Here’s What to Make of Recent Headlines

It is hard to think about investing, planning, and the future when it feels like the social fabric that has held this country together is fraying in real time.

If you have found yourself distracted, unsettled, or even angry by the headlines around immigration enforcement, you’re not alone. Recent reports over the past few weeks have left a lot of Americans asking, “what’s happening to us?”

And yet, it’s tempting to shrug and say, “This is politics, it has nothing to do with my retirement plan.”

However, this time, I don’t agree.

Not because every headline turns into a market event because most headlines don’t.

It’s because the issues underneath these headlines touch on two things markets care deeply about, and that’s trust and stability.

When trust and stability are strong, capital flows in. When trust and stability are questioned, however, investors begin to demand a higher price for taking risk.

Sometimes that shows up as higher borrowing costs, sometimes it shows up as more volatility and sometimes it shows up as both.

Ultimately, the headlines could be a symptom of a broader trend unfolding, so here’s what I’m watching.

Two channels I am watching

First, it’s crucial to note that the United States is a premier destination for global capital.

And one of the quiet advantages the U.S. has had for decades is not simply innovation or scale, it’s governance and rule of law.

It’s the idea that rules apply consistently, contracts are enforceable, and institutions are resilient. That rules-based order is part of why global investors have been willing to allocate so much money here, even when our politics are loud.

That’s also why perceptions matter because markets don’t need perfection, they need confidence that the basic institutional guardrails will stay in place.

Watching the Fed

A good example is what’s happening with the Federal Reserve.

The Fed’s credibility has always rested on independence, and the belief that policy decisions are aimed at long-term stability, not short-term political goals.

With that said, as leadership transitions approach, it is reasonable for investors to pay closer attention to whether that independence looks protected or pressured. That’s because even the perception of shifting incentives can change how the world prices U.S. assets.

The other example is rule of law. And what do we mean here by rule of law?

Well, it’s the difference between “I own this asset” and “I own it until someone with power decides otherwise.”

Throughout my career, this has been one of the key risks we evaluate when looking to invest in emerging markets or politically unstable regions. Until recently, it has not been a risk most investors felt they had to price heavily in the United States.

Now, it’s starting to change, even at the margins.

Because when headlines start to raise questions about fundamental rights, due process, and institutional constraints, that’s the sort of thing global capital markets pay attention to.

Not instantly, and not always dramatically, but it’s the kind of thing that makes global investment policy committees sit up and begin reviewing their asset allocation decisions.

The Impact on Prices

The second thing I’m watching is how today’s events impact the economic structure behind labor, growth, and prices.

This is a longer-term trend, to be sure, but the seeds being planted today, if not mitigated, could be of consequence years down the line when it matters most in retirement.

Because here’s the thing: What has made America exceptional for so long is that people have been willing to come here, work, build, and contribute to build a new life.

That is the American story, whether your family arrived centuries ago or last generation.

And so, if the U.S. becomes a less attractive destination for legal immigration, then the economic consequences, like labor shortages, don’t stay contained, they could naturally flow into the prices we pay for goods and services.

You can see the contours of this development already unfolding.

Indeed, industries that rely on skilled labor and steady hiring pipelines, like construction, healthcare, and engineering, are sensitive to labor disruption. Add uncertainty for workers on legal pathways, including work visas and student visas, and you risk shrinking the pool of talent over time.

Yes, automation will keep advancing. And AI, robotics, and process improvements will absolutely offset some labor pressure.

Still, there are many jobs where a human eye and a human touch are not optional, at least not yet. If labor supply tightens faster than technology can replace it, the effect is that costs rise.

That is the simplest economic math on the board.

In practical terms, that could mean higher prices in areas that already feel stretched, including food, housing-related labor, and medical services. It could also mean inflation settling at a higher level than the 2% world many retirement models quietly assume.

So what does this mean for your plan?

It’s essential to note here that I don’t say any of this to be dramatic. I say it because looking away is not a strategy. Ignoring reality is not a plan.

If institutional stability is eroded, you could see a world where markets demand a higher risk premium for U.S. assets. And that could translate into lower valuations, more volatility, and higher interest rates than people expect.

And if labor constraints persist because determined, talented individuals are less interested in coming to the United States, well, you could see a world where inflation runs hotter for longer, which might raise your long-term cost of retirement.

Taken together, both of those outcomes matter because they touch the growth of your assets and the purchasing power of your withdrawals.

The good news is that our planning work is not built on best-case assumptions.

We already model conservative growth rates and higher inflation because surprises are not rare, they are the norm.

So then, in moments like this, the question is not “can we predict what happens next?”

But rather, the question should be “is my plan built to endure a range of outcomes, including uncomfortable ones?”

That’s what we will keep focusing on.

What can you do right now?

We can’t control the headlines.

However, we can control how prepared we are for the changing developments.

At this moment in time, it’s worth paying attention to, even if it’s uncomfortable.

Because the things that feel distant, political, or abstract can become personal through our portfolios, prices, job markets, interest rates, and the stability of the institutions we all rely on.

If you have questions about how this environment could affect your plan, now’s a good time to revisit assumptions, stress-test scenarios, and make sure your strategy matches the world as it is, not the world we wish it were.

How Withdrawal Rates Impact Your Portfolio in Retirement

Many people spend years preparing for retirement by saving and investing, but planning shouldn’t stop once the paychecks do. Transitioning from earning income to withdrawing it from your portfolio is a major shift with a new set of risks and decisions. This period, known as the distribution phase, requires careful thought.

How much you withdraw each year can have a bigger impact on long-term financial security than many people realize. Without a well-structured strategy, even a sizable retirement account can be depleted faster than expected.

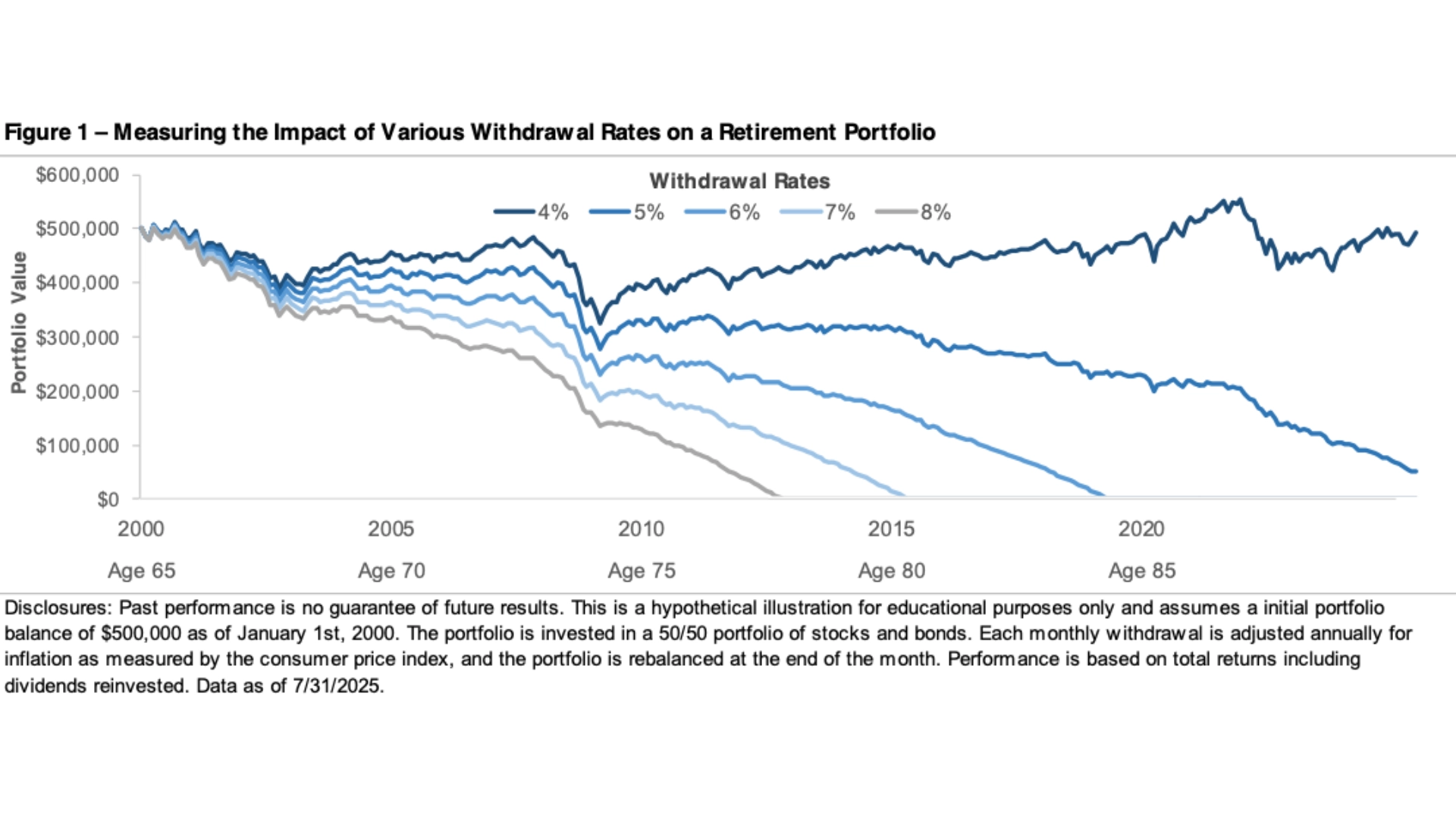

The Impact of Withdrawal Rates

The chart below shows how different withdrawal rates can impact a retirement portfolio’s lifespan. It assumes an individual retired in 2000 at age 65 with $500,000 and started taking monthly withdrawals.

Each line reflects a different withdrawal rate between 4% and 8%, showing how the portfolio fared through age 85. While all scenarios start at the same point, the paths quickly diverge, especially during periods of market volatility. The chart illustrates how a retiree’s withdrawal strategy can determine whether the portfolio lasts or runs out.

The message is clear: higher withdrawal rates tend to exhaust a portfolio sooner, while lower rates can extend its life. In this example, withdrawing 7% or 8% caused the portfolio to run out of money before age 85. In contrast, the 4% and 5% withdrawal rates helped the portfolio weather market declines.

Does a 4% Rate Still Cut It?

The 4% strategy not only preserved the portfolio but grew it over 20 years, showing how compounding can work even during retirement. No strategy can eliminate market risk, but a smaller withdrawal rate can extend the portfolio’s life and reduce the risk of outliving your savings. Taking a more conservative approach in the early years of retirement gives your portfolio time to recover from short-term losses and grow with the market.

A thoughtful withdrawal strategy is an important part of retirement planning. It’s not just about how much you’ve accumulated, but how you manage it. There’s no one-size-fits-all approach, and the method you start with doesn’t have to be permanent. Fixed withdrawal rates can provide a good starting point, but many retirees may benefit from more flexible approaches.

The Big Takeaway

For example, you could adjust withdrawals based on market conditions, taking smaller distributions in down years and larger ones in strong years. Another option is the bucket strategy, which divides assets into short-, intermediate-, and long-term segments.

By keeping at least 18 months worth of expenses in cash or short-term investments, you can avoid selling stocks during major market declines, such as those in 2008 or 2020. This gives long-term investments time to recover and can help create a steadier income stream over time. Everyone’s retirement looks different. Our goal is to help you create a withdrawal strategy tailored to your unique needs and goals when that time comes.

One Big Beautiful Bill: What Smart Families Are Doing Now

A few weeks ago, we shared our perspective on the One Big Beautiful Bill and why it marked a defining moment for retirement savers, tax-conscious investors, and families thinking about legacy.

And since then, we’ve had the chance to review the full scope of the legislation, and the practical steps some families are already taking.

What we’re seeing is this: The ones who act early, with clear intent, are the ones who tend to benefit most.

So today, I want to walk you through the strategic moves that are rising to the top, moves you might want to consider before the window closes:

Revisiting the Estate Plan

One of the more overlooked outcomes of the new law is what it does to the estate and gift tax exemption.

Starting in 2026, the lifetime exemption jumps to $15 million per person, and for now, it’s permanent.

Now, if you’ve already put an estate plan in place, you might be tempted to move on. But here’s the thing: the landscape has shifted underneath that plan.

Because when exemption amounts increase, so do the opportunities to move assets off your balance sheet, whether to heirs, to trusts, or to charitable causes, without triggering transfer taxes. And depending on how your documents were drafted, you may not be taking full advantage.

For some, this may be the time to revisit old credit shelter or bypass trusts that no longer serve their purpose. For others, it might mean accelerating gifts, funding multi-generational trusts, or finally setting up that family limited partnership.

But the bottom line is this: the cost of doing nothing just went up.

Rethinking Generosity

For families who give consistently, whether through tithing, donor-advised funds, or community causes, the new law brings both opportunities and limitations.

Starting in 2026, non-itemizers will be able to deduct up to $1,000 in charitable contributions, or $2,000 if filing jointly. That’s a nice gesture.

But here’s the catch: for those who itemize, charitable gifts will now only count to the extent they exceed 0.5% of your adjusted gross income.

Said differently? Your giving has to cross a higher bar before it starts working for you on your tax return.

That doesn’t mean you should give less. But it might mean you give differently.

It might mean consolidating gifts into one year instead of spreading them out. It might mean funding a donor-advised fund now while deductions are fully available, then distributing those gifts over time. And for some, it may mean rebalancing how you give, cash, stock, appreciated assets, so generosity stays tax-smart.

Because while your heart’s in the right place, your strategy should be too.

More Options for Education Planning

If you’re already funding a 529 plan for a child or grandchild, you’ve probably been doing it for one reason: college.

But starting next year, the rules expand, and that changes the game.

Beginning in 2026, you can use up to $20,000 per year, per beneficiary, for K–12 expenses. And not just tuition, also tutoring, online curriculum, test prep, even educational therapy for kids with learning challenges.

That means families who value private school, specialized support, or just more choice in education now have a stronger planning tool.

It also means that if your 529 plan was funded with a long-term view, you may want to revisit how it fits into your shorter-term needs.

And for those thinking beyond college, toward vocational training, certifications, or post-high school credentials, the bill opens the door to use 529s for those costs too.

Bottom line: the tax advantages are broader, the use cases more flexible, and for families who plan ahead, education just got a little more customizable.

Business Owners, Take Note

If you run a business, own real estate, or generate income through a pass-through entity, the new law offers some of the most substantial and durable benefits we’ve seen in years.

Several key provisions have been made permanent, including the 20% Qualified Business Income (QBI) deduction. That’s the deduction that lowers the taxable income for sole proprietors, S corps, LLCs, and partnerships. If that’s you, this isn’t just a line item, it’s foundational.

At the same time, bonus depreciation is back at 100%, and Section 179 expensing has been expanded to $2.5 million. So if you’ve been thinking about making investments in equipment, vehicles, or other capital assets, this may be the time to act, not just to grow your business, but to reduce your taxable income in the process.

For real estate investors, this also means a window to revisit cost segregation studies, accelerate depreciation, and reconsider how your income is being characterized across properties.

And if your long-term strategy includes developing or investing in underserved areas, the Opportunity Zone rules just got new life, giving you the ability to defer gains, enhance basis, and potentially eliminate future capital gains altogether.

In short: If your business is your biggest asset, this is your reminder to make sure it’s also your most tax-efficient one.

One Last Shot at Green Energy Incentives

For years, the government has offered generous tax credits for homeowners who invest in energy-efficient upgrades, solar panels, heat pumps, insulation, new windows, and more.

That window is closing.

Under the new law, many of those incentives expire after 2025. And not in a vague, “we’ll see what happens” way, these provisions are scheduled to end, full stop.

So if you’ve been thinking about making upgrades to your home, vacation property, or rental units, this may be your final chance to get a federal tax credit worth up to 30% of the project cost.

That could mean thousands in tax savings if you act this year.

And while we don’t recommend rushing into a big-ticket project just to chase a deduction, we do recommend reviewing your broader property strategy. Because combining energy efficiency with tax efficiency? That’s a win worth planning for.

The SALT Cap Relief, But Don’t Get Comfortable

For those of you living in high-tax states, there’s a bit of breathing room coming, at least for a while.

Starting in 2025, the cap on state and local tax (SALT) deductions increases to $40,000 for joint filers. That’s a significant jump from the $10,000 cap we’ve been dealing with since 2018.

But before you get too comfortable, know this: it’s temporary.

This expanded cap is scheduled to last through 2029, and then it drops right back down. There are also income phaseouts that start at $500,000 of modified adjusted gross income for couples, and $250,000 for individuals. Those phaseouts increase gradually over the next few years.

In short: yes, it’s an opportunity. But it’s also a countdown.

So if you’re considering strategies like bunching deductions, charitable stacking, or shifting income across years to make the most of a higher SALT limit, now’s the time to plan. Because in a few short years, we’ll likely be having this same conversation all over again.

What Smart Families Are Doing Right Now

If there’s one pattern we’re seeing from families who are positioned well, it’s this: they aren’t waiting for things to “settle down” in Washington.

They’re moving early. Strategically. And with the long game in mind.

They’re updating estate plans before attorneys get overwhelmed. They’re modeling multi-year Roth conversions while tax rates are still low. They’re adjusting charitable strategies, reviewing education plans, and taking advantage of incentives before the door closes.

Not reactively. But proactively.

Because they understand something important, these opportunities have a shelf life. And by the time most people realize it, the window has already started to close.

So if it’s been a while since you revisited your tax or estate strategy… if your charitable giving hasn’t kept pace with the rules… or if you’re simply not sure whether you’re taking full advantage of this planning environment…

Then let’s talk.

This isn’t just about taxes. It’s about creating clarity for your future, and peace of mind for your family.

What to Make of One, Big, Beautiful Budget Bill?

Washington is moving forward with a new budget proposal that could reshape the tax landscape for years to come. And while the details are still being finalized, it’s crucial that you take the time to understand the broad strokes because they’re worth paying attention to.

Here’s what this means:

Lower Tax Brackets

At the center of the proposal is a permanent extension of the 2017 Tax Cuts and Jobs Act (TCJA).

These were the sweeping tax cuts that congressed passed during President Trump’s first term.

Those lower income tax rates were supposed to expire at the end of next year and this bill will now make them permanent.

What this means is that historically low tax environment we’ve been living in may stick around a bit longer, at least for the next four years.

Higher Itemized Deductions

The bill also adds in a few new deductions. There’s talk of expanding the child tax credit, offering tax breaks for things like tips and overtime, and even bringing back a deduction for interest on car loans.

One change that could really matter to higher-income households is a significant expansion of the deduction for state and local taxes, or SALT.

That’s because the TCJA capped SALT to $10,000 per household, which for many individuals in high-value zip codes, has been a thorn in their sides ever since.

Some Drawbacks

Now, not everything in the bill is a giveback. That’s because the Big Beautiful Bill would also roll back several recent reforms.

For example, remember the IRS’s free tax filing tool? Gone.

Or how about funding for IRS enforcement? Slashed.

And many of the tax credits for clean energy investments would also be reversed.

At the same time, there’s also a push to reduce spending on government assistance programs, like Medicaid and food benefits, by introducing stricter work requirements.

And while those cuts may not directly affect many affluent individuals, they nevertheless reflect a broader shift in where the government’s priorities are headed.

It All Comes at a Cost

When it comes down to it, all of these tax cuts come with a price tag.

Indeed, the Congressional Budget Office (CBO) estimates that the bill would add roughly three trillion dollars to the national deficit over the next decade.

And that’s not going unnoticed. Because credit rating agencies are already sounding alarms, with Moody’s downgrading the U.S. outlook just this past week.

So yes, there are plenty of changes packed into this bill, both good and some maybe not so good.

Some may feel beneficial in the near term, but others raise important questions about what’s sustainable, especially when it comes to how the government will eventually address its growing debt load.

What This Means for You

Now, if this bill passes (which it likely will) it will signal that the window for historically low tax rates may be closing.

How so?

Well, we’re in a rare moment where the rules are still in our favor. But that could change quickly.

But the fact is that the national debt is climbing at an unsustainable rate. At the same time, the budget deficit continues to grow with little sign of letting up.

And while this bill offers short-term tax relief to many high-earners, it does so at a long-term cost for the nation as a whole.

Eventually, future lawmakers may have little choice but to raise taxes to close the gap should borrowing costs rise .

That’s why this moment presents a planning opportunity, especially for families with meaningful income, sizable retirement assets, or a desire to transfer wealth efficiently.

If you’ve been thinking about a Roth conversion, accelerating future income into the present, unwinding a concentrated stock position, or gifting assets to heirs or charitable causes, this may be the most favorable tax environment we’ll see for quite some time.

Now, this isn’t about reacting to the news.

It’s about staying proactive and using what we know today to reduce uncertainty tomorrow because if lower tax rates are extended, that gives us more time to work strategically.

And if they’re not? Well, then we’ll be glad we took action while we still had time.

As always, we’re watching the developments closely. And we’re here to help you think through how this moment might apply to your financial picture.

If it’s been a while since we’ve reviewed your tax strategy, or if you’re wondering whether you’re making the most of this window, let’s talk.

Here's How Retirement is an Endurance Sport

In many ways, retirement isn’t a goal, it’s an endurance sport.

I had the opportunity to compete in the Pittsburgh Marathon over the weekend and wanted to share a quick thought that came to me during the race:

To run the race, you not only have to train, but you’ve also got to be able to adapt your plan to uncontrollable conditions on race day.

We’ve often been led to believe that retirement is a singular destination, that all you need to do is show up at the starting line with the right-sized nest egg, and you’ll be set.

The reality is, however, that you have to prepare not just to be able to show up for race day, but also to sustain yourself along the way.

It’s not just about putting in the miles to go the distance; it’s about pacing, nutrition, hydration and attitude.

In retirement, pacing becomes your spending plan. Nutrition and hydration represent efficiently growing your wealth and protecting it. And your attitude? That’s staying disciplined when markets and life throw challenges your way.

A misalignment in any of these components is likely to fundamentally change your race day experience.

Heading into my taper week ahead of last week’s race, I felt like my training was solid and was certain that by race day, my body and legs would be fresh. But wouldn’t you know it, I woke up on Sunday morning with a cold and a case of bronchitis.

That’s the paradox of endurance training: you can’t control the conditions, but it does equip you to press through them.

You change and test the variables weeks in advance so you know how your body might adapt to the unknown stresses of the event.

And once you’ve trained for an endurance sport, you’re likely forever changed.

Because more often than not, you haven’t prepared for a single race; after months of deliberate effort, you’ve forged a new way of life.

Many people believe retirement planning is about maintaining their current lifestyle for the next 20, 30 or 40 years. But the right plan doesn’t just preserve what you have, it expands your horizons. It equips you to live a lifestyle you may not have envisioned before, opening the door to entirely new races you hadn’t even considered.

You see, retirement success isn’t about reaching a single milestone.

It’s about having the right habits, resources, and mindset to keep going strong over the long run no matter where your journey might take you, even under the least optimal conditions.

Frankly, the conditions presented to me on my race day were certainly less than optimal. In the end, I finished the race, but not in the way I had hoped. Even so, my planning and training enabled me to envision an outcome (finishing the race) beyond current circumstances (illness).

Whether you’re already executing your retirement plan or still fine-tuning it, it’s worth asking: do I have the right systems, support, and strategies in place to thrive mile after mile no matter what life throws my way?

Humble Brag

I had a proud-dad moment this weekend as my oldest, Lily, ran her first timed 5K.

It wasn’t about speed or competition, it was about building grit.

We laughed, we cried, and ultimately, we crossed the finish line together.

Here’s to the first of many more races we’ll run side by side in the years to come.

The Market Feels Unstable — Here’s How to Stay on Track

There are times in market cycles when economic, geopolitical, and financial conditions converge in ways that create palpable uncertainty. In many ways, it can feel like standing on the precipice of an abyss.

Today, I would argue that we are in just one of those moments.

Often, it’s not just one event, but a cascade of interconnected developments that lead one to conclude that things are about to get bad.

History Often Rhymes

Early on in my career, it started with the failures of Bear Stearns and Lehman Brothers, the nationalization of Fannie Mae and Freddie Mac, and the bailouts of AIG and Citi, all of which signaled the fragility of the global financial system in 2008.

In 2020, early reports of health warnings, travel restrictions, and border closures eventually escalated into a near-total shutdown of the global economy, prompting widespread existential fear.

Now, in early 2025, we are experiencing heightened uncertainty as the resumption of trade wars with ambiguous objectives, shifting geopolitical alliances, and a retreat from post-war global institutions and a seeming move towards isolationism create a new political and economic reality. These shifts pose significant implications for the global economy and financial markets.

Needless to say, there is much to worry about in the current political, economic, and market environment. It’s enough to make any sane person want to bury their savings in their backyard.

How to Navigate the Uncertainty

That said, having been through multiple market cycles, being an avid student of history, and considering my background in macroeconomic strategy, I would like to share some thoughts on how to frame today’s environment and what you can do about it financially.

Firstly, I want to acknowledge that we are in the midst of an anxiety-provoking time in U.S. history. I am not going to discount the legitimate fear that many of us may be feeling right now amidst all the political tumult and economic uncertainties. This is a natural response.

With that said, when it comes to investing and the markets, it’s crucial to remember that we’ve been through similar challenges in the past. And with history as our guide, during times like these, it’s essential to remain committed to a long-term, disciplined investment strategy.

Make no mistake, what’s happening today will have significant implications for years to come.

Why It’s Essential to Stay Committed for the Long-term

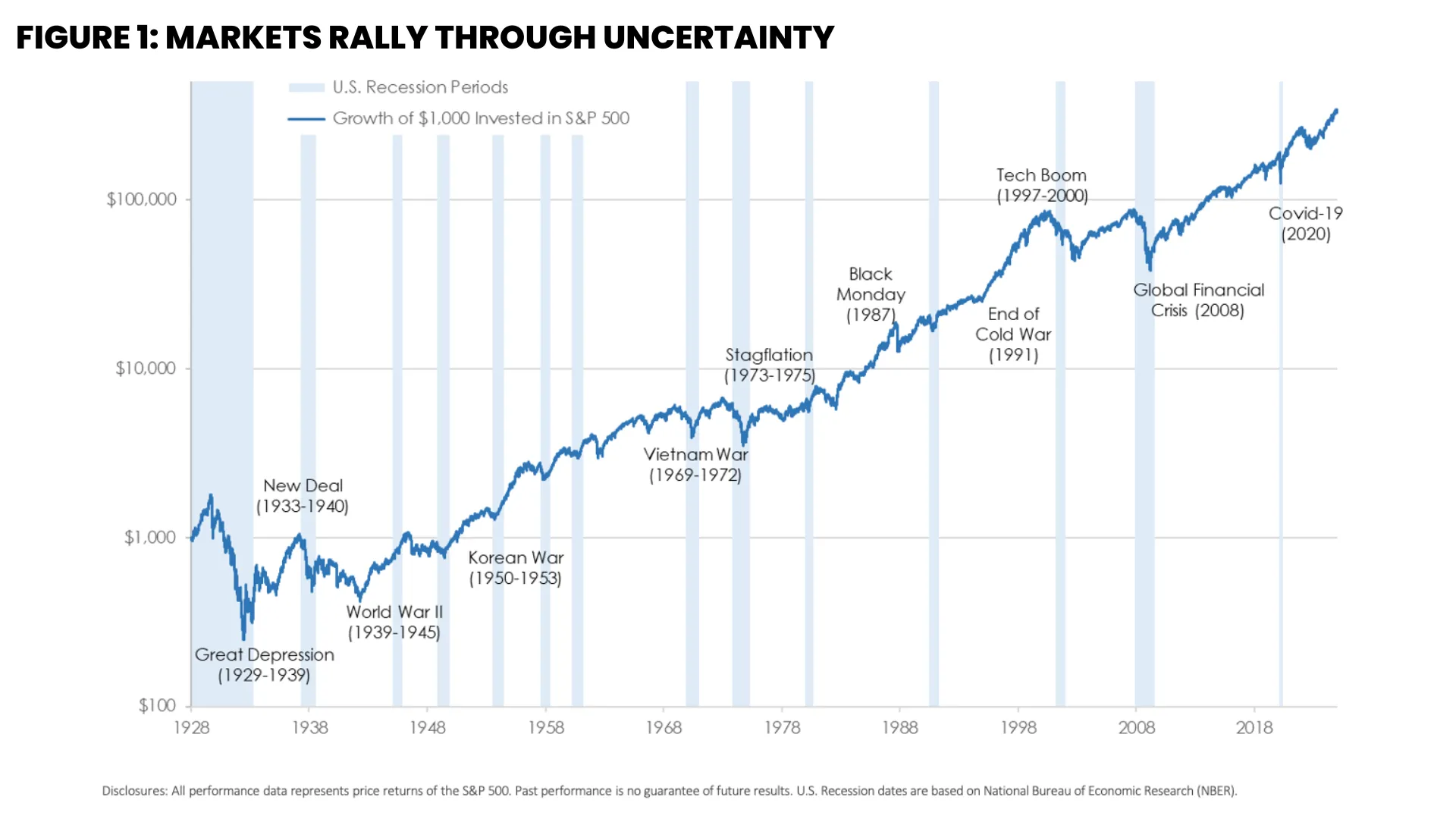

However, history has shown that, from a capital markets perspective, risk assets tend to sell off during political and economic inflection points, before eventually recovering. These ebbs and flows are a natural part of the market process when key narratives change.

In fact, over the past 100 years, there have been many paradigm-shifting political and economic events, but stock prices continued to march higher thereafter. This point is evidenced in Figure 1.

To be sure, financial markets, after periods of uncertainty, do eventually recover as investors eventually adapt to new political or economic paradigms. Indeed, as figure 1 illustrates, risk asset prices are naturally biased to the upside because if they weren’t, then investing would not be much different from gambling, would it?

Nevertheless, you might say that now is not the right time to be in the markets and that you would prefer to get out. However, history has also shown us that exiting the markets at the wrong time could lead to major disappointment down the road.

For example, Figure 2 shows how missing even the best five days over the past 20 years could have led to significant missed opportunities in the markets. Indeed, back in 2008, it is arguable that peak market fear occurred at the end of the year, just a few months before the market bottomed out in March 2009.

Similarly, in 2020, peak fear occurred in late February before markets bottomed out in March and then took off again in April. Therefore, trying to time the markets or get out when it feels like things are starting to get bad might work against you over the near- and long-term.

Practical Steps to Take

So then, amidst all of this, what should you do about it all?

Well, in uncertain times, many investors often find themselves torn between taking action and standing still.

Here are six key strategies to consider regardless of where you stand today:

#1 Know Your “Sleep Well Number” (Cash Management)

When it comes to cash management, during times like these, it is crucial to know your “sleep-well” number. Depending on where you are in your retirement journey, having enough cash on hand to cover six to eighteen months of living expenses is something to consider now.

Having this number available will enable you to avoid making knee-jerk decisions with your portfolio, enable you to stay committed to your long-term strategy and avoid selling assets at an inopportune time.

#2 Rebalance Your Portfolio

Rebalancing your portfolio now allows you to take some risk off the table. Markets have rallied handsomely over the past eighteen months, which means that your current holdings are very likely out of alignment with your strategic asset allocation.

Rebalancing includes taking gains from positions that have done well in your portfolio and adding to positions that are underallocated in your portfolio relative to your strategic allocation. This approach ensures that you’re not taking any more risk than necessary with your investments.

#3 Stick to Your Long-term Plan

When in doubt, stick to your plan. Remembering your long-term plan is essential during market uncertainty. That’s because it is easy to become distracted and search for a salve to relieve the unease in the near term when things start going off the rails.

However, it’s crucial to remember that your financial plan was created to help you navigate not just the good times, but also uncertain times like the ones we’re experiencing today.

#4 Reconsider Big-Ticket Purchases

If you are contemplating purchasing a new home, car, or other big-ticket item, you may want to consider holding off on any moves for the next few months. This approach will allow you to preserve cash and ensure that you are not locking yourself into a decision at an inopportune time.

#5 Sharpen Your Pencil

At the same time, it is worth sharpening your pencil. Warren Buffett is known to have said, “Be fearful when others are greedy, and greedy when others are fearful.” Depending on your living situation and cash position, fear-driven market sell-offs often provide opportunities to purchase assets at a discount.

If you are in a solid cash position, keeping an eye out for favorable buying opportunities once we have more clarity on the political and economic environment could be worthwhile.

#6 Consider Tax Planning Opportunities

Finally, market sell-offs also present an opportune time for tax planning. And a key tax planning approach includes completing a Roth conversion. That’s because lower portfolio values often translate to lower taxable values. Remember, Roth conversions are not just a fourth-quarter tactic but a year-round opportunity.

Similarly, market downturns can present opportunities for tax-loss harvesting. This approach involves selling stocks at a loss and buying a similar but not identical asset. Even if you do not have gains to offset the losses, you can carry forward the losses as a tax asset to offset future capital gains.

The Big Takeaway

When it comes down to it, the big takeaway from an investment perspective is to stay invested for the long term even though the near term seems so uncertain. While we may be headed for a dark period in the months ahead, I am reminded of how essential it is to remain optimistic.

Viktor Frankl, a Holocaust survivor and author of the book, “Man’s Search for Meaning”, points out in his work that those who adapted and sought meaning in each moment, especially in trying times, had greater ability to endure trials and uncertainty than those who did not.

Make no mistake, we are likely headed for some very trying times in the weeks and months ahead. From a political and social perspective, we do not have a roadmap for navigating what lies ahead, which means we will have to take things one moment at a time. As difficult as that may be, however, finding purpose and direction in uncertain times has always been a defining trait of those who successfully emerge from such events.

What’s more, from a financial perspective, history has repeatedly shown that uncertain times like these often create opportunities for those who stay the course. That’s why having a solid financial plan and a disciplined investment strategy is essential now more than ever. While the near-term outlook may be uncertain, remaining objective and committed to a well-thought-out financial plan continues to be the best way forward.

Five Reasons Why a Roth Conversion Might be Right for You

You've done everything right: you've worked hard, built a successful career, and saved for the future. But there's one piece of the puzzle that could quietly erode your wealth if you don't plan for it: taxes.

Retirement isn't just about how much you've saved, it's about how much you get to keep. And if most of your retirement savings are in tax-deferred accounts like a 401(k) or traditional IRA, the IRS has plans for that money. That’s why tax planning is crucial now more than ever.

In fact, when it comes to IRAs, those withdrawals you take in retirement will be taxed as ordinary income, and when you turn 75, Required Minimum Distributions (RMDs) will force you to take money out, even if you don't need it.

But here's the thing: what if you could pay taxes on your own terms?

What if you could lock in today's lower tax rates, reduce your future tax burden, and create a more flexible income strategy for retirement?

That's where a Roth conversion comes in.

In fact, by converting a portion of your tax-deferred retirement savings into a Roth IRA, you pay taxes on that money now and at a rate you can control.

In return, your Roth IRA grows tax-free, and when you need to withdraw in retirement, there are no additional taxes owed.

What's more, there are no RMDs, no surprise tax bills, and a better plan for passing wealth to your heirs when it comes to your Roth IRA.

But the big question here is is it the right move for you?

Well, the answer depends on several factors, including your current and future tax rates, your retirement timeline, and how you want to structure your income.

So then, let's break down five key reasons why a Roth conversion could be one of the smartest financial decisions you make in 2025.

#1 Would You Rather Pay Taxes at Today's Rates or Risk Higher Rates in the Future?

First things first, would You Rather Pay Taxes at Today's Rates or Risk Higher Rates in the Future? Think about it: do you believe taxes will be lower in the future? Or do you think they'll go up?

If you're like most people, you're betting on higher taxes. And that's not just a guess. The tax cuts currently in place are set to expire after 2025, which means tax rates for high earners could rise significantly. If nothing changes, the top tax bracket will jump from 37% back up to 39.6%.

And even if the Tax Cuts and Jobs Act is extended, there's no guarantee that tax rates won't go higher in the future given our country's massive debt burden.

Indeed, with rising government debt and shifting tax policies, higher taxes could become the norm. So then, if you wait to withdraw from your tax-deferred accounts in retirement, you could find yourself paying much more in taxes than if you had acted earlier.

That's where a Roth conversion lets you take control. Because instead of waiting to see what happens, you can lock in today's lower rates and create tax-free income for the future.

How so? Well, let's say you convert $500,000 from a traditional IRA to a Roth IRA today while you're in the 24% tax bracket. In this case, you'll likely owe $120,000 (24% of $500,000) in taxes today.

Now, let's assume you wait 10 years, but by then, higher tax rates push you into the 35% bracket. With that same amount, assuming no growth of your savings, you'd likely owe $175,000 (35% of $500,000).

That's a $55,000 difference, just for waiting.

And here's where it really adds up: if that $55,000 in tax savings were invested instead at an average 7% annual return, it could grow to over $400,000 in 30 years, all because you converted when rates were lower.

So then, by making a move today, you're not just reducing taxes, you're potentially adding hundreds of thousands of dollars to your retirement savings all by paying some tax today, to save a lot more in the future.

#2 Do You Want to Avoid Required Minimum Distributions (RMDs) That Could Inflate Your Tax Bill?

The next thing to consider when it comes to determining whether a Roth Conversion is right for you is whether you're comfortable paying your anticipated RMDs.

Now, you may not need the money, but the IRS does.

That's because by the time you're age 75, you'll be required to start withdrawing money from your traditional IRA or 401(k), whether you want to or not. And these Required Minimum Distributions (RMDs) aren't just forced withdrawals, they're taxable income.

Now, depending on how large your retirement accounts are, RMDs can push you into a higher tax bracket, trigger higher Medicare premiums, and cause more of your Social Security benefits to be taxed.

That's where a Roth conversion can help you get ahead of this problem. Because Roth IRAs aren't subject to RMDs, converting today means you keep more control over your income in retirement, instead of letting the government decide for you.

So then, how does this work? Well, let's say you're 65 years old with a $2 million traditional IRA, and it grows at 6% per year. Here's what happens if you don't convert any of it to a Roth.

By age 75, your RMD starts at $87,591 per year. But each year, Uncle Sam forces you to take out more and more money from your IRA each year. So then, by age 90, your RMD balloons to $258,741 per year.

That means you'll be withdrawing more and paying more in taxes, whether you need the money or not.

However, if you convert a portion of your IRA to a Roth before RMDs kick in, you might be able to reduce your future tax burden and avoid being forced into withdrawals you don't want to take.

Put a different way, this isn't just about tax savings, it's about having more flexibility in how you use your money in retirement. So then, wouldn't you rather make that decision yourself or have Uncle Sam force you to take money out of your savings? That’s where prudent tax planning comes into play.

#3 Do You Want to Leave More to Your Heirs Without a Tax Burden?

You've spent a lifetime building wealth, and now you're preparing to pass it on. But do you really want the IRS to take a big chunk of what you leave behind to your children?

Because here's the thing: if your heirs inherit a traditional IRA, they'll be forced to withdraw the full balance within 10 years, and every dollar they take out is taxed as ordinary income.

So then, if they're in their peak earning years, those withdrawals could push them into a much higher tax bracket, costing them hundreds of thousands in unnecessary taxes.

A Roth IRA, on the other hand, passes on tax-free savings to your heirs, and no forced distributions for a spouse. In other words, no income taxes for your kids and no surprises when they inherit your wealth.

How does this work? Well, let's compare a $1 million traditional IRA and a $1 million Roth IRA passed down to your children.

If the money stays invested for 30 years at 7% annual growth, here's what happens. With a traditional IRA, your heirs must withdraw all funds within 10 years, and assuming they invest it, after taxes, it grows to $5.8 million.

However, if you left behind the same $1 million in a Roth IRA, it's possible that the portfolio would grow tax-free to $7.6 million and be available for tax-free withdrawals. That's a $1.8 million difference, all because of taxes.

Even if your heirs don't need the money right away, a Roth IRA lets them delay withdrawals until it makes sense for them, avoiding tax spikes and keeping more of your legacy intact.

So then, if you're planning to pass on wealth, the question is simple: Do you want your money to go to your family, or to the IRS?

#4 Could a Roth Conversion Help You Save on Medicare and Social Security Taxes?

Most people don't realize that their Medicare premiums and Social Security benefits are tied to their taxable income. In fact, the more income you report in retirement, the more you could pay for healthcare and the less of your Social Security you'll actually get to keep.

How does this happen? Well, it happens because withdrawals from a traditional IRA count as taxable income. So then, even if you don't need the money, those withdrawals could push you above key income thresholds, and trigger higher Medicare premiums which could make up to 85% of your Social Security benefits taxable.

A Roth IRA on the other hand avoids this issue because withdrawals don't count as taxable income. That means you can take money out as needed without pushing yourself into a higher tax bracket or triggering unexpected penalties.

How so? Well, let's take a couple who are 67 years old and are planning to retire soon. They have $1.5 million in a traditional IRA and $60,000 in combined Social Security benefits per year.

Now, if they start taking $80,000 per year from their IRA, they're likely to face a few complications. First, their Medicare premiums likely will increase due to IRMAA (Income-Related Monthly Adjustment Amounts). Next, they could find that up to 85% of their Social Security benefits become taxable and so, their total tax bill and healthcare costs jump by over $112,000 over their retirement.

Now, let's say this same couple converts $300,000 over three years into a Roth IRA before claiming Social Security and Medicare. In this case, their taxable income stays below Medicare surcharge limits, their Social Security remains largely untaxed and they save over $112,000 in combined healthcare and tax costs.

So then, this isn't about avoiding taxes, it's about planning ahead, especially when it comes to balancing retirement income with goverment benefits. From this perspective, why give more to the IRS when you can keep more for yourself through prudent tax planning?

#5 Are You Planning a Move to a Lower-Tax State?

Finally, where you live in retirement matters a lot, especially if you're considering a Roth conversion.

In fact, if you're planning to move from a high-tax state like California or New York to a no-income-tax state like Florida, Texas, or Nevada, the timing of your Roth conversion could save you tens, if not hundreds of thousands of dollars in state taxes.

That's because when you complete a Roth conversion, you'll also end up paying state taxes in the year you convert. So then, if you do a Roth conversion while living in a high-tax state, you could owe state income tax on that conversion. But if you wait until after you move, you could pay zero state tax on the conversion.

How does this work? Well, let's say you have a $1.5 million traditional IRA and are moving from California to Florida. You decide to convert the full amount before moving and California state tax (13.3%) on $1.5M conversion leads to $199,500 owed in taxes.

Now, let's say you wait until after you move to Florida where you pay no income tax. Here, you could effectively save $199,500 in taxes just by planning your move before coverting.

But what if you plan to stay in a high-tax state? A Roth conversion might still be a smart move, especially if state tax rates are expected to rise. In other words, locking in today's rates could still be a win.

Regardless, if you're thinking about moving, or even if you aren't, state taxes should be part of your Roth conversion decision. Because when it comes to taxes, timing is everything.

So, What's Your Next Move?

Let's be honest. Nobody enjoys thinking about taxes. However, whether you think about them or not, you will pay them on way or another. So then, the real question is not if you will pay taxes, but when and how much.

Right now, you have an opportunity to do some prudent tax planning. Tax rates are at historic lows, and you still have time to plan. Most importantly, you have the ability to decide what happens next, which might not always be the case.

So what's your plan?

Are you going to wait and hope the tax code works in your favor? Are you going to let the IRS determine how much of your wealth stays with you and how much goes to them? Or are you going to take control of your financial future while you still can?

Here is what we know. Tax rates are expected to rise in the coming years. Required Minimum Distributions could force you to withdraw more than you need, potentially pushing you into a higher tax bracket. If you plan to pass on wealth, your heirs could face a significant tax burden unless you make a plan.

Medicare premiums and Social Security taxes can increase unexpectedly, but with the right strategy, you can avoid these unnecessary costs. And if you are planning to move to a state with lower or no income tax, the timing of your Roth conversion could save you thousands of dollars.

That sounds like a lot. But here's the good news.

You do not have to figure this out on your own. You have time to plan. You have the ability to make smart decisions today that will give you more financial freedom in the future. Most importantly, you have options.

That is why I am here. Let's run the numbers, talk through your options, and build a strategy that works for you. The best time to plan for your future is today.

If you are ready to take the next step, schedule a call and let's get started.

Market Update: Geopolitical Tensions & Your Financial Plan

Given the deeply concerning headlines about the conflict in the Middle East, I imagine this is a time of worry for you as it is for many.

While the violence and loss of life is distressing, I want to reassure you that your financial plan is designed to weather turbulence, and I’m watching the situation closely on your behalf.

There are still many open questions about how the geopolitical situation will unfold, and near-term market volatility is likely amid the uncertainty.

Some Historical Context

However, in times like these, the chart below offers important historical context in that the U.S. has navigated many challenging periods in the past, so staying focused on your long-term plan is critical.

Indeed, history has shown the wisdom of sticking to your investment discipline and not overreacting to short-term events, difficult as that can feel in the moment.

What to Do Next

As a next step, I would recommend reviewing last week’s email (see link below) because the key takeaways bear repeating:

https://franklinmadisonadvisors.com/cio-corner/market-volatility-heres-what-to-do-about-it/

Rest assured, if I’ve personally worked on your plan with you, your portfolio is built to withstand choppy markets, and we are monitoring developments diligently and ready to make prudent adjustments if warranted.

If You Still Need Help

Ultimately, I'm here as a resource and sounding board for you.

Please don't hesitate to schedule a quick call or reply to this email with any specific questions or concerns you have, I'm happy to talk things through and revisit any details of your plan so you can feel more confident.

While the macro situation is troubling, I have deep faith in the resilience of our country and economy. We will get through this, and I remain optimistic about the long-term future.