Top 5 Considerations When Shopping for Life Insurance

Any expected death is always a tragedy. But if the person who passed away was earning a large percentage of a family's income, it can leave the grieving family members in a difficult financial situation. A life insurance policy can help to offset the loss of income and spare those who are left behind from being forced to deal with tough economic decisions. When shopping around for the right life insurance coverage for you and your family it's important to ask yourself the right questions.

1. How Much Life Insurance Do I Need?

While you may be tempted to buy the most extensive policy which you can afford, the basic rule of thumb is to buy at least 10 times your annual salary. This is a good starting point, but for parents who have younger children, it is essential to consider the costs associated with education. Some suggest an additional $100,000 of coverage for each child. Other considerations such as outstanding debts need to be acknowledged, as well.

2. What Are the Different Types of Insurance Policies?

The most popular options for life insurance are term life, whole life, and universal life policies.

- Term life insurance coverage lasts for a certain number of years and then ends. These types of policies have the lowest premiums but offer limited protection and the fewest number of options. Many term life insurance policies let you renew policies but at a higher premium.

- Whole life insurance requires you to pay the same amount in premiums for a certain number of years for a fixed amount of coverage. Once your policy is paid off, any death benefits are secured. This type of policy places part of your premiums in a tax-deferred saving plan which you can borrow against.

- Universal life insurance allows the most flexibility since it will enable you to increase or decrease the amount of your coverage. Whole life policies usually offer the option for a fixed death benefit or an increasing benefit based on the value of the policy at the time of passing.

Each insurer has its own rules, so make sure to speak with your insurance agent to fully understand the terms and options available in your policy.

3. Which Life Insurance Policy Is Right for Me?

The decision of which type of insurance policy you choose is entirely dependent on your personal financial and family situation. But it is important to note that most people will require more life insurance as their family grows and will need less life insurance as they age. It is best to speak with your financial advisor to determine the best policy for you. Don't depend on the advice of an insurance agent who typically earns more money with whole life and universal life policies.

4. Who Should My Beneficiaries Be?

Your choice of the primary beneficiary for your policy is a critical decision to make. Usually, people choose a spouse or significant other, but you may choose anyone to make your primary beneficiary. You can even assign a charity or a trust as the primary beneficiary. Besides a primary beneficiary, make sure to designate a contingent beneficiary if your primary beneficiary passes first.

5. What Other Types of Life Insurance Are Available?

Guaranteed issue life insurance is an option for people who only wish to avoid having your loved ones pay for your funeral and minor outstanding debt. This type of insurance pays out a small sum, typically under $30,000, but does not require a medical check. Accidental death insurance is an option for those who want to ensure that in the event of an untimely death due to an accident, their loved ones will have the money they need. This type of life insurance will not pay out if a person dies from natural causes.

Although it can be difficult to think about preparing for the end of life, it is a significant financial decision everyone needs to think about.

How Do I Know How Much of a Health Benefit I Need?

Making decisions regarding your health insurance can be complicated. it's important to strike a balance between value and coverage, getting the most out of your hard-earned dollars – even if your employer provides a good health care plan. When you are just starting out in the work world and your parent’s insurance plan no longer covers you, you’ll need to make the best choice given your new circumstances.

10 Essential Health Benefits

Fortunately, the Affordable Care Act (ACA) gives us a good starting point. The Act lists 10 categories of what it calls essential health benefits that any qualifying plan must contain.1 Those categories are:

- Ambulatory patient services (outpatient services)

- Emergency services

- Hospitalization

- Maternity and newborn care

- Mental health and substance use disorder services, including behavioral health treatment

- Prescription drugs

- Rehabilitative and habilitative services (those that help patients acquire, maintain, or improve skills necessary for daily functioning) and devices

- Laboratory services

- Preventive and wellness services and chronic disease management

- Pediatric services, including oral and vision care

Additionally, plans that cover children must have dental care available. While employee health plans cover dental care, government plans like Medicare and Medicaid do not. That bias is reflected in the ACA.

If you are new to the health insurance market, the government’s 10 essential health care items is a good place to begin when you are trying to decide what type of plan you will purchase. Most of them are self-explanatory. Some may require a deeper dive to help you decide what you really need if you are looking to cut monthly costs.

Inpatient Outpatient and Emergencies

It’s likely that you are going to need to see a doctor at some point in your life. Getting health insurance that covers basic procedures like a check-up makes good sense. You should also be covered in case of emergencies or when you need to have an ambulance or EMT come for you. Ambulance services can be extraordinarily expensive.

Laboratory services cover the cost of any tests a physician might order. If you get a full check-up, a doctor may order blood work. If you are hospitalized, a doctor may run a battery of tests on you. This seems an essential part of a health insurance plan.

Prescription Drugs

A 2017 report conducted by the American Association of Retired Persons’ public policy arm showed that costs for prescription drugs are rising at an alarming rate. The average price for some drugs in 2015 were three times higher than they were in 2005.2

Some generic drugs you may take like an antibiotic may be manageable. Drugs used to treat common diseases like Type 2 diabetes can become very expensive. Rather than be surprised with a giant bill at the pharmacy, it would be wise to buy health insurance that covers prescription drugs.

Child Services

Plans that cover pediatric care, prenatal care and maternity care may seem like a luxury if you are single, something that you can handle when the need arises. In the past, insurance providers considered pregnancy to be a pre-existing condition. So if you tried to buy health insurance while you or your spouse was pregnant, you would have been denied coverage. The ACA changed all that, and you can receive coverage even if you are already pregnant. Currently, some politicians are investigating removing that part of the ACA.

Weigh Your Options

Most plans on the ACA’s Health Insurance Marketplace will cover the 10 essentials. You may be able to find plans that aren’t on the ACA’s marketplace that are less costly but cover less. You should discuss the decision with someone knowledgeable about the health insurance market and weigh their advice against your adverseness to the risk of going with a cheaper insurance plan.

- https://www.healthcare.gov/coverage/what-marketplace-plans-cover/

- https://www.aarp.org/health/drugs-supplements/info-2017/prescription-drug-costs-fd.html

5 Steps to Determining Your Risk Tolerance

There’s a degree of risk in any financial investment. There are no sure winners and no sure losers, either. How comfortable you are with the latter statement may give you a clue as to your risk tolerance. You can think of risk tolerance not only as how much you are willing to lose on your investments but rather how much uncertainty you can live with from day to day.

Are you the type to sit and watching to stock ticker pass by all day? If so, does it fill you with dread or excitement? These are the kinds of questions you should be asking yourself. The answers will, in turn, help you pick out an investment portfolio that’s right for you.

1. A Personality Test

The individual identity component of risk tolerance assessment shouldn’t be ignored. Some of your risk tolerance can be measured, meaning that the amount of risk you can tolerate is based on factors like your age or your income. However, you may simply dislike making risky investments. That’s okay. You should be comfortable with spending (or not) your money the way you like.

2. What are Your Financial Goals?

Do you save money to accumulate wealth or are you looking for ways to retire early? If your only goal is to have a nice pile of money to retire on when you’re 70, slow and steady is your investment pace. You’re looking to have a steady accumulation over time that will be just enough for a happy retirement. If you want to go out while you’re relatively young, you’re looking for investments that are a high risk/reward ratio. You don’t mind some volatility if it can get you to the finish line faster.

These retirement-focused goals aren’t the only goals that can impact your investment strategy. You may be saving for a house or considering buying a business.

3. How Much Time Do You Need?

If you’re relatively young, you have plenty of time to ride out the peaks and valleys of the economy. You can tolerate a little more risk by design. If you have a goal you need to meet quickly (buying a home) or you are nearing retirement age, you may want to think more conservatively so that you don’t lose too much money.

4. Your Wealth and Income

If you have $5 million to invest, you can take more chances than you should if you have $50,000. That’s fairly straightforward. You may also consider additional factors, such as the amount of debt you’re carrying, or whether your personal ecosystem (job, family, assets, etc.) is strong and stable.

5. Get Good Advice

Working with a financial advisor can reveal clues about your risk tolerance and map out a strategy. You can prepare yourself for the discussion by looking at one of the many online questionnaires that can help you look at yourself. You can ask some of the more obvious questions yourself, such as, what would you do if presented with $25,000 to invest, or whether you like to participate in extreme sports.

Even after you’ve asked yourself the tough questions, you may still want to talk about risk tolerance and assessment with an experienced financial advisor. You may find that you are not as risk averse or risk tolerance as you thought. You can learn about yourself and make better decisions regarding your future.

Four Ways to Prepare for Heightened Market Volatility

Many investors know that managing volatility is central to achieving essential financial goals. But how much should you worry about volatility, and what can you do to prepare for it? Volatility represents the ups and downs of asset prices over time. And quite often it’s not the volatility that you should be worried about as it is periods of heightened market volatility.

What’s more, human expectations about the future tend to influence asset price movements. And it's during periods of changing expectations and uncertainty that asset prices swing wildly. Being aware of the narratives driving the markets and having a plan in place before they change is central to financial success. The bottom line is that if you're unprepared for periods of heightened volatility, you might be exposing your savings to unnecessary losses.

#1 Become Familiar with Volatility

Volatility is a normal part of investing. Asset prices do not move up in a straight line but tend to ebb and flow as they appreciate over time. Volatility is the price that you pay to earn a return on your investment. Indeed, what should be at the top of your list of in terms of investing concerns is not volatility itself, but periods of heightened volatility. Before diving deeper into the topic, let's explore some basic concepts.

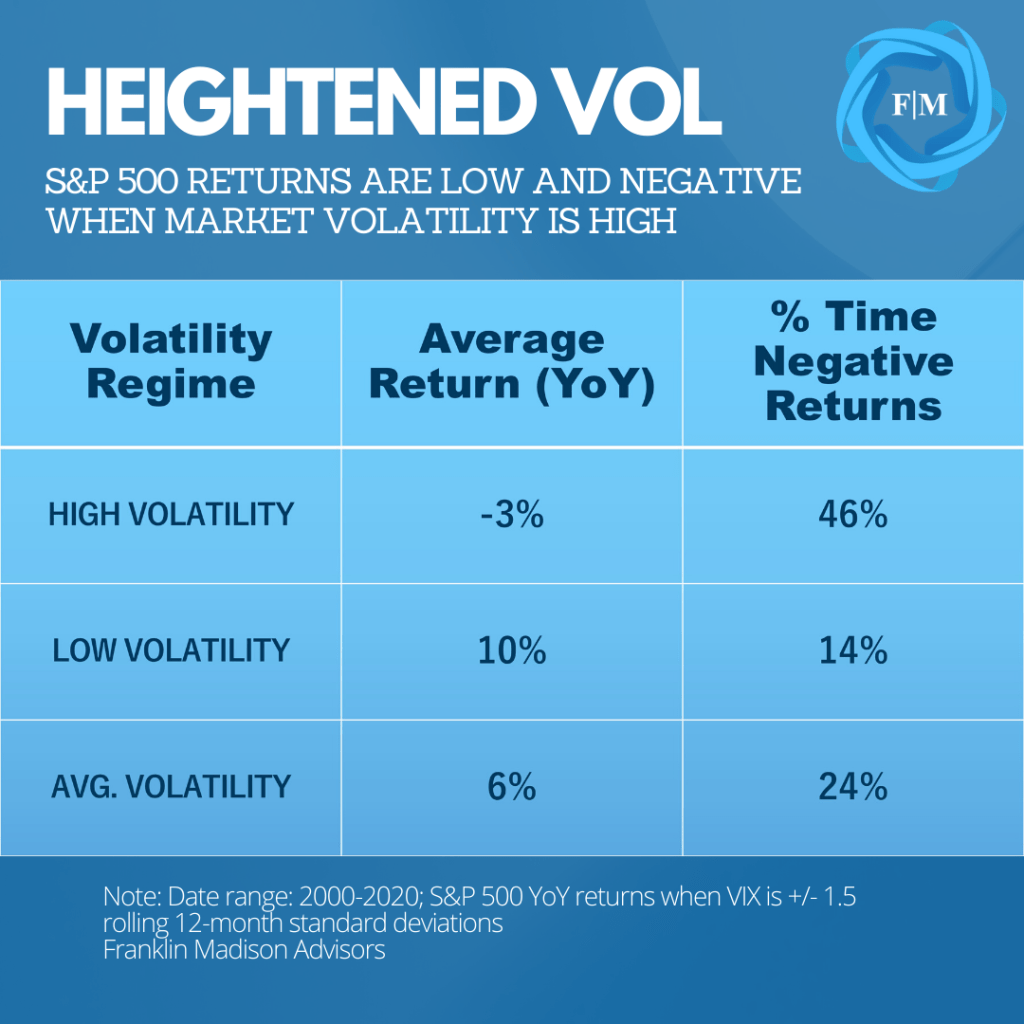

One way to quantitatively measure volatility is through a mathematical standard deviation of an asset's return. This measure describes the historical tendency for prices to swing up or down versus their long-term average. The higher the standard deviation, the higher the volatility. This understanding is essential because the wider the swings in price returns relative to their long-term average, the less certainty you may have about future returns from one period to the next. And less certainty tends to go hand in hand with higher investment risk.

Let's look at an example. From the turn of the century, the S&P 500 index has averaged a modest yearly gain of about 5.3%. This average return, however, masks some of the sharp market moves over the past two decades. If we looked at periods when market volatility was elevated during this time, the S&P 500 returned an average year-over-year loss of -3.3%. However, periods of lower volatility were associated with a higher average annual gain of around 10%.

The takeaway here is that volatility can be used to generate investment returns, mainly when it is low. More crucially, however, history tells us that sudden moves higher in volatility can detract from those returns. Therefore, awareness of the potential impact of a sudden rise in market volatility is vital to improving your investment outcomes.

Source: Broadview Macro Research

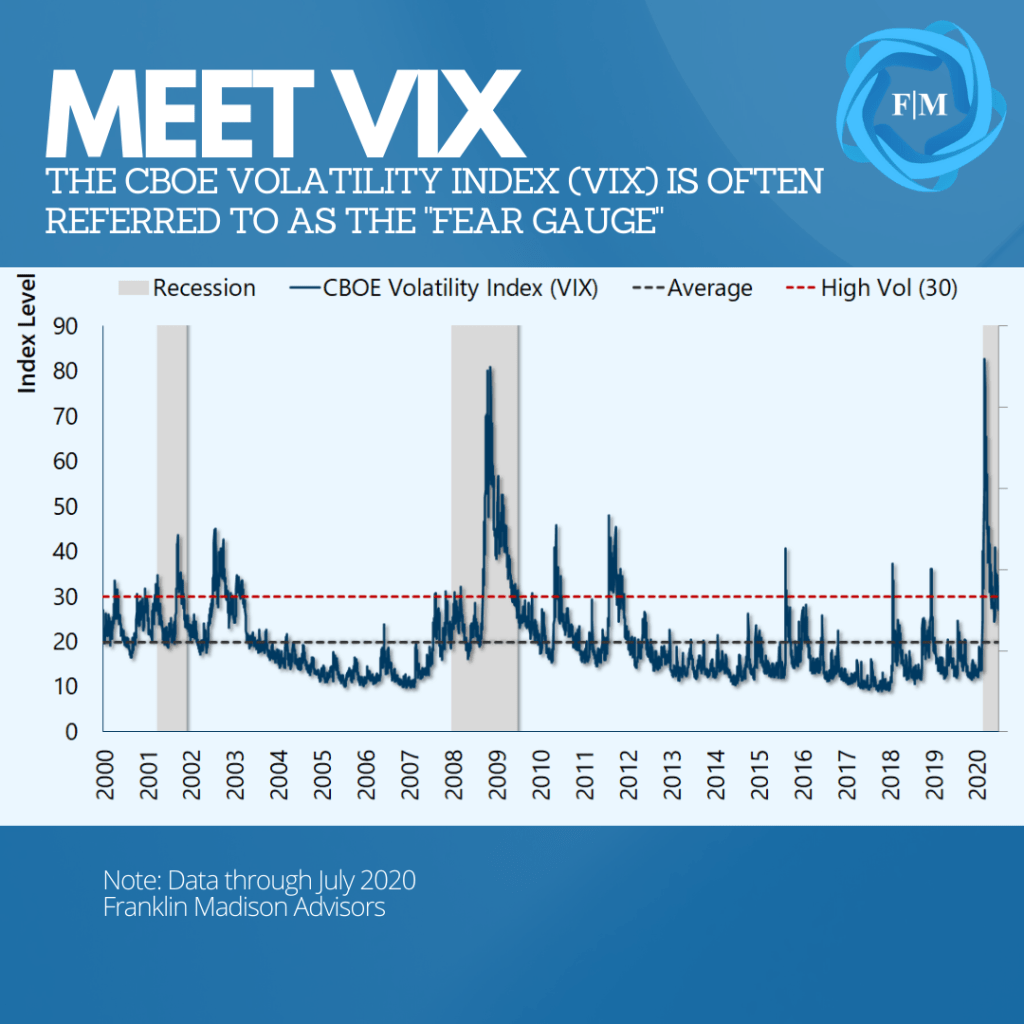

#2 Understand Volatility Trends

Another way to look at volatility is through market participants' expectations about the future. One widely tracked measure of such expectations is the VIX. The CBOE Volatility Index (VIX) uses a sophisticated method to express the future implied moves of the S&P 500 index. Often referred to as a "fear gauge," sudden moves higher in the VIX are often associated with periods of uncertainty and heightened market volatility.

Compared to the backward-looking statistical measure of volatility mentioned earlier, the VIX is forward-looking. It is also based on investor's directional expectations of the S&P 500 in the month ahead expressed through options market activity. A higher reading generally reflects greater pessimism about the expected direction of the markets.

Over the past two decades, the reading on the VIX has averaged a level of around 20. During the height of the Global Financial Crisis, VIX shot up to a level of 80 and, more recently, bested in February by the uncertainties related to the COVID19 pandemic. Historically speaking, a level below 20 has been consistent with favorable market conditions. A reading above 30 tends to occur during down moves in the market. Why is VIX important?

If you don't know where you are, then it becomes that much harder to figure out where you might be heading. From a volatility perspective, VIX offers a simple way to know how much uncertainty might be priced into the markets at a given time. This understanding is useful before making investment decisions, particularly when history has shown that higher levels of volatility are associated with the potential for lower returns.

Source: Broadview Macro Research

#3 Anticipate Changing Narratives

While financial markets are often viewed as a singular entity, the truth is that they are composed of thousands of assets, each with a host of participants. While algorithmic (computer-based) trading plays an increasingly essential role in the markets, the value of an asset is primarily driven by what human buyers and sellers think it's worth.

Investors are more inclined to bid up prices when they feel confident about the future. For example, when there is certainty about a company's earnings prospects, the policy environment, and the economy's health, asset prices tend to grind steadily higher, and volatility remains low. However, during times of uncertainty about these factors, investors are less willing to pay more for an asset, prices fall, and volatility rises.

One way to measure broad expectations about the economic and policy environment and its potential impact on earnings is by evaluating work compiled by researchers at Northwestern, Stanford, and the University of Chicago. Their Economic Policy Uncertainty Index brings together three components that track 1) news about the economy, 2) tax policy changes and 3) economic forecasts. Their research aims to provide a quantitative measure of what is often a qualitative event (feeling uncertain).

When comparing this measure against the VIX, the data confirm what we know intuitively from a historical perspective: market volatility tends to rise during times of heightened economic uncertainty. From an investment perspective, when uncertainty rises, market participants often change their expectations about the future. And it's during this time of shifting expectations when the price of an asset that may have otherwise seemed reasonable an hour, day or week ago comes into question.

Look for Changes in the Narrative

These periods of uncertainty are driven by a catalyst that often takes time to develop, and that's why measures like the Economic Policy Uncertainty index can help. We only have to look back to the events in February to see how this relationship between uncertainty and heightened volatility played out. Coming into 2020, concerns about a recession had been on the rise, yet many economists expected only softer overall US growth.

In February, however, this hopeful view on the economy changed as Chinese provinces were under lockdown amid a healthcare crisis while the US began reporting rising COVID19 infection rates. As large parts of the US went into lockdown, prospects rose of a deep economic downturn, fueling a volatility spike by late February and ushering in one of the sharpest market selloffs in history.

The point here is that market sentiment is regularly driven by a broad story that is often evident in many quantitative indicators. When factors that support the dominant narrative are challenged, market participants that had been prepared for one set of developments may suddenly change their market positioning to re-evaluate their investment thesis.

When the story changes, the market direction will likely go along with it. Being aware of the narrative driving market sentiment, potential inconsistencies in the story, and how individual market participants might respond can help you better anticipate periods of heightened market volatility.

#4 Know What You Own

Another vital point to understand about volatility is that not all financial assets behave the same way when volatility rises. During periods of heightened market volatility, assets with higher risk levels tend to see wider price swings.

To this point, it is generally understood that stocks are riskier than bonds. This is because equity holders often share in the benefits of company ownership, like stock price appreciation and earnings paid out in dividends. During times of financial distress, like a bankruptcy, however, bondholders are often first in line to be paid back while equity holders might lose a sizeable share of their investment.

Other factors, like the type of issuer (government vs. private sector), company size, market characteristics, and country of domicile, all affect an asset's risk characteristics. Taken together, the higher the likelihood that these factors might expose an investor to a loss, the higher an asset's level of expected risk.

When uncertainties rise and market volatility spikes, individuals holding riskier investments are likely to experience wide swings in asset prices. How do we know this? Well, take, for example, the March market selloff. During the first quarter, the S&P 500 experienced a historic price drop of 20%. At the same time, US government bonds rallied nearly 8% as market participants shed risk assets in preference for perceived safe havens.

The critical takeaway here is that higher-risk assets tend to underperform when uncertainties arise and volatility spikes. If you're anticipating higher market volatility levels, then it's vital to know what you own. Understanding your risk exposures may enable you to trim less favorable holdings and align your investments with your long-term goals ahead of a rise in market volatility.

Source: Broadview Macro Research

Improve Your Volatility Preparedness

We've addressed the various characteristics of volatility and its impact on the markets and investing. So, what can you do to help mitigate the effects of heightened market volatility in your investment portfolio?

Here are three suggestions:

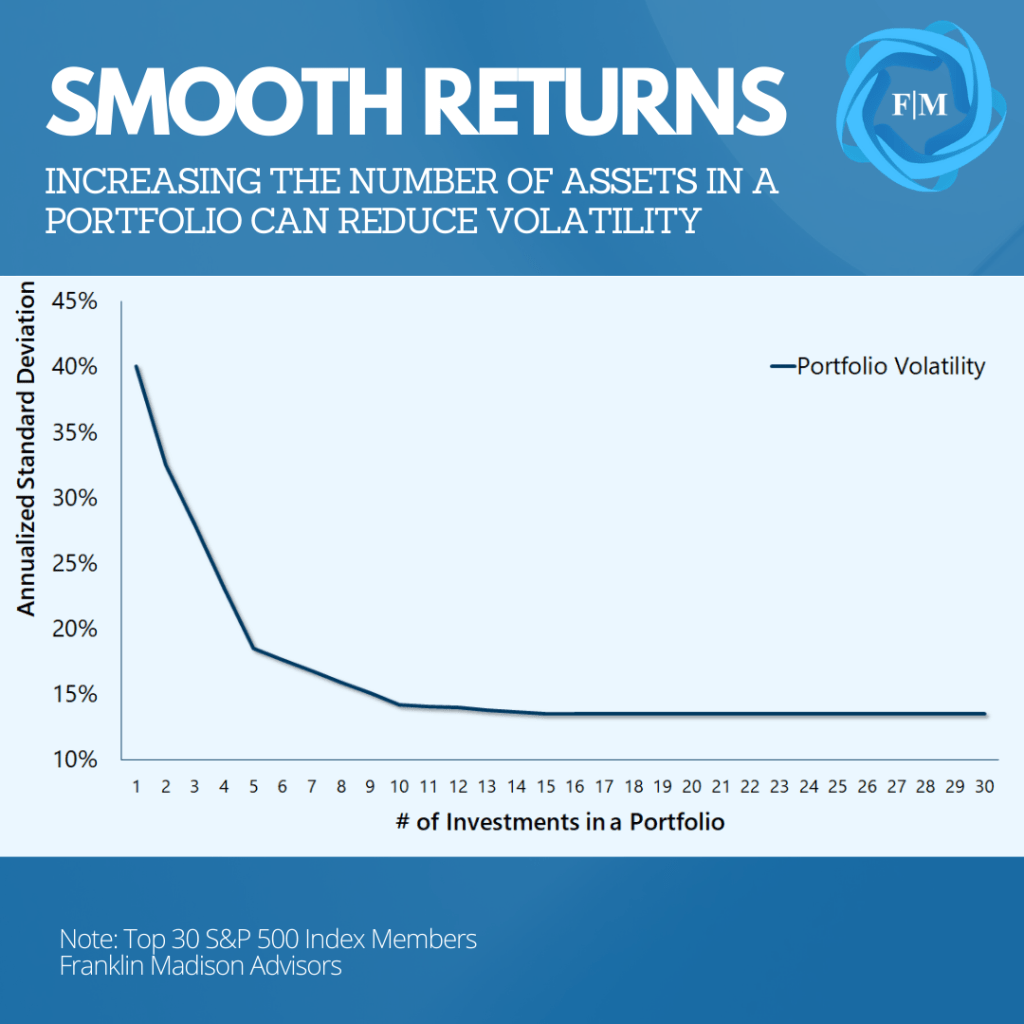

First, don't put your eggs in one basket. As we've written about recently, diversification is one crucial way to reduce portfolio volatility and smooth out investment returns for the long term. Studies have shown that increasing the number of securities held can reduce overall volatility in an investment portfolio. Therefore, if your goal is to invest for the long term, be sure to diversify your portfolio across various securities and asset classes to help reduce risk.

Second, build situational awareness. It's easy to get caught up in the market's daily price action or stay focused on a particular asset when your investments are doing well. Even so, markets are often driven by one or more underlying stories that can evolve. And it's at those turning points in market narratives where volatility tends to spike. That's why it's critical to stay informed about broadly relevant market topics so that you don't get caught unprepared when they change.

Finally, have a plan and act accordingly. Start with knowing what you own. Then, try to anticipate how those assets might perform during wild market swings and adjust your holdings accordingly. Heading into a period of heightened market volatility, it's also vital to have a higher level of cash on hand. Doing so accomplishes two ends. One, it reduces the likelihood that you'll need to sell an investment at an inopportune time to pay for necessary expenses. And two, it may allow you to have dry powder on hand for an opportunity to add discounted assets to your investment portfolio.

Volatility is a normal part of investing. It's the price you pay to earn an investment return. That's why what should be at the top of your list in terms of investing concerns is not volatility itself, but periods of heightened market volatility.

Whether you measure it using backward- or forward-looking means, the fact is that spikes in volatility are often drive by changing human expectations about the future and associated with lower investment returns. Being aware of the narratives driving the markets and having a plan in place before they change is central to investing success. The bottom line is that if you're unprepared for periods of heightened volatility, then you might be exposing your savings to unnecessary losses.

What’s the Best Way to Protect Your Hard-Earned Wealth?

What’s the best way to protect your hard-earned wealth? That’s the million-dollar question that’s on a lot of people’s minds right now. The fact is that the coronavirus has demonstrated in absolute terms how an unexpected event can quickly take away your earnings ability and deplete your life savings.

Events surrounding the coronavirus have also demonstrated how life’s surprises can come at you from all directions. And when they do, your ability to build enduring wealth can evaporate in the blink of an eye. So how can you protect your hard-earned wealth today?

Figure 1: Our Risk Management Process

Source: Broadview Macro Research

Well, we believe that one way to prepare for life’s unexpected events is to incorporate a disciplined risk management process into your wealth management framework. This involves identifying outstanding risks, using tools to mitigate these threats and monitor for evolving challenges to your wealth.

Risks to Creating, Growing and Preserving Enduring Wealth

Before we dive into our discussion on the methods you can use to protect your wealth. Let’s take a closer look at some of the ways that risks may come your way.

Risk – a situation involving exposure or danger

The word “risk” can mean many things to many people, so we’ll frame our discussion on the topic within the context of our wealth management framework. As you’ll recall from our previous reports, the wealth management framework focuses on the actions you need to take today to build enduring wealth over time.

Figure 2: Our Wealth Management Framework

Source: Broadview Macro Research

This includes: 1) being intentional and efficient with your time and resources, 2) making your money work for you and 3) the topic of today’s discussion: taking steps necessary to protect your hard-earned money from both expected and unexpected events.

Indeed, the wealth management framework is just one tool you can use to build wealth. But the reason we believe that it's important is that it’s a disciplined process that can help you create, grow, and preserve financial wealth for the long-term.

Being Risk Aware: Creating Wealth

The aim of our wealth creation process centers on steps necessary to generate a productive source of financial savings. These actions include being intentional with your money, maximizing your value to others and optimizing your net worth.

Your goals during this time should be to hone your innate talents and abilities and leverage a systematic, disciplined process to build a solid financial base. Now, what would you do if your ability to create wealth became impaired? For some people, COVID-19 has done just that.

Many of us spend a lot of time thinking about various ways we can get ahead and produce results. And often we do this without really giving much thought to what could derail our efforts or take us out of the game completely.

As of this today's publishing date, Coronavirus infections continue to rise across the US. And there’s no doubt that the outbreak has impacted many lives in many different ways. The current events also illustrate the kind of risk awareness you must have if your goal is to produce enduring wealth during the creation process.

Figure 3: U.S. Unemployment Rises to a Post-War Record

Source: Broadview Macro Research

More specifically at this stage, your awareness should focus on identifying risks that can impede your ability to earn an income and address hazards that can impair the value of assets you use to grow wealth. So, what are some of these risks?

Well, we’re talking about events that could lead to short term or long-term disability, property damage, lawsuits, and in some cases, death. We’ll talk about measures you can take to protect yourself against such events in just a moment. But the point here is that you need to develop an awareness of the risks that could derail your ability to create wealth before they even happen.

Being Risk Aware: Growing Wealth

Sustaining your disciplined wealth creation habits and then using 1) your base of savings, 2) a rate of return, and 3) some time to make your money work for you are the goals of the growing wealth process.

The obvious risks to growing wealth are financial market volatility and other losses related to investing. With that said, there more insidious threats working against you as you’re growing your wealth.

These are menaces waiting to separate you from your hard-earned money – one basis point at a time. These factors include excess fees eating into your investment rate of return and the IRS taking a bigger bite of your earnings. So, what exactly do we mean here?

Figure 4: Excess Fees Can Reduce Potential Long-term Returns

Source: Broadview Macro Research

Well, here are a couple of examples. First, let’s think about fees charged on investment products for a moment. Did you know that a one-percent investment management fee difference can lead to more than $400,000 in wealth forgone on a million dollars invested over 20 years?

What about taxes? As it relates to investing, you could have income on the same two savings vehicles taxed at many different rates simply based on the structure of one savings vehicle versus another.

The takeaway here is that if you’re not careful with how you put your money to work, you may be growing your money, but at a much slower rate than you otherwise could during your growth phase.

Being Risk Aware: Preserving Wealth

Seeing through important life goals like retirement or even leaving behind a legacy is the aim of the wealth preservation process. During this time, you’ll need to ensure that the money that you’ve spent time accumulating and growing is still around to pay for your important life goals years from now.

And not only that, but that there’s enough left over to pass along to people or charities closest to your heart if that’s important to you. The risk here is that there won’t be enough money to meet your retirement needs or the needs of your loved ones.

This can occur, for example, when financial markets experience a sharp sell-off just as you’re preparing to enter retirement. There's no question, this year’s financial market volatility has acutely illustrated how a sudden and deep pullback in the markets can derail even the best-laid retirement plans.

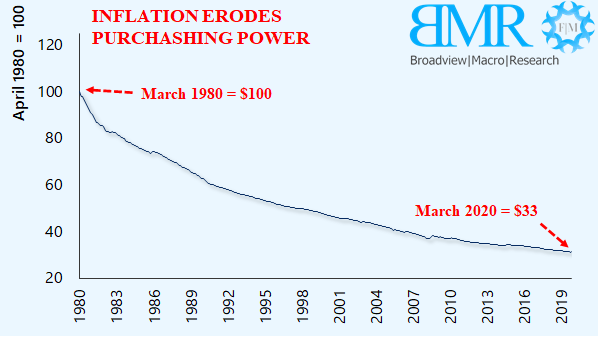

Figure 5: Inflation Erodes Purchasing Power

Source: Broadview Macro Research

Another risk to wealth longevity is having your purchasing power reduced over time by inflation. For example, did you know that when inflation is running at around 2% per year, it takes about 36 years to cut your purchasing power in half?

Or put differently, a million dollars today may only buy half that amount of today’s goods or services in less than two generations when inflation is present. Taken together, the important point here is that at each phase of the wealth management process there are risks that could prevent you from building enduring wealth.

Protect Your Wealth Today

So, what steps can you take to protect your hard-earned wealth today? Well, one way to prepare for life’s unexpected events is to incorporate a disciplined risk management process into your wealth management framework. Let’s take a look at some examples of how this risk management process applies as we create, grow, and preserve financial wealth.

Risk Management: Creating Wealth

Events that hamper your ability to use your innate talents to produce income and generate savings are key risks during the wealth creation process. One way to protect your wealth during this time is to utilize insurance as a tool to protect against financial loss.

The key to preserving your wealth during this time is ensuring you have the right amount of insurance coverage to meet every one of your financial needs. For example, COVID-19 has reminded us all of our mortality. At the same time, it has served as an important reminder that life insurance can be a useful way to create financial wealth.

This is especially true if you experience unexpected tragedy in your own life before you’ve had a chance to build the kind of wealth that will leave your loved ones protected. In a similar vein, now’s also the time to take a look at your disability coverage. More specifically, you should consider whether the limits on your disability insurance policy are sufficient to cover your living expenses should you become injured and can no longer work.

The point here is that if your goal is to build enduring wealth, you will need a method to defray some of the risks if life’s curveballs threaten to take you out of the game. In our case, insurance provides a way to defray some unknown risks and immediately creates a financial source of wealth in case of an unexpected tragedy.

Risk Management: Growing Wealth

Fees and taxes are factors that can hinder your ability to quickly build enduring wealth during the growing wealth process. Your goal during the growth process should be to maximize your risk-to-reward ratio. And one way to do this is to reduce unnecessary investment fees.

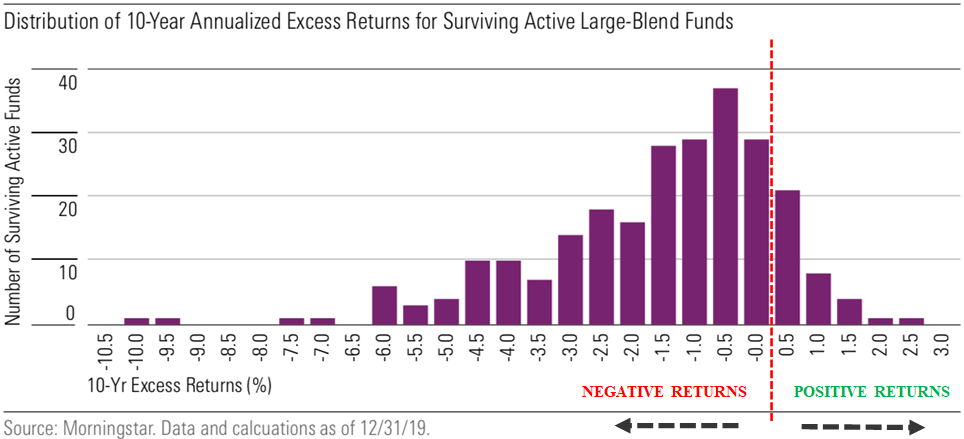

Figure 6: Active Management Has Largely Underperformed

For instance, actively managed investment funds tend to charge a premium when compared to passive funds. Therefore, now’s a good time to look at the performance of these funds and consider whether what you're paying for active management is worth the premium. This is notably important at a time when active managers in some cases have underperformed their passive benchmarks.

Addressing unnecessary taxes is another way to cut your losses during the growing wealth process. This is especially true if your investments produce income and you’re not yet retired.

For example, you can minimize the taxes that you pay by making sure that income producing investments are held in tax deferred vehicle like a 401k or IRA rather than a brokerage account which is taxable.

Risk Management: Preserving Wealth

If you are planning on taking distributions from your retirement within the next year or expect to leave a legacy, protecting wealth at this phase is important now more than ever. You’ve put in the hard work to grow your money, so now’s a critical time to protect it as you move from accumulating wealth to distributing wealth.

We mentioned earlier how a sudden drop in markets can derail even the best-laid retirement plans. That’s why you’ll want to have a distribution strategy in place that addresses how retirement assets will be liquidated during periods of heightened market volatility.

For example, giving more distribution weight to an asset that is less sensitive to sharp moves in the markets and ensuring you have an adequate level of cash on hand to weather volatility is one way to prepare for such times. When it comes to leaving a lasting legacy, having a solid estate plan is where it all starts.

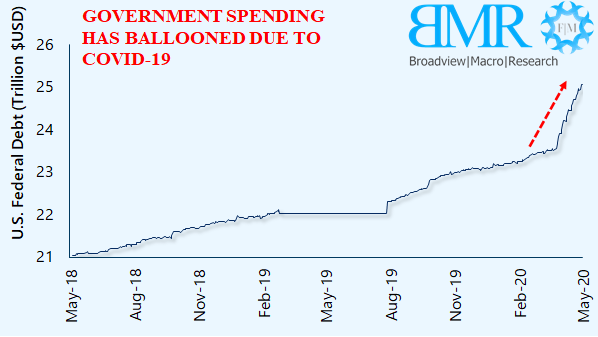

Figure 7: Federal Debt Has Ballooned Due to COVID-19

Also, you’ll want to make sure that your long-term investment management process reflects the realities of inflation. Remember, purchasing power can be cut in half in less than two generations when inflation is running at around 2% per year.

With government debt issuance ballooning by $3 trillion and Federal Reserve assets growing at an exponential rate, you’ll want to make sure that how your legacy assets are managed align with today's inflation expectations. This is important because doing so will help ensure that your wealth can adequately serve generations now and into the future.

Protecting Wealth Begins with a Process

The coronavirus certainly has exposed our varying levels of financial risk preparedness. Even so, we believe that you can take some especially important take steps right now to protect your wealth, starting with being risk-aware.

This means identifying the kinds of threats that may crop up at various life phases and then preparing for those threats as part of a disciplined risk management process. There's no doubt that when it comes to building enduring wealth it’s important to think about the steps you need to take today to create and grow your money over the long term.

However, another important step is taking the time to protect yourself against the threats that are waiting to separate you from your hard-earned wealth. Some of these steps include utilizing tools like insurance, tax and cost-efficient investing vehicles, and a solid investment, estate, and distribution plan to protect your money.

Finally, be sure to manage risks for the long term. This involves continuously evaluating the current economic and market environment to identify evolving threats to your wealth. Then use some of the tools that we’ve discussed to help mitigate those risks.

We believe that incorporating an active risk management process into your wealth management framework could ensure that your wealth endures for the long-term no matter what surprises life throws your way.

Why the coronavirus is relevant to your finances

It’s getting harder and harder to ignore the potential financial fallout from the novel coronavirus (nCoV-2019) outbreak underway. Some of this fallout was evidenced in the global stock selloff on Friday and futures (as of this writing) point to a weaker start at Monday’s open. Indeed, the concerns surrounding the ongoing spread of nCoV is likely to weigh on market sentiment for weeks. But why is nCoV relevant from a financial perspective?

Well, in our opinion, the quickening spread of the coronavirus illustrates how fast unexpected events can alter near term economic assumptions and upend best laid financial plans, notably at a time when the U.S. economy is primed for a recession. Amidst the potential for outbreak-related market and economic volatility, we provide a few recommendations that households can use to increase their financial preparedness as Wall Street and Main Street worries potentially intensify in the weeks ahead.

It’s going to get worse before it gets better

Coming into the year we expected several key events (like geopolitics, central bank policies and elections) to raise uncertainties and simply make getting ahead in life financially harder for some households in 2020. In last week’s post, we wrote about one strategy investors can use to increase portfolio returns as economic growth falls and market volatility picks up.

We’ll talk about some additional financial strategies that can be used to help mitigate uncertainties later, but before we do that we need to highlight two key reasons why we think the coronavirus is important to consider from a financial perspective.

First, reports on the spread of nCoV and the subsequent global response suggest that the outbreak is likely to get worse before it gets better. While Beijing has stepped up its efforts to quarantine suspected infected zones, other governments, like Russia and Singapore have sealed their borders with China while countries like the U.S. have put up their own restrictions on travel to-and-from China amidst the outbreak.

This comes as the World Health Organization (WHO) declared a “public health emergency of international concern” last week. To be sure, the rapid spread of nCoV compared to other coronaviruses like SARS suggests that the current outbreak has the potential to only get worse before it gets better. Barring a rapid de-escalation of current events, what this likely means is that discretionary international travel is poised to slow in the coming weeks not just into and out of China, but potentially among countries that are seeing infections rise and more importantly as deaths outside of China begin to increase in number as well. This brings us to our second point.

Figure 1: U.S. recession risks are elevated in 2020

U.S. economy primed for a slowdown

The restriction on travel and closing of borders could very well aggravate a downturn in a U.S. economy already primed to slow this year. As we’ve written about in past posts, we believe that the risks related to a U.S. recession remains elevated this year as business spending and hiring activity declines. And while discretionary household spending supported the U.S. economy in 2019, last week’s fourth quarter GDP print remained soft even as the Fed primed its quantitative easing pump during the last three months of the year.

And from this perspective, we expect corporate earnings growth to remain subdued in 2020, challenging already stretched financial valuations. In other words, risky assets have broadly had a strong run in recent months, but now appear expensive on historical basis. And this fact increases the chances that already expensive risky assets could come under increased selling pressure as some sudden shock causes the recent bullish euphoria in the markets to fade. Today, the economic implications of nCoV are only likely to complicate the current market backdrop.

Assuming the uncertainty surrounding nCoV is not reversed quickly, there is a potential that growth in the world’s second largest economy (China) could slow to a rate below current year estimates, contributing to broadly weaker global growth in 2020. This could happen if a further spread of the nCoV outbreak expands quarantine zones and halts economic activity across Chinese provinces as the movement of people and goods grinds to a halt.

What’s more, demand for goods and services globally are likely to fall as people stay home and consume less, impacting exports of goods and services in affected regions and slowing commerce between China and its key trade partners. For the U.S., such uncertainties are likely to only galvanize the willingness of business leaders to postpone discretionary hiring and spending this year. While it is still too soon to tell how the U.S. economy would be affected, the risks related to a U.S. recession are likely to increase in a scenario where global trade declines, business hiring and spending falls and consumers stay home. This leads us to our point about financial preparation.

Coronavirus: how to prepare financially

Without being overly alarmist, we believe that it is important for households to use current events surrounding the novel coronavirus as a reason to take a few steps to ensure financial preparedness as economic and market volatility rise in the coming weeks. This is important because as the economy slows, plentiful jobs may become harder to find when unemployment rises and the ability to borrow money becomes harder as banks tighten lending conditions. So, what steps can households take to increase their financial preparedness?

First, we recommend households look for ways to increase net cash flows. This includes reducing discretionary (or non-essential) spending and finding ways to advantageously use today’s low interest rate environment to refinance high-cost debts. We also suggest maxing out employer-matching retirement savings contributions, putting off big-ticket spending and using excess cash flows to build up emergency savings. We believe that these steps can better prepare households for unexpected life events, particularly as labor market conditions show signs of weakening in the coming months.

Figure 2: Strategies to help financially prepare for the unexpected

Second, for investors oriented towards asset growth, we recommend trimming exposure to higher-beta, lower quality investments and broadly ensuring that aggregate portfolio holdings across all investment accounts reflect long-term goals. While volatility exposes risks in the markets, it is also likely to present opportunities. And this is one reason why we believe that investors should rebalance portfolios, not only to align allocations with long-term goals, but also to generate cash that can be deployed opportunistically as market volatility creates favorable buying prospects.

Finally, for households preparing to take distributions from their investment, we recommend rebalancing accounts to long-term investment objectives and reduce unnecessary risk taking. As we pointed out last week, we investors can increase overall returns (without increasing risks) by trimming unnecessary expenses in their portfolios. Further, we recommend ensuring that cash positions are adequate to meet 6-12 months of living expenses. This is intended to avoid forced selling at depressed prices when market volatility increases.

Economic update: Downside risks still increasing

The outlook for the U.S. and global economy has deteriorated yet again. Unsurprisingly, the culprit behind the outlook downgrade has been news of the coronavirus’ continued spread. To be sure, risk assets sold off this week and financial market volatility increased as concerns about the virus and its potential impact on the global economy dented investors’ up-until-recent euphoric sentiment.

More importantly, worries about the coronavirus come at a time when economic conditions in the U.S. and around the world remain weak and susceptible to unforeseen shocks. Our view remains that the coronavirus outbreak is likely to have a material impact on the global economy and financial markets assuming its spread is not quickly stemmed. Therefore, we believe that households and investors should prepare for economic and market weakness in the coming months, notably as the effects of the coronavirus remain wildly uncertain.

Data pointing to further 2020 weakness

Each month we evaluate a host of quantitative and qualitative factors that help guide our U.S. and global economic and market outlook. Indeed, we utilize econometric models that rely on developments in the labor market, consumer spending, business and household sentiment and rates, among others, to help frame our U.S and global economic views. The result of this work includes forecasts on U.S. gross domestic product (GDP) growth, inflation and employment conditions as well as a view on major currencies and commodities. So, what does our latest work show?

Well, the latest update to our models for February suggests that economic growth in the U.S. is likely to deteriorate further relative to our view in January. More specifically, our quantitative models show that household spending growth is likely to lag behind 2019 even before accounting for the effects of the coronavirus. At the same time, our models suggest that business investment could slow further as global manufacturing remains weak, while a rebound in the U.S. housing market largely supports positive U.S. private investment activity.

Looking abroad, various data releases over the past few weeks have pointed to potentially stabilizing global economic growth. To be sure, the latest reading of the Organization for Economic Cooperation’s and Development (OECD) Composite Leading Indicators (CLIs) are consistent with a potential growth rebound in both developed and emerging market economies. And this improving trend has been supported, in part, by some better than mixed global business sentiment and a broad rally in risk assets, especially U.S. stocks, from the start of the year.

Figure 1: Downward revision to 2020 growth outlook

Coronavirus uncertainties intensify

Taken by itself, the data would lead us to believe that the growth outlook for the U.S. and global economy, while sluggish today, could pick up into the tail end of 2020. This is because broad money printing by the world’s key central banks and a still resilient consumer have underpinned spending activity.

Nevertheless, as we look into the future, we believe that the hard data will begin to reflect renewed weakness in the global economy as coronavirus concerns take hold. And, as they do, this will challenge corporate earnings growth and subsequently the stock market’s ability to charge to new weekly highs.

To be sure, this view was reflected in one of our past writings and comes as the coronavirus is poised to change the way firms do business and the way households spend. For example, just a few weeks ago, as far as market participants were concerned, the coronavirus was largely a China issue as headlines centered on developments in Wuhan.

Today however, virus headlines have taken a dourer tone as cities in Italy deal with quickly growing number of infections and more reports reflect the spread of the coronavirus across the European continent. Adding insult to injury, even leaders from the Centers for Disease Control (CDC) report a heightened risk for a widespread coronavirus outbreak in the U.S. And what does all this mean for the economy and markets?

Figure 2: Pre-coronavirus tentative signs of global economic stabilization

Unforeseen disruptions

We expect discretionary spending among households in the U.S. and abroad to decline should cases of the coronavirus continue to increase globally. This consumption slowdown is likely to come from not only mandatory quarantines, but also from voluntary confinements reflecting a desire among the general public to avoid places where the virus could potentially spread.

This is important because, while eCommerce has increased notably in recent years, spending at brick and mortar stores still accounts for a large portion of retail sales in the U.S. and many developed and developing economies. And, with household spending being a key component of GDP growth, a slowdown in spending could put renewed downward pressure on the overall global economy and hence earnings growth.

Another impact stemming from the coronavirus spread is that of supply chain disruptions. China remains a key supplier of manufactured goods and is integrated into global supply chains that span not just the Asia Pacific region, but also across Europe, the U.S. and other parts of the world. This is important because it only takes the loss of just one critical component to halt the entire production of a key good. Today, some governments are exploring ways to get around such supply chain disruptions, but the fact is that China remains a key global supplier of critical manufacturing components. How do these developments affect our forecasts for the year?

The prospect of a widespread coronavirus outbreak in the U.S. is likely to notably alter of our current estimates of economic growth. That is, assuming a quick resolution to the viral outbreak is not found and coronavirus concerns intensify, economic growth in the U.S. and globally are likely to move from a moderate slowing in 2020 to sharp slowdown with yet to be determined consequences. How bad could it get?

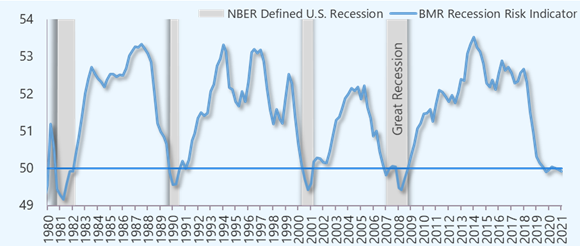

At this point the severity of the slowdown will largely depend on the adaptability of businesses and resilience of consumers to deal with host of uncertainties amidst the threat of a global outbreak. With that said, the virus comes at a time when our quantitative recession risk indicator is pointing to a rising likelihood of an economic downturn in the second half of 2020. What this means is that a sharp decline in business and household spending as a result of the coronavirus could be enough to tip the U.S. and global economy into a recession sooner rather than later.

Figure 3: U.S. recession risk indicator reflects rising likelihood of a 2020 downturn

Preparing for the unexpected

What are households and investors to do in an environment that is charged for more market and economic volatility in the weeks and months ahead? The fact that risk asset prices remain elevated even amidst the coronavirus headlines has given us reason for pause. As we’ve noted in prior reports, we believe that the current rally in risk assets has more to do with the Fed’s unsustainable easy money policies rather than solid economic fundamentals. And this could set the stage for more market pullbacks this year.

While central bank asset purchases have been supportive of lower borrowing rates and a boost to housing market sentiment, we are hard pressed to find positive catalysts that would support a sharp economic rebound this year, particularly as coronavirus risks have yet to be contained and hence challenge the feasibility of a sustained rally in financial markets.

With the economic outlook set to weaken in 2020 and financial market volatility likely to remain elevated, we recommend that households take some constructive steps to prepare for the unexpected. For instance, one way to increase financial preparedness and resilience in a time of uncertainty is to reevaluate big-ticket spending decisions and divert more cash flows toward emergency savings.

This can be accomplished by reducing non-essential spending and refinancing high interest debts in today’s low interest rate environment. We believe that these steps will better prepare households for unexpected life events, particularly as job opportunities have become less plentiful and labor market conditions show signs of continued weakening into the months ahead.

For investors oriented towards asset growth, we recommend maintaining a diversified exposure in investment portfolios. This means not chasing hot stocks or trying to time a market bottom. At the same time, we recommend reevaluating exposure to risky investments to ensure that aggregate portfolio holdings across all investment accounts are in line with long-term goals. This includes rebalancing to target allocations and trimming winning positions to raise cash to keep as dry powder for when market volatility creates favorable buying opportunities.

Finally, for households taking distributions from investment, we recommend rebalancing accounts to long-term investment objectives and reduce unnecessary risk taking. Further, we recommend ensuring that cash positions are adequate to meet 6-12 months of living expenses. This is intended to avoid forced selling at depressed prices, especially as economic and market uncertainties are likely to rise in the coming weeks and months most notably as the overall impacts of the coronavirus remain wildly uncertain.