A Roth Conversion Is Not the Goal

There's a quiet enthusiasm building around Roth conversions.

You hear about them at the water cooler. You read about them in the financial press. A friend mentions what their advisor recommended over lunch.

The pitch makes sense on the surface.

Pay tax now while rates are favorable. Move money into a Roth account. Watch it grow tax-free for the rest of your life. Pass what's left to your children without the IRS taking another bite.

It's a compelling idea.

It can also be a costly one.

Here's what the headlines rarely mention. A Roth conversion is helpful, right up until it isn't. The same move that saves one retiree thousands can cost another retiree even more.

The difference isn't the strategy.

The difference is the size.

The Goldilocks Problem

Roth conversions create a Goldilocks problem.

Convert too little, and you may leave a real opportunity on the table.

Convert too much, and you may trigger consequences that show up on this year's tax return, or, in the case of Medicare premiums, a year or two later.

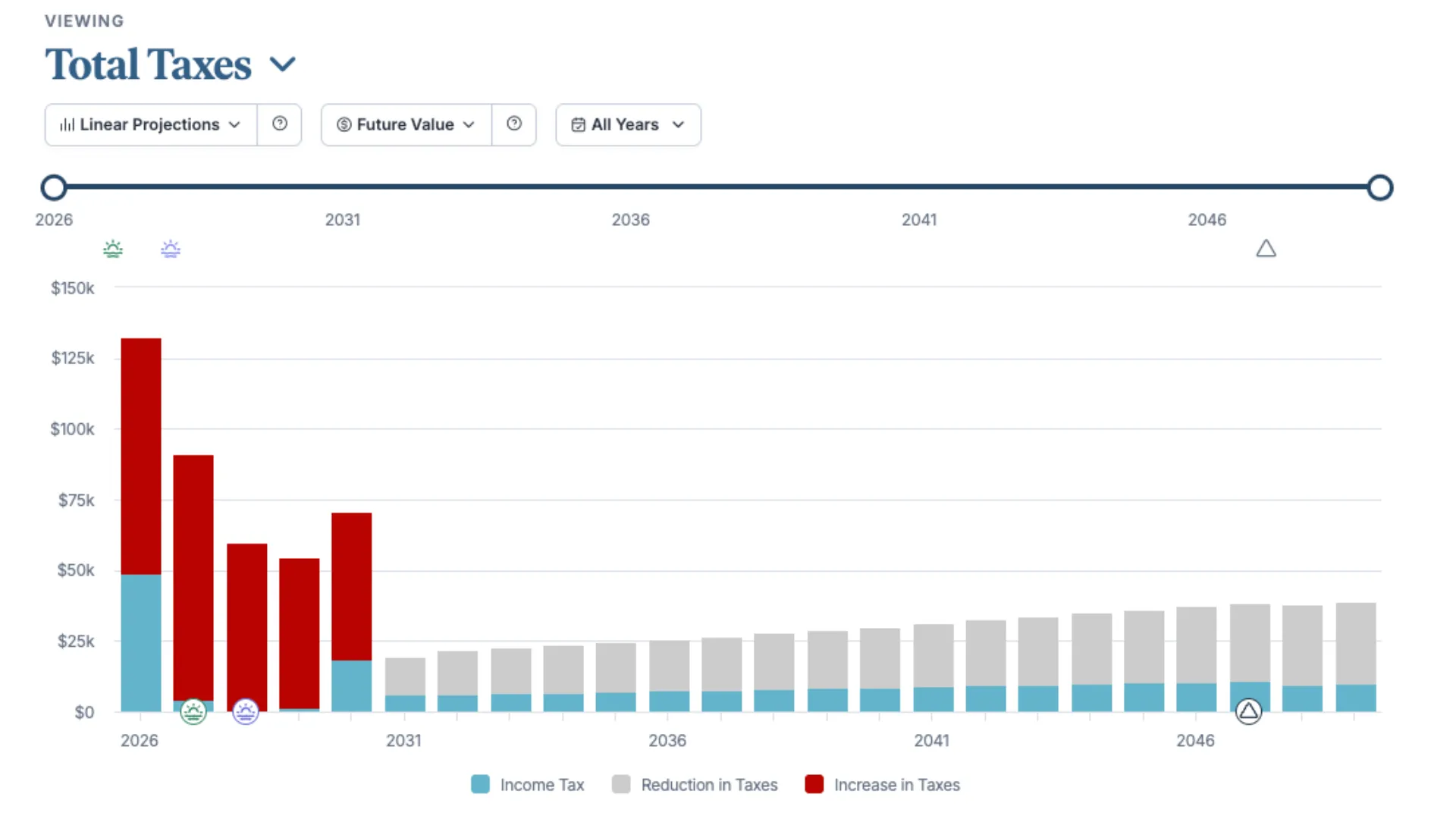

Consider two retirees in similar situations.

Both are sixty-seven. Both have around two million dollars in pre-tax IRAs. Both want to soften the impact of future required minimum distributions and leave a more flexible legacy for their family.

The first retiree maps out the next ten years. She runs the numbers. She converts roughly eighty thousand dollars each year, using the lower tax brackets available to her without pushing too much income into higher-cost territory.

By the time her required distributions begin, her pre-tax IRA is meaningfully smaller. Her future tax bill is smaller too. She feels lighter.

The second retiree hears the same advice in broad strokes and decides bigger is better. He converts three hundred thousand dollars in a single year.

The conversion itself is taxed at higher rates. His Medicare premiums may jump in a future year because Medicare looks back at prior income when calculating IRMAA surcharges. If he's already claimed Social Security, more of those benefits may become taxable. A modest stock sale may be taxed at a higher capital gains rate. His state income tax may rise too.

None of those costs were on the brochure.

Same strategy. Different outcomes.

The strategy wasn't the problem.

The size was.

Why Rules of Thumb Don't Work Here

You may have heard rules like, "Convert while tax rates are low," or, "Fill up the lower tax brackets before required minimum distributions begin."

Those rules sound clean.

They're also incomplete.

A proper Roth conversion analysis looks at far more than your marginal tax bracket. It considers your Medicare premium thresholds. Your Social Security taxation. Your state tax exposure. Your capital gains tier. The shape of your future required distributions. The expected tax bracket of your heirs. Your charitable intentions. The order in which you plan to draw from different accounts in retirement.

Each of those factors moves the right answer.

Sometimes by a little.

Sometimes by a lot.

That's why the question is never simply, "Should I convert?"

The question is always, "How much, and over how many years, makes sense for the life I'm actually living?"

The Move and the Math

The Roth conversion is the move.

The math is what makes the move work.

A well-sized conversion plan isn't a one-time decision. It's a multi-year roadmap. It treats the years between retirement and required distributions as a window of opportunity, then fills that window thoughtfully, year by year, bracket by bracket, with awareness of every secondary cost that could be triggered along the way.

That's not the kind of analysis you do in your head.

It's not the kind of analysis a generic online calculator can do.

And it's rarely the kind of analysis built into the tax preparation conversation, where the focus is reporting last year, not designing the next ten.

That's the difference between tax preparation and tax planning.

One reports what happened.

The other helps decide what should happen next.

It takes time, the right tools, and someone who understands how every line of your financial life connects to every other line.

Bottom Line

If you've been wondering whether a Roth conversion belongs in your plan, that's a fair question to be asking.

The instinct is a good one.

Just don't stop at the instinct.

Before you convert anything, run the full picture. Map the next ten years of income. Stress test the secondary costs. Look at what happens to Medicare, Social Security, capital gains, and state taxes when you change one number on your return.

Then, and only then, decide what to do.

A Roth conversion isn't the goal.

Clarity is.

Confidence is.

Peace of mind is.

The conversion is just one of the tools we use to get there.

If you'd like a full evaluation of whether a Roth conversion belongs in your plan, when to do it, and how much is too much, that's a conversation worth having while there's still time on the calendar to act on it.

Post-Filing Tax Hygiene: Three Things to Do With the Return You Just Filed

There's a category of financial work I think of as tax hygiene.

It isn't the headline-grabbing stuff. It's the small, recurring habits that quietly determine whether your tax life feels under control or chronically off-kilter. Most of the trouble I see with clients doesn't come from missing some clever strategy. It comes from a withholding number that drifted out of date, an estimated payment that slipped past a deadline, or a return that got signed and filed away without anyone asking what it was actually saying.

That last point is where I want to start.

Once your 2025 return is filed, you have something useful in hand: a year's worth of financial data, organized and reconciled. Most people treat the finished return as a chore that's finally over. I'd encourage you to treat it as information. It can tell you a fair amount about what to adjust for the year ahead, and three areas in particular are worth a look.

Review the Return Before You File It Away

Before the return goes into your records, spend twenty minutes with it.

Look at the bottom line first. A meaningful balance due usually means your withholding or estimated payments weren't keeping pace with your actual income. If that goes uncorrected, it can compound into underpayment penalties. A meaningful refund isn't a crisis, but it does mean you lent money to the federal government interest-free for a year.

Either result is worth understanding before you move on.

Then look at what's on the return itself. Sometimes a capital gain shows up that you'd forgotten about, or a side project generated more income than you realized, or a deduction you'd planned around didn't materialize the way you expected. These are the items that often hint at planning opportunities, or planning gaps, for the year ahead. They're easier to act on now than to reconstruct next March.

Finally, take stock of any carryforwards. Capital losses, charitable contributions over your AGI limit, passive activity losses, and foreign tax credits can all carry into future years, but they don't manage themselves. Knowing what's available to you is the first step in using it well.

The return is the most accurate picture you'll have of your financial year. It's worth using.

Recalibrating Your Withholding

Withholding is one of those settings most people configure once and forget.

Life moves on. You change jobs, retire, start Social Security, begin drawing from an IRA, get married, sell a property, or pick up a side venture. Each of those events can quietly knock your withholding out of alignment with your actual tax bill. If your 2025 return showed a meaningful balance due or refund, recalibration is what fixes it.

The IRS publishes a withholding estimator on its website that walks you through your income sources, credits, and deductions, and gives you a target for what your withholding should look like. It takes about twenty minutes if you have a recent pay stub and your 2025 return handy, which conveniently you do.

If the numbers are off, the fix is usually just a fresh form. Employees submit a new W-4 to their employer. People receiving pension or annuity payments use Form W-4P. IRA owners use Form W-4R. And if you'd like more federal tax pulled from your Social Security check, Form W-4V handles that.

The best time to do this is in the weeks right after filing, while the numbers are fresh and the relevant documents are already on your desk.

Tuning Your Estimated Tax Payments

Withholding solves the problem when tax can be pulled directly from a paycheck, pension, IRA distribution, or Social Security benefit. Estimated payments solve the problem when income arrives without withholding attached.

If you have income from self-employment, investments, partnership distributions, rental properties, or retirement income where withholding hasn't been elected, the IRS generally expects quarterly estimated payments. The 2026 installments are due April 15, June 15, September 15, and January 15, 2027. Taxpayers in federally declared disaster areas may have additional time, but absent that, the dates are firm.

Your 2025 return is the natural starting point for sizing these payments. If your non-withholding income was steady, last year's numbers are a reasonable baseline. If something changed materially, whether a business grew, a portfolio started throwing off more income, or a property was sold or acquired, the baseline needs adjusting before you set the year's payment schedule.

The mechanics of paying have quietly modernized. If you have an IRS online account, you can pay through it directly. IRS Direct Pay and the Treasury's Electronic Federal Tax Payment System both work well. The IRS also has a phone app, and the agency accepts credit card payments with a processing fee that's worth weighing against any rewards you'd earn.

Paper checks may still be available, but electronic payments are increasingly the cleaner and more reliable option. If you're a check-by-mail holdout, this is a good year to switch to electronic payments. The transition is genuinely painless once you set it up.

The June 15 deadline is the one that catches people, since it arrives only two months after April. Putting all four dates on your calendar now is one of the cheaper investments you can make in your own peace of mind.

The Big Takeaway

None of this is glamorous.

But the discipline of reading your return as information, recalibrating withholding while the data is fresh, and setting estimated payments with intention is the foundation everything else sits on.

Our work with clients begins here, with the maintenance items that don't generate excitement but quietly add up to clarity, confidence, and fewer surprises next April. If you'd like a second set of eyes on what your 2025 return is telling you, we're glad to help.

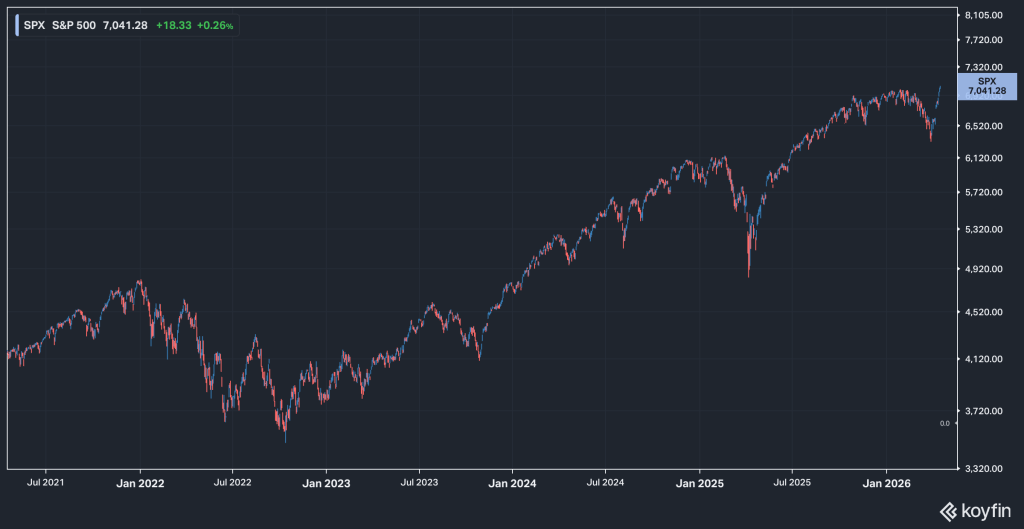

Weekly Market Update: Rally Slows as Geopolitics Take Center Stage

Markets moved higher for a fourth consecutive week, with the S&P 500 and Nasdaq both closing at fresh all-time highs for the second week in a row.

The pace of the rally slowed, however, and the gains were uneven beneath the surface. Small cap stocks outperformed both major indexes, while international stocks traded lower as oil prices rebounded and the U.S. dollar strengthened.

Value stocks modestly outperformed growth stocks, and despite the S&P 500’s new high, 5 of 11 sectors traded lower, with defensive sectors lagging the rally.

Bonds ended the week with modest gains despite yields drifting higher, with Treasury and corporate bonds producing similar returns. Oil prices rose after two consecutive weeks of declines, and a measure of market volatility ticked up as investors responded to geopolitical developments during the week.

Key Takeaways

Week Defined by Geopolitical Whipsaw in Middle East

The week was defined by geopolitical whipsaw as U.S.-Iran tensions swung between diplomatic progress and physical deterioration. The headline was constructive: Trump extended the ceasefire indefinitely.

However, the U.S. naval blockade of Iranian ports remained in place, scheduled peace talks were canceled, and questions emerged about a potential Iranian leadership change.

Why it matters: The diplomatic path forward remains open, but the physical confrontation has not been resolved, and the disruption to oil supply has not been removed. Both factors could continue to impact financial markets.

Oil Prices Rise as Naval Blockade Remains in Place

Crude oil surged more than +5% on the week, erasing a portion of the prior two weeks' decline, and Brent crude, the international benchmark, rose back above $100. The move was driven entirely by geopolitical developments, and the ceasefire extension did little to lower oil prices.

On the economic side, March retail sales showed consumer spending held up despite rising energy costs, a sign of resilient demand.

Why it matters: The two-week decline in oil prices had offered an encouraging signal that energy-driven inflation pressures might ease. That picture changed this week. The longer oil remains elevated, the greater the risk that energy costs begin to weigh on consumer spending, corporate profit margins, and broader economic activity. Oil prices are one of the most important variables to monitor in the coming months.

S&P 500 Continues to Set New All-Time Highs

Stocks reached new highs, but the pace of the rally slowed. The S&P 500 and Nasdaq both closed at fresh all-time highs mid-week, supported by the ceasefire extension and a solid start to first-quarter earnings season. Nearly 25% of S&P 500 companies have reported Q1 2026 results, with roughly 80% beating estimates.

Even so, the market's appetite for additional risk appeared to pause. Volatility edged higher, and high-yield credit spreads were flat after three consecutive weeks of tightening, a sign that markets are digesting recent gains rather than pressing further.

Why it matters: The rally remains intact, and the early earnings results are encouraging. However, the pause suggests the market may need a clearer geopolitical signal, such as a geopolitical resolution or positive diplomatic development, before moving higher.

Treasury Yields Reverse Higher as Oil Prices Rise

The 2-year Treasury yield gave back nearly half of a three-week decline that had built on ceasefire optimism and falling oil prices.

Two factors drove the reversal: the collapse of Iran peace talks and the Senate confirmation hearing for Fed Chair nominee Kevin Warsh, which added uncertainty around the future direction of Federal Reserve leadership.

Why it matters: Last week's Fed policy forecast suggested the Fed could have room to cut rates later this year if oil prices continued to fall. This week, that conviction softened. With oil reversing higher and Fed leadership in transition, markets are weighing both inflation risk and institutional uncertainty heading into next week's Fed meeting.

Next Week’s Calendar is Busy

The main event is the Federal Reserve meeting, which will include Chair Powell's second-to-last press conference. The policy decision is widely expected to be a hold, but Powell's characterization of the inflation and growth outlook will be closely watched.

The week also brings a cluster of earnings reports from major technology companies, including Microsoft, Alphabet, Meta, and Amazon, which will offer a window into the state of AI capital spending.

Why it matters: The Fed meeting and tech earnings together make next week one of the more consequential on the calendar this quarter. How Powell frames the inflation picture, and whether leading technology companies confirm or temper expectations around AI investment, could set the tone for markets heading into May.

More Money, More Mess: The Hidden Cost of Uncoordinated Wealth

Many people assume that as their net worth grows, their financial life gets simpler. In practice, the opposite is often true. Growing wealth tends to create a quiet kind of clutter that doesn't show up on a balance sheet, but shows up in missed opportunities, unnecessary taxes, and decisions that no longer match the life you're living today.

This clutter rarely announces itself. It builds slowly, one account and one decision at a time, until it becomes difficult to see how all the pieces fit together.

How Financial Clutter Builds Over Time

Financial clutter isn't usually a sign of poor discipline. It's often a sign of a life that has moved forward. You changed jobs, so you left a 401(k) behind. You inherited an IRA. You opened a brokerage account at one firm, then another at a different firm because someone recommended it. You bought a life insurance policy in your thirties, and another one later for estate purposes. You worked with a CPA, then a different CPA, then an attorney who drafted a trust your current advisor has never reviewed.

Each of those decisions made sense at the time. The issue is that no one stepped back to ask how they all fit together. Most clutter isn't the result of bad advice. It's the result of good advice given in isolation, year after year, without a plan to connect the pieces.

What Coordinated Planning Does

Turning clutter into clarity isn't a matter of starting over. It's a matter of giving every piece of your financial life a defined role and making sure those roles work together. A coordinated plan does a few specific things that piecemeal decisions can't.

It gives each account a job. Some assets are better suited for current income, others for long-term growth, and others for heirs or charitable goals. When each account has a clear purpose tied to the overall plan, day-to-day decisions become easier and more consistent.

It sequences withdrawals with taxes in mind. The order in which you draw from taxable, tax-deferred, and Roth accounts can meaningfully affect your lifetime tax bill, your Medicare premiums, and how long your portfolio lasts. A coordinated plan looks at these decisions together rather than one year at a time.

It uses planning windows that are easy to miss. The years between retirement and the start of Required Minimum Distributions can be one of the most valuable periods for Roth conversions, capital gains planning, and charitable strategies. Without a plan, those years often pass without being fully used.

It revisits the pieces you may have forgotten. Older insurance policies, annuities, and legacy accounts sometimes continue to serve a purpose, and sometimes they no longer do. A coordinated review asks whether each one still fits, and what to do if it doesn't.

It aligns your accounts with your estate plan. Beneficiary designations often override what your will or trust says. A coordinated plan makes sure the titling of your accounts, the designations on retirement plans and insurance, and the structure of your estate documents all point in the same direction.

The Big Takeaway

A well-built plan doesn't add. It organizes. It ties your investments, tax planning, insurance, and estate documents together into a single picture of the life you want to fund and the legacy you want to leave. The goal isn't to own more. It's to make sure what you already own is working together.

Every household's situation is different, and the right path forward depends on your goals, your family, and how you want retirement and legacy to look. Our goal is to help you turn financial clutter into clarity, so the wealth you've worked hard to build can serve the life you actually want.

The Tax Items Congress Wants, But Probably Won’t Pass Yet

Most months, there isn’t much new tax law to report. This is one of those months.

No major tax rules have changed. But there’s still a useful update worth sharing, because what Congress is debating now can tell us something about where tax policy may be headed, even when nothing has changed yet.

The Short Version

Republicans are working on another budget reconciliation bill before the midterm elections.

Reconciliation is the procedural workaround that lets the Senate pass certain budget-related legislation with a simple majority instead of the usual 60-vote threshold. It’s how last year’s major tax bill became law on a strictly partisan vote, and it’s the most likely vehicle for any significant tax legislation between now and then.

GOP taxwriters would like to see tax provisions included in this next bill. Their wish list includes priorities that didn’t make it into last year’s bill, a framework for taxing digital assets, changes to health savings accounts, easings to the corporate alternative minimum tax, and reforms to refundable credits.

That’s the wish list. The problem is that the vehicle for carrying it may not be available this time.

The next reconciliation package now looks likely to be narrow. The current direction from the White House and congressional leadership is to limit the bill to funding for two Department of Homeland Security agencies, Immigration and Customs Enforcement and Customs and Border Protection.

The administration wants the bill enacted by June 1, which puts pressure on lawmakers to move quickly and reduces the appetite for expanding the package.

In other words, taxes probably aren’t in the next bill. But the wish list itself is still informative.

What We’re Watching, and Why

When tax provisions are debated and then deferred, it’s tempting to file the news away as not relevant yet.

We treat it differently.

The items being discussed today are often the items that resurface when the next legislative opportunity appears. The planning value of knowing what may be coming is highest before the rules are final, not after.

A few specific items are on our watch list.

Digital Assets

A clear federal framework for taxing cryptocurrency and other digital assets has been on the wish list for years and keeps getting pushed.

When it does pass, it could create new reporting obligations and may affect how gains, losses, and transactions are documented. Clients with meaningful digital asset positions should expect this issue to land eventually.

Health Savings Accounts

Proposed changes generally aim to expand who can contribute and how the funds can be used.

HSAs are already one of the most tax-efficient accounts in the code. Any expansion could create new planning opportunities for clients who qualify, especially those trying to coordinate healthcare costs, retirement planning, and long-term tax efficiency.

Refundable Credits

Reform here usually means tightening eligibility and increasing verification.

That connects directly to the broader IRS enforcement story we wrote about separately. The trend is toward more scrutiny of these credits, whether through legislation, enforcement, or both.

Corporate Alternative Minimum Tax

Most individual clients aren’t directly affected by the corporate alternative minimum tax.

But executives, business owners, and investors with exposure to companies affected by the rule may still care about how changes could flow through to valuation, cash flow, compensation, or transaction planning.

The Big Takeaway

None of these tax changes appear imminent.

But they’re still worth watching, because tax legislation tends to move in long pauses punctuated by short bursts of activity. The pauses are when planning happens. The bursts are when the rules change.

We watch the legislative calendar so that when something does move, we already know what it means for the clients it affects. More importantly, we’ve already had the conversations that need to happen.

If any of the items above touch your situation and you’d like to talk through the implications, we’re glad to do that.

Weekly Market Recap: New All-Time Highs as Markets Look Past a Failed Ceasefire

Stocks climbed to new records this week, shrugging off a failed ceasefire deal and a U.S. naval blockade of Iranian ports.

The S&P 500 gained nearly +3%, completing an 11-session V-shaped recovery from the late-March bottom, while the Nasdaq gained nearly +5% to set its own record. Smaller companies participated in the advance but lagged, and defensive sectors along with energy, industrials, and materials declined.

Bonds finished roughly flat, oil ended the week lower despite an early surge, and volatility measures continued to ease as geopolitical risk premiums faded.

Key Takeaways

The S&P 500 Set a New All-Time High

The index traded above 7,000 for the first time since late January, completing a full recovery from the nearly -10% late-March drawdown. Monday was the week's test, with oil briefly surging above $100 on news of the U.S. Navy's blockade of Iranian ports before markets recovered after confirmation that non-Iranian shipping would be unaffected.

The past six weeks were a reminder that trying to time geopolitical events carries a real cost for investors who moved to the sidelines.

Market Risk Premiums Continue to Fade

The VIX, which spiked above 30 at the height of the conflict in late March, has since fallen below 20 and is approaching pre-conflict levels. Credit spreads have tightened steadily, and equity volatility, credit conditions, and interest rate volatility are all improving in tandem.

With the Strait of Hormuz still effectively closed and no official ceasefire in place, these risk metrics will remain closely watched.

Growth and Technology Stocks Have Reasserted Their Leadership

After spending much of the first quarter lagging behind value, smaller companies, and international markets, growth and technology stocks have outperformed value by more than +11% since the late-March low. As a result, the year-to-date performance gap between growth and value has nearly closed.

This year has already cycled through two distinct market environments, underscoring the value of maintaining diversified exposure.

Manufacturing Contracted in March, But April Data Signals Recovery

Industrial production pulled back in March as energy costs surged and supply chain disruptions weighed on activity. More recent data offers a more encouraging picture, with the April Philadelphia Fed Manufacturing Index coming in above expectations as tensions eased and energy prices fell.

The March weakness appears tied to conflict-related disruption rather than a broader deterioration in economic conditions.

Bank Earnings Provided an Encouraging Start to Earnings Season

Major Wall Street banks reported strong first-quarter results, driven by elevated market volatility and increased capital markets activity, while consumer credit quality remained healthy.

Several banks did flag the increasingly complex backdrop as a development worth monitoring going forward.

As always, feel free to reach out with any questions or concerns as they come up.

A Smaller IRS, a Different Kind of Enforcement

The IRS is meaningfully different than it was eighteen months ago. The agency has lost more than a fifth of its workforce since the start of 2025, its budget has been cut, and most of the funding boost it received from the 2022 Inflation Reduction Act has been clawed back.

What this adds up to isn't just a smaller IRS. It's a different IRS.

The agency is reshaping what it enforces, how it enforces it, and which taxpayers are most likely to hear from it. That story is worth understanding, both because it's genuinely consequential and because the practical implications for taxpayers aren't what you might first assume.

The numbers behind the change

Congress set the IRS's fiscal year 2026 budget at $11.2 billion, about 9% below FY25. House appropriators are pushing for a further cut to $10.2 billion in FY27. The agency has lost more than 20% of its workforce since January 2025 through deferred resignations and layoffs, with additional departures expected this year.

The Trump administration's FY27 budget request includes an 18% reduction in enforcement activity and projects an enforcement workforce below 25,000. Within that already shrunken enforcement arm, some of the largest losses have hit the examination and collection groups, and many of those who left were experienced agents and managers carrying years of institutional knowledge that won't be easy to replace.

In plain English, the IRS has fewer people, fewer experienced reviewers, and less capacity to conduct traditional enforcement the way it once did.

Fewer audits, especially at the top

The audit rate for individuals has been well below 1% for several years, and we expect it to keep falling, at least over the next few years.

Audits of individuals with $10 million or more of income, which numbered 6,786 in FY25, dropped to 2,264 in FY26. Partnership audits fell from 3,174 to 2,932 over the same period. The agency forecasts further declines in both categories in FY27.

For clients in higher income brackets, who historically faced disproportionate audit attention, the near-term picture is meaningfully different than it was even two years ago. The headline probability of a traditional audit appears lower.

But that doesn't mean enforcement risk has disappeared. It means the nature of that risk is changing.

The odds of a traditional audit may be lower, but the audits that remain are less likely to be random noise. They're more likely to be tied to something specific in the return, such as a mismatch, an anomaly, a complex transaction, or an item that doesn't reconcile cleanly with third-party data.

What's replacing the lost capacity

That's the headline. The more interesting story is what's replacing the lost capacity.

IRS leadership has said publicly that fewer audits will be paired with more targeted ones, and the mechanism for that targeting is increasingly data analytics and artificial intelligence. The agency has been investing in software that mines taxpayer data to surface anomalies, flag suspicious activity, and identify cases for review.

Even with reduced funding, the direction of travel is clear: the IRS is leaning harder on technology because it no longer has the same human capacity. The intent is to compensate for the loss of human reviewers by being more precise about who gets reviewed in the first place.

We'll see how well it works in practice. But the direction is clear: less of the broad coverage that audit rates traditionally measured, and more of the targeted attention those same rates fail to capture.

Where enforcement is concentrating

Two areas in particular look like they'll absorb a disproportionate share of the enforcement capacity that remains.

The first is refundable credits, where the IRS estimated improper payments of $21.4 billion in FY24 alone. The earned income credit, the American Opportunity credit, and the premium tax credit are all on this list, and all are well-suited to algorithmic review.

For many higher-income households, refundable credit reviews may not be the primary concern. But they illustrate the broader enforcement shift. The IRS is favoring areas where software can flag returns quickly and where discrepancies can be identified without a large team of experienced agents.

For you, the more relevant version of that same shift is income matching.

The IRS's automated underreporting program compares the W-2s, 1099s, and other third-party tax forms it receives against what taxpayers report on their returns. Significant mismatches generate a CP2000 notice, which is computer-driven and doesn't require an experienced agent to produce.

This matters for households with brokerage accounts, equity compensation, retirement income, business income, K-1s, real estate activity, charitable giving, or multiple sources of income. The more moving pieces there are, the more important it becomes that the return tells a clean and consistent story.

Traditional enforcement may shrink, but automated enforcement can still expand because it requires fewer experienced agents to initiate. As enforcement leans further into automation, expect more of this kind of correspondence, not less.

What it means for you

For you, this all means a few things.

First, the headline audit risk for high-income clients is genuinely lower than it was. That's a real shift, and it's worth naming rather than dismissing. But it isn't a license for casual recordkeeping.

The audits that do occur will be more precisely chosen. That means the cases that get pulled are more likely to be cases where something genuinely doesn't reconcile. Clean books, good documentation, and coordinated reporting matter at least as much in this environment as they did before, possibly more.

Second, the surface area for automated correspondence is growing.

CP2000 notices, refundable credit reviews, and other algorithm-driven inquiries don't feel like audits and may not show up in the headline audit statistics. They may not require the same scope of work as a full audit, but they still require careful review, documentation, and a timely response.

If you receive one, the worst thing to do is ignore it. The deadlines on these notices are real, and the IRS's response to silence is rarely favorable.

Third, the shape of the agency is going to keep changing.

Budget proposals are still being debated, workforce attrition is ongoing, and the technology is still maturing. What looks like a settled picture today may shift again over the next year or two.

That's part of why we follow this closely. Tax planning is most useful when it accounts for where the enforcement environment is going, not just where it is.

Why coordination matters more now

This is also why tax planning and wealth planning shouldn't live in separate silos.

The more complex your income, investments, retirement withdrawals, equity compensation, business interests, or estate planning becomes, the more important it is that the tax return tells the same story as the financial plan.

A smaller IRS may conduct fewer traditional audits. But a more automated IRS may still notice when the pieces don't line up.

That's why tax planning isn't just about finding deductions or reacting before year-end. It's about making sure decisions are coordinated before they show up on a return. Investment decisions, retirement income decisions, Roth conversion decisions, charitable giving decisions, and estate planning decisions can all create tax consequences. The goal is to understand those consequences ahead of time rather than explain them after the fact.

The Big Takeaway

None of this changes the fundamentals of what we do for clients.

We aim to file accurately, document thoroughly, and structure things so that when the IRS does ask a question, the answer is already on the shelf.

That discipline mattered when audit rates were higher, and it matters now, even as the agency asking the questions becomes smaller, more automated, and more selective.

The goal hasn't changed: clarity in your filings, confidence in your position, and the peace of mind that comes from knowing the work was done right the first time.

Weekly Market Recap: Ceasefire, Oil Reversal, and the Rally Markets Were Waiting For

Stocks traded higher for a second consecutive week as de-escalation triggered the strongest single day rally in a year. The S&P 500 gained +3.7%, with the Nasdaq and the Russell 2000 both returning +4.3%.

Most of the rally occurred on Wednesday after the announcement of a two-week ceasefire contingent on Iran reopening the Strait of Hormuz. Oil plunged -11%, the VIX dropped below 20, and international stocks rose as energy-importing nations benefited from the oil reversal. Industrials were the top-performing sector, gaining +5%, with broad strength across most sectors excluding energy.

Treasury yields fell modestly, and corporate bonds outperformed as credit spreads tightened to late January levels. However, the ceasefire was already being tested late in the week, with the market closely monitoring this weekend’s talks.

Key Takeaways

The U.S. and Iran agreed to a two-week ceasefire, triggering a relief rally.

Late Tuesday, the White House announced an agreement contingent on Iran reopening the Strait of Hormuz, less than two hours before a stated deadline to launch strikes on Iranian infrastructure.

Markets reacted decisively Wednesday: the S&P 500 surged +2.5%, its best single-day gain in a year, the Dow jumped +2.9%, the Russell 2000 gained +3.0%, and international equities rallied +3.5%. Unlike prior headlines, this was an actual agreement confirmed by both sides, with talks scheduled for this weekend.

Implication: The ceasefire is meaningful, but its durability was tested within hours. Israel launched strikes across Lebanon, Iran accused the U.S. of violating three conditions, and the Strait remained effectively closed Thursday morning. This weekend's talks will determine whether the agreement marks a turning point.

Oil plunged -16% on Wednesday, its largest single-day decline since April 2020, as the market priced in a Hormuz reopening.

WTI fell from $112 to around $94, erasing weeks of the war-driven rally that had pushed oil up over +65% YTD. The decline triggered immediate secondary effects: airline stocks surged, and the odds of a rate cut increased as inflation expectations eased.

However, the physical reopening remains uncertain. As of Thursday morning, the Strait was still effectively closed, and oil was moving back toward $100.

Implication: Oil is the transmission mechanism through which the conflict reaches inflation, the Fed, consumers, and corporate profits. Wednesday's decline showed how quickly the geopolitical premium can unwind, with the market watching for actual follow-through.

Credit spreads tightened and volatility declined, confirming the risk-appetite shift across asset classes.

High-yield spreads compressed during Wednesday's ceasefire rally and are now the lowest since late January after tightening nearly -0.50% over the past two weeks. Credit spread tightening is an indication the market is starting to price in less stress.

The VIX fell to 21, its first close below 22 since late February, after touching 28 intraday Tuesday before the ceasefire was announced.

Implication: Credit and volatility are the market's most reliable stress indicators, and both confirmed the equity rally as broad-based rather than speculative.

Treasury yields barely moved despite the ceasefire rally.

The 10-year yield fell just -0.03% to 4.28%, a muted response given the magnitude of the oil crash and equity rally. The bond market's reaction reflects the Fed's policy forecast. Seven of nineteen Fed members forecast zero cuts in 2026, and the Fed's March minutes, released this week, reaffirmed its patient approach.

Implication: The bond market's restraint suggests it is waiting for confirmation that the ceasefire will meaningfully improve the inflation and growth outlook.

Next week unofficially kicks off Q1 earnings season, with the big Wall Street banks reporting.

The focus will extend beyond the usual revenue and earnings beats to management commentary on the conflict's impacts, from energy costs and supply chain disruptions to consumer demand and forward estimates.

Implication: Earnings calls will provide the first corporate read on how the energy shock is flowing through margins, pricing, and demand. Forward guidance and tone may matter more than the headline numbers this quarter.

1Q26 Market & Economic Recap & 2Q26 Outlook

Key Updates on the Economy & Markets

The first quarter of 2026 was one of those periods that reminded investors why markets don't move in a straight line.

Stocks started the year on solid footing with January modestly positive, February quiet, and then March arriving with a jolt. The escalation of geopolitical tensions in the Middle East, including the closure of the Strait of Hormuz, sent oil prices surging and rattled markets in ways that few anticipated heading into the year.

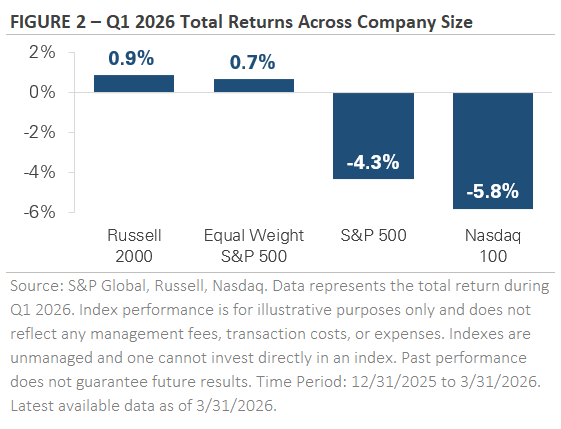

By the time the quarter closed, the S&P 500 was down -4.3%, with the bulk of that decline concentrated in a single month. And if you looked only at that headline number, you might walk away with a grim picture.

But the quarter was more nuanced than the index suggests, and I think it's worth taking a step back to understand what actually happened and what it means for your portfolio going forward.

Higher Oil Prices Changed the Rate Cut Conversation

Indeed, to understand why March felt so disruptive, you have to start with oil.

Crude prices had already been moving higher before tensions escalated with supply concerns tied to Venezuelan output pushing prices up nearly 13% in January, and climbing another 4% in February as geopolitical risks continued to build.

Then March arrived.

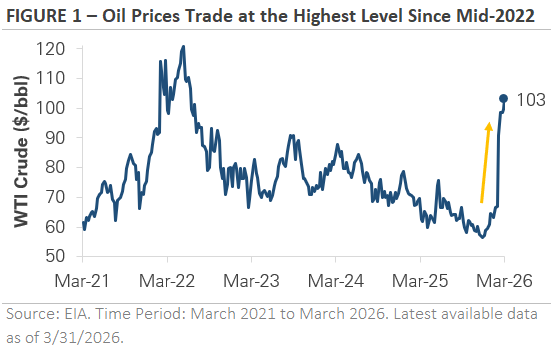

The conflict between the U.S. and Iran intensified, and the closure of the Strait of Hormuz, a waterway that carries roughly 20% of the world's oil, sent crude prices surging nearly 50% in a single month. For the full quarter, oil prices rose more than 70%, reaching levels not seen since mid-2022.

And why does that matter for your portfolio?

Because oil prices don't exist in a vacuum. Higher energy costs flow through to what consumers and businesses pay for goods and services. And as a matter of fact, you've likely already noticed it at the pump, as gasoline prices have risen nearly a dollar per gallon since late February.

And this is happening at a moment when inflation was already showing signs of firming before the conflict began. The Federal Reserve's preferred inflation measure, Core PCE, remains near 3%, and producer prices have been trending higher.

So then, coming into 2026, the market expected the Federal Reserve to cut interest rates two to three times by year end.

That expectation quietly eroded as the quarter progressed.

And by the time March ended, those rate cuts had been priced out entirely, and there was even early discussion about whether a rate hike might come back into the conversation.

The situation is still evolving.

The Strait of Hormuz remains closed as of quarter-end, negotiations are ongoing, and oil is trading near $100 per barrel, a signal that the market expects the disruption to persist for some time.

The April and May inflation reports will be the first data to fully reflect the energy price surge, and they'll go a long way toward shaping the Federal Reserve's next move. In the meantime, headlines out of the Middle East are likely to continue influencing how both stocks and bonds behave in early Q2.

Diversification Quietly Did Its Job

Now, one of the most important, and most overlooked, stories of Q1 was what happened beneath the surface of the S&P 500.

The S&P 500 is a market-cap weighted index, meaning the largest companies carry the most influence over the index's return. When those large companies, particularly those in the technology sector, sold off, the headline number felt worse than what most diversified investors actually experienced.

To put it in perspective, the average S&P 500 stock outperformed the broad index by nearly 5% in Q1. Small-cap stocks, as measured by the Russell 2000, actually gained nearly 1%. And international stocks finished the quarter with a gain of nearly 1% as well, outperforming the S&P 500 by more than 5 percentage points.

And what drove that gap? Well, there were two competing forces at work.

The first was a rotation away from mega-cap tech stocks. For the past two years, a handful of the largest companies drove the majority of the market's gains.

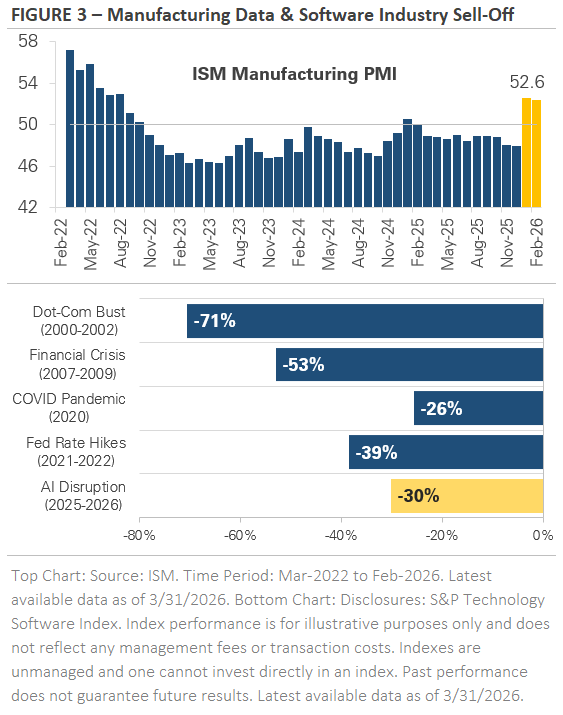

In January, investors started moving away from that concentrated trade. The rotation accelerated in February when concerns about artificial intelligence disruption spread through the software sector, and markets began to price AI not just as a productivity enhancer, but as a potential replacement for entire categories of professional services.

The software sector has now declined nearly 30% from its peak last October, one of the largest non-recessionary drawdowns in over 30 years.

The second force was a genuine improvement in manufacturing activity. After spending nearly a year in contraction, the ISM Manufacturing Index crossed into expansion territory in February and held there in March.

That's a meaningful sign for the economy and potentially for corporate earnings.

Indeed, the manufacturing sector had been a soft spot in the economy since 2022, and the data suggested it was gaining real traction before the conflict began. Industrials was one of the few sectors to set a new all-time high during the quarter.

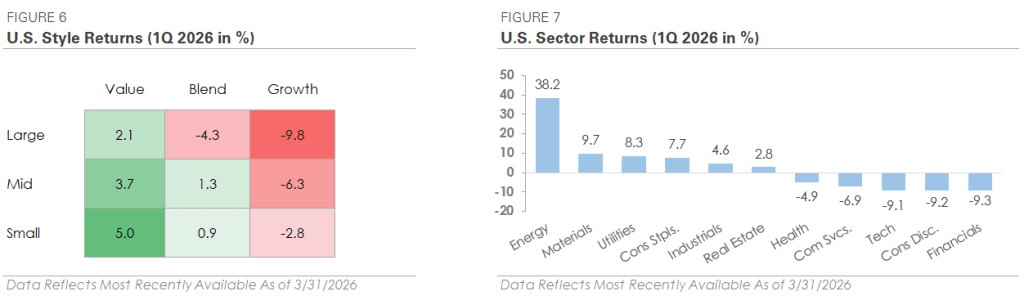

Across the broader equity market, six of the eleven S&P 500 sectors outperformed the index, a sharp contrast to recent years when gains were driven by just a few names. Energy led everything with a 38% return as oil surged.

Materials, Utilities, and Consumer Staples each gained more than 7.5%. On the other end, Technology, Consumer Discretionary, and Financials each declined more than 9%.

The gap between the best and worst sectors was wide. But for investors with diversified exposure across company sizes, sectors, and geographies, the quarter felt more moderate than the S&P 500 return alone would suggest.

Diversification didn't eliminate the volatility. It helped manage it, and that's exactly what it's designed to do.

Bonds Navigated a Volatile Quarter

The bond market had its own version of the quarter's turbulence.

Interest rates rose in January as tariff concerns resurfaced, then fell sharply in February as growth worries, particularly around AI disruption, pulled investors toward safer assets.

March reversed that move quickly.

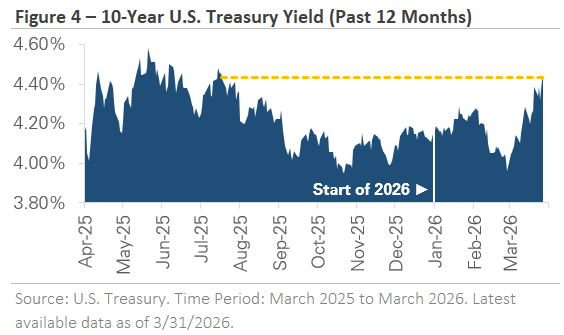

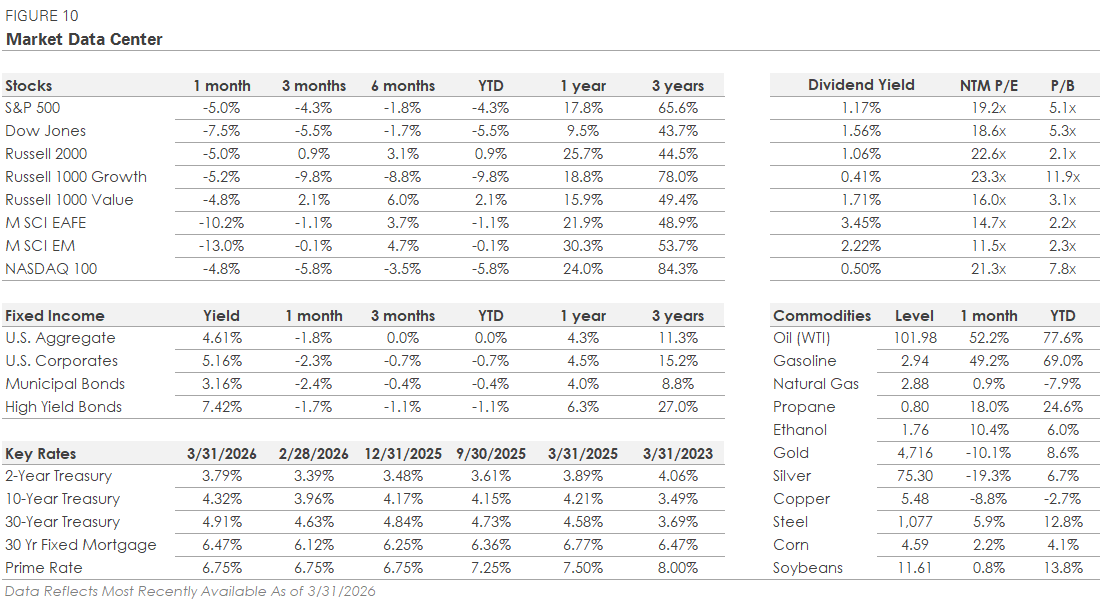

And as oil prices spiked and rate cut expectations faded, yields climbed again. The 10-year Treasury yield ended the quarter near 4.32%, its highest level since mid-2022. The 2-year yield rose nearly 0.35% for the quarter, reflecting how quickly rate cut expectations shifted.

The Bloomberg U.S. Aggregate Bond Index finished the quarter flat, a meaningful step down from the 1% or better returns it produced in each of the prior four quarters. Corporate bonds modestly underperformed higher-quality Treasuries, and credit spreads widened to their highest levels since early 2025.

That widening reflects caution, not crisis, with corporate spreads remaining well below the levels reached during past recessions and financial dislocations.

And what are we to take of all this data?

Well, the bond market is telling us that investors are being careful, but it's not telling us something is broken yet.

What to Watch in Q2

As we move into the second quarter, the central story remains the same: the Middle East, oil prices, inflation, and what the Federal Reserve does next.

Progress toward resolving the Strait of Hormuz closure would ease energy costs and give the Fed more room to maneuver on rates. However, a prolonged disruption means higher oil prices have more time to work through to consumers and businesses, keeping inflation elevated and leaving the Fed in a difficult position.

From a data perspective, the April and May inflation reports are the ones to watch. They'll be the first readings to capture the full impact of higher energy costs, and they'll shape the rate outlook for the rest of the year.

While you're watching those headlines, I want to offer some perspective on the bigger picture.

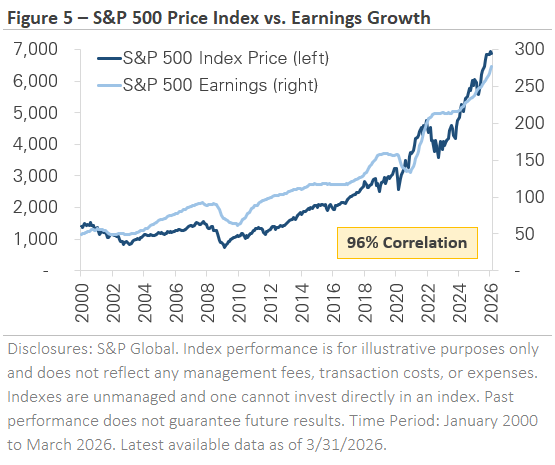

Over the past 26 years, corporate earnings and stock prices have moved together with a 96% correlation.

When earnings rise, prices generally follow.

When earnings deteriorate, as they did in 2001, 2008, and 2020, prices tend to fall with them. What's notable about today's environment is that earnings estimates have continued to rise even as the S&P 500 has pulled back.

Analysts still expect earnings growth in the coming quarters, and profit margins to remain healthy.

Put differently, the market's decline in Q1 was driven by uncertainty around oil, inflation, and Federal Reserve policy, not by a deterioration in the underlying fundamentals that drive stock prices over time.

And that distinction matters.

Certainly, uncertainty is uncomfortable, but it's different from a breakdown in the economic foundation.

The quarter also reinforced something I believe deeply in that staying invested, staying diversified, and keeping a long-term perspective is one of the most effective strategies available to investors. The areas of the market that led over the past two years underperformed in Q1.

Investors with broad exposure across company sizes, styles, and geographies experienced a meaningfully different quarter than the headlines suggested.

When it comes down to it, markets will work through the uncertainty in the Middle East. The data will come in, the Fed will respond, and conditions will shift, as they always do.

In the meantime, your plan was built for periods like this one, and I remain confident in the approach we have in place.

Weekly Market Update: Relief Rally Lifts Markets to New Highs as Ceasefires Hold

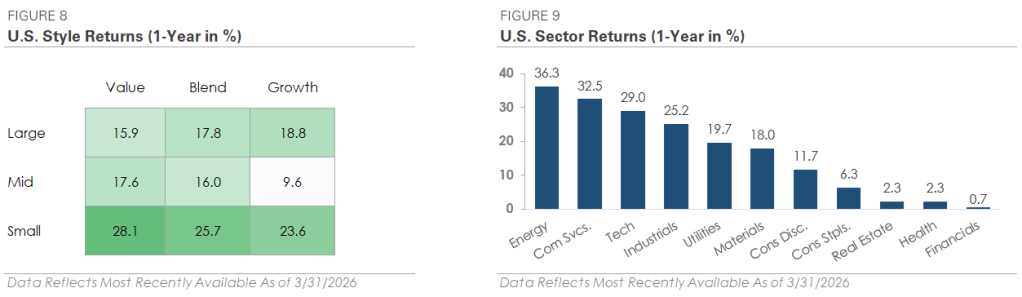

Markets surged in April as a series of diplomatic breakthroughs lowered the risk of further military escalation, with the S&P 500, Nasdaq, and Russell 2000 all closing at fresh all-time highs and erasing the first quarter's losses.

Leadership was narrow, however, and the gains were uneven beneath the surface. Growth stocks outpaced value by +8%, reversing the first quarter's rotation, and semiconductors rallied +40% on a 17-day winning streak. The average stock across the S&P 500 underperformed the index by nearly -4.5%, and all ten remaining sectors trailed technology.

Bonds were mixed. Treasury bonds produced modest losses as yields drifted higher, while corporate bonds traded higher as credit spreads tightened. Oil whipsawed on geopolitical headlines, with WTI crude rising +7% but trading in a wide $80 to $115 range, and a measure of market volatility fell sharply as investors unwound the geopolitical risk premium.

Ceasefires Drove the Rally, Oil Supply Disruption Remains

Stocks surged as the U.S.-Iran ceasefire was extended, the Israel-Lebanon ceasefire held, and de-escalation rhetoric reduced the risk of a wider ground war. Markets responded by unwinding the geopolitical risk premium that had weighed on equities throughout the first quarter.

The U.S. naval blockade of Iranian ports remains in effect, however, and the Strait of Hormuz remains functionally closed.

Why it matters: The diplomatic track and the physical supply situation are moving in opposite directions. Whether April's rally holds may depend on whether the Strait reopens.

Fed Outlook Shifts from Possible Hikes to Possible Cuts

Markets repriced Fed expectations at each remaining 2026 meeting, shifting from pricing in possible hikes to pricing in possible cuts. The most likely outcome is still no change, with cut probabilities below 15%, but the move reflects a meaningful change in tone driven by oil's pullback easing near-term inflation fears.

The Fed is also preparing for a leadership transition, with Kevin Warsh set to succeed Jerome Powell when his term expires in May.

Why it matters: The Fed's policy path has become harder to read at the same moment its leadership is changing hands, leaving markets to navigate both inflation risk and institutional uncertainty.

Q1 Earnings Off to a Strong Start, Margins Hit Record

First-quarter earnings season started strong, with the quarter on pace for a sixth consecutive quarter of double-digit growth and profit margins reaching a record 13.4%. Analysts now forecast +18% earnings growth over the next 12 months.

Forward valuations rose to 21x from 19.7x at quarter-end, with a meaningful portion of the move tied to rising earnings estimates rather than pure multiple expansion.

Why it matters: With valuations elevated and the geopolitical backdrop still volatile, earnings growth has become the primary path to further upside, and the rising bar means continued delivery will be needed to sustain current levels.

Rally Breadth Narrow Despite New Highs

The S&P 500 reclaimed key trend levels and closed near an all-time high, fully erasing March's -9% drawdown. Risk appetite surged as credit spreads tightened, volatility fell, and institutional equity futures positioning moved to its highest level since late 2024.

Beneath the surface, the rally was concentrated in semiconductors and mega-cap stocks rather than broad-based participation, and some measures of investor sentiment remained subdued.

Why it matters: Sustained rallies historically require broadening participation, and the current concentration leaves the index vulnerable if sentiment around the AI and growth trade shifts.

Economy Rebounds, Inflation Picture Worsens

The U.S. economy grew +2% in the first quarter, rebounding from +0.5% in the fourth quarter as the government shutdown effect reversed. Manufacturing held above the expansion threshold for a third consecutive month, and unemployment edged lower to 4.3%.

The inflation picture is less encouraging. Headline consumer prices surged +0.9% in March, the highest since June 2022, and the Fed's preferred core inflation measure remains elevated at +3.2% year-over-year and trending higher.

Why it matters: The growth picture is firming up at the same time the inflation picture is deteriorating, and the longer oil remains elevated, the harder it becomes for the Fed to ease policy later this year.

May Calendar Brings Fed Transition and Continued Earnings

The month ahead is one of the more consequential on the calendar this quarter. The Fed meets in May for what will be Chair Powell's final meetings before Kevin Warsh takes over, and the second half of Q1 earnings season continues with results from a broad range of companies.

Oil and the status of the Strait of Hormuz remain the key variables outside of corporate fundamentals.

Why it matters: How Powell frames the inflation and growth outlook on his way out, the tone Warsh signals on his way in, and any movement on the physical oil supply situation could each set the tone for markets heading into the summer.