Before You Roll Over Your 401(k), Check This Hidden Tax Break

Rolling an old 401(k) into an IRA often feels like the obvious move.

It is simple. It is clean. It consolidates your retirement assets in one place and gives you more control over how the money is invested. For many retirees, it becomes the default path. And in many cases, it is the right call.

But if your 401(k) holds highly appreciated company stock, that automatic rollover could accidentally erase a valuable tax planning opportunity. One that, once lost on those shares, generally cannot be recovered.

That opportunity is called Net Unrealized Appreciation, or NUA.

Why the Default Answer Is Not Always the Right One

Most assets inside a traditional 401(k) share the same tax character. When the money comes out, whether through withdrawals, required minimum distributions, or a rollover that is later converted to Roth, it is generally taxed as ordinary income. That is the deal with pre-tax retirement accounts. The government deferred the tax on the way in, and it collects on the way out at whatever ordinary income rates apply at the time.

But employer stock can be different, if it qualifies for NUA treatment and is handled correctly at distribution.

Here is the distinction that matters. Instead of rolling the company stock into an IRA where it will eventually be taxed as ordinary income, some retirees may be able to distribute the employer stock in kind directly into a taxable brokerage account.

When that happens, ordinary income tax is owed only on the original cost basis of the stock, meaning what the plan originally paid for the shares. The appreciation that occurred inside the plan, the NUA itself, is not taxed at ordinary income rates. Instead, when the stock is later sold, that NUA may qualify for long-term capital gains treatment.

Any additional appreciation after the stock is distributed into the taxable brokerage account is treated differently. That gain is taxed under the normal capital gains rules, depending on how long the stock is held after distribution.

That distinction is not cosmetic. Long-term capital gains rates are often significantly lower than ordinary income rates. For some retirees, the spread between those two rates can be 10, 15, or even 20 percentage points. On a large block of appreciated employer stock, that gap translates into real dollars.

So before deciding whether to roll over, convert, or liquidate retirement assets, retirees with company stock inside the plan need to slow down.

The question is not simply, "Should I roll this 401(k) into an IRA?" The better question is, "Is there company stock inside this plan, and does NUA change the tax math?"

Running the Numbers on a Real Scenario

Consider a retiree with a $1.2 million 401(k).

Inside the plan is $400,000 of employer stock. The original cost basis of that stock is $80,000. The remaining $320,000 is appreciation accumulated over years of employment and company growth.

If the entire 401(k) is rolled into an IRA, the NUA opportunity disappears. Every future dollar that comes out of that account, including the $320,000 of appreciation, will be taxed as ordinary income.

But if the company stock qualifies for NUA treatment and is distributed properly, the picture changes. The retiree pays ordinary income tax on the $80,000 cost basis in the year of distribution. That is a real tax bill, and it needs to be planned for. But the $320,000 of appreciation may eventually qualify for long-term capital gains treatment when the stock is sold, rather than being taxed at ordinary income rates later through IRA withdrawals.

That does not automatically make NUA the right answer for every retiree who finds themselves in this position.

Holding a large block of a single employer's stock in a taxable account creates concentration risk. Market conditions change. Companies that looked strong at retirement can look very different five years later. Cash flow timing matters too, because the ordinary income tax on the cost basis is due in the distribution year, which requires liquidity.

Medicare thresholds, Social Security taxation, and estate planning considerations all factor into the analysis. And the IRA rollover route, while less tax-efficient in this scenario, offers simplicity and diversification that have genuine value.

But all of those tradeoffs deserve a careful evaluation. Not a default answer and a signature on a transfer form.

Because once the employer stock is rolled into an IRA, the NUA window on those shares is generally closed. The stock becomes IRA money. The favorable tax character is gone. And there is no going back.

What to Do Before You Sign the Transfer Form

NUA is not for everyone. For retirees whose company stock has minimal appreciation, or whose cost basis is high relative to the current value, the math may not favor a taxable distribution.

The strategy generally requires a qualifying triggering event, a lump-sum distribution of the plan balance within the required timeframe, an in-kind distribution of the employer stock, and careful coordination of any rollover of the remaining assets.

But for retirees with highly appreciated company stock in a 401(k), it can be too important to ignore.

Before rolling over an old employer plan, take the time to review the holdings. Identify whether employer stock is present. Understand the cost basis. Compare the tax impact of leaving the assets in the plan, rolling the account to an IRA, distributing the employer stock under an NUA strategy, and later using Roth conversions where appropriate.

A smart retirement tax plan is not just about choosing between traditional and Roth accounts. It is about understanding every asset, every tax character, and every decision point before making a move that cannot be undone.

Because the goal is not just to move the money somewhere convenient. The goal is to make sure that every dollar you spent decades building works as hard as possible on your behalf, with clarity, confidence, and peace of mind.

How to Reduce RMDs Without a Roth Conversion

Most retirees think the only way to reduce future IRA taxes is through Roth conversions.

Convert now, pay the tax today, and let the money grow tax-free for the rest of your retirement. It is a sound strategy. For many people, it is the right one.

But if you are charitably inclined and over age 70½, there may be another strategy sitting in plain sight. One that does not require writing a check to the IRS today, does not require a market timing decision, and does not add to your taxable income for the year.

It is called a Qualified Charitable Distribution, or QCD.

And for the right retiree, it can reduce taxable IRA income, satisfy charitable goals, and potentially lower the tax pressure created by required minimum distributions, all at the same time.

Why This Matters Beyond Your Tax Bracket

A Roth conversion can be powerful. But it is not always the best first move.

That is especially true for retirees who already give to charity each year. And more retirees fit that description than you might think. Giving to a church, a hospital, a university, a community foundation, or a cause that has been important to a family for decades is not unusual. It is often one of the most consistent line items in a retiree's annual spending.

The problem is how most retirees handle that giving.

The typical pattern looks like this. You take a distribution from your IRA. The distribution hits your checking account and shows up as taxable income. Then you write a check to the charity. The gift is generous. But from a tax standpoint, the sequence can work against you.

This is especially true for retirees who take the standard deduction. In that case, the charitable gift may not produce a separate federal income tax deduction, even though the IRA withdrawal still shows up as income.

When you give directly from a traditional IRA using a QCD, the distribution can go to the charity without showing up as taxable income on your return. The money moves from your IRA to the organization you care about, and for federal income tax purposes, the qualifying portion may be excluded from taxable income.

That matters more than most retirees realize.

Taxable income does not just affect your tax bracket. It influences whether more of your Social Security benefits become taxable. It affects your Medicare Part B and Part D premiums through a mechanism called IRMAA, which can add hundreds or thousands of dollars per year to your healthcare costs.

It affects how much of your long-term capital gains and qualified dividends are taxed. And over time, as IRA balances grow and required minimum distributions increase, all of those pressures can compound together.

So the real question is not simply, "Should I convert more IRA money to Roth?"

The better question is, "If I am already giving to charity, should some of those gifts come directly from my IRA?"

Seeing It in Action

Consider a retired couple in their early seventies with a $1.8 million traditional IRA.

They give $25,000 per year to their church and several charities they have supported for decades. For years, they have made those gifts from their checking account after withdrawing money from their IRA. It has always felt generous, and it has always been. But the tax math has quietly worked against them.

Every dollar they withdraw from the IRA to fund that giving is a dollar of taxable income. That income pushes up their adjusted gross income. That higher adjusted gross income can affect their Medicare premiums and the taxation of their Social Security. And if their IRA continues to grow, their future required minimum distributions may make the problem larger.

Now imagine they redirect that same $25,000 gift directly from the IRA to charity using a QCD.

They still support the causes they care about. The church still receives the same gift. The charities they love still receive the same support. But the money moves directly from the IRA instead of first passing through the couple's checking account.

Same gift. Same charity. Different tax outcome.

One important detail matters here. QCD eligibility begins at age 70½, even though required minimum distributions generally begin later. That creates a planning window where charitable IRA gifts may begin reducing the account balance before required distributions start.

And when that strategy is layered into a multi-year retirement income plan, it can change the overall picture significantly. A retiree who is already giving $25,000 per year through QCDs may need fewer Roth conversions, or may be able to convert more selectively, to keep income in a manageable range.

That means fewer years of deliberately triggering taxable income to move money across the tax wall. It means more flexibility. And it means a retirement income plan that is built around the life you are actually living, not just the account balance on paper.

What to Review Before Your Next Gift

A QCD is not a replacement for Roth conversion planning. The two strategies often work best together, layered intentionally across the years leading up to and following the required minimum distribution age.

But for charitably inclined retirees, the QCD may be one of the most overlooked tools in the retirement tax planning toolbox.

Before converting more IRA money this year, take a step back and look at the full picture. Review your giving history, your IRA balance, your projected RMD timeline, your Medicare thresholds, and your long-term income plan. Because charitable giving and tax planning are not separate conversations. For many retirees, they belong in the same room.

The goal is not simply to convert more. The goal is to keep more control over your income, reduce avoidable taxes, and use your wealth in a way that reflects your values, not just your account statements.

If charitable giving is already part of your life, it may be time to ask whether your IRA should be part of that giving strategy. Because the most powerful retirement tax moves are often the ones that align what you already believe with how your money actually works.

That is where clarity, confidence, and peace of mind begin.

Weekly Market Update: When Rates Rise, Markets Start Asking Harder Questions

The stock market rally slowed this week as investors reacted to a mix of higher interest rates, geopolitical headlines, and a cooling technology rally.

Stocks traded lower early in the week as Treasury yields climbed to levels we have not seen in nearly two decades. Higher rates raised concerns about borrowing costs and put pressure on stock valuations, especially in growth-oriented areas of the market.

Sentiment improved later in the week after reports of potential progress in negotiations with Iran helped push oil prices back below $100 per barrel and steadied interest rates. Even with that improvement, the S&P 500 finished with a modest loss, ending its multi-week winning streak. The Nasdaq also moved lower as the technology rally cooled.

Energy and defensive sectors held up better than the broader market, while more economically sensitive areas like materials and industrials lagged. Bonds declined as rates continued to rise, and the VIX remains near levels last seen in late January despite the week’s equity market volatility.

Key Takeaways

Treasury Yields Continue to Rise, Touching Levels from the Mid-2000s

Interest rates rose again this week, extending a trend that began in late February.

The 30-year Treasury yield touched 5.19% on Tuesday, its highest level in nearly 19 years. Rates moved higher across the curve, with the 2-year and 5-year Treasury yields each rising for a second straight week.

This builds on last week’s move, which followed hotter inflation readings and renewed concerns that price pressures may remain more persistent than investors had hoped.

Why it matters: Several forces are pushing rates higher, including rising oil prices, Fed commentary, and recent inflation data. Interest rates are now sitting near multi-decade highs, and markets are watching closely to see whether this becomes another sustained move higher.

Federal Reserve Commentary Suggests Rate Hikes Are Possible

Minutes from the Fed’s April meeting reinforced the message that interest rates may stay higher for longer.

The meeting included several dissents, and multiple officials appeared less comfortable maintaining a bias toward cutting rates. The message was clear: rate hikes are no longer off the table.

Investors had already started lowering their expectations for rate cuts. While markets still expect the Fed to hold rates steady over its next three meetings, expectations have shifted toward the possibility of a rate increase later this year, potentially at the October or December meeting.

Why it matters: The Fed’s next meeting takes place in mid-June. The setup has changed. Earlier this year, investors were focused on when the Fed would cut rates. Now, the conversation has shifted to whether the Fed may need to raise rates again.

Geopolitical Headlines Continue to Impact Stocks

Stocks rebounded midweek as reports of easing tensions with Iran pushed oil prices lower and improved investor sentiment.

Crude oil, which had spiked on geopolitical concerns, fell from near $110 to below $100 per barrel. That decline helped ease concerns that higher energy prices could add to inflation and keep interest rates elevated.

Stocks responded positively as rates eased, with the S&P 500 and Nasdaq trading back toward record highs and the Dow briefly rising above 50,000.

Why it matters: The quick midweek reversal shows how closely markets are tracking both energy prices and interest rates right now. If oil prices move higher, inflation concerns may rise with them. If oil prices ease, it can take pressure off rates and support investor sentiment.

Major Stock Indexes Continue to Set Highs, but the Rally Remains Narrow

The largest companies continued to lead the market, helping the S&P 500 stay near record highs despite rising interest rates.

Technology stocks have driven much of the gain since late March, especially companies tied to artificial intelligence. While much of the market has participated in the rally, leadership has narrowed in recent weeks.

Interest-rate-sensitive areas, including smaller companies, have traded lower as rising rates weigh on valuations and investor appetite for risk.

Why it matters: Major stock indexes remain near all-time highs, but the rally is slowing and becoming more selective. That does not mean the rally is over, but it does mean investors should be mindful of what is actually driving index-level performance.

Nvidia’s Earnings Results Signal Strong Demand for AI Infrastructure

Nvidia’s earnings release was the major company-specific event of the week.

Investors continue to watch the company’s results closely because Nvidia has become one of the clearest gauges of demand for AI-related technology. The company reported roughly $81.6 billion in revenue, up about 85% from a year earlier, along with strong earnings and an $80 billion stock buyback.

Why it matters: The report suggests that spending on AI infrastructure remains strong and continues to grow. At the same time, expectations for Nvidia and the broader AI theme are already high. That means future results will need to keep impressing investors to justify current expectations.

When Gas Prices Move, Your Plan Shouldn’t Panic

Gas prices are back in the headlines.

The national average price of a gallon of gasoline has moved above $4.50, up nearly 50% since the start of the U.S.-Iran conflict in late February. The main issue is oil supply. Roughly 20% of the world’s oil moves through the Strait of Hormuz, a major shipping route in the Middle East, and traffic through that route remains well below pre-conflict levels.

When less oil is moving through the system, crude prices rise. When crude prices rise, gas prices usually follow.

And this does not stop at the pump.

Higher diesel prices eventually show up in the cost of moving goods by truck. That means the pressure can work its way into grocery prices, household goods, and other everyday expenses. In other words, what begins as an energy story can quickly become a household budget story.

Moments like this tend to produce a lot of predictions.

Where will oil go next? How high will gas prices get? How long will this last?

Those are interesting questions, but they are not always the most useful ones.

The better question is: what, if anything, should this change in your financial life right now?

For most households, the answer is not “rewrite the plan.” The answer is usually much simpler. It is to look at where the pressure is showing up and make sure the adjustment is intentional.

Three questions are worth asking.

Question #1: Where is the gas price increase being absorbed?

For a household with two cars, higher fuel prices may add roughly $1,200 to $1,800 per year in additional spending.

That money has to come from somewhere.

For some families, it quietly reduces the amount being saved each month. For retirees, it may increase the amount being withdrawn from the portfolio. For others, it may simply crowd out other discretionary spending.

None of those outcomes is automatically wrong.

The issue is whether the change is happening by choice or by default.

That is the practical planning question. Are you comfortable absorbing the increase where it is currently landing? Or would it make more sense to temporarily adjust something else, such as delaying a purchase, trimming a discretionary category, or reducing short-term savings for a season?

In most cases, this kind of price increase does not require a major financial planning change.

But it does deserve a quick look.

Small pressures are easier to manage when they are noticed early.

Question #2: Is this year’s spending still tracking the retirement income plan?

For retirees, the question becomes more specific.

Is this year’s spending still in line with the plan, or is it beginning to run ahead of it?

A temporary stretch of higher fuel and grocery costs is usually something a well-built retirement plan can absorb. That is one reason we build plans with flexibility, not precision down to the penny.

But it is still worth checking.

The simple exercise is to compare actual spending over the past several months with what the plan assumed for the year. Then look at the trend.

Is the gap closing as prices stabilize? Or is it widening as higher costs spread into more parts of the budget?

That distinction matters.

The goal is not to overreact. The goal is to identify whether a small adjustment today can prevent a larger adjustment later.

That is one of the quiet benefits of ongoing planning. It gives you room to respond before something becomes urgent.

Question #3: Does higher inflation change the long-term plan?

Usually, no.

A financial plan is not built around one year of inflation. It is built around long-term assumptions that play out over decades.

That means a stretch of 4% inflation, even if it lasts several quarters, does not automatically change the long-term plan. The plan was designed with the understanding that some years will be higher, some years will be lower, and the actual path will never move in a straight line.

For those approaching retirement, the better question is whether the retirement income target still reflects the life you are planning to live.

For those still saving, it is a reminder that the cost of the future is not fixed. The number you are working toward needs to be reviewed over time because life, markets, taxes, and inflation all change.

That is not a flaw in the plan.

That is the reason planning is an ongoing process.

The Bottom Line

Higher gas prices are frustrating because they are visible, frequent, and hard to ignore.

You see the price every time you fill up. You feel it when the grocery bill runs higher. You notice it when the monthly budget feels a little tighter than it did a few months ago.

But from a planning perspective, this is not a reason to panic.

It is a reason to pay attention.

The price at the pump is a reminder that the cost of living is not a fixed number. But it is still only one input in a plan designed around a much longer time horizon.

Good planning does not require reacting to every headline.

It requires knowing which headlines matter, asking the right questions, and making small adjustments before they become large ones.

Weekly Market Update: Hot Inflation Tests a Narrow Rally

Markets traded higher for a seventh consecutive week, extending the rally that began in late March. The S&P 500 and Nasdaq set new all-time highs, but the rally remained narrow.

Small-cap stocks and the equal weight S&P 500 produced only modest gains, with technology again the strongest sector and the largest tech names pulling the broader index and growth factor higher.

The week's defining story was inflation. Both consumer and producer prices rose at the fastest pace in years, and Treasury yields climbed across the curve in response. Corporate bonds outperformed as credit spreads tightened, while oil prices moved higher on renewed Middle East tensions.

International stocks once again lagged U.S. stocks. Next week's big event is Nvidia's earnings report, which will provide more insight into AI capex spending.

Key Takeaways

Inflation Came in Hot at Both the Consumer and Wholesale Level

Consumer prices rose +3.8% year-over-year in April, the highest reading in nearly three years. Wholesale prices delivered the bigger surprise at +6.0% y/y, the largest annual gain since December 2022.

The two reports measure inflation at different points in the supply chain (wholesale captures what businesses pay, while consumer prices capture what households pay), and a hot wholesale print signals the potential for more inflation pass-through. Higher gas prices drove a large share of both increases, but the rise wasn't limited to energy, with service categories like airfare, hotels, and rent also rising.

Why it matters: The inflation that's been building in energy markets is now showing up in the broader data, and the pressure is spreading beyond energy.

Oil Prices Rose as U.S.-Iran Tensions Re-Escalated

Oil rose more than +5%, with most of the move coming Monday after President Trump told reporters the Iranian ceasefire was "on life support." Energy was the second-best-performing sector of the week.

Gasoline prices remain near $4.50 a gallon nationally, and the White House floated suspending the federal gas tax, an acknowledgment that pump prices have become a political concern.

Why it matters: The supply side of the inflation story remains unresolved. The longer oil stays elevated, the more the cost shows up in everyday spending categories like fuel, food, and transportation.

Interest Rates Rose as Investors Absorbed the Inflation Data

Treasury yields rose across the yield curve, including longer-term yields, which was notable. The move higher in long-term yields suggests the market expects inflation to remain elevated, with the 30-year yield rising above 5%.

Shorter-term rates also rose, an indication the market believes persistent inflation could pressure the Fed to raise interest rates. In related news, the Senate confirmed Kevin Warsh as the next Fed chair by the slimmest margin in modern history, with his first meeting in June.

Why it matters: Futures markets price in zero rate cuts for the rest of 2026, with consensus shifting toward interest rates staying higher for longer.

Major Indexes Set New Highs Despite a Narrow Rally

The S&P 500 and Nasdaq both closed at new all-time highs, gaining more than +2% each. Most of the move came Wednesday on the start of a Trump-Xi summit in Beijing and strong gains in mega-cap tech, with Apple crossing $300 a share for the first time.

Beneath the index level, small-cap stocks and the equal weight factor produced modest gains. Sector leadership rotated as well, with energy and defensive areas like healthcare and consumer staples rising while financials and industrials declined.

Why it matters: The major indexes continue to set new highs, but the broader market paused this week. The divergence doesn't necessarily break the rally's longer trend, but it's worth watching as the inflation and interest rate situation develops.

Consumers Continue to Spend Despite Rising Energy Costs

April retail sales beat expectations, growing +4.9% year-over-year. Excluding autos and fuel, the categories most affected by inflation, spending rose +0.5% month-over-month.

Why it matters: April's retail sales data suggests consumer spending is holding up despite rising energy costs. If spending slows under the weight of higher prices, it could translate into slower economic growth.

When Exercising Stock Options Creates More Tax Than You Have Cash

Some option exercises create taxable consequences before there is liquidity. On paper, value was created. In real life, that does not mean cash is available.

You exercise options in a private company or ahead of a liquidity event expecting long-term upside, and then realize you may have triggered a tax bill without having sold anything. The IRS does not wait for your shares to become sellable. It taxes what it sees as income or gain at the moment of exercise, regardless of whether you can actually convert any of it to cash.

This catches well-prepared people off guard. They make a thoughtful, forward-looking decision and then receive a tax obligation that has no obvious source of funds behind it. The decision was reasonable. The result feels punishing. Usually, the gap between the two is a planning gap, not a strategy mistake.

Why this happens

The tax code treats different option types differently, and most of those treatments do not align with when cash actually arrives.

With non-qualified stock options (NSOs), exercising creates ordinary income equal to the difference between the strike price and the fair market value at exercise. That income is reported on your W-2 and subject to withholding. If the company is private, there is no market to sell into, but the tax still applies.

Incentive stock options (ISOs) can be even more confusing. A regular-tax exercise of ISOs does not create ordinary income, which sounds favorable. But the spread between strike price and fair market value becomes a preference item for the alternative minimum tax. AMT can quietly create a six-figure liability on an exercise that produced no cash and no sale. People often discover this in April, well after the decision is final.

Restricted stock and 83(b) elections add another layer. Early exercises, secondary tender offers, and pre-IPO planning each have their own timing rules. The common thread is that taxable events are tied to specific moments in the equity, not to when you can sell.

Liquidity makes this worse. In a public company, you can usually sell shares to cover taxes, even if the timing is not ideal. In a private company, you may hold restricted stock that cannot be sold for years. Tender offers, if they happen at all, are unpredictable and often capped. So the tax obligation arrives on schedule, while the cash to pay it does not.

A common scenario

Consider an employee at a late-stage private company. She has a meaningful ISO grant, has been at the company for several years, and is told an IPO is "probably next year." She wants to start the holding period for long-term capital gains treatment, so she exercises a significant portion of her options.

Her strike price is low because she joined early. The 409A valuation has climbed substantially. The spread between the two is several hundred thousand dollars. There is no W-2 income from the exercise, so her paycheck looks normal and nothing is withheld.

Months later, her CPA runs the AMT calculation. The preference item from her ISO exercise pushes her into AMT with a tax bill in the six figures. She has no liquid shares to sell, no tender offer in sight, and the IPO timeline has slipped. She now has to fund the tax from savings, a margin loan, or specialty financing, none of which were part of her original plan.

Her decision was not wrong. The long-term math could still work out well if the company exits at a strong valuation. But the cash strain in the meantime is significant, and it could have been anticipated and sized differently before the exercise was finalized.

The same pattern plays out with NSO exercises that generate large ordinary income, with disqualifying dispositions that change ISO treatment after the fact, and with 83(b) elections on restricted stock at higher valuations. The underlying issue is consistent: equity decisions and cash flow decisions are made on different timelines, and the tax code only respects one of them.

Plan the cash before you exercise

Before exercising, model the tax cost and cash needed so a proactive move does not turn into a liquidity problem.

A useful equity exercise plan answers a few questions in writing, before any forms get signed:

- What will this exercise cost in federal, state, and AMT terms under realistic valuation assumptions?

- Where will the cash to pay that tax come from, and what is the cost of using each source?

- What happens if the liquidity event is delayed by a year, two years, or longer?

- How does this exercise interact with other income, charitable planning, and existing concentrated positions?

- If the company does not reach the expected exit, can the household absorb the loss without disrupting other goals?

These questions are not meant to discourage exercising. They are meant to make the exercise a decision that fits into a broader plan rather than one that creates pressure on it. Equity compensation can be one of the most powerful wealth-building tools available, but only when the tax timing, the cash timing, and the longer-term strategy are coordinated in advance.

If you are weighing an exercise, evaluating a tender offer, or watching a possible liquidity event approach, the most valuable work usually happens before the calendar forces a decision. Run the numbers, stress test the assumptions, and make sure the cash plan is as well thought through as the equity plan.

Selling Startup Stock? This Tax Break That Could Shelter Millions

Selling startup stock can feel like the kind of financial win you have been waiting years to realize.

The company you believed in early, the equity you accepted in place of a higher salary, the shares that sat quietly on paper for years. Suddenly, they are worth something real. And the instinct is to celebrate, close the deal, and move on.

But before you sell, there is one tax question worth asking.

Does this stock qualify for the qualified small business stock exclusion?

For certain founders, early employees, and startup investors, QSBS can potentially exclude a significant amount of capital gain from federal income taxes. We are talking about gains that might otherwise face a combined federal rate well above 20 percent, including the net investment income tax.

State taxes may also matter, and not every state follows the federal QSBS rules the same way. But even at the federal level alone, the difference between planning ahead and missing the window entirely can be measured in hundreds of thousands of dollars, or more.

Why QSBS Is Worth Understanding

QSBS is valuable because it can turn a highly appreciated stock sale into a much more tax-efficient liquidity event.

But the rules are technical, and the details matter.

The first step is understanding what you actually own, because founders’ shares, exercised options, restricted stock, RSUs, and secondary shares may not all receive the same QSBS treatment.

The company generally needs to be a qualifying C corporation when the stock is issued. The stock usually must be acquired at original issuance, meaning secondary market purchases typically do not qualify.

The business must meet certain size requirements at issuance and must satisfy active business requirements during the relevant holding period. Certain industries are specifically excluded, including professional services, financial services, hospitality, and others. And the holding period is critical. Generally, the stock must be held for more than five years to qualify for the full exclusion.

Recent tax legislation has added new layers to consider. The law enhanced the QSBS rules, including a higher gain exclusion cap for some stock acquired after July 4, 2025, and partial exclusions for certain qualifying stock held less than five years.

For qualifying stock acquired after July 4, 2025, the per-issuer exclusion cap generally increased from $10 million to $15 million, or ten times basis, with inflation adjustments beginning after 2026. Importantly, these enhanced rules generally apply to stock acquired after July 4, 2025, while earlier-acquired QSBS remains subject to the prior framework.

The IRS has also signaled increased scrutiny around more aggressive planning strategies involving multiple trusts designed to multiply the exclusion across family members and entities.

So the real planning issue is not simply, "How much will I owe when I sell?"

The better question is, "What needs to be documented and reviewed before the sale so I do not miss a major tax opportunity?"

What It Looks Like in Practice

Imagine a startup employee who exercised options early and acquired shares directly from the company when the valuation was modest and the future uncertain.

Years pass. The company grows. A strategic buyer emerges, and the employee's shares are now worth several million dollars.

Without any planning, this looks like a straightforward capital gain event. Long-term rates apply, the gain is reported, the tax is paid, and life moves forward.

But if the stock qualifies as QSBS, that same employee may be able to exclude some or all of the gain from federal income tax, subject to the applicable limits. The exclusion can be substantial. Under prior law, up to 100 percent of eligible gain, capped at the greater of $10 million or ten times the taxpayer's basis, could be excluded for qualifying stock.

The enhanced rules for post-July 4, 2025 acquisitions raise that ceiling further for some taxpayers.

That single determination changes the entire liquidity plan.

It may affect when to sell and how much to sell in a given tax year. It may affect whether pre-transaction gifting to family members, certain trusts, or charitable vehicles makes sense, though these strategies require careful tax and legal review.

It may also affect whether charitable planning makes sense before the transaction, especially if the shares are still privately held and the client already has philanthropic goals. It changes how to coordinate estimated tax payments and how to think about reinvesting the proceeds to maintain tax efficiency after the exit.

But here is the key point every founder, executive, early employee, and startup investor needs to understand.

QSBS planning needs to happen before the transaction, not after the wire hits the account. Once the sale closes, many of the most valuable planning levers, including timing, ownership, gifting, and charitable-transfer decisions, may be gone.

What to Review Before You Sell

If you are holding startup stock and a liquidity event is on the horizon, here is where to start.

Review what type of equity you own. Founders’ shares, exercised options, restricted stock, RSUs, and secondary shares can have very different tax histories. The answer is not simply whether you worked at the company early. The answer depends on how and when you actually acquired the stock.

Review how the shares were acquired. Were they issued directly by the company, or purchased from another stockholder? Original issuance is a core requirement, and secondary purchases typically do not qualify.

Confirm when the shares were acquired and whether the five-year holding period has been met for the full exclusion, or whether a partial exclusion under the newer rules may apply for qualifying stock acquired after July 4, 2025.

Verify that the company qualifies. Not every C corporation meets the active business and size requirements, and certain industries are excluded entirely. This confirmation requires documentation, not assumptions.

Consider whether any pre-transaction gifting or charitable planning makes sense. In some cases, transferring shares before a sale to family members, certain trusts, or a charitable vehicle can be a meaningful strategy worth evaluating. But these strategies need to be reviewed before a transaction is substantially certain, not after a buyer is already at the finish line.

And make sure the documentation exists. QSBS status is not automatically verified at closing. It needs to be established, supported, and preserved in your records.

The Goal Is Not Just the Exit

QSBS can be one of the most powerful tax breaks available to founders, startup employees, and early investors.

But it is not automatic.

The planning does not create QSBS status where it does not exist. But it can help determine whether the opportunity exists, preserve the documentation, and avoid decisions that accidentally waste it.

A liquidity event without proper planning can mean paying taxes you did not have to pay, on gains that a well-structured strategy could have legally sheltered. That is not a small difference. For many clients, it may be the single largest tax planning opportunity they will ever encounter.

When startup stock becomes real wealth, the goal is not just to celebrate the exit. The goal is to preserve the opportunity, manage the tax bill, and turn a concentrated liquidity event into long-term clarity, confidence, and peace of mind.

Weekly Market Update: Rally Extends to Six Weeks as Iran Talks Advance

Markets traded higher for a sixth consecutive week, extending the rally that began in late March and pushing several major indexes to new highs.

Technology and growth stocks led the advance, with the Nasdaq gaining nearly 4%, outpacing the S&P 500 and small-cap stocks, which each rose roughly 1.5%. Technology, consumer discretionary, and communication services were the top-performing sectors, all of which carry significant exposure to the largest companies in the market.

Beneath the surface, the picture was more mixed. Six of eleven sectors finished the week lower, highlighting how the rally has been driven by a relatively narrow group of market leaders. Bonds produced modest gains as interest rates drifted lower, and oil fell more than 8% on reports of progress toward an Iran deal.

The week closed with a stronger-than-expected April jobs report, adding to the picture of an economy that continues to hold up despite the geopolitical backdrop.

Key Takeaways

The Middle East Conflict, Now in its 10th Week, Remains the Top Story in Financial Markets

The week opened with Iran's most serious provocation since the April ceasefire, including strikes on the UAE and attacks on commercial ships in the Strait of Hormuz. The tone shifted quickly as regional allies pressed for de-escalation and reports emerged of a framework agreement to end the conflict.

Oil fell nearly 10% early in the week, trading near $90 per barrel for the first time since mid-April.

Why it matters: The acute market stress from earlier in the conflict has eased, but the situation continues to drive significant swings in oil prices and broader market sentiment. Progress toward a resolution would be a positive development for markets, while a breakdown in talks could trigger more volatility.

Major U.S. Equity Indices Continue to Set New Highs

U.S. stocks extended their rally to six consecutive weeks, with three of the four major indexes reaching new highs. The S&P 500 gained 2.0%, the Nasdaq rose 4.0%, and small-cap stocks climbed 1.5% to set a new high of their own.

Most of the week's gains came in a single session, following reports of progress on an Iran deal.

Why it matters: The pattern has been consistent through this stretch of geopolitical uncertainty. Headlines create short bursts of volatility, but the market has recovered as conditions stabilize. Six consecutive weeks of gains, including new highs across multiple broad equity indexes, reflects a market that continues to look through near-term uncertainty toward the underlying fundamentals.

Leading Tech Companies Report Strong Earnings and Increasing AI Capital Expenditures

The largest technology companies reported earnings over the past two weeks, and their commitment to AI infrastructure spending continues to grow. Alphabet, Amazon, Meta, and Microsoft all beat estimates, but the capital spending figures drew the most attention.

Meta raised its full-year capital spending guidance to $125 to $145 billion, Microsoft spent nearly $32 billion in a single quarter, and Alphabet's cloud backlog nearly doubled. Combined, the top four U.S. cloud providers are now projected to spend over $660 billion on infrastructure in 2026.

Why it matters: The spending isn't speculative in the way it once appeared, with the group posting strong revenue growth. Given these companies' large index weights, the reported growth is one of the forces pushing broad market indexes higher.

April Payrolls Beat Expectations as the Labor Market Holds Steady

The April employment report came in stronger than expected. Nonfarm payrolls rose by 115,000, down from the 185,000 created in an unusually strong March but better than the 55,000 forecast in the Dow Jones consensus estimate.

The unemployment rate held at 4.3%, further proof that the labor market has reached a point where only modest job creation is needed to keep the jobless level steady, given little growth in the labor force. Average hourly earnings came in lower than expected, increasing 0.2% for the month and 3.6% on an annual basis.

Beneath the headline, the picture was softer. A broader measure that includes discouraged workers and those holding part-time jobs for economic reasons rose to 8.2%, and the participation rate declined to 61.8%, the lowest since October 2021.

Why it matters: The labor market continues to defy expectations for a slowdown, but the softer details, slower wage growth and falling participation, point to a more cautious picture underneath. For investors, the report supports the view of a stable but cooling labor market, one that doesn't pressure the Fed in either direction at a time when policymakers are already navigating an oil shock and ongoing geopolitical risk.

Here's the Cost of Moving to the Sidelines

Markets rarely tempt investors to make bad decisions when things feel calm.

They tempt investors when the headlines are loud, losses are fresh, and moving to cash feels less like panic and more like prudence.

That is what made the first quarter so difficult.

From its late-January high through the end of March, the S&P 500 fell nearly 10% as the U.S.-Iran conflict pushed oil prices more than 60% higher. Headlines about the Strait of Hormuz, rising energy costs, and the potential economic fallout created the kind of environment where investors naturally begin asking a very human question:

Should I get out before this gets worse?

Market Timing Rarely Feels Like Market Timing

That question is understandable. It is also dangerous.

The problem with market timing is that it rarely feels like market timing in the moment. It feels like caution. It feels like discipline. It feels like protecting what you have built.

But getting out is only half the decision.

You also have to know when to get back in.

And that second decision is often the harder one.

When ceasefire talks emerged in late March, markets quickly began to recover. Investors who moved to the sidelines during the selloff were then faced with a new question:

Do I get back in now, after the market has already bounced, or do I wait until things feel calmer?

That is where many investors get hurt.

By the time the environment feels safe again, the market has often already moved. The recovery does not usually announce itself ahead of time. It often begins while the headlines are still uncomfortable, while the outcome is still uncertain, and while investors are still waiting for confirmation.

The Best and Worst Days Arrive Together

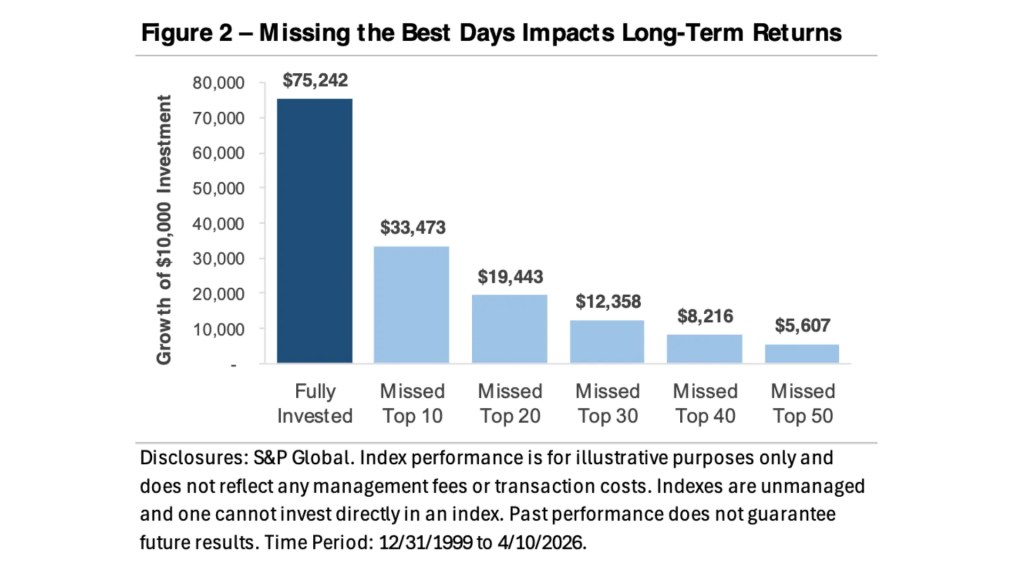

That is why the best and worst days in the market tend to arrive close together.

Figure 1 illustrates this pattern. The chart shows the S&P 500's daily returns over the past 26 years and highlights an important truth: the market's largest moves tend to cluster. The biggest selloffs do not happen in isolation. They are often surrounded by some of the strongest rallies.

We saw this during the 2008 financial crisis. We saw it during the 2020 pandemic. We saw it during the tariff-driven volatility of 2025. And we saw it again during the recent U.S.-Iran volatility, when the S&P 500 posted its strongest daily return since April 2025 on optimism around a possible ceasefire, only days after escalating tensions had pushed stocks lower.

That is the uncomfortable reality of investing through uncertainty.

The same environments that produce sharp selloffs often create the conditions for sharp recoveries.

Missing a Few Days Can Cost You Decades

Figure 2 puts a dollar amount on that lesson. A $10,000 investment in the S&P 500 on December 31, 1999, would have grown to $75,242, despite a period that included the dot-com bust, the global financial crisis, the pandemic, inflation shocks, rising rates, wars, and political uncertainty.

That result did not come from avoiding every downturn.

It came from staying invested through them.

Missing just the 10 best trading days would have reduced the ending value to $33,473, less than half the fully invested result. Missing the 20 best days would have lowered it to $19,443. Missing the 30 best days would have brought it down to $12,358. And missing the 50 best days would have turned the original $10,000 into just $5,607.

In other words, an investor could have lived through a period when the market created substantial wealth, yet still lost money by missing too many of the right days.

That is what makes market timing so costly.

You do not have to be wrong all the time. You only have to be wrong at a few critical moments.

Bottom Line

This year's volatility may feel unsettling, but it reinforces one of the most important principles of long-term investing: the plan has to be built before the panic arrives.

A well-constructed financial plan does not assume markets will always cooperate. It assumes there will be downturns. It assumes there will be recessions. It assumes there will be geopolitical shocks, energy price spikes, scary headlines, and stretches of time when discipline feels uncomfortable.

That is why cash reserves matter.

That is why diversification matters.

That is why rebalancing matters.

And that is why your investment strategy should be connected to your broader financial plan, not just to your feelings about the latest headline.

Selling during a decline may provide temporary emotional relief, but it also locks in losses and creates a difficult re-entry problem. Staying invested does not mean ignoring risk. It means managing risk through a plan rather than reacting to fear.

What the Market Actually Rewards

The market does not reward perfect timing.

It rewards patience, discipline, and the ability to stay anchored when the headlines are loud.

And as the first quarter reminded us, missing just a few of the market's best days can come at a very high cost.

Weekly Market Update: Stocks Set New Records as Oil Pulls Back and Rates Ease

Stocks continued their climb through a holiday-shortened week, with the major indexes setting fresh records along the way. The S&P 500, Nasdaq, and Dow each closed at new all-time highs, and the rally showed signs of widening beyond the largest technology companies. Small-cap stocks and the equal-weight S&P 500 participated more meaningfully than they had in recent weeks.

Technology remained the strongest sector, helping lift both the market-cap-weighted index and growth stocks higher. Defensive sectors and energy lagged as investors responded to signs of diplomatic progress in the Middle East. Oil prices moved lower, which helped Treasury yields reverse some of their recent climb. That decline in rates offered relief to bonds and other rate-sensitive areas of the market. Volatility also eased, with the VIX drifting lower as geopolitical concerns cooled and stocks moved higher.

Key Takeaways

Inflation Remains Elevated, But the Pace of Price Increases Eased Last Month

The April PCE price index, the Fed’s preferred inflation measure, rose +3.8% year-over-year, its highest reading since May 2023. However, the monthly increase of +0.4% came in below the +0.5% forecast and slowed from March’s +0.7% increase. Much of the pressure in the headline number was tied to energy prices following the ongoing Strait of Hormuz oil disruption.

Core PCE, which excludes food and energy, rose just +0.2% for the month, below the +0.3% consensus estimate. On a year-over-year basis, core inflation edged up from +3.2% to +3.3%.

Why it matters: The energy shock is still showing up in the annual inflation data, but the softer monthly core reading suggests that price pressures have not yet broadened across the economy. Investors will be watching upcoming inflation reports closely for signs that higher energy costs are beginning to spill over into other areas.

Economic Growth in Q1 Was Slower Than Initially Estimated

The second estimate of first-quarter GDP was revised lower to a +1.6% annualized pace, down from the initial +2% reading. The downgrade arrived the same morning as the hotter inflation report, underscoring the tension between slower growth and still-elevated prices.

Why it matters: Growth rebounded in Q1 following the Q4 government shutdown, but the combination of slower growth and elevated inflation raises the possibility of a more challenging backdrop. That type of environment would make the Fed’s job more difficult, because cutting rates to support growth could risk putting additional pressure on inflation.

Major Stock Indexes Continued to Set New Highs This Week

The Dow, S&P 500, and Nasdaq each reached new records, extending the rally that began in late March. Importantly, the gains were not limited to the largest technology companies. Small-cap stocks and the equal-weight S&P 500 also moved to new highs.

Why it matters: Large technology stocks have carried much of the market’s advance since late March, and market breadth has been uneven at times. This week’s broader participation from the Dow, small caps, and the average S&P 500 stock is a constructive sign that the rally is becoming less dependent on a narrow group of companies.

Middle East Headlines Continue to Drive Oil Prices and Impact Market Sentiment

Iran reported a preliminary agreement to extend the ceasefire and guarantee shipping through the Strait of Hormuz, briefly sparking a risk-on move before U.S. officials disputed the document. Later in the week, renewed ceasefire headlines helped push stocks toward new all-time highs.

Oil prices pulled back over the week, with crude trading near $90 and on pace for a second consecutive weekly decline as markets priced in the possibility of an eventual agreement.

Why it matters: The Strait of Hormuz remains the biggest wildcard for energy prices and, by extension, inflation. A genuine resolution would be a meaningful positive for both markets and consumers. However, this week’s back-and-forth is a reminder that the headlines remain volatile and the outcome is still uncertain.

Interest Rates Reversed Lower as Oil Prices Declined

Treasury yields had climbed sharply in recent weeks, with the 30-year yield reaching a two-decade high as the oil price spike raised inflation concerns. That pressure eased this week as crude prices moved lower. The 10-year Treasury yield fell to around 4.45%, while the 30-year yield dropped back below 5.00%.

The move reflected the broader shift in Middle East sentiment. Reported progress toward reopening the Strait of Hormuz pulled oil prices lower, which also reduced some of the inflation premium that had been built into bond yields.

Why it matters: The recent path of interest rates has been closely tied to oil prices and developments in the Middle East. This week’s reversal provided some relief for bonds, mortgages, and other rate-sensitive parts of the market. Whether that relief lasts will likely depend on whether oil prices remain contained and diplomatic progress continues.