Early Retirement: Don’t Make these Five Mistakes

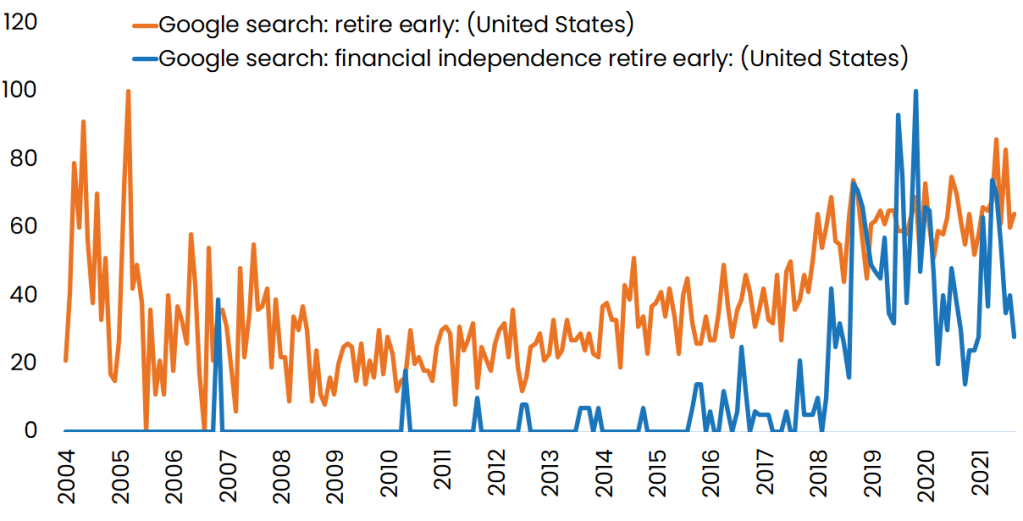

Handing in a resignation letter and walking away from an unfulfilling career may be one of the most satisfying acts in an individual's life. By some measures, there are an increasing number of satisfied people in the world today. Indeed, recent accounts increasingly show that people are leaving their jobs in droves. These developments are evident in articles about quit and vacancy rates and even rising Google Search trends for early retirement. To be sure, one study found that COVID has prompted a growing wave of early retirements, especially for people who had not planned to quit their jobs but are now thinking of doing so. Can you relate?

Maybe your investments have performed solidly over the past 18 months, and now you have the financial resources and confidence you need to pull the trigger and finally step into financial independence. Maybe your company has recently gone public, and you've come into a large financial windfall that has set you up for early retirement. Or, perhaps you've had time to consider whether the work you're doing today truly aligns with what matters most to you in your life.

Whatever the case may be, now could finally be the time for you to take the next steps towards early retirement. But before you walk into your boss's office and hand in that resignation letter, you'll likely want to consider some potential pitfalls that might derail your financial independence early retirement plans. Indeed, not thinking through some crucial early retirement mistakes could leave your financial goals falling short.

Here are five financial mistakes that you'll likely want to avoid as you take your next step towards becoming the master of your financial independence journey:

Mistake #1: Underestimating your retirement cash flow needs

Let's assume that you're 45 years old, have saved one million dollars, and are now ready to pull the trigger on early retirement. If this is you, I'd like to give you a round of applause because, according to a study from Fidelity, the average 401k balance for an individual in their forties is roughly $93,000. So, if you've accumulated one million dollars by this age, you're well ahead of your peers. But will this savings be enough to cover your lifestyle expenses if you decide to retire tomorrow?

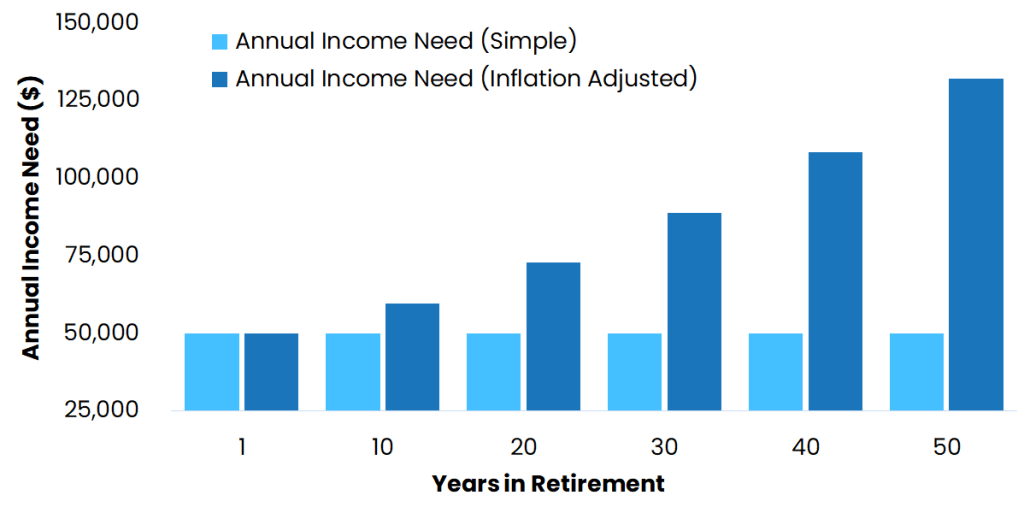

Let's take a look at an example to understand when a million dollars may not cut it when it comes to covering your retirement cash flow needs. First, if we assume that you'll need $50,000 per year to keep the lights on and allow you to enjoy your current lifestyle and your investments grow by about five percent annually, you should be fine, right?

Well, one problem with this assumption is that your living expenses will stay fixed at $50,000 annually over the next half-century. Realistically, however, your cost of living is likely to creep higher by an average of 2% per year. Rising inflation means that the lifestyle that costs you $50,000 today could well rise to over $130,000 in 50 years. At this rate, your million-dollar savings could be wiped out well into retirement if specific lifestyle changes aren't made today.

Therefore, if you're trying to determine whether a million dollars or any amount for that matter is enough to retire early, start by figuring out what your inflation-adjusted household expenses may be throughout retirement.

This analysis involves developing realistic expectations for your lifestyle spending in the years ahead, evaluating the effects of inflation on your annual income needs, and setting some realistic expectations about your investment return rate. Only then can you determine with some certainty whether the nest egg you have today is enough to cover your living expenses for the rest of your life.

Mistake #2: Relying solely on your 401k or IRA for early retirement

Another mistake that some early retirees make is concentrating their savings in qualified accounts and not putting enough away in taxable investment accounts. Why is this a problem? Well, with some exceptions, money in a qualified account, like a 401k or IRA, won't be available penalty-free until you reach age 59 ½.

So, if you're 45 years old, ready to retire early, and have all of your savings tied up in a 401k, your options likely will be limited when it comes to using your savings to cover everyday expenses. That's because tapping your qualified savings early could lead to a host of penalties that could otherwise derail your best laid financial plans. How can you ensure that you're prepared for early retirement without incurring unnecessary costs?

One option is to save enough money in a taxable account to cover your living expenses until you can begin safely drawing down money from a 401k or IRA at 59 ½. So, how much money should you have saved up in each type of account?

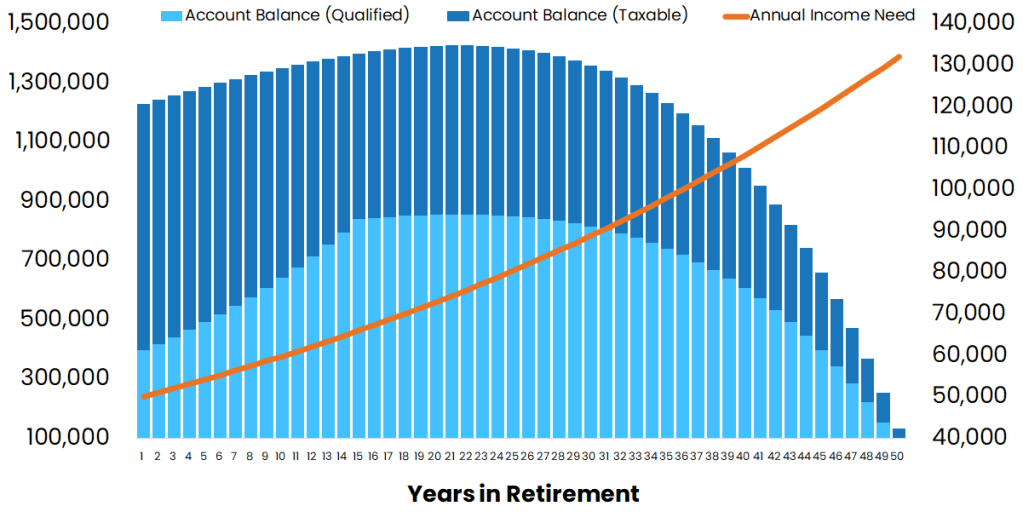

Well, let's assume that you're 45 years old and plan to spend $50,000 per year on living expenses, inflation-adjusted over the next 50 years. Based on several simplified assumptions, you'll likely need to have saved 1.3 million dollars before you quit your job. Two-thirds of that amount (or about $830,000) should be in a taxable account to pay for day-to-day expenses.

The remaining amount of your retirement savings (about $400,000) should be spread across qualified accounts like 401ks or IRAs. As you draw down your taxable account early in retirement, your qualified accounts likely will continue to appreciate, untouched but for periodic contributions or rebalancing, hypothetically appreciating to a level of $850,000 by the time you reach age 59 ½. At that point, you can begin spreading living expenses between both taxable and qualified accounts.

Complex calculations aside, the key takeaway here is that the farther out you are from retiring at age 59 ½, the more of your retirement savings you'll need to have allocated to a non-qualified savings account. Not anticipating this mistake could derail your early retirement goal for quite some time.

Mistake #3: Dismissing social security benefits entirely

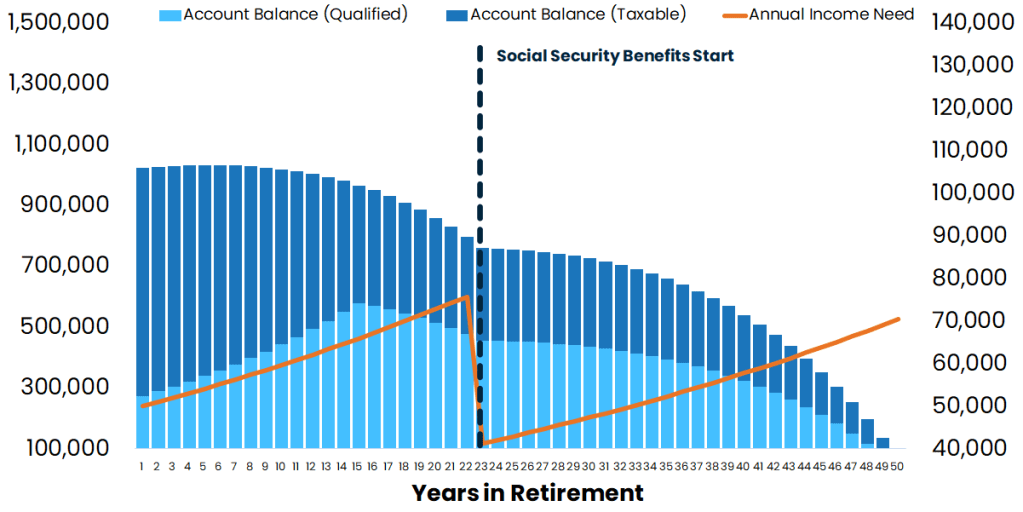

One financial planning component that many financial independence retire early (FIRE) proponents often overlook is social security's effects on how much you'll need to have saved for early retirement. For example, recall from our previous example that an individual might need $1.3 million to cover lifestyle expenses of $50,000 (inflation-adjusted) over fifty years. A $36,000 annual social security income benefit could reduce your investment savings need by about $200,000 starting at age 45 and put you closer to that $1 million savings target.

How? Let's take a closer look.

You'll recall that between various retirement savings accounts, we estimate that an individual with an income need of $50,000 per year, retiring at 45, would likely need about $830,000 in taxable accounts and $400,000 in their qualified accounts. Factoring in social security benefits starting at age 67, this same individual would likely need about $750,000 in their taxable account and $274,000 in their qualified accounts. The added social security benefit lowers the amount of money drawn down from retirement savings in later years, naturally reducing the total amount of money that needs to be saved before quitting their job.

The good news is that making one million dollars work for retirement is feasible, so long as the savings are spread across the proper accounts, and social security benefits kick in as expected. So, how can you determine the social security benefit amount to use in your financial projections? One of the simplest ways to obtain this number is to visit https://ssa.gov/myaccount. Here you'll be able to get a copy of your social security benefit statement, which outlines your projected future benefits based on what you've already paid into the system.

But what if you're 45 years old today, and you expect that social security will go broke by the time you start drawing down benefits twenty years from now? This concern certainly is legitimate. Even so, it's possible that being such a politically sensitive topic, lawmakers won't let the social security program die entirely. Even so, the further you are away from receiving projected social security benefits, the more of a discount you'll likely want to apply to projected future income benefits as a way to account for uncertainty related to the program.

Mistake #4: Forgetting to factor in healthcare expenses

So, you're 45 years old, in good health, and doing everything right to take care of your body and mind. You exercise regularly, eat a balanced meal, and take your vitamin supplements daily. You don't have any health concerns right now and expect to live a long life. Why should you care about potential healthcare expenses?

Well, what happens if your health situation unexpectedly changes somewhere down the road, say in 10 years or so. Indeed, the events of 2020-2021 have taught many of us that our health, no matter how hard we try, can be drastically affected by circumstances entirely out of our control.

Add to this the fact that the cost of medical care has been outpacing the average level of inflation for years. From this perspective, if you're not building in rising healthcare costs into your financial independence early retirement plans, you could be setting yourself up for a big disappointment in the years ahead.

So, how do you know whether you're accounting for the right amount of healthcare spending?

To answer this question, you'll need to take time to think through the kind of care you will need in old age and account for their related costs. While medical expenses (like paying for insurance premiums) may only constitute a sixth of your early retirement income need at age 45, by the time you reach age 70, those expenses could rise to a third of your income needs. And depending on your living situation, these numbers could increase to over half of your spending by your late 80's when considering expenses related to assisted or long-term care needs.

So, if we take a simple 6% appreciation in medical costs from age 45 and extrapolate it out through retirement, how does that affect our earlier projections? Recall that with social security benefits, your financial independence retire early savings need would be about 1 million dollars spread across taxable and qualified accounts at age 45.

When factoring in rising medical costs, you'd likely need to have saved an extra $300,000 at age 45 even after factoring in the bump from social security benefits. When accounting for rising medical costs, this time around, you'd likely need $870,000 in taxable accounts and $420,000 in qualified accounts compared to $750,000 and $274,000 in our previous example when you begin early retirement.

Again, the key consideration here is ensuring that you'll have enough saved to cover unexpected medical expenses when you're healthy while being prepared for the unexpected over the long term. Without employer medical coverage, you'll need to be prepared for private healthcare coverage, which you can purchase in your state's insurance marketplace. You can visit healthcare.gov to get a better sense of the options available to you. Either way, no matter how healthy you are today, don't make the mistake of being unprepared for some form of medical care that you'll likely need in the decades ahead.

Mistake #5: Not giving your money a purpose

One final but a fundamental mistake that some individuals who retire early make is not having a purpose for their money. These individuals often have one goal, and it's simple: save money so you can quit your job. But then what? If your goal has been to live frugally and save every penny so you can leave the workforce but don't have a purpose for life after that, then what's this journey been about?

For many of us with financial independence retire early (FIRE) aspirations, these qualitative, squishy questions may seem irrelevant at face value. You may say, "I already know how much I intend to spend." Or "I'm content with my life today; nothing will change." But honestly, how can you be so sure? Many of us don't know where our lives will take us a year from now, let alone a decade or half-century from now.

One analogy that we use when discussing an individual's finances is to think about it as a home divided into two parts. The right-hand side of the house defines the financial resources and tactics used to make retirement a reality. In other words, it encompasses a lot of the items that we discussed here today: tactics.

However, the left-hand side of the home defines your values, your relationship with money, and your life goals in retirement. In order words, it contains the elemental component: strategy. It represents, "where is my life headed, and what's all this money for?"

The point here is to spend time thinking about the general direction you'd like your life to go. One analogy that we often share is that of taking a flight from Los Angeles to New York. A pilot's five-degree navigation error at the start of the journey could put the plane thousands of miles off course when it reaches the East Coast.

Giving your money purpose will take some deep thought, and at times involve having uncomfortable conversations and thinking through some harsh realities. But in the end, the outcome produces greater clarity and direction for your money's use. At the same time, if you do plan to retire at age 45, it can help you define exactly how much savings you'll need to cover your lifestyle expenses over the next 50 years.

Avoiding Early Retirement Mistakes

Before we wrap things up, we need to talk about one of the biggest mistakes individuals aspiring for financial independence retire early make: blindly following the four-percent rule. A lot has changed since this concept was introduced nearly 30-years ago, and, quite frankly, this approach to calculating how much money you need to retire early is likely outdated.

To be sure, financial markets, central banks, and government policies have fundamentally changed since the four-percent rule was introduced in 1994. So, what can you do to ensure that you've saved the right amount of money for retirement to maximize your chances of avoiding a savings shortfall? First, start by spending the time to think through what you want your post-career years to look like. Ultimately, answer the question, "what is this money for?"

Next, think about how you expect your lifestyle spending to change over the coming years and decades while being mindful that inflation will create a greater demand on your savings. Here again, you'll want to ensure that your financial plan is realistic regarding income needs as prices rise, even if you don't anticipate a significant change in lifestyle spending today.

Then, be sure that you've put enough money away in savings accounts that you can access today. Recall that qualified accounts, like a 401k and IRAs, aren't accessible penalty-free until age 59 ½. Therefore, you'll want to have money socked away in taxable investment accounts to cover living expenses before tapping your retirement savings.

Finally, consider how social security benefits and medical costs will impact your overall income drawdowns, and more broadly, your retirement savings needs for the long-term. Recall that factoring social security benefits into your income projections could cut your retirement savings need at age 45 by hundreds of thousands of dollars. At the same time, not preparing for unforeseen healthcare concerns could leave you with unexpected medical expenses not accounted for in your savings plan.

Are you ready to quit your job and live life on your own terms? While you might think you have enough money saved today, one way to ensure that your retirement savings are on the right track is by avoiding some common early retirement mistakes. While calculating your retirement need is no simple task, it nevertheless highlights a key reason why developing a financial plan is an essential component of early retirement preparation. Indeed, doing the work today could maximize your chances of success for the long term and help you finally become the master of your financial independence journey.

Four Ways to Set Your Retirement on FIRE

Retiring early is an aspiration that many individuals can get excited about. Vicki Robin and Joe Dominguez, in their best-selling book, “Your Money or Your Life”, arguably introduced the concept of early retirement to the mainstream culture decades ago. Today, thousands of individuals are actively pursuing their goal of becoming financially independent and quitting their nine-to-five grind.

According to one Gallup study, individuals in their early 20’s were generally optimistic about their ability to save for retirement before age 60. However, those same individuals curbed their early retirement enthusiasm when later surveyed in their 30’s as savings and other lifestyle realities made it increasingly clear that early retirement might just be an elusive goal.

Even so, data from Hearts & Wallets suggests that one out of every six Americans surveyed by the group expects to retire before the age of 55 - ten years sooner than the standard retirement age of 65.

This data illustrates one key point when it comes to the concept of retirement: individuals across all walks of life increasingly want to start the journey to become financially independent and retire early, rather than walking down the path of a traditional retirement later on in life. To be sure, retiring early has become so popular that it’s even earned its own name: the FIRE movement.

So, what is FIRE? Well, the acronym FIRE stands for ‘financial independence, retire early,’ and the goal is to create an opportunity where you can stop chasing an unfulfilling career and live life on your terms without being tied down to the demands of a full-time job. Many individuals have accomplished this goal by living frugally through their working years, carefully planning out their finances, and prioritizing saving and investing over other frivolous lifestyle activities.

Does becoming financially independent and retiring early sound appealing to you? And how would it feel to hand your boss a resignation letter today, knowing that you would be financially set to live your best life however you choose tomorrow? If you’re in the camp that’s excited about early retirement but not sure that you can commit to a restrictive savings plan, you can take heart knowing that there are several options for achieving FIRE. Certainly, the idea of retiring early may seem like a pipe dream to some individuals. Still, with proper planning and the determination to make it happen, early retirement may be closer than you think.

Understanding the FIRE Movement

Now some individuals might get the impression that in order to achieve FIRE, one must live a spartan lifestyle and disown nearly all earthly pleasures. While such an approach may work for some individuals, the truth is that we all have varying degrees of tolerance for postponing consumption today so that we can save for tomorrow. That’s why over the past couple of decades, some individuals have developed a few different ways to achieve financial independence. These include traditional FIRE, LeanFIRE, FatFIRE, and Barista FIRE.

Let’s first talk about traditional FIRE.

Traditional FIRE

So, what is traditional FIRE? Well, it’s the most basic way to achieving financial independence and retiring early. The concept is simple: identify your early retirement goals, calculate your financial independence number, then save as much of your income as possible. Traditional FIRE is centered on the idea of acquiring enough income-producing assets, like financial investments or rental property to produce a steady stream of income to cover living expenses for the rest of an individual’s life.

Achieving FIRE along this path often involves living a somewhat traditional lifestyle while finding ways to save a large portion of money received from a traditional job. An individual pursuing a traditional FIRE journey often has already achieved contentedness with their current lifestyle. That’s why their goal is to focus their financial efforts on building up a nest egg that will help them maintain their current lifestyle for the rest of their lives.

LeanFire

Another way to retire early is by LeanFIRE. Its very name suggests that this approach takes a more modest, frugal path to early retirement and requires living with a bare minimum budget in your current lifestyle, as well as in retirement. Many households in this camp earn six-figure paychecks but spend only a fraction of their income to cover living expenses. LeanFire is a genuine commitment and takes a different kind of mindset compared to the traditional FIRE path.

In fact, individuals pursuing this path often develop a minimalist mindset, finding ways to live off of less than $40,000 per year while developing a savings strategy centered around their financial retirement number. For example, Joshua Fields and Ryan Nicodemus, who dub themselves “The Minimalists”, claim to have helped over 20 million people live meaningful lives by choosing to reevaluate their relationship with material wealth.

Now, this path to FIRE may not be for everyone because it requires an individual to challenge their emotions and mindset to live a life well below their potential means. Nevertheless, LeanFIRE is still an attractive option because it provides one of the most accessible and quickest paths to early retirement.

FatFire

Next up, we have FatFire. How is FatFire different from LeanFire? Well, in many ways, FatFire is the opposite of LeanFire. FatFIRE might be appealing for those individuals who can appreciate the finer things in life and would like to use their savings to experience a more extravagant retirement lifestyle. Retirement income goals for individuals in this space typically start at around $100,000 per year. Individuals taking the FatFire path are often high earners who spend their early years balancing quick career progression, a commitment to a disciplined savings strategy with acquiring that house by the lake or all the toys they’d like to enjoy in retirement while having the opportunity to travel when they’re finally able to quit their jobs.

This approach typically requires more time to attain FIRE, but can make early retirement more enjoyable than LeanFIRE, which generally requires living on the bare necessities. The idea here is to acquire financial and lifestyle assets that produce an income capable of covering your minimum living expenses while allowing you some room for additional spending as your lifestyle permits.

Barista FIRE

Now, similar to LeanFIRE, Barista FIRE focuses on living a minimalist lifestyle, acquiring revenue-producing assets, and counting on a side hustle to supplement your lifestyle income. With Barista FIRE, there’s less pressure to save money like a minimalist. Additionally, one often overlooked need for individuals on their journey to financial independence, and early retirement is covering the cost of healthcare. While insurance marketplaces have improved accessibility, paying for medical coverage, especially for a family on the FIRE path, can be rather expensive.

One thing that makes Barista FIRE attractive is the ability to work a less demanding job while having access to affordable medical coverage available through an employer-sponsored benefits plan. Additionally, this path can help ensure individuals earn the 40 Social Security credits they need to become eligible for government retirement benefits, like Medicare and Medicaid. Barista Fire is increasingly becoming a more common alternative to LeanFire, given that the idea is to have enough money saved and invested that you can quit your full-time job all the while working a less demanding side hustle that can help you cover some monthly expenses.

Planning for Early Retirement

Whether you want to live lavishly or are comfortable living a spartan lifestyle, the path of financial independence and the FIRE movement essentially comes down to living life on your terms without being tied down to an unfulfilling job. And achieving this end almost always requires a little bit of planning.

So which path to FIRE is right for you? Well, just like planning for retirement at age 65, to achieve FIRE it’s essential to define your near- and long-term lifestyle goals while at the same time having a clear understanding of your current financial situation. Doing so will help you determine what steps need to happen first and what actions you need to prioritize.

The most significant difference between planning for traditional retirement and planning for FIRE is the time horizon. This means that to retire early, savings rates and investment contributions need to be maximized as soon as possible so you have enough money invested to draw income from.

Now, determining how much money you need to have saved can be a challenge. That’s why in 1994, retired financial advisor William Bengen established a savings guideline called the 4% rule. This rule suggests that if you have 25x your annual living expenses saved, you can withdraw 4% from the portfolio and not run out of money for 30 years.

So, for example, if you need $75,000 per year to cover your lifestyle expenses in retirement, you’d need approximately $1.9 million saved and invested. This $1.9 million is what many in the movement would consider your financial independence number.

Now, rules of thumb are a good place to start. Realistically, however, you’ll likely need to make some modifications to the 4% rule. For example, you’ll likely need to account for a retirement time horizon greater than 30 years, varying inflation levels, life expectancy changes, variable spending, and rising medical costs as part of inputs to calculate a more accurate financial independence number. That’s why it’s essential to develop a plan that’s tailored for your unique goals, values, and desired life outcomes.

Outside of being able to retire early, one of the most significant benefits of planning for FIRE is that it requires you to think about the kind of life you want to live. That’s what makes Vicki Robin’s and Joe Dominguez’s work so appealing for so many people. Too often, we fail to dream big and think about our future, but the exercise of planning for a post-employment life creates an opportunity to honestly think about what goals and experiences you want to accomplish in life.

Being able to retire early really comes down to asking yourself a few questions:

- What would my life look like if I didn’t have to work again?

- How soon do I want to be able to live such a life?

- What’s my financial independence number?

- What has to change in my life today to achieve this goal?

Once you get solid answers to these questions, you can begin working backward to determine the necessary savings rates and the action items needed to achieve FIRE.

How to Make It a Reality

While your lifestyle needs will play a significant role in deciding which FIRE path is appropriate for you, keeping expenses as low as possible while still maintaining a quality way of life is generally what makes FIRE possible. Based on the financial independence number you discovered in your planning sessions, you can then determine how much money needs to be saved each month and each year to hit that savings goal.

Even so, saving money is only a start to your financial independence journey. Investing is the most crucial piece of the FIRE puzzle because you need to put your money to work today so that it can quickly grow tomorrow. Depending on your situation, it’s generally recommended to make annual 401(k) contributions that at least qualify you for your employer match to take advantage of free money. At the same time, keep in mind that if you do plan to retire early, you’ll need a source of savings to draw on to avoid penalties from the IRS.

Being as debt-free as possible is also crucial to keeping expenses low and simplifying your lifestyle while in FIRE. Remember, investment income is a reward you pay yourself for being a diligent saver. Interest on debt is income you pay to someone else for lending you their savings.

Even so, if you find yourself needing additional income, working a side hustle during your years of accumulation can help supercharge your savings and may also prove to be a fallback source of income after taking a step off the corporate ladder.

The Takeaway

Whether we’re talking about LeanFIRE, FatFIRE or BaristaFIRE, the common denominator among these early retirement paths is to take cash earned today and convert it into future cash flows for tomorrow. Being financially independent with the ability to retire early is a dream that many people have. Even if you don’t desire to retire early, everyone can benefit from the fundamentals of the FIRE movement.

Planning out your future, being intentional with your spending, and investing for retirement are essential steps to evaluate whether you want to retire early or retire at the traditional age of 65. And that’s why working with the right financial planner can help you work through the numbers and build a plan to live life on your own terms, a reality.