Plan Your Way into Tax-Free Income

Let’s face it, no one likes paying Uncle Sam more than his fair share. But what if there was a way to take advantage of financial planning techniques to not only grow your savings, but also help protect your family and transfer wealth tax-free?

Sounds too good to be true, right?

Well, it’s more possible than you think. And as a highly driven individual, you likely have multiple streams of income to consider, like your salary, bonuses, stock options, and perhaps even revenue from a side hustle or business.

And with these multiple income streams and your high earnings, you’re likely setting yourself and your family up for an even higher tax liability in the years ahead unless you do something about it today.

That’s where tax planning comes in.

Now, tax planning is essential because it provides a structured approach to minimize the taxes you owe. And without adequate tax planning, you could end up paying more to Uncle Sam than necessary, which reduces the amount of wealth available to you and your family.

To be sure, the financial decisions you make today can have significant tax implications on your future wealth. That’s why understanding how to harness techniques to gain tax-free income can help you avoid paying thousands to the IRS, leave more to your family, and to ultimately make more informed financial decisions.

Understanding Legit Ways to Produce Tax-Free Income

Alright, so, when you hear tax planning you might think to yourself, “isn’t creative tax planning what got Al Capone put away in jail?” Well, the truth is that the US tax code, as complex as it is, has features written into it that gives certain advantages to those individuals with the time and patience to see them through, like sidestepping taxes on income.

To be sure, tax-free income is like a treasure that’s hidden in plain sight. It's income you or your loved ones receive that, as the name suggests, is free from obligation to the IRS. And what this means is that every dollar you receive stays a dollar, without a portion being reduced by what you would otherwise owe to Uncle Sam.

Now, it’s essential to keep in mind that we all earn income under a progressive tax system here in the United States. And what does this mean? Well, a progressive tax system means that the more money you make, the more you will owe Uncle Sam because your tax rate rises, or progresses, with your rising income.

And this rising tax rate doesn’t apply just to your wage income. In fact, in many cases it also applies to your interest and investment income applied towards the substantial savings you’re likely to receive now and into retirement as well. That’s why it’s essential, now more than ever, for you to understand some of the basic techniques of creating tax-free income so you can substantially boost your wealth while legally mitigating your future tax liability.

And, so, what are those techniques?

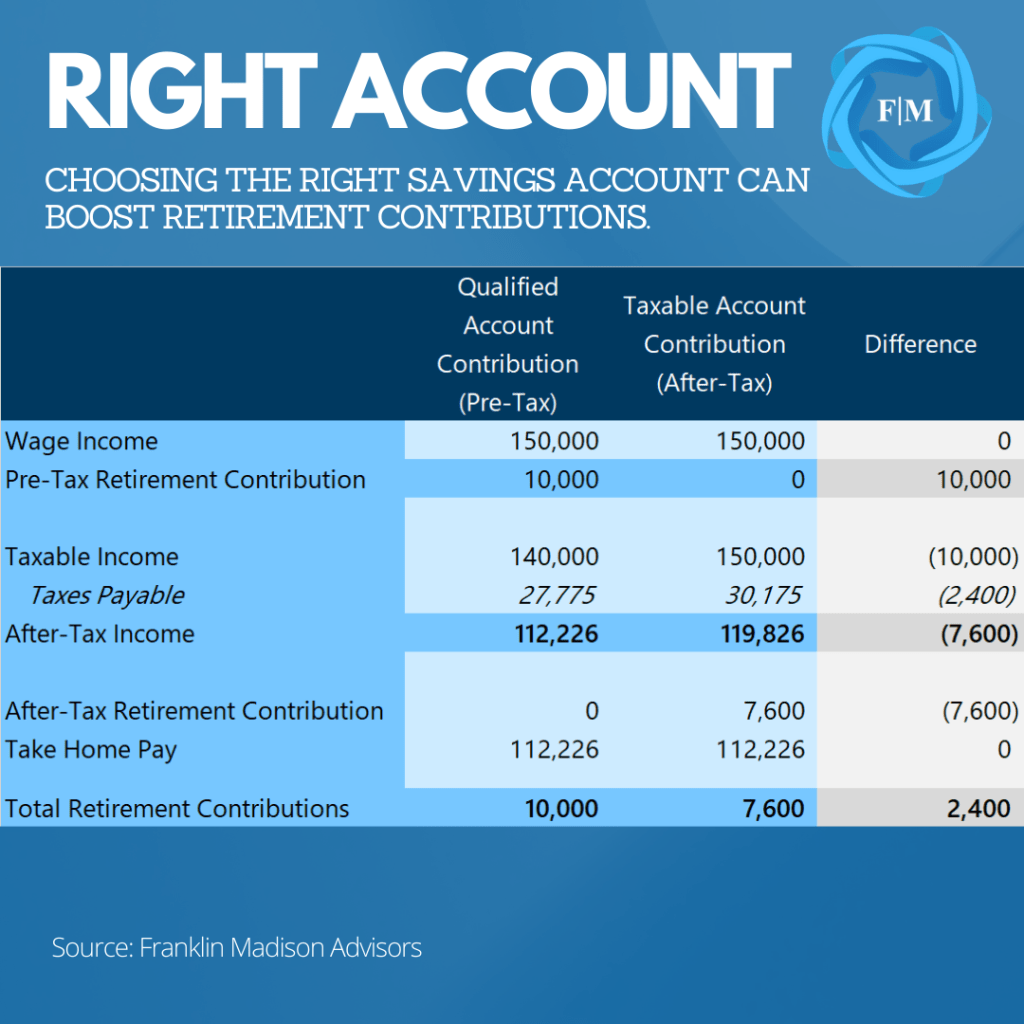

Well, when it comes to reducing your future tax obligations, there are generally three ways to produce tax-free income for yourself and your family. The first is putting money away in a tax-free investment account. The second option is to purchase securities or insurance products that offer tax-free income now and into the future. And, finally, you can mitigate a significant tax liability through the decisions you make about your home, when you gift money to loved ones and the decisions you make before you pass away.

Tax-Free Investment Accounts: Vehicles to Hold Taxable Investments

Alright, so let’s talk about some ways to use investment accounts to mitigate your tax liability. Now, before diving deep down this rabbit hole, let’s take a moment to make a distinction here between tax-free investment accounts and tax-free investment products.

And why is this important?

Well, it’s important because investment accounts and financial products are in many ways entirely different beasts. For example, tax-free investment accounts, like Roth IRAs, 529 Plans and HSAs act as shelters or holding containers, that allow a range of otherwise taxable investments within them to grow tax-free.

On the other hand, tax-free securities or insurance products like municipal bonds or life insurance, offer tax advantages inherent to the instrument itself, regardless of the account they're housed in. Indeed, another way to think about this is that tax-free accounts shelter holdings from future tax liabilities, while tax-free products inherently sidestep income tax altogether.

Ok, so then with this distinction in mind, let's explore tax-free investment accounts in greater detail.

Roth IRA – Tax-Free Lifestyle Savings

More specifically, let's start with the Roth IRA. Now, a Roth is an individual retirement account and acts like a container that offers specific tax breaks for the otherwise taxable investments you hold inside. And the way it works is that you put money into a Roth IRA using after-tax, take-home dollars.

And now while you don’t get an immediate tax break for your contributions to this account, the magic happens as your investments grow and when you start to withdraw your funds later in retirement. That’s because all the withdrawals, including earnings from the investments, are received tax-free if you meet certain conditions.

529 Plan – Tax-Free Education Savings

Another investment account that allows you to earn tax-free returns is a 529 Plan.

Now you may have heard of a 529 Plan before.

But if you haven’t, a 529 plan is an education savings program designed to encourage you to save for your or your children’s future education costs. Now, these plans operate in much the same way as a Roth IRA, meaning that you fund them with money you've already paid taxes on.

And while there's no federal tax deduction on the front-end for these contributions, the investments still grow tax-free so that when it’s time to use these funds for qualified education expenses, the withdrawals often come out without owing a cent to the IRS.

HSA Savings – Tax-Free Healthcare Savings

And finally, when discussing tax-free investment accounts, we can’t forget about Health Savings Accounts, or HSAs. Now, these accounts are a little different from Roth and 529 accounts in several ways.

How so?

Well, for starters, these accounts allow you to set aside money on a pre-tax basis before Uncle Sam gets a cut of your pay. What’s more, the contributions you make to this account grow tax-free, meaning you don’t pay taxes on dividends, interest or capital gains and for an added benefit, the money comes out tax-free when it’s time to spend your savings.

Therefore, an HSA creates tax-free income by providing a tri-fold tax benefit which is pre-tax contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

Tax-Free Considerations

So then, with all this discussion about tax-free income from these various investment accounts, you might be asking yourself, “these benefits all sound great, what the catch?” Well, while each of these accounts offer tremendous benefits, there are some things that you’ll want to consider.

For example, in most cases, you can’t money out of a Roth until you’re at least 59 ½ (or have a qualifying event) and there are limitations about when and how much you can put into the account. Now, there are ways around these limits, but that’s a discussion for another time. Even so, if you expect to be in a higher tax bracket by the time you reach retirement age, then looking into Roth contributions might be worth your time.

As for 529 and HSA accounts, there are a few things you’ll want to consider before you start putting money into these accounts. For starters, while you can begin taking money out of the accounts almost immediately after making contributions, you need to keep in mind that to qualify for tax-free status on those withdrawals, the money must be used for qualifying expenses.

Either way, the big takeaway here is that if you’re looking to put money to work now so you can fund your future lifestyle, education or healthcare expenses in a tax-free manner, then you should consider looking into a Roth IRA, 529 or HSA account.

Unlocking the Hidden Gems: Tax-Free Financial Products and Securities

Alright, so now that we’ve talked about certain tax-free investment account types out there, let’s talk about financial products and securities that offer similar tax advantages.

Here again it’s essential to make the distinction between accounts and products or securities. Remember, accounts are like baskets that hold all kinds of investments and shelter them from taxes.

And when it comes to securities and financial products, on the other hand, they can exist either inside or outside of a financial account and offer tax-free income.

Insurance Products: Tax-Free Income and Financial Security

For example, insurance products, like disability, long-term care and life insurance can be purchased directly from an insurer, or through your employers group coverage, without opening a specific type of financial account. That’s because these types of products are more like contracts between you and the insurer, rather than purchasing an investment security in the open market that needs to be held in an account.

And so, how does the tax-free aspect of these products factor in? Well, imagine that you decide to purchase a disability insurance policy. Essentially, what you're doing is entering into a contract with an insurance company to safeguard your income against the potential risk of being unable to work due to illness or injury.

Alright, now, fast forward to a situation where you unfortunately become disabled and start receiving benefits from this policy. In this situation, these benefits typically would come to you tax-free if you've paid the premiums with after-tax dollars.

And when it comes to long-term care insurance, this type of coverage operates in a similar way, except that it helps defray future costs associated with extended medical care with the benefits paid out from such a policy generally coming to you tax-free.

Now, life insurance is another insurance product that offers tax-free income, but this time not to you specifically, but to your loved ones instead. Here an insurance company offers what’s called a death benefit to your designated beneficiaries upon your passing. And, typically, this death benefit is like a gift received tax-free by your beneficiaries.

With all of this said, it’s essential to keep in mind that there are some situations where insurance payouts could be taxable. For example, in certain situations, if policy premiums are paid by your employer, then you could find a portion of your disability or long-term care proceeds taxable. And on the life insurance side, if your estate is the beneficiary of your policy, then you could find yourself paying estate tax on the state side, or federal tax if that life insurance policy pushes your estate above certain exemption limits.

Financial Securities: Exploring Tax-Free Investments

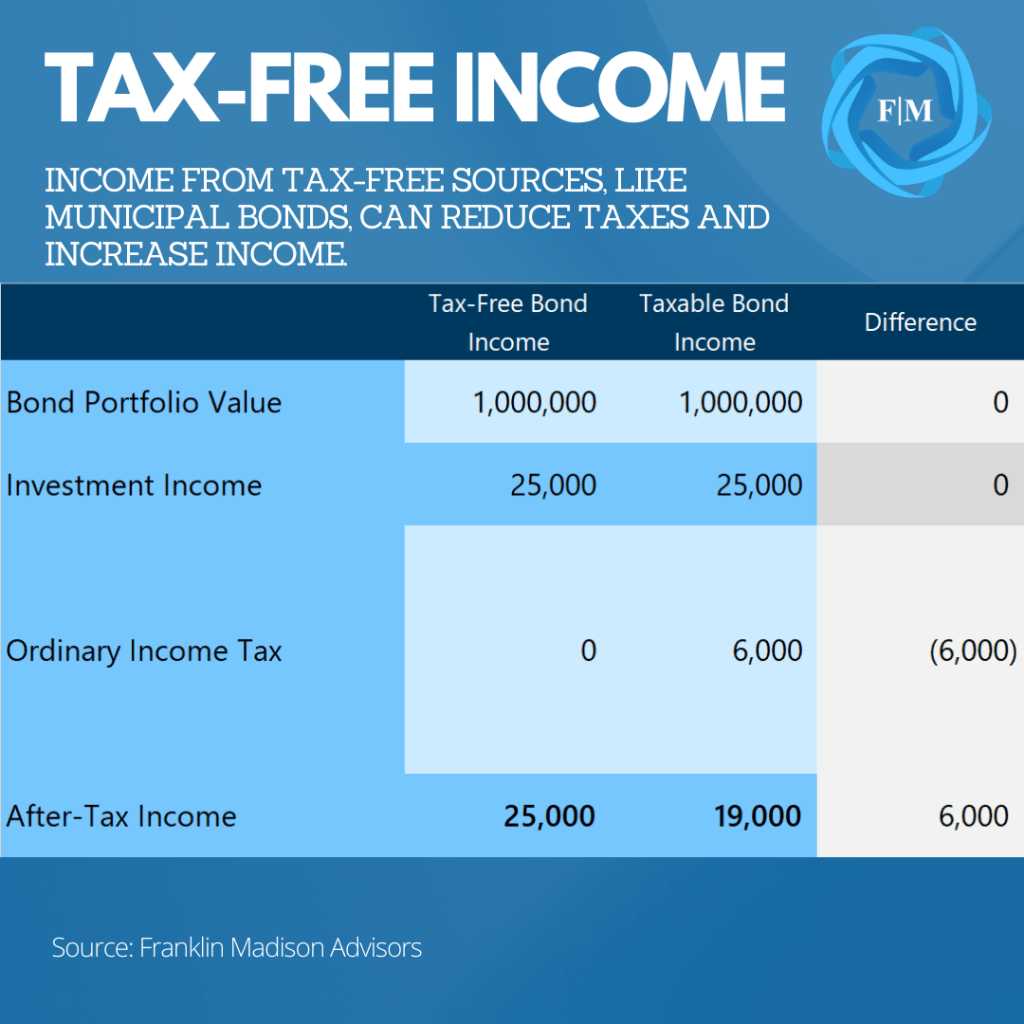

Ok, so now that we’ve talked about insurance products, let’s take a few minutes to talk about tax-free securities. Here again, whereas an insurance policy is a contract between you and the insurance company, purchasing a tax-free security, like a municipal bond, often times means holding the security in a financial account.

Now, municipal bonds, also known as "munis," are certain investments where you’re lending money to a municipality, such as a city, county, or state. And these entities often borrow money from investors to finance public projects, like building schools, highways, or sewage systems.

And here's where the tax-free part comes into play.

The borrowers pay you interest for lending them money, and, because of laws that are currently in place for these muni bonds, the interest income that you earn is typically exempt from federal income taxes. So, instead of giving a portion of your investment returns to the government, in many ways, you're allowed to keep all of your earnings.

What’s more, depending on the specifics of the bond and where you live, your interest income might also be free from state and local income taxes. And so, as a result, investing in municipal bonds from your own state could provide an even greater tax advantage and offer a completely tax-free source of income in some instances.

Now, when it comes to investing in tax-free securities like munis, there are some key caveats to keep in mind. For example, munis may offer lower interest rates than other bonds, so it’s crucial to evaluate whether the tax exemption makes them more attractive on an after-tax basis relative to taxable bonds.

And another thing to keep in mind is that while the income you receive from munis is often tax-free, you’re still likely to pay capital gains tax from selling a municipal bond before maturity. And finally, it’s crucial to keep in mind that you don’t get a double benefit from holding a muni in a tax-sheltered investment account like an IRA, 529 or HSA account, so that’s something to keep in mind as well.

Real Estate and Estate Planning: Strategies for Tax-Free Asset Transfers

Alright, so now that we’ve talked about how various financial accounts and products can help you navigate the tax man in the present, let’s talk about how navigating real estate and estate planning can also lead to tax-free asset transfers for yourself and your loved ones.

Tax-Free Income from Real Estate: Capitalizing on Home Sales

To start, let’s focus on how you can generate tax-free income from the sale of your home. Now, when you sell real estate, you’re likely to make a capital gain if the sales price is higher than what you originally paid for it. For example, if you bought your house for $500,000 and you sell it for $750,000, then your potential capital gain is $250,000.

Now, imagine that you've decided to sell your home in a high-cost part of the country so that you can move to a more affordable cost-of-living state. So, to go about this approach, you make your preparations and after the sale, you find that you've got a capital gain of $250,000. And because you met the necessary criteria, the entire amount is exempt from taxes, leaving you with a sizable sum of money you can now use however you want.

Now, it’s crucial to keep in mind that in order to make this all work you must meet certain criteria to be eligible for this exclusion. The first requirement is that you have owned the property for at least two years during the five-year period ending on the date of the sale. This is what’s known as the ownership test. The second condition is that the home must have been your primary residence for at least two years during that same five-year period, also known as the use test.

And finally, you’re not allowed to have excluded the gain from the sale of another home during the two-year period prior to the sale of your current home. That’s because this rule ensures that you’re not flipping homes and constantly taking advantage of this tax benefit over and over. Even so, if you meet all of the criteria to get the exclusion, you could tap your home as a source of tax-free income as a way to hasten your journey to financial independence.

Gifting Tax-Free Income: Sharing Wealth While Reducing Taxes

Alright, so now that we’ve talked about using real estate to generate tax-free income, let’s take a few moments to talk about gifting and estate planning to set your loved ones up for tax-free income in the future.

Now, some individuals may feel overwhelmed by the mere mention of the term estate planning. And if that’s you, that’s ok because we recently published a post on how to navigate the complexities of estate planning to make it work for you, so be sure to check out that resource.

But for now, let’s talk about a few ways that you can transfer assets to your loved ones without paying income tax. The first way is through gifting. Now, when you gift assets or money to someone while you’re still alive, it can potentially allow them to avoid giving a portion of that money to Uncle Sam.

How so?

Well, that’s because when you’re gifting an asset, what you’re doing is essentially passing on the responsibility for any income generated by those assets to the recipient. And, if the recipient falls within a lower tax bracket than you or if they have deductions or credits that offset the income, they may end up paying little or no tax on the gifted income.

Let’s look at an example to explain this a little better. Now, let's say that you have investments that generate significant income each year, and you’re in a high tax bracket. By gifting some of those investments to a family member or loved one who is in a lower tax bracket, any income generated from those investments may be taxed at a lower rate or possibly not taxed at all, which can result in tax savings for the receiver. Now, while we’ve talked about transfers of assets, this approach also applies to cash gifts.

Now, cash gifts are a little different than asset transfers, it's crucial to note here that there are specific rules and limitations surrounding gifting for tax purposes. For instance, there is an annual gift tax exclusion that allows you to give a certain amount to an individual each year without triggering gift tax consequences, which is currently $17,000 or $34,000 for a couple.

Tax-Free Inheritance: Step-Up in Basis and Its Wealth-Building Potential

Alright, while gifting allows you to provide tax-free income to your loved ones while you’re still alive, inheritance planning allows you to offer tax-free income after you pass away, and one way this is done is through a set-up in basis.

And how does this work?

Well, let's say you inherit a million-dollar investment property from your wealthy uncle Frank who recently passed away. Now, the trouble is that Uncle Frank has depreciated that property over the years, and it now has a low cost-basis. Normally, if you were to sell that asset, you would have to pay taxes on the capital gains.

However, with a step-up in basis, what happens is that the cost-basis of the inherited asset is adjusted to its fair market value at the time of the Uncle Frank’s death. In other words, the cost basis for tax purposes is "stepped up" to its current value, erasing any potential capital gains that may have accrued during Frank’s lifetime.

Now, when it comes to bequeathing, or transferring your assets, this step-up in basis can come as a substantial advantage for individuals who inherit assets with significant appreciation. That’s because it allows them to potentially sell the asset and realize a profit without owing capital gains taxes on the appreciation that occurred before the inheritance.

So then, from an estate planning perspective, thinking about which assets you want to gift now and which ones you want to leave as an inheritance is a critical component of creating tax-free income through the estate planning process.

Plan Your Way into Tax-Free Income

Indeed, by now, you’ve likely come to realize that tax planning is a cornerstone of a sound wealth management strategy. In many ways, it's the unsung hero that safeguards your hard-earned wealth, curtails tax liabilities, and unearths the chance for tax-free income. And by mastering these techniques and tactics, you can sail through the labyrinth of the US tax code and harness many strategies to create wealth that lasts a lifetime.

To be sure, tax-free income can come from tax-advantaged investment accounts like Roth IRAs, 529 Plans, and HSAs. That’s because they offer tax-free growth of otherwise taxable investments, and, eventually, tax-free withdrawals for specific purposes like funding your lifestyle, healthcare, or education expenses.

Beyond investment accounts, certain financial products and securities carry their weight in gold when it comes to tax-free income. That’s because insurance policies like disability, long-term care, and life insurance can serve up tax-free benefits under certain situations, which ensures that your income is secure and offers financial protection for you and your loved ones. And, at the same time, investments in tax-free securities like municipal bonds can provide you a tax edge, which can exempt the interest income from federal, state, and even local income taxes.

And, as we just discussed a moment ago, it’s essential to remember that real estate and estate planning can be a real game-changer in generating tax-free income. Indeed, by decoding various tax strategies and deploying them effectively, you can take one step closer to becoming the master of your own financial independence journey.

Is a Roth Conversion Right for You?

A Roth conversion is a critical consideration for many high-earning tech professionals and business owners, but is it right for you?

To be sure, as you delve into the work of planning for your financial independence journey, it's essential to understand the intricate dance between taxable and tax-free retirement accounts. And as we've pointed out in recent articles, with a strategic approach, you can make the most of your hard-earned money and ensure a comfortable retirement that aligns with your aspirations.

But, now, at what point should you consider a Roth conversion?

Well, picture this: You're diligently setting aside a portion of your earnings in a traditional 401k or a similar taxable retirement account. It's a tried-and-true method, offering immediate tax benefits, but there are long-term implications that you may not have considered.

For example, as your savings grow, so does the potential tax liability. From this perspective, then, the question arises, "how can you strike a balance between receiving tax advantages today and dealing with a future tax burden?"

That's where tax-free retirement savings vehicles like Roth IRAs come into play.

That’s because with a Roth IRA, you pay taxes on your contributions upfront, but the growth and withdrawals are entirely tax-free in retirement. It's like planting seeds today that will blossom into a tax-smart future.

But, again, the big question here is is this the right strategy for you? Should you maximize your 401k contributions to take advantage of immediate tax benefits? Or would it be wiser to prioritize Roth IRA contributions, offering tax-free growth potential. So then, how do you navigate these choices and find your optimal balance?

Now, make no mistake, retirement planning is rarely a one-size-fits-all endeavor because it's about crafting a strategy that suits your unique circumstances. That’s why as you embark on the journey of maximizing your retirement savings, understanding the interplay between taxable and tax-free accounts is paramount.

By strategically considering your order of operations, leveraging 401k contributions, evaluating your traditional and Roth IRA options, and even delving into the realm of Roth conversions, you can lay a solid foundation for a financially secure future.

Understand the Difference Between Tax-Deferred (Taxable) and Tax-free Retirement Accounts

Now, as you embark on your journey towards financial independence, it is crucial to grasp the distinction between taxable and tax-free retirement savings contributions. This understanding likely will empower you to make informed decisions about your savings options, optimize tax efficiency, and potentially enhance the longevity of your retirement savings.

Now, to achieve these objectives, one powerful tool at your disposal is a Roth conversion. Before delving into its benefits, let's explore the concept of taxable retirement savings options like the 401(k) and Traditional Individual Retirement Account (IRA), as well as tax-free options such as the Roth IRA. That’s because by understanding these choices and how they differ, you can strategically plan for your future in a more thoughtful manner.

Tax-Deferred (Taxable) Retirement Savings

So, what exactly is a taxable retirement account? In simple terms, it refers to savings accounts like 401(k)s and Traditional IRAs, where contributions grow without tax consequences in the present, but future withdrawals are subject to ordinary income taxes.

401(k) Plans

And how does this work with a 401(k)?

Well, as you’ll recall, these types of accounts are employer-sponsored retirement savings programs enabling you to allocate a portion of your pre-tax earnings towards your retirement fund.

Now, one notable benefit of these accounts is that the contributions you make are not taxed in the year that the income is earned. This reduces your taxable income, allowing your savings to grow tax-deferred and potentially reducing your overall income tax liability. Furthermore, any employer matching contributions effectively yield a 100% return on your own savings.

However, when it comes time to withdraw funds from your 401(k), these distributions are treated as ordinary income and subject to taxation. This makes 401(k)s tax-deferred accounts, as all distributions are typically taxed either upon withdrawal or when required minimum distributions (RMDs) become mandatory.

Traditional IRA

Now, let's shift our focus to the tax-deferred cousin of the 401(k): the Traditional IRA. Similar to a 401(k), a Traditional IRA allows you to defer taxes on contributions made with after-tax income.

Contributions to this type of account are typically tax-deductible, reducing your taxable income for the year. Like a 401(k), capital gains, dividends, and interest earned within a Traditional IRA remain untaxed until you start withdrawing funds.

Even so, upon withdrawal or when RMDs are required, the distributions are taxed as regular income, with the tax bracket in retirement determined by your total annual income.

Tax-Free Retirement Savings

Alright, now that we’ve explored tax-deferred accounts, let's now turn our attention to tax-free retirement savings options. These include accounts like the Roth IRA, where contributions are made with after-tax dollars, and withdrawals are completely tax-free.

Roth IRA

And how does a Roth IRA work?

Well, as we mentioned earlier, a Roth IRA is funded with after-tax income, meaning you contribute to the account using your take-home pay. And while this may seem less advantageous compared to pre-tax contributions, the real benefit lies in tax-free withdrawals during retirement.

That’s because, as long as the Roth IRA has been open for at least five years, and you are at least 59 ½ years old, any distributions you make from this account will be entirely tax-free.

And this makes the Roth IRA a compelling choice if you anticipate being in a higher tax bracket during retirement, expect future tax rate increases, or simply want to avoid mandatory distributions altogether.

Now, after exploring the differences between taxable and tax-free accounts, the question remains, “how do you decide which type of account to fund?” Well, the answer depends on several factors.

Current vs. Future Tax Bracket

If you anticipate being in a lower tax bracket during retirement compared to your current situation, sticking with a 401(k) or Traditional IRA may be advantageous. That’s because by deferring taxes now and paying a lower tax rate upon withdrawal, you can potentially minimize your overall tax burden.

However, if you expect to be in a higher tax bracket in retirement, a Roth IRA becomes a more appealing option. That’s because paying taxes upfront allows you to enjoy tax-free withdrawals later, effectively sidestepping potentially higher taxes in the future.

Now, it's crucial to note that you don't have to choose one account type exclusively. In fact, a mix of both taxable and tax-free retirement savings accounts can provide optimal flexibility and tax diversification. This approach allows you to manage taxable income in retirement and hedge against future changes in tax rates.

Indeed, understanding the differences between taxable and tax-free retirement savings options is a crucial step when considering a Roth conversion. Both types of accounts offer unique advantages and disadvantages, and the right choice depends on your individual circumstances, including your current income, expected future income, and retirement goals.

Consider Your Order of Operations

Alright, now that we've discussed the differences between taxable and tax-free accounts, let's review your order of operations when it comes to savings contributions. Just like solving a complex math equation, there's an ideal way to put your income to work before fully converting your savings to a Roth IRA.

Maximizing Your 401k Contributions

So, then, where should you put your money to work first?

Well, when it comes to saving for retirement, your employer-sponsored retirement plan, such as a 401k, can be a potent resource. That’s because these plans offer unique advantages that significantly enhance your long-term savings strategy.

And as we’ve mentioned before, one of the biggest benefits is the potential for an employer match. Now, this happens when your employer contributes additional money to your 401k based on how much you contribute in the first place.

And it's essentially free money, providing an immediate 100% return on your investment that you can't get through most other retirement savings strategies. And the fact is that many people leave money on the table every year by not taking full advantage of the employer match.

And so, why is an employer match so important?

Let's consider an example to illustrate why matching is so important. Suppose your employer offers a 100% match on your contributions up to 6% of your salary. If you contribute 6%, your employer adds an additional 6% (i.e., 100% of your 6% contribution). That’s why failing to contribute that 6% in the first place means missing out on that extra 6% from your employer, effectively leaving money on the table.

So then from this perspective, the first step in maximizing your retirement savings should always be to contribute at least enough to your employer-sponsored retirement plan to fully capture your employer's matching contribution.

Now, it’s also worth noting that the Internal Revenue Service (IRS) sets limits on how much you can contribute to these types of retirement accounts each year. As of 2023, the maximum contribution limit for a 401k, 403(b), or TSP is $22,500. And if you're aged 50 or older, you can contribute an additional $7,500 per year. And this catch-up contribution is designed to help individuals who are closer to retirement age bolster their savings.

So then, if your financial situation permits, consider maximizing your contributions to these accounts up to their limits. Doing so not only allows you to take full advantage of the tax benefits these plans offer but can also significantly enhance your long-term savings due to the power of compounding on a pre-tax basis.

Taking Advantage of Traditional IRA Contributions

Alright, so now that you’ve taken full advantage of your employer's 401k match or reached your contribution limit, another smart strategy to consider is funding a Traditional IRA. A Traditional Individual Retirement Account (IRA) offers numerous advantages that can help you grow your retirement savings more effectively and efficiently.

And the primary advantage of a Traditional IRA is the tax deductibility of contributions. That’s because any money you contribute to a Traditional IRA can be deducted from your income for a given tax year, effectively reducing your taxable income. This means you'll owe less income tax, freeing up more of your money for saving or investing.

And as of 2023, the contribution limit for a Traditional IRA is $6,500 per year. And this contribution limit applies collectively to all of your IRAs, including both Traditional and Roth accounts.

While the tax benefits of a Traditional IRA are notable, it's crucial to be aware of certain limitations that apply if you or your spouse have a retirement plan through work. The IRS imposes income limits that can reduce or even eliminate your ability to deduct your Traditional IRA contributions if you or your spouse are covered by a workplace retirement plan.

For example, in 2023, if you're covered by a retirement plan at work, the deduction for contributions to a Traditional IRA is phased out for singles and heads of household with modified adjusted gross incomes (MAGI) between $73,000 and $83,000.

For married couples filing jointly, where the spouse making the IRA contribution is covered by a workplace retirement plan, the income phase-out range is $116,000 to $136,000. If you're not covered by a workplace retirement plan but your spouse is, the deduction is phased out if your combined income is between $204,000 and $214,000.

Now, it’s important to note that these income ranges are subject to change and can vary from year to year, so it's essential to verify the current ranges with the IRS before making a contribution.

So then, if you're eligible, it's wise to contribute the maximum amount to your Traditional IRA each year. Doing so provides you with an immediate tax deduction and allows your savings to grow tax-deferred over time. This means you won't owe taxes on your investment earnings until you start taking distributions in retirement, enabling your money to compound more effectively.

Prioritizing Roth IRA Contributions

Now, once you've maximized your contributions to your 401k and Traditional IRA, the next logical step in your retirement savings journey is to consider a Roth IRA. While Roth IRA contributions don't provide an immediate tax deduction like Traditional IRA contributions, they offer several unique benefits that make them a valuable part of a balanced retirement savings strategy.

Now, before we talk about these benefits, let’s take a step back and recap what makes a Roth different from a Traditional IRA or employer-sponsored plan.

Unlike 401k and Traditional IRA accounts, contributions to a Roth IRA are made with after-tax dollars. This means you pay income tax on the money before contributing it to the account. While this might seem like a disadvantage compared to tax-deductible contributions, it still offers a significant payoff down the line in the form of tax-free withdrawals.

To be sure, with a Roth IRA, both your contributions and the earnings on those contributions can be withdrawn tax-free during retirement, provided the withdrawals meet certain qualifications. This means the money you invest in a Roth IRA today could grow substantially over time, and all of that growth will be yours to keep when you retire.

Now, as of 2023, the Roth IRA contribution limit is the same as that of a Traditional IRA which is $6,500 per year and $7,500 for those aged 50 or older. Even so, with a Roth IRA it’s essential to note that certain income restrictions can limit your ability to put money into these accounts.

For those filing single and head of household, the ability to contribute to a Roth IRA begins to phase out at a modified adjusted gross income (MAGI) of $129,000 and is eliminated entirely at $144,000. For married couples filing jointly, the phase-out range is between $204,000 and $214,000.

Put simply, if you make too much money, more often than not you likely can’t make a direct contribution to a Roth IRA.

Even so, the Roth IRA is a powerful retirement savings tool because it allows you to pay taxes now in exchange for tax-free income later. This can be particularly beneficial if you anticipate being in a higher tax bracket in retirement than you are currently or if you believe that tax rates are likely to increase in the future.

And by contributing to a Roth IRA, you're essentially locking in your current tax rate. This could result in substantial tax savings in the long term, as you won't owe taxes on the growth of your investments when you start taking distributions.

Additionally, Roth IRAs aren't subject to required minimum distributions during the account owner's lifetime, unlike Traditional IRAs and 401ks. This flexibility allows you to manage your retirement savings and withdrawal strategy on your terms.

Calculate the Benefit of a Roth Conversion Using the NPV Approach

Alright, so what if you find yourself in a position where you’ve maximized your contributions to your employer-sponsored plan, and taken full advantage of your Traditional IRA but make too much money to contribute to a Roth IRA? Well, you could consider doing a Roth conversion.

And what is a Roth conversion?

Well, a Roth conversion is the process of transferring assets from a traditional IRA or 401k into a Roth IRA. Now, as we’ve mentioned before, this is a strategic financial decision that can offer significant tax benefits, enabling you to maximize your retirement savings. However, like any financial decision, it entails complexities and requires careful consideration.

Indeed, understanding the benefits of a Roth conversion is just one aspect of the puzzle. To determine if it is the right move, you need to compare the cost of the conversion which is essentially the taxes you would have to pay now versus the potential benefits which is mainly the tax-free withdrawals in the future.

And how do you do this comparison? Well, this is where the net present value (NPV) approach comes into play.

The NPV approach is a financial calculation used to determine the present value of an investment while taking into account the time value of money. In essence, it calculates the worth of future cash flows in today's dollars.

And when applied to a Roth conversion, the NPV calculation helps compare the current tax cost of the conversion with the present value of future tax-free withdrawals. And so, how do we determine if the NPV is good or bad?

Well, if the NPV is positive, it suggests that the present value of the future benefits of a Roth IRA outweighs the immediate tax cost, indicating a beneficial conversion. Conversely, a negative NPV suggests that the conversion may not be advantageous.

How to Calculate NPV for a Roth Conversion

To calculate the NPV for a Roth conversion, several variables need to be estimated:

- Current Tax Cost: This represents the tax amount you would pay if you converted your traditional Individual Retirement Account (IRA) to a Roth IRA today. For example, if you have a traditional IRA worth $100,000, and your current tax rate is 25%, the tax cost of converting to a Roth IRA would be $25,000.

- Future Tax Savings: This estimates the value of the tax you would save on distributions from a Roth IRA in the future. Unlike traditional IRAs, Roth IRA withdrawals are tax-free during retirement. To calculate this, you need to estimate your future tax rate and the expected annual withdrawal amount. For instance, if you anticipate withdrawing $50,000 per year from your Roth IRA in retirement and expect your tax rate to be 25% at that time, your annual tax savings would amount to $12,500.

- Discount Rate: This is an estimate of the rate of return you could expect to earn on your investments if you didn't convert to a Roth IRA. For example, if you expect your investments to earn an average of 6% per year, this would be your discount rate.

- Investment Horizon: This refers to the number of years until you plan to start withdrawing money from your retirement account. If you intend to retire in 20 years, your investment horizon would be 20 years.

Once you have estimates for these variables, you can use the following formula to calculate NPV:

NPV = (Future Tax Savings / (1 + Discount Rate)^Investment Horizon) - Current Tax Cost

The result of this calculation will provide you with the net present value of your Roth conversion in today's dollars. A positive NPV suggests that the conversion is likely a good financial decision, while a negative NPV suggests that you may be better off not converting to a Roth IRA.

Considerations When Using the NPV Approach

Make no mistake, the Net Present Value (NPV) approach is a powerful tool in the decision-making process when considering a Roth IRA conversion. With that said, this approach is not without its complexities, that’s because this approach relies on several estimates and assumptions that can significantly influence the results.

The Impact of Changes in Tax Law

Now, one fundamental assumption in an NPV calculation is that current tax laws will remain constant. However, tax laws are subject to political forces and can change over time.

For example, future changes could affect the tax benefits associated with Roth IRAs, such as tax-free distributions, or modify the tax rates applicable to Traditional IRA distributions. If income tax rates were to decrease in the future, the tax savings from a Roth conversion would be less than what you might have estimated using current rates.

Predicting Your Future Tax Rate: A Not-So-Certain Exercise

Another factor to consider when conducting conversion analyses is that the trajectory of your future specific tax bracket is largely unknown. Indeed, while determining your current tax rate is relatively straightforward in the present, estimating your future tax rate can be much more challenging. That’s because numerous factors can influence this rate, many of which are difficult to predict accurately.

And these factors can include changes in your income, whether from employment, investments, or retirement distributions, which can significantly impact your future tax bracket. And even your personal circumstances, like a change in marital status, can also alter your future tax liabilities.

The Role of the Assumed Rate of Return

And, finally, another key assumption in the NPV calculation to take into consideration is the discount rate, which represents the assumed rate of return on your investments. This rate plays a pivotal role in determining the present value of future tax savings or costs.

Now, while history is typically a useful indicator of market direction, predicting the rate of return can be challenging due to the variability of market conditions and investment performance. And this uncertainty is a key consideration when performing an NPV analysis because the rate of return significantly influences the results of the NPV calculation.

That’s because a higher assumed rate of return reduces the present value of future tax payments, making a Roth conversion appear less attractive. Conversely, a lower rate increases the present value of these future tax savings, potentially favoring the conversion.

Either way, using the NPV approach to evaluate a Roth IRA conversion is a powerful method for understanding the potential long-term financial impact of this decision. However, it's important to remember that this calculation relies on estimates and assumptions that are subject to change. That’s why it’s essential to consider multiple scenarios and work with a professional who can provide personalized advice based on your specific circumstances.

Is a Roth Conversion Right for You?

Taken together, in the ever-evolving landscape of preparing for financial independence, the thing that remains constant is the need for a strategic and informed decision-making process. And, as high-earning tech professionals and business owners, you possess the power to shape your financial destiny and secure a measure of financial independence that reflects your purpose and values.

Remember, the path to financial freedom is as unique as your fingerprint. That's why it's essential to understand the intricacies of balancing taxable and tax-free accounts, strategically leveraging your 401k contributions, and making informed choices regarding traditional and Roth IRA contributions.

And by calculating the net present value of a Roth conversion, you can gain a clearer understanding of the potential benefits and make decisions that align with your long-term goals and help ensure that you're making a decision that's right for you.

Indeed, by understanding the various tradeoffs, considering the order of operations, and harnessing the power of Roth conversions, you'll be well-equipped to make confident and informed decisions about your wealth. Even more crucial, doing so will take you one step closer to becoming the master of your own financial independence journey.

Asset Location vs. Asset Allocation: The Winning Formula for Wealth

Have you ever wondered why your savings aren't growing even though you're contributing to an investment account? It may be because you haven't set your investment strategy.

That's what happened to Mariam.

Now, Mariam knew the importance of investing and that her bank account wouldn't cut it when it came to satisfying her long-term financial independence goals. But, like many uninitiated investors, Mariam misunderstood the concept of investing and believed that simply opening an investment account would guarantee high returns.

Sound familiar?

Well, in Mariam's case, she opened a Roth IRA, because that's what she's heard she's supposed to do. In fact, Mariam believed that her Roth IRA was all she needed, not realizing that the account itself was just a vessel for her investment strategy.

And how many of us have ever made that same mistake?

Well, everything changed when Mariam discovered that her Roth IRA wasn't performing as well as she had hoped. And it turns out that her account was all sitting in cash and not actually invested. That's when she realized that she had focused too much on the account itself and not enough on the underlying investment strategy.

So, what did she do?

Well, frustrated with her situation, Mariam took the time to track down resources and professional assistance that helped her discover that focusing solely on her Roth IRA may not have been a solid strategy from the start.

To be sure, Mariam discovered that the key to a solid investment strategy begins with putting her savings not only in suitable buckets, but also in choosing an ideal mix of stocks, bonds, and other assets that align with her near- and long-term life and savings goals.

Now, with a renewed sense of confidence, Mariam implemented her new investment strategy. And it was at that point that she knew she was making informed decisions and using all available savings vehicles, like her brokerage, employer retirement plan, and her IRA in an orderly manner.

So, what's the moral of the story here? Well, to build real wealth, it's essential to not just put money in an investment account, but also to understand the difference between asset location (that's the types of investment accounts) and asset allocation (or your investment strategy) and use them effectively within your overall financial plan.

Understand Your Investment Account Options

Indeed, understanding the difference between asset location and asset allocation is just as crucial as knowing which type of account to stash your cash in and how to make that money work for you once it's saved.

Account Asset Location

So, what is asset location? Well, this approach refers to placing your savings contributions into different savings buckets, or types of accounts based on their tax treatment. Now, these accounts might include taxable accounts, tax-deferred accounts (like a 401k and traditional IRA), and tax-free accounts (like a Roth IRA).

And, what's the whole point of asset location? Well, the point of asset location is to maximize the tax efficiency of your investment portfolio. And while you're likely aware of some of the immediate tax benefits of putting your money into these various accounts, the real focus should be on how your investments will be taxed when the money comes. That's because not being aware of your tax location could mean having less money to cover your living expenses when you need it the most.

So then, how does asset allocation differ from asset location? Well, asset allocation is the art of spreading your investments across various asset classes like stocks, bonds, cash, and other investments. The goal here is to build a balanced and diversified portfolio that vibes with your risk tolerance, time horizon, and financial goals.

Indeed, a well-diversified portfolio keeps your overall risk in check since your investments are spread across different assets, which react differently to market ups and downs. Now, before we talk about how to invest your savings, let's discuss the various savings buckets, or account types, and what they're typically used for.

Brokerage Accounts

Let's begin by taking a look at brokerage accounts. Now, a brokerage account is the most basic type of investment account that you'd open at a firm like Schwab, Fidelity, or Vanguard. And you can think of a brokerage account as your flexible platform for chasing various financial goals, like growing your wealth, saving for retirement, or funding major life expenses.

These accounts let you buy and sell various assets, like stocks, bonds, mutual funds, and ETFs, which promotes portfolio diversification and long-term growth.

Now, unlike retirement accounts such as 401ks and IRAs, brokerage accounts don't offer tax-deferral benefits. This means that you fund these accounts with after-tax dollars, and you'll likely have to pay taxes on your capital gains, dividends, and interest in the year they are earned. Now, it's possible to reduce these tax burdens through various investment strategies, but we'll save that discussion for a future report.

For now, what's essential to note here, though, is that while brokerage accounts don't have the same tax perks as other tax-advantaged accounts, they still allow you to put your savings to work for the long-term while giving you the flexibility to pull your money out penalty-free anytime you need it.

Retirement Accounts (401k, 403b, IRA)

Now, retirement accounts like 401ks, 403bs, and IRAs are tailor-made to help you save for your golden years. Now, when it comes to retirement accounts available through your employer, what’s essential to note is that in most cases these account types allow you to make contributions on a pre-tax basis, which means that you're putting more money to work before Uncle Sam gets his share of your earnings.

And in the case of Traditional IRAs, after-tax contributions can be tax deductible in certain circumstances. Either way, money in these accounts grow tax-free until you’re ready to take the money out.

Sounds good so far, right? What's the catch, you ask?

Well, the catch is that you typically can't access these accounts penalty-free until age 59 1/2, and when you do, you'll likely be taxed at ordinary income tax rates. Even so, because more money is going in on a pre-tax basis in the early years as far as your contributions are concerned, the more money you're putting to work and allowing to compound over time.

Now, one caveat to note here when it comes to retirement accounts is the Roth IRA. A Roth IRA is an account that you typically set up with a brokerage firm (or Roth 401k if your employer offers it), and is funded with after-tax dollars. While you generally can't access the funds penalty-free until age 59 1/2, the benefit of a Roth IRA is that the money grows tax free, and you typically pay no tax when you take the money out.

Education Savings Accounts (529 Plans)

Now, education savings accounts, like 529 Plans, are another kind of savings bucket designed to help families save for future education expenses. And they're useful because these accounts offer a tax-advantaged way to invest and grow funds for educational purposes.

That's because earnings in a 529 Plan grow tax-free, and withdrawals for qualified education expenses don't get hit with federal income tax. What's more, some states offer tax deductions for 529 Plan contributions, which make them a compelling savings vehicle in certain situations.

Health Savings Accounts (HSAs)

And finally, health savings accounts (or HSAs) allow you to save and pay for qualified medical expenses while offering some nice tax advantages.

In fact, HSAs offer a triple tax advantage and that's because 1) contributions are made on pre-tax basis and lower your taxable income; 2) earnings grow tax-free; and 3) withdrawals for qualified medical expenses are also tax-free. And these combined tax perks make HSAs an attractive option for healthcare expenses.

So, to sum it up, there are plenty of investment accounts designed to address specific savings goals, each with its own unique tax advantage. Brokerage accounts, for example, serve as a flexible platform for pursuing various financial goals, while retirement accounts, like IRAs and 401(k)s, are all about helping you save for your retirement, offering tax-deferred growth and, in some cases, tax-deductible contributions.

Asset Location in Action

And so, why is it important to understand the difference between taxable and tax-advantaged accounts?

Well, in the book, "The Bogleheads' Guide to Investing," the authors highlight the importance of asset location in maximizing after-tax investment returns. They point out that different investments are subject to different tax treatments, and placing them in the right types of accounts can significantly impact your overall tax bill.

The authors suggest prioritizing tax-advantaged accounts, like 401(k)s and IRAs, for tax-inefficient investments, such as actively managed mutual funds and real estate investment trusts (REITs). These investments generate more taxable income, so holding them in tax-advantaged accounts can potentially shrink your overall tax bill.

On the flip side, tax-efficient investments, like broad-based index funds and municipal bonds, might be best held in taxable accounts. These investments generate less taxable income, so holding them in taxable accounts can potentially reduce your overall tax liability.

Taken together, understanding these investment accounts and their respective tax benefits can empower you to make informed decisions that align with your unique financial goals and help optimize your savings strategies.

Understand How Asset Allocation Puts Your Money to Work

Okay, so now that you understand where your savings should go and why, let's discuss how you can actually put your money to work through asset allocation.

And, what is asset allocation?

Well, as we mentioned earlier, asset allocation refers to the process of dividing your savings among different asset classes in order to balance risk and return. Again, these assets include stocks and bonds, and US and international investments. And we take this approach because what we're trying to do is not only grow your savings, but reduce the chance for losses by diversifying risk across various assets.

The Power of Asset Allocation

So how much does asset allocation matter? Well, years ago a group of financial researchers led by Gary Brinson, Ralph Hood, and Gilbert Bebower wanted to figure out which factors influenced the returns investors earned from their portfolios.

So, to do this, they looked at the performance of a big group of pension funds. And what they found was that there are generally three main factors that determine the returns earned by the funds themselves, including security selection, market timing, and asset allocation.

Now, when it comes to security selection, this process refers to the act of choosing individual investments held in a portfolio, like which stocks or bonds to buy. And what the researchers wanted to understand was whether fund performance was driven by terrific stock picking, or some other factor.

And, so what did they find? Well, what the researchers found in their study was that stock picking was actually the least important factor in determining a portfolio's long-term returns.

In fact, the researchers found that the asset allocation decision was the most critical factor in determining a portfolio's returns. Indeed, the paper shows that even trying to time the market was less important than getting the asset allocation right.

And why's that?

Well, that's because different types of investments have different levels of risk and return. For example, stocks are generally riskier than bonds, but also have the potential for higher returns. Cash, on the other hand, is less risky but also has lower returns.

And the fact is that, over the long-term, markets typically don't move up, or down, in a straight line. Therefore, by choosing a mix of investments that matches your goals and risk tolerance, you can maximize your chances of earning solid returns over the long run. Indeed, trying to time the market or pick individual investments is less important in the grand scheme of things than holding a diversified basket of investments.

The Benefits of Diversification and Risk Management

So, what makes asset allocation the most important decision when it comes to long-term investors? Well, when it comes down to it, as the old adage goes, it doesn't matter how much you make but how much you keep.

Indeed, Benjamin Graham, once a professor at Columbia Business School and regarded as the father of value investing, says that "the essence of portfolio management is the management of risks, not the management of returns."

Indeed, if we were to boil down the purpose of asset allocation to its essence, it could be encompassed in that single quote from Graham. Now, I know what you're likely going to say at this point and that's, "doesn't a diversified portfolio produce returns that are less than those of a single stock, or highly concentrated investment position?"

And, well, the answer here is, "it depends…"

The fact is that asset allocation is not so much about optimizing returns as it is about managing risk so you can stay in the investing game when markets inevitably fall, allowing you to achieve your long-term savings goals.

What do we mean here? Well, let me give you an example from the perspective of workers who concentrated their retirement savings in employer stock.

Now, in 2008, Wachovia, one of the largest financial institutions here in the US, suffered significant losses due to its exposure to toxic mortgage assets which ultimately led to its failure. Now, at its peak, the company had over 3,400 retail banking branches and employed more than 120,000 people.

Even so, a few bad business decisions combined with a perfect storm that was the Global Financial Crisis, led to a steep decline in the value of Wachovia's stock, ultimately wiping out the retirement savings of many of its workers.

More recently, many tech investors who had jumped on board the tech stock rally that took place between 2020-2021 ultimately saw their savings diminished after inflation, war tensions and aggressive rate hikes led to a notable tech stock selloff in 2022. Indeed, remember all of the unicorn IPOs and SPACs that were supposed to make many millionaires? Well, there are likely many unfortunate souls out there who decided against diversification in exchange for diamond hands, and are now paying the price of holding onto their concentrated positions.

Make no mistake, diversification and risk management are essential elements of successful investing. That's because diversification helps investors spread their risk across different types of investments, while risk management helps minimize losses and maximize returns. And, by understanding the benefits of diversification and risk management, you can build an investment portfolio that is well-positioned to weather market volatility and help you achieve you long-term financial goals.

Risk Management's Role in Asset Allocation

Alright, now that we've covered the basics, let's talk about how asset allocation and asset location work together to put your money to work in a tax-efficient manner.

To this end, you'll recall that asset allocation is all about putting together your investment dream team. It's like picking players from all the different asset classes like stocks, bonds, and other risk assets. Then, by spreading your money across these various options, you're tapping into their unique strengths and making sure market ups and downs don't mess with your overall life and savings goals.

Sounds like a winning strategy, right?

Well, before you can put this money to work, you'll need to determine where your investments will hang out. More specifically, you'll need to determine how much of your investments are held in taxable accounts, tax-deferred retirement accounts, or tax-exempt places like Roth IRAs. Remember, each account type has its own set of tax advantages and distribution setbacks.

The trick here is to be savvy about which investments go where, so you get the biggest bang for your tax buck. That means putting tax-inefficient investments in tax-advantaged accounts and tax-efficient investments in taxable accounts. This way, you keep more of your hard-earned money and preserve it for the long-term.

For example, you can stash tax-inefficient investments, like high-yield bonds, in tax-deferred accounts, and tax-efficient investments, like index funds or municipal bonds, in taxable accounts.

How to Put Asset Allocation and Location to Work for You

So then, now that you know why asset location and asset allocation are essential investing decisions, the next big question that you likely have is, "where do I start?"

Saving in the Right Buckets

Well, the first decision in any disciplined investment strategy is to identify what you're saving for, and how much you need to have saved. Now, you'll likely recall that this is a topic that we've covered at length in previous reports, so we won't go into it here today. Even so, be sure to check out our previous posts if you need help on figuring out how to calculate your savings need.

Alright, so once you figure out how much you need to have saved, then the next thing we need to do is to determine which accounts need to be funded to meet your savings goals.

As you'll recall, you have three investment buckets to which you can contribute your savings, and these are taxable, tax-exempt and tax-free accounts. The key difference between these account types is the tax treatment of the investments held in each account and how gains are taxed when they occur.

Remember, in taxable accounts, for example, you could be subject to taxes on any income or capital gains generated by the investments, which can reduce your overall investment return. In tax-exempt and tax-free accounts, however, you're likely not subject to taxes on the income or gains generated by the investments, which can result in higher overall returns if you have a long enough savings horizon.

Now, to this point, when making asset location decisions, Larry Swedroe, in his book, "The Only Guide You'll Ever Need for the Right Financial Plan", recommends that you prioritize first making contributions to your tax-advantaged accounts, such as your 401(k)s, IRAs, and HSAs. That's because these accounts provide tax benefits, such as tax-deductible contributions, tax-free growth, and employer-matching contributions. Therefore, it makes sense to take advantage of these benefits as much as possible whenever you can.

Swedroe also suggests that you should consider holding tax-inefficient assets, like bonds or REITs, in your tax-advantaged accounts. By doing so, you can allow these investments to grow tax-free and reduce your tax burden on the income generated by them.

On the other hand, it may be better to hold tax-efficient assets, like stocks or ETFs, in your taxable accounts. Again, these types of investments generate less taxable income and therefore have a lower tax impact on your overall investment returns.

What's more, Swedroe believes that prioritizing tax efficiency in your asset location decisions is essential because taxes can significantly eat away at your investment returns over time. And by following a disciplined asset location strategy, you can maximize your after-tax returns and achieve your financial goals more efficiently.

Identify Your Risk Tolerance

Alright, so now that you've identified the ideal buckets to contribute money into, you're ready to invest, right?

Not so fast.

Before your money goes into your taxable, tax-exempt or tax-free account, the next decision in any disciplined investment strategy is to identify your risk tolerance.

And what is risk tolerance, you ask?

Simply put, risk tolerance reflects the amount of money you're willing to put at risk over a period of time for a given amount of gain. As the saying goes, the higher the risk, the higher the reward.

Now, in his book, "The Little Book of Common Sense Investing", Vanguard founder Jack Bogle talks about how you can identify your own investment risk tolerance by evaluating your time horizon, financial goals, comfort with volatility, and prior investment experience.

For example, when it comes to your time horizon, the longer you're willing to hold onto your investments before selling, the higher your risk tolerance. On a similar note, if you made it through the recent market selloffs without batting an eye and can handle taking short-term losses with the hope for longer-term gains, then that may be a sign that you're more risk-tolerant.

On the other hand, if your investment goal is to save for the down payment on a house, or retire in less than five years, then you may likely have a lower tolerance for risk than someone who otherwise has life goals that are years down the road. And if you're still not sure about your risk tolerance, you can complete a questionnaire to help provide you with a better gauge of where you stand.

And what is a risk tolerance questionnaire?

Well, a risk tolerance questionnaire typically consists of a series of questions about your financial situation, investment goals, time horizon, and comfort level with various investment risks. And based on your responses, the questionnaire generates a risk profile that suggests an appropriate asset allocation strategy for your investment portfolio.

Either way, Bogle believed that you should be honest with yourself about your risk tolerance, as it can be a crucial factor in determining your investment strategy. And by understanding your own risk tolerance, you can make more informed decisions about asset allocation and portfolio diversification.

Find Your Ideal Asset Allocation Framework

Now, once you have a better understanding of your risk tolerance, it's time to identify your ideal asset allocation framework. Now, you'll recall that asset allocation refers to the ideal mix of stocks and bonds held in a portfolio that reflects, in addition to your risk tolerance, your overall investment goals, income needs, and savings time horizon.

Now, generally speaking, securities like bonds have lower risk than stocks do. Therefore, if you have a low-risk tolerance, you'll likely have an investment portfolio with more bonds than stocks. Alternatively, if you have a higher risk tolerance or a longer savings horizon, you'll likely have a higher allocation to riskier assets like stocks in your portfolio.

So, how do we put these pieces together? Well, let me illustrate these two points about varying asset allocations by sharing Warren and Rebecca's story.

Now, Warren was a seasoned investor, who had spent decades building his wealth. Now on the verge of retirement, his focus was on preserving his capital and generating a steady income to support his golden years. He spent his days evaluating his portfolio, seeking out stable income-generating assets, and reminiscing about the financial lessons he had learned over the years.

Rebecca, on the other hand, still had years to go in her investment journey. To be sure, with many years ahead of her until retirement, she was keen to grow her wealth and embrace the power of compounding. That's why Rebecca spent her nights researching high-growth opportunities and learning from experienced investors like Warren.

Now, one day, Warren and Rebecca decided to learn from each other's investment strategies by sharing their insights and experiences.

That's when Warren, with his retirement just around the corner, explained to Rebecca how he crafted his own conservative asset allocation strategy. He emphasized that his strategy centered on the importance of low-risk assets such as government bonds, blue-chip stocks, and dividend-paying stocks. That's because he wanted to ensure that his investments were safe from market volatility and so his portfolio could provide a steady income stream.

Rebecca, on the other hand, shared her perspective on taking advantage of her long investment horizon. She explained to Warren that her strategy involved a more aggressive asset allocation, focusing on high-growth opportunities. She allocated a significant portion of her portfolio to emerging markets, small-cap stocks, and disruptive technology start-ups. And, she believed that the potential for outsized returns outweighed the risks, because she had plenty of time to recover from any short-term losses.

Now, as months passed, the two friends watched the markets move in different directions. Warren's portfolio, with its emphasis on stable investments, slowly but steadily gained in value. He knew that his primary goal was capital preservation and income generation, rather than chasing high returns.

Rebecca's portfolio, however, experienced substantial fluctuations, soaring to new heights one day, only to plummet the next. And throughout the year, they continued to share their experiences and insights, learning from each other's successes and failures. And by the end of the year, they discovered that both of their portfolios had performed quite well overall.

Indeed, Warren's cautious approach had provided the stability and income he needed for his impending retirement, while Rebecca's bold strategy had produced some impressive gains, setting her up for long-term wealth accumulation.

Overall, they each realized that their different investment horizons had led them to different asset allocations, and ultimately, different paths to success. Warren’s conservative approach was well-suited to his impending retirement, while Rebecca's growth-oriented strategy was ideal for her long investment horizon.

Don’t Forget About Your Investment Strategy

Warren and Rebecca’s story illustrates how different investment horizons and risk tolerances can lead to distinct asset allocation strategies, each tailored to an investor's unique circumstances and objectives. But more importantly, the big takeaway here is that by understanding the differences between various account types and their tax implications, you can avoid a common mistake of confusing account contributions with an investment strategy.

And this knowledge is essential because it can help you create personalized, effective financial plans that align with your unique goals and circumstances. And, when you understand the distinction between accounts and strategies, you can better allocate your financial resources, choose appropriate investments, and monitor their progress toward your financial goals. More importantly, having this understanding and actually doing the work can put you one step closer to becoming the master of your own financial independence journey.

Manage Your Tax Anxiety and File Your Returns with Confidence

Is tax anxiety causing you to wait until the last minute to file your tax returns? If so, then you’re in good company.

According to one survey, over thirty percent of respondents said they waited until the tax filing deadline to prepare their returns last year.

Now, if you’re one of these individuals, there’s likely many reasons why you’ve chosen not to file your taxes yet.

Maybe you anticipate owing money to the government this year and you’re using every last moment to wait to pay Uncle Sam his owed money. Or, you might find the process to file your returns complicated and it just stresses you out. Or maybe, you haven’t found the time to sit down and complete your returns and you just need to put it on your to do list.

Whatever your case may be, you should know that the April 18 deadline to file your tax returns is just a few weeks away. And while it may seem like you have enough time to get the work done, in some instances, the longer you delay, the more it could cost you.

Indeed, for many individuals, filing your taxes is just a process of sitting in front of your computer, entering your tax documents into planning software and either choosing how you want to receive your tax refund or cutting a check to the IRS.

So, what can you do if you find yourself paralyzed by indecision and hesitant to prepare your returns?

Well, the truth is that you can overcome the anxiety that comes with filing your returns by following a simple process to get the job done. Indeed, knowing what you should do before, during and after you file could give you the motivation to finally complete your returns sooner rather than later.

And, at a basic level, using a stepwise approach to navigating your returns process may help you reduce your anxiety levels and avoid some costly mistakes commonly associated with procrastination and avoidance this tax season.

What to do Before You File Your Returns

Now, depending on your situation, one of the first things that you'll likely want to do before filing your returns is to evaluate whether you should file your returns on your own or take the time to go about hiring a professional to help complete your returns.

If you're still trying to determine which route you should take, be sure to take a moment to review our recent article where we discuss the criteria for evaluating when to go it alone and when hire a tax pro.

Either way, before you begin calculating your tax for the year, you’ll likely want to make sure that you have gathered all the proper documents to complete your tax return. Doing so will ensure that you’re accurately accounting for all income received, and not missing out on potential tax penalties or opportunities down the road.

And, so, how do you know whether you've gathered all the necessary information to complete your return?

Well, start by creating a checklist of all the documents and forms needed to complete your tax return, such as W-2s, 1099s, and receipts for charitable donations, medical costs, and other deductible expenses.

And if you need help figuring out where to start with your checklist, take a moment to review last year's tax returns. Indeed, by reviewing last year's return, you can identify the documents and forms that were required to complete your return and can help ensure that you have not overlooked any necessary paperwork.

Another option for ensuring that you have all the necessary documents to file your return is to log in to online portals for your current and former employers, financial institutions, and other organizations that may be required to provide tax documents, such as W2s, 1099s, mortgage or interest statements.

And finally, you can complete a tax organizer to ensure that you have gathered all of the documents necessary to prepare your return.

And, so, what is a tax organizer?

Well, a tax organizer is a tool that is used by tax professionals to help individuals gather and organize the information needed to prepare an accurate tax return. It typically includes a list of questions and prompts to help you identify and provide all the necessary information to complete your return, as well as worksheets to organize and summarize the data.

And when in doubt, completing your organizer can facilitate better communication between you and your tax professional, ensuring that all necessary information is obtained and questions are answered promptly.

Either way, before you get started with filing your returns, be sure to organize all tax-related documents in a secure and easily accessible location, such as a dedicated digital vault or online storage service.

And if you’re not sure how to go about this process, be sure to check out our FI|Mastery January action items for tips on ideal storage locations for critical documents and how tax organizers work.

Which institutions should I contact if I have problems?

Now, it's vital to note that reporting institutions can and do make errors in the tax documents they send to you. These errors can be as simple as omitting a taxpayer ID number to something as costly as reporting the wrong cost basis on a 401k rollover that could potentially cost you thousands of dollars in taxes due.

So, what can you do if you discover an error in one of your tax documents?

Well, first things first, contact the issuer of the tax document, such as your employer or the financial institution that sent you the tax form, and inform them of the error as soon as you discover it. Then, explain the nature of the error and provide any supporting documentation if necessary.

Next, request that the issuer provide a corrected tax document as soon as possible. In most cases, they’re required to provide a corrected form by January 31st, but, given that we’re past that deadline now, it will likely take a week or two to receive the updated document so plan accordingly.

That’s why getting started on your taxes sooner rather than later can help you avoid the anxiety related to working against a tight deadline. And when you do receive the corrected tax document, take a moment to review it to ensure that the error has been corrected and that all other information is accurate.

Now, keep in mind that if you discover an error on a tax document after you've already filed your return, you have the option to file an amended tax return to correct the error. With that said, the amended return must be filed within three years from the original filing deadline or two years from the date the tax was paid.

Overall, however, as you’re working to get your tax documents corrected, keep records of all communications with the document issuer regarding the error, as well as copies of the original and corrected tax documents and any other relevant paperwork.

These records may be necessary if the error is not corrected or if the IRS questions your returns down the road. And when in doubt or if the error is complex and you're unsure how to proceed, you may need to seek the assistance of a tax professional or accountant.