package is not a matter of "if," but "when," and this potentially could help prevent the economy from slipping further into a recession.

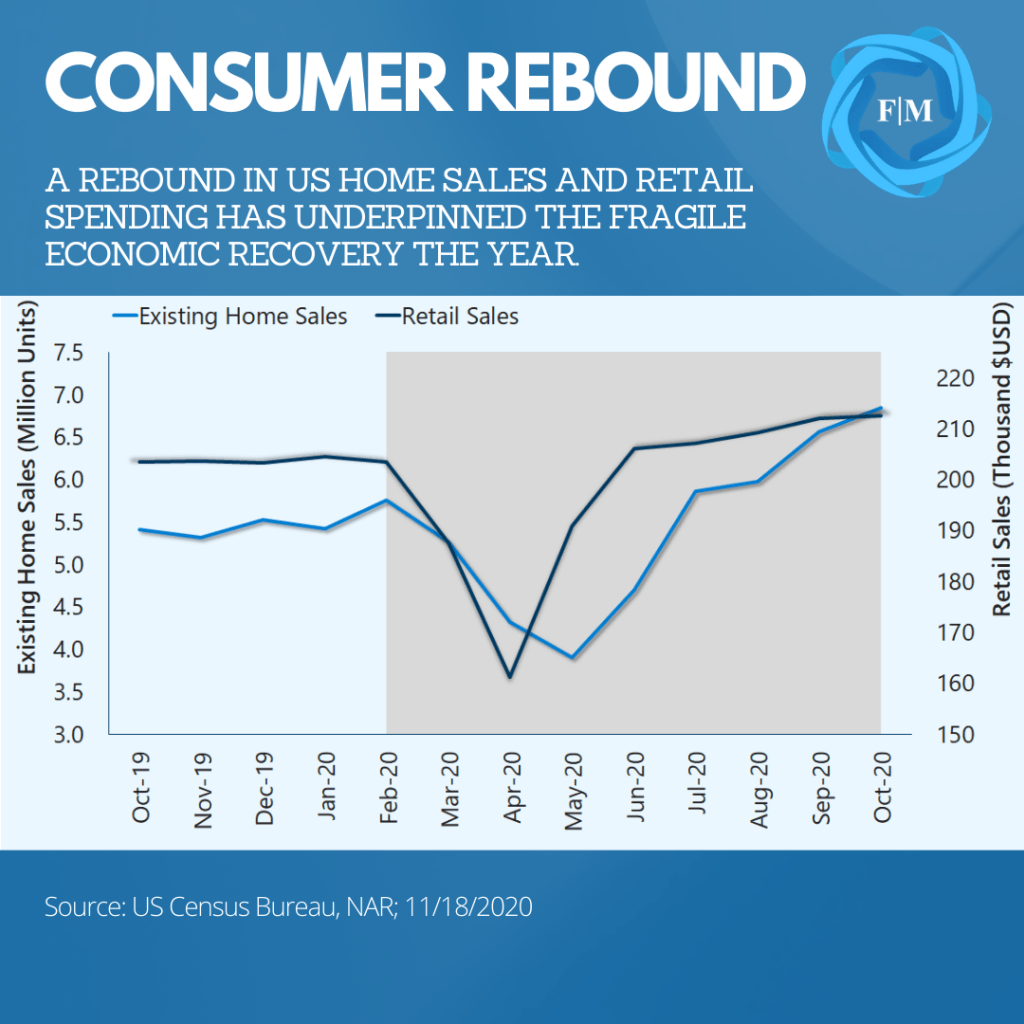

Figure 3: US Consumers Contributing to Stabilizing Economic Growth

Pricing in an Economic Recovery

From this vantage point, clarity around a vaccine, a concerted response to the healthcare crisis, and more fiscal spending may provide the markets with hope that the economy likely will recover even as near-term concerns (like rising infection rates) continue to surface.

Certainly, incoming economic data suggest that the US economy is on the mend. Business sentiment has stabilized recently, and hiring activity has somewhat improved, as evidenced by a declining unemployment rate even as weekly jobless claims remain stubbornly elevated. Consumer confidence is also steadying and evident in solid retail sales and a surge in demand for home purchases.

Cyclical sectors of the markets (those that move in tandem with the economy have benefited from an improving economic narrative and greater post-election policy clarity. These sectors include US small-cap and value-oriented stocks and a weaker US dollar that has led to gains in emerging markets. As the US economy recovers, this rotation could likely overshadow the liquidity theme that supported gains in the work-from-home and the Fed’s money printing theme that has benefited the tech sector.

To be sure, as we pointed out in last month's report, a Biden win and the prospect for higher levels of government spending has set the stage for a pivot towards cyclically oriented sectors of the markets. This view has played out in small-cap and value stocks outperforming tech in the weeks following the elections (see figure 1). Looking ahead, we anticipate this trend to continue as lingering election uncertainties fade, inauguration day passes, and business and consumer confidence steadily improve.

Are Vaccine Hopes a Shot in the Arm for the Markets?

While there is a genuine reason for markets to be optimistic about a COVID vaccine, the very real risk today is that infection rates in the US and around the globe will continue to rise. Local leaders are walking a fine line between enacting more stringent safety protocols and shuttering businesses altogether. To this point, the Fed indicated the real potential for a double-dip US recession if infection rates aren’t mitigated soon. And if this happens, the market’s appetite for cyclical investments might come to a pause.

Nevertheless, this week's vaccine news combined with prospects of a concerted national response to the pandemic and potentially trillions of dollars in additional fiscal spending in the months ahead signals that light is beginning to shine at the end of the tunnel. If hope holds out, and the US economy largely remains open, then the current market sentiment driving a rotation into cyclical sectors could continue ahead of an economic recovery next year.

Has the US Dollar Lost its Dominant Reserve Currency Status?

Is US dollar dominance poised to end, and what might it mean for your finances? Uncertainties surrounding US dollar strength have been top-of-mind for some individuals for many years and for a good reason. A significant decline in our nation's currency could lead to higher prices for the goods and services you consume and make it more expensive to borrow money for big-ticket purchases like a house or a new car.

Today, there is a sensible argument to be made for a diminished worth of the US dollar. Ballooning government borrowing, massive central bank money printing, and the decline of US geopolitical influence suggest to some that the end of the dollar's global dominance may have finally come. Some individuals even point to a near-term rise in gold prices and a falling exchange rate as evidence for such a move.

That being said, the dollar's role is more nuanced than such simple near-term explanations would presume. For now, evidence suggests that the dollar's prominence is likely to remain in place for many years to come. Even so, the growing importance of the euro and Chinese yuan over the long-term could reduce the world's dependence on the dollar. So, what does this mean for your money? A structurally weaker US dollar might lead to higher future living costs and is a vital reason why your savings should account for rising inflation.

Making Sense of Foreign Exchange Market Moves

Is the US dollar in decline? One indicator that some individuals use to signal a fall in the dollar is recent foreign exchange market activity. Between March and August of 2020, the dollar, as measured by the US Dollar Index, lost 9% of its value. At the same time, gold prices pushed past record highs. And these combined moves might suggest that something ominous is happening with the US dollar. While it's tempting to extrapolate near-term developments into the future, let's look at what history has to say about the dollar's movements.

From a purely data-driven perspective, history has shown that periods of US dollar weakness are often preceded by strength, especially during crisis times. In the months leading up to its March 2020 highs, the US dollar rose in value versus its key global trading partners. This move occurred as individuals and institutions piled into perceived safe have US assets as coronavirus uncertainties weighed on the global economic outlook.

Certainly, during times of financial stress and economic uncertainties, the US dollar is often sought after as a globally secure destination to park savings. This ebb and flow in value is not unique to 2020. In fact, it is evident in prior crises, like in March 2009, amidst the Great Recession and during the popping of the Tech Bubble in 2001. In fact, after appreciating in 2008 and early-2009, the US dollar gave up 13% of its value in the five months following stock market lows in March. And in 2001, even with the events surrounding September 11, the dollar trimmed 4% of its value during the year.

The point here is that a dollar decline today might coincide with legitimate concerns about massive fiscal and monetary spending. Even so, correlation should not be confused with causation. Instead, one way to look at the recent dollar moves is from the perspective of a safe-haven currency. When economic and geopolitical uncertainties rise, there is greater demand for the safety of the US dollar. Today, it can be argued that movements in the foreign exchange market reflect less demand for US dollars as global market participants look past economic uncertainties.

What Makes a Global Reserve Currency?

If we presume that dollar fluctuations in foreign exchange markets are consistent with near-term risk-on/risk-off trends, what then can we make of the US dollar's role as a preeminent reserve currency? In other words, why wouldn't market participants look to the euro or Chinese yuan as dollar-alternatives during times of uncertainty? In its simplest form, there are generally three factors that make a currency a dominant global reserve: 1) it's used to settle foreign financial obligations, 2) a means to pay for international trade, and 3) as a store of value.

Settling Foreign Obligations (Liquidity)

It's often assumed that central banks print money out of thin air. The fact is that financial institutions are primarily responsible for affecting money supply in circulation. This occurs as banks take in deposits and issue loans. One factor that has propelled the dollar into its global reserve status is how financial institutions outside of the US have issued US dollar-based loans. We refer to these dollar-based foreign obligations as Eurodollars.

While the term was originally coined to represent dollar-based borrowing in a post-World War II Europe, today it applies to US dollar-based obligations in other parts of the world. Experience tells us that interest is often paid back to a lender on top of the principal owed when we borrow money.

Foreign individuals and firms earning money outside of the US might need to convert their own local currencies in exchange for US dollars to make their lenders whole. And by some estimates, today there well over $10 trillion is Eurodollar deposits outside of the $18 trillion in the US financial system. Taken together with loans issued by the International Monetary Fund, the World Bank and Asian Development Bank the dollar is a key source of liquidity for the global financial system.

Use to Settle Global Trade (Size)

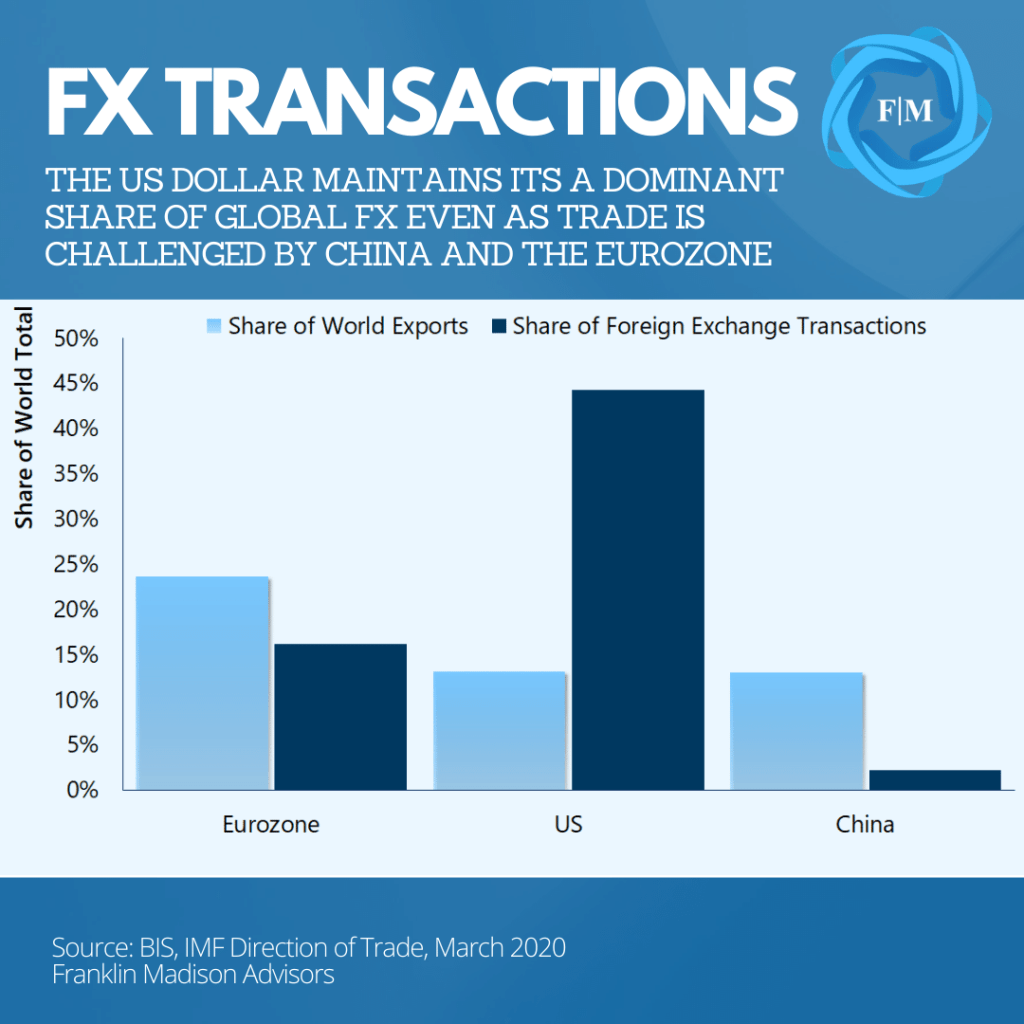

Another factor that distinguishes a global reserve currency is its use to settle trade in international goods and services. In the post-War era, the US was a dominant leader in global trade, given the fact that it was essentially the last major economy standing. In the decades since the Eurozone has become one of the world's largest trading powerhouses and China has risen in prominence as an essential exporter of global goods. Even so, data continue to show that the lion's share of world trade is settled in US dollars.

According to data from the Bank for International Settlements, foreign exchange transactions in US dollars were nearly three times higher than the euro. Indeed, even as China has risen to be a key leader in terms of global trade volumes, the use of the yuan in foreign exchange markets remains a mere fraction compared to the US dollar’s use.

Looking beyond manufactured goods, essential commodity items like gold, oil, and soybeans contracts are largely priced and settled in US dollars. The point here is that buyers and sellers of goods and services globally affect millions of transactions that follow through foreign exchange markets every year and remain overwhelmingly reliant on the US dollar.

Store of Wealth (Stability)

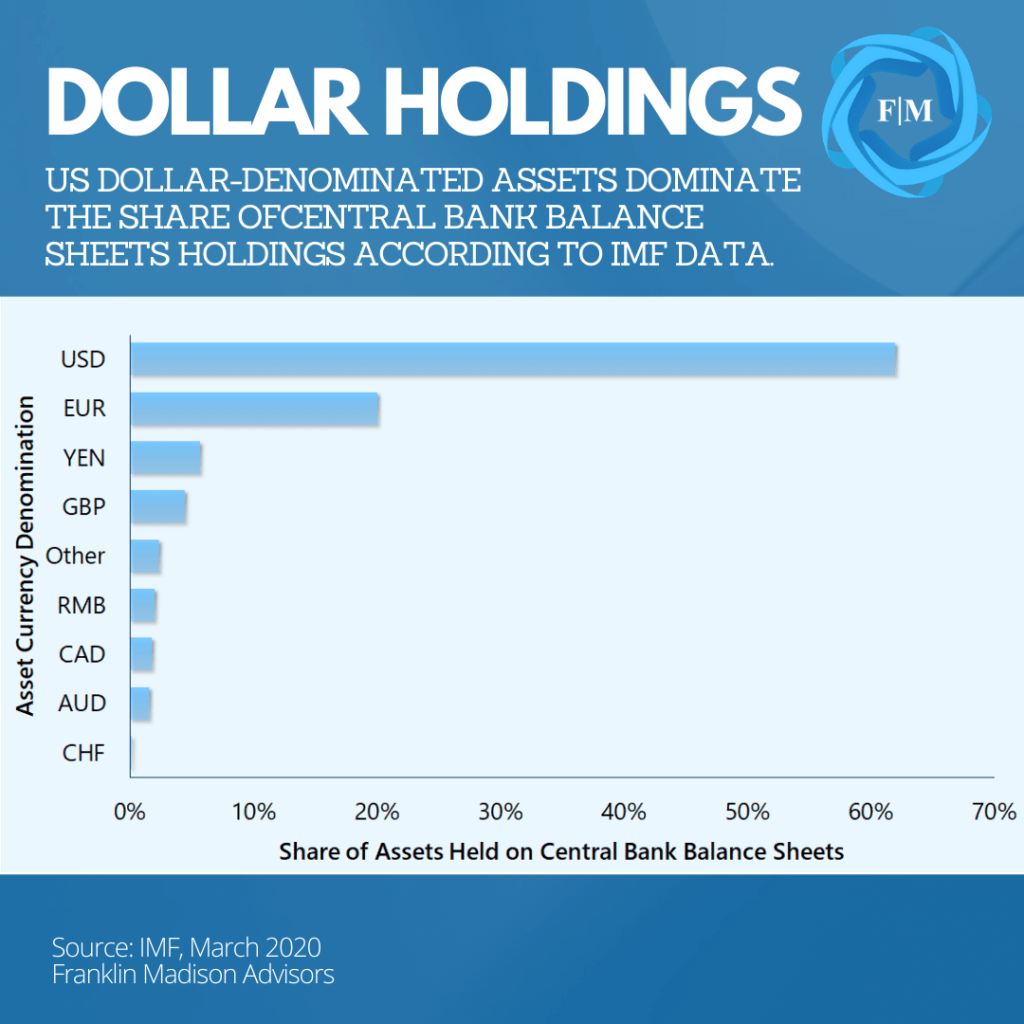

A third factor that makes a global reserve currency is in its perceived ability to store wealth. Put differently, holders of a currency must have a strong belief that its value will remain generally stable over time. Strength in a country's economy, government, and monetary system all contribute to the collective perception of stability underpinning a country's currency.

And despite a number of developments over the past decade, the fundamental factors underpinning the US economy, its government institutions, and monetary system remain on solid footing compared to other global alternatives. To be sure, it's this stability in growth and governance that has led to demand foreign capital flows into US markets and a still outsized demand among foreign central banks for US reserve assets.