More Money, More Mess: The Hidden Cost of Uncoordinated Wealth

Many people assume that as their net worth grows, their financial life gets simpler. In practice, the opposite is often true. Growing wealth tends to create a quiet kind of clutter that doesn't show up on a balance sheet, but shows up in missed opportunities, unnecessary taxes, and decisions that no longer match the life you're living today.

This clutter rarely announces itself. It builds slowly, one account and one decision at a time, until it becomes difficult to see how all the pieces fit together.

How Financial Clutter Builds Over Time

Financial clutter isn't usually a sign of poor discipline. It's often a sign of a life that has moved forward. You changed jobs, so you left a 401(k) behind. You inherited an IRA. You opened a brokerage account at one firm, then another at a different firm because someone recommended it. You bought a life insurance policy in your thirties, and another one later for estate purposes. You worked with a CPA, then a different CPA, then an attorney who drafted a trust your current advisor has never reviewed.

Each of those decisions made sense at the time. The issue is that no one stepped back to ask how they all fit together. Most clutter isn't the result of bad advice. It's the result of good advice given in isolation, year after year, without a plan to connect the pieces.

What Coordinated Planning Does

Turning clutter into clarity isn't a matter of starting over. It's a matter of giving every piece of your financial life a defined role and making sure those roles work together. A coordinated plan does a few specific things that piecemeal decisions can't.

It gives each account a job. Some assets are better suited for current income, others for long-term growth, and others for heirs or charitable goals. When each account has a clear purpose tied to the overall plan, day-to-day decisions become easier and more consistent.

It sequences withdrawals with taxes in mind. The order in which you draw from taxable, tax-deferred, and Roth accounts can meaningfully affect your lifetime tax bill, your Medicare premiums, and how long your portfolio lasts. A coordinated plan looks at these decisions together rather than one year at a time.

It uses planning windows that are easy to miss. The years between retirement and the start of Required Minimum Distributions can be one of the most valuable periods for Roth conversions, capital gains planning, and charitable strategies. Without a plan, those years often pass without being fully used.

It revisits the pieces you may have forgotten. Older insurance policies, annuities, and legacy accounts sometimes continue to serve a purpose, and sometimes they no longer do. A coordinated review asks whether each one still fits, and what to do if it doesn't.

It aligns your accounts with your estate plan. Beneficiary designations often override what your will or trust says. A coordinated plan makes sure the titling of your accounts, the designations on retirement plans and insurance, and the structure of your estate documents all point in the same direction.

The Big Takeaway

A well-built plan doesn't add. It organizes. It ties your investments, tax planning, insurance, and estate documents together into a single picture of the life you want to fund and the legacy you want to leave. The goal isn't to own more. It's to make sure what you already own is working together.

Every household's situation is different, and the right path forward depends on your goals, your family, and how you want retirement and legacy to look. Our goal is to help you turn financial clutter into clarity, so the wealth you've worked hard to build can serve the life you actually want.

Mega Backdoor Roth Might Not Be Your Biggest Tax Problem

You've worked hard to build a sizeable retirement account. Now you’ve heard about a strategy called the mega backdoor Roth, and it sounds like the next smart move.

Maybe it is, but before you redirect another dollar, there's a question worth asking first, “is where you put your next dollar actually your biggest tax problem?”

For a lot of people I work with, the answer is no.

What the Mega Backdoor Roth Actually Does

Here's what I mean. The mega backdoor Roth is a legitimate tax planning tool. That’s because it allows you to contribute after-tax dollars to a 401(k) and then convert those dollars into a Roth account, creating a larger pool of money that can grow tax-free. For the right person in the right situation, it is absolutely worth pursuing.

But the strategy is often discussed in isolation, as if the only question on the table is where to put new savings. And for people who already have large pre-tax balances sitting in traditional IRAs or old 401(k)s, that framing misses the real issue.

The real issue is what’s already in the account.

The Hidden Tax Burden Inside Your Pre-Tax Retirement Accounts

How so?

Well, when you contribute to a traditional IRA or a pre-tax 401(k) over a thirty-year career, you build up a balance that feels like wealth because it is wealth. But it is wealth with a tax bill attached to it, and that bill does not come due until you start taking money out.

And for most people, that moment arrives in retirement, either by choice or by requirement. The IRS calls those requirements RMDs, or required minimum distributions, and they begin at age 73. At that point, the government sets a minimum amount you must withdraw each year whether you need the income or not.

This is where large pre-tax balances can quietly become a tax problem in disguise.

How RMDs Can Increase Your Tax Burden in Retirement

As those balances grow over time, the RMDs attached to them grow too. And when you layer those distributions on top of Social Security, a pension, or other retirement income, you can find yourself pushed into a higher tax bracket than you expected.

If that’s not enough, it can get even more complicated. Higher taxable income in retirement can trigger IRMAA surcharges, which are income-based adjustments to your Medicare Part B and Part D premiums.

It can also affect how much of your Social Security benefit is subject to tax and ultimately, it can reduce your flexibility to make smart financial decisions, because so much of your income is no longer optional.

So then, when someone with a seven-figure traditional IRA asks me whether they should pursue a mega backdoor Roth for their new savings, my honest answer is this that the strategy might help at the margins, but it is not addressing the source of your future tax pressure.

It’s putting a fresh coat of paint on a house that needs foundation work.

Why Partial Roth Conversions May Deserve Greater Priority

So what’s the solution here?

Well, the strategy that deserves more attention in situation with high balance pre-tax accounts is the partial Roth conversion. Rather than focusing only on where to direct new dollars, a partial conversion takes money that already exists in a pre-tax account and moves it into a Roth account.

You pay the tax today, at a rate you can plan around, and in exchange you reduce the size of the account that will generate mandatory distributions later.

When done thoughtfully over several years, especially in the lower-income years between retirement and when RMDs begin, a Roth conversion strategy can meaningfully reduce your future tax burden and give you back flexibility you did not know you were losing.

How to Think About Both Strategies Together

Here’s the key takeaway: the mega backdoor Roth still has a place in this conversation.

If you have the cash flow to fund it and you have already addressed the larger pre-tax balance issue, positioning new savings for tax-free growth is a smart move.

But it is a second step, not a first one.

The bigger point is that tax planning in retirement is not just about optimizing where you put your next dollar, it’s about understanding the full picture of what you have already saved and what that savings will cost you when it comes out.

And the best time to address that future tax liability is before it becomes unavoidable. If your pre-tax balances are growing faster than your plan accounts for, that conversation is worth having now.

Here’s What to Make of Recent Headlines

It is hard to think about investing, planning, and the future when it feels like the social fabric that has held this country together is fraying in real time.

If you have found yourself distracted, unsettled, or even angry by the headlines around immigration enforcement, you’re not alone. Recent reports over the past few weeks have left a lot of Americans asking, “what’s happening to us?”

And yet, it’s tempting to shrug and say, “This is politics, it has nothing to do with my retirement plan.”

However, this time, I don’t agree.

Not because every headline turns into a market event because most headlines don’t.

It’s because the issues underneath these headlines touch on two things markets care deeply about, and that’s trust and stability.

When trust and stability are strong, capital flows in. When trust and stability are questioned, however, investors begin to demand a higher price for taking risk.

Sometimes that shows up as higher borrowing costs, sometimes it shows up as more volatility and sometimes it shows up as both.

Ultimately, the headlines could be a symptom of a broader trend unfolding, so here’s what I’m watching.

Two channels I am watching

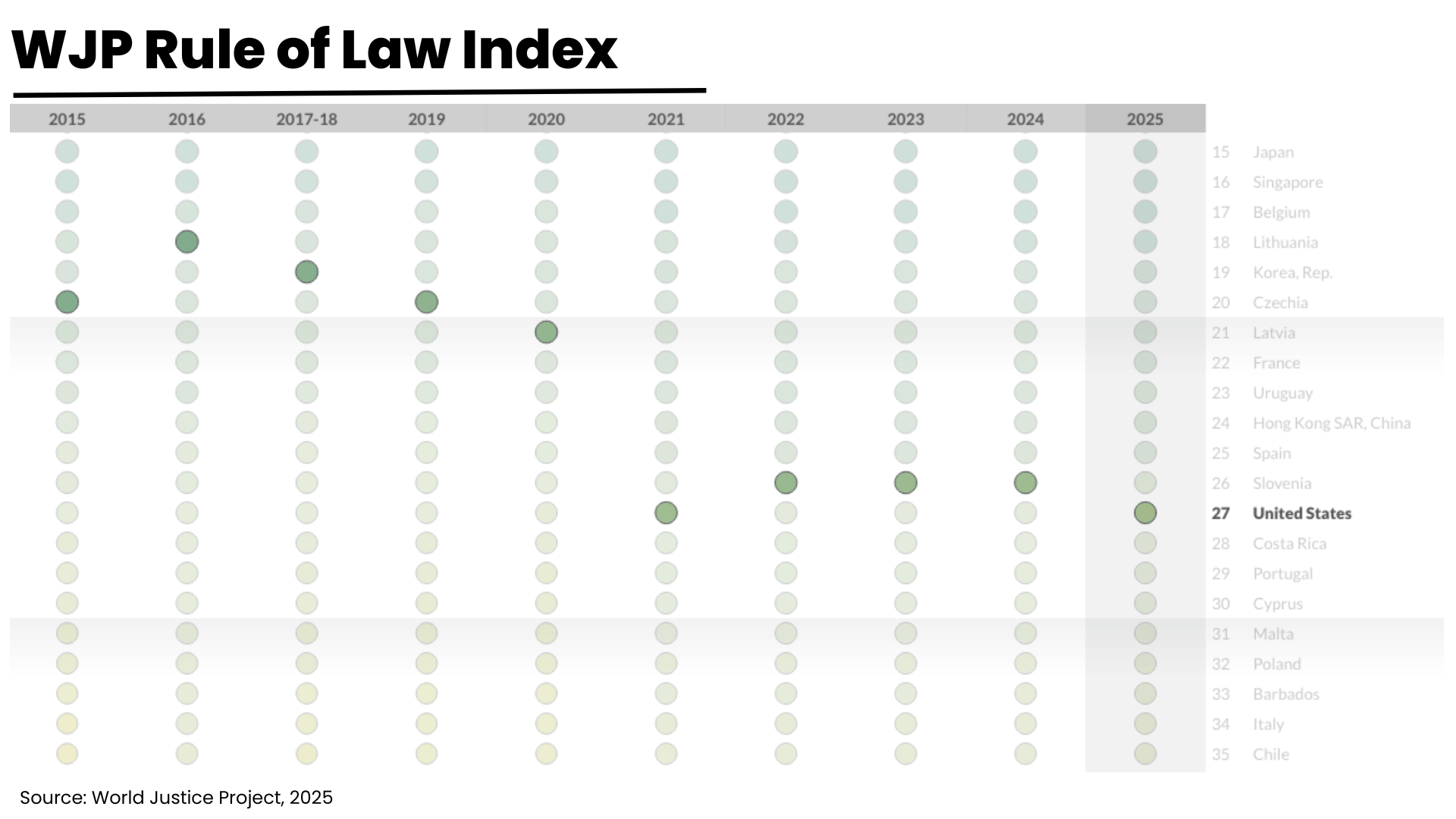

First, it’s crucial to note that the United States is a premier destination for global capital.

And one of the quiet advantages the U.S. has had for decades is not simply innovation or scale, it’s governance and rule of law.

It’s the idea that rules apply consistently, contracts are enforceable, and institutions are resilient. That rules-based order is part of why global investors have been willing to allocate so much money here, even when our politics are loud.

That’s also why perceptions matter because markets don’t need perfection, they need confidence that the basic institutional guardrails will stay in place.

Watching the Fed

A good example is what’s happening with the Federal Reserve.

The Fed’s credibility has always rested on independence, and the belief that policy decisions are aimed at long-term stability, not short-term political goals.

With that said, as leadership transitions approach, it is reasonable for investors to pay closer attention to whether that independence looks protected or pressured. That’s because even the perception of shifting incentives can change how the world prices U.S. assets.

The other example is rule of law. And what do we mean here by rule of law?

Well, it’s the difference between “I own this asset” and “I own it until someone with power decides otherwise.”

Throughout my career, this has been one of the key risks we evaluate when looking to invest in emerging markets or politically unstable regions. Until recently, it has not been a risk most investors felt they had to price heavily in the United States.

Now, it’s starting to change, even at the margins.

Because when headlines start to raise questions about fundamental rights, due process, and institutional constraints, that’s the sort of thing global capital markets pay attention to.

Not instantly, and not always dramatically, but it’s the kind of thing that makes global investment policy committees sit up and begin reviewing their asset allocation decisions.

The Impact on Prices

The second thing I’m watching is how today’s events impact the economic structure behind labor, growth, and prices.

This is a longer-term trend, to be sure, but the seeds being planted today, if not mitigated, could be of consequence years down the line when it matters most in retirement.

Because here’s the thing: What has made America exceptional for so long is that people have been willing to come here, work, build, and contribute to build a new life.

That is the American story, whether your family arrived centuries ago or last generation.

And so, if the U.S. becomes a less attractive destination for legal immigration, then the economic consequences, like labor shortages, don’t stay contained, they could naturally flow into the prices we pay for goods and services.

You can see the contours of this development already unfolding.

Indeed, industries that rely on skilled labor and steady hiring pipelines, like construction, healthcare, and engineering, are sensitive to labor disruption. Add uncertainty for workers on legal pathways, including work visas and student visas, and you risk shrinking the pool of talent over time.

Yes, automation will keep advancing. And AI, robotics, and process improvements will absolutely offset some labor pressure.

Still, there are many jobs where a human eye and a human touch are not optional, at least not yet. If labor supply tightens faster than technology can replace it, the effect is that costs rise.

That is the simplest economic math on the board.

In practical terms, that could mean higher prices in areas that already feel stretched, including food, housing-related labor, and medical services. It could also mean inflation settling at a higher level than the 2% world many retirement models quietly assume.

So what does this mean for your plan?

It’s essential to note here that I don’t say any of this to be dramatic. I say it because looking away is not a strategy. Ignoring reality is not a plan.

If institutional stability is eroded, you could see a world where markets demand a higher risk premium for U.S. assets. And that could translate into lower valuations, more volatility, and higher interest rates than people expect.

And if labor constraints persist because determined, talented individuals are less interested in coming to the United States, well, you could see a world where inflation runs hotter for longer, which might raise your long-term cost of retirement.

Taken together, both of those outcomes matter because they touch the growth of your assets and the purchasing power of your withdrawals.

The good news is that our planning work is not built on best-case assumptions.

We already model conservative growth rates and higher inflation because surprises are not rare, they are the norm.

So then, in moments like this, the question is not “can we predict what happens next?”

But rather, the question should be “is my plan built to endure a range of outcomes, including uncomfortable ones?”

That’s what we will keep focusing on.

What can you do right now?

We can’t control the headlines.

However, we can control how prepared we are for the changing developments.

At this moment in time, it’s worth paying attention to, even if it’s uncomfortable.

Because the things that feel distant, political, or abstract can become personal through our portfolios, prices, job markets, interest rates, and the stability of the institutions we all rely on.

If you have questions about how this environment could affect your plan, now’s a good time to revisit assumptions, stress-test scenarios, and make sure your strategy matches the world as it is, not the world we wish it were.

2025 Year-in-Review: A Market That Felt Uncertain, Yet Finished Strong

If I had told you at the start of this year what the headlines would look like, you probably would have guessed the market would struggle.

Trade tensions. Tariffs. Policy whiplash. Growth scares. Interest rates. Post-election political noise.

And yet, here we are near year-end with stocks having logged another record-setting year.

So, what happened? And more importantly, what should we take from it as we head into 2026 with your plan intact?

The Thread That Ran Through the Whole Year: Policy Didn’t Just Matter, It Moved Markets

Well, after the election and into the January inauguration, markets began pricing in a new policy direction. Early optimism around pro-growth expectations gave way to something more complicated and that’s uncertainty.

And the fact of the matter is that uncertainty does not just make headlines feel louder. It changes behavior as consumers hesitate spending, businesses delay investing and market participants reprice risk.

And that policy uncertainty became the steady drumbeat behind most of 2025’s major moves.

Q1: From Optimism to a Valuation Reset

Now, to understand where we’re going, we often need to understand where we came from.

Indeed, you’ll likely recall that the S&P 500 hit an all-time high in February before markets took a breather.

So, what changed?

Well, simply put, valuations reset. What this means is that many investors became less willing to pay top dollar for future earnings as plans out of Washington led to more uncertainty. And when the market’s mood shifts, prices can fall even if fundamentals are still solid.

At the same time, the mega-cap tech stocks that carried the market in 2024 became a drag in early 2025. In other words, yesterday’s winners stopped winning, at least for a season.

Then we got the Q1 GDP headline that the economy shrank, which got the market’s attention.

In fact, the data put a spotlight on why growth dipped, and a big part of the answer came from behavior around tariffs.

To be sure, what the data showed was that imports surged as businesses and consumers pulled forward purchases to get ahead of higher prices. Government spending also appeared to fall on a quarter-to-quarter basis, which mechanically dragged GDP lower.

In other words, the data was real, but the story underneath it was nuanced.

And that is why we kept coming back to the same point: the economy can slow without breaking, and markets can fall without it meaning that something is fundamentally wrong.

April: The Market Tantrum (and the Quick Recovery)

Now, if Q1 felt uneasy, then early April felt like panic.

That’s because a sweeping tariff announcement from the Trump administration escalated the trade war narrative, prompting the S&P 500 index to drop more than 10% in a week.

But where things got interesting is that shortly thereafter, the administration paused tariffs, and the market clawed back most of the decline by month-end.

This behavior was essentially a preview of what we saw repeatedly this year which included policy headlines creating short-term market drama that moved faster than the underlying economy.

So then, by mid-year, we had lived through two completely different quarters.

Q1 was caution. Q2 was rebound.

Indeed, markets found their footing as some tariff fears proved less disruptive than expected, headlines softened, and corporate earnings held up better than many feared.

But even then, things still did not feel settled. For many of us, it felt like there was still another shoe to drop. That’s because markets can recover faster than confidence does.

Nevertheless, the market snapped back near highs while sentiment stayed shaky, in part because tariffs were paused in 90-day windows and deadlines kept moving. While this approach didn’t lead to a concrete resolution to trade uncertainties, it did give markets breathing room.

In other words, the real story wasn’t “everything is fine.” The story was, “markets are pricing in a middle path, and they’re doing it before the human heart feels ready to believe it.”

Q3: New Highs, Softening Labor, and a Fed That Finally Moved

Either way, investors began looking past the uncertainty and in the third quarter, markets pushed to new highs again.

Earnings stayed resilient as AI continued to dominate headlines, trade tensions eased somewhat as tariff deadlines were repeatedly pushed out, and market breadth improved.

What this means is that more parts of the market contributed to the overall rally, including small caps which finally broke above their old 2021 highs.

These optimistic moves in the market happened even as incoming data showed that the US economy was in transition. That’s because by late summer, labor market data softened as unemployment rose to around 4.3% and job growth slowed meaningfully.

And that shift mattered because it changed the Federal Reserve policymakers’ position on interest rates.

Indeed, after a long pause, the Fed cut rates in September, framing it as a risk-management move to keep the expansion on track, not an emergency response.

And this distinction is important because a “panic cut” feels like trouble, while a “risk-management cut” feels like a central bank trying to extend the runway.

Q4 Into Year-End: Record Highs… With a Quieter Story Under the Surface

No matter how you cut it, it has not felt like a normal year. And yet the market has quietly spent a lot of time at record highs, with the S&P 500 setting dozens of new all-time highs.

But the more important detail is that even with breadth improving from earlier in the year, much of the strength has been narrow.

That’s because AI has remained the dominant theme, with enormous investment flowing into chips, cloud infrastructure, and data centers. Those moves have boosted major indexes because the biggest companies have the biggest weight.

So, you can have a market that looks strong in headlines while the “average” stock feels far less exciting.

And that disconnect is why the emotional experience of investing rarely matches the scoreboard.

Even so, this is why we keep emphasizing two principles at the same time throughout the course of the year: Stay invested and stay diversified.

The Planning Lesson of 2025: Don’t Waste a Good Rally, and Don’t Fear the Next Dip

To be sure, one of the most practical messages we repeated this year was that pullbacks are not unusual, and in fact, they are to be expected.

Dips of a few percent happen regularly, and 5% corrections happen multiple times in many years.

So, what do we do with that?

We prepare.

And that preparation is not pessimism. It’s how you participate in the upside without losing your footing when markets take a breather.

So then, as we look to the year ahead, we continue to home in on two key principles:

- Cash reserves

Working investors: typically 6–9 months.

Retirees or near-retirees: often 12–18 months.

Because the last thing you want in a downturn is to be forced to sell at the wrong time. - Tax-aware opportunities when markets dip

Market weakness can create windows for strategies like Roth conversions and other planning moves that can improve long-term after-tax outcomes.

Remember, the goal is not to predict the next pullback. The goal is to know what you will do when it comes.

A Look Ahead to 2026: AI Optimism, Real Opportunity, and Real Risk

As we step into 2026, it helps to start with a simple expectation that the economy does not need to be great for your plan to work.

Right now, the most reasonable base case is continued expansion, just not a boom like parts of the post-pandemic expansion. Think steady but unspectacular growth that looks more like low two percent than the kind of upside that makes every risk feel justified.

Indeed, the first half of 2026 may also feel slower as a few of the same forces we wrestled with in 2025 keep showing up. Tariffs are still a drag at the margin, more folks are choosing to retire and the productivity boost everyone wants to see usually arrives later than the market hopes.

Inflation Concerns Linger

And while growth is one immediate concern, inflation is the second part of the equation where investors can get tripped up. That’s because inflation does not have to reaccelerate to create stress. It simply has to stay sticky enough that the Federal Reserve cannot pivot quickly and aggressively the moment markets get uncomfortable.

In that environment, rate cuts can still happen, but they are more likely to be measured than dramatic. And this matters because “easy money” is not the same tailwind it was in prior cycles, and it means returns tend to feel more earned.

So then, when you put those pieces together, you get a familiar setup historically that includes a normal economy, inflation that stays above 2%, and a Fed that has less room for deep cuts below what it considers neutral.

Market Outlook

And what does this mean for the markets?

Well, the key narrative is still likely to be AI, and the capital spending wave is real. We anticipate that this investment cycle can support growth and earnings. Nevertheless, the market has already built a lot of optimism into prices, especially in the biggest growth names.

And when expectations get stretched, the risk is not that the theme disappears. So then, the risk is that the timeline disappoints, competition shows up faster than expected, or leadership rotates while investors are still anchored to the last set of winners.

This is why I want to be careful about how we think about “upside” in 2026. Yes, there are scenarios where things run hotter than expected and risk assets do very well.

Nevertheless, our expectation is for a year where the economy keeps moving, inflation stays firm enough to keep the Fed cautious, and markets have less room to absorb surprises.

In that kind of year, concentration risk tends to show itself faster, and valuation matters more than it did when liquidity was abundant.

That brings me to what I think is the most practical takeaway heading into the new year.

Staying Disciplined for the Long-term

If 2025 reminded us how quickly narratives can change, 2026 looks like the year where discipline gets rewarded. Not by avoiding every bout of volatility, but by being positioned so you are not forced to make decisions on the market’s timetable.

This is also a moment where bonds deserve more respect than they have gotten in the past decade. When yields are meaningful, high-quality fixed income can do two jobs at once. It can provide real income, and it can add stability if stocks go through a period where expectations cool off.

That’s why the best forward-looking risk-return profiles are increasingly found in high-quality fixed income, and why a more balanced stock-bond mix has a stronger case than it did when yields were near zero.

On the equity side, I still expect the market to be pulled in two directions. In the near-term, earnings can remain supportive, even with modest growth. And in the longer-term, the market is wrestling with a more complex reality with high expectations, crowded leadership, and the simple truth that technology cycles tend to produce new winners over time.

That is one reason value-oriented stocks and international developed markets look more compelling on a forward-looking basis than simply doubling down on U.S. growth at any price.

The Big Takeaway

When it comes down to it, as we head into 2026, AI remains the central economic and market storyline likely to dominate attention. And while it may feel like this theme is growing tired, there is still a balanced way to hold the story.

AI can be a genuine economic tailwind through capital investment and productivity gains. At the same time, solid economic upside does not automatically guarantee strong stock returns from today’s market leaders, especially when expectations and valuations are already high.

That’s why, heading into next year, we continue to emphasize quality, diversification, and the discipline to avoid building a portfolio that is overly dependent on one theme.

Because even when a theme is real, leadership can change.

And history has a way of reminding us that tomorrow’s winners often look different than today’s.

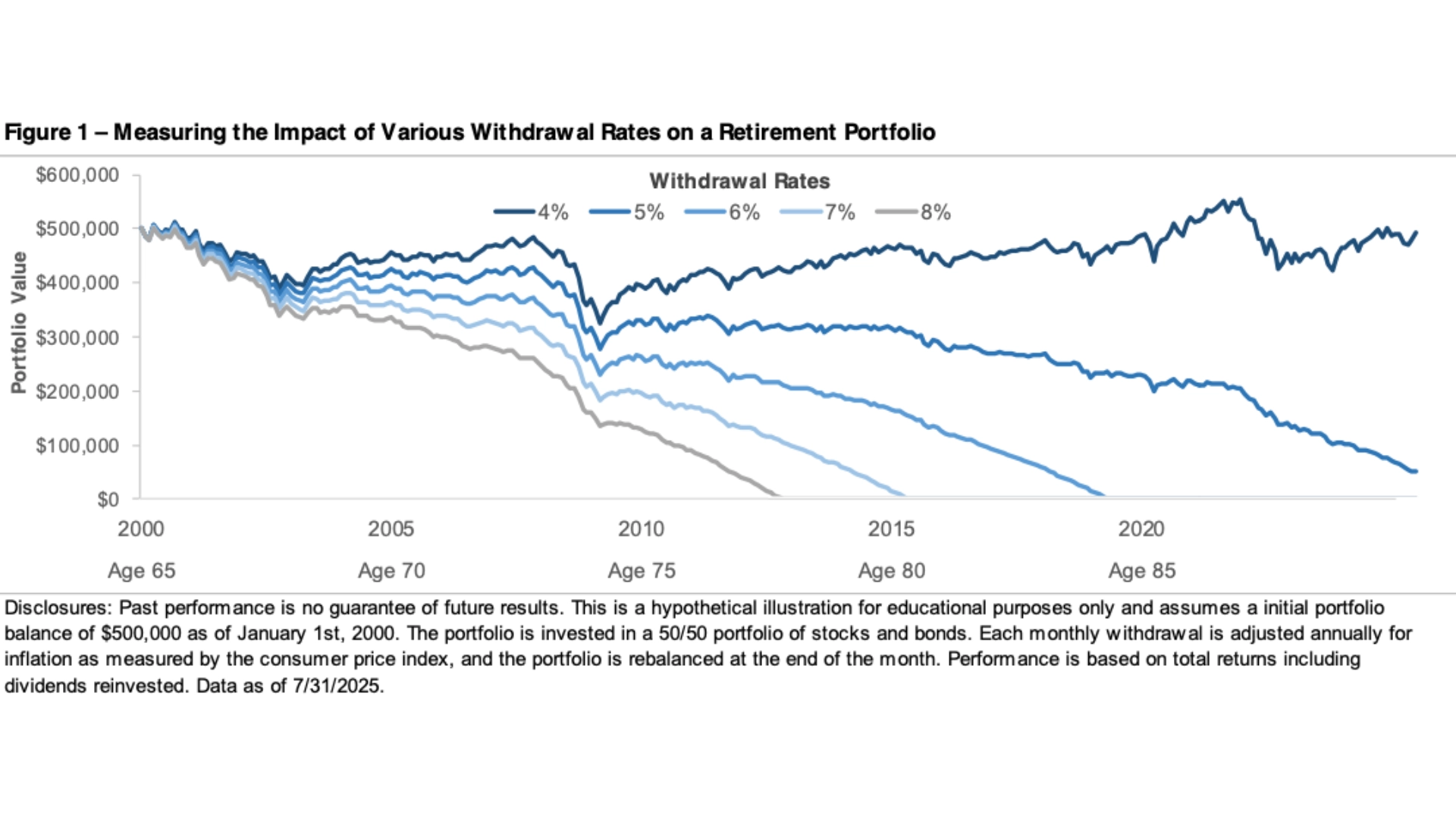

How Withdrawal Rates Impact Your Portfolio in Retirement

Many people spend years preparing for retirement by saving and investing, but planning shouldn’t stop once the paychecks do. Transitioning from earning income to withdrawing it from your portfolio is a major shift with a new set of risks and decisions. This period, known as the distribution phase, requires careful thought.

How much you withdraw each year can have a bigger impact on long-term financial security than many people realize. Without a well-structured strategy, even a sizable retirement account can be depleted faster than expected.

The Impact of Withdrawal Rates

The chart below shows how different withdrawal rates can impact a retirement portfolio’s lifespan. It assumes an individual retired in 2000 at age 65 with $500,000 and started taking monthly withdrawals.

Each line reflects a different withdrawal rate between 4% and 8%, showing how the portfolio fared through age 85. While all scenarios start at the same point, the paths quickly diverge, especially during periods of market volatility. The chart illustrates how a retiree’s withdrawal strategy can determine whether the portfolio lasts or runs out.

The message is clear: higher withdrawal rates tend to exhaust a portfolio sooner, while lower rates can extend its life. In this example, withdrawing 7% or 8% caused the portfolio to run out of money before age 85. In contrast, the 4% and 5% withdrawal rates helped the portfolio weather market declines.

Does a 4% Rate Still Cut It?

The 4% strategy not only preserved the portfolio but grew it over 20 years, showing how compounding can work even during retirement. No strategy can eliminate market risk, but a smaller withdrawal rate can extend the portfolio’s life and reduce the risk of outliving your savings. Taking a more conservative approach in the early years of retirement gives your portfolio time to recover from short-term losses and grow with the market.

A thoughtful withdrawal strategy is an important part of retirement planning. It’s not just about how much you’ve accumulated, but how you manage it. There’s no one-size-fits-all approach, and the method you start with doesn’t have to be permanent. Fixed withdrawal rates can provide a good starting point, but many retirees may benefit from more flexible approaches.

The Big Takeaway

For example, you could adjust withdrawals based on market conditions, taking smaller distributions in down years and larger ones in strong years. Another option is the bucket strategy, which divides assets into short-, intermediate-, and long-term segments.

By keeping at least 18 months worth of expenses in cash or short-term investments, you can avoid selling stocks during major market declines, such as those in 2008 or 2020. This gives long-term investments time to recover and can help create a steadier income stream over time. Everyone’s retirement looks different. Our goal is to help you create a withdrawal strategy tailored to your unique needs and goals when that time comes.

Roth Conversion Opportunities Now that Tax Cuts are Law

While many of us have been easing into the holiday weekend, policymakers in Washington have been working overtime.

Yesterday, the House passed Donald Trump's One Big Beautiful Bill Act of 2025 (OBBB), and today, the president is expected to sign it into law.

But, let's be honest: When Washington passes something with a name like "One Big Beautiful Bill," most of us tune out, right?

Because it sounds political.

Because it sounds complicated.

Because frankly, we might not care.

But here's the truth: if you're saving for retirement or already living in it, this bill just changed your wealth blueprint.

How so?

Strategic Roth Conversion Opportunities

Well, one of the biggest changes in the bill is that it makes the individual tax cuts from the 2017 Tax Cuts and Jobs Act (TCJA) permanent.

And while that may sound like a Washington talking point, it carries real weight for investors.

Why's that?

Because it extends what might be the longest window we've ever had for historically low income tax rates. And for those with sizable pre-tax retirement balances, that opens the door for one of the most powerful tax strategies available: Roth conversions.

Whether you're still saving, newly retired, or years into retirement, this is an opportunity worth paying attention to.

For example, if you're in the pre-retirement phase, converting to Roth now means locking in today's known tax rates, rather than gambling on what future tax policy might bring. And given the projected trillions in national debt added by this bill, the odds of higher taxes down the road just got higher.

And if you're already retired, this could be your moment to smooth out future Required Minimum Distributions (RMDs). Indeed, converting during your lower-income retirement years might reduce future taxable income and potentially save tens or even hundreds of thousands in lifetime taxes.

But Roth conversions aren't just about your tax bracket today. They're also about preserving your legacy for your heirs.

Because when you convert now, you're essentially prepaying the tax bill for your heirs at today's rates. And that's an enormous advantage, especially given the SECURE Act rules that now require most non-spouse beneficiaries to deplete inherited IRAs within 10 years.

At the same time, if your children are in their peak earning years when you pass on, then inheriting a traditional IRA could push them into higher brackets, eroding much of what you hoped to pass on.

But a Roth IRA, on the other hand, grows and distributes its proceeds tax-free and still gets ten years of tax-free compounding after your death.

No RMDs for you. No tax bill for them.

In short: A Roth conversion is one way to say to your family, "I've got this part covered for you."

What This Means for Your Retirement Strategy

Ultimately, Roth conversions are a powerful tool, but they're not without complexity.

That's because converting too much in one year can drive up your income, affecting more than just your tax bracket, it can increase your Medicare premiums.

At the same time, it can cause more of your Social Security to be taxed and for some, it may trigger the 3.8% net investment income tax or other surtaxes.

That's why this isn't a "just convert and see" strategy, it needs to be a coordinated, multi-year focused approach.

You need to time conversions wisely and you need to understand your marginal brackets, IRMAA thresholds, charitable giving opportunities, and how other deductions might offset conversion income.

Because you're not just trying to minimize taxes this year, you're trying to manage taxes and asset growth over decades, across generations.

And when lawmakers eventually raise taxes down the road, those who've already paid taxes at today's lower rates may be in a far stronger position, especially those with Roth assets.

So the smartest move right now might not be deferring taxes. It might be paying them strategically, while the sale is still on depending on what phase of retirement you're still in:

Pre-Retirement: You're Still Working

If you're still a few years away from retirement, the bill gives earners like you a bit of short-term breathing room: lower tax rates, enhanced deductions, and even some new savings tools.

That's good news on paper.

But zoom out.

The national debt is rising, future benefits could shift and market volatility may increase as policymakers navigate these tradeoffs in real time down the road.

That's why now's the time to take a fresh look at your tax strategy, both in terms of contributions (Roth 401k), Backdoor Roths and Roth conversions.

If You're Already Retired

If you're already retired, then the message here is even clearer: don't count on the government to do what it used to do.

Medicare and Social Security rules are evolving. Medicaid funding is tightening and support systems that once felt secure are becoming more fragile.

That's why clarity matters.

You can't control Washington, but you can create a retirement income strategy that works regardless of what happens there.

With smart planning, you can reduce your taxable income by taking advantage of income tax valleys to covert, preserve benefits, and make the most of the resources you've spent a lifetime building.

Where to From Here?

If you're still not sure how this bill affects your financial picture or how to use the current tax landscape to your advantage, then let's schedule some time to talk.

Because the key takeaway here is that there's likely a limited-time opportunity to make smart, strategic decisions that could save you and your family thousands in taxes over time, and position your retirement savings for tax-free growth long after this bill fades from the headlines.

That's why this moment presents a planning opportunity, especially for families with meaningful income, sizable retirement assets, or a desire to transfer wealth efficiently.

If you've been thinking about a Roth conversion, accelerating future income into the present, unwinding a concentrated stock position, or gifting assets to heirs or charitable causes, this may be the most favorable tax environment we'll see to do so for quite some time.

What to Make of One, Big, Beautiful Budget Bill?

Washington is moving forward with a new budget proposal that could reshape the tax landscape for years to come. And while the details are still being finalized, it’s crucial that you take the time to understand the broad strokes because they’re worth paying attention to.

Here’s what this means:

Lower Tax Brackets

At the center of the proposal is a permanent extension of the 2017 Tax Cuts and Jobs Act (TCJA).

These were the sweeping tax cuts that congressed passed during President Trump’s first term.

Those lower income tax rates were supposed to expire at the end of next year and this bill will now make them permanent.

What this means is that historically low tax environment we’ve been living in may stick around a bit longer, at least for the next four years.

Higher Itemized Deductions

The bill also adds in a few new deductions. There’s talk of expanding the child tax credit, offering tax breaks for things like tips and overtime, and even bringing back a deduction for interest on car loans.

One change that could really matter to higher-income households is a significant expansion of the deduction for state and local taxes, or SALT.

That’s because the TCJA capped SALT to $10,000 per household, which for many individuals in high-value zip codes, has been a thorn in their sides ever since.

Some Drawbacks

Now, not everything in the bill is a giveback. That’s because the Big Beautiful Bill would also roll back several recent reforms.

For example, remember the IRS’s free tax filing tool? Gone.

Or how about funding for IRS enforcement? Slashed.

And many of the tax credits for clean energy investments would also be reversed.

At the same time, there’s also a push to reduce spending on government assistance programs, like Medicaid and food benefits, by introducing stricter work requirements.

And while those cuts may not directly affect many affluent individuals, they nevertheless reflect a broader shift in where the government’s priorities are headed.

It All Comes at a Cost

When it comes down to it, all of these tax cuts come with a price tag.

Indeed, the Congressional Budget Office (CBO) estimates that the bill would add roughly three trillion dollars to the national deficit over the next decade.

And that’s not going unnoticed. Because credit rating agencies are already sounding alarms, with Moody’s downgrading the U.S. outlook just this past week.

So yes, there are plenty of changes packed into this bill, both good and some maybe not so good.

Some may feel beneficial in the near term, but others raise important questions about what’s sustainable, especially when it comes to how the government will eventually address its growing debt load.

What This Means for You

Now, if this bill passes (which it likely will) it will signal that the window for historically low tax rates may be closing.

How so?

Well, we’re in a rare moment where the rules are still in our favor. But that could change quickly.

But the fact is that the national debt is climbing at an unsustainable rate. At the same time, the budget deficit continues to grow with little sign of letting up.

And while this bill offers short-term tax relief to many high-earners, it does so at a long-term cost for the nation as a whole.

Eventually, future lawmakers may have little choice but to raise taxes to close the gap should borrowing costs rise .

That’s why this moment presents a planning opportunity, especially for families with meaningful income, sizable retirement assets, or a desire to transfer wealth efficiently.

If you’ve been thinking about a Roth conversion, accelerating future income into the present, unwinding a concentrated stock position, or gifting assets to heirs or charitable causes, this may be the most favorable tax environment we’ll see for quite some time.

Now, this isn’t about reacting to the news.

It’s about staying proactive and using what we know today to reduce uncertainty tomorrow because if lower tax rates are extended, that gives us more time to work strategically.

And if they’re not? Well, then we’ll be glad we took action while we still had time.

As always, we’re watching the developments closely. And we’re here to help you think through how this moment might apply to your financial picture.

If it’s been a while since we’ve reviewed your tax strategy, or if you’re wondering whether you’re making the most of this window, let’s talk.

Here's How Retirement is an Endurance Sport

In many ways, retirement isn’t a goal, it’s an endurance sport.

I had the opportunity to compete in the Pittsburgh Marathon over the weekend and wanted to share a quick thought that came to me during the race:

To run the race, you not only have to train, but you’ve also got to be able to adapt your plan to uncontrollable conditions on race day.

We’ve often been led to believe that retirement is a singular destination, that all you need to do is show up at the starting line with the right-sized nest egg, and you’ll be set.

The reality is, however, that you have to prepare not just to be able to show up for race day, but also to sustain yourself along the way.

It’s not just about putting in the miles to go the distance; it’s about pacing, nutrition, hydration and attitude.

In retirement, pacing becomes your spending plan. Nutrition and hydration represent efficiently growing your wealth and protecting it. And your attitude? That’s staying disciplined when markets and life throw challenges your way.

A misalignment in any of these components is likely to fundamentally change your race day experience.

Heading into my taper week ahead of last week’s race, I felt like my training was solid and was certain that by race day, my body and legs would be fresh. But wouldn’t you know it, I woke up on Sunday morning with a cold and a case of bronchitis.

That’s the paradox of endurance training: you can’t control the conditions, but it does equip you to press through them.

You change and test the variables weeks in advance so you know how your body might adapt to the unknown stresses of the event.

And once you’ve trained for an endurance sport, you’re likely forever changed.

Because more often than not, you haven’t prepared for a single race; after months of deliberate effort, you’ve forged a new way of life.

Many people believe retirement planning is about maintaining their current lifestyle for the next 20, 30 or 40 years. But the right plan doesn’t just preserve what you have, it expands your horizons. It equips you to live a lifestyle you may not have envisioned before, opening the door to entirely new races you hadn’t even considered.

You see, retirement success isn’t about reaching a single milestone.

It’s about having the right habits, resources, and mindset to keep going strong over the long run no matter where your journey might take you, even under the least optimal conditions.

Frankly, the conditions presented to me on my race day were certainly less than optimal. In the end, I finished the race, but not in the way I had hoped. Even so, my planning and training enabled me to envision an outcome (finishing the race) beyond current circumstances (illness).

Whether you’re already executing your retirement plan or still fine-tuning it, it’s worth asking: do I have the right systems, support, and strategies in place to thrive mile after mile no matter what life throws my way?

Humble Brag

I had a proud-dad moment this weekend as my oldest, Lily, ran her first timed 5K.

It wasn’t about speed or competition, it was about building grit.

We laughed, we cried, and ultimately, we crossed the finish line together.

Here’s to the first of many more races we’ll run side by side in the years to come.

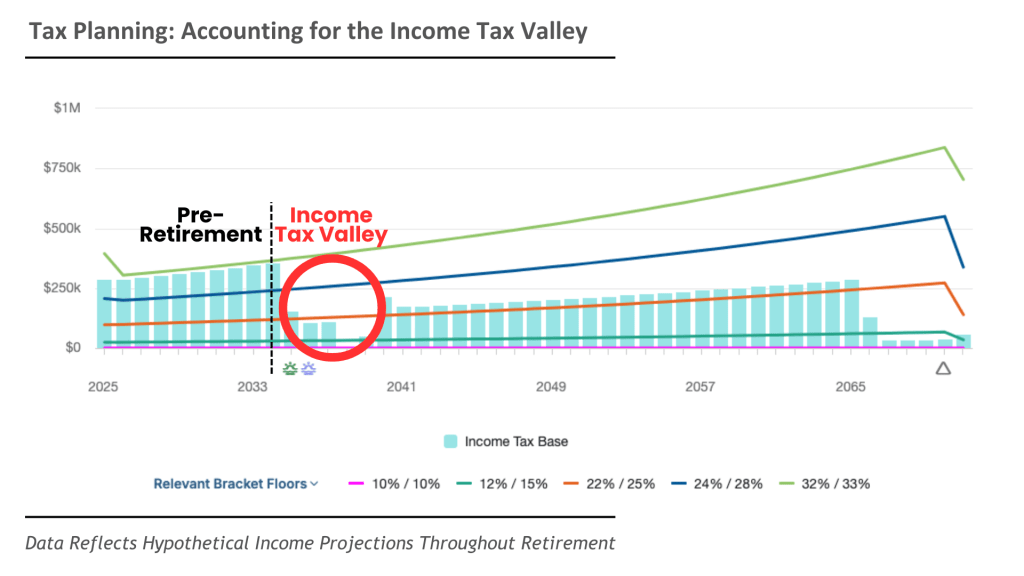

Income Tax Valley: The Most Overlooked Years in Retirement Planning

One of the biggest and most preventable tax mistakes high-net-worth retirees make is waiting too long to address the growing tax liability in their pre-tax retirement accounts.

Sure, you may have done everything right, like saving diligently and building a sizable nest egg so you can enter retirement with confidence.

But now, your IRA or 401(k) sits like a tax time bomb, waiting to trigger Required Minimum Distributions (RMDs) and inflate your taxable income well into your 70s and beyond.

Indeed, what many investors don't realize is that the years between age 59½ and when you begin taking Social Security represent a golden opportunity to defuse that tax burden.

That's because, with no 10% early withdrawal penalty, reduced earned income, and RMDs still a few years away, you're in a low-tax window, but one that won't last for too long.

And that's where Roth conversions come in.

That's because converting your pre-tax account during this window gives you more control over how and when you pay your taxes.

In fact, it allows you to strategically move money from tax-deferred to tax-free accounts, locking in today's rates and reducing tomorrow's surprises.

With that said, the key here is recognizing that this isn't just a planning opportunity; it's a problem-solving moment. One that can dramatically improve your long-term tax picture if handled wisely.

Why Timing Matters

Now, if you've just retired, the years between when you stop working and begin claiming Social Security is strategic.

That's because, more often than not, your income is temporarily low.

We call this the income tax valley.

You're no longer working, you haven't started taking Social Security, and Required Minimum Distributions haven't kicked in.

In fact, for many high-net-worth retirees, this is the lowest tax bracket they'll be in for the rest of their lives.

That's what makes Roth conversions so powerful in this window.

You can move money from tax-deferred accounts, like IRAs and 401(k)s, into a Roth IRA and pay taxes at a rate you choose, not one the IRS forces on you later.

What this means is that every dollar you convert now is one less dollar subject to RMDs down the road. That means lower future taxes, fewer Medicare surcharges, and more flexibility in how you take income later.

Ultimately, when it comes to tax planning in the income tax valley, you're either proactive now, or you'll be forced to be reactive later.

Even so, this is your chance to get ahead.

How This Works in Practice

So, what does this kind of planning look like in practice?

Well, let me tell you about my friend, Susan.

Susan is 62 years old, recently retired, and sitting on about $3.2 million in retirement savings, mostly in her traditional IRA and 401(k).

She's healthy and financially secure and plans to delay Social Security until age 70 to lock in the maximum benefit.

At first, Susan figured she didn't need to do much until her benefits started. But when she sat down with her advisor, she saw the bigger picture.

Her income during this income tax valley was low, around $50,000 a year, including capital gains distributions from a taxable account and some small dividends.

That gave her a unique opportunity to convert $100,000 a year from her IRA to a Roth and allowed her to stay within a lower tax bracket and avoid triggering higher Medicare premiums.

In fact, over the next eight years, Susan moved $800,000 into a Roth IRA.

More importantly, she paid the taxes on these conversions on her terms.

In fact, she reduced her future RMDs by nearly $30,000 a year. And in doing so, she built a tax-free pool of money for later retirement and legacy planning.

Same accounts. Same retirement. It's just a smarter sequence, with a major long-term impact.

Why Roth Conversions Before Social Security Can Be Advantageous

So then, when it comes down to it, the window between age 59½ and claiming Social Security isn't just a quiet phase of retirement, it's one of the most powerful tax planning opportunities you'll ever have.

That's because Roth conversions during this time can reduce future RMDs, minimize your lifetime tax liability, avoid Medicare premium surcharges, and give you more control over how your retirement income is taxed.

And for high-net-worth individuals like yourself, the cost of inaction isn't small; it means tax savings that are compounded over decades.

If you don't take action now, it can mean bigger RMDs, potentially putting you in higher tax brackets, offering less flexibility, and allowing more of your retirement savings to go to the IRS instead of your family.

With that said, with the right strategy, this window of opportunity, your income tax valley, becomes a moment of leverage. It becomes a chance to take control, preserve more wealth, and shape a smarter financial legacy on your own terms.

At the end of the day, tax planning isn't about reacting to the past; it's about anticipating and being proactive about the future. And the retirees who plan ahead are the ones who spend with confidence and leave more behind.

Market Update: Is it a Correction or Something Bigger?

What do you do when the market takes a turn you didn’t expect? Do you panic? Do you make quick decisions? Or do you take a step back and look at the bigger picture?

As we step into the first few months of 2025, the market has given investors plenty to think about. Stocks started the year on a strong note, but since then, we've seen a pullback. The S&P 500 briefly entered correction territory, bringing its year-to-date return down to -5%.

Similarly, the Nasdaq 100, home to some of the biggest names in tech, is down 7% this year, while the small-cap Russell 2000 has fallen 9%. And the what about the Magnificent 7 of Microsoft, Apple, Meta, Alphabet, Amazon, Nvidia, and Tesla? They’re down nearly 15%.

So what’s really going on? More importantly, what should you do about it?

What’s Behind the Market Selloff?

Well, it’s easy to blame market swings on one big event. But in reality, it’s rarely just one thing because there are likely a few reasons this year’s recent pullback.

First, the stocks that led the charge last year are the ones struggling the most today. And it’s not unusual to have yesterday’s winners become today’s laggards. Indeed, figure 2 shows us that the biggest winners of 2024, like tech stocks and the Magnificent 7, have become 2025’s underperformers.

Why?

Because last year’s rally was built on enthusiasm, especially around artificial intelligence. And when enthusiasm drives prices higher, valuations get stretched. Investors pile in, positioning gets crowded, and eventually, the weight of that momentum starts to break down.

That’s what’s happening now.

Second, investors, both individual and institutional, came into 2025 with a high level of exposure to stocks. In fact, some of the largest institutional investors like pension funds, endowments, and insurance companies held a record share of their wealth in equities.

And that strategy works well when markets are climbing, but when momentum reverses, institutional investors start deleveraging. And when they unwind positions quickly, it amplifies the selling pressure.

Finally, there’s the policy backdrop. What started as optimism around pro-growth policies under the Trump administration has shifted to uncertainty. As we’ve written about before, concerns about spending cuts and the impact of tariffs have raised questions about economic growth.

Because the fact of the matter is that investors don’t like uncertainty, and right now, they’re adjusting to a new, highly uncertain reality.

Market Volatility vs. Economic Reality

So, does all this mean the economy is struggling? That’s a great question. And here’s where we need to separate perception from reality.

The stock market reacts quickly to new information, but that doesn’t always mean the economy is following the same path. One way we can test that is by looking at real-time economic data.

For example, the Federal Reserve’s Weekly Economic Index (WEI) tracks real-world activity using data points like unemployment claims, rail traffic, steel production, and tax withholdings.

And right now? It’s still positive (Figure 3).

Another piece of the puzzle is the bond market. High-yield credit spreads, which are essentially the difference in yield between risky corporate bonds and safer U.S. Treasuries, are a great way to measure financial stress.

And today, those spreads remain near all-time lows (Figure 4). Indeed, if we were facing a deeper economic problem, we’d expect to see those spreads widen. The fact that they haven’t tells us this market selloff could be more about repositioning than it is about a fundamental crisis.

With that said, no one rings a bell when we’ve entered a recession. And it’s very well possible that a policy error from the current administration could push the economy into a downturn. For now, however, the data continue to reflect modest economic growth.

Is This Normal and Can the Market Selloff Continue?

Now, if you’ve been investing for a while, you likely know that market volatility isn’t new. But let’s be honest, knowing that doesn’t make it feel any better when stocks drop, does it?

So what should you do?

Well, one of the best things we can do is put this moment in perspective. For example, since 1928, the S&P 500 has experienced a decline of 5% or more in 91 of the past 98 years.

Read that again.

In almost every year on record, we’ve seen the market pull back like this. And yet, time after time, markets have recovered. Investors who stay the course, who focus on the long-term, are the ones who have been rewarded.

So let me ask you: What’s your plan?

Because the difference between reacting and responding is having a plan. The key isn’t trying to predict every market move. It’s making sure you’re positioned to succeed no matter what happens next.

And that’s why sticking to a disciplined process and having a long-term perspective matter over the long-run.

The Bottom Line

Market volatility often feels personal. It’s your retirement savings on the line, isn’t it?

And so, when you see headlines about market swings, it’s easy to wonder, “Is this the beginning of something bigger? Am I missing something? Should I be doing something differently?”

So then, if that’s where your mind is right now, you’re not alone.

But more importantly, you’re not powerless. You don’t have to let fear dictate your financial future. You can make decisions based on a thoughtful strategy rather than short-term emotions.

Whether you’ve been working with our team for years or you’re just starting to explore your options, here’s what I want you to hear: clarity, confidence, and peace of mind don’t come from guessing the market’s next move. They come from knowing you have a plan that’s built for moments like this.

Because at the end of the day, the market will move up.

It will move down.

That’s a given.

But those who stay focused on the long term, those who stay diversified and patient, won’t just weather today’s volatility. They’ll be in the best position to thrive beyond it.

So, the real question isn’t what will the market do next? The real question is: Are you ready for whatever comes next?