Retirement: 8 Tests Before You Leave Your Paycheck Behind

Retirement shouldn’t begin with a guess.

Still, that’s effectively what happens when someone chooses a retirement date based primarily on the balance of an investment account.

The number may look substantial. The financial projection may show a high probability of success. And after decades of working and saving, it may finally feel like the right time to leave.

However, retirement readiness isn’t determined by one number.

Instead, it depends on whether the major pieces of your financial life can continue working together after your paycheck stops.

In our planning work, we don’t begin the retirement conversation by asking whether someone has reached a particular portfolio balance. We begin by looking at what the paycheck currently supports, what will replace it, and which financial decisions could put the most pressure on the plan after retirement.

That process usually requires more than an investment projection.

It requires a retirement readiness test.

Why Your Retirement Number Isn’t Enough

Most people begin with a straightforward question:

Do I have enough money to retire?

That’s an important question. However, it’s also incomplete.

Two couples could each have $4 million saved and have very different levels of retirement readiness.

One couple may have no debt, predictable spending, substantial taxable savings, two pensions, and both spouses already enrolled in Medicare.

Meanwhile, the other couple may have a large mortgage, most of its wealth in tax-deferred retirement accounts, several years to go before Medicare, and ongoing financial responsibilities for parents or adult children.

The account balances may be identical.

Nevertheless, the retirement decisions aren’t.

That’s because a portfolio can tell you how much you’ve accumulated, but it can’t tell you whether your spending is realistic, whether your tax strategy is coordinated, or whether your family is prepared for an unexpected health or caregiving event.

So, before choosing a retirement date, we believe the plan should pass eight readiness tests.

Test 1: Do You Know What Retirement Will Actually Cost?

First, you need a dependable estimate of what you’ll spend.

That sounds simple. Yet, in practice, it’s often one of the least developed parts of a retirement plan.

Many households know approximately what comes out of their checking account each month. However, that number may not include irregular expenses such as travel, home repairs, vehicle replacements, financial support for family members, or large insurance premiums.

Additionally, retirement spending rarely remains constant.

During the early years, you may spend more on travel, hobbies, dining, or home projects. Later, those expenses may decline while healthcare, home assistance, or caregiving costs increase.

As a result, one static spending assumption may not adequately describe a retirement that could last 25 or 30 years.

When we review retirement spending, we separate expenses into three broad categories:

- Core expenses are the costs required to maintain your household, including housing, utilities, food, insurance, and basic healthcare.

- Lifestyle expenses include travel, entertainment, gifts, hobbies, and other discretionary spending.

- Contingent expenses are costs that may not occur every year but still need to be planned for, such as major home repairs, helping an aging parent, or replacing a vehicle.

This distinction matters because each category has a different level of flexibility.

If markets decline, you may be comfortable postponing a large trip. However, you probably won’t be able to postpone property taxes, health insurance premiums, or a new roof.

Therefore, the first readiness test isn’t whether your portfolio can support one spending number.

It’s whether you understand which expenses are essential, which are flexible, and which could surprise you.

Test 2: Do You Know What Will Replace Your Paycheck?

Once spending is clear, the next step is mapping out your retirement income.

That may include Social Security, pensions, investment income, retirement account withdrawals, rental income, deferred compensation, or part-time work.

However, income planning isn’t simply a matter of adding those sources together.

Timing matters.

For example, you may retire several years before claiming Social Security. A pension may not begin immediately. Deferred compensation may arrive in large installments rather than predictable monthly payments.

Consequently, the first several years of retirement may place more pressure on your portfolio than the later years.

The plan should also consider what happens after the first spouse dies.

A married couple receiving two Social Security payments may eventually become a surviving household receiving one benefit. A surviving spouse may qualify for the higher applicable benefit, but the two payments generally aren’t added together.

Meanwhile, many household expenses may remain largely unchanged.

The surviving spouse may still have the same house, property taxes, insurance premiums, and maintenance costs. However, the household may now have less income and narrower federal tax brackets.

Therefore, a retirement income plan shouldn’t work only while both spouses are alive.

It should also be tested for the survivor.

Test 3: Do You Have Enough Liquidity?

Next, you need to determine how much money should remain readily available.

Retirement changes the role of cash.

While you’re working, a paycheck can replenish your checking account after a large expense. Once you retire, that expense may need to be funded by selling investments or withdrawing money from a retirement account.

That can become a problem during a market decline.

If you’re forced to sell investments after they’ve fallen, you’re not only realizing the loss. You’re also removing assets that would otherwise have the opportunity to participate in a recovery.

That’s why we don’t view a retirement cash reserve as idle money.

Instead, it’s a source of financial flexibility.

The appropriate amount will vary by household. However, it should generally reflect near-term spending needs, known major purchases, the reliability of outside income, and the level of risk in the investment portfolio.

At the same time, holding too much cash can create another problem. Over long periods, inflation can reduce its purchasing power.

So, the goal isn’t to move everything out of the market before retirement.

Rather, the goal is to maintain enough liquidity that you won’t need to make a rushed investment decision simply because a bill is due.

Test 4: Have You Built a Retirement Tax Strategy?

Taxes don’t disappear when your paycheck stops.

In many cases, they become more complicated.

During your working years, income may come primarily from wages. In retirement, however, cash flow may come from several sources with different tax characteristics.

Traditional retirement account withdrawals are generally taxable. Qualified Roth withdrawals may be tax-free. Brokerage account sales may create capital gains. Social Security may become taxable depending on the household’s other income.

Meanwhile, higher income can also increase Medicare Part B and Part D premiums through income-related monthly adjustment amounts.

Therefore, the question isn’t simply which account has money available.

The better question is which account should fund spending this year without creating unnecessary problems in future years.

For instance, the period after retirement but before required minimum distributions begin may create an opportunity to recognize income intentionally through Roth conversions.

However, that doesn’t mean converting as much as possible.

A Roth conversion can affect federal and state taxes, Medicare premiums, capital-gain taxation, healthcare subsidies before Medicare, and the amount of cash available for spending.

Additionally, required minimum distributions generally apply to traditional IRAs and many employer retirement plans under current tax rules.

As a result, the tax strategy should look beyond this year’s tax return.

It should consider the full retirement timeline.

The objective isn’t necessarily to pay the least amount of tax in one particular year. Instead, it’s to manage lifetime taxes while preserving the flexibility to fund the life you want.

Test 5: Have You Planned for Healthcare?

Healthcare is one of the biggest variables in the retirement decision.

If you retire before age 65, you’ll need to determine how you’ll maintain coverage until Medicare begins.

Depending on your circumstances, that may involve coverage through a spouse, COBRA, an Affordable Care Act marketplace plan, or private insurance.

However, the premium is only part of the cost.

You’ll also need to consider deductibles, copays, prescription expenses, dental care, vision care, and out-of-pocket limits.

Then, once Medicare begins, the planning doesn’t stop.

Original Medicare doesn’t cover every healthcare expense. For example, it generally doesn’t cover most routine dental care, hearing aids, or long-term custodial care.

That distinction is important.

Medicare may cover qualifying short-term skilled nursing care under certain conditions. However, it generally doesn’t cover ongoing custodial care when help with activities such as bathing, dressing, or eating is the only care required.

Therefore, a complete healthcare review should address two different risks:

The first is how you’ll pay for medical coverage and routine healthcare expenses.

The second is how you’d fund an extended-care need that Medicare may not cover.

Without both pieces, an otherwise strong retirement plan may still contain a significant blind spot.

Test 6: Do Your Debt and Housing Decisions Support the Plan?

Next, consider the role of debt.

A mortgage payment that felt manageable during your working years may feel different when it’s funded through portfolio withdrawals.

At the same time, paying off the mortgage immediately before retirement isn’t automatically the right answer.

For example, withdrawing a large amount from a traditional IRA could create a sizable tax bill. Using taxable savings to eliminate the mortgage could reduce the liquidity available for healthcare, home repairs, or a market downturn.

Therefore, the question isn’t simply whether you can pay off the house.

It’s whether paying it off improves the overall plan.

Housing also needs to be evaluated beyond the mortgage.

Consider whether the home will remain:

- Affordable to maintain

- Physically accessible

- Close to family and healthcare

- Appropriate for the lifestyle you want

- Practical if one spouse is living there alone

A retirement projection may assume that you’ll stay in the same home indefinitely. However, that assumption should be tested rather than accepted automatically.

Ultimately, the home should support your retirement.

Your retirement shouldn’t exist primarily to support the home.

Test 7: Are Your Protection and Estate Plans Current?

As retirement approaches, insurance needs often change.

Disability insurance may become less important once earned income stops. Meanwhile, long-term care, property, liability, and umbrella coverage may become more important.

Life insurance also deserves a fresh review.

Some policies may no longer be necessary because the original income-replacement need has declined. However, other policies may still play a role in supporting a surviving spouse, providing liquidity, funding a legacy goal, or covering an estate-planning need.

The objective isn’t to cancel every policy once you retire.

Instead, it’s to determine whether each policy still has a specific job.

The same principle applies to your estate plan.

Wills, trusts, financial powers of attorney, healthcare directives, and beneficiary designations should reflect your current wishes and family circumstances.

However, estate planning isn’t only about transferring assets after death.

It’s also about preparing for incapacity.

Your family should know who can make financial and medical decisions, where important documents are located, and how essential accounts and bills will be managed during an emergency.

Otherwise, a financially sound retirement plan may become difficult to implement precisely when your family needs it most.

Test 8: Are You Personally Ready to Retire?

Finally, retirement readiness isn’t purely financial.

Work provides more than income.

It may also provide structure, identity, relationships, intellectual stimulation, and a sense of purpose.

Once work ends, those things don’t automatically replace themselves.

That’s why we ask clients to think beyond the retirement date.

What will an ordinary Tuesday look like?

How will you spend your time after the initial travel and home projects are complete?

How will you maintain friendships and social connections?

What will give you a sense of progress or contribution?

And if you’re married, have you and your spouse discussed what each of you expects retirement to look like?

A person can be financially prepared to retire and still struggle with the transition.

Conversely, someone may feel emotionally ready to leave but discover that the financial pieces haven’t yet been coordinated.

A durable retirement plan needs both.

What a $4 Million Portfolio Doesn’t Tell You

Consider a hypothetical married couple with $4 million in total savings and investments.

At first glance, they appear ready to retire.

However, the account balance doesn’t reveal the full picture.

Of the $4 million, assume $2.8 million is held in traditional tax-deferred retirement accounts. Another $700,000 is held in a taxable brokerage account, $300,000 is in Roth accounts, and $200,000 is in cash.

The couple estimates that they spend approximately $160,000 per year. However, that estimate doesn’t fully include irregular home repairs, vehicle replacements, or travel.

They also have a mortgage costing approximately $4,000 per month.

Additionally, one spouse is several years away from Medicare eligibility. The couple expects to provide roughly $18,000 per year of support to an aging parent, and their estate documents haven’t been updated in more than 10 years.

Neither spouse has started Social Security.

So, are they ready?

Possibly.

However, the $4 million balance alone can’t answer the question.

Before choosing a retirement date, the couple would need to determine:

- Whether $160,000 accurately reflects their full spending

- How much additional money is needed for health insurance

- Whether the mortgage should be maintained, refinanced, or paid off

- How family support affects sustainable withdrawals

- Which accounts should fund the first several years

- Whether partial Roth conversions improve the long-term tax picture

- How the plan changes when Social Security begins

- Whether the surviving spouse can maintain the household

- How much cash should remain outside the investment portfolio

- Whether estate and incapacity documents need to be updated

The couple may discover that they can retire as planned.

Alternatively, they may decide to work one more year, reduce a planned expense, restructure the mortgage, or create a more deliberate withdrawal strategy.

The purpose of the analysis isn’t to push retirement further away.

Instead, it’s to replace uncertainty with informed tradeoffs.

Test the Full Plan Before Choosing the Date

Before submitting your retirement notice, step back and review the entire financial system that will need to replace your paycheck.

Do you understand what retirement will cost?

Do you know where your income will come from?

Do you have enough liquidity to avoid selling investments at the wrong time?

Have you coordinated taxes, healthcare, housing, insurance, and estate planning?

Have you tested what happens if markets fall, inflation remains elevated, a spouse dies, or a family member needs help?

And just as importantly, do you know what you’re retiring to?

The goal isn’t to eliminate every uncertainty.

That’s impossible.

Instead, the goal is to identify the decisions that matter most, understand the tradeoffs, and make sure the major pieces of your financial life can continue working together.

Because retirement readiness isn’t determined by whether you’ve reached one particular number.

It’s determined by whether the full plan is ready to support the life that comes next.

Sources

- Internal Revenue Service, required minimum distribution guidance. https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-required-minimum-distributions-rmds

- Social Security Administration, retirement and survivor-benefit guidance. https://www.ssa.gov/survivor/amount

- Centers for Medicare & Medicaid Services, Medicare premiums and income-related adjustments. https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles

- Medicare.gov, services not covered by Original Medicare and long-term-care guidance. https://www.medicare.gov/coverage/long-term-care

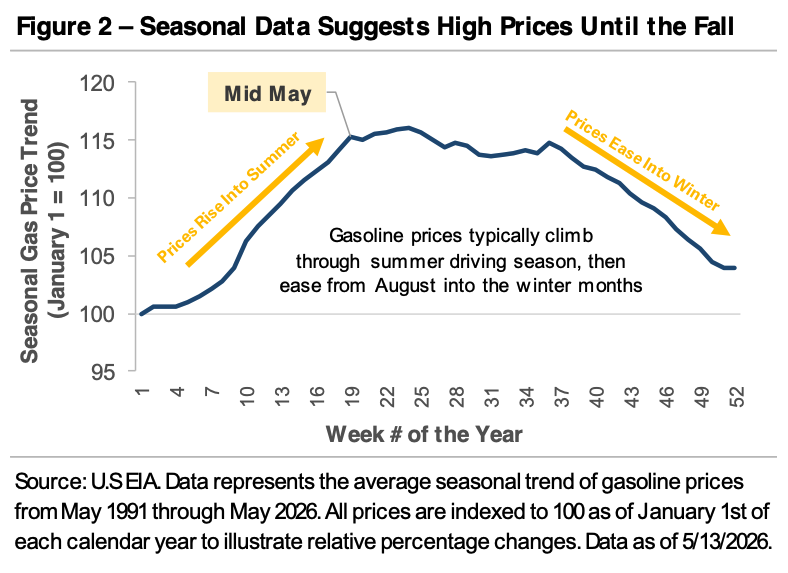

When Gas Prices Move, Your Plan Shouldn’t Panic

Gas prices are back in the headlines.

The national average price of a gallon of gasoline has moved above $4.50, up nearly 50% since the start of the U.S.-Iran conflict in late February. The main issue is oil supply. Roughly 20% of the world’s oil moves through the Strait of Hormuz, a major shipping route in the Middle East, and traffic through that route remains well below pre-conflict levels.

When less oil is moving through the system, crude prices rise. When crude prices rise, gas prices usually follow.

And this does not stop at the pump.

Higher diesel prices eventually show up in the cost of moving goods by truck. That means the pressure can work its way into grocery prices, household goods, and other everyday expenses. In other words, what begins as an energy story can quickly become a household budget story.

Moments like this tend to produce a lot of predictions.

Where will oil go next? How high will gas prices get? How long will this last?

Those are interesting questions, but they are not always the most useful ones.

The better question is: what, if anything, should this change in your financial life right now?

For most households, the answer is not “rewrite the plan.” The answer is usually much simpler. It is to look at where the pressure is showing up and make sure the adjustment is intentional.

Three questions are worth asking.

Question #1: Where is the gas price increase being absorbed?

For a household with two cars, higher fuel prices may add roughly $1,200 to $1,800 per year in additional spending.

That money has to come from somewhere.

For some families, it quietly reduces the amount being saved each month. For retirees, it may increase the amount being withdrawn from the portfolio. For others, it may simply crowd out other discretionary spending.

None of those outcomes is automatically wrong.

The issue is whether the change is happening by choice or by default.

That is the practical planning question. Are you comfortable absorbing the increase where it is currently landing? Or would it make more sense to temporarily adjust something else, such as delaying a purchase, trimming a discretionary category, or reducing short-term savings for a season?

In most cases, this kind of price increase does not require a major financial planning change.

But it does deserve a quick look.

Small pressures are easier to manage when they are noticed early.

Question #2: Is this year’s spending still tracking the retirement income plan?

For retirees, the question becomes more specific.

Is this year’s spending still in line with the plan, or is it beginning to run ahead of it?

A temporary stretch of higher fuel and grocery costs is usually something a well-built retirement plan can absorb. That is one reason we build plans with flexibility, not precision down to the penny.

But it is still worth checking.

The simple exercise is to compare actual spending over the past several months with what the plan assumed for the year. Then look at the trend.

Is the gap closing as prices stabilize? Or is it widening as higher costs spread into more parts of the budget?

That distinction matters.

The goal is not to overreact. The goal is to identify whether a small adjustment today can prevent a larger adjustment later.

That is one of the quiet benefits of ongoing planning. It gives you room to respond before something becomes urgent.

Question #3: Does higher inflation change the long-term plan?

Usually, no.

A financial plan is not built around one year of inflation. It is built around long-term assumptions that play out over decades.

That means a stretch of 4% inflation, even if it lasts several quarters, does not automatically change the long-term plan. The plan was designed with the understanding that some years will be higher, some years will be lower, and the actual path will never move in a straight line.

For those approaching retirement, the better question is whether the retirement income target still reflects the life you are planning to live.

For those still saving, it is a reminder that the cost of the future is not fixed. The number you are working toward needs to be reviewed over time because life, markets, taxes, and inflation all change.

That is not a flaw in the plan.

That is the reason planning is an ongoing process.

The Bottom Line

Higher gas prices are frustrating because they are visible, frequent, and hard to ignore.

You see the price every time you fill up. You feel it when the grocery bill runs higher. You notice it when the monthly budget feels a little tighter than it did a few months ago.

But from a planning perspective, this is not a reason to panic.

It is a reason to pay attention.

The price at the pump is a reminder that the cost of living is not a fixed number. But it is still only one input in a plan designed around a much longer time horizon.

Good planning does not require reacting to every headline.

It requires knowing which headlines matter, asking the right questions, and making small adjustments before they become large ones.

When Exercising Stock Options Creates More Tax Than You Have Cash

Some option exercises create taxable consequences before there is liquidity. On paper, value was created. In real life, that does not mean cash is available.

You exercise options in a private company or ahead of a liquidity event expecting long-term upside, and then realize you may have triggered a tax bill without having sold anything. The IRS does not wait for your shares to become sellable. It taxes what it sees as income or gain at the moment of exercise, regardless of whether you can actually convert any of it to cash.

This catches well-prepared people off guard. They make a thoughtful, forward-looking decision and then receive a tax obligation that has no obvious source of funds behind it. The decision was reasonable. The result feels punishing. Usually, the gap between the two is a planning gap, not a strategy mistake.

Why this happens

The tax code treats different option types differently, and most of those treatments do not align with when cash actually arrives.

With non-qualified stock options (NSOs), exercising creates ordinary income equal to the difference between the strike price and the fair market value at exercise. That income is reported on your W-2 and subject to withholding. If the company is private, there is no market to sell into, but the tax still applies.

Incentive stock options (ISOs) can be even more confusing. A regular-tax exercise of ISOs does not create ordinary income, which sounds favorable. But the spread between strike price and fair market value becomes a preference item for the alternative minimum tax. AMT can quietly create a six-figure liability on an exercise that produced no cash and no sale. People often discover this in April, well after the decision is final.

Restricted stock and 83(b) elections add another layer. Early exercises, secondary tender offers, and pre-IPO planning each have their own timing rules. The common thread is that taxable events are tied to specific moments in the equity, not to when you can sell.

Liquidity makes this worse. In a public company, you can usually sell shares to cover taxes, even if the timing is not ideal. In a private company, you may hold restricted stock that cannot be sold for years. Tender offers, if they happen at all, are unpredictable and often capped. So the tax obligation arrives on schedule, while the cash to pay it does not.

A common scenario

Consider an employee at a late-stage private company. She has a meaningful ISO grant, has been at the company for several years, and is told an IPO is "probably next year." She wants to start the holding period for long-term capital gains treatment, so she exercises a significant portion of her options.

Her strike price is low because she joined early. The 409A valuation has climbed substantially. The spread between the two is several hundred thousand dollars. There is no W-2 income from the exercise, so her paycheck looks normal and nothing is withheld.

Months later, her CPA runs the AMT calculation. The preference item from her ISO exercise pushes her into AMT with a tax bill in the six figures. She has no liquid shares to sell, no tender offer in sight, and the IPO timeline has slipped. She now has to fund the tax from savings, a margin loan, or specialty financing, none of which were part of her original plan.

Her decision was not wrong. The long-term math could still work out well if the company exits at a strong valuation. But the cash strain in the meantime is significant, and it could have been anticipated and sized differently before the exercise was finalized.

The same pattern plays out with NSO exercises that generate large ordinary income, with disqualifying dispositions that change ISO treatment after the fact, and with 83(b) elections on restricted stock at higher valuations. The underlying issue is consistent: equity decisions and cash flow decisions are made on different timelines, and the tax code only respects one of them.

Plan the cash before you exercise

Before exercising, model the tax cost and cash needed so a proactive move does not turn into a liquidity problem.

A useful equity exercise plan answers a few questions in writing, before any forms get signed:

- What will this exercise cost in federal, state, and AMT terms under realistic valuation assumptions?

- Where will the cash to pay that tax come from, and what is the cost of using each source?

- What happens if the liquidity event is delayed by a year, two years, or longer?

- How does this exercise interact with other income, charitable planning, and existing concentrated positions?

- If the company does not reach the expected exit, can the household absorb the loss without disrupting other goals?

These questions are not meant to discourage exercising. They are meant to make the exercise a decision that fits into a broader plan rather than one that creates pressure on it. Equity compensation can be one of the most powerful wealth-building tools available, but only when the tax timing, the cash timing, and the longer-term strategy are coordinated in advance.

If you are weighing an exercise, evaluating a tender offer, or watching a possible liquidity event approach, the most valuable work usually happens before the calendar forces a decision. Run the numbers, stress test the assumptions, and make sure the cash plan is as well thought through as the equity plan.

A Roth Conversion Is Not the Goal

There's a quiet enthusiasm building around Roth conversions.

You hear about them at the water cooler. You read about them in the financial press. A friend mentions what their advisor recommended over lunch.

The pitch makes sense on the surface.

Pay tax now while rates are favorable. Move money into a Roth account. Watch it grow tax-free for the rest of your life. Pass what's left to your children without the IRS taking another bite.

It's a compelling idea.

It can also be a costly one.

Here's what the headlines rarely mention. A Roth conversion is helpful, right up until it isn't. The same move that saves one retiree thousands can cost another retiree even more.

The difference isn't the strategy.

The difference is the size.

The Goldilocks Problem

Roth conversions create a Goldilocks problem.

Convert too little, and you may leave a real opportunity on the table.

Convert too much, and you may trigger consequences that show up on this year's tax return, or, in the case of Medicare premiums, a year or two later.

Consider two retirees in similar situations.

Both are sixty-seven. Both have around two million dollars in pre-tax IRAs. Both want to soften the impact of future required minimum distributions and leave a more flexible legacy for their family.

The first retiree maps out the next ten years. She runs the numbers. She converts roughly eighty thousand dollars each year, using the lower tax brackets available to her without pushing too much income into higher-cost territory.

By the time her required distributions begin, her pre-tax IRA is meaningfully smaller. Her future tax bill is smaller too. She feels lighter.

The second retiree hears the same advice in broad strokes and decides bigger is better. He converts three hundred thousand dollars in a single year.

The conversion itself is taxed at higher rates. His Medicare premiums may jump in a future year because Medicare looks back at prior income when calculating IRMAA surcharges. If he's already claimed Social Security, more of those benefits may become taxable. A modest stock sale may be taxed at a higher capital gains rate. His state income tax may rise too.

None of those costs were on the brochure.

Same strategy. Different outcomes.

The strategy wasn't the problem.

The size was.

Why Rules of Thumb Don't Work Here

You may have heard rules like, "Convert while tax rates are low," or, "Fill up the lower tax brackets before required minimum distributions begin."

Those rules sound clean.

They're also incomplete.

A proper Roth conversion analysis looks at far more than your marginal tax bracket. It considers your Medicare premium thresholds. Your Social Security taxation. Your state tax exposure. Your capital gains tier. The shape of your future required distributions. The expected tax bracket of your heirs. Your charitable intentions. The order in which you plan to draw from different accounts in retirement.

Each of those factors moves the right answer.

Sometimes by a little.

Sometimes by a lot.

That's why the question is never simply, "Should I convert?"

The question is always, "How much, and over how many years, makes sense for the life I'm actually living?"

The Move and the Math

The Roth conversion is the move.

The math is what makes the move work.

A well-sized conversion plan isn't a one-time decision. It's a multi-year roadmap. It treats the years between retirement and required distributions as a window of opportunity, then fills that window thoughtfully, year by year, bracket by bracket, with awareness of every secondary cost that could be triggered along the way.

That's not the kind of analysis you do in your head.

It's not the kind of analysis a generic online calculator can do.

And it's rarely the kind of analysis built into the tax preparation conversation, where the focus is reporting last year, not designing the next ten.

That's the difference between tax preparation and tax planning.

One reports what happened.

The other helps decide what should happen next.

It takes time, the right tools, and someone who understands how every line of your financial life connects to every other line.

Bottom Line

If you've been wondering whether a Roth conversion belongs in your plan, that's a fair question to be asking.

The instinct is a good one.

Just don't stop at the instinct.

Before you convert anything, run the full picture. Map the next ten years of income. Stress test the secondary costs. Look at what happens to Medicare, Social Security, capital gains, and state taxes when you change one number on your return.

Then, and only then, decide what to do.

A Roth conversion isn't the goal.

Clarity is.

Confidence is.

Peace of mind is.

The conversion is just one of the tools we use to get there.

If you'd like a full evaluation of whether a Roth conversion belongs in your plan, when to do it, and how much is too much, that's a conversation worth having while there's still time on the calendar to act on it.

Post-Filing Tax Hygiene: Three Things to Do With the Return You Just Filed

There's a category of financial work I think of as tax hygiene.

It isn't the headline-grabbing stuff. It's the small, recurring habits that quietly determine whether your tax life feels under control or chronically off-kilter. Most of the trouble I see with clients doesn't come from missing some clever strategy. It comes from a withholding number that drifted out of date, an estimated payment that slipped past a deadline, or a return that got signed and filed away without anyone asking what it was actually saying.

That last point is where I want to start.

Once your 2025 return is filed, you have something useful in hand: a year's worth of financial data, organized and reconciled. Most people treat the finished return as a chore that's finally over. I'd encourage you to treat it as information. It can tell you a fair amount about what to adjust for the year ahead, and three areas in particular are worth a look.

Review the Return Before You File It Away

Before the return goes into your records, spend twenty minutes with it.

Look at the bottom line first. A meaningful balance due usually means your withholding or estimated payments weren't keeping pace with your actual income. If that goes uncorrected, it can compound into underpayment penalties. A meaningful refund isn't a crisis, but it does mean you lent money to the federal government interest-free for a year.

Either result is worth understanding before you move on.

Then look at what's on the return itself. Sometimes a capital gain shows up that you'd forgotten about, or a side project generated more income than you realized, or a deduction you'd planned around didn't materialize the way you expected. These are the items that often hint at planning opportunities, or planning gaps, for the year ahead. They're easier to act on now than to reconstruct next March.

Finally, take stock of any carryforwards. Capital losses, charitable contributions over your AGI limit, passive activity losses, and foreign tax credits can all carry into future years, but they don't manage themselves. Knowing what's available to you is the first step in using it well.

The return is the most accurate picture you'll have of your financial year. It's worth using.

Recalibrating Your Withholding

Withholding is one of those settings most people configure once and forget.

Life moves on. You change jobs, retire, start Social Security, begin drawing from an IRA, get married, sell a property, or pick up a side venture. Each of those events can quietly knock your withholding out of alignment with your actual tax bill. If your 2025 return showed a meaningful balance due or refund, recalibration is what fixes it.

The IRS publishes a withholding estimator on its website that walks you through your income sources, credits, and deductions, and gives you a target for what your withholding should look like. It takes about twenty minutes if you have a recent pay stub and your 2025 return handy, which conveniently you do.

If the numbers are off, the fix is usually just a fresh form. Employees submit a new W-4 to their employer. People receiving pension or annuity payments use Form W-4P. IRA owners use Form W-4R. And if you'd like more federal tax pulled from your Social Security check, Form W-4V handles that.

The best time to do this is in the weeks right after filing, while the numbers are fresh and the relevant documents are already on your desk.

Tuning Your Estimated Tax Payments

Withholding solves the problem when tax can be pulled directly from a paycheck, pension, IRA distribution, or Social Security benefit. Estimated payments solve the problem when income arrives without withholding attached.

If you have income from self-employment, investments, partnership distributions, rental properties, or retirement income where withholding hasn't been elected, the IRS generally expects quarterly estimated payments. The 2026 installments are due April 15, June 15, September 15, and January 15, 2027. Taxpayers in federally declared disaster areas may have additional time, but absent that, the dates are firm.

Your 2025 return is the natural starting point for sizing these payments. If your non-withholding income was steady, last year's numbers are a reasonable baseline. If something changed materially, whether a business grew, a portfolio started throwing off more income, or a property was sold or acquired, the baseline needs adjusting before you set the year's payment schedule.

The mechanics of paying have quietly modernized. If you have an IRS online account, you can pay through it directly. IRS Direct Pay and the Treasury's Electronic Federal Tax Payment System both work well. The IRS also has a phone app, and the agency accepts credit card payments with a processing fee that's worth weighing against any rewards you'd earn.

Paper checks may still be available, but electronic payments are increasingly the cleaner and more reliable option. If you're a check-by-mail holdout, this is a good year to switch to electronic payments. The transition is genuinely painless once you set it up.

The June 15 deadline is the one that catches people, since it arrives only two months after April. Putting all four dates on your calendar now is one of the cheaper investments you can make in your own peace of mind.

The Big Takeaway

None of this is glamorous.

But the discipline of reading your return as information, recalibrating withholding while the data is fresh, and setting estimated payments with intention is the foundation everything else sits on.

Our work with clients begins here, with the maintenance items that don't generate excitement but quietly add up to clarity, confidence, and fewer surprises next April. If you'd like a second set of eyes on what your 2025 return is telling you, we're glad to help.

More Money, More Mess: The Hidden Cost of Uncoordinated Wealth

Many people assume that as their net worth grows, their financial life gets simpler. In practice, the opposite is often true. Growing wealth tends to create a quiet kind of clutter that doesn't show up on a balance sheet, but shows up in missed opportunities, unnecessary taxes, and decisions that no longer match the life you're living today.

This clutter rarely announces itself. It builds slowly, one account and one decision at a time, until it becomes difficult to see how all the pieces fit together.

How Financial Clutter Builds Over Time

Financial clutter isn't usually a sign of poor discipline. It's often a sign of a life that has moved forward. You changed jobs, so you left a 401(k) behind. You inherited an IRA. You opened a brokerage account at one firm, then another at a different firm because someone recommended it. You bought a life insurance policy in your thirties, and another one later for estate purposes. You worked with a CPA, then a different CPA, then an attorney who drafted a trust your current advisor has never reviewed.

Each of those decisions made sense at the time. The issue is that no one stepped back to ask how they all fit together. Most clutter isn't the result of bad advice. It's the result of good advice given in isolation, year after year, without a plan to connect the pieces.

What Coordinated Planning Does

Turning clutter into clarity isn't a matter of starting over. It's a matter of giving every piece of your financial life a defined role and making sure those roles work together. A coordinated plan does a few specific things that piecemeal decisions can't.

It gives each account a job. Some assets are better suited for current income, others for long-term growth, and others for heirs or charitable goals. When each account has a clear purpose tied to the overall plan, day-to-day decisions become easier and more consistent.

It sequences withdrawals with taxes in mind. The order in which you draw from taxable, tax-deferred, and Roth accounts can meaningfully affect your lifetime tax bill, your Medicare premiums, and how long your portfolio lasts. A coordinated plan looks at these decisions together rather than one year at a time.

It uses planning windows that are easy to miss. The years between retirement and the start of Required Minimum Distributions can be one of the most valuable periods for Roth conversions, capital gains planning, and charitable strategies. Without a plan, those years often pass without being fully used.

It revisits the pieces you may have forgotten. Older insurance policies, annuities, and legacy accounts sometimes continue to serve a purpose, and sometimes they no longer do. A coordinated review asks whether each one still fits, and what to do if it doesn't.

It aligns your accounts with your estate plan. Beneficiary designations often override what your will or trust says. A coordinated plan makes sure the titling of your accounts, the designations on retirement plans and insurance, and the structure of your estate documents all point in the same direction.

The Big Takeaway

A well-built plan doesn't add. It organizes. It ties your investments, tax planning, insurance, and estate documents together into a single picture of the life you want to fund and the legacy you want to leave. The goal isn't to own more. It's to make sure what you already own is working together.

Every household's situation is different, and the right path forward depends on your goals, your family, and how you want retirement and legacy to look. Our goal is to help you turn financial clutter into clarity, so the wealth you've worked hard to build can serve the life you actually want.

The Tax Items Congress Wants, But Probably Won’t Pass Yet

Most months, there isn’t much new tax law to report. This is one of those months.

No major tax rules have changed. But there’s still a useful update worth sharing, because what Congress is debating now can tell us something about where tax policy may be headed, even when nothing has changed yet.

The Short Version

Republicans are working on another budget reconciliation bill before the midterm elections.

Reconciliation is the procedural workaround that lets the Senate pass certain budget-related legislation with a simple majority instead of the usual 60-vote threshold. It’s how last year’s major tax bill became law on a strictly partisan vote, and it’s the most likely vehicle for any significant tax legislation between now and then.

GOP taxwriters would like to see tax provisions included in this next bill. Their wish list includes priorities that didn’t make it into last year’s bill, a framework for taxing digital assets, changes to health savings accounts, easings to the corporate alternative minimum tax, and reforms to refundable credits.

That’s the wish list. The problem is that the vehicle for carrying it may not be available this time.

The next reconciliation package now looks likely to be narrow. The current direction from the White House and congressional leadership is to limit the bill to funding for two Department of Homeland Security agencies, Immigration and Customs Enforcement and Customs and Border Protection.

The administration wants the bill enacted by June 1, which puts pressure on lawmakers to move quickly and reduces the appetite for expanding the package.

In other words, taxes probably aren’t in the next bill. But the wish list itself is still informative.

What We’re Watching, and Why

When tax provisions are debated and then deferred, it’s tempting to file the news away as not relevant yet.

We treat it differently.

The items being discussed today are often the items that resurface when the next legislative opportunity appears. The planning value of knowing what may be coming is highest before the rules are final, not after.

A few specific items are on our watch list.

Digital Assets

A clear federal framework for taxing cryptocurrency and other digital assets has been on the wish list for years and keeps getting pushed.

When it does pass, it could create new reporting obligations and may affect how gains, losses, and transactions are documented. Clients with meaningful digital asset positions should expect this issue to land eventually.

Health Savings Accounts

Proposed changes generally aim to expand who can contribute and how the funds can be used.

HSAs are already one of the most tax-efficient accounts in the code. Any expansion could create new planning opportunities for clients who qualify, especially those trying to coordinate healthcare costs, retirement planning, and long-term tax efficiency.

Refundable Credits

Reform here usually means tightening eligibility and increasing verification.

That connects directly to the broader IRS enforcement story we wrote about separately. The trend is toward more scrutiny of these credits, whether through legislation, enforcement, or both.

Corporate Alternative Minimum Tax

Most individual clients aren’t directly affected by the corporate alternative minimum tax.

But executives, business owners, and investors with exposure to companies affected by the rule may still care about how changes could flow through to valuation, cash flow, compensation, or transaction planning.

The Big Takeaway

None of these tax changes appear imminent.

But they’re still worth watching, because tax legislation tends to move in long pauses punctuated by short bursts of activity. The pauses are when planning happens. The bursts are when the rules change.

We watch the legislative calendar so that when something does move, we already know what it means for the clients it affects. More importantly, we’ve already had the conversations that need to happen.

If any of the items above touch your situation and you’d like to talk through the implications, we’re glad to do that.

A Smaller IRS, a Different Kind of Enforcement

The IRS is meaningfully different than it was eighteen months ago. The agency has lost more than a fifth of its workforce since the start of 2025, its budget has been cut, and most of the funding boost it received from the 2022 Inflation Reduction Act has been clawed back.

What this adds up to isn't just a smaller IRS. It's a different IRS.

The agency is reshaping what it enforces, how it enforces it, and which taxpayers are most likely to hear from it. That story is worth understanding, both because it's genuinely consequential and because the practical implications for taxpayers aren't what you might first assume.

The numbers behind the change

Congress set the IRS's fiscal year 2026 budget at $11.2 billion, about 9% below FY25. House appropriators are pushing for a further cut to $10.2 billion in FY27. The agency has lost more than 20% of its workforce since January 2025 through deferred resignations and layoffs, with additional departures expected this year.

The Trump administration's FY27 budget request includes an 18% reduction in enforcement activity and projects an enforcement workforce below 25,000. Within that already shrunken enforcement arm, some of the largest losses have hit the examination and collection groups, and many of those who left were experienced agents and managers carrying years of institutional knowledge that won't be easy to replace.

In plain English, the IRS has fewer people, fewer experienced reviewers, and less capacity to conduct traditional enforcement the way it once did.

Fewer audits, especially at the top

The audit rate for individuals has been well below 1% for several years, and we expect it to keep falling, at least over the next few years.

Audits of individuals with $10 million or more of income, which numbered 6,786 in FY25, dropped to 2,264 in FY26. Partnership audits fell from 3,174 to 2,932 over the same period. The agency forecasts further declines in both categories in FY27.

For clients in higher income brackets, who historically faced disproportionate audit attention, the near-term picture is meaningfully different than it was even two years ago. The headline probability of a traditional audit appears lower.

But that doesn't mean enforcement risk has disappeared. It means the nature of that risk is changing.

The odds of a traditional audit may be lower, but the audits that remain are less likely to be random noise. They're more likely to be tied to something specific in the return, such as a mismatch, an anomaly, a complex transaction, or an item that doesn't reconcile cleanly with third-party data.

What's replacing the lost capacity

That's the headline. The more interesting story is what's replacing the lost capacity.

IRS leadership has said publicly that fewer audits will be paired with more targeted ones, and the mechanism for that targeting is increasingly data analytics and artificial intelligence. The agency has been investing in software that mines taxpayer data to surface anomalies, flag suspicious activity, and identify cases for review.

Even with reduced funding, the direction of travel is clear: the IRS is leaning harder on technology because it no longer has the same human capacity. The intent is to compensate for the loss of human reviewers by being more precise about who gets reviewed in the first place.

We'll see how well it works in practice. But the direction is clear: less of the broad coverage that audit rates traditionally measured, and more of the targeted attention those same rates fail to capture.

Where enforcement is concentrating

Two areas in particular look like they'll absorb a disproportionate share of the enforcement capacity that remains.

The first is refundable credits, where the IRS estimated improper payments of $21.4 billion in FY24 alone. The earned income credit, the American Opportunity credit, and the premium tax credit are all on this list, and all are well-suited to algorithmic review.

For many higher-income households, refundable credit reviews may not be the primary concern. But they illustrate the broader enforcement shift. The IRS is favoring areas where software can flag returns quickly and where discrepancies can be identified without a large team of experienced agents.

For you, the more relevant version of that same shift is income matching.

The IRS's automated underreporting program compares the W-2s, 1099s, and other third-party tax forms it receives against what taxpayers report on their returns. Significant mismatches generate a CP2000 notice, which is computer-driven and doesn't require an experienced agent to produce.

This matters for households with brokerage accounts, equity compensation, retirement income, business income, K-1s, real estate activity, charitable giving, or multiple sources of income. The more moving pieces there are, the more important it becomes that the return tells a clean and consistent story.

Traditional enforcement may shrink, but automated enforcement can still expand because it requires fewer experienced agents to initiate. As enforcement leans further into automation, expect more of this kind of correspondence, not less.

What it means for you

For you, this all means a few things.

First, the headline audit risk for high-income clients is genuinely lower than it was. That's a real shift, and it's worth naming rather than dismissing. But it isn't a license for casual recordkeeping.

The audits that do occur will be more precisely chosen. That means the cases that get pulled are more likely to be cases where something genuinely doesn't reconcile. Clean books, good documentation, and coordinated reporting matter at least as much in this environment as they did before, possibly more.

Second, the surface area for automated correspondence is growing.

CP2000 notices, refundable credit reviews, and other algorithm-driven inquiries don't feel like audits and may not show up in the headline audit statistics. They may not require the same scope of work as a full audit, but they still require careful review, documentation, and a timely response.

If you receive one, the worst thing to do is ignore it. The deadlines on these notices are real, and the IRS's response to silence is rarely favorable.

Third, the shape of the agency is going to keep changing.

Budget proposals are still being debated, workforce attrition is ongoing, and the technology is still maturing. What looks like a settled picture today may shift again over the next year or two.

That's part of why we follow this closely. Tax planning is most useful when it accounts for where the enforcement environment is going, not just where it is.

Why coordination matters more now

This is also why tax planning and wealth planning shouldn't live in separate silos.

The more complex your income, investments, retirement withdrawals, equity compensation, business interests, or estate planning becomes, the more important it is that the tax return tells the same story as the financial plan.

A smaller IRS may conduct fewer traditional audits. But a more automated IRS may still notice when the pieces don't line up.

That's why tax planning isn't just about finding deductions or reacting before year-end. It's about making sure decisions are coordinated before they show up on a return. Investment decisions, retirement income decisions, Roth conversion decisions, charitable giving decisions, and estate planning decisions can all create tax consequences. The goal is to understand those consequences ahead of time rather than explain them after the fact.

The Big Takeaway

None of this changes the fundamentals of what we do for clients.

We aim to file accurately, document thoroughly, and structure things so that when the IRS does ask a question, the answer is already on the shelf.

That discipline mattered when audit rates were higher, and it matters now, even as the agency asking the questions becomes smaller, more automated, and more selective.

The goal hasn't changed: clarity in your filings, confidence in your position, and the peace of mind that comes from knowing the work was done right the first time.

Here’s What to Make of Recent Headlines

It is hard to think about investing, planning, and the future when it feels like the social fabric that has held this country together is fraying in real time.

If you have found yourself distracted, unsettled, or even angry by the headlines around immigration enforcement, you’re not alone. Recent reports over the past few weeks have left a lot of Americans asking, “what’s happening to us?”

And yet, it’s tempting to shrug and say, “This is politics, it has nothing to do with my retirement plan.”

However, this time, I don’t agree.

Not because every headline turns into a market event because most headlines don’t.

It’s because the issues underneath these headlines touch on two things markets care deeply about, and that’s trust and stability.

When trust and stability are strong, capital flows in. When trust and stability are questioned, however, investors begin to demand a higher price for taking risk.

Sometimes that shows up as higher borrowing costs, sometimes it shows up as more volatility and sometimes it shows up as both.

Ultimately, the headlines could be a symptom of a broader trend unfolding, so here’s what I’m watching.

Two channels I am watching

First, it’s crucial to note that the United States is a premier destination for global capital.

And one of the quiet advantages the U.S. has had for decades is not simply innovation or scale, it’s governance and rule of law.

It’s the idea that rules apply consistently, contracts are enforceable, and institutions are resilient. That rules-based order is part of why global investors have been willing to allocate so much money here, even when our politics are loud.

That’s also why perceptions matter because markets don’t need perfection, they need confidence that the basic institutional guardrails will stay in place.

Watching the Fed

A good example is what’s happening with the Federal Reserve.

The Fed’s credibility has always rested on independence, and the belief that policy decisions are aimed at long-term stability, not short-term political goals.

With that said, as leadership transitions approach, it is reasonable for investors to pay closer attention to whether that independence looks protected or pressured. That’s because even the perception of shifting incentives can change how the world prices U.S. assets.

The other example is rule of law. And what do we mean here by rule of law?

Well, it’s the difference between “I own this asset” and “I own it until someone with power decides otherwise.”

Throughout my career, this has been one of the key risks we evaluate when looking to invest in emerging markets or politically unstable regions. Until recently, it has not been a risk most investors felt they had to price heavily in the United States.

Now, it’s starting to change, even at the margins.

Because when headlines start to raise questions about fundamental rights, due process, and institutional constraints, that’s the sort of thing global capital markets pay attention to.

Not instantly, and not always dramatically, but it’s the kind of thing that makes global investment policy committees sit up and begin reviewing their asset allocation decisions.

The Impact on Prices

The second thing I’m watching is how today’s events impact the economic structure behind labor, growth, and prices.

This is a longer-term trend, to be sure, but the seeds being planted today, if not mitigated, could be of consequence years down the line when it matters most in retirement.

Because here’s the thing: What has made America exceptional for so long is that people have been willing to come here, work, build, and contribute to build a new life.

That is the American story, whether your family arrived centuries ago or last generation.

And so, if the U.S. becomes a less attractive destination for legal immigration, then the economic consequences, like labor shortages, don’t stay contained, they could naturally flow into the prices we pay for goods and services.

You can see the contours of this development already unfolding.

Indeed, industries that rely on skilled labor and steady hiring pipelines, like construction, healthcare, and engineering, are sensitive to labor disruption. Add uncertainty for workers on legal pathways, including work visas and student visas, and you risk shrinking the pool of talent over time.

Yes, automation will keep advancing. And AI, robotics, and process improvements will absolutely offset some labor pressure.

Still, there are many jobs where a human eye and a human touch are not optional, at least not yet. If labor supply tightens faster than technology can replace it, the effect is that costs rise.

That is the simplest economic math on the board.

In practical terms, that could mean higher prices in areas that already feel stretched, including food, housing-related labor, and medical services. It could also mean inflation settling at a higher level than the 2% world many retirement models quietly assume.

So what does this mean for your plan?

It’s essential to note here that I don’t say any of this to be dramatic. I say it because looking away is not a strategy. Ignoring reality is not a plan.

If institutional stability is eroded, you could see a world where markets demand a higher risk premium for U.S. assets. And that could translate into lower valuations, more volatility, and higher interest rates than people expect.

And if labor constraints persist because determined, talented individuals are less interested in coming to the United States, well, you could see a world where inflation runs hotter for longer, which might raise your long-term cost of retirement.

Taken together, both of those outcomes matter because they touch the growth of your assets and the purchasing power of your withdrawals.

The good news is that our planning work is not built on best-case assumptions.

We already model conservative growth rates and higher inflation because surprises are not rare, they are the norm.

So then, in moments like this, the question is not “can we predict what happens next?”

But rather, the question should be “is my plan built to endure a range of outcomes, including uncomfortable ones?”

That’s what we will keep focusing on.

What can you do right now?

We can’t control the headlines.

However, we can control how prepared we are for the changing developments.

At this moment in time, it’s worth paying attention to, even if it’s uncomfortable.

Because the things that feel distant, political, or abstract can become personal through our portfolios, prices, job markets, interest rates, and the stability of the institutions we all rely on.

If you have questions about how this environment could affect your plan, now’s a good time to revisit assumptions, stress-test scenarios, and make sure your strategy matches the world as it is, not the world we wish it were.

Market Update: Geopolitical Tensions & Your Financial Plan

Given the deeply concerning headlines about the conflict in the Middle East, I imagine this is a time of worry for you as it is for many.

While the violence and loss of life is distressing, I want to reassure you that your financial plan is designed to weather turbulence, and I’m watching the situation closely on your behalf.

There are still many open questions about how the geopolitical situation will unfold, and near-term market volatility is likely amid the uncertainty.

Some Historical Context

However, in times like these, the chart below offers important historical context in that the U.S. has navigated many challenging periods in the past, so staying focused on your long-term plan is critical.

Indeed, history has shown the wisdom of sticking to your investment discipline and not overreacting to short-term events, difficult as that can feel in the moment.

What to Do Next

As a next step, I would recommend reviewing last week’s email (see link below) because the key takeaways bear repeating:

https://franklinmadisonadvisors.com/cio-corner/market-volatility-heres-what-to-do-about-it/

Rest assured, if I’ve personally worked on your plan with you, your portfolio is built to withstand choppy markets, and we are monitoring developments diligently and ready to make prudent adjustments if warranted.

If You Still Need Help

Ultimately, I'm here as a resource and sounding board for you.

Please don't hesitate to schedule a quick call or reply to this email with any specific questions or concerns you have, I'm happy to talk things through and revisit any details of your plan so you can feel more confident.

While the macro situation is troubling, I have deep faith in the resilience of our country and economy. We will get through this, and I remain optimistic about the long-term future.